TEACHER RETIREMENT SYSTEM of TEXAS

EMPLOYMENT

AFTER RETIREMENT

How it Works for You

September 2022

Our Mission

Improving the

retirement security

of our members by

prudently investing

and managing the

trust assets and

delivering benets

that make a positive

difference in their lives.

Our Vision

Earning your trust

every day.

EMPLOYMENT AFTER RETIREMENT

Introduction ........................................................................................................................... 1

Denitions .............................................................................................................................. 1

Things You Should Know ....................................................................................................... 2

EAR Restrictions .............................................................................................................................................................3

What Happens if My Employment Does Not Qualify for an EAR Exception? .......................................................................3

Service Retirement Before Jan. 1, 2021 ...........................................................................................................................3

Mandatory One-Month Break in Service ........................................................................................................................... 4

June 15 Rule ...................................................................................................................................................................4

Volunteering and Independent Contractor Services ..........................................................................................................4

Working for a Third-Party Entity .......................................................................................................................................4

Medicare Secondary Payer for Return-to-Work Retirees ...................................................................................................4

EAR Exceptions ...................................................................................................................... 5

EAR Exceptions for Service Retirees ............................................................................................................................6

Substitute ........................................................................................................................................................................7

One-Half Time or Less .....................................................................................................................................................8

Full Time (After a 12 Full, Consecutive-Calendar-Month Break in Service) ........................................................................9

Non-Prot Tutor ..............................................................................................................................................................9

COVID-19 Surge Personnel ..............................................................................................................................................10

Combining EAR Exceptions for Service Retirees .......................................................................................................... 11

Substitute + One-Half Time or Less .................................................................................................................................12

One-Half Time or Less + COVID-19 Surge Personnel ........................................................................................................ 13

One-Half Time or Less + Non-Prot Tutor .........................................................................................................................14

Substitute + Non-Prot Tutor ...........................................................................................................................................15

EAR Exceptions for Disability Retirees .........................................................................................................................16

Substitute (For up to 90 Days) ..........................................................................................................................................17

One-Half Time or Less (For up to 90 Days) .......................................................................................................................18

Non-Prot Tutor (For up to 90 Days) .................................................................................................................................19

Three-Month Trial Work Period .........................................................................................................................................19

Combining EAR Exceptions for Disability Retirees.......................................................................................................20

Substitute + One-Half Time or Less .................................................................................................................................21

Substitute + Non-Prot Tutor ...........................................................................................................................................22

One-Half Time or Less + Non-Prot Tutor .........................................................................................................................23

Compensation Limits for Disability Retirees ........................................................................ 24

Additional Information .......................................................................................................... 26

INTRODUCTION

If you’re considering returning to work for a TRS-covered employer after you retire, we’re here to help you understand the

concepts and processes related to the restrictions on employment after retirement. The information and examples in this

brochure will also help you make decisions to avoid revoking your retirement or forfeiting your annuity payments.

In general, a TRS retiree who works for a TRS-covered employer during a month will forfeit his or her annuity for that

month unless the retiree or the retiree’s employment qualies for an exception. This brochure describes these exceptions

and provides examples of how a retiree might comply with or exceed the limits of the exceptions.

Service retirees may work without limits for an employer not covered by TRS without losing any monthly annuity

payments. Disability retirees may also work an unlimited amount of time for an employer not covered by TRS but may be

subject to compensation limits.

If you still have questions after reading this brochure, please contact TRS. We’re here to help and are the experts on your

retirement. Do not rely on information provided to you by another retiree, co-worker or even your employer.

Employment after retirement restrictions can vary depending on when you retired or what kind of job you have, and TRS

can help you understand the specic limits or requirements that apply to you.

DEFINITIONS

EAR

“EAR” is a common TRS acronym that stands for “employment after retirement.” Generally, it refers to any work a

TRS retiree performs for a TRS-covered employer and the TRS laws and rules that apply to that employment.

Effective Retirement Date

Your effective retirement date with TRS will always be the last calendar day of the month that you retire, regardless

of the last day you reported to work for your employer. This date is stated on your Retirement Application

Acknowledgment (Form TRS 32).

Service Retirement

Service retirement eligibility is based upon your age, membership tier and years of service credit you have at TRS. If you

meet the requirements for service retirement, you may apply to receive a monthly annuity calculated according to state law.

Disability Retirement

Members are approved by the TRS Medical Board for disability benets. If you meet the requirements for disability

retirement, you may apply to receive a monthly annuity as a disability retiree regardless of your age or years of

service credit. Disability retirement annuity benets are approved if a member is mentally or physically disabled

from further performance of duty and has a disability that is probably permanent.

Surcharges

Surcharges are additional contributions that TRS-covered employers must pay to TRS for employing TRS retirees who

retired after Sept. 1, 2005 and who work more than one-half time during a month. There are two types of surcharges:

pension surcharges and health care surcharges. The amount of the pension surcharge is equal to the amount of both

member and state contributions on the compensation paid. The health care surcharge only applies for employed

retirees who are TRS-Care participants. The amount of the health care surcharge is determined by TRS. Please keep

in mind: These amounts are owed by your employer, not you. Effective Sept. 1, 2021, surcharges may not directly or

indirectly be passed on to you through payroll deduction, fees or other means designed to recover the cost.

TRS-Covered Employer

A public, state-supported educational institution in Texas, including school districts, charter schools, education

service centers, and institutions of higher education.

EMPLOYMENT AFTER RETIREMENT

1

Whether you are retired or considering retiring

this year and are planning to return to work

for a TRS-covered employer, it’s important to

understand limitations that may apply. This

section includes information on some things

that may be helpful to understand before

returning to work.

THINGS

YOU SHOULD

KNOW

EAR Restrictions

In general, a TRS retiree who works for a TRS-covered employer during a month will forfeit his or her annuity for that month

unless the retiree or the retiree’s employment qualies for an exception.

What Happens if My Employment Does Not Qualify for an Exception?

Effective May 2021, a service retiree does not automatically forfeit his or her annuity if the service retiree’s employment

with a TRS-covered employer does not qualify for an EAR exception. Instead, service retirees are subject to a “three strikes”

warning procedure before forfeiting their annuity payments.

This means if you exceed the EAR limits, you will rst be notied of an EAR violation without loss of annuity. You will only

receive a warning or “rst strike.” If you exceed the EAR limits again, after TRS issues your rst strike warning, you will

receive a second warning and be required to pay TRS what you earned for the month that you exceeded the EAR limits or

the gross amount of your annuity payment for that month, whichever is less. This second warning and partial repayment

requirement is your “second strike.” If you exceed the EAR limits again, after receiving your second strike, that is your “third

strike” and you will forfeit your full monthly annuity for each month that you exceeded the limits.

Each EAR notication will include the months the violations occurred as well as the amount owed for each strike, if

applicable. Please keep in mind you will only receive a rst and second strike once in your retirement. Your strikes do not

reset each school year.

Service Retirement Before Jan. 1, 2021

Service retirees with an effective retirement date on or before Jan. 1, 2021 are not subject to the EAR restrictions.

They may work up to full time for a TRS-covered employer without forfeiting their annuity.

Services retirees with an effective retirement date after Jan. 1, 2021 are subject to the EAR restrictions. They may

only work for a TRS-covered employer without forfeiting their annuity if that work qualies for an EAR exception.

Please note the three strikes warning procedure does not apply to disability retirees. Disability retirees are still subject to

annuity forfeiture for all months that their employment does not qualify for an exception to the EAR restrictions applicable to

disability retirees.

Disability retirees are subject to the EAR restrictions regardless of their effective retirement date.

