1

The NAIC’s Capital Markets Bureau monitors developments in the capital markets globally and analyzes

their potential impact on the investment portfolios of U.S. insurance companies. A list of archived Capital

Markets Bureau Primers is available via the INDEX.

Auto Asset-Backed Securities (Auto ABS) Primer

Analyst: Jennifer Johnson

Executive Summary

• Auto asset-backed securities (auto ABS) are structured finance securities that are a subset of

consumer ABS; they are collateralized by pools of auto loans and/or leases made to prime

(high quality) or subprime (poor quality) borrowers.

• Similar to other structured finance securities, the capital structure of auto ABS includes several

layers of debt (or tranches/notes) plus a junior-most layer of equity that serves as the first-loss

position.

• Auto ABS typically have a servicer that is responsible for “managing” the portfolio of auto

loans/leases and a trustee that is responsible for distributing periodic reports to investors.

• Unlike other types of consumer ABS, auto lease ABS have residual risk; i.e., the risk that the

market value of a returned vehicle will be less than its base value.

• Historically, auto ABS have been the largest component of U.S. insurers’ consumer ABS

exposure, but they have not been a substantial proportion of U.S. insurers’ overall total cash

and invested assets (less than 1%).

Background

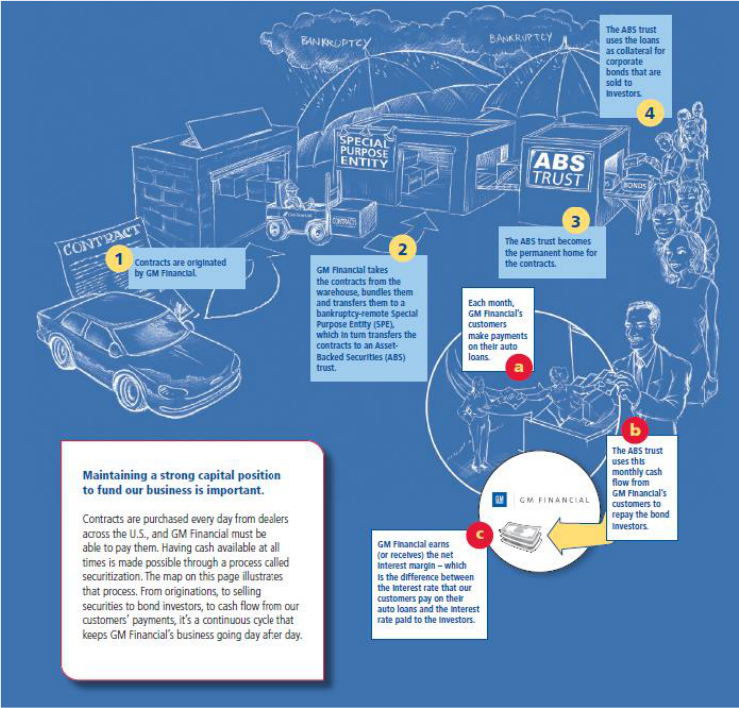

Auto asset-backed securities (auto ABS) are structured finance securities that are collateralized by auto

loans or leases, such as those to prime (good credit standing) and subprime (poor credit standing)

borrowers. Loans or leases are bundled into pools and transferred to a special-purpose entity (SPE),

which, in turn, transfers the pool to a (bankruptcy remote) trust. Payments on the underlying auto loans

and leases are pooled in the trust, and the funds are used to pay note investors their respective principal

and interest when due. Any leftover funds — known as excess spread, or the net interest margin — are

paid to the equity holder (usually the issuer, such as an auto finance company). This process is illustrated

in Picture 1 [a promotional diagram from an auto lender].

2

Picture 1:

Source: GMFinancial.com.

Auto ABS Capital Structure

Similar to other structured finance transactions, the capital structure of auto ABS is comprised of several

tranches, or notes, that range from senior to subordinated. The more subordinated the notes, the lower

the credit quality and the less credit enhancement (i.e., the ratio of the principal value of the collateral

to the principal value of the auto ABS notes). As such, senior notes are rated higher (investment grade or

better) than subordinated notes by the nationally recognized statistical ratings organizations (NRSROs),

such as Standard & Poor’s, Fitch Ratings and Moody’s Investors Service. Auto ABS notes typically have

four- to seven-year (legal final) maturities.

Also, like other structured finance transactions, the junior-most layer in an auto ABS capital structure, or

the equity tranche, serves as the first-loss position in the event of a default. That is, losses from defaults

are allocated in reverse priority of payment, beginning with equity, then up to the senior notes.

Typically, each note balance is reduced to zero before any losses are allocated to a more senior note.

