CENTRE FOR CHARITY EFFECTIVENESS

Inspiring transformation within the nonprot sector.

The vision of the Centre for Charity Eectiveness (CCE) at Bayes Business School is that

of a nonprot sector leading positive social change. We support the sector to achieve

this through the services that we deliver: education, knowledge sharing, research and

independent consultancy advice.

As one of Bayes Business School’s centres of excellence, impactful knowledge

exchange has been at the heart of what we do since our inception over 20 years ago.

CCE aspires to see a voluntary, community and social enterprise sector constantly

extending its own knowledge boundaries and driving performance excellence – whilst

developing and inspiring the next generation of leaders.

A number of the wider CCE team have made valuable contributions to this guide,

including Caroline Copeman, Alex Skailes and Ros Oakley. This edition has been

updated and edited by Christine Fogg.

1

Centre for Charity Eectiveness

E: CCE@city.ac.uk

www.bayes.city.ac.uk/cce

Foreword

The unwavering vision of the Centre

for Charity Eectiveness (CCE) is that

of a strong nonprot sector leading

positive social change. We support

the sector to achieve this through

the services we deliver: education,

knowledge sharing, research and

independent consultancy advice.

We know that the need for good governance

in our sector is greater than ever with

recent public concern and media scrutiny

which is oen about the eectiveness of an

organisation’s governance. As the Charity

Governance Code says, ‘good governance

in charities is fundamental to their success’.

Our governance practice team is regularly

commissioned to undertake reviews or

other activities in support of more eective

governance.

This is one of a series of updated Building

Better Governance (BBG) good practice

guides covering key governance activities

including:

■

Board & trustee performance review

■

Board involvement in strategy and

planning

■

Board reports that add value

■

Developing a balanced scorecard &

dashboard

■

Developing the whole top team

■

Eective board meetings.

We are condent that, taken together, these

guides will be an extremely useful resource

for trustees and the senior team, covering the

key areas of practice that make the dierence

between a board that does the minimum and

one that is truly eective. If you need further

information or advice, please get in touch.

Alex Skailes

Director, Centre for Charity Eectiveness

(CCE)

BOARD REPORTS THAT ADD VALUE

2

CENTRE FOR CHARITY EFFECTIVENESS

Contents

What is eective board reporting? 3

Key benets of eective board reporting 4

Board reports and good governance 5

Key principles/approach for three dierent types of report 6

Hallmarks of an eective report 8

The role of sub-committees in eective reporting 9

Common types of report 10

Top tips 11

Resources 12

Appendix 1: Sample contents for decision making report 13

Appendix 2: Presentation of performance data 14

Appendix 3: Board committee calendar 15

Appendix 4: Summarising committee discussions to the board 16

Appendix 5: Chief Executive report 17

Appendix 6: Financial reporting 19

Appendix 7: Key nancial reports 20

BOARD REPORTS THAT ADD VALUE

3

What is eective

board reporting

1

?

Eective board reporting is about

providing the board with information

that is concise, relevant, reliable,

timely, material and t for purpose.

The various reports that the Chief

Executive and senior management

team present to the board, together

with the agenda, provide the

essential mechanisms for the board

to exercise its strategic, duciary and

leadership roles.

Each report or paper provided to the board

should have a clear purpose. Together the

various reports that come to the board enable

it to:

■

Understand the external environment

of the organisation and the needs of its

diverse stakeholders

■

Be condent in setting strategic goals

for the organisation and understand the

progress being made towards them

■

Be condent that the organisation is well-

run, compliant with necessary legislation

and regulations, and that risks are

appropriately managed

■

Be assured the board’s decisions are

carried out

■

Know that the organisation is achieving

the objects for which it was established

eectively.

1. This guide deals with internal reporting to the board, not external reporting

4

CENTRE FOR CHARITY EFFECTIVENESS

Key benets of eective

board reporting

Eective reports facilitate

transparency and accountability and

enable board members to:

■

Get a strategic overview of how the charity

is performing:

- get advance warning of problem areas

- delve into key issues facing the charity

■

Keep learning about the charity including

what works well and how things could be

improved

■

Constructively challenge and exchange

knowledge with sta

■

Focus attention and time on the issues that

matter most.

