2

Abstract

Private and public sector analysts and subject matter experts working in the cyber

financial landscape gathered through a series of meetings to examine the use of financial

technologies and cryptocurrencies by illicit actors. The key research points investigated include

discovering the most common illicit finance activities, the most exploited elements of financial

technologies, the legal vulnerabilities that allow exploitation, pseudo-anonymity in online

transactions, weaknesses in Know-Your-Customer laws, and the risks of use associated with

other emerging blockchain applications (i.e. NFTs). The research gathered from investigating

these areas led to the development of suggested, effective changes to reduce illicit activity in

this space and identifying the key stakeholders to implement these changes. This paper seeks to

provide guidance in navigating cryptocurrencies, emerging digital payment solutions, and other

blockchain applications to both consumers and stakeholders to minimize the illicit use of these

platforms. While illicit use cannot be eliminated altogether, it can certainly be reduced with

better consumer knowledge and better practices/regulations issued by key stakeholders.

3

DISCLAIMER STATEMENT: The views and opinions expressed in this document do not necessarily

state or reflect those of the United States Government or the Companies whose analysts

participated in the Public-Private Analytic Exchange Program. This document is provided for

educational and informational purposes only and may not be used for advertising or product

endorsement purposes. All judgments and assessments are solely based on unclassified sources

and the product of joint public and private sector efforts.

4

Team Introductions

MEMBERS COMPANY/AGENCY

Champion: Alexander Angert FBI

Champion: Stephen Deininger NSA

Kevin Lyons Sec+, CFE U.S. Secret Service

Chris Kachenko Federal Reserve Bank of Cleveland

Danie Evariste Saint Cyr, CPA, CFE, CCI FBI

Kristen Peters DoD

Mattonna Wahlgren, CFCS Western Union

Madison Malarkey Invesco

Kathy Novak NICB

5

Table of Contents

Most Common Illicit Finance Activities

Most Exploited Elements of Financial Technology

Legal and Technological Vulnerabilities

Pseudo-Anonymity & Weaknesses in KYC Laws

NFTs and Other Blockchain Applications Risk of Illicit Use

Key Findings and Recommendations

Impact on Government and Private Sector

Future Regulations, Forecast, and Areas for Future Study

Analytic Deliverable Dissemination Plan

Endnotes Separated by Sections

Full Citations Separated by Sections

Appendices

6

Most Common Illicit Finance Activities

Illicit finance activity continues to grow in value and variation, especially with the use of

digital assets and cryptocurrency. Some of the most common illicit activities in this digital space

are money laundering, cybercrime, and consumer scams.

Money Laundering

Money laundering traditionally begins with ill-gained fiat currency that criminals wish to

make usable. One strategy is to have money mules transfer these funds into bank accounts for

later transfer/withdrawal. Cryptocurrency has opened new avenues for money launderers

utilizing bank deposits by mules who then purchase cryptocurrency. Bitcoin ATMs are another

popular method for money mules to convert fiat currency into cryptocurrency. Bitcoin ATMs

are physical machines where people can buy cryptocurrency with cash, requiring varying

amounts of personal information to use. Once the fiat currency is converted into

cryptocurrency, there are multiple ways it can be laundered, making it difficult for law

enforcement to track.

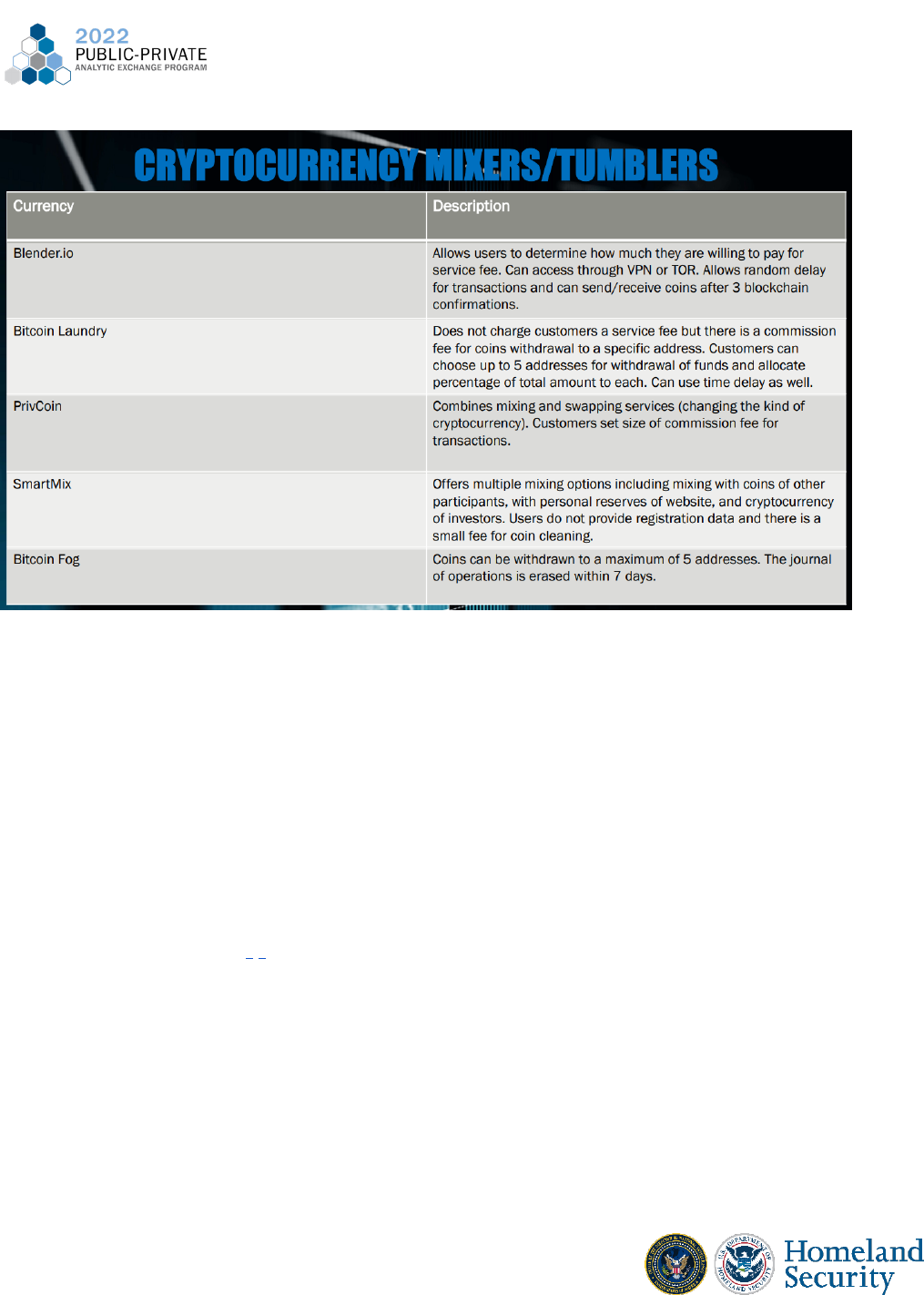

Cryptocurrency mixers, for example, aid in obfuscating the origins of the processed

cryptocurrency. This happens by rapidly pooling currency streams into many small transactions

across many wallets. Mixers allow illicit actors to launder high amounts very conveniently and

are not inherently illegal. The co-founder of Tornado Cash, a popular cryptocurrency mixer, told

Bloomberg in March 2022 that their service can be defined as an “anonymizing software

provider” which does not subject them to money transmitter regulations in the U.S. Our group

examined some of the most popular and common mixers/tumblers used today and our findings

are reviewed in the chart below. 1

DeFi, or Decentralized Finance platforms are another common way illicit actors launder

their money through cryptocurrency. The defining characteristic of a DeFi service is its lack of a

centralized intermediary for transactions or other services. Additionally, most of the DeFi

platforms used by illicit actors are outside of the U.S. and are often not subject to or compliant

with Know Your Customer (KYC) and Anti-Money Laundering (AML) laws. Some DeFi platforms

also allow chain hopping, which allows users to exchange one cryptocurrency for another.

Moving to a new blockchain through chain hopping aids in obfuscating transaction history.

7

Case Study: Roman Stirlingov and Bitcoin Fog

In April 2021 Roman Stirlingov, the principal operator of cryptocurrency mixer Bitcoin

Fog, was arrested by the FBI. Bitcoin Fog emerged as one of the first cryptocurrency mixers that

especially helped illicit actors hide their illegal proceeds. This service particularly aided darknet

market and Silk Road users to hide trafficking activity in drugs and other illegal payments. Over

1.2 million Bitcoin equating to approximately $336 million at the time of transactions were

reported to be sent over Bitcoin Fog. Stirlingov was discovered as the operator due to a mix of

resources utilized by investigators including bitcoin transactions, financial records, internet

service provider records, email records, and additional general records. This case emphasizes

that with the right combination of resources, investigators can identify illicit actors utilizing

Bitcoin as a cryptocurrency.

1

2

Cybercrime

The laundering techniques noted above are regularly used by hackers who have funds

originating as cryptocurrency from cybercrime such as ransomware and hacking digital assets

from persons or exchanges. The rapid growth of digital assets usage has created a landscape of

insecure and often unregulated trading platforms and exchanges, leading to increased

consumer risk. Cryptocurrency and blockchain platforms are now targets for hackers due to

their large consolidation of assets. In March 2022 the North Korea associated hacking group

8

Lazarus stole $620 million of Etherium from the Ronin Network, a blockchain platform used by

the Axie Infinity online game. In addition to these large scale attacks, some consumers’

personal digital wallets have been compromised due to unencrypted private keys stored by

exchanges, and through social engineering tactics.2

Today’s ransomware model is built upon the use of cryptocurrency for payments.

Ransomware payments in 2021 and 2022 each totaled over $600 million according to

Chainanalysis’ 2022 Crypto Crime Report. Most ransomware groups are located outside the U.S.

which makes any traditional ransom payment using fiat currency difficult for the victims to pay

and the ransomware groups to receive and launder. Global crypto exchanges and DeFi

platforms help facilitate the illicit transfers and are typically out of reach to the U.S. and Mutual

Legal Assistance Treaty (MLAT) countries. For more information on Ransomware attacks and

their impact to critical infrastructure sectors, review the 2022 AEP whitepaper on

“Ransomware Attacks on Critical Infrastructure Sectors”.3

Consumer Scams

Consumer targeted cryptocurrency crime ranging from investment rug pulls and

romance scams to social engineering and account takeovers continues to be the largest subset

of illicit transactions. These scams reportedly cost consumers over $7.7 billion in 2021

according to Chainanalysis’ 2022 Crypto Crime Report. Rug pulls are investment scams, usually

associated with a new token, in which the developers of the project collect investments from

consumers and then take the funds and abandon the project. This scam is often tied to

romance scams in which victims are pressured or persuaded into an investment. The FBI’s 2021

IC3 Report found over $429 million in losses associated with romance scam victims who

reported the use of investments and cryptocurrencies.3 4

Case study - Zelle Digital Wallet Takeover

Bruce Barth was hospitalized in 2020 with COVID and his phone disappeared from his

hospital room. Soon after his Zelle account was used to conduct three transfers totaling $2,500.