3

The notes may be amortized on a pro-rata basis — whereby principal amounts earned by the underlying

portfolio are shared in proportion to the note balances (i.e., the amount due to each note is an amount

proportional to the note’s fraction of the total outstanding principal amount on the closing date) — or

sequentially — whereby principal amounts generated by the portfolio are first used to pay senior notes

until paid in full, before being allocated to junior notes. Trigger events, such as a decrease in credit

enhancement below a predetermined level, could — depending on the transaction’s terms as indicated

in legal documents — switch a pro-rata amortization structure to sequential or turbo payment (in the

latter of which, all excess spread is used to make principal payments) to pay down senior notes first,

then the junior classes, followed by equity. According to S&P Global research, most auto lease ABS

securitizations have a sequential principal payment structure.

1

An auto ABS transaction may also be structured with a revolving period, whereby the principal collected

on the underlying auto loans and leases may be used to purchase additional receivables instead of

paying down the notes.

Auto Loans and Leases

As stated in the NAIC Capital Markets Bureau primer on Consumer ABS that was published in April 2019,

auto ABS are backed by auto loan or lease receivables. Auto loans and leases typically are:

• Fixed simple interest.

• Level-pay installments.

• Payable monthly over a predetermined time frame.

• Structured with terms that typically range from 12 to 84 months.

• Secured by an automobile.

Each installment of an auto loan includes a portion of principal repayment plus interest and fees

amortized over the life of the loan. The monthly installment on an auto lease is not for the repayment of

principal; rather, it is the difference between the price of the vehicle and the residual value (RV) of the

vehicle at lease-end plus interest and fees. The RV is the expected fair market value of a vehicle at the

end of the lease term.

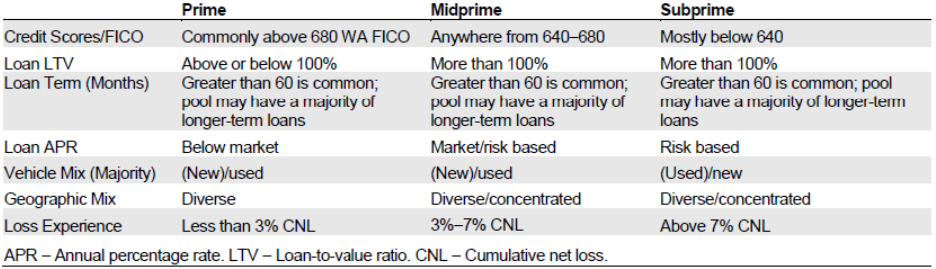

Auto financing includes lending or leasing to a variety of borrowers with various credit scores,

segregated by prime, midprime and subprime, with characteristics as shown in Chart 1. According to

Fitch Ratings,

2

a prime borrower has a credit score of at least 680, a mid-prime borrower has a credit

score of 640–680, and a subprime borrower has a credit score of less than 640. For some transactions,

midprime and subprime may be combined and referred to collectively as subprime and, in general, the

limits of the credit bands can vary. The pool of auto loans or leases may also be diversified by borrower,

mitigating concentration risk.

1

S&P Global Ratings, Criteria/Structured Finance/ABS: Revised General Methodology and Assumptions for Rating

U.S. ABS Auto Lease Securitizations, December 2018.

2

Fitch Ratings, U.S. Auto Loan ABS Rating Criteria, March 2019.

4

Chart 1: Auto ABS – Summary of General Collateral Characteristics

Source: Fitch Ratings.

Certain characteristics of the auto loans and leases are important for understanding credit quality. They

include not only the borrower’s credit score, but also loan-to-value (LTV) ratios (i.e., a debt advance

rate), loan terms, annual percentage rate (APR) of the loans, vehicle segment (e.g., car/truck/SUV), the

auto’s condition (e.g., new/used/pre-owned), as well as geographic diversification.

Loans vs. Leases

There are a few noteworthy differences between auto loans and auto leases. With auto loans, the

lending bank owns the vehicle until the borrower pays off the loan; auto leases, however, are like long-

term rentals, where the borrower pays rent to use the vehicle. At the end of the lease, the borrower has

the option to purchase the vehicle or return it. Auto loans typically have a term of four to six years,

whereas lease terms are usually two to four years. And, monthly auto loan payments are generally

based on the total amount financed by the borrower, while lease payments are based on a vehicle’s

expected depreciation value over the term of the lease.

