Standards for

Internal Control

in the Federal

Government

By the Comptroller General of the

United States

September 2014

GAO-14-704G

United States Government Accountability Office

What is the Green Book and how is it used?

Important facts and concepts related to the Green Book and internal control

Page

structure

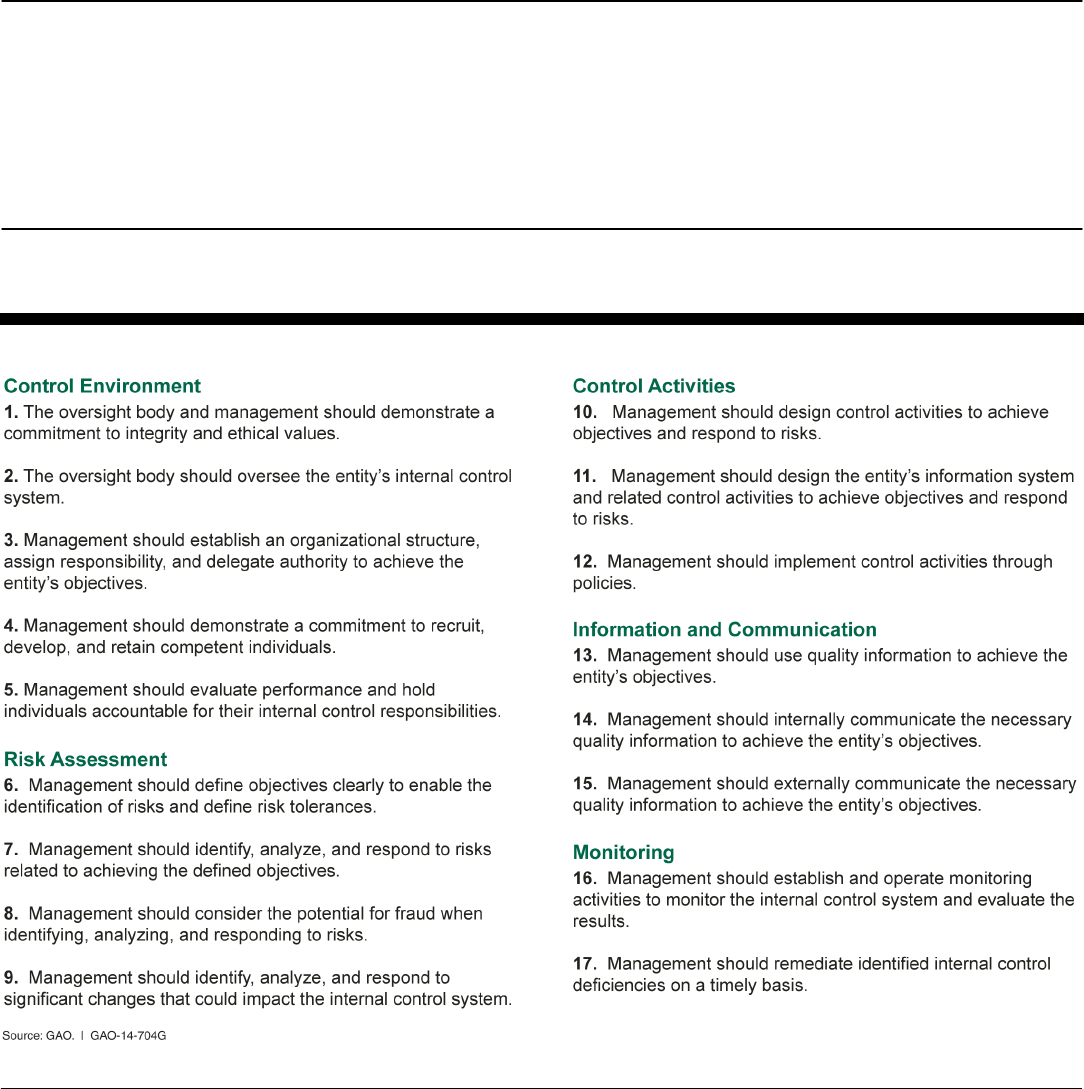

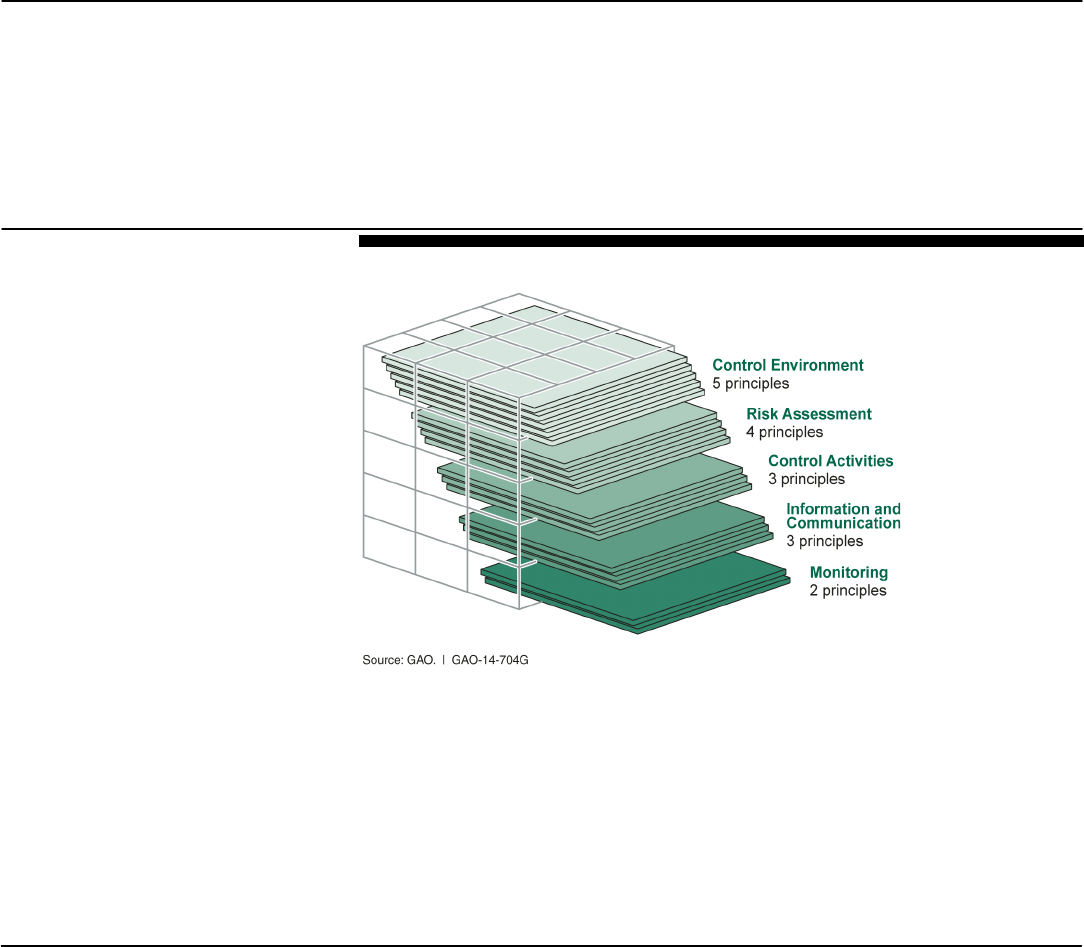

Control Environment

5 principles

Risk Assessment

4 principles

Control Activities

3 principles

Information and Communication

3 principles

Monitoring

2 principles

Each of the five

components of internal

control contains several

principles. Principles are the

requirements of each component.

Attributes

Each principle has important characteristics, called attributes,

which explain principles in greater detail.

Principles

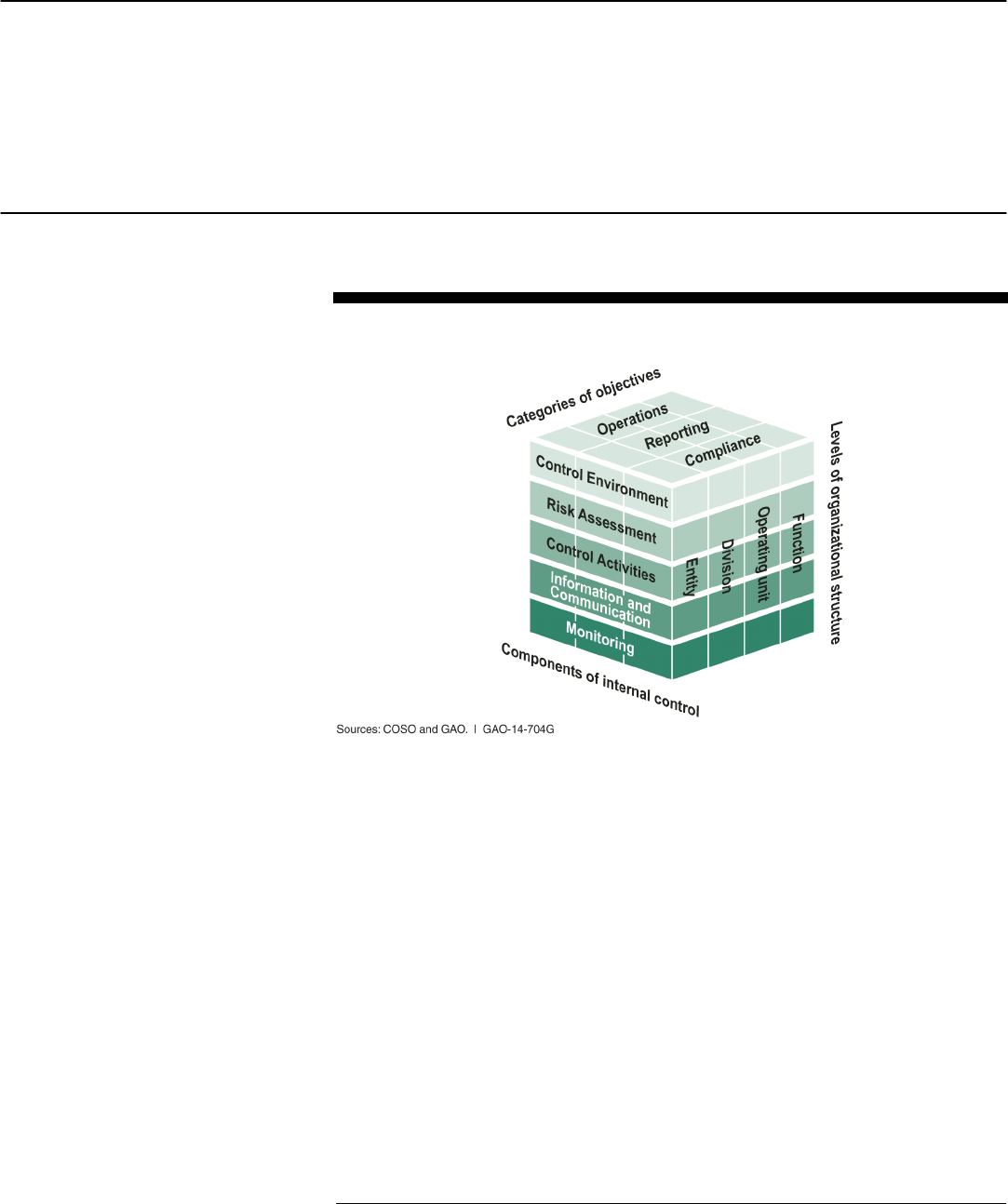

The

cube

The standards in the

Green Book are organized

by the five components of internal

control shown in the cube below. The five

components apply to staff at all organizational

levels and to all categories of objectives.