BOARD REPORTS THAT ADD VALUE

5

Board reports and good

governance

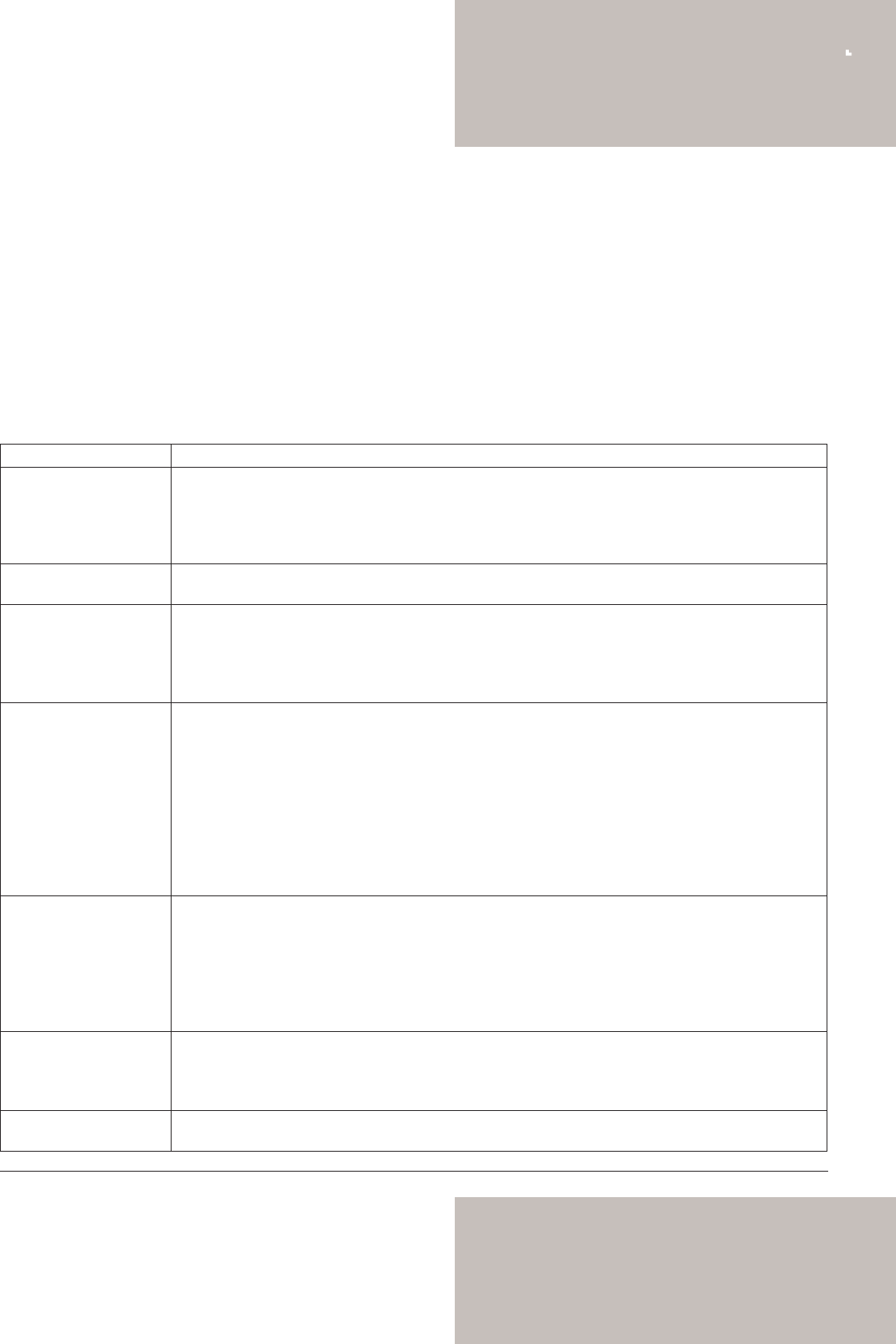

The principles from the Charity Governance Code

2

will be reflected in board reporting.

2. The Charity Governance Code for larger charities (2017)

Code principle How this might be observed in board reporting

Organisational purpose Reports, research and other data will support the board in periodically reviewing the external environment

in which the organisation works to make sure that the charity, and its purposes, stays relevant and valid.

The board looks at the entire organisational performance in the round, evaluating impact by measuring

and assessing results, outputs and outcomes – and receives this data through regular reports that could

include a scorecard or dashboard

Leadership Trustees give sucient time to carry out their responsibilities including preparing for meetings by reading

reports and asking questions

Integrity Trustees understand, disclose, report and deal with actual or potential conflicts of interest and maintain

their independence; reports give consideration to potential conflicts of interest and clearly set this out

The board safeguards the charity’s reputation and considers when and how reputational management and

risk are reported to the full board

The board ensures that the charity follows the law with board reporting assuring trustees of compliance

Decision making, risk

and control

Board reports enable the board to maintain a focus on strategy, performance and assurance rather than

operational management

The board regularly monitors performance using reports with a consistent framework that checks

performance against delivery of the strategy

The board regularly considers information from other organisations to benchmark or compare

performance and receives regular/annual reports that provide such information

The board retains overall responsibility for risk and is clear about how risks are identied, managed and

mitigated against including through (agreed) periodic reporting

The board describes the charity’s approach to risk in its annual report

The board is clear on the information and reporting mechanisms required of committees to the full board

Board eectiveness The chair (working with trustees and sta) plans the board’s work programme, ensuring trustees have the

information they need to explore issues and inform decision making

There are opportunities for on-going learning and development which will include the circulation of new or

relevant research and analysis and changes to the operating environment

The board may wish to seek specialist, independent external advice to enable it to discharge its duties

eectively and report ndings to the board

Annual board reviews and development plans come to the board for discussion

Diversity The board makes positive eorts to reduce or prevent obstacles to people becoming trustees including

looking at the presentation of papers; for example, communications provided in dierent formats

Trustees ensure that mechanisms are in place to monitor and achieve the board’s diversity objectives –

this may include reports to the board on progress

Openness and

accountability

The board receives regular reports on positive and negative feedback received and on sta/volunteer

engagement

6

CENTRE FOR CHARITY EFFECTIVENESS

Key principles and approach for

three dierent types of report

The key to a successful board

report is to be clear about why it is

being brought to the board.

Understanding the purpose of the report

is crucial to deciding what information is

needed and how it should be presented.

The exact purpose may vary, but most

board reports fall into one of three broad

categories, for which dierent approaches

are appropriate:

■

To enable the board to make a decision

■

To report progress and performance

to the board and to ensure control and

compliance

■

To learn, build knowledge and generate

new thinking.

REPORT/PAPER FOR DECISION

These papers enable the board to set

direction, or to set boundaries. They

provide a framework to guide the work of

the charity.

Examples: Proposed budget, proposal

for a new project, proposal for a new

or amended policy or procedure; risk

management process; strategy; vision,

mission, values; terms of reference for

committees.

