Running Head: HISTORICAL PATTERNS AND RECENT IMPACTS 1

Historical Patterns and Recent Impacts of Chinese Investors on United States Real Estate

Kevin Sun

Unionville High School

HISTORICAL PATTERNS AND RECENT IMPACTS 2

Abstract

Since supplanting Canada in 2014, Chinese investors have been the lead foreign buyers of U.S.

real estate, concentrating their purchases in urban areas with higher Chinese populations like

California. The reasons for investment include prestige, freedom from capital confiscation, and

safe, diversified opportunities from abroad simply being more lucrative and available than in

their home country, where the market is eroding. Interestingly, since 2019, Chinese investors

have sold a net 23.6 billion dollars of U.S. commercial real estate, a stark contrast to past

acquisitions between 2013 to 2018 where they were net buyers of almost 52 billion dollars worth

of properties. A similar trend appears in the residential real estate segment too. In both 2017 and

2018, Chinese buyers purchased over 40,000 U.S. residential properties which were halved in

2019 and steadily declined to only 6,700 in the past year. This turnaround in Chinese investment

can be attributed to a deteriorating relationship between the U.S. and China during the Trump

Presidency, financial distress in China, and new Chinese government regulations prohibiting

outbound investments. Additionally, while Chinese investment is a small share of U.S. real estate

(~1.5% at its peak), it has outsized impacts on market valuations of home prices in U.S. zip

codes with higher populations of foreign-born Chinese, increasing property prices and

exacerbating the issue of housing affordability in these areas. This paper investigates the rapid

growth and decline of Chinese investment in U.S. real estate and its effect on U.S. home prices in

certain demographics.

Keywords: real estate, Chinese investors, housing markets, historical patterns

HISTORICAL PATTERNS AND RECENT IMPACTS 3

Historical Patterns and Recent Impacts of Chinese Investors on U.S. Real Estate

Introduction

*In this paper, the term “Chinese investors” is solely used to describe investors from China*

Today, many of the largest cities in the United States face housing affordability crises, as a

relatively stagnant housing supply fails to uphold the high demand of people wanting to live in

urban cities. Simultaneously, there has been a substantial influx of wealthy home buyers from

overseas investing in the domestic housing markets. Specifically, this paper outlines the behavior

of Chinese buyers in the U.S. real estate market. This demographic has been leading foreign

investments in U.S. homes for the past nine years and the capital flow from China to the U.S. has

shown substantial impacts on American consumers by increasing housing prices in certain

locations and zip codes. The following content of this research paper examines the existing

surrounding theories, problems, and impacts of Chinese investors in U.S. real estate.

Chinese Investor Profile

First, when considering the typical Chinese investor profile, the dominant players are

state-owned enterprises, sovereign wealth funds, banks, and high-net-worth private investors. In

particular, Chinese banks and sovereign wealth funds show a sincere interest in the U.S.

commercial real estate sector. For instance, from 2005 to 2014, the Bank of China made over 35

transactions in U.S. CRE, amassing over $8.4 billion in refinancing and sales, a huge figure in its

timeframe (Mahajan & Sheth, 2014). Likewise, the Chinese Investment Corporation, the largest

sovereign wealth fund in the world with more than $1.3 trillion in assets around the globe, is an

active participant in U.S. CRE through lending and fund vehicles. However, while these original

investors were the makeup and composition of nearly all Chinese investing in the early 2010s,

HISTORICAL PATTERNS AND RECENT IMPACTS 4

the investor profile has diversified since and expanded beyond these original entities with

Chinese regulators opening up international investments to other financial institutions like

insurance companies.

Background

Up until 2010, direct Chinese investment in the U.S. real estate market had been fairly negligible

(Ehrlich, 2022). Yet, within the last decade, Chinese investors have risen to become the lead

foreign buyers of U.S. homes, spurring the question of what drew them to the United States in

particular, especially with similar opportunities available in western countries such as the United

Kingdom (Olick 2021). Furthermore, while Chinese overall investment in foreign real estate

assets has increased across all countries, this decade introduced a major shift in focus to U.S.

investment specifically, from treasury bonds to stocks to venture capital, with real estate having

seen some of the most significant growth (Fung, 2019). Although there is a multitude of reasons

for the redirection of resources to the U.S., the most attractive features of investing in real estate

in the U.S. are detailed below.

Reasons for Investing

One of the motivating factors behind investing in the United States is that it is home to about

three-quarters of the top schools in the world. Because education is deeply ingrained in

traditional Chinese culture, the best universities are highly desirable. In fact, many wealthy

Chinese parents seek a second home in the U.S. so that their children can establish residency to

have easier access in attending elite American colleges. According to a 2012 Hurun Report, one

in four Chinese nationals who are worth more than $16 million have emigrated for this reason

HISTORICAL PATTERNS AND RECENT IMPACTS 5

with another 47 percent considering emigration (Carlson, 2012). A hotspot for this type of

migration is California, where state legislation requires a person to live in the state for only 366

days before they can establish residency and receive benefits for college such as in-state tuition,

a nearby home, and higher acceptance rates among the prestigious public universities like the

University of California, Berkeley or the University of California, Los Angeles, the number one

and two ranked public universities according to U.S. News (“Top Public”, 2022).

Even historically, Chinese home

buyers have largely targeted their efforts on

the U.S. coasts such as New York and

California (both culturally friendly states).

