Bartik Instruments:

An Applied Introduction

Matthias Breuer

*

This version: December 2021

Abstract

This article provides an applied introduction to Bartik instruments. The instruments

attempt to reduce familiar endogeneity concerns in differential exposure designs

(e.g., panel regressions with unit and time fixed effects). They isolate treatment

variation due to the differential impact of common shocks on units with distinct

pre-determined exposures. As a result, the instruments purge the treatment variation

of possibly confounding factors varying across units over time. Given their broad

applicability, Bartik instruments promise to provide researchers with a versatile

new tool in their empirical toolbox to investigate relevant accounting questions.

Keywords: Bartik Instruments; Shift Shares; Simulated Instruments

JEL Classification: C51, M40

Acknowledgements:

I thank Ed deHaan (editor), two anonymous reviewers, Lulseged Asegu, John Barrios, Thomas

Bourveau, Raphael Duguay, Sehwa Kim, Christian Leuz, Anthony Le, Rongchen Li, Miguel

Minutti-Meza, Harm Schütt, Felix Vetter, Li Yang, and participants at the 2021 FARS and Journal

of Financial Reporting: Research Methods Mini-Conference for helpful comments and

discussions. All errors are my own. The simulation code is available at:

https://github.com/mb4468/bartik_intro

*

Columbia University, Graduate School of Business - m[email protected]

1

1 Introduction

Accounting research overwhelmingly relies on observational data, often panel data (i.e.,

data containing multiple units over time), to empirically examine core accounting questions. While

panel data allow reducing concerns about static differences across units and common changes over

time via unit and time fixed effects (deHaan 2021), we typically remain worried about first-order

endogeneity issues such as reverse causality, simultaneity, and omitted variable bias. In examining

the impact of accounting quality on the cost of capital, for example, we may worry that observed

changes in capital costs may cause accounting quality changes, instead of the other way around

(Balakrishnan et al. 2014; Lo 2014). We may also worry that changes in capital costs and

accounting quality commingle supply and demand forces (Gerakos and Syverson 2017). Lastly,

and most prominently, we tend to worry that other omitted factors (e.g., operating activities) drive

both, changes in capital costs and accounting quality (Hribar and Nichols 2007; Beyer et al. 2010).

To alleviate these endogeneity concerns, we could, in principle, use instrumental variables. In

practice, the use of instrumental variables in accounting research is limited though given the

challenge to identify credible instruments that explain the treatment and only affect the outcome

of interest through their impact on the treatment (Larcker and Rusticus 2010).

This article provides an applied introduction to Bartik or shift-share instruments, a class of

instruments that can be constructed in various settings, including typical accounting settings.

Pioneered by Bartik (1991), these instruments aim to focus on the plausibly (more) exogenous

subpart of the treatment variation of interest due to the differential impact of common shocks on

units with distinct pre-determined exposures. They are particularly useful for reducing

endogeneity concerns in differential exposure designs (e.g., panel regressions with unit and time

effects), one of the most popular designs in recent accounting studies (deHaan 2021; Armstrong

2

et al. 2021). Notably, the idea behind Bartik instruments is closely related to the familiar

difference-in-differences approach which exploits the differential impact of a common shock on

treated and control firms. Unlike standard difference-in-differences designs, Bartik instruments

tend to exploit continuous instead of dichotomous treatment exposures though.

In the canonical example, Bartik (1991) develops this class of instruments to estimate the

impact of county-level employment changes, due to labor demand shifts, on wages. Like the

accounting-quality and cost-of-capital relation, the employment-wage relation is challenging to

identify due to concerns about reverse causality, simultaneity, and omitted factors. To isolate

plausibly exogenous variation in counties’ employment rates, Bartik exploits the fact that

nationwide trends in industry employment rates (e.g., a decline in US manufacturing employment)

impact counties’ employment rates differently, depending on their pre-existing industrial structure

(e.g., their share of employment in manufacturing). This subpart of the variation in counties’

employment rates is less likely to reflect changes due to local wage developments (reverse

causality), local shifts in labor supply (simultaneity), or omitted factors such as local growth

opportunities (omitted variable bias).

Bartik instruments have been frequently used in empirical studies in economics for more

than two decades (e.g., Blanchard and Katz 1992; Card 2009; Autor et al. 2013).

1

Yet, they have

only recently found their way into accounting research. An important barrier to the adoption of

Bartik instruments is their added complexity compared to typical instrumental variables and

difference-in-differences approaches (e.g., due to their multidimensionality and continuous

treatment exposures). A recent methodological literature attempts to address the complexity

1

Recent studies, for example, use Bartik instruments to examine topical and important questions such as the impact

of pandemic-related policies (Granja et al. 2021) and the causes behind the decline of the natural interest rate over the

past decades (Mian et al. 2021).

3

concern by formally exploring and clarifying the conditions under which Bartik instruments allow

for causal inferences (e.g., Goldsmith-Pinkham et al. 2020; Borusyak et al. 2021; Borusyak and

Hull 2020).

To aid the adoption of Bartik instruments in accounting research, I complement the formal

discussion in the recent methodological literature with an applied introduction to this class of

instruments. I specifically focus on the empirical challenge addressed by Bartik instruments, the

general idea behind the construction of the instruments, the conceptual links to approaches familiar

to accounting researchers (e.g., instrumental variables and difference-in-differences designs), and

practical considerations in implementing the instruments and assessing their validity.

As the leading example, I use the canonical application of Bartik instruments to the

estimation of the employment-wage relation (Bartik 1991). Although this specific application may

be of lesser concern to accounting researchers, the empirical challenge underlying this example is

present in many accounting settings and the proposed empirical approach can be applied in various

accounting settings. To highlight the relevance for accounting research, I discuss a possible

application of Bartik instruments to the question of how accounting quality impacts the cost of

capital and present recent applications of Bartik instruments in accounting research.

This article is structured as follows. In Section 2, I introduce the canonical application of

Bartik instruments to the estimation of the employment-wage relation. In Section 3, I discuss the

general idea behind the construction and use of the instruments. In Section 4, I highlight a special

case of the instruments designed for threshold-based regulations. In Section 5, I describe select

examples of applications of Bartik instruments in accounting research. I conclude in Section 6.

2 Canonical Bartik Example

In Bartik’s canonical application, we are interested in estimating the impact of employment

4

changes, due to labor demand shifts, on wages.

2

We observe panel data on employment rates (x

i,t

)

and wages (y

i,t

) for counties (i) over time (t). The panel data allow us to account for cross-sectional

differences across counties using county fixed effects and common time trends using time fixed

effects. However, we remain concerned that reverse causality, simultaneity, and time-varying

correlated omitted factors could confound our estimate of interest. Local employment, for

example, may increase due to local wage increases, instead of the other way around. Additionally,

local wages and employment are not only determined by labor-demand shifts, but also reflect

labor-supply shifts. Labor-supply shifts, however, exhibit the opposite effect on wages as labor-

demand shifts (i.e., positive supply shifts decrease wages, whereas positive demand shifts increase

wages). Simultaneous supply shifts, accordingly, threaten to bias our estimate downward. Lastly,

and most prominently, we worry that other factors such as local technology shocks, growth

opportunities, or financing conditions affect both, changes in wages and employment.

To address the endogeneity concerns, Bartik proposes an instrumental variable approach.

The basic idea behind instrumental variable approaches is to find another variable, the instrument

(z

i,t

), that drives part of the treatment variation (x

i,t

), and only affects the outcome (y

i,t

) through its

impact on the treatment (e.g., Wright 1928; Angrist and Krueger 2001). To construct such

instrument, Bartik first notes that the local employment rates can be represented by the sum-

product of two industry-level components: the employment rate (e

i,k,t

) and the employment share

(w

i,k,t

) of a given industry (k) in a given county. Based on this insight, he constructs an instrument

for local employment rates by weighting nationwide employment rates (e

k,t

) for each industry (k)

with pre-determined (e.g., initial) county-industry-level employment shares (w

i,k

).