Risk Assessment

Control Activities

Components of

internal control

Entity

Division

Operating unit

Function

Levels of

organizational structure

Operations

Categories

of objectives

Compliance

Control Environment

Reporting

Green Book pages

show components, principles,

and attributes.

GAO.GOV/GREENBOOK

How does an entity use the Green Book?

Who would use the Green Book?

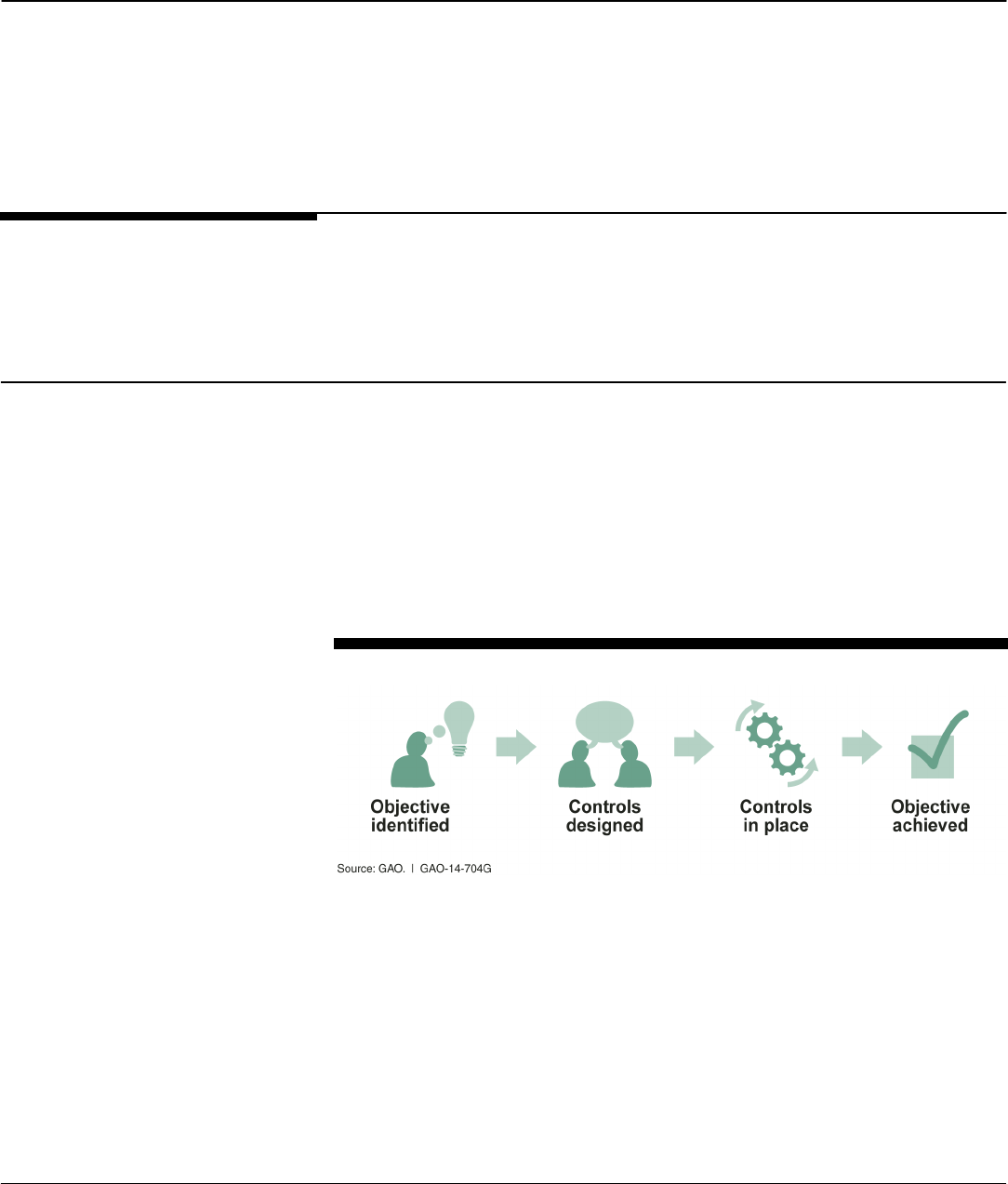

What is internal control?

Internal control is a process used by management to help an

entity achieve its objectives.

An entity uses the Green Book to design, implement, and

operate internal controls to achieve its objectives related to

operations, reporting, and compliance.

How is the Green Book related to

internal control?

Standards for Internal Control in the

Federal Government, known as the

Green Book, sets internal control

standards for federal entities.

Internal control and the Green Book

Sources: GAO and COSO. GAO-14-704G

Controls

designed

Objective

achieved

Objective

identified

Controls

in place

An independent public accountant

conducting an audit of expenditures

of federal dollars to state agencies

A compliance officer

responsible for making

sure that personnel have

completed required

training

A program

manager at a

federal agency

Inspector general staff

conducting a financial or

performance audit

How does internal control work?

