CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Semi

-Annual Report of the

Consumer Financial

Protection Bureau

1 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Table of Contents

Table of Contents ........................................................................................................1

Division Reporting.......................................................................................................2

Consumer Education and External Affairs........................................................ 2

Office of Equal Opportunity and Fairness ...................................................... 11

Operations....................................................................................................... 22

Research, Markets and Regulations ................................................................ 29

Supervision, Enforcement and Fair Lending ................................................... 45

Appendix .....................................................................................................................87

Annual report on the Truth in Lending Act, the Electronic Fund Transfer Act,

and the Credit Card Accountability Responsibility and Disclosure Act.......... 87

Public enforcement actions and reimbursements – TILA, EFTA,

CARD Act ....................................................................................................................88

TILA: Public enforcement actions and reimbursements ................................. 88

EFTA: Public enforcement actions and reimbursements ................................ 91

CARD Act: Public enforcement actions and reimbursements ......................... 96

Outreach related to TILA and EFTA........................................................................98

List of Director remarks from speaking engagements during the reporting

period .............................................................................................................. 99

Congressional engagement activity............................................................... 100

2 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Division Reporting

Consumer Education and External Affairs

The Consumer Education and External Affairs (CEEA) Division seeks to protect and promote

the financial well-being of consumers and strengthen the CFPB’s work and impact through broad

and consistent engagement with the public.

Significant problems faced by consumers in shopping for or

obtaining consumer financial products or services

The effect of the COVID-19 pandemic on accuracy in tenant screening reports. Income

shocks from the COVID-19 pandemic contributed to an increase in housing and financial

insecurity for many households, particularly for renters.

1

Some data and estimates

indicated that millions of renter households were at risk of eviction over the course of the

pandemic.

2

Federal, state, and local actions were taken to alleviate the rental housing-

related impacts of the pandemic. However, public reports as well as complaints to the

CFPB indicated that some tenants were being evicted in violation of applicable

moratoria. Consumers also expressed concern about questionable debt collection

activities following eviction.

3

The CFPB is concerned all of these factors are likely to

lead to an increase in negative rental information in the consumer reporting system,

which, combined with an increase in the number of consumers seeking new rental

housing, could create new risks that inaccurate negative rental information will be

included in tenant screening reports and such inaccuracies could impair the ability of

renters, negatively impacted by the pandemic, to secure new rental housing and otherwise

recover from the pandemic’s economic effects.

In response, the CFPB issued an enforcement compliance bulletin noting that the CFPB

will continue to look carefully at consumer reporting agencies’ and furnishers’

compliance with the FCRA accuracy obligations relating to rental information, and

1

https://files.consumerfinance.gov/f/documents/cfpb_Housing_insecurity_and_the_COVID-19_pandemic.pdf.

2

https://www.aspeninstitute.org/blog-posts/the-covid -19-eviction-crisis-an-estimated-30-40-million-peop le-in-america-are-at-

risk/.

3

Consumer Fin. Prot. Bureau, Complaint Bulletin: COVID-19 issues described in consumer complaints (July 2021),

https://files.consumerfinance.gov/f/documents/cfpb_covid-19-issues-described-consumercomplaints_complaint-bulletin_2021-

07.pdf (CFPB Complaint Bulletin).

3 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

outlined specific areas of focus and concern.

4

The CFPB also issued a consumer-facing

blog entitled, Errors in your tenant screening report shouldn’t keep you from finding a

place to call home, as well as new consumer education content to help consumers

understand their tenant screening reports and how to dispute and correct errors.

5

Consumer use of Buy Now, Pay Later products. Public reports have indicated a dramatic

increase in the number of consumers using Buy Now, Pay Later products, particularly for

online purchases.

6

Some reports have also indicated that some consumers are struggling

to make payments on time, resulting in late fees;

7

experiencing a drop in their credit score

after using these products;

8

facing difficulties returning goods purchased using a BNPL

product;

9

and are potentially unaware that these products lack some consumer protections

provided by credit cards.

10

In July 2021, the CFPB published a blog for consumers

entitled, Should you buy now and pay later?

11

The blog describes how these products

work, in general, and benefits and risks that consumers should consider before deciding

whether to use such a product. The blog also included specific information for

servicemembers as part of Military Consumer Protection Month.

12

Credit and consumer reporting. From January 2020 to September 2021, the CFPB

received more than 800,000 credit or consumer reporting complaints. Of these

complaints, more than 700,000 were submitted about Equifax, Experian, or TransUnion.

Complaints submitted about these companies accounted for more than 50 percent of all

complaints received by the CFPB in 2020 and more than 60 percent in 2021. In their

complaints to the CFPB, consumers describe harms stemming from their failed attempts

to correct incomplete and inaccurate information on their credit reports (e.g., consumers

are caught in an automated system where they are unable to have their problem

addressed; consumers waste time, energy, and money to try to correct their reports). In

4

https://files.consumerfinance.gov/f/documents/cfpb_consumer-reporting-rental-information_bulletin-2021-03_2021-07.pdf.

5

https://www.consumerfinance.gov/about-us /blog/errors-in-your-tenant-screening-report-s houldnt-keep-you-fro m-finding-a-

place-to-call-home/

6

https://www.cutoday.info/Fresh-Today/Study-Suggests-The-Explosive-Growth-in-Buy-Now-Pay-Later-is-Just-Going-to-Keep-

Exploding.

7

https://www.creditkarma.com/insights/i/buy-now-pay-later-missed-payments.

8

https://www.creditkarma.com/insights/i/buy-now-pay-later-missed-payments.

9

https://www.consumerreports.org/shopping-retail/hidden-risks-of-buy-now-pay-later-plans-a7495893275/.

10

https://www.consumerreports.org/shopping-retail/hidden-risks-of-buy-no w-pay-later-plans-a7495893275/.

11

https://www.consumerfinance.gov/about-us /blog/s hould-you-buy-now-and-pay-later/..

12

Additional activity has occurred since the end of the reporting period. More information can be found here: Know before you

buy (now, pay later) this holiday season | Consumer Financial Protection Bureau (consumerfinance.gov).

4 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

January 2022, the CFPB published the annual report of credit and consumer reporting

complaints.

13

This report analyzed how Equifax, Experian, and TransUnion respond to

complaints, including complaints they are required to respond to under the Fair Credit

Reporting Act (FCRA).

Significant initiatives

Appraisal Bias. On June 15, 2021, the CFPB hosted a roundtable examining racial bias in

home appraisals. The roundtable included participants from partner agencies, including

the National Credit Union Administration (NCUA), the Office of the Comptroller of the

Currency (OCC), and the Department of Housing and Urban Development (HUD). Also

participating in the roundtable were experts who spoke about how unconscious biases can

play out in the appraisal process as well as civil rights activists, consumer advocates, and

local leaders who described the biases they see in their communities every day. They

offered valuable insights and creative ideas, sparking important conversations across the

Federal government about how we can work together with stakeholders to tackle racial

bias and other inequities in housing.

Housing Insecurity – Public Awareness and Education Campaign.

14

During the reporting

period, the CFPB’s housing insecurity efforts expanded into a comprehensive, cross-

federal campaign aimed at connecting homeowners and renters facing housing insecurity

due to the COVID-19 pandemic with the resources available to help them stay in their

homes. The CFPB continued its partnership with the Department of Agriculture, the

Department of Housing and Urban Development, the Department of the Treasury, the

Department of Veterans Affairs, and the Federal Housing Finance Agency on a federal

interagency Housing Portal within ConsumerFinance.gov. Resources include information

on forbearance, foreclosure, eviction prevention, and specific action consumers can take

to utilize protections to stay in their homes. The Housing Portal received regular

enhancements as legal protections changed, key deadlines shifted, and user research

highlighted ways the CFPB could improve its offerings to consumers in need, ultimately

creating ConsumerFinance.gov’s most visited material. In July 2021, the CFPB launched

a Rental Assistance Finder Tool to help consumers find their local programs disbursing

emergency rental assistance made available through the Consolidated Appropriations Act

(2021) and the American Rescue Plan Act of 2021. The launch of this tool was the most

successful product launch in the CFPB’s history; in only two months (when the reporting

period for this report closes) users engaged the tool through more than 3.1 million

14

https://www.consumerfinance.gov/coronavirus/mortgage-and-hous ing-assistance/.

