Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 1 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

Overview /

Product

Summary

Correspondent

Seller Guide –

Section 2.01c -

Texas Section

50(a)(6)

Mortgages

Standard

Agency

Loan

Standard

&

Key Loan

Standard

Product Summary

A Texas Section 50(a)(6) mortgage is a loan originated in accordance with and secured by a lien permitted under the

provisions of Article XVI, Section 50(a)(6), of the Texas Constitution, which allow a borrower to take equity out of a

homestead property under certain conditions. Texas Section 50(a)(6) mortgage loan programs are offered through

traditional underwriting (i.e., non-AUS), Fannie Mae’s Desktop Underwriter (DU), and Freddie Mac’s Loan Product

Advisor (LPA).

The lender must meet the eligibility criteria specified in the Texas Constitution Section 50(a)(6).

Eligible loan products available under the Texas 50 (a)(6) loan program include the following:

• Fully Amortizing Fixed Rate, and

• Fully Amortizing 7/6-Month and 10/6-Month SOFR ARMs.

All Texas Section 50(a)(6) first mortgage transactions must comply with the more restrictive of Section 2.01: Agency

Loan Standard requirements or the Texas Section 50(a)(6) Mortgages standards, as outlined in this product

description. Standards not addressed in this product description will follow standard Agency requirements, as

outlined in Section 2.01: Agency Loan Standard of the Correspondent Seller Guide. If not specified in this product

description, the standards apply for all underwriting methods.

Product Summary

A Texas Section 50(a)(6) mortgage is a loan originated in accordance with and secured by a lien permitted under the

provisions of Article XVI, Section 50(a)(6), of the Texas Constitution, which allow a borrower to take equity out of a

homestead property under certain conditions. Texas Section 50(a)(6) mortgage loan programs are offered through

traditional underwriting (i.e., non-AUS), Fannie Mae’s Desktop Underwriter (DU), and Freddie Mac’s Loan Product

Advisor (LPA).

The lender must meet the eligibility criteria specified in the Texas Constitution Section 50(a)(6).

Eligible loan products available under the Texas 50 (a)(6) loan program include the Key Loan Standard and Agency Loan

Standard, as follows:

• Fully Amortizing Fixed Rate, and

• For Agency Loan, fully Amortizing 7/6-Month and 10/6-Month SOFR ARMs.

For Agency programs, all Texas Section 50(a)(6) first mortgage transactions must comply with the more restrictive of

Section 2.01: Agency Loan Standard requirements or the Texas Section 50(a)(6) Mortgages standards, as outlined in this

product description Standards not addressed in this product description will follow standard Agency requirements, as

outlined in Section 2.01: Agency Loan Standard of the Correspondent Seller Guide. If not specified in this product

description, the standards apply for all underwriting methods.

For the Key Loan Standard, Texas Equity 50(a)(6) first mortgage standard must comply with the more restrictive of

Section 2.06: Key Loan Standard or Section 2.01c of Texas Section 50(a)(6) Mortgages Standard, as outlined in this

product description. Standards not addressed in this product description will follow standard Key Loan Standard

requirements, as outlined in Section 2.06: Key Loan Standard section of the Correspondent Seller Guide. If not specified

in this product description, the standards apply for all underwriting methods.

References:

• See the “Limited Cash-Out Refinance (LPA Terminology: “No Cash-Out” Refinance)” subtopic Section 2.01 - Agency

Loan Standard for information regarding Texas Section 50(f)(2) refinance transactions (i.e., converting a 50(a)(6)

loan to a 50(a)(4) standard limited cash-out refinance loan) in the state of Texas.

• See the “Limited Cash-Out (Rate/Term) Refinance” subtopic outlined in Section 2.06 – Key Loan Standard for

information regarding Texas Section 50(f)(2) refinance transactions (i.e., converting a 50(a)(6) loan to a 50(a)(4)

standard limited cash-out refinance loan) in the state of Texas.

• See the “Cash-Out Refinance” subtopic outlined in Section 2.01 - Agency Loan Standard for information regarding

standard cash-out refinance transactions in the state of Texas.

• See the “Cash-Out Refinance” subtopic outlined in Section 2.06 – Key Loan Standard for information regarding

standard cash-out refinance transactions in the state of Texas.

Non-Equity Refinance Transactions Defined Under the Texas Constitution

Truist permits the following non-equity refinance transactions in the state of Texas:

• Texas Section 50(a)(3): the refinance of an owelty of partition imposed against the entirety of the property by a

court order or a written agreement of the parties to the partition, including a debt of one spouse in favor of the

other spouse resulting from a division or award of a family homestead in a divorce proceeding.

• Texas Section 50(a)(4): The refinance of a lien against a homestead, including a federal tax lien resulting from the

tax debt of both spouses, if the homestead is a family homestead, or from the tax debt of the owner. Under Texas

law these transactions are considered rate-term refinances, however, refinance transactions must be identified

based on Truist standards.

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 2 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

• Texas Section 50(a)(5): Home improvement loan or new construction on homestead property. Under Texas law

these transactions are considered rate-term refinances, however, refinance transactions must be identified based

on Truist standards.

Loan Terms

Correspondent

Seller Guide –

Section 2.01c -

Texas Section

50(a)(6)

Mortgages

Standard

Agency

Loan

Standard

&

Key Loan

Standard

Loan Terms

Note: Below is an EXCERPT only of the standards from the above referenced section.

