Wealth Optimization for Professional

Athletes and Entertainers

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

2 Table of contents

Investing involves risk. There is always the potential of losing money when you invest in securities.

Asset allocation, diversification, and rebalancing do not ensure a profit or protect against loss in declining markets.

Merrill, its affiliates, and financial advisors do not provide legal, tax, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”) makes available certain investment products sponsored, managed, distributed or provided

by companies that are affiliates of Bank of America Corporation (“BofA Corp.”). MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC and a wholly owned

subsidiary of BofA Corp.

Trust, fiduciary, and investment management services are provided by Bank of America, N.A. and its agents, Member FDIC. Insurance and annuity products are offered through Merrill

Lynch Life Agency Inc. (“MLLA”), a licensed insurance agency. Bank of America, N.A., and MLLA are wholly owned subsidiaries of BofA Corp.

Banking products are provided by Bank of America, N.A. and affiliated banks, Members FDIC and wholly owned subsidiaries of Bank of America Corporation.

Investment products offered through MLPF&S and insurance and annuity products offered through MLLA:

Are Not FDIC Insured Are Not Bank Guaranteed May Lose Value

Are Not Deposits

Are Not Insured by Any Federal

Government Agency

Are Not a Condition to Any

Banking Service or Activity

Table of Contents

Powerful ways Merrill can help 3

Sophisticated strategies designed with you in mind 4

“Thank you” trap 5

Are your current advisors up to it? 6

Checklist for selecting or retaining a wealth advisor 6

A focus on financial education 7

A difference in planning approaches 8

Tips for rookies and fledgling entertainers 10

Advanced planning for elite athletes and A-list entertainers 14

•

•

•

Estate tax considerations 14

Philanthropic goals 15

Asset protection strategies 17

Conclusion 19

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

3Table of contents

Congratulations! Your countless hours of hard work and personal sacrifices

have paid off. Using the unique skills you developed along the way, you are

now among an elite group of individuals who can practice their sport or cra

as a paid athlete or entertainment professional.

The physical and emotional skills that you used to build your career and

create your wealth are very different from the financial skills that are needed

to help preserve and grow it. Every financial decision you make today will

affect you and your family’s future.

Just as your professional career has started, so has your wealth building

j

ourney. This means creating a wealth management strategy that will

allow you to live the life you have always wanted and pass wealth down to

the heirs and charities of your choosing. Your Merrill advisor will help you

with these decisions by delivering cutting-edge wealth planning advice and

investment strategies, helping to keep you on track as you focus on your

profession and your future.

Powerful ways Merrill can help

We recognize that you are a sports and entertainment “business enterprise.”* Like a chief

executive officer or president of a well-run company, you will need to delegate critical tasks

to trusted individuals so that you can concentrate on other things — like winning the next

game, writing the next song or rehearsing for the next performance.

Successful businesses typically deploy teams of experts to handle complex tasks like

i

nvestments, taxes, insurance, lending/banking needs and reporting obligations. This is so

each employee can contribute their expertise to the business to help make it as successful

as possible. As the CEO of your “business,” think about how you can bring in the right people

for the right tasks.

By working with your Merrill advisor, you’ll have access to the full breadth of our global

guidance, services and solutions through a single point of contact. Your Merrill advisor will

use the latest technology, in-depth research and cutting-edge tools to create and help

manage a comprehensive wealth management plan tailored specifically for you and your

family. The more we can do for you, the more you can concentrate on your sport or cra —

and personal life.

* The use of the term “entertainers” in this paper is meant to describe a broad spectrum of talent, including, but not limited to:

actors, artists, choreographers, comedians, dancers, designers, directors, magicians, musicians, producers, screenwriters, singers,

songwriters and writers.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

4 Table of contents

Sophisticated strategies designed with you in mind

Focusing on you

• Goals-based wealth management

1

• Investment management

1

• Financial statement (budgeting/

forecasting) reporting

1

• Online account access, bill pay

and fund transfer

1

• Lifestyle financing

(such as planes, yachts,

art & collectibles)

2

Leaving a philanthropic

legacy

• Donor advised funds

2

• Charitable planning

1

• Charitable trusts:

2

Cha

ritable lead trusts &

Charitable remainder trusts

2

• Private foundations

1

• Giing strategies

1

Investing towards

your goals

• Core equity & fixed

income portfolios

1

• Private placements

1

• Hedge funds

1

• Alternative investments

1

• Concentrated stock

1

• Retirement strategies

1

Accessing cash when

you need it from

Bank of America

2

• Major asset financing

• Home financing solutions

• Loan-based diversification

strate

gies

• Credit cards

• Custom credit solutions

Passing on wealth efficiently

• Personal trust services

2

• Life insurance trusts

2

• Estate settlement and administration

2

• Family wealth education & governance

1

• Family office solutions

4

Navigating risk

• Portfolio risk management

strategies

1

• Property & casualty

insurance reviews

1

• Life insurance trusts

2

• Wealth replacement trusts

2

• Asset preservation strategies

1

1

Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”) makes available certain investment products sponsored, managed, distributed or provided by companies

that are affiliates of Bank of America Corporation (“BofA Corp.”). MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC and a wholly owned subsidiary of BofA Corp.

2

Banking, mortgage and home equity products offered by Bank of America, N.A., and affiliated banks, Members FDIC and wholly owned subsidiaries of Bank of America Corporation.