2

The structural parameter of interest is the (inverse) labor-supply elasticity, that is, the slope of the labor-supply curve.

To identify the elasticity, we need to hold the supply curve fixed and only shift the demand curve.

5

The instrument essentially isolates variation in local employment-rate changes due to

differential impacts of national employment trends on local counties arising from the counties’

distinct industrial structure. The employment rate in the US manufacturing sector, for example,

declined in response to import competition from China. This nationwide trend affected counties

with a historically strong manufacturing sector more adversely than other counties (Autor et al.

2013). By focusing on such differential impact of nationwide trends on distinct counties, the

instrument purges the treatment of variation due to county-specific changes in industrial structure

or employment rates. As a result, the instrument’s variation in employment rates cannot be driven

by local wages (i.e., reverse causality). Similarly, the instrument, by construction, does not vary

with local factors such as technological shocks and growth opportunities, reducing first-order

omitted variable concerns. In addition, Bartik argues that the differential exposure of counties to

nationwide employment trends likely captures variation in industry-specific labor-demand shifts

rather than local labor-supply shifts. The basic idea behind this argument is that differences in

industry-employment shares across counties tend to reflect the relative importance of industries

exporting to national or even international markets, not locally oriented industries (Bartik 1991, p.

274). As a result, the instrument can be expected to capture industry-specific labor-demand shifts

due to nationwide trends in the competitiveness and fortunes of a given industry (e.g., the

reallocation of manufacturing from the US to China). While the ultimate validity of the instrument

remains an identifying assumption (e.g., rests on the plausibility of theoretical and institutional

arguments), the instrument construction tends to reduce first-order endogeneity concerns by

focusing on a plausibly more exogenous subpart of the variation in local employment rates.

Notably, the endogeneity issues in the canonical Bartik example are familiar to accounting

researchers and the proposed instrumental variable approach can be implemented in and adapted

6

to various settings, including typical accounting settings. To clarify the idea behind Bartik

instruments and illustrate their wide-ranging applicability, I discuss the general approach

underlying the construction and use of the instruments in the next section.

3 General Approach: Bartik Instrument

3.1 Empirical Challenge

Bartik instruments aim to address familiar endogeneity concerns (e.g., reverse causality,

simultaneity, and correlated omitted variables). The instruments are particularly useful in cases

where we can exploit multidimensional data (e.g., panel data with observations for multiple units,

i = {1,...,I}, over time, t = {1,...,T}). In these cases, we can take advantage of the multidimensional

data structure to account for first-order endogeneity concerns related to the treatment of interest

(x

i,t

) by including fixed effects for each dimension (i.e., unit effects, α

i

, and time effects, α

t

):

3

(1)

The identifying variation in such differential exposure designs is limited to differential

changes across units over time. This variation is often less confounded than the full treatment

variation. We, for example, do not need to worry about static differences in terms of industrial

structure and economic activity across counties, after accounting for county fixed effects.

Similarly, we do not need to worry about common trends in industrial structure and economic

activity, after accounting for time fixed effects. Still, even the variation in differential exposure

designs is subject to endogeneity concerns (

) relating to reverse causality,

simultaneity, and correlated omitted factors varying at the level of the differential exposure (i.e.,

3

Bartik (1991) uses a changes specification. As differential exposure designs using fixed effects are more prevalent

in accounting research, I opt to introduce Bartik instruments using a levels specification with unit and time fixed

effects. This within-unit design implicitly exploits changes.

7

at the unit-time level (i,t)). Such factors (e.g., growth opportunities, technology shocks,

competitive threats, financing needs, and the like) are typically abundant and unobservable to us.

Accordingly, we cannot simply control for such factors. Instead, Bartik (1991) proposes the use of

a novel type of instrument to address the endogeneity concerns.

3.2 Instrument Construction

Bartik instruments reduce endogeneity concerns by focusing on a subset of the differential

exposure variation that is plausibly exogenous (e.g., uncorrelated with local growth opportunities).

To construct such variation, we must first identify a subdimension (k) which allows decomposing

the treatment variation (x

i,t

). In the canonical example of Bartik (1991), the treatment (i.e., county-

level employment rates) can be decomposed into industry-specific employment rates (e

i,t,k

) in a

given county weighted by industry-specific employment shares (w

i,t,k

):

(2)

This decomposition is an identity. It does not require any assumption. The only requirement

for such decomposition to be useful for constructing a Bartik instrument is that the individual

components are observable.

4

In the case of Bartik (1991), this means we need to observe

employment data at the county-industry level, not just at the county level. Notably, this

requirement does not pertain to the outcome data (e.g., wages) as the ultimate regression is still

run at the county-level, not county-industry level.

The decomposition shows that both components, the shares (w

i,t,k

) and the rates (e

i,t,k

), vary

at the level of the identifying assumption (i.e., across counties over time (i,t)). Accordingly, we

need to worry about any factors determining wages and driving changes in counties’ industrial

4

For the canonical example, we only need to observe the employment share at the county-industry level. For the

employment rate, we can use national industry statistics.

8

structure and/or industry-specific employment rates.

To reduce the number of possibly confounding factors, Bartik instruments (

) focus on

plausibly exogenous dimensions of the components making up the treatment (x

i,t

). In Bartik (1991),

those dimensions are the pre-determined industry-specific employment shares in a given county

level (w

i,k

) and nationwide industry-specific employment rates (e

t,k

):

(3)

While the pre-determined shares and the nationwide rates are unlikely to be randomly

assigned, the idea is that, compared to the full treatment variation, the pre-determined shares and

nationwide rates are less likely to reflect current choices (e.g., responses to local growth

opportunities) at the county level. Importantly, the instrument exclusively focuses on changes in

county-level employment rates due to the interaction of pre-determined shares and nationwide

rates. It does not use level differences in shares or rates across counties or over time. Hence, the

Bartik instrument can be viewed as following the logic underlying the familiar difference-in-

differences approach (Section 3.3.2).

More generally, Bartik instruments focus on the inner product of a pre-determined share

varying across units (i,k) (e.g., local employment shares as of the beginning of the sample) and a

common trend (t,k) (e.g., changes in nationwide employment rates over time). Hence, the

instruments only vary at the level of the identifying variation (i,t) due to the differential impact of

common trends on local units with distinct pre-determined shares.

5

Notably, the instruments, by

construction, do not vary across units over time due to endogenous changes of the shares (e.g.,

changes in industrial structure of counties) or endogenous unit-specific trends (e.g., county-

5

Hence, Bartik instruments are also often referred to as shift-share instruments.

9

specific employment rate shocks). This feature reduces concerns about reverse causality,

simultaneity, and important correlated omitted factors.

To see this point more formally, we can decompose the full treatment variation into the

Bartik variation, driven by the interaction of pre-determined shares (w

i,k

) and common shocks (e

t,k

),

and unit-specific changes in shares and shocks:

(4)

The unit-specific changes in the shares and shocks (e.g., (e

i,t,k

− e

t,k

)) can be correlated with a host

of possibly confounding factors (e.g., local growth opportunities). These timevarying factors

cannot be controlled for via unit and time fixed effects. By contrast, unit and time fixed effects can

control for first-order endogeneity concerns related to the Bartik instrument’s variation:

endogenous differences across units correlated with the shares and endogenous changes over time

correlated with the common trends. Accordingly, conditional on the fixed effects, Bartik

instruments isolate plausibly exogenous variation due to the differential impact of common trends

on units with distinct pre-determined shares.

3.3 Identifying Conditions

The construction of Bartik instruments can reduce endogeneity concerns if certain

10

conditions are satisfied. In the following subsections, I provide an intuition for the relevant

conditions by analogy to two related and familiar empirical approaches: instrumental variables

(IV) and difference-in-differences (DID) approaches. For a formal derivation of the relevant

conditions, see the excellent discussions in Goldsmith-Pinkham et al. (2020), Borusyak et al.

