Implementation of e-Commerce VAT changes in

Northern Ireland

Who is likely to be affected:

The package of reforms will affect businesses involved in cross border supplies of goods to

non-VAT registered customers between Northern Ireland and the EU, businesses involved in

the supply of low value imports of goods into Northern Ireland (NI), including goods imported

into NI from Great Britain (GB), and non-EU and UK businesses with goods located in NI at

the point of supply.

In particular, these changes specifically affect businesses importing low value goods (at or

under £135) into NI and businesses making distance sales of goods between NI and the EU.

General description of the measure:

The changes simplify the way VAT is administered for some goods sold between Northern

Ireland and the EU, and some low value imports into Northern Ireland from 1 July 2021. This

mirrors an EU-wide reform, which the UK is implementing in Northern Ireland in line with the

obligations set out under the Northern Ireland Protocol, where EU VAT rules with respect to

goods will continue to apply in Northern Ireland.

Low value consignment relief (LVCR) relieves import VAT on consignments of goods not

exceeding £15. From 1 January, in order to combat widespread abuse and to avoid trade

distortion the UK removed LVCR in GB. This relief continues to apply in NI as required by

the Protocol to the Withdrawal Agreement but does not apply to goods that are ordered

remotely. From 1 July, this will be fully removed in NI and will align with the removal of the

relief in GB.

Online marketplaces that facilitate supplies of goods that are sold by non-EU businesses

located in the UK are responsible for collecting and accounting for VAT on sales made to UK

customers except where goods are located in NI and sold to NI customers. From 1 July

online marketplaces will also be liable for collecting and accounting for the VAT on goods

sold by non-EU businesses located in NI at the point of sale and sold to NI customers. The

online marketplace liability will not apply in relation to GB businesses that make sales of

goods located in NI at the point of sale to NI customers.

The provisions will also provide for an optional Import One Stop Shop Scheme (IOSS). This

is a single simplified accounting scheme to be made available to those businesses who wish

to use it to facilitate the collection of VAT on imports of non-excise goods in consignments

not exceeding £135 in value to customers in NI and the EU. This includes where goods are

imported into NI from GB. UK VAT registered GB businesses that opt to register for IOSS

would need to account for VAT due on their sales of these goods to NI on their IOSS return.

GB businesses that are not VAT registered in the UK because they are below the UK VAT

registration threshold, but that are registered for IOSS, will not be required to charge VAT on

their sales of these goods to NI. All GB businesses registered for IOSS making sales of

these goods to NI will be able to report their IOSS number to HMRC prior to moving the

goods. All GB businesses that do not opt to register for IOSS must continue to account for

the VAT on their sales to NI on their UK VAT return.

The IOSS scheme is also available to online marketplaces that facilitate the sale of imports

of non-excise goods in consignments not exceeding £135 in value into NI and the EU.

Where an online marketplace opts to register for IOSS they will become liable for the VAT on

sales of goods within scope of the scheme facilitated through their platform. Where a

business, or online marketplace, opts to register for IOSS import VAT will no longer be

required to be paid upon importation of goods within the scope of the scheme. Instead VAT

will be collected by the IOSS registered business and paid via the IOSS return in the country

of registration.

Online marketplace liability will not apply in relation to GB businesses that make sales of

these goods through their platform to NI customers.

For imports into NI, where the business, or online marketplace, has not opted to register for

IOSS import VAT will continue to be collected in the same way as it is now.

Under the provisions, businesses not established in the EU or NI that opt to register for IOSS

can do so in any EU Member State or in NI. However, the IOSS system will not be available

for businesses to register in NI on 1 July. In the interim period until the IOSS system is

available in NI, GB businesses that opt to register for IOSS can register in any EU Member

State and account for the VAT due via their IOSS return.

