CONNOR, CLARK & LUNN UCITS ICAV

An Irish collective asset-management vehicle constituted as an umbrella fund with variable capital and

segregated liability between Sub-Funds with registration number C400076 and authorised by the

Central Bank of Ireland pursuant to the Irish Collective Asset-Management Vehicles Act 2015, the

European Communities (Undertakings for Collective Investment in Transferable Securities)

Regulations 2011 (as amended) and the Central Bank (Supervision and Enforcement) Act 2013 (Section

48 (1)) (Undertakings for Collective Investments in Transferable Securities) Regulations 2019

ANNUAL REPORT AND AUDITED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2023

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

1

TABLE OF CONTENTS

Page

Directory

2

Investment Manager’s Report

3-4

Directors’ Report

5-8

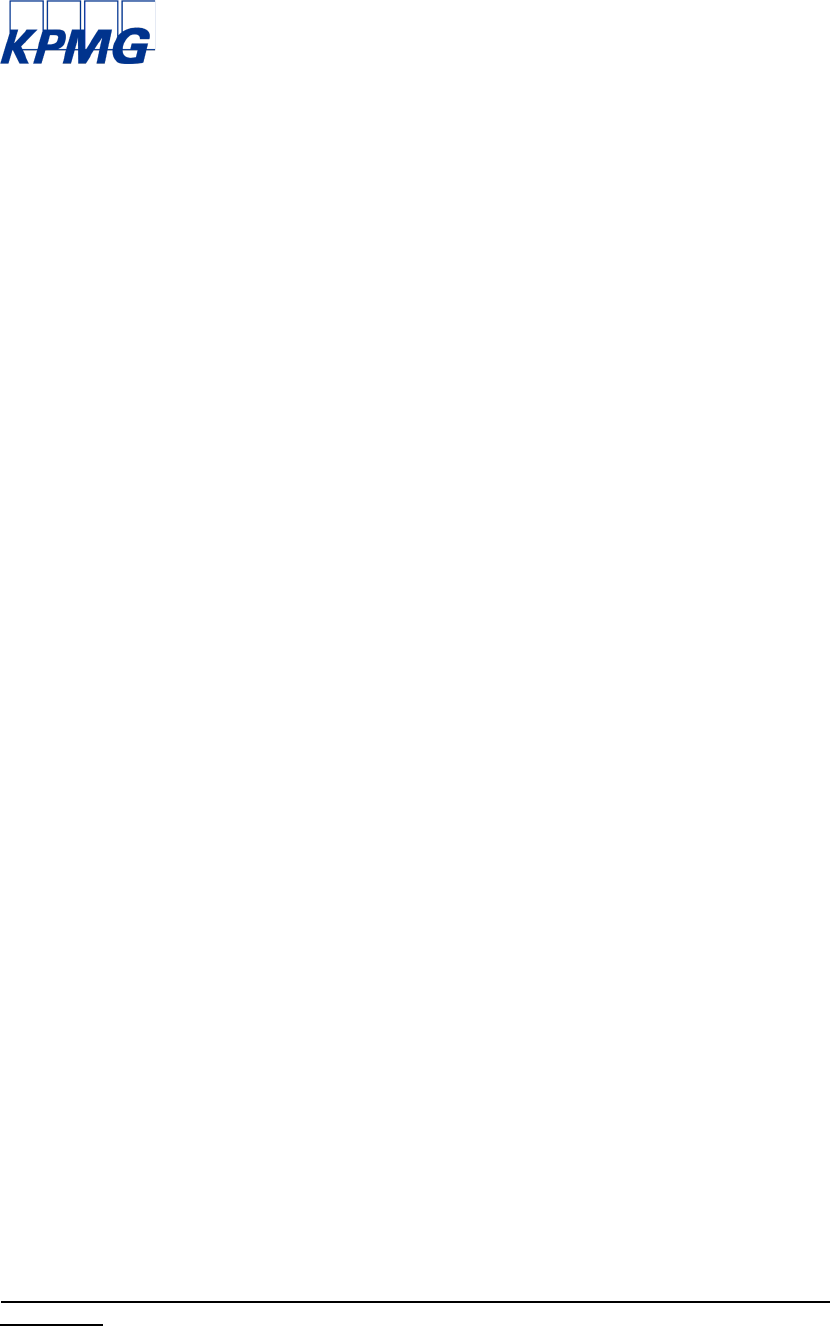

Annual Depositary Report to the Shareholders

9

Independent Auditor’s Report to the Shareholders

10-12

Statement of Financial Position

13-14

Statement of Comprehensive Income

15-16

Statement of Changes in Net Assets attributable to the Holders of Redeemable

Participating Shares

17-18

Statement of Cash Flow

19-22

Notes to the Financial Statements

23-48

Schedule of Investments

49-90

Schedule of Changes in Investments (Unaudited)

91

Other Additional Disclosures (Unaudited)

92-95

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

2

DIRECTORY

DIRECTORS OF THE ICAV

ADMINISTRATOR, REGISTRAR AND

Mike Freund*

TRANSFER AGENT

Fiona Mulcahy**

HSBC Securities Services (Ireland) DAC

Sheila Rohan*

1 Grand Canal Square

Grand Canal Harbour

MANAGER

Dublin 2

Carne Global Fund Managers (Ireland) Limited

Ireland

3rd floor, 55 Charlemont Place

Dublin 2

DEPOSITARY

D02 F985

HSBC Continental Europe, Dublin Branch

Ireland

1 Grand Canal Square

Grand Canal Harbour

DIRECTORS OF THE MANAGER

Dublin 2

Neil Clifford

Ireland

Teddy Otto

Sarah Murphy

SECRETARY OF THE ICAV

Elizabeth Beazley

Carne Global Financial Services Limited

Christophe Douche

3rd floor, 55 Charlemont Place

Aleda Anderson (appointed on 1 January 2023)

Dublin 2

Jacqueline O’Connor

D02 F985

Ireland

INVESTMENT MANAGER

Connor, Clark & Lunn Investment Management Ltd.

1111 West Georgia Street, Suite 2300

LEGAL ADVISORS AS TO IRISH LAW

Vancouver, British Columbia

Matheson

V6E 4M3

70 Sir John Rogerson’s Quay

Canada

Dublin 2

Ireland

INDEPENDENT AUDITORS

KPMG

1 Harbourmaster Place

PROMOTERS OF THE ICAV

International Financial Services Centre

Connor, Clark & Lunn UK Limited

Dublin 1

8th Floor

Ireland

1 Knightsbridge Green

SW1X 7QA

London

* Non-executive

** Independent Non-executive

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

INVESTMENT MANAGER’S REPORT

FOR THE YEAR ENDED 31 DECEMBER 2023

3

Financial Market Review

The global macroeconomic backdrop strengthened early in 2023 and contributed to a strong start for

global equity markets in January, largely in response to China’s economic reopening and lower

natural gas prices in Europe. In March, financial markets experienced a significant shock when a

confluence of factors led to a bank run across US regional banks that ultimately resulted in the

second- and third-largest US bank failures in history. Despite support from federal regulators, the

turbulence spilled over into Europe with the collapse of Switzerland’s Credit Suisse, a systematically

important financial institution that was ultimately merged with its largest domestic peer, UBS.

Inflation has remained higher than expected which has resulted in further interest rate hikes by central

banks in developed markets. Overall, despite recession fears, economic activity and corporate

earnings have proved more resilient against higher interest rates. In the second quarter, investor

sentiment improved in response to multiple factors, including the resolution of the US debt ceiling

discussions, as well as growing enthusiasm regarding artificial intelligence (AI) that helped to bolster

the outlook for the technology sector.

