8-303-2023

2023

Nebraska

Corporation

Income Tax Booklet

Included in this Booklet are:

Form 1120N;

Schedules A, I, II, III, and IV;

Forms 7004N and PTC; and

Use Tax information.

Electronic ling and payment options are available.

Questions?

revenue.nebraska.gov

Sign up for a FREE subscription service at the Department of

Revenue’s website to get email updates on your topics of interest.

800-742-7474 (NE or IA) or 402-471-5729

revenue .nebraska.gov

2023 Nebraska Corporation Income Tax Return

Instructions

What’s New

Corporate Tax Rate Change (LB 432). For the 2023 taxable year the corporate tax rate for

Nebraska taxable income in excess of $100,000 is reduced from 7.50% to 7.25%. The corporate

rate for the rst $100,000 of Nebraska taxable income remains 5.58%.

Pass-Through Entity Tax (PTET) (LB 754). A partnership or S corporation may elect to be

subject to Nebraska income tax for tax years beginning on and after January 1, 2018. The

partners and shareholders of an electing entity will receive a refundable credit for their share

of the PTETs paid by the electing entity.

Nebraska Employer Tax Credit for Employing Convicted Felons (LB 917). Employers may

receive a nonrefundable credit for wages paid to an employee convicted of a felony. The

credit is equal to 10% of the wages paid to the employee during the taxable year. The credit

is limited to $20,000 for each eligible employee and applies to the wages paid during the

rst 12 months of employment. The employer must le an application with the Nebraska

Department of Revenue (DOR) to receive the credit.

Important Information for All Filers

Purpose. The instructions in this booklet provide guidance in completing the most common

Nebraska corporation income tax forms and schedules. This booklet is intended to be useful to

the greatest number of taxpayers. Nothing in these instructions supersedes, alters, or otherwise

changes any provisions of the Nebraska tax code, regulations, rulings, or court decisions.

We encourage the preparer of any Corporation Income Tax Return, Form 1120N, to review

applicable Nebraska law regarding any issue that may have a material effect on this return.

Nebraska law and other useful information may be found at revenue.nebraska.gov.

Income Subject to Nebraska Taxation. Nebraska income tax applies to the portion of the

corporate taxpayer’s taxable income derived from or attributable to sources within Nebraska.

A corporate taxpayer that is subject to tax in another state must apportion its income, unless

approval has been granted by the Tax Commissioner for an alternative method prior to

ling the return.

If a corporate taxpayer engaged in business in Nebraska is not subject to tax in another state,

its entire taxable income must be reported to Nebraska.

Combined Return. When a group of corporations conducts a unitary business, a single combined

return must be led reporting the income of the entire group. A unitary group engaged in

business within and without Nebraska will determine its Nebraska income using a single

factor, sales only, apportionment formula. See the Nebraska Schedule I — Apportionment

for Multistate Business instructions for additional information.

Enter All Amounts as Whole Dollars. Do not include cents on the return or schedules. Do not

change the pre-printed zeros in the cents column of the Form 1120N or schedules. Round

any amount from 50 cents to 99 cents to the next higher dollar. Round any amount less than

50 cents to the next lower dollar.

Penalties and Interest. Either or both may be imposed under the following conditions:

u Failing to le a return and pay the tax due on or before the due date;

u Failing to pay the tax due on or before the due date;

u Failing to le an amended Nebraska income tax return when required;

u Preparing or ling a fraudulent income tax return; or

u Understating income on an income tax return.

2

revenue .nebraska.gov

Filing a false or fraudulent Nebraska return is subject to penalty, even if the amounts reported

are taken from your federal return. Unpaid tax is subject to interest at the statutory rate of

5% from the original due date to the date the tax is paid. See Revenue Ruling 99-22-1 for

applicable interest rates.

Reporting Changes or Corrections. If information on a Nebraska corporation income tax

return previously led is incorrect, an Amended Nebraska Corporation Income Tax Return,

Form 1120XN, must be led. When ling an amended return, remember:

u Changes made by the IRS or another state must be reported to DOR within 60 days;and

u You must attach a copy of the related federal or other state amended return and all

related schedules or other documentation to explain the changes shown on the amended

Nebraska return.

Any corporation ling an amended return with the IRS, resulting in a credit or refund, must

report the change or correction within 60 days after receiving proof that the IRS accepted the

federal return. The Nebraska amended return must include documentation showing that the

IRS accepted the changes made on the federal return.

Corporate taxpayers are required to provide DOR with a copy of every executed Federal

Form872, Consent to Extend the Time to Assess Tax; Form 872-A, Special Consent to

Extend the Time to Assess Tax; or any other federal form used to extend the time to assess

income taxes. If copies of these federal forms are not provided to DOR within 30 days after

they are executed, DOR may issue a notice of deciency determination within one year after

discovery of the extension by DOR and may limit the time period for which interest is paid

on a refund.

Nebraska Extension of Time. An extension to le may only be obtained by:

u Attaching a copy of a timely-led Application for Automatic Extension of Time to File

Certain Business Income Tax, Information, and Other Returns, Federal Form 7004,

to the Nebraska return when led;

u Attaching a schedule to the Nebraska return listing the federal conrmation number

and providing an explanation that the electronic request for automatic federal extension

was not denied; or

u Filing a Nebraska Application for Extension of Time to File Corporation, Fiduciary,

or Partnership Return, Form 7004N, on or before the due date of the return, when you

need to make a tentative Nebraska payment or when a federal extension is not being

requested. When a federal extension of time has been granted, and additional time is

necessary to le the Nebraska return, the Nebraska Form 7004N must be led on or

before the date the federal extension expires. Remember to attach proof of the federal

extension to the Form 7004N.

Failure to attach the applicable extension document may result in a late ling penalty. An

extension of time only extends the date to le the return. It does not extend the due date

to pay the tax. Any tax not paid by the original due date is subject to interest. By timely

requesting an extension of time to le your federal return using the Federal Form 7004, you

are granted an automatic Nebraska extension for the same number of months granted by the

IRS. When a federal extension of time has been granted and additional time is necessary to

le the Nebraska return, the Nebraska Form7004N must be led on or before the date the

federal extension expires. An extension of time cannot exceed a total of seven months after

the original due date of the return.

Accounting Methods. The accounting method used for federal income tax purposes must be

used for Nebraska income tax purposes. A taxpayer may not change the accounting method

used to report income in prior years, unless the change is approved by the IRS. A copy of this

approval must accompany the rst return that shows the change in the method of accounting.

Federal Return. A copy of the federal return and supporting schedules, as led with the IRS,

must be attached to this return. This includes, at a minimum, a copy of the rst ve pages,

ScheduleD, Form 4797, and other supporting schedules of the Federal Form 1120. If a

consolidated federal return is led, a copy of the consolidating schedules or workpapers for

income and expenses, cost of goods sold, and balance sheets, as well as the Afliations Schedule,

Form851, must also be attached. Provide copies of schedules and other information that

3

revenue .nebraska.gov

support the numbers reported on the Nebraska return. Other voluminous information that

is part of the federal return led, but that is not directly related to the Nebraska reporting,

may be kept by the taxpayer, but must be made available upon request. A pro-forma federal

return is not acceptable. The Nebraska return is based upon the actual federal return as led

or prepared for ling.

Estimated Income Tax Payments. Estimated income tax payments must be made by every

corporation subject to taxation under the IRC, with income derived from Nebraska, if the

Nebraska income tax liability can reasonably be expected to exceed allowable credits by $400

or more. For additional information, see the 2024 Nebraska Corporation Estimated Income

Tax Payment Voucher Booklet.

Underpayment of Estimated Income Tax Penalty. A corporation may owe a penalty if the

amount of tax due, after allowable credits, is $400 or more.

If the amount of tax due is $400 or more, the corporation must complete a Corporation

Underpayment of Estimated Income Tax, Form 2220N, to calculate any applicable penalty.

A corporation may reduce or eliminate the penalty by using the annualized income or adjusted

seasonal installment method. To use one or both of these methods to calculate one or more

required installments, recalculate (and attach) the Federal Form 2220, Schedule A, “Adjusted

Seasonal Installment Method and Annualized Income Installment Method” using Nebraska

income and other Nebraska amounts. Enter the corresponding amount from the recalculated

Federal Schedule A on the appropriate lines of the Form 2220N.

Adjustment of Overpayment of Estimated Income Tax. A corporation that overpaid estimated

income tax must use the Corporation Application for Adjustment of Overpayment of Estimated

Income Tax, Form 4466N, to apply for refund of the overpayment when the overpayment is:

u At least 10% more than the expected tax liability calculated on the Form 4466N; and

u At least $500.

Form 4466N must be led by the 15th day of the third month after the end of the tax year

and before the corporation les its corporation income tax return. A Form 4466N led after

this date will not be considered. An extension of time to le the corporation income tax return

will not extend the time for ling Form 4466N.

Use Tax A corporation may be subject to use tax. A corporation owes use tax when the proper sales

tax has not been paid on purchases delivered into Nebraska. This often occurs when purchases

are made from out-of-state, mail order, or Internet sellers. Use tax is also due when items

purchased for resale are withdrawn from inventory for business or personal use.

Example 1.

The corporation purchased a computer from a seller in South Dakota over the Internet

for $1,570 plus $30 shipping and handling charges. Both charges are taxable. The

computer is shipped to the corporation in Scottsbluff, Nebraska and no tax is charged

or collected by the seller. The state tax is $88 ($1,600 X 5.5%) and the local tax is $24

($1,600 X 1.5%). The total use tax owed is $112 ($88 + $24 = $112).

Example 2.

A repair shop in Scottsbluff, Nebraska provides motor vehicle repair service. The repair

shop also owns a tow truck used for towing customers’ motor vehicles needing repair.

The shop purchases oil and oil lters tax exempt for resale using the Nebraska Resale

or Exempt Sale Certicate, Form 13. When oil and oil lters are removed from sales

tax exempt inventory and used to change the oil in the business-owned tow truck, state

and local use tax is due on the cost of the oil and oil lters.

For additional information, see the Nebraska Use Tax Information Guide.