They additionally withdrew cash from an ATM and used his credit card with all accounts being

at Bank of America. Although he was able to get refunds for his credit card and cash losses after

filing a fraud report, Bank of America denied his claims for Zelle refunds. Even though Barth’s

phone was stolen, since the transactions were validated by authentication codes sent to a

phone under the account, they claimed the Zelle transactions were authorized. After filing

grievances through a variety of agencies, Barth eventually received refunds for the Zelle

transactions after the New York Times contacted Zelle. This case exemplifies how difficult it is

for customers to receive refunds on fraudulent Zelle transactions.

3

9

Most Exploited Elements of Financial Technologies

Financial Technology (“FinTech”) is a term used to describe the use of software, mobile

applications, and other technological tools to improve and automate the delivery of financial

services to business entities and consumers to more efficiently manage their finances. In its

infancy, FinTech involved primarily the implementation of technological advances and

improvements to update and enhance existing functions and services provided to consumers

and businesses without challenging the underlying business models.

1

In the last decade, FinTech has shifted to become more revolutionary and disruptive to

the underlying business models of many different industries including banking and capital

markets. Instead of focusing on improvements, FinTech companies are redesigning the

process of delivering financial services to customers using cutting edge technologies. FinTech

has become so disruptive that it has created new business infrastructure, products, and

services.

While Fintech has grown rapidly in the last decades and offers a lot of advantages such

as ease, adaptability, faster service, substantial reduction in costs, expanded access to

investment opportunities, it also presents a number of challenges and areas that are prone to

exploitation. Data privacy, information security, consumer protection, cybersecurity, and

financial protection are all areas that are subject to exploitation. First let’s examine the

different types of Fintech services available to customers.

Different Types of FinTech

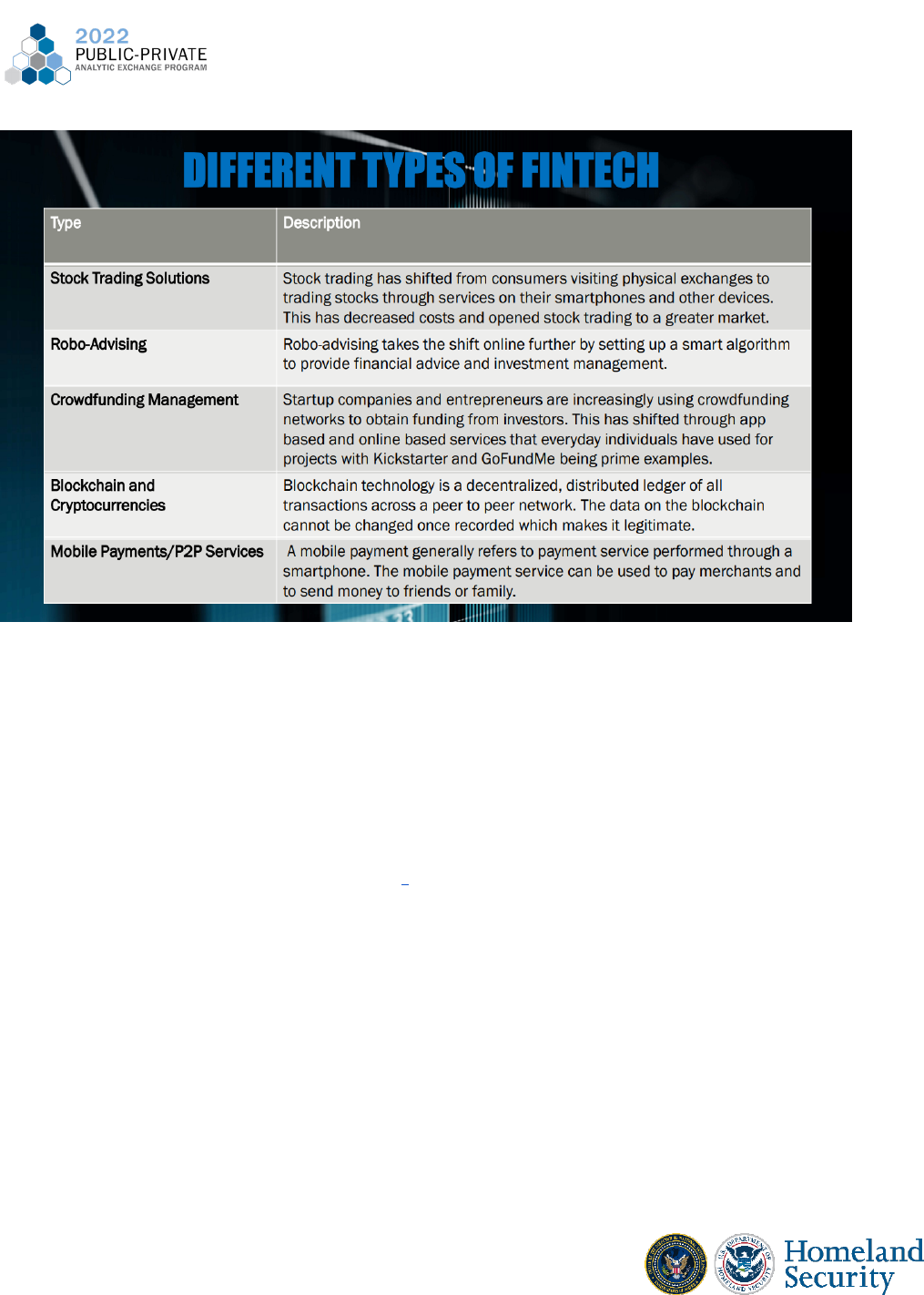

FinTech companies focus on employing technology to enable, enhance, and disrupt

financial services. FinTech companies provide a wide range of services such as stock trading,

robo-advising, crowdfunding platforms, blockchain technology and cryptocurrencies, as well as

mobile payments and P2P services . The increased use of smartphones and ease of conducting

transactions electronically, have been central to the adoption and growth of the multitude of

FinTech products and services by everyday consumers.

10

Stock Trading Solutions

One of the services offered by FinTech companies is stock trading. The traditional

method that investors used to buy or sell stocks was to physically visit an exchange. Stock

trading FinTech companies have revolutionized the industry by allowing investors to easily

trade stocks using their smartphones or other portable devices. Furthermore, the low cost of

these stock trading solutions have made them even more attractive to consumers. According

to Bankrate, the top five Stock trading companies in 2022 are Charles Schwab, Fidelity

Investments, TD Ameritrade, and Robinhood.

2

Robo-Advising

Robo-advisors are digital platforms that provide automated, algorithm-driven financial

planning services with little to no human supervision. A typical robo-advisor asks questions

about your financial situation and future goals through an online survey; it then uses the data

to offer advice and automatically invest for you. Robo Advisors have disrupted the wealth

management industry by providing access to investment management at a fraction of the price

a typical financial advisor might charge. As such, wealth management has now become

accessible to consumers who could not afford it in the past. A Morningstar Inc. analysis of 16

robo-advisors rated the products offered by Vanguard Group and Betterment as the best

11

overall options to help investors achieve their financial goals. The two rose to the top of the list

thanks to their “low cost, transparency, reasonable asset allocation approach and broad range

of financial planning tools,” the report said.

3

Crowdfunding Management

Fintech has enabled startups, self-employed entrepreneurs, and individuals or groups of

individuals to obtain funding from investors through the use of crowdfunding. Crowdfunding

networks allow users to receive or send money online or via mobile apps. While crowdfunding

is often used by businesses to raise equity, the funds have also been used to fund other

projects such as travel, funeral, wedding, medical expenses, and other bills. Kickstarter and

GoFundMe have both successfully funded millions of pledges and raised funds.

Blockchain Technology and Cryptocurrencies

A blockchain is a distributed database that is shared among the nodes of a computer

network. As a database, a blockchain stores information electronically in digital format, in

blocks that are then linked together via cryptography. As new data comes in, it is entered into

a fresh block. Once the block is filled with data, it is chained on the previous block, which

makes the data chained together in chronological order. Different types of information can be

stored on a blockchain, but the most common use so far has been as a ledger for transactions.

Blockchain technology is regarded as one of the biggest innovations of the 21st century

as a result of its wide range of application to various sectors from financial to manufacturing, as

well as education. Blockchain Technology was first introduced in 1991 by two researchers,

Stuart Haber and W. Scott Stornetta who were working on a project that would implement a

system where document timestamps could not be tampered with. In 1992, the system was

upgraded to incorporate Merkel trees that enhanced efficiency which allowed the collection of

more documents on a single block.

In 2009, Blockchain technology gained popularity and relevance by Satoshi Nakomoto, a

pseudonymous person or team who outlined the technology in a whitepaper and

conceptualized the development of bitcoin, the first application of digital currency. In the

Whitepaper, Nakomoto proposed bitcoin as “A purely peer-to-peer version of electronic cash

that would allow online payments to be sent directly from one party to another without going

through another financial institution. Digital signatures provide part of the solution, but the

main benefits are lost if a trusted third party is still required to prevent double-spending. We

propose a solution to the double-spending problem using a peer-to-peer network. The network

12

timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work,

forming a record that cannot be changed without redoing the proof-of-work.”

Bitcoin is the first application and most popular type of digital or cryptocurrency built on

blockchain technology. Cryptocurrency is decentralized meaning any two people, from

anywhere in the world, can send cryptocurrency to each other without the use of a financial

institution or government entity. Cryptocurrency transactions are tracked on the blockchain, a

distributed ledger that allows the storage of all information in a secure and accurate manner

using cryptography. Once the information is stored on the distributed ledger, it cannot be

altered, deleted or destroyed.

In addition to monetary transactions such as cryptocurrency, blockchain technology is

also used in other sectors and industries. Blockchain technology is used by healthcare

providers to store their patients’ medical records. As a result, patients can have proof and

confidence that their medical records cannot be changed. Blockchain technology is also utilized

to facilitate, verify, and negotiate contract agreements using a computer code referred to as

smart contract. Blockchain technology is also used to record and track supply chains as well as

facilitate voting systems.

Mobile Payments/P2P Services

FinTech companies offer mobile payment services for both peer to peer and merchant

payment transactions. A mobile payment generally refers to payment service performed

through the use of a portable electronic device such as a tablet or cell phone. The mobile

payment service can be used to pay merchants for goods and services, but to also send money

to friends or family through mobile applications such as Paypal, Zelle, and CashApp.

13

Exploited Elements of FinTech

Data Privacy and Security

Data privacy and information security are the top concerns for consumers of Fintech.

The increase of online and phone banking services have provided fintech companies access to

tremendous amounts of data about customers and visitors, which can be exploited and

analyzed to generate insights about consumer behavior, interests, networks, and personalities,

but also makes the data more susceptible to security breaches. According to PwC’s Global

FinTech Survey 2016, almost 56% of the respondents identified information security and

privacy as threats to the rise of fintech.

4

As more services go online, data privacy and security,

are proving to be a major challenge for fintech as consumers are becoming more concerned

with how their data are being exploited by enterprises for business and marketing decisions

and the security of their data in terms of who ultimately have access to such datam legally or

illegally.

