1

ANNUAL INFORMATION FORM

For the financial year ended December 31, 2020

March 31, 2021

2

TABLE OF CONTENTS

PRELIMINARY NOTES AND CAUTIONARY

STATEMENT .................................................................. 3

DATE OF INFORMATION ............................... 3

CURRENCY AND EXCHANGE RATES .............. 3

CONVERSION TABLE AND TECHNICAL

ABBREVIATIONS ..................................................... 3

CAUTION ON FORWARD-LOOKING

STATEMENTS ......................................................... 4

CORPORATE STRUCTURE ....................................... 5

GENERAL DEVELOPMENT OF THE BUSINESS OF

THE CORPORATION ....................................................... 7

OVERVIEW OF THE BUSINESS ....................... 7

THREE-YEAR CORPORATE HISTORY .............. 8

DESCRIPTION OF THE BUSINESS ................... 9

MINERAL PROPERTIES OF THE CORPORATION .... 14

MINERAL RESERVES AND RESOURCES ........ 14

BOUNGOU MINE, BURKINA FASO .............. 19

HOUNDÉ MINE, BURKINA FASO ................. 27

ITY MINE, CÔTE D'IVOIRE ............................ 35

KARMA MINE, BURKINA FASO .................... 44

MANA MINE, BURKINA FASO ..................... 51

SABODALA MASSAWA MINE, SENEGAL ..... 59

WAHGNION MINE, BURKINA FASO ............ 66

FETEKRO PROJECT, CÔTE D'IVOIRE ............. 74

KALANA PROJECT, MALI ............................. 79

GOLDEN HILL PROJECT, BURKINA FASO ..... 83

OTHER PROPERTIES .................................... 84

RISK FACTORS ...................................................... 85

OPERATIONAL RISKS ................................... 85

FINANCIAL RISKS ....................................... 106

DIVIDENDS AND DISTRIBUTIONS ....................... 109

DESCRIPTION OF CAPITAL STRUCTURE OF

ISSUER 109

GENERAL DESCRIPTION OF CAPITAL

STRUCTURE ........................................................ 109

ENDEAVOUR SHARES ................................ 109

MARKET FOR SECURITIES .................................. 109

PRICE RANGE AND TRADING VOLUMES

OF ENDEAVOUR SHARES ................................... 109

PRIOR SALES ............................................. 110

DIRECTORS AND OFFICERS ................................ 111

CORPORATE CEASE TRADE ORDERS OR

BANKRUPTCIES .................................................. 113

PERSONAL BANKRUPTCIES ....................... 113

PENALTIES OR SANCTIONS ....................... 114

CONFLICTS OF INTEREST ........................... 114

AUDIT COMMITTEE ........................................... 114

AUDIT COMMITTEE CHARTER .................. 114

COMPOSITION OF THE AUDIT

COMMITTEE ...................................................... 114

RELEVANT EDUCATION AND

EXPERIENCE ....................................................... 114

NON-AUDIT SERVICES ............................... 115

EXTERNAL AUDITOR SERVICE FEES ........... 115

LEGAL PROCEEDINGS AND REGULATORY

ACTIONS ................................................................... 115

INTEREST OF MANAGEMENT AND OTHERS IN

MATERIAL TRANSACTIONS ....................................... 116

TRANSFER AGENT AND REGISTRAR ................... 116

MATERIAL CONTRACTS ...................................... 116

INTERESTS OF EXPERTS ..................................... 116

AUDITORS ................................................. 116

OTHER EXPERTS ........................................ 116

ADDITIONAL INFORMATION.............................. 117

APPENDIX "A" – AUDIT COMMITTEE CHARTER ............ 1

3

PRELIMINARY NOTES AND CAUTIONARY STATEMENT

DATE OF INFORMATION

In this Annual Information Form ("AIF"), information is given as at December 31, 2020, unless stated otherwise.

Except as otherwise required by the context, reference to "Endeavour" or the "Corporation" in this AIF means,

collectively, Endeavour Mining Corporation and its subsidiaries.

All references in this AIF to mine-level all-in sustaining cost ("AISC") exclude depreciation, amortization, corporate

general administrative costs and other non-cash related adjustments, unless otherwise indicated.

CURRENCY AND EXCHANGE RATES

All currency references in this AIF are in United States dollars, unless otherwise indicated. Reference to "Canadian

dollars" or the use of the symbol "C$" refers to Canadian dollars. The daily average rate of exchange reported by the

Bank of Canada for the conversion of Canadian dollars into United States dollars on March 29, 2021 was C$1.00 =

$0.7940 (US$1.00 = C$1.2594).

CONVERSION TABLE AND TECHNICAL ABBREVIATIONS

Amounts in this AIF are generally in metric units. Conversion rates from Imperial measure to metric and from metric

to Imperial are provided below. All ounces are troy ounces and 14.58 troy ounces equal one pound (containing 16

imperial ounces).

Table 1: Conversion from Imperial measure to Metric and from Metric to Imperial

Imperial Measure Metric Unit

Metric Measure Imperial Unit

2.47 acres 1 hectare

0.4047 hectares 1 acre

3.28 feet 1 metre

0.3048 metres 1 foot

0.62 miles 1 kilometre

1.609 kilometres 1 mile

35.315 cubic feet 1 cubic metre

0.0283 cubic metres 1 cubic foot

0.032 ounces (troy) 1 gram

31.103 grams 1 ounce (troy)

1.102 tons (short) 1 tonne

0.907 tonnes 1 ton

0.029 ounces (troy/ton) 1 gram/tonne

34.28 grams/tonne 1 ounce (troy/ton)

Unless otherwise defined, abbreviations used in this AIF have the following meanings:

Table 2: Abbreviation Definitions

Abbreviation Definition

Au gold

CFA French West African currency (CFA franc)

DD diamond drilling

g gram

ha hectare

kg kilogram

km kilometre

koz thousands of ounces (troy)

kV kilovolt

LOM Life of Mine

4

Abbreviation Definition

m metre

M million

Moz million ounces (troy)

Mt million metric tonnes

Mtpa million metric tonnes per annum

MW megawatt

Mwh megawatt hour

oz(s) ounce or ounces (troy)

RAB rotary air blast

RC reverse circulation

ROM run of mine

t metric tonne

CAUTION ON FORWARD-LOOKING STATEMENTS

This AIF contains "forward-looking statements". Forward-looking statements include, but are not limited to,

statements with respect to Endeavour's plans or future financial or operating performance, the estimation of mineral

reserves and resources, the realization of mineral reserve estimates, commodity prices, conclusions of economic

assessments of projects, the timing and amount of estimated future production, costs of future production, future

capital expenditures, costs and timing of the development of new deposits, success of exploration activities,

permitting timelines, requirements for additional capital, sources and timing of additional financing, economic,

political and regulatory conditions, realization of unused tax benefits and the future outcome of legal and tax

matters. Generally, these forward-looking statements can be identified by the use of forward-looking terminology

such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts",

"intends", "anticipates" or "does not anticipate", "will continue" or "believes", or variations of such words and

phrases or statements that certain actions, events or results "may", "could", "would", "might", "have potential" or

"will be taken", "occur" or "be achieved". The material factors or assumptions used to develop material forward-

looking statements are disclosed throughout this document and other publicly available filings of Endeavour. Factors

that could cause future results or events to differ materially from current expectations expressed or implied by the

forward looking statements include the ability to deliver gold production growth coupled with a further decline in

total cash cost per ounce produced and a reduction in capital expenditures in 2021, attaining 2021 production

guidance, the ability to fund all of Endeavour's cash requirements for 2021 with existing sources of liquidity and

forecasted cash flow from operations, the ability to carry out the planned 2021 exploration program and obtain

results within anticipated schedules, political and social stability in West Africa (including Endeavour's ability to

maintain or renew licenses and permits) and other risks described in this AIF and in other documents filed from time

to time with Canadian securities regulatory authorities.

Forward-looking statements, while based on management's best estimates and assumptions, are subject to known

and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance

or achievements of Endeavour to be materially different from those expressed or implied by such forward-looking

statements, including but not limited to: risks related to the successful integration of acquisitions; risks related to

international operations; risks related to joint venture operations; risks related to general economic conditions and

credit availability; actual results of current exploration activities; unanticipated reclamation expenses; changes in

project parameters as plans continue to be refined; fluctuations in prices of metals including gold; fluctuations in

foreign currency exchange rates; increases in market prices of mining consumables; possible variations in ore

reserves, grade or recovery rates; failure of plant, equipment or processes to operate as anticipated; accidents,

labour disputes, title disputes, claims and limitations on insurance coverage and other risks of the mining industry;

delays in obtaining governmental approvals or financing or in the completion of development or construction

activities; changes in national and local government regulation of mining operations, tax rules and regulations, and

5

political and economic developments in countries in which Endeavour operates; actual resolutions of legal and tax

matters, as well as those factors discussed in the section titled "Risk Factors" in this AIF. Although Endeavour has

attempted to identify important factors that could cause actual results to differ materially from those contained in

forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or

intended. There can be no assurance that such statements will prove to be accurate, as actual results and future

events could differ materially from those anticipated in such statements. Accordingly, readers are cautioned not to

place undue reliance on forward-looking statements. Except as required under applicable securities legislation,

Endeavour undertakes no obligation to publicly update or revise forward-looking statements, whether as a result of

new information, future events or otherwise.

