© JANNEY MONTGOMERY SCOTT LLC MEMBER: NYSE, FINRA, SIPC REF: 10655010523 PAGE 1 OF 5

UNDERSTANDING YOUR FORM 1099

CONSOLIDATED TAX STATEMENT

BEYOND INVESTING. CONNECTING.

Reporting investment income and related expenses on your tax forms is simpler with a bit of guidance.

To help you navigate the Form 1099 Tax Reporting Information Statement you receive from investment

firms such as Janney, review this handy guide.

THINGS TO KEEP IN MIND

The Tax Reporting Information Statement, Form 1099, is a record of activity in your account at Janney Montgomery

Scott LLC.

This statement provides a comprehensive record of reportable income and securities transactions posted to your

Janney account during the taxable year. The information provided by Janney on Form 1099 will be reported to the

Internal Revenue Service (IRS) as indicated.

If you are required to file a tax return with the IRS, you could be subject to a negligence penalty or other sanctions if

the IRS determines that the income reported on this statement is taxable and has not been reported.

All information that Janney provides here should not be a substitute for obtaining tax-filing advice from a professional

tax advisor as this guide is general in nature and every taxpayer’s tax situation is unique.

If you have any questions regarding your 1099 Consolidated Tax Statement, please contact your Janney Financial

Advisor. Tax preparation questions should be directed to your professional tax advisor.

Your 1099 Consolidated Tax Form consists of several sections

which are summarized below in the order in which they appear

on the form. Sections reportable by Janney directly to the IRS

are indicated where applicable on your 1099 Form.

1099-DIV: DIVIDENDS AND DISTRIBUTIONS

This section includes all dividend income received

in your Janney account during the year. Below are

explanations of commonly populated lines:

• Line 1a: Total Ordinary Dividends – Shows the total

ordinary dividends.

• Line 1b: Qualified Dividends – Shows the portion of

the dividends displayed in Line 1a that may be eligible

for a reduced capital gains rate, also known as

“qualified dividends.”

• Line 2a: Total Capital Gain Distributions – Shows the total

capital gain distributions from a regulated investment

company or real estate investment trust.

• Line 2e: Section 897 Ordinary Dividends – Shows the

portion of the dividends displayed in box 1a that is Section

897 gain attributable to disposition of U.S. Real Property

interests (USRPI).

• Line 2f: Section 897 Capital Gain – Shows the portion of

the amount in box 2a that is Section 897 gain attributable

to disposition of USRPI.

• Line 3: Non-dividend Distributions – Also known as Return

of Capital, this line shows the total amount of any non-

dividend distributions received which is a return of your initial

investment. This amount generally reduces the basis for the

security by the same amount of the distribution.

• Line 4: Federal Income Tax Withheld – Shows the total

amount of Federal dividend income withholding.

• Line 5: Section 199A dividends – Shows the total “qualified

REIT dividends” (also called “Section 199A dividends”)

resulting from the Tax Cuts and Jobs Act.

1099-MISC: MISCELLANEOUS INCOME

This section includes payments in cash (including certain

monetary instruments) or foreign currency received in any

of the following transactions: royalty income payments, fees,

non-employee compensation, and substitute payments in

lieu of dividends.

• Line 3: Other Income – This line can include payments

received from the Fully Paid Lending Program

© JANNEY MONTGOMERY SCOTT LLC MEMBER: NYSE, FINRA, SIPC REF: 10655010523 PAGE 2 OF 5

• Line 4: Federal Income Tax Withheld – Shows the total

amount of miscellaneous income withholding.

• Line 8: Substitute Payments in Lieu of Dividends or

Interest – Shows the total amount of payments in lieu

of dividend or interest when your securities are out on

loan. Income received during the period when you are

not holder of record is considered a substitute payment,

rather than dividend or interest income.

1099-INT: INTEREST INCOME

This section includes interest income received in your

Janney account during the year. Below are explanations

of commonly populated lines:

• Line 1: Interest Income – Shows the total taxable interest

paid to you during the calendar year by the payer. This

line does not include Line 3.

• Line 3: Interest on US Savings Bond & Treasury

Obligations – Shows the total interest from US

Savings Bonds, Treasury Bills, Treasury Bonds and

Treasury Notes.

• Line 4: Federal Income Tax Withheld – Shows the total

amount of interest income withholding.

• Line 8: Tax Exempt Interest – Shows the total amount of

tax-exempt interest paid to you during the calendar year

by the payer.