Early in the third quarter, widespread expectations for a soft landing were supported by resilient

economic activity and slowing inflation. As the quarter progressed, however, the increased likelihood

that interest rates could remain elevated for a prolonged period of time negatively impacted market

sentiment. Robust North American economic releases suggested the economy might be able to

withstand higher interest rates, while monetary policymakers maintained a somewhat aggressive

stance on interest rates. This caused a spike in bond yields, which reached new highs for this

economic cycle near the end of September. Equity markets, which had been relatively stable over the

summer months, declined in the final weeks of the quarter, and posted negative returns over the

period. Oil production cuts led to a surge in crude oil prices, which also heightened concern about

higher inflation.

US economic releases pointed to strength early in the fourth quarter, which fuelled concern about

further interest rate increases. In November, however, the market narrative shifted in response to

signs of a slowing economy and data showing the potential for a return to a broader disinflationary

trend. This rejuvenated the “soft landing” theme, where inflation and economic growth slow but

avoid a recession, which would allow monetary policymakers to shift away from their tightening

measures. This notion gained further momentum when the US Federal Reserve (Fed) pivoted toward

a more “dovish” stance, meaning the potential for interest rate reductions, even as US economic

indicators remained largely resilient. Bond yields initially spiked, particularly in the US and equity

markets were relatively weak through October. There was a sharp turnaround in November and

December, however, with plunging bond yields and surging stock prices resulting in a strong quarter

for both bond and equity markets. Despite the announcement of additional production cuts by major

producers, crude oil did not participate in the year-end rally, as there was some market concern about

the sustainability and consistency of these cuts.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

INVESTMENT MANAGER’S REPORT (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

4

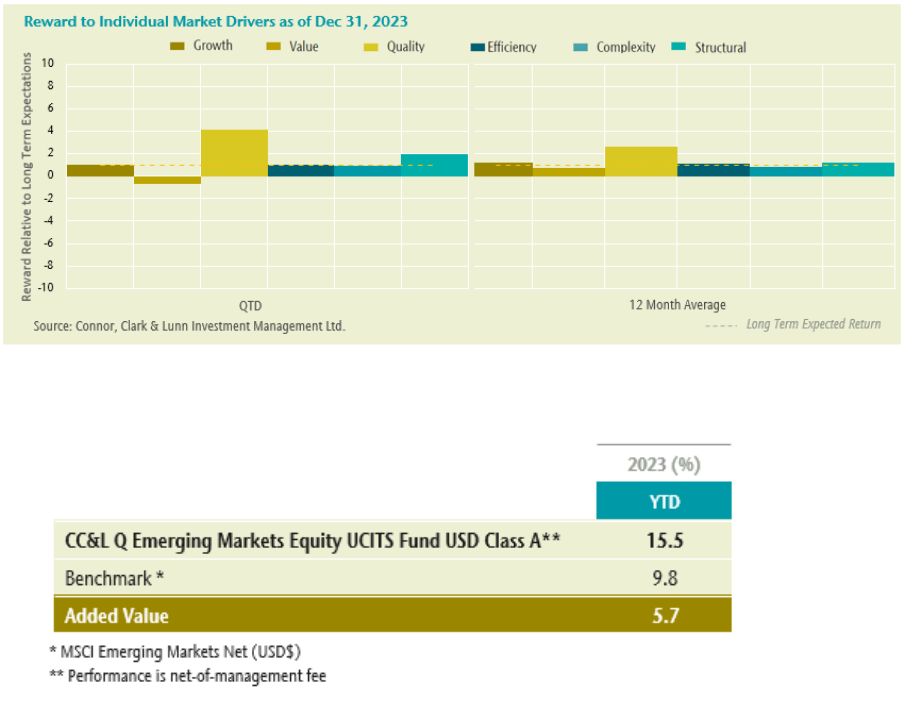

Market Review

Market leadership sharply contrasted that of 2022, with 9 out of the 11 GICs sectors reversing their

2022 market-relative performance in 2023.

Most factor groups in our investment model were well-rewarded in 2024. Despite the dramatic shift

in market themes in the latter part of the year, and the accompanying underperformance of industry

trend-based factors, our Growth composite performed well due to the robustness of stock-specific

growth metrics. Our Quality composite had an exceptional year of performance as investors

continued to favour companies generating sustainable earnings and deploying capital in an efficient

manner. Opportunity measures generally performed at or above long-term expectations.

Portfolio Performance

Outlook & Strategy

Going into 2024, the overall level of investment opportunity across our model (as measured by the

dispersion of return forecasts) as well as levels of forecast risk remain stable and close to their long-

term average levels.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

DIRECTORS’ REPORT

FOR THE YEAR ENDED 31 DECEMBER 2023

5

The Directors present their report for Connor, Clark & Lunn UCITS ICAV (the “ICAV”) and audited

financial statements for the financial year ended 31 December 2023.

Principal activities, business review & future prospects

The ICAV was incorporated as an Irish collective asset-management vehicle constituted as an

umbrella fund with segregated liability between sub-funds with registration number C400076 and

authorised by the Central Bank of Ireland (the “Central Bank”) pursuant to the European

Communities (Undertakings for Collective Investment in Transferable Securities) Regulations 2011

(as amended) (the “UCITS Regulations”) and the Central Bank (Supervision and Enforcement) Act

2013 (Section 48 (1)) (Undertakings for Collective Investments in Transferable Securities)

Regulation 2015, as amended (the “Central Bank UCITS Regulations”).

As at the date of this report the ICAV comprised of two Sub-Funds – one active Sub-Fund CC&L Q

Emerging Markets Equity UCITS Fund (the “EME Sub-Fund”) and one unlaunched Sub-Fund

CC&L Q Global Equity Market Neutral UCITS Fund together, (the “Sub-Funds”).

The ICAV is organised in the form of an umbrella fund with segregated liability between Sub-Funds.

The Instrument of Incorporation provides that the ICAV may offer separate Sub-Funds. Each Sub-

Fund will have a distinct portfolio of investments. The ICAV has obtained the approval of the Central

Bank for the establishment of the Sub-Fund set out below. Information specific to a Sub-Fund will

be set out in a separate Supplement to the Prospectus.

The investment objective of CC&L Q Emerging Markets Equity UCITS Fund is to seek long-term

growth of capital relative to emerging market equity indices by structuring and maintaining a

diversified portfolio of primarily emerging market equity securities and the investment objective of

CC&L Q Global Equity Market Neutral UCITS Fund is to generate returns that have a low correlation

with global equity markets and to maximise long-term total return.

A detailed business review is outlined in the Investment Manager’s Report on pages 3 to 5.

Principal risks and uncertainties

Investment in the ICAV carries with it a degree of risk including, but not limited to, the risks referred

to in the prospectus of the ICAV dated 9 April 2020 (the “Prospectus”). Details of the risks associated

with financial instruments are included in Note 7 to the financial statements.

Results and dividends

The results for the financial year are shown in the Statement of Comprehensive Income on page 16.

The Board of Directors may declare at its discretion, dividends in respect of each distribution share

class of each Sub-Fund. For the year ended 31 December 2023, the ICAV paid dividends to the

shareholders in the EUR A distributing class.

Future Developments

The Financial Statements have been prepared on a going concern basis.

The ICAV will continue to act as an investment vehicle as set out in its Prospectus. A review and

outlook of the Sub-Funds is included in the Investment Manager's Report.