Amortization Terms

•

Fully Amortizing Fixed Rate: 10-30 years

•

The minimum original term permitted is 85 months

•

Fully Amortizing 7/6-Month SOFR ARM: 10-30 years

•

Fully Amortizing 10/6-Month SOFR ARM: 15-30 years

Minimum Loan Amount

There is no minimum loan amount

Maximum Loan Amount

647,200

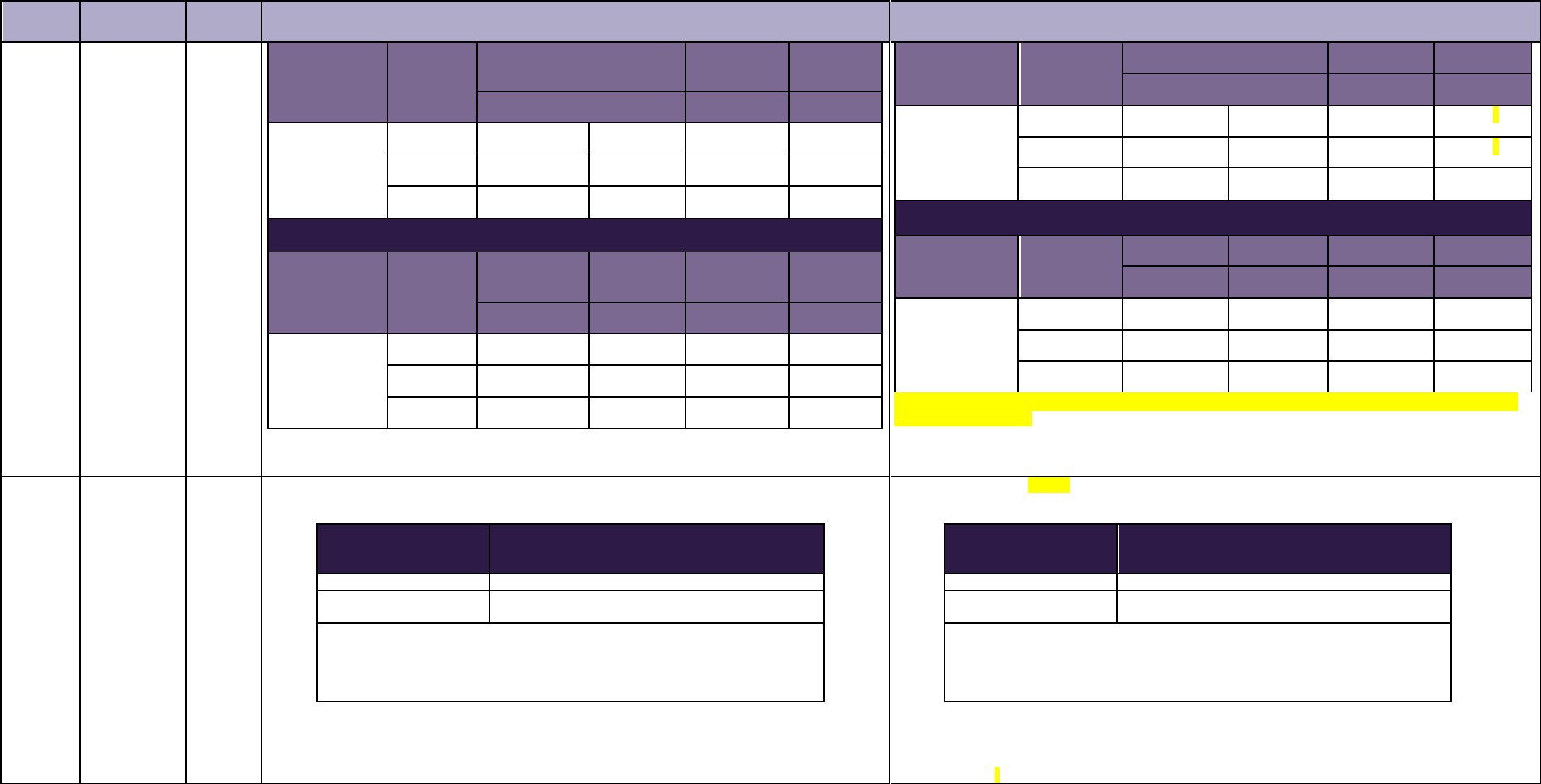

Maximum LTV/TLTV/HTLTV Ratio Requirements

Texas Section 50 (a)(6) Mortgages

Primary Residence – Fixed Rate

Purpose

# of

Units

LTV/TLTV/HTLTV

for Non-AUS Loans

LTV/TLTV/HTLTV

for DU Loans

LTV/TLTV/HTLTV

for LPA Loans

Limited Cash-

Out Refinance

(Rate/Term)

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

Cash-Out

Refinance

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

1

Home Equity Lines of Credit (HELOCs) are not permitted.

Loan Terms

Note: Below is an EXCERPT only of the standards from the above referenced section.

Amortization Terms

Agency Loan Standard:

•

Fully Amortizing Fixed Rate: 10-30 years

•

The minimum original term permitted is 85 months

•

Fully Amortizing 7/6-Month SOFR ARM: 10-30 years

•

Fully Amortizing 10/6-Month SOFR ARM: 15-30 years

Key Loan Standard:

• Fully Amortizing Fixed Rate: 15 or 30 Years

----------------------------------------------------------------------------------------------------------------------------------------------

Minimum Loan Amount

Agency Loan Standard: There is no minimum loan amount.

Key Loan Standard: The minimum loan amount is always one ($1) dollar above the conforming loan limit.

----------------------------------------------------------------------------------------------------------------------------------

Maximum Loan Amount

Agency Loan Standard: $647,200

Key Loan Standard: see the first mortgage product description for the maximum loan amount

Maximum LTV/TLTV/HTLTV Ratio Requirements

Texas Section 50 (a)(6) Mortgages

Primary Residence – Fixed Rate

Purpose

# of

Units

LTV/TLTV/HTLTV

for Agency Non-AUS Loans

Standard

LTV/TLTV/HTLTV

for DU Loans

LTV/TLTV/HTLTV

for LPA Loans

Limited Cash-

Out Refinance

(Rate/Term)

1

80%/80%/NA

1

80%/80%/N/A

1

80%/80%/N/A

1

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 3 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

Texas Section 50 (a)(6) Mortgages

Primary Residence – 7/6-Month & 10/6-Month SOFR ARM

Purpose

# of

Units

LTV/TLTV/HTLTV

for Non-AUS Loans

LTV/TLTV/HTLTV

for DU Loans

LTV/TLTV/HTLTV

for LPA Loans

Limited Cash-

Out Refinance

(Rate/

Term)

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

Cash-Out

Refinance

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

1

Home Equity Lines of Credit (HELOCs) are not permitted.

All other currently published standards in this section remain the same.

Cash-Out

Refinance

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

1

Home Equity Lines of Credit (HELOCs) are not permitted.

Texas Section 50 (a)(6) Mortgages

Primary Residence – 7/6-Month & 10/6-Month SOFR ARM

(offered on Agency only)

Purpose

# of

Units

LTV/TLTV/HTLTV

for Non-AUS Loans

LTV/TLTV/HTLTV

for DU Loans

LTV/TLTV/HTLTV

for LPA Loans

Limited Cash-

Out Refinance

(Rate/

Term)

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

Cash-Out

Refinance

1

80%/80%/NA

1

80%/80%/NA

1

80%/80%/NA

1

1

Home Equity Lines of Credit (HELOCs) are not permitted.

All other currently published standards in this section remain the same.

Appraisal

Requiremen

ts / General

Correspondent

Seller Guide –

Section 2.01c -

Texas Section

50(a)(6)

Mortgages

Standard

Agency

Loan

Standard

&

Key Loan

Standard

General

Non-AUS

• Lenders must obtain a new full appraisal, including both interior and exterior inspections, to determine current

value on either Uniform Residential Appraisal Report (Form 1004), or Individual Condominium Unit Appraisal

Report (Form 1073). The appraisal must be attached to the written acknowledgement of fair value.

• The appraisal for the property and the acknowledgment of fair market value must not include any property

other than the homestead.

• The survey (or other acceptable evidence) must demonstrate that:

• the homestead property and any adjacent land are separate parcels, and

• the homestead property is a separately platted and subdivided lot for which full ingress and egress is

available.

• The lender must not have any interest (such as an option to purchase, a security interest, or an easement) in

any parcel adjacent to the homestead property that is owned by the borrower, if such interest could constitute

additional security for the Texas Section 50(a)(6) mortgage loan.