3

Merrill Lynch Life Agency Inc. (“MLLA”) is a licensed insurance agency and wholly owned subsidiary of BofA Corp. Insurance and annuity products are offered through MLLA, a licensed insurance agency.

4

Merrill Family Office Services are offered through Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”). In connection with its Family Office Services,

Merrill is not acting in the capacity as a broker-dealer, nor as a registered investment adviser. Accordingly, through its Family Office Services, Merrill is not offering, and its clients are not paying

for, advice with respect to securities, the purchase or sale of securities, or the valuation thereof, nor do Merrill’s Family Office Services encompass financial planning, discretionary account

management, or any other securities-related accounts, products or services. Merrill offers a broad array of brokerage and investment advisory accounts, products and services through other

parts of its business outside of Family Office Services, which are subject to separate agreements, disclosures, and fee arrangements, and may be procured by applying or enrolling and contracting

through those other business channels. Please contact your Financial Advisor or Private Wealth Advisor with questions regarding Merrill’s brokerage or investment advisory offerings.

Managing the impact of taxes

• Insurance planning & services

3

• Tax loss harvesting strategies

1

• Philanthropic giving

2

• Income deferral strategies

1

You, your

family and

your legacy

Global Investments

Bank of

America Cash

Management,

Liquidity &

Lending

Strategies for Business

Owners

Wealth

Planning

Your Merrill advisor can provide access to a range of financial offerings. However, we know that you don’t need

everything listed here all at once. Your Merrill advisor, at the forefront of their advice, will work with you to

assess what you need and when you need it.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

5Table of contents

“Thank you” trap

We recognize that you didn’t do it alone — that you’re most likely where you are today

because of the support of so many wonderful individuals. However, unless those

people possess certain specialized skills, licenses and experience, you should avoid

the temptation to fill certain financial roles with family members and friends as a

way to thank them for their support. Unfortunately, assigning key money-related roles

to family members and friends has been known to produce improper oversight, fraud,

conflicts of interest, self-dealing and personal biases into the decision-making process.

Using a team of licensed financial professionals like our advisors at Merrill can help

you identify and reduce or eliminate these risks.

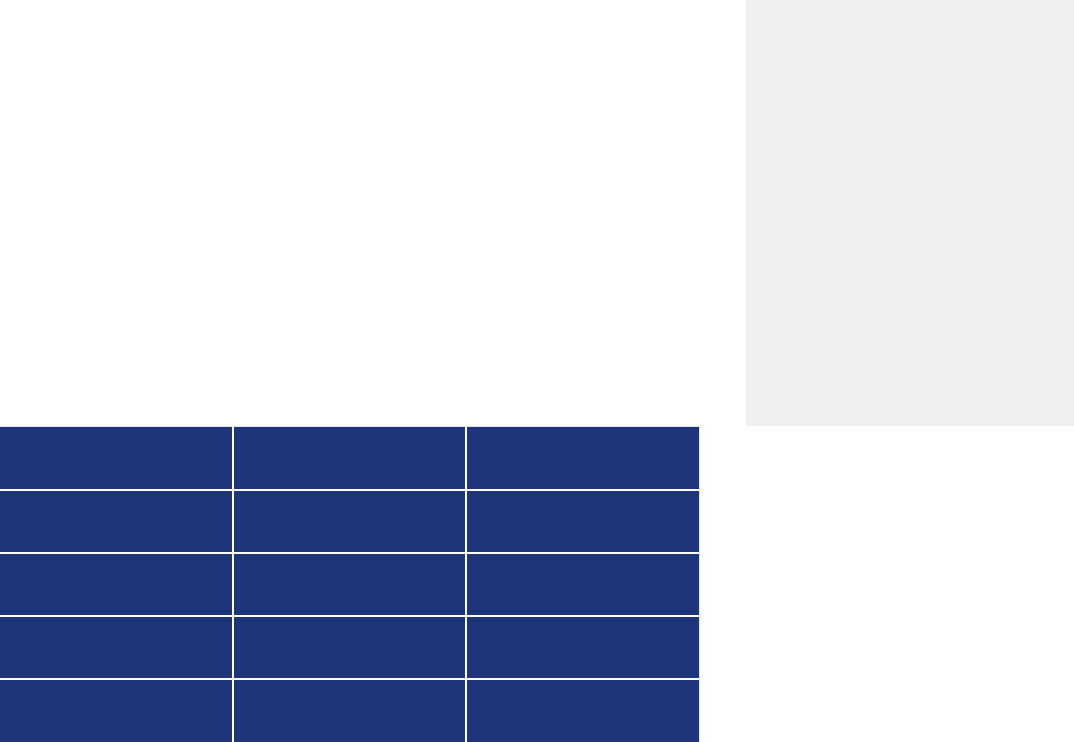

Selecting Merrill vs. Family/Friends Professional

Family/

Friend

Subject to personal biases No Yes

Compensated Yes Yes

Serving as wealth manager is their "professional calling" Yes No

Vast resources/worldwide footprint Yes No

Experience serving clients in the sports and

entertainment industry

Yes Likely no

Access to investment, philanthropy,

lending and trust

planning services through a single point of contact

Yes No

Held to highest fiduciary standards under the law Yes Yes

Permanence — life span is multi-generational

and perpetual

Yes No

Subject to government oversight and recurring

internal audits

Yes No

Expert in investment reporting Yes No

Available any business day of the year Yes No

Teams of support staff Yes No

Our team of licensed

financial professionals

at Merrill can help

you with long-term

wealth management

strategies for both

your professional and

personal career.