Key principles on approach to use:

■

Contains sucient information to make

a decision

■

Considers alternatives and makes

reasoned recommendations

■

Highlights risks

■

For big decisions it may be appropriate

to have a series of reports brought to

successive meetings e.g. rst reports

set out issues, agrees principles,

second reports sets out options, third

report sets out implementation and

monitoring plan for preferred option.

Key questions for trustees

■

Do we have sucient information to

make this decision? Are there important

angles that have not been suciently

considered?

■

Are we condent that the people

who have draed the report have the

necessary skills and knowledge? Do we

need external specialist help?

■

Do we understand the resource

implications? What are the

opportunities and risks? How will risks

be managed?

■

Is the approach consistent – e.g. With

legal requirements? With our vision,

values, strategy, other decisions we

have made? With user needs and

wishes?

■

Is it clear how progress will be

monitored and reported? Or in the case

of policies how can we be sure they are

being followed?

■

How will we document the decision

making process and demonstrate

transparency and compliance?

A suggested format for decision making

reports is in Appendix 1.

PROGRESS, PERFORMANCE, CONTROL

AND COMPLIANCE REPORTS

These reports enable the board to assess

performance.

Examples: Scorecard or dashboard,

nancial report, strategy progress report,

project update, investment report, equal

opportunities report, risk management

register; results of audits, survey results.

Key principles:

■

Compares what has happened with

what was planned/forecast, or what has

happened before

■

Provides trend data and compares with

other organisations where possible

■

Uses a consistent format, preferably

making use of graphs and colour coding

so that key information can be absorbed

at a glance

■

Provides high level information – but

also provides the opportunity to ‘drill

down’ into the data if needed

■

Makes clear any limitations of data

presented

■

Includes management comment

on areas that are under- or over-

performing, and explains action

being taken to address problem

areas. Root cause and implications of

underperformance are explained.

In addition to performance reporting the

board will also want audits and verication

– these provide an additional level of

assurance that the information being

reported is reliable. For example, the board

can agree policies and procedures, but

how does the board know they are being

followed?

BOARD REPORTS THAT ADD VALUE

7

Key questions for trustees

■

Are we doing better or worse than

planned?

■

Do we understand the reasons for this?

■

Has the management got a credible plan

to deal with this?

■

Do we need to commit more resource to

ensure the sta have the support they

need?

■

Are our decisions being carried out?

■

What potential improvements to

performance can we see?

■

How will these results aect our future

direction?

■

Are our controls eective?

Some suggestions on presenting data are

given in Appendix 2.

REPORTS FOR LEARNING, BUILDING

KNOWLEDGE AND GENERATING NEW

THINKING

These reports enable the board to learn

from experience and from others and to

generate ideas about future direction and

how to be more eective.

Examples: Evaluation reports,

benchmarking data, research reports,

beneciary case studies, trends in

volunteering/fundraising/outcomes

monitoring; legislative update.

Key principles:

■

These reports are likely to come in a

variety of formats and from dierent

sources both internal and external, so

the board might want an external expert

or a team leader to present on a specic

topic

■

Create opportunities for information

to flow to and from board members so

that the experience and expertise in the

room is being used.

Key questions for trustees

■

What are the implications for us and for

our future strategic direction?

■

How can we apply this learning?

■

What new thinking could this generate?

■

What knowledge isn’t available that

would be helpful for us to have for

future decision making?

■

How do we ensure sta get appropriate

recognition for key achievements?

Two of the most common reports to the

board, the Chief Executive’s report and

nancial reports are explored in more

detail in Appendix 7.

Hallmarks of an

eective report

An eective report:

■

Is clear about its purpose, in particular

what trustees are being asked to consider,

do, or decide

■

Contains sucient information to full the

purpose i.e. sucient information to make

a decision, sucient information to assess

performance

■

Presents information so that it is easy to

absorb and is concise

■

Considers alternatives and highlights risks

■

Generates more questions than answers

(in a good way, i.e. stimulates new

thinking).

In contrast poor reports:

■

Are muddled about purpose

■

Provide incomplete, outdated, inaccurate,

confusing or misleading information

■

Take too long to compile and too long to

read

■

Include data and narrative but little

analysis

■

Result in inconclusive discussion

■

Generate more questions than answers

(in a bad way, i.e. because it’s hard to

understand)

■

Provide inappropriate levels of detail,

with the danger that trustees stray

into operational matters that are more

appropriately dealt with by sta.

It’s a good idea to create a board calendar

setting out a reporting schedule for key

reports. In this way the board can be sure

it covers all the main areas over an agreed

period (e.g. 12 or 18 months).

You may wish to create linked calendars for

sub-committees, see Appendix 3.

8

CENTRE FOR CHARITY EFFECTIVENESS

The role of sub-committees in

eective reporting

Sub-committees have an important

role to play in ensuring boards

get the balance right between

maintaining an overview of

everything that goes on in the

organisation and having enough

time at meetings to debate and

discuss the strategic governance

issues.

The sub-committee’s role and performance

in enabling this needs to be reviewed

periodically by the board. A sub-

committee’s role in eective reporting (as

permitted by the governing document) will

include preparing recommendations to the

board based on:

■

Commissioned research

■

Synthesis and analysis of implications

of information they receive

■

Consideration of a range of options

■

Narrowing down options and/or making

a recommendation (but keeping a

decision making trail).

Reports/papers for decision are likely to

have been worked on in more detail by

the sub-committee in advance of them

arriving at the board. It would be usual

for the sub-committee to be involved

at an early stage in the development of

a new initiative, and to keep the board

informed of progress, deciding when

and how the board gets more involved. A

sub-committee may attach a cover sheet to

such reports containing key messages and

recommendations.