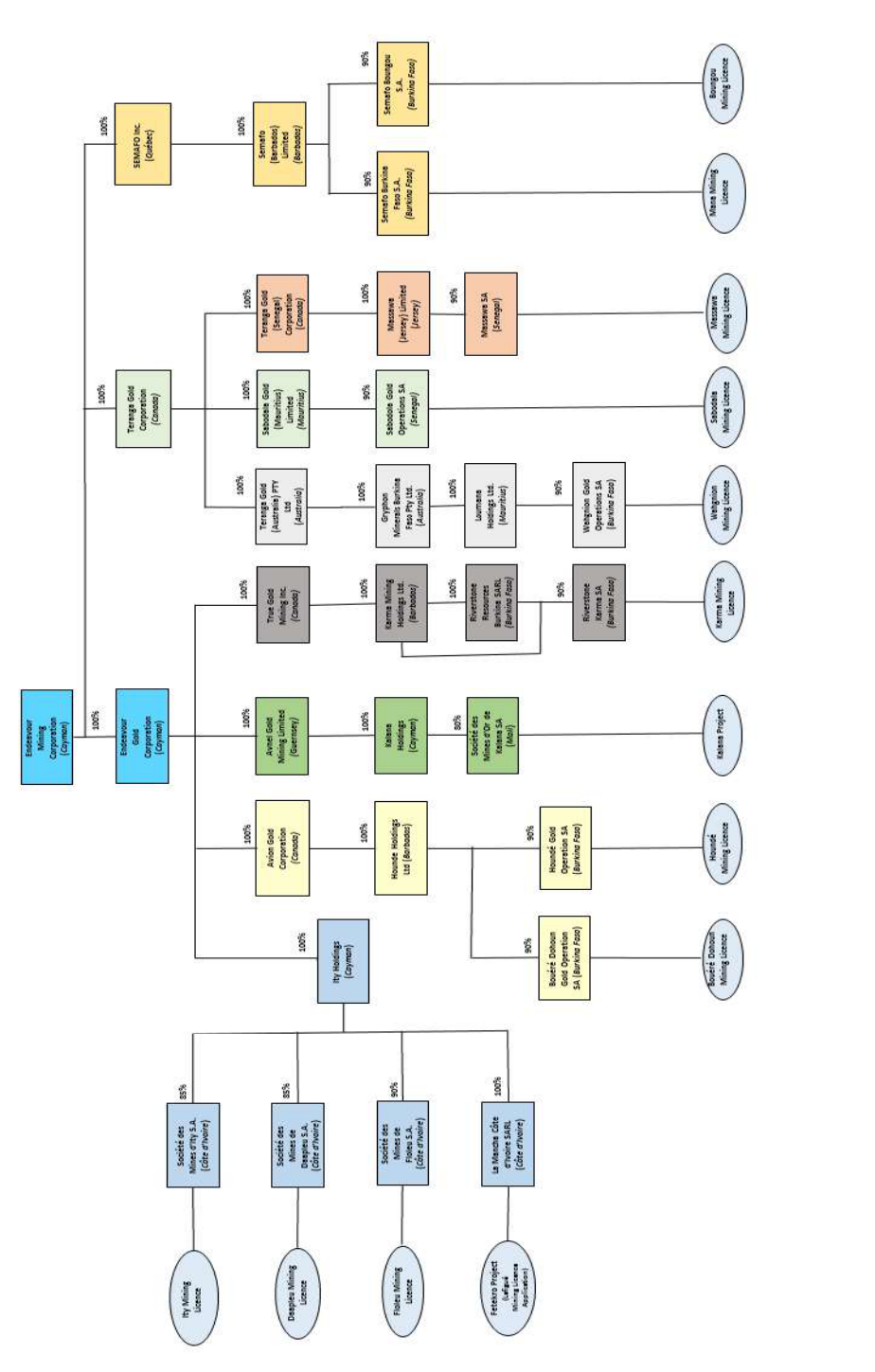

CORPORATE STRUCTURE

Endeavour Mining Corporation was incorporated on July 25, 2002 under the laws of the Cayman Islands under the

name "Endeavour Mining Capital Corp". On July 16, 2008 it changed its name to "Endeavour Financial Corporation"

and then on September 14, 2010 it changed its name to "Endeavour Mining Corporation". The Corporation's

registered office is located at 94 Solaris Avenue, Camana Bay, PO Box 1348, Grand Cayman, Cayman Islands. Its

corporate office is located at 5 Young Street, London, United Kingdom and its executive office is located at 7

Boulevard des Moulins, Monaco.

Endeavour's ordinary shares ("Endeavour Shares") are listed on the Toronto Stock Exchange ("TSX") under the

symbol "EDV" and quoted in the United States on OTCQX International under the symbol "EDVMF".

As at March 30, 2021, the intercorporate relationships between the Corporation and its material subsidiaries, the

Corporation's percentage ownership of the voting securities of each material subsidiary and their respective

jurisdictions of incorporation are set out below.

6

7

GENERAL DEVELOPMENT OF THE BUSINESS OF THE CORPORATION

OVERVIEW OF THE BUSINESS

Endeavour is a TSX-listed senior gold producer focused on developing and operating a portfolio of high quality low-

cost, long-life mines in West Africa. With its technical teams based in proximity to its mines, Endeavour has

established a solid track record of successful operational management, project development and exploration in the

highly prospective Birimian greenstone belt.

As of the date of this AIF, Endeavour's continuing mining operations comprise of the following:

› In Burkina Faso, the Boungou mine, Houndé mine, Karma mine, Mana mine and Wahgnion mine;

› In Côte d'Ivoire, the Ity mine; and

› In Senegal, the Sabodala-Massawa mine.

Endeavour considers its material properties to be the Boungou, Houndé, Mana, Wahgnion, Ity and Sabodala-

Massawa mines.

In 2020, Endeavour’s operations produced 1,066koz of gold at an AISC of $890/oz on a pro forma basis (inclusive of

Agbaou and SEMAFO Inc.’s properties for the full year) and 908koz of gold at an AISC of $873/oz on a consolidated

basis. In 2021, Endeavour

expects to produce 1,365-1,495koz of gold at an AISC of $850-900/oz (inclusive of Agbaou

for January and February 2021 and Teranga Gold Corporation’s properties from February 10, 2021, the date of

acquisition).

The Corporation also has an extensive exploration portfolio in Burkina Faso, Côte d'Ivoire, Guinea, Mali and Senegal.

In late 2016, Endeavour set out a five-year exploration program, aiming to discover 10-15Moz of Indicated Resources

by 2021. To date, 8.4Moz have already been discovered.

8

THREE-YEAR CORPORATE HISTORY

2021

LA MANCHA INVESTMENT

In connection with the acquisition of Teranga Gold Corporation (“Teranga”), La Mancha Holding S.à r.l. ("La

Mancha"), Endeavour's material shareholder, exercised its anti-dilution right and invested $200 million via a

placement (under a short form base shelf prospectus) of approximately 8.9 million Endeavour Shares. The

investment closed on March 30, 2021. Following this investment, La Mancha’s antidilution right has been

extinguished.

SALE OF AGBAOU

On March 2, 2021, Endeavour closed the sale of its non-core Agbaou mine in Côte d’Ivoire to Allied Gold Corp (“Allied

Gold”) for a consideration of up to $80 million with further upside through equity exposure and a Net Smelter Return

(NSR) royalty. The total consideration consists of $20 million in cash payable in the first quarter of 2021, $40

million in Allied Gold shares and a contingent payment of up to $20 million, comprised of $5 million for each quarter

of 2021 where the average gold price exceeds $1,900/oz. In addition, Endeavour has an NSR royalty on ounces

produced in excess of the Agbaou reserves estimated as at December 31, 2019.

TERANGA ACQUISITION

On November 16, 2020, Endeavour entered into an Arrangement Agreement with Teranga pursuant to which

Endeavour agreed to acquire all of the issued and outstanding common shares of Teranga by way of a Plan of

Arrangement under the Canada Business Corporations Act, and holders of common shares of Teranga received 0.47

of an Endeavour Share for each Teranga share. On February 10, 2021, Endeavour completed the acquisition of

Teranga to create a new senior gold producer.

2020

REFINANCING

On December 24, 2020, Endeavour closed an $800 million debt refinancing package. The refinancing consists of an

amendment and extension of Endeavour’s existing $430 million revolving credit facility (“RCF”) and a $370

million bridge facility (“Bridge Loan”). The amended RCF will bear interest at the same rate as previously, at LIBOR

plus a margin between 2.95% and 3.95%, on a sliding scale depending on leverage. The Bridge Loan will bear interest

at 2.25%, increasing by 0.5% every six months until both facilities mature in January 2023. The refinancing proceeds

are to retire Teranga’s various higher cost debt facilities.

INCREASES OWNERSHIP OF FETEKRO

On December 21, 2020, Endeavour announced an increase in its stake in the Fetekro Project. Under the terms of the

agreement, once the mining permit is granted, Endeavour will be entitled to an 80% stake in the Fetekro Project,

compared to 65% currently, while Société pour le Développement Minier de la Côte d'Ivoire ("SODEMI"), the State-

owned mining company, and the State of Côte d’Ivoire will each have a 10% stake. Endeavour will retain full

ownership of the Fetekro exploration license until it is converted into a mining license. The exploitation license

application was submitted on February 2, 2021. Endeavour acquired the additional stake from SODEMI for a

consideration of $19 million plus contingent payments of $3 per ounce for future Proven and Probable Reserves

defined outside of the existing Measured and Indicated Resource boundary.

9

SEMAFO ACQUISITION

On July 1, 2020, Endeavour completed the acquisition of SEMAFO Inc. (“SEMAFO”) pursuant to the terms of an

arrangement pursuant to which Endeavour agreed to acquire all of the issued and outstanding common shares of

SEMAFO by way of a Plan of Arrangement under the Business Corporations Act (Quebec), and holders of common

shares of SEMAFO received 0.1422 of an Endeavour Share for each SEMAFO common share.

Following the acquisition of SEMAFO, La Mancha exercised its anti-dilution right and invested $100 million via a

placement (under a short form base shelf prospectus) of approximately 4.5 million Endeavour Shares.

