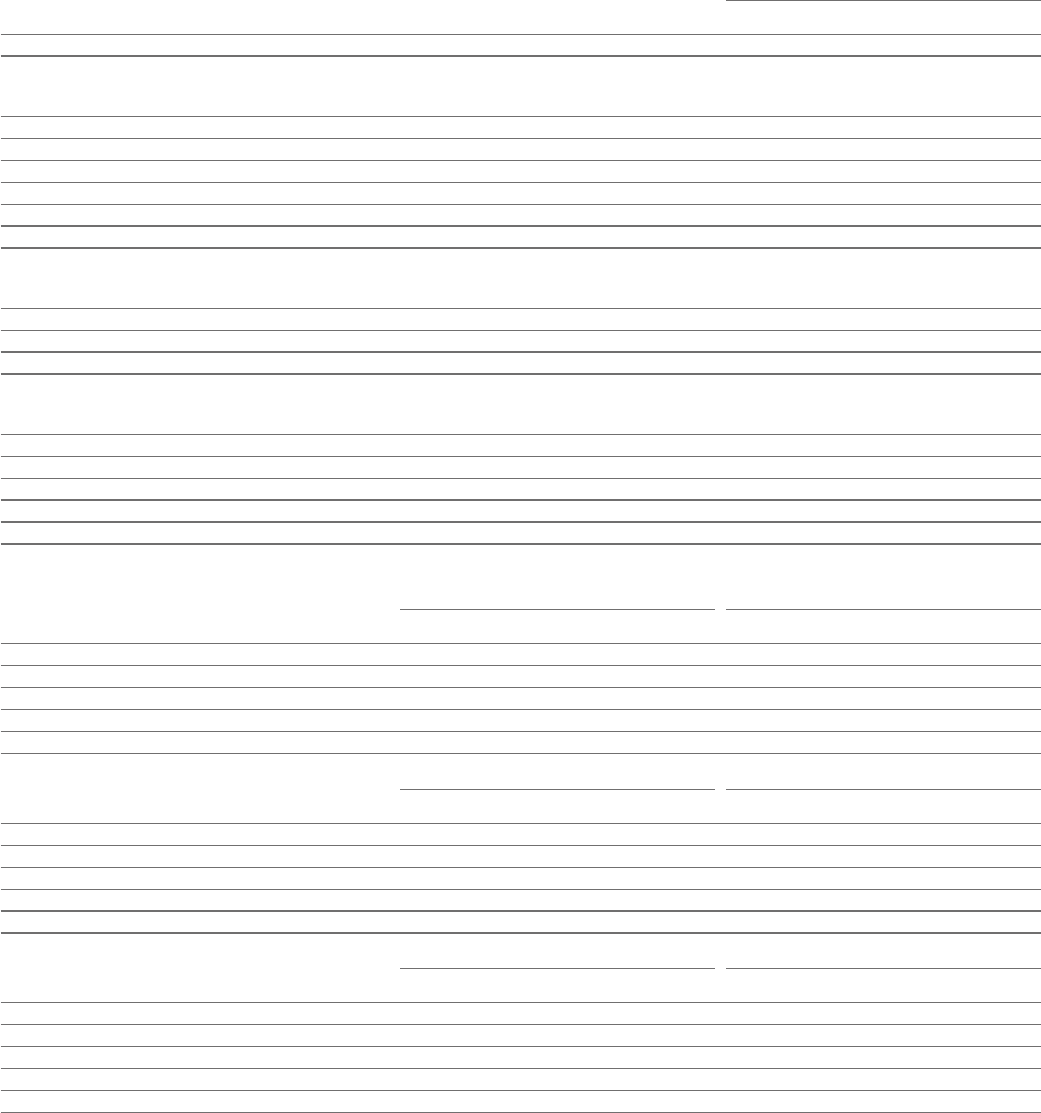

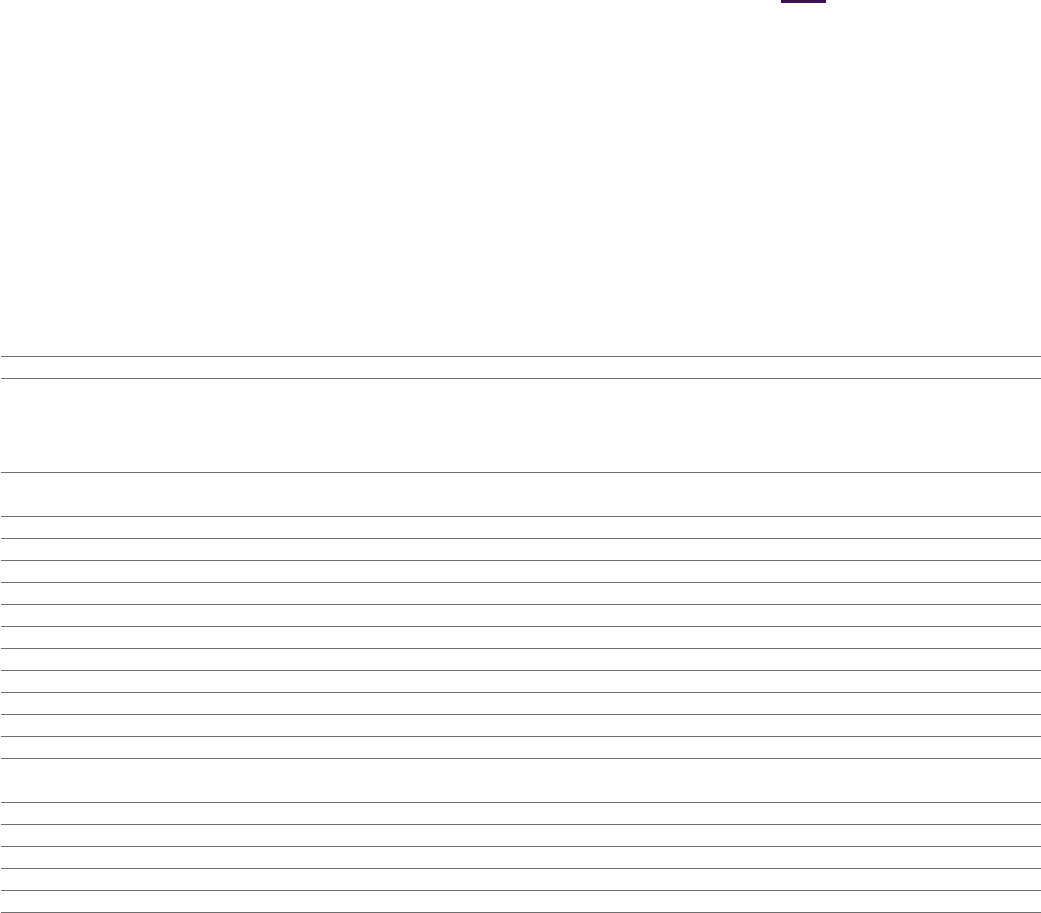

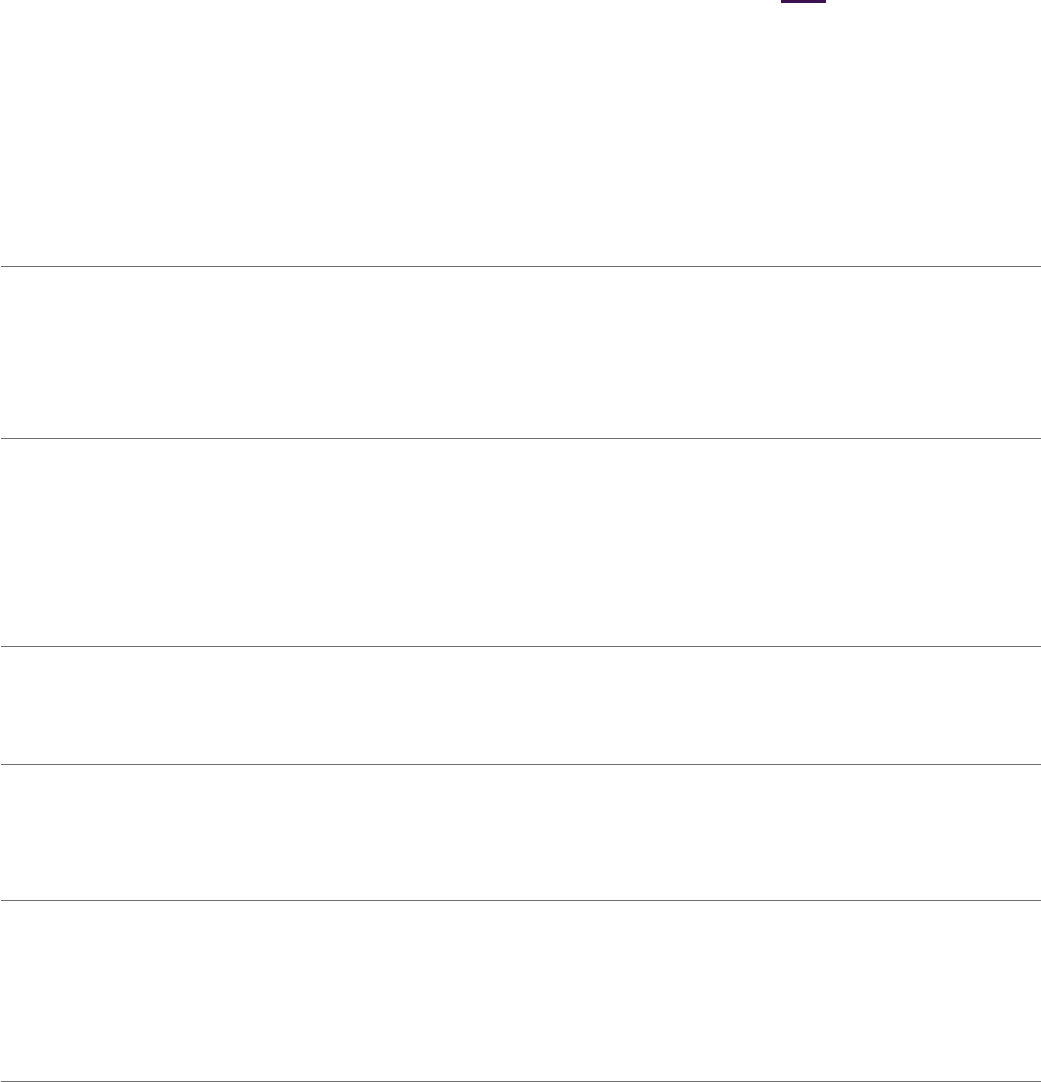

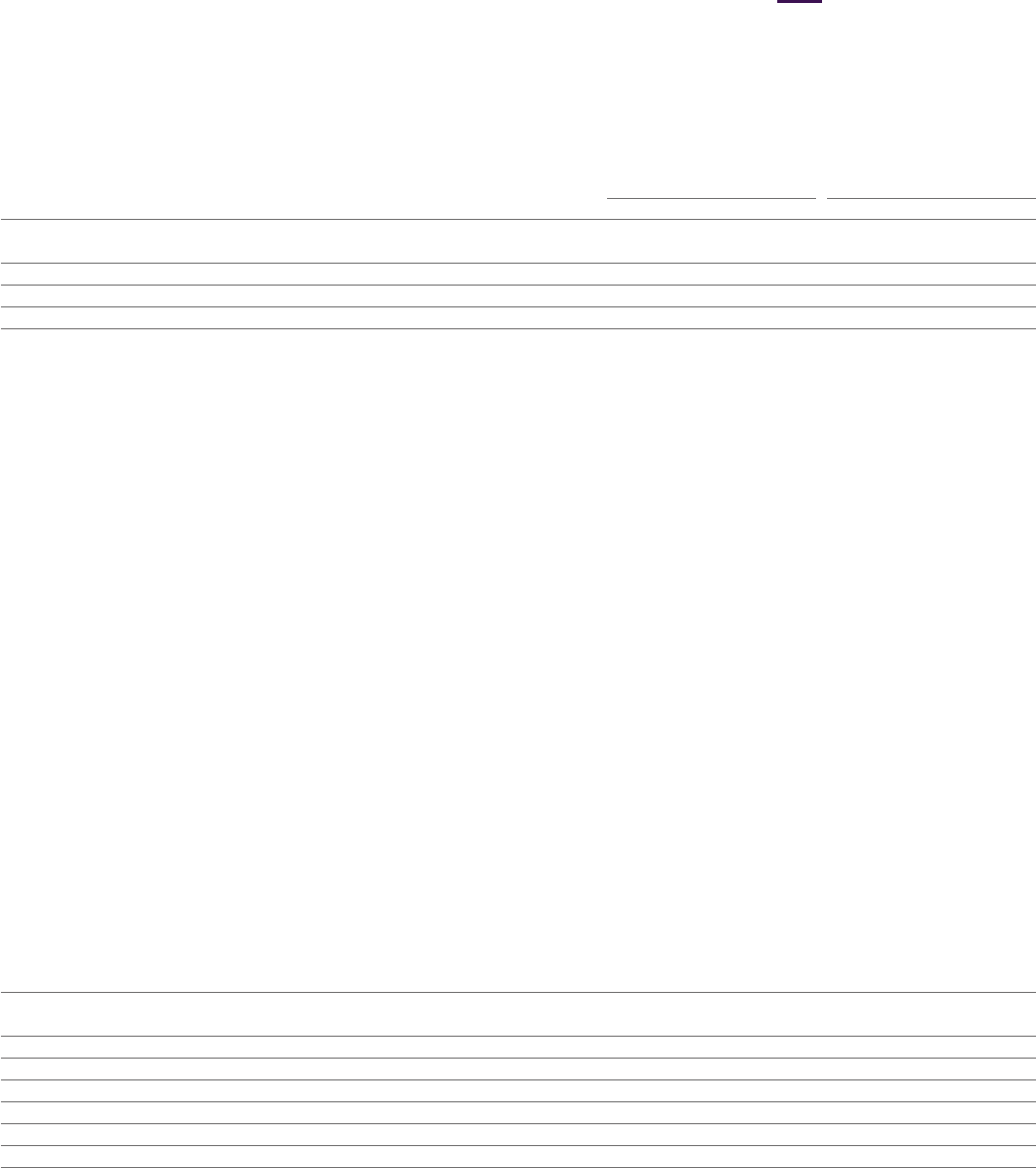

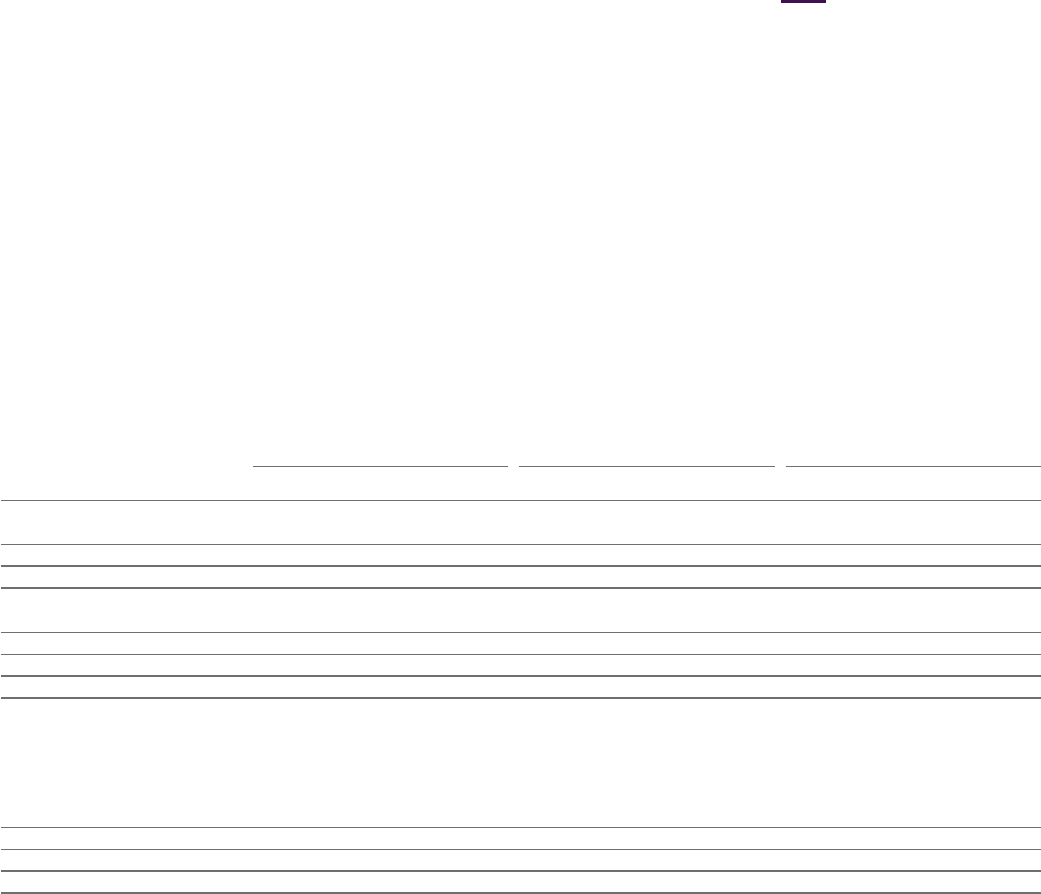

Consolidated Statement of Comprehensive Income

for the year ended 31December

2023 2022 2021

Notes $m $m $m

Product Sales 1 43,789 42,998 36,541

Alliance Revenue 1 1,428 755 388

Collaboration Revenue 1 594 598 488

Total Revenue 45,811 44,351 37,417

Cost of sales (8,268) (12,391) (12,437)

Gross profit 37,543 31,960 24,980

Distribution expense (539) (536) (446)

Research and development expense 2 (10,935) (9,762) (9,736)

Selling, general and administrative expense 2 (19,216) (18,419) (15,234)

Other operating income and expense 2 1,340 514 1,492

Operating profit 8,193 3,757 1,056

Finance income 3 344 95 43

Finance expense 3 (1,626) (1,346) (1,300)

Share of after tax losses in associates and joint ventures 11 (12) (5) (64)

Profit/(loss) before tax 6,899 2,501 (265)

Taxation 4 (938) 792 380

Profit for the period 5,961 3,293 115

Other comprehensive income:

Items that will not be reclassified to profit or loss:

Remeasurement of the defined benefit pension liability 22 (406) 1,118 626

Net gains/(losses) on equity investments measured at fair value through other comprehensive income 278 (88) (187)

Fair value movements related to own credit risk on bonds designated as fair value through profit or loss (6) 2 –

Tax on items that will not be reclassified to profit or loss 4 101 (216) 105

(33) 816 544

Items that may be reclassified subsequently to profit or loss:

Foreign exchange arising on consolidation 23 608 (1,446) (483)

Foreign exchange arising on designated liabilities in net investment hedges 23 24 (282) (321)

Fair value movements on cash flow hedges 266 (97) (167)

Fair value movements on cash flow hedges transferred to profit and loss (145) 73 208

Fair value movements on derivatives designated in net investment hedges 23 44 (8) 34

Costs of hedging (19) (7) (6)

Tax on items that may be reclassified subsequently to profit or loss 4 (12) 73 46

766 (1,694) (689)

Other comprehensive income/(expense) for the period, net of tax 733 (878) (145)

Total comprehensive income/(expense) for the period 6,694 2,415 (30)

Profit attributable to:

Owners of the Parent 5,955 3,288 112

Non-controlling interests 26 6 5 3

Total comprehensive income/(expense) attributable to:

Owners of the Parent 6,688 2,413 (33)

Non-controlling interests 26 6 2 3

Basic earnings per $0.25 Ordinary Share 5 $3.84 $2.12 $0.08

Diluted earnings per $0.25 Ordinary Share 5 $3.81 $2.11 $0.08

Weighted average number of Ordinary Shares in issue (millions) 5 1,549 1,548 1,418

Diluted weighted average number of Ordinary Shares in issue (millions) 5 1,562 1,560 1,427

Dividends declared and paid in the period 25 4,487 4,485 3,882

All activities were in respect of continuing operations.

$m means millions of US dollars.