Progress, performance control and

compliance reports are also likely to have

been considered by the sub-committee

whilst en-route to the board. Oen,

the sub-committee will receive a more

detailed and in depth report on progress or

performance than the board, and will agree

what information will be sent forward to

the board, attaching a summary note to the

progress report. In all cases it is important

that the board has the ability to drill down

into the detail as it decides is appropriate,

and be provided with a decision trail if

required.

Reports for learning, building knowledge

and generating new thinking may originate

at a sub-committee as they usually have

a horizon scanning role, and will be

seeking out opportunities to build board

knowledge and interest in their area of

responsibility. They will also encourage

board debate and discussion of the key

issues and to consider likely future events.

It is usual for the sub-committee to submit

the minutes of its meetings to the board,

and for there to be opportunity at the

board meeting for trustees to discuss any

items they wish to pursue that are not

covered elsewhere on the agenda. One

way for the sub-committee to keep the

board focussed on the things that matter

is to attach a summary sheet (see

Appendix 4) to the minutes, detailing those

areas it feels are most important. The

purpose of this summary sheet is to:

■

Enrich the board’s understanding

■

Enable them to drill down if they want to

■

Stimulate discussion about the right

things

■

Assure the board that the organisation

is well run, compliant and is managing

risks in line with the risk policy.

BOARD REPORTS THAT ADD VALUE

9

Common types

of report

In this section we look in depth at

two of the most common reports to

the board and set out some pointers

specic to these reports.

CHIEF EXECUTIVE REGULAR REPORT

Most boards have a regular report from their

Chief Executive, but may not have claried the

purpose of the report and what information

they actually need. Of course the style and

format of Chief Executive reports will vary

enormously.

Appendix 5 provides some pointers about

its focus and what is and is not helpful to

include. We suggest the role of the report is

primarily about progress and performance

reporting; and the building of knowledge and

generation of new thinking. A routine report is

rarely appropriate for decision-making – this

is usually better suited to a separate paper.

FINANCE REPORTS

The board needs to ensure the organisation’s

nancial health and that internal controls are

adequate. This is not just about oversight

and stewardship. Financial reporting needs

to be set within the organisation’s vision and

strategic objectives and to contribute to the

organisation’s longer term sustainability.

As with other areas of the organisation,

board papers on nance tend to fall into three

categories

10

CENTRE FOR CHARITY EFFECTIVENESS

Decision making papers that set the

framework for allocation of resources and

nancial control. For example, the board

needs to agree and update appropriate

policies and procedures such as nancial

controls, investment and reserves policies,

and agree budgets.

Progress, performance, control and

compliance reports

A range of dierent reports are needed by the

board for it to know that proper accounting

records are kept, assets are safeguarded and

resources properly applied, and to enable

the board to assess the eectiveness of

the organisation’s activities and the use of

resources in meeting the agreed strategic

goals. Key reports here include management

accounts, the use of reserves and cashflow.

Learning, building knowledge and generating

new thinking

Financial reports can also add value to the

organisation by providing the nancial

framework for exploring options, developing

new ideas and working assumptions and to

plan for longer term sustainability

Appendix 7 contains suggestions about the

range of dierent nancial reports likely to be

needed by the board and more information

about their purpose.

Top tips

Invest time in improving reports to

the board – good reports provide the

foundation for eective discussion,

save time and can avoid unnecessary

repetition or conflict.

Create a board calendar setting out a

reporting schedule for key reports – in

this way the board can be sure it covers

all the main areas over an agreed period

(e.g. 12 or 18 months).

Consider using a scorecard – this is a

select set of indicators the board has

identied as being key to success. They

should include measures that help

predict future performance as well as

reporting on what has already been

achieved. For more information on this

see BBG: Developing a dashboard and

balanced scorecard

For Chair and Chief Executive – the task

is to be clear about what kind of board

conversation they want each report to

generate.

Give feedback on reports coming to

the board – suggesting improvements

and giving praise when a report is

highly eective. Notice whether reports

succeed in generating insightful

discussion or are received passively.

Rapidly reacquaint trustees with key

context – e.g. provide a brief summary

of previous discussions or decisions.

Don’t assume they will delve back into

past papers for important information.

Ask eective questions – some

questions are more eective than

others in generating constructive

debate. Asking ‘why’ can put people

on the defensive. It may be more

productive to ask ‘what if . . .’

Focus on what is material – summarise

and concentrate on signicant

categories, variances and other

changes. Present and discuss

information in order of magnitude or

importance.

BOARD REPORTS THAT ADD VALUE

11

Resources

Carver J (3rd Edition 2006) Boards That Make a Dierence: A New Design for Leadership in

Nonprot and Public Organizations, John Wiley & Sons

Charity Commission (2017) Charity Finances, Trustee Essentials (C25)

Charity Commission (2012) Internal Financial Controls for Charities (CC8)

Charity Commission (2013) It’s Your Decision: Charity Trustees and Decision Making

Charity Commission (2017) Charity Governance, Finance and Resilience – 15 questions that

trustees should ask

Butler L (2012) The non-prot dashboard: Using Metrics to Drive Mission Success,

BoardSource

ICSA (2018) Specimen Report Cover Sheet for Charity Board Meetings

ICSA (2018) Eective Board Reporting

ICSA (2017) Challenges to Eective Board Reporting

Moon J (2008) How to Make an impact, influence, inform and impress with your reports,

presentations and Business Documents Financial Times / Prentice Hall

Tue E (2001) The Visual Display of Quantitative Information

12

CENTRE FOR CHARITY EFFECTIVENESS

1. Title of report

2. Summary

3. Author(s) and date

4. Purpose of the report including what is

needed from trustees

5. Background/context

6. Issues

7. Implications:

a. Strategic

b. Financial

c. Risk management

8. Recommendations and/or options

9. Reporting back

Appendix 1: Sample

contents for decision

making report

BOARD REPORTS THAT ADD VALUE

13

Careful thought about how to present

information can transform its usefulness

3

.