Directors

The Directors of the ICAV who served during the year, and up to the date the financial statements

were signed, were as follows:

Mike Freund

Fiona Mulcahy

Sheila Rohan

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

DIRECTORS’ REPORT (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

6

Directors’ and ICAV Secretary’s interests

None of the Directors nor the ICAV Secretary or their respective families held any interest, beneficial

or otherwise, in the share capital of the ICAV during or at the end of the financial year.

The Board of Directors are not aware of any contracts or arrangements of any significance in relation

to the business of the ICAV in which the Directors had any interest at any time during the year ended

31 December 2023.

Accounting Records

The measures taken by the Directors to secure compliance with the ICAV’s obligation to keep

adequate accounting records are the use of appropriate systems and procedures and the employment

of competent service providers. The accounting records are kept at HSBC Securities Services

(Ireland) DAC, 1 Grand Canal Square, Grand Canal Harbour, Dublin 2, Ireland.

Political donations

There were no political donations made by the ICAV or the Investment Manager from the Sub-Fund

during the financial year.

Significant events during the financial year

The armed conflict between Russia and Ukraine continued throughout 2023. In the prior period, the

Board had authorized the write down to zero of all the local RUB denominated Russian equities held

in the amount of USD1,161,258. Based on continued market circumstances, these positions were

valued at zero throughout 2023. The Fund has had no exposure to securities directly exposed to

Ukraine.

The ICAV has exposure to the banking sector. In certain cases, government agencies have assumed

control or otherwise intervened in the operations of certain banks due to liquidity and solvency

concerns. The extent of the situation remains uncertain and, as such, the Investment Manager

continues to assess risks across the broader financial sector and will take potential actions, as deemed

necessary. The ultimate resolution of these liquidity and solvency concerns and the extent of the

related impact to the ICAV is uncertain and could be significant.

The new distributing share class, Class A Distributing EUR Shares, was launched in April 2023,

There were no other material significant events that have occurred in respect of the ICAV during the

financial year end.

Events since the financial year end

A distribution of USD 491,916 was made on 24 January 2024 from the EUR A distributing class.

On 21 March 2024, two additional Sub-Funds, CC&L Q Global Small Cap Equity UCITS Fund and

CC&L Q Global Equity UCITS Fund, were authorized by the Central Bank of Ireland as a result of

filing Supplements for each respective Sub-Fund along with a revised Prospectus for the ICAV.

There were no other material significant events that have occurred in respect of the ICAV subsequent

to the financial year end.

Principal material changes

There have been no material changes in the objectives and strategies of the ICAV since inception.

Independent auditors

In accordance with Section 125 of the Irish Collective Asset-management Vehicles Act 2015 (the

“ICAV Act”), the Directors have appointed KPMG, Chartered Accountants and Registered Auditors,

as the ICAV’s auditor and have indicated their willingness to continue in office.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

DIRECTORS’ REPORT (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

7

Corporate Governance Code

The ICAV is subject to the requirements of the ICAV Act, the UCITS Regulations and the Central Bank

UCITS Regulations. The ICAV is subject to corporate governance practices imposed by:

1. The ICAV Act which is available for inspection at the registered office of the ICAV at,

3rd floor, 55 Charlemont Place, Dublin 2 D02 F985, Ireland; and may also be obtained: -

http://www.irishstatutebook.ie

2. The Instrument of Incorporation of the ICAV (“the Instrument”) which may be obtained at the

ICAVs Registration Office in Ireland and is available for inspection at the registered office of the

ICAV; and

3. The Central Bank UCITS Regulations and Guidance Notes which can be obtained from the Central

Bank of Ireland website at: -

http://www.centralbank.ie/regulation/industry-sectors/funds/Pages/default.aspx

The ICAV has adopted the voluntary Irish Funds Industry Association (Irish Funds) Corporate

Governance Code for Irish domiciled Collective Investment Schemes and Management Companies

(the “IF Code”). The Board of Directors have reviewed and assessed the measures included in the IF

Code and consider its corporate governance practices and procedures since the adoption of the IF

Code as consistent therewith.

Connected Persons

Regulation 43(1) of the UCITS Regulations “Restrictions on transactions with connected persons” states

that “A responsible person shall ensure that any transaction between a UCITS and a connected person is

conducted a) at arm’s length; and b) in the best interest of the unit-holders of the UCITS”.

As required under UCITS Regulation 81.4, the Directors of the Manager (the Responsible Person) are

satisfied that there are in place arrangements, evidenced by written procedures, to ensure that the

obligations that are prescribed by Regulation 43(1) are applied to all transactions with a connected

persons; and all transactions with a connected persons that were entered into during the financial period

to which the report relates complied with the obligations that are prescribed by Regulation 43(1).

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

DIRECTORS’ REPORT (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

8

UCITS ICAV: STATEMENT OF DIRECTORS’ RESPONSIBILITIES IN RESPECT OF

THE DIRECTORS’ REPORT AND THE FINANCIAL STATEMENTS

The directors are responsible for preparing the Directors’ Report and financial statements, in

accordance with applicable law and regulations.

The Irish Collective Asset-management Vehicles Acts 2015 and 2020 requires the directors to

prepare financial statements for each financial year. Under that law they have elected to prepare the

financial statements in accordance with International Financial Reporting Standards (IFRS) as

adopted by the EU and applicable law.

The financial statements are required to give a true and fair view of the assets, liabilities and financial

position of the ICAV at the end of the financial year and of the increase in net assets attributable to

holders of redeemable participating shares in the ICAV for the financial year. In preparing these

financial statements, the directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and estimates that are reasonable and prudent;

• state whether applicable Accounting Standards have been followed, subject to any material

departures disclosed and explained in the financial statements;

• assess the ICAV’s ability to continue as a going concern, disclosing, as applicable, matters related

to going concern; and

• use the going concern basis of accounting unless they either intend to liquidate the ICAV or to cease

operations or have no realistic alternative but to do so.

The directors are responsible for keeping adequate accounting records which disclose with

reasonable accuracy at any time the assets, liabilities, financial position and changes in net assets

attributable to holders of redeemable participating shares in the ICAV and enable them to ensure that

the financial statements comply with the Irish Collective Asset-management Vehicles Acts 2015 and

2020 and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings

for Collective Investment in Transferable Securities) Regulations 2019. They have general

responsibility for taking such steps as are reasonably open to them to safeguard the assets of the

ICAV. In this regard they have entrusted the assets of the ICAV to a depositary for safe-keeping.

They are responsible for such internal controls as they determine is necessary to enable the

preparation of financial statements that are free from material misstatement, whether due to fraud or

error, and to prevent and detect fraud and other irregularities. The directors are also responsible for

preparing a Directors’ Report that complies with the requirements of the Irish Collective Asset-

management Vehicles Acts 2015 and 2020.

The directors are responsible for the maintenance and integrity of the corporate and financial

information included on the ICAV’s website. Legislation in the Republic of Ireland governing the

preparation and dissemination of financial statements may differ from legislation in other

jurisdictions.

On behalf of the board

Sheila Rohan Fiona Mulcahy

Director Director

22 April 2024

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

KPMG

Audit

1 Harbourmaster Place

IFSC

Dublin 1

D01 F6F5

Ireland

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS OF CONNOR, CLARK & LUNN

UCITS ICAV

Report on the audit of the financial statements

Opinion

We have audited the financial statements of Connor, Clark

& Lunn UCITS ICAV (‘the ICAV’) for the

year ended December 31, 2023 set out on pages 13 to 48, which comprise the Statement of Financial

Position, Statement of Comprehensive Income, Statement of Changes in Net Assets attributable to

Holders of Redeemable Participating Shares, Statement of Cash Flows and related notes, including

the summary of significant accounting policies set out in note 2.