148

AstraZeneca Annual Report & Form 20-F Information 2023 Financial Statements

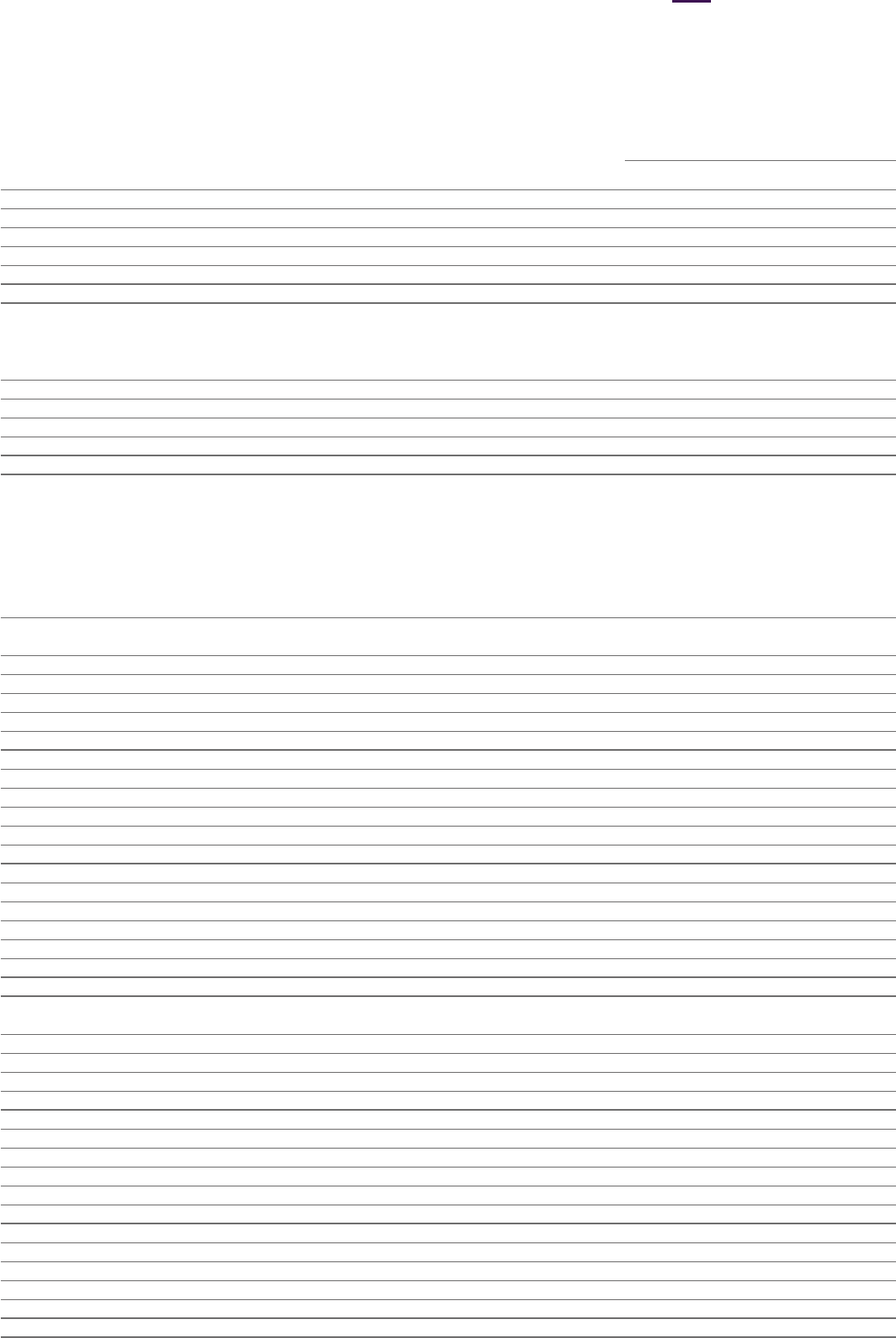

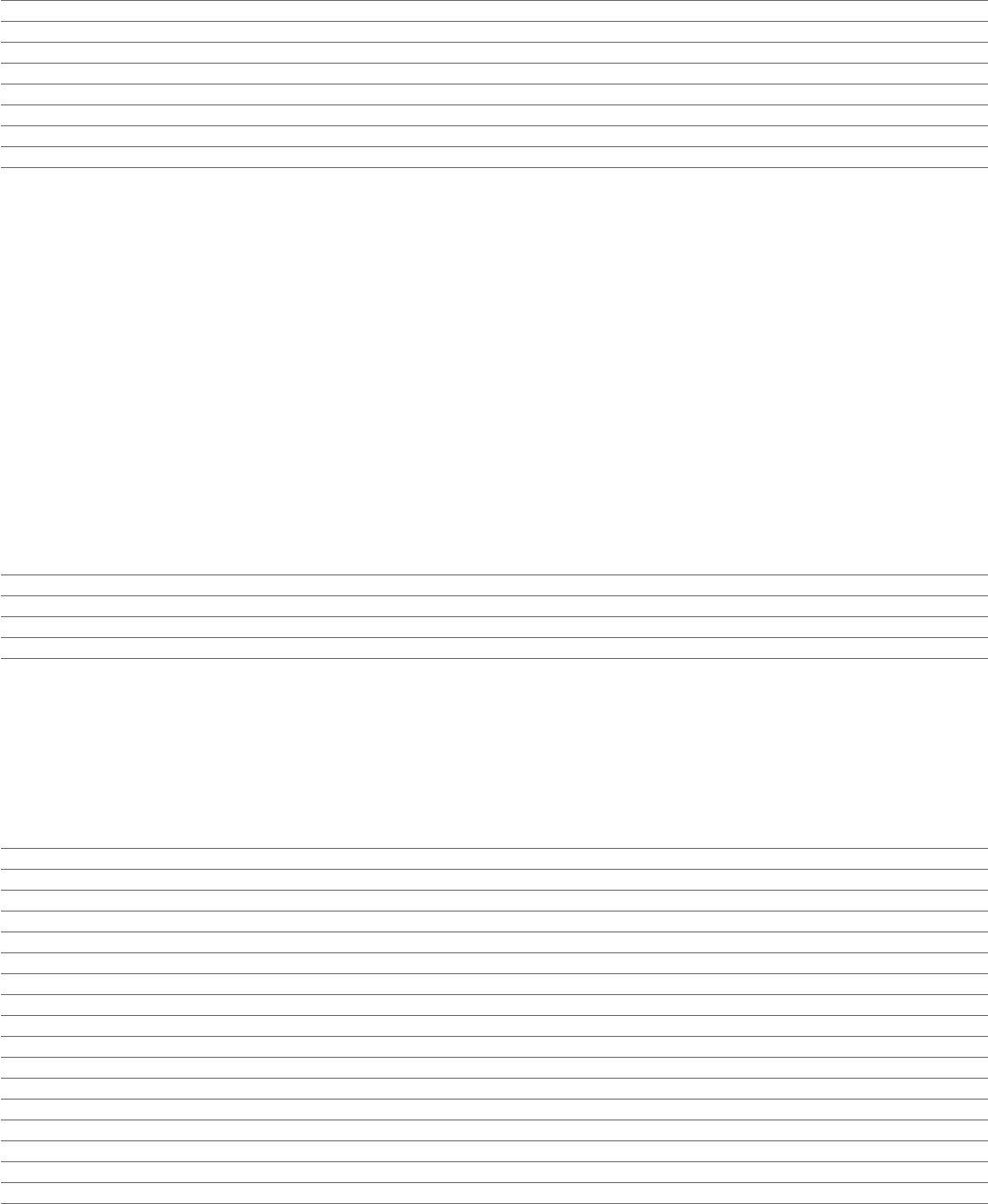

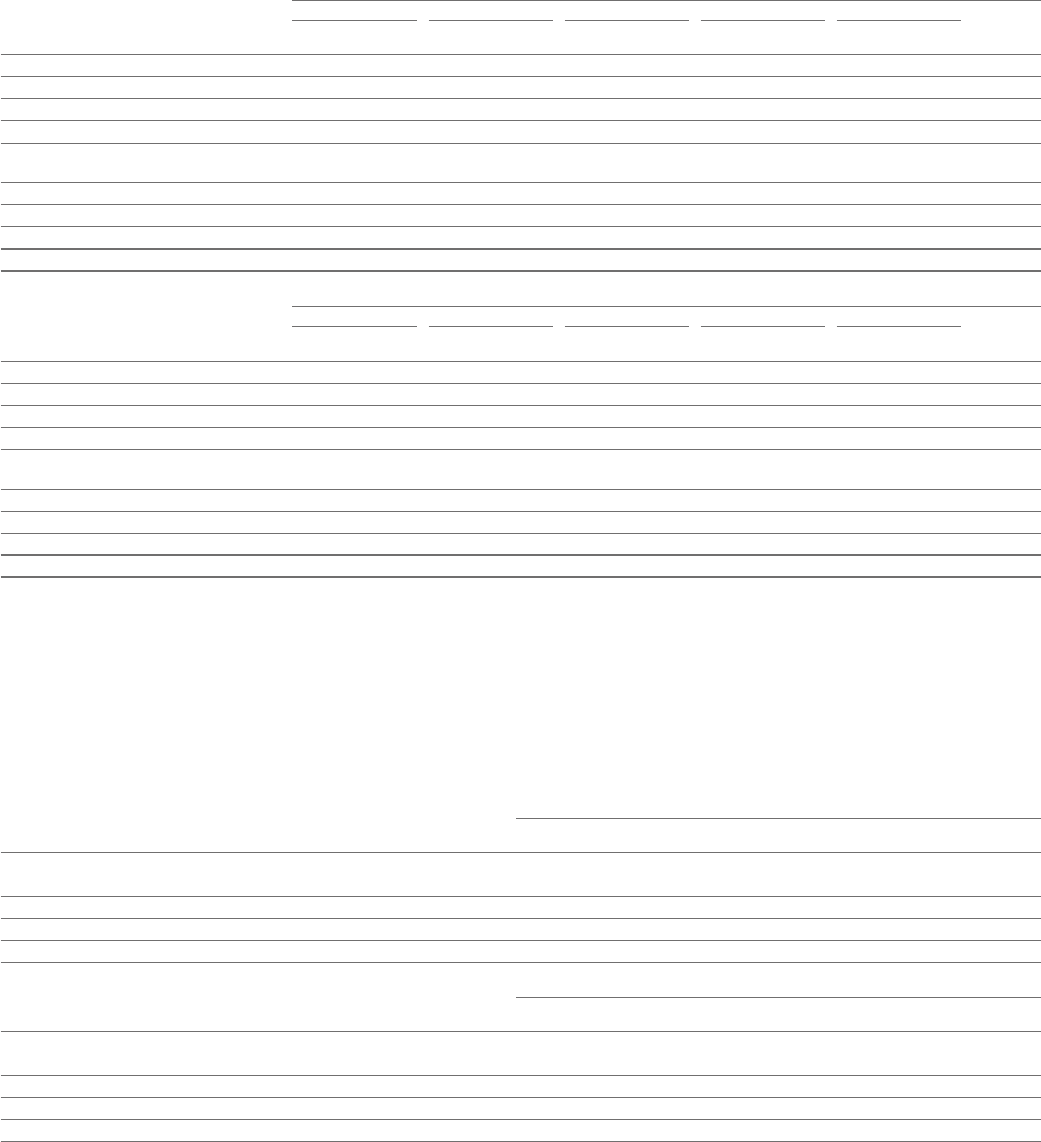

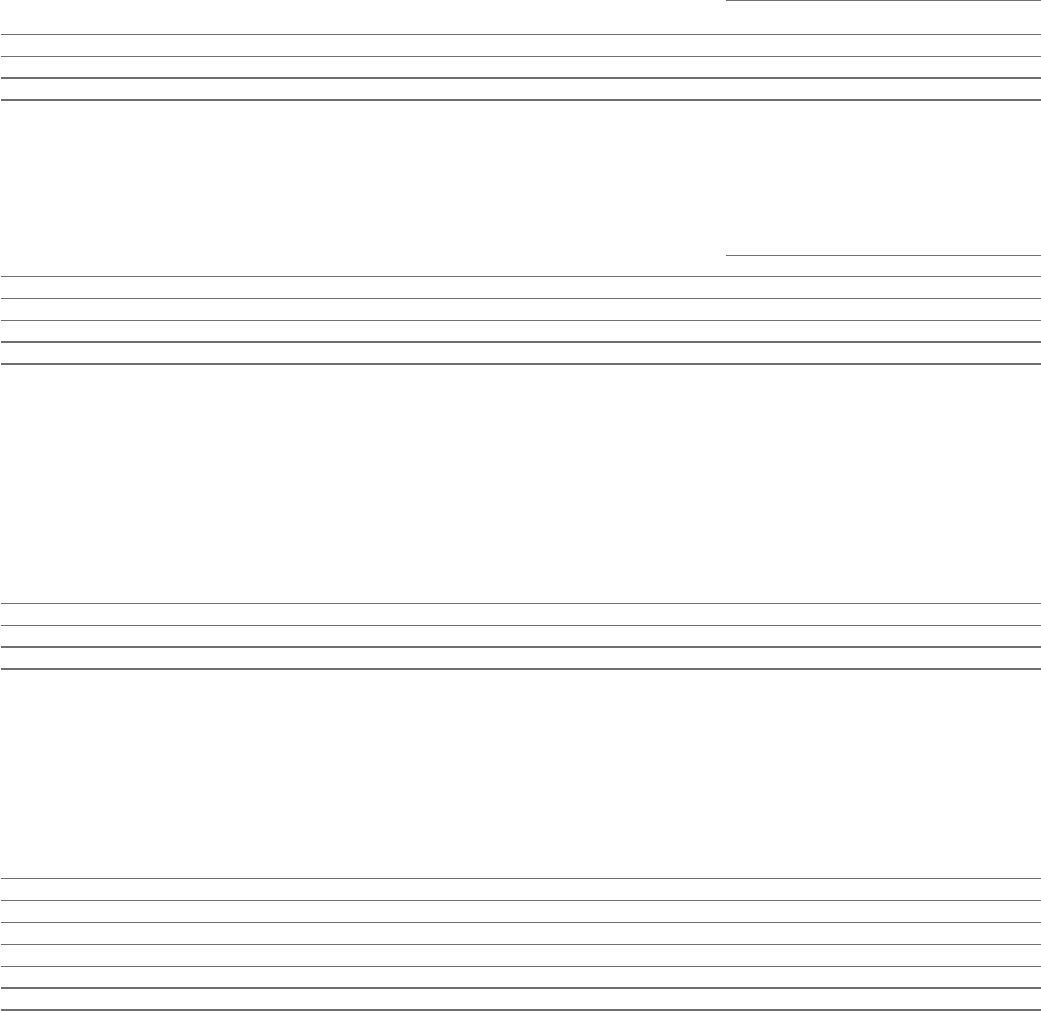

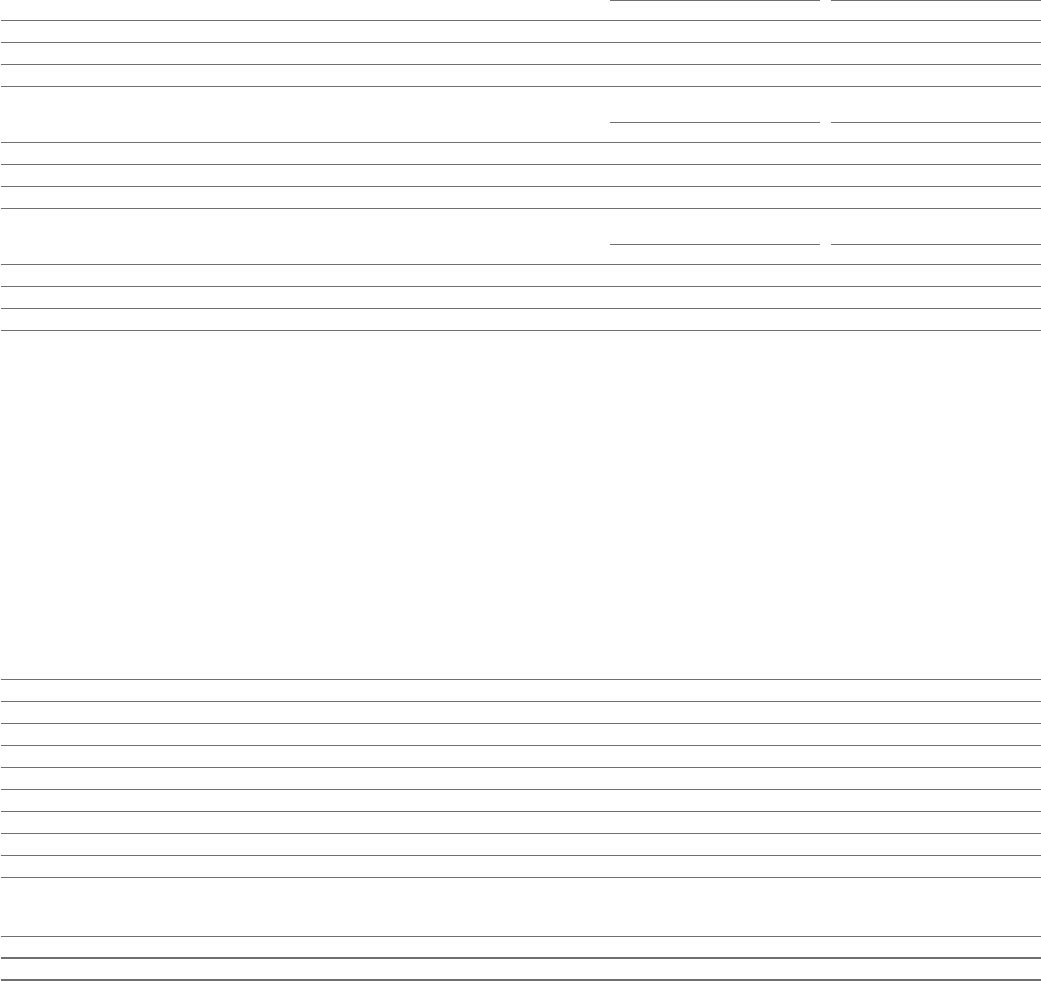

Consolidated Statement of Financial Position

at 31December

2023 2022 2021

Notes $m $m $m

Assets

Non-current assets

Property, plant and equipment 7 9,402 8,507 9,18 3

Right-of-use assets 8 1,100 942 988

Goodwill 9 20,048 19,820 19,997

Intangible assets 10 38,089 39,307 42,387

Investments in associates and joint ventures 11 147 76 69

Other investments 12 1,530 1,066 1,16 8

Derivative financial instruments 13 228 74 102

Other receivables 14 803 835 895

Deferred tax assets 4 4,718 3,263 4,330

76,065 73,890 79,119

Current assets

Inventories 15 5,424 4,699 8,983

Trade and other receivables 16 12,126 10,521 9,644

Other investments 12 122 239 69

Derivative financial instruments 13 116 87 83

Intangible assets 10 – – 105

Income tax receivable 1,426 731 663

Cash and cash equivalents 17 5,840 6,166 6,329

Assets held for sale 18 – 150 368

25,054 22,593 26,244

Total assets 101,119 96,483 105,363

Liabilities

Current liabilities

