Key findings from this report include:

Total Marketplace Plan Selections: During the 2024 OEP, over 21.4 million

consumers selected or were automatically re-enrolled

2

in health insurance

coverage through HealthCare.gov Marketplaces and SBMs. 5.1 million more

consumers signed up for coverage during the 2024 OEP compared to the 2023

OEP, a 31% increase. Nearly 7 million more consumers signed up compared to

the 2022 OEP and 9.4 million more consumers signed up compared to the 2021

OEP, reflecting a 48% and 79% increase respectively.

•

HealthCare.gov Marketplaces Plan Selections: In HealthCare.gov

Marketplaces, 16.4 million consumers selected plans during the 2024 OEP

between November 1, 2023 and January 16, 2024.

•

State-based Marketplaces Plan Selections: Across the 19 SBMs, 5.1 million

consumers selected plans during the 2024 OEP from November 1, 2023

through the end of their respective OEPs.

HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT

The Health Insurance Marketplaces 2024 Open Enrollment Report summarizes

health plan selections through the individual Marketplaces during the 2024 Open

Enrollment Period (OEP). This report includes OEP data for the 32 states with

Marketplaces that use the HealthCare.gov eligibility and enrollment platform for the

2024 plan year (HealthCare.gov Marketplaces), as well as for the 19 State-based

Marketplaces (SBMs) that use their own eligibility and enrollment platforms.

1

1

Plan selections and other data by Marketplace platform for each OEP reflects the status of the state’s platform at

the time of that OEP unless noted otherwise. Data for SBMs that use their own eligibility and enrollment platforms

are retrieved from the respective states’ information systems and have not been fully validated by CMS; thus,

metrics for these states may vary. The 19 SBMs that use their own eligibility and enrollment platforms in 2024 are

California, Colorado, Connecticut, the District of Columbia, Idaho, Kentucky, Maine, Maryland, Massachusetts,

Minnesota, Nevada, New Jersey, New Mexico, New York, Pennsylvania, Rhode Island, Vermont, Virginia and

Washington. Virginia transitioned to a SBM for the 2024 plan year; Kentucky, Maine, and New Mexico transitioned

to SBMs for the 2022 plan year; New Jersey and Pennsylvania transitioned to SBMs for the 2021 plan year; and

Nevada transitioned to a SBM for the 2020 plan year.

2

As in prior years, consumers with Marketplace coverage at the end of 2023 who did not make an active plan

selection were generally automatically re-enrolled for 2024 coverage. When consumers had 2024 Marketplace plans

available to them from their 2023 issuer, they were generally automatically re-enrolled into the same plan as 2023 or

a different plan from the same issuer. Depending on the Marketplace, they could also be automatically re-enrolled

into a suggested alternate plan from a different issuer if no plan from their current issuer was available to them.

Beginning in plan year 2024, CMS finalized a change to the hierarchy at 45 CFR 155.335(j)(4) that allows

Marketplaces to modify their automatic re-enrollment hierarchies such that some consumers who are eligible for

CSRs and are currently enrolled in a bronze level QHP are instead automatically re-enrolled in a silver-level QHP

(with CSRs).

•

New Consumers: Nationwide, the number of new consumers selecting

Marketplace coverage during the 2024 OEP increased by 41%, to 5.2 million

from 3.7 million in the 2023 OEP.

•

Demographic Trends: Among consumers who attested to a race or ethnicity,

22% identified as Hispanic/Latino in the 2024 OEP, compared to 21% in the

2023 OEP, and the percent of consumers who attested to a race or ethnicity

and identified as Black remained at 9% in the 2024 OEP.

•

Premiums and Financial Assistance: Nationwide, 9.6 million more consumers

are receiving Advance Payments of the Premium Tax Credit (APTC) in 2024

compared to 2021. Additionally, 1.5 million consumers reported household

incomes over 400% of the Federal Poverty Level (FPL) during the 2024 OEP.

Without the continued expansion of subsidies made available through the

American Rescue Plan (ARP) and Inflation Reduction Act (IRA), these

consumers would have been ineligible for APTC. The average monthly

premium after APTC fell by 32%, from $164 in 2021 to $111 in 2024, and 44%

of consumers, or nearly 9.4 million people, selected a plan for $10 or less per

month after APTC during the 2024 OEP.

•

Cost-Sharing: For the 2024 OEP, 50% of all Marketplace consumers received

cost-sharing reductions (CSRs).

•

Consumer Savings due to ARP and IRA: National estimates show that most

consumers qualify for $0 premiums or are continuing to see annual premium

savings exceeding $800, underscoring the continued impact of expanded

subsidies made available through the ARP/IRA.

3

In HealthCare.gov

Marketplaces, consumers with APTC are saving an average of 48% on

monthly premiums, due to the continued availability of expanded subsidies

through the IRA.

3

As a result of ARP/IRA changes to the applicable percentage table (https://www.irs.gov/pub/irs-drop/rp-23-

29.pdfhttps://www.irs.gov/pub/irs-drop/rp-23-29.pdf), households with incomes under 150% FPL have access to

QHPs with $0 or near-$0 premium amounts. Table 8 reports the average premium savings from ARP/IRA across all

income categories at $705 per year. For income groups above 150% FPL, the average premium savings from

ARP/IRA exceed $800 per year.

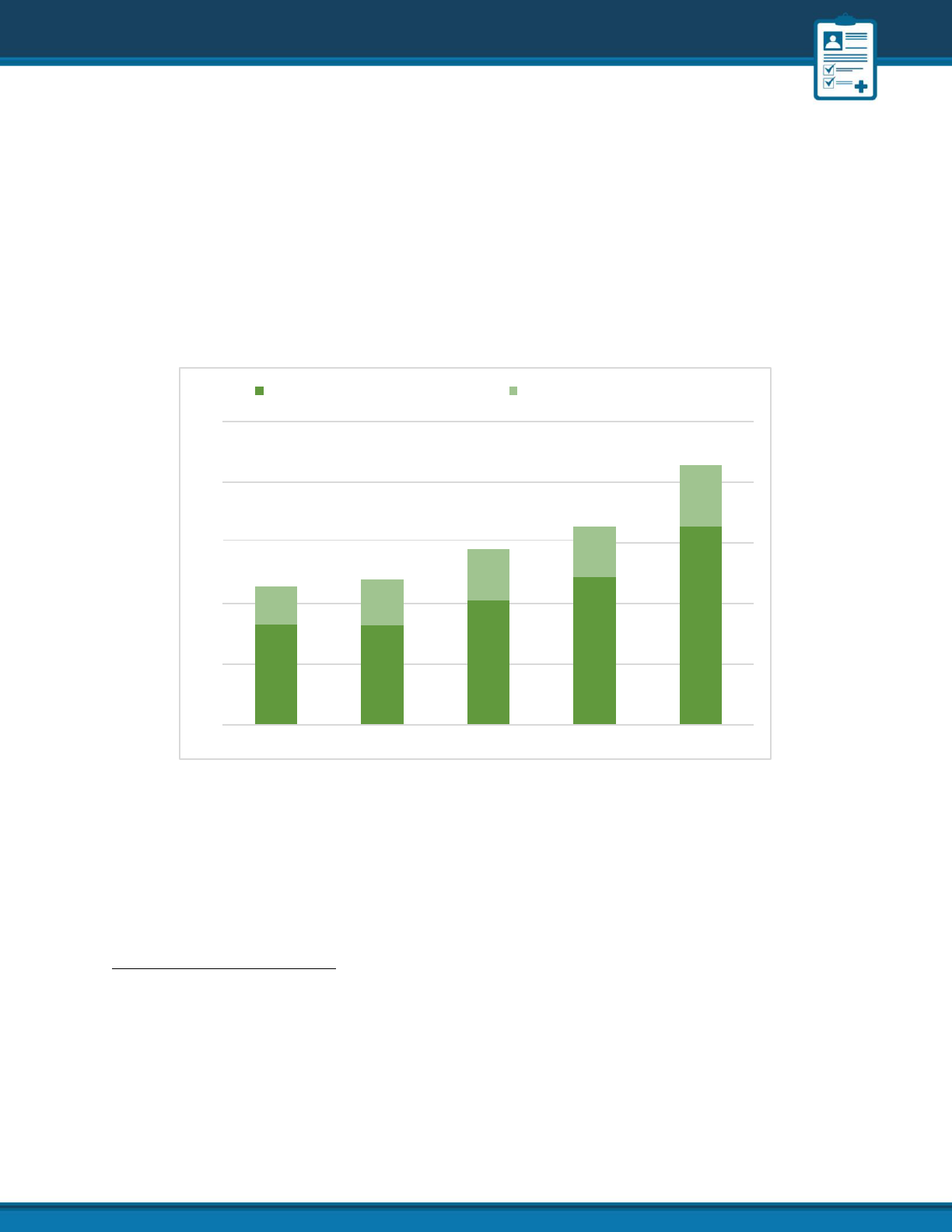

HealthCare.gov Marketplaces State-based Marketplaces

25

21.4M

20

5.1M

16.4M

15

14.5M

4.2M

11.4M

12.0M

4.3M

10

3.1M

3.8M

16.4M

5

8.3M 8.3M

10.3M

12.2M

0

2020 2021 2022 2023 2024

CONSUMERS SELECTING PLANS THROUGH THE MARKETPLACES: 50 STATES,

PLUS DC

During the 2024 OEP, 21.4 million consumers selected or were automatically re-

enrolled in a Marketplace plan. This includes 16.4 million consumers in Marketplaces

using the HealthCare.gov platform and 5.1 million consumers in SBMs using their

own platforms (see Figure 1).

Figure 1: Plan Selections during 2020 - 2024 Open Enrollment Periods

4

4

For HealthCare.gov Marketplaces: the 2020 OEP was from 11/1/2019 to 12/15/2019, with data reported through

12/21/2019 (this includes the additional time provided to consumers who were unable to enroll by the original

deadline); the 2021 OEP was from 11/1/2020 to 12/15/2020, with data reported through 12/21/2020 (this includes

the additional time provided to consumers who were unable to enroll by the original deadline); the 2022 OEP was

from 11/1/2021 to 1/15/2022, with data reported through 1/15/2022; the 2023 OEP was from 11/1/2022 to

1/15/2023, with data reported through 1/15/2023; the 2024 OEP was from 11/1/2023 to 1/16/2024, with data

reported through 1/16/2024. Dates through which data are reported vary for SBMs; see the PUF FAQs for detailed

information.

Nationwide, the number of plan selections during the 2024 OEP increased by 31% in

comparison to the 2023 OEP, 48% in comparison to the 2022 OEP, and 79% in

comparison to the 2021 OEP (see Table 1). In HealthCare.gov Marketplaces, plan

selections increased by 34%, to 16.4 million during the 2024 OEP from 12.2 million

during the 2023 OEP. In comparison to the 2022 OEP, plan selections increased by

60% from 10.3 million. Plan selections in SBMs increased by 22% to 5.1 million during

the 2024 OEP from 4.2 million during the 2023 OEP and by 19% from 4.3 million

during the 2022 OEP. HealthCare.gov data reflects the HealthCare.gov platform’s

2024 OEP which ran from November 1, 2023 through January 16, 2024. For the SBMs,

the number of plan selections included in this report reflects data from the

timeframe of each SBM’s 2024 OEP, which varies by state.