(2021), and Borusyak and Hull (2020).

3.3.1 Instrumental Variables Approach

As the name already reveals, Bartik instruments are just a particular type of instrument.

They follow the basic idea of the instrumental variable approach: isolating a plausibly exogenous

subpart of the treatment variation. Bartik instruments do so explicitly by starting with the full

treatment variation, decomposing it to its key dimensions, and then focusing on the most plausibly

exogenous parts of these dimensions (e.g., pre-determined shares and common trends).

6

Accordingly, the familiar instrumental variable conditions apply. The first condition is the

relevance condition. It is a necessary condition. It requires that the instrument is a key determinant

of the treatment (

). For Bartik instruments, this condition essentially requires

some degree of persistence in the pre-determined shares (w

i,k

) and commonality in the trend across

units (e

t,k

). In particular, the pre-determined shares need to be predictive of the actual shares during

the sample period for the Bartik instrument to be relevant. Similarly, the common trend (e.g.,

changes in nationwide employment rates per industry) needs to be predictive of the trend observed

in individual units (e.g., at the county-industry level).

The relevance condition is typically satisfied for Bartik instruments, because the

6

This approach is in the spirit of familiar instrumental variable approaches using lagged values or industry averages

to reduce concerns about reverse causality and unit-specific omitted factors. Unlike these familiar approaches,

however, the Bartik approach isolates the interaction of pre-determined characteristics and common trends. It does

not simply use variation in the pre-determined characteristics over time or variation in common characteristics across

units. As Reiss and Wolak (2007) and Larcker and Rusticus (2010) point out, this variation is unlikely to be plausibly

exogenous.

11

instruments, by construction, capture important dimensions of the treatment variation. To test the

condition, we can run the usual first-stage regression:

(5)

The first-stage coefficient (β

FS

) should be positive and significant as long the shares are somewhat

persistent and there is some commonality in trends across units.

Bartik instruments may not one-for-one determine the treatment of interest (i.e., β

FS

can be

different from one). Accordingly, the following reduced-form regression can yield a coefficient

estimate which quantifies the impact of the instrument instead of our treatment of interest:

(6)

To obtain a quantification in terms of the treatment of interest, we can scale the reduced-form

coefficient (β

RF

) by the first-stage coefficient (β

FS

). The resulting coefficient is the second-stage

coefficient (β

SS

= β

RF

/β

FS

), which quantifies the impact of the instrumented treatment. Accordingly,

we can adjust for variation in the relevance of the Bartik instruments (e.g., due to systematic

deviations from persistence or commonality) by following the standard two-stage instrumental

variable approach. We should not adjust for limited persistence or commonality by simply using

the actual instead of the pre-determined shares as our right-hand-side variation. As discussed

earlier, this OLS approach would raise substantial endogeneity concerns.

For the instrumented coefficient estimate to be unbiased, we need the second condition

underlying the instrumental variables approach: the exclusion restriction. It requires that the

instrument is (conditionally) independent of other determinants of the outcome

(

).

7

This condition is the identifying assumption. It is untestable (i.e., remains

7

Besides independence, the exclusion restriction requires that the instrument affects the outcome only through its

impact on the treatment. This (sub)condition is often plausible in the case of Bartik instruments given that the

12

an assumption). The plausibility of this assumption needs to be argued for with the help of theory

and institutional details. Goldsmith-Pinkham et al. (2020), Borusyak et al. (2021), and Borusyak

and Hull (2020) explore different sets of formal assumptions (e.g., exogeneity of the shares vs. the

shocks) required for the validity of the exclusion restriction for Bartik instruments. In the following

subsection, I attempt to provide an intuitive understanding for the identifying assumption of Bartik

instruments, when used in a differential exposure design, by analogy to the familiar difference-in-

differences approach and its identifying assumption.

3.3.2 Difference-in-Differences Approach

Bartik instruments essentially focus on the subpart in the treatment variation that is driven

by the interaction of a pre-determined characteristic varying across units and a common trend

varying over time. This approach is reminiscent of the familiar difference-indifferences approach.

The difference-in-differences approach exploits the differential impact of a common dimension

(e.g., time) across units with distinct pre-determined characteristics (e.g., treatment status):

(7)

The canonical difference-in-differences approach exploits the interaction of a dichotomous

pre-determined treatment indicator varying across units (

) with a dichotomous time indicator (1

t

)

as its treatment variation:

(8)

In the IFRS literature, for example, the treatment indicator takes the value of one for European

firms and zero for US firms; and the time indicator takes the value of one for years from 2005

instruments explicitly focus on a subpart of the treatment variation rather than use a completely distinct source of

variation. The only-through (or one-channel) condition may be violated though if there are spillovers across counties

(e.g., Berg et al. 2021). Nationwide employment trends, for example, may directly affect local counties’ outcomes by

luring employees away from a given county toward other booming counties elsewhere in the nation (which drive the

nationwide trend). Such spillovers (e.g., across counties) can invalidate or complicate the use of Bartik instruments.

13

onward and zero before 2005 (e.g., Christensen et al. 2013).

The same logic extends to difference-in-differences designs with continuous treatments:

(9)

Bloomfield (2021), for example, examines the differential impact of Compensation Discussion

and Analysis (CD&A) disclosure requirements after 2006 on firms with varying levels of pre-

determined market shares (x

i

).

8

The common idea behind these approaches is to exclusively focus on the interaction of a

characteristic varying at the unit dimension (i) and one varying at the time dimension (t), while

accounting for level differences across units and time using unit and time fixed effects. As a result,

the treatment only varies at the identifying unit-time level (i,t) (e.g., firm-year level) due to the

interaction of a unit-fixed component (e.g., treatment status) and a time-fixed component (e.g., pre

vs. post period). It does not vary at the identifying unit-time level due to either of the components

varying both at the unit and time dimension. This feature reduces the number of potentially

correlated omitted variables that we must worry about.

9

The identifying assumption underlying the difference-in-differences approaches is that the

interaction between a characteristic varying across units (i) and another characteristic varying

8

Notably, difference-in-differences designs with the share of treated firms in a given unit (e.g., county) as the

continuous treatment variable are just a special (and simple) case of a Bartik instrument (e.g., Breuer et al. 2020). To

see the equivalence, note that the treatment indicator

for firm k in county i corresponds to the pre-determined

share, w

i,k

. Similarly, an indicator

taking the value of one for treated firms in the post period corresponds to the

common trend, e

t,k

. Accordingly, the Bartik instrument is given by:

,

which corresponds to the continuous treatment-share difference-in-differences design.

9

In difference-in-differences designs, just as in the construction of Bartik instruments, the treatment exposure (e.g.,

treatment indicator) should be pre-determined and held fixed. This approach avoids conflating the intent-to-treat effect

with endogenous selection into or out of the treatment status over time. As described in the previous section, we can

adjust the intent-to-treat estimate for imperfect compliance via the two-stage instrumental variable approach to arrive

at the treatment effect on the treated.

14

across time (t) is conditionally independent, after controlling for the level differences of both

dimensions (i and t). For the canonical case of a temporal difference-in-differences approach (i.e.,

where one of the dimensions is time), this assumption translates into the familiar parallel-trends

assumption. That is, levels across units can be different, but trends over time across units should

be the same absent any treatment. More generally, it requires that there are no other factors that

are correlated with the interaction and differentially impact outcomes across units.

10

By analogy, Bartik instruments (in differential exposure designs) can be viewed as relying

on the same basic identifying assumption. Goldsmith-Pinkham et al. (2020) illustrates that the

parallel-trends assumption corresponds to the conditional share-exogeneity assumption for Bartik

instruments. This assumption requires that there are no other factors correlated with the pre-

determined shares that can explain why a common trend affects units differentially. Accordingly,

the pre-determined shares can be correlated with levels of omitted factors but should not be

correlated with differential changes of those factors, just as we know it from the parallel-trends

assumption in standard difference-in-differences designs.