5 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

sessions to find local programs. Since its inception in May 2020, the Housing Portal has

seen over 5.25M unique users. The Housing Portal has also been translated into six non-

English languages (Spanish, Arabic, Korean, Tagalog, Traditional Chinese, Vietnamese).

COVID-19 Consumer Information.

15

Since the onset of the COVID-19 pandemic, the

CFPB has published a collection of education resources to help consumers protect

themselves financially during the health crisis. The CFPB created a microsite at

ConsumerFinanace.gov/coronavirus to help consumers quickly find accurate and up-to-

date COVID-19 related resources. Topics covered include mortgages, rental assistance,

credit reporting, debt collection, student loans, frauds and scams, retirement funds,

economic impact payments and more. The CFPB also published resources for specific

audiences such as servicemembers and veterans, older adults and their families, small

business owners, parents, and kids, and more. Additionally, since the beginning of the

pandemic, the CFPB has produced 33 COVID-19 related videos; 1,127 social media

messages with a reach of 93,189,000; and over 325 translations of blogs and web content

into other languages. During the reporting period, approximately 7 million users accessed

the CFPB’s educational web content in response to COVID-19 – accounting for more

than one quarter of all these users that accessed ConsumerFinance.gov during this time.

These users generated 3.1 million engagements and more than 13 million pageviews.

Friends and Family Exchanges Toolkit. The COVID-19 pandemic caused financial

hardship for millions of Americans, forcing many to turn to family and friends for help.

Many families rely on informal lending and borrowing arrangements to weather the

storm, especially in acute financial emergencies or when there is a lack of available

assistance from lending institutions. To support financial educators helping clients

through these often-sensitive conversations about these arrangements, the CFPB released

the Friends and Family Exchanges Toolkit, a four-part guide for coaching clients in

asking for financial help or changing an existing agreement due to their own financial

hardship. Based in research and tested with educators, the guide is available for download

from the CFPB website.

Financial Literacy Annual Report.

16

The CFPB reports annually on its statutory mission

to conduct financial education programs and to ensure consumers receive timely and

understandable information to make responsible decisions about financial transactions.

The 2020 report highlights the CFPB’s financial education programs and initiatives.

15

https://www.consumerfinance.gov/coronavirus/.

16

https://www.consumerfinance.gov/data-research/research-reports /2020-financial-literacy-annual-report/

6 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Your Money, Your Goals.

17

The CFPB continued to disseminate financial empowerment

resources to consumers and stakeholders, and provide training on its interactive Your

Money, Your Goals (YMYG) digital and print resources. Training was offered to a wide

array of public sector and non-profit organizations, focusing on emerging issues as a

result of the COVID-19 crisis such as credit protection, debt management, financial

planning, rental assistance, accessing CARES Act benefits and more; resources were also

used by the CFPB for direct-to-consumer outreach. A training page entitled Videos to

Spark Action shares engaging and brief training videos rooted in the YMYG toolkit, such

as How Do I Get a Copy of My Credit Report?

18

The YMYG materials include issues-

focused booklets that are consumer-facing such as Behind on Bills?;

19

the financial

empowerment toolkit that includes several modules such as Dealing with Debt; and

companion guides to the toolkit for special populations, such as Focus on Native

Communities.

20

New materials released include 11 individual digital tools in Spanish and

a new companion guide for military communities. Updated materials include Focus on

Reentry: Criminal Justice,

21

a companion guide with complementary digital tools and

training materials to assist those working with people with criminal records. YMYG

publications can be easily accessed through the ConsumerFinance.gov website, and free

print copies are available for order.

22

Appraisal and Valuation Bias. On Wednesday, November 3, 2021, the CFPB hosted a

virtual Consumer Advisory Board (CAB) meeting via WebEx. During this meeting,

Board members met to discuss appraisal and Valuation Bias. For this one-hour long

session, CFPB staff from the Office of Fair Lending and Equal Opportunity, along with

the Office of Markets, provided an overview of the CFPB’s current work related to

Appraisal and Valuation Bias. The CFPB looked to receive the Board’s perspective on

how the CFPB can help to eliminate racial bias in home valuations, including current

trends that are being seen in the use of automated valuation models (AVM) and remedies

or solutions that are being seen that could help to address and eliminate potential

valuation bias both for in-person appraisals and AVMs.

23

17

https://www.consumerfinance.gov/practitioner-resources/your-money-your-goals/

18

https://www.consumerfinance.gov/consumer-tools/educator-tools/your-money-your-goals/videos/

19

https://www.consumerfinance.gov/consumer-tools/educator-tools/your-money-your-goals/booklets-talk-about-money/

20

https://www.consumerfinance.gov/consumer-tools/educator-tools/your-money-your-goals /

21

https://www.consumerfinance.gov/about-us /blog/everyone-deserves-a-second-chance-use-our-tools-to-financially-em p ower -

people-in-transition-from-incarceration/

22

https://pueblo.gpo.gov/CFPBPubs/CFPBPubs.php?PubID=13272&PHPSESSID=ic71h6c6025t3mi0rj9ldg5gi5

23

November 2021 Consumer Advisory Board Meeting | Consumer Financial Protection Bureau (consumerfinance.gov)

7 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Back-End Fees in Consumer Financial Products and Services. On January 26, 2022, the

CFPB launched an initiative to reduce fees that consumers are charged by banks and

financial companies. CFPB’s research has found several areas where back-end fees might

obscure the true cost of a product and undermine a competitive market. For example, in

2019, the CFPB released research finding that the major credit card companies charged

more than $14 billion each year in punitive late fees; and in 2019, bank revenue from

overdraft and non-sufficient funds fees surpassed $15 billion. The CFPB is seeking to use

its authorities to seek input from the public on experiences with back-end fees associated

with banks, credit unions, prepaid accounts, credit card accounts, mortgages, loans and

payment transfers.

24

Justice-Involved Individuals and the Consumer Financial Marketplace. From arrest to

incarceration and reentry, people who come into contact with the justice system are

confronted with numerous financial challenges. These challenges include financial

products and services that may contain exploitative terms and features, offer little or no

consumer choice, and that can have long-term negative consequences for the affected

individuals and families. The CFPB will issue a report outlining some of the challenges

faced by justice-involved people and their families in navigating their finances at each

stage of the criminal justice system. These challenges raise serious questions about the

transparency, fairness, and availability of consumer choice in markets associated with the

justice system, as well as demonstrating the pervasive reach of predatory practices

targeted at justice-involved individuals and their families.

25

Complaint analysis

Complaints give the CFPB and others insights into problems people are experiencing in the

marketplace and help the CFPB regulate consumer financial products and services under existing

federal consumer financial laws, enforce those laws judiciously, and educate and empower

consumers to make informed financial decisions.

During the period October 1, 2020, through September 30, 2021, the CFPB received

approximately 872,400 consumer complaints.

26

This represents an approximately 33 percent

24

Additional activity has occurred with this matter since the end of the reporting period. Additional information can be found

here: https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-launches-initiative-to-save-

americans-billions-in-junk-fees/.

25

Additional activity has occurred with this matter since the end of the reporting period. Additional information can be found

here: Justice-Involved Individuals and the Consumer Financial Marketplace (consumerfinance.gov).

26

This analysis excludes multiple complaints submitted by a given consumer on the same issue and whistleblower tips. For more

information on our complaint process refer to the CFPB’s website at https://www.consumerfinance.gov/complaint/process.

8 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

increase from the prior reporting period.

27

Consumers submitted approximately 94 percent of

these complaints through the CFPB’s website and 3 percent via telephone calls. Referrals from

other state and federal agencies accounted for 2 percent of complaints. Consumers submitted the

remainder of complaints by mail, email, and fax.

