Userid: CPM Schema:

instrx

Leadpct: 100% Pt. size: 9.5

Draft Ok to Print

AH XSL/XML

Fileid: … ns/I8975/202012/A/XML/Cycle05/source (Init. & Date) _______

Page 1 of 7 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Instructions for Form 8975

and Schedule A (Form 8975)

(Rev. December 2020)

Country-by-Country Report

Department of the Treasury

Internal Revenue Service

Section references are to the Internal Revenue Code unless

otherwise noted.

Future Developments

For the latest information about developments related to

Form 8975, Schedule A (Form 8975), and their instructions,

such as legislation enacted after they were published, go to

IRS.gov/Form8975.

General Instructions

Purpose of Form

Certain U.S. persons that are the ultimate parent entity of a

U.S. multinational enterprise (U.S. MNE) group with annual

revenue for the preceding reporting period of $850 million or

more are required to file Form 8975.

Form 8975 and Schedules A (Form 8975) are used by

filers described under Who Must File to annually report

certain information with respect to the filer’s U.S. MNE group

on a country-by-country basis. The filer must list the U.S.

MNE group’s constituent entities, indicating each entity’s tax

jurisdiction (if any), country of organization and main

business activity, and provide financial and employee

information for each tax jurisdiction in which the U.S. MNE

does business. The financial information includes revenues,

profits, income taxes paid and accrued, stated capital,

accumulated earnings, and tangible assets other than cash.

Form 8975 and its Schedules A (Form 8975) must be filed

with the IRS with the income tax return of the ultimate parent

entity of a U.S. MNE group for the tax year in or within which

the reporting period covered by the Form 8975 ends.

Do not file Form 8975 and its Schedules A (Form

8975) separately from your income tax return.

Definitions

For more information on the terms below, see Regulations

section 1.6038-4.

Applicable financial statement. An applicable financial

statement is a certified audited financial statement that is

accompanied by a report of an independent certified public

accountant or similarly qualified independent professional

that is used for purposes of reporting to shareholders,

partners, or similar persons; for purposes of reporting to

creditors in connection with securing or maintaining

financing; or for any other substantial nontax purpose.

Business entity. A business entity is generally any entity

recognized for federal tax purposes that is not properly

classified as a trust under Regulations section 301.7701-4.

However, any grantor trust within the meaning of section 671,

all or a portion of which is owned by a person other than an

individual, is considered a business entity.

CAUTION

!

Additionally, the term “business entity” includes any entity

with a single owner that may be disregarded as an entity

separate from its owner under Regulations section

301.7701-3, and any permanent establishment (described

below) that prepares financial statements separate from

those of its owner for financial or tax reporting, regulatory, or

internal management control purposes.

A decedent's estate or a bankruptcy estate described in

section 1398 is not a business entity.

Constituent entity. With respect to a U.S. MNE group, a

constituent entity is any separate business entity of such U.S.

MNE group but does not include a foreign corporation or

foreign partnership for which information is not otherwise

required to be furnished under section 6038(a) (determined

without regard to Regulations sections 1.6038-2(j) and

1.6038-3(c)) or any permanent establishment of such foreign

corporation or foreign partnership.

Permanent establishment (PE). The term “permanent

establishment” includes:

•

A branch or business establishment of a constituent entity

in a tax jurisdiction that is treated as a permanent

establishment under an income tax convention to which that

tax jurisdiction is a party,

•

A branch or business establishment of a constituent entity

that is liable to tax in the tax jurisdiction in which it is located

pursuant to the domestic law of such tax jurisdiction, or

•

A branch or business establishment of a constituent entity

that is treated in the same manner for tax purposes as an

entity separate from its owner by the owner's tax jurisdiction

of residence.

Reporting period. The reporting period covered by Form

8975 and Schedules A (Form 8975) is generally the

12-month period of your applicable financial statement that

ends with or within your tax year. If you do not prepare an

annual applicable financial statement, then the reporting

period covered by Form 8975 and Schedules A (Form 8975)

is generally the 12-month period that ends on the last day of

your tax year.

