Sustainability: The future

of investing

GLOBAL INSIGHTS • FEBRUARY 2019

BIIM0219U-733437-1/20

Brian Deese

Global Head of

Sustainable Investing

2 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Philipp Hildebrand

BlackRock

Vice Chairman

Rich Kushel

Head of Multi-Asset

Strategies and

Global Fixed Income

Barbara Novick

Vice Chairman

Mark Wiseman

Global Head of

Active Equities

Introduction

For years, many investors saw sustainable investing as a trade-o.

They viewed it as a sacrifice of value for “values.” And to be fair, they

were often right. But that is no longer the case. What has changed?

More granular data, more sophisticated analysis, and deeper societal

appreciation for and understanding of what sustainability means

for people, companies and countries. There is increasing awareness

that material sustainability-related factors — often characterized

as environmental, social and governance, or ESG — can be tied to

a company’s long-term growth potential. This makes sustainable

investing something investors can no longer aord to ignore.

We are seeing greater interest from our clients in sustainable investing. Investors want

deeper knowledge about the field, more sustainable investing options, enhanced

data and reporting on impact, and increased commitment from asset managers to

integrate sustainability into investment processes. Millennials, in particular, look set

to propel the future of sustainable investing. This group of future financial decision-

makers is asking more of companies. And regulators are expanding their focus

on incorporating sustainability into investment information and decision making.

BlackRock is increasing its focus on sustainability across the board — from our

investment processes to the investment solutions we oer. There is growing

recognition that the field presents a largely untapped source of information that

can potentially identify investment risks and generate excess returns. At the same

time, the data are imperfect, scoring methodologies dier, and investors need

to gain greater clarity on the pitfalls of this emerging field. This paper discusses

three key themes driving transformation in sustainable investing: the aim to create

sustainable portfolios and strategies that do not compromise financial returns;

the eort to use innovative research to go beyond headline ESG scores; and the

integration of sustainability-related issues into traditional investment strategies.

Our work fuels our conviction that the future of investing is sustainable.

A “why not?” moment

Introduction ........................................4

Framework .........................................5

Stocks and bonds .............................6

Factors and resilience .......................7

Beyond headline ESG scores

Importance of “E” ..............................8

Improving the data ............................9

Transition readiness ..................10-11

ESG in EM ........................................ 13

ESG integration

Introduction ..................................... 14

Purpose and stewardship.............. 15

Our approach ................................. 16

Lessons and reflections ................. 17

CONTENTS

BIIM0219U-733437-2/20

3 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

BLACKROCK INVESTMENT INSTITUTE 3

LEF T TO RIGHT

Andre Bertolotti — Head of Global Sustainable Research and Data, BlackRock Sustainable Investing; Tariq Fancy — Chief

Investment Ocer of Sustainable Investing; Isabelle Mateos y Lago — Chief Multi-Asset Strategist, BlackRock Investment

Institute; Giulia Pellegrini — Head of EMD Sustainable Investing and portfolio manager; Ashley Schulten — Head of

Responsible Investing for Global Fixed Income; Josephine Smith — Factor Based Strategies Group

Summary

• Sustainable investing is no longer a niche area; it is going mainstream. Assets in dedicated

sustainable investing strategies have grown at a rapid pace in recent years. We are seeing a surge

in clients’ and portfolio managers' interest in incorporating sustainability-related insights into

their investments. This demand looks poised to accelerate — driven by societal and demographic

changes, increased regulation and government focus, and greater investment conviction.

• Enhanced data and insights make it possible to create sustainable portfolios without compromising

financial goals. Our research, which relies on backtested data, shows how ESG-focused indexes

have matched or exceeded returns of their standard counterparts, with comparable volatility.

We find ESG has much in common with existing quality metrics such as strong balance sheets,

suggesting ESG-friendly portfolios could be more resilient in downturns. These resilience properties

deserve attention as market uncertainty increases. In other words: We have arrived at a “why not?”

moment in sustainable investing.

• Driving innovation in sustainable investing requires going beneath the headlines. ESG data have

evolved, but are still incomplete. We believe the most meaningful investment insights are found

beneath the headline ESG scores. Alpha-seeking strategies focus on understanding and exploiting

key performance indicators at the sector, industry and company level. New technologies and

methodologies have allowed us to make great strides in improving sustainability data. This includes

techniques to estimate missing data, and determine their materiality to investment performance.

• Integration of sustainability considerations into investment processes is on the rise — and for

good reason. BlackRock’s approach, outlined in our 2018 ESG Investment Statement, starts with

making better research and data available to all our investment teams. The goal is to help them

identify and implement investment process enhancements. Incorporating relevant sustainability

insights can provide a more holistic view of investment risks and opportunities. There is no one-

size-fits-all approach, but the opportunity to improve investment processes by integrating material

sustainability considerations is real and growing. BlackRock also actively engages with companies

to encourage business practices consistent with delivering sustainable long-term financial returns.

AUTHORS

BIIM0219U-733437-3/20

4 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Definitions and data

The concept of “sustainable investing” can mean many

dierent things. Asset owners and asset managers

often operate with multiple definitions, messages and

motivations. BlackRock operates from a simple definition

of sustainable investing: Combining traditional investing

with sustainability-related insights in an effort to reduce

risk and enhance long-term returns.

Our view: Companies with strong performance

on material sustainability issues have potential to

outperform those with poor performance. This is in line

with a growing body of academic evidence, including

the 2016 Harvard Business School study Corporate

Sustainability: First Evidence on Materiality.

ESG is often conflated or used interchangeably with the

term “sustainable investing.” We see sustainable investing

as the umbrella and ESG as a data toolkit for identifying

and informing our solutions. Importantly, ESG integration

(page 14) is just one aspect of ESG investing.

Growing up

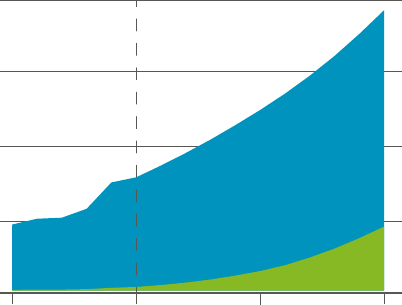

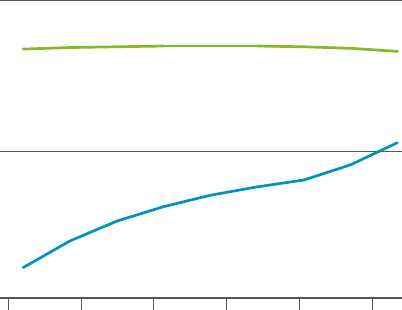

The universe of dedicated sustainable investment

funds is growing: A current combined total of roughly

$760 billion in European and U.S. mutual funds and

exchange-traded funds (ETFs) is up from $453 billion

in 2013. See the Sustainable swell chart. Asset owners’

increasing interest in this area is driving strong growth

in new products and innovation. More than 100 new

sustainable mutual funds and ETFs were launched

in the U.S. alone from 2015 to 2017, according to

Morningstar Research.

We expect significant growth in mainstream sustainable

investing options, and see demand for related funds

growing at a double-digit pace through the next decade,

as the chart shows. This growth will likely be driven by

millennials (those born between the early-1980s and

late-1990s), a generation that tends to be keenly focused

on company values and is set to experience growth in

net wealth as its members advance in the labor force

and grow their incomes.

In addition, governments across most major geographies

are increasing their regulatory focus on incorporating

sustainability considerations into investments. The

European Union and individual European countries

are moving forward with specific directives. In Asia,

an increased regulatory focus has come in response

to environmental issues.