Fannie Mae DU

Follow DU requirements, which are the same as non-AUS requirements, except as follows:

General

Non-AUS Agency Loan Standard and the Key Loan Standard

• Lenders must obtain a new full appraisal, including both interior and exterior inspections, to determine current

value on either Uniform Residential Appraisal Report (Form 1004), or Individual Condominium Unit Appraisal

Report (Form 1073). The appraisal must be attached to the written acknowledgement of fair value.

• The appraisal for the property and the acknowledgment of fair market value must not include any property other

than the homestead.

• The survey (or other acceptable evidence) must demonstrate that:

• the homestead property and any adjacent land are separate parcels, and

• the homestead property is a separately platted and subdivided lot for which full ingress and egress is

available.

• The lender must not have any interest (such as an option to purchase, a security interest, or an easement) in any

parcel adjacent to the homestead property that is owned by the borrower, if such interest could constitute

additional security for the Texas Section 50(a)(6) mortgage loan.

Truist Notes for the Key Loan Standard:

The minimum appraisal requirements for the Key Loan Standard are based on the loan amount.

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 4 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

• Lenders must obtain a new full appraisal, including both interior and exterior inspections, to determine current

value on either Uniform Residential Appraisal Report (Form 1004), or Individual Condominium Unit Appraisal

Report (Form 1073), even if DU recommends a different property valuation method or an appraisal waiver. The

appraisal must be attached to the written acknowledgement of fair value.

Freddie Mac LPA

Follow LPA requirements, which are as follows:

• The lender must provide an appraisal with an interior and exterior inspection that meets Freddie Mac

requirements. An Automated Collateral Evaluation (ACE) is not eligible.

• The lender and the owner of the homestead must execute a written acknowledgment of the "fair market

value" of the homestead property as of the date the extension of credit is made. The appraisal report must be

attached to the acknowledgment.

• Reference: See Section 2.06 Key Loan Standard of the Correspondent Seller Guide for Appraisal Requirements.

• Reference: See Section 1.07: Appraisal Standard the Correspondent Seller Guide for additional information.

Fannie Mae DU

Follow DU requirements, which are the same as non-AUS requirements, except as follows:

• Lenders must obtain a new full appraisal, including both interior and exterior inspections, to determine current

value on either Uniform Residential Appraisal Report (Form 1004), or Individual Condominium Unit Appraisal

Report (Form 1073), even if DU recommends a different property valuation method or an appraisal waiver. The

appraisal must be attached to the written acknowledgement of fair value.

Freddie Mac LPA

Follow LPA requirements, which are as follows:

• The lender must provide an appraisal with an interior and exterior inspection that meets Freddie Mac

requirements. An Automated Collateral Evaluation (ACE) is not eligible.

• The lender and the owner of the homestead must execute a written acknowledgment of the "fair market value" of

the homestead property as of the date the extension of credit is made. The appraisal report must be attached to

the acknowledgment.

Program

Codes/

General

Correspondent

Seller Guide –

Section 2.01c -

Texas Section

50(a)(6)

Mortgages

Standard

Key Loan

Standard

Program Codes/General

The following table shows program codes for Agency Texas Section 50(a)(6) Mortgages:

Program Description

Program Code for Truist Internal Use

Only

Agency FXD TX 50(a)(6) 15 (10-15 Years)

C15TX

Agency FXD TX 50(a)(6) 30 (16-30 Years)

C30TX

Agency 7/6 SOFR TX 50(a)(6) (all terms)

76FNTX

Agency 10/6 SOFR TX 50(a)(6) (all terms)

106FNTX

Program Codes/General

The following table shows program codes for Agency and Key Loan Standard Texas Section 50(a)(6) Mortgages:

Program Description

Program Code for Truist Internal Use

Only

Agency FXD TX 50(a)(6) 15 (10-15 Years)

C15TX

Agency FXD TX 50(a)(6) 30 (16-30 Years)

C30TX

Agency 7/6 SOFR TX 50(a)(6) (all terms)

76FNTX

Agency 10/6 SOFR TX 50(a)(6) (all terms)

106FNTX

Key FXD TX 50(a)(6) 15 (10-15 Years)

15TXKY

Key FXD TX 50(a)(6) 30 (16-30 Years)

30TXKY

Closing and

Loan

Settlement

/ Power of

Attorney

and Title

Insurance

Correspondent

Seller Guide –

Section 2.01c -

Texas Section

50(a)(6)

Mortgages

Standard

Agency

Loan

Standard

&

Key Loan

Standard

Power of Attorney

Non-AUS

Section 2.01: Agency Loan Standard non-AUS standards apply, in addition to the following:

• The lender must meet the execution and evidence of execution requirements authorized by Article XVI, Section

50(a)(6) of the Texas Constitution.

Fannie Mae DU

Follow DU requirements, which are the same as non-AUS requirements.

Freddie Mac LPA

Section 2.01: Agency Loan Standard LPA requirements apply, in addition to the following:

• The lender must meet the execution and evidence of execution requirements authorized by Article XVI, Section

50(a)(6) of the Texas Constitution.

Power of Attorney

Non-AUS Agency Standard and the Key Loan Standard

• For Agency Standard: Section 2.01: Agency Loan Standard non-AUS requirements apply.

• For the Key Loan Program: Section 2.06: Key Loan Standard of the Correspondent Seller Guide manual underwriting

standards apply.

• For Agency Loan Standard and the Key Loan Standard, in addition to the above, the lender must meet the

execution and evidence of execution requirements authorized by Article XVI, Section 50(a)(6) of the Texas

Constitution.

Fannie Mae DU

Follow DU requirements, which are the same as non-AUS requirements.

Freddie Mac LPA

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 5 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

Title Insurance

Non-AUS

• For all Texas Section 50(a)(6) mortgage loans, a title insurance policy written on Texas Land Title Association

forms (standard or short form), supplemented by an Equity Loan Mortgage Endorsement (Form T‐42) and a

Supplemental Coverage Equity Loan Mortgage Endorsement (Form T‐42.1), is required.

Note: There may be no exceptions or deletions to the coverage provided by Paragraphs 2(a) through (e) of the

T-42 endorsement and the endorsement must include the optional coverage provided by Paragraph 2(f), as

well as the additional coverage provide by Endorsement T-42.1.

• The title insurance policy cannot include language that:

• excludes coverage for a title defect that arises because financed origination expenses are held not to be

“reasonable costs necessary to refinance,” or

• defines the “reasonable costs necessary to refinance” requirement as a “consumer credit protection” law

since the standard title policy excludes coverage when lien validity is questioned due to a failure to

comply with consumer credit protection laws.

Fannie Mae DU

Follow DU requirements, which are the same as non-AUS requirements.

Freddie Mac LPA

Follow LPA requirements, which are as follows:

• Texas Equity Section 50(a)(6) Mortgages must be covered by a title insurance policy meeting Freddie Mac

requirements, with the endorsements described below:

• An Equity Loan Mortgage Endorsement (Form T-42). The Form T-42 endorsement must include the

optional coverage provided by paragraph 2(f) of the endorsement and there must not be any exceptions

to, or deletions of, paragraphs 2(a) through 2(e) of the Form T-42 endorsement.

