FEDERAL OMBUDSMAN OF PAKISTAN

A STUDY OF

ORGANIZATION, ROLE, SYSTEMS, PROCEDURES

AND CAUSES OF MAL-ADMINISTRATION AND

MAL-FUNCTIONING OF CENTRAL DIRECTORATE

OF NATIONAL SAVINGS MINISTRY OF FINANCE,

GOVERNMENT OF PAKISTAN

WAFAQI MOHTASIB (OMBUDSMAN)’S SECRETARIAT

36-Constituion Avenue, Islamabad – Pakistan

Ph: +92-51-9213886-7, Fax: +921-51-9217224

www.ombudsman.gov.pk

Table of Contents

Chapters Page No.

Executive Summary

1-40

Chapter 1 Introduction

i. Establishment of Wafaqi Mohtasib Order 1983

ii. Terms of Reference

41

42

43

Chapter 2 Methodology 44

Chapter 3 Role of Savings in An Economy and NSS

A. Significance of CDNS in Mobilizing Private Savings

i. Avenues of Investment for Household or Private Savings

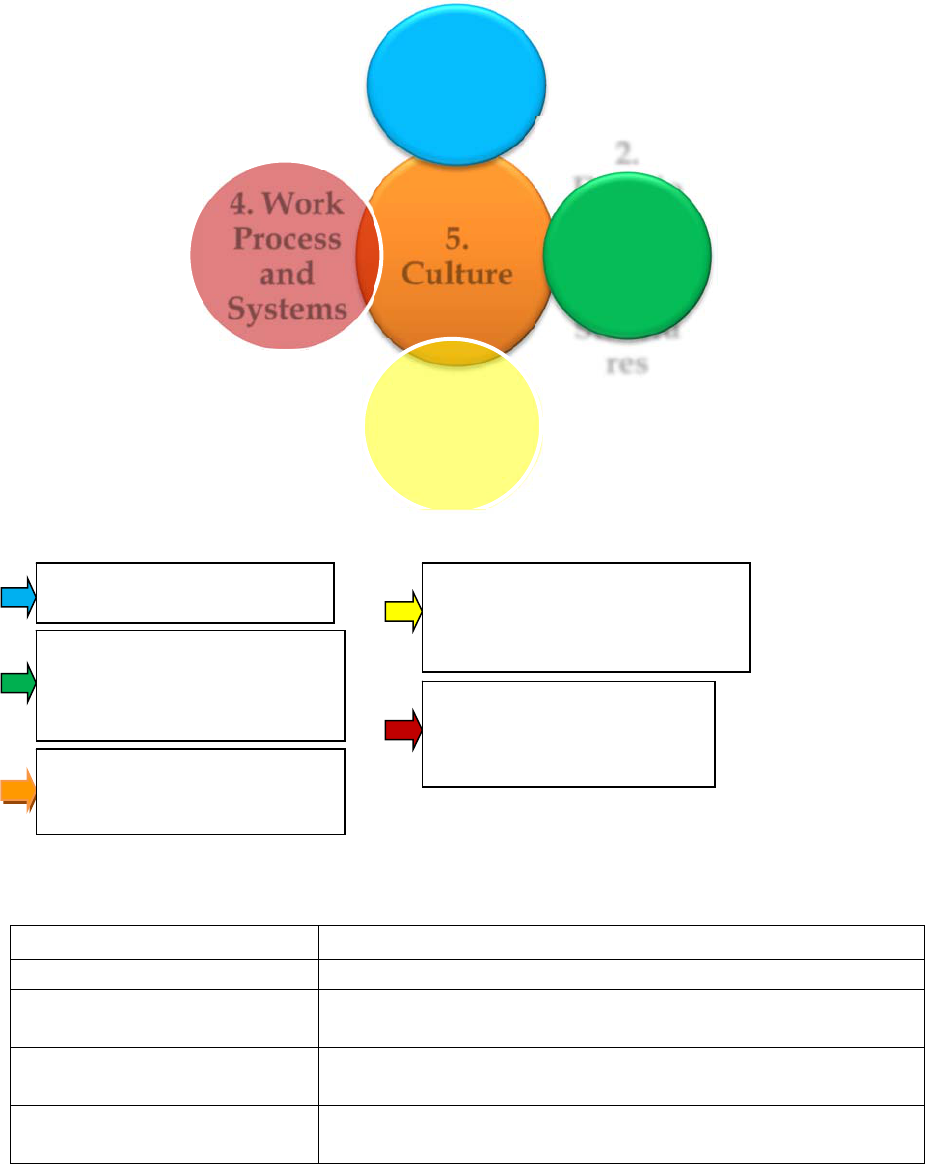

ii. Savings Instruments

iii. Share of Various Savings Schemes

iv. Rate of Return on NSS

v. Performance of NSS

B. Significance of NSS in Deficit Financing & Government Debt

i. NSS and Deficit Financing

ii. NSS and Domestic Debt

iii. NSS and Liquidity Management

iv. NSS and Development of Bond Market

C. Reforms Proposed by DCMC

46

49

49

49

50

52

53

54

54

54

55

55

56

Chapter 4 National Savings in Other Countries

i. United States

ii. United Kingdom

iii. India

iv. Sri Lanka

v. Malaysia

57

57

58

60

62

63

Chapter 5 TOR-1: Study of the organizational set up of CDNS

i. Institutional Growth of CDNS

ii. Vision of CDNS

iii. Mission of CDNS

iv. Core Objectives

v.

Statutory Regime Regulating CDNS and NSS

vi. Structure of CDNS

vii. Functional Hierarchy of CDNS

viii. Administrative Structure of Regional Directorates

ix. Functions of Different Tiers/Offices

x. Indicative Staffing of National Savings Center

xi. Sanctioned Strength of CDNS

65

65

65

66

66

66

67

68

69

69

69

70

ii

Chapters Page No.

Chapter 5

xii. Vacancy Position

xiii. Directorate of Audit and Inspection

xiv. National Savings Treasuries

xv. Data Flow and Reconciliation Process

xvi. Training Arrangements

xvii. Infrastructure of National Savings Centers

xviii. Inflows and Outflows of NSS

xix. Budget of CDNS

xx. Recruitment Rules for Hiring in CDNS

xxi. Computerization of CDNS

xxii. Opening New Account or Encashment or Receiving Profit

xxiii. Scheme-Wise Investors

xxiv. Monthly Transactions

xxv. Competitors of NSOs

xxvi. Number and Nature of Complaints

xxvii. Disciplinary Cases

70

70

71

74

75

76

76

76

77

77

78

79

79

79

80

82

Chapter 6 TOR-2: Institutional, Procedural and Systemic Weaknesses

Which Hinder Efficient Delivery of Service to Clients

TOR-3: To Look into the Causes of Mal-Administration and

Mal-Functioning within Department

Institutional Weaknesses

i. Governance Framework for CDNS

ii. Structure of CDNS

iii. Organizational Culture

iv. Human Resource Management

v. Infrastructure of CDNS

vi. Budgetary Allocations

vii. Audit and Inspection in CDNS

viii. Dormant Cases

ix. Death Cases

x. Other Complaints

xi. Automation in CDNS

xii. Training Institutions

xiii. Cost Structure

xiv. Assigning Annual Target to CDN

83

83

83

85

88

91

95

96

96

99

100

100

100

103

103

103

iii

Chapters Page No.

xv. Capacity to Price NSS Products

xvi. Determining Annual and Future Liabilities

xvii. Reconciliation of Receipts and Repayments

xviii. Inventorying

xix. Financial Statements of CDNS

104

104

105

105

105

Chapter 7 Summary of Findings 106

Chapter 8 TOR-4: Recommendations

Conclusion

115

155

Tables

Table 1

Table 2

Table 3

Table 4

Table 5

Table 6

Table 7

Table 8

Table 9

Table 10

Table 11

Table 12

Table 13

Table 14

Table 15

Table 16

Table 17

Table 18

Table 19

Table 20

Table 21

Table 22

Table 23

Table 24

Table 25

Table 26

Table 27

Country Comparison of National Savings as % of GDP

Structure of Savings and Investment

Trends and Structure of Financial Savings in Pakistan

Profile of Selected NSS Instruments

Share of Various NSS Instruments in Outstanding NSS Stock

Return on Bank Deposits, Government Securities and NSS

National Savings Schemes Indicators

Comparison of NSOs in Select Countries

Province/Region-wise National Savings Centers

Categorization of National Savings Centers

Indicative Staffing of CDNS

Sanctioned Strength of CDNS excluding DIA

Sanctioned Strength of Zonal and Regional Accounts

Vacancy Position of CDNS

Trend of Flows from NSS

Annual Budget of CDNS

Rules of Recruitment for Appointment

Scheme Wise Investors as on 30.6.2015

Average Monthly Transactions

Matrix of Banks Services

Number of Banks and Branches

Number and Nature of Complaints

Disciplinary Action

Types of Internal Linking Mechanism

Passive-Defensive Culture

Paradigms

Pros and Cons of External Hiring

47

47

48

51

51

52

55

64

68

69

70

72

73

74

76

77

77

79

80

80

81

81

82

87

90

91

94

iv

Chapters Page No.

