Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 10

Draft Ok to Print

AH XSL/XML

Fileid: … tions/p974/2023/a/xml/cycle04/source (Init. & Date) _______

Page 1 of 68 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Publication 974

Cat. No. 66452Q

Premium Tax

Credit (PTC)

For use in preparing

2023 Returns

Get forms and other information faster and easier at:

• IRS.gov (English)

• IRS.gov/Spanish (Español)

•

IRS.gov/Chinese (中文)

•

IRS.gov/Korean (한국어)

• IRS.gov/Russian (Pусский)

• IRS.gov/Vietnamese (Tiếng Việt)

Contents

Future Developments ....................... 1

What’s New ............................... 1

Reminders ............................... 2

Introduction .............................. 2

What Is the Premium Tax Credit (PTC)? ......... 3

Who Must File Form 8962 .................... 4

Who Can Take the PTC ...................... 4

Terms You May Need To Know ................ 4

Minimum Essential Coverage (MEC) ........... 8

Individuals Not Lawfully Present in the United

States Enrolled in a Qualified Health Plan ... 19

Determining the Premium for the Applicable

Second Lowest Cost Silver Plan (SLCSP) ... 27

Allocating Policy Amounts for Individuals With

No One in Their Tax Family ............... 27

Allocation of Policy Amounts Among Three or

More Taxpayers ....................... 28

Alternative Calculation for Year of Marriage ..... 38

Self-Employed Health Insurance Deduction

and PTC ............................. 47

How To Get Tax Help ....................... 63

Index .................................. 68

Future Developments

For the latest information about developments related to

Pub. 974, such as legislation enacted after it was

published, go to IRS.gov/Pub974.

What’s New

New Form 7206. Form 7206, Self-Employed Health In-

surance Deduction, and its separate instructions have re-

placed Worksheet 6-A, Self-Employed Health Insurance

Deduction Worksheet, that was previously published in

Pub. 535, Business Expenses. Use Form 7206 and its in-

structions to determine any amount of the self-employed

health insurance deduction you may be able to claim and

report on Schedule 1 (Form 1040), line 17.

New employer-coverage affordability rule for family

members of employees. For tax years beginning after

December 31, 2022, for purposes of determining eligibility

for the PTC, affordability of employer coverage for an em-

ployee's spouse or dependent eligible to enroll in the em-

ployer coverage is no longer based on the employee’s

share of the premium to cover only the employee.

Feb 15, 2024

Page 2 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Affordability of the employer coverage for these family

members is now based on the portion of the annual pre-

mium the employee must pay for coverage of the em-

ployee and these other family members.

Applicable federal poverty line percentages. For tax

years 2023 through 2025, taxpayers with household in-

come that exceeds 400% of the federal poverty line for

their family size may be allowed a PTC.

Reminders

Health Coverage Tax Credit (HCTC). The HCTC ex-

pired on December 31, 2021. Beginning in tax year 2022,

Form 8885 and its instructions have been discontinued by

the IRS.

Health reimbursement arrangements (HRAs). Begin-

ning in 2020, employers can offer individual coverage

health reimbursement arrangements (individual coverage

HRAs) to help employees and their families with their

medical expenses. If you are offered an individual cover-

age HRA, see Individual Coverage HRAs, later, for more

information on whether you can claim a PTC for you or a

member of your family for Marketplace coverage.

Qualified small employer health reimbursement ar-

rangement (QSEHRA). Under a QSEHRA, an eligible

employer can reimburse eligible employees for medical

expenses, including premiums for Marketplace health in-

surance. If you were provided a QSEHRA, your employer

should have reported the annual permitted benefit in

box 12 of your Form W-2 with code FF. If the QSEHRA is

considered affordable coverage for a month, no premium

tax credit (PTC) is allowed for the month. If the QSEHRA

is not considered affordable coverage for a month, you

may still be eligible for the PTC but you must reduce the

monthly PTC (but not below -0-) by the monthly permitted

benefit amount. For more information, see Qualified Small

Employer Health Reimbursement Arrangement, later.

Requirement to reconcile advance payments of the

premium tax credit. If you, your spouse with whom you

are filing a joint return, or a dependent was enrolled in

coverage through the Marketplace for 2023 and advance

payments of the premium tax credit (APTC) were made for

this coverage, you must file a 2023 return and attach Form

8962 to claim a net PTC. You (or whoever enrolled you)

should have received Form 1095-A, Health Insurance

Marketplace Statement, from the Marketplace with infor-

mation about your coverage and any APTC. You must at-

tach Form 8962 even if someone else enrolled you, your

spouse, or your dependent. If you are a dependent who is

claimed on someone else's 2023 return, you do not have

to attach Form 8962.

Report changes in circumstances when you re-enroll

in coverage and during the year. If APTC is being paid

for an individual in your tax family (defined later) and you

have had certain changes in circumstances (see the ex-

amples below), it is important that you report them to the

Marketplace where you enrolled in coverage. Reporting

changes in circumstances promptly will allow the

Marketplace to adjust your APTC to reflect the PTC you

are estimated to be able to take on your tax return. Adjust-

ing your APTC when you re-enroll in coverage and during

the year can help you avoid owing tax when you file your

tax return. Changes that you should report to the Market-

place include the following.

•

Changes in household income.

•

Moving to a different address.

•

Gaining or losing eligibility for other health care cover-

age.

•

Gaining, losing, or other changes to employment.

•

Birth or adoption.

•

Marriage or divorce.

•

Other changes affecting the composition of your tax

family.

For more information on how to report a change in

circumstances to the Marketplace, go to HealthCare.gov

or your state Marketplace website.

Health insurance options. If you need health coverage,

go to HealthCare.gov to learn about health insurance op-

tions that are available for you and your family, how to pur-

chase health insurance, and how you might qualify to get

financial assistance with the cost of insurance.

Additional information. For additional information about

the tax provisions of the Affordable Care Act (ACA), in-

cluding the individual shared responsibility provisions and

the PTC, see IRS.gov/Affordable-Care-Act/Individuals-

and-Families or call the IRS Healthcare Hotline for ACA

questions (800-919-0452).

Photographs of missing children. The Internal Reve-

nue Service is a proud partner with the National Center for

Missing & Exploited Children® (NCMEC). Photographs of

missing children selected by the Center may appear in

this publication on pages that would otherwise be blank.

You can help bring these children home by looking at the

photographs and calling 1-800-THE-LOST

(1-800-843-5678) if you recognize a child.

Introduction

This publication covers the following general topics, relat-

ing to the PTC, which are also covered in the Form 8962

instructions.

•

What is the PTC?

•

Who must file Form 8962.

•

Who can take the PTC. (See Figure A, later.)

This publication also provides additional instructions for

taxpayers in the following special situations.

•

Taxpayers who take the PTC and who are filing a sep-

arate return from their spouses because of domestic

abuse or spousal abandonment.

•

Taxpayers who take the PTC and who are also provi-

ded a QSEHRA.

2 Publication 974 (2023)

Page 3 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

Taxpayers who need to calculate the PTC and APTC

for a policy that covered an individual not lawfully

present in the United States.

•

Taxpayers who need to determine the applicable sec-

ond lowest cost silver plan (SLCSP) premium.

•

Taxpayers who need to allocate policy amounts for in-

dividuals not included in any tax family.

•

Taxpayers who need to allocate policy amounts be-

cause one qualified health plan covers individuals

from three or more tax families in the same month.

•

Taxpayers who married during the tax year and want

to use an alternative PTC calculation that may lower

their taxes.

•

Self-employed taxpayers who wish to take the PTC

and the self-employed health insurance deduction.

This publication also provides additional information to

help you determine if your health care coverage is mini-

mum essential coverage (MEC).

Comments and suggestions. We welcome your com-

ments about this publication and suggestions for future

editions.

You can send us comments through IRS.gov/

FormComments. Or, you can write to the Internal Revenue

Service, Tax Forms and Publications, 1111 Constitution

Ave. NW, IR-6526, Washington, DC 20224.

Although we can’t respond individually to each com-

ment received, we do appreciate your feedback and will

consider your comments and suggestions as we revise

our tax forms, instructions, and publications. Don’t send

tax questions, tax returns, or payments to the above ad-

dress.

Getting answers to your tax questions. If you have

a tax question not answered by this publication or the How

To Get Tax Help section at the end of this publication, go

to the IRS Interactive Tax Assistant page at IRS.gov/

Help/ITA where you can find topics by using the search

feature or viewing the categories listed.

Getting tax forms, instructions, and publications.

Go to IRS.gov/Forms to download current and prior-year

forms, instructions, and publications.

Ordering tax forms, instructions, and publications.

Go to IRS.gov/OrderForms to order current forms, instruc-

tions, and publications; call 800-829-3676 to order

prior-year forms and instructions. The IRS will process

your order for forms and publications as soon as possible.

Don’t resubmit requests you’ve already sent us. You can

get forms and publications faster online.

Questions about Form 1095-A, Health Insurance

Marketplace Statement. If you or a member of your tax

family was enrolled in a qualified health plan through a

Marketplace in 2023, you should have received a Form

1095-A by early February 2024. Contact your Marketplace

if you do not receive a Form 1095-A or if you have ques-

tions about the accuracy of your Form 1095-A.

Useful Items

You may want to see:

Form (and Instructions)

1095-A Health Insurance Marketplace Statement

1095-B Health Coverage

1095-C Employer-Provided Health Insurance Offer

and Coverage

7206 Self-Employed Insurance Deduction

8962 Premium Tax Credit (PTC)

See How To Get Tax Help, at the end of this publication,

for information about getting publications and forms.

What Is the Premium Tax Credit

(PTC)?

Premium tax credit (PTC). The PTC is a tax credit for

certain people who enroll, or whose family member en-

rolls, in a qualified health plan offered through a Market-

place. The credit provides financial assistance to pay the

premiums for the qualified health plan by reducing the

amount of tax you owe, giving you a refund, or increasing

your refund amount. You must file Form 8962 to compute

and take the PTC on your tax return.

Advance payments of the premium tax credit (APTC).

The APTC is a payment made during the year to your in-

surance provider that pays for part or all of the premiums

for a qualified health plan covering you or an individual in

your tax family. Your APTC eligibility is based on the Mar-

ketplace’s estimate of the PTC you will be able to take on

your tax return. If APTC was paid for you or an individual in

your tax family, you must file Form 8962 to reconcile (com-

pare) this APTC with your PTC. If the APTC is more than

your PTC, you have excess APTC and you must repay the

excess, subject to certain limitations. If the APTC is less

than the PTC, you can get a credit for the difference, which

reduces your tax payment or increases your refund.

Changes in circumstances. The Marketplace deter-

mined your eligibility for, and the amount of, your 2023

APTC using projections of your income and the number of

individuals you certified to the Marketplace would be in

your tax family (yourself, spouse, and dependents) when

you enrolled in a qualified health plan. If this information

changed during 2023 and you did not promptly report it to

the Marketplace, the amount of APTC paid may be sub-

stantially different from the amount of PTC you can take on

your tax return. See Report changes in circumstances

when you re-enroll in coverage and during the year, ear-

lier, for changes that can affect the amount of your PTC.

1095-A

1095-B

1095-C

7206

8962

Publication 974 (2023) 3

Page 4 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Who Must File Form 8962

You must file Form 8962 with your income tax return (Form

1040, 1040-SR, or 1040-NR) if any of the following apply

to you.

•

You are taking the PTC.

•

APTC was paid for you or another individual in your

tax family.

•

APTC was paid for an individual you told the Market-

place would be in your tax family and neither you nor

anyone else included that individual in a tax family.

See Individual you enrolled who is not included in a

tax family under Lines 12 Through 23—Monthly Cal-

culation in the Form 8962 instructions.