• A Supplemental Coverage Equity Loan Mortgage Endorsement (Form T 42.1). There must not be any

exceptions to, or deletions of, paragraphs 1(a) through 1(k) of the Form T-42.1 endorsement, or any

subsequent subparagraphs added to Paragraph 1 by any revision of the Form T 42.1 approved by the

Texas Insurance Commission.

• Any other endorsement that provides additional optional mortgagee coverage that is approved by the

State of Texas Insurance Commission. The endorsement must be obtained by the lender for Texas Equity

Section 50(a)(6) Mortgages originated on and after the date the endorsement becomes legally available.

There must be no exceptions to, or deletions of, any paragraphs providing additional coverage in any

such endorsement

Section 2.01: Agency Loan Standard LPA requirements apply, in addition to the following:

• The lender must meet the execution and evidence of execution requirements authorized by Article XVI, Section

50(a)(6) of the Texas Constitution.

______________________________________________________________________________________________

Title Insurance

Non-AUS Agency Loan Programs and the Key Loan Standard

• For all Texas Section 50(a)(6) mortgage loans, a title insurance policy written on Texas Land Title Association forms

(standard or short form), supplemented by an Equity Loan Mortgage Endorsement (Form T‐42) and a Supplemental

Coverage Equity Loan Mortgage Endorsement (Form T‐42.1), is required.

Note: There may be no exceptions or deletions to the coverage provided by Paragraphs 2(a) through (e) of the T-

42 endorsement and the endorsement must include the optional coverage provided by Paragraph 2(f), as well as

the additional coverage provide by Endorsement T-42.1.

• The title insurance policy cannot include language that:

• excludes coverage for a title defect that arises because financed origination expenses are held not to be

“reasonable costs necessary to refinance,” or

• defines the “reasonable costs necessary to refinance” requirement as a “consumer credit protection” law

since the standard title policy excludes coverage when lien validity is questioned due to a failure to comply

with consumer credit protection laws.

Fannie Mae DU

Follow DU requirements, which are the same as non-AUS requirements.

Freddie Mac LPA

Follow LPA requirements, which are as follows:

• Texas Equity Section 50(a)(6) Mortgages must be covered by a title insurance policy meeting Freddie Mac

requirements, with the endorsements described below:

• An Equity Loan Mortgage Endorsement (Form T-42). The Form T-42 endorsement must include the optional

coverage provided by paragraph 2(f) of the endorsement and there must not be any exceptions to, or

deletions of, paragraphs 2(a) through 2(e) of the Form T-42 endorsement.

• A Supplemental Coverage Equity Loan Mortgage Endorsement (Form T 42.1). There must not be any

exceptions to, or deletions of, paragraphs 1(a) through 1(k) of the Form T-42.1 endorsement, or any

subsequent subparagraphs added to Paragraph 1 by any revision of the Form T 42.1 approved by the Texas

Insurance Commission.

• Any other endorsement that provides additional optional mortgagee coverage that is approved by the State

of Texas Insurance Commission. The endorsement must be obtained by the lender for Texas Equity Section

50(a)(6) Mortgages originated on and after the date the endorsement becomes legally available. There must

be no exceptions to, or deletions of, any paragraphs providing additional coverage in any such endorsement

Loan Terms

/ Maximum

Loan-

toValue

(LTV)

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

Maximum Loan-To-Value (LTV)

Note: Below is an EXCERPT only of the standards from the above referenced section

Owner Occupied – Purchase/Rate-Term (1-Unit SFR/1-Unit PUD)

Maximum Loan-To-Value (LTV)

Note: Below is an EXCERPT only of the standards from the above referenced section

Owner Occupied – Purchase/Rate-Term (1-Unit SFR/1-Unit PUD)

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 6 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

Property Type

Loan

Amount

FICO 680-699

FICO 700-

719

FICO 720-739

FICO 740+

LTV/TLTV

LTV/TLTV

LTV/TLTV

LTV/TLTV

1-Unit SFR /PUD

$1,000,000

70%

80%

80%

85%

$1,500,000

70%

80%

80%

85%

$2,000,000

65%

75%

75%

80%

Owner Occupied – Purchase/Rate-Term (Condo)

Property Type

Loan

Amount

FICO 680-699

FICO 700-

719

FICO 720-739

FICO 740+

LTV/TLTV

LTV/TLTV

LTV/TLTV

LTV/TLTV

Condo

$1,000,000

70%

75%

75%

80%

$1,500,000

70%

75%

75%

80%

$2,000,000

60%

70%

70%

80%

All other currently published standards in this section remain the same.

Property Type

Loan Amount

FICO 680-699

FICO 700-719

FICO 720-739

FICO 740+

LTV/TLTV

LTV/TLTV

LTV/TLTV

LTV/TLTV

1-Unit SFR /PUD

$1,000,000

70%

80%

80%

85%

1

$1,500,000

70%

80%

80%

85%

1

$2,000,000

65%

75%

75%

80%

Owner Occupied – Purchase/Rate-Term (Condo)

Property Type

Loan Amount

FICO 680-699

FICO 700-719

FICO 720-739

FICO 740+

LTV/TLTV

LTV/TLTV

LTV/TLTV

LTV/TLTV

Condo

$1,000,000

70%

75%

75%

80%

$1,500,000

70%

75%

75%

80%

$2,000,000

60%

70%

70%

80%

1

Maximum LTV for Texas Section 50 (a)(6) Mortgages is 80%; refer to Section 2.01c - Texas Section 50(a)(6) Mortgages

Standards for more detail.

All other currently published standards in this section remain the same.

Appraisal

Requireme

nts/

General

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

Appraisal Requirements/General

Note: Below is an EXCERPT only of the standards from the above referenced section

The table below reflects minimum appraisal requirements based on loan amount.

Loan Amount or

Combined Total Loan

Amount

1

Appraisal Requirements

< $1,500,000

2

One (1) full appraisal by a State Certified Appraiser

>/= $1,500,000 and </=

$2,000,000

Two (2) full appraisals by State Certified Appraisers

1

The total loan amount includes the outstanding balance on second mortgages and the total

credit line amount on home equity lines of credit (HELOCs).

2

Two full appraisals are required on family transfer transactions when the loan amount or

combined loan amount is >/= $1,000,000.

• Homes that have a geothermal heat pump as the main heating and cooling system are eligible. The

Underwriter must determine that the appraisal supports the market for this type of property.

Appraisal Requirements/General

Note: Below is an EXCERPT only of the standards from the above referenced section

The table below reflects minimum appraisal requirements based on loan amount.

Loan Amount or

Combined Total Loan

Amount

1

Appraisal Requirements

< $1,500,000

2

One (1) full appraisal by a State Certified Appraiser

>/= $1,500,000 and </=

$2,000,000

Two (2) full appraisals by State Certified Appraisers

1

The total loan amount includes the outstanding balance on second mortgages and the total

credit line amount on home equity lines of credit (HELOCs).

2

Two full appraisals are required on family transfer transactions when the loan amount or

combined loan amount is >/= $1,000,000.

