TThhee FFuueell TTaaxx

aanndd AAlltteerrnnaattiivveess ffoorr TTrraannssppoorrttaattiioonn FFuunnddiinngg

Highway programs derive most of their funding from fuel taxes and user fees paid by

vehicle operators, including registration fees and tolls. Most of the revenues from these fees

go to highways, with a share to transit. This study assesses the prospects for continuing to

generate revenue from these fees and identifies alternative financing arrangements.

The study committee concludes that the finance system has contributed to the suc-

cess of the highway program by delivering a positive return on the national investment in

highways; moreover, user fees can remain the primary funding source for another decade

or more. Transitioning to a fee structure that charges vehicle operators directly for the use

of roads, however, could benefit the public by reducing congestion and by targeting

investment to the most valuable projects. The committee recommends that governments

expand tolling on expressways and explore techniques for charging each vehicle accord-

ing to miles traveled on all roads.

Also of Interest

IInntteerrnnaattiioonnaall PPeerrssppeeccttiivveess oonn RRooaadd PPrriicciinngg

TRB Conference Proceedings 34, ISBN 0-309-09375-9,

98 pages, 8.5 x 11 paperback, 2005, $37.00

TTrraannssppoorrttaattiioonn FFiinnaannccee:: MMeeeettiinngg tthhee FFuunnddiinngg CChhaalllleennggee T

Tooddaayy,,

SShhaappiinngg PPoolliicciieess ffoorr TToommoorrrrooww

TRB Conference Proceedings 33, ISBN 0-309-09499-2,

97 pages, 8.5 x 11 paperback, 2005, $37.00

PPeerrffoorrmmaannccee--BBaasseedd MMeeaassuurreess iinn TTrraannssiitt FFuunndd AAllllooccaattiioonn

Transit Cooperative Research Program, Synthesis of Transit Practice 56, ISBN 0-309-07018-X,

74 pages, 8.5 x 11 paperback, 2004, $16.00

TTrraanns

sppoorrttaattiioonn FFiinnaannccee,, EEccoonnoommiiccss,, aanndd EEccoonnoommiicc DDeevveellooppmmeenntt 22000044

Transportation Research Record: Journal of the Transportation Research Board, No. 1864, ISBN 0-

309-09457-7, 159 pages, 8.5 x 11 paperback, 2004, $50.00

TThhee HHyyddrrooggeenn EEccoonnoommyy:: OOppppoorrttuunniittiieess,,

CCoossttss,, BBaarrrriieerrss,, aanndd RR&&DD NNeeeeddss

National Academy of Engineering, National Academies Press, ISBN 0-309-09163-2,

240 pages, 8.5 x 11 paperback, 2004, $32.00

ISBN 0-309-09419-4

The Fuel Tax

AND ALTERNATIVES FOR

TRANSPORTATION FUNDING

SPECIAL

REPORT

285

Special Report 285

The Fuel Tax

AND ALTERNATIVES FOR TRANSPORTATION FUNDING

TRANSPORTATION RESEARCH BOARD

2006 EXECUTIVE COMMITTEE*

Chair: Michael D. Meyer, Professor, School of Civil and Environmental Engineering, Georgia Institute of Technology, Atlanta

Vice Chair: Linda S. Watson, Executive Director, LYNX–Central Florida Regional Transportation Authority, Orlando

Executive Director: Robert E. Skinner, Jr., Transportation Research Board

Michael W. Behrens, Executive Director, Texas Department of Transportation, Austin

Allen D. Biehler, Secretary, Pennsylvania Department of Transportation, Harrisburg

John D. Bowe, Regional President, APL Americas, Oakland, California

Larry L. Brown, Sr., Executive Director, Mississippi Department of Transportation, Jackson

Deborah H. Butler, Vice President, Customer Service, Norfolk Southern Corporation and Subsidiaries, Atlanta, Georgia

Anne P. Canby, President, Surface Transportation Policy Project, Washington, D.C.

Douglas G. Duncan, President and CEO, FedEx Freight, Memphis, Tennessee

Nicholas J. Garber, Henry L. Kinnier Professor, Department of Civil Engineering, University of Virginia, Charlottesville

Angela Gittens, Vice President, Airport Business Services, HNTB Corporation, Miami, Florida

Genevieve Giuliano, Professor and Senior Associate Dean of Research and Technology, School of Policy, Planning, and

Development, and Director, METRANS National Center for Metropolitan Transportation Research, University of

Southern California, Los Angeles (Past Chair, 2003)

Susan Hanson, Landry University Professor of Geography, Graduate School of Geography, Clark University, Worcester,

Massachusetts

James R. Hertwig, President, CSX Intermodal, Jacksonville, Florida

Gloria J. Jeff, General Manager, City of Los Angeles Department of Transportation, California

Adib K. Kanafani, Cahill Professor of Civil Engineering, University of California, Berkeley

Harold E. Linnenkohl, Commissioner, Georgia Department of Transportation, Atlanta

Sue McNeil, Professor, Department of Civil and Environmental Engineering, University of Delaware, Newark

Debra L. Miller, Secretary, Kansas Department of Transportation, Topeka

Michael R. Morris, Director of Transportation, North Central Texas Council of Governments, Arlington

Carol A. Murray, Commissioner, New Hampshire Department of Transportation, Concord

John R. Njord, Executive Director, Utah Department of Transportation, Salt Lake City (Past Chair, 2005)

Sandra Rosenbloom, Professor of Planning, University of Arizona, Tucson

Henry Gerard Schwartz, Jr., Senior Professor, Washington University, St. Louis, Missouri

Michael S. Townes, President and CEO, Hampton Roads Transit, Virginia (Past Chair, 2004)

C. Michael Walton, Ernest H. Cockrell Centennial Chair in Engineering, University of Texas, Austin

Marion C. Blakey, Administrator, Federal Aviation Administration, U.S. Department of Transportation (ex officio)

Joseph H. Boardman, Administrator, Federal Railroad Administration, U.S. Department of Transportation (ex officio)

Rebecca M. Brewster, President and COO, American Transportation Research Institute, Smyrna, Georgia (ex officio)

George Bugliarello, Chancellor, Polytechnic University of New York, Brooklyn; Foreign Secretary, National Academy of

Engineering, Washington, D.C. (ex officio)

Sandra K. Bushue, Deputy Administrator, Federal Transit Administration, U.S. Department of Transportation (ex officio)

J. Richard Capka, Acting Administrator, Federal Highway Administration, U.S. Department of Transportation (ex officio)

Thomas H. Collins (Adm., U.S. Coast Guard), Commandant, U.S. Coast Guard, Washington, D.C. (ex officio)

James J. Eberhardt, Chief Scientist, Office of FreedomCAR and Vehicle Technologies, U.S. Department of Energy (ex officio)

Jacqueline Glassman, Deputy Administrator, National Highway Traffic Safety Administration, U.S. Department of

Transportation (ex officio)

Edward R. Hamberger, President and CEO, Association of American Railroads, Washington, D.C. (ex officio)

Warren E. Hoemann, Deputy Administrator, Federal Motor Carrier Safety Administration, U.S. Department of

Transportation (ex officio)

John C. Horsley, Executive Director, American Association of State Highway and Transportation Officials, Washington, D.C.