TEACHER RETIREMENT SYSTEM of TEXAS

3

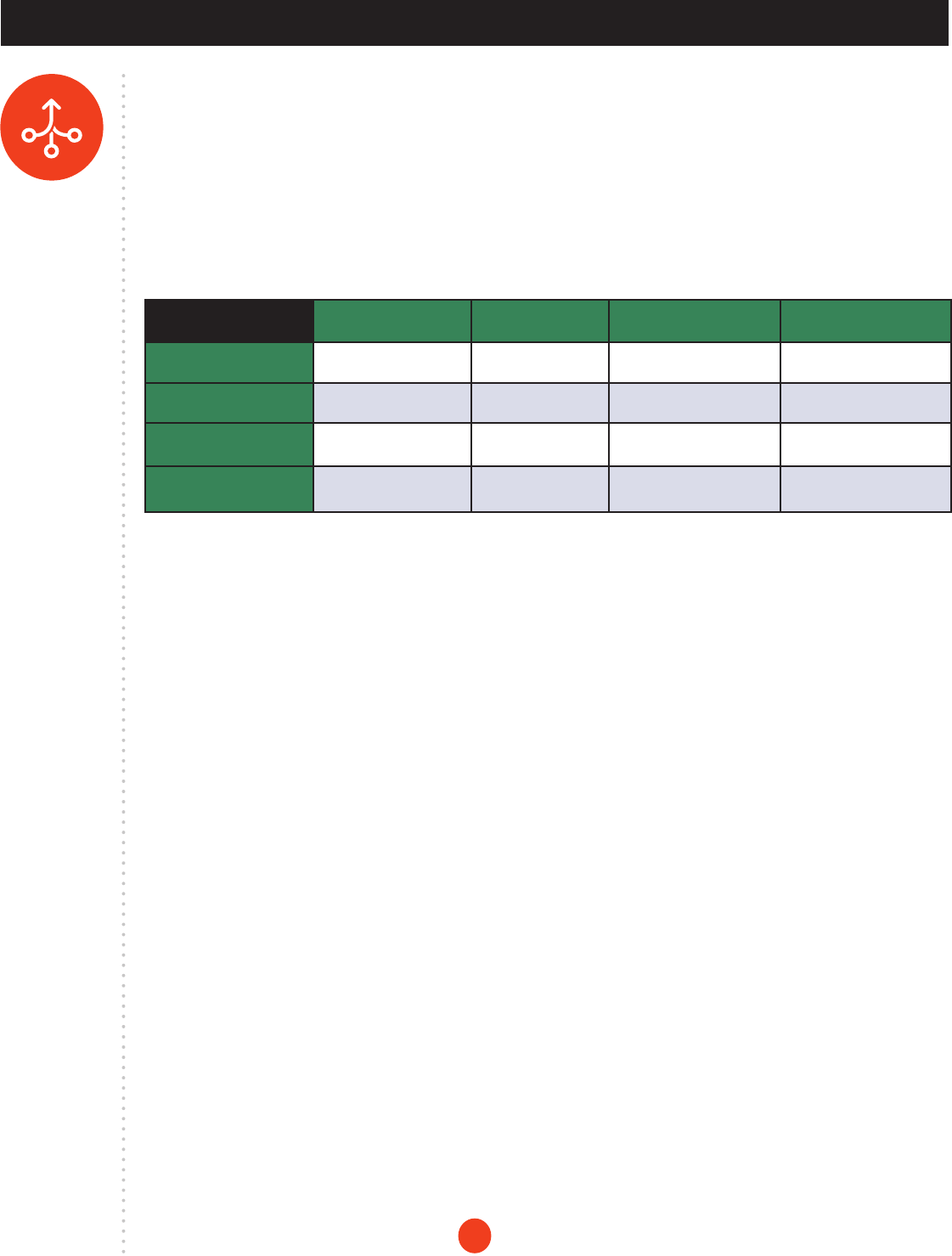

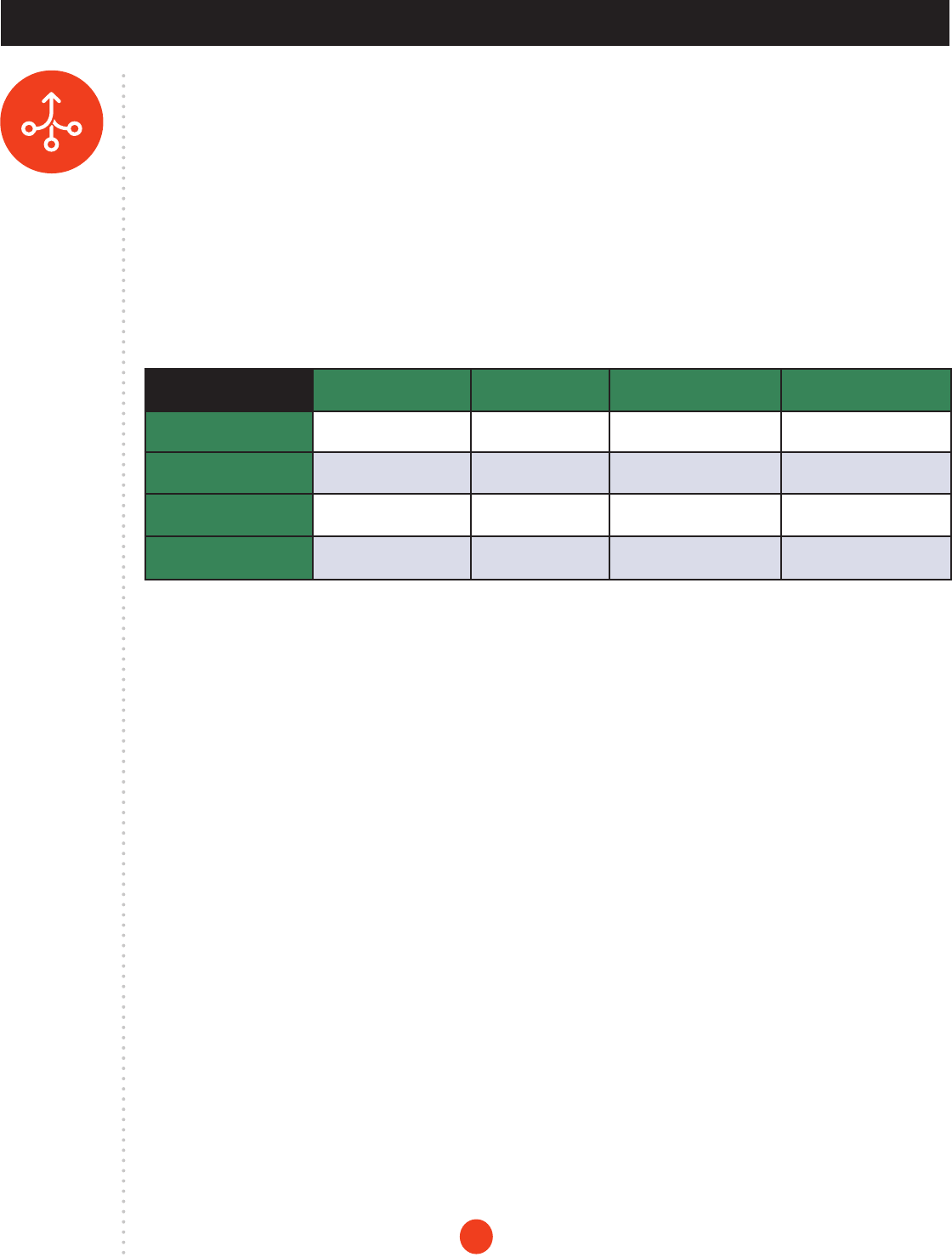

Effective Retirement Date One-Month Break in Service Return to Work

Before Jan. 1, 2021 Required No Restrictions

After Jan. 1, 2021 Required Limits Apply

Note: See June 15 rule if your effective retirement date is May 31 and you work up to June 15.

First-Strike Period Second-Strike Period Third-Strike Period

Months Included Includes month of issuance

of 1

st

warning and all

months prior to 1

st

warning

issuance.

Includes months after the

month of issuance of 1

st

warning letter through the

month of issuance of 2

nd

warning.

Includes months after the

month of issuance of 2

nd

warning letter through the

month of issuance of 3

rd

warning.

Collection None For each month of EAR limits

violation, retiree must pay

either full annuity or dollars

earned, whichever is less.