Internal control helps an entity

Run its operations efficiently and effectively

Report reliable information about its operations

Comply with applicable laws and regulations

Information and

Communication

Monitoring

Control Environment

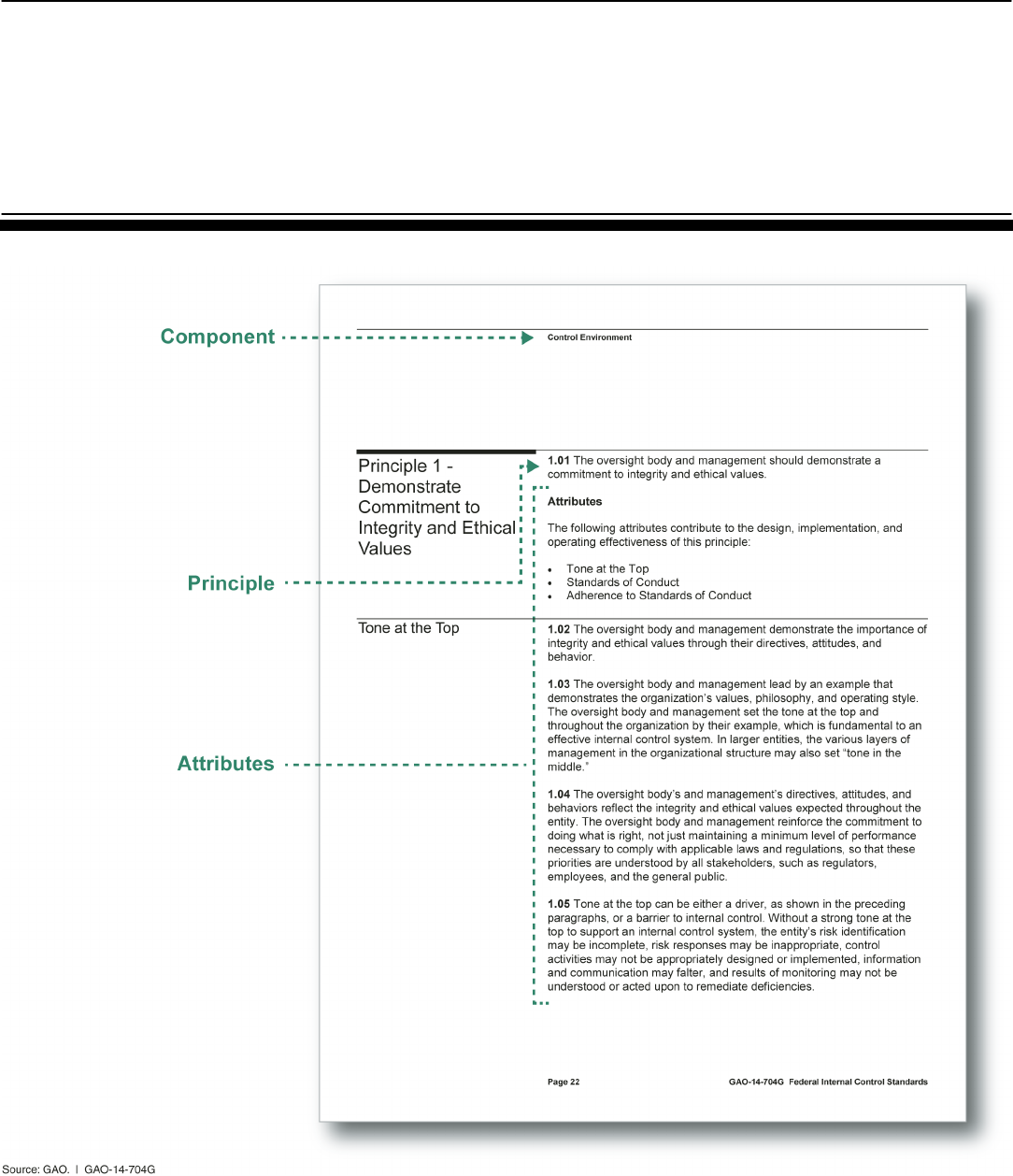

Page 22 GAO-14-704G Federal Internal Control

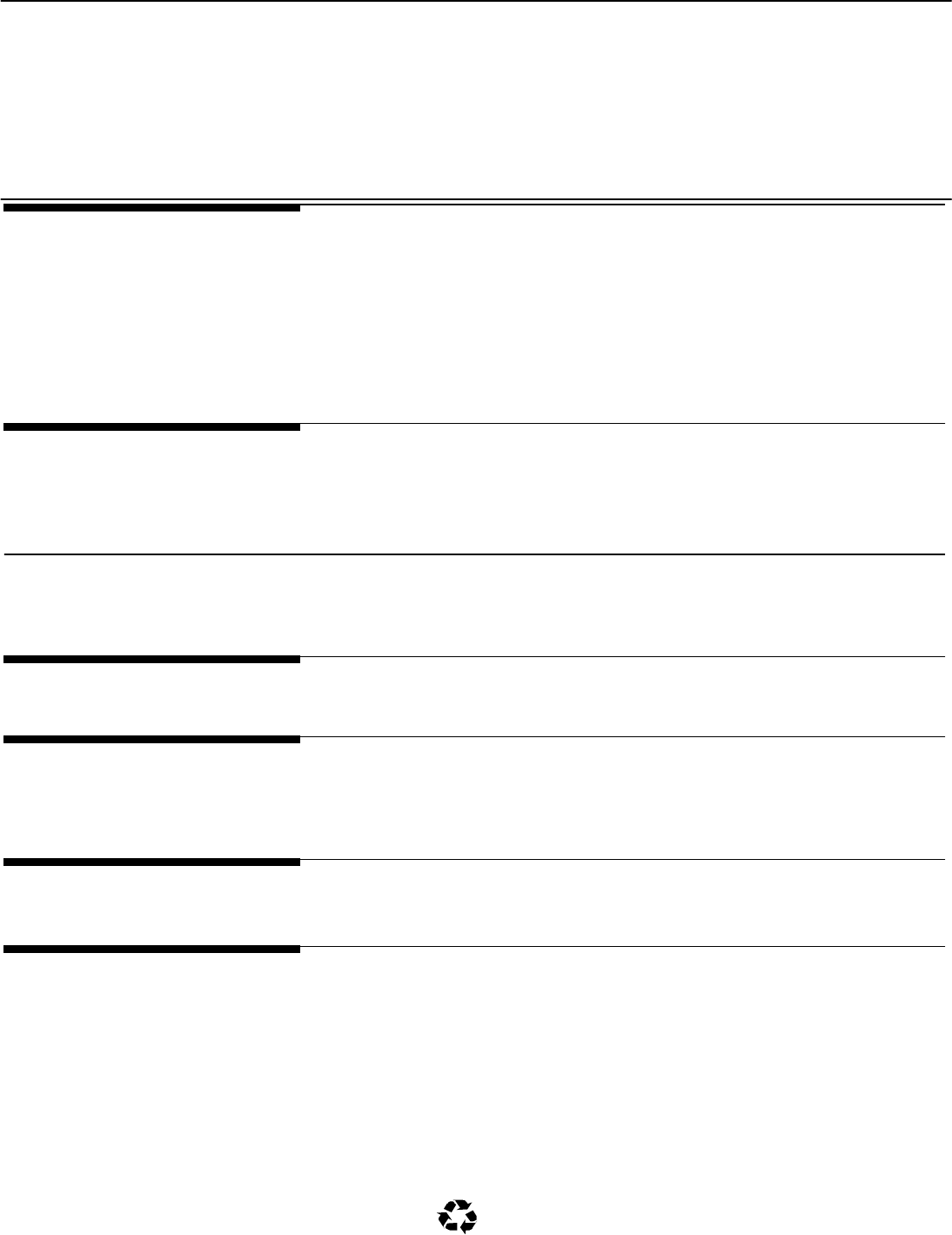

1.01 The oversight body and management should demonstrate a

commitment to integrity and ethical values.

Attributes

The following attributes contribute to the design, implementation, and

operating effectiveness of this principle:

• Tone at the Top

• Standards of Conduct

• Adherence to Standards of Conduct

1.02 The oversight body and management demonstrate the importanc

integrity and ethical values through their directives, attitudes, and

behavior.

1.03 The oversight body and man

agement lead by an example that

demonstrates the organization’s values, philosophy, and operating style.

The oversight body and management set the tone at the top and

throughout the organization by their example, which is fundamental to an

effective internal control system. In larger entities, the various layers of

management in the organizational structure may also set “tone in the

middle.”

1.04 The oversight body’s and management’s directives, attitudes, and

behav

iors reflect the integrity and ethical values expected throughout the

entity. The oversight body and management reinforce the commitment to

doing what is right, not just maintaining a minimum level of performance

necessary to comply with applicable laws and regulations, so that these

priorities are understood by all stakeholders, such as regulators,

employees, and the general public.

1.05 Tone at the top can be either a driver, as shown in the preceding

paragraphs, o

r a barrier to internal control. Without a strong tone at the

top to support an internal control system, the entity’s risk identification

may be incomplete, risk responses may be inappropriate, control

activities may not be appropriately designed or implemented, information

and communication may falter, and results of monitoring may not be

understood or acted upon to remediate deficiencies.

Principle 1 -

Demonstrate

Commitment to

Integrity and Ethical

Values

Tone at the Top

Attributes

Principle

Component

Page i GAO-14-704G Federal Internal Control Standards

Overview 1

Foreword 1

How to Use the Green Book 3

Section 1 - Fundamental Concepts of Internal Control 5

Definition of Internal Control 5

Definition of an Internal Control System 5

Section 2 - Establishing an Effective Internal Control System 6

Presentation of Standards 6

Components, Principles, and Attributes 7

Internal Control and the Entity 9

Roles in an Internal Control System 11

Objectives of an Entity 12

Section 3 - Evaluation of an Effective Internal Control System 14

Factors of Effective Internal Control 15

Evaluation of Internal Control 15

Section 4 - Additional Considerations 17

Service Organizations 17

Large versus Small Entities 18

Benefits and Costs of Internal Control 19

Documentation Requirements 19

Use by Other Entities 20

Control Environment 21

Principle 1 - Demonstrate Commitment to Integrity and Ethical

Values 22

Tone at the Top 22

Standards of Conduct 23

Adherence to Standards of Conduct 23

Principle 2 - Exercise Oversight Responsibility 24

Oversight Structure 24

Oversight for the Internal Control System 26

Input for Remediation of Deficiencies 27

Principle 3 - Establish Structure, Responsibility, and Authority 27

Organizational Structure 27

Assignment of Responsibility and Delegation of Authority 28

Documentation of the Internal Control System 29

Principle 4 - Demonstrate Commitment to Competence 30

Expectations of Competence 30

Recruitment, Development, and Retention of Individuals 31

Succession and Contingency Plans and Preparation 31

Principle 5 - Enforce Accountability 32

Contents

Page ii GAO-14-704G Federal Internal Control Standards

Enforcement of Accountability 32

Consideration of Excessive Pressures 33

Risk Assessment 34

Principle 6 - Define Objectives and Risk Tolerances 35

Definitions of Objectives 35

Definitions of Risk Tolerances 36

Principle 7 - Identify, Analyze, and Respond to Risks 37

Identification of Risks 37

Analysis of Risks 38

Response to Risks 39

Principle 8 - Assess Fraud Risk 40

Types of Fraud 40

Fraud Risk Factors 41

Response to Fraud Risks 41

Principle 9 - Identify, Analyze, and Respond to Change 42

Identification of Change 42

Analysis of and Response to Change 43

Control Activities 44

Principle 10 - Design Control Activities 45

Response to Objectives and Risks 45

Design of Appropriate Types of Control Activities 45

Design of Control Activities at Various Levels 49

Segregation of Duties 50

Principle 11 - Design Activities for the Information System 51

Design of the Entity’s Information System 51

Design of Appropriate Types of Control Activities 53

Design of Information Technology Infrastructure 53

Design of Security Management 54

Design of Information Technology Acquisition, Development,

and Maintenance 55

Principle 12 - Implement Control Activities 56

Documentation of Responsibilities through Policies 56

Periodic Review of Control Activities 56

Information and Communication 58

Principle 13 - Use Quality Information 59

Identification of Information Requirements 59

Page iii GAO-14-704G Federal Internal Control Standards

Relevant Data from Reliable Sources 59

Data Processed into Quality Information 59

Principle 14 - Communicate Internally 60

Communication throughout the Entity 60

Appropriate Methods of Communication 61

Principle 15 - Communicate Externally 62

Communication with External Parties 62

Appropriate Methods of Communication 63

Monitoring 64

Principle 16 - Perform Monitoring Activities 65

Establishment of a Baseline 65

Internal Control System Monitoring 65

Evaluation of Results 66

Principle 17 - Evaluate Issues and Remediate Deficiencies 67

Reporting of Issues 67

Evaluation of Issues 68

Corrective Actions 68

Appendix I Requirements 70

Appendix II Acknowledgments 73

Comptroller General’s Advisory Council on Standards for Internal

Control in the Federal Government (2013-2015) 73

GAO Project Team 74

Staff Acknowledgments 74

Glossary 75

Figures

Figure 1: Green Book Sample Page 4

Figure 2: Achieving Objectives through Internal Control 5

Figure 3: The Five Components and 17 Principles of Internal

Control 9

Figure 4: The Components, Objectives, and Organizational

Structure of Internal Control 10

Page iv GAO-14-704G Federal Internal Control Standards

Figure 5: The 17 Principles Supporting the Five Components of

Internal Control 11

Figure 6: Examples of Common Categories of Control Activities 46

This is a work of the U.S. government and is not subject to copyright protection in the

United States. The published product may be reproduced and distributed in its entirety

without further permission from GAO. However, because this work may contain

copyrighted images or other material, permission from the copyright holder may be

necessary if you wish to reproduce this material separately.

Page 1 GAO-14-704G Federal Internal Control Standards

Policymakers and program managers are continually seeking ways to

improve accountability in achieving an entity’s mission. A key factor in

improving accountability in achieving an entity’s mission is to implement

an effective internal control system. An effective internal control system

helps an entity adapt to shifting environments, evolving demands,

changing risks, and new priorities. As programs change and entities strive

to improve operational processes and implement new technology,

management continually evaluates its internal control system so that it is

effective and updated when necessary.

Section 3512 (c) and (d) of Title 31 of the United States Code (commonly

known as the Federal Managers’ Financial Integrity Act (FMFIA)) requires

the Comptroller General to issue standards for internal control in the

federal government. Standards for Internal Control in the Federal

Government (known as the Green Book), provide the overall framework

for establishing and maintaining an effective internal control system.

Office of Management and Budget (OMB) Circular No. A-123 provides

specific requirements for assessing and reporting on controls in the

federal government. The term internal control in this document covers all

aspects of an entity’s objectives (operations, reporting, and compliance).

The Green Book may also be adopted by state, local, and quasi-

governmental entities, as well as not-for-profit organizations, as a

framework for an internal control system. Management of an entity

determines, based on applicable laws and regulations, how to

appropriately adapt the standards presented in the Green Book as a

framework for the entity.

The Committee of Sponsoring Organizations of the Treadway

Commission (COSO) updated its internal control guidance in 2013 with

the issuance of a revised Internal Control - Integrated Framework.

1

1

See Committee of Sponsoring Organizations of the Treadway Commission, Internal

Control - Integrated Framework (New York: American Institute of Certified Public

Accountants, 2013).

COSO introduced the concept of principles related to the five components

of internal control. The Green Book adapts these principles for a

government environment.

Overview

Foreword

Overview

Page 2 GAO-14-704G Federal Internal Control Standards

The standards are effective beginning with fiscal year 2016 and the

FMFIA reports covering that year. Management, at its discretion, may

elect early adoption of the Green Book.

This revision of the standards has gone through an extensive deliberative

process, including public comments and input from the Comptroller

General’s Advisory Council on Standards for Internal Control in the

Federal Government. The advisory council consists of about 20 experts in

financial and performance management drawn from federal, state, and

local government; the private sector; and academia. The views of all

parties were thoroughly considered in finalizing the standards.

I appreciate the efforts of government officials, public accounting

professionals, and other members of the audit and academic

communities who provided valuable assistance in developing these

standards. I extend special thanks to the members of the Advisory

Council on Standards for Internal Control in the Federal Government for

their extensive input and feedback throughout the entire process of

developing and finalizing the standards.