• Line 11: Bond Premium – Shows the total amount of bond

premium for taxable obligations. Despite being shown as

a positive number, this is a negative line item and the IRS

recognizes that the number is negative and their systems

read it as negative.

SALE TRANSACTIONS

This section, which is for informational purposes, summarizes

the total cost basis, proceeds, and gain/loss information from

the transactions displayed in section 1099-B.

Term

• Short Term: Assets owned for one year or less.

• Long Term: Assets owned for more than one year.

• Undetermined: Assets owned where the date acquired

or cost basis cannot be determined.

Covered vs. Non-covered

• Covered: Janney reports the cost basis information to

the IRS (on a tax lot by tax lot basis).

• Non-covered: Janney does not report the cost basis

information to the IRS, however it is provided on the

Form 1099 for your convenience where we have

the information.

1099-B: PROCEEDS FROM BROKER AND BARTER

EXCHANGE TRANSACTIONS

This section includes reportable information and shows

all sales transactions that occurred in your Janney

account during the year. There are several sub-sections

that separate long-term, short-term and undetermined-

term holding period and covered or non-covered status.

Each sub-section’s header that displays what the type of

transactions are and what information is being reported

to the IRS.

• Short Term Transactions for Covered Tax Lots: This

section displays sales transactions of assets that were

owned for one year or less. The cost basis for these

transactions is reported to the IRS.

• Short Term Transactions for Non-covered Tax Lots: This

section displays sales transactions of assets that were

owned for one year or less. The cost basis for these

transactions is not reported to the IRS.

• Long Term Transactions for Covered Tax Lots: This

section displays sales transactions of assets that were

owned for more than one year. The cost basis for these

transactions is reported to the IRS.

• Long Term Transactions for Non-Covered Tax Lots: This

section displays sales transactions of assets that were

owned for more than one year. The cost basis for these

transactions is not reported to the IRS.

• Undetermined Term Transactions for Non-Covered Tax

Lots: This section displays sales transactions of assets

where the date acquired and/or the cost basis cannot

be determined.

Example of a Long Term Transaction for Covered Tax Lots

transaction displayed on the 1099-B

• 1a-Description of Property/CUSIP/Symbol: Displays the

name of the asset, CUSIP and symbol.

• 1c-Date Sold or Disposed: Displays the date in which the

asset was sold or disposed of.

• Quantity: Displays the total amount of shares or units.

• 1d-Proceeds: Displays the proceeds received from the

transaction which is reported to the IRS.

• 1b-Date Acquired: Displays the date in which the asset

was originally purchased.

© JANNEY MONTGOMERY SCOTT LLC MEMBER: NYSE, FINRA, SIPC REF: 10655010523 PAGE 3 OF 5

• 1e-Cost or other basis: Displays the basis on the tax lot

used to calculate the gain or loss provided.

– Note: This section will display the adjusted cost basis

if there were adjustments such as bond adjustments,

return of capital, or paydowns.

• Adjustments: Displays, if any, the amount of disallowed

loss in a wash sale transaction or the amount of accrued

market discount.

• Gain or Loss: Displays the total amount of gain or loss

which is equal to the dierence between the cost basis

and the proceeds.

• Additional information: Displays what type of transaction

occurred, provides additional footnotes, and will also

note what the original cost basis was if there has been

an adjustment.

DETAIL FOR DIVIDENDS AND DISTRIBUTIONS &

DETAIL FOR INTEREST INCOME SECTIONS

These sections include payment level detail of your qualified

and nonqualified taxable dividends, capital gain distributions,

exempt-interest dividends, non-dividend distributions (return

of capital payments), liquidation distributions, interest income

and associated bond premium.

All amounts are grouped by security, with the income or

distributions listed in chronological order.

• The detail provided is Security Description, CUSIP and/or

Symbol, Date, Amount, Transaction Type and Notes. Any

notes are further explained at the end of the Form 1099.

OTHER RECEIPTS AND RECONCILIATION SECTION

• Unit Investment Trusts: Displays the adjustments made

between cash distributions and reportable income during

the applicable Tax Year. Income recognition may be

taxable in a separate Tax Year from the actual year of

distribution. This section shows the year such income

is recognized, not necessarily distributed.

• Partnerships: This section will show the gross amount of

partnership distributions received throughout the year. This

section does not include information on the final taxability

of these distributions; tax implications are provided on your

Schedule K-1 issued directly from the Partnership.

