WP/15/200

IMF Working Papers describe research in progress by the author(s) and are published to elicit comments

and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and

do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

“But we are different!”:

12 Common Weaknesses in Banking Laws, and What to

Do about Them

By Wouter Bossu and Dawn Chew

© 2015 International Monetary Fund WP/15/200

IMF Working Paper

Legal Department

“But we are different!” 12 Common Weaknesses in Banking Laws, and What to Do

about Them

Prepared by Wouter Bossu and Dawn Chew

Authorized for distribution by Sean Hagan

September 2015

Abstract

Well-designed banking laws are critical for regulating the market access and operations of

banks, as well as their removal from the market in case of failure. While at a financial policy

level there is a broad consensus as to the content of banking laws, from a legal perspective

their drafting often leaves something to be desired. In spite of what is often argued, the types

of weaknesses of banking laws are hardly country-specific; many weaknesses are shared by

many banking laws. This working paper discusses those weaknesses and ways to remedy

them, by focusing on a selected set of legal policy principles.

JEL Classification Numbers:

G21, G28, K22, K23

Keywords: Banking Regulation, Policy Analysis

Author’s E

This Working Paper should not be reported as representing the views of the IMF.

The views expressed in this Working Paper are those of the author(s) and do not necessarily

represent those of the IMF or IMF policy. Working Papers describe research in progress by the

author(s) and are published to elicit comments and to further debate.

3

Contents

Abstract ..................................................................................................................................... 2

I. Introduction ........................................................................................................................... 4

II. Scope and Definitions .......................................................................................................... 6

III. Objectives, Functions and Legal Powers of Supervisor ................................................... 10

IV. Legal Nature and Hierarchy of Secondary Regulatory Instruments ................................. 13

A. Legal Nature ................................................................................................................... 14

Binding Secondary Instruments ...................................................................................... 14

Non-Binding Secondary Instruments .............................................................................. 15

B. Hierarchy of Norms ........................................................................................................ 16

Classification of Instruments Issued by Monetary Authority of Singapore (MAS) ... 17

V. Licensing Requirements ..................................................................................................... 18

A. Licensing Criteria ........................................................................................................... 18

B. Licensing Procedure ....................................................................................................... 20

VI. Ongoing Requirements versus Licensing Criteria ............................................................ 22

VII. Corporate Governance ..................................................................................................... 23

VIII. Power to Control Ownership Changes ........................................................................... 25

IX. Market Access by Foreign Banks: Branches vs. Subsidiaries vs. Representative Offices 28

X. Consolidated Supervision .................................................................................................. 31

XI. Sharing of Information and Inter-agency Cooperation ..................................................... 34

XII. Bank-Related Party and Large Exposure Limits ............................................................. 38

XIII. Supervisory Enforcement, Early Intervention and Resolution ...................................... 39

A. Types of Enforcement Measures .................................................................................... 39

B. Link with License Revocation ........................................................................................ 41

C. Role of Sanctions ........................................................................................................... 43

XIV. Conclusion ..................................................................................................................... 44

4

I. INTRODUCTION

1. Over the last 20 years, the IMF’s Legal Department has made a significant

contribution to the development of banking laws in the Fund’s membership. A “back of

the envelope” exercise suggests that lawyers of the Fund have been involved in the banking

laws of approximately 50 countries. This involvement ranges from comments on surgical

amendments to assistance in redrafting entirely new banking laws. (In some countries, the

banking law is a stand-alone type of legislation whereas in others, it is part of the central

bank law, which is often also enhanced with support of Fund staff.) This law reform support

takes place within the context of financial sector surveillance (including through the

Financial Sector Assessment Program or FSAP), the implementation of financial sector-

related conditionality as part of Fund-supported programs, or voluntary technical assistance

outside such programs. Surveillance, financial support to address balance of payments

problems and technical assistance are the three core functions of the IMF.

2. Summarizing the authors' experience in this field, this paper highlights common

weaknesses in banking legislation and suggests solutions.

1

In discussions with country

officials in the context of law reform, the argument is often made that one or more specific

problems with the local banking law are due to the local circumstances of that jurisdiction.

However, our experience has shown that most weaknesses to banking laws are hardly

idiosyncratic to individual countries. On the contrary, many countries share similar problems,

and these are thus really part of a more global pattern. In fact, the shared problems are caused

more by inherent challenges in designing and drafting banking laws than by local

circumstances. This paper will seek to illustrate those common issues, and why the “but we

are different” argument does not always carry weight. Hence the title. To facilitate the

reader’s access to practical examples of the general points made below, the paper will make

manifold references to current banking laws of countries.

2

3. This paper aims at complementing the existing financial policy standards with

specific legal recommendations for drafters of banking laws. Banking regulation is one

field of economic policy-making with a firm international standard: the Basel Committee on

Banking Supervision’s Core Principles for Effective Banking Supervision (September 2012)

(“BCP”) have evolved into the de facto global minimum standard for sound prudential

1

This paper was written while Dawn Chew was on secondment with the IMF. It has benefitted from the

comments of Nikita Aggarwal, Jean Pierre Deguee, Barend Jansen, Ross Leckow, Nicolas Staner, and Virginia

Rutledge. Colleagues from the IMF’s Monetary and Capital Markets Department have also provided invaluable

comments. While the views expressed in this paper are to some extent based upon the authors’ experience as

Fund counsels, the views expressed herein are their own and should not necessarily be attributed to the Fund.

2

These country examples are chosen for illustrative reasons only; the references do not imply that those

countries have received technical assistance of the Fund with respect to their banking law.

5

regulation and supervision of banks and banking systems.

3

As the legal framework is an

important instrument for implementing banking regulatory policy—the policy preferences

established by the international soft law of the BCP must often be implemented through

national legislation—the BCP include many references to banking laws and regulations. The

problem is that the BCP do not always offer sufficiently granular guidance to drafters of such

laws. This is not a criticism, for it is explained by the very nature of the standard, which is

focused on supervisory policy and practice, and not on the law per se. It is also explained by

the fact that the BCP are the result of decision-making in an intergovernmental committee

structure, which entails decision making by consensus, and at times sacrifices clarity for

compromise. Hence there is a need for more specific legal guidance as to what constitutes

good legal practice in drafting banking laws. This paper intends to make a meaningful

contribution to this. This being said, at times the paper will also make suggestions (in

footnotes) as to how the pronouncements of the BCP on banking law itself can also be

strengthened, so as to ensure that policy and law are bound in a mutually enforcing virtuous

circle.

4. The paper is, however, not intended to advocate any particular “one size fits all”

approach. The paper aims merely to give a flavor of a number of selected, commonly

encountered, legal issues that should be addressed in the legislative framework for banks and

raise inherent legal complexities. Thus, the list below is by no means exhaustive in covering

all legal issues pertaining to banking law—e.g. it does not address legal issues relating to the

liability protection of the banking supervisor and their staff, resolution framework or anti-

money laundering—and is not intended to be so. To design a complete legal framework for

banking legislation would entail issues that go beyond the list set out below. Last not but

least, this paper does not enter too much in the pure, detailed technique for legislative

drafting, even though it touches occasionally upon general drafting principles.