The financial reporting framework that has been applied in their preparation is Irish Law and

International Financial Reporting Standards (IFRS) as adopted by the European Union.

In our opinion:

-

the financial statements give a true and fair view of the assets, liabilities and financial position of

the ICAV as at December 31, 2023 and of its increase in net assets attributable to holders of

redeemable participating shares for the year then ended;

-

the financial statements have been properly prepared in accordance with IFRS as adopted by the

European Union; and

-

the financial statements have been properly prepared in accordance with the requirements of the

Irish Collective Asset-management Vehicles Acts 2015 to 2021 and the Central Bank (Supervision

and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in

Transferable Securities) Regulations 2019.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (Ireland) (ISAs

(Ireland)) and applicable law. Our responsibilities under those standards are further described in the

Auditor's responsibilities for the audit of the financial statements section of our report. We are

independent of the ICAV in accordance with ethical requirements that are relevant to our audit of

financial statements in Ireland, including the Ethical Standard issued by the Irish Auditing and

Accounting Supervisory Authority (IAASA), and we have fulfilled our other ethical responsibilities in

accordance with these requirements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis

for our opinion.

Conclusions relating to going concern

In auditing the financial statements, we have concluded that the directors’ use of the going concern

basis of accounting in the preparation of the financial statements is appropriate.

Based on the work we have performed, we have not identified any material uncertainties relating to

events or conditions that, individually or collectively, may cast significant doubt on the ICAV’s ability to

continue as a going concern for a period of at least twelve months from the date when the financial

statements are authorised for issue.

Our responsibilities and the responsibilities of the directors with respect to going concern are

described in the relevant sections of this report.

KPMG, an Irish partnership and a member firm of the KPMG global organisation of

independent member firms affiliated with KPMG International Limited, a private English

company limited by guarantee

10

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS OF CONNOR, CLARK & LUNN

UCITS ICAV (continued)

Other information

The directors are responsible for the other information presented in the Annual Report together with

the financial statements. The other information comprises the information included in the Directory,

Investment Manager’s report, Director’s report, Annual Depositary Report to the Shareholders,

Schedule of Investments and the Unaudited Appendices. The financial statements and our auditor’s

report thereon do not comprise part of the other information. Our opinion on the financial statements

does not cover the other information and, accordingly, we do not express

an audit opinion or, except

as explicitly stated below, any form of assurance conclusion thereon.

Our responsibility is to read the other information and, in doing so, consider whether, based on our

financial statements audit work, the information therein is materially misstated or inconsistent with the

financial statements or our audit knowledge. Based solely on that work undertaken during the course

of the audit, we have not identified material misstatements in the other information.

Opinion on other matter prescribed by the Irish Collective Asset-management Vehicles Acts

2015 to 2021

In our opinion, the information given in the Directors’ Report is consistent with the financial

statements.

Matters on which we are required to report by exception

The Irish Collective Asset-management Vehicles Acts 2015 to 2021 requires us to report to you, if in

our opinion, the disclosures of Directors’ remuneration specified by law are not made. We have

nothing to report in this regard.

Respective responsibilities and restrictions on use

Responsibilities of directors for the financial statements

As explained more fully in the directors’ responsibilities statement set out on page 8, the directors are

responsible for: the preparation of the financial statements including being satisfied that they give a

true and fair view; such internal control as they determine is necessary to enable the preparation of

financial statements that are free from material misstatement, whether due to fraud or error;

assessing the ICAV’s ability to continue as a going concern, disclosing, as applicable, matters related

to going concern; and using the going concern basis of accounting unless they either intend to

liquidate the ICAV or to cease operations, or have no realistic alternative but to do so.

Auditor’s responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole

are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report

that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee

that an audit conducted in accordance with ISAs (Ireland) will always detect a material misstatement

when it exists. Misstatements can arise from fraud or error and are considered material if, individually

or in the aggregate, they could reasonably be expected to influence the economic decisions of users

taken on the basis of these financial statements.

A fuller description of our responsibilities is provided on IAASA’s website at

https://iaasa.ie/publications/description-of-the-auditors-responsibilities-for-the-audit-of-the-financial-

statements/.

11

INDEP

ENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS OF CONNOR, CLARK & LUNN

UCITS ICAV (continued)

The purpose of our audit work and to whom we owe our responsibilities

Our report is made solely to the shareholders of the ICAV, as a body, in accordance with the Section

120 of the Irish Collective Asset-management Vehicles Act 2015. Our audit work has been

undertaken so that we might state to the ICAV’s shareholders those matters we are required to state

to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do

not accept or assume responsibility to anyone other than the ICAV and the ICAV’s shareholders, as a

body, for our audit work, for this report, or for the opinions we have formed.

22 April 2024

B

rian Clavin

for and on behalf

of KPMG

Chartered Accountants, Statutory Audit Firm

1 Harbourmaster Place

IFSC

Dublin 1

D01 F6F5

12

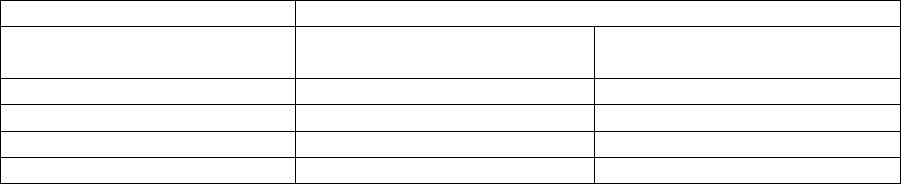

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 2023

13

TOTAL

CC&L Q

Emerging

Markets

Equity UCITS

Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2023

2023

2023*

Note

USD

USD

USD

Assets

Financial assets at fair value through

profit or loss

2(e), 3(a)

- Transferable securities

869,684,261

869,684,261

-

- Financial derivative instruments

1,486

1,486

-

Cash and cash equivalents

2(i)

3,394,602

3,394,602

-

Amounts due from broker

2(m)

3,572,292

3,572,292

-

Dividends receivable

1,706,382

1,706,382

-

Other receivables

15,159

15,159

-

Total assets

878,374,182

878,374,182

-

Liabilities

Bank overdraft

2(i)

2,193

2,193

-

Amounts due to broker

2(m)

4,729,711

4,729,711

-

Investment management fee payable

5(b)

1,175,584

1,175,584

-

Audit fee payable

5(i)

28,641

28,641

-

Management fees payable

5(a)

15,590

15,590

-

Capital gains tax payable

5(g)

4,280,871

4,280,871

-

Other payables

394,568

394,568

-

Total liabilities

10,627,158

10,627,158

-

Net assets attributable to the holders

of Redeemable Participating Shares

867,747,024

867,747,024

Net Asset Value per redeemable

participating shares

Class A

9.88

9.88

-

Class A EUR Distributing (in USD)

12.05

12.05

-

Class A EUR Distributing (in EUR)

10.91

10.91

-

*The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

Signed on behalf of the Board of Directors:

Sheila Rohan

…………………………….

Director:

Fiona Mulcahy

…………………………….