For each month of EAR limits

violation, retiree must pay

full annuity.

THINGS YOU SHOULD KNOW

4

Mandatory One-Month Break in Service

All retirees must observe a one full, calendar-month break in service after their effective retirement date to avoid revoking

their retirement. Returning to work for a TRS-covered employer in the month directly following your effective retirement

date will revoke your retirement. If you revoke your retirement, you will be required to return any annuity payments you

received along with any partial lump-sum option payments (PLSO) or TRS-Care health care payments you received. In

addition, if you wish to retire again, you must terminate all employment with TRS-covered employers and then resubmit

retirement paperwork with a new date.

Keep in mind, an early-age retiree may not negotiate with a TRS-covered employer, for any type of employment, before

completing the one full, calendar-month break in service. Normal-age retirees may not negotiate with a TRS-covered

employer for any type of employment that would not qualify for an EAR exception before completing their one full,

calendar-month break in service.

June 15 Rule

The June 15 rule allows a member to have a retirement date of May 31 if the member terminates his or her employment

no later than June 15 in order to complete all work required for the school year. This option delays the start of your one full,

calendar-month break in service. Therefore, you may not return to work from June 15 through July 31; otherwise, you will

revoke your retirement. Additionally, if you plan to observe a 12 full, consecutive-calendar-month break in service, the rst

full month of the break is July. This means the 12-month break in service ends June 30 of the following calendar year.

Volunteering and Independent Contractor Services

If you perform work as an independent contractor or volunteer for a TRS-covered employer during the rst 12 consecutive-

calendar months after your effective retirement date and that work would normally be done by an employee, you will be

considered an employee instead of a volunteer or independent contractor. This means your work will be subject to the EAR

restrictions. Therefore, if you’re a service retiree who retired after Jan. 1, 2021 or a disability retiree, this could cause you to

forfeit your annuity if your work does not qualify for an EAR exception. Furthermore, your work will restart your 12-month

break in service required to be eligible for full-time employment without restrictions.

After the rst 12 months following your retirement, you may volunteer or work as an independent contractor for a TRS-

covered employer, without being subject to the EAR restrictions, if you meet all the legal requirements for volunteering or

working as an independent contractor.

Working for a Third-Party Entity

A third-party entity is an entity retained by a TRS-covered employer to provide personnel to the institution to perform duties

or provide services that an employee of the institution would normally perform or provide. If a TRS retiree is employed

by a third-party entity and the retiree performs services for or on behalf of a TRS-covered employer, the retiree will be

considered employed in Texas public education for the purpose of EAR. This means the retiree’s work for the third-party

entity will be subject to the EAR restrictions. Any employment with a third-party entity will also restart a retiree’s 12-month

break in service required to be eligible for full-time employment without restrictions.

Medicare Secondary Payer for Return-to-Work Retirees

Beginning Sept. 1, 2022, the Medicare Secondary Payer Law lets Medicare-eligible TRS-Care retirees enroll in

TRS-ActiveCare if they return to work for an employer who participates in TRS-ActiveCare. If you’re a

return-to-work retiree enrolled in TRS-Care and eligible for Medicare, you may enroll in TRS-ActiveCare if you return

to a TRS employer and work 10 or more hours per week. Find more information in the TRS-ActiveCare Benets

Booklets available on the TRS website.

A TRS retiree who is subject to the EAR

restrictions may only work for a TRS-covered

employer without forfeiting his or her annuity

if that employment qualies for an EAR

exception. There are several EAR exceptions

available to TRS retirees. However, it’s

important to know the available exceptions

differ for service retirees and disability retirees.

EAR

EXCEPTIONS

EAR Exceptions for Service Retirees

A service retiree who retired after Jan. 1, 2021 cannot work for a TRS-covered employer

without violating the EAR restrictions and beginning the three strikes process unless the

retiree’s work qualies for an EAR exception. For this reason, it’s important to know what

EAR exceptions are available to you and what work qualies for those exceptions. You must

always have a one full, calendar-month break in service before you may return to work for

a TRS-covered employer even if the work qualies for an EAR exception.

This section explores each of the exception types; provides examples for how a service

retiree’s employment can qualify for each exception and how it can exceed the limits for

that exception; and discusses what happens if a retiree combines more than one EAR

exception in a month.

Substitute

One-Half Time or Less

Full Time (After a 12 Full, Consecutive-

Calendar-Month Break in Service)

Non-Prot Tutor

COVID-19 Surge Personnel

6

EAR EXCEPTIONS

EAR Exceptions Available to Service Retirees:

• Substitute Employment

• One-Half Time or Less Employment

• Full-Time Employment (after a 12 full, consecutive-calendar-month break in service)

• Non-Prot Tutor Employment

• COVID-19 Surge Personnel Employment

TEACHER RETIREMENT SYSTEM of TEXAS

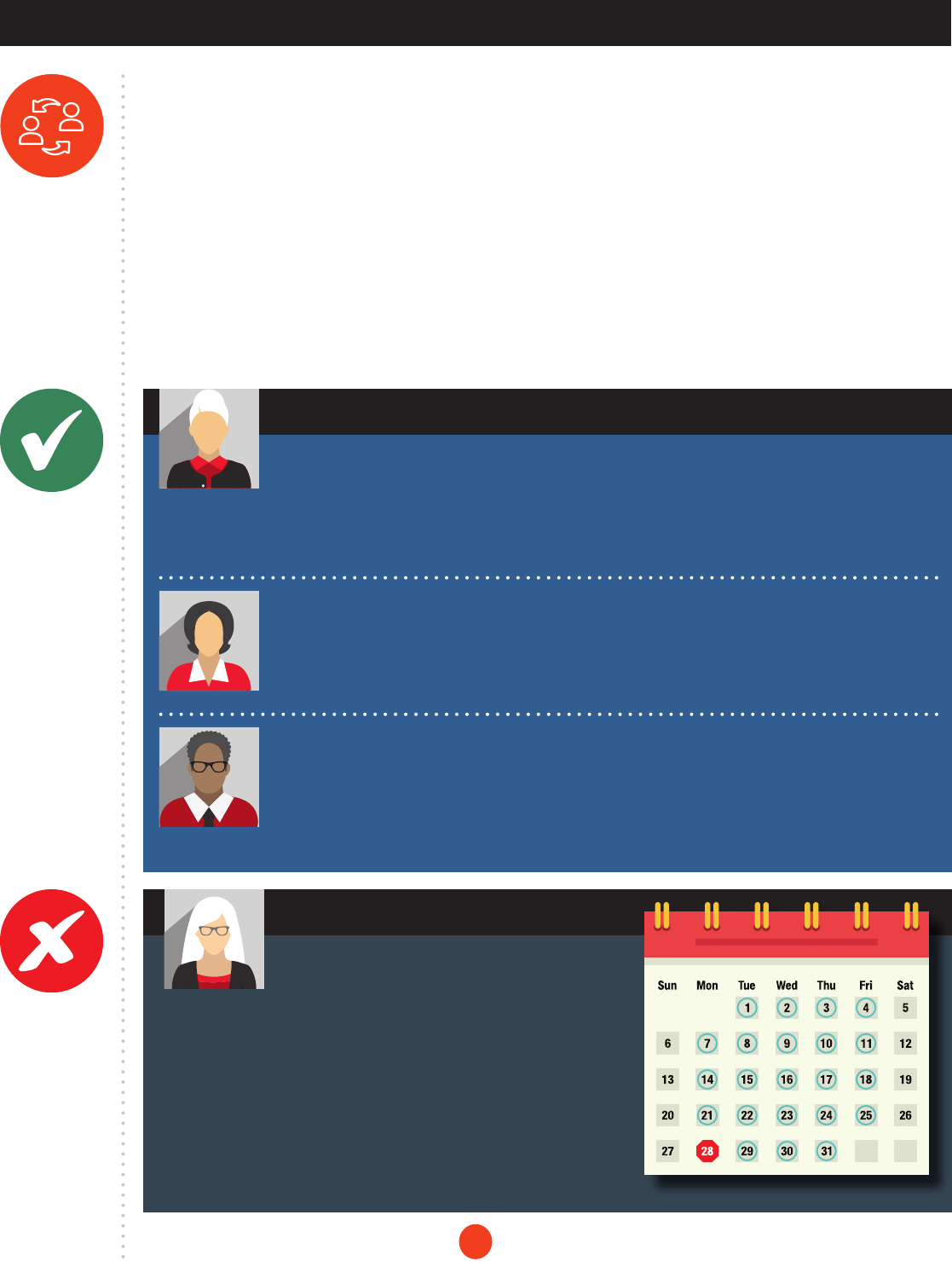

Exceeding EAR Limits

Kay decided to begin substituting in a position that recently

became vacant. She substituted for a total of 23 days.