The CFPB sent approximately 721,500 (83 percent) of complaints received to companies for

review and response. Companies responded to approximately 98 percent of complaints that the

CFPB sent to them for response during the period. The remaining complaints were either

pending response from the company at the end of the period or did not receive a response.

28

Companies’ responses typically include descriptions of steps taken or that will be taken in

response to the consumer’s complaint, communications received from the consumer, any follow-

up actions or planned follow-up actions, and a categorization of the company’s response.

Companies’ responses also describe a range of monetary and non-monetary relief. Examples of

non-monetary relief include correcting inaccurate data provided or reported in consumers’ credit

reports; stopping unwanted calls from debt collectors; correcting account information; issuing

corrected documents; restoring account access; and addressing formerly unmet customer service

issues.

When consumers submit complaints, the CFPB’s complaint form prompts them to select the

consumer financial product or service with which they have a problem as well as the type of

problem they are having with that product or service. The CFPB uses these consumer selections

to group the financial products and services about which consumers complain to the CFPB for

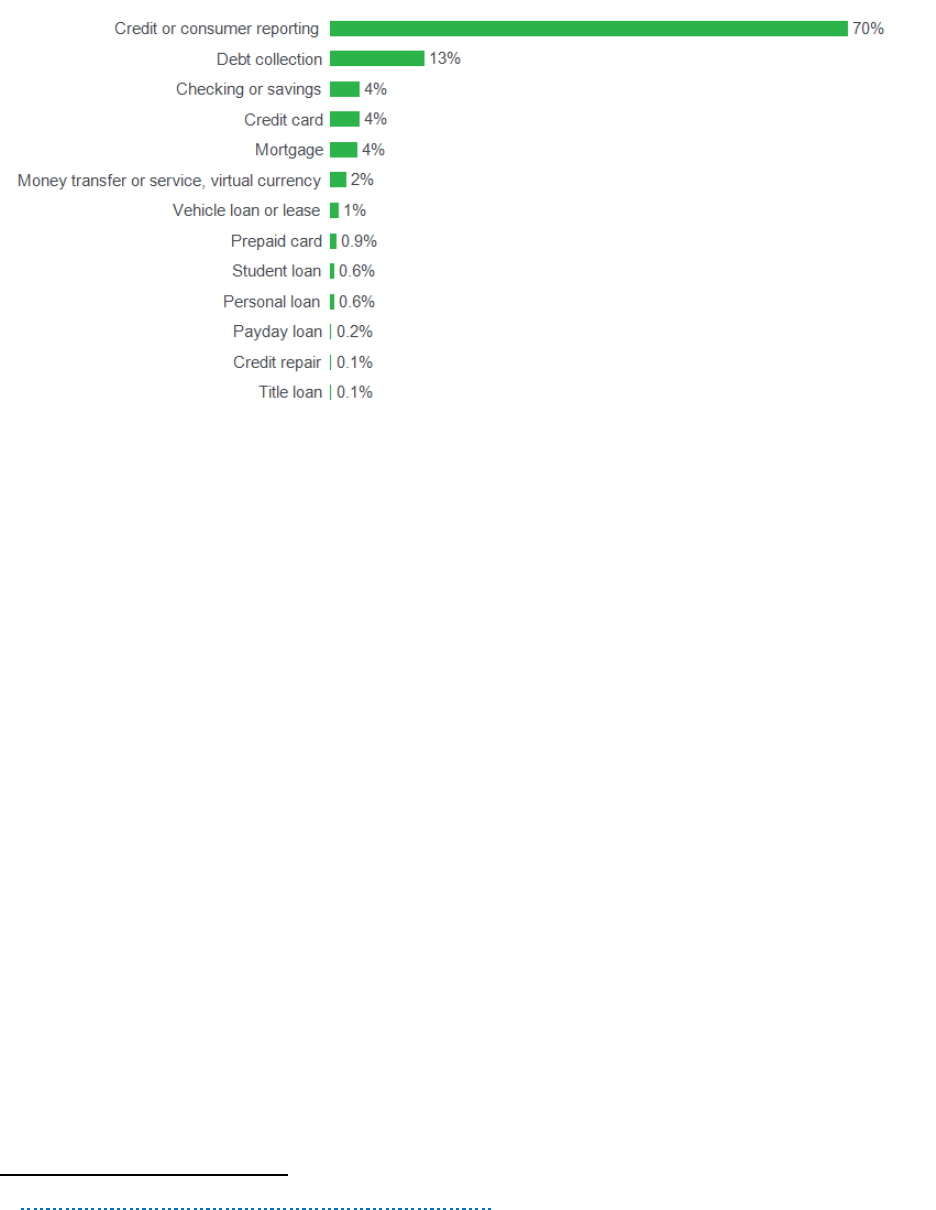

public reports. As shown in Figure 1, credit or consumer reporting was the most complained

about consumer financial product or service during the period, followed by debt collection.

27

The prior reporting period, April 1, 2020 through March 31, 2021, reported 656,200 consumer complaints. See Consumer Fin.

Prot. Bureau, Semi-Annual Report Spring 2021 (October 2021), available at https://www.consumerfinance.gov/data-

research/research-reports/semi-annual-report-consumer-financial-protection-bureau/

28

The CFPB referred 7 percent of the complaints it received to other regulatory agencies and found 8 percent to be incomplete.

At the end of this period, 0.3 percent of complaints were pending with the consumer and 2 percent were pending with the

Bureau. Percentages in this section of the report may not sum to 100 percent due to rounding.

9 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

FIGURE 1

Consumer Response analyzes consumer complaints, company responses, and consumer feedback

to assess the accuracy, completeness, and timeliness of company responses so that the CFPB,

other regulators, consumers, and the marketplace have relevant information about consumers’

challenges with financial products and services. Consumer Response uses a variety of

approaches to identify trends and possible consumer harm. Examples include:

Reviewing cohorts of complaints and company responses to assess the accuracy,

timeliness, and completeness of an individual company’s responses to complaints sent to

them for response;

Conducting text analytics to identify emerging trends and statistical anomalies; and

Visualizing data to highlight geographic and temporal patterns.

The CFPB publishes periodic reports about its complaint analyses. Notable among these is the

Consumer Response Annual Report, which was published on March 24, 2021 and is required by

Section 1013(b)(3)(C) of the Dodd-Frank Act. This report analyzed complaints submitted in

calendar year 2020 about a variety of consumer financial products and services and included

observations about issues consumers experienced related to the coronavirus pandemic.

29

The CFPB makes complaint data available to the public in the Consumer Complaint Database

(Database). The Database contains certain de-identified, individual complaint level data, as well

29

https://www.consumerfinance.gov/data-research/research-reports

10 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

as dynamic visualization tools, including geospatial and trend views based on recent complaint

data to help users of the database understand current and recent marketplace conditions.

Finally, the CFPB also shares consumer complaint information with prudential regulators, the

Federal Trade Commission, other federal agencies, and state agencies.

11 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Office of Equal Opportunity and Fairness

Significant initiatives

The Office of Minority and Women Inclusion (OMWI) is leading the CFPB’s voluntary

response to Executive Order 13985 (racial and economic equity) and guidance from the

White House Domestic Policy Council and on April 20, 2021, submitted a 90-day

progress report to OMB.

In alignment with Executive Order 13985, and guidance from the White House Domestic

Policy Council, the CFPB voluntarily submitted a 200-day equity assessment report to

OMB on August 6, 2021.

The OMWI Director, as the CFPB’s Chief Diversity Officer, is leading the CFPB’s

voluntary response to Executive Order (EO) 14035 (diversity, equity, inclusion, and

accessibility - DEIA) and is leading a cross-agency DEIA Team to facilitate the

development of a 5-year DEIA Strategic Plan for the CFPB.

The CFPB also continued to work on completing action items to eliminate barriers to

equal employment opportunity for Black and Hispanic employees and applicants which

will be expanded upon in the FY 2021 EEO Status Report (MD-715 Report).