“

“

Greg McGauley,

Managing Director

Head of Merrill Private

Wealth Management

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

6 Table of contents

Are your current advisors up to it?

Checklist for selecting or retaining a

wealth advisor

*

Once anyone begins to enjoy a certain amount of financial success, the complexities

that can swirl around financial decisions can be overwhelming. That’s because for

most people who did not grow up wealthy, the issues that higher levels of wealth

present are completely novel — not only to the individual making the money, but

oen to their current advisors, whose skill level or experience falls short of their

clients’ new wealth.

Athletes and entertainers have unique planning issues. They need access to

wealth advisory firms, like Merrill, that can provide access to specialists in many

different disciplines (as highlighted on page 4).

Is your advisor someone who

can adequately educate you

and your family?

What is the range of services

provided by your advisor?

How many (and what

types of) clients does your

advisor serve?

How does the advisor charge

for services?

Has the advisor asked about

the purpose of your wealth?

Who is on the advisor’s

team, and what is their level

of experience?

* A Guide to Navigating Newly Created Wealth, Merrill’s Center for Family Wealth™ (2023).

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

7Table of contents

A focus on financial education

A common thread that exists for many sports and entertainment professionals

is their general unfamiliarity with investment management, tax planning, asset

preservation and estate planning. This is quite normal given that they have likely been

focusing most of their time and effort on becoming successful in their fields.

However, as you start making money and accumulating wealth, it is critical for you

to acquire some basic financial skills — to understand the planning issues that may

have a meaningful impact on your family’s standard of living both now and in the

future. It’s important to build a good foundation to understand how your money

works best for you.

To assist you in getting up to speed and staying abreast of what matters most in

your financial life, Merrill has a vast library of educational tools at your disposal,

including: videos, checklists, calculators, assessment tools and a wide array of digital

content and resources.

Snoop Dogg

“

I

f you stop at

general math,

you’re only going

to make general

math money.

“

Resources for you

• Ongoing, timely Bank of America

Chief Investment Office (CIO)

Market Updates

• Extensive global research

1

on a wide

variety of economic, investment

and tax law change considerations

• Topical wealth planning whitepapers

(Retirement, Divorce, Life Insurance,

Family Governance, Art &

Collectibles, Private Foundations,

Education Funding, Exit Planning

for Private Business Owners,

Non-Fungible Tokens, Hedge

Fund Strategies & Alternative

Investments and more)

• Topical investment whitepapers

(Investment Trends, Portfolio

Strategies, Today’s Market,

Finances and more)

• National client calls

• Topical client seminars

• Financial education “boot camps”

(skill-building & peer-sharing) in

partnership with top universities like

Wharton, Georgetown and UCLA

• Customized training based on a

family’s need or request

See back page for additional disclosures.

Source: U.S. News, November 17, 2009.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

8 Table of contents

A difference in planning approaches

Athletes

According to the U.S. Bureau of Labor Statistics,* there are approximately 17,000

professional athletes in the United States. The majority of these athletes do not hold

second jobs: Their sports activities are their sole source of income. Most professional

athletes are between 20–30 years old, with careers that only last from 3.5 to 9.5 years.

Most of their income is earned in the middle and latter parts of their careers. To make

planning even more challenging, an athlete’s income cannot be fully counted on

because it is oen subject to interruptions and/or reductions — due to injuries, poor

performance, on-the-field and off-the-field personal conduct clauses, lockouts and salary

caps. These inherent risks should be factored into every professional athlete’s planning.

Compared to other professionals, an athlete’s earnings are highly concentrated among a few

short years in the early part of their lives. Therefore, the greatest challenge for any athlete

is how to build enough wealth during their career to continue their lifestyle aer retirement.

Since most athletes retire by the time they are 30, they should draw up financial plans

(in theory) that are designed to make their savings last for another 50 years — taking

into account the various opportunities to earn money aer retiring from their sport.

Because athletes finish their professional careers comparatively early in their life

span, many transition into second full-time careers. For some athletes, these second

careers are directly related to what they did as professional athletes (for example,

coaching or sports analyst) — while in other cases, their second careers have nothing

to do with their sport (such as a restaurateur, politician or real estate developer).

Professional athletes in U.S.

17,000

Age

20–30 years old

Career lifespan

3.5–9.5 years

While athletes and entertainers share many of the same challenges when managing their wealth and personal

careers, there are usually stark differences between these groups regarding timing and sources of income.

Your advisor will consider these differences when helping you build a customized strategy.

Jameel McClain of the Baltimore Ravens

“

It’s always going to be a challenge to tell someone, ‘The moment you get in, you

should be thinking about getting out of it.’ I don’t want to doubt anybody’s drive or

ability, but I want to give them the reality and make it a little less harsh.

“

Source: Baltimoresun.com, Sept. 13, 2019.

* Source: U.S Bureau of Labor Statistics, April 18, 2022.

Source: U.S Bureau of Labor Statistics, April 18, 2022.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

9Table of contents

* Source: Artists and Other Cultural Workers: A Statistical Portrait, National Endowment for the Arts, April 2019.