2019

ITY CONSTRUCTION AND INCREASE IN OWNERSHIP

On January 11, 2019, the Corporation acquired an additional 5% interest in the Ity mine from Keyman Investment

(the Didier Drogba Group) for approximately $15 million. This follows the May 2017 acquisition of a 25% interest

from SODEMI for $52 million (plus $5/oz of additional reserves added post-December 31, 2016). Currently

Endeavour owns 85% of the Ity mine, with the Government of Cote d'Ivoire owning 10% and SODEMI owning 5%.

A feasibility study on a Carbon-in-Leach Plant (the "CIL Project") was completed at Ity in November 2016 and a

technical report was filed in December 2016, which showed economic viability of the CIL Project. Construction

commenced in September 2017 and the CIL Project was completed on-budget and ahead of schedule. The first gold

pour occurred on March 18, 2019 and commercial production was declared on April 8, 2019.

2018

TABAKOTO MINE DISPOSITION

In line with its strategic portfolio optimization goals, following the disposal of the Nzema mine in 2017 and the Youga

mine in 2016, on December 24, 2018, Endeavour completed the sale of the Tabakoto mine, a non-core mine,

to Algom Resources Limited, a subsidiary of BCM International Ltd.

CONVERTIBLE NOTES

On February 6, 2018, Endeavour closed a private placement of convertible senior notes due 2023 (the "Notes") for

an aggregate principal amount of $300 million (plus a fully exercised over-allotment option for $30 million). The

Notes bear a 3% annual coupon maturing in February 2023. The conversion price has been set at C$29.47 ($23.90)

based on a 32.5% premium and the Corporation has the option to settle its obligation through the payment of cash,

the delivery of shares, or any combination of cash and shares (subject to certain conditions). The Notes trade on

the International Stock Exchange (formerly the Channel Islands Securities Exchange).

DESCRIPTION OF THE BUSINESS

PRINCIPAL PRODUCT AND DISTRIBUTION

The Corporation's revenue is generated exclusively from the sale of gold. The Corporation's principal product is gold

doré which, once refined, is sold to one or more market participants on the basis of pricing that is at or close to spot

prices.

Each of the operating subsidiaries has in place offtake and refining contracts which allow them to obtain best terms

for gold sales depending on global gold market conditions. Offtake arrangements for all mines are provided by

StoneX Group Inc. ("StoneX"), a NASDAQ listed company with headquarters in New York which trades in

commodities and in foreign exchange and Auramet Trading LLC, a US based trader of precious metals. Refining

10

arrangements are provided by METALOR Technologies SA ("METALOR"), a Swiss-based refiner of precious metals,

for all mines except the Wahgnion mine. The Corporation has negotiated advantageous terms for all mines (other

than for the Sabodala-Massawa and Wahgnion mines), with both StoneX and METALOR which allow the operating

subsidiaries to pass risk for a shipment at the mine gate, with payment for the gold content of a shipment occurring

on the same day or next day in most cases. The Wahgnion mine ships its doré to be refined by ARGOR-HERAEUS,

also a Swiss-based refiner of precious metals.

Certain amounts of the refined Gold are delivered to Franco Nevada and Sandstorm under streaming arrangements

relating to the Karma and Sabodala-Massawa mines. At the Sabodala-Massawa mine, the streaming agreement (the

“FN Stream”) entitles Franco-Nevada to 6% of Sabodala’s future gold production over life of mine. The FN Stream

does not extend to the Massawa project area. At the Karma mine, the streaming agreement, from March 2021,

entitles Franco-Nevada and Sandstorm in aggregate to 6.5% of Karma’s future gold production for LOM.

The Corporation has two gold offtake agreements with Taurus Funds entered into on May 31, 2018 (the "Wahgnion

Gold Offtake") and March 4, 2020 (the “Massawa Gold Offtake”). Taurus Funds is entitled to make payments per

ounce on the basis of a defined quotational period look-back formula. The Wahgnion Gold Offtake is for a volume

up to 1,075koz and the Massawa Gold Offtake is for ounces produced over the life of mine. The Corporation is

entitled to extinguish Taurus’s rights in exchange for an amount based on a net present value calculation.

Gold is traded on a world-wide basis. The demand for gold is primarily for jewelry fabrication purposes and bullion

investment. The use of gold as a store of value and the large quantities of gold held for this latter purpose play a role

in pricing, as well as current supply and demand trends, which play some part in determining the price of gold.

However, easily measurable macroeconomic factors do not play the same role in price discovery to the same extent

as with other commodities. Gold prices are significantly affected by factors such as US dollar strength, expectations

for US inflation and US bond yields, US interest rates cycle, international exchange rates, changes in reserve policy

by central banks and global or regional political and economic crises. Due to these factors, the gold price fluctuates

continually, and such fluctuations are beyond the Corporation's control.

SPECIALIZED SKILLS AND KNOWLEDGE

All aspects of Endeavour's business require specialized skills and knowledge. Such skills and knowledge include, but

are not limited to, the areas of strategic development, geology, exploratory drilling, engineering, construction, mine

planning, mining operations, processing, regulatory compliance, legal and finance and accounting. Endeavour relies

on skilled and experienced personnel to fulfill these requirements.

COMPETITIVE CONDITIONS

The gold mining industry is competitive, particularly in the acquisition of mineral reserves and mineral resources.

The continued growth of Endeavour relies on the organic growth and development of gold projects, as well as

strategic acquisitions. Although Endeavour has acquired and developed such assets in the past, there can be no

assurance that its acquisition or organic development efforts will succeed in the future.

ENVIRONMENTAL PROTECTION

Endeavour's primary objective is to minimize the potential environmental impacts of its mines throughout the

lifecycle, from discovery through to post-closure. The Corporation's sustainability and environmental policies,

standards, systems and processes are designed to ensure that environmental risks are addressed while ensuring the

environment is maintained, if not enhanced, for current and future generations of its host communities.

All of Endeavour's mining, exploration and development activities are subject to extensive local laws and specific

statutory and regulatory regulations and requirements relating to the protection of the environment, including, but

not limited to, air quality, water management and quality, solid and hazardous waste management and disposal,

11

land use and reclamation. Failure to comply with these environmental laws or regulations could result in fines,

penalties, the suspension or revocation of permits, civil sanctions or lawsuits.

As part of its business planning, Endeavour identifies significant environmental risks and reviews and updates the

closure costs for each property to account for additional knowledge acquired with respect to a property or for

changes in applicable laws or regulations. This process ensures that the Corporation properly budgets for the costs

associated with closure and with implementing appropriate sustainability management measures.

The International Cyanide Management Code ("ICMC") is a voluntary industry program for companies involved in

the production of gold by the cyanidation process. The ICMC addresses, among other things, the production of

cyanide, its transport from the producer to the mine, its on-site storage and use, and decommissioning. In 2020,

Endeavour completed an ICMC compliance audit (remotely) at all six of its mines (Agbaou, Boungou, Houndé, Ity,

Karma and Mana).

The financial and operational effects of environmental protection requirements on the capital expenditures and

earnings for each of the Corporation's mines is not significantly different than that of similar sized mines, and

therefore are not expected to significantly impact Endeavour's competitive position in the future.

The Corporation's (excluding Teranga) total liability for reclamation and closure cost obligation as at December 31,

2020 was approximately $80 million and Teranga’s corresponding liability was approximately $56 million. The

Corporation’s actual reclamation expenses for the year ended December 31, 2020 was $0.6 million and for Teranga,

it was approximately $0.8 million. For more information, refer to Note 18 in the Annual Financial Statements.

EMPLOYEES

As at December 31, 2020, the Corporation (including Agbaou but excluding Teranga) employed approximately 4,860

employees and 6,370 contractors and consultants. Of Endeavour’s total employees, 95% were nationals, of which

31% were from local communities. Among management, 67% were West African, comprised of 47% nationals, 16%

regional expatriates from West Africa and 3% from local communities. A total of 8% of the Corporation's employees

were women, with 9% in management positions and 11% in technical roles. In 2020 20% of the new hires were

women.

Boungou had 287 employees of which 86% were nationals, 6% were women, and 34% were from locally impacted

communities. West African staff represented 33% of senior management, with 11% being nationals.

Houndé had 1,287 employees of which 97% were nationals, 11% were women and 23% were from locally impacted

communities. West African staff represented 52% of senior management, with 33% being nationals.

Ity had 967 employees of which 94% were nationals, 10% were women and 19% were from locally impacted

communities. West African staff represented 66% of senior management, with 56% being nationals.

Karma had 447 employees of which 98% were nationals and 2% were women. West African staff represented 100%

of senior management, with 25% from locally impacted communities.

Mana had 731 employees of which 95% were nationals, 1% were women, and 20% were from locally impacted

communities. West African staff represented 34% of senior management, with 14% being nationals.

As at December 31, 2020, Teranga employed approximately 3,260 employees and 1,298 contractors and consultants.

Of Teranga’s Senegalese and Burkina Faso employees, 94% were nationals, with 34% from local communities. Among

management, 57% were West African, including 47% nationals, 3% regional and 1% from local communities. A total

of 8% of Teranga’s Senegalese and Burkina Faso employees were women, with 10% in management positions, and

43% in technical or supervisory roles. In 2020, 26% of the new hires were women.

12

Sabodala had 1,621 employees, of which 95% were nationasl, 30% were from local communities, and 8% were

women. Among management, 61% were West African, including 51% nationals and 2% from local communities.

Wahgnion had 1,214 employees, of which 93% were nationals, 40% were from local communities, and 7% were

women. Among management, 46% were West African, including 43% nationals.

HEALTH AND SAFETY

Endeavour places the highest priority on the health, safety and welfare of its employees and contractors. The

Corporation's business principles and policies are based on targeting the achievement of "zero harm" performance.

All of Endeavour's Occupational Health and Safety ("OH&S") policies, standards and procedures are aligned to best

industry practices (ISO 45001).