14

Case Study: Equifax Data Breach

In September of 2017, Equifax announced a data breach that exposed the personal

information of approximately 150 million people. The company agreed to a global settlement

with the Federal Trade Commission, the Consumer Financial Protection Bureau, and 50 U.S.

states and territories. The settlement amount was approximately $425 million to help people

affected by the data breach. In February 202, the U.S. government indicted four members of

China's military on charges of hacking Equifax to exploit the personal data of 150 million

Americans. They allegedly conspired to hack into Equifax's computer networks, maintain

unauthorized access to those computers, and steal sensitive, personally identifiable information

of nearly half of all American citizens.

5

Fraud and Money Laundering

While many customers are choosing Fintech banking over traditional banking for the

ease of use, competitive prices and better quality of service, others are making the choice

because a fintech bank account provides easy access to a bank account and payment card in a

matter of minutes with minimal KYC requirements. In fact, the emergence of Fintech banking

has allowed individuals to open up multiple bank accounts without proof of residence or

salaries providing them greater access to launder illicit funds in countries where KYC regulations

are minimal or nonexistent. As a result, Fintech firms have inadvertently facilitated financial

crimes by illicit actors and money launderers.

Case Study: Wirecard Money Laundering Scandals

Since June 2020, in Germany, a serious financial scandal involving the online payment

company Wirecard is underway, after the discovery of a shortfall of 1.9 billion euros which was

thought to be deposited as trust funds in two banks in the Philippines but which never existed.

The former Wirecard’s CEO has been arrested in Germany on suspicion of fraud, while his

former CEO has disappeared after fleeing the country. In addition to this fraud, according to

the Financial Times, Wirecard processed payments for a Maltese online casino which was later

accused of laundering money for a powerful member of the ’Ndrangheta, one of Europe’s most

dangerous mafia organizations. Wirecard processed payments for CenturionBet, a Malta-based

gaming company that was later found by Italian courts to be an ’Ndrangheta way for moving

money out of the country in a sophisticated money laundering operation. Wirecard continued

to trade with CenturionBet, which was incorporated in Malta but owned by a Panamanian

company, until 2017 when its gambling license was suspended by the Maltese authorities and

15

ceased trading after an anti-mafia raid that saw the arrest of 68 people. Since then over 30

people have been convicted of mafia related crimes. CenturionBet’s revenues included only a

fraction of Wirecard’s global operations, but the discovery raises further questions about the

German company’s business model, once deemed to be a pioneer of European fintech. As a

regulated payment institution, Wirecard is required to abide by the strict anti-money

laundering rules and report suspicious transactions to the competent authorities. Wirecard also

processed payments for another larger Maltese gambling company that has been investigated

by the Italian authorities for money laundering for organized crime groups. It is possible that

Wirecard was unaware of the company’s alleged ties to organized crime.

6

Case Study: Coin Ninja Money Laundering

In February 2020, the U.S. federal government arrested Larry Harmon, CEO of the Coin

Ninja media platform and founder of the DropBit cryptocurrency wallet. In particular, Harman

was accused of conducting money laundering activities and running a business for the exchange

of funds without a specific license from FinCEN. According to the arrest warrant filed in early

February 2020, Harmon would have laundered over 354,468 Bitcoin (BTC), equivalent to

approximately $311 million at the time of the transaction, allowing users of Helix and Grams,

respectively, a privacy and privacy tool, a dark web search engine, to transact on AlphaBay, a

very popular dark market but closed in 2017. In 2021, Harmon pleaded guilty today to a money

laundering conspiracy arising from his operation of Helix.

As part of his plea, Harmon also agreed to the forfeiture of more than 4,400 bitcoin,

valued at more than $200 million at the time of his plea deal, and other seized properties that

were involved in the money laundering conspiracy. Harmon is expected to be sentenced at

later date and faces a maximum penalty of 20 years in prison, a fine of $500,000 or twice the

value of the property involved in the transaction, a term of supervised release of not more than

three years, and mandatory restitution.

7

Hacking and Ransomware

Also, Fintech companies are susceptible to cybercrime such as hacking and ransomware

which have become a growing problem for both the private and government sector lately.

During ransomware attacks, criminals deploy malicious software that encrypts a victims’ files

and renders its systems unusable and the data unusable. The attackers then issue a ransom

demand, oftentimes in cryptocurrency to allow remote and anonymous payment that cannot

be easily traceable to them. The attackers then promise that if they receive the ransom, they

will provide the victims with a key to decrypt their systems and data but that is not often

guaranteed.

16

Ransomware has become a major problem as a result of the emergence and acceptance

of cryptocurrencies. Ransomware has also become a national security threat of the United

States and various other countries around the world. Private companies including Fintech are

also subject to becoming victims of hacking and ransomware attacks to steal customers’ data

and money, and cripple their systems.

Case Study: Binance Ransomware

On August 6, Malta-based cryptocurrency exchange Binance became the victim of

ransomware when attackers demanded 300 bitcoin, the equivalent of approximately $3.5

million at the time in exchange for a Know Your Customer (KYC) database containing the

personal information of around 10,000 users. The KYC database allegedly contained personal

identification information and photographs of users with documents like passports. The

company contested the authenticity of the documents, claiming that they lacked digital

watermarks, refused to pay the ransom, and contacted law enforcement for assistance in

pursuing the attackers.

8

Legal & Technological Vulnerabilities

The name cryptocurrency is somewhat of a misnomer. For all intents and purposes, it is

not truly a currency, has no inherent value beyond what its investors are willing to pay, and has

no government or central agency to back up its value or insure deposits. Eventually, the US

government will have to make a determination of how to classify cryptocurrency to establish

regulations and enforcement jurisdiction. The Security and Exchange Commission (SEC)

considers it a security, the US Commodity Futures Trading Commission (CFTC) considers it a

commodity, and the Comptroller’s Office of the Currency considers it a currency.[i] Depending

on how cryptocurrency is eventually categorized, this will determine which agency has

jurisdiction over this technology, how to regulate it, how to tax it, and how to enforce

regulations. Currently, the Department of Justice (Justice) has taken on most of the public

responsibility for recovering stolen assets in terms of cryptocurrency while other actors

involved in these investigations have been the SEC, the Department of Homeland Security,

Cyber Command, the National Security Agency, and the Internal Revenue Service. The main

issues that the USG and global law enforcement agencies face are jurisdiction and regulations

and reporting requirements. The US Treasury has jurisdiction over any transaction that involves

the US dollar because the US government has given the Treasury that power through the Office

of the Comptroller of the Currency (Office of the Comptroller).

1

However, cryptocurrencies,

because they are decentralized and have no overarching jurisdictional power or issuer with the

exception of the miner or the developer, have no such overreaching authority. The

17

transnational nature of the blockchain and a lack of residency confuse any jurisdictional

arguments. However, the SEC has been making steps in the direction of considering

cryptocurrencies securities, such as in the case of Ripple (XRP). In December 2020, the SEC

brought a lawsuit against XRP stating that the Initial Coin Offering (ICO) was an “unregistered

securities offering” raising $1.3billion through sales. By considering XRP as a security rather

than, as Ripple’s issuers argued, a currency, the SEC claimed jurisdiction over the token rather

than the Office of the Comptroller under Treasury.

2

The SEC considers cryptocurrencies as

securities and applies securities law to digital wallets and exchanges, while the CFTC considers

Bitcoin, specifically, a commodity and allows cryptocurrency derivatives to trade publicly.

In the United States, cryptocurrency exchanges and trading is legal, though inadequately

monitored or regulated. Cryptocurrency exchanges fall under the regulatory aegis of the Bank

Secrecy Act (BSA) and must register with the Financial Crimes Enforcement Network (FinCEN).

Under the BSA, they are considered money service businesses and must implement an Anti-

Money Laundering/Counter Financing of Terrorism (AML/CFT) regime, maintain records, and

submit reports to the proper authorities. However, the US Treasury has no jurisdiction over

exchanges that are not registered in the US or those that choose not to comply with AML/CFT

practices. The Internal Revenue Service (IRS) wants increased ability to request cryptocurrency

transactions at exchanges and brokers, presumably for tax purposes, while FinCEN has

proposed reporting requirements for accounts that exchange over $10,000 per day and KYC

requirements on international transactions similar to banking institutions and money service

businesses (MSB). Money service businesses like EBay and PayPal come under the jurisdiction

of the Treasury because of the type of transactions they enable in the US dollar. One of the

main issues authorities face with regulation is how to get exchanges to agree to

standardization, anti-money laundering (AML) practices, and oversight. In the United States,

several state governments have proposed or passed laws affecting cryptocurrency and

blockchain technology, lacking any overarching legislation on the federal level. While there is

no uniform definition of cryptocurrency, virtual currency, digital assets, cryptoassets, or crypto,

states have largely approached legislation toward a broad definition to encompass the entire

asset class.

3

Legal regulations worldwide vary and are largely inconsistent between jurisdictions. In

the United States, the White House released an Executive Order committing to taking part in

research on cryptocurrencies in a “whole-of-government approach to addressing the risks and

harnessing the potential benefits of digital assets and their underlying technology.”

4

On the

international level, the Financial Action Task Force (FATF) has made progress releasing guidance

on Virtual Asset Service Providers (VASPs). The FATF stated that VASPs are subject to the same

relevant standards that cover more traditional financial entities and that countries should

18

assess and mitigate risks associated with virtual asset financial activities and providers, to

include licensing, registering, and monitoring.

5

In response to FATF guidance, FinCEN clarified

that it expected cryptocurrency exchanges to comply with the Travel Rule, proposing that

exchanges must collect, retain, and transmit certain information related to funds transfers and

transmittals of funds over $250 for international transactions and $3000 for domestic

transactions. It further stated that these rules apply to convertible virtual currencies, to include

any transactions involving digital assets with legal tender status.