Tax jurisdiction. A tax jurisdiction is a country or a

jurisdiction that is not a country but that has fiscal autonomy.

A U.S. territory or possession of the United States is

considered to have fiscal autonomy.

Tax jurisdiction of residence. A business entity is

generally considered a resident in a tax jurisdiction if, under

the laws of that tax jurisdiction, the business entity is liable for

tax therein based on place of management, place of

organization, or another similar basis. A business entity is not

considered a tax resident in a tax jurisdiction if the business

entity is liable for tax in such tax jurisdiction only by reason of

a tax imposed by reference to gross amounts of income

without any reduction for expenses, provided such tax

applies only with respect to income from sources in such tax

jurisdiction or capital situated therein.

Sep 10, 2020 Cat. No. 69160R

Page 2 of 7 Fileid: … ns/I8975/202012/A/XML/Cycle05/source 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

A corporation that is organized or managed in a tax

jurisdiction that does not impose an income tax on

corporations will be treated as resident in that tax jurisdiction,

unless such corporation is treated as resident in another tax

jurisdiction under the previously described rules.

The tax jurisdiction of residence of a permanent

establishment is the jurisdiction in which the permanent

establishment is located.

A business entity that does not have a tax jurisdiction of

residence is considered “stateless.”

Ultimate parent entity of a U.S. MNE group. The ultimate

parent entity of a U.S. MNE group is a U.S. business entity

that:

•

Owns directly or indirectly a sufficient interest in one or

more other business entities, at least one of which is

organized or tax resident in a tax jurisdiction other than the

United States, such that the U.S. business entity is required

to consolidate the accounts of the other business entities

with its own accounts under U.S. GAAP (or that would be so

required if publicly traded); and

•

Is not owned directly or indirectly by another business

entity that consolidates the accounts of such U.S. business

entity with its own accounts under GAAP in the other

business entity's tax jurisdiction of residence (or that would

be so required if publicly traded in its tax jurisdiction of

residence).

U.S. business entity. A U.S. business entity is a business

entity that is organized or has its tax jurisdiction of residence

in the United States. Foreign insurance companies that elect

to be treated as domestic corporations under section 953(d)

are U.S. business entities that have their tax jurisdiction of

residence in the United States. A business entity that is a

limited liability company that is organized in the United

States, and is wholly owned (directly) by another business

entity that has its tax jurisdiction of residence and is

organized in the United States, will be considered a U.S.

business entity that has its tax jurisdiction of residence in the

United States.

U.S. MNE group. A U.S. MNE group comprises the ultimate

parent entity of a U.S. MNE group and all of the business

entities required to consolidate their accounts with the

ultimate parent entity's accounts under U.S. GAAP (or that

would be so required if publicly traded), regardless of

whether any such business entities could be excluded from

consolidation solely on size or materiality grounds.

Business entities are not considered part of the U.S. MNE

group if the income or assets of the business entities are

included in the financial statements of the ultimate parent

entity based on the equity method or fair value accounting.

U.S. territory or possession of the United States. The

term “U.S. territory or possession of the United States”

means American Samoa, Guam, the Northern Mariana

Islands, Puerto Rico, and the U.S. Virgin Islands.

U.S. territory ultimate parent entity. A U.S. territory

ultimate parent entity is a business entity organized in a U.S.

territory or possession of the United States that controls (as

defined in section 6038(e)) a U.S. business entity and that is

not owned directly or indirectly by another business entity

that consolidates the accounts of the U.S. territory ultimate

parent entity with its accounts under GAAP in the other

business entity's tax jurisdiction of residence (or would be so

required if equity interests in the other business entity were

traded on a public securities exchange in its tax jurisdiction of

residence).

Who Must File

A U.S. person must file Form 8975 and Schedules A (Form

8975) if it is the ultimate parent entity of a U.S. MNE group

with revenues of $850 million or more in the immediately

preceding reporting period. A U.S. territory ultimate parent

entity may designate a U.S. business entity to file on its

behalf.

When making the determination of whether you are the

ultimate parent entity of a U.S. MNE group, a business

entity’s tax jurisdiction of residence is the business entity’s

country of organization if the business entity does not

otherwise have a tax jurisdiction of residence.