• Deferred Income: If you have deferred income, it may be

shown in this section but reportable and taxable in the

following Tax Year (on 1099-DIV). Any information shown

in this section as “Deferred Income” is shown therefore

as informational only to assist account holders in any

reconciliation of their income received during the year,

and is not being reported.

IMPORTANT TAX INFORMATION

Amended Tax Forms

Holding certain asset types could cause an amended 1099

to be issued due to late income taxability announcements

by the issuing companies. Types of assets that could cause

an amended form are mutual funds, regulated investment

companies (RIC), real estate investment trusts (REIT), unit

investment trusts (UIT), foreign securities or any other asset

that has late income taxability announcements. Janney

strives to deliver the most accurate information to you at

the earliest available time.

TurboTax®

• Janney clients have the ability to import their 1099

Tax Form data directly into TurboTax® software which

will provide clients the benefit of saving valuable

time and eort as the information will not have to be

manually entered.

• TurboTax® is a leading tax-preparation software

product from Intuit, Inc. that allows you to download

W-2 and 1099 data from participating employers and

financial institutions.

• Step by step instructions to import 1099 data into

TurboTax® are located at www.janney.com/taxes

under “Janney Download Guide for TurboTax®.”

H&R Block®

• Janney clients have the ability to import their 1099 Tax Form

data directly into H&R Block® software which will provide

clients the benefit of saving valuable time and eort as the

information will not have to be manually entered.

• H&R Block® is a leading tax-preparation software product

that allows you to download W-2 and 1099 data from

participating employers and financial institutions.

• Step by step instructions to import 1099 data into H&R

Block® are located at www.janney.com/taxes under

“Janney Download Guide for H&R Block®.”

CSV File

• Janney also oers clients a download capability for 1099 tax

statement data (1099 Consolidated, 1099 Non-reportable

Summaries, and 1099-R forms) into a CSV file format.

• This download feature allows clients with large

amounts of tax data to download CSV or ZIP files that

are commonly used by tax professionals with many

professional tax and accounting software programs.

• Clients are encouraged to request further information

from their Financial Advisor or local Branch team to

take advantage of this option if their tax preparer

or professional suggests a data file rather than the

traditional 1099 form.

© JANNEY MONTGOMERY SCOTT LLC MEMBER: NYSE, FINRA, SIPC REF: 10655010523 PAGE 4 OF 5

HELPFUL TAX TERMINOLOGY & DEFINITIONS

Managed Account Fees

• Fees that are paid to investment/fund advisors for

portfolio management from investment/fund assets.

Typically these fees are a certain percentage of assets

under management, which are comprehensive. Under

the Tax Cuts and Jobs Act (2018), these fees are no

longer deductible as itemized deductions as they have

been curtailed by the new law. The fees are no longer

displayed on the 1099 Consolidated Form in order to

reduce confusion with previous tax year’s deductibility.

If you would like to review your yearly total, please

review your monthly statements or feel free to reach

out to your Financial Advisor.

Investment Expenses

• Certain products such as Unit Investment Trusts (UIT)

classify expenses as Investment Expenses, which

includes operating expenses related to portfolio

supervision, administration, evaluation, trustee fees

and bookkeeping. The trustees supply investment

factors in a variety of formats, most often as a factor

of distributed income. Additional information on how

these factor values are determined can usually be

found on the UITs public website in their tax section.

Please note, depending on the type of UIT you hold,

information may be released later in tax season than

other types of securities.

Grantor Trust (UIT organization type) and Regulated

Investment Company (UIT organization type)

• Grantor Trust UITs act as pass-through vehicles where

UIT holders are deemed to own the underlying assets

of the UIT directly and tax reporting is subject to WHFIT

rules. Currently in-kind distributions are not taxable.

• Regulated Investment Company UITs (“RICs”) are

not treated as pass-through entities, and therefore

holders are not deemed to own the underlying assets

directly. Tax reporting on RICs are not subject to WHFIT

rules, however in-kind distributions, if applicable, are

considered taxable.

Limited Partnership Distributions (K-1)

• If you owned units in a limited partnership during the Tax

Year you will receive a Schedule K-1 (Form 1065) from the

partnership you own. General Partners have until March

15 to issue K-1’s. If you do not receive your Schedule K-1,

please contact the partnership directly as Janney does

not generally have access to your K-1 forms. Janney

does not produce K-1 forms. Two main websites that

allow you to access your form electronically are

www.taxpackagesupport.com and www.partnerdatalink.com.

These public websites are not maintained or aliated

with Janney Montgomery Scott, LLC and are being

provided for informational purposes only.