(ex officio)

John E. Jamian, Acting Administrator, Maritime Administration, U.S. Department of Transportation (ex officio)

J. Edward Johnson, Director, Applied Science Directorate, National Aeronautics and Space Administration, John C. Stennis

Space Center, Mississippi (ex officio)

Ashok G. Kaveeshwar, Administrator, Research and Innovative Technology Administration, U.S. Department of

Transportation (ex officio)

Brigham McCown, Deputy Administrator, Pipeline and Hazardous Materials Safety Administration, U.S. Department of

Transportation (ex officio)

William W. Millar, President, American Public Transportation Association, Washington, D.C. (ex officio) (Past Chair, 1992)

Suzanne Rudzinski, Director, Transportation and Regional Programs, U.S. Environmental Protection Agency (ex officio)

Jeffrey N. Shane, Under Secretary for Policy, U.S. Department of Transportation (ex officio)

Carl A. Strock (Maj. Gen., U.S. Army), Chief of Engineers and Commanding General, U.S. Army Corps of Engineers,

Washington, D.C. (ex officio)

*Membership as of April 2006.

Committee for the Study of the Long-Term Viability of

Fuel Taxes for Transportation Finance

Transportation Research Board

Washington, D.C.

2006

www.TRB.org

The Fuel Tax

AND ALTERNATIVES FOR

TRANSPORTATION FUNDING

SPECIAL REPORT 285

71340_001_012.qxd 5/30/06 9:50 AM Page i

Transportation Research Board Special Report 285

Subscriber Category

IA planning and administration

Transportation Research Board publications are available by ordering individual publica-

tions directly from the TRB Business Office, through the Internet at www.TRB.org or

national-academies.org/trb, or by annual subscription through organizational or individual

affiliation with TRB. Affiliates and library subscribers are eligible for substantial discounts.

For further information, contact the Transportation Research Board Business Office, 500

Fifth Street, NW, Washington, DC 20001 (telephone 202-334-3213; fax 202-334-2519;

or e-mail [email protected]).

Copyright 2006 by the National Academy of Sciences. All rights reserved.

Printed in the United States of America.

NOTICE: The project that is the subject of this report was approved by the Governing

Board of the National Research Council, whose members are drawn from the councils of

the National Academy of Sciences, the National Academy of Engineering, and the Institute

of Medicine. The members of the committee responsible for the report were chosen for their

special competencies and with regard for appropriate balance.

This report has been reviewed by a group other than the authors according to the pro-

cedures approved by a Report Review Committee consisting of members of the National

Academy of Sciences, the National Academy of Engineering, and the Institute of Medicine.

This study was sponsored by the National Cooperative Highway Research Program, the

Federal Highway Administration of the U.S. Department of Transportation, and the Trans-

portation Research Board.

Cover and design by Tony Olivis, Studio 2.

Library of Congress Cataloging-in-Publication Data

National Research Council (U.S.). Committee for the Study of the Long-Term Viability

of Fuel Taxes for Transportation Finance.

The fuel tax and alternatives for transportation funding / Committee for the Study of

the Long-Term Viability of Fuel Taxes for Transportation Finance, Transportation

Research Board of the National Academies.

p. cm.

ISBN 0-309-09419-4

1. Transportation—United States—Finance. 2. Motor fuels—Taxation—United

States. 3. User charges—United States. 4. Infrastructure (Economics)—United States—

Finance. 5. Transportation and state—United States—Evaluation. I. Title.

HE206.2.N39 2006

336.2′7866538270913—dc22

2006040428

71340_001_012.qxd 5/30/06 9:50 AM Page ii

The National Academy of Sciences is a private, nonprofit, self-perpetuating society of dis-

tinguished scholars engaged in scientific and engineering research, dedicated to the furtherance

of science and technology and to their use for the general welfare. On the authority of the char-

ter granted to it by the Congress in 1863, the Academy has a mandate that requires it to advise

the federal government on scientific and technical matters. Dr. Ralph J. Cicerone is president

of the National Academy of Sciences.

The National Academy of Engineering was established in 1964, under the charter of the

National Academy of Sciences, as a parallel organization of outstanding engineers. It is

autonomous in its administration and in the selection of its members, sharing with the

National Academy of Sciences the responsibility for advising the federal government. The

National Academy of Engineering also sponsors engineering programs aimed at meeting

national needs, encourages education and research, and recognizes the superior achievements

of engineers. Dr. William A. Wulf is president of the National Academy of Engineering.

The Institute of Medicine was established in 1970 by the National Academy of Sciences to

secure the services of eminent members of appropriate professions in the examination of pol-

icy matters pertaining to the health of the public. The Institute acts under the responsibility

given to the National Academy of Sciences by its congressional charter to be an adviser to the

federal government and, on its own initiative, to identify issues of medical care, research, and

education. Dr. Harvey V. Fineberg is president of the Institute of Medicine.

The National Research Council was organized by the National Academy of Sciences in 1916

to associate the broad community of science and technology with the Academy’s purposes of

furthering knowledge and advising the federal government. Functioning in accordance with

general policies determined by the Academy, the Council has become the principal operat-

ing agency of both the National Academy of Sciences and the National Academy of Engi-

neering in providing services to the government, the public, and the scientific and engineering

communities. The Council is administered jointly by both the Academies and the Institute

of Medicine. Dr. Ralph J. Cicerone and Dr. William A. Wulf are chair and vice chair, respec-

tively, of the National Research Council.

The Transportation Research Board is a division of the National Research Council, which

serves the National Academy of Sciences and the National Academy of Engineering. The

Board’s mission is to promote innovation and progress in transportation through research. In

an objective and interdisciplinary setting, the Board facilitates the sharing of information on

transportation practice and policy by researchers and practitioners; stimulates research and offers

research management services that promote technical excellence; provides expert advice on trans-

portation policy and programs; and disseminates research results broadly and encourages their

implementation. The Board’s varied activities annually engage more than 5,000 engineers, sci-

entists, and other transportation researchers and practitioners from the public and private sec-

tors and academia, all of whom contribute their expertise in the public interest. The program is

supported by state transportation departments, federal agencies including the component

administrations of the U.S. Department of Transportation, and other organizations and indi-

viduals interested in the development of transportation. www.TRB.org

www.national-academies.org

71340_001_012.qxd 5/30/06 9:50 AM Page iii

71340_001_012.qxd 5/30/06 9:50 AM Page iv

Committee for the Study of the Long-Term Viability

of Fuel Taxes for Transportation Finance

Rudolph G. Penner, Urban Institute, Washington, D.C., Chair

Carol Dahl, Colorado School of Mines, Golden

Martha Derthick, Charlottesville, Virginia

David J. Forkenbrock, University of Iowa, Iowa City

David A. Galt, Montana Petroleum Association

Shama Gamkhar, University of Texas, Austin

Thomas D. Larson, Lemont, Pennsylvania

Therese J. McGuire, Northwestern University, Evanston, Illinois

Debra L. Miller, Kansas Department of Transportation

Michael Pagano, University of Illinois, Chicago

Robert W. Poole, Jr., Reason Foundation, Los Angeles, California

Daniel Sperling, University of California, Davis

James T. Taylor II, Bear, Stearns & Co., Inc., New York

Martin Wachs, RAND Corporation, Santa Monica, California

Transportation Research Board Staff

Joseph R. Morris, Study Director

71340_001_012.qxd 5/30/06 9:50 AM Page v

71340_001_012.qxd 5/30/06 9:50 AM Page vi

Preface

The Transportation Research Board (TRB) formed the Committee for the Study

of the Long-Term Viability of Fuel Taxes for Transportation Finance to respond

to concerns that present funding arrangements, especially fuel taxes, may become

less reliable revenue sources for transportation programs in the future. At the same

time, transportation agencies are interested in developments in toll collection

technology and in public–private road projects that suggest opportunities to try

fundamentally new approaches to paying for transportation facilities. The goals

of the study were to assess what recent trends imply for the future of traditional

transportation finance, identify finance alternatives and the criteria by which they

should be evaluated, and suggest ways in which barriers to acceptance of new

approaches might be overcome. The study was sponsored by the state trans-

portation departments through the National Cooperative Highway Research

Program, the Federal Highway Administration, and TRB.