With almost 40% of Chinese real estate

investments concentrated in California and

over a billion dollars invested from 2005 to

2014 (see Fig. 1), California is a

converging hotspot due to its thriving

Chinese community, diversified economy,

and plentiful prestigious academic universities (Passy, 2019). Recently, however, a new wave of

Chinese investors has emerged, looking for real estate opportunities in areas that were never

sought after before, such as properties in the Midwest and Southwest which are home to

distinguished institutions such as the University of Chicago (“5 Reasons”, 2022).

In addition to the vast educational opportunities, an increase in demand for residential

real estate by Chinese buyers can also be attributed real estate investing serving as a viable

option for citizenship. More specifically, the EB-5 visa can be used as a green card for wealthy

HISTORICAL PATTERNS AND RECENT IMPACTS 6

Chinese investors, allowing for a direct path to U.S. citizenship. Under this program, investors

(and their spouses and children under 21) are eligible to apply for a Green Card and permanent

residence if they make the necessary minimum investment of $1,050,000 in a commercial

enterprise in the United States. Furthermore, a 2014 survey conducted by Hurun, a Shanghai

research firm, revealed that approximately 64 percent of Chinese individuals with assets of more

than $1.6 million were either emigrating or planning to do so. By replacing their Chinese assets

with U.S. assets, these individuals can obtain citizenship in just six months with the EB-5 visa,

further highlighting the attractiveness of U.S. citizenship through real estate investing (“Hurun

Report Chinese,” 2014).

Perhaps most important, U.S. real estate is a much more enticing, lucrative, and safer

vehicle to invest in than mainland China. Because Chinese investors primarily purchase in urban

cities, many Chinese and Hong Kong nationals will choose the U.S. because of its cheaper

housing prices compared to the metro areas of other western countries. Foreign investments also

allow for the diversification of assets and avoiding domestic taxes. As for the wealthy Chinese

billionaires, U.S. real estate serves as an outlet to appreciate their already-attained wealth. From

data about foreign tax havens, the International Consortium of Investigative Journalists reported

in 2014 that over 22,000 clients of offshore financial institutions had addresses in China and

Hong Kong, including some of China’s most powerful, rich, and influential men and women

(Walker et al., 2014). The U.S. is particularly desirable for these rich individuals because of its

political stability and the fact that it is one of the fairest and most just countries in the world

(Dogen, 2022). Because of this, the U.S. serves as a safer place to invest in comparison to

China’s sudden-changing policies and volatile environment for investing. For instance, with

China’s one-party political system, Chinese money is susceptible to new policies confiscating

HISTORICAL PATTERNS AND RECENT IMPACTS 7

their wealth. Investors abroad are looking to protect their wealth from the volatility at home and

the U.S. market provides that reassurance. After all, investors need to feel financially secure to

feel rich.

Prestige is another alluring feature evident through past Chinese acquisitions. In 2015,

Anbang Insurance Group Co. paid the highest purchase price ever for a U.S. hotel with its 1.95

billion dollar purchase of the Walford Astoria in New York (Fung, 2019). By investing in

blockbuster deals and acquiring trophy buildings, investors are able to strengthen China’s

prestige and reputation. Other landmarks like the Vista Tower, a nearly $1 billion skyscraper in

Chicago developed by China’s largest commercial property company, Dalian Wanda, and an

eight-acre luxurious housing development project in Beverly Hills are clear demonstrations of

this initiative (Fung, 2019).

Finally, investing across the world in a completely different country is a learning process

for Chinese investors. According to a staff report by the U.S.-China Economic and Security

Review Commission, the acquisition of assets like office buildings and hotels that require a

long-term commitment for rental incomes is viewed as an opportunity to become familiar with

the local tax system, and a foundation for further developments in the future (Koch-Weser &

Ditz, 2015). These larger Chinese investors seek to better understand local markets before

expanding to high-stakes ventures such as greenfield projects and billion-dollar development

projects.

The Prosperity Era

The early 2010s have proved to be an extremely successful period for Chinese investors

in both commercial and residential U.S. real estate. In 2014, China supplanted Canada to become