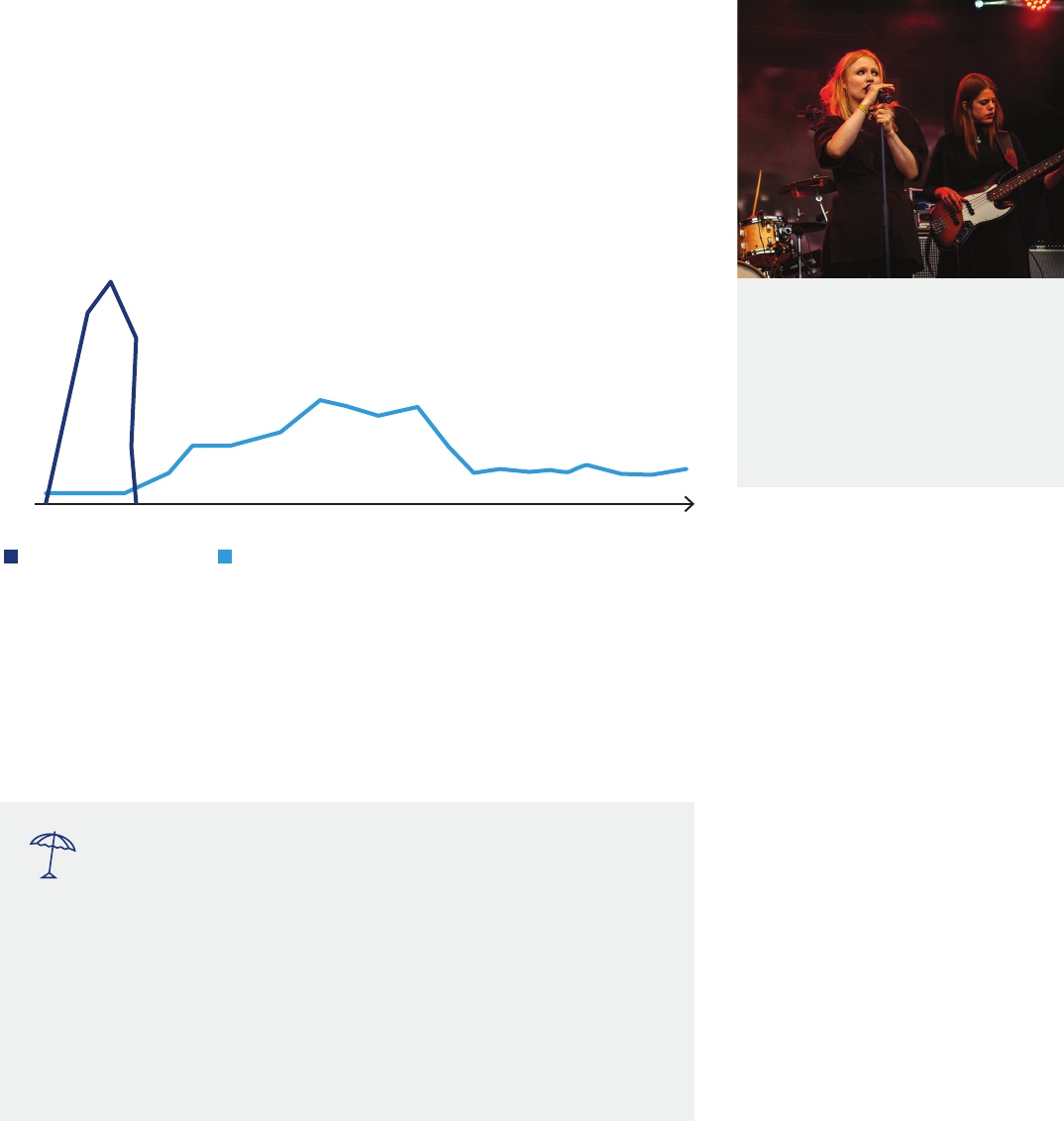

Entertainers

According to the National Foundation for the Arts,* there are approximately 2.5

million entertainers in the United States. Most of these entertainers have a second

job. They usually have modest incomes from their cras in the early years, and tend

to earn and save more in later years. Compared to professional athletes, entertainers

tend to have longer careers, oen spanning decades. But unlike athletes, their

earnings tend to be sporadic — and come mostly in the latter part of their careers.

It is never too early in your professional career to think about what comes next.

Putting together a succession plan now can help alleviate some of the fear and

anxiety that may arise when you voluntarily or involuntarily stop doing the only thing

you’ve done for most of your life.

Earnings profile over time

Chart is for illustrative purposes only.

Professional athletes Entertainers

$

10 YR 20 YR0 30 YR 40 YR 50 YR

Entertainers in U.S.

2.5 million

Career lifespan

Decades

Source: Artists and Other Cultural Workers: A Statistical

Portrait, National Endowment for the Arts, April 2019.

Many athletes and entertainers embark on a second career aer their playing

days or gigs come to an end. While these individuals may adjust to another

career in the same industry, others move on to an entirely different business.

However, these second careers likely will not have the same income stream as

their first careers. Working with a Merrill advisor will help you plan accordingly

for a second career and offer asset preservation strategies to help make your

wealth last as long as possible.