Director:

22 April 2024

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

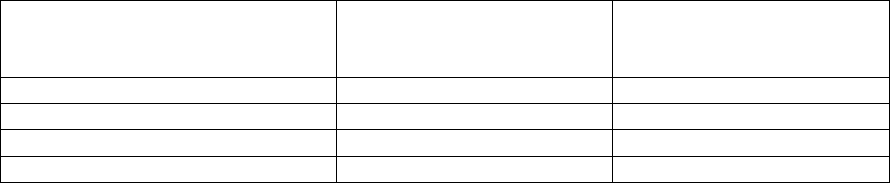

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF FINANCIAL POSITION (CONTINUED)

AS AT 31 DECEMBER 2022

14

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2022

2022

2022*

Note

USD

USD

USD

Assets

Financial assets at fair value through

profit or loss

2(e), 3(a)

- Transferable securities

168,281,892

168,281,892

-

- Financial derivative instruments

1,980

1,980

-

Cash and cash equivalents

2(i)

375,798

375,798

-

Amounts due from broker

2,429,781

2,429,781

-

Dividends receivable

273,773

273,773

-

Other receivables

10(a)

238,385

238,385

-

Total assets

171,601,609

171,601,609

-

Liabilities

Bank overdraft

2(i)

171,610

171,610

-

Amounts due to broker

2(m)

2,233,175

2,233,175

-

Investment management fee payable

5(b)

142,628

142,628

-

Audit fee payable

5(i)

25,930

25,930

-

Management fees payable

5(a)

7,939

7,939

-

Other payables

333,678

333,678

-

Total liabilities

2,914,960

2,914,960

-

Net assets attributable to the holders

of Redeemable Participating Shares

168,686,649

168,686,649

Net Asset Value per redeemable

participating shares

Class A

8.54

8.54

-

Class A EUR (in USD)

9.91

9.91

-

Class A EUR (in EUR)

9.29

9.29

-

*The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 DECEMBER 2023

15

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2023

2023

2023*

Note

USD

USD

USD

Income

Dividend income

2(g)

13,279,196

13,279,196

-

Interest income

7,260

7,260

-

Other income

1,251,037

1,251,037

-

Net gain on financial assets and

liabilities at fair value through profit

or loss

3(b)

81,093,512

81,093,512

-

Net foreign exchange loss

(1,164,843)

(1,164,843)

-

Total income

94,466,162

94,466,162

-

Expenses

Investment management fees

5(b)

3,862,033

3,862,033

-

Management fees

5(a)

118,091

118,091

-

Administration fees

5(c)

394,619

394,619

-

Depositary fees

5(d)

705,548

705,548

-

Transaction costs

5(i)

1,584,399

1,584,399

-

Audit fees

5(j)

30,715

30,715

-

Director fees

5(e)

51,908

51,908

-

Other expenses

170,004

170,004

-

Total expenses

6,917,317

6,917,317

-

Net gain before finance costs and tax

87,548,845

87,548,845

-

Finance costs

Interest expense

62,453

62,453

-

Net gain before tax

87,486,392

87,486,392

-

Withholding tax on dividends

1,531,923

1,531,923

-

Capital gains tax

5,175,514

5,175,514

-

Net increase in net assets from

operations attributable to the

holders of Redeemable Participating

Shares

80,778,955

80,778,955

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF COMPREHENSIVE INCOME (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2022

16

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2022

2022

2022*

Note

USD

USD

USD

Income

Dividend income

2(g)

3,705,290

3,705,290

-

Interest income

363

363

-

Other income

10(a)

382,945

382,945

-

Net gain on financial assets and

liabilities at fair value through profit

or loss

3(b)

(16,647,305)

(16,647,305)

-

Net foreign exchange loss

(153,707)

(153,707)

-

Total income

(12,712,414)

(12,712,414)

-

Expenses

Investment management fees

5(b)

995,248

995,248

-

Management fees

5(a)

44,718

44,718

-

Administration fees

5(c)

129,618

129,618

-

Depositary fees

5(d)

371,125

371,125

-

Transaction costs

5(h)

414,354

414,354

-

Audit fees

5(i)

25,104

25,104

-

Director fees

5(e)

50,011

50,011

-

Other expenses

222,774

222,774

-

Total expenses

2,252,952

2,252,952

-

Net loss before finance costs and tax

(14,965,366)

(14,965,366)

-

Finance costs

Interest expense

(11,870)

(11,870)

-

Net loss before tax

(14,977,236)

(14,977,236)

-

Withholding tax on dividends

(431,707)

(431,707)

-

Capital gains tax

(28,596)

(28,596)

-

Net decrease in net assets from

operations attributable to the

holders of Redeemable Participating

Shares

(15,437,539)

(15,437,539)

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF CHANGES IN NET ASSETS ATTRIBUTABLE TO HOLDERS OF

REDEEMABLE PARTICIPATING SHARES

FOR THE YEAR ENDED 31 DECEMBER 2023

17

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2023

2023

2023*

USD

USD

USD

Net assets attributable to holders of

redeemable participating shares at the

beginning of the year

168,686,649

168,686,649

-

Increase in net assets from operations

attributable to holders of Redeemable

Participating Shares

80,778,955

80,778,955

-

Issuance of Redeemable Participating

Shares

674,652,607

674,652,607

-

Redemption of Redeemable

Participating Shares

(56,371,187)

(56,371,187)

-

Net assets attributable to the holders

of Redeemable Participating Shares

at the end of the year

867,747,024

867,747,024

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF CHANGES IN NET ASSETS ATTRIBUTABLE TO HOLDERS OF

REDEEMABLE PARTICIPATING SHARES (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2022

18

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2022

2022

2022*

USD

USD

USD

Net assets attributable to holders of

redeemable participating shares at the

beginning of the year

105,383,072

105,383,072

-

Decrease in net assets from operations

attributable to holders of Redeemable

Participating Shares

(15,437,539)

(15,437,539)

-

Issuance of Redeemable Participating

Shares

78,741,116

78,741,116

-

Net assets attributable to the holders

of Redeemable Participating Shares

at the end of the year

168,686,649

168,686,649

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 31 DECEMBER 2023

19

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2023

2023

2023*

USD

USD

USD

Cash flows from operating activities

attributable to the holders of Redeemable

Participating Shares

Net increase in net assets attributable to the

holders of Redeemable Participating Shares

80,778,955

80,778,955

-

Adjustments to reconcile income attributable

to Redeemable Participating shareholders to

net cash provided by operating activities:

Net gain on financial assets at fair value

through profit or loss

(81,093,512)

(81,093,512)

-

Purchase of investment in securities

(1,107,704,280)

(1,107,704,280)

-

Proceeds from sale of investment in securities

487,395,917

487,395,917

-

Increase in dividend receivable

(1,432,609)

(1,432,609)

-

Increase in due from broker

(1,142,511)

(1,142,511)

-

Decrease in other receivables

223,226

223,226

-

Increase in investment management fees

payable

1,032,956

1,032,956

-

Increase in management fees payable

7,651

7,651

-

Increase in due to brokers

2,496,536

2,496,536

-

Increase in audit fees payable

2,711

2,711

-

Increase in other payables

4,341,761

4,341,761

-

Net cash outflow from operating activities

(615,093,199)

(615,093,199)

-

Cash flows from financing activities

Proceeds from issuance of shares

674,652,607

674,652,607

-

Redemption of shares

(56,371,187)

(56,371,187)

-

Net cash inflow from financing activities

618,281,420

618,281,420

-

Net increase in cash and cash equivalents

3,188,221

3,188,221

-

Cash and cash equivalents at beginning of the

year

204,188

204,188

-

Cash and cash equivalents at end of the year

3,392,409

3,392,409

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF CASH FLOWS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

20

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2023

2023

2023*

USD

USD

USD

Cash and cash equivalents at end of the year

is comprised of :

Cash and cash equivalents

3,394,602

3,394,602

-

Bank overdraft

(2,193)

(2,193)

-

Cash and cash equivalents at end of the year

3,392,409

3,392,409

-

Supplemental disclosure of cash flow

information:

Dividends received (net of withholding tax)