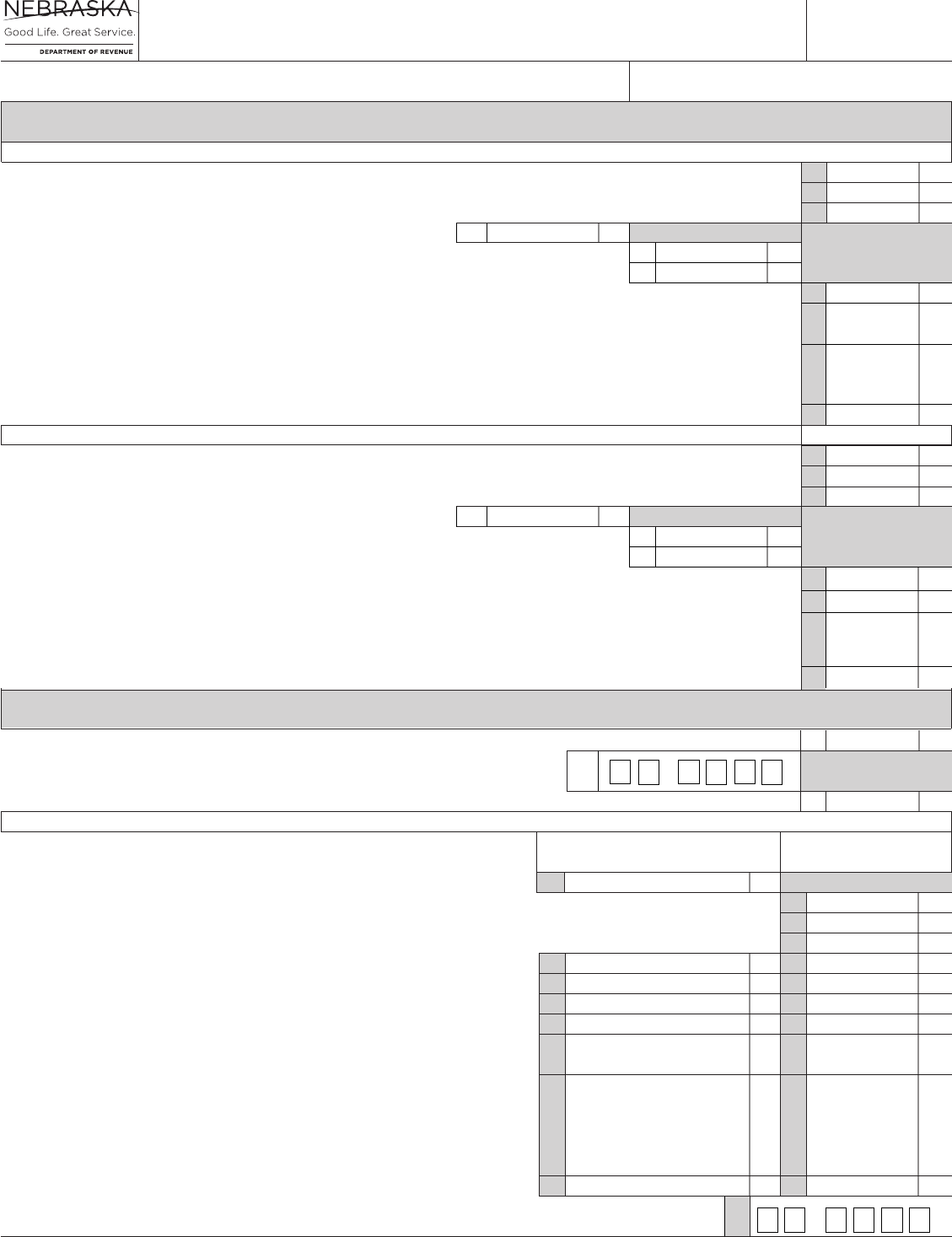

Purpose of Form The Nebraska Corporation Income Tax Return, Form 1120N, is used to report income,

gains, losses, deductions, and credits, and to calculate the income tax liability of the

corporate taxpayer.

4

revenue .nebraska.gov

Who Must File?

The Nebraska Corporation Income Tax Return, Form 1120N, must be led by every

corporation engaged in business in Nebraska, or having sources of income from Nebraska

and subject to federal corporation income tax. This includes:

uCooperative organizations. Cooperative organizations must le Form 1120N. Exempt farm

cooperatives must attach their U.S. Income Tax Return for Cooperative Associations,

Form 1120-C. Cooperatives may exclude patronage dividends, dividends on capital

stock, and nonpatronage income allocated to patrons that are allowable deductions

or exclusions for federal income tax purposes.

u Exempt organizations. All exempt organizations required to le a federal return and

pay tax at the federal corporation income tax rates on unrelated business income are

required to le the Form 1120N.

Corporations that must le a different Nebraska return:

u S corporations. Corporations that have elected to le under Subchapter S, as dened

by IRC § 1361, le a Nebraska S Corporation Income Tax Return, Form 1120-SN.

u Financial institutions. Institutions that are chartered or qualied to do business in

Nebraska, or maintain a permanent place of business in Nebraska and actively solicit

deposits from residents of Nebraska must le a Nebraska Financial Institution Tax

Return, Form1120NF.

When and Where to File

This return must be led on or before the date the related federal income tax return is due.

Use the Federal/State e-le program to e-le both federal and state tax returns. Or mail the

Form 1120N to:

Nebraska Department of Revenue

PO Box 94818

Lincoln, NE 68509-4818

How to Complete Form 1120N

Tax Period. A 2023 Form 1120N must be used to le for the calendar year 2023, or a scal

year beginning in 2023. Space is provided at the top of the return to enter the beginning and

ending dates for short-period or scal-year lers. The taxable year for Nebraska must be the

same as the taxable year used for the federal income tax return.

If a corporation changes its federal taxable year, it must also change its Nebraska taxable

year. A copy of the approval from the IRS to change accounting periods must accompany

the rst return that shows the change.

Business Classication Code. Enter the six-digit code that best describes the corporation’s

principal business activity in Nebraska. Carefully review the business classication codes

before you select one.

Principal Business Activity in Nebraska. Enter the principal business activity of the corporation

from the Business Classication Code listing.

Federal ID Number. Enter the Federal ID number assigned to the corporation by the IRS.

5

revenue .nebraska.gov

Nebraska ID Number. Enter the Nebraska ID number assigned to the corporation by DOR.

Corporations that do not have a Nebraska state ID for corporate income tax should e-le

using their Nebraska income tax withholding or sales tax number. The prex (for example, 24-)

is not part of the state ID number and should not be included in the number. Corporations

that do not have an existing Nebraska state ID, should apply using DOR’s Online Nebraska

Tax Application.

Final Return. Check the “Final Return” box if the corporation will not le a Nebraska

corporate return after the 2023 tax year. This may occur when the corporation ceases to

exist due to dissolution or merger, or when the corporation will be included in a new unitary

group of corporations led under a different Nebraska ID number.

Corporation Filing Status. All taxpayers must complete this portion of the return and answer

all questions applicable to the corporation’s status.

Question A. Check “Yes” if any of the following conditions apply:

u The corporation was included in a federal consolidated return;

u The corporation owns 50% or more of another corporation; or

u The corporation is owned at least 50% by another corporation.

If none of the above conditions apply, check “No” and skip questions B, C, and D.

Question B. Check “Yes” if this return includes the income, deductions, or credits of all

corporations with common ownership.

Check “No” if one or more of the corporations with common ownership are not included

in this return.

Question C. Check “Yes” if a return led in any other state included the income, deductions,

or credits of more than one corporation.

Check “No” if the returns led in all other states included only your corporation.

Question D. Under Nebraska law, a unitary group generally encompasses all corporations

included in the federal consolidated income tax return. Therefore, only under extremely unusual

circumstances may a corporation compute its Nebraska liability using the “separate report

by a member of a controlled group of corporations” method. Documentation supporting

the separate company ling should be attached to the Nebraska return when led. This

documentation must show that the corporation is not part of a single economic unit as dened

in section .08 of Corporate Income Tax Regulation 24-058, Denitions.

Line 1 Federal Gross Sales or Receipts, Less Returns and Allowances. Enter the amount of federal

gross sales or receipts reported on Federal Form 1120, less returns and allowances. If the

corporate taxpayer is ling a combined Form 1120N, enter the amount of combined gross

receipts or sales less returns and allowances from Nebraska Schedule IV.

Line 2 Federal Taxable Income (FTI). Enter the federal taxable income. A unitary group must enter

the amount from line 30, Nebraska Schedule IV.

Line 3 Adjustments Increasing FTI. Enter the amount from line 10, Nebraska Schedule A.

The federal deduction for state income tax is not an adjustment increasing federal

taxableincome.

State and local government bond interest and dividend income should be included on line3.

See the instructions for line 1, Nebraska Schedule A.

Line 4 Adjustments Decreasing FTI. Enter the amount from line 20, Nebraska Schedule A.

Line 5 Adjusted FTI. Enter line 2 plus line 3 minus line 4.

Line 6 Nebraska Taxable Income Before Nebraska Carryovers. If all of the income earned by the

corporation is derived from Nebraska sources, enter the amount from line 5 on line 6.

Corporate taxpayers that derive income from sources within and without Nebraska and are

taxable in another state, must enter the amount from line 3, Nebraska Schedule I, Form 1120N.

6

revenue .nebraska.gov

Line 7 Nebraska Capital Loss Carryover. Enter the allowable Nebraska capital loss carryover.

For a multistate taxpayer, a Nebraska capital loss consists of the loss on property that was

used by the unitary business that did business in Nebraska, multiplied by the Nebraska

apportionment factor for the year of the loss. If the corporate taxpayer reported a capital

loss on corporate stock or other assets, the income from which was not previously treated as

income apportionable to Nebraska, the loss cannot be treated as a Nebraska loss. Capital loss

carryovers may only be deducted to the extent of capital gains in the year of the deduction.

Attach a detailed schedule that shows the computation of the capital loss carryover along

with copies of the applicable Federal Schedule D to substantiate the Federal capital (loss)/

gain. A Nebraska capital loss may only be carried forward, and only for a maximum period of

ve tax years.

Line 8 Nebraska Taxable Income After Nebraska Capital Loss Carryover. Enter line 6 minus line7.