Exceptions from filing. You are not required to file Form

8975 if the annual revenue of your group for the immediately

preceding reporting period was less than $850 million.

When To File

Attach Form 8975 and Schedules A (Form 8975) to your

income tax return and file them with the IRS by the due date

(including extensions) for that income tax return. The Form

8975 and Schedules A (Form 8975) should be attached, as

applicable, to Forms 1120, 1120-C, 1120-RIC, 1065, 1120-S,

1120-L, 1120-PC, 1120-REIT, 990-T, and 1041.

Extension of time to file. To request an extension of time

to file Form 8975, you must follow the instructions for the

income tax return to which Form 8975 and Schedules A

(Form 8975) will be attached.

How To File

Electronic Filing

If you file your income tax return electronically, see the

instructions for the income tax return for general information

about electronic filing.

If you are filing Forms 1120, 1065, 1120-S, 990-T, or 1041

electronically, you must attach Form 8975 and Schedules A

(Form 8975) electronically in the correct format, not as a

binary attachment.

Note. Beginning January 2021, Form 990-T can be filed

electronically.

Note. In order to ensure the timely automatic exchange of

the information on Form 8975 and Schedules A (Form 8975),

you are encouraged to file your return electronically. In

certain cases, you are required to file your return

electronically.

Amended Form 8975. If you file a Form 8975 and

Schedules A (Form 8975) that you later determine should be

amended, file an amended Form 8975 and all Schedules A

(Form 8975), including any that have not been amended,

with an amended tax return. Use the amended return

instructions for the return with which you originally filed Form

8975 and Schedules A (Form 8975) and check the amended

report checkbox at the top of Form 8975.

If the return and Form 8975 that you are amending were

filed electronically with the IRS, then the amended return and

Form 8975 should be filed electronically with the IRS in order

to ensure timely automatic exchange of the information on

Form 8975 and Schedules A (Form 8975).

-2-

Instructions for Form 8975 (Rev.12-2020)

Page 3 of 7 Fileid: … ns/I8975/202012/A/XML/Cycle05/source 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Where To File

While most entities will be electronically filing their country-by

country reports, some filers will not be able to file

electronically. This includes those filing Form 1120-REIT,

filers of Forms 1120-C, 1120-L, 1120-PC, and 1120-RIC that

are filing as parent entities, and filers of Form 1041 that

choose not to or are not required to file electronically. These

filers should use the mailing addresses provided for the

applicable income tax return. The Form 8975 and Schedules

A (Form 8975) must be attached to the applicable paper tax

return.

Paper-filed returns. If filing on paper only, mail a copy of

page 1 of your Form 8975 to the IRS. Mailing a copy of

page 1 of Form 8975 will notify the IRS that you have filed

Form 8975 and Schedules A (Form 8975) with a paper return

and will assist the IRS in identifying paper returns that have

Form 8975 and Schedules A (Form 8975) attached. Mail to

the following address:

Internal Revenue Service

Mailstop 4950

1973 N. Rulon White Blvd.

Ogden, UT 84201

Record Maintenance

You are required to maintain records to support the

information provided on Form 8975 and Schedules A (Form

8975). However, you are not required to create and maintain

records that reconcile the amounts provided on Form 8975

and Schedules A (Form 8975) with the income tax returns of

any tax jurisdiction or your applicable financial statements.

Penalties for Failure To File

Penalties under section 6038(b) may apply for failure to

report the information required on this form.

Specific Instructions for Form

8975

There are two parts to Form 8975. You must complete the

information at the top of the form regarding reporting period

and Part I. Completing Part II is optional.

At the top of Form 8975, enter the reporting period for which

you are filing.

If filing an amended report (see Amended Form 8975,

earlier), check the amended report box.

Enter the number of Schedules A (Form 8975) attached to

Form 8975. You must attach at least one Schedule A (Form

8975) to your Form 8975 for each tax jurisdiction in which

your group operates, including the United States. Therefore,

you will file a separate Schedule A (Form 8975) for at least

two tax jurisdictions.