4

5. The paper will cover the following twelve selected issues: (i) scope and definitions,

(ii) the supervisory mandate, (iii) the legal nature of secondary regulatory instruments, (iv)

licensing requirements, (v) the distinction and relationship between licensing criteria and

ongoing requirements, (vi) corporate governance, (vii) the power to control changes in

ownership, (vii) the difference between branches and subsidiaries, (viii) consolidated

supervision, (ix) sharing of information and inter-agency coordination, (x) related-party

transactions and large exposure limits, and (xii) the legal distinction between enforcement,

early intervention and resolution.

3

See paragraph 1 of the Executive Summary of the BCP: http://www.bis.org/publ/bcbs230.htm

4

For an overview of legislative drafting in the context of tax laws: see Chapter III of IMF (Ed. V. Thuronyi),

Tax Law Design and Drafting, 1996. http://www.imf.org/external/pubs/nft/1998/tlaw/eng/

6

II. SCOPE AND DEFINITIONS

6. The scope of application of the banking law must be clear and appropriate.

Naturally, banking laws apply first and foremost to “banks”—or “credit institutions” as they

are sometimes referred to—and below we will discuss the importance of defining this

concept adequately. In addition to banks, countries have submitted credit unions, deposit-

taking micro-finance institutions, and lending-only institutions to the personal scope of

application of their banking laws. Recently, policy makers have been considering subjecting

institutions that finance their lending activities through short term financing distinct from

deposits also to the banking law with the aim to address the so-called “shadow-banking”

problem. The exact determination of which types of non-bank financial institutions should

(partly or in whole) be covered by the banking law is a matter of policy. To discuss the legal

ramifications of the possible approaches would require a separate working paper. What

matters here from a legal perspective is that all entities providing banking activities in the

pure sense of the word—lending financed by taking deposits from the public—must be

adequately covered by the banking law.

7. To that end, the design of banking laws needs to distinguish between two related,

but distinct, legal concepts, namely (i) the activities subject to licensing and (ii) the

permissible activities of banks. Many banking laws tend to conflate those two concepts,

which complicates their application.

5

What matters for the scope of the law is the first

concept, and not the second.

Activities subject to licensing—The banking law should require that any person or

entity that carries on a “banking business” obtains a license to do so. Breach of this

requirement should be punished by criminal sanctions. In this context, the question

arises whether the mere taking of deposits from the public should also be subject to

licensing. The answer is affirmative, for with very few exceptions (central banks,

postal check services, and under strict conditions brokers-dealers), only licensed

banks should have the “monopoly” of taking deposits from the public.

Permissible Activities of banks— The banking law should set out what activities a

duly licensed bank is by law allowed to undertake.

6

These activities are additional to

what constitutes the core of banking business (see below), and are as such not

otherwise subject to licensing. Examples of typical permissible activities for banks

5

An example of this problem can be found in Article 54 of the Law 32/1968 concerning Currency, the Central

Bank of Kuwait, and the Organization of Banking Business (hereafter the “Kuwaiti banking law”). The Articles

3 and 4 of the Turkish banking law (2011) are a good example of how this conceptual distinction can be

appropriately reflected in legislation.

6

Some banking laws also include a list of activities banks are prohibited to undertake.

7

are the provision of payment services, the issuance of electronic money, foreign

exchange transactions, safekeeping and vaults, etc.

8. Definitions are critical to determine the personal and material scope of

application of the banking law. To achieve an appropriate scope, the banking law needs to

define with utmost precision who is required to obtain a license to exercise which activities.

Definitions are less important for the permissible activities. What matters is that the activities

which a duly authorized bank is permitted to exercise are clearly listed. It is less important to

define those activities.

7

However, another aspect of banking laws for which definitions are

also important are the main regulatory provisions of the law, such as those on governance,

lending restrictions, and consolidated supervision. These aspects will be discussed in the next

paragraphs, but for now we focus on the definitions pertaining to the scope of the law, which

need to focus on the following two points.

9. First, every banking law needs to define what is considered to be the “banking

business” subject to licensing. The standard practice is to define this concept as “the taking

of deposits from the public and the making of loans on its own account.” This may require

the banking law also to define the concept of “deposit,” which raises the question on the

extent to which this definition in the banking law relies on the definition in the civil code, if

any. (On the interaction between definitions in different laws more generally: see below) In

that regard, one should bear in mind that deposits of money with a bank are legally not

deposits, but actually loans—the bank has contractually the right to use the deposit funds by

lending them on. Hence the need for a sui generis definition of “deposits” in the banking law.

Establishing the precise contours of that definition may be hazardous: a too broad definition

may improperly include ordinary borrowing and the issuing of bonds and commercial paper,

while a too narrow definition may open the gates for regulatory arbitrage and evasion.

10. Secondly, definitions need to ensure that the scope of the banking law covers

both individuals and corporations. Requiring only a “company” or “entity” that carries on

banking business to be licensed is insufficient, as it leaves open the possibility that banking

business be carried out by an individual or a non-corporate entity, without running afoul of

the licensing requirement.

8

The law needs to be clear that all individual persons as well as

corporations and non-corporate legal entities can be caught by the relevant provision. This is

achieved by (i) requiring that any “person” exercising banking business or otherwise taking

deposits from the public is subject to licensing and (ii) defining “persons” as both natural and

7

BCP 4 requires the permissible activities of institutions that are licensed and subject to supervision as banks to

be clearly defined. From a legal perspective, this appears to require too many definitions than may be necessary.

8

Section 7A (f) of the Bangladeshi Bank Order highlights this issue.

8

legal persons. If it is the policy intent to only allow corporate entities to hold a banking

license, this should be stated as a qualifying license criteria,

9

and not through the definitions.

11. The core definitions should be enshrined in the banking law itself. As a legal

matter, definitions that shape the personal and material scope of application of a primary law

cannot, and should not, be provided for in secondary regulation; their place is in the primary

law.

10

This does not mean that some more detailed aspects of certain central definitions

cannot be elaborated upon in secondary regulation.

11

As regards the more operative

definitions (e.g., “exposure,” “subsidiary,” “bank-related party,”), there is more tolerance for

inserting them in secondary regulation. This being said, the overall legal certainty and

transparency of the banking law would be served by putting most operative definitions in the

primary law itself.

12. In spite of their criticality, many banking laws lack relevant and robust

definitions. The extent to which terms used in the law are defined differs between legal

traditions. Our experience has shown that the extent to which terms used in banking and

other financial sector legislation are defined differs between common and civil law traditions,

with the former generally defining more terms and the latter sometimes relying on definitions

already found in the Civil or Commercial Codes. This being said, this difference should not

be overestimated: civil law banking laws increasingly include a list of definitions,

12

and many

common law banking laws refer to definitions enshrined in other laws.

13

Be that as it may,

our experience is that, both in civil and common law traditions, definitions are however often

overlooked in banking laws.

14

9

See for instance Article 56.1 of the Kuwaiti banking law, Article 7 a) of the Turkish banking law, and Article

5.2.d of the Rwandan banking law of 2008.

10

The prescriptions of the BCP with regard to the legal establishment of definitions could be stricter. For

instance, the Essential Criteria (“EC”) 1 of BCP 4 requires the term “bank” to be clearly defined in laws or

regulations. We would, however, advise that in the interest of legal certainty such a fundamental definition be

clearly set out in the law, as a primary legal instrument.