Alternatively, Borusyak et al. (2021) show that Bartik instruments can also be valid under

the conditional shock-exogeneity assumption. This assumption requires the common shocks to be

as-good-as-randomly assigned and large in number. Notably, this alternative assumption does not

require the exogeneity of the shares and the corresponding parallel-trends assumption.

11

Accordingly, concerns about endogenous shocks or shares alone do not invalidate the use of Bartik

instruments. Which of the identifying assumptions is most plausible in a given setting depends on

theory and institutional knowledge, as usual in design-based research (e.g., Leuz and Wysocki

10

Recent research by Callaway et al. (2021) shows that effect of continuous treatments can be identified under a

generalized parallel trends assumption that is similar to the binary treatment case. Its interpretation can be particularly

challenging due to treatment effect heterogeneity though. For a related discussion, see Section 3.4.3.

11

Intuitively, bias from endogenous shares cancels out in case of exogenous shocks as the shares sum to one.

15

2016).

3.4 Practical Considerations

Bartik instruments, by combining variation from three dimensions (i, t, and k), exploit

continuous treatment variation (e.g., Angrist and Imbens 1995). This variation can aid

identification by exploiting more heterogeneity in the exposure to a treatment than a typical

dichotomous difference-in-differences design. At the same time, it complicates the understanding

of the identifying variation and the interpretation of the resulting estimates.

12

These “black box”

concerns can be reduced by complementing the estimates from Bartik instruments with descriptive

statistics and diagnostic tests.

3.4.1 Extent and Sources of Variation

In a first set of tests, we can explore the extent and sources of the Bartik instrument’s

variation. Descriptive statistics on the distribution of the instrument (z

i,t

) or instrumented treatment

(

) can inform us about the range and frequency of treatment values spanned by the instrument.

This information not only helps us to understand the treated population, but also to interpret the

instrumented treatment-effect estimate, as the estimate reflects a weighted average across the

various treatment values. Descriptive statistics on the distributions of the individual components

of the Bartik instrument (w

i,k

and e

t,k

) can additionally inform us about the underlying sources of

the instrument’s variation. These statistics, for example, can tell us about differences in county-

level employment shares and national employment rates across industries (i.e., the subdimension

k). Hence, they help us understand which component (e.g., pre-determined employment shares or

12

This issue is reminiscent of the trade-off between the extent of treatment variation (e.g., the number of shocks)

versus the ease of interpretation of the treatment estimate in generalized difference-in-differences designs (e.g., de

Chaisemartin and D’Haultfœuille 2020; Barrios 2021; Goodman-Bacon 2021). Multiple shocks reduce concerns about

concurrent events but complicate the interpretation of the weighted average treatment effect, especially in case of

treatment effect heterogeneity (e.g., across units or time).

16

national employment rate trends) or subdimension (e.g., manufacturing vs. service industry)

primarily drives the instrument’s variation.

Importantly, we want to explore both the raw variation in the instrument and its

residualized variation, after accounting for the fixed effects of the differential exposure design

(e.g., unit i and time t effects). While the raw variation allows assessing the levels of the instrument

(e.g., across counties), the residualized variation provides the relevant information for

understanding the variation exploited in the differential exposure design (deHaan 2021). To

describe the levels and variation, we can make use of graphical illustrations. We, for example, can

use histograms or box plots to illustrate the raw and residualized levels and variation of the

instrument and its components along the various dimensions (i, t, and k).

3.4.2 Correlated Factors

In a second set of tests, we can examine possible bias from confounding factors correlated

with the Bartik instrument’s variation. In the spirit of the confounder analysis in Breuer (2021),

we can regress the full treatment variation (x

i,t

) and the instrument (z

i,t

) on observable confounders

(e.g., proxies for growth opportunities) and the fixed effects of the differential exposure design

(e.g., unit i and time t effects). If the observable confounders are important, they will explain a

notably fraction of the treatment’s residual variation (i.e., the within-R

2

after purging the fixed

effects). By contrast, the observable confounders should explain significantly less of the

instrument’s residual variation if the instrument is successful in reducing correlated variable

concerns.

In a similar vein, we can gauge the importance of correlated omitted variables by running

our differential exposure designs with and without controls for observable confounders. Following

Oster (2019), we would want to see a limited change of the instrument’s coefficient value upon

17

inclusion of the observable confounders. At the same time, we would want to see a substantial

increase in the explanatory power of the design with controls for the observable confounders. The

combination of these two patterns would suggest that the observable confounders are indeed

important determinants of our outcome of interest but do not seem to be significantly correlated

with our instrument. Hence, we can be confident that endogeneity concerns related to the observed

confounders are successfully allayed by the instrument. We can even hope that endogeneity

concerns related to unobserved confounders may similarly be allayed if we have good reasons to

expect that, compared to the observed factors, unobserved factors are less important determinants

of the outcome or less correlated with the instrument. Admittedly though, this condition is typically

challenging to argue for and naturally subjective.

Lastly, we can try to explicitly control for concerns that the differential impact identified

with the Bartik instrument reflects other factors correlated with the underlying characteristics (e.g.,

pre-determined shares and common trends). We, for example, can construct controls by using one

of the two characteristics underlying the Bartik instruments (e.g., pre-determined shares) and

combining it with other trends (e.g., common production trends instead of employment trends).

13

By constructing and including these controls, we can reduce concerns that the Bartik instruments’

differential impact across units with distinct pre-determined shares occurs due to trends in

variables (e.g., production) other than the one used in the Bartik instrument construction (e.g.,

employment).

14

This approach is akin to interacting control variables with unit (i) and/or post-

13

Similarly, we can interact the common trend of interest (e.g., industry employment rates) with other pre-determined

shares (e.g., industry shares of production or external finance dependence).

14

In this vein, Borusyak and Hull (2020) propose constructing a control for the non-random exposure of units to

exogenous shocks by combining the endogenous shares with various possible shocks. The average of such (placebo)

Bartik instruments, constructed using possible shocks instead of the actual shock realization, provides a useful control

for the possibility that some units are just naturally more exposed to certain shocks than others. This placebo control

can be included in the differential exposure design. Alternatively, it can directly be deducted from the Bartik

18

period (t) indicators in standard difference-in-differences designs. This controlling approach is

useful if we worry that other factors exhibit a differential relation (across units) or changing

relation (over time) with the outcomes. It is noteworthy though that this approach may control

away part of the effect we are interested in (e.g., if the other factors only change due to our

treatment). Accordingly, we should not necessarily reject the validity of a given Bartik instrument

just because its coefficient attenuates/changes with the inclusion of these Bartik-instrument-like

controls.

3.4.3 Treatment Heterogeneity

In a third set of tests, we can examine possible heterogeneity in the Bartik instrument’s

treatment effect. To this end, we can rerun our Bartik estimation dropping each unit (i), time (t),

or subdimension (k) at a time, in the spirit of a jackknife approach. If the resulting estimates are

relatively stable, the treatment effect does not appear to be driven by any given unit, time period,

or subdimension (e.g., industry). This result would be comforting as it suggests that there is limited

treatment-effect heterogeneity, which simplifies the interpretation of the (weighted average)

treatment effect. It would further suggest that there is limited risk for bias from any given unit,

time period, or subdimension, as none individually is chiefly driving the treatment effect. If, by

contrast, the estimates are sensitive to the exclusion of individual units, time periods, or

subdimensions, we must worry about heterogeneity or bias.

To differentiate between heterogeneity and potential bias, Goldsmith-Pinkham et al. (2020)

provide a possible way to decompose the Bartik estimate. They recast the Bartik instrument

approach as a generalized method of moments (GMM) approach with multiple instruments (e.g.,

instrument. Borusyak and Hull (2020) even suggest that deducting such placebo control from the raw treatment

variation can in some cases be enough to reduce bias. The benefit of this approach, compared to the usual Bartik

approach, is that we can use more variation than would be used by the Bartik instrument, which focuses on a specific

subpart of the full treatment variation.