Generally, at least one Schedule A (Form 8975) will be for

the United States. However, certain U.S. MNE groups may

have only U.S.-organized constituent entities that are fiscally

transparent. These fiscally transparent U.S. business entities

do not have a tax jurisdiction of residence for purposes of

reporting information on Form 8975. Thus, these fiscally

transparent U.S. business entities, along with all other

constituent entities of the U.S. MNE group that do not have a

tax jurisdiction of residence, should be reported on one

Schedule A (Form 8975) that indicates the tax jurisdiction

“stateless.”

If a filer does not have either a U.S. Schedule A (Form 8975)

or a “stateless” Schedule A (Form 8975) that contains fiscally

transparent U.S. business entities, then the Form 8975 has

not been completed properly.

Part I—Identification of Filer

Use Part I to provide your identifying information.

Line 1a. Enter your complete legal name.

Line 1b. You are the reporting entity. Enter the code for your

reporting role. The reporting role indicates whether you are

filing as the ultimate parent entity of your group (enter code:

ULT) or if you are filing because you were designated by a

U.S. territory ultimate parent entity to file on its behalf (enter

code: SUR).

Line 1c. Enter your employer identification number (EIN).

Lines 2 and 3a through 3c. Enter your legal address.

Include the suite, room, or other unit number after the street

address. If the post office does not deliver mail to the street

address and you have a P.O. box, show the box number

instead.

Foreign address. Follow the country's practice for

entering the postal code, if any. Do not abbreviate the

country name.

Line 4. Enter the common name of the U.S. MNE group if it

is significantly different from the reporting entity's name on

line 1a.

Part II—Additional Information

You can enter additional information related to your group,

such as a narrative description of the overall business

operations and structure of your group or an overall

assumption or convention that you used which might have an

effect on your report. Any financial amounts entered in Part II

must be stated in U.S. dollars. You will have an opportunity to

enter specific information regarding financial information and

constituent entities in each tax jurisdiction on the appropriate

Schedule A (Form 8975).

If the additional information you choose to enter in Part II

will not fit in the allotted space, complete as many additional

page 2, Part II, Additional Information sections as you need,

and submit these additional page(s) with Form 8975.

Note. If the common name of the U.S. MNE group is

significantly different from the reporting entity’s name, explain

in the Additional Information section.

Specific Instructions for Schedule A

(Form 8975)

You must file a separate Schedule A (Form 8975) for each

tax jurisdiction in which your group has one or more

constituent entities resident. If you have any constituent

entities in your group that do not have a tax jurisdiction of

residence (that is, the constituent entity is “stateless”), then

you must also fill out a Schedule A (Form 8975) providing the

information for each constituent entity that is stateless,

reporting the financial and employee information in the

aggregate with respect to those stateless constituent entities,

and indicating that there is no tax jurisdiction by providing the

appropriate “stateless” code. See

Tax jurisdiction under Part

I—Tax Jurisdiction Information, later.

Instructions for Form 8975 (Rev.12-2020)

-3-

Page 4 of 7 Fileid: … ns/I8975/202012/A/XML/Cycle05/source 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

The financial amounts furnished should be based on

applicable financial statements, books and records

maintained with respect to the constituent entities, regulatory

financial statements, or records used for tax reporting or

internal management control purposes for an annual period

of each constituent entity ending with or within the reporting

period.

At the top of each Schedule A (Form 8975), enter the

reporting period, your name, and EIN. These should match

the information entered on Form 8975.

If a constituent entity in your group is the owner of another

constituent entity in your group that is stateless, then the

owner's share of such stateless entity's revenues and profits

should be aggregated with the information for the owner's tax

jurisdiction of residence.

At each level, the owner entity includes its share of the

stateless entity’s revenue and profits in the owner’s tax

jurisdiction of residence only if the owner has a tax

jurisdiction of residence (that is, only if the owner is not

stateless), and the amount of revenue of the top-tier stateless

entity from which the owner entity calculates its share should

include any allocations from stateless entities owned, directly

or indirectly, by the top-tier stateless entity, even if such

allocations are excluded from the intermediate stateless

entity’s revenue and profit.