The committee’s conclusions address the viability of present revenue sources,

the merits of present transportation finance arrangements, and the potential value

of various reform options. The recommendations propose immediate changes to

strengthen the existing highway and transit finance system and actions to prepare

the way for more fundamental reform in the long term. Because the impetus

for the study was concern for the continued reliability of the revenues derived

from the special fees and taxes paid by highway users, most of this report is

devoted to questions about future tax revenue, alternative forms of highway user

charges, how these charges affect highway system performance, and related aspects

of highway finance. Problems relating to finance of public transit were not con-

sidered as comprehensively. An important feature of present transportation

finance arrangements is the dedication of portions of highway user revenues to

transit. The committee considered transit funding primarily insofar as it is linked

in this way to highway user fee revenue.

The committee received briefings at its meetings from federal, state, and

local government transportation administrators and from experts in various

aspects of transportation finance. The committee thanks Tyler Duvall, Patrick

vii

71340_001_012.qxd 5/30/06 9:50 AM Page vii

DeCorla-Souza, Michael Freitas, and James March of the U.S. Department of

Transportation; Elizabeth Paris of the staff of the U.S. Senate Finance Com-

mittee; Charles Stoll of the California Department of Transportation; James

Whitty of the Oregon Department of Transportation; Ellen Burton of the

Orange County Transportation Authority; Brian Mayhew of the Metropolitan

Transportation Commission; Marlon Boarnet of the University of California at

Irvine; Helen Sramek of AAA; Darrin Roth of the American Trucking Associa-

tions; Greg Hulsizer of California Transportation Ventures, Inc.; Arlee Reno

and Gary Maring of Cambridge Systematics; Dawn Levy of Cassidy & Associ-

ates; Arthur Guzzetti of the American Public Transportation Association; Jeffrey

Parker; Alan Pisarski; and Arthur Bauer. The committee also thanks Paul Sorensen

and Brian Taylor of the University of California at Los Angeles, authors of a

resource paper prepared for the committee on road use metering systems. The

executive summary of that paper is included as Appendix C of this report. The

contents of the resource paper are the responsibility of the authors.

The report has been reviewed in draft form by individuals chosen for their

diverse perspectives and technical expertise, in accordance with procedures

approved by the National Research Council’s (NRC’s) Report Review Com-

mittee. The purpose of this independent review is to provide candid and critical

comments that assist the authors and NRC in making the published report as

sound as possible and to ensure that the report meets institutional standards for

objectivity, evidence, and responsiveness to the study charge. The review com-

ments and draft manuscript remain confidential to protect the integrity of the

deliberative process. The committee thanks the following individuals for their

participation in the review of this report: David L. Greene, Oak Ridge National

Laboratory, Knoxville, Tennessee; Karen J. Hedlund, Nossaman, Guthner,

Knox, & Elliott LLP, Arlington, Virginia; Herbert S. Levinson, Herbert S.

Levinson Transportation Consultant, New Haven, Connecticut; David

Luberoff, Harvard University, Cambridge, Massachusetts; Jeff Morales, Parsons

Brinckerhoff Quade and Douglas, Inc., Sacramento, California; Ian W. H. Parry,

Resources for the Future, Washington, D.C.; Arlee T. Reno, Cambridge Sys-

tematics, Inc., Chevy Chase, Maryland; and Paul P. Skoutelas, PB Consult, Inc.,

Pittsburgh, Pennsylvania.

Although the reviewers listed above provided many constructive comments

and suggestions, they were not asked to endorse the committee’s conclusions or

recommendations, nor did they see the final draft of the report before its release.

The review of this report was overseen by John S. Chipman, University of Min-

nesota, and C. Michael Walton, University of Texas at Austin. Appointed by

NRC, they were responsible for making certain that an independent examination

of the report was carried out in accordance with institutional procedures and that

all review comments were carefully considered. Responsibility for the final con-

tent of this report rests entirely with the authoring committee and the institution.

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

viii

71340_001_012.qxd 5/30/06 9:50 AM Page viii

Joseph R. Morris managed the study and drafted the final report under the

guidance of the committee and the supervision of Stephen R. Godwin, Director

of Studies and Information Services. Suzanne Schneider, Associate Executive

Director of TRB, managed the report review process. Special appreciation is

expressed to Norman Solomon, who edited the report; Jennifer Weeks, who pre-

pared the prepublication copy; and Juanita Green, who managed the book design

and production, all under the supervision of Javy Awan, Director of Publications.

Frances Holland assisted with meeting arrangements and communications with

committee members.

PREFACE

ix

71340_001_012.qxd 5/30/06 9:50 AM Page ix

71340_001_012.qxd 5/30/06 9:50 AM Page x

Contents

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Study Origin: Transportation Finance Problems . . . . . . . . . . . . . . . . . .11

Charge to the Committee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Guidelines for Finance Arrangements . . . . . . . . . . . . . . . . . . . . . . . . . . .18

Outline of the Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

2 Present Finance Arrangements . . . . . . . . . . . . . . . . . . . . . . . .23

Highway Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

Transit Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

Comparisons with Other Infrastructure and International Practices . . . .36

Trends in the Evolution of the Finance System . . . . . . . . . . . . . . . . . . . .40

3 Evaluating the Present Finance System . . . . . . . . . . . . . . . . .62

Criteria for Evaluating Funding Sources . . . . . . . . . . . . . . . . . . . . . . . . .64

Highway System Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .68

Transit Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81

Evaluation of Finance Program Features . . . . . . . . . . . . . . . . . . . . . . . . .83

4 Effects of Automotive Technology, Energy,

and Regulatory Developments on Finance . . . . . . . . . . . . . .95

Supply, Price, and Consumption of Petroleum Fuels . . . . . . . . . . . . . . . .96

Motor Vehicle Technology Projections and Fuel Tax Revenue . . . . . . .102

Possible Regulatory Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . .112

5 Finance Reform Proposals:

Toll Road Expansion and Road Use Metering . . . . . . . . . .121

Toll Roads and Toll Lanes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .124

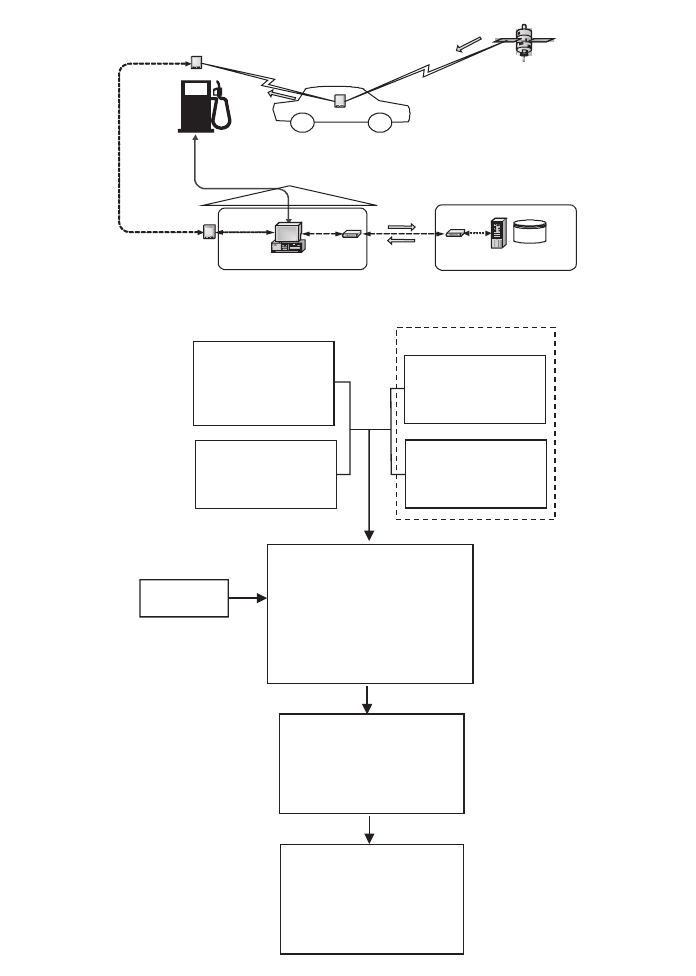

Road Use Metering and Mileage Charging . . . . . . . . . . . . . . . . . . . . . .137