Table 28

Table 29

Table 30

Table 31

Summary of Audit Pendency as on 30.9.2015

Region and NSC-wise Audit Pendency as on 30.9.2015

Recoverable Amount as on 30.9.2015

Proposed Rules of Recruitment

97

98

99

134

Figures

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Figure 11

Figure 12

Figure 13

Figure 14

Figure 15

Figure 16

Figure 17

Figure 18

Figure 19

Figure 20

Structure of CDNS

Organizational Hierarchy of CDNS

Administrative Structure of RDNS

Data Flow and Reconciliation Process

Flow Chart for New Account Opening in NSC

Flow Chart for Profit Payment at NSC

Effective Organization Design

Strategies for Strengthening Organizational Culture

Organizational Culture Types

Why Technology is Difficult in Government

Proposed Organizational Structure of Pakistan Savings

Proposed Directorate of Product Development and Marketing

Proposed Structure of Directorate of Operations

Proposed Structure of National Savings Center Category A &

Proposed Structure of National Savings Center Category C & D

Proposed Directorate of Human Resource Management & Security

Proposed Directorate of Finance and Accounts

Proposed Directorate of Legal Services

Proposed Directorate of Audit and Inspection

Proposed Directorate of Information Technology & MIS

67

68

69

75

78

79

87

88

90

102

125

126

126

127

127

128

129

129

130

130

Appendix-1

Appendix-2

Appendix-3

Appendix-4

Appendix-5

Appendix-6

Appendix-7

Appendix-8

Appendix-9

Appendix-10

Notification of Federal Ombudsman Secretariat

NSS Rates Formula Devised by IMF

DCMC Recommendations Regarding NSS

Functions of Different Tiers/Offices of CDNS

Functions of National Savings Treasuries

Training Courses Conducted by NS Training Institutions

Posts Approved in PC-I for Phase II Automation

Audit Paras and Reconciliation Pending with Post Office

Audit Para Against CDNS for FY2014

Rules of Recruitment 2014 for CDNS

157

159

160

161

165

166

169

170

172

176

Page1of176

Executive Summary

1

The Wafaqi Mohtasib (Federal Ombudsman) was pleased to constitute a

Committee to undertake an in-depth study into mal-functioning and mal-

administration in the Central Directorate of National Savings under

Establishment of the Office of Wafaqi Mohtasib (Federal Ombudsman)’s Order,

1983, in July 2015 after receipt of large number of complaints and persistent stories

appearing in the print media (See Chapter 1).

2. The Committee held six meetings from August to December, 2015. The

Committee was briefed extensively by the officers of the Ministry of Finance as well

as the CDNS. The Committee was further benefitted by previous studies about

CDNS in addition to comprehensive feedback given by the employees of CDNS.

The Committee also paid a surprise visit to model branch of CDNS. Chapter 2

explains the methodology the Committee pursued while doing this study.

3. National Savings, comprising private savings (household), corporate

savings (retained earnings) and public savings (government’s revenues minus

expenditures), is extremely vital for economic growth and sustainable

development as countries invest their savings in development and growth.

Although, there had been earlier savings schemes, such as Priscilla Wakefield’s

Female Benefit Club in Tottenham, in 1798, it is generally recognized that the

savings bank movement began in Scotland, in May 1810 when Revd Henry Duncan

first opened the doors to his parish bank in Ruthwell, Dumfriesshire, Scotland. His

business model was based on “Set up a bank. Open it from 1.00 - 2.00 p.m. once a

week. Do not allow customers to deposit more than £20 a year. Fine them if they do

not deposit regularly.” Celebrating the World Savings Day on October 31 every

year since 1924, following the 1st International Savings Bank Congress (World

Society of Savings Banks) in Milano, Italy, amplifies the significance of savings.

4. The efforts of mobilizing national savings in the sub-continent dates back

to 1873 when the Government Savings Bank Act, 1873 was promulgated. The

British Government launched it as a measure to muster funds from its colonies to

finance War expenditures (World Wars I and II) through Post Office Cash

Certificates in 1916 and Post Office Defense Savings Certificates in 1941-42. For

details, see Chapter 3.

1

Report has been drafted by the Chairman of the Committee and has been endorsed by the Members

of the Committee.

Page2of176

5. To institutionalize the national savings, National Savings Bureau was

established in 1944 as an Attached Department of the Ministry of Finance headed

by National Savings Commissioner with the status of a Joint Secretary which was

mainly concerned with the policy and planning matters relating to Savings

Schemes. Post-independence in 1947, the Bureau was renamed as “Pakistan Savings

Central Bureau” headed by Central National Savings Officer with the status of

Under Secretary to the Government of Pakistan with far less freedom. It was again

renamed as Central Directorate of National Savings (CDNS) in 1953 with the status

of an “Attached Department” of the Ministry of Finance and was made responsible

for all policy matters and execution of various National Savings Schemes. For

details, see Chapter 5.

6. The avenues available for investment for household or private savings in

Pakistan include: National Saving Schemes, Bank Deposits (Fixed Term, Savings

Deposits), Mutual Funds, Life Insurance Policies, Business Equity and Corporate

Bonds---both through acquisition of securities listed on the stock exchange as well

as direct investment in other private businesses, Real Estate, Contractual Retirement

Savings---Individual interests in provident, gratuity and pension funds, Money

Accounts for investment in PIBs and T-Bills.

7. CDNS currently offers three types of products for savings: (i) Fixed Income

Guaranteed Products: Regular Income Certificates, Saving Accounts, Special

Savings Accounts, Defense Savings Certificates, Special Savings Certificates; (ii)

Index Linked Products (with capital guarantees): None; (iii) Products with return

wholly or partly in the form of prizes: Prize Bonds; and (iv) Welfare Products:

Behbood Savings Certificates, Pensioners Benefit Accounts. These saving

instruments are non-tradable long-term bonds having different maturity profiles,

ranging from 3 years to 10 years, with varying interest rates and other features

(Table 4).

8. The share of Defense Saving Certificates has decreased from 67.7 percent

in 1971 to 12.4 percent of the total NSS portfolio of Rs 2,417 billion net of Prize

Bonds in FY2015. Likewise, share of Regular Income Certificates has declined from

26.8 percent in 2000 to 15.7 percent in FY2015. Concomitantly, share of Behbood

Saving Certificates has increased to 26 percent and that of Pensioners’ Benefit

Accounts share increased to 8.6 percent. The share of BSC and PBA is likely to

increase further as the investment ceiling has been enhanced from Rs 3 million to Rs

4 million effective from July 1, 2015 (Table 5). Average rate of return on NSS peaked

to 18 percent in FY1996 and has now declined to 8.29 percent in December 2015

Page3of176

(Table 6). The rate of return is fixed closer to market except welfare based products

since FY2000 following an agreement with the IMF (Appendix 2). The Government

moved from annual adjustment of rate of return to bi-annual to quarterly and now

bi-monthly on the basis of immediate first auction of PIBs and T-Bills post-

announcement of policy rate by the State Bank of Pakistan.

9. Mobilization of funds through NSS surged from Rs 132 billion in 1990 to

Rs 634 billion in 2000, growing at a compound average growth rate of 17 percent,

reaching to Rs 2,417 billion in FY2015, net of prize bonds the outstanding stock of

which is Rs 522.5 billion. Accumulated investment in NSS rose from 3.75 percent in

1980 to 18.3 percent of GDP in FY2001 which has declined to 10.7 percent of GDP in

FY2015. As against this, accumulated deposits in the banking sector declined from

37 percent of GDP in FY2005 to 29 percent in FY2009 before rising to 33.4 percent of

GDP in FY2015. Share of NSS net flows in deficit financing moved from 31.8 percent

in 1990 to 74 percent in FY1999 and declined to 17.9 percent in 2015. Share of NSS in

domestic debt surged to 37.5 percent in 1990 which peaked to 48.6 percent in 2000

has now declined to 24.1 percent (Table 7).

10. However, the savings to GDP ratio in Pakistan has been quite low as it

declined from 20.8 percent in FY2003 to 11 percent of GDP in FY2008 before

demonstrating some improvement from FY2009 reaching 14.1 percent of GDP in

FY2015 (Table 1). Concurrently, domestic savings declined from 18.1 percent in

FY2002 to 7.8 percent of GDP in FY2013 before reaching 8.0 percent in FY2015 (Table

2). A cross-countries comparison revealed that Pakistan’s national savings rate has

remained the lowest not only vis-à-vis selected developed countries but also its peer

group: Bangladesh (29.5%), Canada (21%), China (50%), France (20%), Germany

(26%), India (30.1%), Italy (19%), Japan (22%), Sri Lanka (25.8%) and United States

(18%) in FY2013 (Table 1).