Management and performance of OH&S starts with the Board, assisted by the Technical, Health & Safety Committee.

The Chief Executive Officer is the Executive responsible, supported by the Chief Operating Officer and the Vice

President for Health, Safety and Environment.

Each mine site has a dedicated health and safety team. They are responsible for identifying occupational health and

safety hazards based on job safety analysis and comprehensive hazard and risk assessments, using widely established

methodologies. Going beyond the regulatory requirements, Endeavour's prevention programs include awareness

sessions, operational training and inspections and are supplemented by additional initiatives that promote its health

and safety objectives.

In 2020, the Corporation reported a solid overall safety performance, although regrettably, in February 2020, the

Corporation recorded a fatality at its Karma mine. There were three lost time injuries during the year, resulting in a

low Lost Time Injury Frequency Rate ("LTIFR") of 0.12 per million-man hours worked. The All Injury Frequency Rate

decreased to 3.68 compared to 3.96 for the previous year.

SUSTAINABLE DEVELOPMENT

At Endeavour we are committed to being a responsible miner, building and maintaining meaningful and mutually

beneficial long-term partnerships with key stakeholders, including our local communities, host countries and our

investors.

In Côte d’Ivoire, Endeavour contributes 0.5% of its revenue from Ity and, in Burkina Faso, 1.0% of its revenue from

Boungou, Houndé, Karma, Mana and Wahgnion to the mandatory local mining development funds that finance

community projects in accordance with community-approved local development plans. For 2020, Endeavour,

including Wahgnion, contributed a total $17.83 million to the local mining development funds in Côte d’Ivoire and

Burkina Faso.

In 2018, Endeavour set up an economic development fund, named EcoDev, to promote and generate sustainable

economic activity in the area of influence of Endeavour's mines that can endure beyond the life of Endeavour's

individual assets.

In 2019, EcoDev made its first investment, investing $1 million for a 35% share in an industrial shea butter processing

facility based in Bamako, Mali. Mali is the world’s second largest producer of shea nuts and accounts for 20% of the

global market however it lacked any industrial processing capability. This initiative is targeting approximately 14,000

tonnes of production at full capacity and has created 128 direct jobs and currently supports 21,000 women farmers,

from the local communities surrounding the Kalana Project in Mali, with a long term aim to economically empower

more than 120,000 local women. The goal is for this investment to be profitable and sustainable within seven years,

repaying Endeavour's original investment. Construction of the production plant began in 2020, and the plant was

commissioned in March 2021.

13

In 2020, EcoDev worked on setting up Ranch du Tuy in Burkina Faso. Ranch du Tuy is an intensive cattle feedlot

project to produce fresh, export-quality meat to supply neighbouring countries. During the year, 40 hectares of land

was acquired near the Houndé mine, and two Burkinabe industrial partners and co-investors for the project were

identified.

In January 2019, Endeavour became a member of the World Gold Council ("WGC"), the market development

organization for the gold industry. In September 2019, the WGC launched the Responsible Gold Mining Principles

("RGMPs"). The RGMPs reflect the commitment of the WGC's members to responsible mining and provide an over-

arching framework that sets out clear expectations as to what constitutes responsible gold mining to provide

confidence to investors and supply chain participants. Endeavour has commenced implementing the RGMPs, in

accordance with the WGC’s timetable. In 2019, the Corporation conducted an internal GAP analysis and received

external assurance for RGMP 1.7: accountabilities and responsibilities. In 2020, Endeavour continued to progress

the implementation of the RGMPs, including commissioning an independent external readiness assessment report

to confirm Endeavour’s internal gap assessment and provide additional recommendations in preparation for

external assurance.

COMMUNITY RELATIONS AND SOCIAL

Endeavour views itself as an integral part of the countries and communities in which it operates, as well as a

responsible development partner. It is committed to building and maintaining strong, transparent relationships,

underpinned by open and constructive dialogue, with its host communities, host governments, NGOs and other local

and national stakeholders.

The Corporation has a range of policies in place to govern its approach to stakeholder engagement, including anti-

bribery and anti-corruption, business conduct and ethics, diversity, harassment, sanctions, environmental, safety

and health, human rights and whistleblower. These policies can be found on Endeavour's website:

www.endeavourmining.com.

Key stakeholder groups at the local, regional and national levels at each mine have been identified. All mines, except

the Boungou and Mana mines, have site-specific annual stakeholder engagement plans that identify the

stakeholders' main concerns and expectations, along with a strategy to communicate and engage with them. These

plans include a functional, accessible and widely published external grievance mechanism. Engagement is managed

by the mine's Social Performance teams. In 2021, stakeholder engagement plans will be established for the Mana

and Boungou mines.

The Corporation believes that providing employment and procuring from local suppliers are two of the most

significant economic contributions it can make to the communities in which it operates.

Endeavour aims to hire much of its workforce from the local region in which the operation is located. In 2020, 95%

of Endeavour's mine level workforce were West African nationals.

The Corporation also aims to procure as much as possible locally, in-country or from within the West African

region. In 2020, Endeavour procured approximately $786 million worth of goods, being about 77% of its supplies,

from West African suppliers.

Alongside employment and procurement, Endeavour also undertakes a number of community investment projects

at each of its mines and development projects, including skills training, educational scholarships, healthcare, water

and sanitation, public infrastructure maintenance, capacity building and livelihood programs. Further details can be

found in the Minerals Properties of the Corporation section under each mine, as well as in Endeavour's annual

sustainability reports, available on its website: www.endeavourmining.com.

