United States Government Accountability Office

Washington, DC 20548

September 9, 2005

The Honorable Charles E. Grassley

Chairman

The Honorable Max Baucus

Ranking Minority Member

Committee on Finance

United States Senate

The Honorable John D. Rockefeller, IV

United States Senate

Subject:

Overview of the Long-Term Care Par nership Program

t

In 2003, the most recent year for which data are available, national spending on long-

term care totaled $183 billion,

1

and nearly half of that was paid for by the Medicaid

program, the joint federal-state health care financing program that covers basic

health and long-term care services for certain low-income individuals. Private

insurance paid a small portion of long-term care expenditures—about $16 billion or

9 percent in 2003. With the aging of the baby boom generation, long-term care

expenditures are anticipated to increase sharply in coming decades. The projected

spending on long-term care presents a looming fiscal challenge for federal and state

governments. As a result, some policymakers are looking for ways to reduce the

proportion of long-term care spending financed by Medicaid and promote private

insurance as a larger funding source.

The Long-Term Care Partnership Program is a public-private partnership between

states and private insurance companies, designed to reduce Medicaid expenditures

by delaying or eliminating the need for some people to rely on Medicaid to pay for

long-term care services. Individuals, who buy select private long-term care insurance

policies that are designated by a state as partnership policies and eventually need

long-term care services, first rely on benefits from their private long-term care

insurance policy to cover long-term care costs before they access Medicaid. To

qualify for Medicaid, applicants must meet certain eligibility requirements, including

income and asset requirements. Traditionally, applicants cannot have assets that

exceed certain thresholds and must “spend down” or deplete as much of their assets

as is required to meet financial eligibility thresholds. To encourage the purchase of

private partnership policies, long-term care insurance policyholders are allowed to

1

Long-term care includes nursing home services, home health, personal care services, assisted living,

and noninstitutional group living arrangements.

GAO-05-1021R Long-Term Care Partnership Program

protect some or all of their assets from Medicaid spend-down requirements during

the eligibility determination process, but they still must meet income requirements.

2

You asked that we provide summary information about the Long-Term Care

Partnership Program. As agreed with your staff, we examined the demographics of

program participants, the types of policies purchased, and the benefits accessed by

policyholders. On August 18, 2005, we briefed your staff on this information, and this

letter formally conveys our findings. Enclosure I contains the slides we provided

during our briefing with some revisions to incorporate updated information.

To do our work, we interviewed officials from the four states that offer Long-Term

Care Partnership Programs—California, Connecticut, Indiana, and New York—and

reviewed their quarterly reports and other official documents. While all four of the

states with partnership programs collect some information on their programs, the

states do not all collect the same information. The programs began in different years

and data reported by the states are based on different time periods. Therefore, in

some cases, we report information only for those states that had available data.

Based on discussions with state officials and reviewing documentation on uniformly

collected insurer data and surveys of policyholders, we determined that the

information we report was sufficiently reliable for our purposes. We also examined

reports on the program from the Congressional Budget Office, the Congressional

Research Service, and other research organizations. We provided a draft of the

enclosure to officials in the four partnership states for their review. They provided us

with technical comments that we incorporated as appropriate. We conducted our

work from July through September 2005 in accordance with generally accepted

government auditing standards.

Background

The Long-Term Care Partnership Program began in 1987 as a demonstration project

funded through the Robert Wood Johnson Foundation. As part of the demonstration

project, four states—California, Connecticut, Indiana, and New York—developed

partnership programs.

3

These programs are designed to encourage the purchase of

private long-term care insurance, especially among moderate income individuals,

thereby potentially reducing future reliance on Medicaid as a funding source for long-

term care services. Based on the most recently available data, there are over 172,000

active partnership policies in the four states.

2

The definition of assets differs between the Long-Term Care Partnership Program and Medicaid. The

Long-Term Care Partnership Program uses the term assets to denote savings and investments, and

excludes income. For purposes of Medicaid eligibility, assets include both income, which is anything

received during a calendar month that is used or could be used to meet food, clothing, or shelter

needs, and resources, which are anything owned, such as savings accounts, stocks, or property.

3

In general, federal statute limits most states from implementing new partnership programs. To

protect assets under the Long-Term Care Partnership Program, participating states exempt some or all

assets from Medicaid’s estate recovery requirement, which generally requires adjustment or recovery

from an individual’s estate for the costs of medical assistance provided. With the enactment of the

Omnibus Budget Reconciliation Act of 1993, states were no longer allowed to disregard estate assets

from recovery unless the practice had been approved as of May 14, 1993.

GAO-05-1021R Long-Term Care Partnership Program

2

The four states vary in how their partnership programs protect policyholders’ assets.

The programs in California and Connecticut have dollar-for-dollar models, in which

the dollar amount of protected assets is equivalent to the dollar value of the benefits

paid by the long-term care insurance policy. For example, a person purchasing a

long-term care insurance policy with $300,000 total coverage would have $300,000 of

assets protected if she were to exhaust the long-term care insurance benefits and

apply for Medicaid. New York’s program requires the purchase of a comprehensive

long-term care insurance policy, covering a minimum of 3 years of nursing home care

and 6 years of home and community-based care, but offers total asset protection for

all of the purchaser’s assets at the time of Medicaid eligibility determination.

Indiana’s program uses a hybrid model that allows purchasers to obtain

dollar-for-dollar protection up to a certain benefit level as defined by the state; all

policies with benefits above that threshold provide total asset protection for the

purchaser.

Demographics of Program Participants

The average age of partnership policyholders at the time of purchase ranged from 58

to 63 in Connecticut, Indiana, and New York. The median age of partnership

policyholders in California was 60. Most partnership policyholders were female,

married, and purchasing long-term care insurance for the first time. In California and

Connecticut surveys of persons who purchased a partnership policy, most

policyholders reported being in good or very good health. In the three states that

surveyed a sample of partnership policyholders—California, Connecticut, and

Indiana—the majority of policyholders in each of these states reported that their total

assets were greater than $350,000.

4

About half or more of the policyholders in each of

these three states also reported average monthly household incomes of greater than

$5,000.

Policies Purchased

In 2004, the number of partnership policies purchased ranged from about 4,000 in

Indiana to nearly 10,000 in California. The number of partnership policies purchased

each year has increased significantly since the programs began in the early 1990s,

though there has been a decline or leveling off in the number of policies purchased in

recent years. State partnership officials from two states reported that the reason for

the decline in sales of partnership policies in recent years is not specific to

partnership policies but is reflective of overall trends in the long-term care insurance

market. Most partnership policies are comprehensive, covering both nursing home

care and home and community-based care, and are bought individually rather than

through group or organization-sponsored programs. While most applications for

partnership policies were approved, approximately 16 percent were denied.

4

In a policyholder survey, California and Connecticut instructed policyholders to exclude the value of

homes and cars when reporting their assets. Indiana instructed policyholders to include the value of

their homes.

GAO-05-1021R Long-Term Care Partnership Program

3

The amount of coverage purchased by partnership policyholders varies across the

four states. The average daily benefit amount for nursing home care in Connecticut

was approximately $188 per day. The most common daily benefit amounts purchased

for nursing home care in Indiana were $110 and $120 per day. These amounts were

calculated using the daily benefit amounts at the time of purchase and are not

adjusted for inflation.

5

Average premiums for partnership policies differ across states and are based on age

and benefits purchased. For example, in Connecticut average annual premiums for a

comprehensive policy covering 1 year of care with a $200 daily benefit amount range

from $1,500 for a 55-year-old purchaser to $3,400 for a 70-year-old. If the 55-year-old

purchased the same policy with a 3-year benefit period rather than a 1-year benefit

period, the annual premiums would have been $2,500.

Data from Indiana suggest that when consumers are given the incentive of total asset

protection, they are likely to purchase more insurance coverage. Prior to 1998, when

Indiana introduced total asset protection as an option in addition to dollar-for-dollar

asset protection policies, only 29 percent of policies purchased had total coverage

amounts large enough to trigger total asset protection. In contrast, in the first quarter

of 2005, 87 percent of policies purchased were large enough to trigger total asset

protection.

Benefits Accessed by Policyholders

Less than 1 percent of active partnership policyholders are currently accessing their

long-term care insurance benefits. Since the programs began, 251 policyholders in all

four states have exhausted their long-term care insurance benefits. Of those 251

policyholders, 119 (47 percent) have accessed Medicaid. The remaining 53 percent

have not accessed Medicaid. According to interviews with state officials, this may be

because they are spending down income or unprotected assets, their health has

improved, or their families provide informal care. More policyholders have died

while receiving long-term care insurance benefits (899 policyholders) than have

exhausted their long-term care insurance benefits (251 policyholders), which could

suggest that the Long-Term Care Partnership Program may be succeeding in

eliminating some participants’ need to access Medicaid. However, it is difficult to

determine whether and to what extent the Long-Term Care Partnership Program has

resulted in cost savings to the Medicaid program because there are insufficient data

to determine if those individuals who have purchased partnership policies would

have accessed Medicaid had they not purchased long-term care insurance benefits.