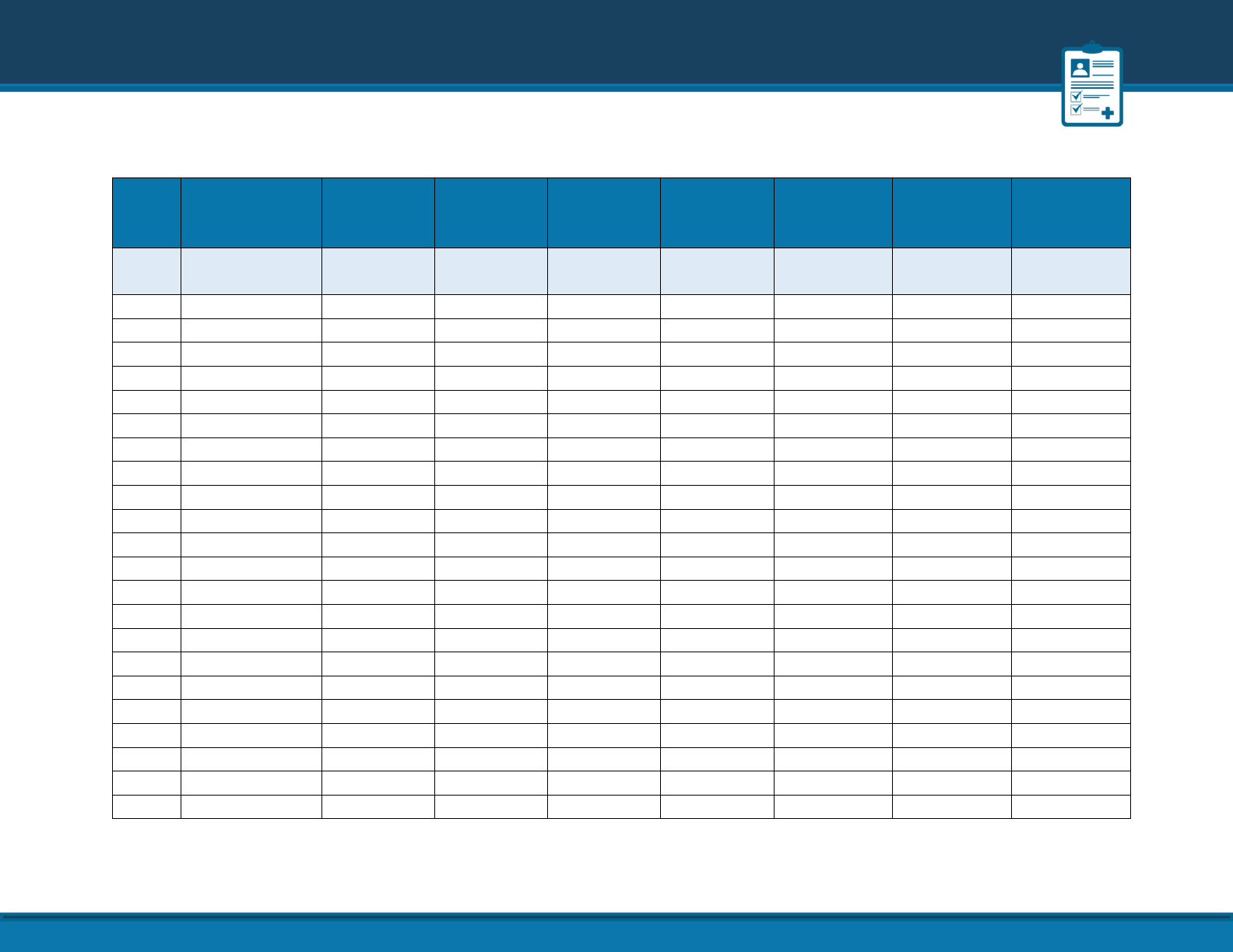

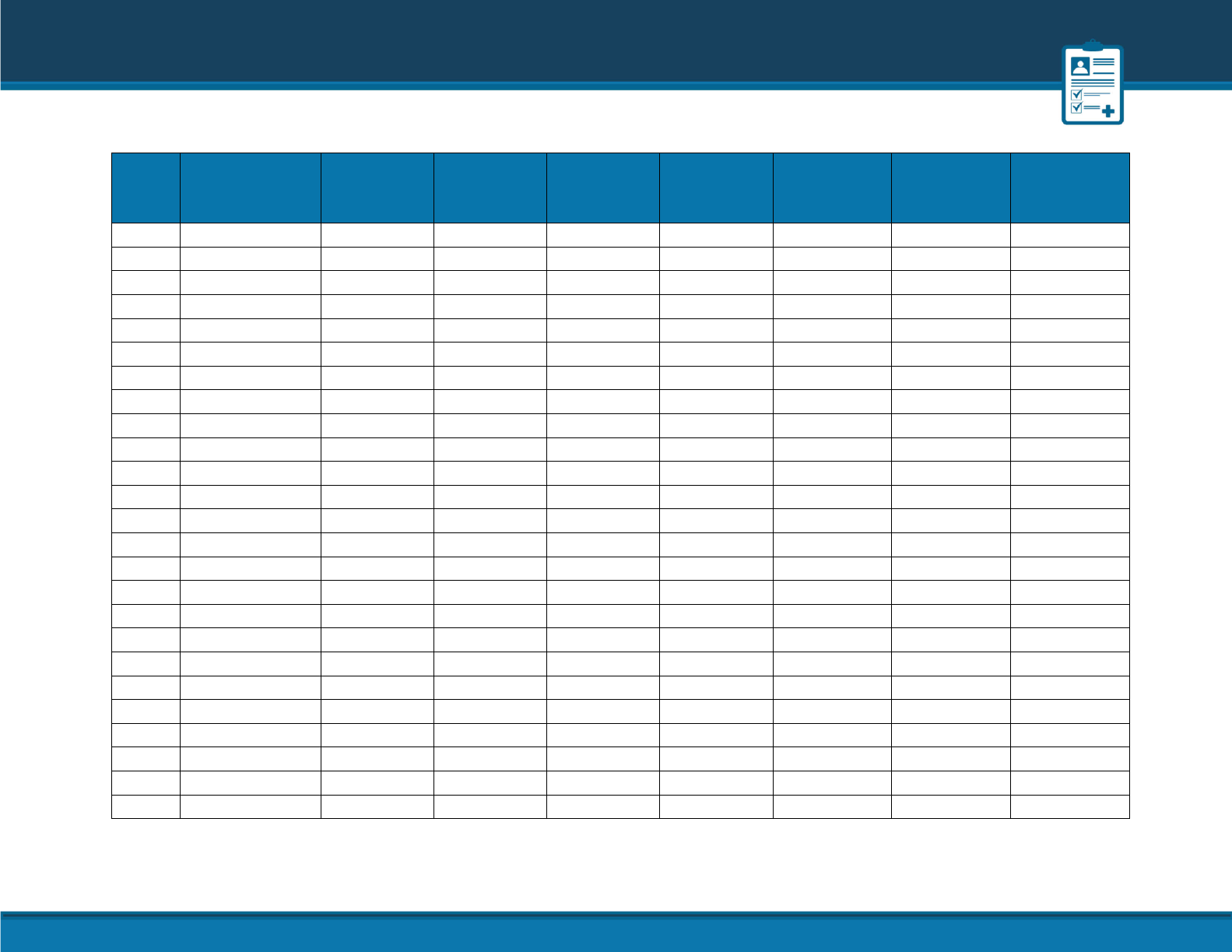

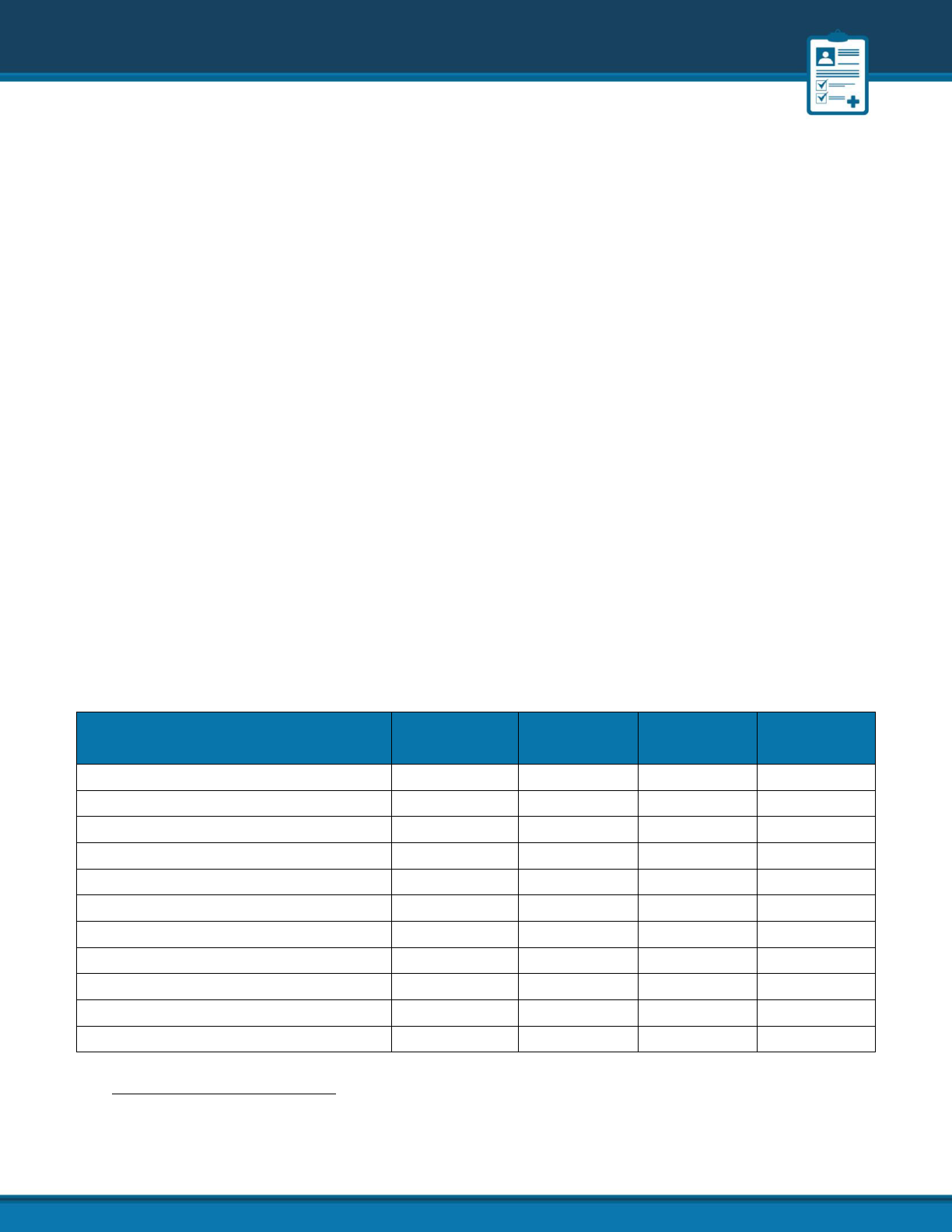

From 2023 to 2024, 44 of the 51 Marketplaces saw increases in plan selections of at

least 10%. While plan selections in Medicaid non-expansion states accounted for over

half of total 2024 OEP plan selections, several Medicaid expansion states experienced

greater increases in plan selections. The states with the highest increases in plan

selections, from 2023 to 2024, included West Virginia (80%), Louisiana (76%), Ohio

(62%), Indiana (60%), and Tennessee (59%). In contrast, the Marketplaces with the

smallest increases in plan selections, from 2023 to 2024, included California and

Nevada (3%), Hawaii and Oregon (2%), and the District of Columbia (0%). Notably,

only one Marketplace, Maine (-1%), saw a decrease in plan selections.