The U.S. stands apart — in particular, U.S. guidance

for private-sector retirement plans stresses fiduciaries

must not put ESG goals ahead of financial ones. Yet

the U.S. regulatory regime does allow consideration of

sustainability issues as a way to generate returns. The

thrust of these global regulatory actions could herald

greater capital allocation to sustainable companies

and assets over time.

A “why not?” moment

We detail our framework for thinking about sustainable investing, and show how building

sustainable portfolios need not mean giving up performance.

Sustainable swell

Assets of sustainable mutual funds and ETFs, 2013–2028

0

1.5

1

0.5

$2

Assets (USD trillions)

Actual Estimate

2028202320182013

Mutual funds

ETFs

There’s no guarantee that forward-looking estimates will come to pass.

Sources: BlackRock, with data from Broadridge/Simfund, June 2018. Notes: The

chart shows the total assets under management in ESG mutual funds (MFs) and ETFs

globally. The 2019 to 2028 figures are based on BlackRock estimates, assuming a 5%

annual growth rate in the underlying markets. Other assumptions: MF asset growth

starts at 5% in 2019 and declines by 0.5% annually through 2022, then at a zero-

to-0.5% rate annually thereafter. ETF asset growth starts at 45% and decreases by 5%

annually through 2022, with a zero-to-3% pace thereafter.

BIIM0219U-733437-4/20

5 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Forming a framework

Starting from our simple definition, we then distill client

motivations into a spectrum from Avoid to Advance.

“Avoid” eliminates exposures to certain companies or

sectors that pose reputational risks or violate the asset

owner’s values. “Advance” aligns capital with certain

behaviors, activities and outcomes. This might include

using ESG scores as an additional layer in the traditional

investment process. Other ways to advance include

thematic and impact investing, as detailed below. We

use this framework to think about sustainable investing

solutions (note that ESG integration is a separate

process — see page 14 for more).

ESG data is most often categorized as “non-accounting”

information because it captures components important

for valuations that are not traditionally reported. The

valuation of companies has become more complex,

with a growing portion tied up in intangible assets. ESG

metrics provide insights into these intangibles, such

as brand value and reputation, by measuring decisions

taken by company management that aect operational

eciency and future strategic directions. At a high level:

• Environmental (E) covers themes such as climate

risks, natural resources scarcity and pollution.

• Social (S) includes labor issues and product

liability risks such as data security.

• Governance (G) encompasses items such

as corporate board quality and eectiveness.

From “why” to “why not”

ESG research has come a long way. Information was

once manually gathered from limited sources. Now, a

growing industry provides robust data culled from the

public sphere, gives ESG ratings and helps improve

ESG reporting and disclosures. Gaps remain, but better

quality and coverage in data and research give us more

confidence in using ESG insights for both index and

alpha-seeking investment strategies. See page 10.

The challenge with ESG data is not just an issue of quality

and consistency. Dierent definitions and approaches can

lead ESG providers to diering conclusions on the same

asset or security. It is important to understand which data

sources asset managers are relying on, and how that data

is being built into investment strategies. It’s a key reason

we advocate greater transparency in ESG data. See

BlackRock’s Exploring ESG: A practitioner’s perspective.

ESG-focused strategies carry risks like any other

investments. Yet we see encouraging evidence that

investors can make their portfolios more sustainable

without compromising on traditional financial goals. We

show how backtests of ESG indexes reveal risk/return

metrics in line with conventional benchmarks in stocks

and bonds (page 6), and how investors can combine

the value factor and ESG exposures. We analyze ESG

through a factor lens; show how ESG can add resilience

to portfolios (page 7); and explore how enhanced data

can help increase investment conviction in emerging

markets (page 13).

Avoid and advance

Sustainable investing styles

Sources: BlackRock Investment Institute and BlackRock Sustainable Investing, December 2018.

Avoid Advance

Screened ESG Thematic Impact

Objective

Remove specific

companies/industries

associated with

objectionable activities

Invest in companies

based on ESG scores/

rating systems

Focus on particular

E, S or G issues

Target specific non-

financial outcomes along

with financial returns

Key

considerations

Definition of and financial

impact of screens

ESG data sources;

active risk taken

Broad versus specific

exposures

Report on progress

toward outcomes

Examples

Screening out producers

of weapons, fossil fuels

and/or tobacco

Optimized ESG

benchmarks; active

strategies overweighting

strong ESG performers

Environmental focus

(low carbon or renewable

energy); social focus

(diversity)

Specific green bond

or renewable power

mandates

BIIM0219U-733437-5/20

6 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

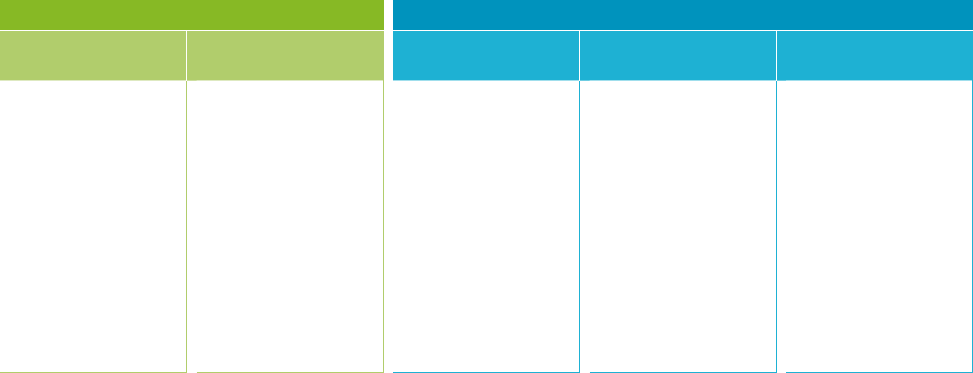

ESG in equities

Our research suggests investors do not need to choose

between the pursuit of returns and ESG excellence.

ESG-focused indexes are still relatively young and

performance histories include backtested data, but

we see the evidence as promising. When looking at

traditional indexes alongside MSCI’s ESG-focused

derivatives of them, annualized total returns since

2012 matched or exceeded the standard index in

both developed and emerging markets (EMs), with

comparable volatility. Valuation metrics were nearly

identical. See the An ESG lens for equities table below.

Traditional sustainable indexes were designed to select

top-rated ESG securities within a given sector or remove

certain business involvement areas. They were based on

an exclusions-focused approach, and performance and

portfolio characteristics notably deviated from market-

cap-weighted indexes. In contrast, optimized indexes

can help improve a portfolio-level ESG rating while still

tracking traditional benchmarks. They allow investors

to invest in higher-rated ESG companies without taking

on unintended risks such as sector concentration. The

optimized approach can be tailored to achieve carbon-

reduction goals, whether through a low-carbon strategy

or a dual-objective (ESG + low carbon) strategy.

A proxy for quality in bonds

Results are similar in fixed income. Over the past

decade, global high yield bonds from issuers with

higher ESG ratings (A or AA on MSCI’s rating scale) have

generated stronger information ratios — a gauge of risk-

adjusted returns — than bonds with lower ESG ratings,

despite their lower yields. See BlackRock’s Sustainable

investing: a ‘why not’ moment for details. Notably, the

global high yield issuers in our study without historical

ESG rating coverage (almost half) generated lower risk-

adjusted returns than rated issuers. Growing coverage

should help provide more granular analysis over time.

In the investment grade market, we found an ESG-

friendly version of the U.S. corporate index generated

near-identical risk-adjusted performance to its parent

index over the past decade. See page 9 of the paper

cited above for details. This research underscores our

view that ESG-friendly bond portfolios should generate

total returns similar to traditional portfolios over a

full market cycle — even if they sacrifice a little yield.