If any of the circumstances above apply to you, you

must file an income tax return and attach Form 8962 even

if you are not otherwise required to file. You must use

Form 1040, 1040-SR, or 1040-NR. For help in determining

which of these forms to file, see the Instructions for Form

1040 or the Instructions for Form 1040-NR.

If you are filing Form 8962, you cannot file Form

1040-SS or 1040-PR.

If someone else enrolled an individual in your tax family

in coverage, and APTC was paid for that individual’s cov-

erage, you must file Form 8962 to reconcile the APTC. You

need to obtain a copy of the Form 1095-A from the person

who enrolled the individual.

If you are claimed as a dependent, the person

who claims you will file Form 8962 to take the PTC

and, if necessary, repay excess APTC for your

coverage. You do not need to file Form 8962.

Who Can Take the PTC

You can take the PTC for 2023 if you meet the conditions

under (1), (2), and (3) below.

1. For at least 1 month of the year, all of the following

were true.

a. An individual in your tax family was enrolled in a

qualified health plan offered through the Market-

place on the first day of the month.

b. That individual was not eligible for MEC for the

month, other than individual market coverage. An

individual is generally considered eligible for MEC

for the month only if they were eligible for every

day of the month (see Minimum Essential Cover-

age, later).

c. The portion of the enrollment premiums (descri-

bed later) for the month for which you are respon-

sible was paid by the due date of your tax return

(not including extensions). However, if you

CAUTION

!

TIP

became eligible for APTC because of a successful

eligibility appeal and you retroactively enrolled in

the plan, then the portion of the enrollment pre-

mium for which you are responsible must be paid

on or before the 120th day following the date of

the appeals decision.

2. No one can claim you as a dependent for the year.

3. You are an applicable taxpayer for 2023. To be an ap-

plicable taxpayer, you must meet all of the following

requirements.

a. Your household income for 2023 is at least 100%

of the federal poverty line for your family size (see

Line 4 in the Form 8962 instructions). However,

having household income below 100% of the fed-

eral poverty line will not disqualify you from taking

the PTC if you meet certain requirements descri-

bed under Household income below 100% of the

federal poverty line under Line 5 in the Form 8962

instructions.

b. If you were married at the end of 2023, you must

generally file a joint return. However, filing a sepa-

rate return from your spouse will not disqualify you

from being an applicable taxpayer if you meet cer-

tain requirements described under Married tax-

payers, later.

You are not entitled to the PTC for health coverage for

an individual for any period during which the individual is

not lawfully present in the United States.

For additional requirements and more details, see Ap-

plicable taxpayer, later.

Terms You May Need To Know

The terms defined below are generally the same as those

in the Form 8962 instructions. However, additional infor-

mation is provided below on what documentation to keep

if you are a victim of domestic abuse or spousal abandon-

ment, and on MEC, later.

Tax family. For purposes of the PTC, your tax family con-

sists of the following individuals.

•

You, if you file a tax return for the year and you can't be

claimed as a dependent on someone else's 2023 tax

return.

•

Your spouse if filing jointly and they can't be claimed

as a dependent on someone else's 2023 tax return.

•

Your dependents whom you claim on your 2023 tax re-

turn. If you are filing Form 1040-NR, you should in-

clude your dependents in your tax family only if you

are a U.S. national; a resident of Canada, Mexico, or

South Korea; or a resident of India who was a student

or business apprentice.

Your family size equals the number of qualifying individ-

uals in your tax family (including yourself).