10,379,575

10,379,575

-

Interest received (net of withholding tax)

7,260

7,260

-

Interest paid

(62,453)

(62,453)

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF CASH FLOWS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2022

21

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2022

2022

2022*

USD

USD

USD

Cash flows from operating activities

attributable to the holders of Redeemable

Participating Shares

Net Decrease in net assets attributable to the

holders of Redeemable Participating Shares

(15,437,539)

(15,437,539)

-

Adjustments to reconcile income attributable

to Redeemable Participating shareholders to

net cash provided by operating activities:

Net loss on financial assets at fair value

through profit or loss

16,647,305

16,647,305

-

Purchase of investment in securities

(251,307,122)

(251,307,122)

-

Proceeds from sale of investment in securities

171,266,336

171,266,336

-

Increase in dividend receivable

(45,284)

(45,284)

-

Increase in due from broker

(1,202,042)

(1,202,042)

-

Increase in other receivables

(23,140)

(23,140)

-

Decrease in investment management fees

payable

(21,270)

(21,270)

-

Decrease in management fees payable

(215)

(215)

-

Increase in due to brokers

1,607,339

1,607,339

-

Decrease in audit fees payable

(1,248)

(1,248)

-

Decrease in other payables

(58,664)

(58,664)

-

Net cash outflow from operating activities

(78,575,544)

(78,575,544)

-

Cash flows from financing activities

Proceeds from issuance of shares

78,741,116

78,741,116

-

Net cash inflow from financing activities

78,741,116

78,741,116

-

Net decrease in cash and cash equivalents

165,572

165,572

-

Cash and cash equivalents at beginning of the

year

38,616

38,616

-

Cash and cash equivalents at end of the year

204,188

204,188

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

STATEMENT OF CASH FLOWS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2022

22

TOTAL

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund

2022

2022

2022*

USD

USD

USD

Cash and cash equivalents at end of the year

is comprised of :

Cash and cash equivalents

375,798

375,798

-

Bank overdraft

(171,610)

(171,610)

-

Cash and cash equivalents at end of the year

204,188

204,188

-

Supplemental disclosure of cash flow

information:

Dividends received (net of withholding tax)

3,234,170

3,234,170

-

Interest received (net of withholding tax)

363

363

Interest paid

(11,870)

(11,870)

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The accompanying notes form an integral part of these financial statements

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2023

23

1. General information

Connor, Clark & Lunn UCITS ICAV (the “ICAV”) was registered in Ireland pursuant to the Irish

Collective Asset-Management Vehicles Act 2015 on 7 October 2019 under registration number

C400076. The ICAV has been authorised by the Central Bank of Ireland (the “Central Bank”) as an

“Undertaking for Collective Investment in Transferable Securities” (“UCITS”) under the European

Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011

(as amended) (“UCITS Regulations”) and has been established as an Irish collective asset-management

vehicle constituted as an umbrella fund with segregated liability between Funds and will comply with

the Central Bank UCITS Regulations.

As at the date of this report, the ICAV comprised of two Sub-Funds – one active Sub-Fund CC&L Q

Emerging Markets Equity UCITS Fund (the “EME Sub-Fund”) and one inactive Sub-Fund CC&L Q

Global Equity Market Neutral UCITS Fund together, (the “Sub-Funds”). The Sub-Funds were

authorised as a UCITS by the Central Bank under the UCITS Regulations on 9 April 2020. The

investment objective of CC&L Q Emerging Markets Equity UCITS Fund is to seek long-term growth

of capital relative to emerging market equity indices by structuring and maintaining a diversified

portfolio of primarily emerging market equity securities. The Investment objective of CC&L Q Global

Equity Market Neutral UCITS Fund is to generate returns that have a low correlation with global equity

markets and to maximise long-term total return.

CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

The ICAV has appointed Carne Global Fund Managers (Ireland) Limited (the “Manager”) as Manager

of the ICAV pursuant to the Management agreement. Connor, Clark & Lunn Investment Management

Ltd. (the “Investment Manager”) was appointed as the Investment Manager of the ICAV providing

discretionary investment management and advisory services in relation to the ICAV. Connor, Clark &

Lunn UK Limited is the promoter of the ICAV. Connor, Clark & Lunn UK Limited’s principal business

and occupation is to provide distribution services to clients.

2. Material Accounting Policies

The material accounting policies adopted by the ICAV in the preparation of these financial statements

are set out below. The Company adopted 'Disclosure of Accounting Policies (Amendments to IAS 1

and IFRS Practice Statement 2)’ from 1 January 2023. The amendments require the disclosure of

'material' rather than 'significant' accounting policies. The amendments did not result in any changes in

accounting policies themselves

(a) Basis of accounting

The financial statements have been prepared in accordance with International Financial Reporting

Standards (“IFRS”) as adopted for use in the European Union, Irish statute comprising the ICAV Act

2015 and the Central Bank UCITS Regulations.

(b) Basis of measurement

The financial statements have been prepared on a going concern basis, applying the historical cost

convention, except for the financial instruments at fair value through profit or loss.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

24

2. Material Accounting Policies (continued)

(c) Judgements

(i) Going Concern

These financial statements have been prepared on a going concern basis as the Directors have made an

assessment of the ICAV’s ability to continue as a going concern and are satisfied that the ICAV has

the resources to continue for the foreseeable future.

(ii) Functional and presentation currency

The Board of Directors considers the US Dollar the currency that most faithfully represents the

economic effect of the underlying transactions, events and conditions. The US Dollar is the currency

in which the ICAV measures its performance and reports its results, as well as the currency in which it

principally receives subscriptions and redemptions from its investors. The ICAV has also adopted the

US Dollar as its presentation currency.

The preparation of financial statements in conformity with IFRS requires management to make

judgements, estimates and assumptions that affect the application of policies and the reported amounts

of assets and liabilities, income and expense. The estimates and associated assumptions are based on

historical experience and various other factors that are believed to be reasonable under the

circumstances, the results of which form the basis of making the judgements about carrying values of

assets and liabilities that are not readily apparent from other sources. If in the future such estimates and

assumptions, which are based on management's best judgement at the date of the financial statements

deviate from the actual outcome, the original estimates and assumptions will be modified as appropriate

in the financial year in which the circumstances change.

(d) Changes in accounting policies and disclosures

New standards, amendments and interpretations effective from 1 January 2023.

New or amended standards

Impact on Financial Statements

Insurance Contracts (Amendments to

IFRS 17)

The application of the Amendment resulted in

no significant changes to the ICAV’s Financial

Statements.

Definition of Accounting Estimates

(Amendments to IAS 8)

The application of the Amendment resulted in

no significant changes to the ICAV’s Financial

Statements.

Disclosure of Accounting Policies

(Amendments to IAS 1 and IFRS Practice

Statement 2)

The application of the Amendment resulted in

no significant changes to the ICAV’s Financial

Statements.

Deferred Tax related to Assets and Liabilities

arising from a Single Transaction

(Amendments to IAS 12)

The application of the Amendment resulted in

no significant changes to the ICAV’s Financial

Statements.

None of the accounting standards had a material effect on the financial statements.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

25

2. Material Accounting Policies (continued)

(d) Changes in accounting policies and disclosures (continued)

New standards, amendments and interpretations effective for future reporting financial periods

that have not been early adopted

A number of new standards are effective for annual periods beginning after 1 January 2023 and earlier

application is permitted, however the ICAV has not adopted the new or amended standards early in

preparing these Financial Statements.

The following amended standards and interpretations are not expected to have a significant impact on

the ICAV's Financial Statements:

• Classification of Liabilities as Current or Non-current - Amendments to IAS 1 - effective 1 January

2024;

• Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendments

to IFRS 10 and IAS 28 - no effective date yet.

