BC Financial Services Authority

(“BCFSA”)

2023/24 – 2025/26

Service Plan

February 2023

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 3

Board Chair’s Accountability Statement

The 2023/24 – 2025/26 BC Financial Services Authority (“BCFSA”)

Service Plan was prepared under the Board’s direction in accordance

with the Budget Transparency and Accountability Act. The plan is

consistent with government’s strategic priorities and fiscal plan. The

Board is accountable for the contents of the plan, including what has

been included in the plan and how it has been reported. The Board is

responsible for the validity and reliability of the information included

in the plan.

All significant assumptions, policy decisions, events and identified

risks, as of February 2023, have been considered in preparing the

plan. The performance measures presented are consistent with the Budget Transparency and

Accountability Act, BCFSA’s mandate and goals, and focus on aspects critical to the

organization’s performance. The targets in this plan have been determined based on an

assessment of BCFSA’s operating environment, forecast conditions, risk assessment and past

performance.

Signed on behalf of the Board by:

Stanley Hamilton

Board Chair, BC Financial Services Authority

February 14, 2023

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 4

Table of Contents

Board Chair’s Accountability Statement ............................................................................................... 3

Strategic Direction ................................................................................................................................... 5

Purpose of the Organization and Alignment with Government Priorities ....................................... 6

Operating Environment .......................................................................................................................... 6

Annual Economic Statement .................................................................................................................. 8

Performance Planning ............................................................................................................................ 9

Financial Plan ......................................................................................................................................... 24

Appendix A: Mandate Letter from the Minister Responsible .......................................................... 26

Appendix B: (RECBC) Letter of Direction from the Minister Responsible ....................................... 33

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 5

Strategic Direction

In 2023/24, public sector organizations will continue working to make life better for people in

B.C., improve the services we all rely on, and ensure a sustainable province for future

generations. Government will focus on building a secure, clean, and fair economy, and a

province where everyone can find a good home – whether in a rural area, in a city, or in an

Indigenous community. B.C. will continue working toward true and meaningful reconciliation

by supporting opportunities for Indigenous Peoples to be full partners in an inclusive and

sustainable province. The policies, programs and projects developed over the course of this

service plan period will focus on results that people can see and feel in four key areas:

attainable and affordable housing, strengthened health care, safer communities, and a secure,

clean, and fair economy that can withstand global economic headwinds.

This 2023/24 service plan outlines how BC Financial Services Authority (“BCFSA”) will support

the government’s priorities and selected action items identified in the Crown Agency Mandate

Letter and letter of direction.

BCFSA is a Crown agency of the Government of British Columbia headquartered in Vancouver.

BCFSA oversees the financial services sector which includes pension plans, mortgage brokers,

real estate services, real estate development marketing, and financial institutions (including

credit unions, insurance, and trust companies). BCFSA also administers the Credit Union

Deposit Insurance Corporation of British Columbia (“CUDIC”).

BCFSA was established by the Financial Services Authority Act (“FSAA”) and has accountabilities

under the following ten statutes (which are accessible via the applicable hyperlink) and

associated regulations:

• Financial Services Authority Act, 2019

• Credit Union Incorporation Act

• Financial Institutions Act

• Insurance Act

• Insurance (Captive Company) Act

• Mortgage Brokers Act

• Pension Benefits Standards Act

• Real Estate Services Act

• Real Estate Development Marketing Act

• Strata Property Act

BCFSA’s operations are aligned with the priorities set out in its Mandate Letter issued by the

Minister of Finance of British Columbia (“Minister of Finance”).

A properly functioning and efficient financial services sector in which British Columbians can

place their trust and confidence is essential to the Province’s economy. To achieve this

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 6

objective, BCFSA safeguards the interests of depositors, policyholders, beneficiaries, pension

plan members, and participants in the real estate market, while at the same time allowing the

financial sector to take reasonable risks and compete effectively. BCFSA’s goal is to balance

sector competitiveness with financial stability as well as federal and international standards

with local market realities.

Purpose of the Organization and Alignment with

Government Priorities

In support of the Government of British Columbia’s priority to help build a better Province for

everyone, BCFSA oversees many of the most important financial services used by British

Columbians by regulating credit unions, trust companies, insurance companies, pension plans,

mortgage brokers and real estate licensees. BCFSA focusses on the safety and soundness of

the sector and its participants as well as consumer protection for the prosperity of both

individual British Columbians and the province of B.C. Through modern, effective, efficient

oversight, enforcement, and guidance, BCFSA works to make B.C. a place where people can

have confidence in the financial services they receive.

BCFSA serves the public by regulating financial services and is accountable to the public

through the Minister of Finance.

Operating Environment

BCFSA began operations as a new Crown agency on November 1, 2019, by assuming the

regulatory accountabilities of the Financial Institutions Commission (“FICOM”). The transition

was driven by the need to create a modern, effective, and efficient regulator with the

independence and flexibility necessary to regulate a financial services sector that has grown

both in importance and complexity.

On August 1, 2021, BCFSA assumed accountability for regulation of real estate services,

including the licensing, conduct, investigations, and discipline of real estate licensees, and real

estate development marketing.

The Employee Engagement goal has been removed from this year’s Annual Service Plan as

BCFSA has effectively addressed the employee issues that precipitated the need for such a

goal in the past. Through the effective operationalization of a range of people practices, it has

significantly lowered its vacancy and employee attrition rates compared to those experienced

by FICOM. Further, last year which was its first full year as an integrated regulator following

integration with the Real Estate regulators, BCFSA achieved Great Place To Work

©

status.

Employee Engagement is now a strength of the organization, contributing to its success

delivering against its mandate. Looking forward, BCFSA will continue to focus on Employee

Engagement through ongoing dialogue and action plans.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 7

Financial Services Landscape

The scope of BCFSA’s regulatory mandate reflects the size and complexity of the financial

services sector in B.C. which, as of December 31, 2022, included:

• 34 credit unions with more than $77.6 billion in assets;

• 636 pension plans with approximately $212.2 billion in assets;

• Over 215 insurance and trust companies (including extra-provincials);

• Over 7,000 mortgage brokers and brokerages; and

• Over 37,000 real estate licensees, brokerages, branches, and personal real estate

corporations.

Central 1 Credit Union, which undertakes various centralized activities such as clearing and

payments for credit unions, acts as a “central” in both B.C. and Ontario. Some pension plans

with members in B.C. also have members in other provinces. Many of the insurance and trust

companies BCFSA oversees operate in other provinces. Mortgage brokers and real estate

licensees may be authorized to do business in other provinces.

This landscape makes cooperation and harmonization with other regulators in Canada a

priority. BCFSA is an active partner in national regulatory associations including: the Canadian

Council of Insurance Regulators (“CCIR”); Credit Union Prudential Supervisors Association

(“CUPSA”); Canadian Association of Pension Supervisory Authorities (“CAPSA”); Mortgage

Broker Regulators’ Council of Canada (“MBRCC”); and the Real Estate Regulators of Canada

(“RERC”).

BCFSA’s Approach to Supervision and Market Conduct

BCFSA uses a risk-based prudential supervisory framework to identify imprudent or unsafe

business practices and intervenes on a timely basis, as required. The rationale, principles,

concepts, and core processes in the supervisory framework apply to all the BCFSA regulated

financial entities in British Columbia. The primary focus of BCFSA’s supervisory work is to

determine the impact of current and potential future financial events, both within British

Columbia and externally.

BCFSA is focused on protecting and achieving fair outcomes for consumers of financial

services in British Columbia. BCFSA works to ensure that regulated entities and individuals

provide British Columbians with the information and advice they need to make the right

decisions from them.

The COVID-19 pandemic has brought increased risk and uncertainty to the financial services

sector. As the B.C. economy moves forward from the pandemic, BCFSA will continue its focus

on the safety and soundness of the financial services sector and ensuring that consumers are

protected from unfair practices.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 8

To date, the financial entities regulated by BCFSA, as a whole, have shown resilience in the face

of the risks posed by the pandemic. BCFSA will continue to monitor the marketplace to ensure:

(i) consumer expectations are met by the products they have purchased; (ii) misconduct is

addressed particularly when targeted towards vulnerable British Columbians; and (iii) that new

and innovative products are understood and appropriately regulated.

Annual Economic Statement

B.C.’s economy has been resilient to pandemic, geopolitical and climate-related disruptions.

However, higher interest rates are expected to weigh on the economy in the coming years.