2nd Career: Retirement

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

10 Table of contents

Tips for rookies and fledgling entertainers

Assemble a team of qualified professionals

A successful team or group includes a variety of people who are experts in their chosen

fields, working together toward a common goal. Your financial advisors should operate in

the same way in supporting your goals. For example, when purchasing life insurance, it is

oen necessary to engage a trust and estate lawyer, insurance specialist, trust company

specialist and financial planner. This team can assist you with determining the size and type

of the policy, the best carrier and policy for your stated goals, and the most tax-efficient

way to own and administer the policy. So when you pull together trusted persons to rely

upon, we suggest you build a deep bench of professionals that also includes:

CPA Financial advisor

Investment

manager

Trusts and

estates lawyer

Life insurance

specialist

Property and casualty

insurance specialist

The importance of a budget

The number of professional athletes in the U.S. who file for bankruptcy within five

years of leaving their sport is a staggering 78%. Unfortunately, overspending and

overestimating the number of years they could remain in their sport have caused many

well-known athletes to lose it all. This does not have to be you! By using some basic

financial tools and practices, you can avoid being part of this unfortunate statistic.

Create a balance sheet, cash-flow summary, income and expense summary

(know what you earn aer taxes — and keep track of what you spend, a.k.a.

your “personal burn rate”)

Establish savings goals (have a realistic view of your earnings potential and

estimated years in your profession)

Participate in qualified and nonqualified retirement plans

Avoid going into debt (pay off mortgages, credit cards, personal lines of

credit, student loans)

Manage your existing debt efficiently

Save more than you spend, and avoid supporting an entourage of people

before you have put away savings for yourself

Avoid making large luxury purchases and “keeping up with the Joneses”

(buying expensive cars, boats, planes, jewelry and houses)

Professional athletes who file

for bankruptcy within 5 years.

78

%

Source: Fox Business News, Feb. 2022.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

11Table of contents

If you are an entertainer in the early part of your career, chances are you’re not

making much money from your hard work. That’s why it’s important to have a

process in place to save money for those “rainy days” between gigs, until your cash

flow becomes larger and more dependable. As you slowly build your net worth, you

can devote some of your excess capital — if not needed for expenses or rainy-day

savings — to making investments for the future.

Pay your federal and state income taxes

Perhaps more than any other group of professionals, athletes and entertainers tend

to have varied and complex sources of income. That income can be a challenge to

report properly to the state and federal taxing authorities. You want to get your tax

filings correct from the start!

Multiple revenue streams

Signing Bonus Incentives Endorsements

Licenses Salary Performance Bonuses

Deferred Compensation Merchandise Contingent Compensation

Sponsorships Appearance Fees Residuals

Royalties Social Media Platforms NF Ts

The jock tax

State level income tax filings tend to make tax compliance for athletes and

entertainers very complicated. Athletes and entertainers can be subject to state

income taxes in multiple states for services performed in those states. For example, a

National Football League player can expect to file between 8 to 12 non-resident state

income tax returns a year. A National Basketball Association player can expect to file

between 16 to 20 non-resident state income tax returns a year.* This multi-state income

ta

x liability is oen referred to as the “jock tax” but it can apply to any person who

performs services in more than one state if certain income and/or presence tests are

reached. Each state with an income tax will have its own rules as to when its income

tax law applies.

Will Rogers

“

T

oo many people

spend money

they haven’t

earned, to buy

things they don’t

want, to impress

people they

don’t like.

“

* Source: Andrew Osterland, CNBC; State Tax Departments Set their Sights on Pro Athletes’ Earnings (Jan. 11, 2021).

Source: Albuquerque Journal, 1975.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

12 Table of contents

Last will and testament

(or “pour-over” will plus

revocable trust)

Durable power of attorney

(allows someone other than you

to make financial decisions for you

when you can’t)

Advance health care directive

(allows someone other than you

to make medical decisions for you

when you can’t)

Signing bonuses are typically taxed on the federal level and in the state where the

athlete lives. Consequently, establishing residency in low or no state income tax

states like Florida or Texas can avoid having to pay state level income taxes on a huge

signing bonus. However, not all bonuses are created equal. Bonuses that are paid for

completing a service (such as winning an Oscar, voted MVP, winning a batting title)

can be subject to state income tax in multiple states if such services were performed

in those states.

Underpaying or not paying the proper amount of taxes owed will subject you to fines,

penalties and interest — and sometimes those penalties can be greater than the

amount of unpaid taxes. Once you are in arrears with payments owed to the IRS and

state taxing authorities, digging yourself out of back taxes, penalties and interest

charges can be extremely difficult and expensive. In some instances, failure to pay taxes

can lead to criminal penalties. In fact, that’s how the infamous gangster Al Capone

was eventually put behind bars.

Unfortunately, there are not many legal options available that can shelter your

salary and bonuses, but there are strategies you can consider. Your Merrill advisor

can bring a team of planning specialists — who can lay out options for you and

your tax advisors to consider.

Basic estate planning documents

Every professional athlete and entertainer should have a set of basic estate planning

documents that address what will happen upon their death or if they become

incapacitated. These documents are crucial because they inform people what to do

with your property or your body if you are unable to tell them.

At a minimum,

we suggest that

you have the

following

in place:

If you are single and

contemplating marriage, you

should also consider putting a

prenuptial agreement in place

— to protect your current and

future net worth from a

potential divorce.