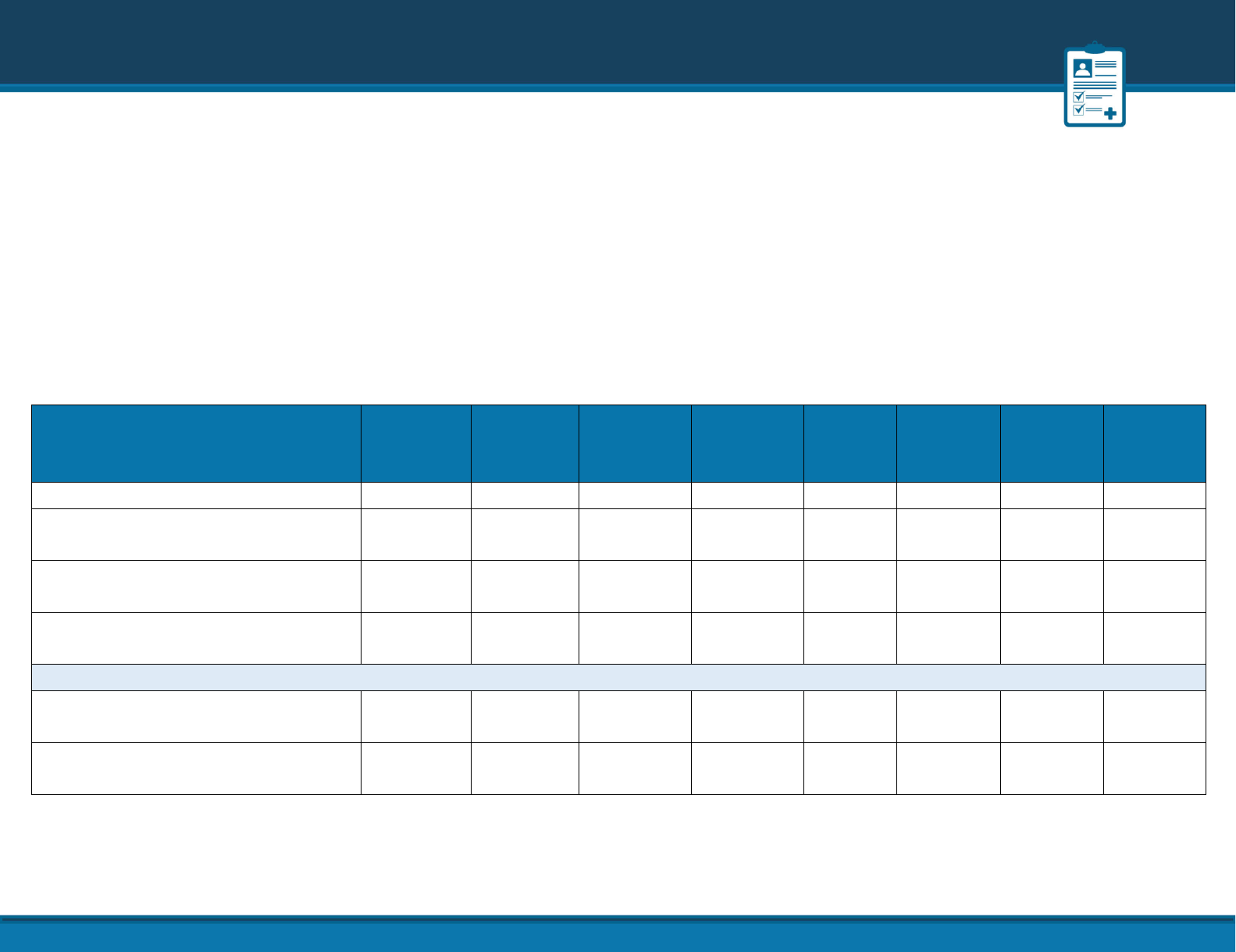

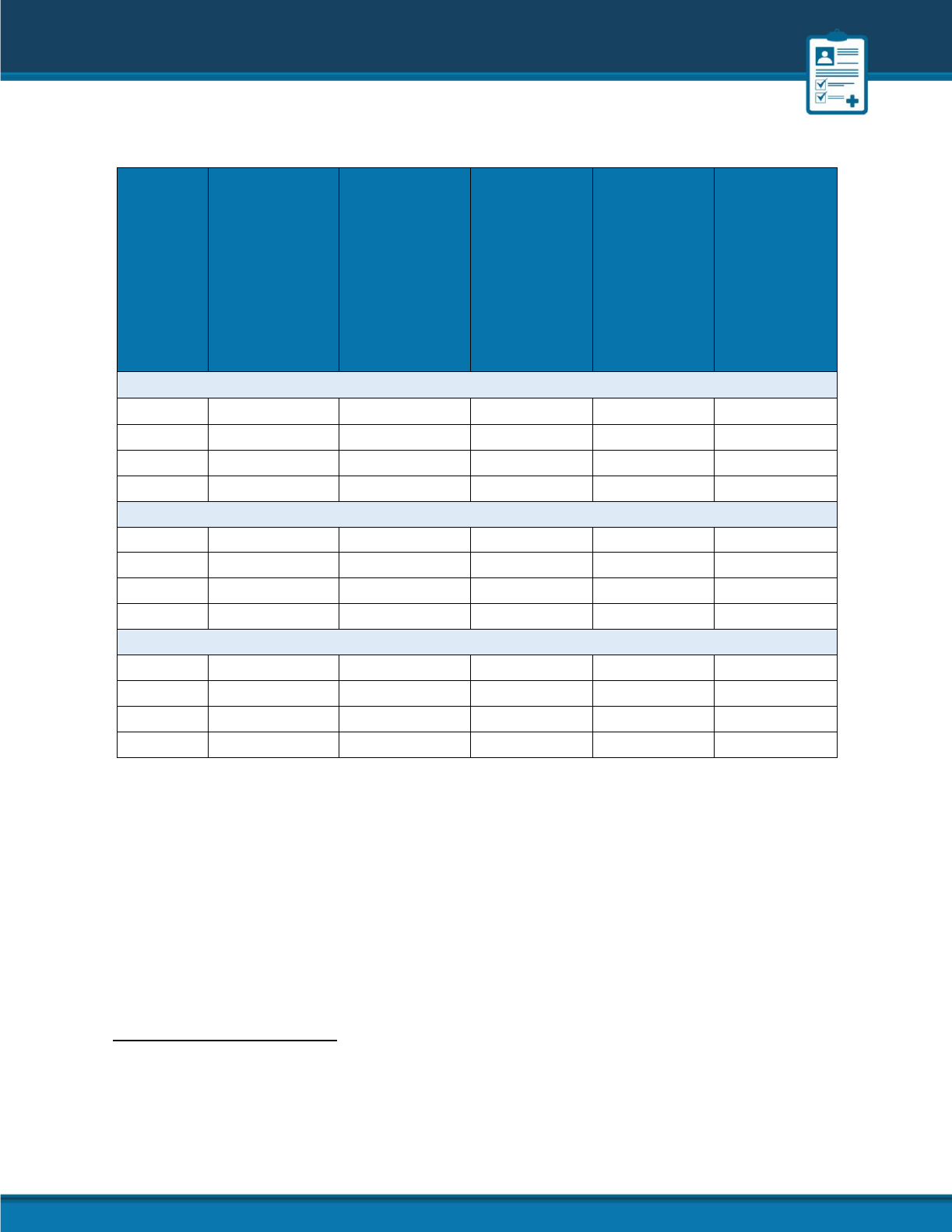

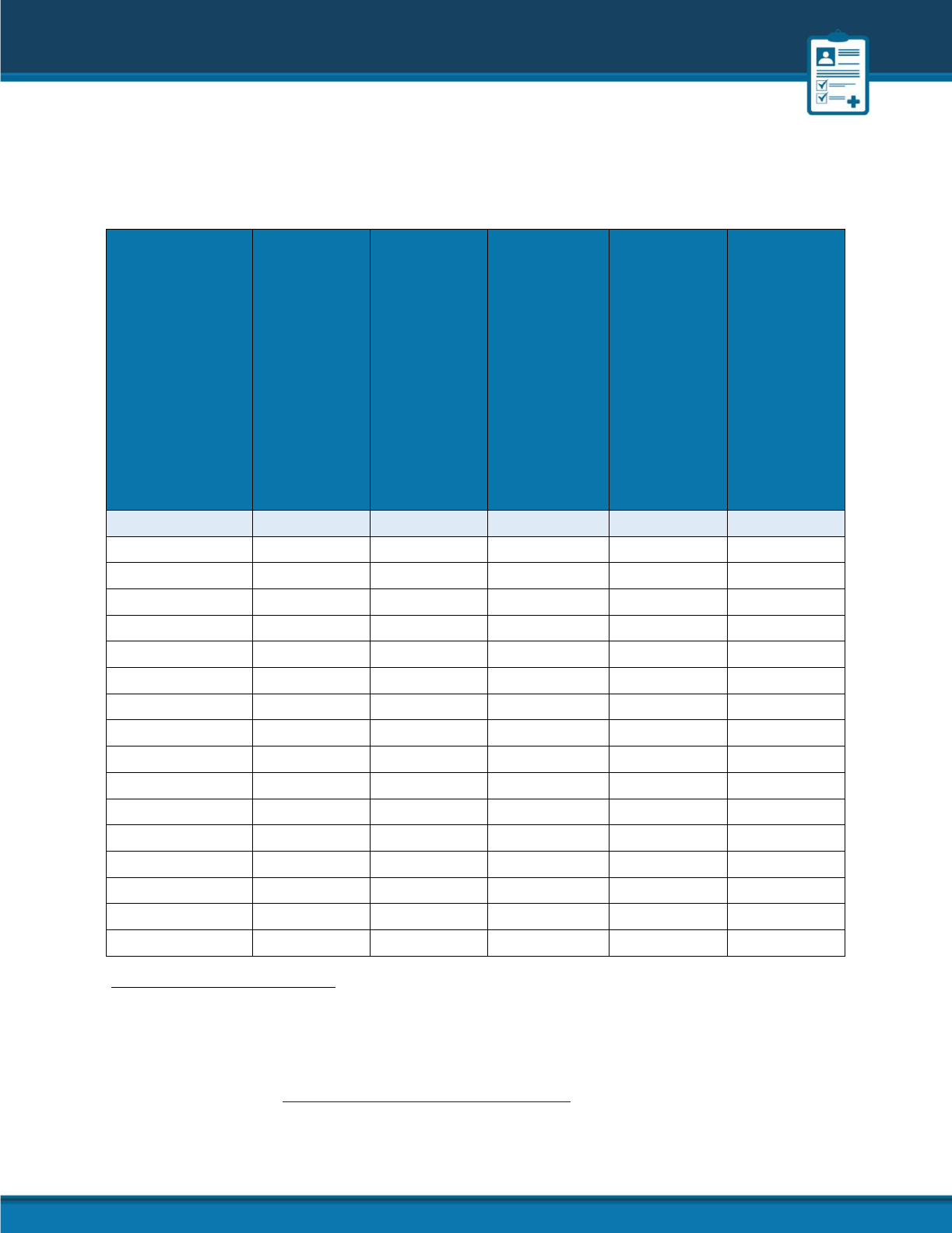

Table 1: OEP Plan Selections by State

State

2024

Platform

2024

2023

2022

2021

% Change

2023 to

2024

% Change

2022 to

2024

% Change

2021 to

2024

Total

HC.gov

SBM

&

21,446,150

16,357,030

14,511,077

12,004,365

31%

48%

79%

AK

HC.gov

27,464

25,572

22,786

18,184

7%

21%

51%

AL

HC.gov

386,195

258,327

219,314

169,119

49%

76%

128%

AR

HC.gov

156,607

100,407

88,226

66,094

56%

78%

137%

AZ

HC.gov

348,055

235,229

199,706

154,504

48%

74%

125%

CA

SBM

1,784,653

1,739,368

1,777,442

1,625,546

3%

0%

10%

CO

SBM

237,106

201,758

198,412

179,607

18%

20%

32%

CT

SBM

129,000

108,132

112,633

104,946

19%

15%

23%

DC

SBM

14,799

14,768

15,989

16,947

0%

-7%

-13%

DE

HC.gov

44,842

34,742

32,113

25,320

29%

40%

77%

FL

HC.gov

4,211,902

3,225,435

2,723,094

2,120,350

31%

55%

99%

GA

HC.gov

1,305,114

879,084

701,135

517,113

48%

86%

152%

HI

HC.gov

22,170

21,645

22,327

22,903

2%

-1%

-3%

IA

HC.gov

111,423

82,704

72,240

59,228

35%

54%

88%

ID

SBM

103,783

79,927

73,359

68,832

30%

41%

51%

IL

HC.gov

398,814

342,995

323,427

291,215

16%

23%

37%

IN

HC.gov

295,772

185,354

156,926

136,593

60%

88%

117%

KS

HC.gov

171,376

124,473

107,784

88,627

38%

59%

93%

KY

SBM

75,317

62,562

73,935

77,821

20%

2%

-3%

LA

HC.gov

212,493

120,804

99,626

83,159

76%

113%

156%

MA

SBM

311,199

232,621

268,023

294,097

34%

16%

6%

MD

SBM

213,895

182,166

181,603

166,038

17%

18%

29%

ME

SBM

62,586

63,388

66,095

59,738

-1%

-5%

5%

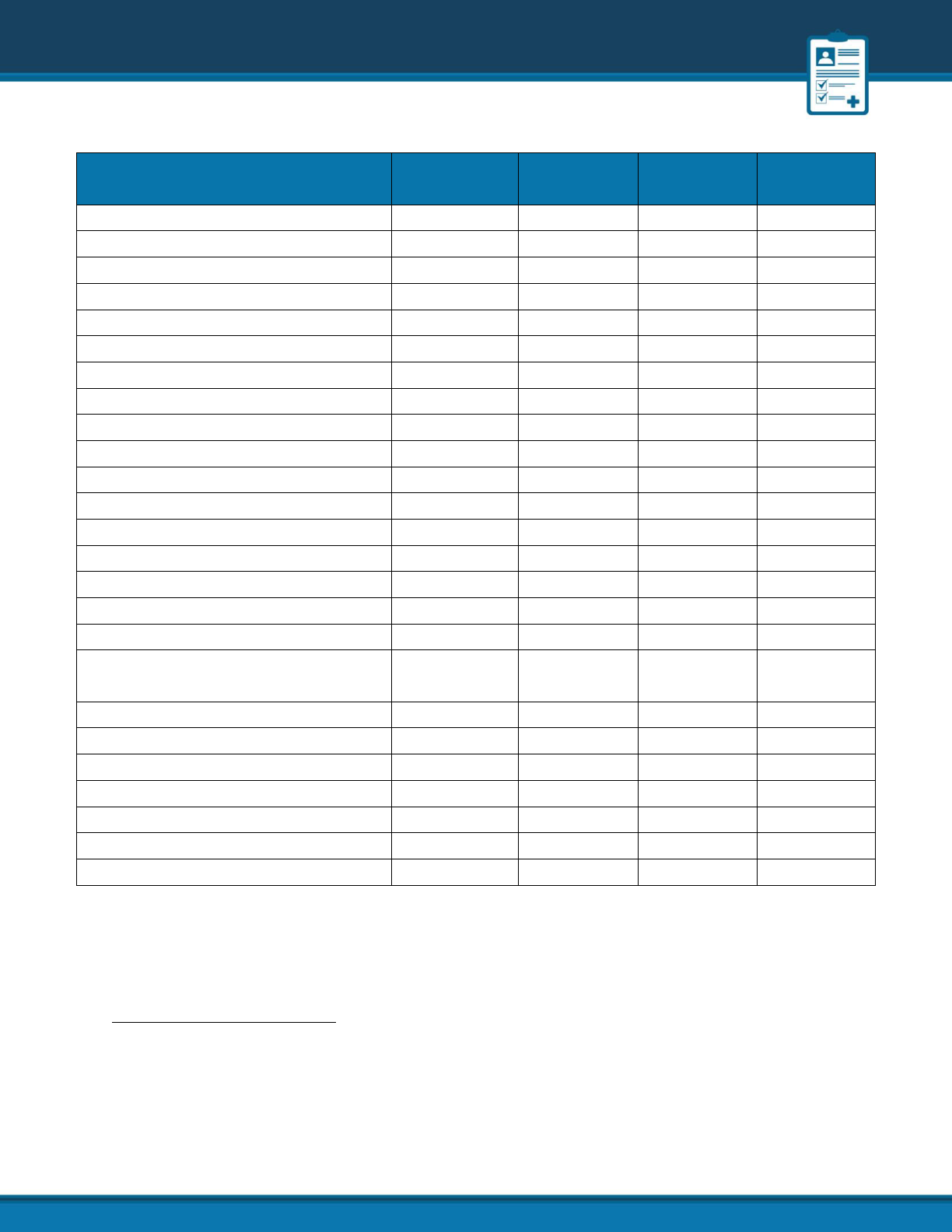

State

2024

Platform

2024

2023

2022

2021

% Change