Following a rapid recovery from the economic impacts of the COVID-19 pandemic, high

inflation led to successive interest rate increases from the Bank of Canada in 2022. The impact

of higher interest rates has been evident in housing markets and there is uncertainty over its

transmission to the rest of the economy in B.C. and among our trading partners. B.C. is

heading into this challenging period in relatively strong position, with a low unemployment

rate. The Economic Forecast Council (EFC) estimates that B.C. real GDP expanded by 3.0 per

cent in 2022 and expects growth of 0.5 per cent in 2023 and 1.6 per cent in 2024. Meanwhile

for Canada, the EFC estimates growth of 3.4 per cent in 2022 and projects national real GDP

growth of 0.5 per cent in 2023 and 1.5 per cent in 2024. As such, B.C.’s economic growth is

expected to be broadly in line with the national average in the coming years. The risks to B.C.’s

economic outlook center around interest rates and inflation, such as the risk of further

inflationary supply chain disruptions, the potential for more interest rate increases than

expected, and uncertainty around the depth and timing of the impact on housing markets.

Further risks include ongoing uncertainty regarding global trade policies, the emergence of

further COVID-19 variants of concern and lower commodity prices.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 9

Performance Planning

BCFSA will engage in regular communications with the Ministry of Finance toward the

achievement of the goals as well as on matters within its regulatory accountabilities.

Goal 1: Enhance Risk Based Supervision

Risk based supervision forms the foundation for a modern, effective, and efficient supervisory

approach. Specifically, the approach is to ensure risk assessments are forward-looking and

focused on key risks facing the system while addressing these risks in a proportional manner

relative to severity and impact.

Objective 1.1: Advance BCFSA’s risk-based and proportionate

supervision of the financial services sector and efforts to enhance the

overall safety and soundness of the sector.

BCFSA’s supervisory mandate relates to the safety and soundness of the sector and includes

overseeing financial institutions and pension funds. Protecting the public is a key part of this

mandate. A proportionate approach to supervision is required to protect the public while

recognizing that sector participants vary in size and complexity. BCFSA’s framework for risk-

based supervision is informed by federal and international standards as adjusted for local

market realities.

Key Strategies

• Continual review of BCFSA’s supervisory framework (the “Supervisory Framework”)

ensures a consistent and modern approach to supervision of the financial services

sector that evolves with the changing macro-economic environment risk drivers to

remain a relevant tool overseeing the B.C. financial services sector.

• Revise the Supervisory Framework as required to reflect and align advancements in

BCFSA’s regulatory approach with other federal and provincial regulators including the

management of risks related to cyber, anti-money laundering, and retail credit.

• Develop an internal operational playbook for supervisory activities to enable a

consistent methodology and approach to proportionate monitoring and risk

assessment reviews reflective of varying size, scope, and complexity of regulated

entities in BC.

• Design and pilot of monitoring processes to complete risk assessments for pension

plans. This risk assessment process, based on application of the risk framework, will

include both desk and on-site reviews.

Discussion

In order to deliver against BCFSA’s key strategic imperatives for safety and soundness of the

financial services sector, developing, maintaining, and implementing an agile Supervisory

Framework that can reflect the changing financial service and market environments is critical.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 10

Fundamental elements of risk-based, proportional, and forward-looking oversight

methodologies are imbedded within the Supervisory Framework. BCFSA will focus on the key

risks including credit, market, and operational risk such as interest rates and climate change,

while ensuring the sector has an awareness of current, emerging, and potential risk drivers

requiring effective governance and risk management oversight by each regulated Financial

Institution. Supporting this, at least one (1) meeting per quarter (in-person or virtual) with

each financial institution (credit union, insurance company, and trust company) will be

conducted and supervisory letters will be delivered no later than 60 days from the exit

meeting.