Comments from Partnership States

We provided a draft of the enclosure to officials in the four partnership states for

their review. They provided us with technical comments that we incorporated as

appropriate.

5

Most partnership policies are required to have inflation protection. For example, New York generally

requires inflation protection; however, purchasers age 80 or older are not required to have inflation

protection as part of their policies.

GAO-05-1021R Long-Term Care Partnership Program

4

- - - - -

As agreed with your offices, unless you publicly announce the contents earlier, we

plan no further distribution of this report until 30 days after its date. We will then

provide copies of this report upon request. In addition, the report will be available at

no charge on the GAO Web site at

http://www.gao.gov.

If you or your staff have any questions about this report please contact me at (202)

512-7119 or dickenj@gao.gov. Contact points for our Offices of Congressional

Relations and Public Affairs may be found on the last page of this report. GAO staff

who made major contributions to this report are Krister Friday, Clare Mamerow, and

Anna Theisen-Olson.

John E. Dicken

Director, Health Care

Enclosure – 1

GAO-05-1021R Long-Term Care Partnership Program

5

1

The Long-Term Care Partnership Program:

An Overview

Briefing to Congressional Staff

Enclosure 1

6 GAO-05-1021R Long-Term Care Partnership Program

2

Enclosure 1

Briefing contents

• This briefing provides information about the Long-Term Care

Partnership Program:

• Background and overview

• Demographics of program participants

• Policies purchased

• Benefits accessed by policyholders

Enclosure 1

GAO-05-1021R Long-Term Care Partnership Program

7

3

Enclosure 1

Background and overview

• The Long-Term Care Partnership Program is a public-private partnership designed

to encourage persons with moderate income to purchase private long-term care

insurance to fund their long-term care needs rather than relying on Medicaid

• Individuals who buy a partnership policy and eventually need long-term care

services first rely on benefits from their private long-term care insurance policy

to cover long-term care costs

• If the policyholders exhaust private long-term care insurance benefits and need

assistance from Medicaid to fund long-term care, they may protect some or all

of their assets

1

from Medicaid spend-down requirements during the eligibility

determination process;

2

however, they are still subject to Medicaid income

requirements

• One goal of the Long-Term Care Partnership Program is to save money for Medicaid

by delaying or eliminating the need for participants to access Medicaid for long-term

care services

1

The Long-Term Care Partnership Program uses the term assets to denote savings and investments, and excludes

income. For purposes of Medicaid eligibility, assets include both income, which is anything received during a

calendar month that is used or could be used to meet food, clothing, or shelter needs, and resources, which are

anything owned, such as savings accounts, stocks, or property.

2

In some cases, policyholders can access Medicaid before exhausting their private insurance benefits if their actual

assets are less than or equal to the amount of insurance benefits paid.

GAO-05-1021R Long-Term Care Partnership Program

8

4

Enclosure 1

Background and overview (continued)

• As a result of a Robert Wood Johnson Foundation

demonstration project, four states have operated

partnership programs since the early 1990s (California,

Connecticut, Indiana, and New York)

• Over 172,000 partnership policies are active in the four

states

• The Omnibus Budget Reconciliation Act of 1993 limits

most states from implementing partnership programs

GAO-05-1021R Long-Term Care Partnership Program

9

5

Enclosure 1

Background and overview (continued)