Line 9 Nebraska Net Operating Loss Carryover. Enter the allowable Nebraska net operating loss

(NOL) carryover. The amount allowable is based on the loss previously reported to Nebraska,

and is not based on a percentage of the federal carryover. Any net operating loss can only

be carried forward. An NOL incurred in tax years beginning on and after January 1, 2014,

may be carried forward for a maximum period of 20 taxyears. Nebraska imposes limitations

on the use of a NOL carryforward after certain reorganizations and mergers, when a NOL

incurred in years after 2017 is carried forward to a year after 2020, and when a corporation

with a Nebraska NOL carryforward becomes a member of a unitary group. For additional

information, see Corporate Income Tax Regulation 24-060, Net Operating Losses and Capital

Losses. If any of the limitations apply to the NOL carryforward reported on this return,

attach a schedule showing the computation of the allowablecarryforward.

Attach a Nebraska Corporation Net Operating Loss Worksheet showing the calculation of

the amount of Nebraska net operating loss carryover. If the Nebraska NOL carryforward

was increased due to reclassifying part or all of the charitable contribution carryforward,

details of the reclassication and the NOL modication must be provided.

Line 10 Net Nebraska Taxable Income. Enter line 8 minus line 9.

Line 11 Nebraska Tax. Use the following tax rate schedule to calculate the amount of total Nebraska

tax to enter on line 11.

2023 Tax Rate Schedule

If Net Nebraska Taxable

Income from line 10 is —

Over But Not Over Tax Rate is On Excess Over

$ 0 $100,000 5.58% $ 0

$100,000 $5,580 + 7.25% $100,000

The tax rate is the rate in effect on the rst day of the corporation’s taxable year. Corporations

ling on a scal-year basis or ling a short-period return will compute the tax liability for

the entire taxable period by using the tax rate in effect on the rst day of the taxable period.

A corporation using a 52-53 week scal year beginning during the last week in December

must use the rate in effect on the following January 1st.

Insurance Companies. Check the box to indicate you are an insurance company. The tax rate

used by an insurance company is the lesser of the rates listed above, or the corporation income

tax rate imposed by the state or country where the insurance company is domiciled, provided:

u The insurance company can show the Tax Commissioner that it is domiciled in a state

other than Nebraska, or out of the country; and

u The state or country of domicile imposes on Nebraska domiciled insurance

companies a retaliatory tax against Nebraska’s corporation income tax under

Neb. Rev. Stat. § 77-2734.02.

7

revenue .nebraska.gov

Line 12 Premium Tax Credit. Enter the total amount of premium taxes paid (not accrued) by the

corporate taxpayer in this taxable year. These taxes include:

u Premium taxes paid to the Nebraska Department of Insurance (NDOI) under

Neb. Rev. Stat. §§ 77-908 and 81-523; and

u Assessments paid to the NDOI for the Comprehensive Health Insurance Pool that are

allowed as an offset against any related premium and related retaliatory tax liability

under Neb. Rev.Stat. § 44-4233.

Premium taxes do not include amounts shown on the NDOI annual tax return as fees or the

Workers’ Compensation Court cash fund tax.

Example 3.

An insurance company made the following 2023 estimated premium tax payments and

payments with its 2022 and 2023 NDOI returns.

Tax Payment Payment Payment 2023 Premium

Year Type Date Amount Tax Credit

2022 Payment with return March 1, 2023 $3,000

Less: Fees included on the 2022 return 100 $ 2,900

2023 Estimated April 15, 2023 4,000 4,000

2023 Estimated June 15, 2023 4,000 4,000

2023 Estimated Sept. 15, 2023 4,000 4,000

2023 Payment with return March 1, 2024 4,000 0

Total $14,900

In this example, the insurance company will enter $14,900 on line 12 as a credit for premium

taxes paid.

A corporation claiming this credit must attach a copy of the NDOI annual tax return related

to any payment claimed as a credit for premium taxes paid. A schedule listing the date and

amount of payment and the payee must also be attached.

Amounts paid by an electric cooperative organized under the Joint Public Power Authority

Act, Neb. Rev. Stat. § 70-1401, as in lieu of intangible tax, may also be included on this line.

Line 13 Employer’s credit for expenses incurred for TANF (ADC) recipients. Enter the total credit

from line 2, Form TANF.

Line 14

Community Development Assistance Act Credit. The Nebraska Community Development

Assistance Act credit is allowable for contributions to approved projects of community

betterment organizations recognized by the Nebraska Department of Economic Development

(DED). Attach the 2023 Nebraska Community Development Assistance Act Credit

Computation, Form CDN, to the Form 1120N. Corporations do not need to attach a copy of

the Form 1099NTC. DOR will receive the Form 1099NTC information directly fromDED.

For more details regarding this credit, contact:

Nebraska Department of Economic Development

245 Fallbrook Blvd, Suite 002

PO Box 94666

Lincoln, Nebraska 68521

opportunity.nebraska.gov

Darin Lubke

402-471-3116

Line 15 Form 3800N Nonrefundable Credit. Enter the total nonrefundable tax credits reported on

the Nebraska Incentives Credit Computation, Form 3800N. Attach a copy of Form 3800N

and any supporting schedules.

8

revenue .nebraska.gov

Line 16 Nebraska Employer Tax Credit for Employing Convicted Felons. Enter the certied credit

amount and the certicate number from the Nebraska Employer Tax Credit Application for

Employing Convicted Felons, Form ETC-A.

Line 17 Total Nonrefundable Credits. Enter the total of lines 12 through 16.

Line 18 Nebraska Tax After Nonrefundable Credits. Subtract line 17 from line 11. If line 17 is more

than line 11, enter zero. Any excess will not be allowed as an overpayment on line 31; nor

may it be used as a carryback or carryover to other taxable years.

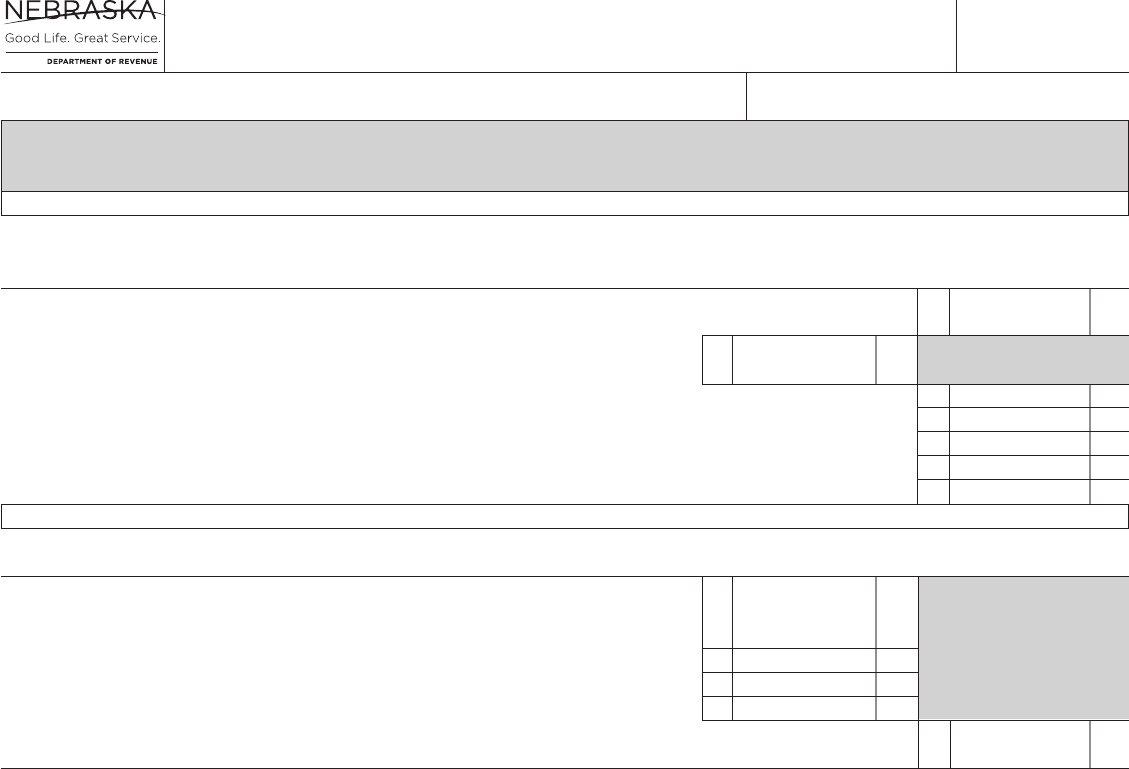

Line 19 Form 3800N Refundable Credit. Enter the total refundable tax credits reported on Form

3800N. Attach a copy of Form 3800N and any supporting schedules.

Line 20 Tax Deposited With Form 7004N. Enter the amount of the tentative tax payment entered on

line 11 of the Form 7004N.

Line 21 2023 Estimated Income Tax Payments. Enter the total 2023 estimated income tax payments,

less any Form 4466N adjustment. Combined lers must complete and attach Nebraska

ScheduleIII.

Line 22 Beginning Farmer Credit. Enter the amount of Beginning Farmer credit from the Statement of

Nebraska Tax Credit, Form 1099BFC. The Beginning Farmer credit is available to owners of

agricultural assets, when the agricultural assets are rented to qualifying beginning farmers or

livestock producers. Any claimant eligible for the credit will receive a copy of the Statement

of Nebraska Tax Credit, Form 1099BFC, from the Nebraska Department of Agriculture.

Corporations do not need to attach a copy of the Form 1099BFC. DOR will receive the

Form 1099BFC information directly from the Nebraska Department of Agriculture.

For more details regarding this credit, contact:

Nebraska Department of Agriculture

PO Box 94947

Lincoln, NE 68509-4947

402-471-4876

nextgen.nebraska.gov

Line 23 Nebraska Income Tax Withheld. Enter the amount of Nebraska withholding from

Form1099-MISC or Form 1099-NEC. Construction contractors are required to withhold

5% of any payment or payments exceeding $600 made to construction subcontractors that are

not registered on the Nebraska Department of Labor’s Contractor Registration Database. If

an amount was withheld from your corporation under this provision, a credit for the amount

withheld is claimed on line 23.

Line 24 Credit for School District Property Taxes. Enter the amount from line 1, Form PTC and

attach Form PTC.

Line 25 Credit for Community College Property Taxes. Enter the amount from line 2, Form PTC and

attach Form PTC.

Line 26 PTET Credit. Enter the name, Nebraska ID Number, and amount of pass-through entity tax

(PTET) credit received from a partnership in which you hold an ownership interest. Attach

a schedule if you received the credit from more than one partnership. Also attach a copy of

the Nebraska Schedules K-1N supporting the credit claimed.