19

county-industry shares). In this framework, the Bartik estimate is a weighted combination of just-

identified estimates based on each instrument (e.g., the shares).

15

This decomposition allows

explicitly assessing the heterogeneity across estimates and the importance of individual estimates

(i.e., their weights). The importance of the individual estimates helps understanding which source

of the treatment variation chiefly drives the Bartik instrument. Ideally, we would like to see

dispersed and exclusively positive weights. In that case, no individual source of variation

dominates the Bartik estimate and the interpretation of the Bartik instrument is simplified. By

contrast, if any individual estimate exhibits an outsized weight, the weighted average Bartik

estimate may be susceptible to bias due to factors correlated with the instrument (i.e., share)

identifying the dominating estimate. Similarly, if there are several estimates receiving negative

weights, the Bartik instrument may provide a hard-to-interpret combination of individual effects

of limited interest. This concern is related to the complication of interpreting the weighted average

effect in generalized difference-indifferences designs (e.g., de Chaisemartin and D’Haultfœuille

2020; Barrios 2021; Goodman-Bacon 2021).

3.5 Numerical Example

We can make the general insights about the construction of Bartik instruments and their

estimation more concrete with a numerical example using simulated data. In the spirit of the

canonical Bartik example, the simulated data features mean-reverting local industry employment

shares, local industry employment rates with a common (nationwide) industry-specific factor, and

a confounder affecting both employment (shares and rates) and wages in a given county, industry,

15

The insights and diagnostic tests described in Goldsmith-Pinkham et al. (2020) are based on a framework which

assumes conditional share exogeneity. By contrast, the insights and tests described in Borusyak et al. (2021) are based

on a framework which assumes conditional shock exogeneity. Borusyak et al. (2021) stress that we should choose the

appropriate diagnostic tests ex ante based on which of the two distinct assumptions is most plausible in our particular

setting.

20

and year.

16

,

17

Table 1 shows an excerpt of the data for two counties (150 and 151), two years (1 and 2),

and two industries (10 and 11). We observe that the employment shares (w

i,t,k

) and employment

rates (e

i,t,k

) vary across counties (i), years (t), and industries (k). The sum-product of local industry

employment shares and local industry employment rates generates the county-level employment

rate (

), which represents our county-year-varying treatment of interest.

The Bartik instrument (

) also varies at the county-year level. Unlike

the full treatment variation, the instrument, however, is generated by taking the sum-product of

pre-determined local industry employment shares (w

i,k

) and time-varying nationwide industry

employment rates (e

t,k

). The pre-determined local industry employment shares are constructed by

using the employment shares in a given county and industry observed in the first year of the panel

across all subsequent years. Accordingly, the share for industry 10 in county 150 is 3.1% in the

first year and every sample year thereafter (highlighted in bold). The nationwide industry

employment rates are constructed by aggregating the local industry employment rates across

16

The simulated data comprise 1,000 counties, 30 industries, and 15 years. For simplicity, the data abstract from

confounding heterogeneity across counties and years, as this heterogeneity would be accounted for by the fixed effects

structure (e.g., Gormley and Matsa 2013). The only confounder in the data is a factor driving wages and employment

(rates) in random county-industry-year combinations. For the specific parameterization of the simulation, please refer

to the program code.

17

I deviate from the actual implementation in Bartik (1991) by using a hypothetical county-industry employment rate.

In the actual data, such rate is not available at the industry level (e.g., because we do not know how many employees

would work in a given industry). For the sake of illustrating Bartik instruments, the use of such employment rate has

two benefits. First, the employment rate, in contrast to total employment, exhibits a convenient scale that is comparable

across various aggregation levels (e.g., county vs. national rates). As a result, the treatment and Bartik instrument

exhibit the same scale and the instrument represents a direct decomposition of the treatment. Second, the employment

rate allows separating the employment shares and shocks. As a result, we can examine the impact of confounders on

either of the components. Using total employment as the basis for both the shares and shocks, by contrast, would not

allow such separate investigation. Given that Bartik instruments often use distinct shares (e.g., import shares) and

shocks (e.g., leniency laws), such separate evaluation appears useful. I caution though that the employment-rate

approach is not immediately applicable to the available employment and wage data. To apply the Bartik logic to actual

employment and wage data, one would have to use an appropriate scaler (e.g., total county-level employment) or use

a logarithmic transformation of employment (e.g., Bartik 1991).

21

counties using local employment data.

18

As a result, the employment rate for industry 10 in county

150 varies from year 1 (81.1%) to year 2 (82.3%). This time-series variation, however, is only due

to the nationwide employment rate trend. Accordingly, the rate for industry 10 in a given year is

the same in both counties 150 and 151 (e.g., 81.1% in year 1; highlighted in bold).

By construction, the Bartik instrument is purged of treatment variation due to local

industry-specific factors (e.g., growth opportunities). Hence, it uses only a subpart of the full

treatment variation. While this approach reduces power, it also reduces endogeneity concerns as

the instrument is widely uncorrelated with local industry-specific confounders affecting both local

employment (shares and rates) and wages.

Table 2 documents the bias-variance trade-off. Panel A shows estimates from OLS and IV

regressions in a simulated sample without a confounder correlated with both local industry

employment and wages. Absent a confounder, the OLS estimate closely approximates the true

impact of employment rates on wages (β = 1), as parameterized in the simulated data. The reduced-

form estimate, which uses the instrument (z

i,t

) instead of the full treatment variation (x

i,t

) as the

right-hand-side variation, also produces a positive coefficient estimate. The magnitude of the

estimate (β

OLS

= 0.515) is attenuated though. The first-stage regression shows the reason for the

attenuation. The instrument does not one-for-one translate into greater local employment rates.

Although the first-stage estimate is less than one (β

FS

= 0.493), it nevertheless indicates that the

instrument is highly relevant. Its sizable t-statistic of 23.64 translates into an F-statistic of over

18

The simulated data contain employment levels (in terms of number of employees) at the county-industry-year level.

With this granular data, we can calculate the nationwide industry employment rate excluding the own employment

rate of each county-industry-year. This leave-one-out approach addresses finite sample bias (Goldsmith-Pinkham et

al. 2020). This adjustment matters little if our data span a large number of counties. In this case, we can neglect the

adjustment, especially if data constrains us to observing only aggregate data (e.g., nationwide industry employment

rates instead of local employment rates and levels), such that we cannot reconstruct the adjusted nationwide rate from

bottom up.

22

500.

19

A high relevance is typical for Bartik instruments, given they are constructed using two key

sources of the full treatment variation. After adjusting the reduced-form estimate with the first-

stage estimate, the second-stage (IV) estimate closely approximates the true impact (β

IV

= β

RF

/β

FS

= 0.515/0.493 = 1.045), just like the OLS estimate. Notably, however, the OLS coefficient is

estimated with substantially greater precision (t-stat: 12.54) than the IV coefficient (t-stat: 4.07).

The greater precision is owed to the fact that the full treatment variation uses more variation than

the Bartik instrument. Absent local time-varying confounders, we can use all the variation

available to us (i.e., x

i,t

).

In the presence of local confounders, we not only care about precision but also need to

worry about bias. Panel B documents the impact of an omitted factor, such as growth opportunities,

which positively impacts both local industry employment rates (e

i,t,k

) and wages (y

i,t,k

). The

presence of such factor biases the OLS estimate (β

OLS

= 4.937) significantly upwards. By contrast,

the second-stage (IV) estimate (β

IV

= 0.982) remains close to the true value. Panel C, likewise,

documents the impact of an omitted factor, such as skill- or capital-biased technological change,

which negatively impacts local industry employment rates and positively impacts wages. The

presence of such factor biases the OLS estimate (β

OLS

= −2.929) significantly downwards. By

contrast, the second-stage (IV) estimate (β

IV

= 1.114) remains close to the true value again.