The argument for ESG becomes even more compelling

over longer time horizons. This is because ESG-

related risks tend to compound. Consider long-term

infrastructure bonds where projects are exposed to

flood risks that could intensify due to rising sea levels.

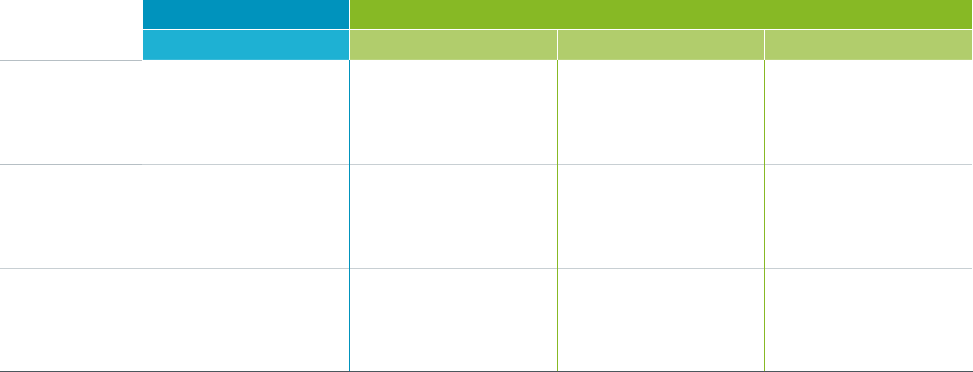

An ESG lens for equities

Comparison of traditional equity benchmarks and backtested ESG-focused counterparts by region, 2012–2018

Past performance is not a reliable indicator of current or future results. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data

from MSCI, November 2018. Notes: The data cover May 31, 2012, to Nov. 30, 2018. Returns are annualized gross returns in U.S. dollar terms. Number of stocks, price-to-earnings ratio

and dividend yield are monthly averages. Indexes used are the MSCI USA Index, MSCI World ex-U.S. Index, MSCI EM Index (“Traditional” columns) and MSCI’s ESG-focused derivations

of each (MSCI USA ESG Focus Index, MSCI World ex-U.S. Focus Index and MSCI Emerging Markets ESG Focus Index). The data shown prior to inception for each MSCI ESG Focus index

(August 2016 for U.S.; March 2017 for World ex-U.S.; April 2016 for EM) are backtested. They are optimized to maximize ESG exposure within constraints (example: a tracking error of

50 basis points and maximum active weight of 2% for each index constituent for USA ESG Focus). Backtested performance is hypothetical, simulated and is not indicative of actual or

future returns. Backtested performance is developed with the benefit of hindsight, has inherent limitations and invariably shows positive rates of return. ESG scores shown are average

scores for each index based on MSCI data. See important notes on the back page.

U.S. World ex-U.S. Emerging markets

Traditional ESG Focus Traditional ESG Focus Traditional ESG Focus

Annualized return 14.4% 14.5% 7.7% 8.1% 4.3% 5.7%

Volatility 9.7% 9.8% 11.5% 11.5% 14.4% 14.4%

Sharpe ratio 1.42 1.42 0.62 0.64 0.25 0.35

Maximum monthly

drawdown

-13.9% -13.9% -23.3% -22.7% -35.2% -33.1%

Price-to-earnings 19.6 19.9 17.0 16.9 13.4 13.6

Dividend yield 2.0% 2.0% 3.2% 3.2% 2.7% 2.8%

Number of stocks 621 313 1,012 453 855 300

ESG score 5.4 6.5 6.6 7.8 4.4 6.1

BIIM0219U-733437-6/20

7 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

ESG with a value bent

Can investors incorporate ESG considerations into

their portfolios while maintaining their desired factor

exposures? We partnered with index provider FTSE

Russell to find out. The goal: to develop a customized

value index with an ESG tilt, based on the FTSE

Developed Index of global developed market equities.

A key consideration was whether incorporating an

ESG adjustment to the index design would result in

unintended impacts to its value exposure — and vice

versa. Security weights were tilted based on how well

(or poorly) companies manage ESG risks according

to FTSE Russell’s ESG ratings data.

We started with the ESG-tilted FTSE Developed Index,

with the trade-o of a greater tracking error from

the market-cap-weighted parent index. Our finding:

Increasing the value exposure did not result in a

material decline in its average ESG score. See the

blue and green lines in the Best of both worlds chart.

In short, we found investors could increase their

exposure to the value factor while also maintaining a

higher overall ESG score than the parent benchmark.

ESG, factors and resilience

Factor-based investing oers a dierent lens for viewing

equity performance by isolating traits that are broad,

persistent drivers of return. We analyzed the relationship

between four style factors — quality, low-volatility, value

and momentum — and ESG scores using Thomson

Reuters ASSET4 data on 2,800 global stocks. We then

built hypothetical factor exposures that stripped out

the impact of broad market moves. Our findings: Low-

volatility and quality embed a stronger tilt to high ESG

scorers; the momentum factor showed modestly greater

ties to lower ESG companies. See page 7 of Sustainable

investing: a ‘why not’ moment for details.

We have not yet found reliable evidence to suggest

ESG has been a factor itself. But the idea that companies

with higher ESG scores exhibit quality and low-volatility

characteristics is an important insight. It suggests an

ESG tilt may add resilience to portfolios.

Resilience is a key consideration for long-term investors.

Given enough time, periods of negative returns can

rattle even the most experienced investors. And resilience

is a particularly welcome characteristic at a time when

the economic cycle is entering its latter stages. Quality

companies with strong balance sheets and cash flows

can provide a measure of resilience, we believe. They

can extend a larger buer against equity market

downturns than weaker peers. See BlackRock’s 2019

Investment Outlook and page 8 for details.

We believe the same principle applies to companies

that exhibit strong ESG characteristics. Strong

ESG performers may be better at managing legal,

reputational and financial risks. These findings are

consistent with external research. Example: AQR finds

that stocks with the worst ESG scores are 10% to 15%

more volatile than those with the best scores — and

that poor ESG performance points to future risks not

captured in standard risk models. See AQR’s 2017

paper Assessing Risk Through Environmental, Social

and Governance Exposures. Other research shows

companies that provide greater transparency into their

operations have outperformed others during equity

market down drifts. See the 2017 academic study

ESG Shareholder Engagement and Downside Risk.

Best of both worlds

Value and ESG exposures of hypothetical global equity index

0

2

4

ESG ratings / value exposure

Annual tracking error

6.5%5.54.51.5

2.5 3.5

ESG ratings

Value exposure

Past performance is not a reliable indicator of current or future results. It is not

possible to invest directly in an index. Sources: BlackRock Sustainable Investing

and BlackRock Investment Institute, with data from FTSE Russell as of January 2018.

The chart shows the ESG and value exposures of a hypothetical optimized global

equity index, based on the FTSE Developed Index. FTSE Russell applies an ESG tilt to

the parent index; the chart shows its active value exposure for given levels of tracking

error (active risk relative to the parent index). ESG ratings refer to FTSE Russell’s ESG

ratings, ranging from 0 (no disclosure) to 5 (best practice).

BIIM0219U-733437-7/20

8 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

What does it mean for investors? Climate change has

been shown to pose significant financial challenges,

as well as potential opportunities. A study from The

Economist Intelligence Unit (EIU) in 2015 pegged the

average expected loss from climate change to the total

global stock of manageable financial assets at $4.2

trillion through the end of the century — roughly equal to

Japan’s GDP. And a faster pace of global warming could

significantly inflate the damage, especially when lower

rates are used to discount future losses into present

value. See the EIU’s 2015 paper, The cost of inaction:

recognizing the value at risk from climate change.