4 Publication 974 (2023)

Page 5 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

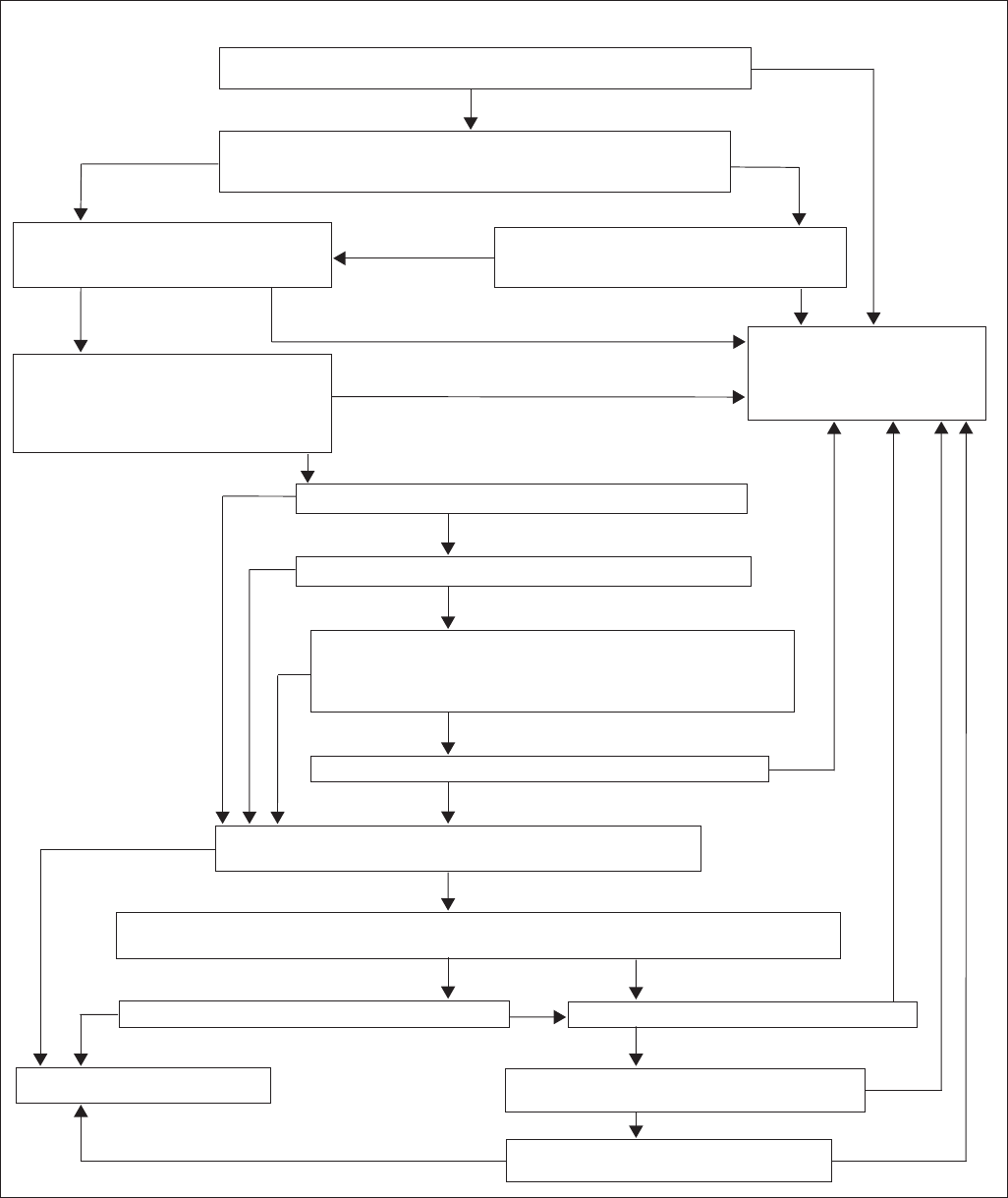

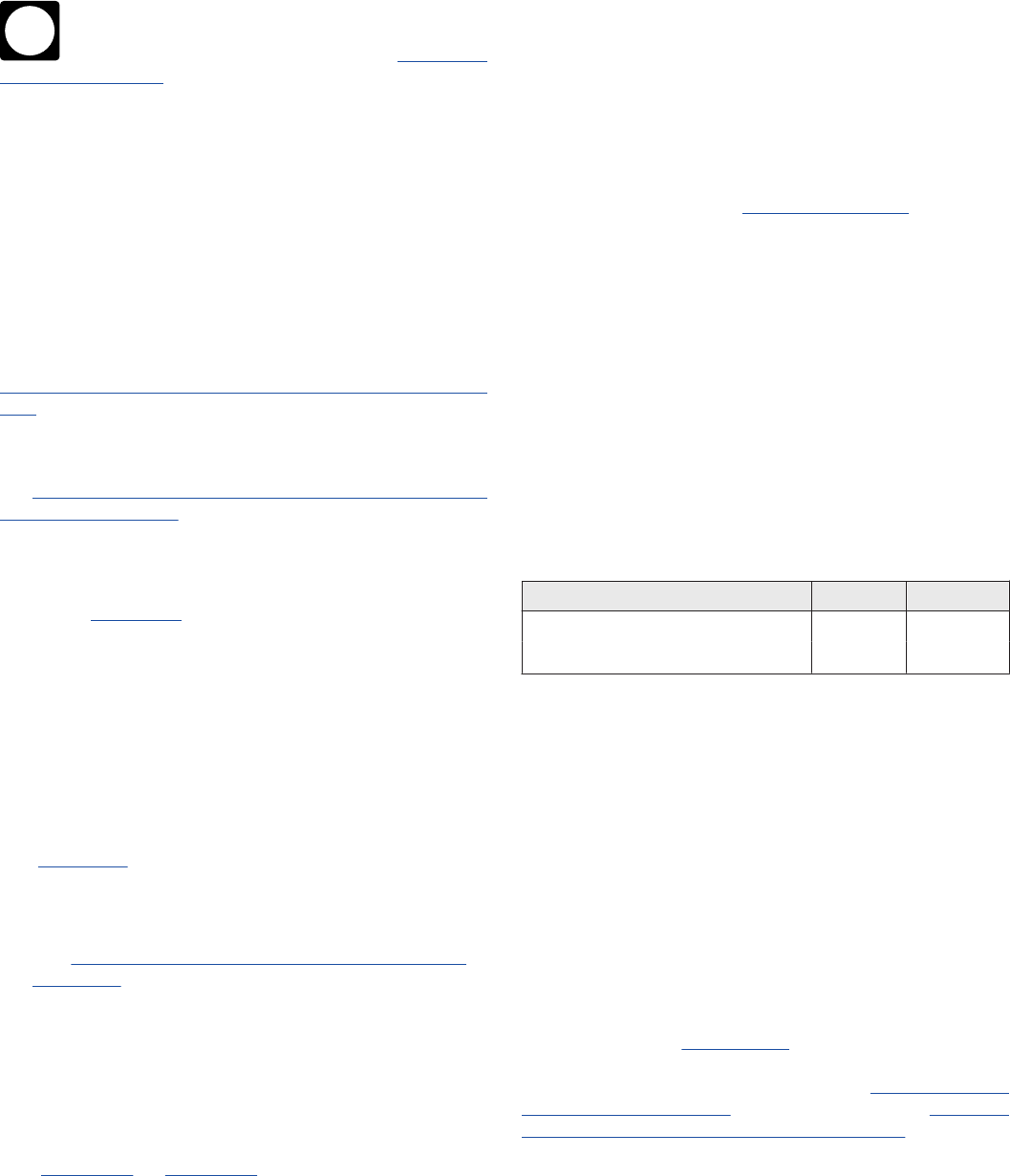

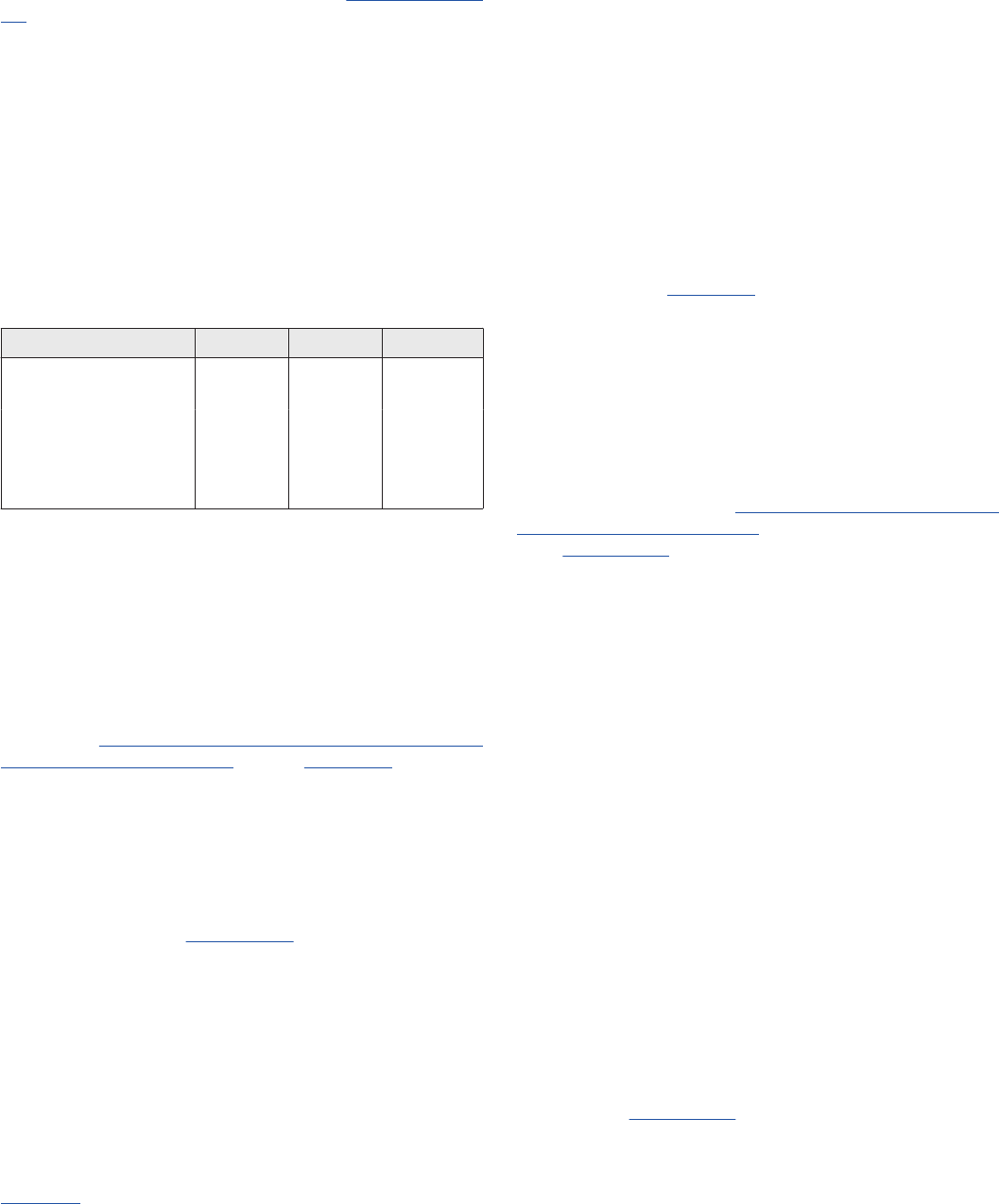

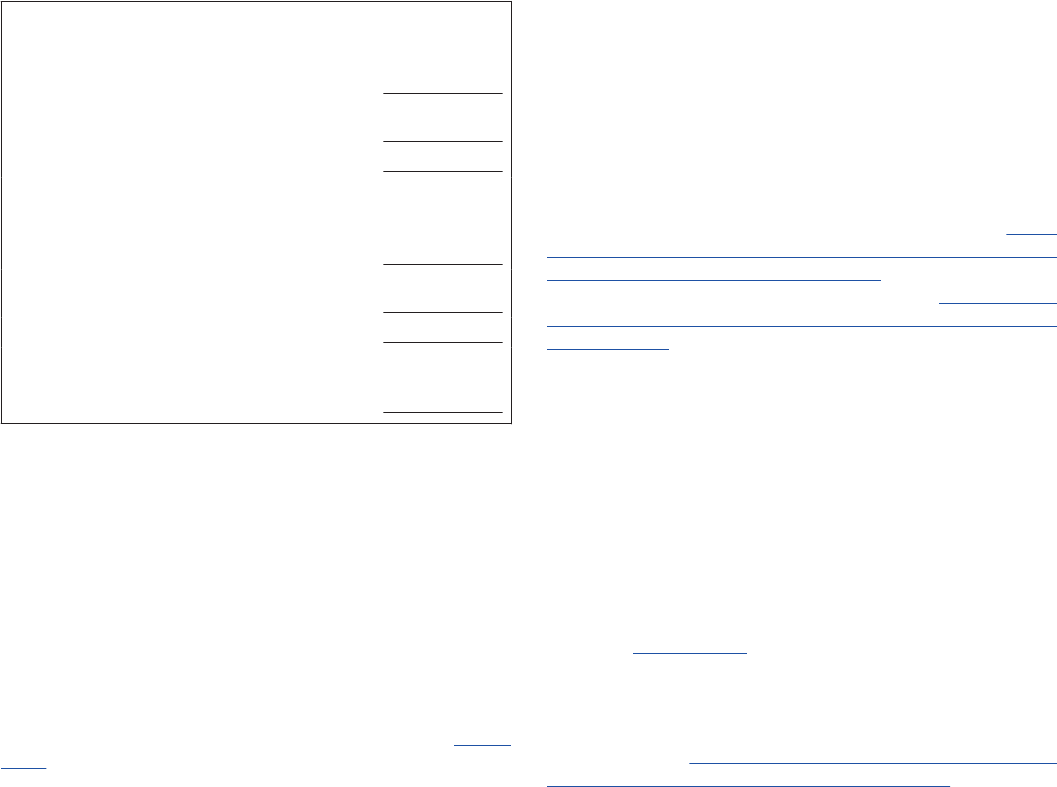

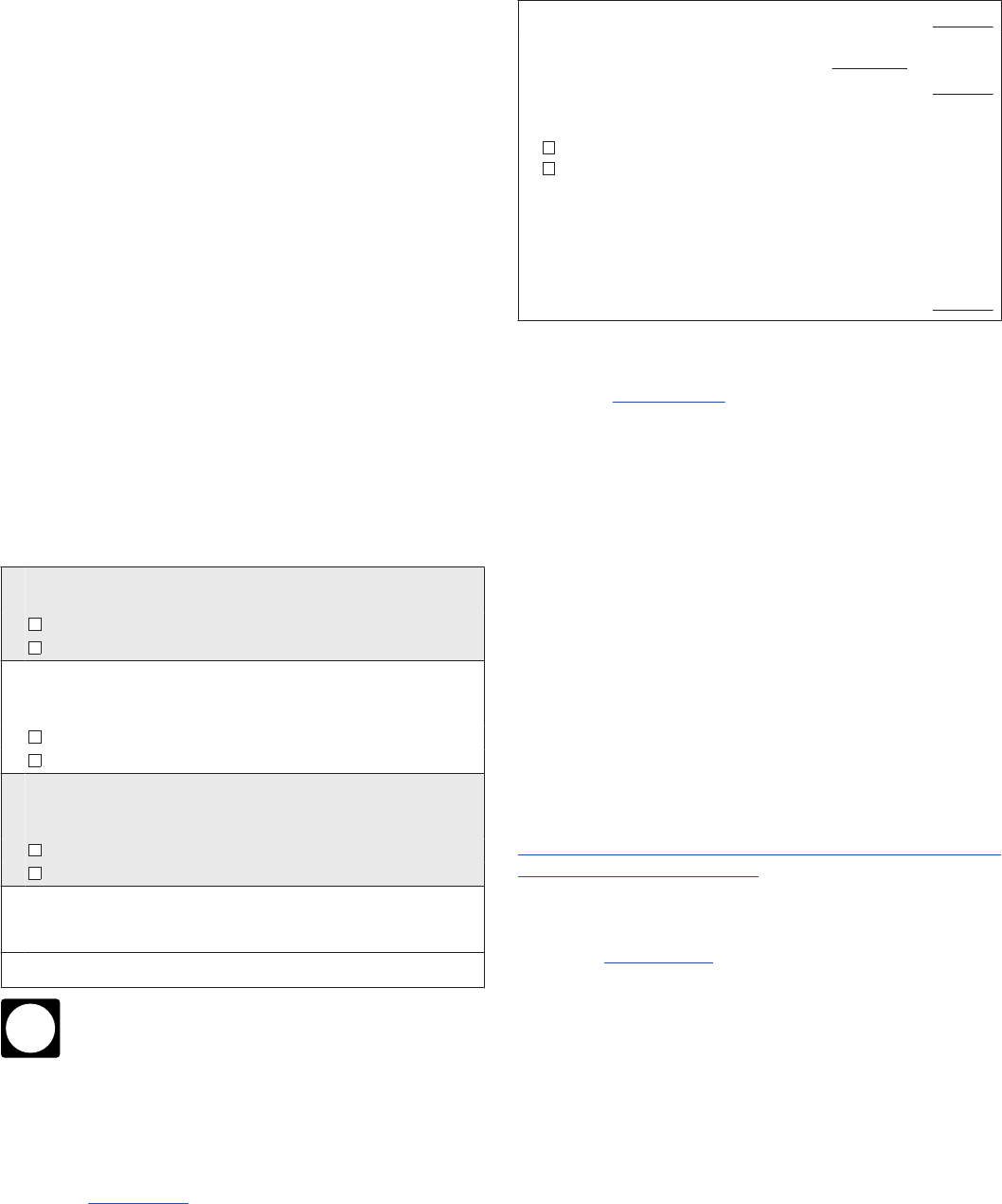

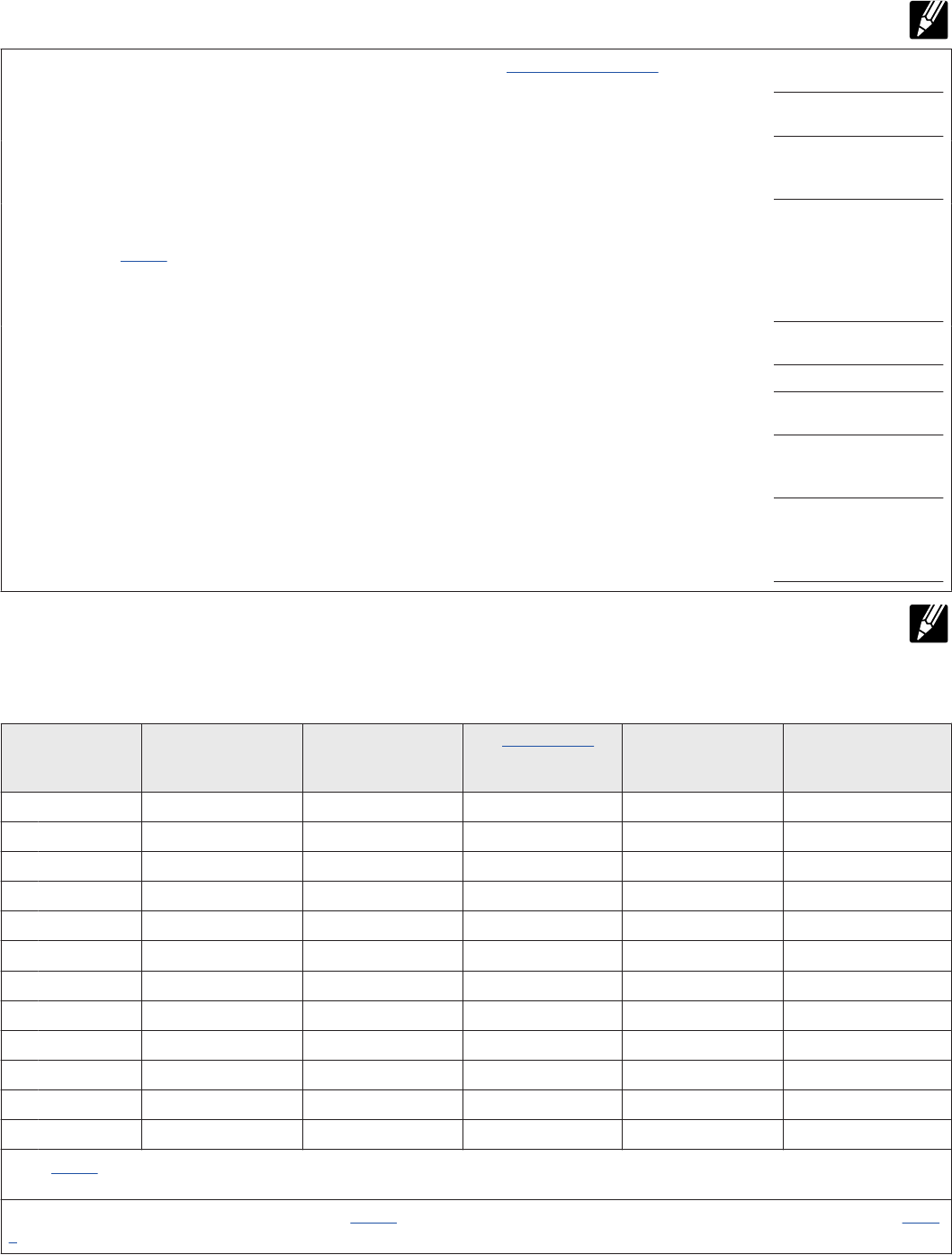

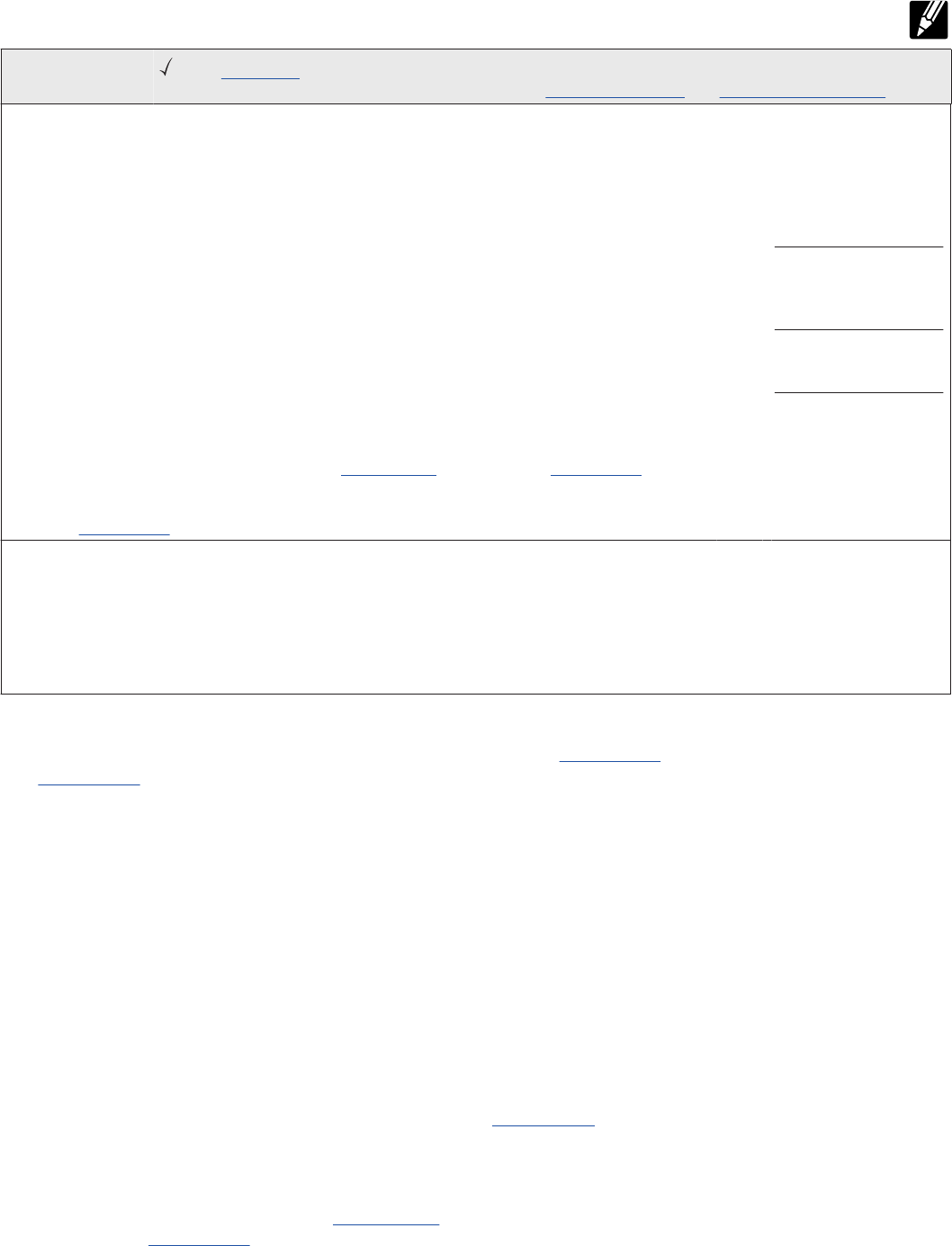

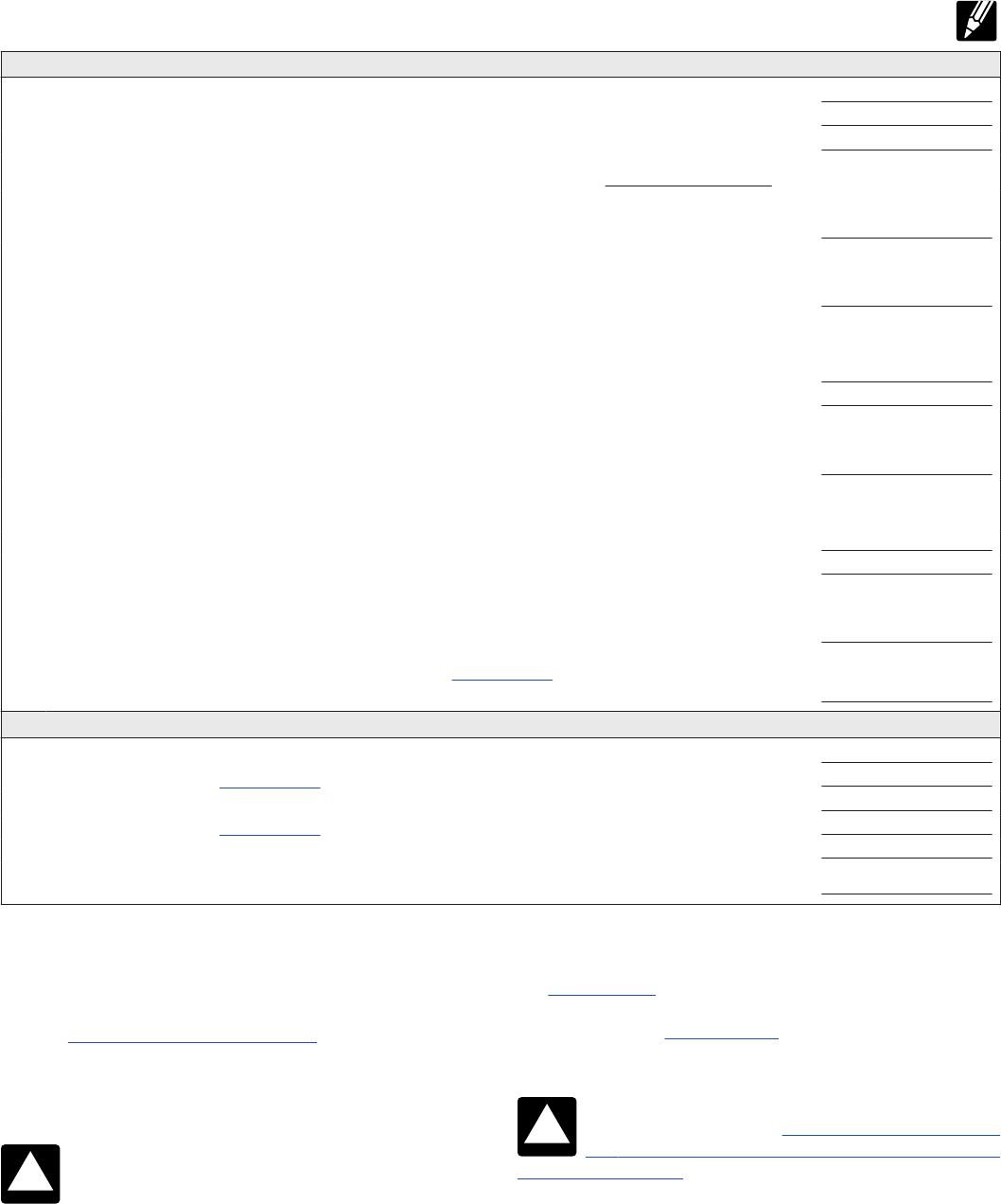

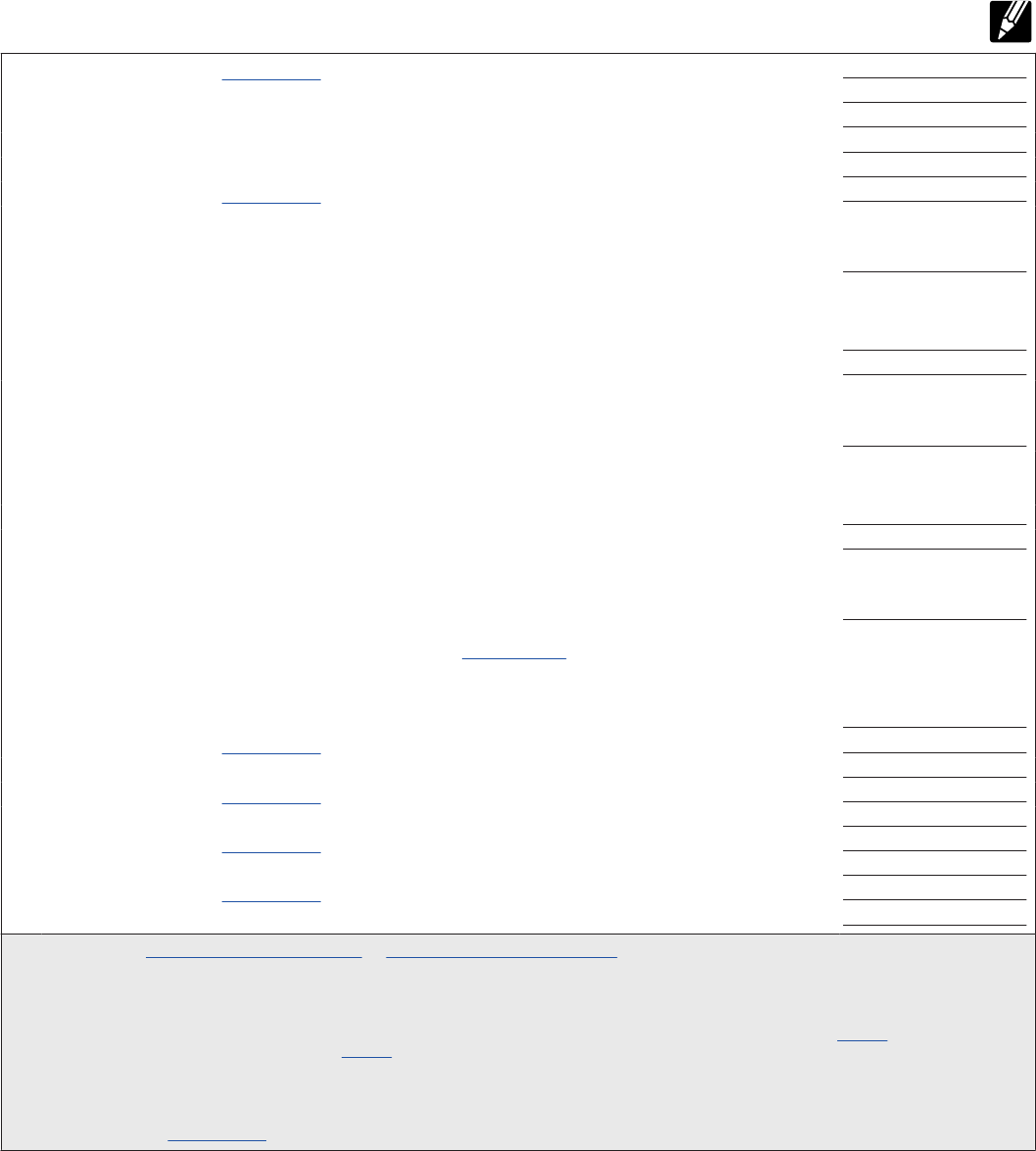

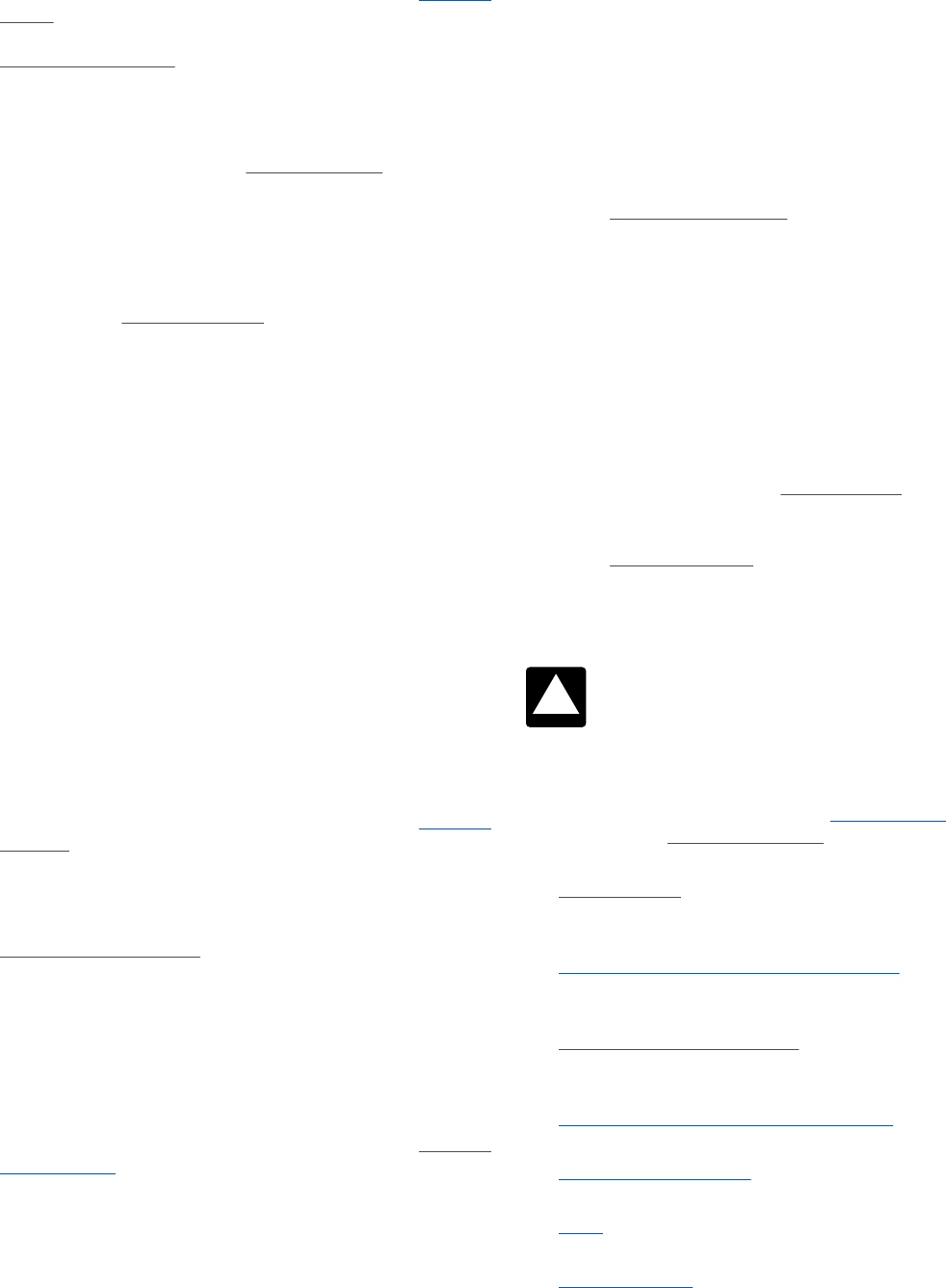

Figure A. Can You Take the PTC?

This flowchart can help you determine whether you can take the PTC. But do not rely on this flowchart alone. Be sure you

read Who Can Take the PTC, earlier, or in the Form 8962 instructions.

Were any of the individuals included in your tax family enrolled in a qualied

health plan through the Marketplace for at least 1 month during 2023?

Were any of these individuals eligible for MEC (other than individual

market coverage) for the months they were enrolled in the qualied health

plan? (See Minimum Essential Coverage, later.)

Can someone else claim you asadependent

on another tax return for 2023?

Were you married at the end of 2023?

Are you and your spouse ling a joint return?

Are youavictim of domestic abuse or spousal abandonment?

Do you meet the requirements for Married persons who live apart

under Head of Household in the Instructions for Form 1040, or

Married Filing Separately under Filing Status in the Form 1040-NR

instructions?

Was your household income at least 100% of the federal poverty

line for your family size? (See the Form 8962 instructions.)

You cannot take the PTC.

Yes

No

Start here

Yes

No

No

No

No

No

No

No

No

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Was APTC paid for 1 or more months during 2023?

Yes

You may be able to take the PTC.

Was at least one individual enrolled inaqualied

health plan lawfully present in the United States?

Yes

Was at least one enrolled individual ineligible

for Medicaid due to immigration status?

Yes

Yes

At the time of enrollment, did the Marketplace estimate that your household income would be at least

100% of the federal poverty line for your family size for 2023?

Were all of these individuals eligible for MEC for

all of the months they were enrolled in the

qualied health plan?

No

Yes

No

No

Was everyone in your tax family a U.S. citizen?

No

No

No

Were the premiums paid by the due date of

your tax return (not including extensions)?

(A different due date applies in the case of a

successful eligibility appeal. See Enrollment

premiums.)

Publication 974 (2023) 5

Page 6 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Note. Listing your dependents by name and social se-

curity number (SSN) or individual taxpayer identification

number (ITIN) on your tax return is the same as claiming

them as a dependent. If you have more than four depend-

ents, see the Instructions for Form 1040 or the Instructions

for Form 1040-NR.