6

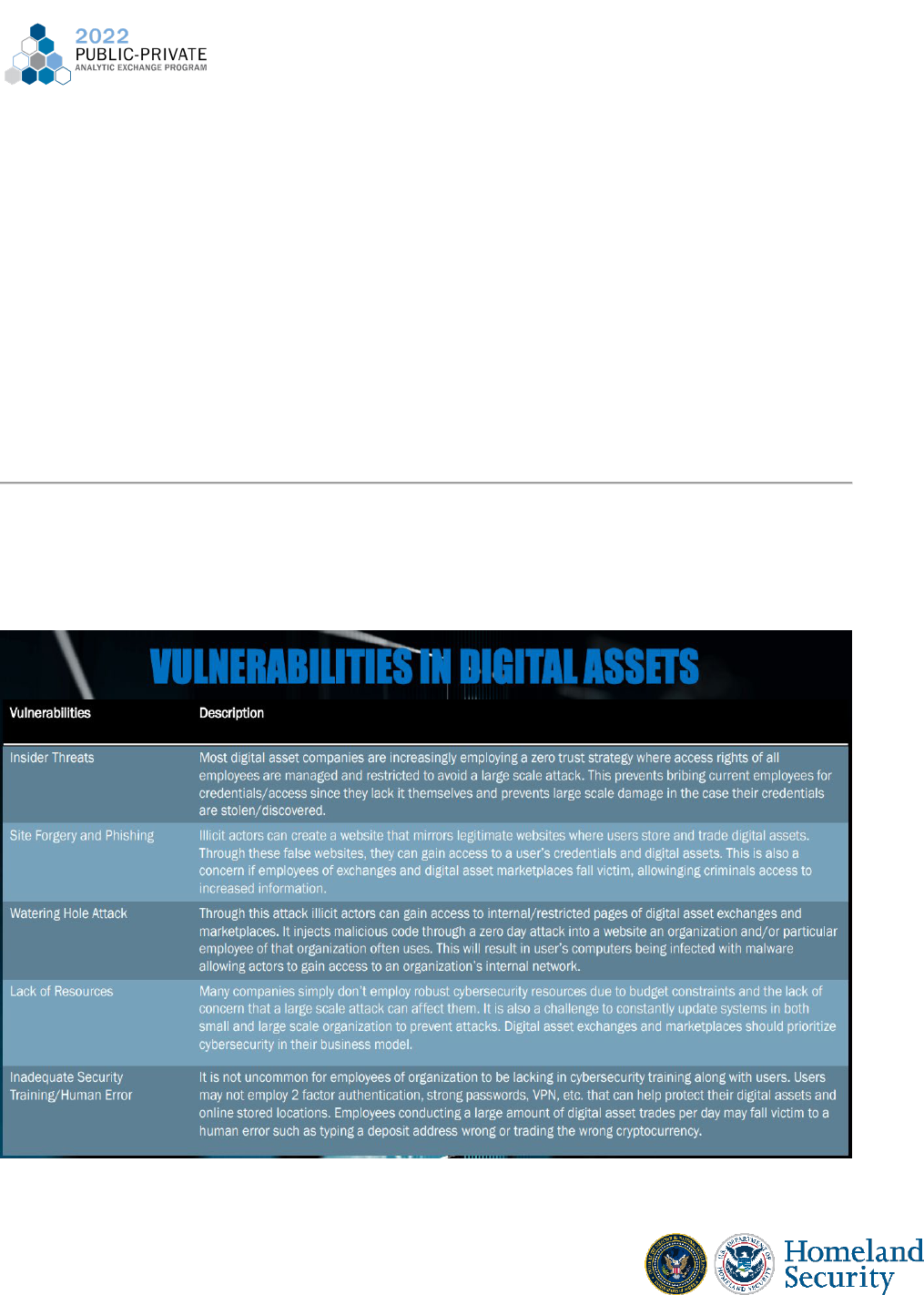

Technological Vulnerabilities

19

Blockchain technology has been advertised as sound but under certain conditions, has

specific vulnerabilities mostly due to human error, the economics of the blockchain, or the

code. A majority of the weaknesses of blockchain technology comes in the forms of mistakes in

account security, fraud, scams, hacking, ransomware, and a lack of resources for adequate

security protections. Account Security is a vulnerability for both the individual user and

cryptocurrency exchanges and platforms. The most common weaknesses for exchanges and

platforms include phishing, missing wallet protections, weak login credential protections in

addition to software vulnerabilities and transaction manipulations. For individual users, the

most common weaknesses include phishing, poor wallet security, fraud, and scams.

Wallets/Accounts: Inadequate protection of account passwords to include two factor

identification, private keys, and seed phrases are one of the most common vulnerabilities to

account security. These represent the most common way an individual’s account or systems’

platform is accessed by an unauthorized entity.

Fraud/Scams: A variety of scams or frauds to induce users to invest money or allow access to

their cryptocurrencies have proliferated in recent years. These can run anywhere from ‘pump

and dump,’ fraudulent websites or coins, rug pulls, romance schemes, giveaways, ponzi

schemes, or celebrity endorsements.

Social Engineering/Phishing: Social engineering to obtain access to account passwords, keys,

seed phrases, or other sensitive data involves inducing victims to download malware onto their

computers or networks, allowing outside access. The five types of social engineering methods

are phishing, pretexting, baiting, quid pro quo attacks, and tailgating.

Inadequate Resources/Security:

Cross-Blockchain Interoperable Bridge: The bridge that enables users to transfer digital assets

from one blockchain to another has recently been the target of several attacks to exploit these

technical weaknesses. The Poly Network attack in 2021 resulted in theft of approximately $610

million in digital assets, locking up nearly $1 billion across the entire network. The recent attack

on the Ronin Network, with a reported loss of over $625 million in assets attacked the

Ethereum-linked bridge the network used to execute transactions for the game, Axie Infinity, to

transfer assets in and out of the Ronin network for use in the game. The attackers managed to

get control of four of the nine validator signatures needed to access the system held by the

parent company, and backdoor access to a centralized server to obtain the final required

signature to validate transactions.

20

51% vulnerability attacks: Blockchains that use proof-of-work as their protocol for verifying

transactions are susceptible to manipulation if an individual or pool of miners is able to gain

control of a majority of a network’s mining. The miners or pool of miners could potentially

change blockchain information by reversing a transaction, allowing double-spending by creating

a fork in the blockchain. These types of attacks usually occur on smaller coins where gaining

control of the majority of a network is much easier than on larger blockchains such as Bitcoin.

Routing Attacks: Blockchains rely on large real-time data transfers to communicate and execute

transactions, which are vulnerable to hacking. Hackers are able to hijack IP prefixes to intercept

data transfers, reroute traffic to hacker-controlled destinations, or drop connections to prevent

consensus and confirmation of transactions.

[i] SoFi. 27 April 2021. SoFi.Com. “Is Crypto a Commodity or Security.” Accessed 9 February 2022.

https://www.sofi.com/blog/crypto-commodity-vs-security/

21

Pseudo-Anonymity and Weaknesses in KYC

Pseudo-anonymity is a key factor in propelling the use of cryptocurrencies and other

emerging digital assets for illicit purposes. Bitcoin is the original catalyst for this element due to

its pseudo-anonymous nature. A person’s identity is tied to a fake name or pseudonym in using

bitcoin which serves as their public key and bitcoin address. Bitcoin has never been truly

anonymous because all transactions are available on the public network leaving anyone easily

being able to see records of all transactions a bitcoin address has conducted. It is up to the

bitcoin address holder to prevent their actual identity from being linked to their pseudonym in

bitcoin. As other cryptocurrencies have emerged the same principles have applied in that they

provide pseudo-anonymity and a means for people to make transactions that aren’t under their

true identity. As we’re entering a new phase of digital assets, they are taking it a step further by

providing complete anonymity or near complete anonymity which is discussed with Monero

and NFTs in a later section. However it has largely been a misconception that cryptocurrencies

are completely anonymous and even with their pseudo-anonymous nature, illicit actors have

not been able to hide from authorities.

Case Study - FBI $3.6 Billion Bitfinex Seizure

A recent seizure from the FBI that demonstrates the pseudo-anonymous nature of

Bitcoin and how it can ultimately be traced back to a person is the $3.6 billion bitfinex seizure.

Married couple Ilya Lichtenstein and Heather Morgan were charged with conspiracy to commit

money laundering and conspiracy to defraud the U.S. They were charged after years of

investigating by the FBI as to the source of a 119,754 Bitcoin theft from the cryptocurrency

exchange Bitfinex where the proceeds were placed into a single crypto wallet. The money

remained in that wallet largely untouched for years; however once the currency started to

move out of that wallet and into traditional bank accounts, the transactions were able to be

traced to Lichtenstein and Morgan. Although the couple was careful to evade authorities for a

long time, they were ultimately caught due to the public nature of the blockchain and any

errors in hiding their identities being a permanent feature on the blockchain. The couple did

utilize a few different dark web currency exchanges including Hydra and Alphabay that allowed

them to still conceal their identities while moving funds. However these services has since been

shut down by law enforcement and in this case Alphabay’s internal logs allowed law

enforcement to link the wallet in the Bitfinex hack to the laundered accounts. Ultimately once

law enforcement was granted access to Lichtenstein’s cloud storage account, they found a list

of wallet addresses linked to the hack and were able to seize the funds. This case exemplifies

how most cryptocurrencies aren’t truly anonymous and the difficulty in concealing a large

amount of illicit funds generated in illicit activity. Criminals will likely use these illegal exchanges

22

and make large scale purchases through traditional accounts allowing them to be discovered by

law enforcement.

4

Case Study - Miami Feds $34 Million Crypto Seizure

Another recent bitcoin seizure which demonstrates the pseudo-anonymous nature of

the currency but ultimately how it can be tied to someone’s true identity is the joint federal

seizure between the FBI, IRS, and HSI of $34 million from a Miami resident. The unnamed

Miami resident is accused of using numerous anonymous identities on the dark web to carry

out fraudulent online transactions between 2015 and 2017. The accused person is suspected of

selling people’s account information that had been hacked from popular services such as HBO,

Netflix, and Uber. Authorities did not have enough evidence to pursue a criminal case so they

pursued a civil case to seize his cryptocurrency. The suspect additionally used tumblers to

conceal the movement of his funds. This seizure and civil case illustrates that bitcoin and other

cryptocurrencies do not provide a complete anonymous nature.