Merrill has gathered insights

and created tools meant to

help guide you and your future

spouse through this process,

like the Merrill Center for Family

Wealth’s Tying a Better Knot and

Taking the Taboo out of Money

and “I Do.” Ask your advisor for

these resources.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

13Table of contents

Max out your retirement savings options

Most professional players associations in the U.S., and many of the entertainment guilds/

associations, offer their members the ability to make annual contributions to a qualified

retirement plan such as a 401(k) plan. These tax-advantaged savings vehicles provide

numerous benefits. When you make pre-tax contributions to the plan, your taxable income

in the year of contribution is reduced — potentially resulting in less income taxes for that

year. While your pre-tax money is invested in the 401(k) plan and has the potential to earn

income, that income will not be subject to federal income tax. Also, most states have laws

that protect 401(k) assets from the participant’s creditors. Depending on the terms of your

plan, you can control the investments in the account, and you control when you withdraw

money from the account. It’s only when you withdraw that you have to pay ordinary income

tax on the amount of the distribution. In addition, withdrawals made before age 59½ are

generally subject to an additional 10% federal income tax, unless an exception applies.

You should be aware of whether your association or guild offers a pension plan, how it

works, and how best to use it in conjunction with other retirement plans like 401(k)s

and individual retirement accounts (IRAs). Pension plans are another type of qualified

retirement plan offered by some employers. Generally, these plans provide participants

with an accrued benefit usually payable as an annual or monthly payment over a period of

years, usually for life, that typically start at a specified time (usually when the participant

reaches “normal retirement age” as defined under the applicable plan). Pension plans may

permit distributions to commence before normal retirement age, and in some cases before

reaching age 59½. To qualify, each player or entertainer must satisfy their plan’s specific

qualifications and vesting rules. The accrued benefit is determined under the plan’s accrual

formula and tends to be based on how long the employee works for the organization.

Another retirement solution typically available to entertainers — because they are

usually self-employed — is to fund a simplified employee pension called a SEP-IRA.

Just like IRAs, SEP-IRAs are tax-advantaged income deferral solutions that have been

authorized by Congress. Distributions are taxed under federal ordinary income tax

rates, and any distributions prior to 59½ would be subject to an additional 10% tax.

Your Merrill advisor can work with you to determine which plans are available to you

and which one may best support your goals.

401(k) SEP-IRA

• Your federal taxable income in the

year of contribution is reduced —

potentially resulting in less federal

income taxes for that year

• Pre-tax money will not generally be

subject to federal income tax until

distributed

• Most states have laws that protect

401(k) assets from creditors

• 10% additional federal tax for

early withdrawals

• Contributions an employer can

make to an employee’s SEP-IRA

cannot exceed the lesser of: 25%

of the employee’s compensation,

or $66,000 for 2023 ($61,000

for 2022, $58,000 for 2021 and

$57,000 for 2020)

• Distributions are taxed under

federal ordinary income tax rates

• 10% additional federal tax for early

withdrawals

In 2023, the maximum

401(k) contribution

$22,500

If 50 or over at any time

during the calendar year, you

can contribute an additional

$7, 50 0

Additional federal tax on

withdrawals before age 59½

unless an exception applies

10

%

Some employers will

match some or all of your

401(k) contributions, which

would allow more than

$22,500

(plus an additional $7,500 if

50 or over) to be contributed

to your plan in 2023.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

14 Table of contents

Take ownership of your financial destiny

Managing your wealth does not have to be your second (or third) full-time job.

You should, however, devote enough time and attention to your assets, liabilities

and investment performance to become well-informed in order to make informed

and reasonable decisions.

Scheduling regular meetings with your advisors is a good place to start. Occasionally,

these meetings should consist of a number of different advisors from numerous

disciplines in order to collaborate and determine an appropriate path forward

for you. By establishing short- and long-term goals and objectives, creating

benchmarks against which you can measure your advisors’ ongoing performance,

and checking in with those advisors on a regular basis, you can stay fully abreast of

how close you are to attaining your goals — and quickly revisit or correct anything

that is not turning out to your satisfaction.

Estate tax considerations

If you have managed to amass a small fortune, further advanced planning is required

in order to protect your money from creditors and to reduce (and sometimes

eliminate) estate taxes. For example, the current federal estate tax is 40%. In 2023,

federal law exempts up to $12.92 million per person from federal estate tax. That

means married athletes and entertainers can shield up to $25.84 million from federal

estate taxes. If you die with an estate worth more than these exemption amounts,

it may be subject to a 40% federal estate tax on the excess — unless you engage in

advanced planning during your lifetime.

For others with estates valued at less than $12.92 million (or $25.84 million for

married couples), their estates could be subject to federal estate tax in the future.

Under the 2017 Tax Cuts and Jobs Act, the estate tax exemption amount is scheduled

to drop to $5 million in 2026, adjusted for inflation. Based on current interest rates in

effect as of the date of this paper, Merrill is projecting that the exemption will drop

and be adjusted to $6.5 million in 2026. This means that if the exemption drops to

$6.5 million per taxpayer in 2026, the estate of a single person above $6.5 million

could be hit with a 40% federal estate tax, and married couples could only shelter

$13 million before potentially being subject to estate taxes on the excess. What does all

of this mean? For very wealthy persons, failure to use available exemptions before the

end of 2025 may cost their beneficiaries millions of dollars per parent in estate taxes.