Example. Assume US Corp is the ultimate parent entity

of a U.S. MNE group. US Corp owns 90% of partnership P1,

which in turn owns 80% of partnership P2. Both P1 and P2

do not have a tax jurisdiction of residence (that is, they are

stateless), each earns $100 of revenue and has no expenses

(P1’s $100 of revenue does not include its allocable share of

P2’s revenue), and neither creates a permanent

establishment (that is, taxable presence) in any tax

jurisdiction. Assume US Corp earns $100 of revenue, not

including its share of P1’s revenue, and has no expenses.

P2 has $100 of revenue and profit that is reflected on the

stateless Schedule A (Form 8975) revenue and profit lines.

P1 has $100 of revenue and profit that is reflected on the

stateless Schedule A (Form 8975) revenue and profit lines.

Since P1 is stateless, it does not include its share of P2’s

revenue and profit again on the stateless Schedule A (Form

8975) revenue or profit lines. The total revenue and profit on

the stateless Schedule A (Form 8975) is $200.

US Corp has $100 of revenue and profit, not including any

allocations from other constituent entities. Since US Corp

has a tax jurisdiction of residence, it includes its share of P1’s

revenue and profit on the Schedule A (Form 8975) for the

United States. P1’s revenue and profit, of which US Corp is

allocated 90%, includes any allocations from stateless

entities that P1 owns, even if such allocations were not

included on the stateless Schedule A (Form 8975) revenue

or profit lines. P1’s revenue and profit when determining US

Corp’s allocable share is $180 (P1’s own $100 of revenue

and profit plus 80% of P2’s revenue and profit, or $80). US

Corp is allocated 90% of $180, or $162, of revenue and profit

due to its ownership of P1. The total revenue and profit on

the United States Schedule A (Form 8975) revenue and profit

lines is US Corp’s own revenue and profit of $100 plus its

allocation of $162 of revenue and profit from P1, or $262.

Currency Translation

All currency amounts furnished must be in U.S. dollars. If an

exchange rate is used other than in accordance with U.S.

GAAP for translation to U.S. dollars, the exchange rate must

be indicated in Part III, Additional Information, on the

Schedule A (Form 8975) relating to the amounts that are not

translated in accordance with U.S. GAAP.

Multiple Schedules A (Form 8975) for a Single

Tax Jurisdiction

If you are filing on paper and the information you want to

enter for a single tax jurisdiction does not fit on a single

Schedule A (Form 8975), you can attach additional

Schedules A (Form 8975). Complete the additional

Schedules A (Form 8975) as follows.

Above Part I. Enter the reporting period beginning and

ending dates, the name of the reporting entity, and the EIN.

Part I. Enter the tax jurisdiction only. Do not complete lines

1 through 8 of Part I.

Part II. Complete Part II as needed to list all of the

constituent entities resident in the tax jurisdiction.

Part III. Enter a statement that indicates this is a

continuation sheet, the tax jurisdiction to which the

continuation sheet applies, and the page number of the

continuation sheets (for example, “Page 3 of 9”). Complete

the rest of Part III as necessary.

Part I—Tax Jurisdiction Information

For each tax jurisdiction in which one or more constituent

entities of your group is tax resident, you must provide

financial amounts and number of employees as an aggregate

of the information for the constituent entities resident in that

tax jurisdiction.

Tax jurisdiction. This field is mandatory. Enter the

two-letter code for the tax jurisdiction to which the

Schedule A (Form 8975) pertains. The country code for the

United States is “US” and the country code for “stateless” is

“X5.” All other country codes can be found at

IRS.gov/

CountryCodes.

Form 8975 and Schedule A (Form 8975) information is

exchanged using the OECD Country Code List that is based

on the ISO 3166-1 Standard. Although the country codes

found in the IRS link above contain the jurisdictions listed in

the table below, those jurisdictions do not correspond to a

valid OECD country code for purposes of exchanging the

information. Therefore, do not enter any of these country

codes on the tax jurisdiction line of Part I of Schedule A

(Form 8975).