Gene L. Dodaro

Comptroller General

of the United States

September 2014

Overview

Page 3 GAO-14-704G Federal Internal Control Standards

The Green Book provides managers criteria for designing, implementing,

and operating an effective internal control system. The Green Book

defines the standards through components and principles and explains

why they are integral to an entity’s internal control system. The Green

Book clarifies what processes management considers part of internal

control. In a mature and highly effective internal control system, internal

control may be indistinguishable from day-to-day activities personnel

perform.

The Green Book is structured as follows:

1. An Overview, which includes the following sections:

• Section 1: an overview of the fundamental concepts of internal

control

• Section 2: a discussion of internal control components, principles,

and attributes; how these relate to an entity’s objectives; and the

three categories of objectives

• Section 3: a discussion of the evaluation of the entity’s internal

control system’s design, implementation, and operation

• Section 4: additional considerations that apply to all components

in an internal control system

2. A discussion of the requirements for each of the five components and

17 principles as well as discussion of the related attributes, including

documentation requirements.

The Green Book clearly indicates the component and principle

requirements through the use of “must” and “should.” Further discussion

of these requirements is included in section 2 of the Overview.

Documentation requirements are summarized in section 4 of the

Overview.

Figure 1 depicts a sample page from the Green Book. This illustration

identifies the components, principles, and attributes of the Green Book,

which are further discussed in section 2 of the Overview.

How to Use the

Green Book

Overview

Page 4 GAO-14-704G Federal Internal Control Standards

Figure 1: Green Book Sample Page

Overview

Page 5 GAO-14-704G Federal Internal Control Standards

OV1.01 Internal control is a process effected by an entity’s oversight

body, management, and other personnel that provides reasonable

assurance that the objectives of an entity will be achieved (see fig. 2).

These objectives and related risks can be broadly classified into one or

more of the following three categories:

• Operations - Effectiveness and efficiency of operations

• Reporting - Reliability of reporting for internal and external use

• Compliance - Compliance with applicable laws and regulations

Figure 2: Achieving Objectives through Internal Control

OV1.02 These are distinct but overlapping categories. A particular

objective can fall under more than one category, can address different

needs, and may be the direct responsibility of different individuals.

OV1.03 Internal control comprises the plans, methods, policies, and

procedures used to fulfill the mission, strategic plan, goals, and objectives

of the entity. Internal control serves as the first line of defense in

safeguarding assets. In short, internal control helps managers achieve

desired results through effective stewardship of public resources.

OV1.04 An internal control system is a continuous built-in component of

operations, effected by people, that provides reasonable assurance, not

absolute assurance, that an entity’s objectives will be achieved.

Section 1 -

Fundamental

Concepts of Internal

Control

Definition of Internal

Control

Definition of an Internal

Control System

Overview

Page 6 GAO-14-704G Federal Internal Control Standards

OV1.05 Internal control is not one event, but a series of actions that occur

throughout an entity’s operations. Internal control is recognized as an

integral part of the operational processes management uses to guide its

operations rather than as a separate system within an entity. In this

sense, internal control is built into the entity as a part of the organizational

structure to help managers achieve the entity’s objectives on an ongoing

basis.

OV1.06 People are what make internal control work. Management is

responsible for an effective internal control system. As part of this

responsibility, management sets the entity’s objectives, implements

controls, and evaluates the internal control system. However, personnel

throughout an entity play important roles in implementing and operating

an effective internal control system.

OV1.07 An effective internal control system increases the likelihood that

an entity will achieve its objectives. However, no matter how well

designed, implemented, or operated, an internal control system cannot

provide absolute assurance that all of an organization’s objectives will be

met. Factors outside the control or influence of management can affect

the entity’s ability to achieve all of its objectives. For example, a natural

disaster can affect an organization’s ability to achieve its objectives.

Therefore, once in place, effective internal control provides reasonable,

not absolute, assurance that an organization will achieve its objectives.

OV2.01 The Green Book defines the standards for internal control in the

federal government. FMFIA requires federal executive branch entities to

establish internal control in accordance with these standards. The

standards provide criteria for assessing the design, implementation, and

operating effectiveness of internal control in federal government entities

to determine if an internal control system is effective. Nonfederal entities

Section 2 -

Establishing an

Effective Internal

Control System

Presentation of Standards

Overview

Page 7 GAO-14-704G Federal Internal Control Standards

may use the Green Book as a framework to design, implement, and

operate an internal control system.

2

OV2.02 The Green Book applies to all of an entity’s objectives:

operations, reporting, and compliance. However, these standards are not

intended to limit or interfere with duly granted authority related to

legislation, rulemaking, or other discretionary policy making in an

organization. In implementing the Green Book, management is

responsible for designing the policies and procedures to fit an entity’s

circumstances and building them in as an integral part of the entity’s

operations.

OV2.03 An entity determines its mission, sets a strategic plan,

establishes entity objectives, and formulates plans to achieve its

objectives. Management, with oversight from the entity’s oversight body,

may set objectives for an entity as a whole or target activities within the

entity. Management uses internal control to help the organization achieve

these objectives. While there are different ways to present internal

control, the Green Book approaches internal control through a

hierarchical structure of five components and 17 principles. The hierarchy

includes requirements for establishing an effective internal control

system, including specific documentation requirements.

OV2.04 The five components represent the highest level of the hierarchy

of standards for internal control in the federal government. The five

components of internal control must be effectively designed,

implemented, and operating, and operating together in an integrated

manner, for an internal control system to be effective. The five

components of internal control are as follows:

• Control Environment - The foundation for an internal control system.

It provides the discipline and structure to help an entity achieve its

objectives.

• Risk Assessment - Assesses the risks facing the entity as it seeks to

achieve its objectives. This assessment provides the basis for

developing appropriate risk responses.

2

See para. OV4.10 for further discussion on use by other entities.

Components, Principles,

and Attributes

Overview

Page 8 GAO-14-704G Federal Internal Control Standards

• Control Activities - The actions management establishes through

policies and procedures to achieve objectives and respond to risks in

the internal control system, which includes the entity’s information

system.

• Information and Communication - The quality information

management and personnel communicate and use to support the

internal control system.

• Monitoring - Activities management establishes and operates to

assess the quality of performance over time and promptly resolve the

findings of audits and other reviews.

OV2.05 The 17 principles support the effective design, implementation,

and operation of the associated components and represent requirements

necessary to establish an effective internal control system.

OV2.06 In general, all components and principles are relevant for

establishing an effective internal control system. In rare circumstances,

there may be an operating or regulatory situation in which management

has determined that a principle is not relevant for the entity to achieve its

objectives and address related risks. If management determines that a

principle is not relevant, management supports that determination with

documentation that includes the rationale of how, in the absence of that

principle, the associated component could be designed, implemented,

and operated effectively. In addition to principle requirements, the Green

Book contains documentation requirements.

OV2.07 The Green Book contains additional information in the form of

attributes. These attributes are intended to help organize the application

material management may consider when designing, implementing, and

operating the associated principles. Attributes provide further explanation

of the principle and documentation requirements and may explain more

precisely what a requirement means and what it is intended to cover, or

include examples of procedures that may be appropriate for an entity.

Attributes may also provide background information on matters

addressed in the Green Book.

OV2.08 Attributes are relevant to the proper implementation of the Green

Book. Management has a responsibility to understand the attributes and

exercise judgment in fulfilling the requirements of the standards. The

Green Book, however, does not prescribe how management designs,

implements, and operates an internal control system.

Overview

Page 9 GAO-14-704G Federal Internal Control Standards

OV2.09 Figure 3 lists the five components of internal control and 17

related principles.