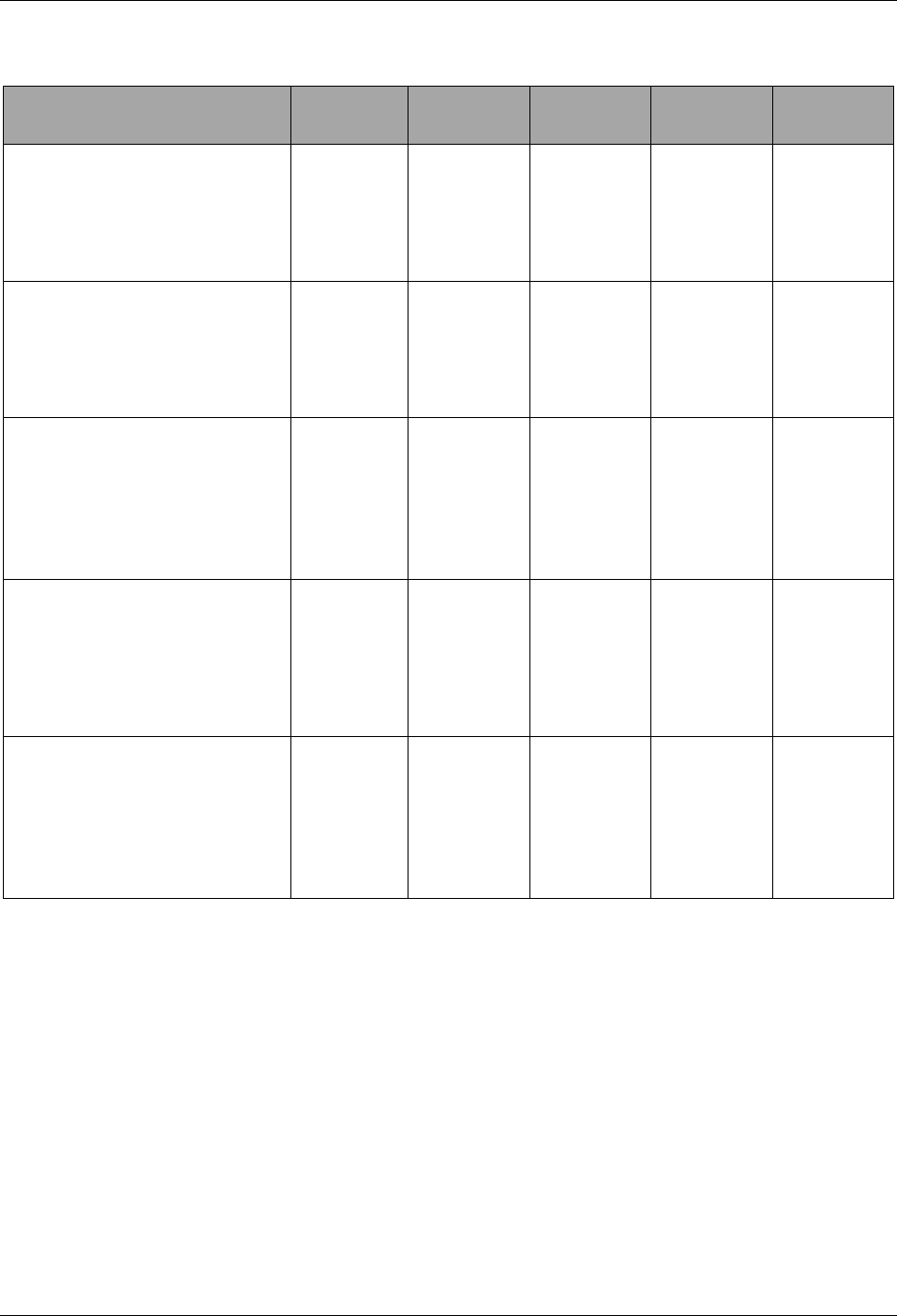

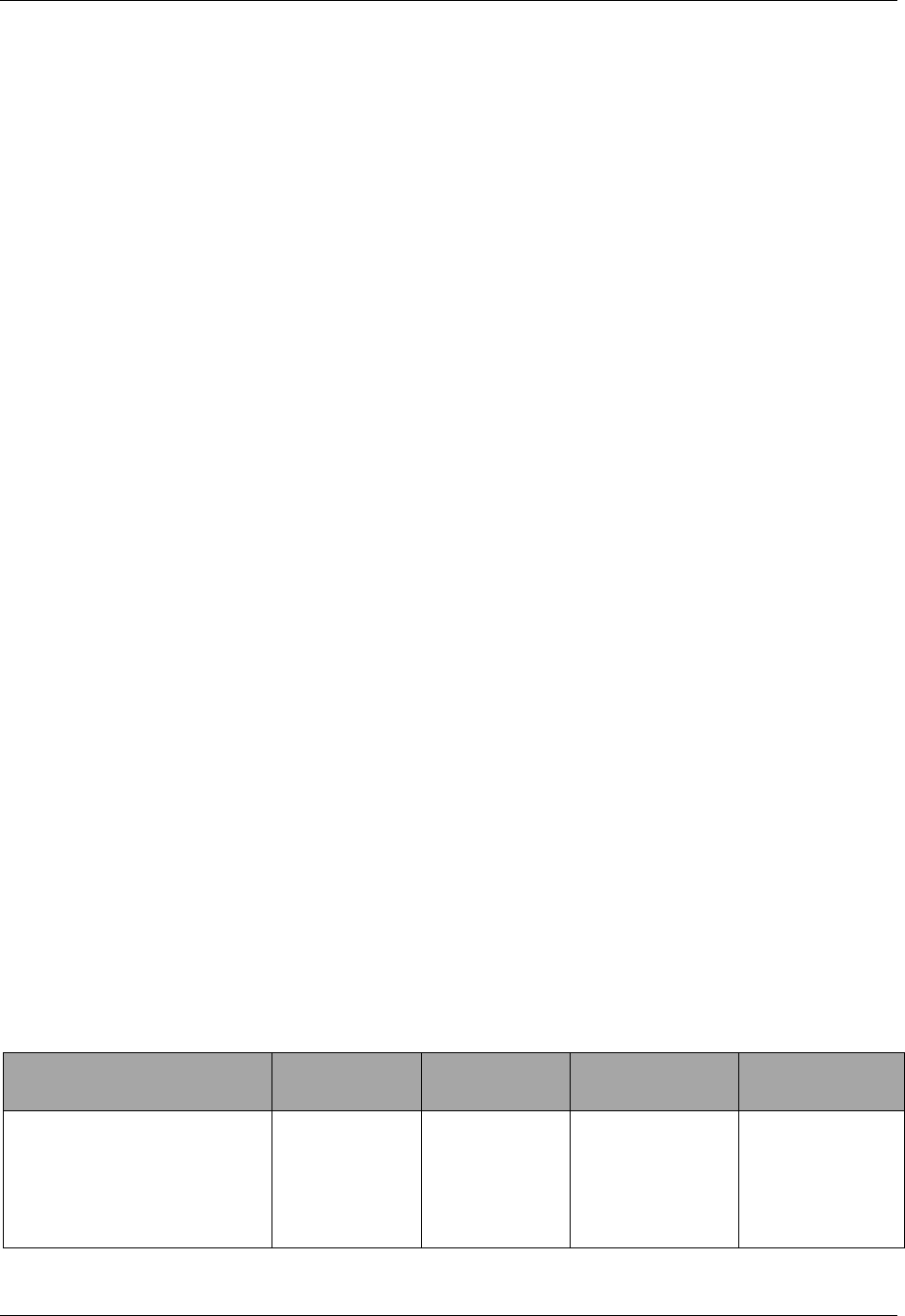

Performance Measures

Performance Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[1a] Supervisory Framework

to be reviewed at least

annually for applicability with

revisions as required to reflect

changes in the financial

services environment (new

risks) and evolution in BCFSA

tools and risk assessment

processes or priorities.

100%

reviewed and

revised as

needed

100%

reviewed and

revised as

needed

100%

reviewed and

revised as

needed

100%

reviewed and

revised as

needed

[1b] Percentage of

supervisory meetings

(includes in person and virtual

meetings) with financial

institutions (credit unions,

insurance companies and

trust companies) in the fiscal

year.

100% 100% 100%

100%

Data source: BCFSA Operational Data

Discussion

Ensuring the Supervisory Framework reflects current and emerging risk drivers is foundational

to modern, effective, and efficient supervision of the financial services sector. The Supervisory

Framework provides the methodology which BCFSA follows in assessing the risk profiles of

regulated entities.

The goal for increasing supervisory meetings is to establish a mutual understanding of issues

facing B.C. financial institutions and foster a better understanding of the issues by BCFSA.

Through the expanded engagement with the Provincially Regulated Financial Institutions,

there is a shared accountability for ensuring regular dialogue between stakeholders remains

key to ensuring the ongoing strength and viability of the. financial services system. These

quarterly meetings have been facilitated with the use of virtual meeting platforms, greatly

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 11

enhancing the effectiveness and efficiency of these engagements for both the Provincially

Regulated Financial Institutions and BCFSA.

Goal 2: Provide effective consumer protection

BCFSA protects British Columbians by upholding conduct standards in the financial services

sector including credit unions, insurance companies, trust companies, pension plans,

mortgage brokers, real estate licensees, and real estate developers.

Objective 2.1: Modern, effective, and efficient consumer protection

regulation.

BCFSA supports effective consumer protection by administering a range of proactive

monitoring activities (i.e., audit/examination programs, and industry data calls and surveys) to

identify and respond to emerging risks, and by setting robust requirements for registration or

licensing with BCFSA. In circumstances where there is non-compliance, the goal of BCFSA’s

compliance and enforcement model ensures that BCFSA is to resolve complaints efficiently

using proportionate discipline actions to enforce regulatory requirements.

Key Strategies

• Assess each complaint for risk, assign a priority, and action appropriately to provide a

timely and responsive resolution.

• Proactively monitor market conduct activities to identify and intervene to address

harmful business practices in the financial services sector.

• Entry standards to apply more focus on identifying and responding to higher risk

applications, which require more information gathering and investigation to

adequately assess an individual’s or entity’s suitability to do business in B.C.

• Review all real estate developer disclosures for completeness and risk ensuring that

consumers can make informed decisions when purchasing strata properties.

• Explore opportunities to expand the use of the regulatory toolbox (e.g., administrative

penalties) to take proportionate and meaningful enforcement action to address non-

compliance across all regulated segments.

Discussion

BCFSA protects consumers though the implementation of a multipronged approach of setting

entry-to-practice requirements, proactive monitoring of compliance, and taking proportionate

enforcement action for non-compliance.

BCFSA will continue to ensure that all applicants that are licensed or registered have the

knowledge and skills that are required so that their practice meets high standards of

professionalism. A focus on entry standards will ensure suitable applicants undergo

appropriate examination to ensure they do not pose a risk to consumers.

Regulated entities will continue to be proactively monitored to ensure that they are complying

with regulatory requirements. Where issues are identified, BCFSA may intervene to address

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 12

harmful business practices in the financial services sector. BCFSA will also risk-asses all

allegations for non-compliance, and action complaints appropriately to provide a timely and

responsive resolution.

Where required, BCFSA may require more complete disclosure from developers, or exercise

regulatory powers including orders to cease marketing.

Objective 2.2: Support industry to adopt best practice conduct

standards

BCFSA provides industry with resources, knowledge, and education to support regulated

entities to understand regulatory requirements and obligations and to ensure that they

maintain a high conduct of standards, at all times, in their practice. Many regulated entities are

required to complete continuing education courses as part of the licence or registration

renewal cycle to ensure that they maintain and enhance their skills and that they understand

their role in the protection of the public.

Key Strategies

• Develop and expand continuing education standards.

• Develop and deliver continuing education for mortgage brokers by 2024.

• Equip industry with the information, tools, and practices to help it comply with its

market conduct accountabilities.

Discussion

Consumers rely on financial services at key moments in their life – buying a home, obtaining a

loan, protecting their health and possessions and retirement – and must have trust and

confidence in the services they are receiving.

Consumers are protected by having services delivered by competent and ethical regulated

entities and individuals. The availability of relevant resources that address emerging risks

across the sector is critical to ensuring that regulated entities and individuals have the tools

that they need to properly service consumers in accordance with regulatory requirements.

Continuing education supports consistency in knowledge and high standards of

professionalism and service delivery among regulated entities and individuals.

BCFSA is committed to continuous improvement in industry education. That commitment

includes a focus on key competencies and current issues (for example, anti-money laundering)

and exploration of opportunities to leverage infrastructure to service the needs of other

regulatory sectors.

In 2023/24, BCFSA will continue to publish resources and guidelines to respond to new

regulatory requirements or emerging industry risks and trends. This will include education and

resources to support the implementation of new rules for real estate teams.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 13

Objective 2.3: Work collaboratively with government to improve

financial crisis preparedness and in particular, ensure a sustainable and

effective deposit insurance program is in place.

CUDIC is a statutory corporation continued under the Financial Institutions Act (“FIA”) and

administered by BCFSA. CUDIC is responsible for administering and operating the credit union

deposit insurance fund. CUDIC guarantees the deposits and non-equity shares (issued before

January 1, 2020) of British Columbia incorporated credit unions.