Household income. For purposes of the PTC, house-

hold income is the modified adjusted gross income (modi-

fied AGI) of you and your spouse (if filing a joint return)

(see Line 2a in the Form 8962 instructions) plus the modi-

fied AGI of each individual whom you claim as a depend-

ent and who is required to file an income tax return be-

cause their income meets the income tax return filing

threshold (see Line 2b in the Form 8962 instructions).

Household income does not include the modified AGI of

those individuals whom you claim as dependents and who

are filing a 2023 return only to claim a refund of withheld

income tax or estimated tax.

Modified AGI. For purposes of the PTC, modified AGI

is the AGI on your tax return plus certain income that is not

subject to tax (foreign earned income, tax-exempt interest,

and the portion of social security benefits that is not taxa-

ble). Use Worksheet 1-1 and Worksheet 1-2 in the Form

8962 instructions to determine your modified AGI.

Taxpayer's tax return including income of a de-

pendent child. A taxpayer who includes the gross in-

come of a dependent child on the taxpayer’s tax return

must include on Worksheet 1-2 the child’s tax-exempt in-

terest and the portion of the child’s social security benefits

that is not taxable.

Coverage family. Your coverage family includes all indi-

viduals in your tax family who are enrolled in a qualified

health plan and are not eligible for MEC (other than indi-

vidual market coverage). The individuals included in your

coverage family may change from month to month. If an

individual in your tax family is not enrolled in a qualified

health plan, or is enrolled in a qualified health plan but is

eligible for MEC (other than individual market coverage),

they are not part of your coverage family. Your PTC is

available to help you pay only for the coverage of the indi-

viduals included in your coverage family.

Monthly credit amount. The monthly credit amount is

the amount of your tax credit for a month. Your PTC for the

year is the sum of all of your monthly credit amounts. Your

credit amount for each month is the lesser of:

•

The enrollment premiums (described next) for the

month for one or more qualified health plans in which

you or any individual in your tax family enrolled, or

•

The amount of the monthly applicable SLCSP pre-

mium (described later) less your monthly contribution

amount (described later).

To qualify for a monthly credit amount, at least one indi-

vidual in your tax family must be enrolled in a qualified

health plan on the first day of that month. Generally, if cov-

erage in a qualified health plan began after the first day of

the month, you are not allowed a monthly credit amount

for the coverage for that month. However, if an individual

in your tax family enrolled in a qualified health plan in 2023

and the enrollment was effective on the date of the individ-

ual's birth, adoption, or placement for adoption or in foster