We believe company disclosure on climate change

strategy and performance can meaningfully impact the

companies in which we invest, particularly those that

face a material climate risk. See BlackRock’s Adapting

portfolios to climate change of 2016 for details.

The level of disclosure has been improving over the past

few years, but there is still little scrutiny on the quality of

the disclosure. Existing data providers do not yet oer

a holistic assessment of this quality. BSI developed a

proprietary climate risk disclosure indicator to fill the

gap. The indicator provides a standardized disclosure

score for North American and European energy and

utility companies that BlackRock has engaged with since

2017. The score is based on a company’s governance,

strategy and targets in regard to climate risk disclosure.

We incorporated the indicator into a new low-carbon

transition framework in an eort to:

1 gain forward-looking insights into a company’s

long-term performance;

2 leverage insights based on our engagements with

the largest carbon emitters in our holdings; and

3 enhance our ongoing engagement with companies

most exposed to climate-related risk.

We provide details of this framework on page 11.

Consensus is limited when it comes to which ESG issues

and information are material. Universally accepted

reporting standards are still lacking, despite the eorts

of standard-setting organizations. Part of the problem:

too many standard setters. Company-level ESG ratings

from dierent rating agencies can vary greatly due to

dierences in methodologies. As a result, investors need

to undertake their own due diligence to understand

the ESG rating agency’s process and methodology.

To be sure, ESG scores oer valuable insight about an

issuer. Yet the top-line ESG score is an amalgamation

of measures — think gender pay gap, pollution, board

structure — that came together over time under the

“ESG” label. A lot of granularity, and critical insight,

can be hidden below.

The opportunity in sustainable investing is to recognize

and exploit the utility of headline ESG scores for eorts

like portfolio building blocks, while also going below

the headline to explore the insights that more granular

component data can provide. Progress on the “E” front

illustrates this point:

Environmental risks are increasing in prominence and

impact. Three of the top-five risks deemed most likely

to occur over the next 10 years are environmental in

nature, according to the World Economic Forum’s

Global Risks Report 2018. Extreme weather events

ranked first, natural disasters second, and failure of

climate change mitigation and adaption came in fifth.

Environmental risks also account for four of the five

risks expected to have the biggest impact over the

next 10 years, the World Economic Forum found.

Last year alone brought massive hurricane damage

on the East Coast of the U.S. and wildfires on the

West Coast; flooding and mudslides in Japan; and

a 7.5 magnitude earthquake and coincident tsunami

in Indonesia — to name just a few.

Beyond headline ESG scores

We explain how it is necessary to go deeper than headline ESG metrics to drive

innovative research in sustainable investing and generate alpha insights.

BIIM0219U-733437-8/20

9 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Improving the data

With the growing interest in sustainable investing, data

providers have increased their eorts in gathering and

reporting varied ESG indicators. For example, MSCI,

an ESG data provider, has boosted the number of

companies under its coverage more than fourfold

over the past decade — and today reports on more

than twice as many key performance indicators (KPIs).

See the Broader coverage chart.

However, the lack of accepted data-reporting standards

means investors cannot readily compare or combine

insights across providers. This limits the ability to fully

harness the potential of ESG information. We view the

remaining data deficiencies as an opportunity. We

have created a customized database that combines

data across many ESG sources, aording us expanded

coverage across companies, a richer description of each

company across KPIs, and a deeper history of ESG data.

This allows us to develop and test investment ideas

based on our own sustainable insights by building

on the diverse KPI measures we believe are material.

The early history of ESG data providers has roots

in small companies serving a limited investor base.

Over time, these small firms have been acquired and

resourced to grow beyond their modest origins to cover

more companies and markets. The result is a historical

database with good coverage of the present but

patchy coverage in older periods, making historical

analysis challenging.

This lack of historical data is an impediment, particularly

the gaps in granular level data points such as renewable

energy use, corruption management and labor

management scores that aggregate to overall ESG

scores. In looking through the historical data, we

noticed the missing ESG data was not absent because

companies did not report, but because the companies

simply were not covered by the data providers. We

approached this missing data challenge with the

hypothesis that gaps in historical ESG data could

be estimated given enough other data from similar

companies. We apply a statistical method that estimates

data missing from older ESG datasets in an eort to

address the gaps.

The challenge of estimating missing data cuts across

industries. Consider the example of Netflix. The media-

services provider started a competition in 2006 for any

researcher that could develop an ecient approach to

estimating missing data in the company’s broad movie-

rating dataset. Solutions to these types of challenges

have become more popular (and robust) in recent

years thanks to improvements in machine learning and

big-data techniques. We draw on one such method,

called generalized low rank modeling (GLRM), to help

us estimate the missing data in big sets of ESG data.

This approach helped us discover patterns in ESG data

that persisted through time. Why is this important?

It gives us confidence in estimating missing data.

We believe the ability to compare companies across a

particular ESG metric is important in explaining relative

performance. The estimation of missing ESG values with

GLRM provides a richer set of historical ESG data that

can be used to compare companies across the market —

or to analyze the trends of a specific company over the

course of time.

Other early research by BlackRock includes applying

cutting-edge physical climate models to assess risks to

assets in specific locations — from flooding, wildfires and

other weather events. We plan to detail this work in an

upcoming publication.

Broader coverage

ESG reporting by MSCI ACWI companies, 2009 and 2017

2009

33.8%

66.2%

2017

41.7%

58.3%

Reported

Missing

vs.

132,175 229,294

data points

reported

Sources: BlackRock Sustainable Investing and BlackRock Investment Institute, with

data from MSCI, December 2018. Notes: We consider all 150 key metrics used by

MSCI in its ESG corporate ratings system. A company reporting a given key metric at

least once in a given year is considered one data point. The total number of potential

data points are calculated by multiplying the number of companies in the MSCI ACWI

Index (2,607 in 2009 and 2,622 in 2017) by 150. The green portion of each ring

shows the share of those data points that were actually reported by companies.

BIIM0219U-733437-9/20

10 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Differentiating insights

We assess companies across each of the five pillars by

distilling over 200 individual key performance indicators

— from both external and proprietary BlackRock data

sources — into a single value. This process is based on

a qualitative assessment of the data and quantitative

testing to evaluate the robustness of our calculations.

Once pillar assessments are made for each company,

they are combined into a single score based on the

industry in which that company functions. The relative

weighting of a company’s performance across the

five pillars will depend on what we believe to be most

financially relevant for its industry. The framework

draws from the Sustainability Accounting Standards

Board (SASB) sector-specific standards and BlackRock’s

own analysis to determine which issues are most

financially material for each industry. For example,

health care companies are primarily evaluated relative

to their energy, water and waste management,

whereas transportation companies are evaluated on

their greenhouse gas emissions and carbon-ecient

technology exposure.

We looked at our transition readiness assessment versus

environmental and headline ESG scores published by

popular data providers and found a positive but low

correlation to both. This implies it may be capturing

new — and potentially dierentiating — financial insights

relative to existing data sources.

Putting data to work

An example of some of the deep work being done

to go beyond headline ESG scores is seen in our

analysis of companies’ readiness to function in a

low-carbon society.

The transition to a low-carbon economy refers to

the global shift to a society that is more e cient in

producing goods and services, and less reliant on

carbon dioxide (CO2) emissions. We see this transition

creating risks and opportunities for companies, and

creating winners and losers in the process.