Figure 3: The Five Components and 17 Principles of Internal Control

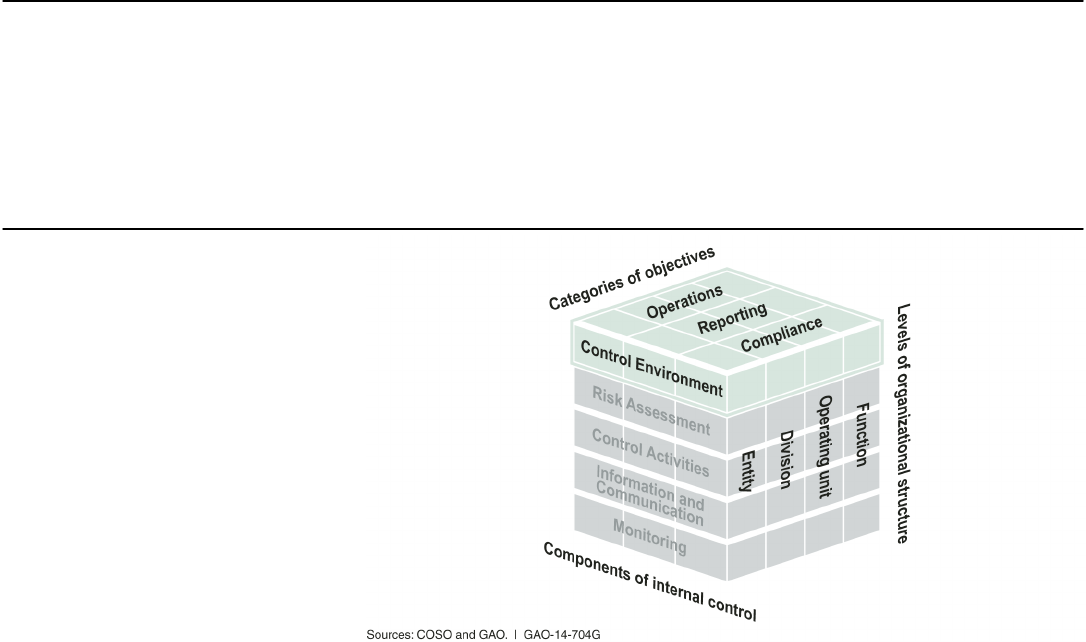

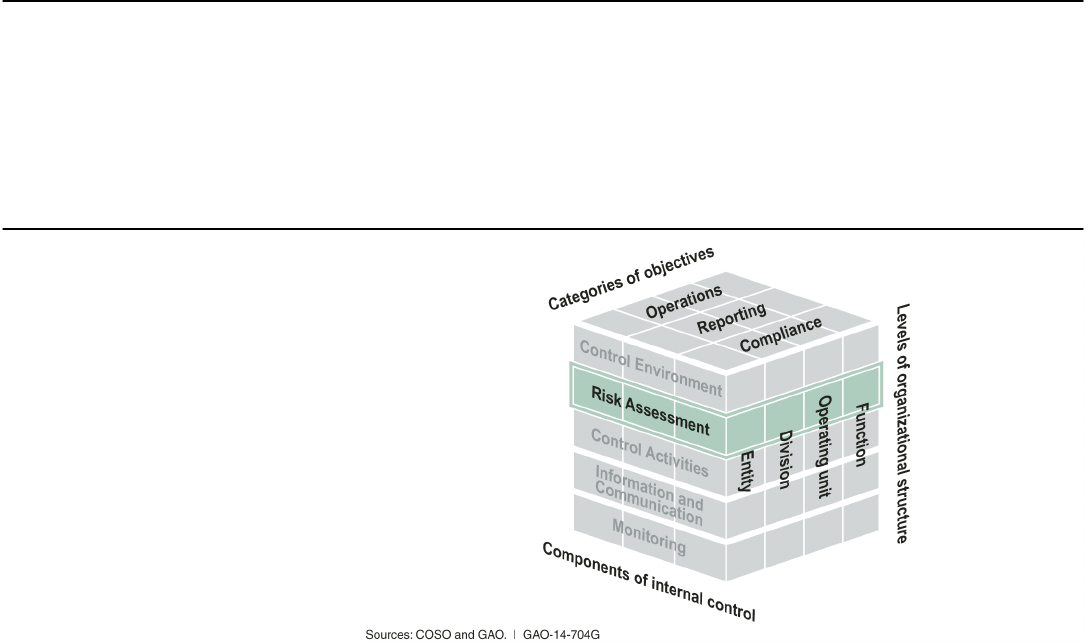

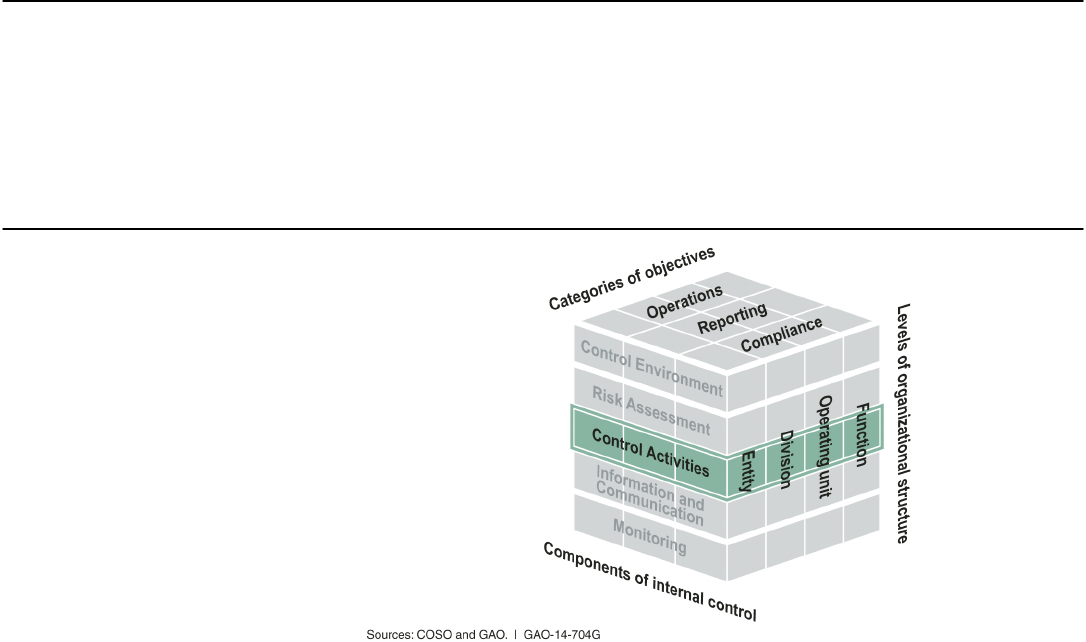

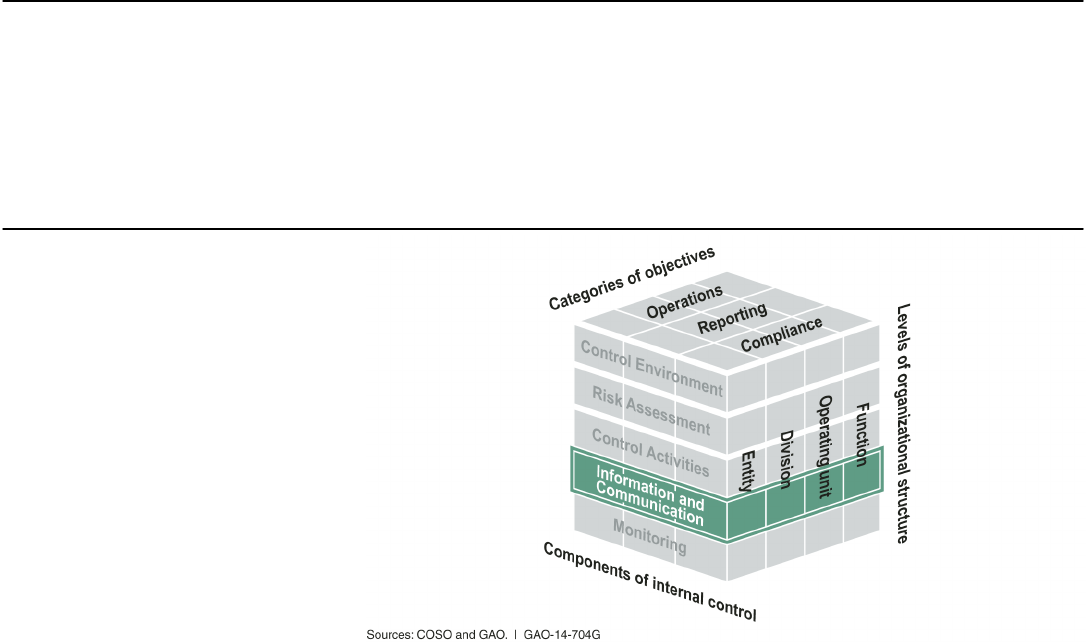

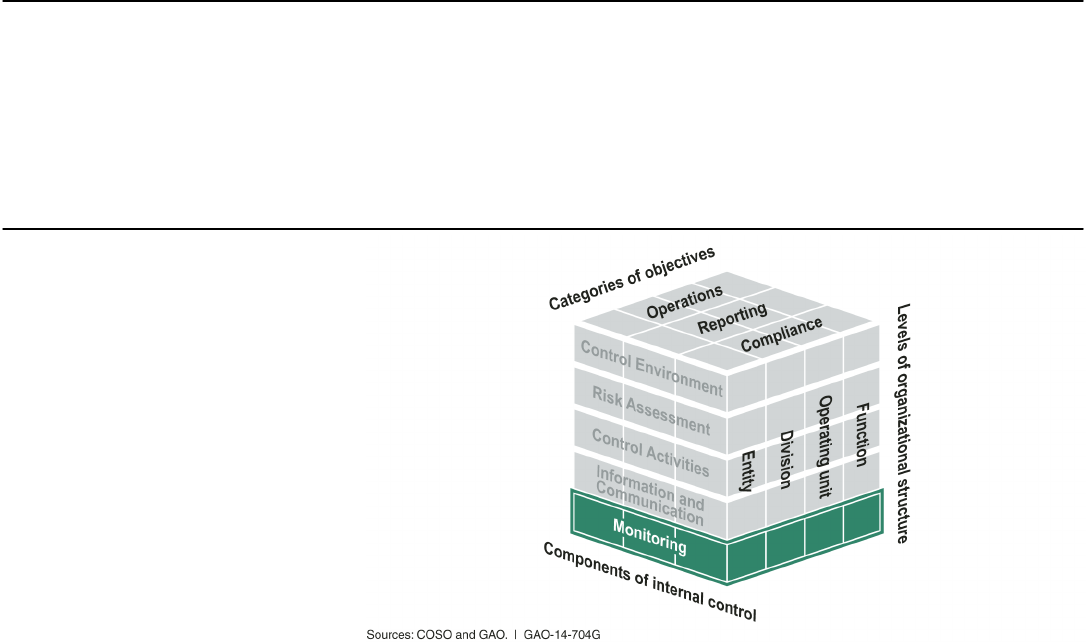

OV2.10 A direct relationship exists among an entity’s objectives, the five

components of internal control, and the organizational structure of an

entity. Objectives are what an entity wants to achieve. The five

components of internal control are what are required of the entity to

achieve the objectives. Organizational structure encompasses the

operating units, operational processes, and other structures management

Internal Control and the

Entity

Overview

Page 10 GAO-14-704G Federal Internal Control Standards

uses to achieve the objectives. This relationship is depicted in the form of

a cube developed by COSO (see fig. 4).

3

Figure 4: The Components, Objectives, and Organizational Structure of Internal

Control

OV2.11 The three categories into which an entity’s objectives can be

classified are represented by the columns labeled on top of the cube. The

five components of internal control are represented by the rows. The

organizational structure is represented by the third dimension of the cube.

OV2.12 Each component of internal control applies to all three categories

of objectives and the organizational structure. The principles support the

components of internal control (see fig. 5).

3

See paras. 3.02 through 3.05 for further discussion of organizational structure.

Overview

Page 11 GAO-14-704G Federal Internal Control Standards

Figure 5: The 17 Principles Supporting the Five Components of Internal Control

OV2.13 Internal control is a dynamic, iterative, and integrated process in

which components impact the design, implementation, and operating

effectiveness of each other. No two entities will have an identical internal

control system because of differences in factors such as mission,

regulatory environment, strategic plan, entity size, risk tolerance, and

information technology, and the judgment needed in responding to these

differing factors.

OV2.14 Because internal control is a part of management’s overall

responsibility, the five components are discussed in the context of the

management of the entity. However, everyone in the entity has a

responsibility for internal control. In general, roles in an entity’s internal

control system can be categorized as follows:

• Oversight body - The oversight body is responsible for overseeing

the strategic direction of the entity and obligations related to the

accountability of the entity. This includes overseeing management’s

design, implementation, and operation of an internal control system.

For some entities, an oversight body might be one or a few members

of senior management. For other entities, multiple parties may be

members of the entity’s oversight body. For the purpose of the Green

Book, oversight by an oversight body is implicit in each component

and principle.

Roles in an Internal

Control System

Overview

Page 12 GAO-14-704G Federal Internal Control Standards

• Management - Management is directly responsible for all activities of

an entity, including the design, implementation, and operating

effectiveness of an entity’s internal control system. Managers’

responsibilities vary depending on their functions in the organizational

structure.

• Personnel - Personnel help management design, implement, and

operate an internal control system and are responsible for reporting

issues noted in the entity’s operations, reporting, or compliance

objectives.

4

OV2.15 External auditors and the office of the inspector general (OIG), if

applicable, are not considered a part of an entity’s internal control system.

While management may evaluate and incorporate recommendations by

external auditors and the OIG, responsibility for an entity’s internal control

system resides with management.

OV2.16 Management, with oversight by an oversight body, sets

objectives to meet the entity’s mission, strategic plan, and goals and

requirements of applicable laws and regulations. Management sets

objectives before designing an entity’s internal control system.

Management may include setting objectives as part of the strategic

planning process.