The estimates in Panels B and C document that, while the Bartik instrument comes with

less precision, it promises to significantly reduce bias arising from local time-varying

confounders.

20

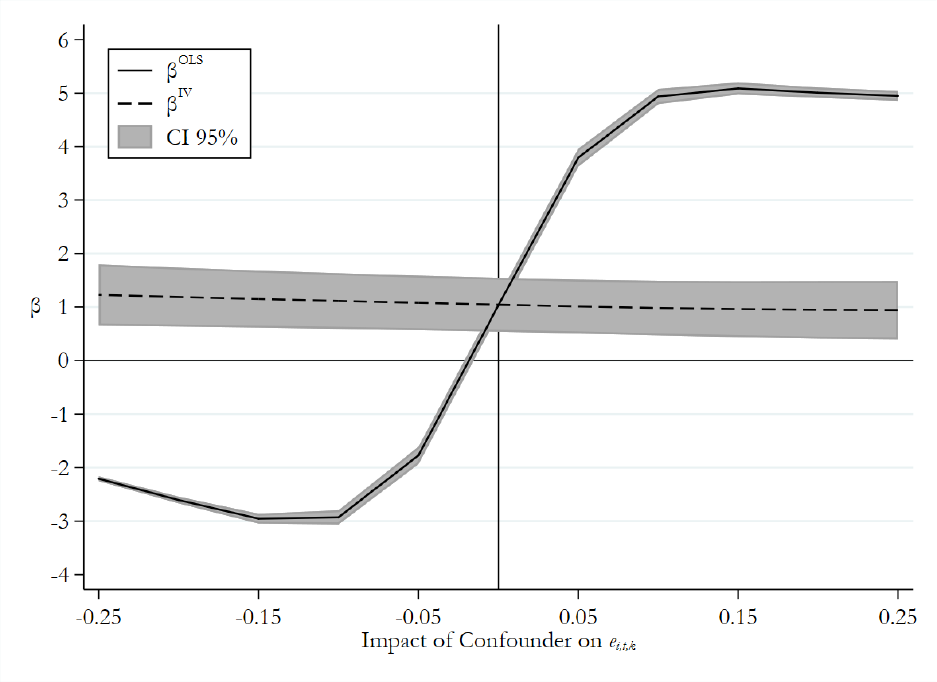

Figure 1 reinforces this insight. For varying levels of impact of the confounder on

19

The partial F-statistic of interest for the first-stage relevance is basically the squared t-statistic of the instrument.

20

The inferences in the simulation are based on standard errors clustered at the county level. Adão et al. (2019)

highlight that cross-unit correlations (e.g., due to similar shares) can complicate inference in shift-share designs. For

a formal treatment of the issue and practical solutions (e.g., programs to adjust the standard errors appropriately), refer

to Adão et al. (2019) and Borusyak and Hull (2020).

23

local industry employment rates (e

i,t,k

), it documents coefficient estimates and confidence intervals

obtained using the OLS and the IV approaches. While the confidence intervals of the OLS

estimates are significantly narrower, the coefficient estimates exhibit substantial bias compared to

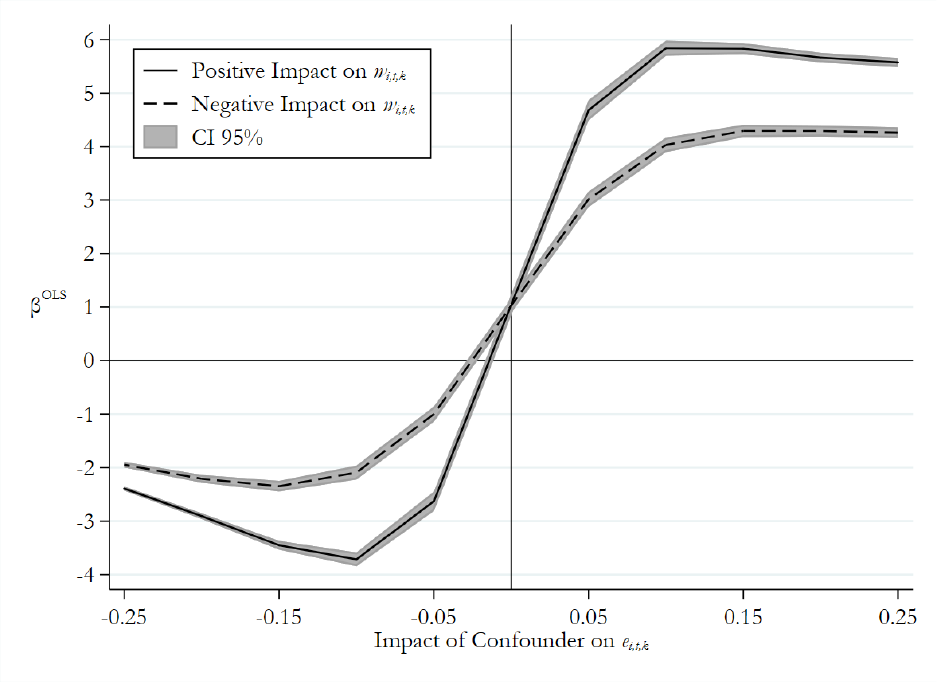

the IV estimates. Figure 2 documents that the bias in the OLS estimates is amplified if the

confounding factor not only impacts the local industry employment rate, but also increases the

local industry employment share (w

i,t,k

). This pattern highlights that bias in the estimates is largest

if the confounder impacts the more important industries.

21

4 Special Case: Simulated Instrument

The Bartik instrument logic not only applies to panel data with information on units (i)

over time (t) but also extends to cross-sectional data with information on units (i) (e.g., industries)

across any other dimension (j) (e.g., countries).

22

A special case of Bartik instruments for cross-

sectional data are the so-called simulated instruments (e.g., Currie and Gruber 1996; Goldsmith-

Pinkham et al. 2020). These instruments exploit cross-sectional variation generated by thresholds,

a frequent feature in accounting-related regulations and contracts (e.g., Degeorge et al. 1999;

Dichev and Skinner 2002; Iliev 2010; Bernard et al. 2018; Breuer et al. 2018). They are related to

regression discontinuity designs (e.g., Lee and Lemieux 2010). Unlike regression discontinuity

designs, simulated instruments, however, do not exploit local variation in the treatment status of

firms just around a given threshold. Instead, they can be used to generate plausibly exogenous

21

The increasing influence of confounders with the importance of a given unit of the subdimension (e.g., industry)

highlights why we care about understanding which dimensions chiefly drive the Bartik instrument variation (Section

3.4).

22

Similarly, the logic of time-series difference-in-differences designs extends to cross-sectional difference-in-

differences designs:

. Rajan and Zingales (1998), for example, exploit the differential impact of

country-level financial development (x

j

) on industries with distinct pre-determined external financing dependence (x

i

)

to examine the impact of financial development on growth.

24

variation in the share of treated firms. Hence, they lend themselves to a market-level instead of a

firm-level investigation and do not merely identify a very local treatment effect.

Simulated instruments can, for example, be used to examine the impact of size-based

regulation varying across countries (e.g., due to distinct reporting thresholds) on product-market

outcomes such as market-share concentration (e.g., to gauge the proprietary cost of reporting). A

simple regression of market-share concentration (y

i,j

) on the share of regulated firms in a given

industry and country (x

i,j

) (i.e., firms above a given country’s threshold) would raise several

endogeneity concerns. We, for example, would be worried that some industries (e.g., capital-

intensive industries) or countries (e.g., France) have systematically higher market-share

concentrations and more large firms (i.e., a higher share of regulated firms) than others. These

systematic differences across industries and countries can be addressed in a differential exposure

design through industry and country fixed effects:

(10)

Still, we would remain concerned that reverse causality, simultaneity, and omitted factors varying

at the country-industry level (i,j) could confound our estimation. We, for example, would worry

that barriers to entry vary not only across industries and countries but also at the country-industry

level. Entry barriers in the manufacturing industry in France, for example, could be particularly

high compared to both the barriers in other French industries and the manufacturing industry in

Britain. Such differential variation in entry barriers would threaten to introduce omitted variable

bias, as the barriers, by favoring larger firms, tend to increase both market-share concentration and

the share of firms above thresholds.