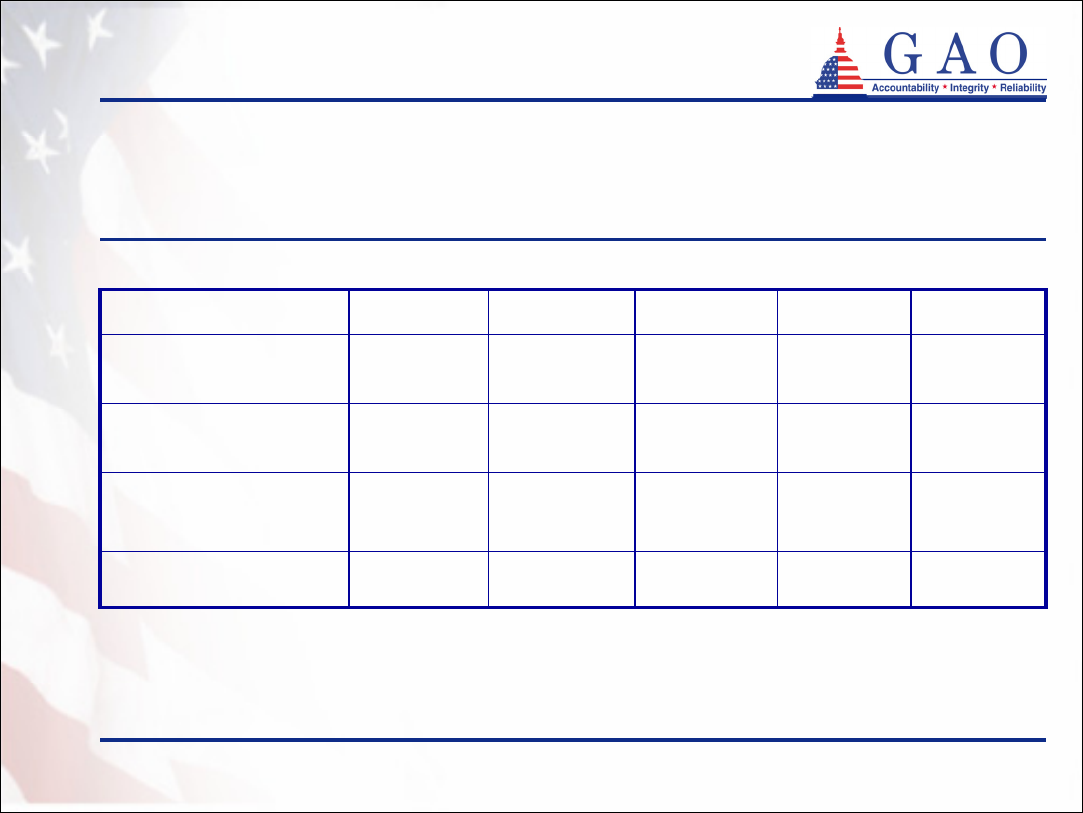

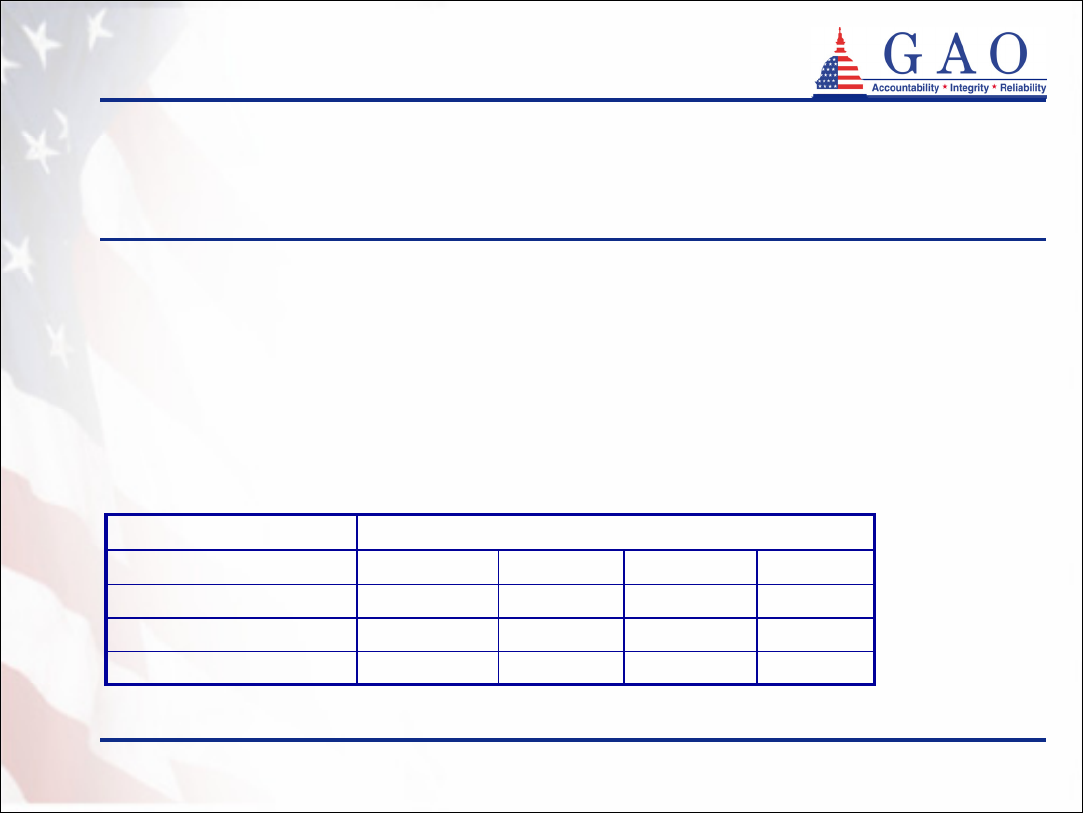

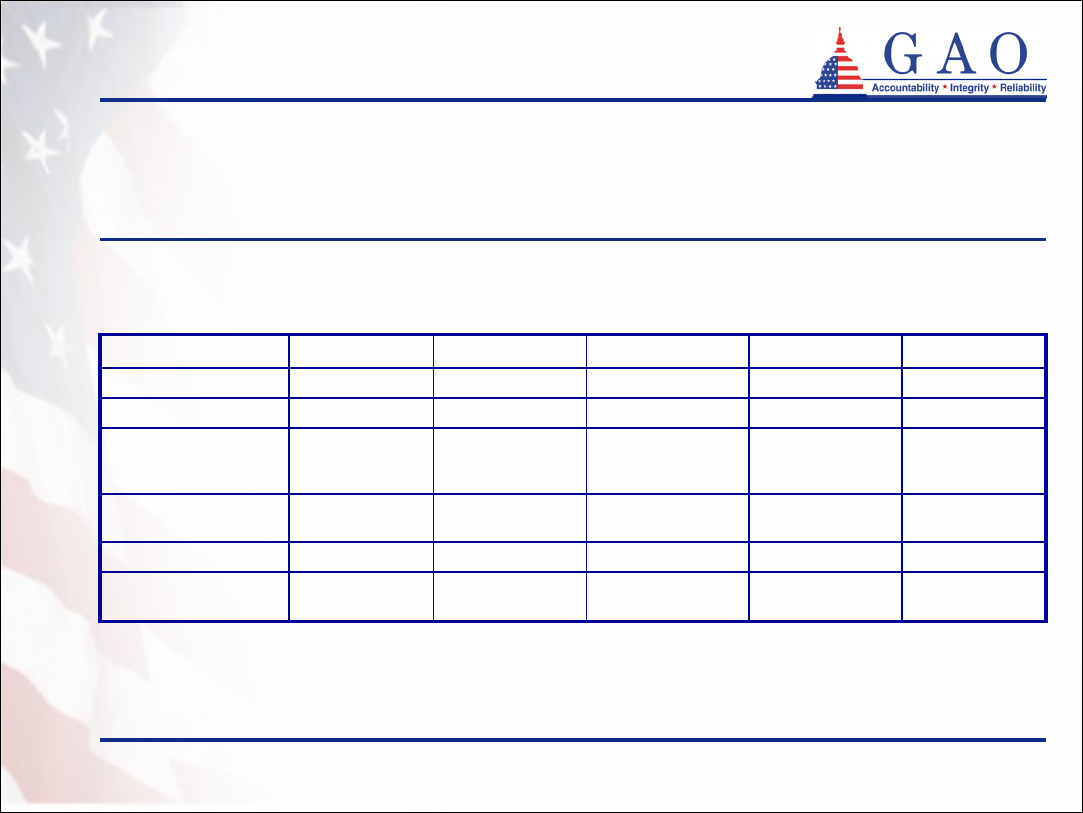

• The four states with partnership programs offer one of three program

models (see table 1). These models exempt different levels of assets from

Medicaid spend-down requirements

• Dollar-for-dollar: Assets are protected up to the amount of the private

insurance benefit paid

• Total asset protection: All assets are protected when a state-defined

minimum benefit package is paid

• Hybrid: Program offers both dollar-for-dollar and total asset protection.

The type of asset protection depends on the initial amount of coverage

purchased. Total asset protection is available for policies with initial

coverage amounts greater than or equal to a coverage level defined by

the state

GAO-05-1021R Long-Term Care Partnership Program

10

6

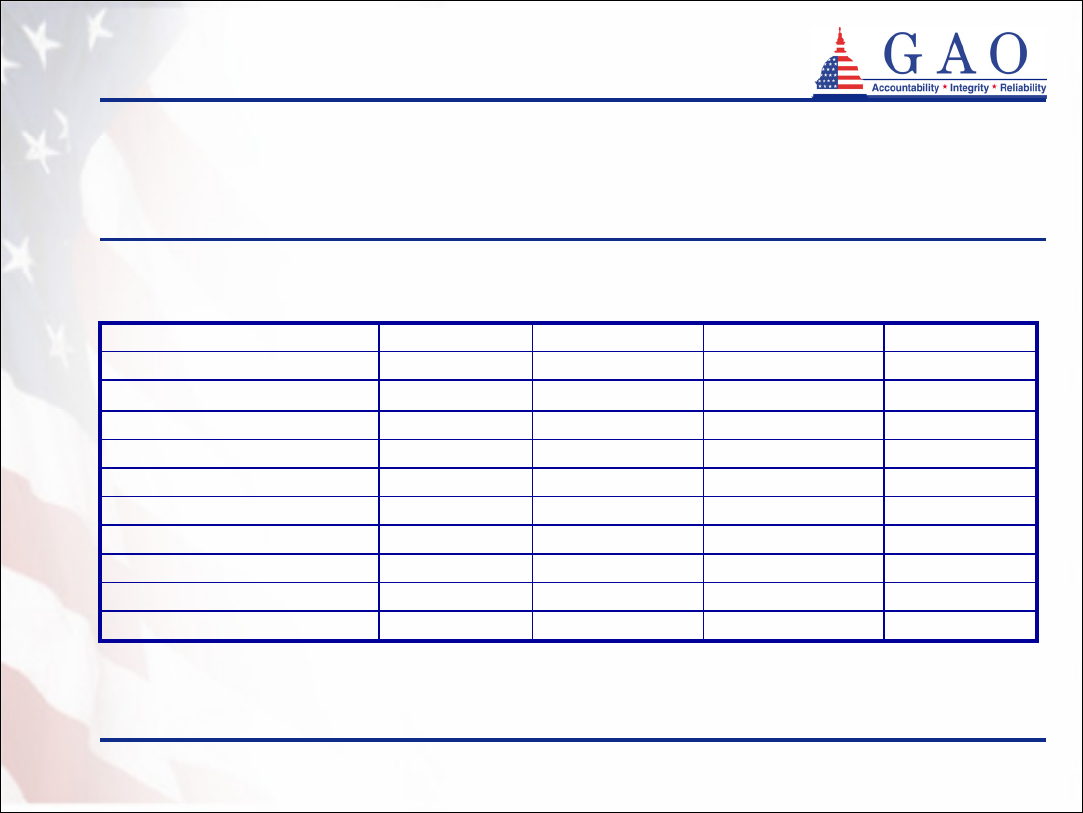

Enclosure 1

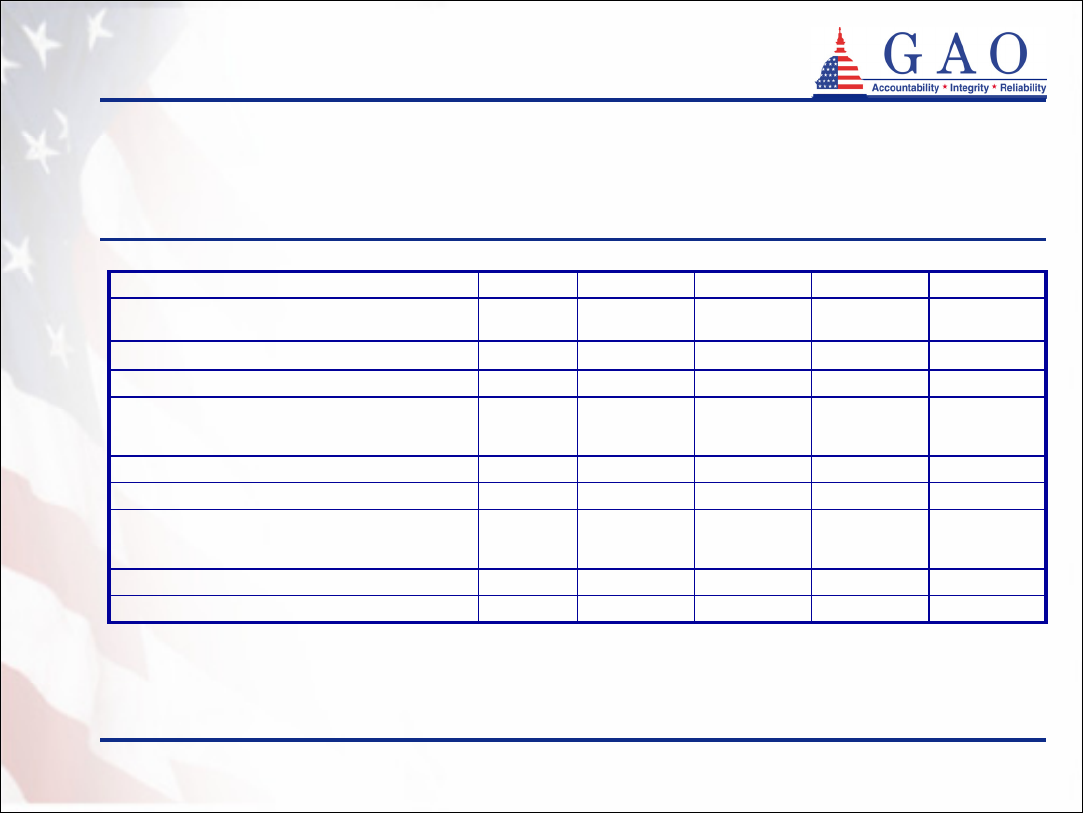

Background and overview (continued)