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .154

71340_001_012.qxd 5/30/06 9:50 AM Page xi

6 Finance Reform Proposals:

Reforms Within the Present Framework . . . . . . . . . . . . . . .158

Measures to Increase Available Resources . . . . . . . . . . . . . . . . . . . . . . .159

Measures to Improve Pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .164

Measures to Direct Spending More Effectively . . . . . . . . . . . . . . . . . . .168

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .176

7 Conclusions and Recommendations . . . . . . . . . . . . . . . . . .179

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .179

Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .192

Appendices

A Highway Benefits Estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .202

B Automotive Technology Projections . . . . . . . . . . . . . . . . . . . . . . . . .209

C Review and Synthesis of Road Use Metering

and Charging Systems: Executive Summary . . . . . . . . . . . . . . . . . . .217

Paul A. Sorensen and Brian D. Taylor

Study Committee Biographical Information . . . . . . . . . . . .232

71340_001_012.qxd 5/30/06 9:50 AM Page xii

Summary

Highway

1

programs derive most of their funding from user fees, which are

special taxes and charges incurred by vehicle operators in relation to their use of

roads. Governments dedicate most highway user fee revenue to highway spend-

ing ($85 billion out of $107 billion collected in 2004) and also devote a share

to transit ($11 billion in 2004). Fuel taxes generate most highway user fee rev-

enue (64 percent of the total in 2004); other user fee revenues are from vehicle

registration fees, excise taxes on truck sales, and tolls.

This study assesses the revenue-generating prospects of fuel taxes and other user

fees and identifies alternatives to the present finance arrangement. Transportation

officials have been concerned that the sources that provided stable and growing

revenue for their programs for many decades could become unreliable in the

future. They see two possible threats to the viability of the established arrange-

ment: that fuel consumption and fuel tax revenue could be depressed by changes

in automotive technology, rising fuel prices, or new energy or environmental reg-

ulations; and that the user fee finance principle that has been the basis of high-

way finance may be eroding in practice, as nonhighway applications of user fee

revenues proliferate and dependence on revenue from sources other than user fees

grows. The vulnerability of excise tax revenue to inflation in an era when tax rate

increases often seem politically infeasible magnifies these concerns.

In judging the merits of the present finance system and alternatives, the

Transportation Research Board study committee focused on how finance arrange-

ments affect the performance of the transportation system by influencing the deci-

sions of travelers and government investment and management decisions. This

1

1

In this report, the term “highway” refers to all public highways, roads, and streets, and “transit” refers

to all public local bus, subway, commuter rail, and trolley services, unless otherwise qualified. Intercity

public transportation is excluded from the definition of transit.

71340_013_020 5/30/06 9:51 AM Page 1

criterion led the committee to give special attention to methods of charging fees

that could be directly related to the cost of providing services—in particular, tolls

and mileage charges.

The committee did not estimate how much governments should spend on

transportation and did not interpret its task as devising revenue mechanisms to

support an increased level of spending. There is no certainty that finance reform

in the direction of improving the efficiency of transportation would increase rev-

enues. A reformed finance system would remain subject to many of the external

political and economic constraints that limit the revenue potential of the present

system. However, reform would help transportation agencies to manage capacity

and to target investment to projects with the greatest benefit to the public. Each

dollar spent would be more effective and services would improve, and it is con-

ceivable that the public would be willing to pay more for transportation programs

that worked better.

CONCLUSIONS

The committee’s conclusions concern the two parts of its charge: to assess threats

to the viability of the present finance system and to identify directions for reform

of transportation finance.

Viability of Revenue Sources

The risk is not great that the challenges evident today will prevent the highway

finance system from maintaining its historical performance over the next 15 years;

that is, it should be able to fund growth in capacity and some service improve-

ments, although not at a rate that will reduce overall congestion.

Threat of Loss of the Tax Base

A reduction of 20 percent in average fuel consumption per vehicle mile is possible

by 2025 if fuel economy improvement is driven by regulation or sustained fuel

price increases. Offsetting the revenue effect of such a gain would not require

unprecedented increases in fuel tax rates. The willingness of legislatures to enact

increases may be in question, but the existing revenue sources will retain the capac-

ity to fund transportation programs at historical levels.

Without new regulations, fuel price increases alone probably will stimulate

only a small improvement in fuel economy in this period.

Three factors will constrain the rate of progress on fuel economy: first, con-

sumers prefer to maintain or enhance the performance and size of the vehicles

they buy; second, new vehicles that offer performance and cost close to those of

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

2

71340_013_020 5/30/06 9:51 AM Page 2

today’s vehicles with significantly lower fuel consumption will require time to be

brought into large-scale production; and finally, the stock of vehicles on the road

turns over slowly. Energy forecasts are speculative; however, there are grounds for

expecting that, although the relatively high prices of 2004–2005 may persist, out-

put will increase sufficiently to moderate the long-term price trend. Supplies are

available from multiple sources that can be developed and brought to market at

lower cost than the 2005 price, and maintaining the price of oil at too high a level

is not in the long-term interest of the major producers because it encourages con-

servation and stimulates development of alternative sources.

Erosion of Established Finance Practices

Government transportation finance practices have been remarkably stable and

resilient since the creation of the present federal highway program in 1956.

However, some potential sources of stress are evident, particularly in certain states

where the local share of responsibility is high. These include pressures to expand

use of highway user fee revenue for nonhighway purposes, the growth of transit

spending as a share of local transportation spending, and the vulnerability of rev-

enues to acceleration of inflation.

Merits of the Present System

The finance system has contributed to the success of the highway program in

delivering a positive return on the national investment in highways because fees

modestly discourage motorists from making trips of little value, spending is lim-

ited by the revenues generated from users, and motorists can see the cost of pro-

viding roads in the fuel taxes and registration fees they pay. However, highway

programs have important failings related to finance. The system does not pro-

vide a strong check that individual projects are economically justified. Conges-

tion and pavement costs are tolerated that could be avoided if motorists were

charged prices that more closely matched the cost of their use of roads.

Directions for Reform

Although the present highway finance system can remain viable for some time, trav-

elers and the public would benefit greatly from a transition to a fee structure that

more directly charged vehicle operators for their actual use of roads. The growing

cost of maintaining acceptable service under present funding and pricing prac-

tices may at some point compel reforms that would increase efficiency. The tran-

sition could proceed in stages, starting with closer matching of present fees to

costs and expanded use of tolling. Ultimately, in the fee system that would pro-

vide the greatest public benefit, charges would depend on mileage, road and

SUMMARY

3

71340_013_020 5/30/06 9:51 AM Page 3

vehicle characteristics, and traffic conditions, and they would be set to reflect the

cost of each trip to the highway agency and the public.

The potential benefits of a transition to direct charging are improved opera-

tion of the road system and better targeting of investment to the most valuable

projects. Revenues from charges set to reflect the cost of providing service would

provide an accurate indication of where capacity expansions would have benefit.

Governments that own and operate roads could control fees and funding, so

dependence on intergovernmental aid would be reduced. Reform in this direc-

tion offers the best opportunity for increasing the cost-effectiveness of spending

and mitigating congestion.

The committee identified two complementary tracks for practical reform:

• Toll roads and toll lanes: An important opportunity exists today to create an

extensive system of tolled expressways and expressway lanes employing

existing electronic toll collection technology and variable pricing. Although

such a toll program probably would not greatly increase the funds available

for highways, it could expedite construction of critical highway improve-

ments, provide a tool for managing congestion, and help gain public accept-

ance of road pricing.