(e) Financial assets and liabilities designated at fair value through profit or loss

(i) Classification

In accordance with IFRS 9, the ICAV classifies its financial assets and financial liabilities at initial

recognition into the categories of financial assets and financial liabilities discussed below.

In applying that classification, a financial asset or financial liability is considered to be held for trading

if:

a) It is acquired or incurred principally for the purpose of selling or repurchasing it in the near term;

b) On initial recognition, it is part of a portfolio of identified financial instruments that are managed

together and for which, there is evidence of a recent actual pattern of short-term profit-taking; or

c) It is a derivative (except for a derivative that is a financial guarantee contract or a designated and

effective hedging instrument).

Financial assets

The ICAV classifies its financial assets as subsequently measured at amortised cost or measured at fair

value through profit or loss on the basis of both:

• The entity’s business model for managing the financial assets

• The contractual cash flow characteristics of the financial asset

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

26

2. Material Accounting Policies (continued)

(e) Financial assets and liabilities designated at fair value through profit or loss (continued)

(i) Classification (continued)

Financial assets at fair value through profit or loss

A financial asset is measured at fair value through profit or loss if:

(a) Its contractual terms do not give rise to cash flows on specified dates that are solely payments of

principal and interest (SPPI) on the principal amount outstanding; or

(b) It is not held within a business model whose objective is either to collect contractual cash flows, or

to both collect contractual cash flows and sell; or

At initial recognition, it is irrevocably designated as measured at fair value through profit or loss when

doing so eliminates or significantly reduces a measurement or recognition inconsistency that would

otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on

different bases. The Fund classifies its investments based on both Fund’s business model for managing

those financial assets and the contractual cash flow characteristics of the financial assets. The portfolio

of financial assets is managed and performance is evaluated on a fair value basis. The Fund is primarily

focused on fair value information and uses that information to assess the assets’ performance and to

make decisions. All investments are measured and evaluated by the Investment Manager on a fair value

basis. The fair value of investments is examined on a regular basis.

Financial liabilities at fair value through profit or loss

A financial liability is measured at fair value through profit or loss if it meets the definition of held for

trading. The ICAV includes in this category derivative contracts in a liability position and investments

in securities sold short since they are classified as held for trading.

Financial assets at amortised cost

Loans and receivables are measured at amortised cost. The ICAV includes in this category cash and

cash equivalents, amounts due from brokers and other short-term receivables.

Financial liabilities at amortised cost

This category includes all financial liabilities, other than those measured at fair value through profit or

loss. The ICAV includes in this category bank overdraft, amounts due to brokers and other short-term

payables.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

27

2. Material Accounting Policies (continued)

(e) Financial assets and liabilities designated at fair value through profit or loss (continued)

(ii) Recognition

The ICAV recognises a financial asset or a financial liability when, and only when, it becomes a party

to the contractual provisions of the instrument.

Purchases or sales of financial assets that require delivery of assets within the time frame generally

established by regulation or convention in the marketplace are recognised on the trade date, i.e., the

date that the ICAV commits to purchase or sell the asset.

(iii) Subsequent measurement

After initial measurement, the ICAV measures financial instruments which are classified as at fair value

through profit or loss, at their fair values. Fair value is the amount for which an asset could be

exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction.

The fair value of financial instruments traded in an active market is based on their quoted market prices

on a recognised exchange or sourced from a reputable broker/counterparty, in the case of non-exchange

traded instruments, at the reporting date without any deduction for estimated future selling costs.

Financial assets and liabilities are stated at market value based on the last traded price within the bid

ask spread on each valuation date.

If a quoted market price is not available on a recognised stock exchange or from a reputable

broker/counterparty, the fair value of the financial instruments may be estimated by the Directors using

appropriate valuation techniques, including use of recent arm’s length market transactions, reference

to the current fair value of another instrument that is substantially the same, discounted cash flow

techniques, or any other valuation technique that provides a reliable estimate of prices obtained in

actual market transactions.

Subsequent changes in the fair value of financial instruments at fair value through profit or loss are

recognised in the Statement of Comprehensive Income (“SOCI”).

An analysis of fair values of financial instruments and further details as to how they are measured are

provided in Note 4.

Financial instruments, other than those at fair value through profit or loss, are measured at amortised

cost using the effective interest rate method, less any impairment for financial assets. Gains and losses

are recognised in profit or loss when the liabilities are derecognised, as well as through the amortisation

process.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

28

2. Material Accounting Policies (continued)

(e) Financial assets and liabilities designated at fair value through profit or loss (continued)

(iv) Derecognition

A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial

assets) is derecognised where:

- The rights to receive cash flows from the asset have expired; or

- The ICAV has transferred its rights to receive cash flows from the asset or has assumed an obligation

to pay the received cash flows in full without material delay to a third party under a ‘pass-through’

arrangement; and

- either (a) the ICAV has transferred substantially all the risks and rewards of the asset, or (b) the ICAV

has neither transferred nor retained substantially all the risks and rewards of the asset, but has

transferred control of the asset.

When the ICAV has transferred its rights to receive cash flows from an asset (or has entered into a

pass-through arrangement), and has neither transferred nor retained substantially all the risks and

rewards of the asset nor transferred control of the asset, the asset is recognised to the extent of the

ICAV’s continuing involvement in the asset. The ICAV derecognises a financial liability when the

obligation under the liability is discharged, cancelled or expires.

(v) Impairment

IFRS 9 requires the ICAV to record expected credit losses (ECLs) on all of its short-term receivables,

either on a 12-month or lifetime basis. Given the limited exposure of the ICAV to credit risk, this

amendment has not had a material impact on the financial statements. The ICAV only holds short-term

receivables with no financing component and that have maturities of less than 12 months at amortised

cost. Therefore, it has adopted an approach similar to the simplified approach to ECLs.

(f) Foreign currency translation

Monetary assets and liabilities denominated in currencies other than the presentation currency are

translated into the presentation currency at the closing rates of exchange at financial year end.

Transactions during the financial year, including purchases and sales of securities, income and

expenses, are translated at the rate of exchange prevailing on the date of the transaction. Foreign

exchange gains and losses arising from translation are included in the SOCI. Foreign exchange

gains/losses relating to cash and cash equivalents are presented in the SOCI within “Net foreign

exchange loss” and foreign exchange gains/losses relating to financial assets and liabilities carried at

fair value through profit or loss are presented in the SOCI within “Net gain on financial assets and

liabilities at fair value through profit or loss”.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

29

2. Material Accounting Policies (continued)

(g) Income

Dividend income is credited to the SOCI on the date on which the relevant securities are listed as “ex-

dividend”. Dividend income is shown gross of any non-recoverable withholding taxes, which are

disclosed separately in the SOCI, and net of any tax credits. The Dividend income for the financial year

ended 31 December 2023 amounted to USD 13,279,196 (2022: USD 3,705,290)

(h) Expenses

Expenses are accounted for on an accruals basis and are charged to the SOCI when incurred.

(i) Cash and cash equivalents

Cash and cash equivalents include current and call accounts with maturities of three months or less.

Cash comprises of cash held with HSBC Bank Plc (Standard & Poor: A+) (2022: Standard & Poor:

A+). Cash and cash equivalents at 31 December 2023 was USD3,394,602 (2022: USD375,798) and

the bank overdraft was USD2,193 (2022: USD171,610).