Interest-bearing loans and borrowings 19 (5,129) (5,314) (1,660)

Lease liabilities 8 (271) (228) (233)

Trade and other payables 20 (22,374) (19,040) (18,938)

Derivative financial instruments 13 (156) (93) (79)

Provisions 21 (1,028) (722) (768)

Income tax payable (1,584) (896) (916)

(30,542) (26,293) (22,594)

Non-current liabilities

Interest-bearing loans and borrowings 19 (22,365) (22,965) (28,134)

Lease liabilities 8 (857) (725) (754)

Derivative financial instruments 13 (38) (164) (45)

Deferred tax liabilities 4 (2,844) (2,944) (6,206)

Retirement benefit obligations 22 (1,520) (1,168) (2,454)

Provisions 21 (1,127) (896) (956)

Other payables 20 (2,660) (4,270) (4,933)

(31,411) (33,132) (43,482)

Total liabilities (61,953) (59,425) (66,076)

Net assets 39,166 37,058 39,287

Equity

Capital and reserves attributable to equity holders of the Company

Share capital 24 388 387 387

Share premium account 35,18 8 35,155 35,126

Capital redemption reserve 153 153 153

Merger reserve 448 448 448

Other reserves 23 1,464 1,468 1,444

Retained earnings 23 1,502 (574) 1,710

39,14 3 37,037 39,268

Non-controlling interests 26 23 21 19

Total equity 39,166 37,058 39,287

The Financial Statements from pages 148 to 215 were approved by the Board and were signed on its behalf by