care, or on the effective date of a court order placing the

individual with your family, the individual is treated as en-

rolled as of the first day of that month. Therefore, the indi-

vidual may be a member of your tax family and coverage

family for the entire month for purposes of computing your

monthly credit amount.

Enrollment premiums. The enrollment premiums are

the total amount of the premiums for the month, reduced

by any premium amounts for that month that were refun-

ded in the same tax year as the premium liability was in-

curred, for one or more qualified health plans in which any

individual in your tax family enrolled. Form 1095-A, Part III,

column A, reports the enrollment premiums.

You are generally not allowed a monthly credit amount

for the month if any part of the enrollment premiums for

which you are responsible that month has not been paid

by the due date of your tax return (not including exten-

sions). However, if you became eligible for APTC because

of a successful eligibility appeal and you retroactively en-

rolled in the plan, the portion of the enrollment premium

for which you are responsible must be paid on or before

the 120th day following the date of the appeals decision.

Premiums another person pays on your behalf are treated

as paid by you.

If your share of the enrollment premiums is not paid, the

issuer may terminate coverage. The termination is gener-

ally effective no sooner than the second month of nonpay-

ment. For any months you were covered but did not pay

your share of the premiums, you are not allowed a monthly

credit amount.

Applicable SLCSP premium. The applicable SLCSP

premium is the second lowest cost silver plan premium of-

fered through the Marketplace where you reside that ap-

plies to your coverage family (described earlier). The

SLCSP premium is not the same as your enrollment pre-

mium unless you enroll in the applicable SLCSP. Form

1095-A, Part III, column B, generally reports the applicable

SLCSP premium. If no APTC was paid for your coverage,

Form 1095-A, Part III, column B, may be wrong or blank or

may report your applicable SLCSP premium as -0-. Also, if

you had a change in circumstances during 2023 that you

did not report to the Marketplace, the SLCSP premium re-

ported on Form 1095-A in Part III, column B, may be

wrong. In either case, you must determine your correct ap-

plicable SLCSP premium. You do not have to request a

corrected Form 1095-A from the Marketplace. See Miss-

ing or incorrect SLCSP premium on Form 1095-A under

Line 10 in the Form 8962 instructions.

Monthly contribution amount. Your monthly contri-

bution amount is used to calculate your monthly credit

amount. It is the amount of your household income you

would be responsible for paying as your share of premi-

ums each month if you enrolled in the applicable SLCSP. It

is not based on the amount of premiums you paid out of

pocket during the year. You will compute your monthly

contribution amount in Part I of Form 8962.