A new single EU wide distance selling threshold of £8,818 (10,000 EUR) will be introduced

for the sales of goods and services in the EU. The threshold will only apply to supplies of

EU-located goods to and from Northern Ireland, which means that EU suppliers who exceed

the threshold will have to register for VAT in the United Kingdom if they wish to sell goods to

consumers in Northern Ireland

The provisions will also provide for a future One Stop Shop scheme (OSS Union scheme) to

facilitate the collection of VAT on supplies of goods and digital services in the EU. The OSS

Union scheme will be an optional alternative available to NI established businesses,

enabling them to register and account for the VAT on supplies of goods to customers

through a single simplified system. The OSS Union scheme is also available to online

marketplaces, where they facilitate the sale of non-EU and UK businesses’ goods located in

the EU at the point of sale. In the interim period, from 1 July until the OSS Union system is

available, NI established businesses making supplies of goods in excess of the threshold

can register and account for VAT in the relevant EU Member State.

The provisions of OSS and IOSS schemes in relation to supplies of goods under the

respective schemes will also include the specific reporting requirements, including time

frames.

Policy objective

The implementation of changes to simplify the way VAT is administered for some goods sold

between Northern Ireland and the EU, and some low value imports into Northern Ireland

from 1 July 2021, in line with the obligations set out under the Northern Ireland Protocol.

Background to the measure

Following the end of the transition period on 31 December 2020, the UK introduced new

rules for imports of goods into NI from non-EU countries, which were in line with the

obligations under the Protocol.

The e-commerce package will introduce changes from 1 July 2021 in respect of the

movement of goods between NI and the EU and imports of goods into NI sold by non-EU

businesses.

The package also introduces two new IT systems for the collection of VAT on imports of low

value consignments not exceeding £135 and the collection of VAT business to consumer

transactions of goods in the EU. Both systems are designed to reduce burdens on business

and facilitate the collection of VAT across Northern Ireland and the EU.

Detailed proposal

Operative date

Changes that will come into effect from 1 July will include the full removal of LVCR and the

introduction of online marketplace liability on supplies of goods sold by non-EU and UK

businesses where the goods are located in NI, and a new EU wide threshold of £8,818 in

respect of supplies of goods by NI businesses to EU consumers.

Relevant elements of the OSS and IOSS systems will have effect in law from a later date.

Current law

Current law is included in the Value Added Tax Act 1994 (VATA), the Value Added Tax

(Imported Goods) Relief Order 1984 (SI 1984/746) and the Value Added Tax Regulations

1995 (SI 1995/2518) (the VAT Regulations 1995).

Proposed revisions

Legislation will be introduced in Finance Bill 2021 which introduces Schedule VAT and

Distance selling: Northern Ireland.

Part 1 of the Schedule provides for amendments to be made to Part 9 of Schedule 9ZA

(Registration in respect of distance sales from the EU to NI) to VATA to change the liability

to register under that Part by replacing the single distance selling registration threshold for

intra-EU supplies of goods with an EU wide threshold of supplies of digital services and

goods. Paragraph 29 of Schedule 9ZB to VATA covering the place of supply for distance

selling between the EU and NI, is also amended to take account of registration under the

OSS scheme set out in Part 2 of the Schedule. (Without further amendment, paragraph 29

will provide that for a NI business selling goods to customers in the EU the new EU wide

threshold will only be calculated by reference to the value of supplies of goods (and not the

value of any supplies of digital services)).

Part 2 of the Schedule amends section 40A of VATA to insert new Schedules 9ZD and 9ZE

into VATA which establish two special accounting schemes, OSS and IOSS.

Schedule 9ZD provides for the OSS which may be used by certain persons established in NI

who make supplies of goods in EU Member States. The OSS is an optional accounting

simplification scheme for businesses to make a single return and payment for business to

consumer supplies within the EU. The Schedule covers the registration, accounting and

return and related provisions for the OSS.

Schedule 9ZE establishes the IOSS for distance sales of imported goods into NI and makes

provision about the equivalent schemes in Member States. The IOSS is an optional

accounting scheme for businesses to make a single monthly return and payment for

qualifying supplies in the EU. The Schedule covers the registration, accounting and return

and related provisions for the IOSS.