11

Section 978(d) of the Canadian Banking Act for instance authorizes the Governor in Council to issue

regulations to “to define words and expressions to be defined for the purposes of this Act.”

12

See for instance Article 3 of the Belgian banking law of 25 April 2014.

13

A good example of the latter point is Section 2 of the Reserve Bank of New Zealand Act 1989, which

includes references to the Companies Act 1993, the Insurance (Prudential Supervision) Act 2010, and the

Financial Markets Authority Act 2011.

14

A good example of circular definitions are the Financial Institutions Act 1998 of Solomon Islands, which

includes in Section 2(1) definitions for banks and financial institutions, with the latter being defined as a “body

corporate doing banking business,” and Egypt, where “banking business” is defined in the Law Nr. 88/2003 on

9

13. A second concern is that definitions should be consistent with one another and

consistent across various interconnected laws. The need to have internally consistent

definitions within the banking law is self-evident. A common example is the definitions of

“parent companies” and “subsidiaries”. These two definitions should be flipsides of each

other, but many banking laws do not necessarily draft them as such. Secondly, as the banking

law is typically only one of many relevant laws (e.g. company law, competition law,

consumer protection law, insolvency law) that are relevant for banking regulation, there is a

need to make sure that definitions are consistent across the various relevant laws, at least to

the extent that those laws are indeed interconnected.

15

This problem often arises when there

are definitions of the same term in different laws and, when the definition of a term is

amended in one law, while the similar definition in another law is not concurrently amended.

One way to avoid such inconsistencies would be to only define the term in one law and for

other laws to simply make cross-references.

16

For example, the definitions of “bank” in a

deposit guarantee law can cross-refer to the definition of “bank” in the banking law. This

simple legislative drafting method overcomes the problems of inconsistent definitions in

various laws and having to amend multiple definitions in various laws each time one law is

amended.

14. A third concern is that definitions should not also provide for substantive

obligations or requirements.

17

This is a general rule of legislative drafting technique, but

often infringed in banking and other laws. This rule certainly applies when banking laws

include upfront a single article/section with all or most of the definitions of the law. Such

approach has an advantage from the perspective of legal clarity, although it may complicate

the ease with which the law is read. When, in contrast, the law spreads definitions throughout

its structure, as in the civil law tradition, it is to be expected that definitions and normative

provisions are more closely interwoven.

15. Finally, without compromising certainty, there should also be sufficient

flexibility afforded to regulators to exercise judgment or prescribe additional categories

within the definitions. For example, for the purposes of consolidated supervision, related

party transactions and large exposure limits, terms such as “parent companies”, “banking

the Central Bank, the Banking Sector and Money as “all that is considered by banking tradition as banking

business.”

15

The authors accept that there may be instances where the same term is appropriately defined differently in

different laws. This will particularly be the case when the more specific law serves a narrow and specific

purpose that is not directly connected with the main purpose of the more general law.

16

Another way is to amend multiple laws in a single amending act or instrument (e.g. a statutes miscellaneous

amendment or consequential amendments to various pieces of legislation), rather than amending each law

individually by way of a distinct piece of legislation.

17

Article 2 of the Mexican banking law (Ley de Instituciones de Credito) is a good example of this problem.

10

groups” and “affiliated parties” will need to be defined with the necessary precision (see

below). However, there should be flexibility for regulators to prescribe additional categories

of affiliated parties. A common legal technique would be to set out specific categories in the

primary law, with a residual discretion to the regulator to prescribe additional categories in

subsidiary legislation.

18

In some cases, this technique can even be used in the other direction,

by exempting certain cases from the general definitions of the banking law.

19

III. OBJECTIVES, FUNCTIONS AND LEGAL POWERS OF SUPERVISOR

16. The legal framework should clearly set out the supervisory authority’s

objectives, functions and legal powers.

20

The banking law, as any type of supervisory law,

is essentially a specialized branch of administrative law. This body of law sets out how the

States and its agencies operate, and under which conditions and modalities the rights of

citizens can be constrained by the State. To protect their citizens, in many jurisdictions the

judiciary construes the powers of the State and its agencies narrowly: they have no functions

and powers but those established by legislation (the legality principle). In that light, to make

banking supervision and regulation legally robust, it is imperative that the contours of the

“mandate” of banking supervisory agencies are adequately laid down in legislation. The

mandate comprises the agency’s objectives, functions and powers. The objectives are the

goals that the supervisory authority aims to accomplish (the “why” of the regulator’s

mandate). The functions (or tasks) are the activities that the supervisory authority should

undertake to attain these goals (the “what”). The powers are instruments and tools (the

“how”) the supervisory authority will need to achieve its objectives and perform its

functions.

17. Many banking laws do not adequately specify the objective of banking

supervision and regulation. To offer an effective anchor for supervisory decision making,

including in the context of accountability exercises of autonomous supervisors, a clear

statement of the supervisory authority’s overall objective in supervising banks should be

specified in the primary law. An alternative approach is to cast the objectives as those of

18

As illustrated by Article 1 of the Iraqi banking law of 2003.

19

See Article 3.30 of the Belgian banking law, which authorizes the supervisory authority to exempt certain

banks from the qualification as “significant” even though the balance sheet threshold established in the primary

law is met.

20

The BCP require that the responsibilities and objectives are clearly set out in the law. EC 1 of BCP 1 requires

that the responsibilities and objectives of the authority involved in banking supervision are clearly defined in

legislation and publicly disclosed. BCP 1 also requires that there is a legal framework in place for the authority

to be provided with the necessary legal powers to authorize banks, conduct ongoing supervision, address

compliance with laws and undertake timely corrective actions to address safety and soundness concerns.

11

banking supervision per se, instead of as objectives of the supervisory authority.

21

Common

supervisory objectives include to promote the safety and soundness of banks and the banking

system and to protect depositors.

22

The drafting of supervisory objectives often raises the

following three complex legal points:

Some jurisdictions may assign other objectives to banking supervisors, such as the

development of the local financial sector.

23

It is however important to ensure that such

other objectives are legally subordinate to, and do not conflict with, the primary

objectives of financial stability and depositor protection.

24

The primary supervisory objectives should also be phrased in an achievable manner.

To phrase an objective as “to prevent bank failures” is unrealistic and conducive to

“moral hazard” problems. In this regard, the BCP clearly state that it should not be

the objective of banking supervision to prevent bank failures. However, an (implied)

objective of banking supervision should be to reduce the probability and impact of a

bank failure, so that when a failure occurs, the failure can be managed in an orderly

manner. This could be achieved by the new supervisory tool of “Recovery and

Resolution Planning.

A final point is that the primary objectives of banking supervisory authorities should

be read in their broader institutional context. For instance, the financial stability

objective of a separate supervisory authority should be read in conjunction with the

central bank’s objective in this regard. In a similar vein, the depositor protection

objective must be considered in light of the depositor guarantee scheme.

25

18. To enable the supervisory authority to pursue its objectives, there should be a

(set of) corresponding statutory function(s). For supervisory authorities that are not

central banks, these functions can easily be discerned from the banking law, and are

generally not specified as such in legislation—in contrast to the objectives and powers. The

reason for such approach is that banking supervisors have few and straightforward functions.