OV2.17 Management, as part of designing an internal control system,

defines the objectives in specific and measurable terms to enable

management to identify, analyze, and respond to risks related to

achieving those objectives.

Categories of Objectives

OV2.18 Management groups objectives into one or more of the three

categories of objectives:

• Operations - Effectiveness and efficiency of operations

• Reporting - Reliability of reporting for internal and external use

• Compliance - Compliance with applicable laws and regulations

4

See paras. 17.02 through 17.04 for further discussion on identifying issues.

Objectives of an Entity

Overview

Page 13 GAO-14-704G Federal Internal Control Standards

Operations Objectives

OV2.19 Operations objectives relate to program operations that achieve

an entity’s mission. An entity’s mission may be defined in a strategic plan.

Such plans set the goals and objectives for an entity along with the

effective and efficient operations necessary to fulfill those objectives.

Effective operations produce the intended results from operational

processes, while efficient operations do so in a manner that minimizes the

waste of resources.

OV2.20 Management can set, from the objectives, related subobjectives

for units within the organizational structure. By linking objectives

throughout the entity to the mission, management improves the

effectiveness and efficiency of program operations in achieving the

mission.

Reporting Objectives

OV2.21 Reporting objectives relate to the preparation of reports for use

by the entity, its stakeholders, or other external parties. Reporting

objectives may be grouped further into the following subcategories:

• External financial reporting objectives - Objectives related to the

release of the entity’s financial performance in accordance with

professional standards, applicable laws and regulations, as well as

expectations of stakeholders.

• External nonfinancial reporting objectives - Objectives related to

the release of nonfinancial information in accordance with appropriate

standards, applicable laws and regulations, as well as expectations of

stakeholders.

• Internal financial reporting objectives and nonfinancial reporting

objectives - Objectives related to gathering and communicating

information needed by management to support decision making and

evaluation of the entity’s performance.

Compliance Objectives

OV2.22 In the government sector, objectives related to compliance with

applicable laws and regulations are very significant. Laws and regulations

often prescribe a government entity’s objectives, structure, methods to

achieve objectives, and reporting of performance relative to achieving

objectives. Management considers objectives in the category of

compliance comprehensively for the entity and determines what controls

Overview

Page 14 GAO-14-704G Federal Internal Control Standards

are necessary to design, implement, and operate for the entity to achieve

these objectives effectively.

OV2.23 Management conducts activities in accordance with applicable

laws and regulations. As part of specifying compliance objectives, the

entity determines which laws and regulations apply to the entity.

Management is expected to set objectives that incorporate these

requirements. Some entities may set objectives to a higher level of

performance than established by laws and regulations. In setting those

objectives, management is able to exercise discretion relative to the

performance of the entity.

Safeguarding of Assets

OV2.24 A subset of the three categories of objectives is the safeguarding

of assets. Management designs an internal control system to provide

reasonable assurance regarding prevention or prompt detection and

correction of unauthorized acquisition, use, or disposition of an entity’s

assets.

Setting Subobjectives

OV2.25 Management can develop from objectives more specific

subobjectives throughout the organizational structure. Management

defines subobjectives in specific and measurable terms that can be

communicated to the personnel who are assigned responsibility to

achieve these subobjectives. Both management and personnel require an

understanding of an objective, its subobjectives, and defined levels of

performance for accountability in an internal control system.

OV3.01 The purpose of this section is to provide management with

factors to consider in evaluating the effectiveness of an internal control

system. For federal entities, OMB Circular No. A-123 provides specific

requirements on how to perform evaluations and report on internal control

in the federal government. Nonfederal entities may refer to applicable

laws and regulations as well as input from key external stakeholders

when determining how to appropriately evaluate and report on internal

control.

Section 3 - Evaluation

of an Effective

Internal Control

System

Overview

Page 15 GAO-14-704G Federal Internal Control Standards

OV3.02 An effective internal control system provides reasonable

assurance that the organization will achieve its objectives. As stated in

section 2 of the Overview, an effective internal control system has

• each of the five components of internal control effectively designed,

implemented, and operating and

• the five components operating together in an integrated manner.

OV3.03 To determine if an internal control system is effective,

management assesses the design, implementation, and operating

effectiveness of the five components and 17 principles. If a principle or

component is not effective, or the components are not operating together

in an integrated manner, then an internal control system cannot be

effective.

OV3.04 In the federal government, FMFIA mandates that the head of

each executive branch agency annually prepare a statement as to

whether the agency’s systems of internal accounting and administrative

controls comply with the requirements of the act. If the systems do not

comply, the head of the agency will prepare a report in which any material

weaknesses in the agency’s system of internal accounting and

administrative control are identified and the plans and schedule for

correcting any such weakness are described. OMB issues guidance for

evaluating these requirements in OMB Circular No. A-123. Nonfederal

entities may refer to applicable laws and regulations for guidance in

preparing statements regarding internal control.

Design and Implementation

OV3.05 When evaluating design of internal control, management

determines if controls individually and in combination with other controls

are capable of achieving an objective and addressing related risks. When

evaluating implementation, management determines if the control exists

and if the entity has placed the control into operation. A control cannot be

effectively implemented if it was not effectively designed. A deficiency in

design exists when (1) a control necessary to meet a control objective is

missing or (2) an existing control is not properly designed so that even if

the control operates as designed, the control objective would not be met.

A deficiency in implementation exists when a properly designed control is

not implemented correctly in the internal control system.

Factors of Effective

Internal Control

Evaluation of Internal

Control

Overview

Page 16 GAO-14-704G Federal Internal Control Standards

Operating Effectiveness

OV3.06 In evaluating operating effectiveness, management determines if

controls were applied at relevant times during the period under

evaluation, the consistency with which they were applied, and by whom or

by what means they were applied. If substantially different controls were

used at different times during the period under evaluation, management

evaluates operating effectiveness separately for each unique control

system. A control cannot be effectively operating if it was not effectively

designed and implemented. A deficiency in operation exists when a

properly designed control does not operate as designed, or when the

person performing the control does not possess the necessary authority

or competence to perform the control effectively.

Effect of Deficiencies on the Internal Control System

OV3.07 Management evaluates control deficiencies identified by

management’s ongoing monitoring of the internal control system as well

as any separate evaluations performed by both internal and external

sources. A deficiency in internal control exists when the design,

implementation, or operation of a control does not allow management or

personnel, in the normal course of performing their assigned functions, to

achieve control objectives and address related risks.

OV3.08 Management evaluates the significance of identified deficiencies.

Significance refers to the relative importance of a deficiency to the entity’s

achieving a defined objective. To evaluate the significance of the

deficiency, management assesses its effect on achieving the defined

objectives at both the entity and transaction level. Management evaluates

the significance of a deficiency by considering the magnitude of impact,

likelihood of occurrence, and nature of the deficiency. Magnitude of

impact refers to the likely effect that the deficiency could have on the

entity achieving its objectives and is affected by factors such as the size,

pace, and duration of the deficiency’s impact. A deficiency may be more

significant to one objective than another. Likelihood of occurrence refers

to the possibility of a deficiency impacting an entity’s ability to achieve its

objectives. The nature of the deficiency involves factors such as the

degree of subjectivity involved with the deficiency and whether the

deficiency arises from fraud or misconduct. The oversight body oversees

management’s evaluation of the significance of deficiencies so that

deficiencies have been properly considered.

Overview

Page 17 GAO-14-704G Federal Internal Control Standards

OV3.09 Deficiencies are evaluated both on an individual basis and in the

aggregate. Management considers the correlation among different

deficiencies or groups of deficiencies when evaluating their significance.

Deficiency evaluation varies by entity because of differences in entities’

objectives.

OV3.10 For each principle, management makes a summary

determination as to whether the principle is designed, implemented, and

operating effectively. Management considers the impact of deficiencies

identified in achieving documentation requirements as part of this

summary determination.

5

OV3.11 Based on the results of the summary determination for each

principle, management concludes on the design, implementation, and

operating effectiveness of each of the five components of internal control.

Management also considers if the five components operate together

effectively. If one or more of the five components are not effectively

designed, implemented, or operating effectively or if they are not

operating together in an integrated manner, then an internal control

system is ineffective. Judgment is used in making such determinations,

which includes exercising reasonable care.

Management may consider the related

attributes as part of this summary determination. If a principle is not

designed, implemented, or operating effectively, then the respective

component cannot be effective.

OV4.01 Management may engage external parties to perform certain

operational processes for the entity, such as accounting and payroll

processing, security services, or health care claims processing. For the

purpose of the Green Book, these external parties are referred to as

service organizations. Management, however, retains responsibility for

the performance of processes assigned to service organizations.

5

See paras. OV4.08 through OV4.09 for further discussion of documentation

requirements.

Section 4 - Additional

Considerations

Service Organizations

Overview

Page 18 GAO-14-704G Federal Internal Control Standards

Therefore, management needs to understand the controls each service

organization has designed, has implemented, and operates for the

assigned operational process and how the service organization’s internal

control system impacts the entity’s internal control system.

OV4.02 If controls performed by the service organization are necessary

for the entity to achieve its objectives and address risks related to the

assigned operational process, the entity’s internal controls may include

complementary user entity controls identified by the service organization

or its auditors that are necessary to achieve the service organization’s

control objectives.

OV4.03 Management may consider the following when determining the

extent of oversight for the operational processes assigned to the service

organization:

• The nature of services outsourced

• The service organization’s standards of conduct

• The quality and frequency of the service organization’s enforcement

of adherence to standards of conduct by its personnel

• The magnitude and level of complexity of the entity’s operations and

organizational structure

• The extent to which the entity’s internal controls are sufficient so that

the entity achieves its objectives and addresses risks related to the

assigned operational process

OV4.04 The 17 principles apply to both large and small entities. However,

smaller entities may have different implementation approaches than

larger entities. Smaller entities typically have unique advantages, which

can contribute to an effective internal control system. These may include

a higher level of involvement by management in operational processes

and direct interaction with personnel. Smaller entities may find informal

staff meetings effective for communicating quality information, whereas

larger entities may need more formal mechanisms—such as written

reports, intranet portals, or periodic formal meetings—to communicate

with the organization.

OV4.05 A smaller entity, however, faces greater challenges in

segregating duties because of its concentration of responsibilities and

Large versus Small

Entities

Overview

Page 19 GAO-14-704G Federal Internal Control Standards

authorities in the organizational structure.

6

Management, however, can

respond to this increased risk through the design of the internal control

system, such as by adding additional levels of review for key operational

processes, reviewing randomly selected transactions and their supporting

documentation, taking periodic asset counts, or checking supervisor

reconciliations.

OV4.06 Internal control provides many benefits to an entity. It provides

management with added confidence regarding the achievement of

objectives, provides feedback on how effectively an entity is operating,

and helps reduce risks affecting the achievement of the entity’s

objectives. Management considers a variety of cost factors in relation to

expected benefits when designing and implementing internal controls.

The complexity of cost-benefit determination is compounded by the

interrelationship of controls with operational processes. Where controls

are integrated with operational processes, it is difficult to isolate either

their costs or benefits.