• Homes that have a geothermal heat pump as the main heating and cooling system are eligible. The

Underwriter must determine that the appraisal supports the market for this type of property.

References:

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 7 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

Reference: See Section 1.07: Appraisal Standards of the Correspondent Seller Guide for additional

information.

All other currently published standards in this section remain the same.

• See Section 1.07: Appraisal Standards of the Correspondent Seller Guide for additional information.

• See Section 2.01c: Texas Section 50(a)(6) Mortgages Standards for additional information on

appraisal requirements..

All other currently published standards in this section remain the same.

Occupancy/

Property

Types /

Maximum

Acreage

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

Maximum Acreage

Maximum acreage is fifteen (15).

Maximum Acreage

Key Loan Standard: Maximum acreage is fifteen (15).

For Texas homestead properties secured by a 50(a)(6) mortgage:

• Texas homestead properties secured by a 50(a)(6) mortgage are limited to a maximum of 15 acres. The borrower’s

property may not exceed the applicable acreage limit as determined by Texas law when the Texas Section 50(a)(6)

loan is originated.

• A borrower that owns adjacent land must submit appropriate evidence, such as a survey, that the mortgaged

homestead property is a separate parcel that does not exceed the permissible acreage.

Note: An inter vivos revocable trust that meets borrower eligibility criteria may be a borrower under a Texas

Section 50(a)(6) mortgage, provided that the trust meets the requirements for a "qualifying trust" under Texas law

for purposes of owning residential property that qualifies for the homestead exemption.

Occupancy/

Property

Types /

Geographic

Restrictions

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

Information

The following table shows the geographic restrictions.

State

Restriction

Alaska

Properties located in the state of Alaska are not eligible for the Key Loan

Standard.

Georgia

Georgia Power leasehold properties are not eligible.

Texas

• Rate/Term refinances are allowed and must meet all Key Loan Program standards. If prepaids

and taxes are included in the loan amount the following conditions must be met:

• The prepaids and taxes are limited to 5% of the loan amount

• The following language must be included in Schedule B of the Title Insurance: “Possible

defect in lien of the insured mortgage because of the insured’s inclusion of reserves or

impounds for taxes and insurance in the original principal of the indebtedness secured by

the insured mortgage."

• The following P-39 Standard Language must be included in the Title Insurance Policy:

“Company insures the Insured against loss, if any, sustained by the Insured under the terms

of this Policy by reason of a final, non-appeasable judgment of a court of competent

jurisdiction that divests the Insured of its interest as Insured because of this right, claim, or

interest. Company agrees to provide the defense to the Insured in accordance with the

terms of this Policy if suit is brought against the Insured to divest the Insured of its interest

as Insured because of this right, claim or interest.”

• Cash-out refinances on primary residence transactions located in the state of Texas are not

eligible.

Information

The following table shows the geographic restrictions.

State

Restriction

Alaska

Properties located in the state of Alaska are not eligible for the Key Loan

Program.

Georgia

Georgia Power leasehold properties are not eligible.

Texas

• Rate/Term refinances are allowed and must meet all Key Loan Program standards. If prepaids

and taxes are included in the loan amount the following conditions must be met:

• The prepaids and taxes are limited to 5% of the loan amount.

• The following language must be included in Schedule B of the Title Insurance: “Possible

defect in lien of the insured mortgage because of the insured’s inclusion of reserves or

impounds for taxes and insurance in the original principal of the indebtedness secured by

the insured mortgage."

• The following P-39 Standard Language must be included in the Title Insurance Policy:

“Company insures the Insured against loss, if any, sustained by the Insured under the terms

of this Policy by reason of a final, non-appeasable judgment of a court of competent

jurisdiction that divests the Insured of its interest as Insured because of this right, claim, or

interest. Company agrees to provide the defense to the Insured in accordance with the

terms of this Policy if suit is brought against the Insured to divest the Insured of its interest

as Insured because of this right, claim or interest.”

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 8 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

Occupancy/

Property

Types /

Ineligible

Properties

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

The following is a list of ineligible properties:

• 2–4-unit properties,

• apartment buildings,

• bed and breakfast properties,

• boarding houses,

• commercial buildings,

• condominium hotels or condotels,

• cooperatives,

• earth/earth-sheltered and geodesic/dome homes,

Notes:

• Homes that have a geothermal heat pump as the main heating and cooling

system are eligible.

• The Underwriter must determine that the appraisal supports the market for

this type of property.

• Georgia Power leasehold properties,

• houseboat projects/properties,

• Indian lands that are leasehold estates,

• investment properties,

• leaseholds that do not extend beyond 5-years the loan term and are not typical in the

market area,

• mixed-use properties,

• mobile/manufactured homes,

• model homes not eligible for occupancy within 60 days of loan closing,

• non-warrantable condominium/PUD projects,

• properties listed for sale within the last six (6) months (if cash-out refinance),

unless Delayed Financing Cash-Out refinance requirements are met,

• properties on acreage exceeding 15 acres,

• projects with legal non-conforming use,

• residential properties zoned commercial or industrial,

• studio condominiums,

• Texas homestead properties secured by a 50(a)(6) mortgage,

• timeshare units,

• unimproved land,

• unique properties, other than those listed above, in which the marketability

cannot be established, and

• working farms, ranches, and orchards.

The following is a list of ineligible properties:

• 2–4-unit properties,

• apartment buildings,

• bed and breakfast properties,

• boarding houses,

• commercial buildings,

• condominium hotels or condotels,

• cooperatives,

• earth/earth-sheltered and geodesic/dome homes,

Notes:

• Homes that have a geothermal heat pump as the main heating and cooling

system are eligible.

• The Underwriter must determine that the appraisal supports the market for

this type of property.

• Georgia Power leasehold properties,

• houseboat projects/properties,

• Indian lands that are leasehold estates,

• investment properties,

• leaseholds that do not extend 5-years beyond the loan term and are not typical in the

market area,

• mixed-use properties,

• mobile/manufactured homes,

• model homes not eligible for occupancy within 60 days of loan closing,

• non-warrantable condominium/PUD projects,

• properties listed for sale within the last six (6) months (if cash-out refinance),

unless Delayed Financing Cash-Out refinance requirements are met,

• properties on acreage exceeding 15 acres,

• projects with legal non-conforming use,

• residential properties zoned commercial or industrial,

• studio condominiums,

• timeshare units,

• unimproved land,

• unique properties, other than those listed above, in which the marketability

cannot be established, and

• working farms, ranches, and orchards.

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 9 of 13

Refinances

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

Refinances/Cash-out Refinance

Note: Below is an EXCERPT only of the standards from the above referenced section

Continuity of Obligation

Reference: See the Cash-Out Refinance, and Limited Cash-Out (Rate/Term) Refinance subtopics for additional

information.

• The objective of the continuity of obligation requirement is to address refinance transactions that include a

borrower that is on title, but not obligated on the original mortgage note being satisfied.

• The continuity of obligation standards do NOT apply for properties recently inherited, spousal/partner buyouts,

installment land contract transactions, or properties owned free and clear.