Line 27 Total Refundable Credits and Payments. Enter the total of lines 19 through 26.

Line 28 Tax Due. Enter the result of line 18 minus line 27. If the amount is less than zero, enter zero.

Line 29 Penalty for Underpayment of Estimated Income Tax. Use Nebraska Corporation Underpayment

of Estimated Income Tax, Form 2220N, to determine if the corporation owes this penalty.

A Form 2220N must be completed if the Nebraska tax less allowable credits is greater than

$400. If the corporation is required to complete Form 2220N, enter the amount of penalty

from line 20, Form2220N.

9

revenue .nebraska.gov

Line 30 Amount Due. There is an amount due when line 27 is less than the total of lines 18 and 29.

Mandates of Electronic Payment. Some entities are required to make their payments (tax,

penalty, and interest) electronically. For mandate purposes, all of the electronic payment

options identied below satisfy the mandate requirement. All entities are encouraged to make

their paymentselectronically.

Electronic Payment Options

Electronic Funds Withdrawal (EFW). With this payment option, you provide your

payment information within your electronically-led return. Your payment will

automatically be withdrawn from your bank account on the date you specify.

Nebraska e-pay. Nebraska e-pay is DOR’s web-based electronic payment system. You

enter your payment and bank account information, and choose a date (up to a year

in advance) to have your account debited. You will receive an email conrmation for

each payment scheduled.

ACH Credit. You (or your bank) create an electronic le in the appropriate ACH le

format. It is submitted to the Federal Reserve and instructs your bank to “credit” the

state’s bankaccount.

Nebraska Tele-pay. Nebraska Tele-pay is DOR’s phone-based electronic payment

system. Call 800-232-0057, enter your payment and bank account information, and

choose a date (up to a year in advance) to have your account debited. You will receive

a conrmation number at the end of your call.

Credit Card. Secure credit card payments can be initiated through ACI Payments,

Inc. at acipayonline.com or via phone at 800-272-9829. Eligible credit cards include

American Express, Discover, MasterCard, and VISA. A convenience fee is charged

to the card you use. This fee is paid to the credit card vendor, not the State, and will

appear on your credit card statement separately from the payment made to DOR. At

the end of your transaction, you will be given a conrmation number. Keep this number

for your records. [If you are making your credit card payment by phone, you will need

to provide the Nebraska Jurisdiction Code, which is 3700.]

Cancel a payment. To cancel a scheduled EFW payment, contact our Taxpayer

Assistance ofce at 800-742-7474 or 402-471-5729 before 4:00 pm Central Time at

least two business days prior to your scheduled payment date. You may cancel a

payment scheduled through Nebraska e-pay by logging into the e-pay program from

our website and selecting “cancel payment.” To cancel a credit card payment, contact

ACI Payments, Inc.

Check or Money Order. If you are not using one of the electronic payment options described

above, include a check or money order payable to the “Nebraska Department of Revenue.”

Checks written to DOR may be presented for payment electronically.

Line 31 Overpayment. If line 27 is greater than the sum of lines 18 and 29, enter the result of line 27

minus the total of lines 18 and 29.

Line 32 Amount Credited to 2024 Estimated Income Tax. Enter the amount of overpayment shown

on line 31 that you want credited as a tax year 2024 estimated income tax payment for

thecorporation.

Line 33 Overpayment to be Refunded. Enter the amount of overpayment shown on line 31 that you

want refunded. The overpayment to be refunded is calculated by subtracting line 32 from line

31. DOR recommends having any refund on line 33 directly deposited to the corporation’s

bank account. See line 34 instructions below.

Line 34 Direct Deposit. To deposit the refund directly into the corporation’s checking or savings

account, enter the routing number and account number found on the bottom of the checks

used with the account. The routing number is listed rst and must be nine digits. The account

number is listed to the right of the routing number and can be up to 17 digits. Enter these

numbers in the boxes found on lines 34a and 34c, and complete line 34b, Type of Account.

The box on line 34d must be checked if the refund will go to a bank account outside the

United States. This is necessary to comply with banking rules regarding International ACH

Transactions (IATs). These refunds cannot be processed as direct deposits and instead will

be mailed.

10

revenue .nebraska.gov

Signature Sign and Date the Tax Return. This return must be signed by a corporate ofcer. Include

a daytime phone number and email address in case DOR needs to contact you about

youraccount.

Email. By entering an email address, the taxpayer acknowledges that DOR may contact

the taxpayer by email. The taxpayer accepts any risk to condentiality associated with this

method of communication. DOR will send all condential information by secure email or

the State of Nebraska’s le share system. If you do not wish to be contacted by email, write

“Opt Out” on the line labeled “email address.”

If a corporate ofcer authorizes another person to sign the return, there must be a Power of

Attorney, Form 33, on le with DOR or attached to the return.

The act of e-ling a return is your signature. By e-ling the return, taxpayers and their tax

preparers, if applicable, are declaring under penalties of perjury, that they have examined the

electronic return, and to the best of their knowledge and belief, it is true, correct, and complete.

Paid Preparer’s Use Only. Any person who is paid for preparing a taxpayer’s return must sign

the return as preparer. Additionally, the preparer must enter their Preparer Tax Identication

Number (PTIN), their rm’s name, and Federal Employer Identication Number (EIN).

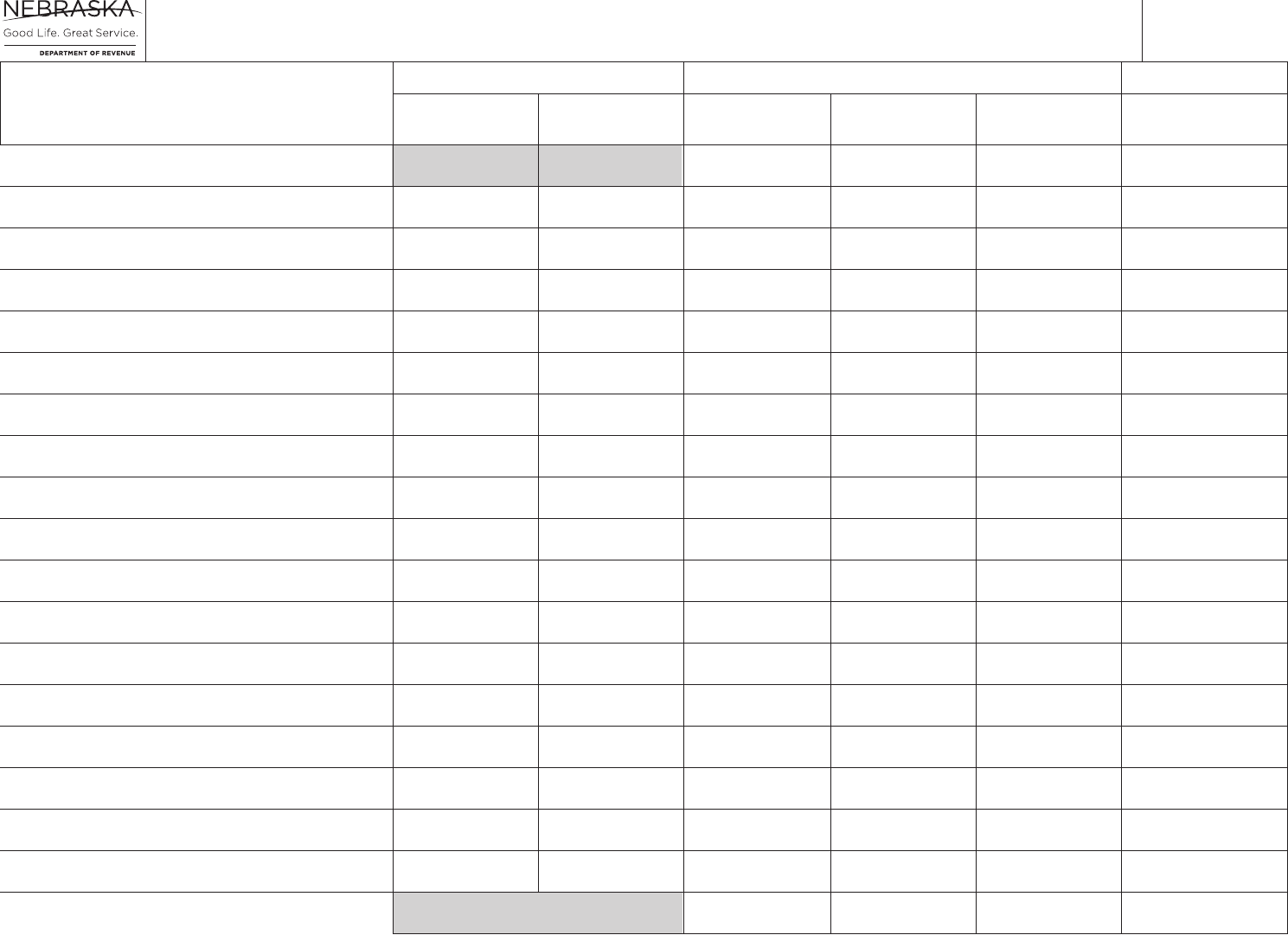

Purpose. The Nebraska Schedule A is used to adjust the corporate taxpayer’s FTI reported

on line2 of the Form 1120N. The Nebraska Schedule A must be completed by all corporate

taxpayers making any adjustments on lines 3 or 4 of Form 1120N. Any adjustments that

are summarized on Nebraska Schedule A are carried forward to lines 3 and 4, Form 1120N.

Adjustments Increasing FTI

Line 1 State and Local Government Interest and Dividend Income. Enter all state and local government

interest or dividends that are exempt from federal income tax and not issued by Nebraska

state and local government subdivisions.

Line 2 Federal Net Operating Loss Deduction. Enter the federal net operating loss allowed as a

deduction on the federal return. See line 9, Form 1120N instructions for allowable Nebraska

net operatinglosses.

Line 3 Federal Capital Loss Carryover. Enter the portion of the federal capital loss carryover

allowed as a deduction this year. See line 7, Form 1120N instructions for allowable Nebraska

capitallosses.

Line 4 Allocable, Nonapportionable Loss. Enter the amount of any claimed allocable, nonapportionable

loss. Allocable, nonapportionable loss is a loss that is not part of the unitary business, and has

not been claimed as a loss that is part of the unitary business that is subject to apportionment

by another state with substantially the same law as Nebraska.