6 Publication 974 (2023)

Page 7 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Qualified health plan. For purposes of the PTC, a quali-

fied health plan is a health insurance plan or policy pur-

chased through a Marketplace at the bronze, silver, gold,

or platinum level. Throughout this publication, a qualified

health plan is also referred to as a “policy.” Catastrophic

health plans and stand-alone dental plans purchased

through the Marketplace, and all plans purchased through

the Small Business Health Options Program (SHOP), are

not qualified health plans for purposes of the PTC. There-

fore, they do not qualify a taxpayer to take the PTC.

Applicable taxpayer. You must be an applicable tax-

payer to take the PTC. Generally, you are an applicable

taxpayer if your household income for 2023 (described

earlier) is at least 100% of the federal poverty line for your

family size (provided in Tables 1-1, 1-2, and 1-3 in the

Form 8962 instructions) and no one can claim you as a

dependent for 2023. In addition, if you were married at the

end of 2023, you must file a joint return to be an applicable

taxpayer unless you meet one of the exceptions described

under Married taxpayers, later.

For individuals with household income below 100% of

the federal poverty line, see Household income below

100% of the federal poverty line under Line 5 in the Form

8962 instructions. However, the exception described un-

der Estimated household income at least 100% of the fed-

eral poverty line in the Form 8962 instructions does not

apply if, with intentional or reckless disregard for the facts,

you provide incorrect information to the Marketplace for

the year of coverage. You provide information with inten-

tional disregard for the facts if you know that the informa-

tion provided is inaccurate. You provide information with a

reckless disregard for the facts if you make little or no ef-

fort to determine whether the information provided is accu-

rate and your lack of effort to provide accurate information

is substantially different from what a reasonable person

would do under the circumstances.

Individuals who are incarcerated. Individuals who are

incarcerated (other than pending disposition of charges,

for example, awaiting trial) are not eligible for coverage in

a qualified health plan through a Marketplace. However,

these individuals may be applicable taxpayers and take

the PTC for the coverage of individuals in their tax families

who are eligible for coverage in a qualified health plan.

Individuals who are not lawfully present. Individuals

who are not lawfully present in the United States are not

eligible for coverage in a qualified health plan through a

Marketplace. They cannot take the PTC for their own cov-

erage and are not eligible for the repayment limitations in

Table 5 (in the Form 8962 instructions) for APTC paid for

their own coverage. However, these individuals may be

applicable taxpayers and take the PTC for the coverage of

individuals in their tax families, such as their children, who

are lawfully present and eligible for coverage in a qualified

health plan. For more information about who is treated as

lawfully present for this purpose, go to HealthCare.gov.

See Individuals Not Lawfully Present in the United States

Enrolled in a Qualified Health Plan, later, for more informa-

tion on reconciling APTC when an unlawfully present per-

son is enrolled individually or with lawfully present family

members.

Married taxpayers. If you are considered married for

federal income tax purposes, you must file a joint return

with your spouse to take the PTC unless one of the two

exceptions below applies to you.

You are not considered married for federal income tax

purposes if you are divorced or legally separated accord-

ing to your state law under a decree of divorce or separate

maintenance. In that case, you cannot file a joint return but

may be able to take the PTC on your separate return. See

Pub. 501, Dependents, Standard Deduction, and Filing In-

formation.

If you are considered married for federal income tax

purposes, you may be eligible to take the PTC without fil-

ing a joint return if one of the two exceptions below applies

to you. If Exception 1 applies, you can file a return using

head of household or single filing status and take the PTC.

If Exception 2 applies, you are treated as married but can

take the PTC with the filing status of married filing sepa-

rately.

Exception 1—Certain married persons living apart.

You may file your return as if you are unmarried and take

the PTC if one of the following applies to you.

•

You file a separate return from your spouse on Form

1040 or 1040-SR because you meet the requirements

for Married persons who live apart under Head of

Household in the Instructions for Form 1040.

•

You file as single on your Form 1040-NR because you

meet the requirements for Married persons who live

apart under Married Filing Separately in the Instruc-

tions for Form 1040-NR.

Exception 2—Victim of domestic abuse or spousal

abandonment. If you are a victim of domestic abuse or

spousal abandonment, you can file a return as married fil-

ing separately and take the PTC for 2023 if all of the fol-

lowing apply to you.

•

You are living apart from your spouse at the time you

file your 2023 tax return.

•

You are unable to file a joint return because you are a

victim of domestic abuse (described next) or spousal

abandonment (described below).

•

You check the box on your Form 8962 to certify that

you are a victim of domestic abuse or spousal aban-

donment.

•

You have not used this exception to take the PTC in

each of 2020, 2021, and 2022.

Domestic abuse. Domestic abuse includes physical,

psychological, sexual, or emotional abuse, including ef-

forts to control, isolate, humiliate, and intimidate, or to un-

dermine the victim's ability to reason independently. All

the facts and circumstances are considered in determin-

ing whether an individual is abused, including the effects

of alcohol or drug abuse by the victim’s spouse. Depend-

ing on the facts and circumstances, abuse of an individu-

al’s child or other family member living in the household

Publication 974 (2023) 7

Page 8 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

may constitute abuse of the individual. If you have con-

cerns about your safety, please consider contacting the

confidential 24-hour National Domestic Violence Hotline

at 1-800-799-SAFE (7233), or 1-800-787-3224 (TTY), or

1-855-812-1001 (video phone, only for deaf callers). For

additional information and resources, see Pub. 3865, Tax

Information for Survivors of Domestic Abuse, available at

IRS.gov/Pub3865; and Part V of Form 8857, Request for

Innocent Spouse Relief, available at IRS.gov/Form8857.

Spousal abandonment. A taxpayer is a victim of

spousal abandonment for a tax year if, taking into account

all facts and circumstances, the taxpayer is unable to lo-

cate their spouse after reasonable diligence.

Records of domestic abuse and spousal abandon-

ment. If you checked the box in the upper right corner of

Form 8962 indicating that you are eligible for the PTC de-

spite having a filing status of married filing separately, you

should keep records relating to your situation, like with all

aspects of your tax return. What you have available may

depend on your circumstances. However, the following list

provides some examples of records that may be useful.

(Do not attach these records to your tax return.)

•

Protective and/or restraining order.

•

Police report.

•

Doctor’s report or letter.

•

A statement from someone who was aware of, or who

witnessed, the abuse or the results of the abuse. The

statement should be notarized if possible.

•

A statement from someone who knows of the aban-

donment. The statement should be notarized if possi-

ble.

Married filing separately. If you file as married filing

separately and are not a victim of domestic abuse or

spousal abandonment (see Exception 2—Victim of do-

mestic abuse or spousal abandonment under Married tax-

payers, earlier), then you are not an applicable taxpayer

and you cannot take the PTC. You must generally repay all

of the APTC paid for a qualified health plan that covered

only individuals in your tax family. If the policy also cov-

ered at least one individual in your spouse’s tax family, you

must generally repay half of the APTC paid for the policy.

See Line 9 in the Form 8962 instructions. However, the

amount of APTC you have to repay may be limited. See

Line 28 in the Form 8962 instructions.

Minimum Essential Coverage

(MEC)

Under the health care law, certain health coverage is

called MEC. You generally cannot take the PTC for an indi-

vidual in your tax family for any month that the individual is

eligible for MEC, except for individual market coverage

(defined below). MEC includes the following.

•

Individual market coverage (including qualified health

plans).

•

Most coverage through government-sponsored pro-

grams (including Medicaid coverage, Medicare Part A

or C, the Children's Health Insurance Program (CHIP),

certain benefits for veterans and their families, TRI-

CARE, and health coverage for Peace Corps volun-

teers).

•

Most types of employer-sponsored coverage.

•

Grandfathered health plans.

•

Other health coverage designated by the Department

of Health and Human Services (HHS) as MEC.

MEC does not include coverage consisting solely

of excepted benefits. Excepted benefits include

vision and dental coverage not part of a compre-

hensive health insurance plan, workers’ compensation

coverage, and coverage limited to a specified disease or

illness.

For more information on what is MEC, see IRS.gov/

Affordable-Care-Act/Individuals-and-Families/Individual-

Shared-Responsibility-Provision.

Note. Your MEC may be reported to you on Form

1095-A, 1095-B, or 1095-C.

MEC eligibility when Marketplace does not discon-

tinue APTC. If an individual in your tax family is enrolled

in a qualified health plan for which APTC was made and

the individual is or will soon become eligible for other

MEC, you must notify the Marketplace about the other

MEC and that the APTC for the individual’s coverage

should be discontinued. If the Marketplace does not dis-

continue APTC for the first calendar month beginning after

the month you notify the Marketplace, the individual is

treated as eligible for the other MEC no earlier than the

first day of the second calendar month beginning after the

first month the individual may enroll in the other MEC. A

different rule applies to Medicaid and CHIP eligibility, dis-

cussed later under Government-Sponsored Programs.

Expatriate Health Plans

In general, an expatriate health plan is certain health in-

surance coverage that is offered to foreign nationals who

are temporarily assigned for work in the United States,

U.S. residents who are temporarily working outside of the

United States, and certain nonemployees (such as stu-

dents and missionaries) who are traveling internationally.

To qualify, the health insurance coverage must generally

offer a minimum level of benefits in the region in which the

covered individual is temporarily located and be offered by

a qualifying expatriate health insurance issuer. An expatri-

ate health plan is considered employer-sponsored cover-

age for a primary insured who receives it through their em-

ployer (and for that employee’s covered dependents). It is

considered individual market coverage for any other pri-

mary insured.

TIP

8 Publication 974 (2023)

Page 9 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Individual Market Coverage

A health plan offered in the individual market is health in-

surance coverage provided to an individual by a health in-

surance issuer licensed by a state, including a qualified

health plan offered through the Marketplace. Even though

these plans are MEC, eligibility for individual market cover-

age does not prevent an individual from qualifying for the

PTC for coverage in a qualified health plan purchased

through the Marketplace.

Individual market coverage also includes coverage un-

der certain expatriate health plans offered to students and

religious missionaries traveling internationally. See Expa-

triate Health Plans, earlier.

Government-Sponsored Programs

The following government-sponsored programs are MEC.

1. Medicare Part A coverage.

2. Medicare Advantage plans.

3. Medicaid, except for the following programs.

a. Optional coverage of family planning services.

b. Optional coverage of tuberculosis-related serv-

ices.

c. Coverage of pregnancy-related services in states

that do not provide full Medicaid benefits on the

basis of pregnancy.

d. Coverage limited to the treatment of emergency

medical conditions.

e. Coverage of medically needy individuals (except

for coverage for medically needy individuals that

HHS has designated as MEC—see Other Cover-

age Designated by the Department of Health and

Human Services, later).

f. Coverage under a section 1115 demonstration

waiver program (except for coverage under a sec-

tion 1115 demonstration program that HHS has

designated as MEC—see Other Coverage Desig-

nated by the Department of Health and Human

Services, later).

Call your state Medicaid office if you have any

questions about the coverage you have.

4. CHIP, except certain CHIP coverage for pregnancy

services. (Certain coverage often called a CHIP

buy-in program is not considered a government-spon-

sored program and is discussed later under Other

Coverage Designated by the Department of Health

and Human Services.)

5. Coverage under the TRICARE program, except for the

following programs.

a. Coverage on a space-available basis in a military

treatment facility for individuals who are not eligi-

ble for TRICARE coverage for private sector care.

b. Coverage for a line-of-duty-related injury, illness,

or disease for individuals who have left active duty.

6. The following coverage administered by the Depart-

ment of Veterans Affairs.

a. Coverage consisting of the medical benefits pack-

age for eligible veterans.

b. Civilian Health and Medical Program of the De-

partment of Veterans Affairs (CHAMPVA).

c. Comprehensive health care for children suffering

from spina bifida who are the children of Vietnam

veterans and veterans of covered service in Ko-

rea.