Section 40A is also amended to insert a new Schedule 9ZF to make modifications to VATA

and the VAT Regulations 1995 and other legislation relating to VAT in connection with

Schedules 9ZD and 9ZE.

Part 3 of the Schedule amends Schedule 9ZC to revoke provisions in the Value Added Tax

(Imported Goods) Relief Order 1984, which were modifications relating to the Northern

Ireland Protocol retaining low value consignment relief for goods imported into NI.

Part 4 of the Schedule amends Schedule 9ZC of VATA to modify the effect of VATA. It

inserts a new section 5B which deems the operator of an online marketplace to be the

supplier of goods in NI where the online marketplace facilitates the supply of non-EU

businesses’ goods in NI, subject to limited exceptions. The seller will be treated as having

supplied the goods to the operator of the online marketplace and the operator will be treated

as having supplied them on to the customer in NI in the furtherance of a business. As such,

the operator will be liable to charge and account for the VAT on those supplies. This

provision will not apply to sales of goods by GB businesses to customers in NI, where the

supply is facilitated by the online marketplace.

It also adds to Group 21 of Schedule 8 to VATA to introduce a zero rate for the deemed

supply between a seller and the operator of the online marketplace. Part 4 also introduces

record keeping requirements on the operator of an online marketplace in relation to such

deemed supplies by way of modifying Schedule 11 to VATA. Related modifications are also

made to invoicing provisions in the VAT Regulations 1995.