Pascal Soriot Aradhana Sarin

Director Director

8 February 2024

Consolidated Statement of Financial Position 149AstraZeneca Annual Report & Form 20-F Information 2023

Corporate Governance Additional InformationFinancial StatementsStrategic Report

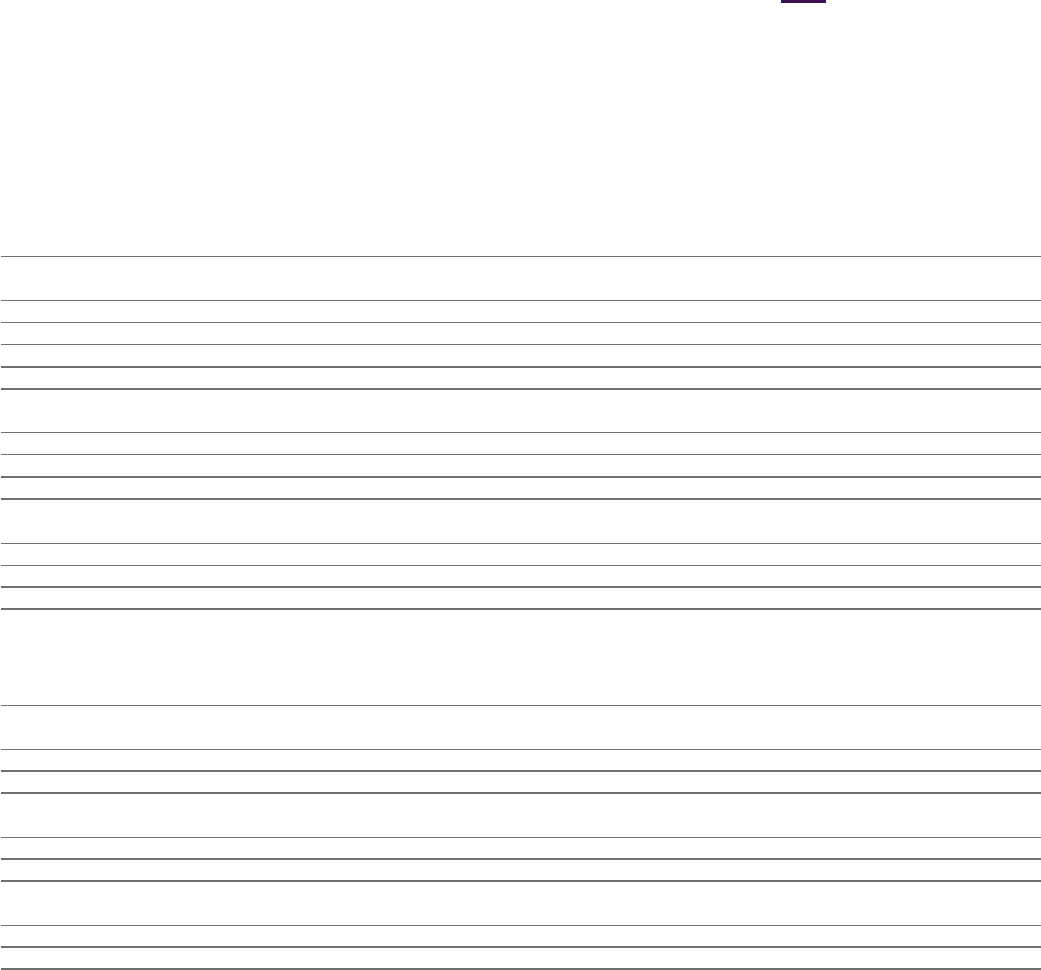

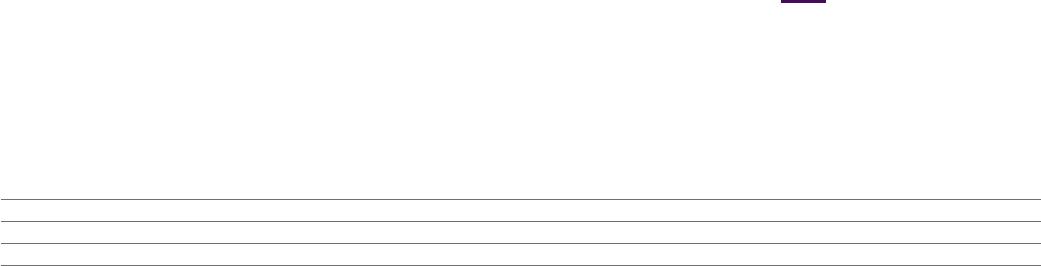

Consolidated Statement of Changes in Equity

for the year ended 31December

Share Capital Total Non-

Share premium redemption Merger Other Retained attributable controlling Total

capital account reserve reserve reserves earnings toowners interests equity

$m $m $m $m $m $m $m $m $m

At 1January 2021 328 7,971 153 448 1,423 5,299 15,622 16 15,638

Profit for the period – – – – – 112 112 3 115

Other comprehensive expense

1

– – – – – (145) (145) – (145)

Transfer to other reserves

2

– – – – 21 (21) – – –

Transactions with owners

Dividends (Note 25) – – – – – (3,882) (3,882) – (3,882)

Issue of Ordinary Shares 59 27,155 – – – – 27, 214 – 27, 214

Share-based payments charge for the period (Note 29) – – – – – 615 615 – 615

Settlement of share plan awards – – – – – (781) (781) – (781)

Issue of replacement Alexion share awards upon

acquisition (Note 27)

3

– – – – – 513 513 – 513

Net movement 59 27,155 – – 21 (3,589) 23,646 3 23,649

At 31December 2021 387 35,126 153 448 1,444 1,710 39,268 19 39,287

Profit for the period – – – – – 3,288 3,288 5 3,293

Other comprehensive expense

1

– – – – – (875) (875) (3) (878)

Transfer to other reserves

2

– – – – 24 (24) – – –

Transactions with owners

Dividends (Note 25) – – – – – (4,485) (4,485) – (4,485)

Issue of Ordinary Shares – 29 – – – – 29 – 29

Share-based payments charge for the period (Note 29) – – – – – 619 619 – 619

Settlement of share plan awards – – – – – (807) (807) – (807)

Net movement – 29 – – 24 (2,284) (2,231) 2 (2,229)

At 31December 2022 387 35,155 153 448 1,468 (574) 37,037 21 37,0 5 8

Profit for the period – – – – – 5,955 5,955 6 5,961

Other comprehensive income

1

– – – – – 733 733 – 733

Transfer to other reserves

2

– – – – (4) 4 – – –

Transactions with owners

Dividends (Note 25) – – – – – (4,487) (4,487) – (4,487)

Dividends paid to non-controlling interests (Note 25) – – – – – – – (4) (4)

Issue of Ordinary Shares 1 33 – – – – 34 – 34

Share-based payments charge for the period (Note 29) – – – – – 579 579 – 579

Settlement of share plan awards – – – – – (708) (708) – (708)