2023 to

2024

% Change

2022 to

2024

% Change

2021 to

2024

MI

HC.gov

418,100

322,273

303,550

267,070

30%

38%

57%

MN

SBM

135,001

118,431

121,322

112,804

14%

11%

20%

MO

HC.gov

359,369

257,629

250,341

215,311

39%

44%

67%

MS

HC.gov

286,410

183,478

143,014

110,966

56%

100%

158%

MT

HC.gov

66,336

53,860

51,134

44,711

23%

30%

48%

NC

HC.gov

1,027,930

800,850

670,223

535,803

28%

53%

92%

ND

HC.gov

38,535

34,130

29,873

22,709

13%

29%

70%

NE

HC.gov

117,882

101,490

99,011

88,688

16%

19%

33%

NH

HC.gov

65,117

54,557

52,497

46,670

19%

24%

40%

NJ

SBM

397,942

341,901

324,266

269,560

16%

23%

48%

NM

SBM

56,472

40,778

45,664

42,984

38%

24%

31%

NV

SBM

99,312

96,379

101,411

81,903

3%

-2%

21%

NY

SBM

288,681

214,052

221,895

215,889

35%

30%

34%

OH

HC.gov

477,793

294,644

259,999

201,069

62%

84%

138%

OK

HC.gov

277,436

203,157

189,444

171,551

37%

46%

62%

OR

HC.gov

145,509

141,963

146,602

141,089

2%

-1%

3%

PA

SBM

434,571

371,516

374,776

337,722

17%

16%

29%

RI

SBM

36,121

29,626

32,345

31,174

22%

12%

16%

SC

HC.gov

571,175

382,968

300,392

230,050

49%

90%

148%

SD

HC.gov

52,974

47,591

41,339

31,375

11%

28%

69%

TN

HC.gov

555,103

348,097

273,680

212,052

59%

103%

162%

TX

HC.gov

3,484,632

2,410,810

1,840,947

1,291,972

45%

89%

170%

UT

HC.gov

366,939

295,196

256,932

207,911

24%

43%

76%

VA

SBM

400,058

346,140

307,946

261,943

16%

30%

53%

VT

SBM

30,027

25,664

26,705

24,866

17%

12%

21%

State

2024

Platform

2024

2023

2022

2021

% Change

2023 to

2024

% Change

2022 to

2024

% Change

2021 to

2024

WA

SBM

272,494

230,371

239,566

222,731

18%

14%

22%

WI

HC.gov

266,327

221,128