21

See for example Article 1.2 of the Belgian banking law.

22

See for instance Article 1 of the Turkish banking law and Article 56, second paragraph, of the Central Bank

of Russia Act. Section 6 of the 2013 Malaysia Financial Services Act also offers an interesting approach: the

Act first sets out the promotion of financial stability as the “primary regulatory objective of the Act,” and then

sets out some intermediate objectives, such as the safety and soundness of financial institutions and the

protection of rights of consumers of financial services.

23

See for instance Article 3 of the Central Bank of Russia Act, which entrusts the Central Bank of Russia with

the objective to “develop and strengthen the banking system of the Russian Federation.”

24

See BCP 1, EC 2

25

E.g. a depositor protection objective does not imply that no depositor, whatever is the size of his deposit,

should ever suffer a loss due to a banking failure. Coverage under the deposit guarantee scheme up to a certain

amount gives an indication of the amounts up to which deposits are socially “worthy” of protection.

12

This issue is more relevant for those central banks that are also banking supervisory

authority, since they are charged with a great many functions. To offer clarity in this regard,

central banks laws often set out a comprehensive list of functions in a single legislative

provision. If that is the case, such a list should ideally also include a supervisory/regulatory

function.

26

A good way to draft such a function is to charge the supervisory authority with

the succinct function “to regulate and supervise banks and other financial institutions.” An

alternative is to draft the regulatory and supervisory function in somewhat more detail,

27

possibly even in the banking law instead of in the central bank law.

28

Whatever approach is

taken, such a function should be clearly distinguished from the objectives of the central bank-

cum-supervisory authority, given that they play legally very different roles.

29

19. The legal framework should also be clear as to whether the supervisory

authority has powers to pursue the statutory objectives. Does the supervisory authority

have the legal powers to pursue the statutory objectives (e.g., powers to issue regulations, to

set prudential standards, to grant and revoke banking licenses, to take corrective action,

impose sanctions etc.), or does the power reside with another authority or agency? Ideally,

the supervisory authority should also be the licensing authority and be able to issue

regulations and take supervisory decisions autonomously. However, constitutional or

administrative law may constrain the level of involvement of autonomous (i.e., non-political)

agencies in general or individual normative decisions, and require a degree of involvement of

political bodies in the establishment and enforcement of banking and other forms of

regulation. For instance, in some countries, the supervisory authority may not have the legal

power to issue or revoke licenses

30

or to promulgate secondary regulation.

31

The question is

26

A good example of this can be found in the Law 1/34 of 2 December 2008 on the Statute of the Central Bank

of Burundi: Article 6 states that the central bank has a secondary objective to contribute to the stability of the

financial system, while Article 7 establishes the function of regulation and supervision of banks and other

financial institutions.

27

See for instance Article 4 (5), (7) and (9) of the Central Bank of Russia Act.

28

The Netherlands is an example of where the central bank is the prudential supervisor, but the supervisory

objective and function is established in the banking law rather than in the central bank law: see next footnote.

29

A good example of how this can be achieved can be found in the Netherland’s Law on Financial Supervision.

Article 1:24.1 provides that the objective of financial supervision is the solidity of financial firms and the

stability of the financial system. Article 1:24.2 charges the Dutch central bank with the function of supervision

over financial firms and their access to financial markets.

30

There are still countries where the supervisory authority is not the licensing authority. For instance, in

Malaysia and Kuwait, the central bank is the supervisor, but banks are licensed by the Minister of Finance. In

Italy, the Ministry of Economy and Finance decides on license revocations, upon proposal by the Bank of Italy.

31

In some countries (e.g. USA, Lebanon and Singapore), regulatory agencies have the legal power to

promulgate secondary regulation in their fields of competence. In other countries (e.g. the UK, Netherlands,

Belgium), constitutional principles require that secondary regulation be approved by political bodies

(Parliament, the Government, or Ministry of Finance).

13

of course to which degree this is the consequence of a political choice or, conversely, legal

constraints.

20. From a drafting perspective, the supervisory authority’s objectives, functions

and legal powers should as much as possible be provided by the banking law. This is

particularly relevant for those central banks that are also banking supervisors. When that is

the case, the central bank law should only refer summarily to—and not intend to

summarize—the legal aspects of the bank supervisory regime; this body of law should as

much as possible be comprehensively enshrined in the banking law itself. If the bank

supervisory regime is spread out over two or more laws, the interpretation and application of

the rules will be complicated, for instance due to a higher risk of contradiction and also to

complexities inherent to the contextual interpretation method.

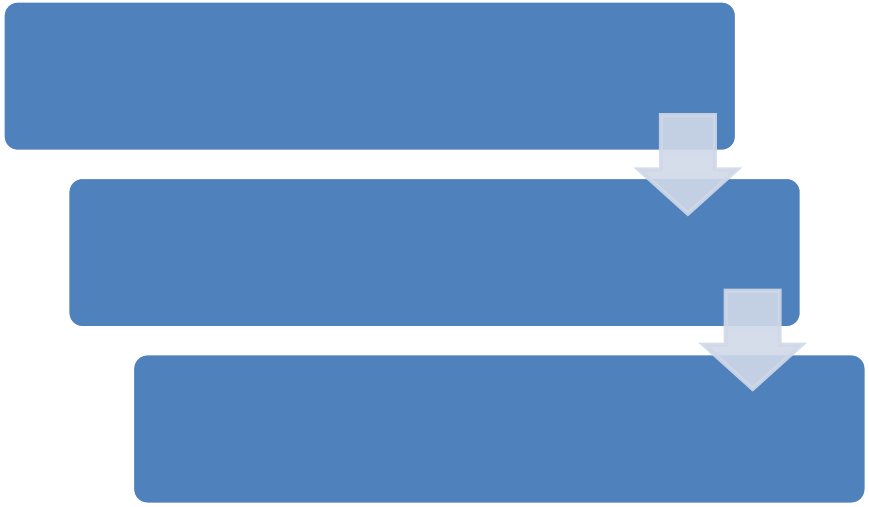

Figure I. Common Objectives, Functions and Powers

21. Finally, effective and efficient bank supervision requires the involved authorities

to have clear mandates, without gaps or overlaps in their responsibilities. Where there is

more than one regulatory authority involved in banking supervision or supervision of a

banking group, the respective roles and responsibilities should be clearly defined in the law.

This is necessary to avoid regulatory and supervisory gaps. Effective domestic inter-agency

cooperation and coordination would also be crucial in such cases (see below).

IV. LEGAL NATURE AND HIERARCHY OF SECONDARY REGULATORY INSTRUMENTS

22. To ensure their effective implementation, most banking laws authorize the

issuance of a variety of secondary legal instruments. It is all but impossible, and moreover

Objectives: To promote the safety and

soundness of banks and the banking

system; to protect depositors

Functions: To regulate and supervise

banks and other financial institutions

Powers: To license banks, conduct

ongoing supervision, enforce laws,

impose sanctions, take corrective action

14

quite impractical, to include all aspects of banking regulation in a single piece of primary

legislation. By consequence, most legislatures have included in their countries’ banking laws

powers for the government and/or banking supervisors to issue legal instruments aimed at

implementing the main banking law. Thus these instruments are “secondary” to the primary

banking law.