14

MINERAL PROPERTIES OF THE CORPORATION

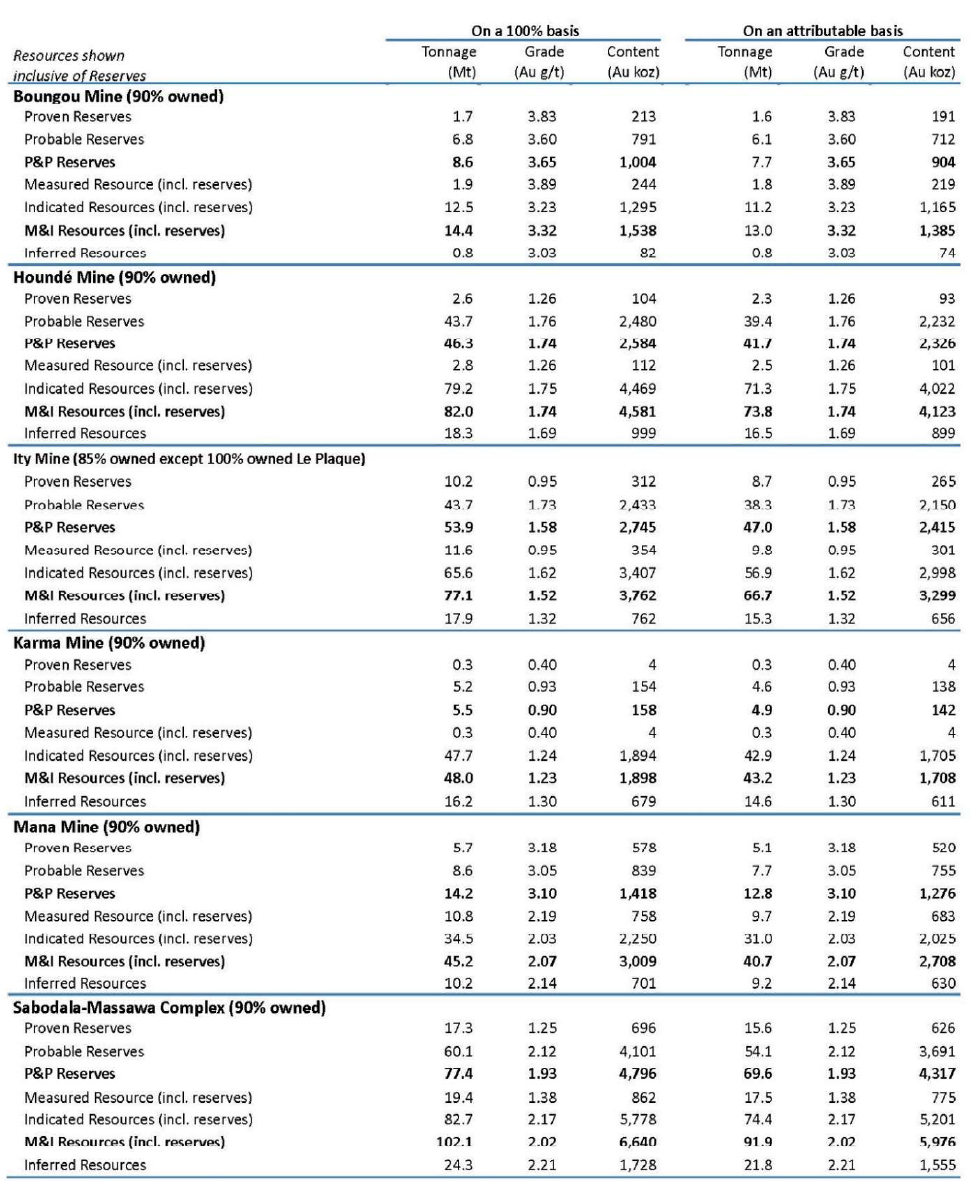

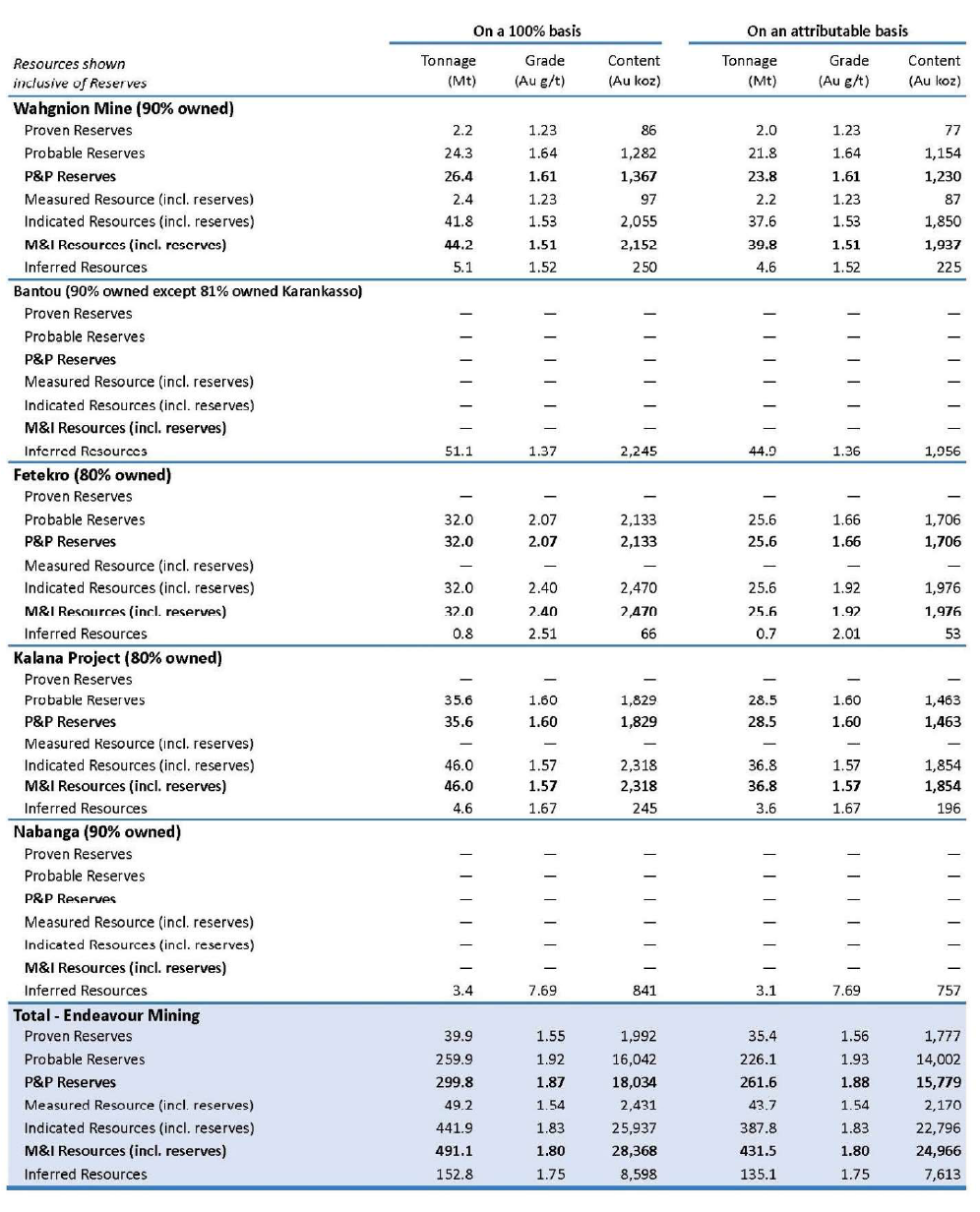

MINERAL RESERVES AND RESOURCES

The following mineral reserves and resources were estimated as at December 31, 2020 in accordance with the

provisions adopted by the Canadian Institute of Mining Metallurgy and Petroleum ("CIM") and incorporated into

Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects ("NI 43-101").

15

Table 3: Mineral Reserves and Mineral Resources

16

17

QUALIFIED PERSONS

The Qualified Persons responsible for the Mineral Reserve and Resource estimates for Endeavour’s material

properties are detailed in the following tables.

MINERAL RESOURCES

QUALIFIED PERSON POSITION PROPERTY/DEPOSIT

Kevin Harris, CPG V.P. Resources, Endeavour Ity (Colline Sud, La Plaque)

Houndé (Bouere, Dohoun, Kari Pump)

Helen Oliver, FGS, CGeol Group Resource Geologist, Endeavour Mining Houndé (Kari West, Kari Center, Kari South, Dafra)

Patti Nakai-Lajoie, P.Geo. V.P. Mine Geology and Grade Control,

Endeavour

Sabodala-Massawa (Sabodala, Masato, Golouma,

Kerekounda, Maki Medina, Niakafiri East, Niakafiri

West, Goumbati West – Kobokoto, Golouma North,

Diadiako, Kinemba, Kourouloulou, Kouroundi,

Koutouniokolla, Mamasato, Marougou, Sekoto,

Soukhoto, Sofia, Massawa Central Zone, Massawa

North Zone, Delya, Tina, Bambaraya)

Wahgnion (Nogbele North and South, Fourkoura,

Samavogo, Stinger)

Michel Plasse, P.Geo Group Manager, OP Geology & Reconciliation

Support, Endeavour

Boungou

Mana (Filon 67, Fobiri, Fofina, Maoula, Siou, Wona-

Kona, Yaho, Yama)

Michael Millad, AIG Cube Consulting Pty Ltd Ity (Ity/Flat/Walter)

Mark Zammit, MAIG Principal Consultant Geologist, Cube

Consulting Pty Ltd

Ity (Mont Ity/Flat/Walter, ZiaNE, Verse Ouest –

Teckraie,

Daapleu, Gbeitouo, Aires, Bakatouo)

Houndé (Vindaloo)

MINERAL RESERVES

QUALIFIED PERSON POSITION PROPERTY/DEPOSIT

Salih Ramazan, FAusIMM Vice President, Mine Planning, Endeavour

Mining

Ity,

Houndé

Mana (except for Siou and Wona underground)

Boungou

Stephen Ling, P.Eng. Director, Integrated Strategy and Asset

Performance, Endeavour

Sabodala-Massawa

Wahgnion

Denis Fleury, P. Eng Chief Engineer, QP Underground, Endeavour. Mana (Siou and Wona underground)

1. The Mineral Resources and Reserves have been estimated and reported in accordance with Canadian National

Instrument 43-101, 'Standards of Disclosure for Mineral Projects' and the Definition Standards adopted by CIM

Council in May 2014.

2. Mineral Resources that are not Mineral Reserves do not demonstrate economic viability.

3. Mineral Resources are reported inclusive of Mineral Reserves.

4. Tonnages are rounded to the nearest 100,000 tonnes; gold grades are rounded to two decimal places; ounces

are rounded to the nearest 1,000 oz. Rounding may result in apparent summation differences between tonnes,

grade and contained metal.

5. Tonnes and grade measurements are in metric units; contained gold is in troy ounces.

6. Processing recoveries vary at each pit by many factors including material types, mineralogy and chemistry of the

ore. The overall average recoveries are around 92% at Boungou, 91% at Houndé, 83% at Ity, 87% at Mana, 82%

Karma, 88% at Sabodala-Massawa, 93% at Wahgnion, 95% at Fetekro and 91% at Kalana.

7. The reporting of Mineral Reserves and Resources are based on gold prices as detailed below:

18

Mines Ity Karma Houndé Mana Boungou Sabodala-

Massawa

Wahgnion

Reserves

1

price $/oz

1,300 1,300 1,300 1,500 OP

1,300 UG

1,300 1,300 OP

1,200 UG

1,300

Resources

2

price $/oz

1,500 1,500 1,500 1,500 -

1,700

1,500 1,500 1,500

Projects Kalana Fetekro Bantou Nabanga Golden Hill

Reserves

price $/oz

1,500 1,500 n/a n/a n/a

Resources

price $/oz

1,500 1,500 1,500 1,500 1,800

1

Gold cut-off grades for Mineral Reserves are as follows:

Boungou is 1.2 g/t for Oxide and 1.3 g/t for transitional and fresh ore.

Ity cut-off grades vary between 0.4 g/t to 0.6 g/t except the Daapleu Transitional and Fresh, which is 0.8 g/t, and Volcano-

Metasediment portion of the Daapleu Fresh cutoff grades is 0.9 g/t.

Houndé cut-off grades vary between 0.4 g/t to 0.7 g/t.

Karma cut-off grades vary between 0.3 g/t to 0.5 g/t.

Mana open pit cut-off grades vary between 0.5 g/t to 0.9 g/t.

Mana Siou UG cut-off grade is 2.5 g/t.

Mana Wona UG cut-off grade is 2.25 g/t.

Kalana cut-off grade varies between 0.4 g/t to 0.6 g/t.

Fetekro cut-off grade is 0.3 g/t for Oxide ore and 0.4 g/t for Transitional and Fresh ore.

Sabodala – Massawa open pit cut-off grades range from 0.37 g/t to 0.55 g/t for Oxide, 0.43 g/t to 0.67 g/t for Sulfide ore and 1.24 g/t

to 1.26 g/t for Refractory ore.

Sabodala – Massawa underground cut-off grades range from 2.5 g/t to 2.6 g/t.

Wahgnion cut-off grades range from 0.40 g/t to 0.48 g/t for Oxide ore and 0.49 g/t to 0.69 g/t for Sulfide ore.

2

Gold cut-off grades for Mineral Resources are as follows:

Mana, Boungou and Bantou are based on a gold price of $1,500/oz except for Wona open pit which is at $1,700/oz.

Mana OP is reported at a cut-off grade as defined by deposit and material type, varying from Oxide at 0.41 to 0.56 g/t, Transition at

0.44 to 0.69 g/t and Sulfide at 0.72 to 2.54 g/t.

Cut-off grade for open-pit at Boungou are defined by material type: Oxide at 0.91 g/t, Transition at 0.91 g/t and Sulfide 1.05 at g/t.

Cut-off grades for the Bantou Project are defined by deposit, varying from 0.43 g/t to 0.86 g/t.