• An acceptable continuity of obligation (assuming that there is an outstanding lien against the property) exists

when:

• there is at least one borrower obligated on the new loan who was also a borrower obligated on the existing

loan being refinanced, OR

• the borrower has been on title for at least 12 months (but not obligated on the existing loan being

refinanced) AND residing in the property for at least 12 months AND has either:

• paid the mortgage for the last 12 months (including the payments for any secondary financing), OR

• can demonstrate a relationship (relative, domestic partner, etc.) with the current obligor.

Note: The existing loan being refinanced and the title must have been held in the name of a natural person or

an LLC (as long as the borrower was a member of the LLC prior to transfer). In addition, a six (6) month history

of ownership between the LLC and the natural person must be documented. Transfer of ownership from a

corporation to an individual does not meet this requirement.

Loans with an acceptable continuity of obligation may be underwritten and priced as either a limited cash-out

(rate/term) or a cash-out refinance based on standard definitions.

• If the borrower is currently on title but is unable to demonstrate an acceptable continuity of obligation, the

following applies:

• the loan must be underwritten and priced as a cash-out refinance transaction,

• the borrower must be on title for a minimum of six (6) months prior to loan application, and

• the maximum LTV/TLTV/HTLTV ratio will be limited to 50% based on the current appraised value.

• If the borrower is currently on title, but there is no outstanding lien against the property, the loan must be

underwritten and priced as a cash-out refinance.

Cash-Out Refinance

• The LTV is based on one of the following:

• If the borrower has owned the property for less than twelve (12) months from the date of the application,

the LTV/TLTV/HTLTV is based on the lesser of the acquisition cost or the current appraised value.

• If the borrower has owned the property for at least twelve (12) months from the date of application, the

LTV/TLTV/HTLTV is based on the current appraised value.

• Gifted property within the most recent twelve (12) month period is limited to a maximum of 60%

LTV/TLTV based on current appraised value.

• Cash-out refinance transactions must be used to pay off existing mortgages by obtaining a new first mortgage

secured by the same property or be a new mortgage on a property that does not have a mortgage lien against

it.

• There is no waiting period if the lender documents that the borrower acquired the property through an

inheritance or was legally awarded the property (divorce, separation or dissolution of a domestic partnership).

• Cash-out transactions are permitted to pay off a construction single-closing loan where six (6) permanent

mortgage payments have been made.

• Cash-out refinance transactions are not eligible if the existing loan is a “restructured mortgage.”

Refinances/Cash-out Refinance

Note: Below is an EXCERPT only of the standards from the above referenced section

Continuity of Obligation

Reference: See the Cash-Out Refinance, and Limited Cash-Out (Rate/Term) Refinance subtopics for additional information.

• The objective of the continuity of obligation requirement is to address refinance transactions that include a borrower

that is on title, but not obligated on the original mortgage note being satisfied.

• The continuity of obligation standards do NOT apply for properties recently inherited, spousal/partner buyouts,

installment land contract transactions, or properties owned free and clear.

• An acceptable continuity of obligation (assuming that there is an outstanding lien against the property) exists when:

• there is at least one borrower obligated on the new loan who was also a borrower obligated on the existing

loan being refinanced, OR

• the borrower has been on title for at least 12 months (but not obligated on the existing loan being refinanced)

AND residing in the property for at least 12 months AND has either:

• paid the mortgage for the last 12 months (including the payments for any secondary financing), OR

• can demonstrate a relationship (relative, domestic partner, etc.) with the current obligor.

Note: The existing loan being refinanced and the title must have been held in the name of a natural person or an LLC

(as long as the borrower was a member of the LLC prior to transfer). In addition, a six (6) month history of ownership

between the LLC and the natural person must be documented. Transfer of ownership from a corporation to an

individual does not meet this requirement.

Loans with an acceptable continuity of obligation may be underwritten and priced as either a limited cash-out

(rate/term) or a cash-out refinance based on standard definitions.

• If the borrower is currently on title but is unable to demonstrate an acceptable continuity of obligation, the following

applies:

• the loan must be underwritten and priced as a cash-out refinance transaction,

• the borrower must be on title for a minimum of six (6) months prior to loan application, and

• the maximum LTV/TLTV/HTLTV ratio will be limited to 50% based on the current appraised value.

• If the borrower is currently on title, but there is no outstanding lien against the property, the loan must be

underwritten and priced as a cash-out refinance.

Cash-Out Refinance

• The LTV is based on one of the following:

• If the borrower has owned the property for less than twelve (12) months from the date of the application, the

LTV/TLTV/HTLTV is based on the lesser of the acquisition cost or the current appraised value.

• If the borrower has owned the property for at least twelve (12) months from the date of application, the

LTV/TLTV/HTLTV is based on the current appraised value.

• Gifted property within the most recent twelve (12) month period is limited to a maximum of 60% LTV/TLTV

based on current appraised value.

• Cash-out refinance transactions must be used to pay off existing mortgages by obtaining a new first mortgage

secured by the same property or be a new mortgage on a property that does not have a mortgage lien against it.

• There is no waiting period if the lender documents that the borrower acquired the property through an inheritance

or was legally awarded the property (divorce, separation or dissolution of a domestic partnership).

• Cash-out transactions are permitted to pay off a construction single-closing loan where six (6) permanent mortgage

payments have been made.

• Cash-out refinance transactions are not eligible if the existing loan is a “restructured mortgage.”

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 10 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

• For cash-out refinance transactions, six (6) months’ minimum seasoning is required, with 0 x 30 day late

payments.

Notes:

• The six (6) months minimum seasoning is based on the date the borrower took title and the current loan

application date.

• The title must have been held in the name of a natural person or an LLC (as long as the borrower was a

member of the LLC prior to transfer). In addition, a six (6) month history of ownership between the LLC

and the natural person must be documented. Transfer of ownership from a corporation to an individual

does not meet this requirement.

• Seasoning requirements do not apply to borrowers meeting the requirements found in the Delayed

Financing Cash-Out Refinance section subsequently presented.

• Recommended documentation to assist in evidencing that the seasoning requirement is met includes, but

is not limited to, a copy of the Closing Disclosure from the previous transaction and a copy of the

borrower’s current credit report.

• In the case of a family transfer that occurred in the previous twelve (12) months, verify the property was not in

default at the time of transfer.

• See the table below for maximum cash-out standards:

Property Type

LTV/TLTV

Max Cash-Out

SFR, PUD, Condo

>50%

$350,000, including paid debts, unseasoned

subordinate financing and cash-in-hand.

SFR, PUD, Condo

≤50%

Unlimited to the maximum loan amount, including

paid debts, unseasoned subordinate financing and

cash-in-hand.

Ineligible Cash-out Transactions

The following list includes examples of transaction types that are not eligible as cash-out refinances. This list is not

comprehensive.

• Cash-out transactions are not permitted to pay off another lender’s interim construction loan.