The BlackRock Sustainable Investing (BSI) team has

performed a transition readiness analysis to help assess

the potential financial impact. The approach looks at

how well positioned companies are to both maximize

the potential opportunities and minimize the risks

associated with the transition to a low-carbon economy.

We plan to provide further details on this approach

in an upcoming academic paper.

The transition readiness of a company is based on its

exposure and management to five financially material

transition characteristics, or “investment pillars.” The

pillars are categorized by a company’s core business

involvement and natural resource management. See

the Transition ready graphic below for descriptions

of each pillar.

Transition ready

Five pillars of BlackRock’s transition readiness assessment process

Sources: BlackRock Sustainable Investing and BlackRock Investment Institute, December 2018.

Note: The table is for illustrative purposes only.

Core business involvement Natural resource management

Energy

production:

Carbon-efficient

technology:

Energy

management:

Water

management:

Waste

management:

Historical direct

emissions as well as

their future potential

emissions through

fossil fuel reserves.

Research and

development, current

revenue and forward-

looking strategy

in solutions across

renewable energy,

energy efficiency,

carbon-efficient

transportation,

green building

and sustainable

agriculture.

Historical indirect

emissions through

energy purchased

as well as company

strategy to manage

future energy

consumption.

Water efficiency as

well as the projected

stress and shortages

in the company’s

water supply.

Waste production,

including hazardous

and non-hazardous

waste, as well as the

company’s strategy

to reduce operational

and product-related

waste.

BIIM0219U-733437-10/20

11 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Putting transition readiness to the test

The goal of a transition-ready investment approach:

directing capital to companies best positioned to

navigate the global transition to a low-carbon economy.

Can this help deliver competitive long-term financial

returns relative to traditional benchmarks? We put

our idea to the test within a hypothetical equity

portfolio. The analysis used a portfolio invested in

non-U.S. developed market stocks from 2010 to 2018.

Going industry by industry, we increased exposure to

companies with high transition readiness assessments

versus their low-performing peers. This hypothetical

portfolio had an annual tracking error of 100 basis points

relative to the broad benchmark, the MSCI World ex-U.S.

Index. The aim was to determine if a focus on transition

readiness might have improved an investor’s historical

risk-adjusted return over that time period.

What we found: Overweighting companies with better

transition readiness characteristics, and underweighting

their less-prepared peers, resulted in outperformance

of our hypothetical portfolio versus the benchmark

index. An analysis using the MSCI USA Index yielded a

similar result. Given our view that the trends driving the

transition are only set to accelerate, we see reason to

envision further upside potential in the future.

A win-win

Regulatory action and technological innovation are the

two primary drivers of the transition to a low-carbon

economy. This is fueled in part by growing recognition

of the risks posed by climate change.

On the regulatory front, the number of climate laws

passed globally has doubled every five years since 1997,

according to a 2015 study from leading climate and

governmental organizations that looked at legislation

in 99 countries. The world has adopted clean energy far

faster than experts expected, and countries have moved

aggressively in the past few years to reach their targets.

Within technological innovation, price reductions

and eciency improvements have accelerated the

deployment of carbon-ecient technologies to replace

existing carbon-emitting activities. We see these forces

advancing the transition to a low-carbon economy.

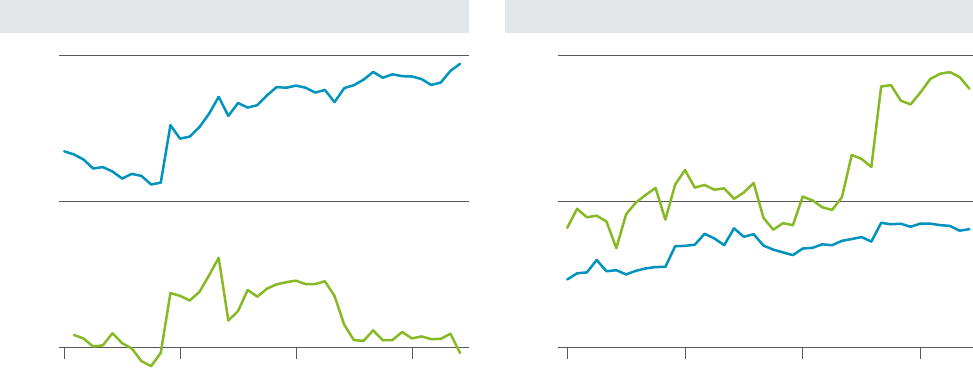

The upshot: Beyond the potential financial uplift, a

transition-ready approach is also designed to provide

better environmental outcomes relative to standard

benchmarks. Returning to our hypothetical equity

portfolio, we find a focus on transition readiness showed

a 50% reduction in emissions intensity and 30% increase

in exposure to clean technology relative to the standard

benchmark. See the Environmental validation chart.

Environmental validation

Environmental metrics of a hypothetical “transition ready” equity index, 2015–2018

Emissions intensity Clean tech exposure

100

150

200

Benchmark

Hypothetical portfolio

2018201720162015

30

45

60

2018201720162015

Benchmark

Hypothetical portfolio

Metric tons CO2/$ million sales

Index (0–100 scale)

Past performance is no guarantee of current or future results. It is not possible to invest directly in an index. Sources: BlackRock Sustainable Investing and BlackRock

Investment Institute, with data from MSCI and Sustainalytics, December 2018. Notes: The chart shows the emissions intensity and exposure to clean technology of a hypothetical

“transition ready” equity portfolio that is based on the MSCI World ex-U.S. Index. The hypothetical portfolio is designed to maximize BlackRock’s “transition ready” signal while

keeping within an annual tracking error of 100 basis points. Emissions intensity refers to MSCI-defined direct (Scope 1) and indirect (Scope 2) greenhouse gas emissions

normalized by annual sales. Clean tech exposure is represented by exposure to clean tech revenue as assessed by Sustainalytics, on a 0-100 scale (from the worst to the best).

BIIM0219U-733437-11/20

12 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Governance insights in Japan

We believe there are important links between “G”

issues and company performance. And yet governance

issues are notoriously hard to measure in a tangible way

— both because disclosure is imperfect and because

governance issues are often regionally dependent.

This underscores the importance of having boots on

the ground with local expertise.

We highlight Japan as an example. Many existing

strategies that aim to use “G” to mitigate risks and/or

improve performance invest primarily in smaller firms.

They tend to take a “hands-on” approach by having

portfolio managers play an active engagement role

with a company’s management committee or through

consultation. Headline ESG ratings do not provide

a holistic view of these companies given a lack of

standardization and the idiosyncracies of local

business environments.

We see an opportunity to focus on large Japanese

firms with strong governance and long-term corporate

strategies. We believe such companies have the

potential to prevail over business cycles, a trend that

could positively accrue to long-run performance.

BlackRock’s Investment Stewardship team in Japan

started internally scoring companies based on

their engagement outcomes. The goal is to make

more informed voting decisions and enhance the

eectiveness of ongoing engagement work. These

scores provide a gauge of each company’s commitment

to its long-term corporate strategy, its quality of

management, capital allocation eciency, sound KPI

procedures, and stakeholder relationships. We draw

on these insights in the portfolio construction process.

Read more on stewardship on page 15.

ESG in the mining industry

Mining is a business known to create noise pollution and

physical disruption, making responsible practices all the

more critical. The mining industry touches every aspect

of ESG, as shown in the Deep roots in ESG chart, and

is important to us as investors in the sector. Yet ESG-

related metrics on miners can be highly subjective and

hard to quantify.

An ESG working group within our natural resources

investment team looks into data alternatives, including

an in-house eort to develop more reliable information.