(j) Dividend distribution

The Directors retain the right to declare dividends in respect of net investment income on the Sub-

Funds' investments in their sole discretion. In the event that the Directors determine to declare

dividends in respect of any class in the Sub-Fund, Shareholders will be notified in advance of any such

change in the dividend policy, including the date by which dividends will be paid and the method by

which dividends will be paid.

(k) Taxation

The IFRS Interpretations Committee (“IFRIC”) published a new interpretation IFRIC 23 ‘Uncertainty

over Income Tax Treatments’, specifying how entities should reflect uncertainty in accounting for

income taxes. IFRIC 23 addresses the previous lack of guidance in IAS 12 ‘Income Taxes’, which

specifies how to account for current and deferred tax, but not how to reflect the effects of uncertainty.

The Investment Manager evaluated the effect of IFRIC 23 and deemed that it did not have a significant

impact on the financial statements since the majority of the Fund’s financial instruments are, in the

opinion of the Investment Manager, not subject to material uncertain tax treatment.

Under current law and practice the ICAV qualifies as an investment undertaking as defined in Section

739B of the Taxes Consolidation Act, 1997, as amended. As such, it is not chargeable to Irish tax on

its income or gains.

However, Irish tax may arise on the happening of a “chargeable event”. A chargeable event includes

any distribution payments to shareholders or any encashment, redemption, cancellation or transfer of

shares.

No Irish tax will arise on the ICAV regarding chargeable events in respect of a Shareholder who is

neither Irish Resident nor Ordinarily Resident in Ireland at the time of the chargeable event provided

that a Relevant Declaration is in place and the ICAV is not in possession of any information which

would reasonably suggest that the information contained therein is no longer materially correct.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

30

2. Material Accounting Policies (continued)

(k) Taxation (continued)

A Chargeable Event does not include:

(i) any transaction in relation to Shares held in a recognised clearing system;

(ii) any exchange by a Shareholder effected by way of a bargain made at arm’s length by the ICAV, of

Shares in the ICAV for other Shares in the ICAV;

(iii) certain transfers of Shares between spouses or civil partners and former spouses or former civil

partners;

(iv) an exchange of Shares arising on a qualifying amalgamation or reconstruction of the ICAV with

another Irish investment undertaking; or

(v) the cancellation of Shares in the ICAV arising from an exchange in relation to a scheme of

amalgamation.

Income, interest and capital gains (if any) received on investments made by the ICAV may be subject

to withholding taxes imposed by the country from which the investment amounts are received and such

taxes may not be recoverable by the ICAV or its shareholders.

(l) Transaction costs

Transaction costs are incremental costs, which are separately identifiable and directly attributable to

the acquisition, issue or disposal of a financial asset or financial liability. Transaction costs for all

financial assets carried at fair value through profit and loss are included in the Statement of

Comprehensive Income. These include fees and commissions paid to brokers and counterparties and

have been classified within gains and losses. Transaction fees paid to the Depositary on trade settlement

are expensed as incurred and included in the Statement of Comprehensive Income. Transaction costs

are detailed in Note 5.

(m) Due to/from broker

Amounts due from/to brokers represent receivables for securities sold and payables for securities

purchased that have been contracted for but not yet delivered by the end of the year. Amounts due from

broker at 31 December 2023 was USD3,572,292 (2022: USD2,429,781) and Amounts due to broker

was USD4,729,711 (2022: USD2,233,175).

(n) Net gain/(loss) from financial assets and liabilities at fair value through profit or loss

Net gain/(loss) from financial assets and liabilities at fair value through profit or loss includes all

realized and unrealized fair value changes and foreign exchange differences, interest and dividend

income, including dividend expenses on securities sold short, if any.

(o) Redeemable participating shares

The redeemable participating shares are classified as financial liabilities at amortized cost and are

measured at the present value of the redemption amount.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

31

2. Material Accounting Policies (continued)

(p) Subscriber shares

The subscriber shares (classified as equity) of no par value are issued for €1.00 each. The Subscriber

Shares entitle the Shareholders holding them to attend and vote at all meetings of the ICAV, but do not

entitle the holders to participate in the dividends or net assets of any Sub-Funds.

3. (a) Financial assets and liabilities at fair value through profit or loss

Total

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund*

2023

31 December 2023

31 December 2023

USD

USD

USD

Financial assets at fair value through

profit or loss

Transferable securities

- Equities

771,653,569

771,653,569

-

- Depositary Receipts

98,030,692

98,030,692

-

869,684,261

869,684,261

-

Financial derivatives

- Warrants

1,486

1,486

-

Total financial assets at fair value

through profit or loss

869,685,747

869,685,747

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

Total

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund*

2022

31 December 2022

31 December 2022

USD

USD

USD

Financial assets at fair value through

profit or loss

Transferable securities

- Equities

136,951,726

136,951,726

-

- Depositary Receipts

31,329,707

31,329,707

-

- Rights

459

459

-

168,281,892

168,281,892

-

Financial derivatives

- Warrants

1,980

1,980

-

Total financial assets at fair value

through profit or loss

168,283,872

168,283,872

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

32

3. (b) Realised/unrealised gain/(loss) on financial assets and liabilities at fair value through

profit or loss

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund*

Total

For the year

ended

31 December

2023

For the year

ended

31 December

2023*

USD

USD

USD

Realised gain on financial assets and

liabilities at fair value through profit or loss

Gain on Equities

5,777,876

5,777,876

-

Gain on Depositary Receipts

6,121,335

6,121,335

-

Net realised gain on financial assets and

liabilities at fair value through profit or loss

11,899,211

11,899,211

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund*

Total

USD

For the year

ended

31 December

2023

USD

For the year

ended

31 December

2023*

USD

Unrealised gain/(loss) on financial assets

and liabilities a fair value through profit or

loss

Gain on Equities

62,187,087

62,187,087

-

Gain on Depositary Receipts

7,007,708

7,007,708

-

Loss on Warrants

(494)

(494)

-

Net unrealised gain on financial assets and

liabilities at fair value through profit or loss

69,194,301

69,194,301

-

Net gain on financial assets and liabilities at

fair value through profit or loss

81,093,512

81,093,512

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

DocuSign Envelope ID: B78383A0-3257-4CFB-A83C-8B89A908EDE1

CONNOR, CLARK & LUNN UCITS ICAV

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR ENDED 31 DECEMBER 2023

33

3. (b) Realised/unrealised gain/(loss) on financial assets and liabilities at fair value through

profit or loss (continued)

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund*

Total

For the period

ended

31 December 2022

For the period

ended

31 December 2022

USD

USD

USD

Realised loss on financial assets and

liabilities at fair value through profit or loss

Loss on Equities

(6,341,360)

(6,341,360)

-

Loss on Depositary Receipts

(6,218,065)

(6,218,065)

-

Net realised loss on financial assets and

liabilities at fair value through profit or

loss

(12,559,425)

(12,559,425)

-

* The CC&L Q Global Equity Market Neutral UCITS Fund was not launched during the year.

CC&L Q

Emerging

Markets Equity

UCITS Fund

CC&L Q

Global Equity

Market Neutral

UCITS Fund*

Total

For the period

ended

31 December

2022

For the period

ended

31 December

2022

USD

USD

USD

Unrealised gain/(loss) on financial assets

and liabilities a fair value through profit or

loss

Loss on Equities

(5,015,341)

(5,015,341)

-

Gain on Depositary Receipts

925,481

925,481

-

Gain on warrants

1,980

1,980

Net unrealised loss on financial assets and

liabilities at fair value through profit or loss

(4,087,880)

(4,087,880)

-

Net loss on financial assets and liabilities at

fair value through profit or loss

(16,647,305)

(16,647,305)

-