Summary of impacts

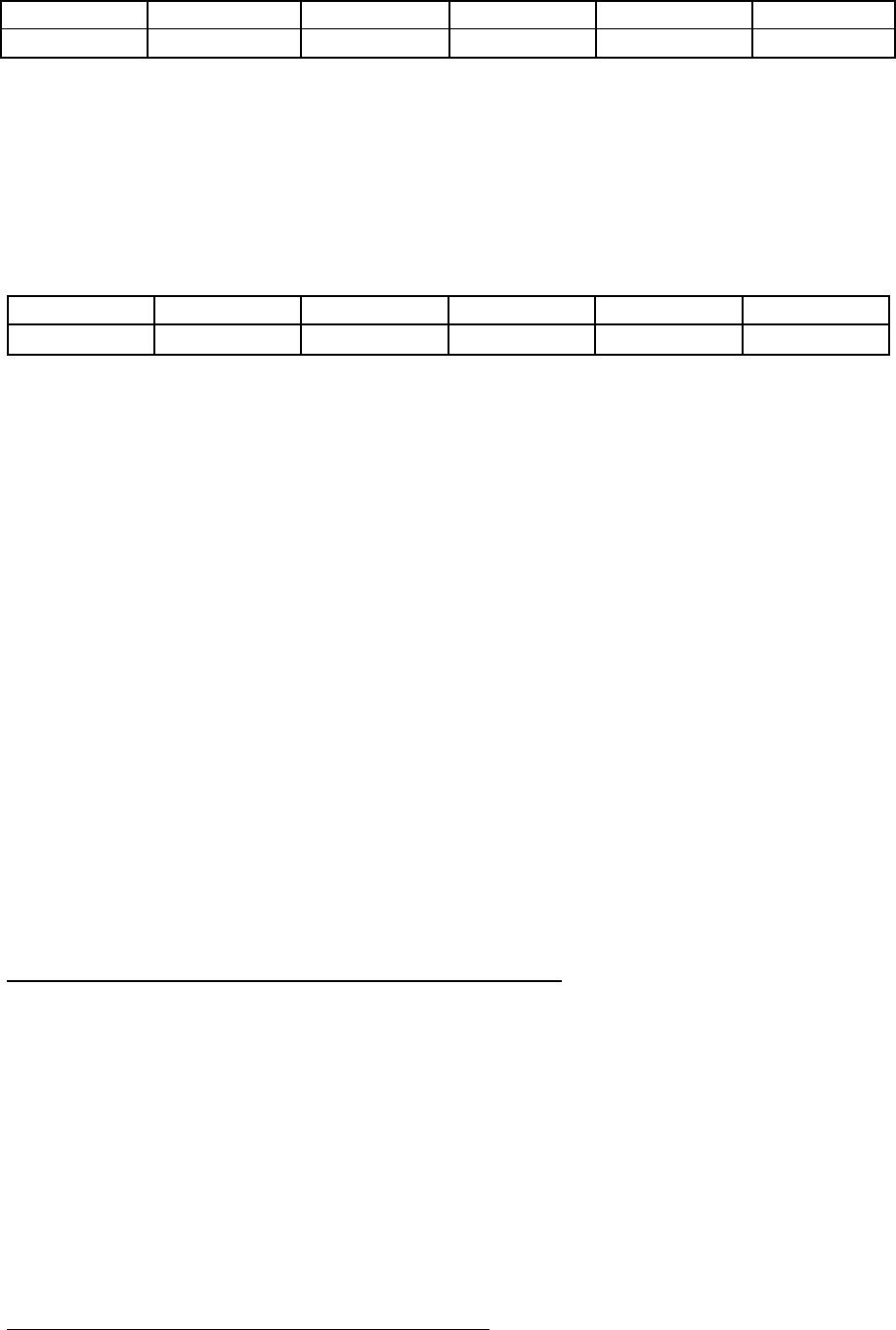

Exchequer impact (£m)

VAT parcel reforms for UK

2020 to 2021

2021 to 2022

2022 to 2023

2023 to 2024

2024 to 2025

2025 to 2026

+85

+360

+320

+305

+295

+280

The Northern Ireland exchequer impact of the implementation of LVCR and online

marketplace liability is captured within Table 1.1 of Spending Review 2020: Policy decisions

since Budget 2020 as “VAT parcel reforms” and has been certified by the Office for Budget

Responsibility. More details can be found in the Policy costings: November 2020 document

published alongside Spending Review 2020.

Additional impacts of the e-Commerce changes

2021 to 2022

2022 to 2023

2023 to 2024

2024 to 2025

2025 to 2026

2026 to 2027

empty

empty

empty

empty

empty

empty

The final costing will be subject to scrutiny by the Office for Budget Responsibility and will be

set out at the next fiscal event.

Economic impact

This measure is not expected to have any significant macroeconomic impacts.

Impact on individuals, households and families

There is expected to be no impact on individuals as this measure only affects businesses.

There is expected to be no impact on family formation, stability and breakdown.

Equalities impacts

It is not anticipated that there will be any impacts for those in groups sharing protected

characteristics.

Impact on business including civil society organisations

These measures will have an impact on NI and EU businesses involved in cross border

supplies of goods to non-VAT registered customers between NI and the EU, NI and EU

businesses involved in the supply of low value imports of goods, and overseas businesses

with goods located in NI at the point of supply.

Impact on business after distance selling changes in place

Lowering the intra EU distance selling threshold from £70,000 to £8,818 is expected to have

an impact on a few thousand businesses. Overall, there is expected to be a negligible impact

on businesses. One-off costs will include familiarisation with the change and could also

include having to register for the distance sale of goods. Continuing costs may include

administrative burdens associated with complying with the scheme.

This change is likely to have an impact on smaller NI businesses selling goods to customers

in the EU. These businesses may have previously fallen below the threshold but are now

captured by the new lower limit.

Customer experience for this aspect of the changes is expected to stay broadly the same as

this is an established online process.

Impact on overseas sellers importing goods into NI

For overseas sellers importing goods into NI there will be little practical change required, as

reforms, including removal of LVCR, were introduced by the UK in NI on 1 January 2021.

These businesses will continue to be able to register and account for import VAT on the

import of low value consignments to HMRC through their UK VAT return. The administrative

costs to these affected businesses are expected to be negligible. Businesses will have one-

off costs of familiarising themselves with this change. There are not expected to be any

continuing costs.