As part of maintaining the deposit insurance fund and guarantee, CUDIC pro-actively plans for

unlikely credit union failures which requires depositors to be paid out from the fund. Financial

crisis preparedness requires CUDIC and BCFSA to work across the entire credit union system

and with other regulatory agencies.

BCFSA and CUDIC are committed to working collaboratively with government to maintain

preparedness and confidence in the credit union system, in the face of changes such as credit

union consolidations and federal continuance, new technologies, climate impacts, and

economic landscape.

Key Strategies

• Implement the approved BCFSA Differential Premium System (“DPS”). BCFSA and CUDIC

are committed to maintaining a modern, effective, and efficient methodology in

determining deposit insurance premiums that responds to the needs of a rapidly

changing credit union system and its depositors.

• Review and set Deposit Insurance Fund Size, reflecting international best practices, to

ensure the Fund size is credible and contributes to depositor confidence and system

stability.

• Review, every four years, the approach, and parameters used to determine the

adequacy of the current target Fund range, target point and funding timeline

leveraging research of cross-jurisdictional best practices regarding the establishment

of deposit insurance fund targets and consult with credit union system and industry

associations.

• BCFSA will review and update as necessary the Manual and Playbook as matters evolve.

• Work collaboratively with Government in continuous improvement in payout readiness,

including contingent funding provisions.

Discussion

Main

tenance of an appropriate Deposit Insurance Fund Size, a fair and equitable assessment

of insurance premiums, and continuous improvement in payout readiness are critical

elements in protecting depositors in B.C. BCFSA and CUDIC are committed to maintaining a

modern, effective, and efficient methodology in determining deposit insurance premiums that

responds to the needs of a rapidly changing credit union system and its depositors.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 14

This is a forward-looking process that involves data collection, analysis, forecasts, and scenario

modelling. In 2023/2024, BCFSA will implement an updated differential premium system that

was approved in June 2021. BCFSA will continue to communicate and engage with the credit

unions and industry associations until implementation occurs and premiums are collected and

processed by CUDIC.

BCFSA is committed to reviewing the CUDIC Deposit Insurance Fund (the “Fund”) target size at

least every four years, or after a shock event (e.g., economic shocks, changes to credit union

system composition due to material consolidations or federal continuance). This reflects),

reflecting international best practices, to ensure the Fund size is credible and contributes to

depositor confidence and system stability. Actions undertaken can include reviewing of the

approach and parameters used to determine the adequacy of the current target Fund range,

target point and funding timeline, leveraging research of cross-jurisdictional best practices

regarding the establishment of deposit insurance fund targets as well as consulting with the

credit union system and industry associations.

CUDIC is committed to continuous improvement of the CUDIC Deposit Payout Program and

the CUDIC Deposit Payout Program Policy Manual and Playbook which outline the policies,

processes, and procedures to be followed in an event of a credit union deposit payout. A

prompt deposit payout of most deposits is required to ensure financial stability of the credit

union system and to protect depositors from undue loss.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 15

Performance Measures

Performance Measure[s]

2022/23

Baseline

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[2a.i] Percentage of

complaints resolved within 3

months of receipt

1

resulting

in timely & responsive

outcomes

Establish

Baseline

75% 75% 75%

75%

[2a. ii] Increase monitoring of

market conduct activities

1

to proactively identify and

prevent harmful business

practices

Establish

Baseline

132

monitoring

activities

130

monitoring

activities

130

monitoring

activities

130

monitoring

activities

[2a.iii] Percentage of

complete applications

(requiring no further

investigation) for new

licensees processed within 15

business days of receipt

2

90% 90% 90% 90%

90%

[2a. iv] Mortgage broker

relicensing continuing

education required for

relicensing is developed and

delivered by BCFSA

2

Develop

Project

Plan

50% of

courses

developed

&

delivered

by BCFSA

100% of

courses

developed

&

delivered

100% of

courses

developed

&

delivered

100% of

courses

developed

&

delivered

[2a.v] Real estate

development and strata

rental disclosures are

reviewed and responded to

within 20 business days of

receipt

2

90% 90% 90% 90%

90%

Data source: BCFSA operational data

1

No baseline available, given 2.a.i and ,2a.ii are combined measures that will include operations of BCFSA, Real Estate

Council of BC, and Office of the Superintendent of Real Estate prior to their integration on August 1, 2021

2

New measures from calendar days to business days.

Discussion

Shorter average turnaround times on complaints demonstrates responsiveness to public

interest in timely resolution of the issues they raise with the regulator. In 2022/23, BCFSA will

establish a baseline that reflects the higher volume of complaints that BCFSA is managing and

the alignment of systems, processes, and file management practices that has occurred since

the integration of the real estate regulators in 2021/22.

An increase in market conduct monitoring activities demonstrates BCFSA’s commitment to

resourcing and growing its proactive market conduct supervision capabilities. Monitoring

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 16

activities across BCFSA’s regulated sectors may include audits, targeted examinations of

specific regulated entities and individuals, increased data collection and reporting

requirements, thematic reviews of products or business practices, the issuance of regulatory

expectations, and implementation of industry codes of conduct.

BCFSA is committed to efficient and effective processing of real estate and mortgage broker

applications to do business in B.C., without compromising the need to undertake a thorough

review and investigation of high-risk applications to prevent unsuitable individuals and entities

from doing business in B.C.

Consumers should be able to expect consistent levels of competence and ethics from real

estate licensees and mortgage brokers. There is an established and robust continuing

education program for real estate licensees consisting of two mandatory regulated courses. By

adopting this program for mortgage brokers, BCFSA will raise standards for this sector by

building off BCFSA’s integrated approach to regulating the financial services sector.

Timely review of filed disclosures helps to ensure that deficiencies and risks are identified

early, and addressed by developers, to better protect the purchasers of multi-unit

developments.

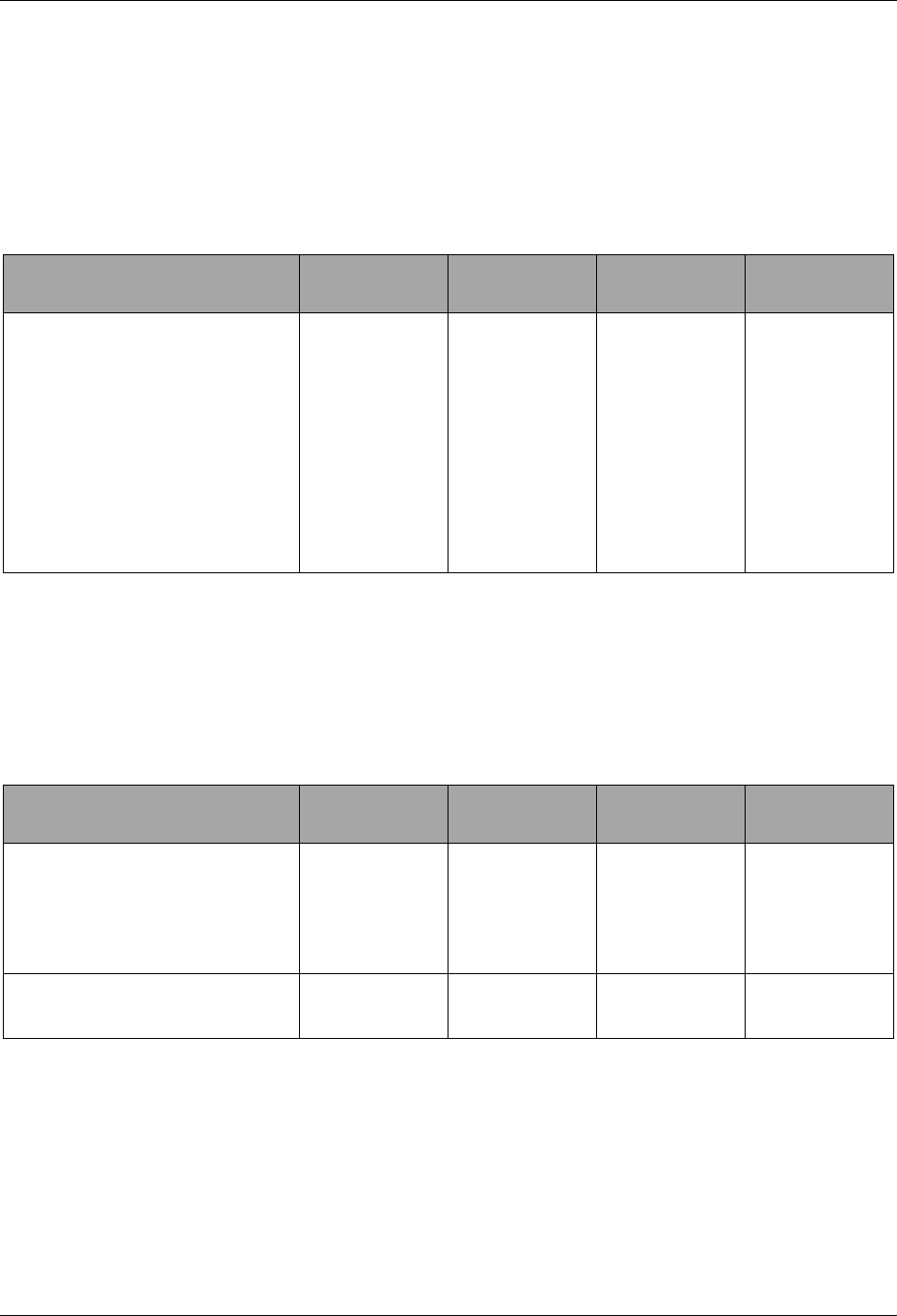

Performance Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[2b.i] Complete

implementation of the

Differential Premium System.