HISTORICAL PATTERNS AND RECENT IMPACTS 8

the lead foreign investor in the

U.S. real estate market. In the

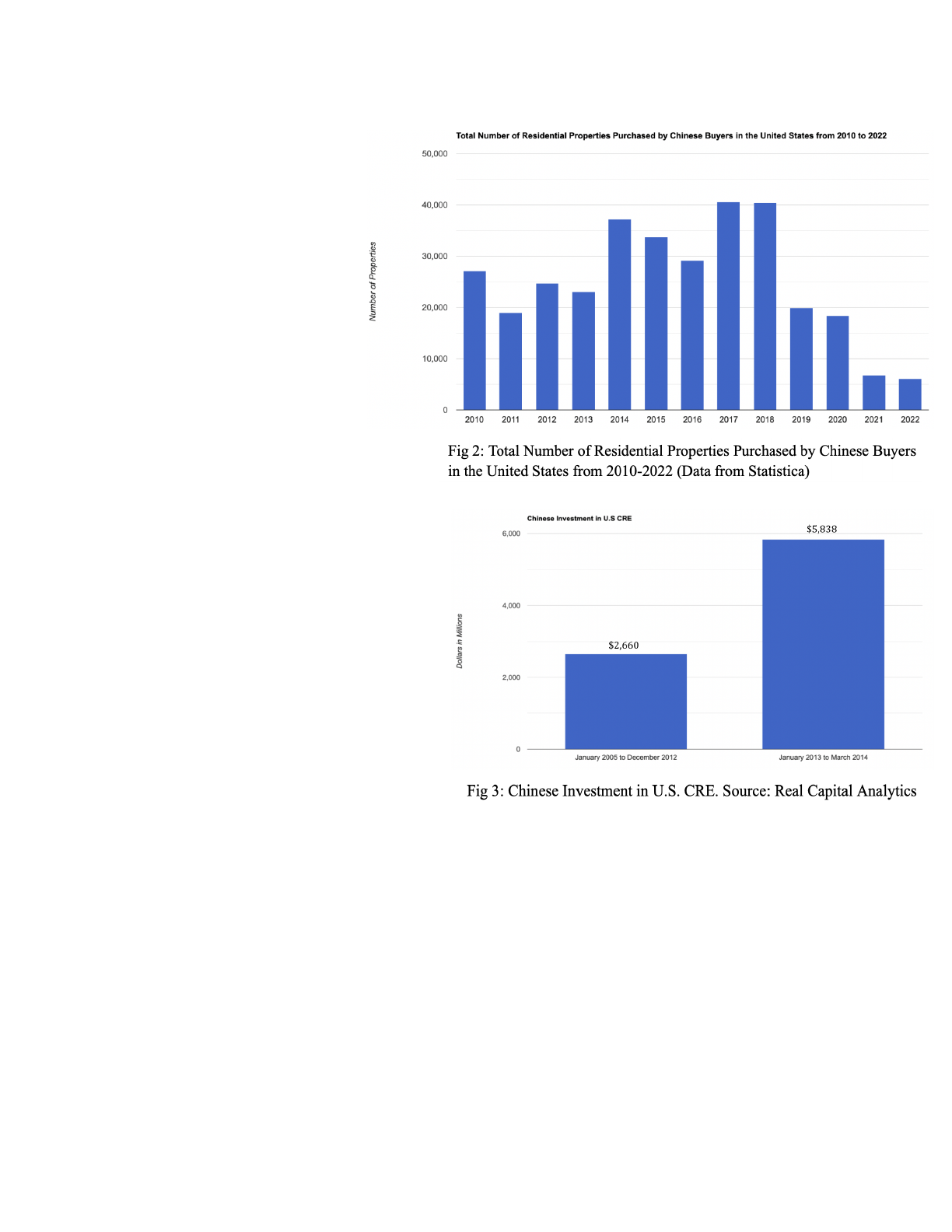

residential sector, from 2013 to

2018, the total number of

properties purchased by the

Chinese nearly doubled from

23,100 to 40,400 (see Fig. 2:

Statistia Research Department,

2022). Additionally, from 2011 to 2016,

Chinese nationals purchased homes valued

at $93 billion, including $28.6 billion in

2015 alone (“Breaking Ground,” 2016).

From the commercial perspective, these

investors have shared an equally

impressive growth where between 2013 to

2018 they were net buyers of almost 52

billion dollars worth of properties (Putzier,

2022). With a peak in commercial investments at $9.3 billion in 2016, the pinnacle represents a

15-fold increase from just six years ago in 2010 (“Breaking Ground,” 2016). In addition, at

approximately $208 billion, China was the biggest foreign holder of U.S.-government-backed

real estate bonds in 2016 (“Breaking Ground,” 2016).

Besides the draws of education, prestige, citizenship, and safe yields in U.S. real estate,

an important factor leading to this era of prosperity was the abundance of lucrative investments

HISTORICAL PATTERNS AND RECENT IMPACTS 9

available after the 2008 housing crash. The real estate market following the crash of 2007-2008

led to spectacular opportunities for individuals with knowledge and access to capital. Higher

inventory and less demand caused deflated property prices, which eventually lead to greater

long-term returns and house appreciations. For example, the average home valuation fell to

$257,000 in 2009, but with an average investor hold of 5 years, the average home valuation

rebounded and jumped to $369,400 (“Average Sales”, 2022). Experienced investors could invest

in a cheap and ripe market and receive a 43% return on investment. Additionally, according to

the latest report from Cohen & Steers, an investment management company with over $56

billion invested in real estate, “superior returns in real estate tend to follow recessionary periods”

(Zhang, 2022). Another reason for this spike in investment is that, until 2012, the Chinese

government prohibited insurance companies from buying foreign property. With these

restrictions uplifted, the Chinese seized their invitation to venture into investments abroad,

flooding Chinese money into U.S. real estate. The Wall Street Journal classified this period as

“the greatest episode of capital flight in history” (Brown, 2016). This pattern of investment

would persist, though not as rapidly, until the end of 2018.

The next year was the first instance where the U.S. real estate market saw a reversal in

behavior and a withdrawal of Chinese investment. Instead of continuing as net buyers of real

estate, investors began selling off their U.S. properties. And although coinciding with the

inception of the coronavirus, surrounding data and statistics reveal that the pandemic was not the

primary factor for this turnaround, at least not directly.

HISTORICAL PATTERNS AND RECENT IMPACTS 10

The Fall

The withdrawal of Chinese investors in U.S. real estate was largely unexpected.

Speculators and industry professionals strongly believed in 2016 that investment would only

continue to flourish to close the decade (Grant, 2016). However, after 2018, purchases dropped

significantly and Chinese investors began to sell more in property valuation than they bought,

becoming net sellers for the first time in the 2010s. Also in 2018, the Beverly Hills Project

bought by the Dalian Wanda Group was sold for only 420 million to a London-based real-estate

firm Cain International and Alagem Capital Group, the exact price the conglomerate paid for the

development back in 2014. Their eagerness to leave the U.S. CRE market was a foreshadowing

of future Chinese companies bailing on U.S real estate after years of acquiring these properties.