USE A CONSISTENT FORMAT

When a board becomes accustomed to seeing

data in the same format over time, it is easier

to spot trends, changes and problems that

may cause concern.

PROVIDE A COMPARISON

To transform data into information, it is oen

useful to ask the question: compared to what?

You can compare actual performance with

target performance, or last year’s, or with

forecast or a chosen benchmark. You might

want to display historical trend information

so you can see whether the underlying

performance is improving or declining.

Comparisons help put performance in

perspective.

USE CHARTS, DIAGRAMS AND OTHER

GRAPHICS TO BRING YOUR DATA TO LIFE

Line charts, colour coding, bar graphs, pie

charts, and data maps can be very eective

in conveying information and revealing

meaningful trends and patterns

4

. Milestones

reached or stages completed can be helpful

for project reporting

GIVE A BRIEF NARRATIVE

It’s oen useful to add a few words of

description, identifying successes and areas

of concern, and possible cause and eect

relationships.

14

CENTRE FOR CHARITY EFFECTIVENESS

Appendix 2:

Presentation of

performance data

3. These suggestions are drawn from THE NONPROFIT DASHBOARD: Using Metrics to Drive Mission Success © 2012

BoardSource

4. For more information see The Visual Display of Quantitative Information, Edward Tue. 2001

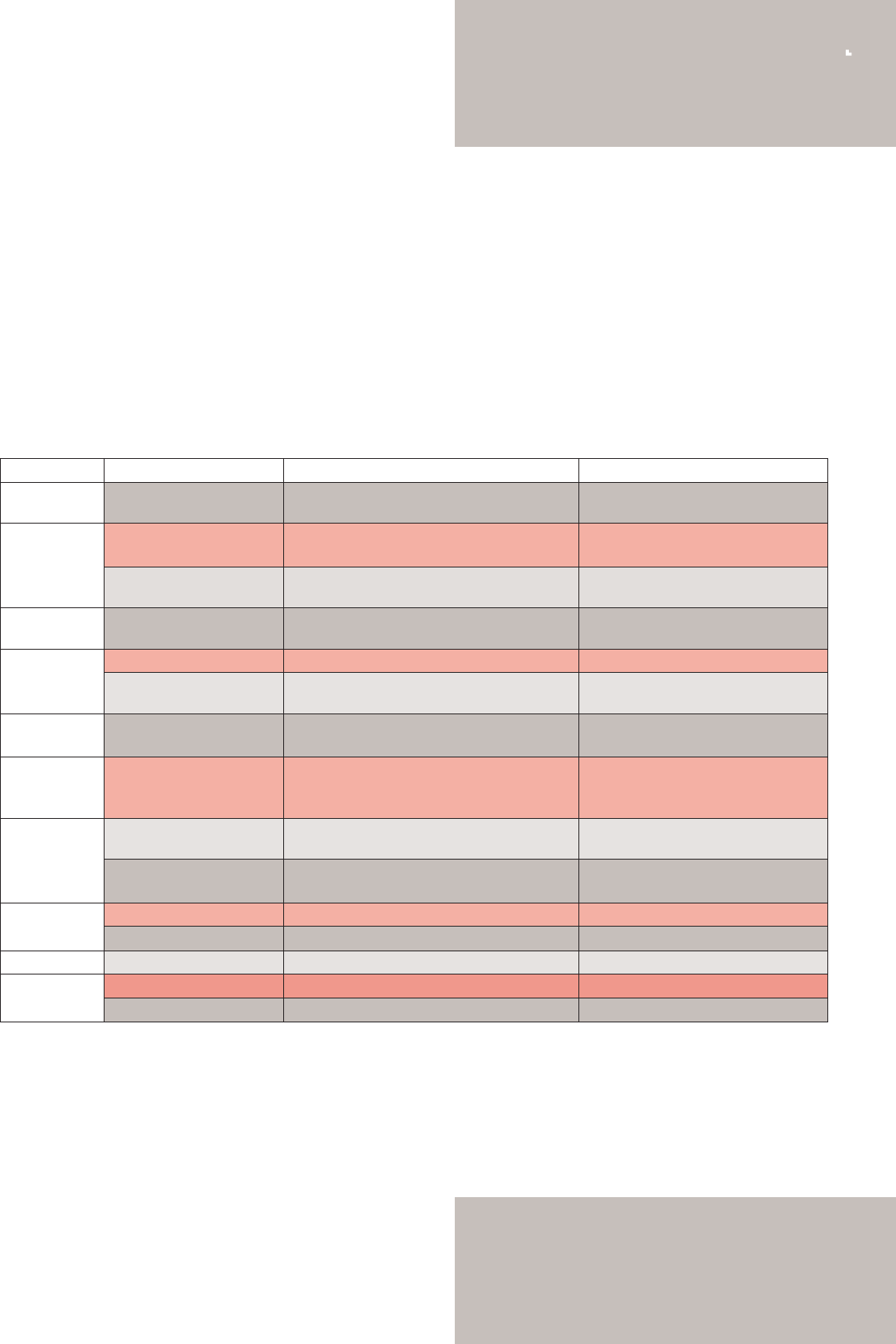

Month Committee Planned activities Report to the board

January Board Agree nancial policies to include:

investments, reserves and pensions

February Fundraising and marketing Agree forthcoming annual plan

Prepare quarterly report to board

Finance Agree budget assumptions and nal version

(agree audit plan)

March Board* Agree nal budget

(nancial year end)

May Fundraising and marketing Prepare annual report to the board

Finance Review Investment performance; property and

estates valuation

June Board Audit report to board

Prepare trustees’ report

July Fundraising and marketing Review of committee eectiveness and update

terms of reference

Prepare quarterly report to board

August Finance Review management letter and propose

actions

Board Review and agree risk management policies

and internal controls

Management letter to board

Sign o report and accounts

October Fundraising and marketing Prepare quarterly report to board

Board

November Finance Prepare annual report to the board

December Fundraising and marketing Prepare quarterly report to board

Board

Appendix 3: Board committee

calendar

BOARD REPORTS THAT ADD VALUE

15

Here’s a possible format for planning board committee agendas and how they t with the

main board – with some sample entries.