In September 2021, the CFPB developed an action plan to address and eliminate barriers

to equal employment opportunity identified for persons with a disability and additional

information will be published in the FY 2021 EEO Status Report (MD-715 Report).

In January 2021, the CFPB issued a Statement to encourage financial institutions to better

serve consumers with limited English proficiency (LEP) and to provide principles and

guidelines to assist financial institutions in complying with the Dodd-Frank Act, Equal

Credit Opportunity Act (ECOA), and other applicable laws.

In October 2021, the CFPB submitted a DEIA self-assessment to the Office of

Management and Budget (OMB) as part of the CFPB’s voluntary response to EO 14035

(DEIA).

The Office of Fair Lending led the CFPB’s involvement in the Interagency Task Force on

Property Appraisal and Valuation Equity (PAVE), a task force focusing on issues of bias

in home appraisals. During the reporting period, the CFPB hosted a roundtable to hear

from stakeholders and participants from partner agencies to look closer at the role of bias

in home appraisals. The Office of Fair Lending expects to continue to participate in this

task force to address appraisal bias during the upcoming reporting period.

12 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

The CFPB is currently developing its 5-year DEIA Strategic Plan. OMWI is working

collaboratively with representatives from business units across the CFPB, including the

Office of Human Capital, the Office of Civil Rights, the Disability and Accessibility

Program Section, Legal, Technology and Innovation, and Administrative Operations, to

develop the DEIA Strategic Plan. The plan is in alignment with EO 14035 (DEIA). The

DEIA Strategic Plan is in alignment with and is referenced in the CFPB’s overall

Strategic Plan.

On November 22, 2021, the CFPB was one of three agencies highlighted in the White

House Domestic Policy Council’s Diversity, Equity, Inclusion and Accessibility (DEIA)

initiative webinar titled “Promising Practices from Agencies.” The CFPB presented on

the outstanding work it has done to promote LGBTQ+ equity and inclusion within the

CFPB and best practices other agencies can adopt.

In January 2022, the CFPB will submit its Equity Action Plan, that aligns with EO 13985

(Racial Equity). In February 2022, the CFPB will submit its annual EEO Status Report

(MD-715 Report). In March 2022, the CFPB will submit its DEIA Strategic Plan, that

aligns with the Government-Wide Strategic Plan, to OMB. The CFPB will also submit its

No FEAR Act Annual Report and OMWI Annual Report to Congress. In April 2022, the

CFPB will submit its Annual Fair Lending Report.

Efforts to increase workforce and contracting diversity

consistent with procedures established by OMWI

During the reporting period, CFPB continued its work to advance diversity and inclusion under

the mandates of Section 342 of the Dodd-Frank Act.

The CFPB continued to execute the objectives and strategies outlined in the Diversity and

Inclusion Strategic Plan Update FY 2019–2022,

30

which complements the CFPB’s overall

Strategic Plan FY 2018–2022.

31

Specifically, Objective 3.2 of the CFPB’s Strategic Plan commits the CFPB to “maintain a

talented, diverse, inclusive and engaged workforce.” The plan requires the CFPB to achieve this

objective with specific strategies, which are:

30

https://www.consumerfinance.gov/data-research/research-reports/cfpb-diversity-and-inclusion-strategic-plan-update-2019-

2022/

31

https://www.consumerfinance.gov/about-us /budget-strategy/strategic-plan/

13 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Establish and maintain human capital policies and programs to help the agency

effectively and efficiently manage a talented, diverse, and inclusive workforce.

Offer learning and development opportunities that foster a climate of professional growth

and continuous improvement.

Develop human capital processes, tools, and technologies that continue to support the

maturation of the CFPB and the effectiveness of human resource operations.

Build a positive work environment that engages employees and enables them to continue

doing their best work.

Maintain comprehensive equal employment opportunity compliance and diversity and

inclusion programs, including those focused on minority and women inclusion.

As of September 2021, an analysis of the CFPB’s current workforce reveals the following key

points:

Women represent 50 percent of the CFPB’s workforce in 2021.

Minorities (Hispanic, Black, Asian, Native Hawaiian/Other Pacific Islander, American

Indian/Alaska Native, and employees of two or more races) represent 43 percent of the

CFPB workforce in 2021 with a 2 percent increase from FY 2020.

As of September 30, 2021, 15 percent of CFPB employees on permanent appointments

identified as individuals with a disability. Of the permanent workforce, 3 percent of

employees identified as individuals with a targeted disability. As a result, the CFPB

continues to exceed the 12 percent workforce goals for employees with disabilities and 2

percent workforce goals for employees with targeted disabilities in both salary categories

as required in the Equal Employment Opportunity Commission’s (EEOC) Section 501

regulation 4.

The CFPB engages in the following activities to increase workforce diversity:

Staffing:

The CFPB had 115 new hires, which included 59 (51 percent) women and 55 (48

percent) minorities

32

.

32

New Hires data is collective over the period from April 1, 2021 to September 30, 2021.

14 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

The CFPB continues to enhance diversity by recruiting, hiring, and retaining

highly qualified individuals from diverse backgrounds to fill positions at the

CFPB:

The CFPB uses social media platforms like LinkedIn, Twitter, and

Facebook to broadly promote vacancies.

The CFPB takes steps to mitigate bias in the hiring process, for example

by removing applicant names from resumes and other application

documents before submitting certain best-qualified lists to selection

officials.

The CFPB regularly analyzes whether any job qualifications may

inadvertently disadvantage individuals who are members of underserved

communities.

The CFPB’s OMWI and OHC collaborate with hiring managers on

strategic diversity and inclusion recruitment options.

The CFPB also utilized other professional development programs, and

recruitment efforts directed to reach veterans and applicants with disabilities to

assist in the CFPB’s workforce needs.

Workforce engagement:

To promote an inclusive work environment, the CFPB focuses on strong

engagement with employees and utilizes an integrated approach of education,

training, and engagement programs that ensures diversity and inclusion, and non-

discrimination concepts are part of the learning curriculum and work

environment. Employee resource groups, cultural education programs, a mentor

program, and mandatory diversity and inclusion training are key components of

this effort.

In June 2021, the CFPB adopted a definition and goals for Racial and Economic

Equity (REE). To help facilitate this work, OMWI developed guidance to assist

CFPB divisions in applying the REE definition and principles to their core work

and internal operations.

Increasing contracting diversity

In addition to the mandates in Section 342(b)(2)(B) of the Dodd-Frank Act, Section 2.4 of the

CFPB’s Diversity and Inclusion Strategic Plan describes the efforts the CFPB takes to increase

15 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

contracting opportunities for diverse businesses including Minority- and Women-owned

Businesses (MWOBs). The CFPB’s OMWI and Procurement offices collectively work to

increase procurement opportunities for participation by MWOBs.

Outreach to contractors

The CFPB promotes opportunities for the participation of small and large MWOBs by:

Actively engaging CFPB business units with MWOB contractors throughout the

acquisition cycle.

During the reporting period, OMWI and the Office of Procurement held technical

assistance events virtually due to COVID-19 restrictions. In fiscal year 2021, OMWI

provided technical assistance to approximately 150 MWOBs and added over 200 vendors

to its MWOB database. Attendance remained consistent at around 100 registrants and 55

attendees per session. These events included expert advice directly from CFPB

procurement and program office professionals. The events aimed to align the CFPB’s

upcoming needs to vendor capabilities in data analytics, management consulting, and

legal support services. With the launch of the CFPB’s first dynamic Supplier Diversity

Registry in May, OMWI aims to provide event participants and other interested vendors

year-round engagement opportunities in its market research process, including status

updates to forecasted requirements, advance notice of procurement industry days and

email news updates of partner agency events and activities.

In addition:

OMWI supports program office stakeholders with updated market research and targeted

outreach to engage current and potential MWOBs, and by providing suggestions for

Divisions on how to incorporate supplier diversity goals into their diversity and inclusion

strategic plans.