5

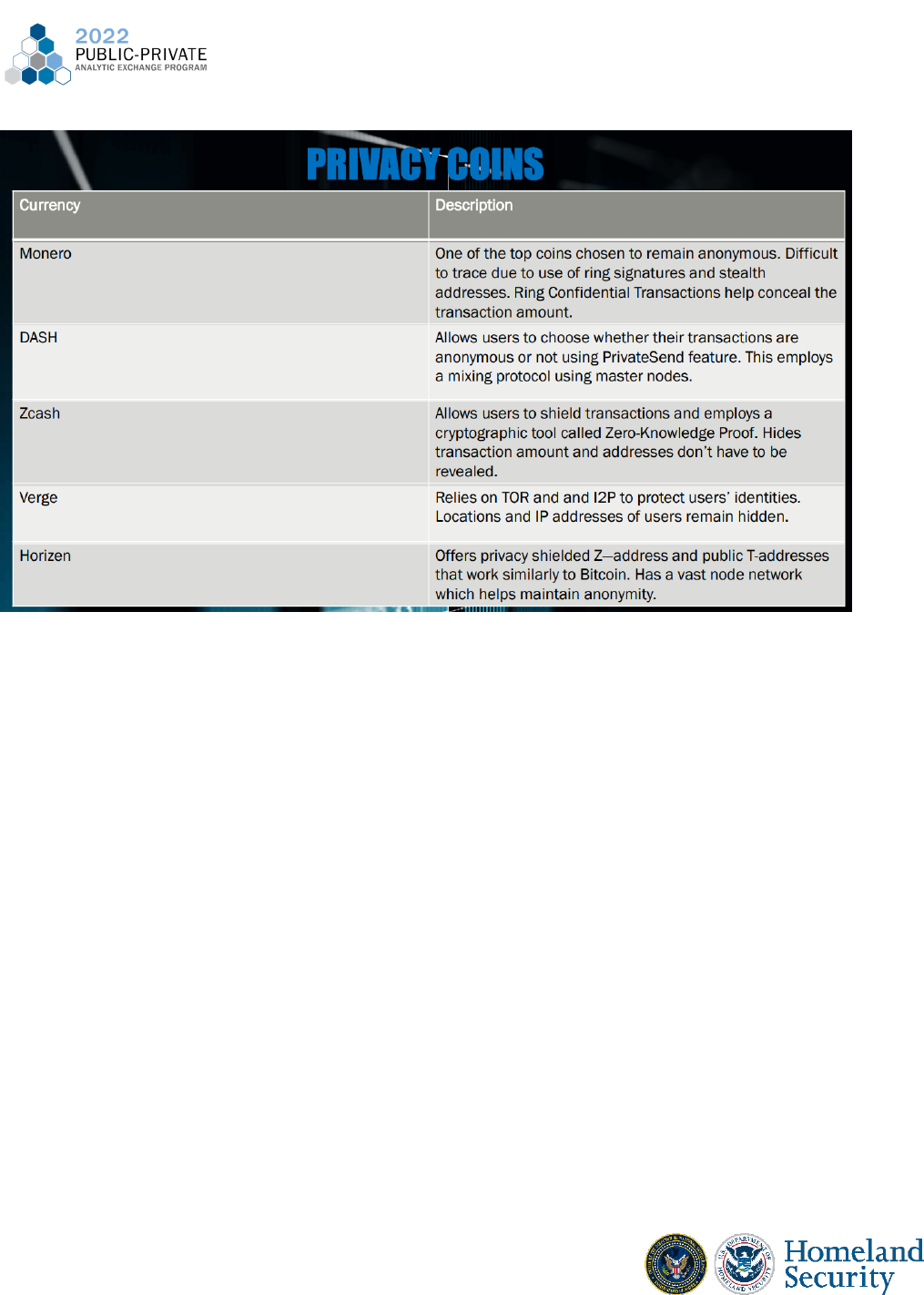

Group Research Task: Privacy Coins & How They Maintain Anonymity

Pseudo-anonymity is becoming harder to maintain due to the emergence of privacy

coins. There are a variety of privacy coins available to consumers to maintain complete

anonymity in online transactions. Our group looked into some of the most popular privacy coins

that are expected to continue to grow and that open the door for further illicit activity by

criminals.

23

Know Your Customer requirements are another important aspect to consider in

cryptocurrency exchanges and digital asset marketplaces that ties directly with the element of

pseudo-anonymity. Although KYC requirements are strongly guarded in the financial institution

industry, when it comes to the emerging digital asset realm there are vast differences among

marketplaces. Some contain the same KYC requirements as traditional financial institutions

including proof of identity with a photograph and proof of address while some just require an

email address upon registration and nothing more. The lack of KYC requirements in

cryptocurrency exchanges and digital asset marketplaces has attracted more illicit actors over

traditional financial institutions. Although the US Treasury is declaring all US crypto exchanges

must register with FinCEN as a Money Service Business, not all have registered yet. This also

only applies to US based exchanges which is only a fraction of the exchanges that exist

worldwide. This will continue to be an obstacle for directly tying someone as an owner of an

account or wallet if the exchange is based in another country and does not require any KYC

upon account registration. It is also important to keep in mind that even though crypto

exchanges are becoming more regulated and more attention is being focused on them, other

digital assets like NFTs remain largely unregulated. FinCen has only released some guidance

that NFTs may be subject to FinCen regulations however there are no concrete regulations yet.

This will likely change as they become more commonly used but it will still be an uphill battle in

attaching regulations to the assets and ensuring that customers are submitting the right

24

identification when purchasing these assets. CipherTrace released a report that ⅓ of the top

120 exchanges have weak KYC requirements.

6

There are multiple obstacles towards implementing KYC requirements in crypto

exchanges and online marketplaces. Firstly, they add increased expenses to these emerging

institutions. It is costly to add increased verification processes, registering with regulatory

bodies, and adding large compliance teams to adhere towards more KYC policies. Secondly,

customers would prefer to use exchanges and marketplaces they can quickly register on rather

than waiting a week or longer for their verification process to be complete. This makes it more

enticing for exchanges to not have a comprehensive verification process so they don’t lose out

on customers who want to register quickly. Another factor are the security implications that

come with storing personal information of users. Over the last decade we’ve seen numerous

large scale data breaches where customer PII has been leaked. It is common for exchanges to

use third party verifiers and there is precedent for these verifiers being leaked, PII being

compromised, and hackers demanding ransom for the “safe” return of the PII. The more KYC

collected, the more responsibility is placed on exchanges and marketplaces. Overall given

current regulations and the promise of more regulations in the future, marketplaces will likely

struggle to properly meet KYC demands. Current and emerging digital asset marketplaces in the

US should all at least have the baseline KYC of photo identification and proof of address to

prevent illicit activity.

7

Improper KYC directly ties in with pseudo-anonymity because anonymous user accounts

are more likely to be used for money laundering and terrorist financing. It also increases the

risk of identity theft crimes and false identities being used as owners of digital assets. One of

our group’s original research tasks included registering under different exchanges and seeing

what kind of KYC factors they implemented. This allowed us to compare and contrast how

exchanges were adhering to KYC protocols and which ones consumers should feel comfortable

using.

Group Research Task: Registering Under Different Cryptocurrency Exchanges

Coinbase - Types of verification required include phone number, photo I.D., SSN, and

other personal details. Founded and based in the U.S., Coinbase is one of the longest standing

exchanges so it has well adapted to regulations over time. Contains different account limits

based on types of verifications tied to accounts.

Kraken - Verification required includes email address, full name, DOB, physical address,

employment info, and SSN. Similarly to Coinbase, this exchange was also founded and based in

the U.S. Contains different account tiers with different verification requirements.

25

Binance- Basic verification required includes name, address, and DOB with other tiers

requiring picture ID and proof of address. Regarded as the largest exchange by trading volume

and has its headquarters in the Cayman Islands. Originally it was based in China however due to

China’s increased regulation of cryptocurrency, it moved its headquarters to a less regulated

location. This exchange provides a great demonstration as to how increased regulations in the

U.S. may drive exchanges outside of the country and into locations with less regulations.

FTX- International exchange that has 3 levels of restrictions. Tier 1 does not require

legal documents but users must provide email, full name, DOB, phone jurisdiction ,country of

residence, and optional SSN. Tier 2 requires government ID, proof of address, description of

source assets, and facial verification which gives access to unlimited withdrawals. Specifically in

the US FTX unverified users can only explore the site, Tier 1 users are subject to $10,000 per

day, and Tier 2 users have full access

Kucoin- This exchange just required email and no other identifiers at sign up. However

users can partake in full ID verification through presenting a valid ID which will allow them to

increase withdrawal limits. This exchange is headquartered in the Seychelles (an island up north

from Madagascar) which, similar to Binance, gives them more freedom when it comes to

following exchange related regulations and compliance.

26

A key thing in common with the exchanges we investigated were that exchanges vary on

requirements depending on the location of the customer. US based users are subject to some

of the heaviest KYC requirements when comparing other requirements worldwide. Exchanges

have adapted to fit US requirements while still maintaining less restrictions in other locations.

Other exchanges we looked into included LocalBitcoins and and Local Monero which are unique

in that they provide direct transactions between parties, essentially cutting out the “middle

man”. These local services provide another unique avenue for illicit actors to engage in money

laundering and other criminal activity without leaving a trail to trace back to them. As KYC

factors become more enforced by US based exchanges, illicit actors will continue to use other

means bypassing typical exchanges to avoid being identified.

8

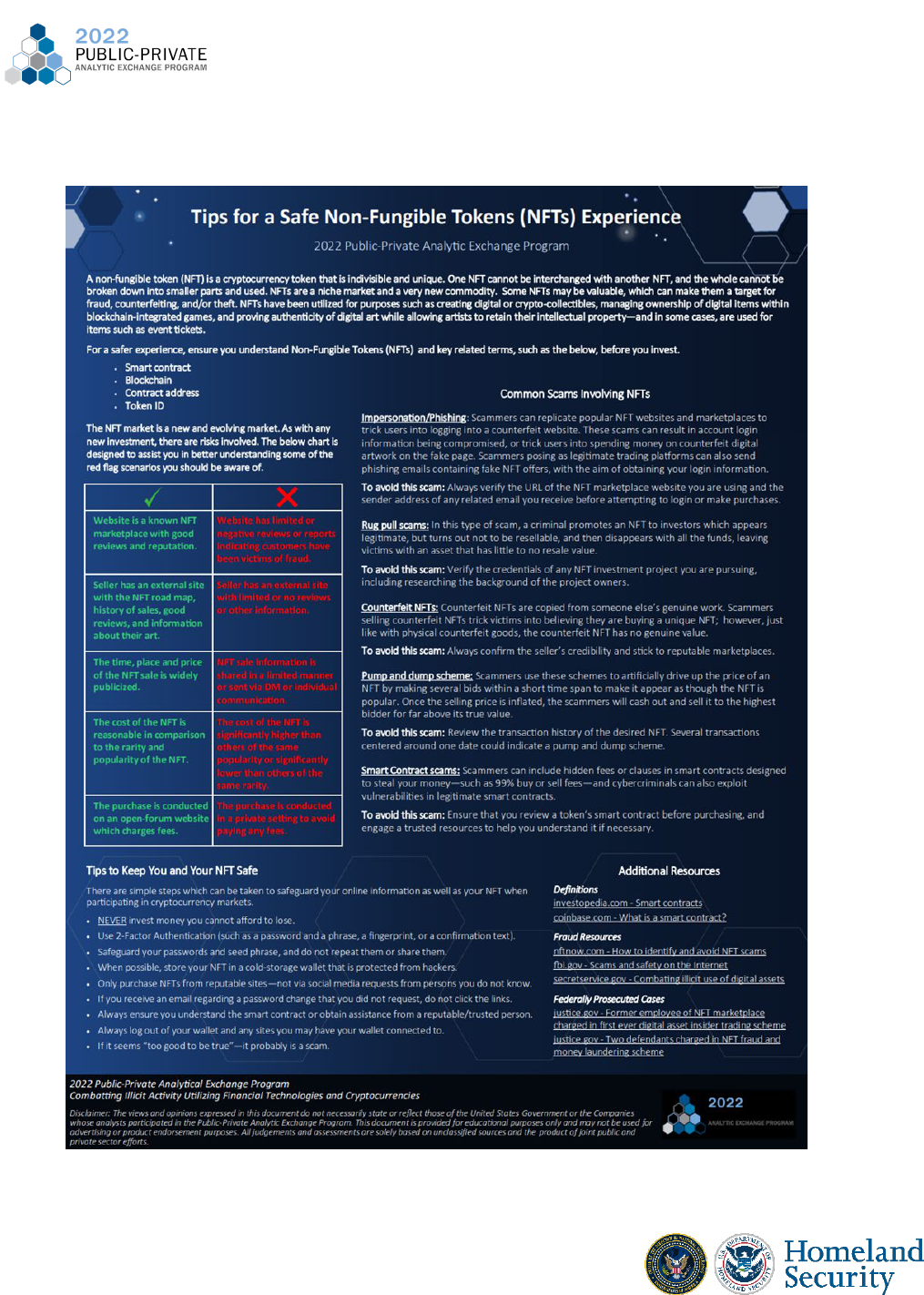

NFTs and Other Blockchain Applications Risk of Illicit Use

Other, emerging blockchain applications such as NFTs and digital payment services such

as gaming currency and P2P services present a great risk of illicit use. While these forms are just

starting to emerge in criminal cases, they have the potential for large-scale mis-use by illicit

actors. The first U.S. federal criminal case involving NFTs occurred in March 2022 and provides a

great case study into how this class of digital assets can be misused.