• For transactions on properties that have a Property Assessed Clean Energy (PACE) loan, borrowers who

refinance the first mortgage loan and have sufficient equity to pay off the PACE loan but choose not to do so

will be ineligible for cash-out refinance transactions.

• The new loan amount includes the financing of real estate taxes that are more than 60 days delinquent, and an

escrow account is not established, unless requiring an escrow account is not permitted by applicable laws or

regulation.

Delayed Financing Cash-Out Refinance

If the property was purchased (or acquired) by the borrower within the prior six (6) months of the disbursement date

of the new mortgage, the following applies:

• The original purchase transaction was an arms-length transaction.

• The original purchase transaction is documented by a Closing Disclosure, which confirms that no mortgage

financing was used to obtain the subject property.

• For cash-out refinance transactions, six (6) months’ minimum seasoning is required, with 0 x 30-day late payments.

Notes:

• The six (6) months minimum seasoning is based on the date the borrower took title and the current loan

application date.

• The title must have been held in the name of a natural person or an LLC (as long as the borrower was a

member of the LLC prior to transfer). In addition, a six (6) month history of ownership between the LLC and

the natural person must be documented. Transfer of ownership from a corporation to an individual does not

meet this requirement.

• Seasoning requirements do not apply to borrowers meeting the requirements found in the Delayed Financing

Cash-Out Refinance section subsequently presented.

• Recommended documentation to assist in evidencing that the seasoning requirement is met includes, but is

not limited to, a copy of the Closing Disclosure from the previous transaction and a copy of the borrower’s

current credit report.

• In the case of a family transfer that occurred in the previous twelve (12) months, verify the property was not in

default at the time of transfer.

• See the table below for maximum cash-out standards:

Property Type

LTV/TLTV

Max Cash-Out

SFR, PUD, Condo

>50%

$350,000, including paid debts, unseasoned

subordinate financing and cash-in-hand.

SFR, PUD, Condo

≤50%

Unlimited to the maximum loan amount, including

paid debts, unseasoned subordinate financing and

cash-in-hand.

• Texas Equity Section 50(a)(6) Transactions

References:

• See Section 2.01c – Texas Section 50(a)(6) Mortgages for guidance regarding Texas Equity Section 50(a)(6)

transactions.

• See the “Overview topic in Section 2.01c – Texas Section 50(a)(6) Mortgages for a description of Texas Non-

Equity 50(a)(4) and 50(a)(5) refinance transactions.

• Texas Section 50(f)(2) Refinance Transactions: Converting a 50(a)(6) loan to a 50(a)(4) standard limited cash-out

(rate/ refinance) loan is referred to as a Texas Section 50(f)(2) refinance transaction and is permitted if the

following conditions are met:

• The Section 50(f)(2) refinance is not closed before the first anniversary of the date the Section 50(a)(6) home

equity loan was closed;

• No additional funds are advanced other than funds advanced to refinance the Section 50(a)(6) equity loan or

actual costs required by the lender to refinance the debt; and the borrower may not receive incidental cash

back;

• The principal amount of the refinance when added to the aggregate total of the outstanding principal

balances of all valid encumbrances of record against the homestead does not exceed 80% of the homestead’s

fair market value on the date of the refinance; and

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 11 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

• The sources of funds for the purchase transaction are documented (such as bank statements, personal loan

documents, or a HELOC on another property).

• Borrower(s) must be able to exhibit a historic level of assets to support the cash purchase (supported by

Schedule B of the last two (2) year’s tax returns) or other supportive documentation to verify receipt of

such funds. Funds must have been on deposit at least 90 days prior to the date of the original

transaction.

• If the source of funds used to acquire the property was an unsecured loan or a loan secured by an asset other

than the subject property (such as a HELOC secured by another property), the closing disclosure for the

refinance transaction must reflect that all cash-out proceeds be used to pay off or pay down, as applicable, the

loan used to purchase the property. Any payments on the balance remaining from the original loan must be

included in the debt-to-income ratio calculation for the refinance transaction.

Note: Funds received as gifts and used to purchase the property may not be reimbursed with proceeds of the

new mortgage loan.

• The new loan amount can be no more than the actual documented amount of the borrower’s initial investment

in purchasing the property plus the financing of closing costs, prepaid fees, and points on the new mortgage

loan (subject to the maximum LTV/TLTV/HTLTV ratios for the cash-out transaction).

Note: Maximum cash-out limitations do not apply.

• The title must have been held in the name of a natural person or an LLC (as long as the borrower was a

member of the LLC prior to transfer). In addition, a six (6) month history of homeownership between the LLC

and the natural person must be documented. Transfer of ownership from a corporation to an individual does

not meet this requirement.

All other cash-out refinance eligibility requirements are met with the exception of continuity of obligation, which need

not be applied.

Home Improvements

• Loan proceeds must be used to reimburse the borrower for cash spent on or lien(s) incurred for home

improvements.

• The loan must be considered a cash-out refinance transaction.

----------------------------------------------------------------------------------------------------------------------------------------------------------

Limited Cash-Out (Rate/Term Refinance)

General

• The LTV is based on the current appraised value, regardless of the length of ownership.

• The transaction must meet all continuity of obligation requirements.

• For rate/term refinance transactions, there is no minimum seasoning requirement.

• Proceeds from a rate/term refinance may be used to payoff the following:

• principal balance of an existing first mortgage lien, regardless of age,

• The lender provides the owner the written notice prescribed by Article XVI, Section 50(f)(2)(D) of the Texas

constitution on a separate document within three business days of application and at least 12 days before the

refinance is closed.

• Texas Non-Equity Section 50(a)(4) and 50(a)(5) Transactions

Reference: See the “Overview” topic in Section 2.01c – Texas Section 50(a)(6) Mortgages Standards for a

description of Texas Non-Equity 50(a)(4) and 50(a)(5) refinance transactions.

Ineligible Cash-out Transactions

The following list includes examples of transaction types that are not eligible as cash-out refinances. This list is not

comprehensive.

• Cash-out transactions are not permitted to pay off another lender’s interim construction loan.

• For transactions on properties that have a Property Assessed Clean Energy (PACE) loan, borrowers who refinance

the first mortgage loan and have sufficient equity to pay off the PACE loan but choose not to do so will be ineligible

for cash-out refinance transactions.

• The new loan amount includes the financing of real estate taxes that are more than 60 days delinquent, and an

escrow account is not established, unless requiring an escrow account is not permitted by applicable laws or

regulation.

Delayed Financing Cash-Out Refinance

If the property was purchased (or acquired) by the borrower within the prior six (6) months of the disbursement date of

the new mortgage, the following applies:

• The original purchase transaction was an arms-length transaction.

• The original purchase transaction is documented by a Closing Disclosure, which confirms that no mortgage

financing was used to obtain the subject property.

• The sources of funds for the purchase transaction are documented (such as bank statements, personal loan

documents, or a HELOC on another property).

• Borrower(s) must be able to exhibit a historic level of assets to support the cash purchase (supported by

Schedule B of the last two (2) year’s tax returns) or other supportive documentation to verify receipt of such

funds. Funds must have been on deposit at least 90 days prior to the date of the original transaction.