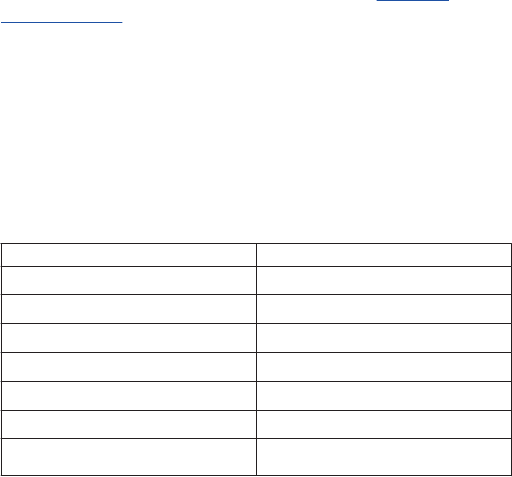

Tax Jurisdiction

Country Code

Akrotiri AX

Ashmore and Cartier Islands AT

Clipperton Island IP

Coral Sea Islands CR

Dhekelia DX

Paracel Islands PF

Spratly Islands PG

If the tax jurisdiction specified in the above list is

associated with a larger sovereignty, use the country code for

the larger sovereignty with which the tax jurisdiction is

associated (for example, Akrotiri and Dhekelia are

considered a British Overseas Territory so the country code

for the United Kingdom would be used (“UK”)). Otherwise,

-4-

Instructions for Form 8975 (Rev.12-2020)

Page 5 of 7 Fileid: … ns/I8975/202012/A/XML/Cycle05/source 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

use a separate Schedule A (Form 8975) for “other country”

using the tax jurisdiction code “OC.” In either case, you

should include in Part III of Schedule A (Form 8975) the

name of the specific constituent entity and the jurisdiction

where the constituent entity is located.

When you enter a country code in Schedule A (Form

8975), Part I, the financial and employee information

in Part I, the constituent entity information in Part II,

and the additional information in Part III, must pertain to the

constituent entities that are tax resident in that jurisdiction.

In Part I, you will provide the aggregate amounts for all of

the constituent entities listed in Part II.

Lines 1a through 1c. On line 1a, enter the aggregate

revenues of the constituent entities listed in Part II that are

generated from transactions with those that are not

constituent entities in your group. On line 1b, enter the

aggregate revenues of the constituent entities listed in Part II

that are generated from transactions with other constituent

entities in your group. On line 1c, enter the total aggregate

revenues of the constituent entities listed in Part II.

The term “revenue” includes all amounts of revenue,

including revenue from sales of inventory and property,

services, royalties, interest, and premiums.

Revenue does not include payments received from other

constituent entities in your group that are treated as

dividends in the payor's tax jurisdiction of residence.

Distributions and remittances from your constituent entities

that are partnerships, other fiscally transparent entities, or

permanent establishments are not considered revenue of the

recipient-owner.

Revenue also does not include imputed earnings or

deemed dividends from other constituent entities in your

group that are taken into account solely for tax purposes and

that otherwise would be included as revenue by a constituent

entity.

For a constituent entity that is an exempt organization,

revenue means only revenue that is reflected in unrelated

business taxable income. See Regulations section

1.6038-4(d)(3)(ii).

Line 2. Enter the aggregate profit or loss before income tax

of the constituent entities listed in Part II.

Consistent with the definition of revenue, profit or loss

before income tax does not include payments received from

other constituent entities in your group that are treated as

dividends in the payor's tax jurisdiction.

Note. An amount representing all or part of a constituent

entity's profit that is required or permitted for financial

reporting purposes to be included in the profit before tax of

another constituent entity in the group should be treated in

the same way as dividends from other constituent entities

and excluded from revenue and profit or loss before income

tax. This instruction does not apply where a constituent entity

includes in profit before tax for financial reporting purposes

an amount representing all or part of the profit of another

constituent entity in the group that is fiscally transparent.

Line 3. Enter the aggregate amount of income tax paid on a

cash basis to all tax jurisdictions by the constituent entities

listed in Part II and any taxes withheld on payments received

by the constituent entities listed in Part II.