According to MSCI Real Assets, these investors sold a net 23.6 billion dollars of U.S. CRE since

2019, while between 2013 to 2018, they were net buyers of almost 52 billion dollars of U.S.

commercial properties (Putzier, 2022).

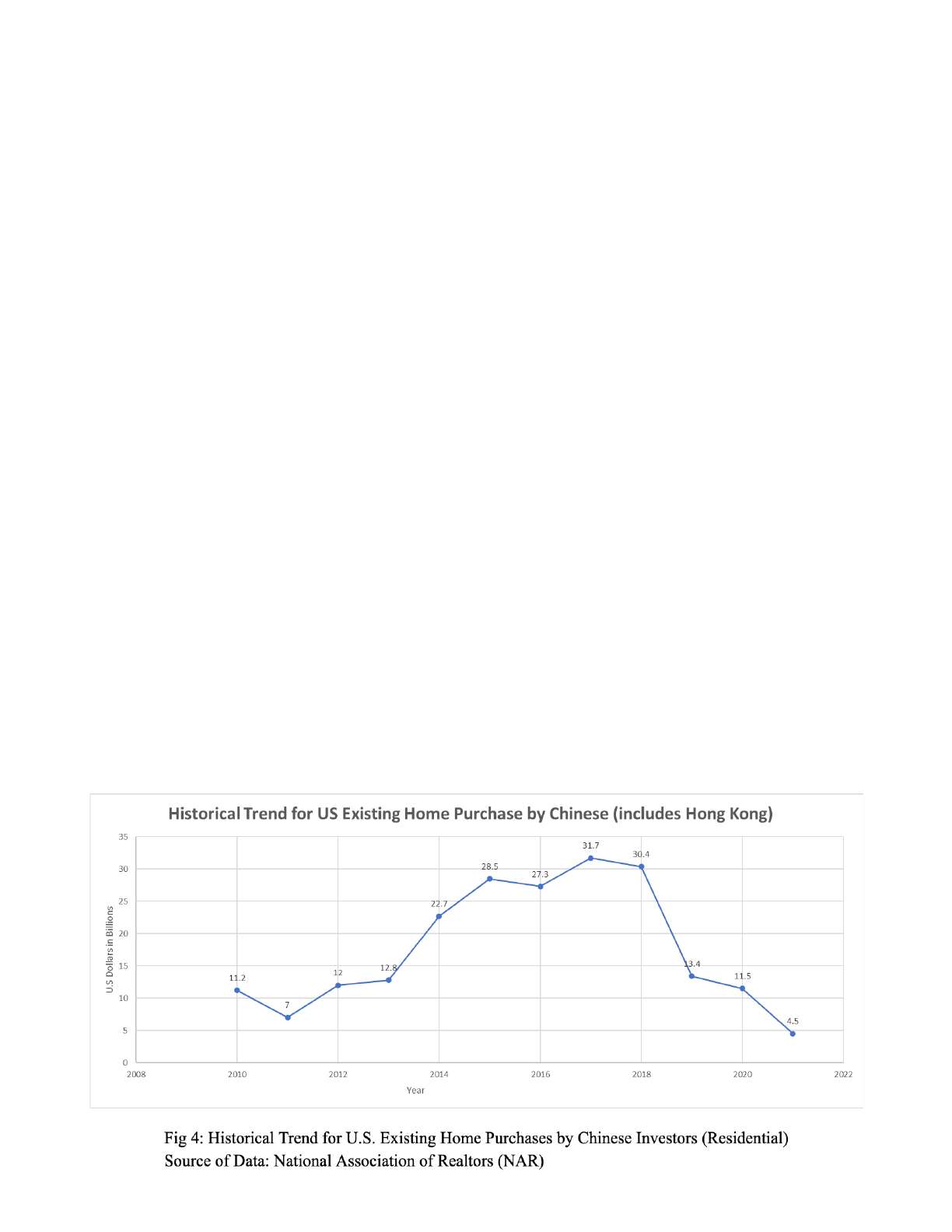

Similarly, a weaker appetite is apparent in residential real estate as well. Research

released by the National Association of Realtors found that the Chinese purchased $17 billion

less on homes in America in 2019, a staggering 56 percent decline within 12 months (see Fig. 4).

HISTORICAL PATTERNS AND RECENT IMPACTS 11

Additionally, in a short two-year window, housing purchases fell from nearly $32 billion in

2016-2017 to only $11.5 billion in 2019 (Keys, 2020). Even as recently as last year, Chinese

buyers only spent a mere $6.1 billion total on both sectors of U.S. real estate, a fraction of what it

had been during the thriving expansion of the early 2010s (Zilber, 2022).

Causes of Withdraw and Selling Behavior

With the pandemic’s inception in 2019, many predictions about real estate went awry. However,

the COVID-19 pandemic may not have been as impactful as many people assume for Chinese

investors beginning to sell off their real estate. The strongest influences for this shifting behavior

are actually restrictive government regulations, a deteriorating relationship with the U.S. during

the trade war, and financial distress for large Chinese corporations and conglomerates.

To begin, in 2016, the Chinese government placed additional hurdles on its citizens.