• Road use metering and mileage charging: This appears to be the most prom-

ising technique for directly assessing road users for the costs of individual

trips within a comprehensive fee scheme that will generate revenue to cover

the costs of highway programs. It uses communications and information

technology to assess charges according to miles traveled, roads used, and

other conditions related to the cost of service. Unlike conventional tolling,

which is applicable only on expressways, road use metering could be used

to manage and provide funding for all roads. Conversion to road use meter-

ing will require a sustained national effort. Governments must decide on

the goals of the effort, authorities for setting fees and controlling revenue,

the basis for determining fees, and how best to involve the private sector.

Resolution of privacy and fairness concerns will be a prerequisite.

As the finance system evolves, governments can keep it on a course leading

to the necessary improvements by adhering to the following rules:

• Maintain the practice of user fee finance, a system in which users of facil-

ities are charged fees or special taxes, rates reflect the costs to serve each

user, and expenditures equal the fee revenue.

• Seek opportunities where possible to apply pricing—that is, allow fees to

ration access to facilities.

• Align responsibilities so that local governments provide facilities that serve

mainly local travel, states serve regional traffic, and the federal government

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

4

71340_013_020 5/30/06 9:51 AM Page 4

retains only functions that it can perform more effectively than state and

local governments. Governments must control the resources required to

carry out these functions; therefore a goal of reform should be to allow each

jurisdiction to collect fees from all users of its facilities.

• Give full consideration to the environmental and equity consequences of

reform. Fundamental finance reform that aligned fees more closely with

costs would eventually have profound effects on the locations of house-

holds and industries. The overall economic and environmental impacts of

reform would be positive, but some individuals and communities would

suffer harm if no provisions were made for compensation.

RECOMMENDATIONS

The committee proposes immediate changes to strengthen the existing highway

and transit finance system and actions to prepare the way for fundamental reform.

1. Maintain and Reinforce the Existing User Fee Finance System

Because superior alternatives will require time to develop, the nation must con-

tinue to rely on the present framework of transportation funding for at least the

next decade. Therefore, governments must take every opportunity to reinforce

the proven features of the present system, in particular, user fee finance in the

highway program. The following actions would help to maintain the effective-

ness of the overall system:

• The federal government and the states should make adjustments to user

fee rates (for example, adjustments in registration and permit fees to bet-

ter align payments with cost responsibilities) that would provide incentives

for more cost-conscious use of highways by operators of large trucks and

other vehicles.

• Congress and the states should consider eliminating fuel tax exemptions

that are commonly abused and take other measures to reduce losses to tax

evasion.

• The states should make provision for advanced-technology vehicles in the

user fee structure so that operators of these vehicles contribute to the upkeep

of highways on a basis similar to that of other users. In particular, future

vehicles that consume fuels not currently taxed should contribute on some

basis, and incentives to promote conservation technologies should be

designed so that they reasonably apportion the cost burden of the promo-

tion among road users and the public and do not encourage inefficient use

of roads.

SUMMARY

5

71340_013_020 5/30/06 9:51 AM Page 5

• Regardless of the overall scope of the federal surface transportation pro-

gram in the future, the federal government should retain certain core re-

sponsibilities, including aid to ensure that the states to not underinvest in

routes of national significance, the setting of standards, environmental reg-

ulation and enforcement, and research and development.

2. Expand Use of Tolls and Test Road Use Metering

The Federal Role in Promoting Toll Road Development

The federal government should encourage states to experiment with arrange-

ments for tolling and private-sector participation in road development. To this

end, states should be allowed to impose tolls on existing roads that were built with

federal aid, and they should be allowed flexibility in the design of toll systems.

Road Use Metering and Mileage Charging

The states and the federal government should undertake serious exploration of the

potential of road use metering and mileage charging. Creation of a structure to sup-

port individual states that decide to conduct trials or pilot implementations may

be the most practical initial arrangement. However, a program with national focus

will be required, with federal leadership and funding aid for research and testing.

The first requirement will be technical trials to evaluate the reliability, flexi-

bility, cost, security, and enforceability of alternative designs and to gain infor-

mation on proper administration of these systems and user acceptance. Once

technically proven designs are available, the federal government should support

one or more trial implementations that would be on a large scale and fully func-

tional but that would be limited in scope with respect to the region, roads, or vehi-

cles involved. The participating states would require federal technical coordination

and financial aid. Evaluation must be integral to the design of trials and must be

provided for in schedules and budgets. Designs and pilot implementations should

be compatible with the principle that each state and local jurisdiction should con-

trol charges on and revenues generated by the roads it owns.

3. Provide Stable, Broad-Based Tax Support for Transit

Reforms of highway finance arrangements in the future will give rise to needs for

reviewing and adjusting the relationship of highway and transit funding. The

following are guidelines that should be considered:

• Transit systems at present require dedicated, broad-based tax support.

Developing such support will be necessary in order to maintain and expand

transit services.

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

6

71340_013_020 5/30/06 9:51 AM Page 6

• Greatly increasing transfers of highway user fee revenues to fund expanded

transit services would risk a loss of travel benefits through declining high-

way performance that could be greater than the transit benefits gained.

This risk imposes a limit on the potential of existing highway user fees as

a source of transit funding.

• Federal and state transportation aid should be provided for the purpose of

relieving local governments of the burden of serving nonlocal needs rather

than subsidizing local services.

• Road pricing instituted in metropolitan areas should be used to increase

transit’s financial self-sufficiency by eliminating subsidies to highway travel,

giving transit the market power to increase fare revenue, and improving bus

service quality.

4. Evaluate the Impact of Finance Arrangements on Transportation

System Performance

Transportation agencies must develop new capabilities for research, evaluation,

and communication with the public in order to manage finance reform success-

fully over the next few decades. If tolls and mileage charges become important

sources of highway funding, agencies will be faced with fundamentally new

kinds of management decisions and information requirements. At the same

time, the effects of the new charges will provide information never before avail-

able about the value of highway facilities. To develop the capability to fulfill the

new management and information requirements, an organized program will be

necessary. The institutional structure of the program must provide for a joint

federal–state effort, guarantee that scientific evaluations of alternatives are car-

ried out, and build public confidence through open processes.

SUMMARY

7

71340_013_020 5/30/06 9:51 AM Page 7

71340_013_020 5/30/06 9:51 AM Page 8

1

Introduction

Like all government agencies in the United States, those charged with pro-

viding highways and public transit

1

are perennially faced with the challenge of

serving growing needs with constrained resources. The past decade has been

particularly challenging as transportation agencies coped first with rapid traffic

growth during the economic boom of the 1990s and then with stagnant rev-

enues and state government fiscal crises in the aftermath of the 2001 recession.

The federal surface transportation aid program was debated for 2 years after its

expiration in 2003 before reauthorization in 2005, as proposals to increase spend-

ing clashed with opposition to any increase in highway user tax rates to fund

the expansion.

Recent circumstances have heightened long-standing worries of transporta-

tion officials that funding sources, particularly fuel taxes, that provided stable

and growing revenue for transportation programs for 40 years are going to

become unreliable in the future. If petroleum price increases or government

interventions to reduce pollutant emissions or petroleum consumption lead to

widespread use of more efficient automobile engines or lighter passenger vehi-

cles, maintaining revenue will require that legislatures accelerate rate increases.