Kay was limited to working no more than 20 days as a substitute in a vacant

position. She began substituting in the vacant position on the rst of the month.

As soon as her work in the vacant position continued past the 20

th

day (which

was the 28

th

of the month), she was no longer considered a substitute for the

month, which means her work on the 29

th

through the 31

st

was considered

one-half time or less employment, not substitute employment. Since she

worked in both a one-half time or less position and as a substitute in the same

month, Kay was subject to the limits for combining EAR exceptions, and she

exceeded those limits by working more than 11 days.

Substitute

A substitute is a person who serves on a temporary basis in place of a current employee. You may work without any limit on

the number of hours and days if:

• the position is not vacant;

• you are not paid more than the daily rate of pay established by the employer;

• and you do not perform any other type of work for a TRS-covered employer in the same calendar month.

You may work as a substitute in a vacant position for up to 20 days during a school year, but that position must not be vacant

because you retired from it. If you continue to work in that vacant position beyond 20 days in a school year, then, on the 21

st

day, your work in that position will no longer be considered as substitute work and may be at risk of exceeding EAR limits.

Your work may also qualify as substitute work if you temporarily serve as a monitor for an in-person class while the

classroom teacher temporarily instructs the class virtually.

Working any part of a day, as a substitute, counts as working a full day.

Complying with EAR Limits

After retiring in December and observing a one full, calendar-month break in service, Julia decided to begin

substituting in February at a local school district for positions that were not vacant. She performed no other work

for a TRS-covered employer during this time.

Julia complied with the EAR limits. She was able to substitute without any limit on the number of hours and days because the

positions she substituted for were not vacant, and she did not perform any other work for a TRS-covered employer during that time.

Sally retired in February 2020. She returned to work in December 2020 as a classroom monitor while Greta, the

teacher of record, was temporarily teaching the class remotely. She worked in this position until February 2021,

when Greta returned to teaching in the classroom after having taught virtually for 12 weeks.

Sally complied with the EAR limits. She was considered a substitute because she was temporarily monitoring the

classroom in person while Greta temporarily provided remote instruction.

Jack retired in February. After a one-month break in service, Jack returned to work as a substitute. Now three

teachers at Jack’s school are currently teaching classes remotely until they complete quarantine. Beginning in

April, Jack will be covering two classes for each teacher every day. He is expected to continue working in these

positions until May 15.

Jack is complying with the EAR limits. He is considered a substitute while temporarily monitoring the classroom

in person while the three teachers provide remote instruction.

7

One-Half Time or Less

This employment type allows you to work up to 92 hours per month. Any work you perform during a month, other than

substitute or COVID-19 surge personnel work, counts toward this 92-hour limit even if the work is done on a weekend or a

holiday. In addition, if you work for more than one TRS-covered employer during a month, you are still limited to 92 hours

total if you wish for that work to qualify for this exception. When determining the total number of hours a retiree worked in

the month, TRS-covered employers are required by law to report all hours worked, even Saturdays and Sundays, and any

paid leave.

For certain higher education positions, TRS uses an alternative calculation to determine whether a retiree’s work in that

position qualies as one-half time or less employment:

Higher Education Instruction in Classroom or Lab*

For employment measured in course hours or semester hours

rather than clock hours, each hour of instruction in the

classroom or lab counts as a minimum of two clock hours in

order to reect preparation, grading, and other time typically

associated with instruction.

Higher Ed Online Instruction*

Online instructors teaching classes taken by students for college

credit must be counted as a minimum of two hours for each

course or semester hour to determine the number of hours worked.

Continuing or Adult Education

Continuing education, adult education, and/or classes offered to employers or businesses for employee training (for which

students/participants do not receive college credit), must be counted based on the number of clock hours worked.

EAR EXCEPTIONS

Exceeding EAR Limits

George decided to go back to work one-half time or less

in May. He agreed to work 10 hours per day on Mondays

and Tuesdays. There were four full weeks and one partial week in May.

George worked 100 hours during the month.

The following month he received a letter from TRS notifying him that he

exceeded EAR limits in May.

George was very confused because he knew that he had followed his

employer’s guidelines and worked according to his agreed schedule.

George looked at the EAR trifold and read that he could only work 92 hours

during the month in a one-half time or less position. He exceeded EAR limits

for one-half time or less employment by eight hours that month.

Complying with EAR Limits

After retiring in May, David decided to go back to work in a one-half time or less position in November. This

means David could work up to 92 hours in November. For the rst two weeks, he was scheduled to work 40

hours a week for a total of 80 hours. He did not work any hours the last two weeks of the month.

David complied with the EAR limits on one-half time or less employment. He had a one full, calendar-month break in service

before going back to work and did not exceed 92 hours of work during November.

* If your employer has established a greater

amount of preparation time for each hour

of instruction, your employer’s established

multiplier will be used to determine the

number of hours you worked. Check with

your employer to determine if they will use

the standard two clock hours or if they have

established a different multiplier. Your employer

will be able to provide this information.