11. Consequently, Pakistan’s savings-investment gap rose from 2.1 in 1973 to

8.2 percent of GDP in FY2008. It has dropped to 1.3 percent of GDP in FY2014 on

the back of deteriorating investment from 19 percent in FY1981 to 15 percent of

GDP in FY2014 (Table 2). Similarly, financial savings nose-dived to 3.0 percent of

GDP in FY2009 from 7.6 percent in FY2005. It increased to 6.8 percent of GDP in

FY2012 and has again dipped to 5.9 percent of GDP in FY2015 (Table 3).

12. While increasing savings-investment gap underscore Pakistan’s

dependence on foreign savings, low savings rate is constraining economic growth

and development in the country. It implies low level of investment from national

Page4of176

savings in infrastructure, water reservoirs and social sectors, slow upward

movement in per capita income, less job opportunities and rising poverty. The

country is left with no other option but to seek foreign assistance to finance

infrastructure and social sectors.

13. A comparison of National Savings Organizations of Pakistan, India, Sri

Lanka, Malaysia, United Kingdom and United States including their management

structure, products they offer and current volume (Table 8) reflects that these

countries have moved far ahead of Pakistan in modernizing the structures of

National Savings Organizations, professionalizing their governance and employing

technology. Generally, the National Savings network in most of these countries is

governed by either Board of Governors or Board of Directors. Even, India is now

moving towards installing ATMs for the savings system. Nonetheless, Pakistan

remained stuck to traditional structures, status and governance of CDNS which it

inherited in 1947 except changing the name from National Savings Bureau to

Central Directorate of National Savings and its management. The controlling

Ministry and the institution itself failed to benefit from the recommendations of

various studies because of intrinsic resistance to change (See Chapter 4).

TOR-1: Study of Organizational Set up of CDNS (For details, see Chapter 5)

14. The core objectives of the CDNS are:

(a) Promoting and mobilizing savings in the country;

(b) Generating funds for financing the budget deficit; and

(c) Providing a system with impeccable integrity, trustable, secure and

enjoys the confidence of the people to channelize their savings for

investment, particularly the small savers, pensioners, widows, etc.

15. CDNS comprises of: (a) Central Directorate of National Savings; (b)

Directorate of Inspection and Accounts; (c) Directorate Legal; (d) Directorate of

Schemes; (e) 7 Zonal Inspection and Accounts Offices and 12 Regional Inspection

and Accounts Offices; (f) 12 Regional Directorates and (g) Training Institute of

National Savings at Islamabad with a Sub-Training Institute at Karachi to perform

various functions (Appendix 4). The organizational structure of CDNS is at Figure 1.

The organizational hierarchy is at Figure 2. The administrative structure of a

Regional Directorate is at Figure 3. The functions of various tiers of CDNS are at

Appendix 4.

Page5of176

15. National Savings Schemes offered by CDNS are sold through a network of

374 National Savings Centers all over the country. However, 237 Tehsils and 6

Agencies of Federally Administered Tribal do not have National Savings Center

(Table 9). The categorization of NSCs is at Table 10 and the indicative staffing

proposed by the CDNS is at Table 11. The National Savings Schemes are regulated

by a stream of laws and rules (Chapter 5, page 66). The sanctioned strength of CDNS

and its directorates as well as NSCs is 4007 (Table 12) and sanctioned strength of

Directorate of Inspection and Accounts including Zonal Inspection and Accounts

Offices is 292 (Table 13). However, 1443 operational positions were vacant at the

time of this study (Table 14) which are now in the process of filling through

Departmental Promotion Committee and Federal Public Service Commission. This

huge vacancy has greatly affected public service delivery of CDNS.

16. There is a regular flow of data from field formations to the Regional

Directorates and CDNS and the process of reconciliation which is reflected at

Figure 4. CDNS has 13 National Savings Treasuries and 3 sub-Treasuries throughout

the country dealing with cash handling (Appendix-5). The training institutions of the

CDNS conduct various training program for new entrants and refresher courses for

in-service employees (Appendix-6).

17. Although, the budget of CDNS has increased from Rs 589 million in

FY2006 to Rs 2,591 million in FY2016, an increase of 340 percent, in nominal

terms. However, 68 percent of this budget is establishment charges leaving 32

percent for operational expenses. Nevertheless, 41% of the operational budget is

meant for rent of various offices leaving a paltry amount for the remaining

operations which is hugely affecting public service delivery, both at the

headquarters as well as retail outlets. It needs to be recognized that during the same

period, the total portfolio of CDNS has increased from Rs 940 billion (inclusive of

Prize Bonds) to Rs 2872 billion, an increase of 205 percent. The total administrative

budget of CDNS is around 0.2 percent of gross inflows and less than 1 percent of

net inflows (Tables 15 and 16). The Recruitment Rules for direct recruitment and

promotions to various positions is at Table 17.

18. The process for opening a new account and encashment of profit or

instruments is reflected at Figures 5 and 6. CDNS currently deals with over 7

million investors/account holders (Table 18). On the average, CDNS network

handles closer to 4 million transactions monthly (Table 19). The competitors of

CDNS are providing far more facilities (Table 20). The geographic reach of

competitors is considerably higher, 374 NSCs vs 10,984 branches (Table 21). The

Page6of176

complaints against NSCs and CDNS are generally in relation to deduction of Zakat

and With-holding Tax, procedural matters, interest rates stamped on back side of

the certificates as these rates change every two months and huge waiting time

besides malpractices (Table 22). The disciplinary action is generally taken against

lower employees and that too, mostly, imposition of minor penalty (Table 23).

TOR 2- To Identify Institutional, Procedural and Systemic Weaknesses

Which Hinder The Efficient Delivery Of Service To The Clients

TOR 3 - To Look into the Causes of Mal-Administration and Mal-

Functioning within the Department (For details, see Chapter 6)

19. The outstanding stock of NSS is approximately Rs 3,000 billion inclusive

of bearer bonds. As of June 30, 2015, the investment in NSS constitutes 9 percent of

GDP, 19.1 percent of domestic debt, 70.1 percent of non-bank borrowings, 18

percent of deficit financing and 25 percent of bank deposits. It clearly reflects that

CDNS is no ordinary organization but is performing a vital role in the financial

sector of Pakistan and the economy since independence.

20. CDNS, as it exists today, does not seem to be a result of planned, systemic

and scientific construction nor serious thinking and strategy. The current

organizational structure has evolved over time as a result of ‘patch-work as and

when needed’ rather than a consequence of any management study or scientific

analysis. Expediencies and deficit financing requirements seem to have been

instrumental in determining the form and status of various Savings Schemes

introduced from time to time without any market survey, financial sector demands

and pricing of the schemes.

21. Apparently, CDNS is not getting due attention and focus of the policy

makers because of perceived captive investors, investment and absence of

strategy to accelerate rate of savings in Pakistan. Good governance of a financial

institution, such as CDNS, requires checks and balances on the power and rights

accorded to it. Besides, behavior in a financial institution is key and focus on right

behviour means a shift from the “hardware” of governance (structures and

processes) to the “software” (people manning the organization, management,

leadership skills and values).

Page7of176

22. In addition, management needs to play a continuous proactive role in the

overall governance process. The vast majority of governance and control processes

are embedded in the organizational fabric, which is woven and maintained by

management. The controlling authority and the stakeholders are dependent on

management for information and for translating sometimes highly technical

information into issues and choices requiring business judgment. Supervisors have

legally defined responsibilities relating to risk control, fraud control and

conformance to laws, regulations and instructions and standards of conduct. To be

effective, this requires regular interaction between the management of a financial

institution and senior people in supervisory agencies (Chapter 6 discusses these issues

at length).

23. The seriousness of the Ministry of Finance to manage this important

financial institution is reflected from the fact that CDNS is without a regular

Director General of BPS-21 for the last two years. Internally, no one qualifies for

the job. Consequently, the CDNS is now being managed by Joint Secretary (Budget)

of the Ministry on part-time basis as additional charge. The supervisors in the

Ministry perceive it as one of the Wings of the Ministry, therefore, the interaction is

quite informal and need and demand based, generally for some appointments or

financing requirements, rather than formal, structured and governance oriented.

24. Ministry’s approach towards the CDNS seems to be characterized by (i)

aversion to long-term planning and goal setting; (ii) focus on ‘fire-fighting’ than

restructuring the organization to make it more compatible with 21

st

Century’s needs

and modernizing systems and procedures; and (iii) tendency to respond only to the

urgent as opposed to the important. The CDNS is neither classified as a financial

institution (bank) in true sense nor categorized as non-banking financial institution

(NBFI), therefore, it is outside the regulatory regimes of either the SBP or the SECP.