212,209

191,702

20%

26%

39%

WV

HC.gov

51,046

28,325

23,037

19,381

80%

122%

163%

WY

HC.gov

42,293

38,565

34,762

26,728

10%

22%

58%

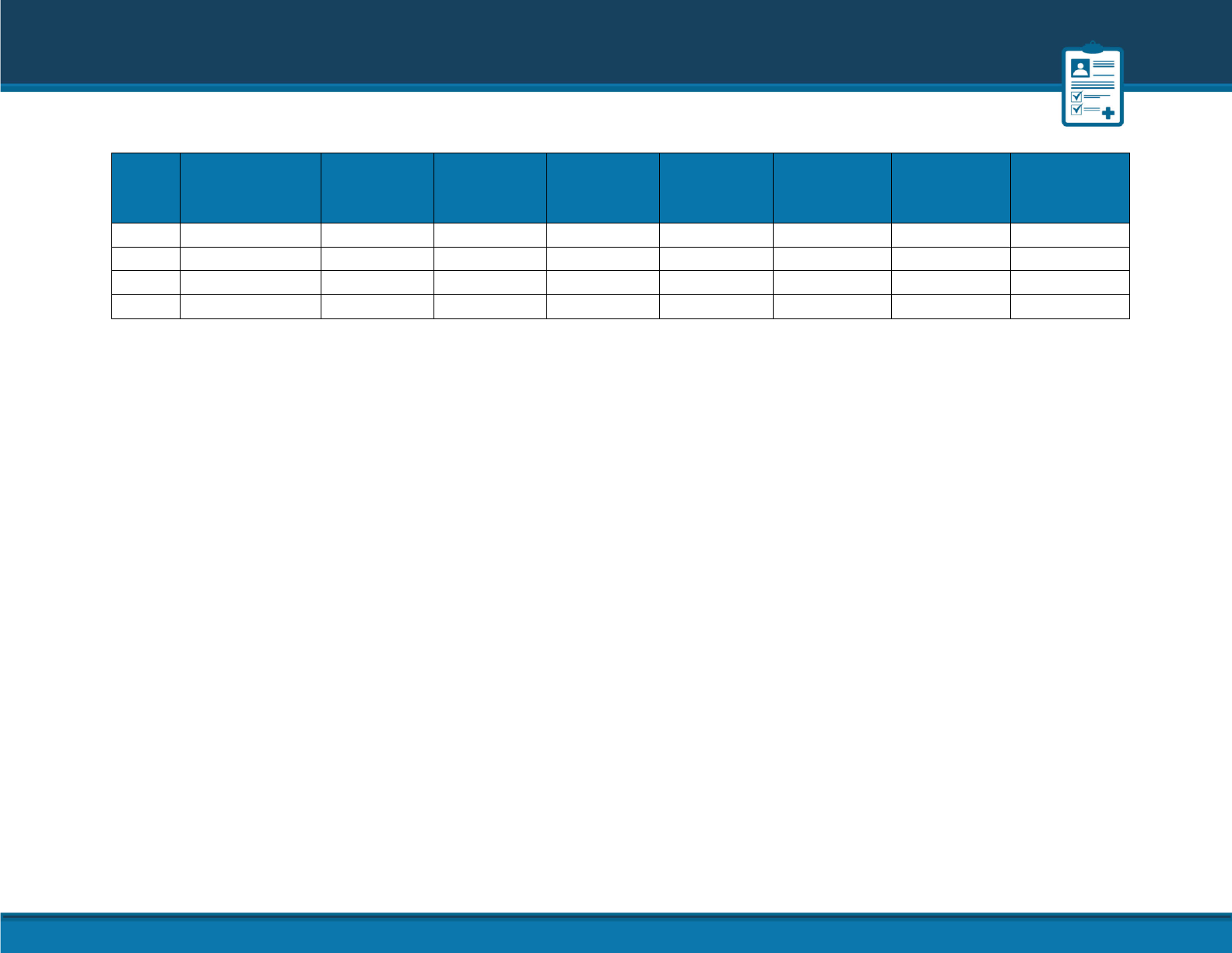

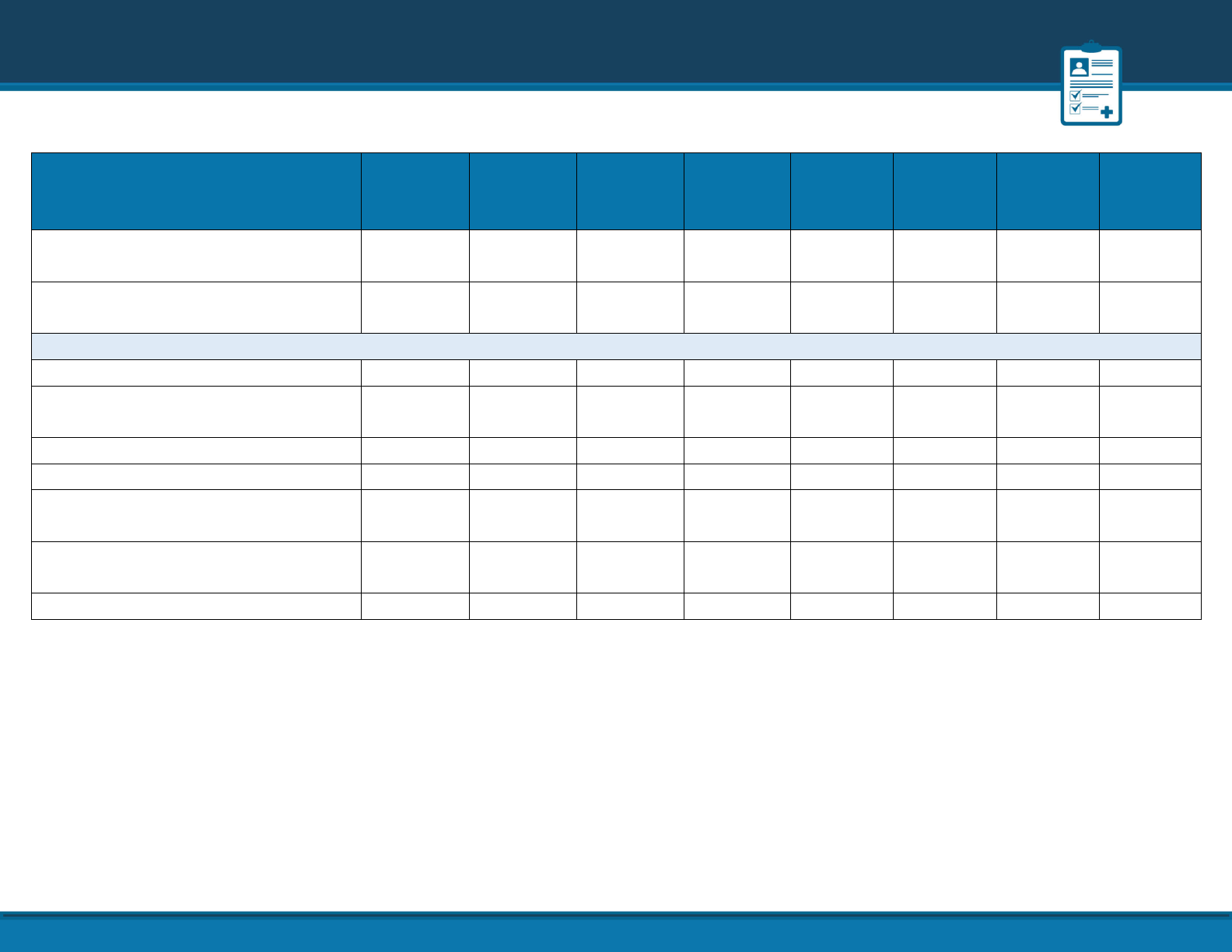

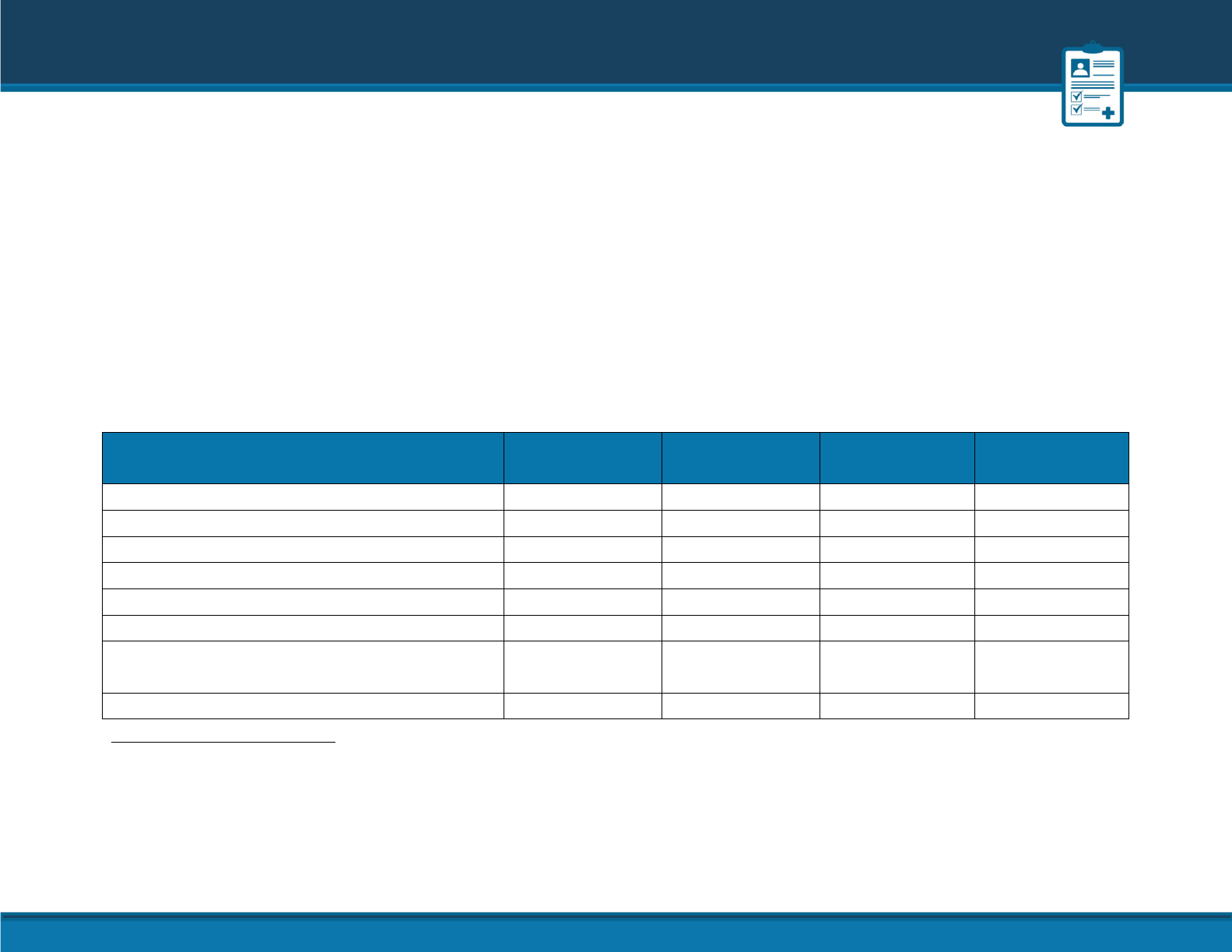

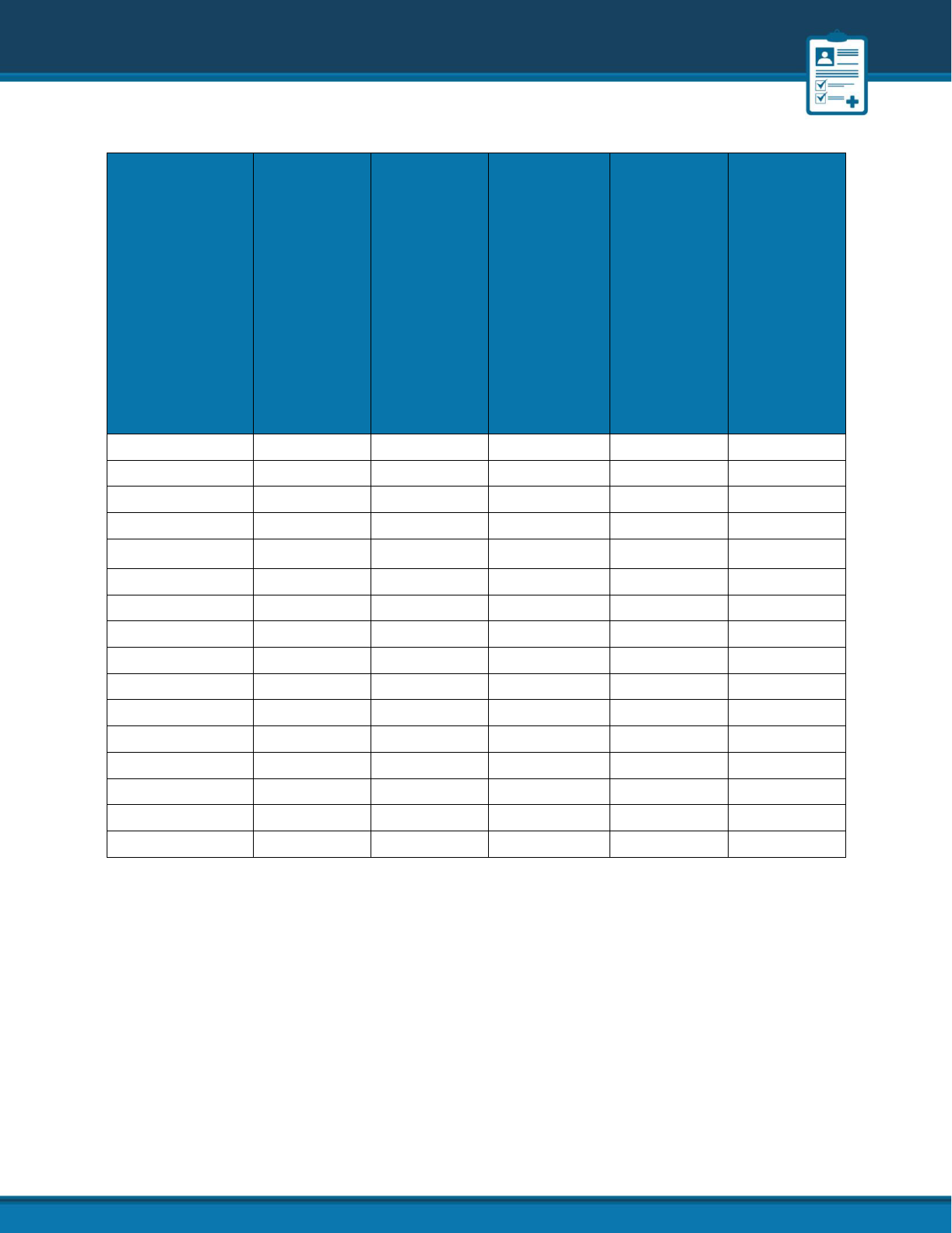

Table 2 shows Basic Health Program (BHP) enrollment for states that have implemented a BHP.

5

In Minnesota and

New York, consumers who apply for coverage with household incomes between 133% and 200% of the FPL and are

not eligible for minimum essential coverage, including Medicaid or the Children’s Health Insurance Program (CHIP),

are enrolled in the applicable state BHP instead of a Qualified Health Plan (QHP).

6

Total BHP enrollment increased

33% from approximately 975,000 enrollees in the 2021 OEP to 1.3 million enrollees during the 2024 OEP. Minnesota’s

BHP enrollment increased 9% and New York’s increased by 7% from 2023 to 2024.

Table 2: Basic Health Program Enrollment

7

State

2024

2023

2022

2021

% Change

2023 to

2024

% Change

2022 to

2024

% Change

2021 to

2024

Total

1,302,034

1,217,921

1,054,603

975,337

7%

23%

33%

Minnesota

103,638

94,811

98,581

91,886

9%

5%

13%

New York

1,198,396

1,123,110

956,022

883,451

7%

25%

36%

5

BHP enrollment is not limited to an OEP; the data reflects BHP enrollments as of the end date of the New York’s and Minnesota’s OEPs. For the 2024 OEP

New York’s data is as of 2/3/2024 and Minnesota’s data is as of 1/15/2024.

6

The BHP also provides coverage to lawfully present noncitizens with household income below 200% FPL who are ineligible for Medicaid or CHIP due to

immigration status.

7

New York's BHP is known as the Essential Plan and Minnesota's BHP is known as MinnesotaCare.