Customer experience is expected to stay broadly the same as this change does not affect

how businesses interact with HMRC.

Impact on businesses of IOSS in NI

From 1 July 2021 businesses importing into NI can continue to register and account for

import VAT on imports of low value goods on the UK VAT return. Businesses already

registered for VAT in the UK will not need to re-register.

Businesses will not be able to register for IOSS in the UK straight away but have the option

to register for IOSS in an EU Member State.

Businesses registering for IOSS will have a one-off cost of familiarising themselves with the

new IOSS system. Businesses importing low value goods that are not already registered for

VAT in the UK will have one-off costs of familiarising themselves with the process of

submitting a UK VAT return. Businesses could also have continuing costs relating to

accounting, reporting and record keeping. The administrative costs to these affected

businesses are expected to be negligible.

Customer experience could be negatively affected given these businesses may need to

familiarise themselves with either the EU IOSS system, or the regulatory regimes in the UK

and incur costs to register for VAT. In order to reduce the negative impact on businesses

HMRC will provide clear guidance outlining the changes and the options available for

businesses.

Impact on NI businesses of OSS

From 1 July 2021 NI businesses that exceed the EU wide distance selling threshold of

£8,818 will be required to register for VAT in each of the EU Member States their goods are

destined for.

When the new OSS system is in operation, NI businesses will have the option to register

through this system, instead of registering for VAT in each relevant EU Member State.

One-off costs to businesses will include familiarising themselves with these regulatory

changes and could include upskilling employee(s) with the knowledge of how to register for

VAT in each of the EU Member States that they wish to import goods into, and

administrative costs associated with each registration.

Continuing costs could include recording additional information on exports to each EU

Member State. This may have associated costs of seeking accounting advice to cover

additional calculations specific to this, as well as the additional cost of collecting and storing

relevant information. An additional continuing cost could include submitting separate VAT

returns. These one-off and continuing costs to these affected businesses are estimated to be

negligible.

This aspect of the changes is expected overall to negatively affect businesses’ experience of

dealing with HMRC as businesses may need to familiarise themselves with regulatory

regimes in multiple EU Member States and incur costs to register for VAT in more than one

place. In order to reduce the negative impact on businesses, HMRC will issue clear

guidance outlining the changes and the potential impacts created.

Online marketplaces

Online marketplaces facilitating sales of non-EU and UK goods located in NI at the point of

sale will be affected by these changes. From 1 July they will be responsible for collecting

and accounting for the VAT on supplies of goods to NI non-business customers. One-off

costs will include familiarisation, and could include training employees so that they are

familiar with the changing legal requirements, and introducing new systems and/or

processes in order to be able to identify and account for transactions in scope. Continuing

costs include recording the VAT due on transactions, as well as reporting and paying this

VAT to HMRC. The administrative costs to these affected businesses are expected to be

negligible.

Customer experience for this aspect of the change is expected to broadly stay the same as

businesses have made changes in GB and partially in NI already.

Overall impact

This measure could disproportionately affect small and medium sized businesses. Impacts

are outlined above. In order to support small and medium sized businesses, HMRC will

issue clear guidance outlining the changes and the potential impacts.

The impacts are being kept under review through continuing stakeholder engagement and an

updated impact assessment will be published if the impacts are determined to be significant.

There is no impact on civil society organisations.

Operational impact (£m) (HMRC or other)

Other impacts

Other impacts have been considered and none has been identified.

Monitoring and evaluation

This measure will be monitored through receipts, VAT returns and other information

collected from HMRC’s systems, as well as through communication with affected taxpayer

groups.

Further advice

If you have any questions about this change, please contact Kshama Purohit on Telephone:

03000 585748 or email: kshama.purohi[email protected]ov.uk.

Declaration

The Right Honourable Jesse Norman, Financial Secretary to the Treasury has read this tax

information and impact note and is satisfied that, given the available evidence, it represents

a reasonable view of the likely costs, benefits and impacts of the measure.