China began restricting outbound investments, allowing residents to take only $50,000 out of the

country in an attempt to raise the value of the Renminbi, the nation’s currency. Although Chinese

investors were still net buyers at this time, 2016 marked a peak in purchases with the

introduction of legislation like this that prompted years of declining investment in the U.S. that

hasn’t happened since the early 2000s. According to data from Thomson Reuters, China’s

outbound M&A volumes nearly halved in the first six months of 2017 to $64.2 billion following

the crackdown on capital outflows, after Chinese companies spent a record $221 billion on assets

overseas in 2016 (Wu, 2017). Also in 2017, the General Office of the State Council of China

released the “Guiding Opinions for Further Guiding and Regulating the Direction of Outbound

Investments” in which they stated they would prohibit “irrational” investments including foreign

real estate and ban domestic enterprises from participating in outbound investments that

HISTORICAL PATTERNS AND RECENT IMPACTS 12

“endanger or may endanger national interests or national security” (“China’s New Policy”,

2017). Essentially, the Chinese government believed that investment corporations were

overpaying for assets abroad and taking on too much risk, prompting many companies to sell

their assets and holdings. Ultimately, efforts from the Chinese government to stabilize its

currency, reduce debt, and alleviate the country’s economic stagnation have made it much more

difficult to purchase real estate in America.

The drastic shift from buying to selling is also caused by escalating political tensions

between the U.S. and China. A report from the New York Times states, “growing distrust

between the United States and China has slowed the once steady flow of Chinese cash into

America, with Chinese investment plummeting by nearly 90 percent since President Trump took

office” and in the period 2017-2019 (Rappeport, 2019). The falloff of investment stems from

increased regulatory scrutiny by the U.S. and a colder attitude toward Chinese investment

overall. For instance, Neil Brookes, Asia Pacific head of capital partners at Knight Frank,

explained that Chinese outbound capital fell 83% in 12 months from 2018-2019 “largely due to

trade wars and the government trying to stop money leaving the country” (Shao, 2019). The

deterioration of their economic relationship during the trade war has scared businesses in both

countries. From the U.S. perspective, a September 2019 study by Moody’s Analytics found that

the trade war had already cost the U.S. economy nearly 300,000 jobs and an estimated 0.3-0.7%

of real GDP (Hass & Denmark, 2020). A 2019 report from Bloomberg Economics estimated that

the trade war cost the U.S. economy $316 billion at the end of 2020, while more recent research

from the Federal Reserve Bank of New York and Columbia University found that U.S.

companies lost at least $1.7 trillion in the price of their stocks as a result of U.S. tariffs imposed

on imports from China (Hass & Denmark, 2020). China also felt economic pain as a result of the

HISTORICAL PATTERNS AND RECENT IMPACTS 13

trade war with a slowdown in industrial output and economic growth. Furthermore, as the trade

war dragged on, Beijing lowered its tariffs for its other trading partners as it reduced its reliance

on U.S. markets (Hass & Denmark, 2020). With efforts to circumvent one another, it is

unsurprising that Chinese buyer inquiries on U.S. property were down 27.5% from the previous

year and up in Canada, the UK, Australia, and Japan, all of which served as alternative

destinations to invest in real estate to the United States (Shao, 2019). Finally, additional

tightening of borders and restrictions on immigration have made U.S. real estate less hospitable

overall for Chinese investors. A May report from Cushman & Wakefield noted that in 2018,

there were 37 property acquisitions by Chinese buyers worth $2.3 billion, but $3.1 billion of

commercial real estate was sold off (Rappeport, 2019). The report said that the treatment of the

Chinese conglomerate HNA Group and the tough trade talk made Chinese investors feel

unwelcome and discouraged from investing (Rappeport, 2019).

The final reason for the withdrawal was that many Chinese investment companies were

in financial distress and needed quick capital which they could easily acquire by selling their

foreign assets. The timing was ripe for selling too. Investors who bought U.S. commercial

properties a decade ago were still able to make profits by selling in 2019. In conjunction with a

decline in business travel and a weak demand for office buildings, the beginning of the pandemic