Target 100%

100% of

implementation

completed

N/A N/A

[2b. ii] Review and set Deposit

Insurance

1

fund size.

Completed

for current

review cycle

N/A N/A

Commence

next review

cycle

[2b.iii] Continuous review and

update of the CUDIC Deposit

Payout Program

25% of

material

updated

75% of material

updated

95% of

material

updated

Continuous

improvement

Data source: BCFSA operational data

1

Previous references to Deposit Insurance assessment methodology have been updated to Differential Premium System.

Discussion

CUDIC and BCFSA are committed to maintaining a modern, efficient, and effective

methodology for setting deposit insurance premiums that respond to the needs of a rapidly

changing credit union system and its depositors. Industry consultation and engagement is an

ongoing cornerstone of that commitment. BCFSA will build on consultations that led to

approval of the methodology in June 2021 and continues to engage the credit unions prior to

implementation in 2023/24.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 17

Reflecting international best practices, BCFSA is committed to reviewing the Fund target size

every four years, or after a shock event, to ensure the Fund size is credible and contributes to

depositor confidence and system stability. In 2020/21, BCFSA engaged an actuarial firm to

provide independent actuarial analysis and advice to the BCFSA and CUDIC Boards of Directors

on the Fund target range, target point, and funding timeline. The actuarial modelling is part of

a comprehensive internal review of both quantitative and qualitative factors, including

regulatory powers and practices. The current cycle of Fund size review was completed in

2022/23.

Continuous improvement of the Deposit Payout Program is an important component of

BCFSA’s crisis preparedness initiatives in the case of Credit Union deposit payout. A prompt

deposit payout of most deposits is required to ensure financial stability of the credit union

system and to protect depositors from undue loss.

Goal 3: Stakeholders are consistently and purposefully

engaged by BCFSA.

In order to regulate effectively, including in a proportionate manner, BCFSA needs to engage

with regulated entities and individuals to understand their views, challenges, and

opportunities. External engagement supports BCFSA’s understanding of risks to industry and

consumers of financial services.

Objective 3.1: Maintain strong and active collaboration with

stakeholders.

BCFSA is focused on engaging with stakeholders, which enables the organization to have a

better understanding of how to develop and advance its regulatory priorities, as well as

continually monitoring risks in the financial services sector.

Key Strategies

• Consult with sector participants on regulatory projects identified in BCFSA’s regulatory

roadmap.

• Develop best practices for these consultations in 2023/24 to ensure consultations are

comprehensive and appropriate to risk and complexity.

• Report against the timely delivery of roadmap projects to stakeholders as measured by

activities occurring within two quarters of their planned timeframe.

Discussion

BCFSA uses different strategies to maintain strong and active engagement with stakeholders.

It uses the regulatory roadmap as a primary means to communicate, and increasingly, receive

feedback on regulatory priorities. The roadmap outlines BCFSA’s regulatory agenda for the

coming three fiscal years. As these are priority projects, sector participants can expect to be

consulted in a comprehensive manner with respect to the project’s impacts on the sector.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 18

Objective 3.2: Stakeholder engagement strategy is operationalized.

BCFSA is building its capacity in external engagement and has expanded existing tools and

strategies to encompass a cross-financial services sector approach. A cross-financial services

approach is one which includes the entire financial services sector regulated by BCFSA to

ensures consistency of approach across the sector. BCFSA has developed and has

operationalized a stakeholder engagement strategy and will advance deliverables against that

strategy.

Key Strategies

• Focus on standing up industry advisory groups to ensure that sector input and

feedback is captured at both a technical and strategic level.

• Implement strategic roundtables for segments regulated by BCFSA.

• Formalize use of technical working groups for feedback from sector participants on

regulatory initiatives; and

• Deliver on an inaugural cross-financial services sector with relevance for all of BCFSA’s

regulated entities and individuals.

Discussion

BCFSA will operationalize its stakeholder engagement strategy by standing up industry

advisory groups and delivering on an inaugural cross-financial services sector event. These

activities are anticipated to become part of BCFSA’s steady-state operations.

Objective 3.3: Strategic communications plan activated

Stronger forward-looking communications efforts will support BCFSA’s goals to build stronger

relationships with all external stakeholders, ensure important regulatory measures are

followed, increase consumer awareness, and allow for refinement of content to make it more

relevant and available to stakeholders.

Key Strategies

• Enhance current communications activities and planning measures by operationalizing

the approved strategic communications plan,

• Ensure deliverables are on-time and completed to a high standard.

• Operationalize use of data analytics and reporting to drive external activities,

commencing internal communications reporting measures by sector to increase

website visitor numbers, email open rates, survey participation and adjust

content/vehicles where required to ensure greater sector engagement.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 19

Discussion

To ensure effective communication by BCFSA to all regulated entities, stakeholders as well as

consumers through its newly developed strategic communications plan, will enhance strategic

planning, implement new ways of working through technology, and boost data analysis to

allow for effective and targeted content development.

Performance Measures

Performance Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[3a] Significant regulatory

projects are included Develop

BCFSA’s consulted on with

sector participants reporting

on how accurate the roadmap

planning is by reporting on

whether activities occur within

two quarters of when planned

on the roadmap

100% of

roadmap

items

consulted;

60% of

activities

happening

within two

quarters

100% of

roadmap

items

consulted;

75% of

activities

happening

within two

quarters

100% of

roadmap

items

consulted;

75% of

activities

happening

within two

quarters

100% of

roadmap

items

consulted;

80% of

activities

happening

within two

quarters

Data source: BCFSA operational data

Discussion

Significant regulatory projects should be included on the regulatory roadmap and the subject

of consultations with sector participants. Use of the regulatory road map demonstrates

consistency and transparency in planning and communicating BCFSA’s external engagement

objectives regarding its regulatory program.