Attach a detailed description of the claimed amount, together with evidence that the loss is

not part of the unitary business. Also, attach an afdavit from a corporate ofcer that the

corporate taxpayer has not claimed the same loss to be a part of a unitary business subject to

apportionment in another state with substantially the same law as Nebraska on apportionability

of losses. Note that Nebraska law is unique on apportionability of losses. Therefore, it may

be extremely difcult for a corporate taxpayer to meet the above requirements.

11

Nebraska Schedule A Instructions

Adjustments to FTI

revenue .nebraska.gov

Line 5 Related Expenses. Enter the amount of related expenses. Related expenses include all direct

and indirect expenses attributable to the activities producing the allocable, nonapportionable

loss entered on line 4.

Line 6 Interest Expense Disallowance. Enter the interest expense calculated for the allocable,

nonapportionable loss.

To calculate the interest expense:

uDivide the taxpayer’s average investment in the activities producing the allocable,

nonapportionable loss by the taxpayer’s average total assets to obtain a ratio; and

u Multiply this ratio by the total interest deduction allowed in the computation of federal

taxable income.

Line 7 Total Allocable, Nonapportionable Loss. Enter the result of line 4 plus lines 5 and 6.

Line 8 Nebraska and Local Income, Sales, and Use Taxes Deducted on Federal Form 1065 Under

Section 164 of the IRC. Enter the amount of taxes from line 15, Schedule K-1N, Form 1065N.

Line 9 Other Increasing Adjustments. Enter any other adjustment increasing FTI not reported on

lines2 through 8. List the type of adjustment on line 9a, Schedule A, and the associated

amount on line9b. Attach a detailed explanation of the basis for each adjustment and any

necessaryschedules.

Line 10 Total Adjustments Increasing FTI. Enter the result of line 1 plus lines 2, 3, 7, 8, and 9 here

and on line 3, Form 1120N.

Adjustments Decreasing FTI

Line 11 Qualied U.S. Government Interest Deduction. Enter the amount of interest and dividend

income from U.S. government obligations exempt from state taxation.

The Taxability of Interest and Dividend Income From State, Local, and U.S. Government

Obligations Information Guide, lists U.S. interest and dividend income that can be included

on line 11, Nebraska Schedule A. Interest income from repurchase agreements involving U.S.

government obligations is not deductible as U.S. government interest.

Gains or losses from the sale or other disposition of federal securities are taxable for state

income tax purposes and should not be included on line 11.

Line 12 Total Foreign Dividends. Enter the amount of total foreign dividends from line 7, Nebraska

Schedule II.

Line 13 Special Foreign Tax Credit Adjustment. Enter the amount of adjustment from line 12, Nebraska

Schedule II.

Line 14 Allocable, Nonapportionable Income. Enter the amount of any claimed allocable,

nonapportionable income. Allocable, nonapportionable income is income that is not part of

the unitary business, and has not been claimed as income that is a part of the unitary business

that is subject to apportionment by another state with substantially the same law as Nebraska

on apportionability of income. Note that Nebraska law is unique on apportionability of

income. Therefore, it may be extremely difcult for a corporate taxpayer to meet the above

requirements.

Note: Entries must be made on lines 15 and 16, or the entire amount of allocable, nonapportionable

income claimed may be disallowed.

Attach a detailed description of the claimed amount, together with evidence that the income

is not part of a unitary business. Also, attach an afdavit from a corporate ofcer that the

corporate taxpayer has not claimed the same income to be a part of a unitary business subject

to apportionment in another state with substantially the same law as Nebraska.

12

revenue .nebraska.gov

Line 15 Related Expenses. Enter the amount of related expenses. Related expenses include all direct

and indirect expenses attributable to the activities producing the allocable, nonapportionable

income amount entered on line 14.

Line 16 Interest Expense Disallowance. Enter the interest expense calculated for the allocable,

nonapportionable income.

To calculate the interest expense:

u Divide the taxpayer's average investment in the activities producing the allocable,

nonapportionable income by the taxpayer's average total assets to obtain a ratio; and

u Multiply this ratio by the total interest deduction allowed in the computation of federal

taxable income.

Line 17 Net Allocable, Nonapportionable Income. Enter the result of line 14 minus lines 15 and 16.

Line 18 Nebraska College Savings Program. Nebraska allows a subtraction from a participant’s federal

taxable income for the amount of annual contributions made to an account established under

the Nebraska Educational Savings Plan Trust. The maximum annual exempt contribution per

return is $10,000. Contributions to other states’ 529 college savings plans cannot be deducted

on line 18.

Interest and earnings from the Nebraska College Savings Program may be deducted to the

extent that the income is included in federal taxable income. This adjustment must be taken

on line 19, Other Decreasing Adjustments.

Line 19 Other Decreasing Adjustments. Enter any other applicable adjustment not reported on

lines 11 through 18. List the type of adjustment on line 19a, Schedule A, and the associated

amount on line19b. Attach a detailed explanation of the basis for each adjustment and any

necessaryschedules.

Note: This line should only be used in extremely unusual circumstances as virtually all valid

adjustments should be claimed elsewhere on Nebraska Schedule A.

The following examples are items that are not allowable adjustments decreasing federal

taxable income:

u Global Intangible Low-Taxed Income (GILTI). See DOR’s General Information

Letters 24-20-1, Global Intangible Low-Taxed Income and Foreign-Derived

Intangible Income for information regarding Nebraska’s treatment of

GILTI inclusions;

uThe wage expense disallowed by the work opportunity tax credit;

u Federal income taxes or other federal taxes paid;

u The depreciation disallowed by the investment credit or other federally-required

basis reduction;

u Income earned in another state. Instead, Nebraska Schedule I, Apportionment for

Multistate Business, must be completed; and

u Income from a partnership. For additional information, see Business Entity Regulation

24-315, Sales Factor; Business Entities As Owners in a Partnership or Joint Venture.

Line 20 Total Adjustments Decreasing FTI. Enter total adjustments here and on line 4, Form 1120N.

13

revenue .nebraska.gov

Purpose. The Nebraska Schedule I is used to determine the amount of Nebraska source

income (Form 1120N, line 6, Nebraska taxable income before Nebraska carryovers) received

by a corporation that derives income from within and without Nebraska.

Nebraska source income is determined by apportioning the corporate income using a single,

sales only factor. Apportionment refers to the division of income between states by the use

of a formula containing one or more apportionment factors.

Sales Factor. The sales factor is a fraction. The numerator is the total sales of the corporate

taxpayer in Nebraska during the taxable year. The denominator is the total sales of the

corporate taxpayer everywhere during the taxable year. Total sales include gross sales of

real and tangible personal property, less returns and allowances, and all other items of gross

receipts, except income for the discharge of indebtedness, amounts received from hedging

transactions involving intangible assets, and net gains from marketable securities held for

investment. The sales factor on this schedule is rounded to six decimal places. It is entered

as a percentage.

When a corporate taxpayer consists of two or more corporations engaged in a unitary

business, a part of which is conducted in Nebraska, the income of the corporate taxpayer

apportioned to Nebraska is determined by applying the ratio of the corporate taxpayer’s

sales in Nebraska to the sales of the entire unitary group. The corporate taxpayer’s sales

in Nebraska should include only those sales made by members of the unitary group with

nexus in this state. Each corporate taxpayer must le one income tax return for the entire

group. The return will include all corporations in the unitary business. Any corporation that

is required, or has received permission, to use an alternative apportionment formula, may

only be included in a return with other corporations using the same apportionment formula.

For tax years beginning January 1, 2014 or after, a corporation may no longer use the costs

of performance method of apportioning sales other than sales of tangible personal property

except for a corporation operating as a communications company. For additional information,

see the Nebraska Apportionment Factor - Sales or Gross Receipts section.

A corporation using an alternative method of apportionment must attach a copy of the

Tax Commissioner’s prior written approval of the alternative method. The alternative

apportionment factor computation must be included. Enter the factor on line 2, Nebraska

Schedule I.

NOTE: Approval of an alternative method of apportionment is rare.

Intercompany sales between unitary corporations using the combined income approach are

excluded from the sales factor.

If the corporate taxpayer is a partner in a partnership or joint venture, see Business Entity

Regulation 24-315, Sales Factor; Business Entities As Owners in a Partnership or Joint Venture.

A corporate taxpayer that operates a trucking business and has income from both within

and without this state, must compute its sales factor in accordance with Business Income

Tax Regulation 24-343, Special Apportionment Rules; All Tax Years; Trucking Companies.

The method of computing the sales factor must be consistent with prior tax years and with the

corporate taxpayer’s lings in other states. If the corporation modies the basis for including

or excluding gross receipts in the sales factor used in returns for prior years, the 2023 return

must disclose the nature and extent of the modication.

If the corporation les returns with other states that are not uniform in the inclusion or

exclusion of gross receipts, the Form 1120N led with DOR must disclose the nature and

extent of the variance.

14

Nebraska Schedule I Instructions

Apportionment for Multistate Business

revenue .nebraska.gov

Computation of Nebraska Source Income

Line 1 Adjusted FTI. Enter the amount from line 5, Form 1120N.

Line 2 Nebraska Apportionment Factor. Enter the amount from line 15, Nebraska Schedule I,

Form1120N.

Line 3 Taxable Income Apportioned to Nebraska. Enter in line 3 the result of line 1 multiplied by

line 2. Also enter this amount on line 6, Form 1120N.

Nebraska Apportionment Factor – Sales or Gross Receipts

Nebraska sales include all items of income received by the corporate taxpayer from Nebraska

sources. The following types of sales are from Nebraska sources:

u Sales of tangible personal property delivered in this state;

u Sales of tangible personal property shipped from Nebraska to the U.S. government;

u Gross receipts from the interest or service charges arising from the sale of tangible

personal property if the sale is attributed to Nebraska;

u Sales of other than tangible personal property –

PTo the extent a service relates to real or tangible personal property located

inNebraska;

P To the extent a service relates to part of the buyer’s trade or business operated

inNebraska;

P A service provided to an individual present in Nebraska at the time the service

isreceived;

PTo the extent an application service is used in Nebraska;

PTo the extent intangible property is used in Nebraska;

PTo the extent an intangible asset used in a treasury function is managed inNebraska;

PTo the extent a loan is secured by real or tangible personal property located

inNebraska;

PTo the extent a loan is not secured by real or tangible personal property, if the

borrower is in this state. The location is presumed to be the borrower’s billing

address.