• If the source of funds used to acquire the property was an unsecured loan or a loan secured by an asset other than

the subject property (such as a HELOC secured by another property), the closing disclosure for the refinance

transaction must reflect that all cash-out proceeds be used to pay off or pay down, as applicable, the loan used to

purchase the property. Any payments on the balance remaining from the original loan must be included in the

debt-to-income ratio calculation for the refinance transaction.

Note: Funds received as gifts and used to purchase the property may not be reimbursed with proceeds of the new

mortgage loan.

• The new loan amount can be no more than the actual documented amount of the borrower’s initial investment in

purchasing the property plus the financing of closing costs, prepaid fees, and points on the new mortgage loan

(subject to the maximum LTV/TLTV/HTLTV ratios for the cash-out transaction).

Note: Maximum cash-out limitations do not apply.

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 12 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

• related closing costs, discount points, prepaids, and/or

• subordinate mortgage liens that have been seasoned for at least one (1) year. For a junior lien that is an

equity line of credit, the seasoning requirement shall be applied to the date of the most recent draw

against the equity line unless the draws were less than $2000 (the total draws cannot exceed a total of

$2000 in the last 12 months).

• Proceeds from a limited cash-out transaction may not be used to pay off the unpaid principal balance of a

Property Assessed Clean Energy (PACE) loan.

• If a subordinate lien (including equity lines) is to be paid off in the refinance transaction, it must be seasoned

for at least one (1) year; otherwise, the transaction will be considered a “cash-out” refinance and not eligible

as a rate term refinance. This includes, but is not limited to, home improvement liens evidenced by a

Materialmens’ or Mechanics’ lien on the title binder.

• If secondary financing is not seasoned, it may be included in the refinance if the second lien was incurred at the

original purchase of the property (evidenced by a copy of Closing disclosure from the original purchase) or the

second was used for documented home improvements.

• If the second was used for home improvements and is not seasoned, the borrower must provide copies of the

cancelled checks and receipts and/or a copy of the contract specifying the total of the improvements (if the

borrower contracted the work). The appraisal should support the value of the improvements.

• The borrower cannot receive more than the following in cash at closing:

• loan amounts </= $1,000,000 will be limited to two thousand dollars ($2,000), OR

• loan amounts > $1,000,000 will be limited to five thousand dollars ($5,000).

All other currently published standards in this section remain the same.

• The title must have been held in the name of a natural person or an LLC (as long as the borrower was a member of

the LLC prior to transfer). In addition, a six (6) month history of homeownership between the LLC and the natural

person must be documented. Transfer of ownership from a corporation to an individual does not meet this

requirement.

All other cash-out refinance eligibility requirements are met with the exception of continuity of obligation, which need not

be applied.

Home Improvements

• Loan proceeds must be used to reimburse the borrower for cash spent on or lien(s) incurred for home

improvements.

• The loan must be considered a cash-out refinance transaction.

---------------------------------------------------------------------------------------------------------------------------------------------------------------

Limited Cash-Out (Rate/Term Refinance)

General

• The LTV is based on the current appraised value, regardless of the length of ownership.

• The transaction must meet all continuity of obligation requirements.

• For rate/term refinance transactions, there is no minimum seasoning requirement.

• Proceeds from a rate/term refinance may be used to payoff the following:

• principal balance of an existing first mortgage lien, regardless of age,

• related closing costs, discount points, prepaids, and/or

• subordinate mortgage liens that have been seasoned for at least one (1) year. For a junior lien that is an equity

line of credit, the seasoning requirement shall be applied to the date of the most recent draw against the

equity line unless the draws were less than $2000 (the total draws cannot exceed a total of $2000 in the last 12

months).

• Proceeds from a limited cash-out transaction may not be used to pay off the unpaid principal balance of a Property

Assessed Clean Energy (PACE) loan.

• If a subordinate lien (including equity lines) is to be paid off in the refinance transaction, it must be seasoned for at

least one (1) year; otherwise, the transaction will be considered a “cash-out” refinance and not eligible as a rate

term refinance. This includes, but is not limited to, home improvement liens evidenced by a Materialmens’ or

Mechanics’ lien on the title binder.

• If secondary financing is not seasoned, it may be included in the refinance if the second lien was incurred at the

original purchase of the property (evidenced by a copy of Closing disclosure from the original purchase) or the

second was used for documented home improvements.

• If the second was used for home improvements and is not seasoned, the borrower must provide copies of the

cancelled checks and receipts and/or a copy of the contract specifying the total of the improvements (if the

borrower contracted the work). The appraisal should support the value of the improvements.

• The borrower cannot receive more than the following in cash at closing:

• loan amounts </= $1,000,000 will be limited to two thousand dollars ($2,000), OR

Texas Equity 50(a)(6) for the Correspondent Key Loan Standard

If not specifically addressed in the matrix below then currently published standards remain unchanged and continue to apply.

Last Revision Date 10/14/2022 (Correspondent) Page 13 of 13

Topic

Impacted

Document

Impacted

Products

Current Standards

Revised Standards

• loan amounts > $1,000,000 will be limited to five thousand dollars ($5,000).

• Texas only: For any refinance of a Texas Constitution Section 50(a)(6) loan that results in a loan originated in

accordance with and secured by a lien permitted by Article XVI, Section 50(a)(4) of the Texas Constitution, an

affidavit referenced in Section 50(f-1) Article XVI of the Texas Constitution must be prepared and recorded in

connection with each such transaction.

Truist Note: In addition to the affidavit requirement outlined above, refinances of an owner’s home equity loan as a

non-home equity refinance [i.e., non-50(a)(6)] loan under Article XVI, subsection 50(a)(4) of the Texas Constitution

must comply with all Texas state-specific requirements for such transactions.

All other currently published standards in this section remain the same.

Closing and

Loan

Settlement

Documentat

ion/General

Correspondent

Seller Guide –

Section 2:06 Key

Loan Standard

Key Loan

Standard

Closing and Loan Settlement Documentation/General

The following closing standards are specific to the Key Loan Standard. Unless specified below, all closing forms and

documentation should follow standard Truist requirements.

Reference: Refer to the following sections of the Correspondent Seller Guide for additional Truist closing information.

• Section 1.08: Loan Delivery and Purchase Review Standard

• Section 1.12: Completion Escrow Standard

• Section 1.14: Hazard and Flood Insurance Standard

• Section 1.16: Title Insurance Standard

Closing and Loan Settlement Documentation/General

The following closing standards are specific to the Key Loan Program. Unless specified below, all closing forms and

documentation should follow standard Truist requirements.

Reference: Refer to the following sections of the Correspondent Seller Guide for additional Truist closing information.

• Section 1.08: Loan Delivery and Purchase Review Standard

• Section 1.12: Completion Escrow Standard

• Section 1.14: Hazard and Flood Insurance Standard

• Section 1.16: Title Insurance Standard

Note: See Section 2.01c: Texas Section(50)(a)(6) Mortgages Standards for Closing and Loan Settlement requirements and

additional information.