Net movement 1 33 – – (4) 2,076 2 ,10 6 2 2,108

At 31December 2023 388 35,188 153 448 1,464 1,502 39,143 23 39,166

150 AstraZeneca Annual Report & Form 20-F Information 2023 Financial Statements

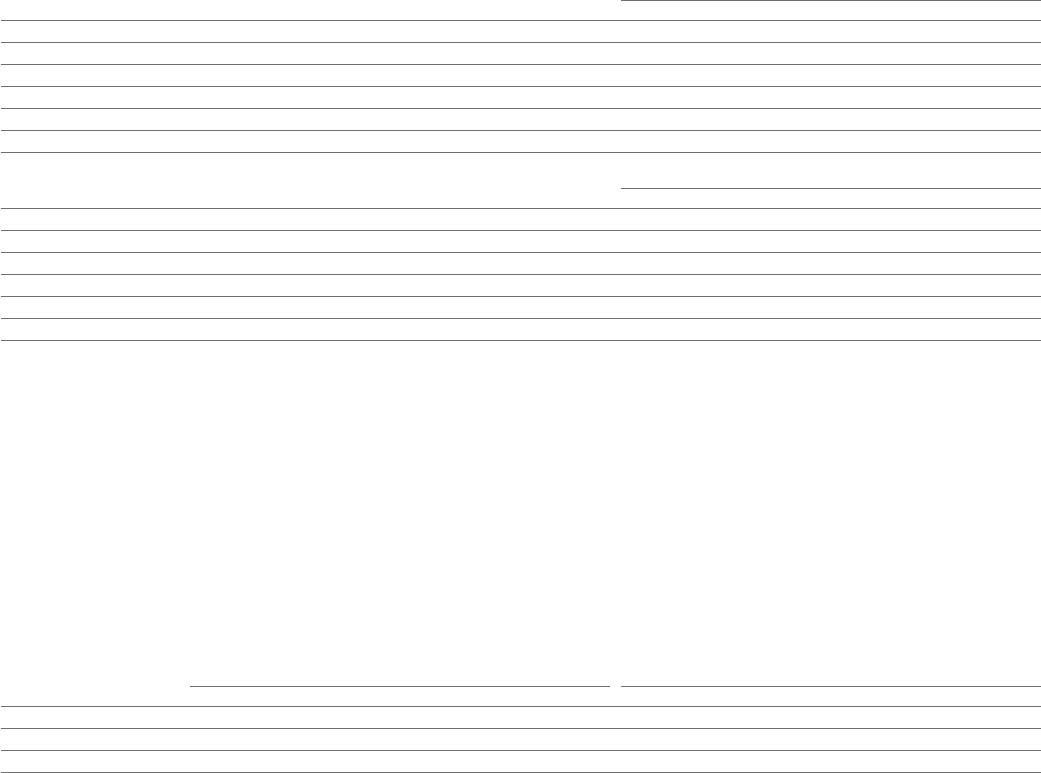

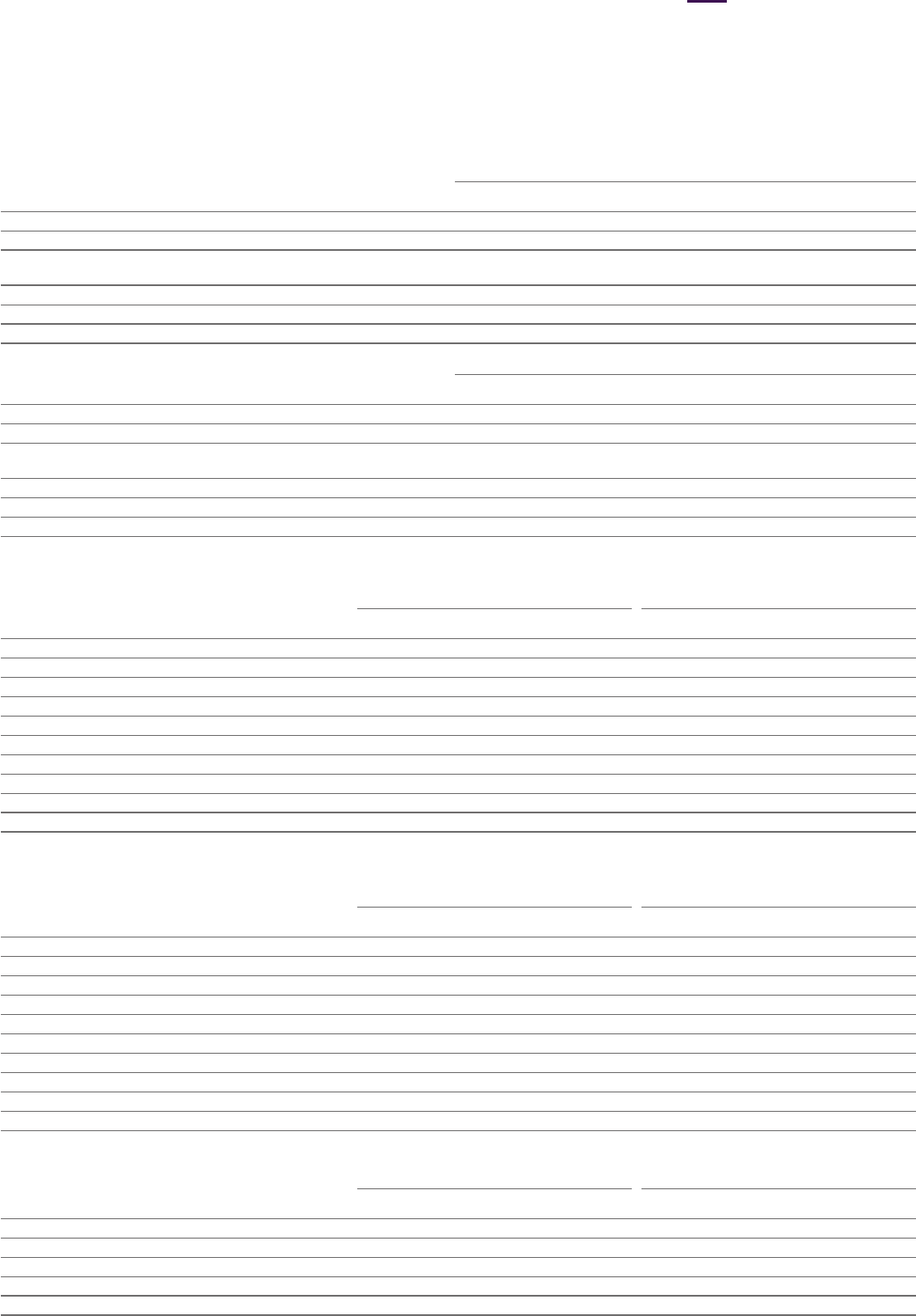

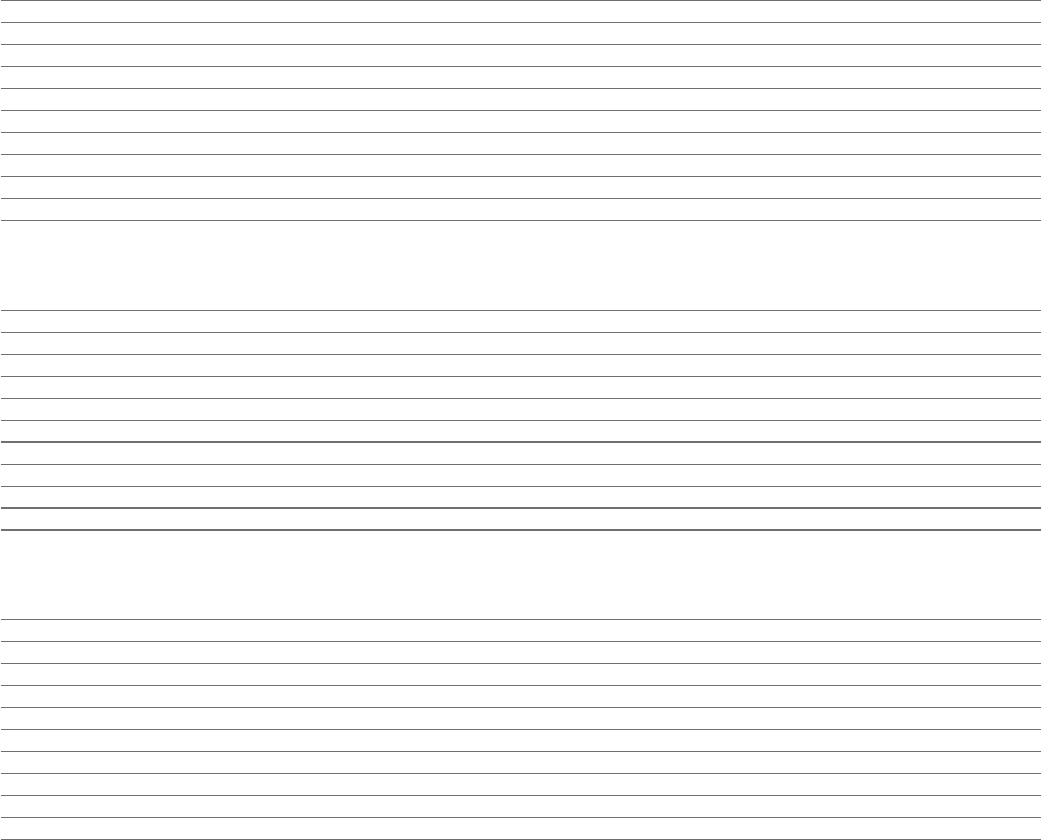

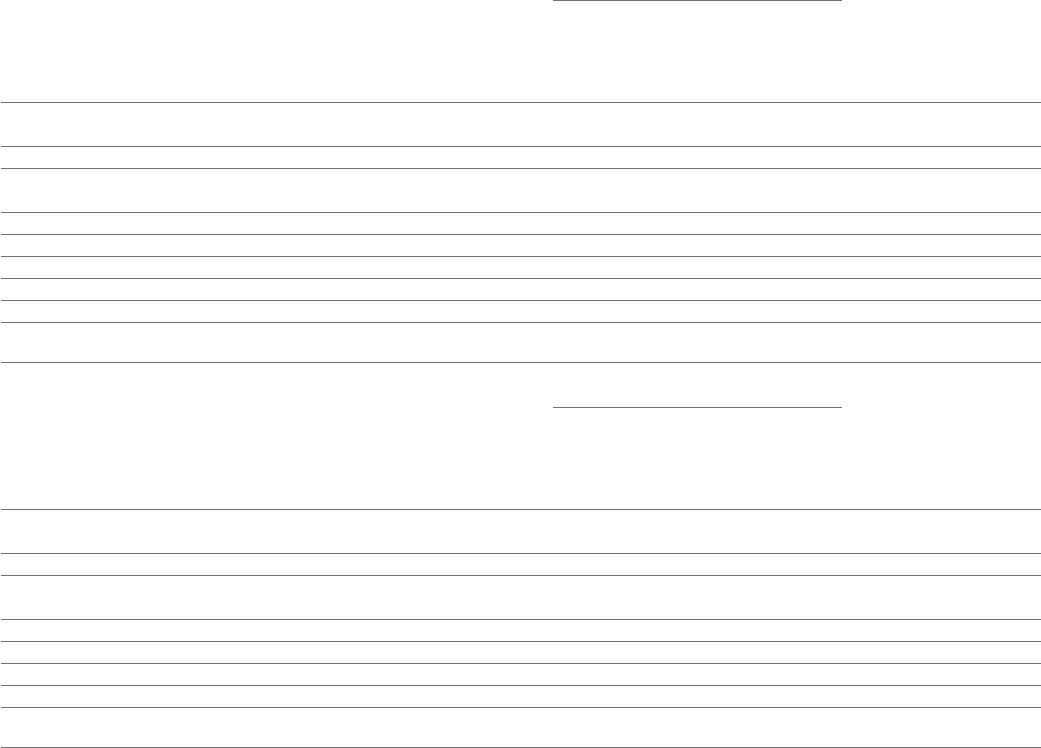

Consolidated Statement of Cash Flows

for the year ended 31December

2023 2022 2021

Notes $m $m $m

Cash flows from operating activities

Profit/(loss) before tax 6,899 2,501 (265)

Finance income and expense 3 1,282 1,251 1,257

Share of after tax losses of associates and joint ventures 11 12 5 64

Depreciation, amortisation and impairment 5,387 5,480 6,530

Increase in trade and other receivables (1,425) (1,349) (961)

(Increase)/decrease in inventories (669) 3,941 1,577

Increase in trade and other payables and provisions 2,394 1,165 1,405

Gains on disposal of intangible assets 2 (251) (104) (513)

Gains on disposal of investments in associates and joint ventures 2 – – (776)

Fair value movements on contingent consideration arising from business combinations 20 549 82 14

Non-cash and other movements 17 (386) (692) 95

Cash generated from operations 13,792 12,280 8,427

Interest paid (1,081) (849) (721)

Tax paid (2,366) (1,623) (1,743)

Net cash inflow from operating activities 10,345 9,808 5,963

Cash flows from investing activities

Acquisition of subsidiaries, net of cash acquired 27 (189) (48) (9,263)

Payments upon vesting of employee share awards attributable to business combinations 27 (84) (215) (211)

Payment of contingent consideration from business combinations 20 (826) (772) (643)

Purchase of property, plant and equipment (1,361) (1,091) (1,091)

Disposal of property, plant and equipment 132 282 13

Purchase of intangible assets (2,417) (1,480) (1,109)

Disposal of intangible assets 291 447 587

Movement in profit-participation liability 2 190 – 20

Purchase of non-current asset investments (136) (45) (184)

Disposal of non-current asset investments 32 42 9

Movement in short-term investments, fixed deposits and other investing instruments 97 (114) 96

Payments to associates and joint ventures 11 (80) (26) (92)

Disposal of investments in associates and joint ventures – – 776

Interest received 287 60 34

Net cash outflow from investing activities (4,064) (2,960) (11,05 8)

Net cash inflow/(outflow) before financing activities 6,281 6,848 (5,095)

Cash flows from financing activities

Proceeds from issue of share capital 33 29 29

Issue of loans and borrowings 3,816 – 12,929

Repayment of loans and borrowings (4,942) (1,271) (4,759)

Dividends paid (4,481) (4,364) (3,856)

Hedge contracts relating to dividend payments (19) (127) (29)

Repayment of obligations under leases (268) (244) (240)

Movement in short-term borrowings 161 74 (276)

Payments to acquire non-controlling interests – – (149)

Payment of Acerta Pharma share purchase liability (867) (920) –

Net cash (outflow)/inflow from financing activities (6,567) (6,823) 3,649

Net (decrease)/increase in Cash and cash equivalents in the period (286) 25 (1,446)

Cash and cash equivalents at the beginning of the period 5,983 6,038 7, 5 4 6

Exchange rate effects (60) (80) (62)

Cash and cash equivalents at the end of the period 17 5,637 5,983 6,038

Consolidated Statement of Cash Flows 151AstraZeneca Annual Report & Form 20-F Information 2023

Corporate Governance Additional InformationFinancial StatementsStrategic Report

Group Accounting Policies

Basis of accounting and preparation

offinancial information

The Consolidated Financial Statements

have been prepared under the historical cost

convention, modified to include revaluation to

fair value of certain financial instruments and

pension plan assets and liabilities as described

below, in accordance with UK-adopted

international accounting standards and with

the requirements of the Companies Act 2006

as applicable to companies reporting under

those standards. The Consolidated Financial

Statements also comply fully with IFRS

Accounting Standards as issued by the

International Accounting Standards Board

(IASB) and International Accounting Standards

as adopted by the European Union.

The Consolidated Financial Statements are

presented in US dollars, which is the Company’s

functional currency.

In preparing their individual financial statements,

the accounting policies of some overseas

subsidiaries do not conform with IASB-

issued IFRSs. Therefore, where appropriate,

adjustments are made in order to present the

Consolidated Financial Statements on a

consistent basis.

New accounting requirements

Other than noted below, amendments to

accounting standards issued by the IASB and

adopted in the year ended 31 December 2023

did not have a material impact on the result or

financial position of the Group.

IAS12

On 23 May 2023, the IASB issued an

amendment to IAS 12 ‘Income Taxes’ to clarify

how the effects of the global minimum tax

framework should be accounted for and

disclosed effective 1 January 2023. This was

endorsed by the UK Endorsement Board on

19 July 2023 and has been adopted by the

Group for 2023 reporting. The Group has

applied the exemption to recognising and

disclosing information about deferred tax

assets and liabilities related to Pillar 2

income taxes.

Alliance and Collaboration Revenue

Effective 1 January 2023, the Group has

updated the presentation of Total Revenue on

the face of the Statement of Comprehensive

Income to include Alliance Revenue as a

separate element to Collaboration Revenue.

Alliance Revenue, previously reported within

Collaboration Revenue, comprises income

related to sales made by collaboration partners,

where AstraZeneca is entitled to a share of

gross profits, share of revenues or royalties,

which are recurring in nature while the

collaboration arrangement remains in place.

Alliance Revenue does not include Product

Sales where AstraZeneca is leading

commercialisation in a territory.

Collaboration Revenue arising from

collaborative arrangements where the Group

retains a significant ongoing economic interest

and receives upfront amounts and event-

triggered milestones, which arise from the

licensing of intellectual property, will continue

to be reported as Collaboration Revenue. In

collaboration arrangements either AstraZeneca

or the collaborator acts as principal in sales to

the end customer. Where AstraZeneca acts as

principal, AstraZeneca records 100% of sales

to the end customer within Product Sales. The

updated presentation reflects the increasing

importance of income arising from share of

gross profit arrangements where collaboration

partners are responsible for booking revenues

in some or all territories.

The comparative revenue reported in the

years to 31 December 2022 and 31 December

2021 has been retrospectively adjusted to

reflect the new split of Total Revenue, resulting

in Alliance Revenue being reported for the

year to 31 December 2022 of $755m and to

31 December 2021 of $388m, however the

combined total of Alliance Revenue and

Collaboration Revenue is equal to the

previously reported Collaboration Revenue

total for each prior year.

Basis for preparation of Financial

Statements on a going concern basis

The Group has considerable financial resources

available. As at 31 December 2023, the Group

has $12.7bn in financial resources (Cash and

cash equivalent balances of $5.8bn and

undrawn committed bank facilities of $6.9bn,

of which $2.0bn are available until February

2025 and the remaining $4.9bn are available

until April 2026, (in February 2024 these

facilities were extended to April 2029), with only

$5.4bn of borrowings due within one year).

The Group’s revenues are largely derived from

sales of medicines covered by patents, which

provide a relatively high level of resilience

and predictability to cash inflows, although

government price interventions in response to

budgetary constraints are expected to

continue to adversely affect revenues in some

of our significant markets. The Group,

however, anticipates new revenue streams

from both recently launched medicines and

those in development, and the Group has a

wide diversity of customers and suppliers

across different geographic areas.

Consequently, the Directors believe that, overall,

the Group is well placed to manage its business

risks successfully. Accordingly, they continue

to adopt the going concern basis in preparing

the Annual Report and Financial Statements.

Estimates and judgements

The preparation of the Financial Statements in

conformity with generally accepted accounting

principles requires management to make

estimates and judgements that affect the

reported amounts of assets and liabilities at

the date of the Financial Statements and the

reported amounts of revenues and expenses

during the reporting period. Actual results

could differ from those estimates.

The accounting policy descriptions set out the

areas where judgements and estimates need

exercising, the most significant of which

include the following Key Judgements

and

Significant Estimates :

> revenue recognition – see Revenue

Accounting Policy from page 152 and

Note 1 on page 161

> expensing of internal development expenses

– see Research and Development Policy

from page 154

> impairment reviews of Intangible assets

– see Note 10 on page 174

> useful economic life of Intangible assets –

see Research and Development Policy

from page 154

> business combinations and Goodwill –

see Business Combinations and Goodwill

Policy from page 156 and Note 27 from

page 193

> litigation liabilities – see Litigation and

Environmental Liabilities within Note 30

on page 204

> operating segments – see Note 6 on

page 167

> employee benefits – see Note 22 on

page 190

> taxation – see Note 30 from page 209 .