23. The legal nature of those secondary legal instruments is often unclear. We are not

concerned here with the powers of the government to issue decree-type instruments as per

general constitutional provisions or principles. Generally speaking, such powers raise few

legal questions. Nor shall we discuss here the question whether banking supervisors ought to

have autonomous regulatory powers per se, which often raises complex constitutional and

administrative law issues (see para. 19), and calls for an altogether different paper. Rather we

are concerned in the context of this paper with the more problematic issue of the “regulatory”

powers granted to banking supervisors to issue regulations, circulars, guidelines, directives,

and similar instruments, the legal nature of which is often unclear. The two most common

questions that arise in this respect concern (i) the binding nature of the instruments in

question, and (ii) their place in the overall “hierarchy of norms.”

A. Legal Nature

24. Banking laws should first be clear as to the legal nature or effect of the

respective secondary instruments issued under them. In doing so, it is critical to

adequately distinguish between those instruments that have direct binding effects on private

entities, and those that do not.

32

Binding Secondary Instruments

25. If a jurisdiction is to have recourse to binding secondary instruments issued by

the supervisor, the banking law itself or another piece of primary legislation should

unequivocally establish the authority to issue such instruments.

33

The manner in which

this is done raises several concerns, grounded in the interaction between the banking law and

administrative and constitutional law. The following four principles apply:

The banking supervisory authority should ensure that it issues its binding secondary

instruments under the categories and conditions foreseen by constitutional and/or

32

The Egyptian banking law is an example of a law referring to a multiplicity of secondary instruments without

defining with precision the legal nature and effect of those instruments.

33

Article 8 of the above-mentioned Law 1/34 of 2 December 2008 on the Statute of the Central Bank of

Burundi gives a good example of how the legal nature of the various secondary legal instruments can be

established. Article 57 of the Central Bank of Russia Act also clearly and unequivocally established the binding

nature vis-a-vis banks of the CBR’s “rules.”

15

administrative law.

34

In this respect, it is often important to distinguish between

binding instruments of general application to all banks (“regulations”), and those that

apply to a single bank (often labeled “instructions” or “orders”). In many

jurisdictions, general and individual normative instruments are subject to different

prescriptions of constitutional and/or administrative law. In our advisory practice, we

have often observed that jurisdictions tend to conflate those two aspects, which may

weaken the legal robustness of those instruments.

Drafters of banking laws must decide whether they will grant the banking supervisor

general executive power over the banking law, or only a specific power to implement

on a case by case basis the provisions of the banking law that need to be implemented

by secondary regulation. Each of those two approaches has advantages and

disadvantages. The advantage of the former is that the supervisor has broad

regulatory powers and can decide to regulate whenever a specific development

requires regulatory action. The disadvantage is that the statutory ground for regulation

is less precise and explicit, which makes the regulation more vulnerable to the

argument that it was established without sufficient legal basis. The latter approach

raises the opposite points.

Banking laws should not create different but similar legal instruments (e.g.

“regulations” and “rules”) if there is no real added value in the distinction. Doing so

would create unnecessary legal confusion that may weaken the legal robustness of

those instruments.

The legal framework should be clear as to how the secondary instruments acquire

their binding effect. To that end, the law should be clear on which decision-making

body of the banking supervisor is competent to issue the instrument, how the

instruments are promulgated and published, and what the consequences of their

breach are.

Non-Binding Secondary Instruments

26. If the banking law provides for non-binding secondary instruments, the law

should equally be clear on their legal effects and nature. If the banking law is silent on

such instruments, than it may generally be assumed that the supervisory authority can issue

non-binding instruments.

35

If however the law establishes such an instrument, then the law

should expressly state that the purpose of the instrument (e.g., a circular) is to merely provide

34

For instance, in the Solomon Islands’ Financial Institutions Act 1998, some secondary rules are not enshrined

in regulations foreseen by the banking law, but rather in so-called “prudential guidelines,” the legal nature of

which is not particularly clear. A similar problem arises in Indonesia, where Article 16.3 of the Act 7/1992

concerning Banking requires Bank Indonesia to “stipulate” licensing criteria and procedures, without clarifying

the nature of such stipulations, whereas Article 20.3 utilizes the clearer category of “Government Regulation.”

35

The “legality principle” only requires an explicit legislative basis for the issuance of binding legal

instruments. This issue is, however, jurisdiction-specific, and different jurisdictions may have different

approaches, also in function of their legal and political traditions.

16

guidance to private entities, so as to avoid confusion on its legal nature. If the legal

instrument is not binding in itself, but still has legal consequences for a supervised entity

(e.g., a warning notice that commences a regulatory delay) or for the supervisor itself, this

should equally be provided for with precision in the law, or at least be clearly determinable

pursuant to the relevant general principles of the relevant jurisdiction. The consequences of

breaching the prescriptions enshrined in non-binding instruments are another issue that may

need to be addressed in the banking law.

27. A particular concern in that regard is that the use of different labels in the

banking law should be consistent with the broader legal framework. For instance, if the

administrative law regime of a jurisdiction recognizes the use of binding secondary

instruments labeled “guidelines,” it would be unwise to refer as “guidelines” to non-binding

legal instruments under the banking law. Conversely, if in a country’s legal tradition

“circulars” are generally used to label summaries of non-binding administrative practice

(e.g., in the field of tax law), it is better not to use the term to designate normative

instruments under the banking law. An example of how a jurisdiction explains to the public

the legal effect (if any) of the various legal instruments can be found in Box 1.

B. Hierarchy of Norms

28. The banking law or broader legal framework should be unequivocally precise on

the place of the secondary instruments in the overall legal “hierarchy of norms.” Most,

if not all, legal systems utilize this concept, pursuant to which all public law acts are ranked

according to a legal hierarchy, entailing that each legal act must be consistent with the legal

acts of a higher rank. If a lower legal instrument is not consistent, judicial review can strike

down the lower, inconsistent legal act, thus rendering it inapplicable and unenforceable. A

common hierarchy looks as follows: (1) the constitution, (2) acts of parliament/congress, (3)

normative instruments (“decrees”) of the executive, i.e. the cabinet as a whole, (4) normative

instruments (sometimes also called “decrees”) of individual ministers/secretaries, (5)

normative instruments (“regulations”) of autonomous regulatory agencies, and (6) normative

instruments of local governments.

36

In designing legal frameworks for banking supervision,

this implies that due care must be given to determining with the highest possible precision

which elements are, or must be, governed by primary law, and which ones may be dealt with

in secondary regulation. Moreover, drafters of secondary instruments should ensure that the

latter are consistent with, as well as grounded in, what is set out in primary legislation, and

are promulgated pursuant to an empowering provision in the primary legislation.

Box 1. Classification of Instruments

36

We note that this is a stylized representation of the concept, and that most jurisdictions will have hierarchies

that differ from it due to, among other factors, their administrative organization (including federal or regionalist

models) and mechanisms for judicial review (some ancient parliamentary traditions do not have judicial review

of the constitutionality of acts of parliament).