25. Generally, the structure of an organization is divided into five different

configurations: (i) simple structure, which is often a small organic organization

characterized by the loose division of labor, small middle level management, an

informal decision making process, and the centralization of power which allows for

rapid response; (ii) machine bureaucracy, which is characterized by centralized

power with a formal decision making chain of authority, highly specialized and

formalized procedures with a clear separation of line workers and management and

communication is preferably formal throughout all the levels; (iii) professional

bureaucracy, has highly specialized jobs and minimal formalization; the structure is

decentralized, both vertically and horizontally, allows for a freer working

Page8of176

environment, but keeps the standardization requirements used by a large

organization in stable and complex ambiance; (iv) divisionalized form, can be

recognized by the limited vertical decentralization; there are different autonomy

divisions which all report to headquarter, thereby making the middle management

a key part of an organization; and (v) adhocracy, where the organization is divided

into functioning project teams; this organic structure has little formulation of

behavior, but extensive horizontal job specialization, this structure shows the least

reverence to classical principles of management and can be divided into two

different subcategories: operating adhocracy and administrative adhocracy.

Operating adhocracy functions on behalf of their clients; on the other hand,

administrative adhocracy serves the organization itself.

26. The organizational structure of the CDNS, at best, can be defined as a

combination of line and function type with configuration of machine

bureaucracy characterized by centralized power, a formal decision making chain

of authority and inward looking top-management having traditional outlook. The

functions of the organization are pretty much standardized and formalized with

least innovation. There is high degree of concentration of authority managing the

lines of work flows across the hierarchy and functions. (For detailed discussion, see

pages 88 to 91 as well as Figure 7 and Table 24).

27. The distribution of manpower is skewed in favour of field operations with

perfunctory focus on important functions of audit and training. Internal linking

mechanisms are weak and there is hardly any effort to change CDNS outlook

moving from a traditional to modern outlook.

28. Around 42 percent of the employees in CDNS are non-technical staff in

BPS 1 to 7 performing duties as gunman and general attendant which clearly

reflects highly skewed human resource structure. While large strength of Gunmen

is understandable, being a financial institution, it is equally important to rationalize

the staffing of CDNS and strengthen the Technical manpower performing duties in

audit, inspection and NSCs.

29. Organizational culture is the basic pattern of shared assumptions, values,

and beliefs. Organizational culture has three main functions: (1) it is a deeply

embedded form of social control; (2) it is also the “social glue” that bonds people

together and makes them feel part of the organizational experience; and (3)

organizational culture helps employees make sense of the workplace. Organizations

have subcultures as well as the dominant culture. Some subcultures enhance the

dominant culture, whereas countercultures have values that oppose the

Page9of176

organization’s core values. Subcultures maintain the organization’s standards of

performance and ethical behavior. They are also the source of emerging values that

replace aging core values.

30. The CDNS can be conveniently classified as closed organization whose

organizational culture can at best be described as “passive-defensive”

characterized by (i) approval-oriented; (ii) traditional and bureaucratic; (iii)

dependent and non-participative and (iv) ignore success. Leadership of the

organization has remained frail and unsteady because of its over dependence on the

bureaucratic hierarchy of the Ministry of Finance for all kinds of decisions.

31. Grouping, simmering internal conflicts amongst the officers as well as

staff and a culture of penalizing the juniors is quite common. The “power

groups” tend to shelter the weak in their groups and cover up employees’ faults

rather than the organization enforcing rules and discipline. Though, the normal

tenure of a NSO is three years, however, he can be transferred “on deputation to

other department(s) of CDNS on the pretext of “demand” or “urgent need” (For

detailed discussion on Organizational Culture, see pages 88 to 91 as well as see Figures 8

and 9 and Tables 25 and 26). This affects not only the public service delivery but also

the internal management. Many of stories appearing in the newspapers is the result

of this internal conflicts and groupings.

32. Culturally, the closed system organizations such as CDNS are always

opposed to external hiring, particularly at the decision-making level. Human

Resource of CDNS suffers from six major challenges: (i) disproportion staffing and

workload; (ii) huge vacant position, around 34 percent; (iii) delayed or stuck up

promotions (iv) enormous cadre of non-technical staff; (v) absence of Deputation,

Training and Leave Reserve; and (vi) narrow space for induction of direct recruits at

senior levels (For detailed discussion on Human Resource Management, see pages 91 to 95

as well as Table 27).

33. During last three decades, a number of schemes have been made available

to the investors of National savings. Resultantly, both the number of investors

(currently over 7 million) as well as frequency of transactions particularly in

disbursement of profits on monthly basis have increased manifold (closer to 4

million). Nevertheless, not only the total strength has not increased in

commensuration to increased work load, the distribution of available staff does not

follow any scientific pattern. There is a huge gap between indicative staffing and

actual staffing at different categories of NSCs which affects the delivery of service.

Page10of176

34. Regional Directorates of Accounts and Zonal Inspection and Audit

Offices which are lynchpin of the system and are required to perform significant

functions within CDNS, being watchdog, are the most manpower starved. The

total strength of 292 is expected to perform 100 percent of audit of closer to 4

million transactions per month, carrying out regular as well as surprise inspections

of the NSCs and Directorates.

35. A large number of vacant positions (currently 1,443 or 34 percent) have

aggravated the situation causing huge shortage of field staff since long.

Nevertheless, very recently efforts are being made to fill these vacancies through

direct recruitment as well as by promotion as per rules. Shortage of staff is also

restraining the management in sending the officers and officials of the CDNS for

necessary training and refresher courses which are of utmost important not only to

develop the human resource’s capacity but also key for the organizational growth.

36. The passive-aggressive culture and group-politics in CDNS has affected

the organization adversely. It manifests in adverse or average Performance

Evaluation Reports of most officers. Consequently, none of the officers in BPS-19

qualifies the threshold to be eligible for promotion in BPS-20 or 21. The meetings of

DPC are held with a lag delaying promotions. It is not only badly affected quality of

service in the National Savings Centers but has relegated vital functions of the audit

and inspection to low priority.

37. It is surprising to note that the CDNS does not have an earmarked DTL

reserve. The Establishment Division notified two Office Memorandums in1960s viz.

Estt. Division O.M. No.3/1/60-C-III, dated 4-10-1961 and Estt. Division O.M.

No.3/1/60-C-III, dated 17-6-1967 for maintaining Deputation, Training and Leave

Reserve equal to 10 percent of total strength of the Section Officers. Consequently,

the senior officers are reluctant to grant paid or unpaid leave as it means losing a

helping hand at the workplace. Both the Controlling Ministry as well as the CDNS

seems to be incognizant of the fact that while maintaining DTL reserve has upfront

cost, it benefits both the organization and the economy as it leads to higher labour

force participation, greater labour productivity and work engagement and better

grooming of human resource. Researchers have concluded that the paid leave

policies are important drivers of labour force participation and better bonding

between the staff and the management.

38. The CDNS new recruitment rules notified in 2014 allows external hiring at

JNSO, ANSO, NSO and Assistant Director level though, it is yet not at the

Page11of176

desired level particularly in the rank of ANSO, DNSO, Assistant Director and

Joint Director/Director. It is important to resolve this issue and open up all level of

positions to external hiring for induction of fresh graduates and market experience

in the organization.

39. CDNS does not own any property, building or office throughout Pakistan

except two open plots: one in Saddar, Rawalpindi and the other in Mauve area,

Islamabad. All operational offices and National Savings Centers including the

Head Office of CDNS are housed in rented properties. Not all NSCs are located at

convenient locations and hired offices are generally small and at times, dimly lit

portraying shabby look or at worst dungeon. Such NSCs become overcrowded

during early days of each month with long queues, angry and frustrated steaming

out their anger against the government. However, there are few exceptions in big

cities and majority of the NSCs do not have Helpdesk or Information Counter

which makes customers’ facilitation very limited.

40. The constraining factors in modernizing and improving the outlook of

NSCs include: (i) gap between per square foot ceiling of Housing Ministry on

renting office space and the appropriate space needed for NSCs being public service

delivery financial organization; (ii) ceiling on current commercial rates prescribed

by the Ministry of Housing in consultation with the Ministry of Finance which

prevents the CDNS to rent offices/NSCs in better localities or better commercial

buildings; (iii) budgetary constraints in renting larger space for the NSCs and

Regional Directorates; and (iv) improving and modernizing rented offices/NSCs

from the public exchequer fearing audit objections and CDNS is at the mercy of

property owners for any renovation and improvements.