Credit Enhancement

Credit enhancement for auto ABS may be in the form of subordinated or junior notes,

overcollateralization, cash reserves and/or excess spread. Subordination means that the junior notes in

the transaction’s capital structure provide credit support to the senior notes. Overcollateralization is the

excess of the principal value of the underlying portfolio over the principal value of notes issued. Many

auto ABS have predetermined overcollateralization levels to achieve (as stipulated in the transaction’s

legal documents) before the flow of funds continues down from senior noteholders to junior

noteholders and equity holders on payment dates. Cash reserves are held in an account to absorb losses

due to defaults within the asset pool; typically, cash reserves are initially funded by the transaction’s

originator when the pool of assets is transferred to a trust, and it is funded ongoing by excess spread.

Excess spread results from the difference between interest payments and fees received from the

underlying asset pool of auto loans and leases and interest payments made to investors, along with

servicing fees and other expenses. Excess spread is typically passed along to equity investors, but in the

event of deterioration in the quality and/or quantity of the underlying loan/lease pool, a “trigger” may

5

be breached that requires the funds to be redirected to either pay down the principal balance of the

senior-most notes outstanding or purchase additional collateral.

3

SPE and Bankruptcy Remoteness

The auto loan or lease originator (also known as a servicer or sponsor) enters into an agreement to

transfer the receivables (i.e., auto loans or leases) to an SPE, where they are isolated from any potential

bankruptcy of the originator. This means that if the originator experiences financial trouble, the assets

of the SPE would not be available to the originator’s other creditors. The originator may be a specialty

finance company or other type of lender.

The transfer of receivables to the SPE is considered a sale of the originator’s rights to the receivables. In

turn, the originator receives note proceeds, or cash, from the transfer of its rights, and the SPE issues

notes to investors. Typically, the SPE transfers the receivables to a trust; SPEs and trusts are established

to isolate transferred financial assets beyond the reach of the originator and its creditors, even in the

event of a bankruptcy of the originator.

Rather than setting up a new trust for each securitization issued, most originators use a single master

trust for multiple issues. A master trust is set up to allow receivables to be added to the trust over time

and notes to be issued in a series. Each series has an undivided interest in the designated receivables

owned by the trust.

Role of the Servicer and Trustee

The servicer is responsible for collecting payments (i.e., principal and interest) on the underlying

portfolio of auto loans or leases and monitoring their performance; it effectively serves the role of

portfolio manager. As such, the servicer can have an impact on the timeliness of cash flows to the

noteholders. Servicer responsibilities include evaluating the borrower’s credit quality before loans are

included in the pool, as well as negotiating pricing and loan terms. In addition, for any non-performing

or delinquent loans or leases, the servicer is responsible for negotiating terms and/or selling the assets.

As a result, when assessing the credit risk of auto ABS (to assign credit ratings), the NRSROs evaluate

servicers’ operations, focusing on corporate performance (including operational and financial stability),

the quality of the underwriting processes and capabilities and the quality of the loan servicing

operations (according to S&P Global criteria).

Typically, the servicer or an affiliate owns the equity in the transaction. This demonstrates favorable

alignment with the noteholders because, in order for the equity holders to be paid, the underlying

portfolio of auto loans and leases must be “managed,” or serviced, to the best interests of all investors.

A trustee is a third-party entity responsible for distributing periodic performance reports on the

underlying portfolio to investors, most often monthly. While usually prepared by the servicer, the

3

Guggenheim, Portfolio Strategy Research – The ABCs of ABS, September 2017.

6

reports provide detailed information about the portfolio’s composition of auto loans and leases, such as

quality and payment performance.

What Are the Risks Related to Investing in Auto ABS?

Credit risk — also known as default risk — is the risk that the underlying portfolio will not be able to

generate enough cash flows to pay investors on a full and timely basis when principal and/or interest

payments are due. The credit score of the underlying borrowers is indicative of portfolio credit quality.

Potential payment default can be influenced by a few factors, one of which is the auto loan and lease

market in general; that is, taking notice of any originators or lenders or servicers that are experiencing

difficulties or challenges in the current environment, as well as trends in the auto industry. Default in

payment on the auto loans and leases results in less cash for the underlying portfolio, and, in turn, less

funds available to pay the auto ABS investors. For this reason, it is important that auto ABS portfolios are

diversified, such as by borrower and geographically. If the auto loan and lease markets experience

difficulties, the liquidity of auto ABS could also be negatively impacted.

Auto lease ABS are exposed to residual value (RV) risk relative to the underlying auto leases; that is, the

risk that the market value of the returned vehicles will be less than the base RV of the vehicles (i.e., the

lower of the contract value at the beginning of the auto lease and a third-party forecasted RV) if the

vehicle is returned (and not purchased) at the end of the lease. The lessees have the option of

purchasing the auto at the end of the lease for the contract value.