* A number of nancial reports will be presented to the board on a quarterly basis. These are detailed in Appendix 6.

16

CENTRE FOR CHARITY EFFECTIVENESS

Summary from board sub-committee:

For board meeting date:

Date of sub-group meeting:

Key issues under discussion:

Information for the board attention:

Actions since last sub-committee meeting:

Board decisions required:

Date of next meeting:

Author of summary:

Appendix 4: Summarising

committee discussions

to the board

WHY IS IT IMPORTANT?

The Chief Executive’s regular report

provides good quality information to the

board about progress and likely future

performance – good and bad – on a timely

basis so that board members can respond

appropriately. It also has a role to play in

sharing intelligence and insight with the

board that may shape future strategy. This

is more about stimulating dialogue about

the organisation’s direction and priorities.

The Chief Executive’s regular report

is a key way for the board to hold the

Chief Executive to account. Good Chief

Executive reports build understanding and

condence. Board members feel they get

reliable and appropriate information and

that there is honesty about challenges

as well as successes. Chief Executive

reports should reflect what is important to

trustees and not just what is important to

the Chief Executive. At the same time the

Chief Executive should feel able to share,

feel supported and able to ask for advice

when appropriate.

Common pitfalls in Chief Executive reports:

■

Random list of what the Chief Executive

or sta team have been doing or who

they have been meeting

■

Is focused on past or current

performance and fails to look forward.

■

Selective – rather than a balanced

overview

■

Overly focused on good news whilst

neglecting to comment on less positive

areas.

■

Duplicates areas included in other

reports or provides conflicting

information to that provided in other

reports.

■

Unrelated to strategic objectives

■

Suggests a change in policy, budget or

strategy without adequate information

or context on which to base such a

decision

■

Lack of analysis: all data and no opinion

or all opinion and no data.

Possible format

You may nd it helpful to think of the Chief

Executive report as falling into 3 parts:

a) Performance: giving an overview of

performance and implications for future

performance

b) Early alerts: giving early notice of

emerging risks and opportunities

c) Insight and ideas: to stimulate strategic

thinking and discussion.

Each of these parts is explored further in

the table below

Appendix 5: Chief Executive report

BOARD REPORTS THAT ADD VALUE

17

18

CENTRE FOR CHARITY EFFECTIVENESS

Chief Executive regular report – a possible structure

Section and purpose Content Questions for Chief Executive to consider

Strategic performance report:

Give an overview of performance

and implications for future

performance

A report of progress against agreed strategic

objectives and/or targets. It should follow the

key principles of performance reporting set out

in Section 4 (progress, performance, control

and compliance reports) of this guide. We

recommend using a scorecard or dashboard

5

,

but you may wish to adopt your own approach.

This could be a set of standard headings

drawn from the strategy or business plan. It

should provide a quick overview for trustees. A

narrative section should comment on areas that

are o target, and what is being done to bring

them back on target.

The Chief Executive may wish to highlight

outstanding performance by individuals and

teams to help trustees ensure they give due

recognition.

Am I giving the trustees a balanced view of

what is going on in the organisation?

Have I struck an appropriate balance between

good news and ‘bad’ news?

Which issues have or potentially have strategic

importance – and should be ‘foregrounded’?

What are the implications for future

performance?

Is there not just data but analysis too?

Are there individuals or teams who deserve

particular recognition?

Early alerts (internal and external):

giving early notice of emerging

risks and opportunities

You may nd it useful to have this section in

which the Chief Executive can identify potential

opportunities and risks at an early stage. It is

worth including internal and external factors.

Items that may feature here include sta

matters, funding opportunities. This is a good

place to raise issues that are not obvious from

the performance reports.

What do I need to forewarn trustees of? How

do I ensure ‘no surprises’

Are there potential problem areas where it

would be helpful to have advice or a steer from

the board?

Are there potential opportunities that it would

be helpful for the board to be aware of e.g.

interest from a particular donor? News about

our funders?

Insights and ideas: to stimulate

strategic thinking

This section provides an opportunity for the

Chief Executive to share insights about, or

questions prompted by recent events internal or

external. (For example what does this say about

our culture, or is this an important trend for the

future, could this be a new funding stream?)

Are there strategic issues here for trustees to

think about?

Do trustees share my interpretation of this?

Do I know whether they attach the same

importance as I do?

5. For more information see BBG: Developing a dashboard and balanced scorecard.

Like other areas of trustee responsibility,

nance is a collective responsibility and

should not sit with an individual board

member. The purpose of the nancial

report is to enable trustees to come

armed with the necessary knowledge

to contribute to the debate and decision

making.

Financial reports should present

nancial information which is consistent,

transparent and can be read as a

standalone report. This will help to build

trust between the board and management

team.