The Group has assessed the impact of climate

risk on its financial reporting. The impact

assessment was primarily focused on the

valuation and useful lives of intangible assets

and the identification and valuation of provisions

and contingent liabilities, as these are judged

to be the key areas that could be impacted by

climate risks. No material accounting impacts

or changes to judgements or other required

disclosures were noted.

Key Judgements are those judgements

made in applying the Group’s accounting

policies that have a material effect on the

amounts of assets and liabilities recognised

in the Financial Statements.

A Significant Estimate has a significant

risk of material adjustment to the carrying

amounts of assets and liabilities within the

next financial year.

Financial risk management policies are detailed

in Note 28 to the Financial Statements from

page 195.

AstraZeneca’s management considers the

following to be the material accounting policies

in the context of the Group’s operations.

Revenue

Revenue comprises Product Sales, Alliance

Revenue and Collaboration Revenue.

Revenue excludes inter-company revenues

and value-added taxes.

152

AstraZeneca Annual Report & Form 20-F Information 2023 Financial Statements

Product Sales

Product Sales represent net invoice value less

estimated rebates, returns and chargebacks,

which are considered to be variable

consideration and include significant estimates.

Sales are recognised when the control of the

goods has been transferred to a third party.

This is usually when title passes to the

customer, either on shipment or on receipt of

goods by the customer, depending on local

trading terms. Revenue is not recognised in

full until it is highly probable that a significant

reversal in the amount of cumulative revenue

recognised will not occur.

Rebates are amounts payable or credited to

a customer, usually based on the quantity or

value of Product Sales to the customer for

specific products in a certain period. Product

sales rebates, which relate to Product Sales

that occur over a period of time, are normally

issued retrospectively.

At the time Product Sales are invoiced, rebates

and deductions that the Group expects to

pay are estimated based upon assumptions

developed using contractual terms, historical

experience and market-related information.

The rebates and deductions are recognised

as variable consideration and recorded as a

reduction to revenue with an accrual recorded.

These rebates typically arise from sales

contracts with government payers, third-party

managed care organisations, hospitals,

long-term care facilities, group purchasing

organisations and various state programmes.

In markets where returns are significant,

estimates of the quantity and value of goods

which may ultimately be returned are accounted

for at the point revenue is recognised. Our

returns accruals are based on actual experience

over the preceding 12 months for established

products together with market-related

information such as estimated stock levels

at wholesalers and competitor activity which

we receive via third-party information services.

For newly launched products, we use rates

based on our experience with similar products

or a predetermined percentage.

When a product faces generic competition,

particular attention is given to the possible

levels of returns and, in cases where the

circumstances are such that the level of

Product Sales are considered highly probable

to reverse, revenues are only recognised when

the right of return expires, which is generally on

ultimate prescription of the product to patients.

The methodology and assumptions used to

estimate rebates and returns are monitored

and adjusted regularly in the light of contractual

and legal obligations, historical trends, past

experience and projected market conditions.

Once the uncertainty associated with returns

is resolved, revenue is adjusted accordingly.

Under certain collaboration agreements

which include a profit sharing mechanism, our

recognition of Product Sales depends on which

party acts as principal in sales to the end

customer. In the cases where AstraZeneca

acts as principal, we record 100% of sales

to the end customer. In the cases where

AstraZeneca does not act as principal, we

record the share of gross profits received

within Alliance Revenue.

Contracts relating to the supply of certain

Vaccines & Immune Therapies medicines

relating to the COVID-19 pandemic include

conditions whereby payments are receivable

from customers in advance of the delivery of

product. Such amounts are held on the balance

sheet as contract liabilities until the related

revenue is recognised, generally upon product

delivery. Certain of these contracts contain

further provisions that restrict the use of

inventory manufactured in specified supply

chains to specified customers, resulting in an

enforceable right to payment as the activities

are performed. Under IFRS 15, such contracts

require revenue to be recognised over time

using an appropriate and reasonably

measurable method to measure progress.

Revenue is recognised on these contracts

based on the proportion of product delivered

compared to the total contracted volumes.

Certain arrangements include bill-and-hold

arrangements under which the Group invoices

a customer for a product but retains physical

possession of the product until it is transferred

to the customer at a point in time in the future.

For these types of arrangements, an

assessment is made to determine when the

performance obligation has been satisfied,

which is when control of the product is

transferred to the customer. If the customer has

obtained control of the product even though

that product remains in the Group’s physical

possession, the performance obligation to

transfer a product has been satisfied and

Product Sales are recognised. Control is

considered to have transferred when the

reason for the bill-and-hold arrangement is

substantive, the product can be identified

separately as belonging to the customer, the

product is ready for physical transfer to the

customer and AstraZeneca is unable to use

or sell the product to another customer.

Alliance Revenue

Alliance Revenue comprises income arising

from the ongoing operation of collaborative

arrangements related to sales made by

collaboration partners, where AstraZeneca

is entitled to a share of gross profits, share

of revenues or royalties, which are recurring

in nature while the collaboration agreement

remains in place. Alliance Revenue does not

include Product Sales where AstraZeneca

is leading commercialisation in a territory,

or reimbursement for AstraZeneca-incurred

expenses such as R&D or promotion

costs, which arise from the license of

intellectual property.

The Group periodically enters into transactions

where it acquires part of the rights to a product

intangible (either on-market or in-process R&D),

but for commercial reasons does not act as

principal in selling the product to the customer

and therefore does not recognise income from

the product in the form of Product Sales. This

may occur where, for example, a collaboration

partner retains the right to commercialise in a

specific territory, and has sufficient local control

over that commercialisation to book Product

Sales, while the Group instead receives a

proportion of the value generated by those

Product Sales, either in the form of a royalty,

a share of gross profits or a share of revenues.

Where the arrangement meets the definition

of a licence agreement, share of gross profits,

share of revenues and sales royalties are

recognised when achieved by applying the

royalty exemption under IFRS 15. All other

sales royalties are recognised when considered

it is highly probable there will not be a

significant reversal of cumulative income.

The determination requires estimates to be

made in relation to future Product Sales.

Collaboration Revenue

Collaboration Revenue includes income arising

from entering into collaborative arrangements

where the Group has out-licensed (sold) certain

rights associated with products and where

AstraZeneca retains a significant ongoing

economic interest in the product. Significant

interest can include ongoing supply of finished

goods, profit sharing arrangements or being

principal in the sales of medicines. These

collaborations may include development,

manufacturing and/or commercialisation

arrangements with the collaborator. Income

from out-licences may take the form of upfront

fees and milestones.

Timing of recognition of clinical and

regulatory milestones is considered to be

a key judgement. There can be significant

uncertainty over whether it is highly probable

that there would not be a significant reversal

of revenue in respect of specific milestones

if these are recognised before they are

triggered due to them being subject to the

actions of third parties. In general, where

the triggering of a milestone is subject to the

decisions of third parties (e.g. the acceptance

or approval of a filing by a regulatory

authority), the Group does not consider that

the threshold for recognition is met until that

decision is made.

Where Collaboration Revenue arises from

the licensing of the Group’s own intellectual

property, the licences we grant are typically

rights to use intellectual property which do

not change during the period of the licence

and therefore related non-conditional revenue

is recognised at the point the licence is

granted and variable consideration as soon

as recognition criteria are met.

Group Accounting Policies 153AstraZeneca Annual Report & Form 20-F Information 2023

Corporate Governance Additional InformationFinancial StatementsStrategic Report

Group Accounting Policies

continu ed

Other performance obligations in the contract

might include the supply of product. These

arrangements typically involve the receipt of an

upfront payment, which the contract attributes

to the license of the intangible assets, and

ongoing receipts for supply, which the contract

attributes to the sale of the product we

manufacture. In cases where the transaction

has two or more components, we account for

the delivered item (for example, the transfer

of title to the intangible asset) as a separate

unit of account and record revenue on

delivery of that component. Where practicable,

consideration is allocated to performance

obligations on the basis of the standalone

selling price of each performance obligation.

However, where there is a licence of intellectual

property, it is not always possible to establish

a reliable estimate of the standalone selling

price of the licence as they are unique.

Therefore, in these rare situations, the

residual approach is used to determine the

consideration attributable to the licence.

Where fixed amounts are payable over one

year from the effective date of a contract, an

assessment is made as to whether a significant

financing component exists, and if so, the

fair value of this component is deferred and

recognised as financing income over the

period to the expected date of receipt.

Where control of a right to use licence for an

intangible asset passes at the outset of an

arrangement, revenue is recognised at the

point in time control is transferred. Where the

substance of a licence arrangement is that

of a right to access rights attributable to an

intangible asset, revenue, in the form of an

upfront fee, is recognised over time, normally

on a straight-line basis over the life of the

contract. Where the Group provides ongoing

development services, revenue in respect of

this element is recognised over the duration

of those services.

Where Collaboration Revenue is recorded

and there is a related intangible asset that is

licensed as part of the arrangement, an

appropriate amount of that intangible asset

is charged to Cost of sales based on an

allocation of cost or value to the rights that

have been licensed.

Cost of sales

Cost of sales are recognised as the

associated revenue is recognised. Cost of

sales include manufacturing costs, royalties

payable on revenues recognised, movements

in provisions for inventories, inventory

write-offs and impairment charges in relation

to manufacturing assets. Cost of sales also

includes co-collaborator sharing of profit

arising from collaborations, and foreign

exchange gains and losses arising from

business trading activities.

Research and development

Research expenditure is charged to profit and

loss in the year in which it is incurred.

Internal development expenditure is

capitalised only if it meets the recognition

criteria of IAS 38 ‘Intangible Assets’. This is

considered a key judgement. Where regulatory

and other uncertainties are such that the

criteria are not met, the expenditure is

charged to profit and loss and this is almost

invariably the case prior to approval of the

drug by the relevant regulatory authority.

Where, however, recognition criteria are

met, Intangible assets are capitalised and

amortised on a straight-line basis over their

useful economic lives from product launch.

At 31 December 2023, no amounts have met

the recognition criteria.

Payments to in-license products and

compounds from third parties for new research

and development projects (in process research

and development) generally take the form of

upfront payments, milestones and royalty

payments. Where payments made to third

parties represent consideration for future

research and development activities, an

evaluation is made as to the nature of the

payments. Such payments are expensed if they

represent compensation for sub-contracted

research and development services not

resulting in a transfer of intellectual property.

By contrast, payments are capitalised if they

represent compensation for the transfer of

identifiable intellectual property developed

at the risk of the third party. Such payments

may be made once development or regulatory

milestones are met and may also be made

on the basis of sales volumes once a product

is launched. Development and regulatory

milestone payments are capitalised as the

milestone is triggered. Sales-related payments

are accrued and capitalised with reference to

the latest Group sales forecasts for approved

indications at the present value of expected

future cash flows. Assets capitalised are

amortised, on a straight-line basis, over their

useful economic lives from product launch.

The determination of useful economic

life is considered to be a key judgement.

On product launch, the Group makes a

judgement as to the expected useful

economic life with reference to the expiry

of associated patents for the product,

expectation around the competitive

environment specific to the product and

our detailed long-term risk-adjusted sales

projections compiled annually across the

Group and approved by the Board.

The useful economic life can extend beyond

patent expiry dependent upon the nature

of the product and the complexity of the

development and manufacturing process.

Significant sales can often be achieved post

patent expiration.

Intangible assets

Intangible assets are stated at cost less

accumulated amortisation and impairments.

Intangible assets relating to products in

development are subject to impairment testing

annually. All Intangible assets are tested for

impairment when there are indications that

the carrying value may not be recoverable.

The determination of the recoverable amounts

include key estimates which are highly sensitive

to, and depend upon, key assumptions as

detailed in Note 10 to the Financial Statements

from page 172.

Impairment reviews have been carried out on

all Intangible assets that are in development

(and not being amortised), all major intangible

assets acquired during the year and all other

intangible assets that have had indicators of

impairment during the year. Recoverable

amount is determined as the higher of value-in-

use or fair value less costs to sell using a

discounted cash flow calculation, with the

products’ expected cash flows risk-adjusted

over their estimated remaining useful economic

life. Sales forecasts and specific allocated

costs (which have both been subject to

appropriate senior management review and

approval) are risk-adjusted and discounted

using appropriate rates based on our post-tax

weighted average cost of capital or for fair value

less costs to sell, a required rate of return for a

market participant. Our weighted average cost

of capital reflects factors such as our capital

structure and our costs of debt and equity.

Any impairment losses are recognised

immediately in Operating profit. Intangible

assets relating to products which fail during

development (or for which development

ceases for other reasons) are also tested for

impairment and are written down to their

recoverable amount (which is usually nil).

If, subsequent to an impairment loss being

recognised, development restarts or other

facts and circumstances change indicating

that the impairment is less or no longer exists,

the value of the asset is re-estimated and its

carrying value is increased to the recoverable

amount, but not exceeding the original value,

by recognising an impairment reversal in

Operating profit.

Government grants

Government grants are recognised in the

Consolidated Statement of Comprehensive

Income so as to match with the related

expenses that they are intended to compensate.

Where grants are received in advance of the

related expenses, they are initially recognised

in the Consolidated Statement of Financial

Position under Trade and other payables as

deferred income and released to net off

against the related expenditure when incurred.

154

AstraZeneca Annual Report & Form 20-F Information 2023 Financial Statements

Each contract is assessed to determine

whether there are both grant elements and

supply of product which need to be separated.

In each case, the contracts set out the specified

terms for the supply of the product and the

provisions for funding for certain costs,

primarily research and development associated

with the IP. It is considered whether there are

any conditions for the funding to be refunded.