PFees, charges, and net gains from credit card receivables, if the credit card holder’s

billing address is in Nebraska;

P Gross receipts from the sale, rental, or lease of real property if the real property

is located in Nebraska;

P Gross receipts from renting, leasing, or licensing tangible personal property if the

property is in Nebraska. If the property was located within and without Nebraska

during the taxable year, then the gross receipts are attributable to Nebraska in

proportion to the percentage of time the property was located in Nebraska;

PFor sales not specically addressed above, sales to an individual if the individual's

billing address is in Nebraska, and sales to a business if the business places its

order from Nebraska or the billing address of the business if the ordering place

cannot be readily determined; and

PSales made by a communications company if the income-producing activity is

performed in Nebraska based on costs of performance.

For additional information, see Neb. Rev. Stat. § 77-2734.14.

Line 4 Sales or Gross Receipts Minus Returns and Allowances. Enter the gross receipts, less any

returns and allowances reported on the Federal Form 1120.

15

revenue .nebraska.gov

16

Line 5 Sales Delivered or Shipped to Purchasers in Nebraska: Shipped From Outside Nebraska.

Delivery in Nebraska is determined without regard to the F.O.B. point or other conditions

of the sale. The amount entered on this line should not include sales to the U.S. government.

Line 6 Sales Delivered or Shipped to Purchasers in Nebraska: Shipped From Within Nebraska. Delivery

in Nebraska is determined without regard to the F.O.B. point or other conditions of the sale.

The amount entered on this line should not include sales to the U.S. government.

Line 7 Sales Shipped From Nebraska to the U.S. Government. The U.S. government is the

purchaserwhen it makes direct payment to the seller. The amount on this line includes all

sales of tangible personal property to the U.S. government that are shipped from an ofce,

store, warehouse, factory, or other place of business in this state. For other sales made to

the U.S. government, use the rules for sales of other than tangible personal property. For

additional information, see Neb.Rev.Stat.§77-2734.14.

Line 8 Interest on Sales of Tangible Personal Property. In the Total column, enter all interest or

service charges received from the sale of tangible personal property.

In the Nebraska column, enter all the interest or service charges related to the sale of tangible

personal property delivered in Nebraska and from sales to the U.S. government shipped

from Nebraska.

Line 9 Interest, Dividends, and Royalties From Intangible Property. In the Total column, enter all

the interest, dividend, and royalty income from intangible property received by

thecorporation.

In the Nebraska column, enter the amount sourced to Nebraska as determined by

Neb.Rev.Stat.§77-2734.14(3).

Line 10 Gross Rents. In the Total column, enter the gross receipts from the rental or lease of all real

or tangible personal property.

In the Nebraska column, enter the gross receipts from the rental or lease of real or tangible

personal property located in Nebraska. If the tangible personal property rented or leased

is located or used both inside and outside this state, the Nebraska receipts are attributable

to Nebraska in proportion to the percentage of time the property was located in Nebraska.

Line 11 Net Gain on Sales of Intangible Property. In the Total column, enter the net gain on sales of

all intangible property made during the tax year.

In the Nebraska column, enter the amount of net gain from sales made to a buyer who uses

the intangible in Nebraska as determined by Neb. Rev. Stat. § 77-2734.14.

NOTE: A net loss on the sale of intangible property is not included in the calculation of the

Nebraska sales factor.

Line 12 Gross Receipts From Sales of Tangible Personal and Real Property Not Included Above. In

the Total column, enter the gross receipts from sales of all tangible personal property and

real property not included above.

In the Nebraska column, enter the gross receipts from sales of real property located in

Nebraska. Also enter the gross receipts from tangible personal property delivered in this

state or delivered to the U.S. government from a location in this state.

Line 13 Other Income. In the Total column, enter any other income not reported above that was

received by the corporation.

In the Nebraska column, enter any other income not reported above that was derived from

Nebraskasources.

The amounts entered on this line include, but are not limited to, net farm income (loss)

subpart F inclusions, GILTI, and the ordinary business income (loss) from partnerships. If

the corporation would be considered unitary with the partnership if the partnership was a

corporation, enter the distributive share of the partnership’s gross receipts. If the corporation

and the partnership would not be considered unitary, enter the distributive share of the income

received from the partnership. See Business Entity Regulation 24-315, Sales Factor; Business

Entities As Owners in a Partnership or Joint Venture, for additional information regarding

the apportionment of income received from a partnership. For additional information on

revenue .nebraska.gov

= .2154014464231428

17

subpart F inclusions and GILTI, see Revenue Ruling 24-21-1 Subpart F Income and General

Information Letter 24-20-1, Global Intangible Low-Taxed Income and Foreign-Derived

Intangible Income.

Line 14 Total Sales or Gross Receipts. In the Total column, add lines 4 and 8 through 13, and enter

the result on line 14.

In the Nebraska column, add lines 5 through 13, and enter the result on line 14.

Line 15 Nebraska Apportionment Factor. Compute the Nebraska apportionment factor by dividing

line 14, Nebraska column, by line 14, Total column; round to six decimal places and enter

as a percent.

Example 4.

Line 14 Nebraska column 107,699

Line 14 Total column 499,992

Enter 21.5401 % on line 15.

Since the seventh digit (4) is less than ve, the sixth digit (1) is not rounded up to 2.

Nebraska Schedule II Instructions

Foreign Dividend and Special Foreign Tax Credit Deduction

Purpose. The Nebraska Schedule II is used to calculate the deduction for dividends included

in federal taxable income (line 30, Federal Form 1120) from corporations whose dividends do

not qualify for the dividends received deduction under Internal Revenue Code (IRC) § 243.

In addition, an adjustment is allowed for income that is taxed by a foreign country, or one

of its political subdivisions, at a rate in excess of the maximum federal corporate tax rate.

The adjustment can be made for each foreign country or group of foreign countries. The

amount of federal taxable income from operations within a foreign taxing jurisdiction must

be reduced by the amount of taxes actually paid to the foreign jurisdiction that are not

deductible solely because the foreign tax credit was elected on the federal income tax return.

The amount of after-tax income is then divided by one minus the maximum tax rate for

corporations in the IRC. The result of this calculation is subtracted from the amount of

federal taxable income from foreign operations.

The difference is reported in the total adjustments decreasing FTI computed on Nebraska

ScheduleA, and is included as an adjustment to federal taxable income on line 4, Form 1120N.

Schedule C, Federal Form 1120, and Parts A and B of Federal Form 1118 must be attached.

Line 1 Dividends From Foreign Corporations and Certain FSCs Subject to the IRC § 245 Deduction.

Enter the total of lines 6 and 7, column (a), Schedule C, Federal Form 1120; or lines 6 and

7, column (a), Schedule A, Federal Form 1120-L.

Line 2 Special Deductions on Line 1 Amount. Enter the total of lines 6 and 7, column (c), Schedule

C, Federal Form 1120; or lines 6 and 7, column (c), Schedule A, Federal Form 1120-L.

Line 3 Net Foreign Dividends Subject to the IRC § 245 Deduction Included in Federal Taxable Income.

Enter the result of line 1 minus line 2.

Line 4 Other Dividends From Foreign Corporations. Enter the amount from line 14, Schedule C,

Federal Form 1120, or line 15, Schedule A, Federal Form 1120-L. A U.S. life insurance

company claiming a deduction for “Other corporate dividends” from line 19, Schedule A,

Federal Form 1120-L, must include a detailed description of the dividends claimed.

Line 5 Income From Controlled Foreign Corporations Under Subpart F Treated as a Foreign Dividend

Under the IRC. Enter the amount of foreign dividends from Schedule C, Federal Form1120.

This includes amounts reported on Federal Schedule C, line 16b. The amount entered on this

line may only include Subpart F inclusion income that is a foreign dividend or deemed foreign

dividend under the IRC. Attach a copy of the Federal Schedule C to support a deduction

for amounts reported on line 16b.

revenue .nebraska.gov

18

Most subpart F inclusions reported on Federal Schedule C, line 16c are not foreign dividends

or deemed foreign dividends under the IRC. Attach a copy of Federal Schedule C; Forms

5471; Schedules I, Form 5471. The above forms and schedules do not identify any amount

reported on line 16c as a dividend or deemed dividend. Therefore, you must also attach

documents or worksheets that identify the amount of foreign dividends or deemed foreign

dividends included in line 16c. See Revenue Ruling 24-21-1 for additional information

regarding Nebraska’s treatment of subpart F income.

Line 6 Foreign Dividend Gross-up (IRC § 78). The amount entered includes dividends reported on

line 18, Schedule C, Federal Form 1120, less the IRC § 78 amount included in the GILTI

deduction. Attach a copy of the forms and schedules supporting the amount entered. Those

forms and schedules include, but may not be limited to, Schedule C of Federal Form 1120,

Federal Form 8993, and Federal Forms 1118.

Line 7 Total Foreign Dividends. Enter the sum of lines 3 through 6 on line 7 and line 12, ScheduleA.

Line 8 FTI From Qualifying Foreign Taxing Jurisdictions. Enter the total federal taxable income that

is also taxed by a foreign jurisdiction at a rate in excess of the maximum federal corporate

tax rate. Attach a schedule detailing FTI and foreign taxes paid by country.

Line 9 Foreign Taxes. Enter the amount of foreign taxes paid on line 8 amounts for which the foreign

tax credit is taken.

Line 12 Special Foreign Tax Credit Adjustment. Subtract line 11 from line 8. If less than zero, enter

zero. Do not enter an amount greater than the amount reported on line 8.