Following the Bartik logic, we can reduce endogeneity concerns by using simulated

instruments. To construct such instruments, we must first decompose the share of regulated firms

25

(x

i,j

) to a subdimension (k). The relevant subdimension in this case is the firm level:

(11)

The share of regulated firms is equivalent to the country-industry-level average of a firm-level

indicator taking the value of one if a given firm’s size (s

i,j,k

) is above its country’s threshold (

),

and zero otherwise. This decomposition shows that the share of regulated firms not only varies

because of differences in countries’ thresholds, but also because firms in a given industry may be

larger in one country than in another. The latter variation is likely driven by a host of country-

industry-specific factors (e.g., entry barriers) which are hard to control for.

In the spirit of the Bartik instrument construction, simulated instruments (

) focus on the

plausibly exogenous dimensions of the components making up the share of regulated firms. Those

dimensions are the industry-specific (not country-industry-specific) firm-size distributions (s

i,k

)

and countries’ thresholds (

):

(12)

The industry-specific firm-size distributions can be constructed by pooling all firms in a given

industry across countries. This approach provides a typical or “simulated” distribution of firm sizes

which is representative for the entire sample of countries. It is akin to using a nationwide

employment rate per industry instead of the county-industry-specific employment rates in the

construction of the canonical Bartik instrument.

The simulated instrument captures the share of firms in a given industry and country that

would typically be regulated had the country’s threshold been applied to the industry’s

representative firm-size distribution. It only varies at the country-industry level, that is, the level

26

of the identifying variation (i,j), as a result of the differential impact of countries’ thresholds on

different industries. Such differential impact occurs because some industries are naturally more

affected by a given threshold than others. A threshold exempting firms with less than 50 employees

from reporting requirements, for example, will systematically affect labor-intensive industries,

where more firms have a high number of employees, more than capital-intensive industries.

Notably, the simulated instrument, by construction, does not vary due to endogenous

differences in firm sizes in a given industry across countries. By using the same firm-size

distribution for the manufacturing industry in France and Britain, for example, the share of

regulated firms only varies across those two country-industries due to differences in those

countries’ regulatory thresholds. It does not vary because one country’s industry has higher

barriers to entry than the other. Hence, we are less worried that omitted country-industry-specific

factors, such as entry barriers, confound our estimation.

5 Accounting Applications

Bartik instruments promise to provide researchers with a new tool in their empirical

toolbox to provide credible inferences regarding questions of interest to the accounting literature.

To illustrate the usefulness for accounting research, I discuss a possible application to the core

accounting question of how accounting quality impacts the cost of capital, present two recent

examples of accounting studies using Bartik and simulated instruments in detail, and list further

studies using versions of Bartik instruments.

23

5.1 Possible Application

The impact of accounting quality on the cost of capital is a question of vital interest to the

23

I chose the specific examples due to my familiarity with the studies, not because they are the only accounting studies

using Bartik instruments.

27

accounting literature (Lambert et al. 2007; Beyer et al. 2010). Estimating this impact is challenging

though, even with panel data. As discussed earlier, endogeneity concerns such as reverse causality,

simultaneity, and correlated omitted factors loom large, just as with the estimation of the

employment-wage relation in the canonical Bartik application.

We can attempt to reduce the endogeneity concerns by using a Bartik instrument that

focuses on a subpart of firms’ accounting quality variation that is plausibly more exogenous than

the full accounting-quality variation. To construct such instrument, we need to first consider a

subdimension along which we can decompose firms’ accounting quality. We, for example, could

use the locations of multi-establishment firms or the industries of multi-segment firms as relevant

subdimensions. We can then create firm-time varying Bartik instruments by weighting location-

specific or industry-wide accounting quality measures with the respective pre-determined sales

share of a given firm in a given location or industry. As location-specific or industry-wide

accounting-quality measures, we could consider outcome-based measures such as the average

earnings/accruals quality or the total number of restatements, comment letters, or AAERs

(excluding each firm’s own value) (e.g., Leuz et al. 2003; Dechow et al. 2010; Nikolaev 2018; Du

et al. 2020; Breuer and Schütt 2021; Nissim 2021).

In a firm-level differential exposure design with firm and year fixed effects, the Bartik

instrument would capture the differential impact of location-specific or industry-wide trends in

accounting-quality outcomes on firms with distinct pre-determined exposures to those locations or

industries. This instrumented treatment variation can be expected to be more plausibly exogenous

than firms’ observed accounting quality (e.g., a restatement indicator). In particular, the

instrumented treatment variation does not vary due to firms’ changes in their industrial focus over

time or idiosyncratic accounting-quality changes that could be due to a host of time-varying factors

28

(e.g., an increase in operating volatility) (e.g., Hribar and Nichols 2007). Notably, the instrumented

treatment variation is also more plausibly exogenous than alternative instruments used (and

criticized) in the literature such as the industry-level average of accounting quality (Larcker and

Rusticus 2010). The industry-level average may reflect changes in economic fundamentals (e.g.,

operating volatility) common to the entire industry. By contrast, the instrumented treatment

variation does not merely vary at the industry-year level. Rather, it varies at the firm-year level

due to the differential exposure of multi-segment firms to various industries. This additional level

of treatment variation allows controlling for any confounding factors varying at the industry level

via industry-year fixed effects. This finer level of variation is not available for the industry-average

instrument, which would be subsumed by the fixed effects (deHaan 2021). Despite these

identification benefits, the outcome-based Bartik instrument is still subject to important

endogeneity concerns. The instrument, for example, could primarily capture changes in the

operating environment in the various industries that multi-segment firms operate in instead of

isolate accounting-related changes.

To improve the identification, we can consider constructing the Bartik instrument using

location-specific or industry-wide shocks to accounting-quality inputs or incentives, instead of

outcomes. We could, for example, use variation in location- or industry-specific changes in

standards, regulations, or enforcement (e.g., Jackson and Roe 2009; Kedia and Rajgopal 2011;

Blackburne 2014; Christensen et al. 2020; Wu 2020). Using these accounting-specific shocks

instead of broad trends in accounting-quality outcomes would allow us to more confidently

attribute the impact of the instrument on firms’ cost of capital to the impact of accounting quality

as opposed to economic fundamentals. Notably, using these shocks as part of a Bartik instrument

instead of a standard difference-in-differences design, with a dichotomous treatment, allows

29

exploiting finer treatment variation due to the differential exposures of firms to the various shocks.

The finer variation allows accounting for broad location- or industry-specific changes via location-

and industry-year fixed effects, as multilocation/segment firms are exposed to various shocks to

different degrees.

This potential application of Bartik instruments to the question of how accounting quality

impacts the cost of capital illustrates the versatility of the generic Bartik approach and its promise

for future accounting research. It also demonstrates that the specific implementation of Bartik

instruments and the choice of the relevant subdimension, in particular, depends on two factors: the

availability of granular data (e.g., sales by location or industry per firm) and the level of the

common shocks (e.g., location- or industry-specific regulations).

24

If data are available for multiple

subdimensions, we would want to select the subdimension with the most plausibly exogenous

shares or shocks (e.g., industry-level enforcement reforms). This judgement needs to be based on

theoretical and institutional arguments. If several of the subdimensions promise to be useful in

constructing valid instruments, we can also construct multiple instruments. Multiple instruments

can be used separately but also jointly. The joint use allows examining the validity of individual

instruments via tests for overidentifying restrictions (Sargan 1958; Hansen 1982; Chao et al. 2014).