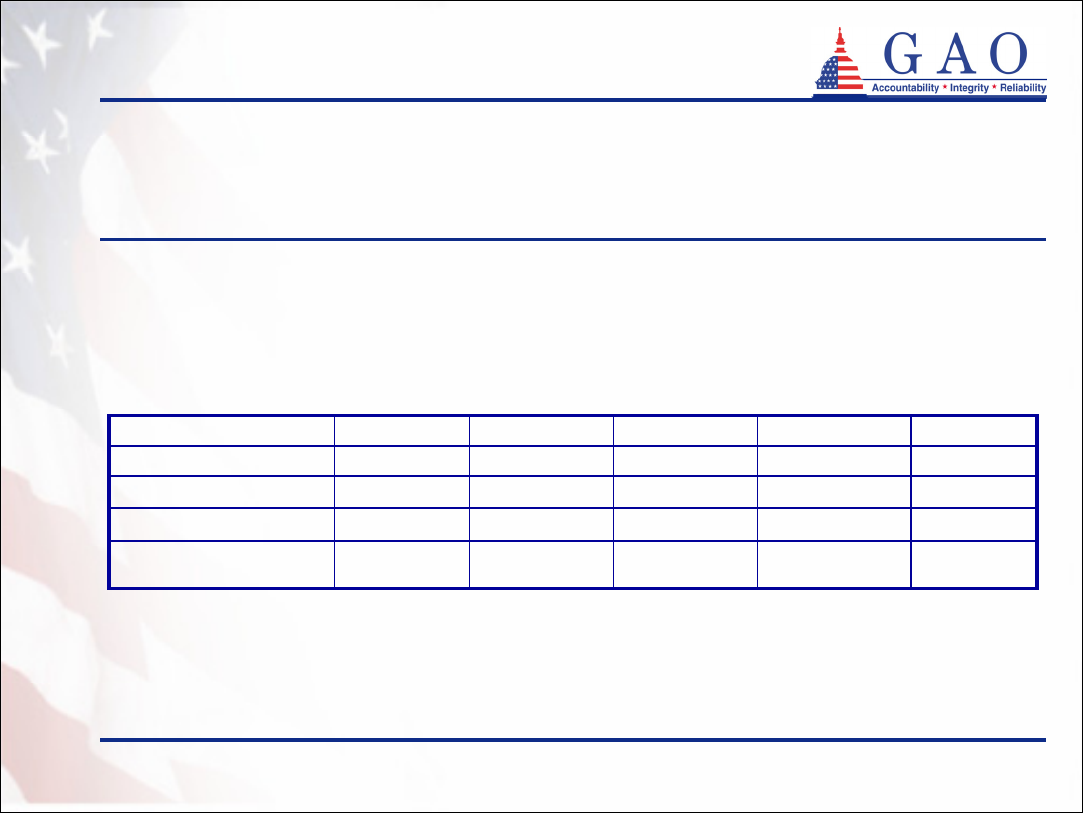

17

c

81385Number of

participating insurance

companies

172,47747,53929,18930,83464,915Number of active

partnership policies

-Total asset

protection

HybridDollar-for-

dollar

Dollar-for-

dollar

Partnership model

-1993199319921994Year implemented

TotalNew York

b

Indiana

a

Connecticut

a

California

a

Table 1: Overview of Partnership Programs

Sources: GAO analysis of data from

Robert Wood Johnson Foundation

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

a

Based on data through March 2005

b

Based on data through December 2004

c

Some insurers participate in more than one state

GAO-05-1021R Long-Term Care Partnership Program

11

7

Enclosure 1

Demographics of program participants

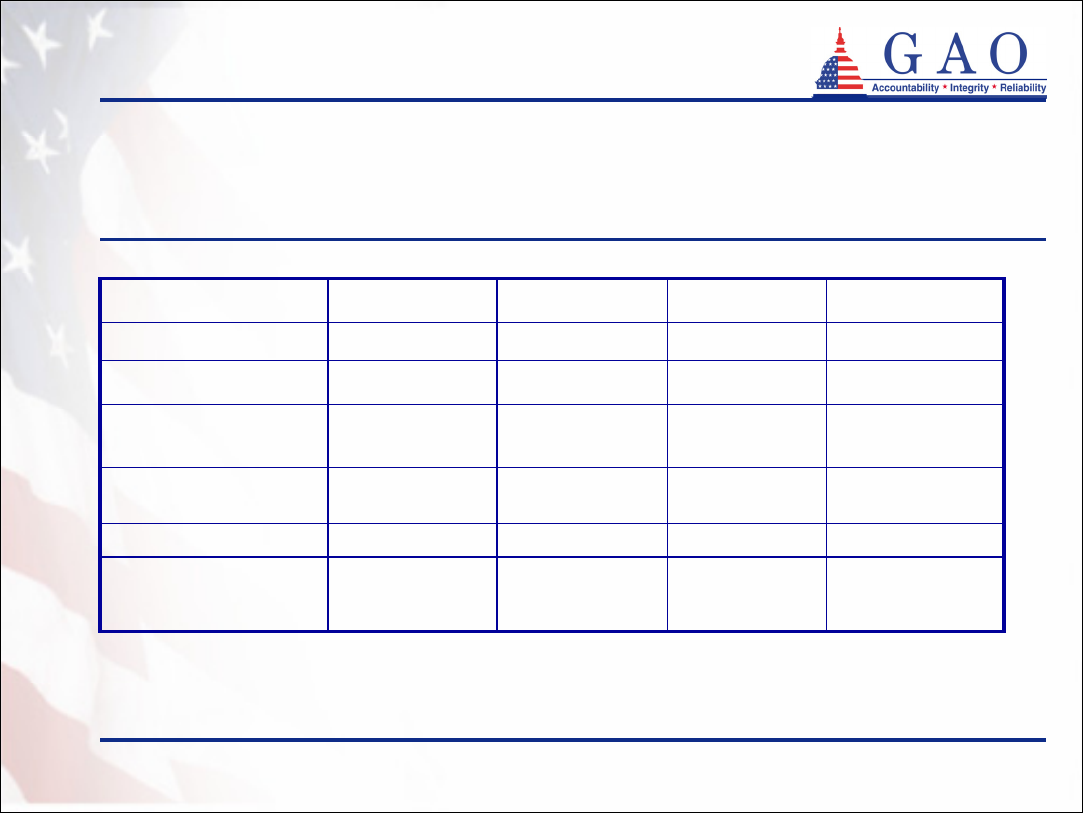

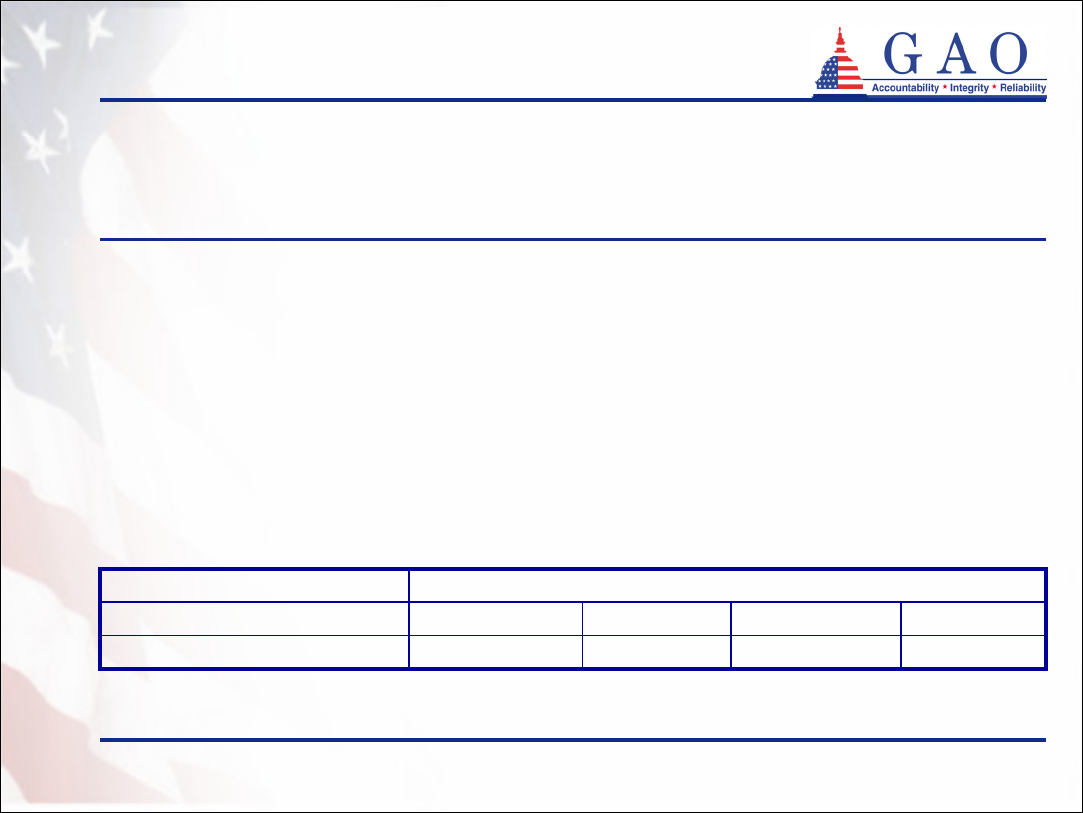

• Average age of partnership policyholders at time of purchase

ranges from 58 to 63 in Connecticut, Indiana, and New York.

The median age of partnership policyholders in California is

60 (see table 2)

• More partnership policyholders are female than male

• Most partnership policyholders are married

• Most partnership policy purchasers are buying long-term care