The consideration in the contract is allocated

between the grant and supply elements.

The standalone selling price for the supply

of products is determined by reference to

observed prices with other customers. The

amount allocated as a government grant is

determined by reference to the specific agreed

costs and activities identified in the contract

as not directly attributable to the supply of

product. Government grants are recorded

as an offset to the relevant expense in the

Consolidated Statement of Comprehensive

Income and are capped to match the relevant

costs incurred.

Other operating income and expense

Other operating income and expense is

generated from activities outside of the

Group’s normal course of business, which

includes Other income from divestments of or

full out-license of assets and businesses

including royalties and milestones where the

Group does not retain a significant continued

interest. Where the arrangement meets the

definition of a licence agreement, sales

milestones and sales royalties are recognised

when achieved by applying the royalty

exemption under IFRS 15. All other milestones

and sales royalties are recognised when it is

considered highly probable that there will not

be a significant reversal of cumulative income.

The determination requires estimates to be

made in relation to future Product Sales.

Joint arrangements and associates

The Group has arrangements over which it

has joint control and which qualify as joint

operations or joint ventures under IFRS 11

‘Joint Arrangements’. For joint operations, the

Group recognises its share of revenue that it

earns from the joint operations and its share of

expenses incurred. The Group also recognises

the assets associated with the joint operations

that it controls and the liabilities it incurs under

the joint arrangement. For joint ventures and

associates, the Group recognises its interest in

the joint venture or associate as an investment

and uses the equity method of accounting.

Employee benefits

The Group accounts for pensions and other

employee benefits (principally healthcare)

under IAS 19 ‘Employee Benefits’. In respect

of defined benefit plans, obligations are

determined using the projected unit credit

method and are discounted to present value

by reference to market yields on high-quality

corporate bonds, while plan assets are

measured at fair value. Given the extent of the

assumptions used to determine the value of

scheme assets and scheme liabilities, these

are considered to be significant estimates.

The operating and financing costs of such plans

are recognised separately in profit; current

service costs are spread systematically over

the lives of employees and financing costs are

recognised in full in the periods in which they

arise. Remeasurements of the net defined

benefit pension liability, including actuarial

gains and losses, are recognised immediately

in Other comprehensive income.

Where the calculation results in a surplus to

the Group, the recognised asset is limited

to the present value of any available future

refunds from the plan or reductions in

future contributions to the plan subject to

consideration of the effect any minimum

funding requirement for future service has

on the benefit available as a reduction in

future contributions.

Payments to defined contribution plans are

recognised in profit as they fall due.

Taxation

The current tax payable is based on taxable

profit for the year. Taxable profit differs from

reported profit because taxable profit

excludes items that are either never taxable or

tax deductible or items that are taxable or tax

deductible in a different period. The Group’s

current tax assets and liabilities are calculated

using tax rates that have been enacted or

substantively enacted by the reporting date.

Deferred tax is provided using the balance

sheet liability method, providing for temporary

differences between the carrying amounts of

assets and liabilities for financial reporting

purposes and the amounts used for taxation

purposes. Deferred tax liabilities are recognised

unless they arise from the initial recognition

(other than in a business combination) of assets

and liabilities in a transaction that affects

neither the taxable profit nor the accounting

profit. Deferred tax liabilities are not recognised

to the extent they arise from the initial

recognition of non-tax deductible goodwill.

Deferred tax assets are recognised to the

extent that there are future taxable temporary

differences or it is probable that future taxable

profit will be available against which the asset

can be utilised. This requires judgements to

be made in respect of the availability of future

taxable income.

No deferred tax asset or liability is recognised

in respect of temporary differences associated

with investments in subsidiaries and branches

where the Group is able to control the timing

of reversal of the temporary differences and it

is probable that the temporary differences will

not reverse in the foreseeable future.

The Group’s deferred tax assets and liabilities

are calculated using tax rates that are

expected to apply in the period when the

liability is settled or the asset realised based

on tax rates that have been enacted or

substantively enacted by the reporting date.

Deferred tax liabilities relating to assets

recognised because of a business combination

which may qualify for intellectual property

incentives are measured at the relevant

statutory tax rate. Deferred tax assets and

liabilities are offset in the Consolidated

Statement of Financial Position if, and only if,

the taxable entity has a legally enforceable

right to set off current tax assets and liabilities,

and the Deferred tax assets and liabilities

relate to taxes levied by the same taxation

authority on the same taxable entity.

Liabilities for uncertain tax positions require

management to make judgements of potential

exposures in relation to tax audit issues.

Tax benefits are not recognised unless the

tax positions will probably be accepted by

the tax authorities. This is based upon

management’s interpretation of applicable laws

and regulations and the expectation of how

the tax authority will resolve the matter. Once

considered probable of not being accepted,

management reviews each material tax benefit

and reflects the effect of the uncertainty in

determining the related taxable result.

Liabilities for uncertain tax positions are

measured using either the most likely amount

or the expected value amount depending on

which method the entity expects to better

predict the resolution of the uncertainty.

Further details of the estimates and

assumptions made in determining our recorded

liability for transfer pricing contingencies and

other tax contingencies are included in Note 30

to the Financial Statements from page 204.

Share-based payments

All plans have been classified as equity settled

after assessment. The grant date fair value

of the market-based performance elements of

employee share plan awards is calculated

using a modified Monte Carlo model, with

other elements at market price. In accordance

with IFRS 2 ‘Share-based Payment’, the

resulting cost is recognised in profit on a

straight-line basis over the vesting period

of the awards. The value of the charge is

adjusted to reflect expected and actual levels

of awards vesting, except where the failure

to vest is as a result of not meeting a market

condition. Cancellations of equity instruments

are treated as an acceleration of the vesting

period and any outstanding charge is

recognised in profit immediately.

Cash outflows relating to the vesting of share

plans for our employees are recognised within

operating activities, as they relate to employee

remuneration. The cash flows relating to

replacement awards issued to employees as

part of the Alexion acquisition (see Note 27

from page 193) are classified within investing

activities, as they are part of the aggregate

cash flows arising from obtaining control of

the subsidiary.

Group Accounting Policies 155AstraZeneca Annual Report & Form 20-F Information 2023

Corporate Governance Additional InformationFinancial StatementsStrategic Report

Group Accounting Policies

continu ed

Property, plant and equipment

The Group’s policy is to depreciate the

difference between the cost of each item of

Property, plant and equipment and its residual

value over its estimated useful life on a

straight-line basis. Assets under construction

are not depreciated until the asset is available

for use, at which point the asset is transferred

into either Land and buildings or Plant and

equipment, and depreciated over its

estimated useful economic life.

Reviews are made annually of the estimated

remaining lives and residual values of individual

productive assets, taking account of

commercial and technological obsolescence as

well as normal wear and tear. It is impractical

to calculate average asset lives exactly.

However, the useful economic lives range from

approximately 10 to 50 years for buildings,

and three to 15 years for plant and equipment.

All items of Property, plant and equipment are

tested for impairment when there are indications

that the carrying value may not be recoverable.

Any impairment losses are recognised

immediately in Operating profit.

Leases

The Group’s lease arrangements are principally

for property, most notably a portfolio of office

premises and employee accommodation, and

for a global car fleet, utilised primarily by our

sales and marketing teams.

The lease liability and corresponding

right-of-use asset arising from a lease are

initially measured on a present value basis.

Lease liabilities include the net present value

of the following lease payments:

> fixed payments, less any lease

incentives receivable

> variable lease payments that depend on an

index or a rate, initially measured using the

index or rate as at the commencement date

> the exercise price of a purchase option if

the Group is reasonably certain to exercise

that option

> payments of penalties for terminating the

lease, if the lease term reflects the Group

exercising that option, and

> amounts expected to be payable by the

Group under residual value guarantees.

Right-of-use assets are measured at cost

comprising the following:

> the amount of the initial measurement of

lease liability

> any lease payments made at or before

the commencement date less any lease

incentives received

> any initial direct costs, and

> restoration costs.

Judgements made in calculating the lease

liability include assessing whether arrangements

contain a lease and determining the lease term.

Lease terms are negotiated on an individual

basis and contain a wide range of different

terms and conditions. Property leases will

often include an early termination or extension

option to the lease term. Fleet management

policies vary by jurisdiction and may include

renewal of a lease until a measurement

threshold, such as mileage, is reached.

Extension and termination options have been

considered when determining the lease term,

along with all facts and circumstances that may

create an economic incentive to exercise an

extension option, or not exercise a termination

option. Extension periods (or periods after

termination options) are only included in the

lease term if the lease is reasonably certain to

be extended (or not terminated).

The lease payments are discounted using

incremental borrowing rates, as in the majority

of leases held by the Group the interest rate

implicit in the lease is not readily identifiable.

Calculating the discount rate is an estimate

made in calculating the lease liability. This rate

is the rate that the Group would have to pay to

borrow the funds necessary to obtain an asset

of similar value to the right-of-use asset in a

similar economic environment with similar

terms, security and conditions. To determine

the incremental borrowing rate, the Group

uses a risk-free interest rate adjusted for

credit risk, adjusting for terms specific to the

lease including term, country and currency.

The Group is exposed to potential future

increases in variable lease payments that are

based on an index or rate, which are initially

measured as at the commencement date, with

any future changes in the index or rate excluded

from the lease liability until they take effect.

When adjustments to lease payments based

on an index or rate take effect, the lease

liability is reassessed and adjusted against the

right-of-use asset.

Lease payments are allocated between

principal and finance cost. The finance cost

is charged to the Consolidated Statement of

Comprehensive Income over the lease period

so as to produce a constant periodic rate of

interest on the remaining balance of the

liability for each period.

Payments associated with short-term leases of

Property, plant and equipment and all leases

of low-value assets are recognised on a

straight-line basis as an expense in the

Consolidated Statement of Comprehensive

Income. Short-term leases are leases with a

lease term of 12 months or less. Low-value

leases are those where the underlying asset

value, when new, is $5,000 or less and

includes IT equipment and small items of

office furniture.

Contracts may contain both lease and

non-lease components. The Group allocates

the consideration in the contract to the lease

and non-lease components based on their

relative standalone prices.

Right-of-use assets are generally depreciated

over the shorter of the asset’s useful life and

the lease term on a straight-line basis. If the

Group is reasonably certain to exercise a

purchase option, the right-of-use asset is

depreciated over the underlying asset’s useful

life. It is impractical to calculate average asset

lives exactly. However, the total lives range from

approximately 10 to 50 years for buildings,

and three to 15 years for motor vehicles and

other assets.

There are no material lease agreements under

which the Group is a lessor.

Business combinations and goodwill

In assessing whether an acquired set of

assets and activities is a business or an asset,

management will first elect whether to apply

an optional concentration test to simplify the

assessment. Where the concentration test is

applied, the acquisition will be treated as the

acquisition of an asset if substantially all of

the fair value of the gross assets acquired

(excluding cash and cash equivalents,

deferred tax assets, and related goodwill) is

concentrated in a single asset or group of

similar identifiable assets.

Where the concentration test is not applied,

or is not met, a further assessment of whether

the acquired set of assets and activities is a

business will be performed.

The determination of whether an

acquired set of assets and activities is a

business or an asset can be judgemental,

particularly if the target is not producing

outputs. Management uses a number of

factors to make this determination, which

are primarily focused on whether the

acquired set of assets and activities include

substantive processes that mean the set is

capable of being managed for the purpose

of providing a return. Key determining

factors include the stage of development

of any assets acquired, the readiness and

ability of the acquired set to produce outputs

and the presence of key experienced

employees capable of conducting activities

required to develop or manufacture the

assets. Typically, the specialised nature of

many pharmaceutical assets and processes

is such that until assets are substantively

ready for production and promotion, there

are not the required processes for a set of

assets and activities to meet the definition

of a business in IFRS 3.

156

AstraZeneca Annual Report & Form 20-F Information 2023 Financial Statements

On the acquisition of a business, fair values

are attributed to the identifiable assets and

liabilities. Attributing fair values is a key

judgement; refer to Note 27 to the Financial

Statements from page 193 for additional

details. Contingent liabilities are also recorded

at fair value unless the fair value cannot be

measured reliably, in which case the value is

subsumed into goodwill. Where fair values of

acquired contingent liabilities cannot be

measured reliably, the assumed contingent

liability is not recognised but is disclosed in

the same manner as other contingent liabilities.

Where not all of the equity of a subsidiary

is acquired, the non-controlling interest is

recognised either at fair value or at the

non-controlling interest’s proportionate

share of the net assets of the subsidiary,

on a case-by-case basis. Put options over

non-controlling interests are recognised as a

financial liability, with a corresponding entry

in either Retained earnings or against non-

controlling interest reserves on a case-by-

case basis.

The timing and amount of future contingent

elements of consideration is an estimate.

Contingent consideration, which may include

development and launch milestones, revenue

threshold milestones and revenue-based

royalties, is fair valued at the date of acquisition

using decision-tree analysis with key inputs

including probability of success, consideration

of potential delays and revenue projections

based on the Group’s internal forecasts.

Unsettled amounts of consideration are held

at fair value within payables with changes in

fair value recognised immediately in profit.

Goodwill is the difference between the fair value

of the consideration and the fair value of net

assets acquired.

Goodwill arising on acquisitions is capitalised

and subject to an impairment review, both

annually and when there is an indication that

the carrying value may not be recoverable.

The Group’s policy up to and including

1997 was to eliminate Goodwill arising upon

acquisitions against reserves. Under IFRS 1

‘First-time Adoption of International Financial

Reporting Standards’ and IFRS 3 ‘Business

Combinations’, such Goodwill will remain

eliminated against reserves.