Taxes paid should include taxes paid in cash by a

constituent entity listed in Part II to its tax jurisdiction and to

CAUTION

!

all other tax jurisdictions. Taxes paid should include

withholding taxes paid by other entities (whether related or

unrelated) with respect to payments to the constituent

entities in Part II.

Example. If, during a reporting period, Company X

(resident in tax jurisdiction X) generates operating income in

tax jurisdiction X that is subject to corporate income tax in tax

jurisdiction X and earns interest income from a company in

tax jurisdiction Y subject to withholding tax in tax jurisdiction

Y, the taxes paid to tax jurisdiction X on the operating income

and the tax withheld on the interest and paid to tax

jurisdiction Y should be reported as part of the income taxes

paid by Company X on the Schedule A (Form 8975) for tax

jurisdiction X.

Line 4. Enter the aggregate of the total accrued current

income tax expense recorded on taxable profits or losses,

reflecting only operations in the relevant annual period and

excluding deferred taxes or provisions for uncertain tax

liabilities, for the constituent entities listed in Part II.

When a constituent entity listed in Part II is a permanent

establishment, the amounts on line 3 and line 4 should not

include the income tax paid or current income tax expense

accrued by the business entity of which the permanent

establishment would otherwise be a part in that business

entity’s tax jurisdiction of residence on the income derived by

the permanent establishment. For example, if Company X

(resident in tax jurisdiction X) has a permanent establishment

“PE Y” in tax jurisdiction Y that is considered a constituent

entity, and Company X pays tax jurisdiction X income tax on

income earned by PE Y, then that income tax paid should be

reflected on the Schedule A (Form 8975) for tax jurisdiction

X. However, income tax paid to tax jurisdiction Y on income

earned by PE Y is not included on the Schedule A (Form

8975) for tax jurisdiction X, but rather on the Schedule A

(Form 8975) for tax jurisdiction Y.

Line 5. Enter the aggregate amount of the stated capital of

the constituent entities listed in Part II.

The stated capital of a permanent establishment must be

reported in the tax jurisdiction of residence of the legal entity

of which it is a permanent establishment unless there is a

defined capital requirement in the permanent establishment

tax jurisdiction for regulatory purposes.

Line 6. Enter the aggregate of total accumulated earnings of

the constituent entities listed in Part II. However, the

accumulated earnings of a permanent establishment are

considered those of the legal entity of which it is a permanent

establishment and should be reported on the Schedule A

(Form 8975) for the tax jurisdiction of the legal entity owner.

Line 7. Enter the aggregate number of employees on a

full-time equivalent basis of the constituent entities listed in

Part II. The number of employees may be reported as of the

year-end, on the basis of average employment levels for the

year, or on any other basis consistently applied across tax

jurisdictions of your group and from year to year.

Reasonable rounding or approximation of the number of

employees is permissible, provided that such rounding or

approximation does not materially distort the relative

distribution of employees across the various tax jurisdictions

of your group. Consistent approaches should be applied from

year to year and across entities.

Line 8. Enter the aggregate of the net book value of tangible

assets of all the constituent entities listed in Part II. For

Instructions for Form 8975 (Rev.12-2020)

-5-

Page 6 of 7 Fileid: … ns/I8975/202012/A/XML/Cycle05/source 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

purposes of this schedule, tangible assets do not include

cash or cash equivalents, intangibles, or financial assets.

For permanent establishments, assets should be reported

on the Schedule A (Form 8975) for the tax jurisdiction in

which the permanent establishment is located.

Part II—Constituent Entity

Information

In this section, you will provide constituent entity information

for your group regarding the constituent entities that have the

tax jurisdiction indicated in Part I. You should complete a row

for each constituent entity providing the information indicated

below.

Line 1. Enter the full legal name of the constituent entity,

including the domestic designation for the legal form, as

indicated in its articles of incorporation or any similar

document. If the constituent entity is a permanent

establishment, the naming convention to use is the name of

the constituent entity of which the permanent establishment

would be a part (if it were not its own constituent entity),

followed by “- (PE).” For instance, if XYZ Corp has a

permanent establishment, that permanent establishment’s

name would be “XYZ Corp - (PE).”