insurance for the first time

GAO-05-1021R Long-Term Care Partnership Program

12

8

Enclosure 1

Demographics of program participants

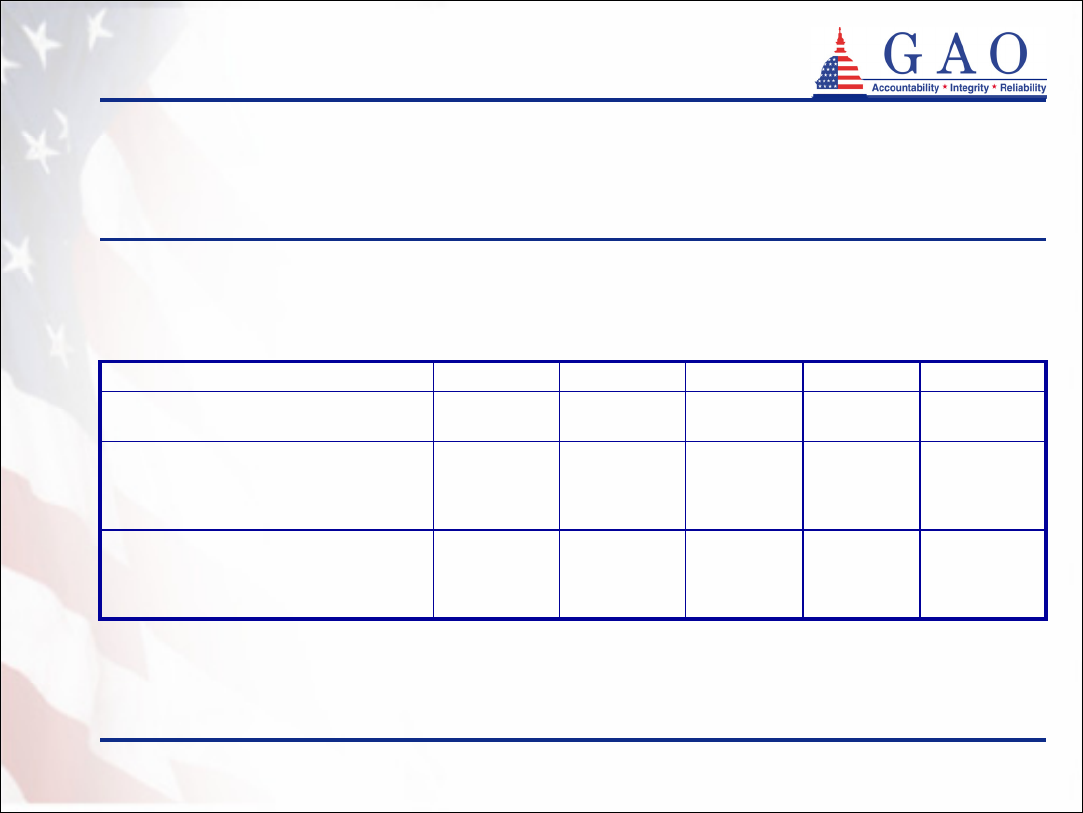

(continued)

Average age: 63Average age: 62Average age: 58Median age: 60Age

19 – 9619 – 9020 – 8918 – 92Age range

95%94%92%94%First time purchasers

3%1%0%

c

1%

Unknown

25%21%23%

c

29%

Not married

72%78%76%

c

70%

Married

Marital status

41%43%44%41%

Male

59%57%56%59%

Female

Sex

New York

b

Indiana

a

Connecticut

a

California

a

Table 2: Demographics of Partnership Policyholders at Time of

Purchase

Sources: California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

a

Based on data through March 2005

b

Based on data through December 2004

c

Based on data through June 2004

Note: Percentages may not add to 100 due to rounding

GAO-05-1021R Long-Term Care Partnership Program

13

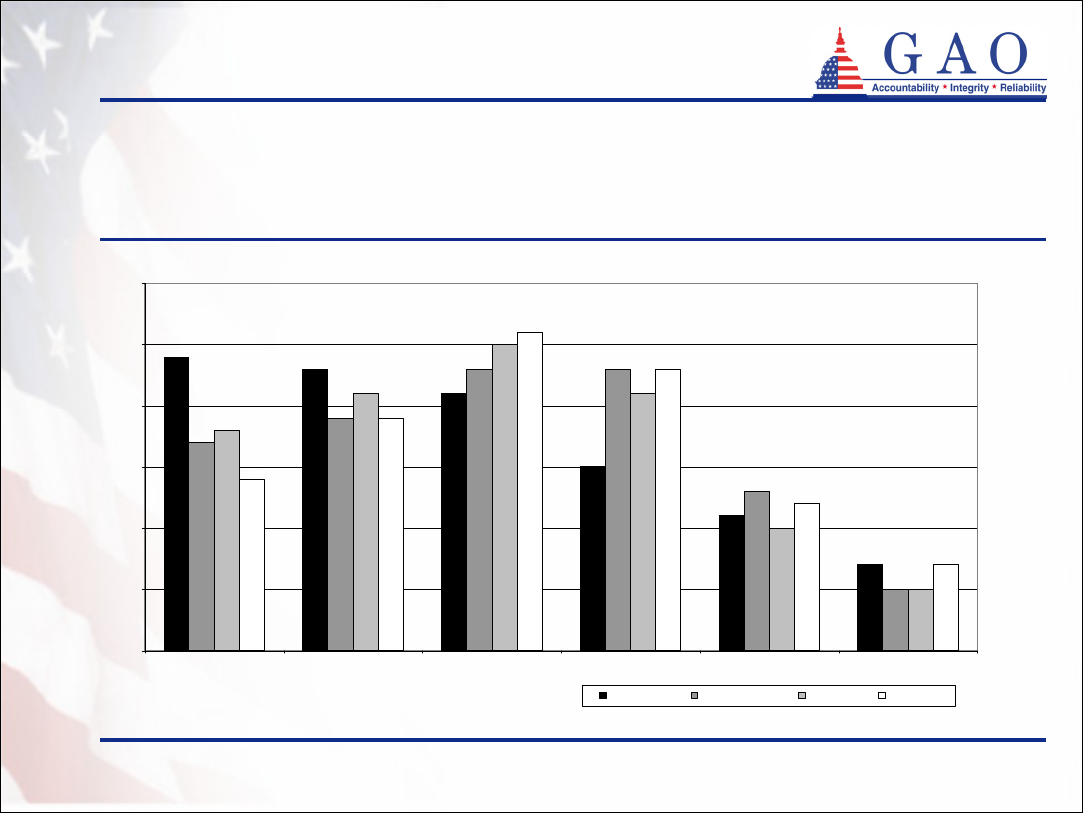

9

Enclosure 1

23%

21%

15%

11%

7%

23%

13%

5%

25%

10%

5%

26%

23%

12%

7%

24%

23%

19%

17%

21%

21%

18%

19%

14%

0%

5%

10%

15%

20%

25%

30%

<55 55-59 60-64 65-69 70-74 75+

California

Connecticut

Indiana

New York

Demographics of program participants

(continued)