Case Study - NFT “Rug Pull Scheme”

Ethan Vinh Nguyen and Andre Marcus Quiddaeon were both arrested in Los Angeles in

March 2022 after they were charged with conning buyers of NFTs worth 1.1 million. They were

charged with both wire fraud and conspiracy to commit money laundering after issuing a set of

NFTs known as “Frosties”. The purchasers of “Frosties” were supposed to be eligible for

exclusive hodler rewards including early access to a meta verse game and giveaways. These

types of NFTs which offer special bonuses are specifically known as utility NFTs. Nguyen and

Quiddaeon subsequently ditched the project after selling out just hours after launching and

transferred the money earned from the sales of the NFTs to multiple cryptocurrency wallets

under their control. They started their project under pseudonyms which further demonstrates

the pseudo-anonymity involved in online blockchain applications. Criminals can hide behind

online identities while promoting their NFTs and ultimately perform a “rug pull” leaving any

investors defrauded.

9

Another interesting case study that exemplifies the volatility of NFT rates and exactly

what they could go for is the sale of an NFT of the first tweet from Jack Dorsey, who is a co-

founder and former CEO of twitter.

27

Case Study - NFT Sale of Jack Dorsey’s First Tweet

NFTs have the value of whatever the public is willing to pay for them which makes them

a volatile investment and an investment anyone should be cautious about. A prime example of

this is how crypto entrepreneur Sina Estavi bought the first tweet by Twitter founder Jack

Dorsey as an NFT for $2.9 million in March 2021. At face value that is already an enormous

amount for an NFT let alone an NFT of just a tweet. In March 2022 Estavi announced that he

would list the NFT for sale by auction and donate fifty percent of the proceeds to charity. Like

any investment, Estavi assumed the NFT appreciated in some value over the year. He expected

the NFT to at least net $25 million especially with the explosion of interest in NFTs. However

once the auction ended for the NFT the highest bid was only 0.09ETH which equates to

approximately $277 market rate at that time. Estavi told CoinDesk afterwards he may never sell

it but if he does eventually get a good offer, he may accept it. This serves as a cautionary tale

for all members of the general public interested in buying an NFT to take into consideration the

long term appreciation of the piece. This is still fairly new territory and although artwork has

shown a history of appreciating in value, it too has its volatile investment risks and NFTs can’t

be directly correlated to physical art. The amount of NFTs that can be produced is almost

limitless so it is likely we will see trends in the coming years of popular ones, such as the Bored

Ape Yacht Club, peaking to a high price and then decline.

10

28

Apart from trying to avoid any blatant NFT scams done by creators, hackers are

increasingly becoming skilled at exploiting vulnerabilities in these platforms. This is exemplified

by someone posting an NFT to OpenSea that contained malicious code. Users who clicked on

the NFT and accepted a gift from the hackers who had designed it would immediately have

their user balance cleaned out. OpenSea investigated this claim and did not find any victims and

claimed victims would have to provide a digital signature before someone would have access to

their funds. Although OpenSea updated its security warning and this vulnerability was

“patched”, crypto users soon reported on a similar scam. Hackers were able to discover another

vulnerability after this one was fixed. Consumers have to be careful with what NFTs they

purchase. They can easily be conned into purchasing a worthless NFT.

11

NFTs are currently not addressed by FinCEN due to their fairly new emergence on the

market. This follows the general art trend where art work has largely been unregulated and has

opened the door to a wide range of illicit activity, in particular money laundering. Although sites

like OpenSea can be registered as money service businesses and large sales can generate SARs

in the future, not all sites permitting the purchase of NFTs will likely ever be covered. FinCen

has only published guidance on how BSA and general regulations that apply to virtual currency

apply to NFTs. (citation) The “underground” art dealing community will always exist in both

physical and digital forms.

12

Another type of digital currency that has the potential for misuse is gaming currency.

One of the most popular games on the market today, Fortnite, has been discovered to be used

for money laundering in some capacity. Fortnite uses a currency known as V-bucks which serves

as in-game currency for players. A joint report issued by the Independent and Sixgill, a

cybersecurity firm, discovered Fortnite money laundering operations on a worldwide scale.

Criminals were using stolen cards to purchase V-bucks and would sell them discounted on the

dark web and auction websites such as Ebay. Sixgill discovered in 2018 there was more than

$250,000 raked in by Fortnite items on Ebay over a 60 day period alone. Epic Games has been

criticized for not doing enough to crack down on suspicious transactions within the game. This

raises the question and discussion of what risk indicators should gaming companies have in

place to monitor transfers of high value goods and players with a large amount of in game

currency.

13

Case Study - Squid Tokens and Smart Contracts

After the success of Netflix’s Squid Games, one scam arose as a play to earn game

modeled after the show. Squid tokens were sold by project leaders and rose nearly 23 million

percent in less than a week. However these tokens were governed by a smart contract which

29

every NFT is governed by. These smart contracts contain code which developers use to build

mini applets in. This code opens the door and potential for scams and malware. The smart

contract for Squid tokens forbade the sale of Squid tokens without burning a number of

Marbles tokens, which players earn in the game. This project was short-lived and fell apart after

a week, before the game launched, with the creators disappearing with the money and the

Squid tokens becoming worthless. Squid tokens remain to be unsold even as a novelty since

Marble tokens can’t be earned. These tokens will most likely remain in wallets of purchasers

forever. This case demonstrates the uncertainty and investment risks that come with

purchasing game related currency. These currencies will not always maintain their value and

the games could one day disappear leaving any in game currency worthless.

14

Case Study - Second Life and Linden Dollars

Second Life provides what can be arguably one of the first examples of widely used

gaming currency and how it can be potentially used illicitly. I was first launched in 2003 and had

around 1 million users at its peak with approximately 800,000 active users in 2017. This game

contained and largely revolved around the ‘Linden dollar’ which served as an in-game currency

to buy items, land, and even use at in-game casinos. Approximately $65 million was paid out to

Second Life users in 2018 for a variety of goods and services. This high amount of users and

money involved in the game obviously leads to the opportunity for illicit use to occur. A former

employee Pearlman spoke up about the issues plaguing the game and company claiming

compliance with anti-money laundering rules were not being properly followed. No KYC

information was being collected on any operators of the game while she was employed. Second

Life later added anti money laundering regulations but for well over a decade it allowed users

to remain pseudo-anonymous and move around money freely. Another concern of gaming

currencies that pertain to general consumers is the possibility for their in game currency to be

stolen and hacked. In 2007 the virtual banks of Second Life experienced multiple bank heists

which gave hackers a reported $3.2million in Linden Dollars. Although there have been

advancements in cybersecurity science then and games are generally more protected, there is

always the chance a vulnerability can be found and exploited by hackers. This is another

concern the general public should have when investing in virtual game currency. The game

might not always have the strongest security in place to prevent funds from being stolen and

unable to be recovered.

15

In addition to gaming currency, there is currently the development and implementation

of metaverses where people can live a virtual existence and by way conduct digital transactions.

This opens the door to a wide range of fraud and illicit activity purposes. Since this is such a

new space, there is not a current case study to analyze illicit activity that can potentially be

30

conducted. However this should be a concern for those developing these mataverses and they

should keep in mind the security implications when developing currency. Another rising

concern with NFTs and other emerging blockchain technologies is the idea to use them for

records including home ownership, medical, and general social media. Wallets in these areas

could open the door for personal data to be leaked and even deleted from the blockchain by

criminals.

P2P platforms such as Zelle and Square that provide digital payments solutions directly

between customers also host the opportunity for an increase in illicit use. These platforms

provide fast transactions directly between parties and the immediacy of transactions opposed

to a day or more wait at banks is very enticing to illicit actors. Although many banks employ

Zelle as a transaction solution, banks say returning money to defrauded customers is not their

responsibility. Regulation E, the federal law for electronic transfers, requires banks to only

cover unauthorized transactions. Most scams will trick people into making the transfers

themselves which loses them the opportunity to claim their money back.

16

Cash App is an emerging financial payment service that is seeing an increase in several

fraud schemes and illicit activity that can be expected from P2P services. Firstly multiple fake

cash app support schemes have emerged in which scammers are imitating customer support to

obtain PII and gain access to accounts. These support lines will ask customers to share their

screens or directly ask for account information to gain access. Secondly, Cash App does an

official sweepstakes called Cash App Friday which is often imitated. Fake accounts are created

on social media sites tricking people into thinking they won the sweepstakes and in turn asking

them to send a small amount of money to verify their identity. In turn they take the money,

block the user, and the user has no way of recovering their funds. Thirdly, Cash App does not

provide complete buyer protection which allows people to sell fake items through the app.

Consumers should use caution when making a purchase over Cash App for items like tickets

because once they send the money, the seller can vanish with the money.

Case Study - Cash App Phone and Sweepstake Scams

Charee Mobley fell victim to the customer support Cash App scam after using the

service during the covid pandemic as a quick means to pay bills and do online banking. After

noticing and online shopping charge on her account, she looked up a cash app support number

for assistance with her account. However this support number was fake and asked her to

download software which allowed them to take control of the app and drain her account.

Mobley was depending on the last $166 in her account to get her through the last two weeks of

August 2020. Another victim, Emily Bradford, fell for the sweepstakes scam. She received a

31

direct message through Twitter informing her that if she sent a clearance payment of $75 she

would receive a prize of $3,000. However as soon as she sent the money, the receiver

disappeared leaving her money gone. This demonstrates the small amount many lose due to

cash app sweepstake scams and how easily people can fall for it across multiple social media

platforms. It was reported by Sixgill that Cash App received about 10,577 posts on the DarkNet,

up 450 percent over the previous year, indicating illicit actors are keeping it in mind as a means

to engage in fraud. Square also implemented the option for people to transact in Bitcoin on the

app which has allowed money to be sent to anonymous addresses and more difficult to trace.

Illicit actors are constantly finding means to exploit these apps and there are many more victim

examples that exemplify the diligence needed by customers when utilizing these services.

Another new development of concern that was addressed earlier in this report are

mixers and tumblrs which mix streams of potentially identifiable cryptocurrency. These make

cryptocurrencies difficult to trace and improves anonymity of transactions making it another

ideal choice for illicit actors. Although actors can use single privatized cryptocurrency, mainly

Monero, to hide their identities there are still other currencies utilized in illicit transactions and

criminals will always have to find creative ways in covering these transactions.

Case Study: Larry Harmon and Helix

In August 2021 Larry Harmon pleaded guilty to conspiracy to launder money

instruments after it was discovered the bitcoin mixer he operated, Helix, was used to hide and

launder money. Harmon was originally arrested for operating Helix as an unlicensed money-

transmitting business and it was reported that more than $300 million in bitcoin was laundered

on the platform. Harmon admitted during his hearing that he colluded with several darknet

marketplaces inducing AlphaBay, Evolution, and Cloud 9 to provide Bitcoin money laundering

services to customers. This case again demonstrated how the transparent nature of the

blockchain allowed investigators to determine Harmon as the operator of the service and the

large amount of bitcoin he was earning from commissions of the service, which was valued at

over $300 million.