7. Health coverage provided to Peace Corps volunteers.

8. Refugee Medical Assistance.

9. Coverage through a Basic Health Program (BHP)

standard health plan.

In general, you cannot get the PTC for your coverage in

a qualified health plan if you are eligible for govern-

ment-sponsored MEC. You are generally considered eligi-

ble for a government-sponsored program if you meet the

criteria for coverage under the program. But see Excep-

tions, later. However, you will not lose the PTC for your

coverage until the first day of the first full month you can

receive benefits under the government-sponsored pro-

gram. If you can be covered under a government-spon-

sored program, you must complete the requirements nec-

essary to receive benefits (for example, submitting an

application or providing required information) by the last

day of the third full calendar month following the event that

establishes eligibility (for example, becoming eligible for

Medicare when you turn 65). If you do not complete the

necessary requirements in this time, you will lose the PTC

for your coverage in a qualified health plan beginning with

the first day of the fourth calendar month following the

event that makes you eligible for the government cover-

age.

Example 1. Ellen was enrolled in a qualified health

plan with APTC. She turned 65 on June 3 and became eli-

gible for Medicare. Ellen must apply to Medicare to re-

ceive benefits. She applied to Medicare in September and

was eligible to receive Medicare benefits beginning on

December 1. Ellen completed the requirements necessary

to receive Medicare benefits by September 30 (the last

day of the third full calendar month after the event that es-

tablished her eligibility, turning 65). She was eligible for

Medicare coverage on December 1, the first day of the

first full month that she could receive benefits. Thus, Ellen

can get the PTC for her coverage in the qualified health

plan for January through November. Beginning in Decem-

ber, Ellen cannot get the PTC for her coverage in the quali-

fied health plan because she is eligible for Medicare.

Example 2. The facts are the same as in Example 1,

except that Ellen did not apply for the Medicare coverage

by September 30. Ellen is considered eligible for govern-

ment-sponsored coverage beginning on October 1. She

can get the PTC for her coverage for January through

Publication 974 (2023) 9

Page 10 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

September. She cannot get the PTC for her coverage in a

qualified health plan as of October 1, the first day of the

fourth month after she turned 65.

Exceptions. While you are generally considered eligible

for government-sponsored MEC (and are ineligible for the

PTC) if you are able to enroll in that coverage, you are

considered eligible for government-sponsored coverage

under the following programs only if you are enrolled in

the program.

1. A veteran’s health care program listed in (6), earlier.

2. The following TRICARE programs.

a. The Continued Health Care Benefit Program.

b. Retired Reserve.

c. Young Adult.

d. Reserve Select.

3. Medicaid coverage for comprehensive pregnancy-re-

lated services and CHIP coverage based on preg-

nancy, if the individual is enrolled in a qualified health

plan at the time the individual becomes eligible for

Medicaid or CHIP.

4. Coverage under Medicare Part A for which the individ-

ual must pay a premium.

In addition, an individual is considered eligible for MEC

under a Medicaid or Medicare program for which eligibility

requires a determination of disability, blindness, or illness

only when the responsible agency makes a favorable eligi-

bility determination.

Retroactive coverage. If APTC is being paid for cover-

age in a qualified health plan and you become eligible for

government-sponsored coverage that is effective retroac-

tively (such as Medicaid or CHIP), you will not retroac-

tively lose the PTC for your coverage. You can get the PTC

for your coverage until the first day of the first calendar

month after you are approved for the government cover-

age.

Example. In November, Freda enrolled in a qualified

health plan for the following year and got APTC for her

coverage. Freda lost her part-time job and on April 10 ap-

plied for coverage under the Medicaid program. Freda’s

application was approved on May 15, with Medicaid cov-

erage retroactively effective April 1. For purposes of the

PTC, Freda is considered eligible for government-spon-

sored coverage on June 1, the first day of the first calen-

dar month after her application was approved. Freda may

be eligible for the PTC for January through May.

Termination for nonpayment of premiums. If Med-

icaid or CHIP coverage for you or a family member is ter-

minated due to nonpayment of premiums, you cannot get

the PTC for the coverage of that individual (for the remain-

der of the year of the termination).

Determining eligibility for Medicaid or CHIP at enroll-

ment. An individual is treated as ineligible for Medicaid,

CHIP, and similar programs (such as a BHP) for the period

of coverage under a qualified health plan if, when the indi-

vidual enrolled in the qualified health plan, the Market-

place determined that the individual was ineligible for

Medicaid or CHIP based on the applicable Medicaid and

CHIP income standards. However, this exception does not

apply if you, or the individual you are including in your tax

family, with intentional or reckless disregard for the facts,

provided incorrect information to the Marketplace for the

year of coverage. You provide information with intentional

disregard for the facts if you know that the information pro-

vided is inaccurate. You provide information with a reck-

less disregard for the facts if you make little or no effort to

determine whether the information provided is accurate

and your lack of effort to provide accurate information is

substantially different from what a reasonable person

would do under the circumstances.

Example. In November, Catelyn enrolled in a qualified

health plan for the following year and got APTC for her

coverage. The Marketplace determined that Catelyn was

ineligible for Medicaid and estimated that her household

income will be 140% of the federal poverty line for her

family size for purposes of determining APTC. During the

year, Catelyn lost her job and her household income for

2023 is 130% of the federal poverty line (within the Medic-

aid income threshold). For purposes of the PTC, Catelyn

is treated as ineligible for Medicaid for 2023. Catelyn may

be eligible for the PTC for the entire year.

Medicaid or CHIP eligibility when Marketplace does

not discontinue APTC. If a determination is made that

an individual who is enrolled in a qualified health plan for

which APTC is made is eligible for Medicaid or CHIP but

the Marketplace does not discontinue APTC for the first

calendar month beginning after the eligibility determina-

tion, the individual is treated as eligible for Medicaid or

CHIP no earlier than the first day of the second calendar

month beginning after the eligibility determination.

Employer-Sponsored Plans

The following employer-sponsored plans are MEC.

1. Group health insurance coverage for employees un-

der:

a. An insured plan or coverage offered in the small or

large group market within a state;

b. A governmental plan, such as the Federal Employ-

ees Health Benefits Program; or

c. A grandfathered health plan offered in a group

market.

2. A self-insured group health plan for employees.

3. Coverage under certain expatriate health plans for

employees (discussed earlier).

4. The Nonappropriated Fund Health Benefits Program

of the Department of Defense.

In general, these employer-sponsored plans may also

include retiree or COBRA coverage.

10 Publication 974 (2023)

Page 11 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Employer-sponsored plans that are MEC are also refer-

red to as “eligible employer-sponsored plans.”

Exceptions. The following paragraphs discuss when em-

ployer-sponsored plans are not considered MEC and the

circumstances in which you may be eligible for the PTC

even if you have an offer of coverage under an em-

ployer-sponsored plan.

Excepted benefits. Employer-sponsored health cov-

erage that is limited to excepted benefits is not MEC. Ex-

cepted benefits include stand-alone vision and dental

plans, workers' compensation coverage, and coverage

limited to a specified disease or illness.

Affordability and minimum value. Even if you had

the opportunity to enroll in coverage offered by your em-

ployer that qualifies as MEC, you are considered eligible

for an employer-sponsored plan (and cannot get the PTC

for your coverage in a qualified health plan) only if the em-

ployer-sponsored coverage is affordable (defined later)

and the coverage provides minimum value (defined later).

Your tax family members may also be unable to get the

PTC for coverage in a qualified health plan for months they

were eligible to enroll in employer-sponsored coverage of-

fered to them by your employer but only if the coverage

qualifies as MEC and was affordable and provided mini-

mum value. In addition, if you or your family member en-

rolls in the employer coverage that qualifies as MEC, the

individual enrolled cannot get the PTC for coverage in a

qualified health plan, even if the employer coverage is not

affordable or does not provide minimum value.

Waiting periods and other periods without access

to benefits. You are not considered eligible for employer

coverage, and can get the PTC for your coverage in a

qualified health plan if you are otherwise eligible, for a

month when you cannot receive benefits under the em-

ployer coverage (for example, you are in a waiting period

before the employer coverage becomes effective). How-

ever, if you could have enrolled in employer coverage that

is MEC and is affordable and provides minimum value and

you did not enroll during an enrollment period, you cannot

get the PTC for your coverage in a qualified health plan for

the remainder of the plan year to which the enrollment pe-

riod related. If the enrollment period related to coverage

for more than one plan year, and you do not have another

opportunity to enroll in the employer coverage for plan

years following the initial plan year, you can take the PTC

for your coverage in a qualified health plan during those

later plan years, if you are otherwise eligible.

Coverage after employment ends. If your employ-

ment with an employer ends and you are offered employer

coverage by your former employer (for example, COBRA

or retiree coverage), you are considered eligible for that

employer coverage for PTC purposes only for the months

that you are enrolled in the employer coverage. This same

rule applies to an individual who may enroll in the cover-

age by reason of a relationship to a former employee.

Individual not in your tax family. An individual who

can enroll in your employer coverage who is not a member

of your tax family (for example, an adult non-dependent

child under age 26) is considered eligible for the employer

coverage for PTC purposes only for the months the indi-

vidual is enrolled in the employer coverage.

How to determine if the plan is affordable. Your em-

ployer coverage is generally considered affordable for you

if your share of the annual cost for self-only coverage,

which is sometimes referred to as the “employee required

contribution,” is not more than 9.12% of your tax family’s

household income for 2023. Your employer coverage is

generally considered affordable for the other members of

your tax family eligible to enroll in the coverage if your

share of the annual cost for coverage for you and your

other tax family members is not more than 9.12% of your

family’s household income for 2023. If your employer cov-

erage is affordable for you but not affordable for your other

family members, you may be able to take the PTC for your

other family members if they enroll in a Marketplace quali-

fied health plan. For 2024, this annual cost threshold will

decrease to 8.39%. However, employer-sponsored cover-

age is not considered affordable if, when you or a family

member enrolled in a qualified health plan, you gave accu-

rate information about the availability of employer cover-

age to the Marketplace, and the Marketplace determined

that you were eligible for APTC for the individual’s cover-

age in the qualified health plan. See Determining afforda-

bility at the time of enrollment, later, for more information

on this rule.

Certain employer arrangements. An employee’s re-

quired contribution for employer-sponsored coverage may

be affected by various arrangements offered by the em-

ployer.

Wellness program incentives. If the employer that

offered you (or your spouse) employer-sponsored cover-

age for 2023 also offered a wellness incentive that poten-

tially affected the amount that you had to pay toward cov-

erage, the following rules apply: If the condition for

satisfying the wellness incentive (in other words, the con-

dition the employee must meet to pay the smaller amount

for coverage) relates exclusively to tobacco use, your re-

quired contribution is based on the amount you would

have paid for coverage if you had satisfied the condition

for the wellness incentive. Wellness incentives relating ex-

clusively to tobacco use are treated as satisfied in deter-

mining your required contribution regardless of whether

you would have actually earned the incentive had you en-

rolled in the coverage. If factors other than tobacco use

are part of the condition for satisfying the wellness incen-

tive, your required contribution is based on the amount

you would have paid for coverage had you not satisfied

the wellness incentive.

Example. George can enroll in employer coverage.

George’s monthly premiums for self-only coverage are

$450. If George, who is a smoker, attends a smoking ces-

sation class, his monthly premiums will be reduced by

$100. If George completes a cholesterol screening, his

monthly premiums will be reduced by $50. Whether or not

George actually completes either of these wellness pro-

gram incentives, for purposes of determining whether the

coverage is affordable for George, his required

Publication 974 (2023) 11

Page 12 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

contribution will be considered to be the amount reduced

by the $100 incentive for attending a smoking cessation

class but not reduced by the $50 incentive for completing

a cholesterol screening. Therefore, for purposes of deter-

mining whether his coverage is considered affordable,

George’s required contribution is $350.