Cut-off grade at Boungou is 2.0 g/t.

Cut-off grade at Siou is 2.2 g/t.

Cut-off grade at Wona is 1.8 g/t.

Cut-off grade at Nabanga is at 3.0 g/t.

Cut-off grades for open pit at Sabodala – Massawa range from 0.31 g/t to 1.09 g/t.

Cut-off grades for underground at Sabodala-Massawa range from 2.0 g/t to 2.84 g/t.

Cut-off grade for open pit at Wahgnion ranges from 0.35 g/t to 0.60 g/t.

Golden Hill Project has been consolidated under the Houndé Mine. Cut-off grades for open pit at Golden Hill range from 0.49 g/t to

0.55 g/t.

8. The reserve estimation study has been carried out internally for Boungou, Ity, Houndé, Karma and Mana,

Sabodala and Wahgnion. Fetekro and Kalana studies were carried out by Snowden.

9. Houndé Mine mineral resources are inclusive of Golden Hill mineral resources as at December 31, 2020.

10. The Sabodala-Massawa Mine and Wahgnion Mine were acquired by Endeavour on February 10, 2021.

TECHNICAL REPORTS

The scientific and technical information relating to the material properties contained in this document has been

derived from or based on the following technical reports, copies of which are available electronically on SEDAR at

www.sedar.com under the Corporation's profile for Ity and Houndé, SEMAFO’s profile for Mana and Boungou, and

Teranga’s profile for Sabodala-Massawa and Wahgnion.

19

Property Report Date Filed

Boungou Technical Report on Natougou Gold Deposit Project, Burkina Faso March 28, 2016

Houndé Technical Report on the Houndé Gold Mine, Republic of Burkina Faso June 15, 2020

Ity Technical Report on the Ity Gold Mine, Republic of Cote D'Ivoire June 15, 2020

Mana Technical Report on the Results of the Siou Underground Prefeasibility Study at

the Mana Property, Burkina Faso

March 29, 2018

Sabodala-Massawa Pre-feasibility Study of Sabodala-Massawa Project, Senegal August 21, 2020

Wahgnion Amended Technical Report on the Wahgnion Gold Operations, Burkina Faso August 1, 2019

BOUNGOU MINE, BURKINA FASO

Information in this section is based on the technical report entitled “Natougou Gold Deposit Project, Burkina Faso”,

dated March 23, 2016 (the “Boungou Report”), prepared under the supervision of Neil Lincoln, Vice President,

Business Development and Studies at Lycopodium Minerals Canada Ltd. (“Lycopodium”), with the participation of

Marius Phillips, MAusIMM (CP), Principal Process Engineer at Lycopodium, Glen Williamson, Principal Mining

Engineer at AMC Consultants (Canada) Ltd, John Graindorge, Principal Consultant – Applied Geosciences at Snowden

Mining Industry Consultants Pty. Ltd. (“Snowden”), Jean-Sébastien Houle, Eng. from WSP Canada Inc. and Timothy

Rowles, MAusIMM (CP) from Knight Piésold Consulting, all “Qualified Persons” under NI 43-101. Portions of the

following information are based on assumptions, qualifications and procedures which are not fully described herein.

Readers should consult the Boungou Report which is available under SEMAFO’s profile on SEDAR at www.sedar.com

to obtain further particulars regarding the Boungou gold deposit. For greater certainty, the Boungou Report is not

incorporated by reference in this AIF.

Unless otherwise indicated, technical information disclosed herein since the release of the Boungou Report has been

updated under the supervision of, or reviewed, in the case of resources, by Michel Plasse, P Geo, Group Manager -

Operations Geology and Reconciliation at Endeavour, and in the case of open pit mining and reserves, by Salih

Ramazan, FAusIMM, Vice President Mine Planning at Endeavour, each of whom is a “Qualified Person” under NI 43-

101.

LOCATION

The Boungou gold deposits lie within the Boungou Permit Group located in eastern Burkina Faso. The property lies

approximately 323 km east-southeast of Ouagadougou, the capital of Burkina Faso. The plant is centred on UTM

coordinates 980,734 mE and 1,329,353 mN (WGS84 Zone 31 North).

Access to the site is by means of Route Nationale RN04, an all-weather bitumen road from Ouagadougou through

Fada n’Gourma to the Ougarou junction. From there, travel is via a laterite road to the property 60 km to the

southeast. Fada n’Gourma is the nearest town with basic hospital, hotel and limited resupply facilities.

The climate of Burkina Faso is semi-arid, with a rainy season from May to September, and a hot dry season from

February to April. Access for exploration activities are limited during the rainy season.

OWNERSHIP

Boungou's mineral rights comprise of one mining exploitation permit (the "Boungou License"). The Boungou License

is held by Semafo Boungou SA. Endeavour, indirectly through its subsidiary Semafo (Barbados) Ltd., holds a 90%

stake in Semafo Boungou SA. The remaining 10% interest in Semafo Boungou SA is held by the State of Burkina Faso.

Pursuant to its mining convention with the State and local legislation, Endeavour is to pay the State of Burkina Faso

a 3% to 5% royalty, on a sliding scale based on prevailing gold prices (i.e. all shipments with gold spot prices lower

or equal to $1,000 per ounce are subject to a royalty rate of 3%, a 4% rate is applied to all shipments with gold spot

20

prices between $1,000 and $1,300 per ounce, and a 5% royalty rate is applied on all shipments with a gold spot price

greater than $1,300 per ounce). Boungou’s tax rate is 27.5%.

The Boungou License has a perimeter of 29.06 km² and will expire on January 22, 2024. It remains renewable for

consecutive five-year periods.

HISTORY

No exploration is known to have occurred on the Tapoa permit group prior to 2010 when Orbis Gold Limited (“Orbis

Gold”) commenced soil and rock chip sampling. The soil and rock chip sampling were followed up in 2012 with a

regional RC drilling program that resulted in the discovery of the Boungou gold deposit. Resource drilling commenced

at Boungou in 2012 and culminated with an initial mineral resource estimate being completed by Snowden in August

2013, which was classified and reported in accordance with the 2004 edition of the Australasian Code for Reporting

Exploration Results, Mineral Resources and Ore Reserves (the “JORC Code”). Orbis Gold completed further infill

drilling at Boungou in 2014 and the mineral resource estimate was updated by Snowden in August 2014 and was

classified and reported in accordance with the 2012 edition of the JORC Code. In February 2015, SEMAFO acquired

Orbis Gold. A conversion of the resource from JORC Code to NI 43 101 was completed by Snowden in March 2015

for SEMAFO and reported in accordance with NI 43-101 regulations. Between March 2015 and August 2015, SEMAFO

completed an infill drilling program at Boungou aimed at upgrading the confidence in the resource estimate along

with exploring targets proximal to the resource area.

No modern production of gold has occurred within the Tapoa permit group. The central part of the Boungou

exploration permit has artisanal activity along the north-to-south trending drainage system. Extraction of gold by

the local community from artisanal workings has occurred for an unknown period of time, with free gold recovered

by gravity methods in gold pans or through simple sluicing methods. The vertical extent of the workings is unknown,

however it is believed to reach a maximum depth of approximately 20m to 40m, although the vast majority of the

workings are less than 5m deep. Snowden noted that the deeper workings are extremely localised and limited in

extent. The total tonnage and grade of material extracted from artisanal workings at the Boungou gold deposit is

unknown, however it is not considered to be material to the current mineral resource estimate

GEOLOGY

The Tawori exploration permit (initially the Boungou exploration permit), which contains the Boungou gold deposit,

lies within the Diapaga greenstone belt, a northeast-southwest orientated belt that extends over 250 km in length

and over 50 km in width. Endeavour holds four contiguous permits, collectively known as the Tapoa permit group,

covering approximately 70 km in strike length along the Diapaga belt.

The stratigraphy at Boungou is relatively simple and quite consistent from hole to hole. The stratigraphy consists of

two volcanic flows separated by a volcaniclastic unit. The footwall flow generally progresses upwards from a massive

basalt flow to pillowed flows followed by flow breccia and volcaniclastics. The hangingwall is characterized by a

medium grained volcanic flow (or sill). All these units are intruded by diorite and/or granodiorite sills, possibly

originating from the felsic intrusion located immediately west of the deposit. Late dolerite dykes are also present

and appear to be sub-vertical and strike northwest. The Boungou Shear Zone, which hosts the main gold

mineralization at Boungou, is located at the contact between the footwall and hangingwall volcanic units, where the

volcanic flow top breccias have formed and the volcaniclastics deposited. The contact zone is thought to have served

as an area of weakness, focusing the deformation. While the volcaniclastic units are not always present (although

the intensity of the alteration can make it difficult to identify), the flow top breccias are interpreted to be ubiquitous

across the deposit area.

The Boungou gold deposit can be described as a West African shear zone hosted greenstone gold deposit. The main

mineralized lode is interpreted as a flat-lying anticlinal shear that outcrops in the southeast and plunges gently to

the northwest. The mineralization has a strike length of approximately 2 km, striking towards a bearing of 315° and

21

an across-strike length of approximately 1 km (towards 45°). The mineralization is gently folded with the fold axis

oriented along strike and the limbs dipping gently at approximately 15°.

Gold mineralization is associated with biotite and silica-sericite alteration, along with disseminated sulphides, such

as pyrrhotite, pyrite and minor arsenopyrite and chalcopyrite, with occasional free gold. The mineralization is

structurally controlled and is hosted primarily within a large shear zone and its associated alteration. Arsenopyrite

is almost invariably associated with the presence of gold in assayed samples. The percent arsenopyrite logged can

be used as an initial identification of the mineralized lode. Although not common, visible gold has been observed in

core in some drill holes.