We are also tracking initiatives to better align mining

companies with sustainable outcomes and integrate

financial and non-financial reporting in areas like ESG.

In the meantime, company managements are acutely

aware that little is made of a job well done in mining,

but any missteps receive intense scrutiny and can have

catastrophic results. This brings heightened attention

to best practices and makes a focus on all aspects of

ESG critical.

Social license and government partnerships are crucial

to avoiding blow-ups, and it’s imperative that investors

have robust means to assess and monitor companies on

these and all dimensions of ESG.

Deep roots in ESG

Role of E, S and G in the mining industry

Source: BlackRock Investment Institute, December 2018. Notes: The table shows the

three ESG pillars and relevance and application in the mining industry.

Environmental

Impact assessment — site clearance,

water courses, road diversions

Monitoring

Rehabilitation

Social

Relocation

Social licenses

Relations — governments, ministers,

community

Mining code — fiscal stability,

sharing profits (tax, royalty)

Permitting

Governance

Sustainability

Health and safety

Security

Employee training

“The external data was patchy, often

outdated and based on global versus

local dynamics material to Japan.

We wanted a means to measure a

company’s leadership at the board and

management levels — and to capture

our own unique perspective.

”

Akitsugu Era — Head of BlackRock’s

Investment Stewardship team in Japan

BIIM0219U-733437-12/20

13 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Sustainable sovereigns

Country weights: ESG vs. standard EMD benchmark, 2018

0

2

4

6%

StandardESG

ChinaUruguayPolandPanamaIndonesiaMexicoHungary

Sources: BlackRock Investment Institute, with data from J.P. Morgan, December 2018.

Notes: The chart shows country weights in the JESG EMBI Global Index versus its

standard counterpart: the JPMorgan EMBI Global Diversified Index, as of December 20,

2018. The countries with the six largest weights in the JESG EMBI Global are shown,

plus China, the country with the largest weighting difference between the two indexes.

ESG in EM

ESG is becoming a critical input in the EM investment

process, helping to identify risks that tend to be more

prevalent than in developed economies. BlackRock’s May

2018 paper Sustainable investing: a ‘why not’ moment

oers details. For example, shareholder protections

tend to be weaker, issuers have a poorer track record

of paying down debt, environmental standards tend

to be more lax, and corruption more prevalent.

These markets were once plagued by inconsistent

standards and disclosure of data, but the quality and

coverage of reported EM data have vastly improved

over the years. In particular, new sources of high-

frequency data — such as ESG data provider RepRisk’s

data on controversies — can fill gaps and help enhance

traditional ESG metrics. This helps address the issue

of timing lag — one of the perennial challenges in ESG

investing. And new computational techniques can

help make up for data deficiencies. We have been

exploring the use of algorithms that analyze and

score the content of sustainability-related media in

real time — and multiple languages.

We have partnered with J.P. Morgan to support the

launch of a suite of new ESG EM debt indexes to help

fill a void of ESG EM debt benchmarks in the market.

Key characteristics of the new indexes include:

• Country exposures are reweighted based on

ESG scores.

• The bottom ESG quintile of issuers is excluded.

• Green bonds receive an outsized index weight.

• Issuers deriving any revenues from weapons,

thermal coal or tobacco are excluded.

These new indexes combine information from multiple

sources, including Sustainalytics, RepRisk and the

Climate Bond Initiative. The Sustainable sovereigns chart

shows country weights in the new JESG EMBI Global

Index versus its standard counterpart.

The ESG tilt results in some meaningful changes

in country weights relative to standard EM debt

benchmarks. The most notable poor ESG performer

— China — sees its index weight reduced by roughly

two-thirds. Leading issuers such as Hungary and Poland

see big uplifts in their index weight thanks to relatively

strong ESG performance. The new index (JESG EMBI

Global) carries a slightly lower yield than its parent

but is designed to deliver similar risk-adjusted returns.

See page 11 of the May 2018 paper for details.

The new ESG indexes also show higher credit quality than

their baseline indexes. J.P. Morgan estimates a single-

notch rating upgrade to just 20% of the JESG EMBI would

take it into investment grade (IG) territory. By contrast,

80% of the parent index constituents would need to be

upgraded for it to become IG. Caveats apply: Future

performance may dier. The quality bias of ESG indexes

means they may underperform in risk-on periods. Yet

this quality can help provide insulation in downturns.

“ESG information has been our primary tool for evaluating qualitative risk when appraising the

standard credit rating of a company. Our inclusion of material ESG metrics in the investment

process has evolved throughout the years as more data metrics and indicators of their materiality

have surfaced.

”

Jack Deino — Head of BlackRock’s Emerging Markets Corporate Debt Team

BIIM0219U-733437-13/20

14 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

More and more investors are looking to integrate

sustainability-related insights and data into their

traditional investment processes. A 2018 BlackRock

study of global insurance companies with almost

$8 trillion in assets under management pointed to

the increasing relevance of ESG in how they invest. A

hefty majority (83%) of insurers indicated that an ESG

investment policy was important to their firm, with 80%

already having one in place or planning to adopt one

within the next year.

A separate annual survey by BlackRock, conducted

in late 2018, found that increasing emphasis on ESG

or impact investing was the most significant focus for

institutional asset owners in the EMEA region (Europe,

Middle East and Africa) as they looked to rebalance

their equity portfolios heading into the new year.

Similarly, a 2018 State Street Global Advisors survey of

475 global institutional investors in the U.S., Europe and

Asia Pacific found that 44% were moving toward deeper

integration of ESG into research and security selection.

Of those investors, 14% said they had fully integrated

ESG into their investment processes.

The challenge: The industry faces a lot of questions

about what ESG integration means in practice for

asset owners, insurers and asset managers. There is

no one standard definition or approach. Some define

ESG integration as adding ESG metrics to investment

analysis; others claim ESG integration occurs at

the strategy level and boils down to the number

of sustainable strategies they oer. The breadth

of industry definitions is stoking confusion.

We draw a clear distinction between dedicated

sustainable investing products and the process of

integrating sustainability-related data or insights into

existing investment processes. ESG integration is about

making research, data and insights available to all of our

portfolio managers, and working with them to identify

potential process enhancements across all investment

activities. Our view is that material ESG insights have

the potential to augment traditional investment

processes, regardless of whether or not a strategy

has a sustainable mandate.

What this means: ESG integration centers on material

sustainability-related information as part of the total mix

of economic and financial indicators associated with

an investment — whether used in the research and due

diligence phase, or in actively monitoring portfolios

later in their lifecycle. ESG integration is not only about

increasing the quantity of information sources available

to portfolio managers, but also identifying information

that is additive to the investment process, whether those

insights are intended to mitigate risks or contribute to

long-term outperformance. The ESG considerations that

are material will vary by investment style, sector/industry,

market trends, and client objectives. (Read more on ESG

data progress and improvements on page 10.)

The quality of data is critical in this process. This is why

we see today’s data deficiencies as an opportunity, rather

than a limitation. Our eorts to go beyond headline

scores and dig deeper into ESG data (pages 9–13) help

propel our integration eorts. We believe more granular

insights can help identify market mispricings and

potentially enhance risk-adjusted returns over time.

ESG integration

There is no one-size-fits-all approach to ESG integration. We see it as using research, data

and insights to drive potential process enhancements across all investment activities.

“Integrating ESG metrics into a cash portfolio can be additive over the long run, despite our highly

restrictive investment universe and the relatively short maturities of cash investments. Companies that

incorporate sustainable practices into their business tend to have lower capital costs, and can be less

susceptible to operational risks. This can ultimately help improve the return profile of an investment.