In addition, there is concern that the political consensus supporting transporta-

tion taxes may be eroding as the goals of the programs become more diffuse, the

public becomes more sensitive to environmental and land use impacts of

expanding infrastructure, and increasing population density and wealth drive up

the costs of infrastructure expansion. The payers of transportation fees and taxes

may view the deterioration of performance as evidence that transportation agen-

9

1

In this report, the term “highway” refers to all public highways, roads, and streets, and “transit” refers

to all public local bus, subway, commuter rail, and trolley services, unless otherwise qualified. Intercity

public transportation is excluded from the definition of transit.

71340_021_034 5/30/06 9:52 AM Page 9

cies are not delivering their money’s worth rather than as evidence that rate

increases are called for.

Opportunities are at hand for fundamentally new approaches that could pro-

vide a sound basis for transportation finance and at the same time improve the

efficiency and quality of transportation services. Progress in the technologies of

toll collection and road use metering has greatly diminished the obstacles of cost

and inconvenience that have discouraged imposition of direct charges on the users

of most roads in the past. With the application of these technologies, highway

services could be paid for by metering each customer’s use and charging accord-

ingly, just as utilities such as water and electricity are paid for today. Development

of this revenue source would maintain the established practice of funding high-

ways largely through fees paid by users, allow fees to be much more closely tied

to the cost of providing service for each user, and provide information to trans-

portation agencies about which investments in capacity would yield the greatest

benefits. Eliminating the connection between highway user revenues and motor

vehicle fuel economy would avoid the potential conflict between transportation

funding objectives and policies intended to promote energy conservation or emis-

sions reductions. In addition, facilities that generated their own revenue would

be suited to operation by private-sector franchisees, so there would be opportu-

nities to supplement public efforts with private capital and skills to carry out infra-

structure projects.

Initial steps toward these new kinds of transportation finance arrangements

are taking place today. Toll roads featuring automatic toll collection and charges

that can be varied to optimize traffic flow, systems to meter vehicle use over an

extensive network of roads and assess charges proportional to mileage, and roads

developed and operated by private firms receiving revenue from road user fees are

in operation in the United States or in other countries. However, before these

arrangements can become major components of the transportation finance sys-

tem, their effectiveness must be demonstrated to the public’s satisfaction and the

institutional capabilities needed to manage them on a large scale must be devel-

oped. In the meantime, it will be worthwhile to seek refinements that could

improve the system’s capacity to provide the right level of funding and direct

funds to the best uses within the established structure of fees, revenue sources,

and assignment of responsibilities among governments.

The Transportation Research Board (TRB) convened the Committee for the

Study of the Long-Term Viability of Fuel Taxes for Transportation Finance to

assess what recent trends imply for the future of traditional transportation finance,

identify finance alternatives and the criteria by which they should be evaluated,

and suggest ways in which barriers to acceptance of new approaches might be over-

come. The study was sponsored by the state transportation departments through

the National Cooperative Highway Research Program, the Federal Highway

Administration, and TRB. This chapter describes the transportation finance prob-

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

10

71340_021_034 5/30/06 9:52 AM Page 10

lems that are the motivation of the study—in particular, as they are seen by state

governments, which are responsible for collecting most highway user taxes and fees

and for most highway spending—and explains the charge to the study committee.

The final section of the chapter identifies guidelines that the committee applied in

its evaluation of alternative government policies for financing transportation.

STUDY ORIGIN: TRANSPORTATION FINANCE PROBLEMS

Several states have undertaken high-level reviews of transportation finance and

tax issues in recent years (Reno and Stowers 1995, Appendix B; CTI 1996; CRC

1996; CRC 1997; CRC 1998; Road User Fee Task Force 2003). These reports

provide examples of the states’ diagnoses of their finance problems. A Commission

on Transportation Investment was formed in 1995 by the state of California “to

investigate California’s investment in transportation infrastructure” (CTI 1996, 5).

The commission’s report defines the finance problem facing the state’s trans-

portation program as follows:

California’s transportation system has been funded from a dedicated gasoline tax

since 1923. . . . Over the last 20 years, however, several trends have occurred which

have led some to question the State’s current reliance on this revenue source.

One of these trends is the increasing fuel economy of today’s vehicles....

This creates the ironic situation of total usage of the system increasing while the

amount of revenue is not increasing at a commensurate rate.

The second trend . . . is the development of alternative fuel vehicles. These

fuels . . . are subject to tax rates that . . . are 12 to 58 percent less than the equiv-

alent tax rate for gasoline. . . . Fuel taxes were originally conceived as a direct user

fee—the more one drives, the more one pays. As alternatives and more efficient

fuels and vehicles come into use, the linkage between the gas tax and the use of

transportation facilities weakens.... This result can be credited to explicit pub-

lic policies stemming from national energy crises and desires to reduce air pol-

lution.... California motorists pay fuel taxes with the assumption that these

revenues are used to maintain and expand the transportation system. But suc-

cessful implementation of the policies noted above [is] causing the fuel tax to be

an unreliable source for all of the system’s needs. (CTI 1996, 13–14)

The commission also cites “a legislative and political climate hostile to new

taxes” as a financial reality (CTI 1996, 25). The report offers a range of options

for coping with the problems, from immediate to long term and from modest

to radical (CTI 1996, 26–28):

1. Living within our means.

2. Increasing the fuel tax.... The disadvantages are that there is little political sup-

port to raise taxes, the fuel tax is not responsive to the increasing fuel efficiency

INTRODUCTION

11

71340_021_034 5/30/06 9:52 AM Page 11

of vehicles, and it does not capture the increasing use that non-gasoline pow-

ered vehicles are likely to be making of the state’s roads.

3. Require alternative fuels . . . to pay taxes that are equivalent on a per mile

traveled basis to the current gasoline and diesel fuel tax.

4. Vehicle Miles Traveled . . . Fee [i.e., a fee proportional to miles traveled].

5. Direct Road Pricing [i.e., a fee depending not only on miles traveled but also

on the road used and traffic conditions].

Immediate actions recommended include curtailing applications of highway user

revenues to nontransportation purposes, expanding opportunities for public–

private partnerships, and introduction of high-occupancy/toll lanes. This list of

immediate and long-term options is representative of current proposals for

resolving state highway program funding problems.

Oregon’s Road User Fee Task Force was formed by the legislature in 2001

with a specific practical charge: “to develop a design for revenue collection for

Oregon’s roads and highways that will replace the current system for revenue col-

lection” (Road User Fee Task Force 2003, 1). The task force defines the state

highway finance problem in nearly the same terms as California’s Commission

on Transportation Investment (Road User Fee Task Force 2001, 1):

Fuel tax revenue constitutes the bulk of the total funding available for Oregon

roads.... New technology will soon greatly improve the average fuel efficiency

of the statewide passenger vehicle fleet.... As a result of fuel efficiency improve-

ments, Oregon fuel tax revenues from the sale of gasoline are likely to level off

during the next 10 years and then drop permanently.

The task force’s proposal has three provisions (Road User Fee Task Force

2003, 25): imposition of new charges in place of existing ones, including a mileage

fee, congestion pricing (i.e., a charge for road travel that is higher at times and loca-

tions where congestion is high), and tolling of all newly constructed roads, bridges,

or lanes; a 20-year phase-in period during which the state would operate both the

mileage fee and the fuel tax; and pilot testing of hardware and administrative

arrangements for the mileage fee as the first step toward implementation. This pro-

posal is described in more detail in Chapter 5.

With similar motivations, 15 states from all regions of the country pooled

funds to conduct the 2002 study A New Approach to Road User Charges. The

study’s report cites, in addition to the concern for revenue adequacy empha-

sized by the Oregon and California panels, other shortcomings of the present

fuel tax system, especially “a weak relationship to the relative costs of particu-

lar trips such that some vehicle operators pay user charges that exceed the costs

they impose, while others pay substantially less than their costs.” Thus, “vehicle

operators are not given signals to make them aware of the costs a particular trip

may impose on society” (Forkenbrock and Kuhl 2002, 1). The report proposes

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

12

71340_021_034 5/30/06 9:52 AM Page 12

technical and administrative arrangements of a system for metering and charg-

ing for each vehicle’s road use and recommends a field test. This proposal also

will be described in Chapter 5.