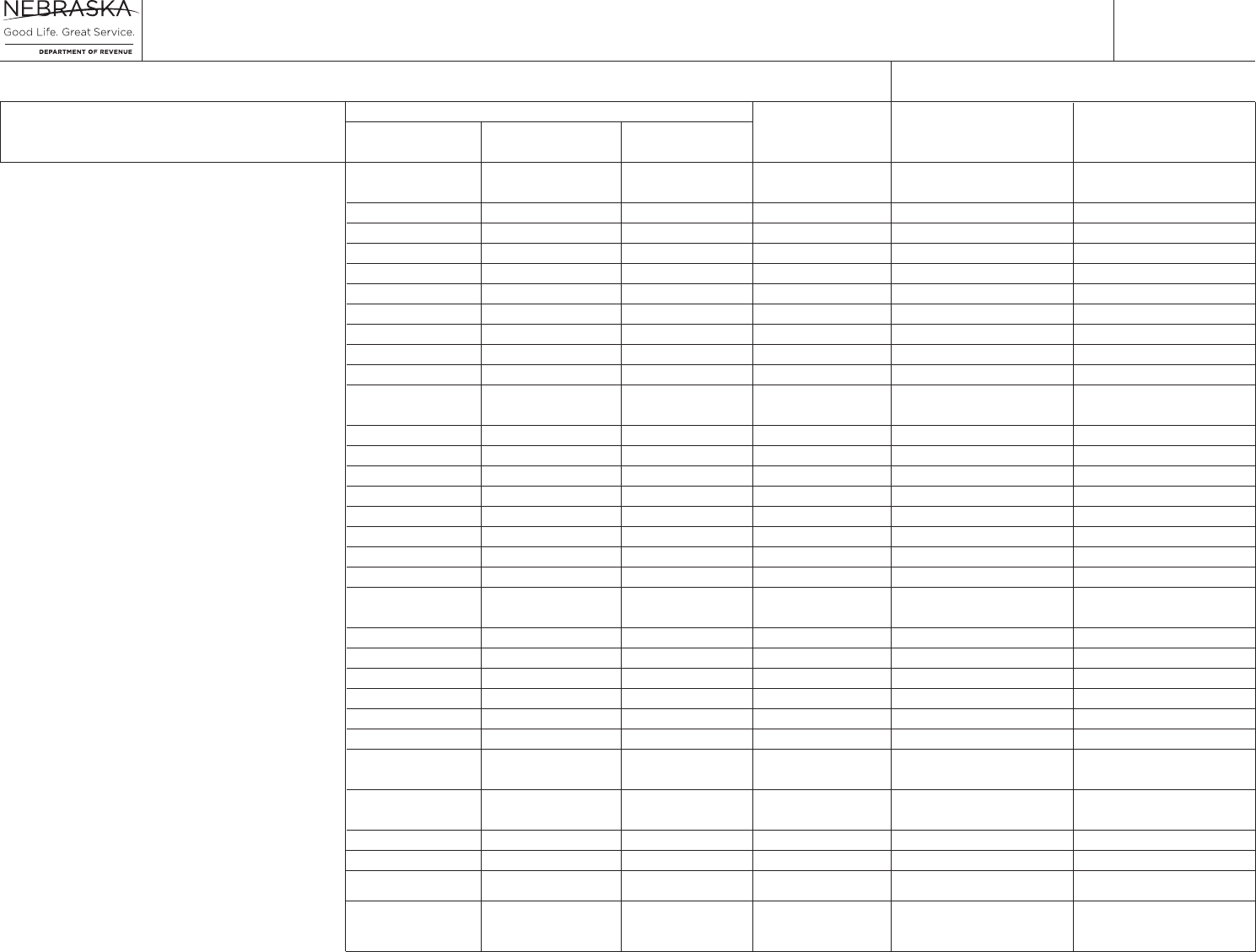

Nebraska Schedule III Instructions

Subsidiary or Affiliated Corporations

Purpose. The Nebraska Schedule III is used to identify the members of a unitary group and

summarize the Nebraska sales or receipts for those members of the unitary group that have

nexus in this state. The Schedule III also summarizes the Nebraska payments, including

deposits made with the Form 7004N and estimated income tax payments made by the

members of the unitary group.

This schedule must be completed if the corporate taxpayer is a member of a unitary group

or if the corporate taxpayer, either individually or as a group, owns 50% or more of another

corporation, or is owned 50% or more by another corporation.

The total amount of column A must equal line 20, Form 1120N.

The total amount of column B must equal line 21, Form 1120N.

The total amount of column D must equal line 14 in the Nebraska column of Schedule I,

Form 1120N.

If additional space is required, attach a schedule using the same format as Nebraska Schedule III.

Nebraska Schedule IV Instructions

Converting Net Income to Combined Net Income

Purpose. The Nebraska Schedule IV is used to determine the combined federal taxable income

of the unitary group.

This schedule must be completed by each corporate taxpayer ling a combined Nebraska

Corporation Income Tax Return, Form 1120N. If additional space is required, attach a

schedule using the same format as Nebraska Schedule IV.

Special Foreign Tax Credit Deduction Computation

Signature of Officer Date Email Address

Title Daytime Phone Number

Preparer’s Signature Date Preparer’s PTIN

Print Firm’s Name (or yours if self-employed), Address and Zip Code EIN Daytime Phone

paid

preparer’s

use only

2023

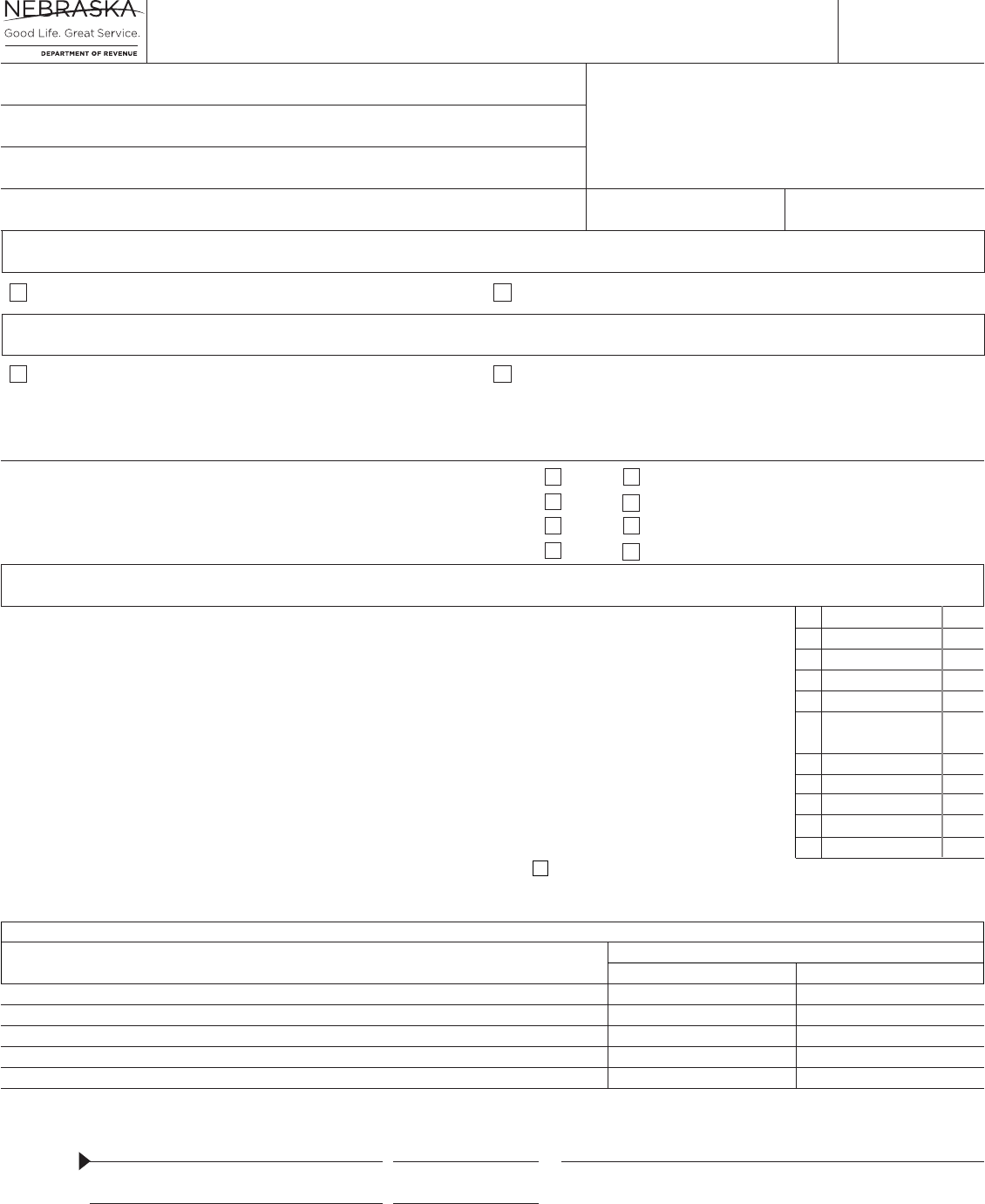

FORM 1120N

8-270-2023

Name Doing Business As (dba)

Legal Name

Street or Other Mailing Address

City State ZIP Code

Business Classication Code Date Business Began in Nebraska Principal Business Activity in Nebraska Federal ID Number Nebraska ID Number

Paper lers must attach a copy of the federal return and supporting schedules, as led with the IRS, to this return.

Check if: Initial Return Address Change Exempt Organization 7004 Attached

Final Return (Example, dissolved. See instr.) Name Change Cooperative Meeting IRC § 6072(d) 3800N, 775N, 312N, or 1107N Attached

Corporation Filing Status (

Answer questions A through D, as applicable.)

A. Does this corporation own at least 50% of another corporation; or is

it owned at least 50% by another corporation?

(1) YES (2) NO

If Yes, attach Federal Form 851 or a schedule of affiliated

corporations and federal IDs. Answer questions B, C, and D.