OV4.07 Management may decide how an entity evaluates the costs

versus benefits of various approaches to implementing an effective

internal control system. However, cost alone is not an acceptable reason

to avoid implementing internal controls. Management is responsible for

meeting internal control objectives. The costs versus benefits

considerations support management’s ability to effectively design,

implement, and operate an internal control system that balances the

allocation of resources in relation to the areas of greatest risk, complexity,

or other factors relevant to achieving the entity’s objectives.

OV4.08 Documentation is a necessary part of an effective internal control

system. The level and nature of documentation vary based on the size of

the entity and the complexity of the operational processes the entity

performs. Management uses judgment in determining the extent of

documentation that is needed. Documentation is required for the effective

design, implementation, and operating effectiveness of an entity’s internal

control system. The Green Book includes minimum documentation

requirements as follows:

6

See paras. 10.12 through 10.14 for further discussion of segregation of duties.

Benefits and Costs of

Internal Control

Documentation

Requirements

Overview

Page 20 GAO-14-704G Federal Internal Control Standards

• If management determines that a principle is not relevant,

management supports that determination with documentation that

includes the rationale of how, in the absence of that principle, the

associated component could be designed, implemented, and

operated effectively. (paragraph OV2.06)

• Management develops and maintains documentation of its internal

control system. (paragraph 3.09)

• Management documents in policies the internal control responsibilities

of the organization. (paragraph 12.02)

• Management evaluates and documents the results of ongoing

monitoring and separate evaluations to identify internal control issues.

(paragraph 16.09)

• Management evaluates and documents internal control issues and

determines appropriate corrective actions for internal control

deficiencies on a timely basis. (paragraph 17.05)

• Management completes and documents corrective actions to

remediate internal control deficiencies on a timely basis. (paragraph

17.06)

OV4.09 These requirements represent the minimum level of

documentation in an entity’s internal control system. Management

exercises judgment in determining what additional documentation may be

necessary for an effective internal control system. If management

identifies deficiencies in achieving these documentation requirements, the

effect of the identified deficiencies is considered as part of management’s

summary determination as to whether the related principle is designed,

implemented, and operating effectively.

OV4.10 The Green Book may be applied as a framework for an internal

control system for state, local, and quasi-governmental entities, as well as

not-for-profit organizations. If management elects to adopt the Green

Book as criteria, management follows all relevant requirements presented

in these standards.

Use by Other Entities

Control Environment

Page 21 GAO-14-704G Federal Internal Control Standards

Overview

The control environment is the foundation for an internal control system. It

provides the discipline and structure, which affect the overall quality of

internal control. It influences how objectives are defined and how control

activities are structured. The oversight body and management establish

and maintain an environment throughout the entity that sets a positive

attitude toward internal control.

Principles

1. The oversight body and management should demonstrate a

commitment to integrity and ethical values.

2. The oversight body should oversee the entity’s internal control system.

3. Management should establish an organizational structure, assign

responsibility, and delegate authority to achieve the entity’s objectives.

4. Management should demonstrate a commitment to recruit, develop,

and retain competent individuals.

5. Management should evaluate performance and hold individuals

accountable for their internal control responsibilities.

Control Environment

Control Environment

Page 22 GAO-14-704G Federal Internal Control Standards

1.01 The oversight body and management should demonstrate a

commitment to integrity and ethical values.

Attributes

The following attributes contribute to the design, implementation, and

operating effectiveness of this principle:

• Tone at the Top

• Standards of Conduct

• Adherence to Standards of Conduct

1.02 The oversight body and management demonstrate the importance of

integrity and ethical values through their directives, attitudes, and

behavior.

1.03 The oversight body and management lead by an example that

demonstrates the organization’s values, philosophy, and operating style.

The oversight body and management set the tone at the top and

throughout the organization by their example, which is fundamental to an

effective internal control system. In larger entities, the various layers of

management in the organizational structure may also set “tone in the

middle.”

1.04 The oversight body’s and management’s directives, attitudes, and

behaviors reflect the integrity and ethical values expected throughout the

entity. The oversight body and management reinforce the commitment to

doing what is right, not just maintaining a minimum level of performance

necessary to comply with applicable laws and regulations, so that these

priorities are understood by all stakeholders, such as regulators,

employees, and the general public.

1.05 Tone at the top can be either a driver, as shown in the preceding

paragraphs, or a barrier to internal control. Without a strong tone at the

top to support an internal control system, the entity’s risk identification

may be incomplete, risk responses may be inappropriate, control

activities may not be appropriately designed or implemented, information

and communication may falter, and results of monitoring may not be

understood or acted upon to remediate deficiencies.

Principle 1 -

Demonstrate

Commitment to

Integrity and Ethical

Values

Tone at the Top

Control Environment

Page 23 GAO-14-704G Federal Internal Control Standards

1.06 Management establishes standards of conduct to communicate

expectations concerning integrity and ethical values. The entity uses

ethical values to balance the needs and concerns of different

stakeholders, such as regulators, employees, and the general public. The

standards of conduct guide the directives, attitudes, and behaviors of the

organization in achieving the entity’s objectives.

1.07 Management, with oversight from the oversight body, defines the

organization’s expectations of ethical values in the standards of conduct.

Management may consider using policies, operating principles, or

guidelines to communicate the standards of conduct to the organization.

1.08 Management establishes processes to evaluate performance

against the entity’s expected standards of conduct and address any

deviations in a timely manner.

1.09 Management uses established standards of conduct as the basis for

evaluating adherence to integrity and ethical values across the

organization. Management evaluates the adherence to standards of

conduct across all levels of the entity. To gain assurance that the entity’s

standards of conduct are implemented effectively, management evaluates

the directives, attitudes, and behaviors of individuals and teams.

Evaluations may consist of ongoing monitoring or separate evaluations.

7

Individual personnel can also report issues through reporting lines, such

as regular staff meetings, upward feedback processes, a whistle-blowing

program, or an ethics hotline.

8

1.10 Management determines the tolerance level for deviations.

Management may determine that the entity will have zero tolerance for

deviations from certain expected standards of conduct, while deviations

from others may be addressed with warnings to personnel. Management

establishes a process for evaluations of individual and team adherence to

standards of conduct that escalates and remediates deviations.

The oversight body evaluates

management’s adherence to the standards of conduct as well as the

overall adherence by the entity.

7

See paras. 16.04 through 16.08 for further discussion of ongoing monitoring and

separate evaluations.

8

See para. 14.06 for further discussion of upward and separate reporting lines.

Standards of Conduct

Adherence to Standards of

Conduct

Control Environment

Page 24 GAO-14-704G Federal Internal Control Standards

Management addresses deviations from expected standards of conduct

timely and consistently. Depending on the severity of the deviation

determined through the evaluation process, management, with oversight

from the oversight body, takes appropriate actions and may also need to

consider applicable laws and regulations. The standards of conduct to

which management holds personnel, however, remain consistent.

2.01 The oversight body should oversee the entity’s internal control

system.

Attributes

The following attributes contribute to the design, implementation, and

operating effectiveness of this principle:

• Oversight Structure

• Oversight for the Internal Control System

• Input for Remediation of Deficiencies

2.02 The entity determines an oversight structure to fulfill responsibilities

set forth by applicable laws and regulations, relevant government

guidance, and feedback from key stakeholders. The entity will select, or if

mandated by law will have selected for it, an oversight body. When the

oversight body is composed of entity management, activities referenced

in the Green Book as performed by “management” exclude these

members of management when in their roles as the oversight body.

Responsibilities of an Oversight Body

2.03 When the oversight structure of an entity is led by senior

management, senior management may distinguish itself from divisional or

functional management through the establishment of an oversight body.

An oversight body oversees the entity’s operations; provides constructive

criticism to management; and where appropriate, makes oversight

decisions so that the entity achieves its objectives in alignment with the

entity’s integrity and ethical values.

Qualifications for an Oversight Body

2.04 In selecting members for an oversight body, the entity or applicable

body defines the entity knowledge, relevant expertise, number of

Principle 2 - Exercise

Oversight

Responsibility

Oversight Structure

Control Environment

Page 25 GAO-14-704G Federal Internal Control Standards

members, and possible independence needed to fulfill the oversight

responsibilities for the entity.

2.05 Members of an oversight body understand the entity’s objectives, its

related risks, and expectations of its stakeholders. In addition to an

oversight body, an organization within the federal government may have

several bodies that are key stakeholders for the entity, such as the White

House, Congress, the Office of Management and Budget, and the

Department of the Treasury. An oversight body works with key

stakeholders to understand their expectations and help the entity fulfill

these expectations if appropriate.

2.06 The entity or applicable body also considers the expertise needed by

members to oversee, question, and evaluate management. Capabilities

expected of all members of an oversight body include integrity and ethical

values, leadership, critical thinking, and problem-solving abilities.

2.07 Further, in determining the number of members of an oversight

body, the entity or applicable body considers the need for members of the

oversight body to have specialized skills to enable discussion, offer

constructive criticism to management, and make appropriate oversight

decisions. Some specialized skills may include the following:

• Internal control mindset (e.g., professional skepticism and

perspectives on approaches for identifying and responding to risks

and assessing the effectiveness of the system of internal control)

• Programmatic expertise, including knowledge of the entity’s mission,

programs, and operational processes (e.g., procurement, human

capital, and functional management expertise)

• Financial expertise, including financial reporting (e.g., accounting

standards and financial reporting requirements and budgetary

expertise)

• Relevant systems and technology (e.g., understanding critical

systems and technology risks and opportunities)

• Legal and regulatory expertise (e.g., understanding of applicable laws

and regulations)

2.08 If authorized by applicable laws and regulations, the entity may also

consider including independent members as part of an oversight body.

9

9

See GAO, Government Auditing Standards: 2011 Revision,

GAO-12-331G (Washington,

D.C.: December 2011), para. 3.03, for further discussion of independence.

Control Environment

Page 26 GAO-14-704G Federal Internal Control Standards

Members of an oversight body scrutinize and question management’s

activities, present alternative views, and act when faced with obvious or

suspected wrongdoing. Independent members with relevant expertise

provide value through their impartial evaluation of the entity and its

operations in achieving objectives.

2.09 The oversight body oversees management’s design,

implementation, and operation of the entity’s internal control system. The

oversight body’s responsibilities for the entity’s internal control system

include the following:

• Control Environment - Establish integrity and ethical values,

establish oversight structure, develop expectations of competence,

and maintain accountability to all members of the oversight body and

key stakeholders.

• Risk Assessment - Oversee management’s assessment of risks to

the achievement of objectives, including the potential impact of

significant changes, fraud, and management override of internal

control.

• Control Activities - Provide oversight to management in the

development and performance of control activities.

• Information and Communication - Analyze and discuss information

relating to the entity’s achievement of objectives.

• Monitoring - Scrutinize the nature and scope of management’s

monitoring activities as well as management’s evaluation and

remediation of identified deficiencies.