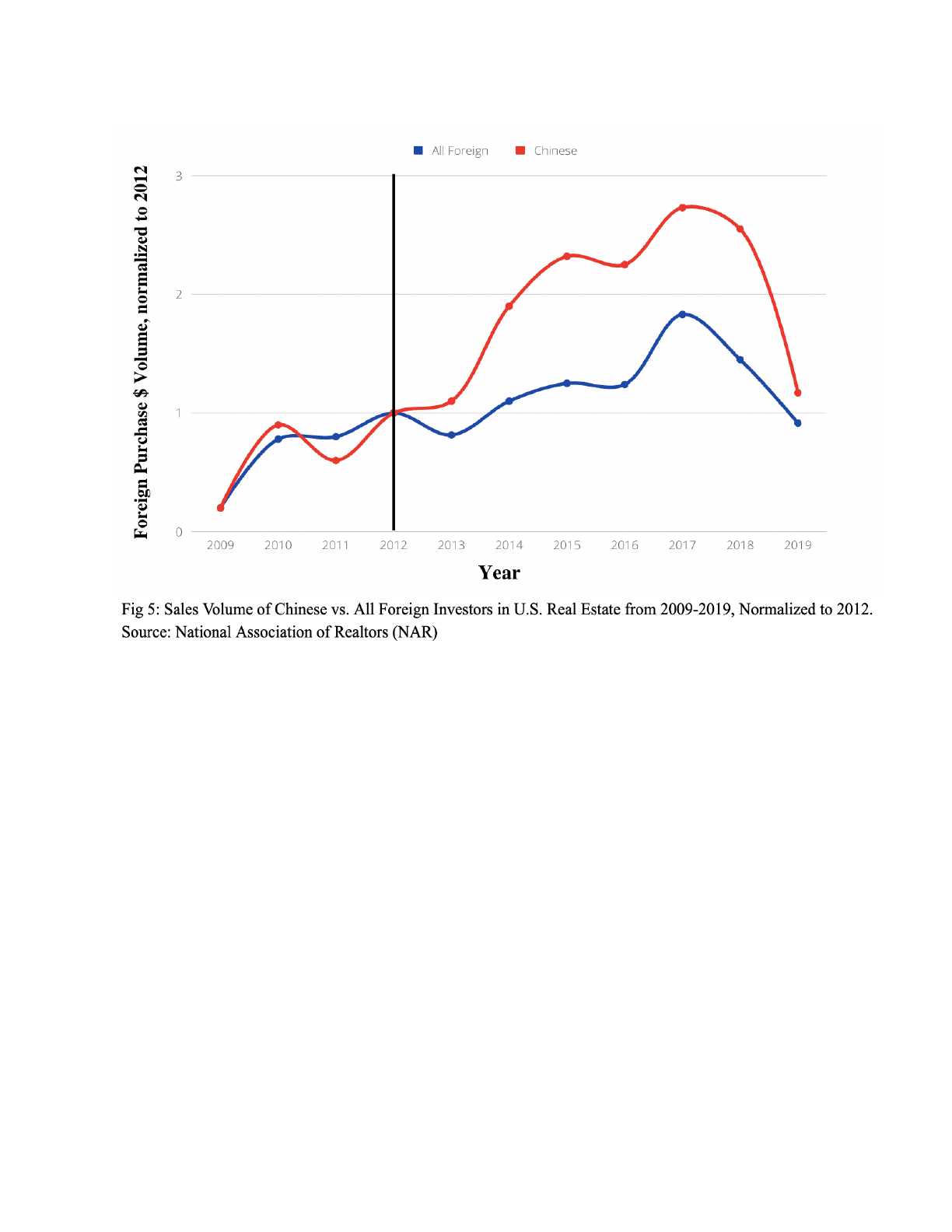

presented the perfect opportunity to sell. But ultimately, it was the combination of all of these

factors that led to a sharp decline in Chinese investment in U.S. real estate, a trend depicted in

Figure 5.

HISTORICAL PATTERNS AND RECENT IMPACTS 14

Implications of Recent Behavior and Impact on Certain U.S. Homes

So far, this paper has outlined the motivations and reasons for the turnaround of Chinese

investment and the appealing factors for why they chose to invest in the U.S. initially. However,

it is equally as important to acknowledge the implications of their recent behavior on the prices

of U.S. properties. Essentially, what was the effect of the flooding of Chinese money on the U.S.

real estate sector? Interestingly, while Chinese money always was a really small share of the U.S.

real estate market even at its peak (around 1.5%), it had outsized impacts on price valuations in

large U.S. cities and in the popular sites of California (“International Transactions”, 2022).

Because Chinese companies would often buy the most expensive hotels and office buildings in

the most expensive cities (like New York and Los Angeles), they would pay incredibly high

HISTORICAL PATTERNS AND RECENT IMPACTS 15

prices which then became benchmarks for other buildings. In this way, Chinese money had

inflated real estate values for a long time. With its removal, the prices of surrounding buildings

have fallen back down (“Spotlight on China”, 2022).

Additionally, research from Wharton professor Benjamin Keys suggests that Chinese

investors also have a significant impact on housing prices in locations with high foreign-born

Chinese ethnic people. According to the findings in their research paper titled “Global Capital

and local Assets: House Prices, Quantities, and Elasticities”, housing prices grew 8 percent more

in zip codes with high foreign-born Chinese populations from 2012 to 2018 (Gorback & Keys,

2020). Another study titled “Capital Flows, Asset Prices, and the Real Economy: A "China

Shock" in the U.S. Real Estate Market” further supports the notion that foreign Chinese

investments have a significant effect on local housing and labor markets. The study found that a

one standard deviation increase in exposure to these purchases explains 24% and 18% of the

cross-ZIP-code variation in local house prices, exacerbating the current worries about housing

affordability and driving out lower-income residents (Li et al., 2020). Additionally, a 1% increase

in housing demand by foreign Chinese, increased local home prices by 0.099% and 0.173%,

respectively (Li et al., 2020). In regards to driving out local low-income residents, they found a

slightly negative relationship between foreign Chinese housing transactions and the number of

tax filings, suggesting that foreign Chinese house purchases drive out local residents on the net.

They concluded that a 1% increase in foreign Chinese housing demand, as measured by

transaction value and count, decreases the number of tax filings by 0.04% and 0.07%,

respectively (Li et al., 2020). Finally, research conducted by Iacob Koch-Weser and Garland Ditz

found that by buying homes chiefly for investment purposes, Chinese buyers can worsen housing

bubbles (Koch-Weser & Ditz, 2015). For example, in San Francisco, the real estate cycles are

HISTORICAL PATTERNS AND RECENT IMPACTS 16

between five to seven years. The current increase in prices from Chinese investment activity that

are only three years old could last for another several years, again making housing less

affordable for lower-income citizens in the area (Koch-Weser & Ditz, 2015).

Future and Long-Term Effects

While investment from China has rapidly declined in recent years, the outlook for the

U.S. real estate market in 2022 is still very positive. Because Chinese money encompasses such a

small portion of U.S. real estate, it has minimal influence on the sector as a whole. Demand

remains strong in this inflationary environment, which commercial real estate has the ability to

hedge against. Furthermore, a retreat by Chinese buyers could actually be good news for

Americans looking to purchase a home, especially in the expensive markets in California, where

its popularity had garnered a double-digit property appreciation. Ultimately, the lack of

competition from foreign buyers, who typically invest with competitive all-cash offers, has

resulted in better deals on homes for local buyers. This effect has been exemplified in the first

half of 2019 in Irvine, where the median home sale price fell from $834,000 to $820,000

according to Zillow (Zhang, 2019). Additionally, in recent years leading up to 2019, Chinese

investors made up about half of all home purchases in the city, but that share has fallen to about

36% in 2019 (Zhang, 2019). Although not solely the cause, the withdrawal of Chinese

investment in Irvine was an important factor contributing to the drop in median home sale prices

in California where house appreciation is rapid and constant.