Figure 1: Age Distribution of Partnership Policyholders at Time of Purchase

Sources: GAO analysis of data from

California Partnership for Long-Term Care, data through March 2005

Connecticut Partnership for Long-Term Care, data through June 2004

Indiana Long-Term Care Insurance Program, data through March 2005

New York State Partnership for Long-Term Care, data through December 2004

Age Range

Note: Percentages may not add to 100 due to rounding

GAO-05-1021R Long-Term Care Partnership Program

14

10

Enclosure 1

Demographics of program participants

(continued)

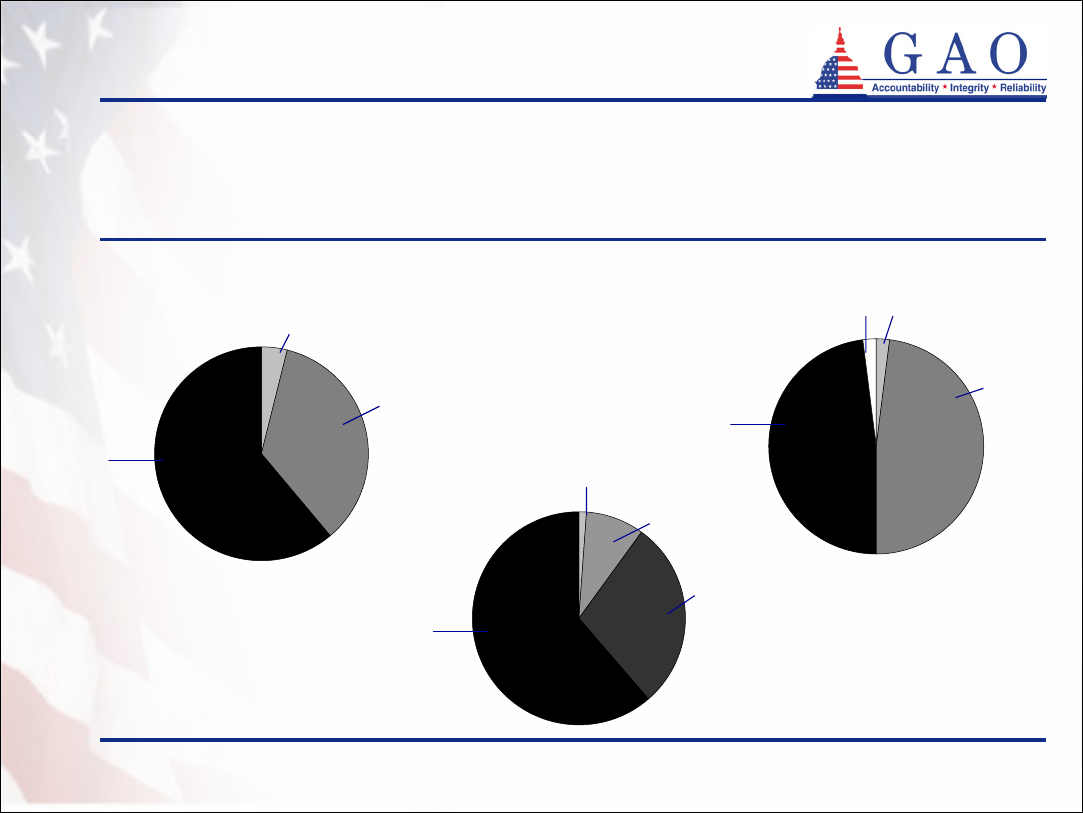

• California, Connecticut, and Indiana surveyed a sample of

policyholders at the time they purchased their policies

1

• The majority of policyholders in each of the three states

reported having total assets greater than $350,000 (see

figure 2)

2

• About half or more of policyholders in each of the three states

reported average monthly household incomes of greater than

$5,000 (see figure 3)

1

Recent income and asset information is not available from New York

2

California and Connecticut instructed policyholders to exclude the value of homes and cars when reporting their

assets. Indiana instructed policyholders to include the value of their homes.

GAO-05-1021R Long-Term Care Partnership Program

15

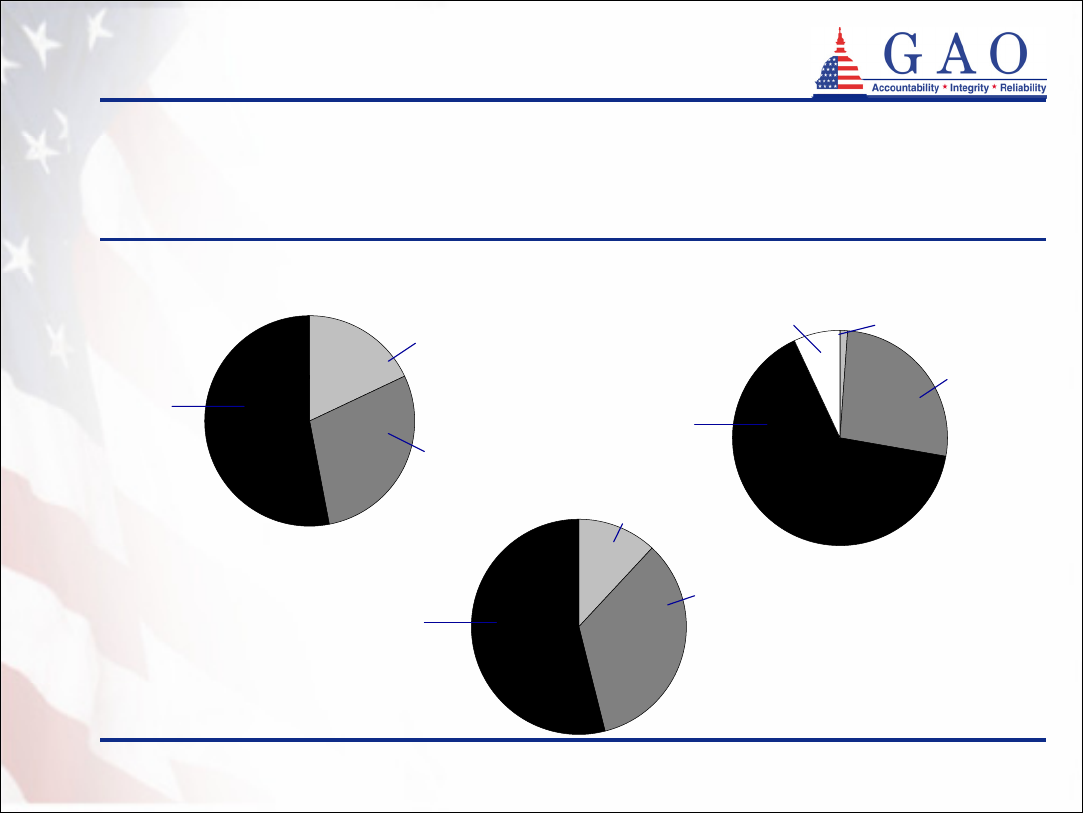

11

Enclosure 1

Demographics of program participants

(continued)

Connecticut

d

Figure 2: Distribution of Policyholders’ Reported Assets in Three

Partnership States

a

Indiana

c

Sources: GAO analysis of survey data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

a

California and Connecticut exclude the value of homes and cars

b

Based on survey data from calendar year 2003

c

Based on survey data from calendar year 2004

d

Based on survey data from July 2003 to June 2004

Less than $100,000

$100,000 - $349,999

Less than $100,000

$100,000 -

$349,999

Unknown

12%

34%

7% 1%

27%

Less than $100,000

California

b

18%

29%

Greater than

$350,000

53%

$100,000 - $350,000

$350,000

or greater

54%

$350,000

or greater

66%

Note: Percentages may not add to 100 due to rounding

GAO-05-1021R Long-Term Care Partnership Program

16

12

Enclosure 1

Demographics of program participants

(continued)

California

a

Connecticut

c

Figure 3: Distribution of Policyholders’ Reported Monthly Household

Income in Three Partnership States

Indiana

b

Greater than

$5,000

$5,000 or

greater

$5,000 or

greater

Less than $2,000

$2,000 - $4,999

Less than $1,000

$1,000 - $2,499

$2,500 - $4,999

Less than $2,000

$2,000 –

$4,999

Unknown

4%

35%

61%

1%

9%

29%

2%

49%

49%

2%

Note: Percentages may not add to 100 due to rounding

Sources: GAO analysis of survey data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

62%

a

Based on survey data from calendar year 2003

b

Based on survey data from calendar year 2004

c

Based on survey data from July 2003 to June 2004

GAO-05-1021R Long-Term Care Partnership Program

17

13

Enclosure 1

Demographics of program participants

(continued)

• In California and Connecticut surveys of persons who purchased a

partnership policy, most policyholders reported being relatively healthy (see

table 3)