8

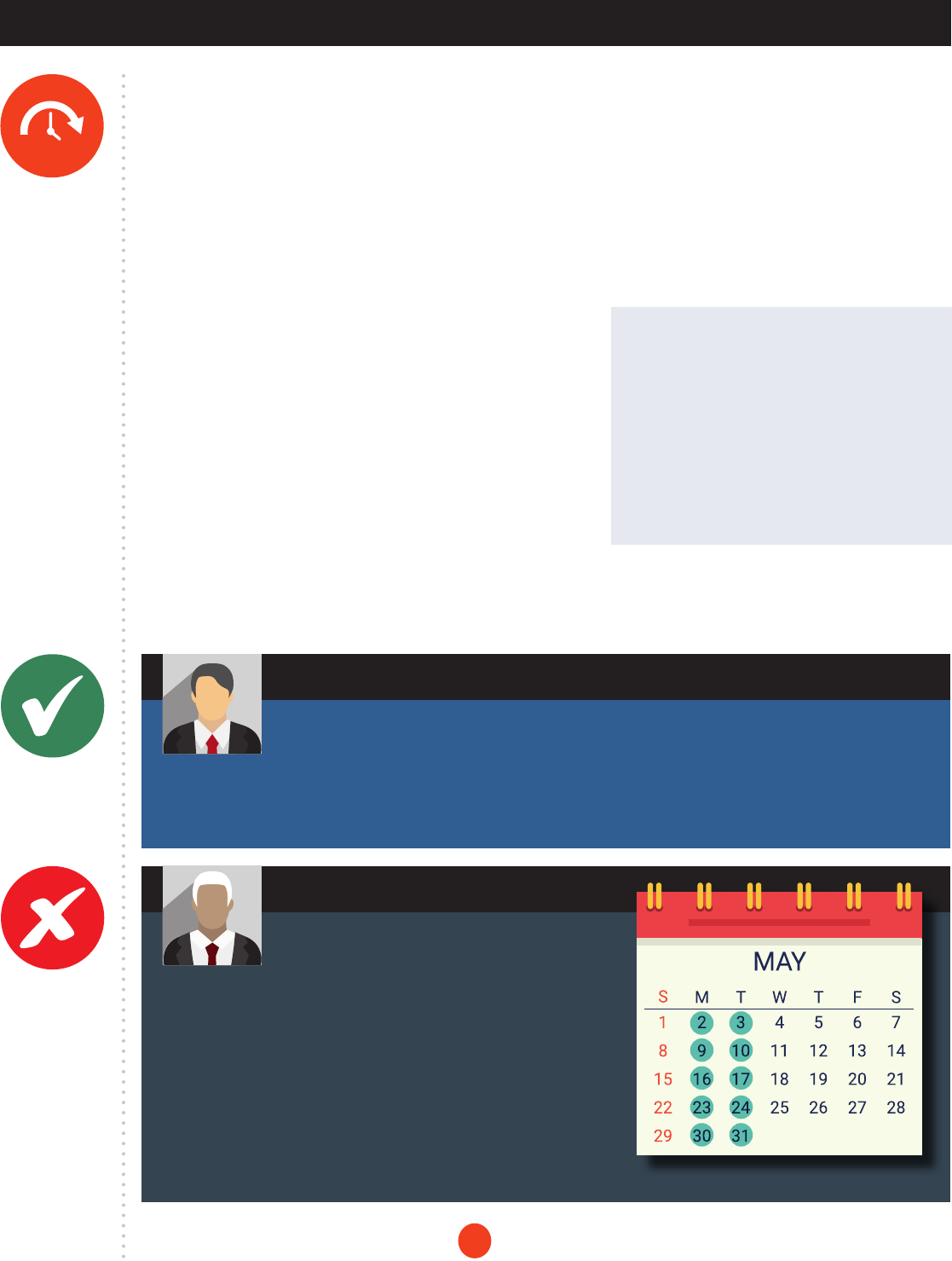

Exceeding EAR Limits

Patrick retired in July and returned to work in September of the same year as a substitute for a teacher

that was out on medical leave. The teacher decided to resign, and the district offered Patrick a full-time

position in January of the following year.

Since Patrick did not have a 12 full, consecutive-calendar-month break in service before going back to work full time and

the position did not qualify for any other EAR exception that would allow him to work full time, he violated the EAR limits

beginning in January.

Full Time (After a 12 Full, Consecutive-Calendar-Month Break in Service)

Service retirees with an effective retirement date after Jan. 1, 2021 may work full time in any position without forfeiting

monthly annuity payments after observing a 12 full, consecutive-calendar-month break in service. This break in service

begins the day after your effective retirement date and ends on the last day of the 12

th

month. You cannot work in any

capacity in Texas public education during the 12-month break in service.

If you retired effective May 31 but used the June 15 rule to continue working in June, the rst full month of your 12 full,

consecutive-calendar-month break is July. This means the 12-month break in service ends June 30 of the following

calendar year.

Non-Prot Tutor

A service retiree may work up to full time for a TRS-covered employer in a non-prot tutor position. This exception does

not cover all tutor work that a retiree performs for a school district if the retiree is afliated with a non-prot entity.

Instead, the retiree’s tutor employment must meet all requirements for qualifying tutor employment under Section

33.913, Education Code. Tutoring programs under Section 33.913 are administered by school districts; you should

contact any school district regarding their local program if you wish to be employed under this exception.

Note: A retiree may not be eligible to work full time under this exception if the work is combined with other types of

employment.

TEACHER RETIREMENT SYSTEM of TEXAS

9

Complying with EAR Limits

Gabriela retired from TRS in March 2022. In April 2023, she decided to take a full-time teaching position

with a local school district. Gabriela did not work in any capacity for any TRS-covered employer after

her retirement prior to taking the teaching position in April 2023.

Gabriela’s work qualied for the full-time exception because she took a 12 full, consecutive-calendar-month break from

all TRS-covered employment after her retirement.

Complying with EAR Limits

Rachel retired in July. She returned to work in October as a tutor that qualied under the Non-Prot

Tutor Exception because the position met all the requirements of Section 33.913, Education Code.

Rachel worked full time in the non-prot tutor position and did not perform any other work.

Rachel complied with EAR limits. The Non-Prot Tutor Exception allows her to work full time without restrictions.

10

COVID-19 Surge Personnel

The COVID-19 Surge Personnel Exception allows a service retiree to return to work up to full time in a federally

funded position that is in addition to normal stafng levels of the school and perform duties related to the mitigation

of student learning loss attributable to the coronavirus disease (COVID-19) pandemic. In addition, the position must

terminate no later than Dec. 31, 2024. This exception does not apply to employment with an institution of higher

education.

Importantly, any work performed under this exception does not count toward a retiree’s total 92-hour limit for one-

half time or less employment during a month. Work performed under this exception does not combine with or affect

a retiree’s employment under any other EAR exception.

Lastly, the COVID-19 Surge Personnel Exception is a surcharge exception. If your employer hires you under this

exception, your employment will not subject your employer to pension or health care surcharges.

EAR EXCEPTIONS

Complying with EAR Limits

Steve retired from TRS in December and completed a one full, calendar-month break in service.

Beginning Feb. 1, he accepted a full-time position that qualied under the Surge Personnel Exception.

He did not perform any other work in the same calendar month.

Steve’s employment qualied for the COVID-19 Surge Personnel Exception. He was allowed to work unlimited without

restrictions. He was not subject to surcharges.

TEACHER RETIREMENT SYSTEM of TEXAS

11

Note: Determining the correct monthly limits when combining EAR exceptions can be complicated in many

cases and a retiree should strongly consider contacting TRS for guidance before doing so.

Combining EAR Exceptions for Service Retirees

If you choose to be employed in multiple positions for either multiple TRS-covered

employers or for the same employer during a month and each of those positions qualify for

EAR exceptions, the limits on the number of hours or days you may work in those positions

may be different than if you worked in either position individually. Here are descriptions and

examples of some of the more common EAR exceptions retirees combine in a month and

the limits that apply.

Substitute + One-Half Time or Less

One-Half Time or Less + COVID-19

Surge Personnel

One-Half Time or Less + Non-Prot

Tutor

Substitute + Non-Prot Tutor

Employment Type Substitute

Tutor Under Section

33.913 Full Time

Tutor Under Section 33.913

One-Half Time

One-Half Time or Less

Substitute No limit for lled positions; if

vacant position, 20-day limit

Cannot be combined Total combined employment

cannot exceed 11 days

Total combined employment

cannot exceed 11 days

Tutor Under Section 33.913

Full Time

Cannot be combined No limit No limit Cannot be combined

Tutor Under Section 33.913

One-Half Time

Total combined employment

cannot exceed 11 days

No limit No limit Total combined employment

cannot exceed 92 hours

One-Half Time or Less Total combined employment

cannot exceed 11 days

Cannot be combined Total combined employment

cannot exceed 92 hours

Total combined employment

cannot exceed 92 hours

12

EAR EXCEPTIONS

Substitute + One-Half Time or Less

You may work as a substitute for one month and then work as much as one-half time or less the next month. However,

if you work as a substitute and in a one-half time or less position in the same month, your combined work must not

exceed 11 workdays in that calendar month. When determining the total number of days a retiree worked in the month,

TRS-covered employers are required by law to report all days worked, even Saturdays and Sundays, and any paid

leave. Working any part of a day counts as working a full day.

You will violate the EAR limits for any month you exceed 11 workdays allowed in the calendar month.

Complying with EAR Limits

Lauren retired in July. After observing a one full, calendar-month break in service, she decided to

perform a combination of substitute and one-half time or less work.

Lauren worked as a substitute for 20 days in September. She knew she could work an unlimited number of days in a

substitute position and complied with EAR limits.

Then, in October she worked in a one-half time or less position. She worked 90 hours which did not exceed the 92-hour

monthly limit for one-half time or less employment.

In November, she combined substitute and one-half time or less work. She worked 11 days. When her employer asked her

to substitute an additional day, she let them know she couldn’t work more than 11 days without violating EAR limits.

Lauren did not violate any restrictions. She had a one full, calendar-month break in service before going back to work and

did not exceed the limits for the months she worked.