• Additional information on limited partnership and their

taxability can also be found in IRS Publication 541.

Covered and Non-Covered Tax Lots

• Covered Tax Lot: An asset purchased or acquired after

a certain date in which Janney is required to send cost

basis information along with proceeds information to

the IRS.

• Non-covered Tax Lot: An asset purchased or acquired

before a certain date in which Janney does not send

cost basis information to the IRS. Janney is still required

to send proceeds information to the IRS.

• Undetermined Tax Lot: An asset where a cost basis and/

or date acquired is unknown. Janney does not send the

cost basis information to the IRS but is still required to

send the proceeds information to the IRS.

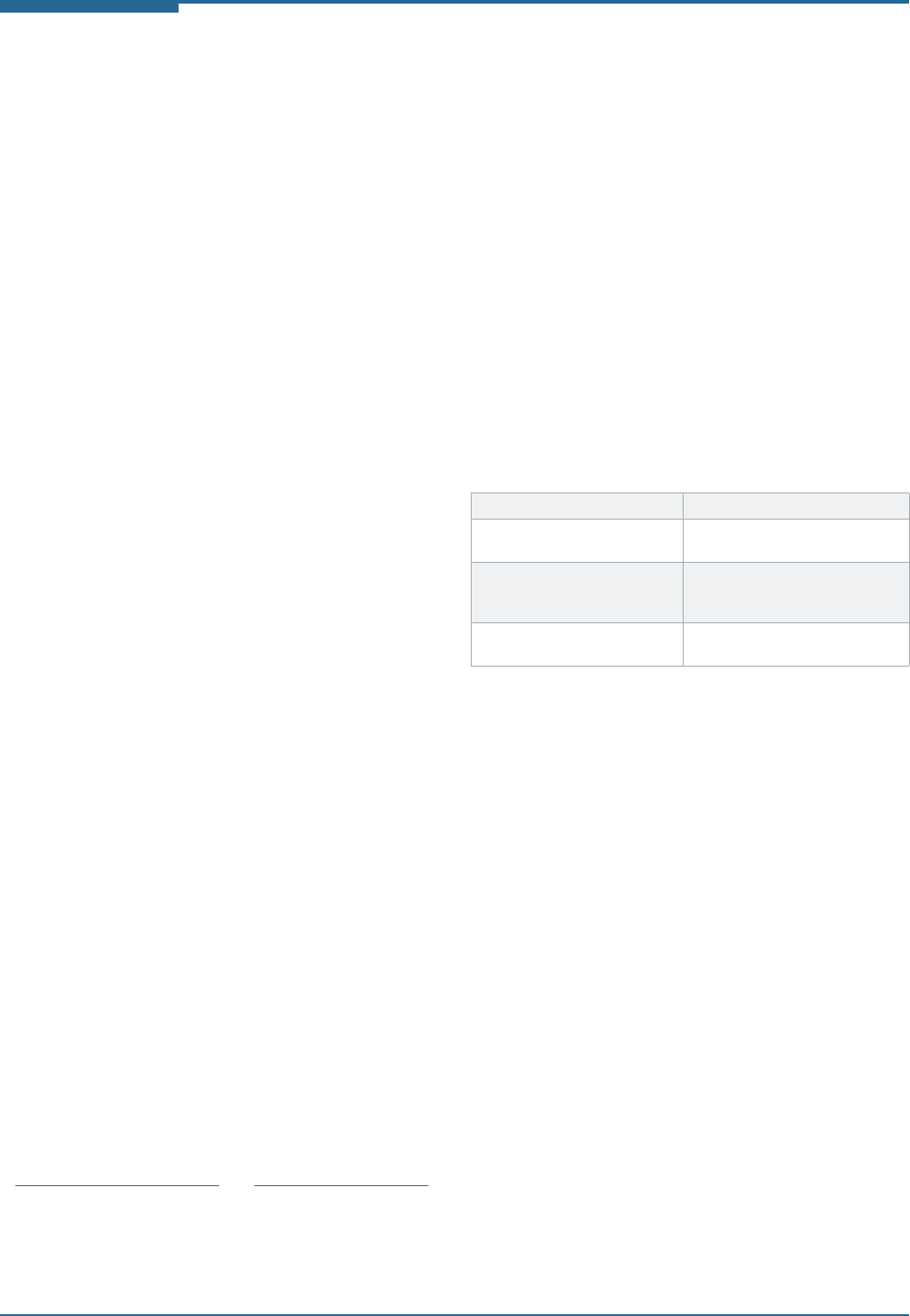

• The below chart states when classes of assets

became covered:

Acquired after January 1, 2011 Equity Securities

Acquired after January 1, 2012 Mutual Funds and Dividend

Reinvestment Plan (DRIP) shares

Acquired after January 1, 2014 Simple Debt securities, OID

bonds, zero coupon bonds,

options, rights and warrants

Acquired after January 1, 2016 Complex Debt Securities, variable

rate bonds

Holding Period Term

• Short Term: An asset that is held for one year or less.