Take advantage of

available exemptions

Failure to use up available

exemptions before the

end of 2025 can cost

beneficiaries millions of

dollars in estate tax

Advanced planning

is necessary

Protect your money from

creditors and reduce

estate taxes

Advanced planning for elite athletes and

A-list entertainers

While your advisors are here to

provide advice and guidance

in helping you manage the

complexities of your wealth,

remember it’s your money and it’s

important you take on an active

role in managing it. Make sure to

have regular meetings with your

advisors to review your financial

goals to help you stay on track.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

15Table of contents

Philanthropic goals

Individuals who lead or support a specific charitable cause are likely to increase

their monetary contributions as their income and net worth grows. Making charitable

donations (either one-time giving or over a lifetime) not only helps those in need,

but it can also reduce the amount of the donor’s taxes that would be otherwise due

in the same year as the donation. While most itemized deductions were reduced

or suspended under the 2017 Tax Cut and Jobs Act until 2026, charitable income

tax deductions are still valid as long as the donation reaches a certain threshold.

Under current tax laws, donors’ total itemized deductions must be more than their

standard deduction in order to claim the charitable deduction on their tax return —

which is $13,850 for single taxpayers and $27,700 for married couples filing jointly

in 2023.

Many wealthy athletes and entertainers elect to create their own charitable giving

structures, either through a private foundation or a donor-advised fund (DAF).

Each option has advantages and disadvantages; the best choice will depend on

the goals of the donor. Private foundations are tax-exempt organizations, generally

created and funded by an individual or a small group of donors (such as a family).

This structure is oen a grant-making entity and usually does not engage in fund-

raising or grant seeking. Typically, family members serve as the foundation’s board

of directors, officers or trustees.

Donor-Advised Fund (DAF) Private Foundation

A charitable giving account that

enables the donor to pursue

their charitable goals without

the administrative expenses of

establishing a foundation

Tax-exempt organizations, generally

created and funded by an individual

or a small group of donors

(such as a family)

However, private foundations have specific reporting requirements. In order to create

a private foundation, a trust or not-for-profit company must be formed, the new

entity must obtain an employer ID number (EIN) from the IRS, and then an application

must be sent to the IRS for “exempt status” (via IRS Form 1023). This process usually

takes anywhere from six months to two years before receiving a “determination

letter.” In addition, for charitable income tax deduction purposes, private foundations

are treated less favorably than a DAF. A foundation must file an annual income

tax return in which it must disclose the names of the directors and officers, the

foundation’s balance sheet, charitable grants and charitable recipients. Finally, a private

foundation is required to pay a minimum of 5% of its asset value each year to charity.

Donors must have itemized

deductions that are more

than their standard deduction

$13,850

for single taxpayers

$27,70 0

for married couples filing

jointly in 2023.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

16 Table of contents

Donor-Advised Fund Private Foundation

Use/Role • Minimize operating costs and administrative

responsibilities

• Provide a training ground for future

generations

• Create a vehicle that can be used to

memorialize a name

• Receive distributions from Donor’s private

foundation

• Due to administrative responsibilities and statutory

compliance requirements, generally more cost

effective for gis in excess of $10 million

• Create a multigenerational charitable organization

• Provide a role for family members and/or

philanthropic training/mentoring

• Create a vehicle that can be used to memorialize

a name

Grant-making Donor makes grant recommendations that are

subject to the approval of the DAF sponsor

Donor has full control over and responsibility for

grant-making activities and decisions

Privacy Donor discretion to grant anonymously Grant activity is a matter of public record

Taxation Some excise taxes apply, such as excise taxes

on non-qualifying distributions, and excess

business holdings

• Excise tax of 1.39% on net investment income

• Payments must be made quarterly

• Possible additional excise taxes, such as taxation

on jeopardy investments, self-dealing and excess

business holdings

Required annual

distributions

None

Minimum of 5% of asset value used for “eligible

expenses” and/or distributions to eligible recipients

Reporting

requirements

None for Donor Must file annual tax return, Form 990-PF

Start-up costs None Substantial legal and accounting fees can apply

Income tax

deduction

Higher AGI limitations Lower AGI limitations

A donor-advised fund is a charitable giving account that enables the donor

to pursue their charitable goals without the legal paperwork of establishing a

foundation. This type of account is easy to open and is a very cost-effective

alternative to a private foundation. Similar to many private foundations, a DAF

is a grant-making entity. However, a DAF account owner does not have to file

an annual tax return for the DAF and/or make any other ongoing disclosures

regarding the account’s balance sheet, charitable grants and charitable recipients.

In addition, DAFs are not required to make any charitable distributions during the

year. One advantage of a foundation compared to a DAF is that the foundation can

specifically choose which organization or group receives the foundation’s grant.

The donor of a DAF can recommend making grants to specific charities, but the

grants are subject to the approval of the fund’s sponsor.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

17Table of contents

Asset protection strategies

As an athlete or entertainer’s wealth grows, they unfortunately become more

prone to being sued, for legitimate and illegitimate reasons. Successful athletes

and entertainers should consider engaging in asset protection strategies that,

when implemented properly, can legally shield creditors from their assets and deter

lawsuits from ever happening. Remember, any lawsuit, whether valid or not, carries

with it “reputational risk,” which can have disastrous results like not having your

contract renewed, forfeiting deferred payments and losing key endorsements.