17

Classification of Instruments Issued by Monetary Authority of Singapore (MAS)

37

MAS, in carrying out its functions as a regulator of the financial services industry, issues various

instruments under Acts administered by MAS. For the purposes of this website, the following

classification of instruments issued by MAS is adopted:

(1) Acts

The Acts contain statutory laws under the purview of MAS which are passed by Parliament. These

have the force of law and are published in the Government Gazette. Examples are the Banking Act

and Financial Advisers Act.

(2) Subsidiary Legislation

Subsidiary legislation is issued under the authority of the relevant Acts and typically fleshes out the

provisions of an Act and spells out in greater detail the requirements that financial institutions or

other specified persons (e.g. a financial adviser's representative) have to adhere to. Subsidiary

legislation has the force of law and may specify that a contravention is a criminal offence. They are

also published in the Government Gazette. Examples are the Insurance (Actuaries) Regulations and

Finance Companies (Advertisements) Regulations.

(3) Directions

Directions detail specific instructions to financial institutions or other specified persons to ensure

compliance. They have legal effect, meaning that MAS could specify whether a contravention of a

direction is a criminal offence.

Directions consist of the following:

(a) Directives - Directives primarily impose legally binding requirements on an individual financial

institution or a specified person.*

(b) Notices - Notices primarily impose legally binding requirements on a specified class of financial

institutions or persons. Examples are the Notice to Banks (MAS 603) on Branches and Automated

Teller Machines and Notice to Life Insurers (MAS 307) on Investment-linked Life Insurance

Policies.

(4) Guidelines

Guidelines set out principles or "best practice standards" that govern the conduct of specified

institutions or persons. While contravention of guidelines is not a criminal offence and does not

attract civil penalties, specified institutions or persons are encouraged to observe the spirit of these

guidelines. The degree of observance with guidelines by an institution or person may have an impact

on MAS' overall risk assessment of that institution or person. Examples are the Technology Risk

Management Guidelines for Financial Institutions and Guidelines on Standards of Conduct for

Insurance Brokers.

(5) Codes

Codes set out a system of rules governing the conduct of certain specified activities. Codes are non-

statutory and do not have the force of law. However, a breach of a Code may attract certain non-

statutory sanctions like private reprimand or public censure. There is currently a Code on Take-overs

and Mergers (which is administered by the Securities Industry Council), a Code on Collective

Investment Schemes and a Code of Conduct for Credit Rating Agencies. A failure to abide by a code

does not in itself amount to a criminal offence but may have certain consequences.**

(6) Practice Notes

Practice Notes are meant to guide specified institutions or persons on administrative procedures

relating to, among others, licensing, reporting and compliance matters. Contravention of a practice

note is not a criminal offence, unless a procedure stated in the practice note is also required by an Act

or regulation. An example is the Practice Note on Lodgment of Documents relating to Offers of

Shares and Debentures.

(7) Circulars

37

http://www.mas.gov.sg/regulations%20and%20financial%20stability/regulatory%20and%20supervisory%20fra

mework/classification%20of%20instruments%20issued%20by%20mas.aspx

18

Circulars are documents which are sent to specified persons for their information or are published on

the MAS website for public information. Circulars have no legal effect. An example is the MAS

Circular to Banks on Outsourcing of Cash And Cheque-Related Transactional Services to Another

Bank.

(8) Policy Statements

Policy statements outline broadly the major policies of MAS.

* An exception relates to a certain class of instruments, Directives to Merchant Banks, which are essentially

"Notices" for the purposes of this classification but, for historical reasons, are known as directives.

**For the Singapore Code on Take-overs and Mergers, please refer to Part VIII and section 321 of the

Securities and Futures Act for its effect. For the Code on Collective Investment Schemes, please refer to Part

XIII, Division 2 and section 321 of the Securities and Futures Act for its effect. For the Code of Conduct for

Credit Rating Agencies, please refer to section 321 of the Securities and Futures Act for its effect.

V. LICENSING REQUIREMENTS

29. Many banking laws tend to conflate the procedure and criteria for licensing

banks; these are two related but legally very different concepts. The licensing procedure

sets out the procedural rules that applicants—and indeed the supervisory authority—are

required to follow in requesting a banking license from the competent licensing authority. As

discussed below, this includes the informational requirements necessary to commence the

licensing procedure. The licensing criteria, in contrast, provide the substantive preconditions

that must be met by an applicant for the licensing authority to grant it the license. Banking

laws often include provisions dealing with both aspects in a confusing manner, whereby it is

not clear which aspects are procedural and which aspects are substantive. It should be noted

that this problem can be general, or specifically related to a particular sub-issue (e.g.

significant shareholders).

38

A. Licensing Criteria

30. To remedy this weakness, the primary law should first clearly set out the

licensing criteria for banks. The details of these criteria can certainly be further elaborated

in subsidiary regulation.

39

However, the core criteria themselves should be clearly set out in

primary legislation.

40

From a drafting perspective, this does not only require that the subject

matter (e.g., governance, accounting mechanisms) be provided, but also the yardstick against

which the subject matter will be judged (e.g., the governance must be appropriate for the

38

A good example of this can be found in the banking law of the DRC: the law only requires applicants for a

license to include a list of prospective shareholders in the license application, but lacks any requirements or

standards regarding significant shareholders in the context of licensing a bank.

39

For instance, Article 16.2 of the Indonesian Banking Law grants Bank Indonesia the power to specify the

licensing criteria.

40

Article 31 of the Bangladeshi Bank Companies Act is an example of too limited criteria being provided in

statute, thus obliging the licensing authority to rely excessively on secondary guidelines.

19

operations and structure of the bank). Further, it is critical that the respective requirements

are well defined. In doing so, a balance should be struck between legal certainty for the

industry to know what licensing requirements are required to be satisfied and the discretion

of the regulator to refuse licensing. In that regard, it is often very useful to provide an

overview to the political bodies, industry, and the public at large, by way of circulars or

similar non-binding instruments, of the licensing authority’s administrative practices in

granting and refusing licenses as well as its understanding of the relevant legal framework.

31. International good practice has now converged upon a comprehensive set of

minimum statutory licensing criteria. The following are the typical criteria that are

expected to figure in well written banking laws:

the minimum paid-up capital of the bank should meet the amount established by law or

regulation; (as opposed to the Capital Adequacy Ratio, which is an altogether different

concept, relying on the ongoing level of risk exposure in relation to qualifying own

funds);

the ownership structure of the bank should be sufficiently transparent and allow for

effective supervision of the bank;

41

fit and proper requirements for directors and senior management of the bank;

suitability requirements for significant shareholders of the bank;

a financial structure, managerial structure, and business plan that are appropriate for the

programme of the bank’s projected activities;

42

adequate arrangements for accounting, internal controls, risk management, and internal

and external audit; and

41

Some banking laws go beyond this criterion, and prohibit for instance, certain types of entities to be

shareholders of banks (e.g. industrial or commercial enterprises), or require banks to have a significant

shareholder of a certain type (e.g. a bank holding company). This raises other specific policy issues, namely

who can own and control a bank.

42

The concept of financial structure is different from the one of minimum paid up capital mentioned under (i).