OMWI tracks the annual percentage of competed contract dollars spent with MWOBs to

advance economic equity. During the third and fourth quarter of FY 2021, the CFPB’s

MWOB spend percentage was 36 percent. Taken as a whole, FY2021 was the fourth

consecutive year the CFPB has increased MWOB-spend over the previous year.

OMWI regularly participates in virtual and in-person national supplier diversity industry

days, such as the National 8(a) Association Conference, that help to foster business

partnerships among the federal government, its U.S. prime contractors, and MWOBs.

16 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

As a result of these efforts, 23 percent of the $84 million in contracts that the CFPB

awarded or obligated during the reporting period went to MWOBs. The following table

represents the total amount of dollars spent and disbursed to MWOBs as a result of

contract billing.

TABLE 1: DOLLARS SPENT TOWARD MINORITY-OWNED AND WOMEN-OWNED BUSINESSES

Dollars Spent percent of Total MWOB Category

$14,288,057 19.8 percent Women Owned

$3,161,999 4.4 percent Black/African American

$1,897,820 2.6 percent American Indian/Alaskan Native

$13,759,367 19.1 percent Asian/Pacific Islander American

$1,045,988 1.4 percent Hispanic American

Diversity within the CFPB contractors’ workforces

The CFPB requires its contractors and sub-contractors to report their diversity and inclusion data

through the Good Faith Effort (GFE) contract requirement. In the fiscal year 2021, the CFPB

Director approved OMWI’s GFE Policy. The CFPB also collected GFE compliance data from a

sample of contractors, providing an opportunity for contractors to demonstrate their efforts to

address the six evaluation criteria: 1) Diversity Strategy; 2) Diversity Policies; 3) Recruitment; 4)

Succession Planning; 5) Outreach; and 6) Supplier – Subcontractor Diversity. OMWI continues

to maximize technical assistance to CFPB contractors throughout this process.

Assessing diversity of regulated entities

Pursuant to Section 342(b)(2)(c) of the Dodd-Frank Act, the CFPB developed a process to assess

the diversity policies and practices of the entities the CFPB regulates. During the reporting

period, the CFPB continued its multi-pronged assessment strategy, collecting assessments

through the Inclusivity online portal designed to make it easier for financial institutions to submit

their diversity and inclusion self-assessments. During the reporting period, three (3) financial

institutions submitted assessments, a decrease from 2020 submissions that is most likely a result

of the pandemic.

OMWI continued its communication strategy by using direct outreach to financial institutions

and working with industry trade associations to help engage financial institutions in the diversity

17 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

and inclusion self-assessment process. OMWI sent quarterly data calls to approximately 1,300

institutions and invited them to submit a diversity self-assessment. To supplement the data

collected through the self-assessment process, the CFPB continued to conduct research on the

publicly available diversity and inclusion information of financial institutions, by industry

segment, and share that information with trade groups. The CFPB also met directly with several

financial institutions to learn more about their internal programming. This information provided

insight into how institutions were publicly reporting on their diversity and inclusion initiatives.

The CFPB reviewed numerous press releases related to diversity and inclusion released during

the year as a follow-up to the racial protests of 2020. Several institutions made public statements,

committed resources and multi-year funding to advance racial and economic equity as a result of

public outcry. The CFPB will continue to follow industry developments related to these

commitments. The CFPB will also continue its outreach to increase awareness and to encourage

voluntary submission of the Diversity and Inclusion self-assessment.

An analysis of efforts to fulfill the Fair Lending education and

interagency coordination mission of the CFPB

Education and outreach

The CFPB is committed to hearing from and communicating directly with stakeholders in a

variety of ways. The CFPB regularly engages in outreach with stakeholders, including consumer

advocates, civil rights organizations, industry, academia and other government agencies to

educate or communicate with external stakeholders about fair lending compliance and access to

credit issues and hear their views on the CFPB’s work to inform policy decisions.

The CFPB achieves its educational objectives through publication of proposed rules and

interpretive rules, issuance of compliance bulletins, policy statements targeted to industry,

requests for information, press releases, blog posts, podcasts, videos, brochures, website updates,

and reports regarding fair lending issues; delivering speeches, panel remarks, webinars, and

presentations addressing fair lending and access to credit issues; and participating in smaller

meetings and discussions with external stakeholders, including federal and state regulators and

agencies.

During the reporting period, CFPB staff participated in 123 fair lending related outreach events.

In these events, staff worked directly with external stakeholders to share and receive information

on fair lending priorities and emerging issues. The CFPB also received feedback on fair lending

issues and how broader market use of special purpose credit programs could promote fair,

equitable, and nondiscriminatory access to credit. In addition to special purpose credit programs,

some examples of the topics covered include: the impacts of the COVID-19 pandemic on the

economy, algorithmic bias and robo-discrimination, appraisal bias, racial and economic equity

18 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

issues, fair lending supervision and enforcement priorities, alternative data and modeling

techniques in credit underwriting, HMDA and Regulation C, ECOA and Regulation B, small

business lending, servicing issues, and access to credit issues for Limited English Proficient

(LEP) consumers.

During the reporting period, the CFPB issued numerous fair lending and access to credit related

blogs, press releases, speeches, and reports. Specifically, The CFPB published six blog posts

including a blog announcing the publication of the 2020 Fair Lending Annual Report;

33

a blog

from the Acting Director announcing the CFPB’s commitment to racial and economic equity;

34

a

blog announcing a report analyzing differences in lending patterns for lenders below and above

the 100-loan closed-end threshold set by the 2020 Home Mortgage Disclosure Act rule;

35

a blog

highlighting the CFPB’s prioritization of resources to focus on the role of racial bias in home

appraisals;

36

a blog highlighting the special purpose credit provisions of ECOA and Regulation

B,

37

and a blog encouraging mortgage servicers to enhance their communication capabilities and

outreach efforts for borrowers.

38

During the reporting period, the CFPB issued five press releases related to fair lending and

access to credit issues, including a press release pertaining to the Libre

39

enforcement action; a

press release announcing the proposed small business lending rule;

40

a press release announcing

the extension of the comment period for the AI RFI;

41

and a press release announcing the

availability of the 2020 HMDA Data.

42

Additionally, during the reporting period, the Acting

Director delivered several fair lending related speeches, including remarks at the National Fair

33

https://www.consumerfinance.gov/data-research/research-reports/fair-lending-report-2020/

34

https://www.consumerfinance.gov/about-us /blog/address ing-racial-inequities-consumer-finance-markets/

35

https://www.consumerfinance.gov/about-us /blog/hmda-thres hold-report-blog/

36

https://www.consumerfinance.gov/about-us /blog/cfpb-prioritizing-resources-against-racial-bias-home-appraisals/

37

https://www.consumerfinance.gov/about-us /blog/expanding-access-credit-underserved-communities/

38

https://www.consumerfinance.gov/about-us /blog/new-rule-ensures-mortgage-servicers-provide-options-potentially-vulnerable-

borrowers-exiting-forbearance/

39

https://www.consumerfinance.gov/about-us /newsroom/consumer-financial-protection-bureau-and-virginia-massachusetts-and-

new-york-attorneys-general-sue-libre-for-predatory-immigrant-services-scam/

40

https://www.consumerfinance.gov/about-us /newsroom/cfpb-proposes-rule-to-shine-new-light-on-small-businesses-access-to-

credit/

41

https://www.consumerfinance.gov/about-us/newsroom/agencies-extend-comment-period-on-request-for-information-on-

artificial-intelligence/

42

https://www.consumerfinance.gov/about-us /newsroom/2020-hmda-data-on-mortgage-lending-now-available/

19 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Housing Alliance’s Virtual Forum on Special Purpose Credit Programs,

43

National Association

of Attorneys General Spring Consumer Protection Conference,

44

and remarks for the Libre

enforcement action.