41. Most of the NSCs endure scruffy operating environment which frustrates

and demoralizes the staff affecting the service delivery negatively. They are far

less motivated than the staff of their competitors who are better dressed up, where

customers are greeted by the Public Relation or Customers Facilitation Officer to

guide and facilitate them. The employees are more knowledgeable about the

products the Banks offer.

42. The budget of CDNS has increased in nominal terms though, the

establishment budget has increased from 52% in 2009 to 68% of the gross budget,

an increase of 159% while the operational budget has declined from 48 to 32% of

the gross budget during the same period. The cumulative inflation during the

same period was 72.3%, thus turning the operational budget negative in real terms.

Page12of176

Almost two-third of the CDNS gross budget is allocated to Establishment charges

leaving only one-third for operational budget. Over 40 percent of the operational

budget is expensed on rentals leaving paltry budget for running the other

operations. The gross budget of CDNS has been only 0.2 percent or less of the gross

inflows and less than 1 percent of net inflows since many years. These skewed

allocations have adversely affected logistic arrangements, operational environment,

efficiency and quality of public service delivery at each NSC.

43. The jurisdiction and span of control of each Zonal Inspection and

Accounts Office, responsible for inspections and audit, is too wide which is

making it difficult to carry out audit of 100 percent transactions at the NSC level

and Regional Directorates. Besides, the ZIAOs have been provided 800 CC

vans/cars that too in unsatisfactory conditions discouraging the Inspecting

Officers/Directors not to move around in the field. As against a sanctioned strength

of 131 Inspecting Officers, there are only 58 incumbents, leaving 73 posts vacant

entailing a shortage of around 56%. The said sanctioned strength was last revised in

1984. Shortage of inspecting officers and pilling up of huge records to be reconciled

and audited is not only affecting the quality of audit but also paves the way to

committing fraud/ forgery/embezzlement which remains undetected in the

absence of regular audit.

44. There is huge audit pendency, both in NSCs as well as other units. Audit

of 64 percent units of CDNS and 65 percent NSCs is pending for the last 2 and 3

years, respectively. It is surprising that audit in 42.5 percent of NSCs is pending for

over three years (Table 28). Decomposition of audit pendency region-wise provides

a deeper insight of the conditions prevalent in CDNS. The worst region is Lahore

where audit in 93 percent units is pending for 24 to 36 months followed by Karachi

(88 percent), Hyderabad (79 percent), Multan (76 percent), Islamabad (72 percent),

Sukkur (71 percent), Faisalabad (56 Percent) and Gujranwala (50 percent). The

regions where audit pendency is in lower than 50 percent units for 24 to 36 months

include: Quetta (45 percent), Bahawalpur (44 percent), Abbottabad (35 percent) and

Peshawar (31 percent). It is pretty alarming situation which requires immediate

attention of the Controlling Ministry (Table 29) because such huge pendency makes

the organization vulnerable to fraud, embezzlement and cheating.

45. Reconciliation of an amount of Rs 37 billion remained pending between

CDNS and Pakistan Post Office and it took huge efforts to carry out this

mandatory effort. Despite these efforts on the part of CDNS, there is still a

pendency in this reconciliation which requires early resolution. An amount of over

Page13of176

Rs 436 million is recoverable since long which has been embezzled, forged, looted

or losses were caused due to overpayments of profit, less deduction of withholding

tax/zakat and allowing ineligible investors to invest (Table 30). For detailed

discussion, see page 96 to 99 and Appendix 8 and 9).

46. The State Bank of Pakistan’s Prudential Regulation M-1 requires that if an

Account (Savings/Current) has not been operated by the Customer during the last

12 months, the Account is classified as Dormant Account and no withdrawal is

allowed until the Account is reactivated. The Bank reserves the right to disallow

debit transaction(s) in the customer account while the account remains dormant/

inactive. If no transaction has taken place in the Account and no statement of

account has been requested or acknowledged by the Customer during the last ten

years, the deposit in the Account is required to be surrendered by the Bank to the

St8ate Bank of Pakistan as required by Section 31 of Banking Companies

Ordinance, 1962, except deposits in the name of a minor or a Government or a court

of law.

47. The CDNS is not practicing this policy nor is maintaining a register of

dormant accounts including the amount involved, NSC-wise, region-wise and in

consolidated form at the HQ. It is learnt that such dormant accounts are

vulnerable to manipulations in the NSCs and such manipulations were detected by

the Audit after a while.

48. Likewise, the NSCs, at the time of opening new accounts, ask the investor

to nominate his or her beneficiaries along with share of each beneficiary in the

investment, in case of death, yet the process of transfer is so long and time

consuming that the beneficiaries are forced, willingly or unwillingly, to pay the

demanded rent. Dormant Accounts and Death Cases are susceptible to

fraud/forgery, rent seeking especially in rural areas and require

systemic/institutional response.

49. Efforts are on the anvil since 2004 to transform the whole system to full

automation, when CDNS purchased the mainframe, albeit at slow pace and with

reluctance because of internal resistance.

Nevertheless, only 83 NSCs have been

computerized without online connectivity and networking under Phase-I approved

at a total cost of Rs 397.32 million. It is proposed to computerize additional 46 NSCs

at Islamabad, Gujranwala, Faisalabad, Lahore, Hyderabad and Karachi under this

phase under Phase-II approved at a total cost of Rs 897.75 million in FY2015 after a

gap of 18 months since termination of Phase-I.

Consequently, the CDNS lost all the

Page14of176

trained manpower in IT and it has to seek fresh recruitment for the new project

delaying the process further. Full automation with current pace and resource

allocation will take at least 10 to 15 years. Even after completion of Phase II, only

129 NSCs (34.5%) will be computerized leaving 245 (65.5%) NSCs, Regional

Directorates, Zonal Inspection and Accounts Offices without automation. (For

detailed discussion on automation, see pages 100 to 103).

50. According to the IT Staff of the CDNS, the existing solution (developed in

2003) has completed its life cycle. The current software solution is unable to cope

with the available modern technologies and CDNS cannot achieve flexibility,

durability, introduce multiple delivery channels for its valued customer and

provision/linking with other Government entities like Ministry of Finance, SBP,

AGPR and Scheduled Banks. The effort of computerization and full automation

received a serious jolt when Ministry of Finance declined to create necessary posts

in the recurring budget on completion of Phase-I completed in 2013 despite

recommendations of the Planning Commission vide its O.M. No. 3 (36)/IT/PC/38

dated: 21 Feb, 2014. Consequently, barring few exceptions the computerized NSCs

have either reverted back to manual system or running concurrent manual and

computer system.

51. There seems to be general resistance to full automation in CDNS which is

in the pipeline since 2004 but no way near to partial or full automation.

Generally, automation is resisted by the employees in the Government for the

reasons they: (i) cannot comprehend the technological developments and its

potential due to lack of knowledge; (ii) are risk averse and lack vision; (iii) lack

skills to manage complex technological projects; (iv) power shifts to automation

which reduces or eliminates opportunities for corruption and rent-seeking; (v) with

automation, power shifts to new players; (vi) systems moves from favours territory

and hierarchy to collaboration amongst all tiers; (vii) patronage is replaced by

public good; (viii) management and employees feel more comfortable with status

quo; and (ix) form negative coalition against change and transformation.

52. The training institutions of CDNS suffer from high turnover ratio which

limits the availability of trained staff. Officers of BPS-18 and above are not

provided any training. Most of the instructors are outsourced.

53. The CDNS does not seek service charges (opening of new accounts, issuing

check books, transfer of accounts), being a government organization, and provide

Page15of176

all services free of cost and all costs are charged to its budget. As against, its

competitors charge fee for the services they provide to the customers.

54. Budgeting for fund flows from NSS is done by the Finance Division in a

very simplistic manner. It assigns an arbitrary target to the CDNS without any

relation to overall savings environment in the country, competitive products

competing with NSS, characteristics of the underlying portfolio or patterns of

encashment or estimated liabilities in a financial year which generates extra

pressure to meet the target arbitrarily determined by the Finance Division (For

details, see page 103).

55. CDNS lacks expertise to carry out pricing of products or determining

coupon rates. As discussed, the pricing is determined at 90 percent of the most

recent auction of PIBs of corresponding maturity which may not be consistent with

market yield because of time lag between the period in which base yield (PIBs) is

measured and that during which the rates are offered. (For details, see page 104).

CDNS and NSCs are not geared to report accrued interest and unpaid interest on

monthly basis or annual basis to assess the liability, scheme-wise, or even reporting

outstanding balances, scheme-wise, by year end. This is particularly important

given the high proportion of amounts outstanding against Defence Savings

Certificates which are a zero coupon investment where interest is payable in lump

sum at maturity or premature encashment. (see page 104).