2.10 These responsibilities are supported by the organizational structure

that management establishes.

10

The oversight body oversees

management’s design, implementation, and operation of the entity’s

organizational structure so that the processes necessary to enable the

oversight body to fulfill its responsibilities exist and are operating

effectively.

10

See paras. 3.02 through 3.05 for further discussion of organizational structure.

Oversight for the Internal

Control System

Control Environment

Page 27 GAO-14-704G Federal Internal Control Standards

2.11 The oversight body provides input to management’s plans for

remediation of deficiencies in the internal control system as appropriate.

2.12 Management reports deficiencies identified in the internal control

system to the oversight body. The oversight body oversees and provides

direction to management on the remediation of these deficiencies. The

oversight body also provides direction when a deficiency crosses

organizational boundaries or units, or when the interests of management

may conflict with remediation efforts. When appropriate and authorized,

the oversight body may direct the creation of teams to address or oversee

specific matters critical to achieving the entity’s objectives.

2.13 The oversight body is responsible for overseeing the remediation of

deficiencies as appropriate and for providing direction to management on

appropriate time frames for correcting these deficiencies.

11

3.01 Management should establish an organizational structure, assign

responsibility, and delegate authority to achieve the entity’s objectives.

Attributes

The following attributes contribute to the design, implementation, and

operating effectiveness of this principle:

• Organizational Structure

• Assignment of Responsibility and Delegation of Authority

• Documentation of the Internal Control System

3.02 Management establishes the organizational structure necessary to

enable the entity to plan, execute, control, and assess the organization in

achieving its objectives. Management develops the overall responsibilities

from the entity’s objectives that enable the entity to achieve its objectives

and address related risks.

3.03 Management develops an organizational structure with an

understanding of the overall responsibilities, and assigns these

responsibilities to discrete units to enable the organization to operate in

11

See para. 17.06 for further discussion of timely remediation of findings.

Input for Remediation of

Deficiencies

Principle 3 - Establish

Structure,

Responsibility, and

Authority

Organizational Structure

Control Environment

Page 28 GAO-14-704G Federal Internal Control Standards

an efficient and effective manner, comply with applicable laws and

regulations, and reliably report quality information.

12

3.04 As part of establishing an organizational structure, management

considers how units interact in order to fulfill their overall responsibilities.

Management establishes reporting lines within an organizational structure

so that units can communicate the quality information necessary for each

unit to fulfill its overall responsibilities.

Based on the nature

of the assigned responsibility, management chooses the type and number

of discrete units, such as divisions, offices, and related subunits.

13

Reporting lines are defined at all

levels of the organization and provide methods of communication that can

flow down, across, up, and around the structure.

14

Management also

considers the entity’s overall responsibilities to external stakeholders and

establishes reporting lines that allow the entity to both communicate and

receive information from external stakeholders.

15

3.05 Management periodically evaluates the organizational structure so

that it meets the entity’s objectives and has adapted to any new

objectives for the entity, such as a new law or regulation.

3.06 To achieve the entity’s objectives, management assigns

responsibility and delegates authority to key roles throughout the entity. A

key role is a position in the organizational structure that is assigned an

overall responsibility of the entity. Generally, key roles relate to senior

management positions within an entity.

3.07 Management considers the overall responsibilities assigned to each

unit, determines what key roles are needed to fulfill the assigned

responsibilities, and establishes the key roles. Those in key roles can

further assign responsibility for internal control to roles below them in the

organizational structure, but retain ownership for fulfilling the overall

responsibilities assigned to the unit.

12

See paras. 13.05 through 13.06 for further discussion of quality information.

13

See paras. 13.02 through 13.06 for further discussion of the use of quality information.

14

See paras. 14.02 through 14.06 for further discussion of internal reporting lines.

15

See paras. 15.02 through 15.06 for further discussion of external reporting lines.

Assignment of

Responsibility and

Delegation of Authority

Control Environment

Page 29 GAO-14-704G Federal Internal Control Standards

3.08 Management determines what level of authority each key role needs

to fulfill a responsibility. Management delegates authority only to the

extent required to achieve the entity’s objectives. As part of delegating

authority, management evaluates the delegation for proper segregation of

duties within the unit and in the organizational structure. Segregation of

duties helps prevent fraud, waste, and abuse in the entity by considering

the need to separate authority, custody, and accounting in the

organizational structure.

16

As with assigning responsibility, those in key

roles can delegate their authority for internal control to roles below them

in the organizational structure.

3.09 Management develops and maintains documentation of its internal

control system.

3.10 Effective documentation assists in management’s design of internal

control by establishing and communicating the who, what, when, where,

and why of internal control execution to personnel. Documentation also

provides a means to retain organizational knowledge and mitigate the risk

of having that knowledge limited to a few personnel, as well as a means

to communicate that knowledge as needed to external parties, such as

external auditors.

3.11 Management documents internal control to meet operational needs.

Documentation of controls, including changes to controls, is evidence that

controls are identified, capable of being communicated to those

responsible for their performance, and capable of being monitored and

evaluated by the entity.

3.12 The extent of documentation needed to support the design,

implementation, and operating effectiveness of the five components of

internal control is a matter of judgment for management. Management

considers the cost benefit of documentation requirements for the entity as

well as the size, nature, and complexity of the entity and its objectives.

Some level of documentation, however, is necessary so that the

components of internal control can be designed, implemented, and

operating effectively.

16

See paras. 10.12 through 10.14 for further discussion of segregation of duties.

Documentation of the

Internal Control System

Control Environment

Page 30 GAO-14-704G Federal Internal Control Standards

4.01 Management should demonstrate a commitment to recruit, develop,

and retain competent individuals.

Attributes

The following attributes contribute to the design, implementation, and

operating effectiveness of this principle:

• Expectations of Competence

• Recruitment, Development, and Retention of Individuals

• Succession and Contingency Plans and Preparation

4.02 Management establishes expectations of competence for key roles,

and other roles at management’s discretion, to help the entity achieve its

objectives. Competence is the qualification to carry out assigned

responsibilities. It requires relevant knowledge, skills, and abilities, which

are gained largely from professional experience, training, and

certifications. It is demonstrated by the behavior of individuals as they

carry out their responsibilities.

4.03 Management considers standards of conduct, assigned

responsibility, and delegated authority when establishing expectations.

Management establishes expectations of competence for key roles.

Management may also establish expectations of competence for all

personnel through policies within the entity’s internal control system.

17

4.04 Personnel need to possess and maintain a level of competence that

allows them to accomplish their assigned responsibilities, as well as

understand the importance of effective internal control. Holding

individuals accountable to established policies by evaluating personnel’s

competence is integral to attracting, developing, and retaining individuals.

Management evaluates competence of personnel across the entity in

relation to established policies. Management acts as necessary to

address any deviations from the established policies. The oversight body

evaluates the competence of management as well as the competence

overall of entity personnel.

17

See paras. 12.02 through 12.04 for further discussion of policies.

Principle 4 -

Demonstrate

Commitment to

Competence

Expectations of

Competence

Control Environment

Page 31 GAO-14-704G Federal Internal Control Standards

4.05 Management recruits, develops, and retains competent personnel to

achieve the entity’s objectives. Management considers the following:

• Recruit - Conduct procedures to determine whether a particular

candidate fits the organizational needs and has the competence for

the proposed role.

• Train - Enable individuals to develop competencies appropriate for

key roles, reinforce standards of conduct, and tailor training based on

the needs of the role.

• Mentor - Provide guidance on the individual’s performance based on

standards of conduct and expectations of competence, align the

individual’s skills and expertise with the entity’s objectives, and help

personnel adapt to an evolving environment.

• Retain - Provide incentives to motivate and reinforce expected levels

of performance and desired conduct, including training and

credentialing as appropriate.

4.06 Management defines succession and contingency plans for key

roles to help the entity continue achieving its objectives. Succession plans

address the entity’s need to replace competent personnel over the long

term, whereas contingency plans address the entity’s need to respond to

sudden personnel changes that could compromise the internal control

system.

4.07 Management defines succession plans for key roles, chooses

succession candidates, and trains succession candidates to assume the

key roles. If management relies on a service organization to fulfill the

assigned responsibilities of key roles in the entity, management assesses

whether the service organization can continue in these key roles,

identifies other candidate organizations for the roles, and implements

processes to enable knowledge sharing with the succession candidate

organization.

4.08 Management defines contingency plans for assigning responsibilities

if a key role in the entity is vacated without advance notice. The

importance of the key role in the internal control system and the impact to

the entity of its vacancy dictates the formality and depth of the

contingency plan.

Recruitment,

Development, and

Retention of Individuals

Succession and

Contingency Plans and

Preparation

Control Environment

Page 32 GAO-14-704G Federal Internal Control Standards

5.01 Management should evaluate performance and hold individuals

accountable for their internal control responsibilities.

Attributes

The following attributes contribute to the design, implementation, and

operating effectiveness of this principle:

• Enforcement of Accountability

• Consideration of Excessive Pressures

5.02 Management enforces accountability of individuals performing their

internal control responsibilities. Accountability is driven by the tone at the

top and supported by the commitment to integrity and ethical values,

organizational structure, and expectations of competence, which

influence the control culture of the entity. Accountability for performance

of internal control responsibility supports day-to-day decision making,

attitudes, and behaviors. Management holds personnel accountable

through mechanisms such as performance appraisals and disciplinary

actions.

5.03 Management holds entity personnel accountable for performing their

assigned internal control responsibilities. The oversight body, in turn,

holds management accountable as well as the organization as a whole

for its internal control responsibilities.

5.04 If management establishes incentives, management recognizes that

such actions can yield unintended consequences and evaluates

incentives so that they align with the entity’s standards of conduct.

5.05 Management holds service organizations accountable for their

assigned internal control responsibilities. Management may contract with

service organizations to perform roles in the organizational structure.

Management communicates to the service organization the objectives of

the entity and their related risks, the entity’s standards of conduct, the role

of the service organization in the organizational structure, the assigned

responsibilities and authorities of the role, and the expectations of

competence for its role that will enable the service organization to perform

its internal control responsibilities.

5.06 Management, with oversight from the oversight body, takes

corrective action as necessary to enforce accountability for internal

Principle 5 - Enforce

Accountability

Enforcement of

Accountability

Control Environment

Page 33 GAO-14-704G Federal Internal Control Standards

control in the entity. These actions can range from informal feedback

provided by the direct supervisor to disciplinary action taken by the

oversight body, depending on the significance of the deficiency to the

internal control system.

18

5.07 Management adjusts excessive pressures on personnel in the entity.

Pressure can appear in an entity because of goals established by

management to meet objectives or cyclical demands of various processes

performed by the entity, such as year-end financial statement preparation.

Excessive pressure can result in personnel “cutting corners” to meet the

established goals.

5.08 Management is responsible for evaluating pressure on personnel to

help personnel fulfill their assigned responsibilities in accordance with the

entity’s standards of conduct. Management can adjust excessive

pressures using many different tools, such as rebalancing workloads or