45

The CFPB issued six fair lending related reports during the reporting

period, including a Data Point article on 2020 mortgage market activity and trends;

46

a report

focused on mortgage servicing COVID-19 pandemic response metrics;

47

a report analyzing how

characteristics of mortgages, borrowers, and lenders vary across Asian American and Pacific

Islanders;

48

a brief overview of the general lending patterns of small to medium size closed-end

HMDA reporters;

49

an analysis of manufactured home loans using HMDA data;

50

and the Fair

Lending Annual Report to Congress.

51

Fair Lending brochures

In September, the CFPB released two brochures on credit discrimination, titled Know Your

Rights, Credit Discrimination is Illegal and Helping Consumers Spot Credit Discrimination. The

brochures are targeted to consumers as well as those who work with consumers. The brochures

are available in English, Spanish, Chinese, Vietnamese, Korean, Tagalog, and Arabic. The

brochures are available at consumerfinance.gov/fair-lending/.

The CFPB’s fair lending activity involves regular coordination with other regulatory and

enforcement governmental partners. During the reporting period, the CFPB coordinated its fair

lending regulatory, supervisory, and enforcement activities with those of other federal agencies

and state regulators to promote consistent, efficient, and effective enforcement of federal fair

lending laws. Interagency engagement occurs in numerous ways, including through several

43

https://www.consumerfinance.gov/about-us /newsroom/prepared-remarks-acting-director-dave-uejio-nfhas-virtual-forum-

special-purpose-credit-programs/

44

https://www.consumerfinance.gov/about-us /newsroom/prepared-remarks-of-acting-director-dave-uejio-at-the-national-

association-of-attorneys-general-spring-consumer-protection-conference/

45

https://www.consumerfinance.gov/about-us /newsroom/prepared-remarks-of-acting-director-dave-uejio-for-the-libre-

enforcement-action-press-call/

46

https://www.consumerfinance.gov/data-research/research-reports/2020-mortgage-market-activity-and-trends/

47

https://www.consumerfinance.gov/data-research/research-reports/mortgage-servicing-covid-19-pandemic-response-metrics/

48

https://www.consumerfinance.gov/data-research/research-reports/asian-american-and-pacific-islanders-in-the-mortgage-

market/

49

https://www.consumerfinance.gov/data-research/research-reports/a-brief-note-on-general-lending-patterns-small-to-medium-

size-closed-end-hmda-reporters/

50

https://www.consumerfinance.gov/data-research/research-reports/manufactured-housing-finance-new-insights-hmda/

51

https://www.consumerfinance.gov/data-research/research-reports/fair-lending-report-2020/

20 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

interagency organizations. This interagency engagement seeks to address current and emerging

fair lending risks.

The CFPB, along with the FTC, HUD, FDIC, FRB, NCUA, OCC, DOJ, and FHFA, constitute

the Interagency Task Force on Fair Lending. This Task Force meets regularly to discuss fair

lending enforcement efforts, share current methods of conducting supervisory and enforcement

fair lending activities, and coordinate fair lending policies. The FDIC is currently the Chair of

this Task Force.

The CFPB also participates in the Interagency Working Group on Fair Lending Enforcement, a

standing working group of federal agencies—with the DOJ, HUD, and FTC—that meets

regularly to discuss issues relating to fair lending enforcement. The agencies use these meetings

to also discuss fair lending developments and trends, methodologies for evaluating fair lending

risks and violations, and coordination of fair lending enforcement efforts.

The Federal Financial Institutions Examination Council’s (FFIEC) Appraisal Subcommittee

(ASC), comprised of designees from the CFPB and certain other federal agencies, provides

federal oversight of state appraiser and appraisal management company regulatory programs, and

a monitoring framework for the Appraisal Foundation. Among other activities, the ASC hosted a

roundtable on September 22, 2021, entitled “Building a More Equitable Appraisal System”,

relating to addressing historical and contemporary factors that have contributed to the inequities

currently challenging the appraisal system.

52

The CFPB engages with other agencies on issues of bias in home appraisals through the PAVE

Taskforce. On August 5, 2021, the PAVE held its first principal-level meeting. The PAVE Task

Force is chaired by HUD Secretary Marcia Fudge and Director of the United States Domestic

Policy Council, Ambassador Susan Rice. The Task Force also includes cabinet-level leaders

from executive departments and additional members from independent agencies, including the

CFPB. On June 15, 2021, the CFPB hosted a roundtable to look closer at the role of bias in home

appraisals.

53

At the roundtable, the CFPB heard from civil rights activists, consumer advocates,

and local leaders who described the impacts of these biases in their communities. The roundtable

also included participants from the NCUA, the OCC, and HUD.

Through the FFIEC the CFPB has robust engagements with other partner agencies that focus on

fair lending issues. For example, throughout the reporting period, the CFPB has chaired the

HMDA/Community Reinvestment Act (CRA) Data Collection Subcommittee, a subcommittee of

52

The Appraisal Subcommittee members are from the FFIEC federal member agencies, HUD, and the FHFA.

https://www.asc.gov/About-the-ASC/BoardMembers.aspx

53

https://www.consumerfinance.gov/about-us/events/archive-past-events/virtual-home-appraisal-bias-event/

21 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

the FFIEC Task Force on Consumer Compliance. This subcommittee oversees FFIEC projects

and programs involving HMDA data collection and dissemination, the preparation of the annual

FFIEC budget for processing services, and the development and implementation of other related

HMDA processing projects as directed by the Task Force.

In addition to these established interagency organizations, CFPB personnel meet regularly with

DOJ, HUD, FTC, FHFA, state Attorneys General, and the prudential regulators to coordinate the

CFPB’s fair lending work.

22 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Operations

The Operations Division focuses on improving the CFPB’s operational functions and related

foundational processes by (1) cultivating an engaging and informed workforce to maximize

talent and development in alignment with the CFPB’s mission; (2) defining and implementing a

modern, forward leaning workplace model responsive to the organization’s needs; and (3)

advancing the work of the CFPB through innovative and optimized operational support.

Significant initiatives

Response to Ensure Safety of Staff During COVID-19 Pandemic. The CFPB instituted

several initiatives to ensure the health, safety, and well-being of the CFPB’s staff during

the COVID-19 pandemic. These included:

Maintaining all examination activity of CFPB-supervised institutions be virtually

conducted from examiners’ home duty stations through April 23, 2022.

Managing the agency’s operating status and posture starting with mandatory telework

through the current maximum telework position, which includes providing appropriate

safety conditions to support voluntary return to the office for those who seek that

option. This included a phased return to work at its Washington, D.C. headquarters

location on July 8, 2020, allowing staff who want to work from the building the

opportunity to do so in a safe and secure manner. On October 1, 2020, the CFPB

began a phased return to work at its regional locations allowing staff who want to

work from the CFPB’s regional offices the opportunity to do so in a safe and secure

manner, similar to the Washington D.C. headquarters. This operating status is in place

through April 23, 2022, and will be reassessed on a regular basis to determine whether

additional extensions are appropriate.

Granting flexibility to staff to vary their work schedules through additional accrual of

credit hours and authorizing staff to use up to 20 hours of administrative leave per pay

period if they are prevented from working due to a lapse in childcare or other reasons

associated with COVID-19, including time needed to get a COVID-19 vaccine.

54

54

Administrative leave is provided through the CFPB’s compensation authority.

23 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Providing up to two weeks (80 hours) of emergency paid sick leave through December

31, 2020, in accordance with the Emergency Paid Sick Leave Act.

Adjusting the CFPB’s annual leave program for 2020 and 2021 by increasing the

amount of the annual leave use or lose payout from 40 hours to 80 hours for

employees who are unable to use their annual leave by the end of the 2020 or 2021

leave years. In addition, in 2020, the CFPB restored up to 40 hours of leave for

employees who had a use or lose annual leave balance after the 80-hour payout.

Providing CFPB employees with updates on prevention measures, workplace

flexibilities, telework options and best practices, and keeping staff informed through a

variety of communication channels.