Property insurance

The first line of defense is to make sure that you have suitable insurance. This should

include having adequate property and casualty insurance like homeowners, automobile,

aircra, boat and umbrella insurance. Generally, the more the family balance sheet

grows, the more property and casualty insurance you should consider.

Disability insurance

The second line of defense is to acquire disability insurance in addition to what your

employer may offer. Athletes and entertainers have a range of insurance policies to

consider that can insure against permanent total disability, temporary total disability,

loss of value due to injury, or lack of endorsement(s) due to injury.

Property ownership

The next line of defense is to make sure assets are titled in such a way as to provide

maximum protection. For example, in about half the states, spouses are permitted to

hold property jointly as “tenants-by-the-entirety” (TBE). This creates a legal fiction

that each spouse is the 100% owner of the property for creditor protection purposes.

If spouse 1 is sued individually, spouse 2 of the TBE property can assert their 100%

ownership and block the creditor from the asset. Conversely, if spouse 2 is sued

individually, spouse 1 of the TBE property can assert their 100% ownership and

block the creditor from the asset. Unfortunately, the creditor protection afforded by

holding assets as TBE is imperfect. For example, if both spouses are sued jointly, then

property held as TBE offers no protection. Additionally, TBE protection only applies

to married persons. Single individuals must look to other asset protection solutions.

Additionally, if married persons hold property as TBE and they divorce or one spouse

dies, the TBE protection ends.

Protect your assets

Any lawsuit, whether valid or not, carries

with it “reputational risk” that can cause

harm to your reputation.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

18 Table of contents

Business ownership

Another line of defense is to consider holding certain assets and separate business

endeavors (like a rental property) in separate limited liability companies (LLCs).

If structured and administered properly, the LLC should prevent a creditor of LLC 1

going aer the assets of LLC 2. However, if the owner of the LLC is personally sued,

and the judgment creditor wins, any of the client’s personal assets, including the

owner’s interests in LLCs, can be taken away by either a “charging order” (client

loses rights to distributions and the creditor steps into client’s distribution shoes)

and in some states like Florida and South Carolina, allow a successful judgment

creditor in certain cases to “foreclose” on LLC interests and force a terminating

distribution out to the creditor.

Unfortunately, many lawsuits that are launched against a private business (or LLC)

also name the business owners “individually” as defendants, which means that a

creditor of LLC 1 might still be able to get at the assets of LLC 2 and LLC 3, by

suing the client personally and getting a charging order or a foreclosure action

against the client’s member interests in LLC 2 and LLC 3. One possible solution

that may protect an owner’s LLC interest from being taken by a creditor might

be to contribute their LLC interests to an irrevocable trust like a spendthri gi

trust, a spousal lifetime access trust (SLAT) or a domestic asset protection trust

(DAPT). Connect with your advisor to discuss more specific details around owning

a business that applies to your situation.

Trust strategies

Finally, as mentioned above, there are numerous irrevocable trust strategies that offer

asset protection. DAPTs have become increasingly popular over the last two decades,

especially for wealthy single persons who cannot deploy protection strategies that

require a spouse. As of this paper, 21 states permit people to establish DAPTs in

their state. The good news is, you do not have to live in one of those states to take

advantage of their DAPT laws.

WEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERSWEALTH OPTIMIZATION FOR PROFESSIONAL ATHLETES AND ENTERTAINERS

Conclusion

Athletes and entertainers have special planning needs — driven in part by the

timing, source and reliability of their income, as well as their retirement account

options, charitable giving goals, asset protection needs, and the potential to have

second careers during or aer they’ve le their current profession.

Let us help — your Merrill advisor can offer access to the firm’s latest tools and

strategies to help you and your team discuss, build and implement your family’s

customized plan. Reach out to your Merrill advisor today or visit the Sports &

Entertainment site for more information.

19Table of contents

1

BofA Global Research is research produced by BofA Securities, Inc. (“BofAS”) and/or one or more of its affiliates. BofAS is a registered broker-dealer, Member SIPC, and wholly owned

subsidiary of Bank of America Corporation.

Merrill Private Wealth Management is a division of MLPF&S that offers a broad array of personalized wealth management products and services. Both brokerage and investment advisory

services (including financial planning) are offered by the Private Wealth Advisors through MLPF&S. The nature and degree of advice and assistance provided, the fees charged, and client

rights and Merrill’s obligations will differ among these services. Investments involve risk, including the possible loss of principal investment. The banking, credit and trust services sold by the

Private Wealth Advisors are offered by licensed banks and trust companies, including Bank of America, N.A., Member FDIC, and other affiliated banks.

Merrill, its affiliates, and financial advisors do not provide legal, tax, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions. Banking and

lending products are provided by Bank of America, N.A., Member FDIC, and a wholly owned subsidiary of Bank of America Corporation.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and

solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., (“Bank of America”) and Merrill Lynch, Pierce,

Fenner & Smith Incorporated (“MLPF&S” or “Merrill”), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation (“BofA Corp.”).

Donor-advised fund and private foundation management are provided by Bank of America Private Bank, a division of Bank of America N.A., Member FDIC and a wholly owned subsidiary

of Bank of America Corporation.

© 2023 Bank of America Corporation. All rights reserved. MAP5833465 | 09/2023

(ADA)

To learn more about Bank of America’s environmental goals and initiatives, go to bankofamerica.com/environment.

Leaf icon is a registered trademark of Bank of America Corporation.