Health reimbursement arrangements (HRAs). If the

employer that offered you employer-sponsored coverage

for 2023 also contributed (or offered to contribute) to an

HRA that may be used to pay premiums for the em-

ployer-sponsored coverage, your required contribution for

the employer-sponsored coverage is reduced by the

amount the employer contributed (or offered to contribute)

to the HRA for 2023, as long as you were informed of the

HRA contribution offer by a reasonable time before you

had to decide whether to enroll in the coverage. Employ-

ers may offer you alternative or additional HRA coverage.

See Individual coverage HRAs next.

Individual coverage HRAs. Starting in 2020, employ-

ers can offer individual coverage HRAs to help employees

and their families with their medical expenses. Under an

individual coverage HRA, employers can reimburse eligi-

ble employees for medical expenses, including premiums

for Marketplace health insurance.

If you were covered under an individual coverage HRA

for 2023, you are not allowed a PTC for your 2023 Market-

place health insurance. Also, if another member of your

tax family was covered under an individual coverage HRA

for 2023, you are not allowed a PTC for the family mem-

ber's 2023 Marketplace health insurance. If you or a family

member could have been covered by an individual cover-

age HRA for 2023, but you opted out of receiving reim-

bursements under the individual coverage HRA, you may

be allowed a PTC for your, and your family member's,

Marketplace health insurance if the individual coverage

HRA is considered unaffordable.

Qualified small employer health reimbursement ar-

rangements (QSEHRAs). If your employer provided you

with a QSEHRA, special rules apply. See Qualified Small

Employer Health Reimbursement Arrangement, later, for

more details.

Health flex contributions. If the employer that offered

you (or your spouse) employer-sponsored coverage for

2023 also made (or offered to make) a health flex contri-

bution for 2023, your required contribution for the em-

ployer-sponsored coverage is reduced by the amount of

the health flex contribution (or offer). A health flex contri-

bution is an employer contribution to a cafeteria plan that

may be used only to pay for medical care (and not taken

as cash or other taxable benefits) and is available for use

toward the purchase of MEC. Cafeteria plan contributions

that may be used for expenses other than medical care

are not health flex contributions and so do not reduce your

required contribution.

Opt-out payments. If the employer that offered you

(or your spouse) employer-sponsored coverage for 2023

offered you an additional payment if you declined to enroll

in the coverage (an “opt-out payment”), your required

contribution for employer-sponsored coverage is in-

creased by amounts that the employer offered to pay you

for declining the coverage. In some cases, an employer

may make this opt-out payment only if the employee both

declines the coverage and also satisfies another condition

(such as enrolling in coverage offered by the employee's

spouse). If your employer imposed other conditions on re-

ceiving the opt-out payment (in addition to declining the

employer's health coverage), you may treat the opt-out

payment as increasing the employee's required contribu-

tion only if you can demonstrate that you met the condi-

tions (such as enrolling in coverage offered by your spou-

se's employer).

More information about employer arrangements.

You should contact your employer if you have questions

about the effect of the employer arrangements described

above on your required contribution.

If your employer or the employer of a family mem-

ber offered MEC providing minimum value and

provided you a Form 1095-C and the employer

also offered a non-health flex contribution or an opt-out

payment, the amount reported on line 15 of Form 1095-C

may not accurately reflect the amount of your required

contribution for purposes of the PTC. If you have ques-

tions about the amount reported on line 15, contact your

employer using the contact number provided on the Form

1095-C.

Determining affordability at the time of enrollment.

Your employer coverage is not considered affordable if,

when you enroll in a qualified health plan, the Marketplace

determines that your required contribution for employer

coverage will be more than 9.12% of what the Market-

place estimates will be your household income and there-

fore that you are eligible for APTC for coverage in the

qualified health plan. Eligibility for employer coverage in

this situation does not disqualify you from taking the PTC

when you file your tax return, even if your required contri-

bution for coverage was not more than 9.12% of the

household income on your return. However, you will be

treated as eligible for affordable employer coverage based

on the household income on your tax return if:

•

You did not provide current information to the Market-

place relating to your household income and the re-

quired contribution for your employer coverage during

each annual re-enrollment period, or

•

You provided incorrect information to the Marketplace

about your required contribution with intentional or

reckless disregard for the facts.

You provide information with intentional disregard for

the facts if you know that the information provided is inac-

curate. You provide information with a reckless disregard

for the facts if you make little or no effort to determine

whether the information provided is accurate and your

lack of effort to provide accurate information is substan-

tially different from what a reasonable person would do

under the circumstances.

CAUTION

!

12 Publication 974 (2023)

Page 13 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

The employer coverage offered by the various employ-

ers in the following examples qualifies as MEC.

Example 1. Celia is single and has no dependents.

Her household income for 2023 was $47,000. Celia’s em-

ployer offered its employees a health insurance plan that

provided minimum value and for which the required contri-

bution was $3,450 for self-only coverage for 2023 (7.34%

of Celia’s household income). Because Celia’s required

contribution for self-only coverage did not exceed 9.12%

of household income, her employer’s plan is considered

affordable for Celia, and Celia is considered eligible for

the employer coverage for all months in 2023. Celia can-

not get the PTC for coverage in a qualified health plan.

Example 2. The facts are the same as in Example 1,

except that Celia is married to Jon, they file a joint return

for 2023, and the employer’s plan required Celia to con-

tribute $5,300 for coverage for Celia and Jon for 2023

(11.28% of Celia’s household income). Because Celia’s

required contribution for coverage for herself and Jon ex-

ceeds 9.12% of household income, her employer’s plan is

considered not affordable for Jon and Jon is considered

not eligible for the employer coverage. Celia is, however,

considered eligible for the employer coverage for all

months in 2023 and cannot get the PTC for coverage in a

qualified health plan because her cost to enroll in the cov-

erage does not exceed 9.12% of their household income.

Jon is allowed a PTC if he does not enroll in the employer

coverage, enrolls in a qualified health plan through the

Marketplace for 1 or more months in 2023, and is other-

wise allowed a PTC.

Example 3. Don was eligible to enroll in employer cov-

erage in 2023. Don’s required contribution for self-only

coverage that provided minimum value was $3,550. Don

applied for coverage in a qualified health plan through the

Marketplace. The Marketplace projected that Don’s 2023

household income would be $37,000 and determined that

Don’s employer coverage was unaffordable because

Don’s required contribution was more than 9.12% of Don’s

household income. Don enrolled in a qualified health plan

through the Marketplace with APTC and not in the em-

ployer coverage. In December, Don received an unexpec-

ted $2,500 bonus, which increased his 2023 household

income to $39,500. Although Don’s required contribution

for the employer coverage was not more than 9.12% of the

household income on Don’s tax return, Don is considered

not eligible for the employer coverage for 2023 because

the Marketplace estimated that the employer coverage

would cost more than 9.12% of Don’s household income.

Don can get the PTC if he otherwise qualifies.

Example 4. Hal was eligible for employer coverage for

2023. His required contribution for self-only coverage was

$3,400, and Hal enrolled in the coverage. His household

income for 2023 was $33,000, which means that his re-

quired contribution was more than 9.12% of his household

income. Even though the employer coverage was not af-

fordable, Hal cannot get the PTC for coverage in a quali-

fied health plan because he enrolled in the employer cov-

erage.

Example 5. Elsa is married and has two dependent

children. Her household income for 2023 was $39,000. El-

sa’s employer offered only self-only coverage to employ-

ees. No family coverage was offered. The plan had a re-

quired contribution of $3,000 for self-only coverage for

2023 (7.69% of Elsa’s household income) and provided

minimum value. Because Elsa’s required contribution for

self-only coverage was not more than 9.12% of household

income, her employer’s plan is considered affordable for

Elsa. Thus, Elsa is considered eligible for the employer

coverage for 2023 and cannot get the PTC for coverage in

a qualified health plan. However, because Elsa’s employer

did not offer coverage to Elsa’s spouse and children, Elsa

could take the PTC for her spouse and two children if they

enrolled in a qualified health plan and otherwise qualify.

Determining affordability for part-year period. If

you are employed for part of a year or employed by differ-

ent employers during the year, you determine whether

your coverage is affordable by looking separately at each

coverage period that is less than a full calendar year. For

each period, the coverage is affordable if your required

contribution for the entire year would not be more than

9.12% of your household income for the year.

Example. Elvis was enrolled in a qualified health plan

without APTC beginning in January 2023. He began work-

ing for a new employer in May that offers health insurance

coverage with a calendar year plan year. Elvis’ required

contribution for the employer coverage for the remainder

of the year was $200/month, which would be $2,400 for

the full plan year. Elvis does not enroll in the employer

coverage or inform the Marketplace of the offer of em-

ployer coverage. Elvis’ household income for the year is

$20,000. Elvis’ employer coverage is considered unafford-

able for the period May through December because his

required contribution for the full plan year, $2,400, is more

than 9.12% of his household income. As a result, Elvis

could take the PTC for January through December if he

otherwise qualifies.

Coverage year not a calendar year. If your employ-

er’s plan year is not the calendar year and you are a calen-

dar year taxpayer, you determine whether your coverage

is affordable by looking separately at the portion of the cal-

endar year in each plan year. A coverage period in 2023

that falls in a plan year beginning in 2022 is considered af-

fordable if your required contribution for the entire plan

year is not more than 9.61% of your household income for

2023. A coverage period in 2023 that falls in a plan year

beginning in 2023 is considered affordable if your required

contribution for the entire plan year is not more than

9.12% of your household income for 2023.

The employer coverage offered by the various employ-

ers in the following examples qualifies as MEC.

Example 1. Tim’s employer offers health insurance

coverage with a plan year of July 1 through June 30. His

required contribution for the plan year that began on July

1, 2022, was $250 per month ($3,000 for the entire plan

year). Tim enrolled in a qualified health plan on January 1,

2023, and did not apply for APTC. Tim’s household

income for 2023 is $30,000. Tim’s required contribution for

Publication 974 (2023) 13

Page 14 of 68 Fileid: … tions/p974/2023/a/xml/cycle04/source 7:31 - 21-Feb-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

the plan year, $3,000, is 10% of his household income for

2023. Because 10% is more than 9.61% (the required

contribution percentage for the plan year beginning in

2022), Tim’s employer coverage for January 1, 2023,

through June 30, 2023, is not considered affordable, and

Tim can take the PTC for those months if he is otherwise

eligible.

For the plan year that began on July 1, 2023, Tim’s re-

quired contribution was reduced to $200 per month (or

$2,400 for the entire plan year). Tim’s required contribu-

tion of $2,400 is 8% of his 2023 household income. Be-

cause 8% is not more than 9.12% (the required contribu-

tion percentage for the plan year beginning in 2023), Tim’s

employer coverage for July 1, 2023, through December

31, 2023, is considered affordable and he is not eligible

for the PTC for those months.

Example 2. Maria’s employer offers health insurance

coverage with a plan year of September 1 through August

31. Maria’s required contribution for the employer cover-

age for the plan year September 1, 2023, through August

31, 2024, is $3,700. Maria’s household income for 2023 is

$37,000. Maria’s employer coverage is considered unaf-

fordable for the period September 1 through December

31, 2023, because her required contribution for the plan

year, $3,700, is more than 9.12% of her 2023 household

income. If Maria enrolls in a qualified health plan for 2024

and requests APTC, the Marketplace will determine

whether the employer coverage is considered affordable

for the period January 1, 2024, through August 31, 2024,

by comparing Maria’s required contribution for the plan

year beginning in 2023, $3,700, to her estimated 2024

household income.

How to determine if a plan provides minimum value.

An employer-sponsored plan provides minimum value

only if the plan pays at least 60% of the total allowed costs