Creating several ways to hear from CFPB employees through National Treasury

Employees Union engagements, a CFPB -wide COVID-19 advisory group, a

Pandemic Inquiries and Re-entry inboxes, leadership involvement, and CFPB

Employee Resource Groups. Additionally, the CFPB maintained a frequent cadence of

communicating with Financial Institutions Reform, Recovery, and Enforcement Act of

1989 (FIRREA) and other federal agencies for situational awareness and alignment,

where possible.

Released the Home Mortgage Disclosure Act (HMDA) 2020 national datasets, aggregate

and disclosure reports and new map function. In expanding upon the utility of the

CFPB’s HMDA program, the HMDA team released 2020 national loan-level datasets,

aggregate and disclosure reports, and a new map function within the Data Browser. The

HMDA data and reports are the most comprehensive publicly available information on

mortgage market activity.

Deployed the Rental Assistance Finder Tool (RAFT). This tool helps renters and

landlords connect with various state and local programs that are distributing federal

assistance and assists both landlords and tenants navigate and identify assistance

available through the U.S. Department of Treasury’s Emergency Rental Assistance

(ERA) program in their communities.

Digital Analytics and Machine Learning. The Digital Analytics artificial intelligence and

machine learning (AI/ML) program provided direct support to CPFB supervision in

completing its first ever examination on machine learning-based loan underwriting and

origination.

Privacy Controls. The CFPB published two privacy impact assessments (PIAs) during

this reporting period, which include a PIA update for the CFPB’s FOIAXpress system to

24 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

document enhancements that implement the Office of Management and Budget (OMB)

Memorandum M-21-04, Modernizing Access to and Consent for Disclosure of Records

Subject to the Privacy Act (Nov. 12, 2020). The new requirements aim to facilitate

transparency and enable access to Federal programs and records through seamless and

secure digital service delivery. The CFPB also developed and posted a new position

description for a Privacy Engineer, the first of its kind in the federal government, to

address new National Institute of Standards and Technology (NIST) Special Publication

(SP) 800-53, Revision 5 (Rev 5) requirements for federal agencies.

Compensation Reform. In January 2019, the CFPB launched a compensation reform

initiative to review compensation practices and agreed with the NTEU to a two-phase

CFPB -wide review and reset of all employee salaries. Part one started in May 2021,

which included collecting and crediting the work experience of all CFPB staff. Joint

management-union committees are tasked with crediting each employee’s work

experience based on agreed-upon definitions.

People Action Planning (PAP) Working Group. In March 2021, the CFPB formed the

People Action Planning Working Group to define the priorities and activities the CFPB

will take to address aspects of the work environment that impact employee engagement

and to ensure the CFPB takes a holistic, consistent approach to considering and planning

bureau-wide people-related plans and initiatives. The Working Group conducted an

extensive review of key CFPB sources of information regarding the employee experience

such as the 2020 Annual Employee Survey and developed an inventory of over 150

actions currently in process or planned and prioritized those with the greatest potential to

improve employee engagement. The Working Group then drafted a People Strategy

containing a roadmap of actions to increase employee engagement and cultivate the

Director’s vision for our work environment, which will be worked on over the next 12

months. Actions have been prioritized within three areas:

Fostering a culture of diversity, equity, and inclusion;

Creating a strong leadership presence and supporting culture; and

Providing development and advancement opportunities.

25 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

COVID-19 Pandemic Response. Continue to work on several initiatives to ensure the

health, safety, and well-being of the CFPB’s staff during the COVID-19 pandemic.

55

Developing a vaccine reporting tool to collect Federal employee vaccination status

and initiate exception requests.

Creating a process for collecting, reviewing, and adjudicating reasonable and

religious accommodations exception requests.

Implementing a progressive disciplinary policy for employees who are not fully

vaccinated and do not have an approved or pending exception request.

Incorporating the FAR Clause 52.223-99 Ensuring Adequate COVID-19 Safety

Protocols for Federal Contractors into new and existing contracts to facilitate

compliance by contractors with the vaccine mandate.

Continue Response to Ensure Safety of Staff in 2022. The CFPB will continue to monitor

and update its workforce flexibilities to ensure the health, safety, and well-being of the

CFPB’s staff during the COVID-19 pandemic. The CFPB will also develop safety

protocols and procedures to determine when and how staff will re-enter its buildings

based on evolving guidance. The CFPB’s maximum telework operating posture remains

in place through April 23, 2022.

Future of Work. Further prompted by the pandemic, the Future of Work initiative is

changing the way organizations look at where we work, how we work, and the nature of

the work itself. Around mid-2022, the CFPB expects to begin implementing changes that

will impact where and how we work as the first outcome of this initiative. The CFPB has

successfully proven its ability to deliver on its mission during the pandemic and will use

the lessons learned, along with feedback from its employees, to assess and define the

future path.

Collective Bargaining Agreement (CBA). The CFPB and NTEU agreed to a four-year CBA,

which was set to expire on October 9, 2021. The CFPB and NTEU agreed to extend the CBA

for one year to prioritize more pressing matters, such as compensation and the Future of

Work. As such, CBA bargaining is expected to start in October 2022 and may take up to a

year to complete.

55

The CFPB is ensuring compliance with the relevant, applicable nationwide preliminary injunctions and will take no action to

implement or enforce the COVID-19 vaccination requirement pursuant to Executive Order 14043 or Executive Order 14042 at

this time.

26 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Implementing PIV Derived Credentials (PIV D). Despite challenges presented by COVID,

the CFPB will continue to migrate users across the entire CFPB to personal identity

verification (PIV) derived credentials (PIV-D). The PIV-D deployment will result in a more

secure and efficient user authentication experience eliminating the need to remember and

maintain passwords. Stronger security will also be implemented through multi-factor

authentication that relies on both a PIV-card and personal identification number (PIN) to gain

access, making it much more difficult for "bad actors" to gain unauthorized access.

Inaugural Open Data Plan. While the CFPB awaits OMB guidance on the OPEN

Government Data Act, Title II of the Evidence Act, the CFPB continues to develop its Open

Data Plan to provide greater transparency and promote access to and use of CFPB datasets.

This plan will detail the CFPB’s strategy and progress toward identifying priority open

datasets and making them more accessible through the comprehensive public data inventory

located at data.gov.

Data Maturity Assessment. In accordance with the Federal Data Strategy Action Plan, the

CFPB is continuing to develop a data maturity assessment framework to document data

management best practices, determine gaps, and identify areas of opportunity to modernize

and improve the CFPB’s ability to harness data to inform policy decisions. This assessment

will provide the foundation to enable the CFPB to mature its use of data to meet its policy

priorities and fulfill its mission.

Justification of the budget from the previous year

The CFPB’s Annual Performance Plan and Report and Budget Overview, which is available

online at www.consumerfinance.gov/about-us/budget-strategy/budget-and-performance/,

includes estimates of the resources needed for the CFPB to carry out its mission. The document

also describes the CFPB’s performance goals and accomplishments, supporting the CFPB’s

long-term strategic plan.

CFPB fund

As of September 30, 2021, the end of the fourth quarter of FY 2021, the CFPB had spent

approximately $598.0 million

in FY 2021

56

funds to carry out the authorities of the CFPB

under federal consumer financial law, including approximately $352.8 million for

56

This amount includes new obligations and upward adjustments to previous year obligations. An obligation is a transaction or

agreement that creates a legal liability and obligates the government to pay for goods and services ordered or received.

27 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

employee compensation and benefits. There were 1,591

57

CFPB employees on board at

the end of the fiscal year.

TABLE 1: FY 2021 SPENDING EXPENSE CATEGORY

Expense Category

Fiscal Year 2021

Personnel Compensation

$247,169,000

Benefit Compensation $102,865,000

Benefit Compensation – Former Employees $2,762,000

Travel

$81,000

Transportation of Things

$117,000

Rents, Communications,

Utilities & Misc.