However, the future for Chinese investors is not quite as certain. Because of government

policy reducing funding available to developers, China’s housing market began experiencing a

real estate crisis in 2021. The property slump has persisted for over a year due to a weak

HISTORICAL PATTERNS AND RECENT IMPACTS 17

economy and strict COVID-19 regulations discouraging buyers. According to a survey in

October 2022 by China Index Academy, a top real estate research firm, the sales of the 100

biggest Chinese real estate developers dropped by 43% since 2021 (He, 2022). Simultaneous in

October, however, are recent indicators that point to a more positive turn of events. According to

brokerage Cinda Securities Co. Ltd., China’s housing market has shown signs of stabilizing

(Cheng, 2022). The Chinese government financed more than 1 trillion RMB to promote

investment and implemented regulations to remove administrative friction, encourage

international investment, lower home purchase costs, and boost rational demand in China

(Cheng, 2022).

Conclusion

This research paper outlined the two-sided story of Chinese investment in U.S. real

estate. The real estate crash of 2008 was a warm welcome to foreign investment which the

Chinese capitalized on, investing in search of political stability, diversification, and prestige.

Then, following a half-decade window of prosperity, 2019 experienced a turnaround of behavior

where investors became net sellers, a stark contrast to tens of billions of dollars in acquisitions

between 2013 to 2018 (Statistia Research Department, 2022). This reversal is attributed to the

combined factors of a deteriorating political relationship between the U.S. and China, financial

distress in China, and government regulations on investment. And finally, this paper discussed

the impacts of Chinese investment on certain U.S. properties. In major cities, landmark

purchases from Chinese corporations inflated nearby office building valuations. In locations with

high foreign-born Chinese populations, high degrees of foreign investment raised local housing

prices and intensified concerns over housing affordability with already expensive rents in

HISTORICAL PATTERNS AND RECENT IMPACTS 18

California. Should Chinese investment in U.S. real estate rebound, further research should

investigate how effective government regulation can limit the inflow of Chinese capital, and thus

reduce the volatility of housing prices in areas significantly impacted by Chinese investment.

HISTORICAL PATTERNS AND RECENT IMPACTS 19

References

Barcelona, William, Nathan Converse, and Anna Wong (2021). “U.S. Housing as a Global Safe

Asset: Evidence from China Shocks,” International Finance Discussion Papers 1332.

Washington: Board of Governors of the Federal Reserve System,

https://doi.org/10.17016/IFDP.2021.1332.

Breaking Ground: Chinese Investment in U.S. Real Estate - Northern California | US-China

Institute. (n.d.). Retrieved October 30, 2022, from

https://china.usc.edu/calendar/breaking-ground-chinese-investment-us-real-estate-norther

n-california

Cheng, E. (2022, October 25). Why China won’t bail out its real estate sector. CNBC.

https://www.cnbc.com/2022/10/25/china-property-why-beijing-wont-bail-out-its-real-esta

te-sector.html

China’s new policy on outbound investment. (n.d.). Buren Legal Tax Notary.

https://www.burenlegal.com/en/news/chinas-new-policy-outbound-investment

Chinese Investment in U.S. Commercial Real Estate: Everything You Need to Know. (2021,

October 1). ProspectNow.

https://www.prospectnow.com/2021/10/01/chinese-investment-in-u-s-commercial-real-est

ate-everything-you-need-to-know/

Denmark, R. H. A. A. (2022, March 9). More pain than gain: How the US-China trade war hurt

America. Brookings.

https://www.brookings.edu/blog/order-from-chaos/2020/08/07/more-pain-than-gain-how-

the-us-china-trade-war-hurt-america/

HISTORICAL PATTERNS AND RECENT IMPACTS 20

Franklin Templeton Investments. (2022, January 5). A Tale Of Two Real Estate Markets: U.S.

And China. SeekingAlpha.

https://seekingalpha.com/article/4478060-a-tale-of-two-real-estate-markets-us-and-china

FRED Economic Data. (2022, October 26). https://fred.stlouisfed.org/series/ASPUS

Fung, E. (2019, January 29). Chinese Exiting U.S. Real Estate as Beijing Directs Money Back to

Shore Up Economy. WSJ.

https://www.wsj.com/articles/chinese-exiting-u-s-real-estate-as-beijing-directs-money-ba

ck-to-shore-up-economy-11548757800

Grant, P. (2016, May 25). Chinese Investors Pour Money Into U.S. Property. WSJ.

https://www.wsj.com/articles/chinese-investors-pour-money-into-u-s-property-14641106

82

Guevara, M. W. (2021, July 9). Leaked Records Reveal Offshore Holdings of China’s Elite. ICIJ.

https://www.icij.org/investigations/offshore/leaked-records-reveal-offshore-holdings-of-c

hinas-elite/

He, L. (2022, November 14). China’s real estate crisis could be over. Property stocks are

soaring. CNN.

https://edition.cnn.com/2022/11/14/investing/china-real-estate-crisis-over-rescue-plan-intl

-hnk/index.html

International Transactions in U.S. Residential. (2017, July 18). www.nar.realtor.

https://www.nar.realtor/research-and-statistics/research-reports/international-transactions-

in-u-s-residential-real-estate

Journal, T. W. S. (2022, September 21). Chinese Firms Flee U.S. Commercial Real-Estate

Market - The Wall Street Journal Google Your News Update - WSJ Podcasts. WSJ.