EXPLORATION

Regional soil sampling and rock chip sampling programs were commenced by Orbis Gold in 2010 and permit scale

mapping was conducted during the 2014 field season. SEMAFO updated the works in 2015 to identify areas for

detailed investigation.

Orbis Gold defined a large-scale high order (+50 ppb Au) gold-in-soil anomaly in the area surrounding the Natougou

discovery. The soil anomaly, defined within a six km by four km survey area, includes multiple zones of higher-order

anomalism that have received minimal exploration drilling to date. The higher order soil anomalies present as

priority areas for follow-up exploration. A group of anomalous rock chip samples immediately to the north of the

Natougou deposit coincided with the +50 ppb Au soil anomaly and are associated with extensive artisanal workings

in the area.

Additionally, Orbis Gold completed 13 trenches between November 2014 and January 2015, with an average length

of approximately 38m. All of the trenches were within the Boungou permit. The trenches were hand dug to an

approximate depth of 1.5m and chip samples collected at one-meter intervals from the side wall close to the base

of the trench. Nine of the trenches showed no significant intersections. The best results were obtained from trench

BOTR006, which returned an intersection of 9m at 9.43 g/t Au (horizontal width; not true width) based on a lower

cut-off of 1 g/t Au (or 12m at 7.15 g/t Au if a lower cut-off of 0.2 g/t Au is used).

In 2018 an exploration budget of $4.96 million contributed to the drilling of 55,512m of RC (526 holes), 615.10m of

DD (three holes) and 26,480m of auger (1,911 holes). On the mine permit, a total of 213 RC holes were drilled

targeting various extensions to the mineralization around the open pit designs. A total of 78 RC holes were

completed on the Tawori permit targeting the continuation of the Boungou Main Shear mineralization, as well as

609 auger holes at the Osaanpalo Target as infill to reconnaissance auger lines drilled in previous years. On the

Dangou permit 1911 auger holes were completed on the Dangou Centre target. Promising results were followed up

with 105 RC holes. A further 131 RC holes and three DD holes for were completed at the Dangou NE target, following

up on anomalous rock chip values collected from an artisanal working site.

In 2019 an exploration budget of $4.02 million contributed to the drilling of 24,496m of RC (222 holes), 587.00m of

DD (3 holes) and 8,169m of auger (807 holes). On the mine permit, 17 RC holes were drilled targeting extensions to

the mineralization around the open pit designs. A total of 110 RC holes were completed on the Tawori permit

targeting the continuation of the Boungou Main Shear mineralization, with the program supporting positive results

from 2018. At the Osaanpalo Target, 13 RC holes and 807 auger holes were completed to follow up on previous years

drill results. On the Dangou permit 35 RC holes drilled on the Dangou Centre target produced irregular but

anomalous intercepts requiring further interpretation before follow-up drilling. At Dangou NE, a further 30 RC and

three DD holes were drilled to investigate possible mineralized trends highlighted by previous drill results in the

artisanal workings. Exploration activities further afield on the permits was restricted due to the security incident in

late 2019.

Endeavour spent a total of $1.0 million following the integration of Boungou. Exploration activities resumed in Q4-

2020 with a total of 4,000m of reverse circulation drilled to test for high grade pockets in the future high wall

between the East and West Open pit designs.

22

SAMPLING AND DATA VERIFICATION

Samples used for resource estimates at Boungou are from exploration and grade control drill chips from RC drilling

or core from diamond drill drilling.

Reverse circulation samples are collected from every one-meter drill run in pre-labelled plastic bags directly from

the cyclone on the drill rig. Approximately 30 kg to 40 kg of material is reduced using a tiered riffle splitter to obtain

a subsample of about 2 kg which is packed in a poly bag. Sample tickets are placed into each poly bag, and the hole

ID and sample depth recorded on the remaining ticket stub. The riffle splitter is cleaned after each sample with a

brush. A second split of the same size is kept on-site for reference, and the rest of the RC-sampled material discarded.

A small sample of chips from each one-meter interval is removed with a sieve, washed and placed in labelled chip

trays for logging and future reference. RC samples are collected dry 99% of the time. Sample bags are then

transported to the on-site preparation laboratory for crushing and pulverizing. Quality control samples, including

reference materials and blanks, are also submitted with these samples.

Diamond core samples are collected on a maximum of 1.2m intervals or to the lithological/alteration/mineralization

boundaries, with a minimum sample length of 0.2m. The core is cut in half lengthwise using a diamond saw and the

sampled half core placed in a plastic bag and labelled with the hole ID and depth. A sample ticket labelled with the

hole ID and depth is also placed in the bag. Quality control samples are also submitted with these samples. The

other half is kept for reference in core storage shelters at the Boungou exploration camp.

In 2020, no RC drilling and subsequent sampling impacting the resources was conducted in the Boungou pits.

Sample pulps are transported to ALS Laboratory (“ALS-OU”) in Ouagadougou for assaying. ALS-OU is part of the ALS

Group of laboratories that operates under a global quality management system ISO 9001:2008, and participates in

international proficiency testing programs. Quality control samples, including reference materials and blanks, are

also submitted with these samples.

Boungou has an on-site laboratory owned by Endeavour and operated by WESTAGO. The laboratory is not

accredited, but regularly participates in international proficiency testing programs. In addition, Mana mine’s site

laboratory facilities (Mana Lab) is owned and operated by Endeavour. This laboratory is also not accredited, but

regularly participates in international proficiency testing programs and acted as referee lab for the annual check

assay as part of the quality control process.

The Quality Assurance/Quality Control ("QA/QC") measures include the insertion of blank samples (“blanks”),

certified reference materials (“CRM”), field duplicates and lab replicates. Additionally, re-assaying of a set number

of sample pulps at a secondary umpire laboratory is performed on a quarterly basis as an additional test of the

reliability of assaying results. The CRMs are supplied by ROCKLABS Limited for a variety of gold grade ranges suitable

for this type of deposit. QC results are monitored by Endeavour geologists as part of the assay data validation process

during data loading. Sample submissions falling outside of acceptable rejection limits are investigated and

resubmitted for re-assay, if deemed necessary.

QA/QC results are reviewed by the appropriate QP on a quarterly basis, and an annual summary report is published

that includes the referee lab results. Endeavour considers that the sampling and analytical methods and security

procedures are adequate for the purposes of the resource estimation.

Exploration drilling data are entered directly into a laptop using Geobank Mobile software and thereafter

synchronized and transferred into a central database using the Geobank data management system from Micromine.

A set of predefined validation rules are run on the data as part of the importation process. Final data validation,

including geological and survey data, is carried out by project geologists and/or database geologists. A separate set

of validation steps is followed for assay data after it is imported into Geobank.

23

Grade control drilling data are handled through Datamine Fusion data repository and management suite. Data are

transferred and stored through secure connection to local-based and central corporate servers.

Sampling and logging procedures are reviewed periodically by the relevant QP and have been found to be

appropriate and conducted to industry standards. The genetic model adopted is appropriate and represents the

mineralization at Boungou. The database used for the resource estimate was generated in a credible manner and

properly assembled and is therefore suitable for use in estimating the mineral resource.

MINERAL RESOURCE AND MINERAL RESERVE ESTIMATE

See Table 3 in section "Mineral Properties of the Corporation" for information on the mineral reserves and mineral

resources.

A resource block model has been created for the entire deposit. A three dimensional (3D) mineralized solid has been

updated from all drill hole data (including grade control drilling), limiting resources to the material inside the solid.

The mineralized envelope has been interpreted using Micromine software and the wireframe were created with

Leapfrog software. All blocks interpolated below the surface topography or the mine surface survey as of December

31, 2020 make up the mineral inventory at that date. Blocks are classified relative to proximity to composites and

corresponding precision/confidence level. Technical and economic factors are then applied to the blocks in the form

of pit-optimization, optimized stope designs and cut-off grades to constrain the resources to those that present a

reasonable prospect of economic extraction. Variographic analysis was then undertaken. Resources were modelled

using Studio RM software package from Datamine.

MINING AND MINERAL PROCESSING

Mining uses a conventional open-pit mining method, with hydraulic excavators in backhoe configuration to mine

both the mineralized zone and waste. The majority of the rock requires blasting and only the softer material located

within the top 5m to 10m of the deposit is free digging and loaded directly by hydraulic excavators. Following the

security incident in November 2019, the mining contractor, African Mining Services, decided to terminate the

contract at Boungou. SFTP Mining was appointed as mining contractor in August 2020 and started mining works at

Boungou on October 15, 2020. Production was maintained through this period with feeding of ore stockpiles to the

ROM crusher through a local contractor.

Golder Associates carried out the geotechnical analysis and design studies at Boungou Deposit for Orbis Gold

between 2013 and 2014 and provided the geotechnical design criteria for Boungou open pits: batter angle, batter

height, berm width and Inter-Ramp Angle (“IRA”) for various geotechnical domains. Rock mass characterisation

indicated a very thin Saprolite/Saprock domain (7m to 15m thick) underlain by very strong and competent

metabasalts and metavolcanic sediments fresh rock mass domain. Structural fabric (joint and bedding) control pit

wall stability.

The average annual rainfall at Boungou is 784 mm, with a wet season from June to September. The geology of the

pit comprises metabasalts and metavolcanic sediments with a relatively flat mineralized shear zone. Historical

records indicate that dewatering rates peak in August (90000 m

3

). Groundwater contribution is in the order of 5000

m

3

/month (167 m

3

/day).

Open pit mine production at Boungou averages approximately 3,600 t/d of ore in bedrock, from the West, East and

West Flank pits, that can be blended with ore currently on the Rompad up to 4,000 t/d for processing in the mill.

The first phase of the West pit was completely mined out in 2020.

Pit optimization was conducted using Datamine’s NPV Scheduler software based on the Lerchs-Grossman algorithm

at $1,300/oz base gold price.