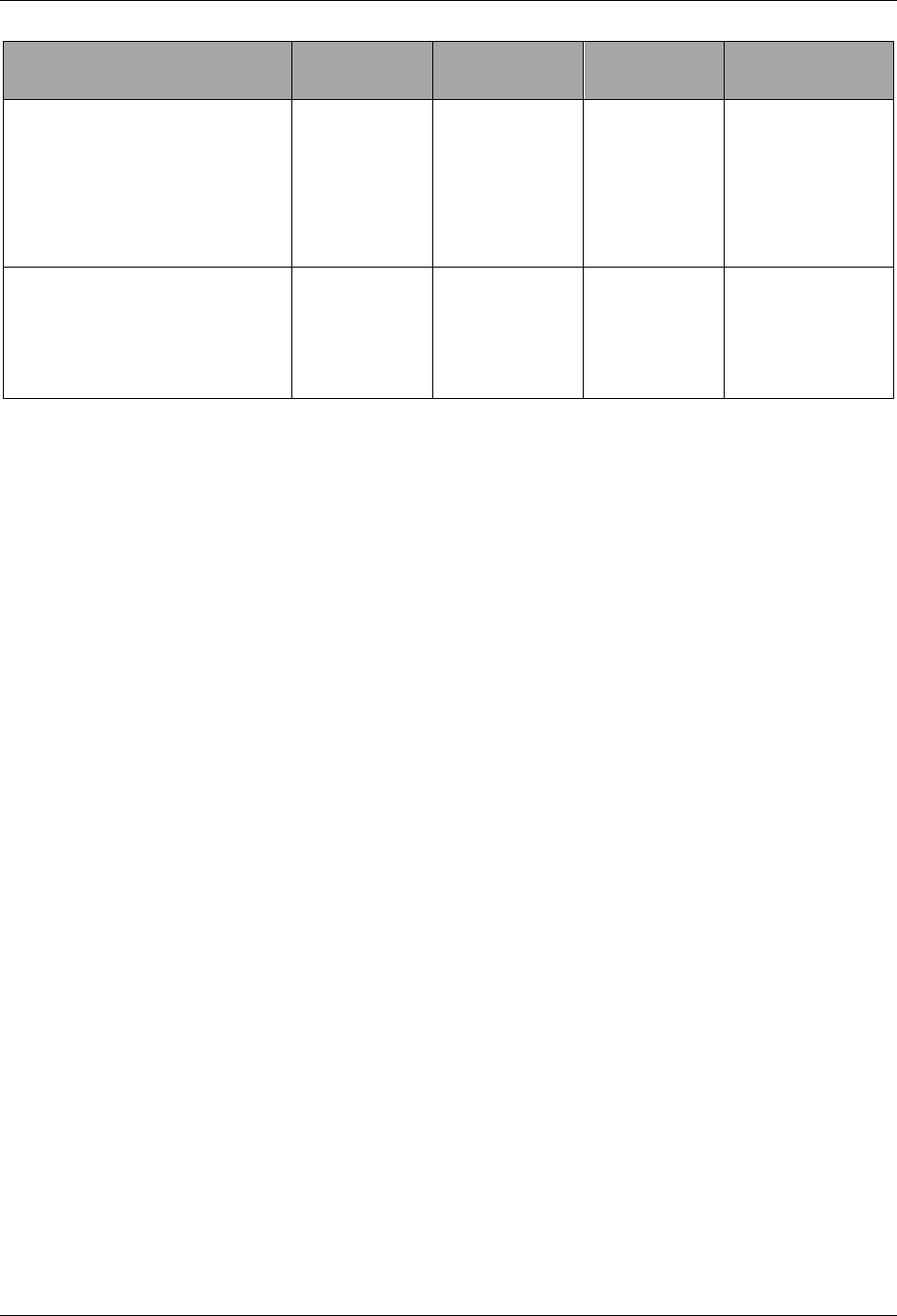

Performance Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[3b] Industry Advisory Groups

formed

Advisory

group

strategy

developed

Stand-up

advisory

group

strategy

Maintain and

refine

advisory

group

strategy

Maintain and

refine

advisory

group

strategy

[3c] Cross-sector event

established

Plan cross-

sector event

Deliver cross-

sector event

Deliver cross-

sector event

Deliver cross-

sector event

Data source: BCFSA operational data

Discussion

Operationalizing a stakeholder engagement strategy which encompasses all BCFSA of the

financial services sectors will promote consistency across the organization, allow for

consideration of best practices and build on existing tools. It will promote consistent and

purposeful engagement and communications with stakeholders.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 20

Performance Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[3d.i] Execute against multi-

year communications

strategy and update annually.

All external sector activities

identified and action plan

underway.

N/A

80%

completion of

annual

activities

90%

completion

of annual

activities

Renewed

communications

audit

undertaken, and

strategy

updated

[3d. ii] Data analysis and

reporting used to make

improvements to

communications activities.

N/A

Benchmarking

and KPIs set

Quarterly

reporting

established

Reset baseline

and new KPIs

set to align with

organizational

goals

Data source: BCFSA operational data

Discussion

Executing against the multi-year communications strategy will build upon current tools,

successes, and best practices to enhance external regulatory content and boost awareness of

BCFSA in the public environment. Strategy will be evaluated and updated annually. Work will

begin in 2025/26 to plan for a consumer strategy. Alongside strategy execution, commence

reporting practices and use of analytical data to allow BCFSA to modernize, target and ensure

communications activities are effective. These activities are anticipated to become part of

BCFSA’s steady-state operations.

Goal 4: Timely Response to Legislative Changes and

Priorities

BCFSA is responsive to a changing regulatory environment and to government priorities in

relation to protection of consumers of financial services in B.C.

Over the past year, BCFSA concluded its follow-on work from its 2020 report: Strengthening

Foundations: A Report on the State of Strata Insurance in British Columbia on the state of the

strata insurance market.

BCFSA also responded to the direction from the Minister of Finance to engage with industry

and experts to provide advice to Government on the parameters of a cooling-off period for

residential real estate transactions, as well as other measures that could enhance

transparency and increase protection for real estate consumers in B.C. This contributed to the

Government bringing the Home Buyer Rescission Period into effect in January 2023, with

extensive work being undertaken by BCFSA in preparing real estate licensees for the new

regulatory requirements.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 21

Objective 4.1: Work with Government to implement the new Mortgage

Services Act.

The Mortgage Services Act, the new legislation, which received Royal Assent on November 3,

2022, is responsive to several recommendations set out of the Cullen Commission Report on

Money Laundering in BC, released on June 15, 2022. The Mortgage Services Act will modernize

the mortgage broker industry in B.C. and greatly expand BCFSA’s tools to regulate the

mortgage broker segment. BCFSA will have the ability to set standards of conduct and

enhance disclosure and reporting obligations through new rule-making powers. BCFSA will

also be able to leverage enhanced compliance and enforcement processes and issue greater

penalties for misconduct.

Key Strategies

• Work with government on the development of regulations and rules to complete the

regulatory framework and manage transition from the previous framework.

• Adapt BCFSA’s compliance and enforcement program to accommodate new regulatory

tools and requirements.

• Execute against a project plan to implement the Mortgage Services Act, including

development of rules, regulations, education, and compliance processes, as well as the

technology changes needed to support the new regulatory regime. develop education

to support mortgage brokers, update pre-licensing education requirements, develop

continuing education and related support material.

Discussion

This legislative change has a profound impact on the regulation of the mortgage broker

segment in B.C. Operationalization of the change will be a phased, multi-year project and will

involve resources across all departments of BCFSA, as well as engagement with stakeholders

and a significant communications and education program.

Education will be developed to support mortgage brokers in understanding the new

regulatory regime and the implications for their business practices and to provide appropriate

educational resources for consumers to understand the new regime and their rights and

responsibilities in it.

Pre-licensing education requirements will be reviewed and updated to incorporate regulatory

changes.

Continuing education and related support material will be developed to ensure licensees

understand and are compliant with new regulatory requirements

Technology changes to accommodate the new licensing regime will be implemented and

compliance and enforcement processes will be adapted as required and appropriate.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 22

Objective 4.2: Collaborate with government and stakeholders to

improve the effectiveness of B.C.’s Anti-Money Laundering Regime

In 2023/24, BCFSA will continue with its efforts to strengthen B.C.’s Anti-Money Laundering

(“AML”) regime by implementing new initiatives where appropriate, sustaining existing

approaches and initiatives, and working with stakeholders to support a broad and integrated

approach to AML in B.C.

Key Strategies

• Fully participate in all relevant activities supporting and strengthening the B.C. AML

regime.

• Provide advice to government, where required, and participate on policy development

and operational matters related to B.C.’s AML regime.

• Develop and implement, as appropriate, an AML strategy to further the government’s

legislative and policy response to the Cullen Commission Report on Money Laundering

in BC released on June 15, 2022 (the “Cullen Commission”).

Discussion

BCFSA will develop an AML strategy and implementation plan that responds to any future

direction from the government following the Cullen Commission. of Inquiry into Money

Laundering in B.C. AML awareness, reporting, and compliance are key obligations throughout

the financial services sector and BCFSA looks to work with government to advance B.C.’s AML

measures.

BCFSA will continue to identify and implement initiatives to strengthen B.C.’s AML regime

where appropriate. This may include undertaking activities to raise industry awareness,

expanded AML education programs, inter-agency collaboration, data collection and

benchmarking, and targeted reviews.

BCFSA is an active participant in the Counter-Illicit Finance Alliance of B.C. as it strengthens

strategic information exchange between law enforcement, industry, and regulators as well as

ongoing collaboration with FINTRAC in accordance with the MOU between BCFSA and

FINTRAC.

Performance Measures

Performance

Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[4a] Execute an

implementation project

plan for a phased approach

to the new Mortgage

Services Act.

Project plan in

place.

Initial

Regulations

and Rules

prepared and

approved.

First phase of

implementation

completed.

Full

implementation

of Mortgage

Services Act.