Exceeding EAR Limits

After retiring in July and having a one full, calendar-month break in service after her effective retirement

date, Valarie was hired by a community college in a one-half time or less position. Valarie worked in this

position October through March.

In March, a previous employer contacted her to perform substitute work. The employer was having a difcult time nding a

qualied substitute and expressed how much they needed her skills. As a result, Valarie substituted for a teacher that was

out on medical leave.

In April, Valarie received a letter notifying her that she exceeded the EAR limits. The limit when combining one-half time or

less and substitute work is 11 workdays. Since she worked 14 days, she violated EAR limits.

During March, Valarie worked the

following dates in both positions:

MARCH

4, 5, 6, 11, 12, 13, 18, 19, 20,

25, 26, 27, 28, and 29

for a total of 14 days.

13

TEACHER RETIREMENT SYSTEM of TEXAS

One-Half Time or Less + COVID-19 Surge Personnel

You may work in a one-half time or less position and a COVID-19 Surge Personnel position in a month, and any

hours you work in the COVID-19 Surge Personnel position will not count toward your 92-hour monthly limit for one-

half time or less employment.

Complying with EAR Limits

After retiring in May and completing a one full, calendar-month break in service, Jane decided to return to

work in a one-half time or less position on Aug. 1. She worked 90 hours that month. She also wanted to

help in another position that qualied for the COVID-19 Surge Personnel Exception. She worked 46 hours in that position.

Jane complied with EAR limits. She did not exceed the 92 hours allowed per month in the one-half time or less position

because the surge personnel employment does not count toward the 92-hour limit.

Exceeding EAR Limits

Rhonda retired in March and completed a one full, calendar-month break in service. Her former

employer asked if she could return to work in a one-half time or less position beginning in June. She

accepted the position. Rhonda also accepted a one-half time position with another employer that qualied under the

COVID-19 Surge Personnel Exception. In June, Rhonda worked 96 hours in the one-half time or less position, and she

worked 34 hours in the COVID-19 Surge Personnel position.

In July, Rhonda received a letter notifying her that she exceeded the EAR limits for one-half time or less employment. Even

though her hours worked in the COVID-19 Surge Personnel position did not count toward her 92-hour monthly limit for

one-half time or less employment, she still worked more than the 92 hours in the one-half time or less position.

14

EAR EXCEPTIONS

One-Half Time or Less + Non-Prot Tutor

You may combine one-half time or less employment and employment under the Non-Prot Tutor Exception during

a month, but any work you perform under the exception will count toward your 92-hour monthly limit for one-half

time or less employment. This means even though you’re able to work up to full time in a non-prot tutor position,

your work when combining these two employment types cannot exceed 92 hours total. When determining the total

number of hours a retiree worked in the month, TRS-covered employers are required by law to report all hours

worked, even Saturdays and Sundays, and any paid leave.

Complying with EAR Limits

After retiring in July and completing a one full, calendar-month break in service, Sarah decided to

return to work in a one-half time or less position on Sept. 1. She worked 60 hours that month. She also

wanted to help in another position that qualied for the Non-Prot Tutor Exception. Sarah worked 20 hours in the non-

prot tutor position during that month.

Sarah complied with EAR limits for combining one-half time or less employment and employment under the Non-Prot

Tutor Exception. The total combined hours did not exceed the 92 hours allowed in a calendar month.

Exceeding EAR Limits

Kevin retired in May and completed a one full, calendar-month break in service. He accepted a full-time

position under the Non-Prot Tutor Exception beginning in September. Kevin also started working in a one-half

time or less position with another employer in the same month.

In October, Kevin received a letter notifying him that he exceeded the EAR limits for one-half time or less employment in a

month. He was not allowed to combine one-half time or less work with work in a full-time non-prot tutor position in the

same calendar month.

Bob retired in May and completed a one full, calendar-month break in service. He accepted a one-half

time or less position under the Non-Prot Tutor Exception beginning in September. Bob worked 82 hours

that month. In September, he also started working in a one-half time or less position that did not qualify

for the Non-Prot Tutor Exception. He worked 22 hours.

In October, Bob received a letter from TRS notifying him that he had exceeded the EAR limits for

September. He worked a total of 104 hours in September which exceeded the 92 hours allowed for one-half time or less

employment in a calendar month.

15

TEACHER RETIREMENT SYSTEM of TEXAS

Substitute + Non-Prot Tutor

You may work unlimited as a substitute for one month and then work unlimited as a non-prot tutor in another

month. However, if you work as a substitute and as a non-prot tutor in the same month, your combined work must

not exceed 11 workdays in that calendar month.

You will violate the EAR limits for any month you combine substitute and non-prot tutor employment in a month and

exceed the 11 workdays allowed.

Complying with EAR Limits

Oliver retired in March. After observing a one full, calendar-month break in service, he decided to perform

a combination of substitute and non-prot tutor work.

In May, Oliver worked as a substitute for eight days and worked as a non-prot tutor for three days. When his employer asked

him to substitute an additional day, he let them know he couldn’t work more than 11 days in the month without violating EAR

limits for substitute and non-prot tutor employment.

Oliver did not violate any restrictions because he stayed within the monthly limits that applied.

Exceeding EAR Limits

Susan retired in May. After observing a one full, calendar-month break in service, she decided to perform

a combination of substitute and non-prot tutor work. In September, Susan worked as a substitute for 11

days and worked as a non-prot tutor for one day.

In October, Susan received notice from TRS that she exceeded the EAR restrictions for September because she worked a

total of 12 days.

16

EAR EXCEPTIONS

EAR Exceptions for Disability Retirees

A disability retiree, regardless of effective retirement date, cannot work for a TRS-covered

employer during a month without forfeiting his or her annuity for that month unless the retiree’s

work qualies for an EAR exception. For this reason, it’s important to know what EAR exceptions

are available to you and what work qualies for those exceptions. Remember, you must always

have a one full, calendar-month break in service before you may return to work for a

TRS-covered employer even if the work qualies for an EAR exception.

EAR Exceptions Available to Disability Retirees:

• Substitute Employment (for up to 90 days in a school year)

• One-Half Time or Less Employment (for up to 90 days in a school year)

• Non-Prot Tutor Employment (for up to 90 days in a school year)

• One-Time Three-Month Trial Work Period

This section explores each of the exception types; provides examples for how a disability

retiree’s employment can qualify for each exception and how it can exceed the limits for

that exception; and discusses what happens if a retiree combines more than one EAR

exception in a month.

For some disability retirees, the law limits the amount of compensation you may earn from

any source without losing annuity payments. This section also includes more information on

this topic.

Please note: The 12 full, consecutive-calendar-month break in service and the COVID-19 Surge

Personnel Exception are not available to disability retirees.

Substitute (For up to 90 Days)

One-Half Time or Less (For up to 90 Days)

Non-Prot Tutor (For up to 90 Days)

Three-Month Trial Work Period

17

Substitute (For up to 90 Days)

A substitute is a person who serves on a temporary basis in place of a current employee. You may work without any

limit on the number of hours and days in a month if:

• the position is not vacant;

• you are not paid more than the daily rate of pay established by the employer;

• and you do not perform any other type of work for a TRS-covered employer in the same calendar month.

You may work as a substitute in a vacant position, but the position must not be vacant because you retired from

it. You may work up to 20 days during a school year without forfeiting your annuity. If you continue to work in that

vacant position beyond 20 days in a school year, then, on the 21

st

day, your work in that position will no longer be

considered as substitute work and may be at risk of exceeding EAR limits.

Your work may also qualify as substitute work if you temporarily serve as a monitor for an in-person class while the

classroom teacher temporarily instructs the class virtually.

However, while a disability retiree may work an unlimited number of days or hours in a month as a substitute

(assuming the retiree does not work more than 20 days in any vacant positions), a disability retiree may not work

more than 90 days TOTAL in a school year as a substitute. Once a retiree exceeds the 90-day limit per school year,

the retiree will forfeit his or her annuity for that month and every month thereafter for the remainder of the school

year in which the retiree works.