56. There is a lag in reporting and reconciliation at different levels. Besides,

GPOs follow inconsistent timeframe for reporting. As a result, monthly figures

reported by the PPO include a mix of figures relating to the reporting month and

those relating to the previous month (see page 105). The CDNS is not well equipped

with modern techniques of inventorying the Savings Certificates to align them with

frequent changes in the NSS rates of return, which have moved from annual to bi-

monthly rates adjustment (see page 105).

57. National Savings Centers/CDNS retain General Journals and Ledgers to

maintain Dr and Cr entries of each account rather than maintaining Balance

Sheets, Income Statement and Cash Flow Statement to determine the soundness

and financial integrity of the system at each functional unit level and consolidated

financial statements of the organization (see page 105).

Page16of176

TOR 4 - To Make Recommendations For Smooth, Effective and Efficient

Functioning Of The Department in Accordance With The Objectives For Which It

Was Established and To Improve Service Delivery

58. The landscape for national savings continues to change around the globe and

so does its regulatory environment. It is important that Pakistan Savings adapts its

processes and procedures as it aims to compete to provide better services, embeds

compliance with relevant regulatory requirements and ensures minimizing risks. If

the CDNS is to be able to operate effectively and efficiently, it is necessary to give it

autonomy with powers to make its own administrative and financial decisions in a

prudent manner.

59. The Committee, considering the growing NSS portfolio, governance,

organizational, managerial and procedural weaknesses as well as rising complaints

of mal-administration against CDNS and best practices in relation to National

Savings Organization around the globe, agreed to make the recommendations: (i)

for implementation immediately, in short-term and medium to long-term. (For

details, see Chapter 7).

60. The proposed measures/recommendations include:

(i) Future Role of Pakistan Savings: The future role of Pakistan Savings may be

to:

(a) mobilize savings by designing, marketing and managing retail

savings schemes which are totally secured and backed by the Federal

Government.

(b) mobilize institutional savings through separate products designed

specifically for institutional savings targeting their pension funds,

provident funds, etc.

(c) introduce products directed at meeting specific needs of the target

savers including senior citizens, pensioners, farmers, small savers,

Children and overseas Pakistani expatriates for which it is important

to carry out regular surveys of the market.

A. Proposed Immediate Measures (0 to 6 Moths)

(i) Appointment of Full Time Chief Executive Officer of CDNS: Ministry of

Finance must take necessary steps to appoint full time Chief Executive

Page17of176

Officer on regular basis, as top priority, from the market having management

and financial experience and capable of implementing reforms before it

creates both legal and financial issues. Such huge organization cannot

continue to be managed on part-time basis as a Section of the Ministry.

Internally, no one is qualified to be appointed as CEO.

(ii) Framework for Addressing Audit Pendency: The Ministry of Finance in

consultation with the CDNS must prepare a framework and a schedule to

ensure that the entire audit pendency must be brought to zero in 12 months

without fail. In addition, steps must be taken to ensure that the audit must

remain current as unnecessary delay makes the system vulnerable to fraud

and embezzlement.

(iii) Recovery of Embezzled Amount: The Ministry of Finance must take

necessary measures to ensure early recovery of embezzled amount,

overpayments and finalize the cases related to dacoities. It is a huge amount

(over Rs 436 million) and recovery must be finalized besides taking

necessary disciplinary action against officers/staff involved in it.

(iv) Finalizing Reconciliation with PPOD: The Ministry of Finance must give a

sunset date to both the CDNS and the Pakistan Post Office Department to

finalize settlement of all outstanding reconciliation and recover outstanding

amount without further delay and all those involved in delaying this

reconciliation may be proceeded against.

(v) Provision of Notes Counting Machines and Counterfeit Currency

Detecting Machines: All Category A and B NSCs in urban areas and selected

rural areas, where volume of transactions on average is high, must have

Notes Counting Machines to save time as well as Notes Detecting Machines

to detect counterfeit currency.

(vi) Provision of Fax Machines: Regional Headquarters and major NSCs must be

provided fax machine facility to fast track inter-regional and headquarter-

regional communication.

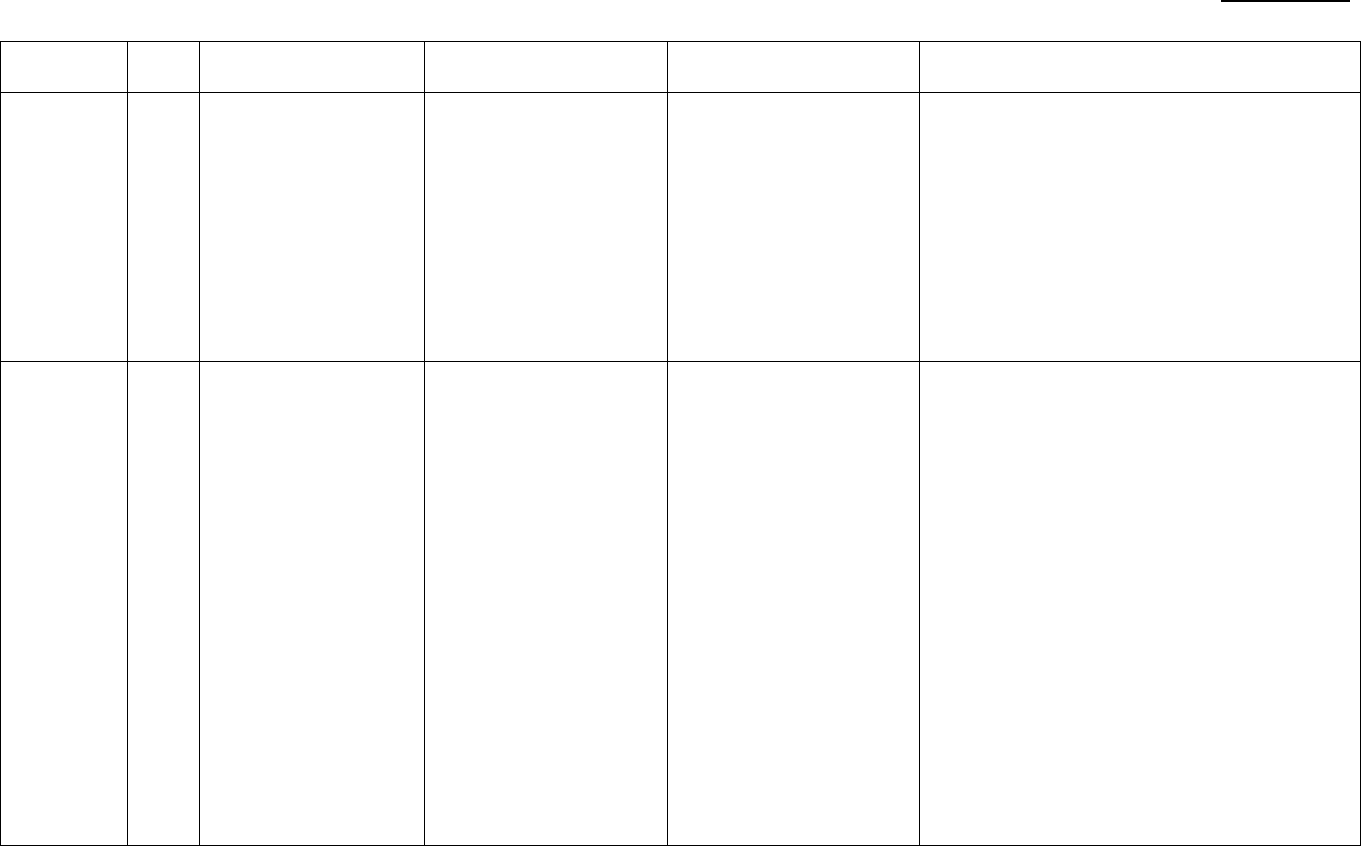

(vii) Performance Evaluation of Employees: The performance of Pakistan

Savings may be measured in the format given below.

Page18of176

Performance Evaluation of Employees

Objective Key Performance Indicators for a Financial Year (Rs in Million)

Gross

Deposits

Less Outflows Net

Inflows

Target Range Actuals Deviation

To raise an

amount of

net financing

within range

agreed with

the Ministry

of Finance

Gross

deposits

mobilized in

a financial

year:

For each

Certificate

For each

Account

Prize

Bonds

Principal repaid

and interest paid

for each certificate

Interest credited in

accounts less

amounts

withdrawn in FY

Bonds redeemed

in the FY

To raise

funds at the

minimum

possible cost

Weighted average cost of new funds raised

through the NSS adjusted for early withdrawals

including the cost of administering the schemes

during the FY

95% of cost of

wholesale

funds raised

by

government

through the

issue of

permanent

debt

instruments

(viii) Special Dispensation for Hiring Space for NSCs and Offices: Ministry of

Finance and CDNS may seek approval of the competent authority to provide

special dispensation to CDNS permitting it to hire appropriate office

accommodation for Regional Directorates as well as NSCs in Quetta,

Karachi, Hyderabad, Larkana, Sukkur, Mirpurkhas, Bahawalpur, Multan,

Sargodha, Faisalabad, Lahore, Gujranwala, Gujarat, Peshawar, Kohat, Dera

Ismail Khan, Swat and Abbottabad in relaxation of standing instructions to

transform their outlook as well as organizational culture. It may require

relocating some of the offices of CDNS to better locations. The Finance

Division may consider delegating these approved powers to the CDNS to

avoid delays.