B. Is one single Nebraska return being led for the entire group?

(1) YES (2) NO

C. Are you ling as a unitary group in any other state?

(1) YES (2) NO

D. Check the method used to determine Nebraska income

(check only one):

(1) Combined report of a controlled group of corporations

(2) Separate report by a member of a controlled group

of corporations (attach supporting documentation)

(3) Alternate method (attach Nebraska Department of Revenue approval)

1 Federal gross sales or receipts, less returns and allowances ...................................................................... 1 00

2 Federal taxable income (FTI) (see instructions) ........................................................................................... 2 00

3 Adjustments increasing FTI (line 10, from attached Nebraska Schedule A) ...... 3 00

4 Adjustments decreasing FTI (line 20, from attached Nebraska Schedule A) ..... 4 00

5 Adjusted FTI (enter line 2 plus line 3 minus line 4) ...................................................................................... 5 00

6 Nebraska taxable income before Nebraska carryovers (see instructions) ................................................... 6 00

7 Nebraska capital loss carryover (see instructions – attach worksheet) ....................................................... 7 00

8 Nebraska taxable income after Nebraska capital loss carryover (line 6 minus line 7) ................................. 8 00

9 Nebraska net operating loss carryover (see instructions – attach worksheet) ............................................. 9 00

10 Net Nebraska taxable income (line 8 minus line 9) ...................................................................................... 10 00

11 Nebraska tax Check this box if you are an insurance company ............................................................ 11 00

12 Premium tax credit (see instructions – attach schedule) .................................... 12 00

13 Employer’s credit for expenses incurred for TANF (ADC) recipients (see instr.) 13 00

14 Community Development Assistance Act credit (attach Form CDN) ................. 14 00

15 Form 3800N nonrefundable credit (attach Form 3800N) ................................... 15 00

16 NE employer tax credit for employing convicted felons. Enter certicate

number from Form ETC-A ______________________ 16 00

17 Total nonrefundable credits (total of lines 12 through 16) ............................................................................. 17 00

18

Nebraska tax after nonrefundable credits. Subtract line 17 from line 11 (if line 17 is more than line 11, enter -0-)

18 00

19 Form 3800N refundable credit (attach Form 3800N) ......................................... 19 00

20 Tax deposited with Form 7004N ........................................................................ 20 00

21 2023 estimated income tax payments (minus any Form 4466N adjustment) .... 21 00

22 Beginning Farmer credit .................................................................................... 22 00

23 Nebraska income tax withheld (see instructions) .............................................. 23 00

24 Credit for school district property taxes (attach Form PTC) ............................... 24 00

25 Credit for community college property taxes (attach Form PTC) ...................... 25 00

26 PTET credit (attach Schedules K-1N) ....................................................................

a Name:__________ b Nebraska ID Number:_________ c Amount: $________

(Attach a schedule if the credit was received from more than one partnership.) ....... 26 00

27 Total refundable credits and payments (total of lines 19 through 26) ........................................................... 27 00

28 Tax Due (line 18 minus line 27) .................................................................................................................... 28 00

29 Penalty for underpayment of estimated income tax (see instructions) .......................................................... 29 00

30 Amount Due (when line 27 is less than the total of lines 18 and 29). If paying electronically, check here 30 00

31 Overpayment (when line 27 is greater than the total of lines 18 and 29) ..................................................... 31 00

32 Amount on line 31 to be credited to 2024 estimated income tax ................................................................. 32 00

33 Overpayment to be refunded (line 31 minus line 32). Direct deposit: Complete lines 34a, 34b, and 34c .... 33 00

Under penalties of perjury, I declare that as taxpayer or preparer, I have examined this return, including accompanying schedules and statements,

and to the best of my knowledge and belief, it is correct and complete.

Please Type or Print

Nebraska Corporation Income Tax Return

for the taxable year January 1, 2023 through December 31, 2023 or other taxable year

beginning , 2023 and ending ,

PLEASE DO NOT WRITE IN THIS SPACE

34a Routing Number 34b Type of Account 1 = Checking 2 = Savings

34c Account Number (see instructions)

34d

Check this box if this refund will go to a bank account outside the United States.

sign

here

( )

( )

PRINT FORM

RESET FORM

FORM 1120N

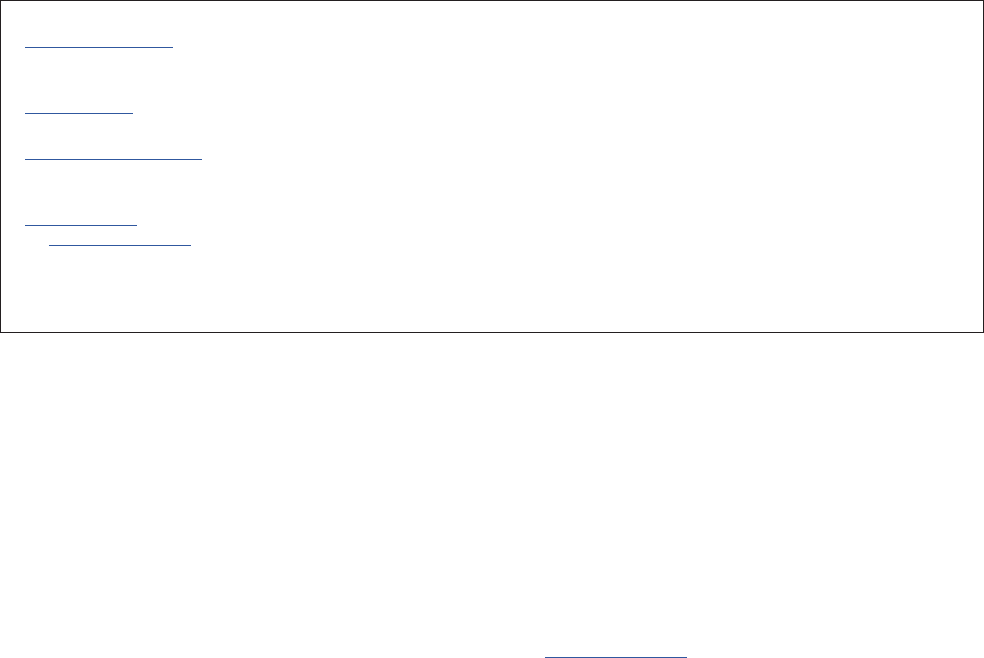

Schedules

A and I

2023

Name on Form 1120N Nebraska ID Number

Nebraska Schedule A — Adjustments to FTI

Nebraska Schedule I — Apportionment for Multistate Business

.

1 Adjusted FTI (line 5, Form 1120N) ...................................................................................................................................................... 1 00

2 Nebraska apportionment factor (from line 15 below) .......................................................... 2 %

3 Taxable income apportioned to Nebraska (line 1 multiplied by line 2). Enter here and on line 6, Form 1120N .................................. 3 00

Nebraska Apportionment Factor – Sales or Gross Receipts

NebraskaTotal

4 Sales or gross receipts minus returns and allowances .................................................. 4 00

5 Sales delivered or shipped to purchasers in Nebraska: shipped from outside Nebraska ............................................................ 5 00

6 Sales delivered or shipped to purchasers in Nebraska: shipped from within Nebraska ............................................................... 6 00

7 Sales shipped from Nebraska to the U.S. government ................................................................................................................ 7 00

8 Interest on sales of tangible personal property .............................................................. 8 00 8 00

9 I

nterest, dividends, and royalties from intangible property

............................................... 9 00 9 00

10 Gross rents .................................................................................................................... 10 00 10 00

11 Net gain on sales of intangible property ........................................................................ 11 00 11 00

12 Gross receipts from sales of tangible personal and real

property not included above .......................................................................................... 12 00 12 00

13 Other income

a List type: ____________________ b Total Amount: $ _____________

c Nebraska Amount: $ ___________

Enter total of lines 13b in rst column. Enter total of lines 13c in

second column ............................................................................................ 13 00 13 00

14 Total sales or gross receipts ...................................................................................... 14 00 14 00

15 Nebraska apportionment factor. (Divide line 14, Nebraska column, by line 14, Total column, and round to six

decimal places). Enter as a percent here and on Schedule I, line 2 above ..................................................................... 15 %

Nebraska Schedule I —

Apportionment for Multistate Business

Nebraska Schedule A

• You must use Schedule A if you make an adjustment on lines 3 or 4 of Form 1120N.

Adjustments Increasing FTI

.

1 State and local government interest and dividend income (see instructions) ..................................................................................... 1 00

2 Federal net operating loss deduction .................................................................................................................................................. 2 00

3 Federal capital loss carryover .............................................................................................................................................................. 3 00

4 Allocable, nonapportionable loss ............................................................ 4

5 Related expenses .................................................................................................................................. 5

6 Interest expense disallowance ............................................................................................................... 6

7 Total allocable, nonapportionable loss (add lines 4-6) (attach affidavit - see instructions) .................................................................. 7 00

8 Nebraska and local income, sales, and use taxes deducted on federal Form 1065 under section 164 of the IRC.

(from Schedules K-1N) ......................................................................................................................................................................... 8 00

9 Other increasing adjustments

a List type: _____________________________________________________________ b Amount: $ _______________

Total other increasing adjustments. Enter total of lines 8b ............................................................................................................. 9 00

10 Total adjustments increasing FTI (total of lines 1, 2, 3, 7, 8, and 9). Enter here and on line 3, Form 1120N ....................................... 10 00

Adjustments Decreasing FTI

11 Qualied U.S. government interest deduction. (attach supporting schedule) ...................................................................................... 11 0 0

12 Total foreign dividends (line 7, Nebraska Schedule II) ........................................................................................................................ 12 00

13 Special foreign tax credit adjustment (line 12, Nebraska Schedule II) ................................................................................................ 13 00

14 Allocable, nonapportionable income....................................................... 14 00

15 Related expenses .................................................................................................................................. 15 00

16 Interest expense disallowance ............................................................................................................... 16 00

17 Net allocable, nonapportionable income (line 14 minus lines 15 and 16) (attach affidavit — see instructions) .................................. 17 00

18 Nebraska College Savings Program (see instructions) ....................................................................................................................... 18 00

19 Other decreasing adjustments

a List type: _____________________________________________________________ b Amount: $ _______________

Total other decreasing adjustments. Enter total of lines 19b .......................................................................................................... 19 00

20 TOTAL adjustments decreasing FTI (total of lines 11, 12, 13, 17, 18, and 19). Enter here and on line 4, Form 1120N ....................... 20 00

8 FTI from qualifying foreign taxing jurisdictions

a Jurisdictions: _____________________________________ b Amount: $ ____________

Total FTI from qualifying foreign taxing jurisdictions. Enter total of lines 8b .......................... 8 00

9 Foreign taxes ............................................................................................................................. 9 00

10 After tax foreign income (line 8 minus line 9) ............................................................................. 10 00

11 After tax foreign income not taxed (divide line 10 result by .79; enter result here) ..................... 11 0 0

12 Special foreign tax credit adjustment (subtract line 11 from line 8. If less than 0, enter 0). Enter here and on line 13,

Schedule A, Form 1120N. ............................................................................................................................................................ 12 00

Foreign Dividend Deduction Computation

Special Foreign Tax Credit Deduction Computation

1 Dividends from foreign corporations and certain FSCs subject to the IRC § 245 deduction

(total of lines 6 and 7, column (a), Schedule C, Federal Form 1120) .......................................................................................... 1 00

2 Special deductions on line 1 amount. Enter the total of lines 6 and 7, column (c), Schedule C,

Federal Form 1120 ..................................................................................................................... 2 00