Working any part of a day, as a substitute, counts as working a full day.

TEACHER RETIREMENT SYSTEM of TEXAS

Complying with EAR Limits

Kate retired due to a disability in March and ended all employment with her TRS-covered employer. In

September, she decided to return to work. Kate substituted 60 days in the current school year while on

disability retirement.

Kate did not violate TRS laws and rules as she did not return to work in the month following her retirement. In addition,

she did not exceed the 90-day limit for the school year.

Exceeding EAR Limits

Ted retired due to a disability in June and ended all employment with his TRS-covered employer. In the fall

semester, he substituted 62 days. Then, he substituted for 20 days in January and another 10 days in February.

Ted exceeded the EAR limits for a disability retiree working as a substitute and will forfeit his annuity in February because he

worked more than 90 days in a school year. In addition, if Ted works any days in the following months during the same school

year, he will also forfeit his annuity for those months because he has already exceeded the 90-day limit.

EAR EXCEPTIONS

One-Half Time or Less (For up to 90 Days)

This employment type allows you to work up to 92 hours per month. Any work you perform during a month, other than

substitute work, counts toward this 92-hour limit even if that work is done on a weekend or a holiday. In addition, if you

work for more than one TRS-covered employer during a month, you are still limited to 92 hours total if you wish for that

work to qualify for this exception. When determining the total number of hours a retiree worked in the month, TRS-covered

employers are required by law to report all hours worked, even Saturdays and Sundays, and any paid leave.

For certain higher education positions, TRS uses an alternative calculation to determine whether a retiree’s work in that

position qualies as one-half time or less employment:

Higher Education Instruction in Classroom or Lab*

For employment measured in course hours or semester hours

rather than clock hours, each hour of instruction in the classroom

or lab counts as a minimum of two clock hours in order to reect

preparation, grading, and other time typically associated

with instruction.

Higher Ed Online Instruction*

Online instructors teaching classes taken by students for college

credit must be counted as a minimum of two hours for each

course or semester hour to determine the number of hours worked.

Continuing or Adult Education

Continuing education, adult education, and/or classes offered to employers or businesses for employee training (for which

students/participants do not receive college credit), must be counted based on the number of clock hours worked.

Remember: The 90-day limit per school year still applies to employment under this exception. Once a retiree exceeds

the 90-day limit per school year, the retiree will forfeit his or her annuity for that month and every month thereafter for the

remainder of the school year in which the retiree works.

Complying with EAR Limits

Kathy retired due to a disability in August and ended all employment with her TRS-covered employer. In

November, she decided to return to work for a school district in a one-half time or less position. Kathy worked

89 hours over the course of 20 days in November. In January, she worked 64 hours over the course of 12 days.

Kathy did not exceed the limits for disability retirees working one-half time or less. She never worked more than 92 hours in a

month and did not exceed the 90-day limit for the school year.

* If your employer has established a greater

amount of preparation time for each hour

of instruction, your employer’s established

multiplier will be used to determine the

number of hours you worked. Check with

your employer to determine if they will use

the standard two clock hours or if they have

established a different multiplier. Your employer

will be able to provide this information.

Exceeding EAR Limits

Maria retired due to a disability in December and decided to return to work in February. She accepted

a one-half time or less position at an education service center. During February Maria worked a total of

120 hours over the course of 16 days.

Maria exceeded the EAR limits for a disability retiree working under the one-half time or less exception because she

exceeded the 92-hour monthly limit.

Xavier retired due to disability in May and accepted a one-half time or less job at a school district.

Beginning in September, he worked a set schedule of 60 hours over 15 days every month. Based on

this schedule, Xavier worked his 91

st

day in March.

Xavier forfeited his annuity in March because he worked more than 90 days in the school year. In

addition, if Xavier works any days in the following months during the same school year, he will also

forfeit his annuity for those months because he has already exceeded the 90-day limit.

TEACHER RETIREMENT SYSTEM of TEXAS

19

Non-Prot Tutor (For up to 90 Days)

A disability retiree may work up to full time for a TRS-covered employer in a non-prot tutor position. This exception

does not cover all tutor work that a retiree performs for a school district if the retiree is afliated with a non-prot

entity. Instead, the retiree’s tutor employment must meet all the requirements for qualifying tutor employment under

Section 33.913, Education Code. Tutoring programs under Section 33.913 are administered by school districts;

contact any school district regarding their local program if you wish to be employed under this exception.

Note: A retiree may not be eligible to work full time under this exception if the work is combined with other types of

employment. As with other EAR exceptions for disability retirees, a disability retiree may not work more than 90 days

in a school year under this exception.

Three-Month Trial Work Period

As a disability retiree, you are allowed a one-time only trial work period to determine if you can return to work full

time. This trial period must be three consecutive months. To opt for the trial work period, you must notify TRS by

submitting the Employment after Retirement Disability Election form (TRS 118D), found on the TRS website. The TRS

118D must be led with TRS before the end of the trial period for the election to be effective. The trial work period

cannot be elected in the same school year you retired.

If you continue to work full time after the trial work period has ended, you will be recovered from disability

retirement and returned to active membership. You must repay any annuity payments that you received after being

restored to active service.

Any days you work during the three-month trial period do not count against the 90-day limit for a school year. In

addition to the trial work period, you can work up to 90 days as a substitute, one-half time or less, a combination

of substitute and one-half time or less, or in a non-prot tutor position. However, you will forfeit your annuity in any

month you work past the 90-day limit or you exceed the monthly limits.

Complying with EAR Limits

Ethan retired due to a disability in July. He returned to work in October as a tutor that qualied under the

Non-Prot Tutor Exception because the position met all the requirements of Section 33.913, Education

Code. Ethan worked full time in the non-prot tutor position and did not perform any other work. Ethan stopped working in

the non-prot tutor position after working 89 days in the school year.

Ethan complied with EAR limits for work under the Non-Prot Tutor Exception. The exception allows him to work full time in a

month as long as he does not work more than 90 days in the school year.

Exceeding EAR Limits

Sandy retired due to a disability in September and decided to return to work in November. She began working

as a tutor that qualied under the Non-Prot Tutor Exception because the position met all the requirements of

Section 33.913. She worked full time in the position and worked her 91

st

day in February.

Sandy forfeited her annuity in February because she worked more than 90 days in the school year. In addition, if Sandy works

any days in the following months during the same school year, she will also forfeit her annuity for those months because she has

already exceeded the 90-day limit.

20

EAR EXCEPTION

Combining EAR Exceptions for Disability Retirees

If you choose to be employed in multiple positions for either multiple TRS-covered

employers or for the same employer and each of those positions qualify for EAR exceptions,

the number of hours or days that you may work in those positions may be limited.

Remember: All days you work in a school year count toward the 90-day limit unless those

days are part of a three-month trial period. The 90-day limit applies regardless of the

employment type or combination of types.

Here are descriptions and examples of some of the more common EAR exceptions that

disability retirees combine in a month and the limits that apply.

Note: Determining the correct monthly limits when combining EAR exceptions can be complicated in many

cases and a retiree should strongly consider contacting TRS for guidance before doing so.

* All days worked in a school year count toward the 90-day limit unless those days are part of a three-month

trial period. The 90-day limit applies regardless of the employment type or combination of types.

Substitute + One-Half Time or Less

Substitute + Non-Prot Tutor

One-Half time or Less + Non-Prot Tutor

Employment Type Substitute*

Tutor Under Section

33.913 Full Time*

Tutor Under Section 33.913

One-Half Time*

One-Half Time or Less*

Substitute* No limit for lled positions; if

vacant position, 20-day limit

Cannot be combined Total combined employment

cannot exceed 11 days

Total combined employment

cannot exceed 11 days

Tutor Under Section 33.913

Full Time*

Cannot be combined No limit No limit Cannot be combined

Tutor Under Section 33.913

One-Half Time*

Total combined employment

cannot exceed 11 days

No limit No limit Total combined employment

cannot exceed 92 hours

One-Half Time or Less* Total combined employment

cannot exceed 11 days

Cannot be combined Total combined employment

cannot exceed 92 hours

Total combined employment

cannot exceed 92 hours

TEACHER RETIREMENT SYSTEM of TEXAS

21

Substitute + One-Half Time or Less

You may work as a substitute for one month and then work as much as one-half time or less the next month.