”

Rich Mejzak — Head of Global Portfolio Management for BlackRock’s Cash Management Group

BIIM0219U-733437-14/20

15 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

A purposeful approach

The core elements of BlackRock’s approach to ESG

integration are:

1 driving research and insights to understand how

fast-improving ESG data influence investment

performance; and

2 integrating this eectively across our firm-wide

investment processes to help achieve better

financial outcomes.

ESG integration is not about imposing values on

investment teams, nor does it mean simply applying an

ESG label to existing products. We see it as a holistic

process that can help all of our teams become better

investors. See the Demystifying ESG integration graphic

for our view of what ESG integration is — and is not.

Our approach is governed by senior leadership

and executed by the professionals responsible for

investment decision-making. BlackRock published an

ESG Investment Statement in July 2018. The goal: to

be transparent about how we define responsibilities

and establish governance for this process. We believe

ESG integration applies to all styles of portfolio

management. In alpha-seeking disciplines, it is about

facilitating investment process enhancements owned by

portfolio management teams. In the case of indexing,

ESG-related matters are typically considered during

engagements with portfolio companies.

Demystifying ESG integration

BlackRock’s approach to ESG integration

Sources: BlackRock Sustainable Investing and BlackRock Investment Institute, December 2018.

Note: The table is for illustrative purposes only.

ESG integration is: ... and is NOT:

Arming portfolio managers with tools and

information to identify risks and opportunities

within portfolios

A values-based exercise

Enhancing the investment process and

implementing this across all our portfolios

Simply developing ESG versions of existing

products while leaving processes unchanged

Making investment decisions that take financially

material ESG information into account

Addressing stakeholder concerns by applying

exclusionary screens based on immaterial ESG

information

Stewards of capital

Those engagements are managed by our global

Investment Stewardship team and seen as a key

component of our mission to create better financial

futures for our clients. BlackRock believes in using

its voice as an investor, through direct engagement

and proxy voting. Companies should be encouraged

to adopt sound business practices consistent with

delivering sustainable long-term financial returns.

BlackRock’s Investment Stewardship team engages with

some 1,500 companies a year on material ESG issues

we believe aect our clients’ long-term economic

interests. When companies demonstrate poor

management of material ESG issues, we engage

constructively and privately to provide feedback and

discuss how the company’s approach may aect its

long-term performance.

Triggers for such discussions may include company

events that could aect shareholder value (e.g., a data

breach) or a concern around company performance

or governance (e.g., lack of board accountability).

Engagement aims to establish an open dialogue to

develop mutual understanding of governance matters.

It helps Investment Stewardship assess the merits of

a company’s approach to its governance and provide

feedback on any company’s practices that, in our

assessment, fall short of operational excellence. See

BlackRock’s The Investment Stewardship Ecosystem.

BIIM0219U-733437-15/20

16 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

One size does not fit all

We recognize there is no one-size-fits-all approach to

ESG integration. The availability and quality of ESG data

used by investment teams depends on factors such

as geography (greater coverage in developed versus

emerging markets), holding period and investing time

horizon. Physical climate risks such as coastal flooding,

for example, tend to compound over time and are more

material for longer-dated real assets than for short-term

assets such as cash.

Processes also vary greatly depending on the type of

investment solution. Case in point: A private equity team

may need to build a template to gather ESG information

on its investments, given the lack of third-party ESG

data on private companies and external fund managers.

Third-party ESG data is more readily available in EM

debt, for example, and could be incorporated into

a team’s credit scorecards and used to complement

internal fundamental analysis.

Ultimately, this diversity of investment approaches

presents an opportunity: We can use it to surface

the best ESG integration practices across a variety of

dimensions and share them across the firm to further

our collective eorts.

We have developed a matrix to help us identify common

characteristics across teams and pinpoint best practices

used to overcome challenges associated with each.

This allows for a deeper understanding of where BSI can

focus its eorts to advance practices that can be shared

firm-wide.

We recognize that, just as with credit ratings, the highest

levels of integration may involve creating proprietary

measures that extend beyond headline ESG scores. The

most eective way to accomplish this is in the context of

the specific investment process and approach.

Ultimately, we see ESG integration as a way of

enhancing the investment process, not a box-ticking

exercise. There is no one-size-fits-all approach. We

believe it needs to be a rigorous, yet flexible process

to reflect the diversity of dierent investment styles

and teams.

“In 2018 BlackRock Real Assets

developed and implemented

a proprietary ESG Investment

Questionnaire, required for all new

acquisitions across our platforms.

This provides a framework to help

identify and collate information on

material ESG risks and opportunities.

”

Teresa O’Flynn — Global Head of BlackRock

Real Assets Sustainable Investing

Team by team

Each of BlackRock’s active investment teams is

responsible for implementing ESG approaches in line

with its investment mandate. BSI acts as a partner to

help ensure consistency across the firm, providing

resources, guidance and best practices. This often takes

what is implicit and makes it explicit, formalizing what

many teams have been doing for years. Each investment

team is required to have a formal ESG integration

statement to underpin its respective approach.

Complementing this team-by-team approach is an internal

benchmarking process designed to measure and monitor

progress firm-wide. Each of BlackRock’s 73 investment

teams had been “baselined” as of late 2018. This includes

the status on ESG integration as well as for the resources,

opportunities and challenges associated with their ESG

integration work. This process will be updated regularly

to provide a diagnostic tool for measuring, managing and

reporting the state of ESG integration across teams to

the firm’s senior investment leadership.

BSI arranges “deep dives” with specific investment

teams to explore more ambitious investment process

improvements based on ESG insights or data. Each

series of deep dives culminates with an internal

symposium, where colleagues present on their key

accomplishments in ESG integration, how new tools

have improved their traditional investment processes,

and highlight and share best practices.

In most cases, these deep dives result in investment

teams creating and integrating proprietary mechanisms

to score securities or assets — measures that extend

well beyond headline ESG scores.

BIIM0219U-733437-16/20

17 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

BL ACK ROC K A ND

SUSTAINABILITY

Sustainability at BlackRock focuses not only on our

investment processes, sustainable investment solutions

and our stewardship of our clients’ assets. It also

involves the operations of BlackRock itself. As an asset

management firm, our objective is to secure better

financial futures for our clients and those they serve.

To achieve this goal, we must ensure the long-term

sustainability of our own firm. We published our mission

statement on sustainability in 2018, outlining our

approach to be an industry leader in how we incorporate

sustainability across the firm.

Governance and board

Our corporate governance framework is governed by

BlackRock’s board of directors and an accountable lead

independent director. Our board regularly reviews our

strategic framework for long-term value creation and

challenges management in executing on it. We believe

our board’s diversity of background and perspective

plays a significant role in its ability to evaluate BlackRock’s

management and operations.

Human impact

As an asset manager, the long-term sustainability of our

firm is heavily dependent on our people. We focus on

fostering a unifying culture; encouraging innovation;

ensuring that we are developing, retaining and recruiting

the best talent; aligning employee incentives and risk-

taking with those of the firm; and incorporating inclusion

and diversity into all levels of our business.

Environmental sustainability

BlackRock’s business model is not carbon intensive,

yet we are committed to managing our impact on the

environment. We approach sustainability in a way that

decouples our growth from our environmental impact.

Our path to sustainability includes measurement and

management of carbon emissions and energy-eciency

goals; consideration of renewable and alternative energy

sources; and disclosure of risks and opportunities around

climate change.

Read more about BlackRock’s approach to sustainability.