0%0.3%Activities of daily living

d

Respondents who reported needing assistance with one or

more:

0.6%1.4%Instrumental activities of daily living

e

36%37%Good

63%61%Excellent

Respondents who reported health status as:

5958Average age of respondents

Connecticut

c

California

b

Table 3: Reported Health Status of Partnership Policyholders in California

and Connecticut

a

a

Comparable data are not publicly available from Indiana and New York

b

Based on survey data from calendar year 2003

c

Based on survey data from July 2003 through June 2004

d

Activities of daily living include such activities as dressing, bathing, transferring, toileting, and eating

e

Instrumental activities of daily living include such activities as preparing meals, shopping for groceries, managing money, doing laundry, and taking medications

Sources: California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

GAO-05-1021R Long-Term Care Partnership Program

18

14

Enclosure 1

Policies purchased

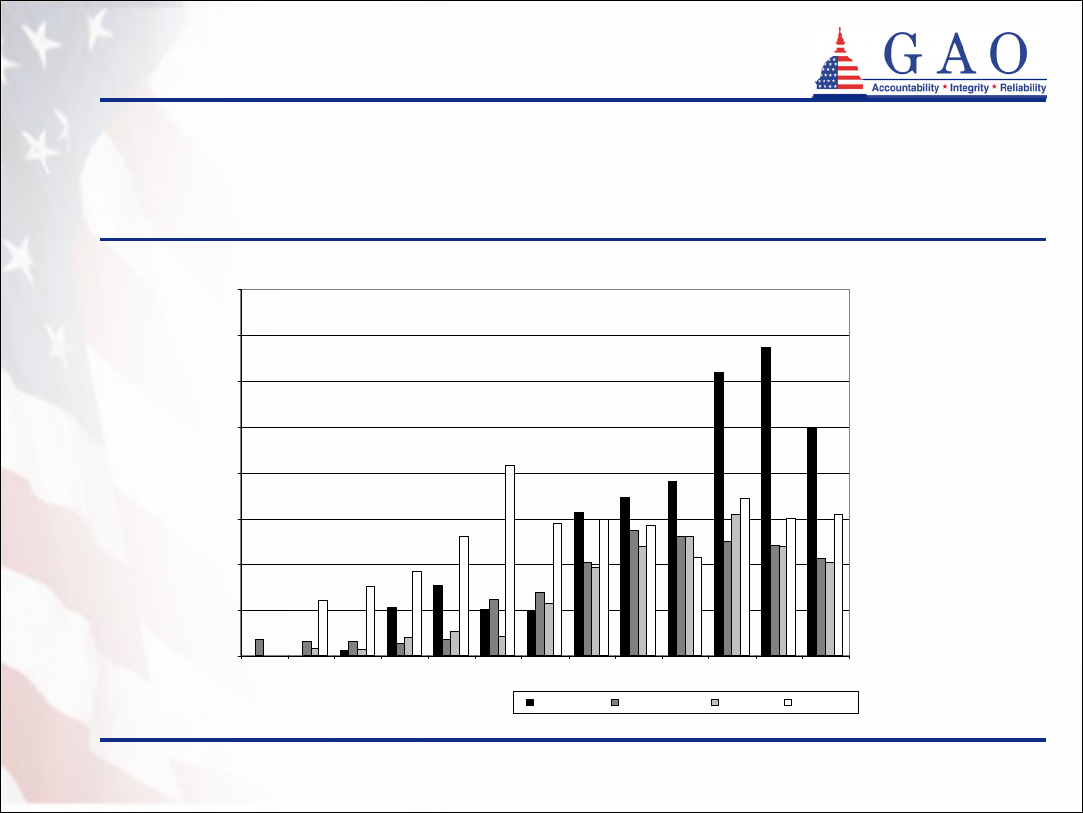

• The purchase of partnership policies has increased

significantly since the programs began (see figure 4)

• However, the partnership states have seen a decline or

leveling off in the number of policies purchased in recent

years

• State partnership officials from two states reported that

the reason for the decline in sales of partnership policies

in recent years is not specific to partnership policies but is

reflective of overall trends in the long-term care insurance

market

GAO-05-1021R Long-Term Care Partnership Program

19

15

Enclosure 1

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

California Connecticut Indiana New York

Policies purchased (continued)

Figure 4: Number of Partnership Policies Purchased by State

Sources: California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

Policies purchased

GAO-05-1021R Long-Term Care Partnership Program

20

16

Enclosure 1

Policies purchased (continued)

11,326 (4%)8,519 (10%)202 (0.5%)2,605 (6%)0 (0%)

Number pending or

withdrawn

42,311 (16%)14,096 (17%)6,324 (15%)5,815 (12%)16,076 (17%)

Number denied

265,60983,97341,49546,56493,577

Number received

Applications

TotalNew York

b

Indiana

a

Connecticut

a

California

a

Table 4: Status of Partnership Applications

Sources: GAO analysis of data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

• Like other long-term care insurance, partnership policies are

subject to medical underwriting

1

• While most applications for partnership policies were

approved, approximately 16 percent were denied (see table 4)

a

Based on data through March 2005

b

Based on data through December 2004

1

Insurance companies evaluate applicants’ health status and possibly deny coverage, offer more limited benefits, or

charge higher premiums to applicants with certain health conditions. However, in some cases, such as with a large

group offering, medical underwriting requirements may be relaxed or eliminated completely.

GAO-05-1021R Long-Term Care Partnership Program

21

17

Enclosure 1

Policies purchased (continued)

• Most partnership policies are comprehensive, covering both

nursing home care and home and community-based care

(see table 5)

• Most purchasers buy partnership policies individually

• Few policies are purchased on the group market or

through organization-sponsored programs

GAO-05-1021R Long-Term Care Partnership Program

22

18

Enclosure 1

Policies purchased (continued)

10%4%16%0%

d

Group market or

organization-

sponsored

90%96%84%100%

d

Individual market

Percent of policies

purchased

0%

c

12%1%5%

Nursing home

only

100%

c

88%99%95%

Comprehensive

Type of coverage

New York

b

Indiana

a

Connecticut

a

California

a

Table 5: Types of Policies Purchased

Sources: California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

a

Based on data through March 2005

b

Based on data through December 2004

c

Comprehensive coverage is a requirement of the New York State Partnership for Long-Term Care

d

California partnership policies are only available on the individual market

GAO-05-1021R Long-Term Care Partnership Program

23

19

Enclosure 1

Policies purchased (continued)

• The amount of coverage purchased by partnership policyholders

varies across the four states

• The average daily benefit amount for nursing home care in

Connecticut was approximately $188 per day. The most

common daily benefit amounts purchased for nursing home

care in Indiana were $110 and $120 per day

• The daily and total benefit amounts on the following pages are

calculated using the daily and total benefit amounts at the time of

purchase and are not adjusted for inflation

1

• For example, a $150 per day policy purchased in 1995 with 5

percent inflation protection is worth approximately $244 per day

today

1

Most partnership policies are required to have inflation protection. For example, New York generally requires

inflation protection; however, purchasers age 80 or older are not required to have inflation protection as part of their

policies.

GAO-05-1021R Long-Term Care Partnership Program

24

20

Enclosure 1

Policies purchased (continued)

• California (policies reported in the first quarter of 2005)

• Daily benefit amount: $150 per day most common

• Benefit coverage period: Lifetime coverage most common

• Connecticut (all active policies with fixed daily benefit amounts)

• Average daily benefit amount for nursing home care:

$187.60 per day

• Average daily benefit amount for home and community-

based care: $166.91 per day

• Benefit coverage period: 2 to 3 years of coverage most

common

• Total benefit amount: median of $200,000

GAO-05-1021R Long-Term Care Partnership Program

25

21

Enclosure 1

Policies purchased (continued)

• Indiana (all active policies)

• Nursing home daily benefit amounts: $110 and $120 per day most

common

• Home and community-based care daily benefit amounts: $120 and

$130 per day most common

• Benefit coverage period: 6 years or greater, excluding lifetime

coverage, most common

• New York (policies reported in the last half of 2004)

• Nursing home daily benefit amount: median of $200 per day

• Home and community-based care daily benefit amount: median of

$100 per day

• Benefit coverage period: 3 years of nursing home care, 6 years of

home and community-based care, which is the minimum required

coverage in New York, most common

GAO-05-1021R Long-Term Care Partnership Program

26

22

Enclosure 1

Policies purchased (continued)

• Average annual premiums in Connecticut for long-term care insurance coverage

based on the following coverage options and purchaser age (see table 6)

1

• $200 per day nursing home coverage

• $200 per day home and community-based care coverage

• 90 or 100 days of care paid for by consumer before long-term care insurance

benefits begin (elimination period)