KEY POINTS

■

The information should be as up to date

as possible, presented in the context

of the agreed strategic objectives of

the organisation. It should help tell

the story about the services you are

delivering and how you do it

■

Try to give consistent material

presented in a standard format for each

reporting period

■

Include an executive summary at the

front which

- summarises the report’s content and

highlights key information

- draws the board member’s attention

to certain points with an explanation

as to why they need to consider

these ahead of the board meeting

- contains a summary report of key

performance indicators (perhaps

using a trac light system to signal

items of particular importance)

■

Non-standing items should be at the

back of the report where they can be

reviewed in one go and not distract from

the expected and regularly provided

information

■

Balance the level of detail to the

information that the board needs

and will use – aim to promote

discussion whilst at the same time

providing sucient information to aid

understanding

■

If and where possible, try to account

for operations during the year by using

the same accounting principles as

those used to draw up the year-end

statutory accounts. The board has an

ongoing responsibility throughout the

year, not simply at the year end and will

be reassured if they can read across

from the cumulative management

information to the statutory accounts

without too many adjustments.

ADDITIONAL REPORTING

One size reporting will not t all

organisations. Dierent stages of growth

and development will require additional

reporting.

Capital projects or new initiatives will call

for specialised budgets.

At times of diculty there will be a

need for additional detail, frequency of

reporting, regularly updated forecasts and

monitoring of cashflow.

The charity Statement of Recommended

Practice (SORP) puts increased emphasis

on the reporting of outcomes and impact

created

6

. A good nance report will help

trustees’ understanding of how outcomes

are being achieved and the organisation

will be able to tell “its story” to external

stakeholders.

More information can be found overleaf

about the kind of information you might

include.

Appendix 6: Financial reporting

BOARD REPORTS THAT ADD VALUE

19

6. See the Institute of Chartered Accountants in England and Wales website for examples of charities demonstrating best practice

7. For some suggested approaches see How to Make an Impact, influence, inform and impress with your reports, presentations and Business Documents by Jon Moon, (2008)

London, Pearson Hall

SOME TIPS:

Try to put narrative on the same lines

as summary gures to answer the

“so what” test.

Round your numbers to the nearest

thousand or million; it helps readers

to engage with information and

makes for easier understanding.

Put negatives in brackets not with a

minus sign which is easy to miss.

Where data falls outside expected

parameters consider reporting by

exception.

Provide tables and visuals

7

if helpful

and put operational detail in an

appendix if necessary.

In practice reporting to the board will include information on nancial control, compliance

and performance evaluation as one package. Some information will need to be presented

more regularly than others and together the papers will contribute to the complete

planning, review and learning cycle. It is usually the nance director or the chair of the

nance sub-committee who will present the information. The table below suggests what

information should be presented at the dierent intervals.