$13,436,000

Printing and Reproduction

$4,326,000

Other Contractual Services

$199,509,000

Supplies & Materials

$5,576,000

Equipment $22,106,000

Land and Structures $86,000

Total (as of September 30, 2021)

$598,033,000

FY 2021 funds transfers received from the Federal Reserve

The CFPB is funded principally by transfers from the Federal Reserve System, up to the limits

set forth in the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-

Frank Act). As of September 30, 2021, the CFPB had received the following transfers for FY

2021. The amounts and dates of the transfers are shown below.

58

TABLE 2: FUND TRANSFERS

Funds Transferred

Date

57

Reflects employees on board during pay-period 19, calendar year 2021.

58

Current year spending in excess of funds received is funded from the prior year’s unobligated balance.

28 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

$203.4M October 01, 2020

$118.6M January 04, 2021

$166.8M April 01, 2021

$107.1M July 04, 2021

$595.9M Total

Additional information about the CFPB’s finances, including information about the CFPB’s

Civil Penalty Fund and CFPB-Administered Redress programs, is available in the annual

financial reports and the Chief Financial Officer (CFO) quarterly updates published online at

www.consumerfinance.gov/about-us/budget-strategy/financial-reports/.

Copies of the CFPB’s quarterly funds transfer requests are available online at

www.consumerfinance.gov/about-us/budget-strategy/funds-transfer-requests/.

29 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

Research, Markets and Regulations

The Division of Research, Markets, and Regulations uses a synthesis of social science research,

market intelligence, legal analysis, and regulatory expertise to develop, recommend, and

implement policy choices to ensure that markets for consumer financial products and services are

fair, transparent, and competitive.

Significant problems faced by consumers in shopping for or

obtaining consumer financial products or services

During the reporting period, the CFPB released reports in the form of Data Points and blogs that

discuss the challenges consumers face in shopping for or obtaining consumer financial products

or services, including reports on payday and auto lending, and a series of blogs and other report

on the effects of the COVID-19 pandemic on consumer credit.

Consumer use of payday, auto title, and pawn loans: Insights from the

Making Ends Meet survey

59

The CFPB’s Making Ends Meet Survey is a nationally representative survey of adults with a

credit record. The survey results provide a deeper understanding of how often U.S. consumers

have difficulty making ends meet, how they cope with these shortfalls, and their subsequent

financial difficulties. The survey is part of the CFPB’s statutory mission to conduct research on

markets for consumer financial products and services, the experiences and access to credit for

traditionally underserved communities, and consumer understanding and choice of products,

among other things.

Using the CFPB’s Making Ends Meet survey, we find that consumers who use a payday, auto

title, or pawn loan in one year are often still using that type of loan a year later. Some users of

these services have lower cost credit available on credit cards, while others lack access to

traditional credit. Among payday, auto title and pawn loan borrowers who experience significant

financial shocks, the costs of these shocks often exceed other possible sources of funds.

Three quarters of payday, auto title, and pawn users report experiencing both a significant

income or expense shock and difficulty paying a bill or expense in the previous year. We

examine the income and expenditure shocks that trigger difficulties for consumers in paying bills

59

More information can be found here: https://www.consumerfinance.gov/data-research/research-reports/consumer-use-of-

payday-auto-title-and-pawn-loans-insights-making-ends-meet-survey/

30 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

and expenses. For payday, auto title, and pawn users, these shocks tend to be larger than other

available credit or savings sources.

Payday, auto title, and pawn users who experience difficulty paying a bill or expense tend to also

use other available credit, suggesting that for some consumers, these loans might be part of a

broader and more complicated debt portfolio to deal with difficulties. For users of these loans,

getting the money quickly, lack of a credit check, and not wanting “anybody to know that I

needed money” were important for deciding on their credit source.

Data Point: Subprime auto loan outcomes by lender

60

Americans owe auto lenders well over a trillion dollars. Consumers with subprime credit scores

–i.e., scores that are significantly lower than average—are especially likely to need loans to

purchase vehicles. But they also pay the highest interest rates and are the most likely to default

on their loans. Because interest rates and default risk can matter so much for consumers, CFPB

researchers took an in-depth look at how they vary across different types of subprime auto

lenders. They found that some types of subprime lenders charge their borrowers significantly

higher interest rates than others, and that differences in default risk are unlikely to fully explain

these differences.

The report found notable differences across lender types in the borrowers they serve and the

types of vehicles they finance. For example, banks and credit unions that offer subprime auto

loans tend to lend to borrowers with higher credit scores than finance companies and buy-here-

pay-here dealerships. In light of these differences, it is perhaps not surprising that different

lender types charge very different interest rates on average. For example, for subprime auto loans

in our sample, average interest rates at banks are approximately 10 percent, compared to 15

percent to 20 percent at finance companies and buy-here-pay-here dealerships. As expected, we

find higher default rates at lender types that charge higher interest rates. For example, we find

that the likelihood of a subprime auto loan becoming at least 60 days delinquent within three

years is approximately 15 percent for bank borrowers and between 25 percent and 40 percent for

finance company and buy-here-pay-here borrowers.

But do differences in default risk fully explain the differences in interest rates across subprime

lender types that we see? Our statistical analysis suggests they do not. For example, adjusting for

many factors in our data that we observe (such as borrowers’ credit scores), we estimate that the

average borrower in our data with a 560+ credit score would have the same default risk with a

60

More information can be found here: https://www.consumerfinance.gov/data-research/research-reports/subprime-auto-loan-

outcomes-lender-type/

31 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

loan from a bank as with a loan from a small buy-here-pay-here lender. But their estimated

interest rate would be 13 percent with a loan from a small buy-here-pay-here lender, while it

would be 9 percent with a loan from a bank. In our data, a typical borrower at a small buy-here-

pay-here lender would save around $900 over the life of a loan if they could reduce their interest

rate from 13 percent to 9 percent.

Significant initiatives

Changes in consumer financial status during the early months of the pandemic.

61

An

analysis using the CFPB’s Making Ends Meet survey series looks at the early impact of

COVID-19 on the financial status of consumers. The results show that fewer consumers

had difficulty paying a bill in the initial months of the COVID-19 pandemic than one year

earlier and that both credit scores and CFPB financial well-being scores increased. These

improvements were largely consistent across demographics like race, ethnicity, gender,

rural status, and income.

Many consumers’ financial status declined, despite the average increase. Consumers

whose income or savings decreased, regardless of whether they became unemployed,

were more likely than others to experience reduced financial well-being and credit scores.

Credit forbearance appears to have helped consumers who were having difficulty paying

bills avoid a decline in financial well-being.

Financial conditions for renters before and during the COVID-19 Pandemic.

62

Using the

Making Ends Meet survey and consumer credit data, CFPB researchers found that

financial conditions faced by renters and homeowners were divergent before the

pandemic, with renters generally experiencing more financial vulnerability than

homeowners. Renters therefore had more to gain from some pandemic relief efforts than

homeowners. They also could have more to lose from the termination of relief. The CFPB

finds that some government relief efforts likely helped maintain the financial stability of

renters and their families, suggesting that many may be at risk as those programs expire.

The report, which compared homeowners and renters, found that, on average, renters’

economic conditions were significantly more responsive to relief measures such as

stimulus payments and changes in unemployment benefits. When these programs end,

61

More information can be found here: https://www.consumerfinance.gov/data-research/research-reports/changes-in-consumer-

financial-status-during-early-months-pandemic/

62

More information can be found here: https://www.consumerfinance.gov/about-us/newsroom/cfpb-report-renters-at-ris k -as-

covid-19-safety-net-ends/

32 SEMI-ANNUAL REPORT OF THE CONSUMER FINANCIAL PROTECTION BUREAU | FALL 2021

renters and their families may be at heightened risk. The findings in today’s report will

help inform the CFPB’s ongoing work to support renters and their families.

The Consumer Credit Card Market.

63

In September 2021, the CFPB released its fifth

biennial report to Congress on the consumer credit card market, finding that the market’s

growth over the last few years reversed course in 2020. In reviewing the market for

potential consumer harm, the report presents the latest research on consumer card use,

cost, and availability. From a 2019 peak of $926 billion, credit card debt fell to $811

billion by the second quarter of 2020, the largest six-month decline on record, before