• 5 percent compounded inflation protection

$5,900$4,100$3,100$2,5003 Years

$4,700$3,300$2,400$2,0002 Years

$3,400$2,400$1,800$1,5001 Year

70656055Minimum duration

Purchaser age

Source: Connecticut Partnership for Long-Term Care

Table 6: Average Annual Premiums in Connecticut for Long-Term Care

Insurance Coverage by Age

1

Comparable premium information for California and Indiana is not available

GAO-05-1021R Long-Term Care Partnership Program

27

23

Enclosure 1

• 3 years of nursing home care ($180 daily benefit in 2005)

• 6 years of home and community-based care ($90 daily benefit in 2005)

• 100 days of care paid for by consumer before long-term care insurance benefits

begin (elimination period)

• 5 percent compounded inflation protection

• No nonforfeiture benefit (no refund or coverage if consumer fails to pay

premiums)

Policies purchased (continued)

• Average annual premiums in New York for long-term care insurance coverage

based on the following coverage options and purchaser age (see table 7)1

Source: New York State Partnership for Long-Term Care

$3,817$2,587$1,968$1,531Average premium amount

70656055

Purchaser age

Table 7: 2005 Average Annual Premiums in New York for Basic Long-Term Care Insurance

Coverage by Age

1

Comparable premium information for California and Indiana is not available

GAO-05-1021R Long-Term Care Partnership Program

28

24

Enclosure 1

Policies purchased (continued)

• In Indiana, since the hybrid model was introduced in 1998,

consumers have purchased more long-term care insurance

coverage to get total asset protection rather than less

coverage to get dollar-for-dollar protection

• To trigger total asset protection in 2005, policyholders

must purchase a policy valued at $196,994 or greater

• Prior to 1998, 29 percent of policies purchased had total

coverage amounts large enough to trigger total asset

protection

• In contrast, in the first quarter of 2005, 87 percent of

policies purchased had total coverage amounts large

enough to trigger total asset protection

Source: Indiana Long-Term Care Insurance Program

GAO-05-1021R Long-Term Care Partnership Program

29

25

Enclosure 1

Policies purchased (continued)

22,129

c

6,2363,802

c

3,9998,092

Dropped (after

30 days)

d

81%77%83%81%84%

Policies that remain

active

172,47747,53929,18930,83464,915

Active

15,721

c

5,9172,557

c

2,7894,458

Dropped

(within 30

days)

211,97261,35834,96938,14477,501

Purchased

Number of policies

Total

New York

b

Indiana

a

Connecticut

a

California

a

Table 8: Status of Partnership Policies

Sources: GAO analysis of data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

• Most partnership policies remain active (see table 8)

a

Based on data through March 2005

b

Based on data through December 2004

c

Some policies may be counted in each of the dropped categories

d

Does not include drops reported as deaths, rescissions, or exhausted benefits

GAO-05-1021R Long-Term Care Partnership Program

30

26

Enclosure 1

• Relatively few partnership policyholders have accessed their

long-term care insurance benefits (see table 9)

Benefits accessed by policyholders

GAO-05-1021R Long-Term Care Partnership Program

31

27

Enclosure 1

Benefits accessed by policyholders

(continued)

172,47747,53929,18930,83464,915

Number of currently active

policies

1,209

(0.7%)

642

(1.4%)

83

(0.3%)

141

(0.5%)

343

(0.5%)

Number of policyholders

currently receiving long-term

care insurance benefits

1,248

(2.0%)

61,358

New York

b

249

(0.7%)

34,969

Indiana

a

211,97238,14477,501

Number of policies ever

purchased

2,761

(1.3%)

351

(0.9%)

913

(1.2%)

Number of policyholders

who have ever received

long-term care insurance

benefits

Total

Connecticut

a

California

a

Table 9: Policies Purchased and Benefits Received in the Partnership

Program

Sources: GAO analysis of data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

a

Based on data through March 2005

b

Based on data through December 2004

GAO-05-1021R Long-Term Care Partnership Program

32

28

Enclosure 1

• Few partnership policyholders have accessed Medicaid (see

table 10)

Benefits accessed by policyholders

(continued)

GAO-05-1021R Long-Term Care Partnership Program

33

29

Enclosure 1

Not available

c

Not available

c

Not available

c

Not available

c

Not available

c

Not available

c

37 (39%)

59 (61%)

96

New York

b

$75,333

d

$69,380

d

$73,028

d

$7,156,597

d

$4,162,812

d

$11,319,409

d

132 (53%)

119 (47%)

251

Total

$83,208

$57,004

$69,683

$1,248,113

$912,067

$2,160,180

15 (48%)

16 (52%)

31

Indiana

a

$2,182,076$3,726,408

Have not accessed Medicaid

$2,018,732$1,232,013

Have accessed Medicaid

$4,200,808$4,958,421

Cumulative asset protection earned by

policyholders who have exhausted long-term

care insurance benefits

$136,380$58,225

Have not accessed Medicaid

$106,249$49,281

Have accessed Medicaid

$120,023$55,713

Per capita asset protection earned by

policyholders who have exhausted long-term

care insurance benefits

16 (46%)64 (72%)

Have not accessed Medicaid

19 (54%)25 (28%)

Have accessed Medicaid

3589

Number of active policyholders who have

exhausted long-term care insurance benefits

Connecticut

a

California

a

Table 10: Medicaid Usage by Partnership Policyholders

Sources: GAO analysis of data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

a

Based on data through March 2005

b

Based on data through December 2004

c

New York does not collect asset protection information

d

Based on data from California, Connecticut, and Indiana

Benefits accessed by policyholders

(continued)

GAO-05-1021R Long-Term Care Partnership Program

34

30

Enclosure 1

Not

available

c

Not

available

c

365

New York

b

$26,685

$1,921,351

72

Indiana

a

$20,355

d

$10,869,369

d

899

Total

$3,699,361$5,248,657

Cumulative asset protection earned

that will not be accessed due to

policyholder dying while receiving

benefits

$30,076$15,483

Per capita asset protection earned

that will not be accessed due to

policyholder dying while receiving

benefits

123339

Number of policyholders who died

while receiving benefits

Connecticut

a

California

a

Table 11: Mortality Statistics for Partnership Policyholders

• 899 partnership policyholders died before exhausting their

long-term care insurance benefits (see table 11)

Sources: GAO analysis of data from

California Partnership for Long-Term Care

Connecticut Partnership for Long-Term Care

Indiana Long-Term Care Insurance Program

New York State Partnership for Long-Term Care

a

Based on data through March 2005

b

Based on data through December 2004

c

New York does not collect asset protection information

d

Based on data from California, Connecticut, and Indiana

Benefits accessed by policyholders

(continued)

(290470)

GAO-05-1021R Long-Term Care Partnership Program

35

This is a work of the U.S. government and is not subject to copyright protection in the

United States. It may be reproduced and distributed in its entirety without further

permission from GAO. However, because this work may contain copyrighted images or

other material, permission from the copyright holder may be necessary if you wish to

reproduce this material separately.

The Government Accountability Office, the audit, evaluation and

investigative arm of Congress, exists to support Congress in meeting its

constitutional responsibilities and to help improve the performance and

accountability of the federal government for the American people. GAO

examines the use of public funds; evaluates federal programs and policies;

and provides analyses, recommendations, and other assistance to help

Congress make informed oversight, policy, and funding decisions. GAO’s

commitment to good government is reflected in its core values of

accountability, integrity, and reliability.

The fastest and easiest way to obtain copies of GAO documents at no cost

is through GAO’s Web site (www.gao.gov). Each weekday, GAO posts

newly released reports, testimony, and correspondence on its Web site. To

have GAO e-mail you a list of newly posted products every afternoon, go

to www.gao.gov and select “Subscribe to Updates.”

The first copy of each printed report is free. Additional copies are $2 each.

A check or money order should be made out to the Superintendent of

Documents. GAO also accepts VISA and Mastercard. Orders for 100 or

more copies mailed to a single address are discounted 25 percent. Orders

should be sent to:

U.S. Government Accountability Office

441 G Street NW, Room LM

Washington, D.C. 20548

To order by Phone: Voice: (202) 512-6000

TDD: (202) 512-2537

Fax: (202) 512-6061

Contact:

Web site: www.gao.gov/fraudnet/fraudnet.htm

E-mail: [email protected]

Automated answering system: (800) 424-5454 or (202) 512-7470

Gloria Jarmon, Managing Director, [email protected] (202) 512-4400

U.S. Government Accountability Office, 441 G Street NW, Room 7125

Washington, D.C. 20548

Paul Anderson, Managing Director, [email protected] (202) 512-4800

U.S. Government Accountability Office, 441 G Street NW, Room 7149

Washington, D.C. 20548

GAO’s Mission

Obtaining Copies of

GAO Reports and

Testimony

Order by Mail or Phone

To Report Fraud,

Waste, and Abuse in

Federal Programs

Congressional

Relations

Public Affairs

PRINTED ON

RECYCLED PAPER