(ix) Web-Based Public Complaints and Grievances Portal: Pakistan Savings

(CDNS) may establish web-based Public Complaints and Grievances Portal

at each Regional Directorate of Operations and the Headquarters to receive

complaints from investors regarding service of field and regional formations,

queries from existing and potential investors and feedback on policies and

Page19of176

public service of CDNS. Arrangements may also be made to receive

complaints in traditional manner. The proposed Framework for Effective

Complaints Management is at Figure 21 reproduced below. Each of these

elements are elaborated in Chapter 8 ( Recommendation No. cli).

Framework for Effective Complaint Management

(x) Follow Up of Complaints: The Headquarters and Regional Headquarters

must follow up these complaints and redress these grievances within two

week of their receipt. Regional Headquarters must send monthly report to

the Headquarters in the following format:

Region District No of

Pending

Complaints

beginning

of the

month

No of

Complaints

Received

during the

month

Total no of

Complaints

Nature of

Complaints

No of

Complaints

Settled

No of

Complaints

Pending at

end of

Month

Effective

Complaints

Management

Commitment

Communication

Visibility and

Accessibility

Responsiveness

Assessment and

Action

Feedback

Remedies

Business

Improvement

External Review

Monitoring

Effectiveness

Page20of176

B. Proposed Short Term Measures ( 0 to 12 Months)

(i) Governance of CDNS: Strategically, four options are available for the

Government for CDNS: (a) Phasing-Out Option where CDNS may be

completely phased-out over a period of 10 years and its functions may be

transferred to Banks and their Asset Management Companies and Primary

and Secondary Dealers in the Market (US Model); (b) Status Quo Option

where CDNS may continue business as usual operating like an ordinary

poor organization; (c) Corporatization of CDNS transforming CDNS into a

Savings Bank incorporated under the Banking Companies Ordinance, 1962,

as a financial institution managed by an independent Board of Directors

(Malaysia and Sri Lanka Model) or incorporating it under the Companies

Ordinance regulated by the SECP or converting it into an Authority; and

(d) Autonomous CDNS which remains fully owned Federal Government

entity under the Ministry of Finance with full autonomy in its

management and day to day operations (UK Model) and no change in

employees’ status. The Committee strongly recommends that given the

current administrative and financial state of affairs, Autonomous CDNS is

the “Way Forward” to provide necessary autonomy and professionalize its

management. For detailed discussion on the proposed governance structure of

CDNS, see pages 116 to 122.

(ii) Committee to Review and Draft Pakistan Savings Bill 2016: The

Ministry of Finance may constitute a four Members Committee including

representatives from the Ministry, State Bank of Pakistan, SECP and

private sector which may review the Draft Pakistan Savings Bill 2007 and

2010 and draft Pakistan Savings Bill 2016. The draft Bill 2016 may provide

legal cover to transformation of CDNS, responsibilities of the Ministry of

Finance, governance structure and the management of CDNS and other

details in a comprehensive manner.

(iii) Transition Plan: The same Committee may be tasked to formulate

Transition Plan, to avoid any disruption or administrative problems, which

must be part of the Draft Bill.

(iv) Board of Governors: Pakistan Savings (CDNS) may be managed under

the stewardship of a Board of Governors which may provide collective

strategic and operational leadership and have clearly defined

responsibilities.

Page21of176

(v) Constitution of Board of Governors: The Board of Governors may

comprise of nine members including: (a) Finance Secretary as Chairman;

(b) Additional Finance Secretary (Budget); (c) Deputy Governor, State Bank

of Pakistan to be nominated by the Governor SBP; (d) Director General

DPCO; (e) four members from the private sector who are well-known for

his integrity, expertise and experience representing each in financial

services & investment, Chartered Accountant including corporate law,

economist and capital markets and banking to be nominated by the Federal

Government; and (f) Chief Executive Officer of Pakistan Savings.

(vi) Board and the Chief Executive: The Board of Governors and the Chief

Executive Officer of Pakistan Savings may be appointed by the Ministry of

Finance in a transparent manner.

(vii) Executive Committee: The Bill may provide for an Executive Committee

comprising the Chief Executive Officer and the Executive Director Generals

of Pakistan Savings responsible for developing Strategic Plan and Annual

Business Plan for Pakistan Savings, day-to-day management and

developing strategy for achieving the assigned target.

(viii) Provision of Token Machine System: Every NSC in urban areas must

have Token Machine System installed to discipline both the visiting

customers and their prompt disposal by NSC staff rather than dealing with

the clients on the basis of acquaintance and friendship.

(ix) Rationalizing and Beefing up Management and Staffing: Ministry of

Finance must undertake urgently (a) rationalizing and beefing up

management at all levels in the light of proposed structures and create the

required number of posts as discussed in the report to improve service

delivery and (b) take immediate steps to fill all vacant posts (see Chapter 8).

For detailed discussions on the proposed organizational structure of

CDNS, see pages 122 to 142

(x) Proposed Organizational Structure: The organizational structure,

irrespective of change in its status and governance as elaborated above,

may be reformed in a manner that head of the institution may be assisted

by six executive Director Generals, viz. (a) DG Products Development and

Marketing; (b) Director General Operations including Regional

Directorates; (c) Director General Human Resource Management and

Page22of176

Security; (d) Director General Finance and Accounts (e) Director General

Legal; and (f) Director General Audit and Inspection. Proposed

Organizational Structure of Pakistan Savings (CDNS) is at Figures 11 to

20 in Chapter 8.

(xi) The new management organizational structures proposed at Figures 11 to

20 will help in rectifying the management and non-management staff

which is highly skewed towards non-management staff. In the proposed

structures, all services, customers as well as professional and management

will be dealt by officers rank which will not only change the outlook of

Pakistan Savings but will also transform CDNS’s organizational culture.

(xii) Establishing Directorate of Product Development and Marketing: The

DG will be responsible for products development and marketing. Proposed

structure is at Figure 12 and functions assigned are at C-3 in Chapter 8.

(xiii) Establishing Directorate of Operations: The DG will be responsible for

all the operations of CDNS and management of NSCs. Proposed structure

is at Figure 13 and functions assigned are at C-4 in Chapter 8.

(xiv) Increasing Number of Regional Directorates of Operations: Regional

Directorates of Operations as well as Regional Directorates of Inspection

and Audit from 12 to 16 by establishing new Regional Directorates at

Larkana, Sargodah, Rawalpindi and Kohat to ensure effective span of

control and efficient discharge of administrative, operational and audit

functions.

(xv) Manning National Savings Centers: To upgrade quality of service and

provide friendly environment, it is proposed that the National Savings

Centers of Category A and B may be headed by Deputy Director (BS-18)

supported by 4 to 5 Assistant Directors (BS-17) and 4 Deputy Assistant

Directors (BS-16), 2 National Savings Assistants (BS-14), Customers

Relations Officer and Database Administrator. Proposed structure is at

Figures 14.

(xvi) NSCs of C and D Category may be headed by Assistant Director (BS-17)

supported by 3 Deputy Assistant Directors, National Savings Assistant and

Database Administrator. Proposed structure is at Figure 15.

(xvii) It is expected that the proposed structures may provide new outlook to

Pakistan Savings, improve its management and public service delivery,

Page23of176

may ensure regular audit and prompt decision-making as is required for

such organizations. For details regarding functions assigned to Regional

Directorate and NSCs, see C-5 and C-6 in Chapter 8.

(xviii) Establishing Directorate of Human Resource Management and

Security: The Directorate will be responsible for management,

administration, recruitment, training, procurement and security. Proposed

structure is at Figure 16 and functions assigned are at C-7 in Chapter 8.

(xix) Establishing Directorate of Procurement: A directorate of procurement

under the DG HRM and Security may be established which may be

responsible for bulk procurement in Pakistan Savings to meet its annual

requirements strictly following PPRA Rules.

(xx) Establishing Separate Security Wing: A separate Security Wing headed

by Chief Security Officer with necessary support staff at the headquarters

and linkages at Regional Headquarters Operations may be established to

streamline security system of the NSC.

(xxi) Establishing Directorate of Finance and Accounts: The Directorate will

be responsible for all matters relating to finance and accounts including

preparation of financial statements. Proposed structure is at Figure 17 and

functions assigned are at C-8 in Chapter 8.