Given the increasing availability of granular data on firms (e.g., establishment-level data) and

regulatory actions at distinct levels (e.g., industry-specific guidance), I expect Bartik instruments

to find applications in various streams of the accounting literature. In the next section, I describe

some recent examples of such applications.

24

In the absence of granular firm-level data, we can still construct Bartik instruments at more aggregate levels such

as the industry or location level (e.g., Bourveau et al. 2020). Treatment variation at such aggregate levels is often used

in firm-level designs in accounting research (e.g., state-level policy adoptions) (Armstrong et al. 2021).

30

5.2 Recent Applications

Bourveau et al. (2020) provide a recent example for an application of Bartik instruments

in accounting research. They study the impact of product-market collusion incentives on firms’

public disclosures. To examine this question empirically, they face two issues. First, successful

product-market collusion, by its very nature, tends to be unobservable. Second, observable

measures related to collusion incentives (e.g., market-share concentration, cartel-detection rates,

or strategic alliances) tend to be related to a host of other determinants of disclosure (e.g.,

proprietary costs, external financing needs, and business-cycle variation).

To identify plausibly exogenous variation in collusion incentives, Bourveau et al. (2020)

build a time-varying industry-level measure of collusion incentives of US firms (z

i,t

; where i

denotes industries and t denotes time). Following the logic of Bartik instruments, this measure

combines a pre-determined import share (w

i,k

), capturing the share of industry i’s sales imported

from country k out of all industry i’s sales in 1990, and a common shock (e

t,k

), capturing the

staggered adoption of leniency laws in foreign country k across time t. This measure captures the

differential impact of foreign countries’ adoption timing of leniency laws on industries with

distinct (pre-determined) product-market links to the foreign countries. Japan, for example,

strengthened its anti-collusion efforts through the introduction of leniency laws in 2005. The

instrument exploits the fact that the automobile industry in the US is especially affected by this

shock because a significant portion of its imports comes from Japan. Unlike other industry- or

firm-year measures of collusion incentives (e.g., engagements in strategic alliances), the Bartik

instrument’s variation is less likely to be confounded by other factors determining firms’ public

disclosures (e.g., external financing needs).

Breuer (2021) provides an example for an application of simulated instruments in

31

accounting research. In that study, I examine how financial-reporting mandates in Europe impact

industry-wide competition and resource allocation. To measure the exposure of a given industry

to the mandates, I use the share of firms in a given industry exceeding a given European country’s

size-based financial-reporting thresholds (x

i,j

; where i denotes industries and j denotes countries).

As discussed in Section 4, we may worry that this share is driven by other determinants of

competition and resource allocation. Entry barriers, for example, by favoring large firms, can lead

to both, greater market-share concentration and more firms above countries’ thresholds. Consistent

with such confounding influence, I, for example, observe that the share of regulated firms is

strongly positively associated with both market-share concentration and firm size.

To reduce endogeneity concerns, I use a “simulated” share of regulated firms following the

logic of simulated instruments. I construct this share (z

i,j

) by calculating the share of firms

exceeding a given country’s size thresholds (

) in a representative Europe-wide sample of firms

(k) in a given industry (with firm sizes s

i,k

).

25

This simulated instrument captures the differential

impact of countries’ thresholds on industries with systematically distinct firm-size distributions

(e.g., labor- vs. capital-intensive industries). A threshold exempting firms below 50 employees

from reporting requirements, for example, affects a greater share of firms in labor-intensive

industries, where more firms will have 50-plus employees, than in capital-intensive industries.

Unlike the actual share of regulated firms in a given industry, the simulated instrument does not

vary with idiosyncratic differences in industry-level firm-size distributions across countries. This

feature reduces concerns about omitted factors driving both the share of regulated firms and

competition measures. Notably, I observe that the simulated share, unlike the actual share, is not

associated with endogenous firm-size differences across countries and industries. As a result, the

25

To obtain such sample, we can simply pool all firms in a given industry across all European sample countries.

32

sign of the association between the share of regulated firms and market-share concentration flips

when using the simulated instrument. The instrumented estimate suggests that more financial-

reporting regulation (e.g., disclosure) appears to reduce rather than increase local market-share

concentration, consistent with proprietary-cost theories.

Other recent studies in accounting research using versions of Bartik instruments include,

for example, Breuer et al. (2020), Granja and Moreira (2020), Duguay (2021), and Kim (2021).

Table 3 provides an overview of the instruments used in these studies. Several of the studies use

Bartik-like instruments to learn about market-level effects (e.g., at the county level). The

instruments, however, can also be used to study firm-level responses (e.g., because the Bartik

instrument varies at the firm level or because the outcome of interest varies at the firm level).

Overall, I expect Bartik instruments to find applications in a vast array of settings, especially given

the increasing availability of granular data (e.g., on economic activity in subdimensions such as

industries, segments, or locations), which enables the treatment decomposition and instrument

construction.

6 Conclusion

Bartik instruments can reduce endogeneity concerns in differential exposure designs (e.g.,

panel regressions with unit and time effects), which are frequently used in accounting research. In

these designs, the treatment effect is identified by differential changes across units over time.

Accordingly, we are concerned about the influence of omitted factors that vary both across units

and over time (e.g., growth opportunities). Bartik instruments attempt to reduce this concern by

focusing on a plausibly exogenous subset of the treatment variation.

Bartik instruments are constructed in two steps. First, we decompose the treatment

variation to a common subdimension. In the canonical Bartik application, we, for example,

33

decompose county-level employment rates into county-industry employment-shares and county-

industry employment rates. Next, we focus only on the variation driven by pre-determined

characteristics and common shocks. In the canonical application, we, for example, use the

interaction of pre-determined county-industry employment shares and nationwide industry

employment rates as our instrument.

Bartik instruments isolate the subpart of the treatment variation across units over time due

to the differential impact of common trends on units with distinct pre-determined exposures.

Accordingly, the instruments, by construction, are typically highly correlated with the full

treatment variation. Importantly, however, the instruments do not vary across units over time as a

result of unit-time specific shocks or changes (e.g., local growth opportunities), unlike the full

treatment variation. Hence, compared to the full treatment variation, the instruments are less likely

to be unduly confounded by omitted factors.

The logic behind Bartik instruments is related to familiar approaches (instrumental

variables and difference-in-differences designs) and extends to several applications and settings.

For the special case of cross-sectional data and (regulatory) thresholds, for example, we can

construct simulated instruments, following the Bartik logic. Given this broad applicability, Bartik

instruments and their variants promise to provide accounting researchers with a versatile new tool

in their empirical toolbox to study accounting questions. This tool, by exploiting continuous

variation in the exposure of units to common shocks, may prove particularly useful to accounting

research as we often lack truly unaffected control groups (Leuz and Wysocki 2016). While this

tool is no silver bullet, if properly applied, it can be expected to at least help reduce important

endogeneity concerns frequently faced in accounting research.

34

References

Adão, R., M. Kolesár, and E. Morales. 2019. Shift-share designs: Theory and inference. Quarterly

Journal of Economics 134 (4): 1949–2010.

Angrist, J.D., and G.W. Imbens. 1995. Two-stage least squares estimation of average causal effects

in models with variable treatment intensity. Journal of the American Statistical Association

90 (430): 431–442.

Angrist, J.D., and A.B. Krueger. 2001. Instrumental variables and the search for identification:

From supply and demand to natural experiments. Journal of Economic Perspectives 15 (4):

69–85.

Armstrong, C., J. Kepler, D. Samuels, and D. Taylor. 2021. The evolution of empirical methods in

accounting research and the growth of quasi-experiments. Working paper, University of

Pennsylvania, Stanford University, University of Chicago. Available at:

www.ssrn.com/abstract_id=3935088.

Autor, D.H., D. Dorn, and G.H. Hanson. 2013. The China syndrome: Local labor market effects

of import competition in the United States. American Economic Review 103 (6): 2121–68.