If filing electronically, the address of the constituent entity

may also be provided.

Line 2. Enter the entity role used by the constituent entity as

one of the following values.

•

CBC801 Ultimate Parent Entity

•

CBC802 Reporting Entity

•

CBC803 Both (Ultimate Parent Entity and Reporting Entity)

If the roles above do not apply to the constituent entity role,

leave blank.

Line 3. Enter the tax identification number (TIN), if any, used

for the constituent entity by the tax administration in the tax

jurisdiction of residence. The TIN is a mandatory field and

must be entered for each constituent entity. If the constituent

entity does not have a TIN, then enter “NOTIN.”

If filing electronically, one or more entity identification

numbers (IN), such as a company registration number, can

be provided, along with the IN’s issuer country and type.

Line 4. Using the two-letter code from the list at IRS.gov/

CountryCodes, enter the tax jurisdiction in which the

constituent entity is organized or incorporated if different from

the tax jurisdiction of residence. However, see

Tax

jurisdiction under Part I—Tax Jurisdiction Information, earlier,

for codes that are not allowed.

Line 5a. Identify the nature of the main business activity of

the constituent entity in the relevant tax jurisdiction by

selecting at least one of the following codes or categories.

•

CBC501 Research and development

•

CBC502 Holding or managing intellectual property

•

CBC503 Purchasing or procurement

•

CBC504 Manufacturing or production

•

CBC505 Sales, marketing, or distribution

•

CBC506 Administrative, management, or support services

•

CBC507 Provision of services to unrelated parties

•

CBC508 Internal group finance

•

CBC509 Regulated financial services

•

CBC510 Insurance

•

CBC511 Holding shares or other equity instruments

•

CBC512 Dormant

•

CBC513 Other

Those that do not file electronically are limited to indicating

a maximum of three main business activities. However, if you

feel this does not properly reflect the main businesses of a

constituent entity, you may use Part III, Additional

Information, on the appropriate Schedule A (Form 8975) to

enter additional codes and explain.

Line 5b. If you entered the code for “Other” on line 4a,

describe the “Other” business activity.

Part III—Additional Information

Briefly describe the sources of data used in preparing Parts I

and II of the Schedule A (Form 8975). The description should

be sufficient to enable an understanding of the source of

each item of information supplied on the Schedule A (Form

8975). The source(s) of data could include consolidation

reporting packages, separate entity financial statements,

regulatory financial statements, tax reporting records, or

internal management accounts reports. If a change is made

to the source of data used from year to year, explain the

reasons for the change and its consequences.

Additionally, you can enter any relevant information or

explanation that you deem necessary or that would facilitate

the understanding of the information provided in Parts I and

II. The information may or may not relate to a specific

constituent entity. The information may be used to explain

the tax jurisdiction financial and employee information in Part

I. You can use the item reference codes listed next to

indicate if the additional information relates to a specific item

in Part I.

•

CBC601 Revenues—unrelated party

•

CBC602 Revenues—related party

•

CBC603 Revenues—total

•

CBC604 Profit or loss

•

CBC605 Income tax paid

•

CBC606 Income tax accrued

•

CBC607 Stated capital

•

CBC608 Accumulated earnings

•

CBC609 Number of employees

•

CBC610 Tangible assets

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the

United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to

allow us to figure and collect the right amount of tax.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless

the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long

as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return

information are confidential, as required by section 6103.

The time needed to complete and file this form and related schedules will vary depending on individual circumstances. The

estimated burden for taxpayers filing this form is approved under OMB control number 1545-2272. The estimated burden for all

other taxpayers who file this form is shown below.

-6-

Instructions for Form 8975 (Rev.12-2020)

Page 7 of 7 Fileid: … ns/I8975/202012/A/XML/Cycle05/source 9:27 - 10-Sep-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Form 8975 and Schedule A (Form 8975) .................... 1hr., 30 min.

If you have comments concerning the accuracy of these time estimates or suggestions for making this form and related

schedule simpler, we would be happy to hear from you. See the instructions for the tax return with which this form is filed.

Instructions for Form 8975 (Rev.12-2020)

-7-