The latter merely seeks to require from all banks a capital beyond a fixed quantitative limit. The former goes

beyond this minimum threshold, and requires that any bank has a starting capital that is adequate in light of its

projected activities. Thus, except for the smaller banks, it is to be expected that the former amount will in most

cases be higher than the latter amount.

20

for branches and subsidiaries of foreign banks, the consent of the foreign bank’s home

supervisor as well as an adequate supervisory arrangement between home and host

supervisor.

43

32. The legal operation of the licensing criteria should also be clear. On the one hand,

it must be beyond doubt that the license can only be granted if the licensing authority is

satisfied that all licensing criteria are (cumulatively) met. On the other hand, the law should

also be clear as to whether the licensing authority can refuse the license even though all

criteria are met. In that regard, there may be good “systemic” reasons to refuse the license,

for instance when the banking system is overbanked, or when there is general state of

systemic distress. In some legal systems, it is necessary to include such systemic licensing

criteria in the law itself, lest applicants enjoy a legal right on a license when all the bank-

specific criteria are met. In other legal systems, such systemic criteria are not necessary,

because the licensing authority can refuse (as per general administrative law principles or on

public interest grounds) to grant a license even though all criteria are met.

B. Licensing Procedure

33. Furthermore, banking laws should lay the legal basis for the licensing

procedures, although the details can very well be established in secondary regulation.

At a minimum, the primary law should grant the licensing authority the power to establish a

comprehensive licensing procedure by means of secondary regulation.

44

This approach is,

however, not the very best practice we have distilled from our advisory practices. Rather, we

believe that the primary banking law itself should include the core provisions of the licensing

procedure. The main argument for this is similar to the one regarding the criteria: because

the licensing procedure, and in particular the refusal to grant a license, may affect third party

interests, it is advisable to enshrine the key mechanisms of the procedure in primary law,

including the possibility to legally challenge the said refusal. An additional but related

argument is indeed that courts may be requested to review the legality of decisions taken

pursuant to the licensing procedure. Firm foundations established in statute rather than in the

licensing authority’s own rules tend to strengthen the position of the licensing authority in

this type of review, in the sense that the review focuses on the legality of the individual

decision rather than of the entire procedure—an illegal procedure would ipso facto affect the

legality of the individual decision.

34. Here too it is possible to distill good legal practice. Without purporting to be

exhaustive, the following elements call for the attention of drafters of banking laws:

43

See EC 10 of BCP 5.

44

See for instance Article 6 of the Turkish banking law.

21

The law should unambiguously state that the licensing criteria operate as such, i.e. they

must all be fully deemed met by the licensing authority for the license to be granted.

45

When not all criteria are fully deemed to be met, the licensing authority must have the

power—if not the duty—to reject the license application. (see also BCP 5)

The law should require the applicant to provide complete and correct information to the

licensing authority. As it is quite impractical to establish all informational requirements

in primary legislation, it is appropriate to stipulate that the licensing authority can specify

those, or impose additional requirements, in secondary regulation.

46

Secondary regulation

may also be useful to prescribe the more practical informational aspects of the licensing

procedure (e.g., forms). Finally, in listing informational requirements in law and

regulations, it is always useful to insert a “catch-all” clause pursuant to which the

licensing authority may require any additional information deemed necessary or useful

for completing the licensing process.

47

The law should set out the legal consequences of any incomplete or untimely provision of

information.

48

For instance, the relevant time period for deciding upon the license should

only commence if and when the licensing authority has determined that it has received all

necessary information to come to a conclusion. Further, the provision of incorrect

information should be a ground for refusing to grant the license,

49

and withdrawing it in

the event the license has already been granted.

The law should lay out the key steps, and the corresponding time-frames, of the licensing

procedure. In some countries, the banking law includes a rule that the licensing authority

will decide upon the license application within (x) months upon receiving a complete

application.

50

Such a rule is sometimes complemented by another rule that the license

application shall be deemed rejected if the licensing authority has not decided within the

required time. In designing such rules, a balance must be struck between the flexibility of

45

As an example of where that is not the case, Section 5.5 of the banking law of the Solomon Islands states a

list of “matters” that must merely “be regarded” by the licensing authority while licensing banks.

46

A good example of a comprehensive regulatory approach is Article 5 of the Sudanese Licensing Regulation.

47

See for instance Article 10 VI of the Mexican banking law.

48

We accept that in jurisdictions with sophisticated administrative law regimes, the latter will include general

principles for dealing with those questions, thus making detailed rules in the banking law superfluous. In all

other jurisdictions, which include many emerging and most developing countries, lawmakers shall find it useful

to elaborate on these issues in the banking law itself.

49

See EC 2 of BCP 5.

50

Some banking laws may not provide for such a time frame, so as not to tie the hands of the authorities.

However, including a time frame would provide for certainty to applicants and discourage authorities from

taking too long to process a license application.

22

the supervisory authority in making complex judgments and the fundamental right of

applicants to seek judicial review of administrative decisions. In doing so, due regard

must be given the application of general administrative law principles, which may

provide guidance as to when an administrative decision is deemed to be made and when

it becomes subject to judicial review. In case there would be no such principles, or if the

general principles would be unclear or problematic, it may be useful to enshrine some

specific principles in the banking law to enhance the overall legal quality of the process.

VI. ONGOING REQUIREMENTS VERSUS LICENSING CRITERIA

35. Many banking laws are unclear as to the extent to which, beyond the licensing

stage, the initial licensing criteria continue to apply on an ongoing basis to maintain the

license. As discussed in the previous section, banking laws should provide the requirements

(“criteria”) for obtaining a banking license. All of these requirements should not only apply

at the licensing stage, but should continue to apply even after the banking license has been

granted. BCP 5, EC 3 provides that the criteria for issuing licenses should be “consistent

with” those applied in ongoing supervision. The manner in which this is legally achieved in

banking laws, however, often leaves something to be desired.

36. The banking law needs to explicitly provide that all licensing criteria continue to

apply to licensed banks as ongoing requirements. Naturally, the legal nature of ongoing

requirements differs considerably from that of licensing criteria and the banking law should

bring out this distinction clearly. This is most obvious in case of breach of ongoing

requirements. In this regard, it is critical that the supervisory authorities have the appropriate

power to take remedial action if any of the criteria is no longer satisfied. To enable the

supervisor to monitor changes, the legal framework could impose an obligation on the bank

to immediately report to the supervisor any changes in information or circumstances after the

grant of the license, to enable the supervisor to make the necessary assessment. A failure to

provide timely notification should in such case attract the appropriate corrective measures

and/or sanctions.

37. Three examples of typical criteria which need to be complied with as long as a

firm holds a banking license are –

Suitability requirements for significant shareholders. At the licensing stage, the

licensing authority determines suitability of the bank’s major shareholders, sources of

initial capital and ability of shareholders to provide additional support. These

requirements should continue to apply once the license is granted as there is a need to

ensure continued suitability and financial soundness of the significant shareholders. As

will be discussed in detail in Section VIII below, in relation to changes in significant

shareholdings in the bank, the authorities should have powers to approve or reject

changes to ensure that the ownership structures do not hinder effective supervision.

23

Fit and proper requirements for directors and senior management. The requirement

for directors and senior management to be fit and proper should continue to apply as well.