However, if you work as a substitute and in a one-half time or less position in the same month, your combined work

must not exceed 11 workdays in that calendar month. When determining the total number of days a retiree worked

in the month, TRS-covered employers are required by law to report all days worked, even Saturdays and Sundays,

and any paid leave. Working any part of a day counts as working a full day.

You will violate the EAR limits for any month you exceed 11 workdays allowed in the calendar month.

Complying with EAR Limits

Michele retired due to a disability in November. After observing a one full, calendar-month break in service,

she decided to perform a combination of substitute and one-half time or less work.

Michele worked as a substitute for 20 days in January. She knew she could work an unlimited number of days in a substitute

position and complied with EAR limits.

Then, in February she worked in a one-half time or less position. She worked 90 hours over the course of 16 days which did

not exceed the 92-hour monthly limit for one-half time or less employment.

In March, she combined substitute and one-half time or less work. She worked 11 days. When her employer asked her to

substitute an additional day, she let them know that she couldn’t work more than 11 days in the month without violating EAR

limits.

Michele did not violate any restrictions. In each month she worked, she stayed within any monthly limits that applied.

Similarly, she did not exceed the 90-day limit for the school year.

Exceeding EAR Limits

After retiring in July due to a disability and having a one full, calendar-month break in service after her

effective retirement date, Rebecca was hired by a community college in a one-half time or less position.

Rebecca worked in this position October through January.

During January, a previous employer contacted her to perform substitute work. The employer was having a difcult time nding a

qualied substitute and expressed how much they needed her skills. As a result, Rebecca substituted for a teacher that was out

on medical leave.

In February, Rebecca received a letter notifying her that she exceeded the EAR limits. The limit when combining one-half time or

less and substitute work is 11 workdays. Since she worked 14 days, she violated EAR limits.

During January, Rebecca worked the

following dates in both positions:

JAN.

3, 4, 5, 11, 12, 13, 18, 19, 20, 23,

25, 26, 27, and 29

for a total of 14 days.

22

EAR EXCEPTIONS

Substitute + Non-Prot Tutor

You may work unlimited as a substitute for one month and then work unlimited as a non-prot tutor in another month,

provided you do not exceed the 90-day limit for the school year. However, if you work as a substitute and as a non-prot

tutor in the same month, your combined work must not exceed 11 workdays in that calendar month.

You will violate the EAR limits for any month you combine substitute and non-prot tutor employment in a month and exceed

the 11 workdays allowed.

Complying with EAR Limits

Thomas retired due to a disability in March. After observing a one full, calendar-month break in service, he

decided to perform a combination of substitute and non-prot tutor work.

In May, Thomas worked as a substitute for eight days and worked as a non-prot tutor for three days. When his employer

asked him to substitute an additional day, he let them know he couldn’t work more than 11 days in the month without

violating EAR limits for substitute and non-prot tutor employment.

Thomas did not violate any restrictions because he stayed within the monthly limits that applied.

Exceeding EAR Limits

Josie retired in May due to a disability. After observing a one full, calendar-month break in service, she decided

to perform a combination of substitute and non-prot tutor work. In September, Josie worked as a substitute

for 11 days and worked as a non-prot tutor for one day.

Josie forfeited her annuity for September because she worked a total of 12 days.

One-Half Time or Less + Non-Prot Tutor

You may combine one-half time or less employment and employment under the Non-Prot Tutor Exception during a month,

but any work you perform under the exception will count toward your 92-hour monthly limit for one-half time or less

employment. This means even though you’re able to work up to full time in a non-prot tutor position, provided you do not

exceed the 90-day limit for the school year, your work when combining one-half time or less employment with non-prot

tutor employment in the same month cannot exceed 92 hours total in that month. When determining the total number of

hours a retiree worked in the month, TRS-covered employers are required by law to report all hours worked, even Saturdays

and Sundays, and any paid leave.

TEACHER RETIREMENT SYSTEM of TEXAS

23

Complying with EAR Limits

After retiring in July and completing a one full, calendar-month break in service, Tonya decided to return

to work in a one-half time or less position on Sept. 1. She worked 60 hours that month. She also wanted

to help in another position that qualied for the Non-Prot Tutor Exception. Tonya worked 20 hours in the non-prot tutor

position during that month.

Tonya complied with EAR limits for combining one-half time or less employment and employment under the Non-Prot Tutor

Exception. The total combined hours did not exceed the 92 hours allowed in a calendar month.

Exceeding EAR Limits

Michael retired in May and completed a one full, calendar-month break in service. He accepted a full-time

position under the Non-Prot Tutor Exception beginning in September. Michael also started working in a one-

half time or less position with another employer in the same month.

In October, Michael received a letter notifying him that he exceeded the EAR limits for one-half time or less employment in

a month. He was not allowed to combine one-half time or less work with work in a full-time non-prot tutor position in the

same calendar month.

If you applied for disability retirement or retired

before Aug. 31, 2007, there is no limit on

compensation you can earn while receiving a

disability retirement annuity from TRS.

COMPENSATION

LIMITS FOR

DISABILITY

RETIREES

Compensation Limits for Disability Retirees

If the following two conditions are met, there is a limit on the amount of annual compensation you may earn:

• you apply for disability retirement after Aug. 31, 2007; and

• your effective retirement date is after Aug. 31, 2007.

The compensation cap is based on your income during a calendar year. It includes compensation for

any work performed for any employer including a TRS-covered employer, self-employment, work as an

independent contractor, and prot from a business.

The limit is the highest salary received in any school year before disability retirement or $40,000,

whichever is greater. This limit does not apply to retirees receiving gross disability retirement benets of

$2,000 or less per year. If you’re subject to the cap, you must correctly report your compensation to TRS by

May 1 of the calendar year after the compensation was earned.

If you exceed the amount of compensation allowed, you will forfeit your disability annuity payment and you

will be required to pay for the full cost of your TRS-Care coverage, until you are able to report that your

compensation is below the established limit.

TEACHER RETIREMENT SYSTEM of TEXAS

25

The following page contains information

to help you nd answers should you have

additional questions concerning employment

after retirement.

ADDITIONAL

INFORMATION

27

TEACHER RETIREMENT SYSTEM of TEXAS

EAR Limits Chart

View the EAR Limits information on the Employment After Retirement (EAR) Limits (for Retirees) page on the

TRS website.

Interactive Employment After Retirement Video

Have you explored our interactive Employment After Retirement video? This video answers some of our active

members’ and retirees’ most common questions about returning to work after retirement as well as rules and

restrictions that may apply. Find the video, along with other videos in our Member Education Video Series, on

the TRS Member Education Videos page on the TRS website.

TRS Website:

www.trs.texas.gov

TRS Mailing Address:

Teacher Retirement System of Texas

1000 Red River Street

Austin, Texas 78701-2698

TRS Telephone Counseling Center:

1-800-223-8778

Monday – Friday, 7 a.m. – 6 p.m. Automated information is available day or night, seven days a week.

TRS Benet Services Fax Number:

512-542-6597

Follow Us On:

i

This brochure has been written in nontechnical terms wherever

possible. However, if questions of interpretation arise as a result

of the attempt to make the information about employment after

retirement easy to understand, TRS laws and rules must remain the

nal authority.

This information is based upon the TRS plan terms in effect on

Nov. 1, 2021. The TRS plan terms are subject to change due to

notications to the law enacted by the Texas Legislature; to the

rules adopted by the TRS Board of Trustees; and to changes in

federal law related to qualied retirement plans.

1-800-223-8778

www.trs.texas.gov

1000 Red River Street

Austin, Texas 78701-2698