17

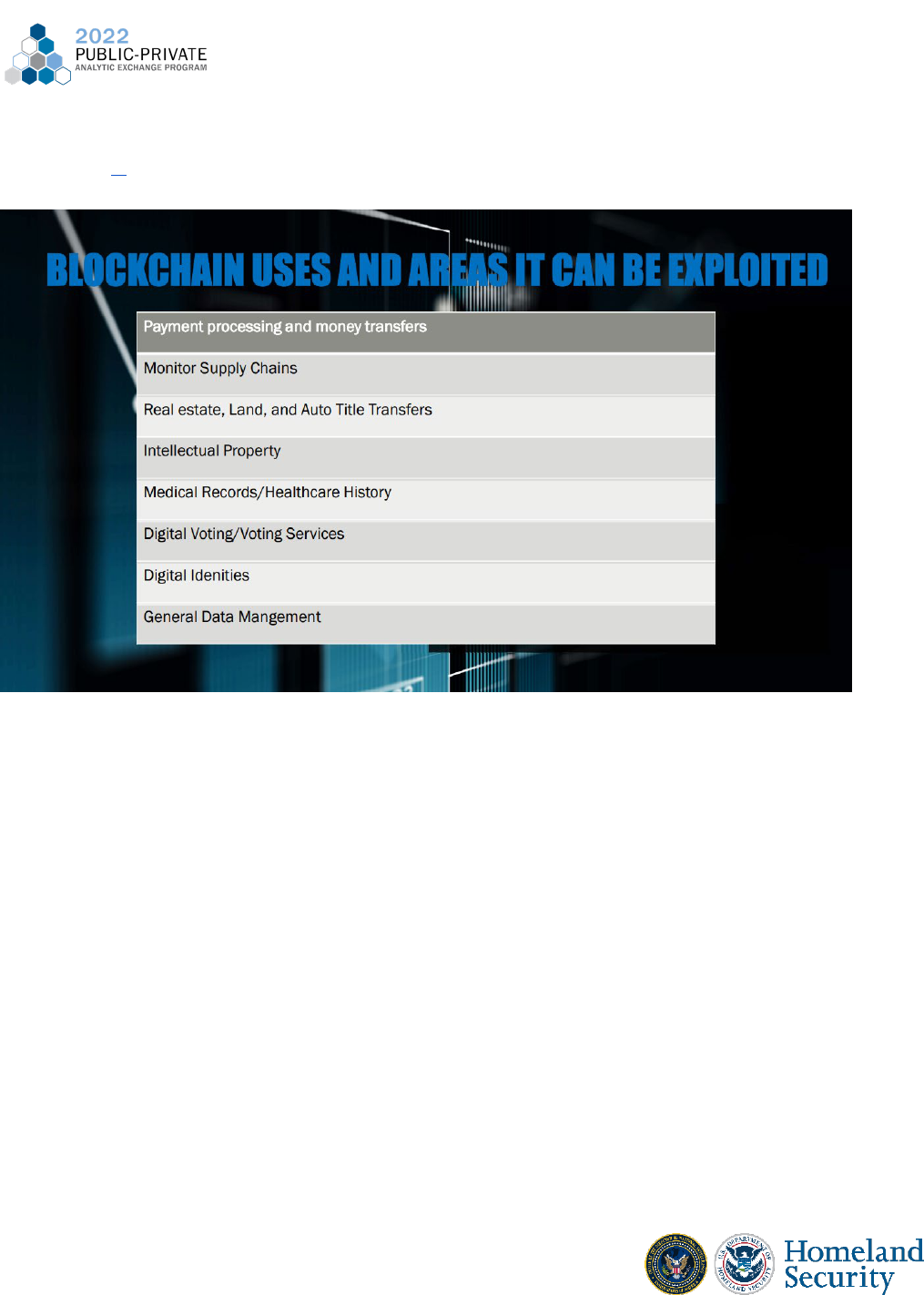

There are a variety of other uses centering on blockchains that have the potential to be

exploited in the future. Although payments processing and money transfers are the first use to

come to mind, there are a variety of uses for blockchain technology. Although this does come

with the benefit of making everyday actions more streamlined, it also comes with associated

risks of putting information online and vulnerable to exploitation. A future research project or

additional phase of this research could address the wide range of uses of blockchain

technologies and the positive and negative implementations it can have. Our group identified

32

some of the key areas that can adopt blockchain technology and potentially be exploited in the

chart below:

18

Key Findings & Recommendations

The most effective changes to reduce illicit activity in emerging financial technologies,

cryptocurrencies, blockchain applications, and other digital payments systems can be

implemented by both stakeholders and consumers. Stakeholders hold the power to implement

regulatory changes that can significantly reduce the opportunity for illicit activity. Consumers

hold the power to be knowledgeable users of cryptocurrencies and online payment platforms

to reduce the opportunities to be defrauded and scammed.

One of the strongest changes cryptocurrency exchanges and other digital payment

companies can implement are stronger KYC factors. Although cryptocurrency exchanges have

adapted more KYC elements, many platforms are significantly lacking any or may not even

possess any at all besides an email to sign up. Defi platforms especially have room for

improvement. As stated in the Chainalysis 2021 Crime Report “DeFi platforms allow users to

swap one type of cryptocurrency for another without a centralized platform ever taking custody

33

of the users’ funds. The lack of custody means that many DeFi platforms believe they don’t

have to take KYC information from customers, making it easier for cybercriminals to move

funds with greater anonymity.” Defi platforms don’t report on transaction activity as some

other platforms are required by the Bank Secrecy Act and other financial regulations.

19

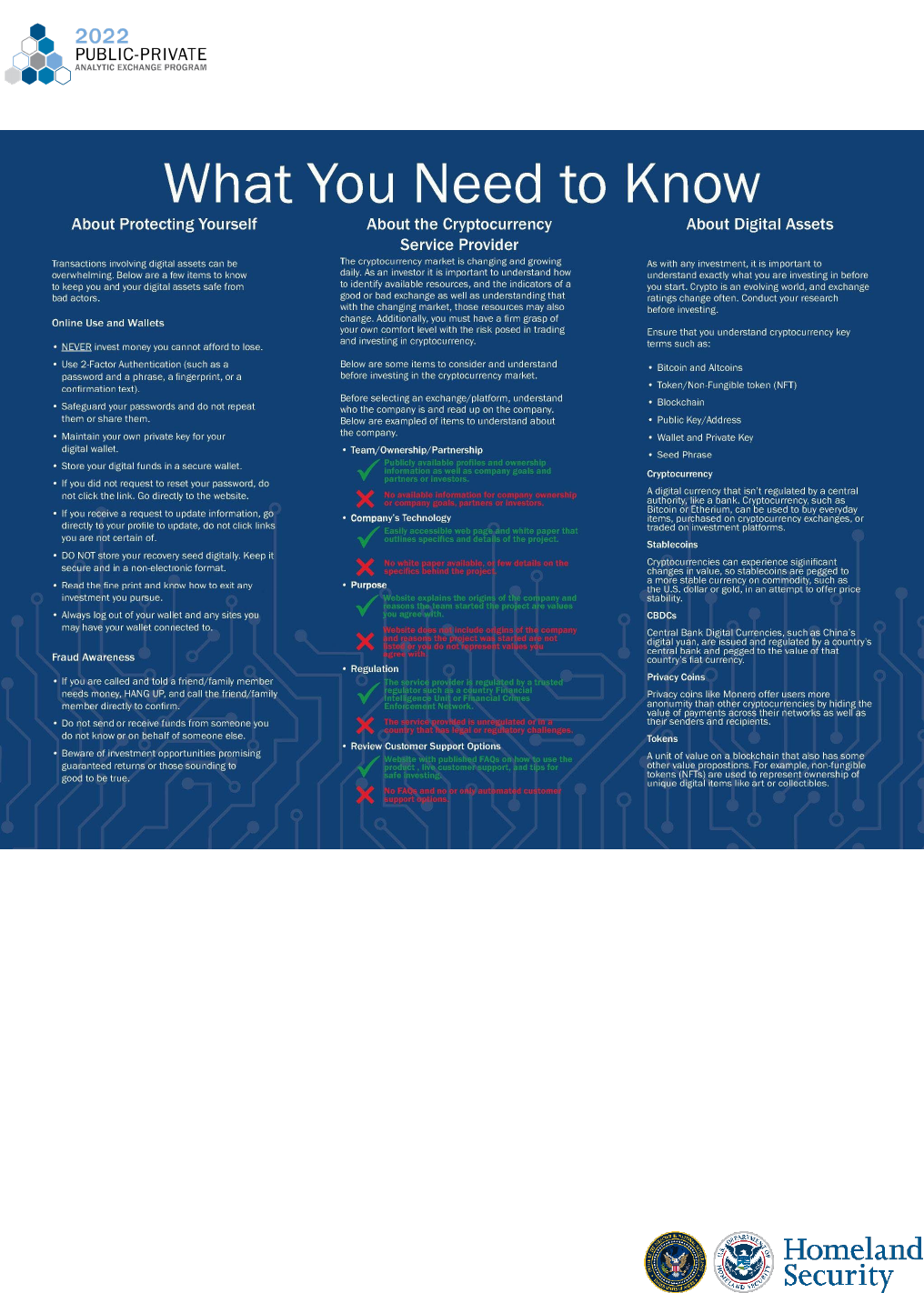

Shifting to the consumer side, there are many precautions that can be taken to reduce

exposure to illicit activity. In the 2021 IC3 Internet Crime Report it was reported that many

victims of romance scams were being pressured into investment opportunities. “The IC3

received more than 4,325 complaints, with losses over $429 million, from Confidence

Fraud/Romance scam victims who also reported the use of investments and cryptocurrencies,

or pig butchering.” In these scams, initial contact is made via social media websites and dating

apps. Once trust is gained, the scammer will bring up a cryptocurrency investment opportunity.

Consumers need to be careful of who they communicate with and befriend online. Consumers

should do their own diligent research before the purchase of any cryptocurrency and should be

cautious when approached about any investment opportunities.

20

Another growing scam is cryptocurrency and online digital payment support

impersonators. In these scams digital currency owners are informed of an issue with their

crypto wallet and are told to give access to their wallet or transfer the content of their current

wallet to a different one. On the other hand, digital currency owners are increasingly seeking

advice and assistance with their currencies which is leading them to the wrong support contacts

and potentially giving their information to the wrong people. Consumers have to guard their

digital currency information closely. They should safeguard their keys and login information and

be weary of any calls or contact from exchanges/providers. Consumers should verify any

support information and contacts from where they currently hold their digital assets in the

event they need assistance.

Account takeover has also been addressed in the Visa Biannual Threat Report where

login credentials are often obtained through social engineering schemes and data breaches can

be sold on the dark web. One of the most effective actions consumers can take to prevent this

occurrence is to enable multi factor authentication on their accounts. This drastically reduces

the potential for threat actors to successfully access a consumer’s account. If informed of a data

breach, users should change their passwords and login information immediately to protect their

data and reduce the risk of their account being hacked.