Therefore, the banking law should require that the subsequent appointment of bank

directors and senior managers be subject to the supervisor’s express prior approval. BCP

14 provides that laws, regulations or the supervisor should require banks to notify the

supervisor as soon as they become aware of any information that may negatively affect

the fitness and propriety of a bank’s Board member or member of senior management.

Should a director or senior management no longer satisfy the fit and proper requirements,

the supervisor should be empowered to require the relevant person to be removed from

his position, whether directly or via the bank.

Internal controls, accounting, risk management, audit requirements. At the licensing

stage, the authority reviews the proposed strategic and operating plans of the bank. This

would entail a determination that there is an appropriate system of corporate governance,

risk management and internal controls that is commensurate with the scope and degree of

sophistication of the proposed activities of the bank.

51

These requirements would continue

to apply beyond the grant of the license and the supervisor would be monitoring the

implementation of these policies.

VII. CORPORATE GOVERNANCE

38. The recent financial crisis has brought corporate governance issues to the fore.

Most banking failures are caused by weaknesses in bank governance. For advanced

economies, this problem consists predominantly of management being insufficiently

accountable to the shareholders and stakeholders of banks. The recent crisis showed up

additional problems with insufficient board oversight of senior management, inadequate risk

management and unduly complex or opaque bank organizational structures and activities. A

good corporate governance framework facilitates efficient decision making, promotes

accountability, transparency and legitimacy. Sound corporate governance practices also

enhance public confidence in individual banks and the banking system

52

.

39. The emphasis on good corporate governance and risk management has resulted

in a new CP on corporate governance in the 2012 version of the BCP. BCP 14, in relation

to corporate governance, requires that banks and banking groups have robust corporate

governance policies and processes covering strategic direction, group and organizational

structure, control environment, responsibilities of the banks’ Boards and senior management

and compensation. These policies and processes should be commensurate with the risk

51

BCP 5, EC 8

52

See also Basel Committee’s Principles for Enhancing Corporate Governance, October 2010

24

profile and systemic importance of the bank. BCP 15 deals with the bank’s risk management

process.

40. There are several aspects of bank corporate governance that should be

addressed in the legal framework. Banks are typically structured as companies, and

companies law requirements would apply to the extent that they do not conflict with express

provisions in the banking law, devised as a lex specialis departing from the general company

law.

53

Provisions on the board of directors, board meetings, audit requirements and the like

would typically be found in the Companies Law. To the extent that there is a need for

specific requirements for banks (e.g., a minimum or maximum number of directors, specific

committees, more detailed requirements for selection of external auditors and external

audits), these should be expressly provided for or varied in the banking law.

54

The legal

framework, whether in the Banking Law or the Companies Law, would need to address the

following:

a. Board of Directors. The law should set out the Board composition and the minimum

number of independent directors

55

. There should also be a clear process for nominating

and appointing directors, clarity on the duration of office, qualification and

disqualification criteria and a requirement for supervisory approval. There should also be

provisions dealing with conflicts of interests and confidentiality obligations which should

survive beyond the term of directorship. Supervisors should have the legal power to

require changes in the composition of the bank’s Board if it believes that any individual

is not fulfilling his duties in relation to the criteria set out in BCP 14

56

.

b. Fit and proper criteria for board directors and senior management. Bank board

members and senior management need to be suitably qualified for their duties and satisfy

fit and proper criteria. Typical criteria would relate to -

i. honesty, integrity and reputation (not refused right to carry on trade, business,

profession, not censured, disciplined or suspended by a professional body, no

criminal proceedings or convictions),

53

As nicely illustrated by Article 6 of the Mexican banking law.

54

See, for instance, Article 21 of the Mexican banking law, which states that the “management of (banks) is

entrusted to the board of directors and a director-general.” The provision also requires the board of directors to

establish an audit committee. Article 23 of the Turkish banking law requires that “the board of directors of any

bank have at least five members including the general manager.”

55

In some countries, a two-tier structure exists where the supervisory function of the board is performed by a

separate entity known as a supervisory board, which has no executive functions. It is outside the scope of this

paper to discuss different board structures and the principles discussed in this paper are intended to be of

general application to different structures.

56

BCP 14, EC 9

25

ii. competence and capability (past performance or expertise, no conflicts of interest,

educational qualifications); and

iii. financial soundness (able to fulfill financial obligations, not a bankrupt, no

outstanding judgment debts).

Typically, a banking law would provide for a general requirement that Board directors

and senior management be fit and proper persons. The details on what constitutes “fit and

proper” could be expanded upon in subsidiary legislation or guidelines. The term “senior

management” is subjective and may be understood differently depending on a bank’s size

and organizational structure. Reiterating the very first point made in this paper, it is thus

essential to define with precision the universe of “senior management” that would be

subject to this test, so as to provide clarity and prevent legal challenges.

c. Audit, risk management and internal control. The law should require an external audit

and internal audit function, with Board oversight over it. Banking supervisors should be

satisfied that banks have in place a comprehensive risk management process to identify,

measure, monitor and control all material risks. The Board and senior management

should know and understand the bank’s and banking group’s operational structure and

risks. The Board approves and oversees implementation of the bank’s strategic direction,

risk appetite and strategy, establishes conflicts of interest policies etc. The Board should

also have audit and risk committees whose duties and membership are segregated from

the executive functions of the bank.

57

VIII. POWER TO CONTROL OWNERSHIP CHANGES

41. The misuse of banking resources by dominant shareholders is a second notable

example of corporate governance failures that are an important cause of bank failures.

Sometimes this problem is caused by an individual shareholder exercising excessive

influence. In other cases banks are owned by conglomerates and the bank’s funds are used to

fund commercial and industrial activities of affiliate firms beyond what would be conducive

to the long term stability of the bank.

42. Many banking laws lack the legal tools to prevent such oft-occurring misuse. All

too many banking laws lack robust mechanisms to vet new significant shareholders acquiring

their stake after the licensing procedure has been completed, as well as tools to remove

inappropriate shareholders once they have illegally acquired their influential position, or

legally acquired it and start misusing it. In some instances, this problem has been considered

by the IMF to be so fundamental to supporting the medium term financial, and consequent

balance-of-payment stability of its members, that the Fund has required strengthening the

rules regarding significant ownership of banks as part of its structural conditionality under

57

BCP 14, EC 3

26

Fund-supported programs. This was for instance the case of the recent arrangements of the

DRC and Bangladesh under the Fund’s Extended Credit Facility, which both required these

countries to significantly strengthen their regulatory frameworks for significant

shareholders.

58

43. In what follows, we will give an overview of the central elements that any legal

framework for significant shareholdings in banks should include.

59

While some of the

details of the broader regime (e.g., in respect of the details of the approval standards, the

procedural aspects of the approval process, and some elements of the enforcement regime)

can be established in secondary regulation, we believe that the central features of this regime

should be established in primary legislation. This would provide legal certainty, reinforce the

importance of those rules, and enhance the effectiveness of supervision and enforcement.

44. The supervisory authority should first and foremost have the power to control

changes in significant ownership in banks. The legal mechanism underpinning this power

consists of several interconnected components. The first component is one of principle: the

law should stipulate with utmost clarity that a person or entity may and can only acquire or