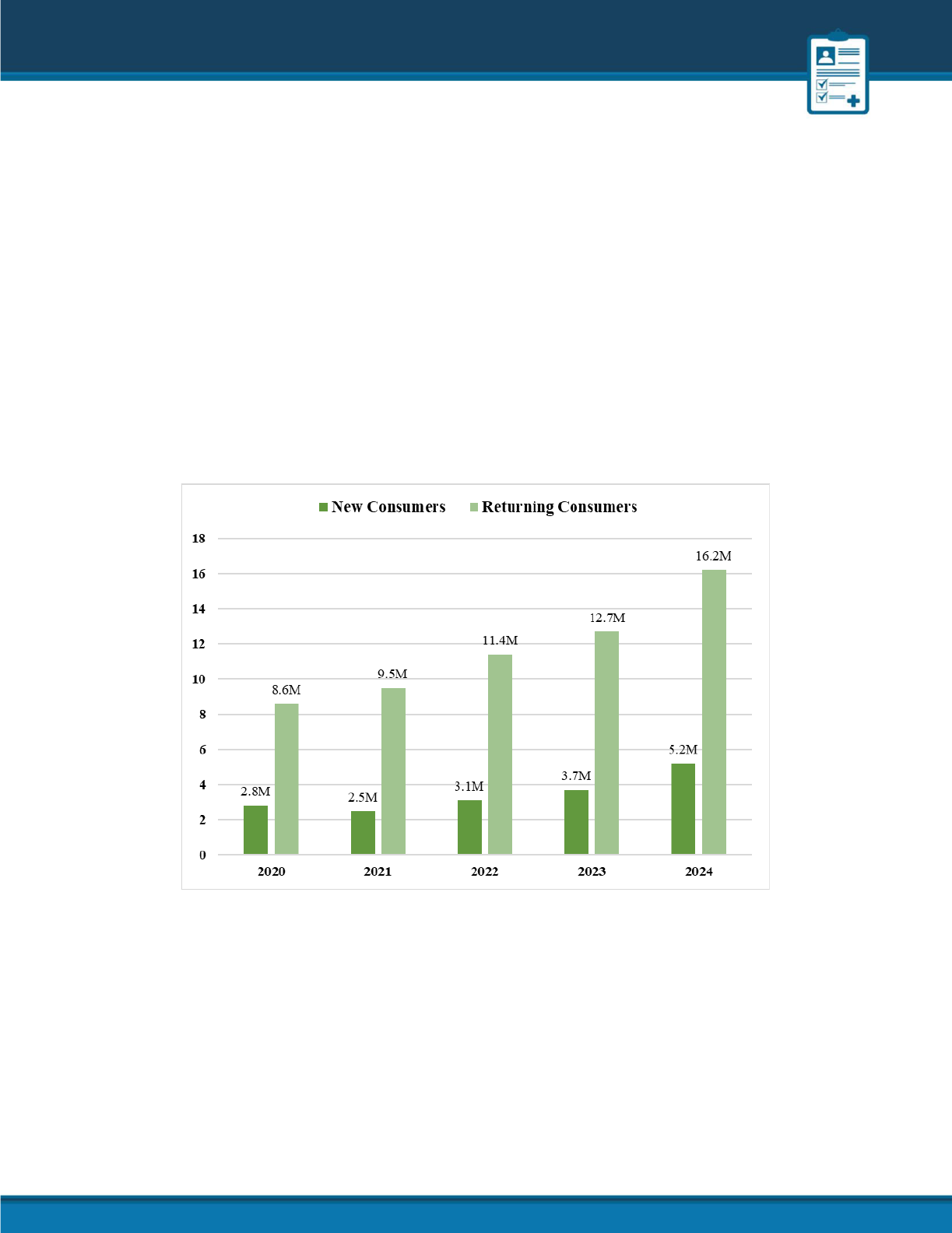

Figure 2 illustrates the comparison of new and returning consumer plan selections

nationwide during OEPs from 2020 to 2024. In the 2024 OEP, new consumer plan

selections across all Marketplaces exceeded 5.2 million, approximately 2.4 million

more than the 2020 OEP. In comparison to the 2023 OEP, new consumer enrollment

increased by 41%. As demonstrated below, 16.2 million enrollees returned to the

Marketplaces actively or through auto re-enrollment, representing a 28% increase

from 12.7 million in 2023.

Figure 2: New and Returning Consumer Plan Selections during 2020 to 2024

Open Enrollment Periods

Table 3 summarizes consumers who selected Marketplace plans during the 2021 to 2024 OEPs by enrollment type.

Nationally, new consumer plan selections, as a percentage of total plan selections, increased from 21% in the 2021

and 2022 OEPs to 24% in the 2024 OEP. Actively returning consumer plan selections decreased from 47% to 45% from

2023 to 2024. In 2024, 52% of HealthCare.gov enrollees represented actively returning consumers, while 26% were

consumers new to the HealthCare.gov platform. For SBMs, 19% of plan selections were new consumers and 23% were

actively returning in 2024. Additional plan selection and demographic data for Marketplaces in all 50 states plus DC

are provided in the accompanying public use files (PUFs).

Table 3: Summary of OEP Plan Selections by Enrollment Type

Count

2024

Count

2023

Count

2022

Count

2021

% of

Total

2024

% of

Total

2023

% of

Total

2022

% of

Total

2021

New Consumers: All Marketplaces

5,215,764

3,699,749

3,066,360

2,545,559

24

23

21

21

Returning Consumers Re-enrolling

in Coverage: All Marketplaces

16,230,386

12,657,281 11,444,717

9,458,806

76

77

79

79

Active Re-enrollees: All

Marketplaces

9,659,365

7,629,744

6,742,948

5,513,796

45

47

46

46

Automatic Re-enrollees: All

Marketplaces

6,571,021

5,027,537

4,701,769

3,945,010

31

31

32

33

HealthCare.gov Marketplaces

New Consumers: HC.gov

Marketplaces

4,226,461

3,000,155

2,380,835

1,884,174

26

25

23

23

Returning Consumers Re-enrolling

in Coverage: HC.gov Marketplaces

12,136,672

9,203,467

7,874,801

6,367,529

74

75

77

77

Count

2024

Count

2023

Count

2022

Count

2021

% of

Total

2024

% of

Total

2023

% of

Total

2022

% of

Total

2021

Active Re-enrollees: HC.gov

Marketplaces

8,511,722

6,654,213

5,680,878

4,648,617

52

55

55

56

Automatic Re-enrollees: HC.gov

Marketplaces

3,624,950

2,549,254

2,193,923

1,718,912

22

21

21

21

State-based Marketplaces

New Consumers: SBMs

989,303

699,594

685,525

661,385

19

17

16

18

Returning Consumers Re-enrolling

in Coverage: SBMs

4,093,714

3,453,814

3,569,916

3,091,277

81

83

84

82

Active Re-enrollees: SBMs

1,147,643

975,531

1,062,070

865,179

23

23

25

23

Automatic Re-enrollees: SBMs

2,946,071

2,478,283

2,507,846

2,226,098

58

60

59

59

Total Plan Selections: All

Marketplaces

21,446,150

16,357,030

14,511,077

12,004,365

100

100

100

100

Total Plan Selections: HC.gov

Marketplaces

16,363,133

12,203,622

10,255,636

8,251,703

100

100

100

100

Total Plan Selections: SBMs

5,083,017

4,153,408

4,255,441

3,752,662

100

100

100

100

CONSUMERS APPLYING FOR AND SELECTING PLANS: DETAILS

Table 4 shows metrics at the individual level for those who requested coverage on submitted Marketplace

applications for the 2021 to 2024 OEPs. During the 2024 OEP, 68% of applicants requesting coverage through the

Marketplaces were determined eligible to make a Marketplace plan selection, compared to 69% during the 2023 OEP.

On the HealthCare.gov platform, 96% of applicants were determined eligible to make a Marketplace plan selection,

and 41% of applicants using the SBMs were determined eligible to make a Marketplace plan selection. The percentage

of consumers who requested coverage through HealthCare.gov and were preliminarily determined eligible for their

state’s Medicaid or CHIP fell by 1 percentage point from 5% in the 2023 OEP to 4% in the 2024 OEP.

Table 4: Marketplace Application Activity and Eligibility for 2021 to 2024

Count

2024

Count

2023

Count

2022

Count

2021

% of

Total

2024

% of

Total

2023

% of

Total

2022

% of

Total

2021

Consumers Requesting Coverage on

Applications Submitted: All Marketplaces

38,036,483 27,653,188 25,830,064 22,415,477

100

100

100

100

Marketplace Eligible: All Marketplaces

25,854,241

19,191,464 17,485,459 14,925,762

68

69

68

67

HealthCare.gov Marketplaces

Consumers Requesting Coverage on

Applications Submitted: HC.gov

Marketplaces

18,568,083 14,036,572 12,194,577

10,161,816

100

100

100

100

Marketplace Eligible: HC.gov Marketplaces

17,795,305 13,324,638

11,486,135

9,479,261

96

95

94

93

Medicaid/CHIP Eligible: HC.gov

Marketplaces

831,411

746,999

743,544

762,533

4

5

6

8

State-based Marketplaces

8

Consumers Requesting Coverage on

Applications Submitted: SBMs

19,468,400

13,616,616

13,635,487

12,253,661

100

100

100

100

Marketplace Eligible: SBMs

8,058,936

5,866,826

5,999,324

5,446,501

41

43

44

44

8

Most State-based Marketplaces have integrated eligibility systems with their state Medicaid. In those states, consumers requesting coverage on applications

submitted includes applications received for modified adjusted gross income (MAGI) Medicaid renewals, in addition to QHP renewal applications and new

applications. Some SBMs do not report on consumers determined eligible for Medicaid/CHIP and, thus, a total number is not provided here. See PUF definitions

for more information.

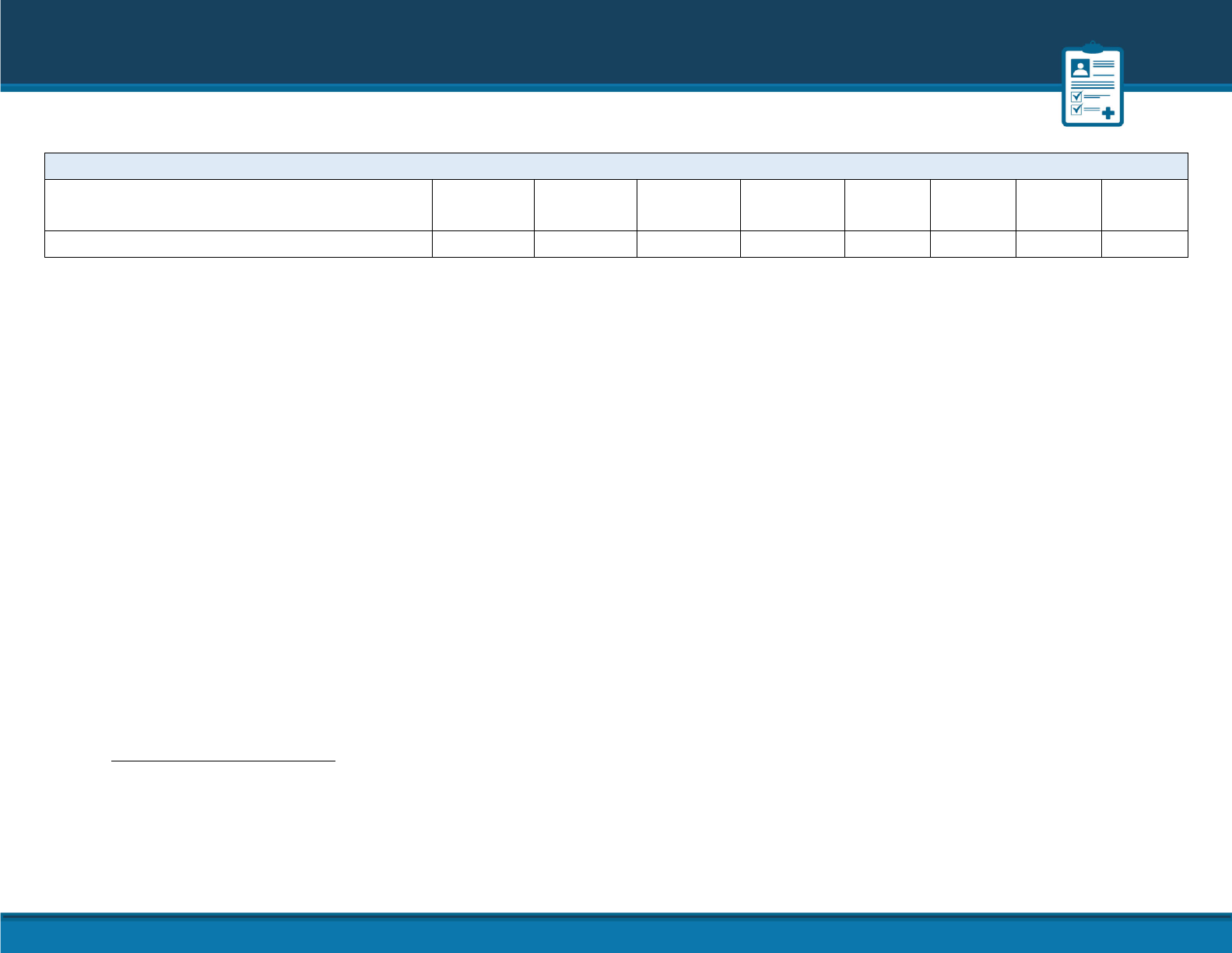

Table 5 shows demographic and plan characteristics among consumers who

selected or were automatically re-enrolled in a Marketplace plan during the 2024,

2023, 2022, and 2021 OEPs. The percentage of consumers with a household income

between 100% and 150% FPL in 2024 increased by 7 percentage points from 37% in

2023. Moreover, it grew by 12 percentage points from 32% in 2021 to 44% in 2024.

7% (1.5 million) of plan selections for the 2024 OEP included consumers with a

household income over 400% FPL.