21

Consumers should only use reputable cryptocurrency and digital currency exchanges

that are U.S. based for purchasing and maintaining funds. Due to a wide range of regulatory

issues and differences that exist with non U.S. based cryptocurrency exchanges, the safest

34

option for consumers is to use U.S. based exchanges. If consumers wish to use exchanges

outside the U.S., they should research the legal restrictions and regulatory environment of the

country that exchange is based in.

For P2P payment services such as Zelle, consumers should treat transactions as actual

cash and should only send the person money if they feel comfortable giving cash to that

individual in person. Banks who utilize Zelle and stand-alone services such as Square and Paypal

should continue to push out education for consumers of their services to protect them from

any fraud. Consumers should use caution when receiving and replying to any text messages

appearing to be P2P service related and bank related. They should not open links or

attachments from texts and should immediately contact a verified bank number to check its

legitimacy. Although federal laws could be strengthened to further combat illicit use of P2P

services, the most effective change to stop criminal activity in this realm is consumer

education.

22

Increased policies and regulations have to be implemented in the digital asset space.

Government should determine the category of asset class for cryptocurrencies to enact and

enforce policy and regulations. As things stand right now, cryptocurrency is still under debate as

to what it should be classified as. Even if cryptocurrency has the classification as a security or

commodity, this could still be challenged and other emerging blockchain financial interests like

NFTs may not fall under the same designation.

Impact on Government and Private Sector

As criminals become more sophisticated in their fraud schemes and take advantage of

emerging financial technologies, it will be important for laws to adapt to new technology and

digital assets that emerge. Districts across the U.S. are at times hesitant to prosecute crimes

involving digital assets due to their unregulated and less restricted nature. It is key for the U.S.

to adapt swift laws and regulations as new digital assets such as NFTs rise in popularity.

Without the right laws being put into effect and precedent taking place, illicit actors will

continue to take advantage of new digital assets. It will also be important for legal personnel to

keep the language of digital assets simple enough for judge, jury, etc. to understand so that

case can successfully be tried. It will increasingly become important for both private and public

sector collaboration to share intelligence and findings as the digital asset space evolves.

There are multiple federal agencies that are stepping up as leaders to combat crimes in

the digital asset space including the FBI, Secret Service, IRS, and SEC. These agencies are

becoming better equipped with cryptocurrency tracing tools and increasing case knowledge

35

that will help take action against illicit actors in the digital asset space and also help the

everyday consumer who falls victim to fraud.

Future Regulations, Forecast, and Areas for Future Study

There are multiple future forecasts and predictions we see illicit actors taking in the

cryptocurrency, digital payment, and financial technology space. Firstly illicit actors will seek to

use more privacy coins, mainly Monero, to conduct illicit activity as opposed to Bitcoin and

other cryptocurrencies. Monero is known as the true private cryptocurrency and that is enticing

for illicit actors to switch their activity towards. Monero already acts as a crypto mixer in

obfuscating transactions, senders, and receivers so it takes a lot less work on behalf of illicit

actors to utilize. Secondly, privacy wallets will increasingly be utilized in illicit activities due to

their ability to combine multiple security features including encryption and IP address

anonymization. Elliptic reported in 2020 that privacy wallets are used in 13% of Bitcoin

proceeds of illicit actors, up 2% from the previous year.

23

This percentage will increase as more

criminals seek to privatize the final source of their funds. There are already darknet markets

emerging and in use which exclusively use Monero. This will likely become more of a common

practice as federal agencies continue to have successful cases in criminals using Bitcoin and

other currencies besides Monero. Darknet markets are implementing increased security and

there will be an increase in direct buyer to vendor communication to avoid further parties in

illicit transactions. Criminals will continue to seek opportunities for decentralization of digital

assets through chain hopping and cashing out to fiat currency to decrease the risk of being

discovered by investigators.

24

The SEC is currently examining NFTs to determine if they are illegal offerings. NFTs will

be considered securities if they pass the Howey test, a standard used to determine if there is an

investment contract in a transaction. SEC Commissioner Hester Peirce stated certain pieces of

NFTs might fall in the SEC’s jurisdictions. As cryptocurrencies see more regulations, people

could potentially turn to NFTs as a main form of hiding money from illicit activity. We could also

see more cryptocurrency exchanges and digital asset providers move headquarters outside the

U.S. due to increased U.S. sanctions. There is already precedent of crypto exchanges moving

their headquarters to other locations worldwide to avoid certain sanctions or even to gain

certain advantages as some countries/locations offer to attract digital asset providers. We will

likely increasingly see exchanges, NFT providers, and other digital asset suppliers be charged

under money laundering or operating an unlicensed money service business. Chainalysis

introduced cross chain investigations to their investigative tool, Reactor, in March 2022. As

cryptocurrency tracing platforms and companies introduce the tools to allow tracing across

36

different blockchains, it will be harder for illicit actors to hide their activity. There will continue

to be greater advancements in tracking activity across different blockchains.

25

Another area that will see increased regulation is the process of cryptocurrency mining.

New York has recently introduced legislation that would restrict the mining of digital assets. In

this legislation, there would be a two year suspension on reactivating fossil fuel plants for off

the grid cryptocurrency mining. Mining has become a hot topic due to the high amount of

energy involved and environmental impact it has. Texas is already becoming a hub to Bitcoin

mining and we will likely see other states embrace mining due to the economic benefits

associated with the practice. However some states will increasingly issue restrictions on the

practice due to the overall environmental implications it has.

26

37

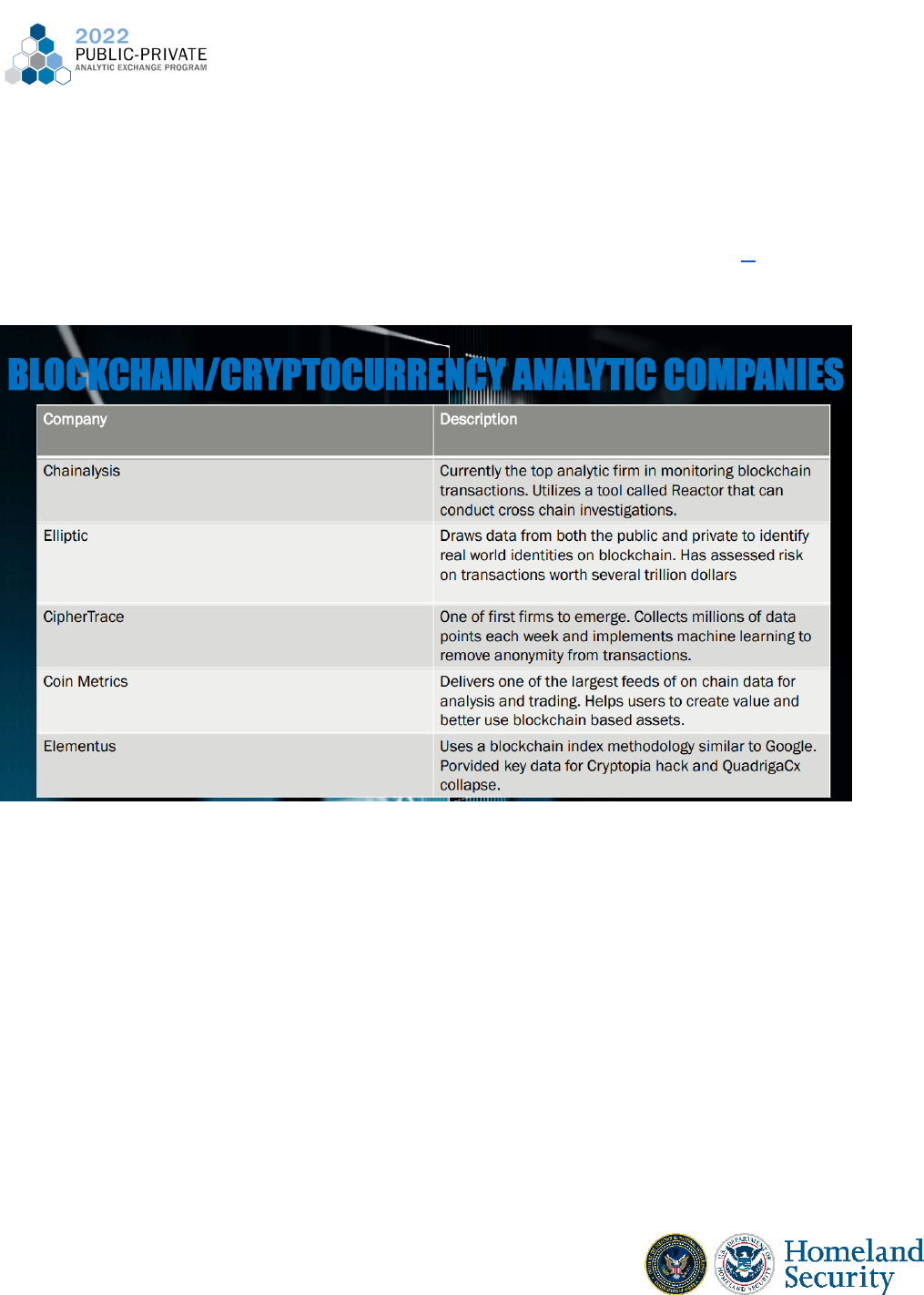

We will also continue to see the creation, rise, and growth of blockchain analytic firms

that work with both the private and public sector to provide greater visibility into digital asset

transactions. This space is still developing and we will likely see new entrants as digital assets

evolve and both compliance and investigations increase. Our group examined some of the top

analytic firms throughout our research and they are summed up in the table below:

27

Analytic Dissemination Plan

List agencies that stand to benefit from research:

Securities and Exchange Commission

Cybersecurity & Infrastructure Agency

Financial Crimes Enforcement Network

Federal Bureau of Investigation

United States Secret Service

38

United States Postal Inspection Service

Homeland Security Investigations

Drug Enforcement Administration

Internal Revenue Service (Criminal Investigative Division)

U.S. Federal Reserve System

Office of the Comptroller of Currency

DISCLAIMER STATEMENT:

The views and opinions expressed in this document do not necessarily

state or reflect those of the United States Government or the Companies whose analysts

participated in the Public-Private Analytic Exchange Program. This document is provided for

educational and informational purposes only and may not be used for advertising or product

endorsement purposes. All judgments and assessments are solely based on unclassified sources

and the product of joint public and private sector efforts.

39

Endnotes Separated by Sections

Most Common Illicit Finance Activities

1. https://www.bloomberg.com/news/articles/2022-03-10/crypto-obfuscator-tornado-says-sanctions-cant-affect-

smart-contracts

2. https://www.bleepingcomputer.com/news/cryptocurrency/620-million-in-crypto-stolen-from-axie-infinitys-

ronin-bridge/

3. https://go.chainalysis.com/2022-Crypto-Crime-Report.html

4. https://www.ic3.gov/Media/PDF/AnnualReport/2021_IC3Report.pdf

Most Exploited Elements of Financial Technologies

1. https://financesonline.com/what-is-fintech/

2. https://www.bankrate.com/investing/best-online-brokers-for-stock-trading/

3. https://www.morningstar.com/articles/1088193/the-best-robo-advisors-of-2022

4. https://www.pwc.co.uk/financial-services/fintech/assets/FinTech-Global-Report2016.pdf

5. https://www.ftc.gov/enforcement/refunds/equifax-data-breach-settlement