(xxii) Establishing Directorate of Legal at HQ and Joint Directorates Legal:

CDNS may establish Directorate of Legal Service at Headquarters

supported by Joint Directors each at provincial capitals at Lahore, Karachi,

and Peshawar which should work in close coordination with Directorate of

Operations. This Directorate shall work in close coordination with

Directorate of Operations. It may advise Directorate of Operations on all

cases of Death and Transfers, Pledges, Issuance of duplicate certificates

expeditiously following due process and legal requirements. The

Directorate may prepare Standard Operating Procedure and the Check List

of documents to be submitted for processing the case which must be

publicized. The Directorate must ensure every case is processed with two

to three weeks from the date of submission. The proposed structure is at

Figure 18 and functions assigned are at C-9 in Chapter 8.

(xxiii) Establishing Independent Directorate of Audit and Inspection: To

promote independent and objective assessments, it is proposed that the

Page24of176

Director General Audit and Inspection may report directly to the Board of

Governors through its Audit Committee. It is extremely important that the

internal auditors must not be dependent on Chief Executive Officer or the

Ministry of Finance for the security of his position. The proposed structure

of this directorate is at Figure 19 and functions assigned are at D-1 in

Chapter 8. It must be ensured that the internal auditors have access to the

Board on confidential basis and the audit function is independent of

Pakistan Savings Management, both by intent and in actual practice.

(xxiv) It is important that the Directorate of Audit and Inspection has

appropriate level of manpower manned by professionals with integrity,

capable of building trust, communicating, continuous learning and have

diversified perspectives, experiences and skills. There can be no

compromise on this as Pakistan Savings is handling public money which

requires continuous diligence and scrutiny.

(xxv) Vigilance of Internal Audit: Regulatory changes, economic headwinds

and the interconnectivity of financial business require most financial

institutions to operate in a more agile manner so they can quickly dodge

threats and exploit opportunities. These dynamic forces internal audit –

which is responsible for providing assurance on internal controls, risk

management and corporate governance as well as consulting services to

the financial institution – to remain vigilantly informed of the latest global

developments affecting the institution and how it may respond to external

drivers of change.

(xxvi) Issuance of Audit Calendar: The Directorate General Audit will issue

Audit Calendar at beginning of financial year (15

th

July) duly approved by

the Executive Committee which must be followed rigidly. While preparing

Audit Calendar, it must be ensured that Audit Staff is provided

appropriate and reasonable time in commensuration with expected

workload for conducting meaningful audit rather than fulfilling mere

formality. The Executive Committee may oversee this function.

(xxvii) CDNS must ensure that Audit staff is paid identical TA/DA as the staff

of Federal Audit is being provided to sustain their motivation.

(xxviii) Internal Audit Report: Directorate of Audit and Inspection may cause to

be prepared an annual internal audit report of Pakistan Savings accounts

Page25of176

which shall be submitted to the Board by the Chief Executive Officer within

180 days after the end of financial year.

(xxix) External Audit: While effective internal audit is an effective management

tool, external audit is equally important for three reasons: (i) it identifies

weaknesses in internal controls; (ii) it lends credibility to Financial

Statements; and (iii) external auditors provide unbiased and expert

recommendations as they work with single purpose of improving the

performance. It is proposed that the statement of accounts of Pakistan

Savings may also be audited by the external auditors to be appointed with

the approval of the Board and the Federal Government who shall be a firm

of Chartered Accountants of repute or by Auditor General of Pakistan.

(xxx) Report of the External Auditors: The external auditors must make a

report to the Board and the Federal Government upon the balance sheet

and statement of accounts and in that report, they shall state whether in

their opinion the balance sheet is full and fair balance sheet containing all

necessary information and properly drawn up so as to exhibit a true and

correct view of affairs of Pakistan Savings.

(xxxi) Sending Report of External Auditors to the Federal Government: The

Board shall, within 180 days of the end of each financial year, send a copy

of accounts certified by the external auditors and a copy of auditors’ report

to the Federal Government.

(xxxii) Audit Committee: The Board is expected to appoint a minimum of three

directors to the Audit Committee. These individuals should be

independent and financially literate (able to understand financial

statements and general finance concepts) and at least one member should

have banking, accounting, or other relevant financial proficiency.

(xxxiii) Members of the Audit Committee: The members of the Audit Committee

should be particularly suited to fulfill the following responsibilities: (a) To

adopt a formal written charter that is approved by the full Board of

Governors which specifies the scope of the audit committee's

responsibilities and how it should carry out those responsibilities, and to

review annually the performance by the audit committee of its

responsibilities, as set forth in the bylaws or charter; (b) To hold regular

meetings to permit adequate and timely discussions of audit results, losses,

and irregular occurrences, and other matters of concern; (c) To obtain from

the internal auditors an independent and objective assessment of the

Page26of176

adequacy and effectiveness of the controls over (i) financial reporting; (ii)

effectiveness and efficiency of operations; and (iii) compliance with laws

and regulations, at such regular meetings and at other times as necessary;

(d) To recommend to the Board of Governors the appointment and

termination (including separation payments) of the external auditors; (e) To

formally evaluate the performance of the internal auditors following

guidelines set forth by the Pakistan Savings for evaluating the performance

of other officers; (f) To review and approve an annual internal audit

program that provides for audits for which the scope and frequency are

reasonably expected to ensure an appropriate level of audit attention and

to coordinate with any external audit conducted at the direction of the

Board of Governors; (g) To review and approve an annual internal audit

budget that is sufficient to carry out an effective audit program, to review

performance against budget, and to determine whether any significant

variances from existing System and guidelines are justified; (h) To meet

with the external auditors to discuss the Pakistan Savings’ financial

statements and issues arising from the annual external audit; and (j) To

establish procedures for (i) the confidential, anonymous submission by

employees of complaints and concerns regarding questionable accounting,

internal accounting control, or auditing matters and (ii) the receipt,

retention, and treatment of such complaints and concerns.

(xxxiv) Establishment of Directorate of Information Technology and MIS: The

lynchpin of proposed organizational structures is the Directorate of

Informational Technology and Management Information System moving

towards enhanced transparency and public disclosures. It will enable

providing real time information, making the internal controls more

effective and decision making efficient. To transform Pakistan Savings into

a modern entity to meet the requirements of 21

st

Century, it is proposed to

establish a separate Directorate of IT and MIS under DG Operations to

accelerate the process of automation. Proposed structure is at Figure 20 and

assigned functions are at F-1 in Chapter 8.

(xxxv) Manning Regional Directorates of Operations: Regional Directors

Operations at Islamabad, Karachi, Hyderabad, Lahore, Peshawar, Quetta,

Rawalpindi, and Faisalabad may be in BS-20 and may be supported by

Joint Director Operations, Deputy Directors HRM, Administration and

Assistant Chief Security Officer, Deputy Director (F&A), Deputy Director

(NST), Deputy Director IT and Support Staff and DDO. Remaining

Page27of176

Regional Directorates may be headed by BS-19 Joint Directors. The support

staff may be in the rank of Assistant Directors (BS-17).

(xxxvi) Abolishing Cadre of JNSOs: CDNS at operational level is manned by low

paid employees as compared to their competitors such as banks. There are

no equivalent to JNSOs (BS-11) or ANSOs (BS-14) dealing with the

customers and operations. All services are handled by Officer level

manpower (OG-1, OG-II and OG-III). Their city-based branches are

managed by AVP level officers. Secondly, National Savings Officers do not

signal dignity of position. Thirdly, the promotions are quite slow and it

takes about 10 to 15 years to move from one rank to the other which adds

to this frustration. It is, therefore, proposed The cadre of JNSO may be

abolished and support staff may be recruited as National Savings Assistant

(BS-14).

(xxxvii) Upgrading and Redesignating Posts in CDNS: The post of Deputy NSO

may be redesignated as Deputy Assistant Director (BS-16). Likewise, post

of National Savings Officers (BS-17) may be redesignated as Assistant

Director (BS-17), Assistant Directors (BS-18) may be redesignated as

Deputy Director (BS-18), Deputy Directors (BS-19) may be redesignated as

Joint Director (BS-19) and the post of Director (BS-19) may be redesignated

as Director (BS-20). Each Wing at the headquarters may be headed by

Director General (BS-21).

(xxxviii) External Hiring in Various Pay Scales: Pakistan Savings must ensure

continuous flow of external hiring in all scales to enhance diversity and to

bring new insights to turnaround the organization. The recruitment ratios

in Pakistan Savings may be revised as proposed below after organizational

restructuring as proposed.

(xxxix) Making IT Diploma Mandatory for Future Recruitment: In future, in all

direct recruitment cases of regular Staff in BPS-14 to BPS-21, One Year or

six months Diploma in IT/Computer Science may be made mandatory

requirement in their recruitment rules as shift towards ICT is now the

game of survival.

(xl) Creation of DTL Reserve: The Ministry of Finance must create TL