• Long Term: An asset that is held for over one year. Assets

inherited from a decedent are also deemed long term by

the IRS.

Dividends & Distributions

• Qualified Dividend: Represent dividends that, based on

published information, may qualify for the tax rate of 15%

if the taxpayer is in a certain income bracket and has

held the shares for the minimum hold period around the

ex-dividend date. The minimum holding period is 61 days

for domestic common stocks and many foreign stocks

and 91 days for domestic preferred stocks.

• Non-qualified Dividend: Represent a dividend that has

no preferential tax treatment and would be taxed at your

ordinary income tax rate.

• Non-dividend Distribution: Represents a return of

your initial investment that will generally reduce the

cost basis for the security by the same amount of the

distribution. This is a non-taxable item until your cost

basis in the asset has been fully recovered. Also

known as Return of Capital.

© JANNEY MONTGOMERY SCOTT LLC MEMBER: NYSE, FINRA, SIPC REF: 10655010523 PAGE 5 OF 5

FREQUENTLY ASKED QUESTIONS

I did not receive any cash payments on my debt

instrument. Why is OID being reported?

• If a debt instrument is issued with OID, we are required

to report a portion of that OID each year the instrument

is held in your account regardless of whether you

actually receive cash payment. If you held a debt

instrument that was issued with OID and also made

cash payments of interest, we report the cash payments

to you in Other Periodic Interest column of the 1099-OID

section of your 1099-REMIC/WHFIT statement.

How are return of capital (Non-dividend) distributions

reported on the 1099-DIV?

• Return of capital (Non-dividend) distributions are

reported on Line 3. It is not always possible to

determine this information at the time of payment,

which means the payment is considered final until the

issuer reallocates the taxability. When Janney receives

these notifications from the issuer a corrected Form

1099-DIV may then be produced.

Why is the interest earned on certain asset-backed

securities not reported on the Form 1099-INT section

of the 1099 Consolidated Form?

• Interest earned on CDO, REMIC, and WHFIT securities

are subject to special information reporting rules

because additional tax information must be provided to

the holders of the securities. The income and additional

tax information is then reported on a Form 1099-OID/

REMIC, which is postmarked to clients no later than

March 15th.

Why are principal payments showing on Form 1099-B

Gross Proceeds?

• Form 1099-B reports receipt of Scheduled and

Unscheduled Principal Payments on the mortgages

held by the WHFIT. Trustees must calculate and provide

information regarding these principal receipts that are

attributable to a unit interest holder. Scheduled and

Unscheduled Principal receipts are aggregated with

the WHFIT’s proceeds from sales and dispositions of

mortgages and reported as trust sales proceeds to the

IRS on Form 1099-B. Unless a trustee reports under

the safe harbor for certain WHFITs, scheduled and

unscheduled principal receipts and trust sales proceeds

are reported separately to beneficial owners.

Why haven’t I received my K-1?

• Partnerships currently have until March 15th to issue

K-1 statements. Many partnerships also oer online

access to their forms via their individual websites once

the forms are produced. Janney does not produce

K-1 forms, therefore you should contact the partnership

directly regarding any inquiry as to the status of your

forms. A large amount of K-1 statements are available

through two websites: www.taxpackagesupport.com

and www.partnerdatalink.com/landing/landing.html.

These are helpful resources for obtaining direct

partnership contact information. Janney is not

aliated with the www.taxpackagesupport.com

or www.partnerdatalink.com/landing/landing.html

websites. These website addresses are provided only

for informational purposes as an outside resource.

Janney does not make any warranties or guarantees

as it relates to their accuracy, accessibility, or security.

Janney Montgomery Scott LLC, its aliates, and its employees are not in the business of providing tax, regulatory, accounting, or legal advice. These

materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any taxpayer for the purpose of

avoiding tax penalties. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

Each taxpayer’s situation is dierent and tax-related information provided herein

is general in nature. Consult with a professional tax advisor with questions specific

to your personal tax situation.