A final example, the report on highway finance of the nongovernmental

Citizens Research Council of Michigan, was issued at a time when Michigan was

ranked low among the states in fuel tax rates and road conditions and a debate on

raising tax rates was under way. The state increased its gasoline tax rate from 15

to 19 cents per gallon the following year. The theme of the report was that

increasing revenue would by itself be an inadequate response to the fiscal prob-

lem. The main proposals were the following (CRC 1996, 4–13): user tax increases

must be accompanied by management reforms in the highway program (“unless

the system is restructured both financially and administratively, it is very likely

that any additional dollars will not purchase the improvement in transportation

services that might be expected”); jurisdictional control of roads should be

updated, with the state taking over responsibility for roads in local hands that

serve mainly through traffic; an increase in truck registration fees should be con-

sidered; methods of determining priorities must be improved; contracting out

should be increased; and indexation of the fuel tax rate to compensate for infla-

tion should be considered.

Three distinct justifications for considering an overhaul of transportation

finance and highway user fees emerge from these state analyses: a potentially

diminishing tax base, erosion of the user fee finance principle, and the opportu-

nity to improve efficiency. In summary, proponents of changing transportation

funding arrangements have claimed that developments in motor vehicle tech-

nology will threaten the revenue capacity of existing fees, that the finance system

has diverged from its founding principles with harmful consequences, and that

reform in the direction of pricing would increase the public benefits of govern-

ment transportation expenditures. The study committee examined the evidence

supporting each claim.

Potentially Diminishing Tax Base

Among the foremost state concerns in the reports is that energy supply, envi-

ronmental constraints, or changes in automotive technology will reduce fuel

consumption, with reduced revenues as the consequence. The implicit assump-

tion behind this fear is that fuel tax rates will not be raised to compensate. Yet if

the transition to alternative energy sources is gradual, it is not self-evident that

the tasks of adjusting rates and incorporating new fuels into the tax base as the

need arises will necessarily entail such a threat to fiscal soundness. The California

report cites rising political resistance to tax rate increases; however, as Chapter 2

will describe, nationwide average constant-dollar user fee revenue per vehicle

mile has held fairly constant for the past 25 years. The fear that new revenues

INTRODUCTION

13

71340_021_034 5/30/06 9:52 AM Page 13

will not come online as needed may arise from three considerations. First, subsi-

dies in the form of waivers of excises have been a popular way to promote alter-

native energy development (e.g., the fuel tax subsidy granted to gasohol). Second,

imposing new kinds of fees presents technical and administrative problems.

Third, state officials recall the period from the mid-1970s to the early 1980s when

the combination of high inflation, slow economic growth, and increasing auto-

motive fuel economy reduced constant-dollar highway user fee revenue by 50 per-

cent. Tax rates were eventually adjusted, but only after a lag of nearly a decade.

Erosion of the User Fee Finance Principle

One characterization of the finance scheme of the federal-aid highway program

(whose centerpiece is a trust fund receiving revenues from user fees), and of the

similar highway finance schemes of many states, is that of a compact between

highway users and the government highway agency. Users agree to pay fees with

the understanding that the agency will spend the revenue to provide highway

services. At the creation of the Federal Highway Trust Fund in 1956, all revenue

from a specified collection of excise taxes on fuels, vehicles, and parts was dedi-

cated to the fund, to be distributed to the states for highway uses. Over time, the

revenue from these taxes has accumulated additional functions, especially at the

federal level. Since 1979, gasohol (a blend of gasoline with ethanol produced

from grain) has received preferential tax treatment to promote alternative fuels

and aid farmers (the revenue loss, after a 2004 change in federal law, is now

borne by the general fund rather than by transportation programs alone); since

1983, a portion of the fuel tax is dedicated to a fund for mass transit capital proj-

ects; since 1987, a small portion of the fuel tax has been dedicated to the Leaking

Underground Storage Tank Trust Fund; and from 1990 to 1997 a significant

portion of the fuel tax was deposited in the general fund for deficit reduction (and

the general fund continued to receive minor amounts until 2005). During the

fiscal crises that many states faced in the early 2000s, a number of legislatures

chose to apply user fee revenues normally devoted to transportation to general

purposes instead (e.g., AAA Mid-Atlantic 2005). Other uses of the revenues are

sometimes proposed. Meanwhile, at the state and local levels, it has become

increasingly common to dedicate revenues from particular taxes other than gaso-

line or motor vehicle excises (for example, sales taxes) as revenue sources for trans-

portation. (When the law that establishes a tax specifies that revenue from the tax

is to be used for certain specified purposes, the tax is called a dedicated tax.)

The accretion of applications of highway user fee revenue to nonhighway

purposes, together with the popularity of dedicated revenue sources that cannot

be regarded as user fees, weakens the principle of linkage between the fees paid

and the cost of maintaining the highways, which has been the traditional politi-

cal rationale for the present finance scheme. Of course, there are legitimate

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

14

71340_021_034 5/30/06 9:52 AM Page 14

grounds for arguing that transit and the other uses to which user fee revenues have

been dedicated are as reasonable uses of the revenue as is highway construction,

and there has always been controversy over the merits of the user fee–trust fund

arrangement in highway finance. However, if the present system on the whole

tends to promote public welfare, then the states are justified in searching for ways

to reinforce its core principles.

Opportunity to Improve Efficiency

In political discussions, the transportation finance problem traditionally has

been defined as primarily a problem of revenue adequacy: how to raise revenues

sufficient to maintain a desired level of spending or serve defined transportation

needs in a manner that is perceived as fair by the public and highway users. This

definition of the problem is incomplete because it does not take into account the

connection between finance arrangements and the performance of the highway

system. Finance provisions affect the quality of investment decisions and the effi-

ciency of operations. Growing congestion and breakthroughs in technology for

metering road use, as well as interest in exploiting new revenue sources, have

spurred public agencies to consider the use of pricing to manage congestion. It

appears to be less widely appreciated that finance reform, especially reform in

the direction of pricing, would exert a powerful influence on project selection

and overall spending levels, with the potential for improving the targeting of

investment spending to the highest-payoff projects and helping the states to

determine the optimum level of highway spending. Reforms that reduced arbi-

trary variation in tax and fee payments among highway users would make the

finance system more fair as well.

CHARGE TO THE COMMITTEE

These motivations for undertaking reform are reflected in TRB’s charge to the

committee (defined in the task statement in Box 1-1). The committee was asked

to judge the significance of the two hypothesized threats to the viability of rev-

enue sources and finance arrangements. The first is that rising fuel prices, new

automotive technology, or new environmental and energy regulations will affect

revenues in the next few decades and that the financial side effects of these forces,

in the absence of reform, will cause a decline in the performance of the highway

system. The second is that trends in the political choices being made about trans-

portation funding at the federal, state, and local levels today threaten the viabil-

ity of finance arrangements and the performance of the transportation system.

Finally, the committee was asked to identify finance alternatives that would

improve the services that transportation programs afford the public. As the term

INTRODUCTION

15

71340_021_034 5/30/06 9:52 AM Page 15

is used here, a viable funding arrangement is one that will retain the capacity to

fund transportation programs at an inflation-adjusted rate comparable with that

of the past 20 years. In that period, revenues were sufficient to fund growth in

highway spending and capacity and some improvements in service but not to

prevent growing highway congestion.