Data source: BCFSA operational data

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 23

Discussion

The new Mortgage Services Act aligns more closely with other financial services legislation in

B.C., including the current Real Estate Services Act, allowing for efficient regulation, and helping

to encourage responsible business conduct with more than 7,000 registered mortgages

brokers in B.C.

This will ultimately provide greater protection for both borrowers and lenders in British

Columbia and harmonize our province with other jurisdictions who have modernized their

mortgage broker legislation.

Performance Measure[s]

2022/23

Forecast

2023/24

Target

2024/25

Target

2025/26

Target

[4b] Participation in ongoing

activities supporting the

strengthening of the B.C. AML

regime

100% 100% 100% 100%

Data source: BCFSA operational data

Discussion

The performance measure demonstrates BCFSA’s commitment to supporting the

strengthening of the B.C. and Canadian AML regime.

BCFSA may receive direction from the B.C. Government on AML in 2023/24 that informs

development of a BCFSA AML strategy.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 24

Financial Plan

Financial Summary

[$000s]

2022/23

Forecast

2023/24

Budget

2024/25

Plan

2025/26

Plan

Revenue

Fees Licenses & Recoveries 65,076 64,045 66,191 67,323

Total Revenue 65,076 64,045 66,191 67,323

Expenses

Salary and Benefits 41,327 42,666 44,721 45,846

Other 23,568 21,379 21,470 21,477

Total Expenses 64, 895 64,045 66,191 67,323

Annual Surplus (Deficit) 181 - - -

Total Debt 8,914 8,914 8,914 8,914

Accumulated Surplus (Deficit) 55,271 55,271 55,271 55,271

Capital Expenditures 7,039 1,000 1,000 1,000

Note: The above financial information was prepared based on current Generally Accepted Accounting Principles.

Key Forecast Assumptions, Risks and Sensitivities

The financial plan does not include any amounts for any further increase in the BCFSA

mandate. For example, there may be future increased expenses related to improving the

effectiveness of B.C.’s Anti-Money Laundering regime, the potential scope of which has yet to

be determined.

Revenue is subject to fluctuation based on volumes or asset holdings of the regulated entities.

Revenue projections are based on an assessment of segment specific historical trends and

assumptions around changing market factors. Minimal to no growth is assumed across the

Sector. Revenue from Real Estate Licencing and associated educational is a substantial

component of revenue and is subject to uncertainty around licencing applications and renewal

rates. There are no future fee changes approved at this time and as such no increases are

included in the budget or plan.

Other expenses which include professional services, information systems, building occupancy

charges and legal fees will be subject to inflationary pressures. These expenses are expected

to reduce due to a moderation in the significant pace of change since 2019.

The financial services sector in B.C. and globally continues to rapidly evolve. BCFSA will need

modern technology and processes to keep up with these changes and its ability to evolve will

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 25

influence its ability to respond in times of crisis. Complexity and interconnectedness across,

and within sectors, necessitates a thoughtful, proportionate, and responsive regulatory

approach.

The success of B.C. and Canada’s AML framework rests on close cooperation and collaboration

between various parts of the AML regime, and failure to work together would impact BCFSA’s

ability to fulfill its mandate and effectively regulate the financial services sector.

Management’s Perspective on Financial Outlook

The ongoing funding model for BCFSA does not include financial support from the

Government of British Columbia. Most of BCFSA’s revenue comes from filing, registration and

application fees paid by regulated entities and individuals under the various statutes.

Management anticipates that revenue growth will slow in the next 2 years and that costs can

be managed to maintain a balanced budget. BCFSA will continue to monitor fees, and seek

new or changes to fees, where the costs to regulate are not supported by revenue. If the

mandate of BCFSA expands then this will require new revenue sources.

Management is committed to protecting the rights of British Columbians by promoting high

standards of market conduct within the financial services sectors we regulate. We are

continually managing costs and looking for ways to operate our business more efficiently and

effectively.

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 26

Appendix A: Mandate Letter from the Minister

Responsible

…/2

Ministry of Finance

Office of the Minister

Mailing Address: Location:

PO Box 9048 Stn Prov Govt 501 Belleville Street

Victoria BC V8W 9E2 Parliament Buildings, Victoria

Telephone: 250 387-3751 website:

Facsimile: 250 387-5594 www.gov.bc.ca/fin

480654

Stanley W. Hamilton, Chair

BC Financial Services Authority

2800 – 555 West Hastings Street

Vancouver BC V6B 4N6

Dear Dr. Hamilton:

On behalf of Premier Horgan and the Executive Council, I would like to extend my thanks to you

and your board members for the dedication, expertise and skills with which you serve the people

of British Columbia.

Every public sector organization is accountable to the citizens of British Columbia. The

expectations of British Columbians are identified through their elected representatives, the

members of the Legislative Assembly. Your contributions advance and protect the public interest

of all British Columbians and through your work, you are supporting a society in which the

people of this province can exercise their democratic rights, trust and feel protected by their

public institutions.

You are serving British Columbians at a time when people in our province face significant

challenges as a result of the global COVID-19 pandemic. Recovering from the pandemic will

require focused direction, strong alignment and ongoing engagement between public sector

organizations and government. It will require all Crowns to adapt to changing circumstances and

follow Public Health orders and guidelines as you find ways to deliver your services to citizens.

This mandate letter, which I am sending in my capacity as Minister responsible for the

British Columbia Financial Services Authority (BCFSA), on behalf of the Executive Council,

communicates expectations for your organization. It sets out overarching principles relevant to

the entire public sector and provides specific direction to the BCFSA about priorities and

expectations for the coming fiscal year.

March 24, 2021

- 2 -

…/3

I expect that the following five foundational principles will inform your agency’s policies and

programs:

• Putting people first: We are committed to working with you to put people first. You and

your board are uniquely positioned to advance and protect the public interest and I expect

that you will consider how your board’s decisions maintain, protect and enhance the

public services people rely on and make life more affordable for everyone.

• Lasting and meaningful reconciliation: Reconciliation is an ongoing process and a

shared responsibility for us all. Government’s unanimous passage of the Declaration of

the Rights of Indigenous Peoples Act was a significant step forward in this journey – one

that all Crown agencies are expected to support as we work in cooperation with

Indigenous peoples to establish a clear and sustainable path to lasting reconciliation. True

reconciliation will take time and ongoing commitment to work with Indigenous peoples

as they move towards self-determination. Guiding these efforts, Crown agencies must

also remain focused on creating opportunities that implement the Truth and

Reconciliation Commission through your mandate.

• Equity and anti-racism: Our province’s history, identity and strength are rooted in its

diverse population. Yet racialized and marginalized people face historic and present-day

barriers that limit their full participation in their communities, workplaces, government

and their lives. The public sector has a moral and ethical responsibility to tackle systemic

discrimination in all its forms – and every public sector organization has a role in this

work. All Crowns are expected to adopt the Gender-Based Analysis Plus (GBA+) lens to

ensure equity is reflected in your operations and programs. Similarly, appointments

resulting in strong public sector boards that reflect the diversity of British Columbia will

help achieve effective and citizen-centred governance.

• A better future through fighting climate change: Announced in December 2018, the

CleanBC climate action plan puts our province on the path to a cleaner, better future by

building a low-carbon economy with new clean energy jobs and opportunities, protecting

our clean air, land and water and supporting communities to prepare for carbon impacts.

As part of the accountability framework established in CleanBC, and consistent with the

Climate Change Accountability Act, please ensure your organization aligns operations

with targets and strategies for minimizing greenhouse gas emissions and managing

climate change risk, including the CleanBC target of a 50% reduction in public sector

building emissions and a 40% reduction in public sector fleet emissions by 2030. Your

organization is expected to work with government to report out on these plans and

activities as required by legislation.

- 3 -

…/4

• A strong, sustainable economy that works for everyone: I expect that you will identify

new and flexible ways to achieve your mandate and serve the citizens of

British Columbia within the guidelines established by the Provincial Health Officer and

considering best practices for conducting business during the pandemic. Collectively, our

public sector will continue to support British Columbians through the pandemic and

economic recovery by investing in health care, getting people back to work, helping

businesses and communities, and building the clean, innovative economy of the future.

As a public sector organization, I expect that you will consider how your decisions and

operations reflect environmental, social and governance factors and contribute to this

future.

The Crown Agencies and Board Resourcing Office (CABRO), with the Ministry of Finance, will

continue to support you and your board on recruitment and appointments as needed, and will be

expanding professional development opportunities in 2021/22. This will include online training

and information about provincial government initiatives to foster engaged and informed boards.