Auto ABS may also experience prepayment risk; that is, in a low interest rate environment, borrowers

may prepay their loans for a reduced rate — resulting in early, unscheduled return of principal on the

underlying auto loans. However, auto ABS tend to experience low prepayment risks, as the relatively

short-term auto loans (usually 36–60 months) and decreasing RV makes refinancing uneconomical for

the borrower, even in a falling interest rate environment.

7

Key Terminology

Base Residual Value

The lower of the contract value at the beginning of an auto lease and a third-party forecasted value.

Credit Enhancement

The ratio of the principal value of the collateral (underlying pool of auto loans and leases) to the

principal value of notes issued by the SPE.

Expected Maturity

Target date for full repayment of principal, even though the legal final maturity may be years later.

Legal Final Maturity

In reference to a bond, it is the date before which the bond must be retired in order not to be in default.

Level-Pay Installments

Fixed number of fixed-amount monthly installments.

Loan Annual Percentage Rate (APR)

Interest rate assigned to the loan based on borrower credit profile and market interest rate trends.

Loan-To-Value (LTV)

Ratio of the (auto) loan to the value of the asset (vehicle).

Master Servicer

A company responsible for making sure that the servicing function is carried out, but that may not

actually perform the function itself. A securitization backed by assets from multiple originators often has

a master servicer. The master servicer subcontracts the collection functions to other companies. A

master servicer generally does not outsource administrative functions, such as processing remittances

and preparing investor reports.

Net Interest Margin

The difference between the income generated by the underlying portfolio and interest due on the

notes, along with any fees and expenses; same as excess spread.

Pass-Through

Pass-through occurs when a security that provides for the distribution of collections or proceeds from

specific underlying assets to investors. The collections or proceeds are said to be “passed through” to

the investors.

Prime

Borrowers with “good” credit quality (generally, with a credit score greater than 680).

8

Principal Balance

The outstanding amount of a loan or bond; it is the amount that must be paid (with interest and any

applicable prepayment penalties) to repay a debt.

Residual Value (RV)

Pertaining to autos, the expected fair market value of a vehicle at the end of the lease term.

Residual Value Risk (RV Risk)

Pertaining to auto leases, the risk that the market value of the returned vehicles will be less than the

base residual value of the vehicle.

Revolving Period

A specified period during which principal collections on the underlying portfolio of loans/leases are used

to purchase additional receivables rather than repay notes.

Seasoning

Changes in the character of loans or accounts (in the case of revolving receivables) as they age.

Servicer/Primary Servicer

An entity that collects payments on securitized assets and administers securitization transactions.

Administrative duties include processing remittances to investors and transmitting periodic reports to

investors, rating agencies and other interested parties. Often, the originator of securitized assets acts as

the servicer. In some cases, a primary servicer refers seriously delinquent loans to a special servicer.

When assets from multiple originators back a single securitization, each originator might be the primary

servicer of the assets that it originated. In such a case, the sponsor of the deal (i.e., a conduit or

aggregator) generally would be the master servicer, and each originator would function as a sub-

servicer.

Special Purpose Entity (SPE)

Also known as special purpose vehicle (SPV) or the “issuer,” an SPE is an entity created for the purpose

of purchasing a specific pool of assets while simultaneously issuing debt (asset-backed securities) to

investors.

Special Servicer

A special servicer is a servicer designated specifically to handle collections on delinquent and

problematic loans. In transactions that use a special servicer, there is also a primary servicer that

handles servicing loans that are current or only mildly delinquent.

Subprime

Borrowers with “poor” credit quality (generally, with a credit score less than 640).

9

Trustee

A third-party entity responsible for distributing periodic performance reports on the underlying portfolio

to investors.

Turn-In Rates

With respect to auto leases, a turn-in rate is the proportion of lessees who do not purchase their vehicle

at the end of the lease contract or who return the vehicle during the term of the contract. Turn-in rates

measure the portion of the lessor’s portfolio that is eventually sold in the open market and, hence,

exposed to RV risk.

Weighted-Average Coupon (WAC)

The WAC is the weighted-average interest rate of loans backing a securitization. In calculating the WAC

of an asset pool, the interest rate of each loan is weighted by its outstanding principal balance.

Weighted-Average Life (WAL)

Used instead of maturity for pricing amortizing securities; it is the weighted-average time to the return

of principal on a security. In calculating a security's WAL, each payment date is expressed as the interval

(in years) between the time of calculation and the payment date. Each interval is weighted by the

amount of principal that will be distributed on the corresponding payment date.

Weighted-Average Maturity (WAM)

The WAM date of loans backing a securitization is calculated by weighing the balance of each loan's

maturity (expressed in years from the time of calculation).

10

Appendix

Source: Securities Industry and Financial Markets Association (SIFMA).