Some of the continued increase in the percentage of consumers receiving financial

assistance in 2024 can be attributed to impacts of the IRA. Nationally, during the

2024 OEP, 92% of consumers had their premiums reduced by APTC compared to

90% in the 2023 OEP and 85% in the 2021 OEP. Split by Marketplace type, 95% of

HealthCare.gov consumers and 83% of SBM consumers selected plans with APTC,

compared to 88% and 78%, respectively, in 2021. During the 2024 OEP, 50% of all

Marketplace consumers selected plans with CSRs in comparison to 48% in 2023.

41% of 2024 OEP HealthCare.gov enrollees selected plans that cover 94% of their

expected health care costs - 94% actuarial value (AV) - an increase of 4 percentage

points from 2023.

Table 5: Demographic and Plan Characteristics of Consumers with OEP Plan

Selections (HealthCare.gov Marketplaces and SBMs, Unless Otherwise Noted)

% of Total

2024

9

% of Total

2023

9

% of Total

2022

9

% of Total

2021

9

Age

< 18

10

9

9

9

18 - 34

27

25

25

25

35 - 54

38

37

36

36

55+

26

29

29

30

Gender

Female

52

53

54

54

Male

48

47

46

46

Location: HealthCare.gov States

Rural

18

18

18

18

Non-rural

82

82

82

82

9

Totals may not sum to 100% due to rounding.

% of Total

2024

9

% of Total

2023

9

% of Total

2022

9

% of Total

2021

9

Household Income

10

< 100%

2

1

2

2

≥ 100% and ≤ 150%

44

37

32

32

≥ 100% and ≤ 138%

32

26

23

NA

> 150% and ≤ 250%

29

29

32

34

> 250% and ≤ 400%

15

19

20

20

> 400% FPL

7

8

8

3

Other Household Income

11

4

5

6

9

Financial Assistance

With APTC: All Marketplaces

92

90

89

85

HealthCare.gov Marketplaces

95

93

92

88

SBMs

83

82

83

78

With CSR: All Marketplaces

10

50

48

49

47

HealthCare.gov Marketplace

53

52

53

51

73% AV

2

3

5

4

87% AV

9

11

13

12

94% AV

41

37

35

34

American Indian/Alaskan

Native

<1

<1

1

1

SBMs

10

39

35

37

39

Metal Level

Catastrophic

<1

<1

1

1

Bronze

31

32

32

35

Silver

54

54

56

55

Gold

13

12

10

8

Platinum

1

1

1

1

10

Idaho has been excluded from 2021 household income metrics as Idaho’s household income data for 2021 was not

available at the time of this report. Nevada has been excluded from 2022 CSR metrics as Nevada’s CSR data for

2022 was not available at the time of this report.

11

Other household income includes plan selections for which consumers were not requesting financial assistance

and unknown household income.

Table 6 provides race and ethnicity demographics for all consumers who enrolled in Marketplace plans during OEPs

2021 to 2024. Aligned with the overall increase in total plan selections, there was a corresponding rise in the number

of individuals identifying as Hispanic/Latino or Black. Based on primary data available in the accompanying PUFs,

among consumers who reported their ethnicity or race (constituting 50% of total plan selections) during the 2024

OEP, enrollees identifying as Hispanic/Latino increased by 17%, and those identifying as Black increased by 16% from

2023 to 2024. As a percentage of total plan selections, among consumers who reported a race or ethnicity, 22%

identified as Hispanic/Latino in the 2024 OEP, compared to 21% in the 2023 OEP. The proportion of consumers who

self-reported as Black, Non-Hispanic remained constant at 9% for 2024, 2023, and 2022.

Table 6: Race and Ethnicity Demographics of Consumers with OEP Plan Selections

% of Total

2024

12

% of Total

2023

12

% of Total

2022

12

% of Total

2021

12

Race/Ethnicity: All Marketplaces

13

Race/Ethnicity Known

50

59

66

69

Hispanic/Latino

22

21

19

18

White, Non-Hispanic

53

54

55

57

Black, Non-Hispanic

9

9

9

8

Asian, Non-Hispanic

11

11

12

13

Native Hawaiian/Pacific Islander, Non-

Hispanic

<1

<1

<1

<1

American Indian/Alaska Native, Non-

1

1

1

1

12

Totals may not sum to 100% due to rounding. Race and Ethnicity data for 2022 was revised to include all states with available data for the 2022 OEP;

therefore, these numbers may not match what was previously published. The 2022 OEP report excluded Colorado.

13

Some SBM applications do not include Other or Multi-Racial as an option. SBM Race and Ethnicity breakouts for the 2022 OEP do not add up to total plan

selections because WA reports consumers choosing more than one race in multiple categories. SBM Race and Ethnicity breakouts for the 2021 OEP do not add

up to total plan selections as NY, VT, and WA reported consumers choosing more than one race in multiple categories.

CONSUMER PREMIUMS AND FINANCIAL ASSISTANCE

Table 7 shows the average premiums for consumers who made Marketplace plan

selections during the 2021 to 2024 OEPs. Nationally, the average monthly premium

after APTC decreased by 14% from $129 in 2023 and by 32% from $164 in 2021 to

$111 in 2024. 44% of consumers selected a plan for $10 or less per month after APTC

in 2024. The average monthly APTC for all consumers increased to $536 in 2024,

representing a 2% increase from $526 in 2023 and an 11% increase from $485 in

2021.

The average monthly premium after APTC for HealthCare.gov consumers fell 43%,

from $143 in 2021 to $81 in 2024. The continued expansion of financial assistance

for consumers resulted in an 8% increase of the average monthly APTC amount for

HealthCare.gov enrollees who selected plans with APTC, from $509 in 2021 to $548

in 2024. As a result, in the 2024 OEP, 51% of all HealthCare.gov consumers had a plan

selection with a premium of $10 or less per month after APTC, compared to 40% in

2023.

In the SBMs, the average monthly premium after APTC was $207 in 2024, and 20% of

consumers selected plans that were $10 or less per month after APTC. Some SBMs,

including those in California, Colorado, Connecticut, Maryland, Massachusetts, New

Jersey, New Mexico, Vermont, and Washington, apply state subsidies in addition to

APTC and/or CSRs to further reduce the cost sharing that consumers pay. These cost

reductions are not reflected in this data.

Table 7: Average Monthly Premium before and after APTC

% of Plan

Selections

with ≤$10

Monthly

Premium

after APTC

% of

Consumers

with APTC

Average

Monthly

Premium

after APTC

Average

Monthly

Premium

before

APTC

Average

Monthly

APTC

Amount

for

Consumers

Receiving

APTC

All Marketplaces

2024

44%

92%

$111

$605

$536

2023

35%

90%

$129

$605

$526

2022

14

28%

89%

$133

$585

$505

2021

14

NA

85%

$164

$579

$485

HealthCare.gov Marketplaces

2024

51%

95%

$81

$602

$548

2023

40%

93%

$102

$607

$542

2022

32%

92%

$111

$594

$524

2021

18%

88%

$143

$590

$509

State-based Marketplaces

15

2024

20%

83%

$207

$615

$492

2023

18%

82%

$209

$598

$473

2022

14

19%

83%

$188

$563

$452

2021

14

NA

78%

$210

$553

$426

14

Nevada has been excluded from average APTC and average premium metrics for 2021 and 2022 as this data was

not available at the time of this report.

15

Premiums in SBMs do not reflect state subsidies available in some SBMs, which are applied in addition to APTC

to further lower premiums for consumers.

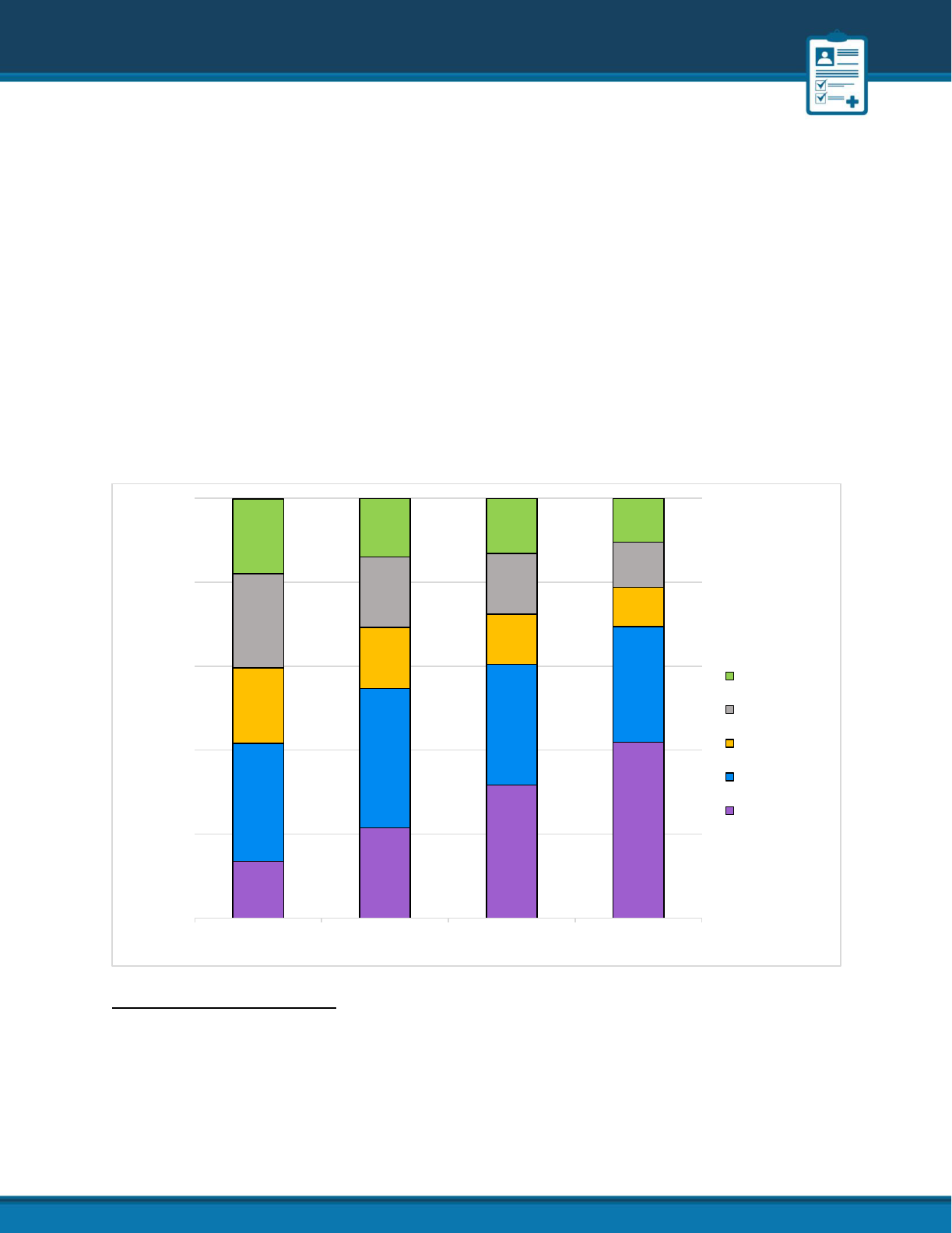

Figure 3 illustrates the distributions of monthly premiums after APTC for

HealthCare.gov consumers during the 2021-2024 OEPs. In 2024, coverage became

more affordable for consumers compared to the preceding three OEPs. During the

2024 OEP, 42% (6.8 million) of consumers selected plans with a $0 monthly premium

after APTC. This percentage represents an increase from 32% (3.8 million), 22% (2.1

million), and 14% (1.1 million) in the 2023, 2022, and 2021 OEPs, respectively.

Additionally, 69% of 2024 OEP consumers had premiums of $50 or less after APTC,

representing an increase of over 8.0 million consumers compared to 2021.

Figure 3: 2021, 2022, 2023, and 2024 OEP Premium Distribution in

HealthCare.gov Marketplaces

16

16

The distribution of monthly premiums after APTC for the 2021 OEP excludes Kentucky, Maine, and New

Mexico, reflecting each state's transition to a SBM for the 2022 coverage year. Similarly, the distribution of monthly

premiums after APTC for the 2021 OEP has been adjusted to exclude Virginia, reflecting the state's transition to a

SBM for the 2024 coverage year. Furthermore, the distribution of monthly premiums after APTC for the 2022 and

2023 OEPs has been adjusted to exclude Virginia, aligning with the state's transition to a SBM for the 2024

coverage year. These adjustments may result in differences from previously published data.