As the Minister Responsible for the BCFSA, I expect that you will make substantive progress on

the following priorities and incorporate them in the goals, objectives and performance measures

in your 2021/22 Service Plan:

• Advance the BCFSA’s risk-based and proportionate supervision of financial

services sectors and efforts to enhance consumer protection.

• Engage and work with government, other B.C. regulators, sector participants, and

applicable provincial and federal governments and regulators to identify and

respond to priority issues in the financial services sector, including issues associated

with the COVID-19 pandemic.

• Continue to work with the Superintendent of Real Estate, the Ministry of Finance

Policy and Legislation Division, and the Real Estate Council of BC to complete

integration of real estate regulation within the BCFSA.

• Work collaboratively with government to improve finance crisis preparedness and

in particular, ensure a sustainable and effective deposit insurance program is in

place.

• Continue to work collaboratively with government, industry and other stakeholders

to review issues related to the cost and availability of insurance for strata

corporations.

- 4 -

…/5

• Collaborate with government to improve the effectiveness of B.C.’s Anti-Money

Laundering Regime.

Each board member is required to sign the Mandate Letter to acknowledge government’s

direction to your organization. The signed Mandate Letter is to be posted publicly on your

organization’s website in spring 2021.

I look forward to continuing to work with you and your Board colleagues to build a better B.C.

Sincerely,

Selina Robinson

Minister

Signed by:

Stanley W. Hamilton, Chair

B.C. Financial Services Authority

Date

Wilma Simone van Norden, Vice Chair

B.C. Financial Services Authority

Date

Charles (Michael) Grist

B.C. Financial Services Authority

Date

April 6, 2021

April 6, 2021

April 6, 2021

- 5 -

…/6

Jo-Ann Shelley Hannah

B.C. Financial Services Authority

Date

Joanne Adele Hausch

B.C. Financial Services Authority

Date

Bruce Howell

B.C. Financial Services Authority

Date

Jacqueline Anne Kelly

B.C. Financial Services Authority

Date

Gerald Matier

B.C. Financial Services Authority

Date

Shannon Nicola Salter

B.C. Financial Services Authority

Date

April 6, 2021

April 6, 2021

April 6, 2021

April 6, 2021

April 6, 2021

April 6, 2021

- 6 -

John Dundas Thwaites

B.C. Financial Services Authority

Date

Joel J. Whittemore

B.C. Financial Services Authority

Date

cc: Honourable John Horgan

Premier

Lori Wanamaker

Deputy Minister to the Premier, Cabinet Secretary and Head of the BC Public Service

Heather Wood

Deputy Minister and Secretary to Treasury Board

Ministry of Finance

Douglas S. Scott

Deputy Minister, Crown Agencies Secretariat

Ministry of Finance

April 6, 2021

April 6, 2021

BC Financial Services Authority

2023/24 – 2025/26 Service Plan Page | 33

Appendix B: (RECBC) Letter of Direction from the

Minister Responsible

…/2

Ministry of Finance

Office of the Minister

Mailing Address: Location:

PO Box 9048 Stn Prov Govt 501 Belleville Street

Victoria BC V8W 9E2 Parliament Buildings, Victoria

Telephone: 250 387-3751 website:

Facsimile: 250 387-5594 www.gov.bc.ca/fin

480091

Elaine Duvall, Chair

Real Estate Council of British Columbia

900 – 750 West Pender Street

Vancouver BC V6C 2T8

Dear Ms. Duvall:

I would like to extend my appreciation to you and your board members for the dedication,

expertise and skills with which you serve the people of British Columbia.

Every public sector organization is accountable to the citizens of British Columbia. The

expectations of British Columbians are identified through their elected representatives, the

members of the Legislative Assembly. Your contributions advance and protect the public interest

of all British Columbians and through your work, you are supporting a society in which the

people of this province can exercise their democratic rights, trust and feel protected by their

public institutions.

You are serving British Columbians at a time when people in our province face significant

challenges as a result of the global COVID-19 pandemic. Recovering from the pandemic will

require focused direction, strong alignment and ongoing engagement between public sector

organizations and government. It will require all Crowns to adapt to changing circumstances and

follow Public Health orders and guidelines as you find ways to deliver your services to citizens.

This letter of direction communicates expectations for your organization. It sets out overarching

principles relevant to the entire public sector and provides specific direction on priorities and

expectations for the coming fiscal year.

I expect that the following five foundational principles will inform your agency’s policies and

programs:

• Putting people first: We are committed to working with you to put people first. You and

your board are uniquely positioned to advance and protect the public interest and I expect

March 15, 2021

- 2 -

…/3

that you will consider how your board’s decisions maintain, protect and enhance the

public services people rely on and make life more affordable for everyone.

• Lasting and meaningful reconciliation: Reconciliation is an ongoing process and a

shared responsibility for us all. Government’s unanimous passage of the Declaration of

the Rights of Indigenous Peoples Act was a significant step forward in this journey – one

that all Crown agencies are expected to support as we work in cooperation with

Indigenous peoples to establish a clear and sustainable path to lasting reconciliation. True

reconciliation will take time and ongoing commitment to work with Indigenous peoples

as they move towards self-determination. Guiding these efforts, Crown agencies must

also remain focused on creating opportunities that implement the Truth and

Reconciliation Commission through your mandate.

• Equity and anti-racism: Our province’s history, identity and strength are rooted in its

diverse population. Yet racialized and marginalized people face historic and present-day

barriers that limit their full participation in their communities, workplaces, government

and their lives. The public sector has a moral and ethical responsibility to tackle systemic

discrimination in all its forms – and every public sector organization has a role in this

work. All Crowns are expected to adopt the Gender-Based Analysis Plus (GBA+) lens to

ensure equity is reflected in your operations and programs. Similarly, appointments

resulting in strong public sector boards that reflect the diversity of British Columbia will

help achieve effective and citizen-centred governance.

• A better future through fighting climate change: Announced in December 2018, the

CleanBC climate action plan puts our province on the path to a cleaner, better future by

building a low-carbon economy with new clean energy jobs and opportunities, protecting

our clean air, land and water and supporting communities to prepare for carbon impacts.

As part of the accountability framework established in CleanBC, and consistent with the

Climate Change Accountability Act, please ensure your organization aligns operations

with targets and strategies for minimizing greenhouse gas emissions and managing

climate change risk, including the CleanBC target of a 50% reduction in public sector

building emissions and a 40% reduction in public sector fleet emissions by 2030. Your

organization is expected to work with government to report out on these plans and

activities as required by legislation.

• A strong, sustainable economy that works for everyone: I expect that you will identify

new and flexible ways to achieve your mandate and serve the citizens of

British Columbia within the guidelines established by the Provincial Health Officer and

considering best practices for conducting business during the pandemic. Collectively, our

public sector will continue to support British Columbians through the pandemic and

economic recovery by investing in health care, getting people back to work, helping

businesses and communities, and building the clean, innovative economy of the future.

As a public sector organization, I expect that you will consider how your decisions and

- 3 -

…/4

operations reflect environmental, social and governance factors and contribute to this

future.

As the Minister Responsible for the Real Estate Council of BC, I expect that you will make

substantive progress on the following priorities and incorporate them in the goals, objectives and

performance measures in your 2021/22 Service Plan:

• Continue to work towards the transition to a single regulator of real estate under the BC

Financial Services Authority (BCFSA). This will require coordinating with the

Superintendent of Real Estate, the Ministry of Finance Policy and Legislation Division,

and the BCFSA to align efforts to deliver seamless service to licensees and the public

before during and after the transition.

• Prior to the amalgamation under the BCFSA, reduce the backlog of complaints and

continue to reduce the time to disposition of complaints and process new licensee

applications on a timely basis.

• Continue to work collaboratively with government as it improves the effectiveness of

B.C.’s Anti-Money Laundering Regime.

As Board chair, please sign the Letter of Direction to acknowledge government’s direction to

your organization. The signed Letter of Direction is to be posted publicly on your organization’s

website in spring 2021.

I look forward to continuing to work with you and your Board colleagues to build a better B.C.

Sincerely,

Selina Robinson

Minister

Signed By:

_____________________________ _____________________________

Marian Elain Duvall, Chair Date

Real Estate Council of British Columbia

April 1, 2021

- 4 -

cc: Heather Wood

Deputy Minister and Secretary to Treasury Board

Ministry of Finance

Douglas S. Scott

Deputy Minister, Crown Agencies Secretariat

Ministry of Finance

Erin Seeley

Executive Officer

Real Estate Council of British Columbia