The production, drilling and blasting operations are carried out on 6m benches on ore and 9m bench on waste. To

be able to achieve the best degree of selectivity, ore mining is undertaken on a 2m flitch. The highly weathered

24

(strongly and moderately oxide) zone are amenable to free digging or soft blasting. Emulsion is used in both wet and

dry blasting conditions for efficiency.

Grade control drilling is carried out by a same mining contractor and the samples are tested at the in-house

laboratory. Sampling commences with grade control drilling ahead of the mining front, aimed at assisting the short

to medium term mine planning process. The grade control is based on 127mm diameter RC drilling and sampling

practice. A grade control pattern of 10m x 10m is used for 30m vertical deep and 1.0m vertical sampling intervals

In 2020, a total of 2.53 Mt ore and waste was mined, 0.46Mt of ore at an average gold grade of 7.24g/t containing

107koz was moved from the pits. A total of 1.11Mt ore at an average grade of 4.79g/t containing 171koz gold was

processed with an overall recovery rate of 95% producing 162koz gold recovered and 154.7koz of gold poured.

In general, the Boungou primary ore is an abrasive, competent ore with above average comminution energy

requirements. The ore has a high-gravity recoverable gold content; leach kinetics are very slow when gravity is not

included in the flowsheet. High dissolved oxygen levels and lead nitrate are required to achieve fast leach kinetics

and adequate gold recovery. Anticipated lime consumption for primary ore is low to moderate, provided good

quality water can be provided on site. Cyanide consumption is moderate. High lime consumption will be experienced

whenoxide ore forms part of the feed blend.

A detailed metallurgical testwork program was undertaken that focused on primary ore from the Boungou gold

deposit. Quantities of oxide ore presented to the process plant are expected to be around 1% of reserves and as

such, this ore type was not included in the master composite work. However, it was tested in the variability work.

The detailed testwork was carried out from March 2013 to August 2015 under the direction of Lycopodium, with

input from the former owners, Orbis Gold and later SEMAFO, using HQ and PQ (123 mm) drill core recovered from

both resource and metallurgical drilling campaigns.

The metallurgical treatment route selected has been based on the results of the testwork program and includes

processing ore at 4,000 tpd via the following unit process operations:

Single-stage primary crushing with a jaw crusher to produce a crushed product size of 80% passing (P80) of

133 mm.

Mill feed surge/overflow bin that overflows to an 8,000-tonne stockpile to provide 48 hours of capacity.

During extended periods of up to two days for primary crusher equipment maintenance, ore from the

stockpile will be reclaimed by a loader to feed the grinding circuit.

The grinding circuit is a SATMC type, which consists of a closed circuit semi-autogenous grinding (“SAG”)

mill, a pebble crusher for SAG mill discharge oversize and a closed-circuit tower mill to produce a P80 grind

size of 63 µm.

A gravity gold recovery circuit.

Hydrocyclones are operated to achieve a cyclone overflow slurry density of 27% solids to promote better

particle size separation efficiency. Subsequently, a pre-leach thickener is included to increase slurry density

to the leach circuit, minimize leach tank volume requirements and reduce overall reagent consumption.

Leach circuit with five tanks to achieve the required 36 hours of residence time at nominal plant throughput.

Carbon-in-pulp carousel circuit consisting of seven stages is a carbon adsorption circuit for recovery of gold

dissolved in the leaching circuit.

AARL elution circuit with gold recovery to doré. The circuit includes an acid wash column to remove

inorganic foulants from the carbon with hydrochloric acid.

Charged solutions (obtained during elution and intensive cyanidation) are both sent to the refinery and

processed in separate electrolysis cells

25

Carbon regeneration kiln to remove organic foulants from the carbon with heat.

Tailings thickener to increase slurry density for water recovery prior to tailings discharge to the tailings

storage facility.

The processing facility also includes water, air and oxygen services (storage and distribution), and reagent and

grinding media storage.

A detailed metallurgical testwork program was undertaken that focused on primary ore from the Boungou gold

deposit. Quantities of oxide ore presented to the process plant are expected to be around 1% of reserves and as

such, this ore type was not included in the master composite work. However, it was tested in the variability work.

The detailed testwork was carried out from March 2013 to August 2015 under the direction of Lycopodium, with

input from the former owners, Orbis Gold and later SEMAFO, using HQ and PQ (123 mm) drill core recovered from

both resource and metallurgical drilling campaigns.

In general, the Boungou primary ore is an abrasive, competent ore with above average comminution energy

requirements. The ore has a high-gravity recoverable gold content; leach kinetics are very slow when gravity is not

included in the flowsheet. High dissolved oxygen levels and lead nitrate are required to achieve fast leach kinetics

and adequate gold recovery. Anticipated lime consumption for primary ore is low to moderate, provided good

quality water can be provided on site. Cyanide consumption is likely to be moderate. High lime consumption will be

experienced if oxide ore forms part of the feed blend.

The variability testwork showed that overall gold recoveries for the Boungou primary ore ranged from 84% to 99%.

There was a distinct relationship between recovery in the gravity stage and overall recovery. LOM head grades for

the process plant are expected to average 4.15 g/t Au with a gold recovery of 92.9%. The results suggest that the

residue grade is moderately correlated with the amount of coarse gold in the sample (measured by % gold in +75

micron fraction of the screen fire assay), arsenic head assay, and gold head assay. A constant tail relationship is not

appropriate. With consideration of the parameters currently in the geological model, a relationship between the

residue grade and the gold head assay was developed to produce the following predictive equation: Gold Residue

(g/t Au) = 0.1378 + 0.0384*Gold Head Assay (g/t Au).

For example, for a gold head assay of 4.36 g/t Au, the gold residue grade would be 0.31 g/t Au.

As silver residue grades are frequently at the assay detection limit and no trend with head grade is apparent, it is

recommended that a simple arithmetic average of all the silver recovery figures be used i.e. 67%.

Following construction and commissioning of the site, commercial production was achieved on September 1, 2018.

For the remainder of the year, a total of 76,138oz was produced (or 63,605oz excluding the commissioning period).

To date, gold recovery appears to be slightly above the predicted model.

Mine production was halted on November 6, 2019 due to the security incident at Boungou. The Boungou Mine was

put on care and maintenance for the rest of the year. On February 6, 2020, the Boungou plant was restarted and

processing of the stockpile began. Open pit mining restarted in July 2020 with a local contractor undertaking load

and haul. Full contract mining with SFTP contractors started on October 15, 2020.

In 2020, 1.1Mt of ore was processed at an average grade of 4.79 g/t Au with an average recovery of 95%.

ENVIRONMENTAL, PERMITTING & SOCIAL

Several environmental studies were conducted from 2013 onwards to document the sensitive environmental and

social components of Boungou. A comprehensive environmental and social impact assessment ("ESIA") was

completed in Q2 2016.

26

Several environmental permits have been granted covering the active mining areas and surrounding the current pits

namely East pit and East flank, West pit and West flank, and process plant, tailings storage facility, mining and surface

infrastructure.

In 2017 a resettlement action plan ("RAP") for the location of the Boungou village was completed and successfully

implemented. A total of 165 concessions and 900 people were relocated. The new village opened in October 2017

and community infrastructure includes water boreholes, a school, a livestock vaccination pen, a church and mosque.

A range of programs to support impacted local communities have also been implemented. In 2020, these included

solar lighting, beekeeping, market gardens, sheep fattening, production of soap and a sesame project.

For the year ended December 31, 2020, the Boungou Mine contributed $2.82 million to the government-mandated

Local Development Mining Fund, which requires a contribution of 1% of revenue.

INFRASTRUCTURE

The infrastructure at site is to support a 4,000 tpd (1.34 Mtpa) mining and processing facility.

Power is generated on site from hybrid heavy fuel oil and light fuel oil generators, generating approximately 15.5

Megawatts. For the throughput of 1.34Mtpa, an estimated 48.3Wh/t is the total power consumption (30.9kWh/t

for crushing and milling, and 17.4kWh/t for the remaining plant). The power plant has been sized at 11.6MW

connected load to accommodate a peak load of 9MW, and average running location of 6.4 MW, with the

configuration of 3 x 2.5MW medium speed HFO units and 5 x 1.6MW high speed diesel units.

The electrical system is based on 6.6 kV distribution and 400 V, 50 Hz working voltage. The 6.6 kV feeder from the

power plant feeds the site distribution 6.6 kV switchboard. For the process plant the 6.6 kV supply is stepped down

to 400 V at each switchroom. 6.6 kV overhead power lines provide power to various remote facilities (TSF pumps,

bore pumps, WSF pump, water storage supply dam pumps, etc.). Pole mounted transformers step down the voltage

at each location and supply an outdoor 400 V switchboard local to each equipment area. The staff camp power is

supplied from a local MCC/transformer fed from the 6.6 kV overhead line.

Bulk fuel supply is provided by TOTAL. There is an onsite fuel storage facility with approximately three-week storage

of HFO (800 m

3

) and diesel (1,155 m

3

) for HFO. Day storage tanks are provided at the power plant and in the process

plant. Diesel fuel dispensing is also provided for the mine trucks and light vehicles.

A common potable water system is provided for the accommodation camps and process plant usage and is located

at the staff camp and distributed to the various users. Water is delivered via a reticulation system using a constant

pressure variable flow pump system. The pump skid includes a UV disinfection unit to provide additional security

against contamination.

The TSF has been designed to store 10 Mt of tailings generated by the process plant required for the LOM with

tailings being produced at a rate of 1.34 Mtpa. The selected site is located 800m to the north east of the process

plant and requires a single embankment along its south and western extents with a total embankment length of

1,665m and with a maximum embankment height of approximately 24m at the southwest corner. The eastern and

northern margins of the storage facility are confined by a natural laterite ridge line, and therefore no supporting

embankment is required along these margins. The tailings beach surface at full capacity covers an area of