Appendix 7: Key nancial reports

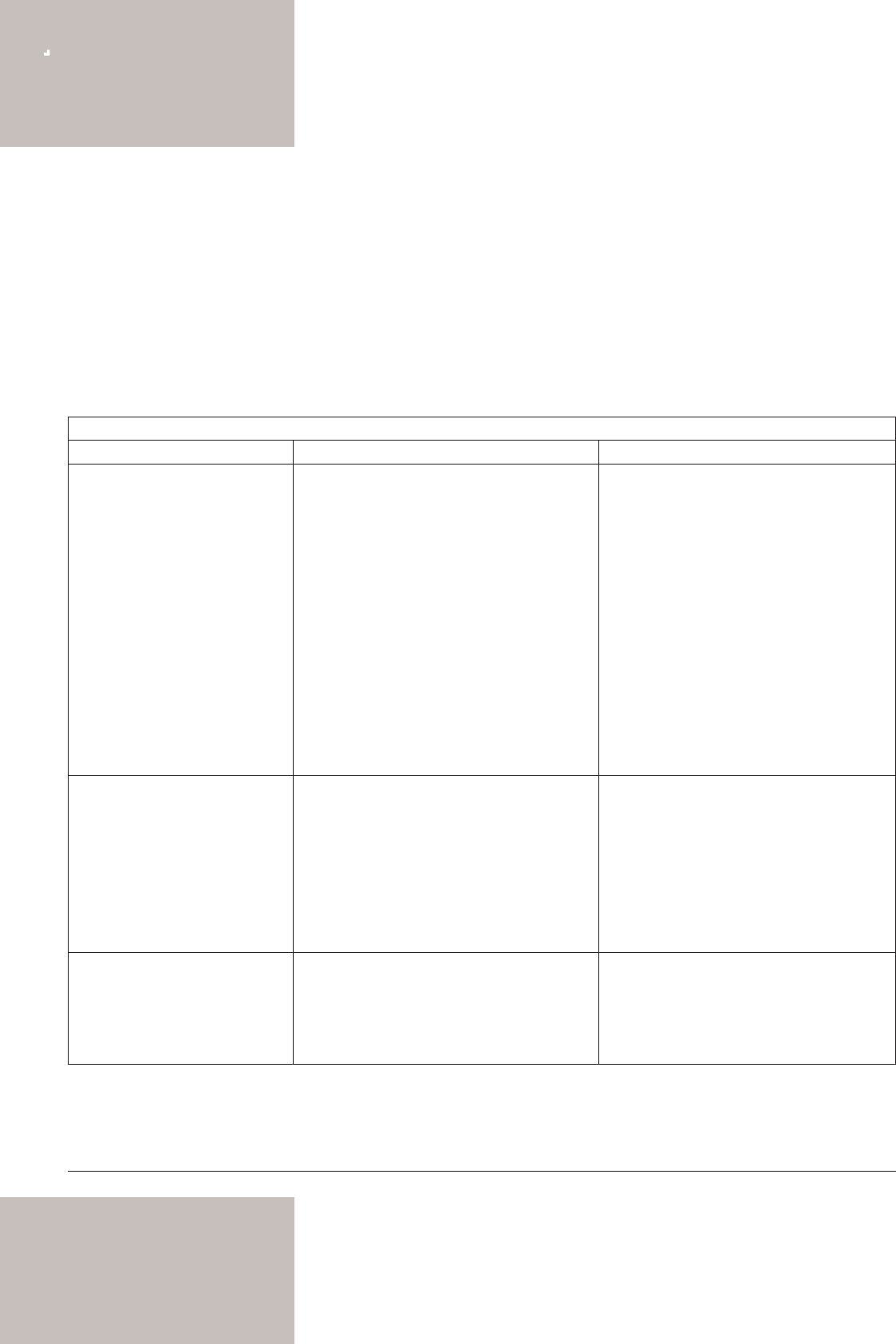

Purpose of reporting

Annually reported To ensure that the trustees can be publicly responsible for the adequacy of internal

controls and for the fairness and accuracy of the annual report and accompanying

nancial statements.

A fully costed budget which is in line with

the strategic plan’s short term objectives

To form part of the system of control to safeguard the assets and apply resources

properly for the objects of the charity. The budget will be agreed by the board and be

reported against on a quarterly basis.

Report and [audited] accounts To prepare and then sign o on the Trustees’ Report and Financial Statements in

accordance with applicable law and the United Kingdom Accounting Standards.

Issues raised in Auditor’s Management letter To enable any material weaknesses in the accounting and internal control systems

identied during the audit to be resolved on a timely basis. To ensure all adjustments

required to the accounts are fully understood and to agree their resolution and timing.

Internal controls policies To comply with best practice and to safeguard the assets and the continued service

delivery of the organisation. To review and set the control polices and ensure they are

clearly linked to the internal and external risk environment.

Risk management assessment To enable the board to determine the nature and extent of the signicant risks it is

willing to take in achieving its strategic objectives. To enable the board to understand,

evaluate and take action on their risks with a view to increasing the probability of their

success and reducing the likelihood of failure.

Financial policies; to include reserves,

investments and pensions

To comply with applicable law and to observe the principles and methods contained in

the Charities SORP.

Investment performance and administration

costs

To ensure the eective use of funds, that maximum Return on Investment (ROI) is being

earned and to assess (and possibly benchmark) the level of investment management

costs. To ensure that any fall in valuation will not impact signicantly on the balance

sheet (see below – property). To review any investment criteria and to amend as

appropriate; for example, ethical investment criteria.

Pension / retirement benets review To enable the board to understand the nancial implications of the pension and benet

plans.

Property and Estates valuation review To provide a current valuation of property assets. This is particularly important in the

current economic environment where a fall in property value, could in the worst case,

result in a charity having an insolvent balance sheet.

20

CENTRE FOR CHARITY EFFECTIVENESS

Disclaimer

While great care has been

taken to ensure the accuracy

of information contained in

this publication, information

contained is provided on

an ‘as is’ basis with no

guarantees of completeness,

accuracy, usefulness,

timeliness or of the results

obtained from the use of the

information and the Centre

for Charity Eectiveness

accepts no responsibility

or liability for any errors or

omissions that may occur. The

publisher and author make

no representation, express

or implied with regard to the

accuracy of the information

contained in this publication.

The views expressed in

this publication may not

necessarily be those of

the Centre for Charity

Eectiveness. Any action you

take upon this information

is strictly at your own risk.

Specic advice should be

sought from professional

advisers for specic

situations.

Purpose of reporting

Quarterly reports To enable the trustees to be continually in touch

with the nances, controls and risk management

of the organisation so that they can discharge

their stewardship and generative responsibilities.

Summary level management accounts

(see template for suggested format) to

include any project accounts

To provide analysis and explanations of all

signicant variances together with information on

options for remedial action / timescales in areas

of concern.

To ensure proper accounting records are

maintained which can disclose with reasonable

accuracy at any time, the nancial position of the

organisation.

To ensure the budget is re-forecast at regular

intervals if signicant changes occur to the

nances.

Cash flow, aged creditors and debtors A charity will fail if it runs out of cash! It may be

appropriate for the board to see the monthly

prole of cash expenditure together with an

analysis of aged debtors and creditors.

A review of signicant movements on

restricted and unrestricted reserves

To ensure that reserves are being correctly

accounted for and that the organisation

has sucient funds to enable medium term

sustainability.

Trading subsidiary performance; prot

and loss against budget and variances

To ensure that the trading performance is in line

with agreed budget.

Comparative reports on other agreed

benchmarks or specic service

programmes

To measure against and compare with other

organisations and assess the reasons for any

dierences.

An annual report on future nancial

scenarios will help sustainability

This will help the board to consider the

opportunities and threats to the funding model

and to know how they will adapt to future

challenges. This might include analysis of:

• Forecasts and trends in the sector

• Internal and external drivers of nancial

performance

• Options for future sustainability and the

potential use of reserves

BOARD REPORTS THAT ADD VALUE

21

Disclaimer: All the information contained within this brochure was correct at the time of going to print. Published March 2019. Updated September 2021.

Bayes Business School

106 Bunhill Row

London EC1Y 8TZ

E: CCE@city.ac.uk

www.bayes.city.ac.uk/cce

City, University of London is an independent member of the University of London which was established by

Royal Charter in 1836. It consists of 18 independent member institutions of outstanding global reputation

and several prestigious central academic bodies and activities.

facebook.com/BayesBSchool

instagram.com/bayesbschool

twitter.com/BayesCCE

youtube.com/bayesbusinessschoolocial

linkedin.com/company/bayescce