HISTORICAL PATTERNS AND RECENT IMPACTS 21

https://www.wsj.com/podcasts/google-news-update/chinese-firms-flee-us-commercial-rea

l-estate-market/10ada6b2-b4d8-4baf-bf5d-371cfa2adb5c

Koch-Weser, I., & Ditz, G. (2015). Chinese Investment in the United States: Recent Trends in

Real Estate, Industry, and Investment Promotion. CreateSpace Independent Publishing

Platform.

Li, Zhimin, Leslie Sheng Shen and Calvin Zhang (2020). Capital Flows, Asset Prices, and the

Real Economy: A "China Shock" in the U.S. Real Estate Market. International Finance

Discussion Papers 1286.

Lueckemeyer, O. (2022, September 20). Chinese Investors Sell Off Nearly >4B In U.S. Real

Estate As Values Of Trophy Properties Fall. Bisnow.

https://www.bisnow.com/national/news/capital-markets/chinese-investors-sell-off-nearly-

24b-worth-of-us-real-estate-as-values-of-trophy-properties-fall-115494

Mahajan, S., & Sheth, S. (2014). Chinese investment in U.S. real estate Collaborate and benefit.

https://www2.deloitte.com/content/dam/Deloitte/us/Documents/financial-services/us-fsi-c

hinese-investment-in-US-real-estate-051614.pdf

Passy, J. (2019, May 16). The Chinese purchase more U.S. residential real estate than buyers

from any other foreign country, but Trump’s trade war may change that. MarketWatch.

https://www.marketwatch.com/story/chinese-investors-buy-more-us-residential-real-estat

e-than-any-other-country-but-trumps-trade-war-could-soon-end-that-2019-05-15

Putzier, K. (2022, September 20). Chinese Firms Flee U.S. Commercial Real-Estate Market

After Big Property Bets Sour. WSJ.

https://www.wsj.com/articles/chinese-firms-flee-u-s-commercial-real-estate-market-after-

big-property-bets-sour-11663622573

HISTORICAL PATTERNS AND RECENT IMPACTS 22

Rappeport, A. (2019, July 29). Chinese Money in the U.S. Dries Up as Trade War Drags On. The

New York Times.

https://www.nytimes.com/2019/07/21/us/politics/china-investment-trade-war.html

Reyes, C. B., & Reyes, C. B. (n.d.). China’s looming real estate crisis casts a shadow in

California | firsttuesday Journal. Retrieved October 30, 2022, from

https://journal.firsttuesday.us/chinas-looming-real-estate-crisis-casts-a-shadow-here-in-ca

lifornia-too/80252/

Dogen, S. (2022, August 21). Foreign Real Estate Investors Are Coming To Buy Up American

Homes. Financial Samurai.

https://www.financialsamurai.com/foreign-real-estate-investors-to-buy-up-american-hom

es/

Shao, G. (2019, June 26). The trade war is weighing on Chinese home buying in the US. CNBC.

https://www.cnbc.com/2019/06/26/the-trade-war-is-weighing-on-chinese-home-buying-in

-the-us.html

Spotlight on China. (2022, September 23). 3 reasons Chinese investors busy selling off their US

real estate. YouTube. https://www.youtube.com/watch?v=KM1I9bTbjoM

Staff, K. A. W. (2020, September 1). How Foreign Purchases of U.S. Homes Impact Prices and

Supply. Knowledge at Wharton.

https://knowledge.wharton.upenn.edu/article/foreign-purchases-u-s-homes-impact-prices-

supply/

Statista. (2022, October 27). Total number of residential properties bought by Chinese buyers in

the U.S. 2010-22.

HISTORICAL PATTERNS AND RECENT IMPACTS 23

https://www.statista.com/statistics/611020/total-number-of-properties-purchased-by-chine

se-buyers-in-the-us/

The Edge - Vol 2 2019. (2019, May 15). Issuu.

https://issuu.com/cw-red/docs/cw_the_edge_vol2_2019

Why Chinese immigrants choose America. (2012, December 21). The World From PRX.

https://theworld.org/stories/2012-12-21/why-chinese-immigrants-choose-america

Wu, K. S. C. (2017, August 4). Exclusive: China regulators plan to crack down further on

overseas deals. U.S.

https://www.reuters.com/article/us-china-conglomerates/exclusive-china-regulators-plan-t

o-crack-down-further-on-overseas-deals-idUSKBN1AK195

Zhang, H. (2022, September 28). The Best Real Estate Returns Come After Recessions.

Institutional Investor.

https://www.institutionalinvestor.com/article/b1zzgchpx627kz/The-Best-Real-Estate-Retu

rns-Come-After-Recessions

Zhang, Y. U. T. (2019, August 26). Chinese buyers pull back from U.S. housing market, hurting

home sales. USA TODAY.

https://eu.usatoday.com/story/money/2019/08/23/homes-sale-chinese-investors-purchasin

g-fewer-u-s-houses/1960142001/

Zilber, A. (2022, July 20). Chinese spent $6.1B on US real estate last year. New York Post.

https://nypost.com/2022/07/20/chinese-buyers-spent-record-6-1b-on-us-real-estate-in-202

1/

HISTORICAL PATTERNS AND RECENT IMPACTS 24