14%

22%

32%

42%

28%

33%

29%

28%

18%

15%

12%

9%

22%

17%

14%

11%

18%

14%

13%

10%

0%

20%

40%

60%

80%

100%

2021 OEP 2022 OEP 2023 OEP 2024 OEP

Distribution of Plan Selections

>$250

>$100 - ≤$250

>$50 - ≤$100

>$0 - ≤$50

$0

Net

Premium

Ranges

Table 8 shows that, on average, consumers receiving APTC in 2024 are seeing more

than $700 per year in premium savings due to the IRA’s continuation of the ARP’s

APTC expansion. The estimate assumes that the same demographic composition of

enrollment and plan choices would exist without the IRA. Using the savings amounts

for 2024 OEP HealthCare.gov consumers receiving APTC and applying the estimated

national income distribution for consumers receiving APTC, the average monthly

savings for 2024 is approximately $59, which equates to an annual total of $705. As

a result of the ARP/IRA subsidy enhancements, consumers below 150% FPL generally

have access to a $0 or near-$0 2024 plan option.

Table 8: Estimated Consumer APTC Savings due to the ARP and IRA by Income

Category

Income

Category

(% of FPL)

Estimated Average

Monthly Premium

Savings from

ARP/IRA APTC

Expansion

17

Estimated Average

Yearly Premium

Savings from

ARP/IRA APTC

Expansion

Estimated Percent of

OEP Plan Selections

with APTC

18

Total

$59

$705

100%

<100%

$9

$113

1%

100-138%

$19

$232

34%

>138-150%

$44

$531

13%

>150-200%

$57

$679

18%

17

The Average Monthly 2024 Premium without ARP/IRA Expansion metric calculates APTC assuming a

consumers’ income, family composition, and OE 2024 plan selection remain the same. However, in the absence of

the expanded APTC available from the ARP/IRA, some consumers would choose not to enroll at all and others

would select less generous plans with lower premiums. APTC is calculated with the applicable percentages that

would be in effect without the ARP/IRA. For coverage year 2024, the applicable percentages at 26 CFR 1.36B-

3(g)(2) would be multiplied by 0.8827984162, the rate of premium growth relative to the rate of income growth for

2013 to 2023 (calculated using the NHEA Projections, 2021-2030, available at: https://www.cms.gov/data-

research/statistics-trends-and-reports/national-health-expenditure-data/projected) as of June 2023, and the

methodology used to calculate the same rates of growth in the Premium Adjustment Percentage guidance for the

2024 benefit year published by the Center for Medicare and Medicaid Services on December 12, 2022, available at:

https://www.cms.gov/files/document/2024-papi-parameters-guidance-2022-12-12.pdf). Estimates are based on

HealthCare.gov state data only.

18

The Estimated Percent of 2024 OEP Plan Selections with APTC is equal to the product of the total plan selections

in each income category (for all states) and the percent of plan selections with APTC in the given income category,

using HealthCare.gov data for the latter percents.

Income

Category

(% of FPL)

Estimated Average

Monthly Premium

Savings from

ARP/IRA APTC

Expansion

17

Estimated Average

Yearly Premium

Savings from

ARP/IRA APTC

Expansion

Estimated Percent of

OEP Plan Selections

with APTC

18

>200-250%

$70

$837

12%

>250-300%

$72

$866

8%

>300-400%

$40

$479

8%

>400%

$354

$4,248

5%

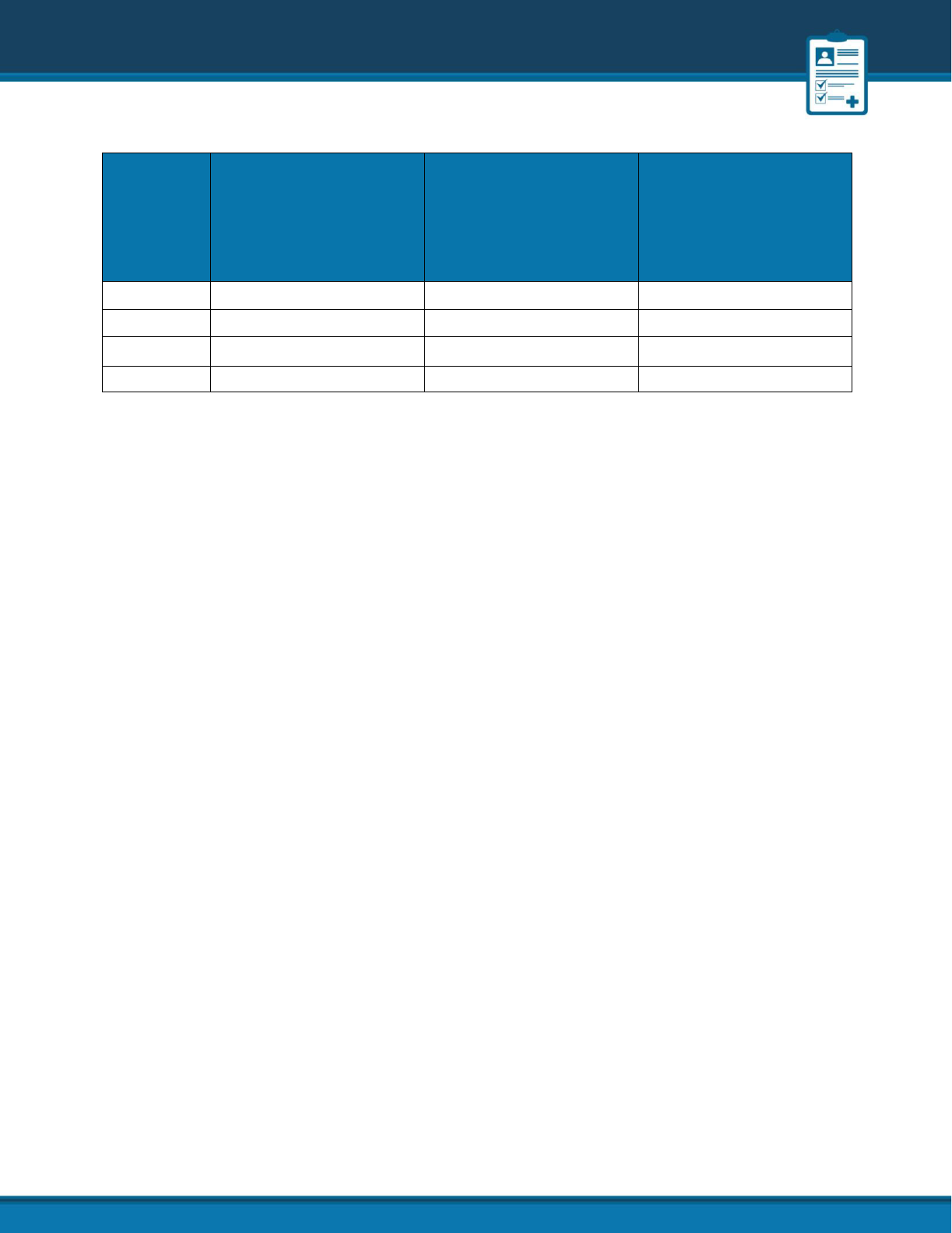

Table 9 details average 2024 monthly premiums for consumers with APTC in

HealthCare.gov Marketplaces due to the IRA’s continuation of the ARP’s APTC

expansion. The table also simulates what the average monthly premium would be

for each HealthCare.gov Marketplace without the ARP/IRA APTC expansion,

assuming the same level and demographic composition of enrollment and plan

choices. The IRA’s continued APTC expansion reduces the average monthly premium

for consumers receiving APTC in 2024 by 48%, or $52 per month. In 29 of the 32

HealthCare.gov Marketplaces, APTC consumers are saving at least 40% on monthly

premiums, on average, due to the IRA APTC expansion. In 26 HealthCare.gov

Marketplaces, the difference in the actual average monthly 2024 premium with APTC

under current law and the average monthly 2024 premium without the IRA’s APTC

expansion is at least $50.

Table 9: Estimated HealthCare.gov Consumer APTC Savings due to ARP and

IRA by State

19,20

State

Actual

Average

Monthly

2024

Premium

with

ARP/IRA

APTC

Expansion

Average

Monthly

2024

Premium

without

ARP/IRA

APTC

Expansion

Average

Monthly

2024

APTC

Amount

for

Consumers

Receiving

APTC

$

Premium

Savings

from

ARP/IRA

APTC

Expansion

%

Premium

Savings

from

ARP/IRA

APTC

Expansion

Total

$56

$108

$548

$52

48%

Alaska

$122

$275

$865

$153

56%

Alabama

$55

$106

$656

$51

48%

Arkansas

$82

$151

$476

$69

46%

Arizona

$75

$140

$452

$64

46%

Delaware

$147

$247

$585

$100

41%

Florida

$49

$93

$568

$44

47%

Georgia

$52

$96

$531

$44

46%

Hawaii

$183

$273

$544

$90

33%

Iowa

$93

$183

$507

$90

49%

Illinois

$141

$227

$545

$86

38%

Indiana

$82

$149

$452

$67

45%

Kansas

$77

$136

$561

$59

44%

Louisiana

$65

$130

$647

$64

50%

Michigan

$98

$167

$426

$69

41%

Missouri

$61

$127

$594

$66

52%

Mississippi

$25

$65

$592

$41

62%

19

The Average Monthly 2024 Premium without the ARP/IRA Expansion metric calculates APTC assuming a

consumers’ income, family composition, and OE 2024 plan selection remaining the same. However, in the absence

of the expanded APTC available from the ARP/IRA, some consumers would choose not to enroll at all and others

would select less generous plans with lower premiums. APTC is calculated with the applicable percentages that

would be in effect without the ARP/IRA. For coverage year 2024, the IRS published these applicable percentages in

Revenue Procedure 23-29 (https://www.irs.gov/pub/irs-drop/rp-23-29.pdf).

20

Table 9 only includes data for HealthCare.gov consumers receiving APTC in 2024.

State

Actual

Average

Monthly

2024

Premium

with

ARP/IRA

APTC

Expansion

Average

Monthly

2024

Premium

without

ARP/IRA

APTC

Expansion

Average

Monthly

2024

APTC

Amount

for

Consumers

Receiving

APTC

$

Premium

Savings

from

ARP/IRA

APTC

Expansion

%

Premium

Savings

from

ARP/IRA

APTC

Expansion

Montana

$112

$203

$504

$91

45%

North Carolina

$55

$111

$558

$56

51%

North Dakota

$99

$189

$433

$90

48%

Nebraska

$93

$184

$580

$92

50%

New Hampshire

$124

$197

$350

$74

37%

Ohio

$81

$148

$498

$67

45%

Oklahoma

$57

$115

$575

$57

50%

Oregon

$164

$275

$524

$112

41%

South Carolina

$50

$99

$553

$49

50%

South Dakota

$92

$199

$611

$108

54%

Tennessee

$45

$90

$580

$45

50%

Texas

$33

$71

$536

$38

54%

Utah

$48

$104

$421

$55

54%

Wisconsin

$117

$217

$572

$100

46%

West Virginia

$88

$205

$1,035

$117

57%

Wyoming

$80

$236

$863

$156

66%

Appendix

Public Use Files

Public Use Files Contents: More information on applications and plan selections is

available in a suite of accompanying public use files (PUFs). The PUFs contain

information on applications submitted and the number of medical and stand-alone

dental plan selections by state, county, and ZIP code. The 2024 OEP state-level PUF

includes other plan and demographic information, including the metal level of

selected plans, premium and financial assistance information, age, gender, rural

location, self-reported race and ethnicity, and household income as a percentage of

the FPL. Within the 2024 OEP state, metal level, and enrollment status PUF, data are

stratified by new, returning, and automatically re-enrolled consumers and by plan

metal level. The methodology for this report and detailed metric definitions are

included in the materials for the PUFs.

An additional PUF is available for HealthCare.gov plan selections, including

deductibles, HSA eligibility, and standardized plan option selection rates.

The PUFs can be found at: https://www.cms.gov/data-research/statistics-trends-

and-reports/marketplace-products/2024-marketplace-open-enrollment-period-

public-use-files