Implicit in the charge is a broad definition of the scope of the transportation

finance system. The system includes three elements: the schedule of fees or spe-

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

16

BOX 1-1

Committee for the Study of the Long-Term Viability of Fuel Taxes

for Transportation Finance: Statement of Task

The study will examine current practices and trends in finance of roads and

public transit and evaluate options for a long-term transition to alternative

finance arrangements from the present system, which relies heavily on fuel

taxes whose revenues are dedicated to transportation spending. The goals

of the study are to

• Assess the future revenue-generating prospects of the present user fee

tax base, especially the gas tax, considering developments in fuel prices,

automotive technology, and environmental and energy regulation, and

the likely time frame for future technology transitions in transportation.

• Examine developments in transportation finance policies of federal,

state, and local governments.

• Assess the implications of finance trends for the performance of the

transportation system, and whether benefits could be attained through

reform.

• Identify alternatives to the present finance scheme and the criteria by

which they should be judged, considering the influence of finance arrange-

ments on the performance of the transportation system. Alternatives may

include long-term prospects for road pricing and for privatization as

well as immediate measures aimed at reinforcing positive features of the

present scheme.

• Identify institutional and technical obstacles that may hinder needed

finance reforms and recommend a transition strategy to new finance

arrangements if reform appears necessary.

71340_021_034 5/30/06 9:52 AM Page 16

cial taxes that governments or other operators collect from users of highways and

public transit; the sources of funds for transportation programs (which may

include dedicated user fees, other dedicated revenues, general fund appropria-

tions, and grants from other governments); and finally, the institutional arrange-

ments and rules that determine budgets, spending priorities, and the distribution

of responsibilities among levels of government. The impetus for this study was

concern for the viability of present highway user fees as a revenue source; there-

fore, the committee has considered transit finance primarily insofar as it is linked

to highway user fees. A prominent feature of the present finance system is the ded-

ication of portions of federal and state highway user fee revenues to transit.

The committee assumed that short-term as well as long-term opportunities

for improvement in finance arrangements were within its charge. A transition to

some form of road pricing or direct mileage-based charges is viewed favorably in

the state finance studies cited above and may be gaining recognition as the desir-

able eventual outcome. However, it is important not to neglect measures aimed

at reinforcing the positive features of the present system. In the short term, depen-

dence on fuel taxes and vehicle registration and license fees as revenue sources for

transportation will continue.

Highway finance practices have consequences for environmental quality and

energy consumption, but they have not been examined in this study. As the report

will describe, one of the failings of present practices is that, although revenues

from the fees and special taxes motorists pay cover most highway agency expen-

ditures to build and operate roads, fees do not reflect other public costs of road

travel, such as congestion delay and automotive pollution. The result is that road

users make many trips that cost the public more to provide than they are worth

to the traveler. A system for road use metering and mileage charging (a concept

described in Chapter 5) could correct this failing, if public officials chose, by

charging fees that approximated the actual costs of trips, taking into account the

time and place of travel.

Within the present framework of highway user fees, proposals have been

made to impose a pollution charge in the form of an increase in the fuel tax as a

way to reduce automotive pollution costs. Before enacting such a tax, governments

would have to consider the costs of overcharging vehicles that produce little pol-

lution and travel in areas where pollution costs are low. A pollution tax would

also complicate administration of the present user fee finance system, because

history suggests a tendency for the revenue from taxes paid by road users to be

devoted to road building eventually, regardless of the original intent. Finally, fun-

damental change in road user charges and the means of paying for roads would

have important impacts on land use. Governments will need to consider such

impacts as the transportation financing system evolves.

Partially or entirely replacing fuel taxes with fees based on mileage would

reduce or eliminate the incentive that fuel taxes provide to motorists to choose

INTRODUCTION

17

71340_021_034 5/30/06 9:52 AM Page 17

more fuel-efficient vehicles or otherwise conserve fuel. If fuel taxes are reduced in

the future, the impact on fuel consumption should be recognized and consider-

ation given to the need for offsetting actions, if the outcome appears contrary to

goals of U.S. energy policy. (Of course, a mileage-charging scheme could incor-

porate conservation incentives.) A mileage-charging scheme that incorporated

peak charges would have an important impact on energy consumption through

its influence on congestion, travel, and land use. These effects have not been

examined in this study. As will be argued in Chapter 4, the most cost-effective

taxes for promoting petroleum conservation would be broad-based taxes applied

equally to all petroleum consumers.

Lack of information makes definitive responses to all the questions raised in

the study charge impossible. Projections of technology and energy futures are

inherently highly uncertain. There is little systematic information on how the

existing structure of charges, subsidies, and grant programs affects the decisions of

users and transportation agencies. Information on the benefits and costs of high-

way investments and other transportation programs is fragmentary because agen-

cies do not routinely conduct rigorous economic evaluations of their projects.

Because of this information gap and lack of experience with some of the

reform measures that have been most prominently proposed, any specific and

detailed recommendation for a new transportation finance system would be pre-

mature. Preparation for long-term reform will require basic research, planning,

the promotion of informed public discussion, and early implementation of new

approaches where circumstances permit, with the goal of learning from experi-

ence. A strength of U.S. transportation programs in this respect is the variety of

conditions, experience, and practices among the states, which provide a natural

laboratory for problem solving. The committee’s conclusions and recommenda-

tions are to point out opportunities in these directions.

GUIDELINES FOR FINANCE ARRANGEMENTS

The study charge calls for evaluating the present transportation finance system

and alternatives. This task requires criteria for comparison and an understanding

of the goals of the finance system. Chapter 3 reviews methods and criteria that

have been used to evaluate finance practices. In this introductory chapter it is

appropriate to state certain premises that the committee believes should under-

lie the evaluations:

1. Finance arrangements are central to the performance of the transportation sys-

tem. Choices about fees and taxes charged to users and about funding

sources are critical not only to the feasibility of a transportation project or

program but also to the likelihood of its success. The finance system is a

THE FUEL TAX AND ALTERNATIVES FOR TRANSPORTATION FUNDING

18

71340_021_034 5/30/06 9:52 AM Page 18

major influence on decisions about which projects and services are pro-

vided and how existing facilities are utilized. Therefore, any fundamental

change in finance arrangements (e.g., replacing current user fees with fees

of a different form) would strongly affect transportation system perform-

ance. Decisions on finance also determine the distribution of the costs and

benefits of transportation programs. Finance alternatives should be evalu-

ated in terms of these impacts.

2. Efficiency is an important test of finance options. The first test that should be

applied to a proposed finance reform is whether it would tend to promote

efficient investment and operation. That is, finance arrangements should

encourage investments in the transportation system that yield economic

benefits and discourage investments that do not, and they should encour-

age operating practices on existing facilities such that service is provided to

those who value the service more highly than the cost of producing it and

is not provided to others. The cost of transportation services includes con-

gestion, environmental costs, and accident costs. Nearly any change in the

finance system—adjustments in highway user fees, changes in the dedica-

tion of particular revenues to particular uses, or changes in grant rules—

will affect efficiency.

3. Pricing is a means to allow users to express what they want from the trans-

portation system. Pricing means a system of imposing charges on users in

which each user recognizes a connection between decisions to use the trans-

portation system and the charges incurred and the operating agency sets

the charges on the basis of the cost of providing service to the user. The

present highway user fee scheme of fuel taxes, registration fees, and licens-

ing fees is an imperfect form of pricing. In a more refined scheme, such as

the proposals for mileage charges cited above, the fee would be much more

closely matched to the cost of each trip. The intent of pricing should be to

give consumers the information they require to make efficient choices,

rather than to dictate choices. In general, the price-setting process should

not set targets for mode shares, congestion or pollution levels, or land use

patterns and then adjust fees until the targets are reached. Rather, fees

should be set according to costs, and travelers should be allowed to choose

their preferred modes, congestion levels, and locations for activities. [The

relevant costs and methods of measuring them were identified in the report

of an earlier TRB committee (TRB 1996).]