Lessons and reflections

BlackRock has dedicated significant resources in a firm-

wide eort to deepen the integration of sustainability-

related insights and data into investment processes

globally. Several initial lessons have emerged. We share

them in an eort to advance the conversation industry-

wide as we improve, test and calibrate our approach:

Setting internal goals and reporting on milestones is

key in helping push forward what is an evolving process.

Producing a clear and transparent diagnostic for senior

investment leaders helps to manage progress. It is also

valuable in identifying areas of strength within certain

teams, so more advanced teams can help others and

collaboratively address common challenges. Finally, it

helps guard against a siloed approach and outcome

whereby all teams work on challenges of ESG integration

independently and at dierent speeds. Following the

initial baselining, we found many teams faced similar

challenges and opportunities in augmenting their

investment processes with material ESG insights.

ESG integration must be viewed as a journey, not a

box-ticking exercise. Training our portfolio managers

in how to make sense of fast-improving ESG data

and insights is an important goal. The alternative of

parachuting ESG “specialists” into investment teams

generates less durable progress. Our teams’ approaches

are dynamic, defined by adaptation and innovation

as new sustainable investing insights and tools arise.

Data and technology tools are crucial. Portfolio

managers need the right data and technology tools to

measure and manage sustainability-related exposures

eectively. BlackRock has been building issuer-level

ESG information into Aladdin, the firm’s investment and

risk-management system, since 2015. Our own portfolio

managers and some clients can use Aladdin to monitor

portfolio risks and help inform investment decisions

based on ESG metrics.

We leverage our technology platform to drive four

objectives of ESG integration: increasing transparency,

mapping exposures, uncovering value and

implementation. We are investing in improving these

data and analytic tools.

BIIM0219U-733437-17/20

18 SUSTAINAB ILITY: T HE FU TURE OF INVESTIN G

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

REL ATED RE SO U RC E S

FROM BLACKROCK

References

Dunn, Jeff, Shaun Fitzgibbons and Lukasz Pomorski, AQR Capital Management, LLC (2017). “Assessing Risk Through

Environmental, Social and Governance Exposures.”

Hoepner, Andreas G. F., Ioannis Oikonomou, Zacharias Sautner, Laura T. Starks and Xiaoyan Zhou (Aug. 10, 2018). “ESG

Shareholder Engagement and Downside Risk.” AFA 2018 paper. Available at SSRN: https://ssrn.com/abstract=2874252 or

http://dx.doi.org/10.2139/ssrn.2874252

Khan, Mozaffar N., George Serafeim and Aaron Yoon (March 2015). “Corporate Sustainability: First Evidence on Materiality.”

Harvard Business School Working Paper, No. 15-073.

Morningstar Research (January 2018). Sustainable Funds U.S. Landscape Report.

Nachmany, Michal, Sam Fankhauser, Jana Davidová, Nick Kingsmill, Tucker Landesman, Hitomi Roppongi, Philip Schleifer, Joana

Setzer, Amelia Sharman, C. Stolle Singleton, Jayaraj Sundaresan and Terry Townshend (2015). “The 2015 Global Climate Legislation

Study, A Review of Climate Change Legislation in 99 Countries, Summary for Policy-makers.” Grantham Research Institute on

Climate Change and the Environment, GLOBE —The Global Legislators Organisation, and the Inter-Parliamentary Union.

State Street Global Advisors (2018). ESG Institutional Investor Survey, “Performing for the Future: ESG’s place in investment

portfolios. Today and tomorrow.”

The Economist Intelligence Unit (2015), “The cost of inaction: Recognising the value at risk from climate change.”

World Economic Forum (2018). The Global Risks Report 2018, 13th Edition.

Adapting portfolios to climate change, September 2016

https://www.blackrock.com/corporate/literature/whitepaper/bii-climate-change-2016-us.pdf

BlackRock ESG Investment Statement, July 2018

https://www.blackrock.com/corporate/literature/publication/blk-esg-investment-statement-web.pdf

BlackRock Mission Statement on Sustainability, 2018

https://www.blackrock.com/corporate/literature/publication/blk-sustainability-mission-statement-web.pdf

BlackRock’s Approach to Sustainability, 2018

https://www.blackrock.com/corporate/responsibility

Exploring ESG: A practitioner’s perspective, June 2016

https://www.blackrock.com/investing/literature/whitepaper/viewpoint-exploring-esg-a-practitioners-perspective-june-2016.pdf

Global Investment Outlook 2019, December 2018

https://www.blackrock.com/investing/literature/whitepaper/bii-2019-investment-outlook.pdf

Sustainable investing: a “why not” moment, May 2018

https://www.blackrock.com/corporate/literature/whitepaper/bii-sustainable-investing-may-2018-us.pdf

The Investment Stewardship Ecosystem, July 2018

https://www.blackrock.com/corporate/literature/whitepaper/viewpoint-investment-stewardship-ecosystem-july-2018.pdf

BIIM0219U-733437-18/20

FOR PUBLIC USE IN THE U.S. ONLY. FOR INSTITUTIONAL, WHOLESALE AND QUALIFIED INVESTORS/CLIENTS ONLY ELSEWHERE.

Important notes: Unless otherwise noted, index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly

in an index. Data for time periods prior to the index inception date is hypothetical and is provided for informational purposes only to indicate historical performance had the index

been available over the relevant time period. Hypothetical data results are based on criteria applied retroactively with the benefit of hindsight and knowledge of factors that may have

positively affected its performance, and cannot account for risk factors that may affect the actual portfolio performance. The index sponsor may make methodology changes from time

to time based on its own policies and procedures. Index methodology is available upon request. Back-tested data is calculated by individual index providers and used in analysis until

live index data is available. This analysis uses back-tested data from MSCI and Thomson Reuters.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be

further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI. There are no assurances that

the hypothetical portfolio’s objectives will be met. Additionally, there are frequently sharp differences between a hypothetical performance record and the actual record subsequently

achieved. Another inherent limitation of these results is that the allocation decisions reflected in the performance record were not made under actual market conditions and, therefore,

cannot completely account for the impact of financial risk in actual portfolio management. The performance shown does not represent any existing portfolio, and as such, is not an

investible product.

General disclosure: This material is prepared by BlackRock and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or

solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 2019 and may change as subsequent conditions vary. The

information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and

are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility

to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical

in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information

in this material is at the sole discretion of the reader. This material is intended for information purposes only and does not constitute investment advice or an offer or solicitation to

purchase or sell in any securities, BlackRock funds or any investment strategy nor shall any securities be offered or sold to any person in any jurisdiction in which an offer, solicitation,

purchase or sale would be unlawful under the securities laws of such jurisdiction. Investment involves risks. Past performance is not a reliable indicator of current or future results and

should not be the sole factor of consideration when selecting a product or strategy.

In the U.S., this material is intended for public distribution. In Canada, this material is intended for permitted clients only. In the EU issued by BlackRock Investment Management

(UK) Limited (authorised and regulated by the Financial Conduct Authority). Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Registered in England No. 2020394. Tel:

020 7743 3000. For your protection, telephone calls are usually recorded. BlackRock is a trading name of BlackRock Investment Management (UK) Limited. This material is for

distribution to Professional Clients (as defined by the FCA Rules) and Qualified Investors and should not be relied upon by any other persons. For qualified investors in Switzerland,

this material shall be exclusively made available to, and directed at, qualified investors as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended.

Issued in the Netherlands by the Amsterdam branch office of BlackRock Investment Management (UK) Limited: Amstelplein 1, 1096 HA Amsterdam, Tel: 020 - 549 5200. In South

Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorised Financial Services provider with the South African Financial Services Board, FSP No.

43288. In Dubai: This information can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is