Subsidiaries

A subsidiary is an entity controlled, directly

or indirectly, by AstraZeneca PLC. Control is

regarded as the exposure or rights to the

variable returns of the entity when combined

with the power to affect those returns. Control

is normally evidenced by holding more than

50% of the share capital of the company,

however other agreements may be in place that

result in control where they give AstraZeneca

finance decision-making authority over the

relevant activities of the company.

The financial results of subsidiaries are

consolidated from the date control is

obtained until the date that control ceases.

Inventories

Inventories are stated at the lower of cost and

net realisable value. The first in, first out or an

average method of valuation is used. For

finished goods and work in progress, cost

includes directly attributable costs and certain

overhead expenses (including depreciation).

Selling expenses and certain other overhead

expenses (principally central administration

costs) are excluded. Net realisable value is

determined as estimated selling price less all

estimated costs of completion and costs to be

incurred in selling and distribution.

Write-downs of inventory occur in the general

course of business and are recognised in

Cost of sales for launched or approved

products and in Research and development

expense for products in development.

Assets held for sale

Non-current assets are classified as Assets

held for sale when their carrying amount is

to be recovered principally through a sale

transaction and a sale is considered highly

probable. A sale is considered highly probable

only when the appropriate level of management

has committed to the sale.

Assets held for sale are stated at the lower

of carrying amount and fair value less costs

to sell. Where there is a partial transfer of a

non-current asset to held for sale, an allocation

of value is made between the current and

non-current portions of the asset based on

the relative value of the two portions, unless

there is a methodology that better reflects the

asset to be disposed of.

Assets held for sale are neither depreciated

nor amortised.

Trade and other receivables

Financial assets included in Trade and other

receivables are recognised initially at fair value.

The Group holds the Trade receivables with the

objective to collect the contractual cash flows

and therefore measures them subsequently at

amortised cost using the effective interest

method, less any impairment, based on

expected credit losses.

Trade receivables that are subject to debt

factoring arrangements are derecognised if

they meet the conditions for derecognition

detailed in IFRS 9 ‘Financial Instruments’.

Trade and other payables

Financial liabilities included in Trade and other

payables are recognised initially at fair value.

Subsequent to initial recognition they are

measured at amortised cost using the effective

interest method. Contingent consideration

payables are held at fair value within Level 3 of

the fair value hierarchy as defined in Note 12.

Financial instruments

The Group’s financial instruments include

Lease liabilities, Trade and other receivables

and payables, liabilities for contingent

consideration and put options under business

combinations, and rights and obligations

under employee benefit plans which are dealt

with in specific accounting policies.

The Group’s other financial instruments include:

> Cash and cash equivalents

> Fixed deposits

> Other investments

> Bank and other borrowings

> Derivatives.

Cash and cash equivalents

Cash and cash equivalents comprise cash in

hand, current balances with banks and similar

institutions, and highly liquid investments

with maturities of three months or less when

acquired. They are readily convertible into

known amounts of cash and are held at

amortised cost under the hold to collect

classification, where they meet the hold to

collect ‘solely payments of principal and

interest’ test criteria under IFRS 9. Those

not meeting these criteria are held at fair

value through profit or loss. Cash and cash

equivalents in the Consolidated Statement

of Cash Flows include unsecured bank

overdrafts at the balance sheet date where

balances often fluctuate between a cash and

overdraft position.

Fixed deposits

Fixed deposits, principally comprising funds

held with banks and other financial institutions,

are initially measured at fair value, plus direct

transaction costs, and are subsequently

measured at amortised cost using the

effective interest method at each reporting

date. Changes in carrying value are

recognised in the Consolidated Statement

of Comprehensive Income.

Other investments

Investments are classified as fair value through

profit or loss (FVPL), unless the Group makes

an irrevocable election at initial recognition

for certain non-current equity investments to

present changes in Other comprehensive

income (FVOCI). If this election is made, there

is no subsequent reclassification of fair value

gains and losses to profit or loss following the

derecognition of the investment.

Bank and other borrowings

The Group uses derivatives, principally interest

rate swaps, to hedge the interest rate exposure

inherent in a portion of its fixed interest rate

debt. In such cases the Group will either

designate the debt as FVPL when certain

criteria are met or as the hedged item under

a fair value hedge.

Group Accounting Policies 157AstraZeneca Annual Report & Form 20-F Information 2023

Corporate Governance Additional InformationFinancial StatementsStrategic Report

Group Accounting Policies

continu ed

If the debt instrument is designated as FVPL,

the debt is initially measured at fair value (with

direct transaction costs being included in profit

as an expense) and is remeasured to fair value

at each reporting date with changes in carrying

value being recognised in profit (along with

changes in the fair value of the related

derivative), with the exception of changes in

the fair value of the debt instrument relating to

own credit risk which are recorded in Other

comprehensive income in accordance with

IFRS 9. Such a designation has been made

where this significantly reduces an accounting

mismatch which would result from recognising

gains and losses on different bases.

If the debt is designated as the hedged item

under a fair value hedge, the debt is initially

measured at fair value (with direct transaction

costs being amortised over the life of the debt)

and is remeasured for fair value changes in

respect of the hedged risk at each reporting

date with changes in carrying value being

recognised in profit (along with changes in the

fair value of the related derivative).

If the debt is designated in a cash flow hedge,

the debt is measured at amortised cost

(with gains or losses taken to profit and direct

transaction costs being amortised over the

life of the debt). The related derivative is

remeasured for fair value changes at each

reporting date with the portion of the gain

or loss on the derivative that is determined to

be an effective hedge recognised in Other

comprehensive income. The amounts that have

been recognised in Other comprehensive

income are reclassified to profit in the same

period that the hedged forecast cash flows

affect profit. The reclassification adjustment is

included in Finance expense in the Consolidated

Statement of Comprehensive Income.

Other interest-bearing loans are initially

measured at fair value (with direct transaction

costs being amortised over the life of the loan)

and are subsequently measured at amortised

cost using the effective interest method at each

reporting date. Changes in carrying value are

recognised in the Consolidated Statement of

Comprehensive Income.

Derivatives

Derivatives are initially measured at fair value

(with direct transaction costs being included

in profit as an expense) and are subsequently

remeasured to fair value at each reporting

date. Changes in carrying value of derivatives

not designated in hedging relationships are

recognised in profit or loss.

The Group has agreements with some bank

counterparties whereby the parties agree to

post cash collateral, for the benefit of the other,

equivalent to the market valuation of all of the

derivative positions above a predetermined

threshold. Cash collateral received from

counterparties is included within current

Interest-bearing loans and borrowings within the

Consolidated Statement of Financial Position.

Cash collateral pledged to counterparties is

recognised as a financial asset and is included

in current Other investments within the

Consolidated Statement of Financial Position.

Cash collateral received is included in

Movement in short-term borrowings within

financing activities in the Consolidated Cash

Flow Statement. Cash collateral paid is included

in Movements in short-term investments within

investing activities in the Consolidated Cash

Flow Statement. The cash flow presentation of

cash paid and received follows the Consolidated

Statement of Financial Position presentation

of the financial asset and financial liability that

is recognised from posting the collateral.

Foreign currencies

Foreign currency transactions, being

transactions denominated in a currency other

than an individual Group entity’s functional

currency, are translated into the relevant

functional currencies of individual Group

entities at average rates for the relevant

monthly accounting periods, which

approximate to actual rates.

Monetary assets and liabilities arising from

foreign currency transactions are retranslated

at exchange rates prevailing at the reporting

date. Exchange gains and losses on loans and

on short-term foreign currency borrowings

and deposits are included within Finance

expense. Exchange differences on all other

foreign currency transactions are recognised

in Operating profit in the individual Group

entity’s accounting records.

Non-monetary items arising from foreign

currency transactions are not retranslated in the

individual Group entity’s accounting records.

In the Consolidated Financial Statements,

income and expense items for Group entities

with a functional currency other than US

dollars are translated into US dollars at

average exchange rates, which approximate

to actual rates, for the relevant accounting

periods. Assets and liabilities are translated at

the US dollar exchange rates prevailing at the

reporting date. Exchange differences arising

on consolidation are recognised in Other

comprehensive income.

If certain criteria are met, non-US dollar-

denominated loans or derivatives are

designated as net investment hedges of foreign

operations. Exchange differences arising on

retranslation of net investments, and of foreign

currency loans which are designated in an

effective net investment hedge relationship, are

recognised in Other comprehensive income in

the Consolidated Financial Statements. Foreign

exchange derivatives hedging net investments

in foreign operations are carried at fair value.

Effective fair value movements are recognised

in Other comprehensive income, with any

ineffectiveness taken to profit. Gains and

losses accumulated in the translation reserve

will be recycled to profit and loss when the

foreign operation is sold.

Provisions

Provisions are recognised when there is either

a legal or constructive present obligation as a

result of a past event, it is probable that an

outflow of economic resources will be required

to settle the obligation and a reliable estimate

can be made of the amount of the obligation.

If the effect of the time value of money is

material, provisions are discounted at the

relevant pre-tax discount rate. Where provisions

are discounted, the increase in the provision

resulting from the passage of time is recognised

as a finance cost.

Litigation and environmental liabilities

AstraZeneca is involved in legal disputes, the

settlement of which may involve cost to the

Group. A provision is made where an adverse

outcome is probable and associated costs,

including related legal costs, can be estimated

reliably. Determining the timing of recognition

of when an adverse outcome is probable is

considered a key judgement, refer to Note 30

to the Financial Statements from page 204.

Where it is considered that the Group is more

likely than not to prevail, or in the extremely

rare circumstances where the amount of the

legal liability cannot be estimated reliably,

legal costs involved in defending the claim are

charged to the Consolidated Statement of

Comprehensive Income as they are incurred.

Where it is considered that the Group has a

valid contract which provides the right to

reimbursement (from insurance or otherwise)

of legal costs and/or all or part of any loss

incurred or for which a provision has been

established, the amount expected to be

received is recognised as an asset only when

it is virtually certain.

AstraZeneca is exposed to environmental

liabilities relating to its past operations,

principally in respect of soil and groundwater

remediation costs. Provisions for these costs

are made when there is a present obligation

and where it is probable that expenditure on

remedial work will be required and a reliable

estimate can be made of the cost.

Restructuring

Restructuring costs are incurred in programmes

that are planned and controlled by the Group

which materially change either the scope of a

business undertaken by the Group, or the

manner in which that business is conducted.

A provision for restructuring costs is recognised

when a detailed formal plan is in place and

has either been announced to those affected

or has started to be implemented. The general

recognition criteria for provisions must also be

met, as described in the Provisions policy.

158

AstraZeneca Annual Report & Form 20-F Information 2023 Financial Statements

Impairment

The carrying values of non-financial assets,

other than Inventories and Deferred tax assets,

are reviewed at least annually to determine

whether there is any indication of impairment.

For Goodwill, Intangible assets under

development and for any other assets where

such indication exists, the asset’s recoverable

amount is estimated based on the greater of

its value in use and its fair value less cost to

sell. In assessing the recoverable amount, the

estimated future cash flows, adjusted for the

risks associated with the probability of success

specific to each asset, as well as inflationary

impacts, are discounted to their present value

using a nominal discount rate that reflects

current market assessments of the time

value of money, the general risks affecting

the pharmaceutical industry and other risks

specific to each asset. For the purpose of

impairment testing, assets are grouped

together into the smallest group of assets

that generates cash inflows from continuing

use that are largely independent of the cash

flows of other assets. Impairment losses are

recognised immediately in the Consolidated

Statement of Comprehensive Income.

Applicable accounting standards

andinterpretations issued but not

yetadopted

At the date of authorisation of these financial

statements, certain new accounting standards

and amendments were in issue relating to the

following standards and interpretations but

not yet adopted by the Group:

> amendments to IAS 1 ‘Presentation of

Financial Statements’, effective for periods

beginning on or after 1 January 2024 –

endorsed by the UK Endorsement Board

(UKEB) on 21 July 2023

> amendments to IFRS 16 ‘Leases’, effective

for periods beginning on or after 1 January

2024 – endorsed by the UKEB on

11 May 2023

> amendments to IAS 7 ‘Statement of Cash

Flows’ and IFRS 7 ‘Financial Instruments:

Disclosures’, effective for periods beginning

on or after 1 January 2024 – endorsed by

the UKEB on 28 November 2023

> amendments to IAS 21 ‘The Effects of

Changes in Foreign Exchange Rates’,

effective for periods beginning on or

after 1 January 2025 – not endorsed by

the UKEB.

These new standards, amendments and

interpretations are not expected to have a

significant impact on the Group’s net results.

Group Accounting Policies 159AstraZeneca Annual Report & Form 20-F Information 2023

Corporate Governance Additional InformationFinancial StatementsStrategic Report

Notes to the Group Financial Statements

1 Revenue

Product Sales

2023 2022 2021

Emerging Rest of Emerging Rest of Emerging Rest of

US Markets Europe World Total US Markets Europe World Total US Markets Europe World Total

$m $m $m $m $m $m $m $m $m $m $m $m $m $m $m

Oncology:

Tagrisso 2,276 1,621 1,120 782 5,799 2,007 1,567 1,023 847 5,444 1,780 1,336 986 913 5,015

Imfinzi 2,317 360 758 802 4,237 1,552 287 544 401 2,784 1,245 277 485 405 2,412

Lynparza 1,254 542 734 281 2,811 1,226 488 655 269 2,638 1,087 384 618 259 2,348

Calquence 1,815 98 493 108 2,514 1,657 45 286 69 2,057 1,089 20 111 18 1,238