Published March 2024

Financial Services and

Pensions Ombudsman

Overview of Complaints

2023

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

3

Contents

1. The Financial Services and Pensions Ombudsman (FSPO) 5

2. Ombudsman’s Message 7

3. FSPO’s referral of complaints to the regulatory authorities during 2023 16

4. Complaints received by location 19

5. Sectoral Analysis 21

Banking Complaints 2023 24

Insurance Complaints 2023 25

Investment Complaints 2023 26

Pension Scheme Complaints 2023 27

Market Exit Complaints 2023 29

Disputed Transactions 31

Tracker Mortgage Complaints 2023 33

6. How we managed complaints in 2023 40

Customer Operations and Information Management 43

Dispute Resolution Services 49

Investigation Services 60

Legal Services 77

7. Report on named nancial service providers 95

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

4

Acronyms/Abbreviaons

AVCs Additional Voluntary Contributions

CBI Central Bank of Ireland

CCR Central Credit Register

COIM Customer Operations and Information Management

CPC Consumer Protection Code 2012

DRS Dispute Resolution Services

FSPO Financial Services and Pensions Ombudsman

IS Investigation Services

LS Legal Services

PRSAs Personal Retirement Savings Accounts

The Act Financial Services and Pensions Ombudsman Act

2017

The Examination Central Bank of Ireland directed Tracker Mortgage

Examination

The regulatory

authorities

The Central Bank of Ireland, the Competition and

Consumer Protection Commission, and the Pensions

Authority.

Trust RACs Trust Retirement Annuity Contracts

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

5

1

The Financial Services and

Pensions Ombudsman (FSPO)

The FSPO was established in January 2018 by the Financial Services and

Pensions Ombudsman Act 2017. The role of the FSPO is to resolve complaints

from consumers, including small businesses and other organisations, against

nancial service providers and pension providers.

We provide an independent, fair, impartial, condential and free service to resolve

complaints through either informal mediation, leading to a potential settlement

agreed between the parties, or formal investigation and adjudication, leading to a

legally binding decision.

When any consumer, whether an individual, a small business or an organisation,

is unable to resolve a complaint or dispute with a nancial service provider or a

pension provider, they can refer their complaint to the FSPO.

We deal with complaints informally at rst, by listening to both parties and

engaging with them to facilitate a resolution that is acceptable to both parties.

Much of this informal engagement takes place by telephone. Where these early

interventions do not resolve the dispute, the FSPO formally investigates the

complaint and issues a decision that is legally binding on both parties, subject only

to a statutory appeal to the High Court.

The Ombudsman has wide-ranging powers to deal with complaints against

nancial service providers. The Ombudsman can direct a provider to rectify the

conduct that is the subject of the complaint. There is no limit to the value of the

rectication that can be directed. The Ombudsman can also direct a nancial

service provider to pay compensation to a complainant of up to €500,000. In

addition, the Ombudsman can publish anonymised decisions and can also publish

the names of any nancial service provider that has had at least three complaints

against it upheld, substantially upheld, or partially upheld during a calendar year.

When dealing with complaints against pension providers, the Ombudsman’s

powers are more limited. While the Ombudsman can direct rectication, the

legislation governing the FSPO sets out that such rectication shall not exceed

any actual loss of benet under the pension scheme concerned.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

6

Furthermore, the Ombudsman cannot direct a pension provider to pay

compensation. The Ombudsman can only publish case studies in relation to

pension decisions (not the full decision) and cannot publish the names of any

pension provider irrespective of the number of complaints it may have had

upheld, substantially upheld, or partially upheld against it during a calendar year.

Formal investigation of a complaint by the FSPO is a detailed, fair and impartial

process carried out in accordance with fair procedures. For this reason,

documentary and audio evidence and other material, together with submissions

from the parties, is gathered by the FSPO from those involved in the dispute and

exchanged between the parties.

Unless a decision is appealed to the High Court, the nancial service provider or

pension provider must implement any direction made by the Ombudsman in a

legally binding decision. Decisions appealed to the High Court are not published

while they are the subject of an appeal.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

7

2

Ombudsman’s Message

I am very pleased to publish this Overview of Complaints for 2023. The FSPO’s

mission is to provide an impartial, accessible, and responsive complaint resolution

service that delivers fair, transparent and timely outcomes for all our customers,

and enhances the nancial services and pension environment. This Overview

serves as a resource for all those who can have an impact on the nancial services

and pension environment, and I would encourage providers to reect on the

nature of the complaints brought to this Ofce, and what I consider to be missed

opportunities in some situations, to have resolved those complaints internally, at

an earlier stage.

I will begin by thanking the entire FSPO team for their hard work and

commitment throughout the year. Due to their concerted efforts, the FSPO closed

5,184 complaints in 2023. This is a 12% increase on the number of complaints

closed in 2022. In doing so, we delivered outcomes worth over €4.7 million to

consumers.

At the same time, we received a record number of complaints. In 2023, the FSPO

received a total of 6,182 complaints, representing a 29% increase on the number

received in 2022.

It is clear that we need to further grow the capacity of the FSPO to meet

the growing challenges. In this regard, 2023 was an important year for the

organisation, as the Minister for Finance provided sanction to increase our

workforce by 42% from 90 to 128. This increase in resources, combined with our

work to continuously increase efciency will signicantly impact on the capacity

of the Ofce to deliver for our customers.

It is also important for providers to consider what measures they can take

to reduce the number of complaints arising. An increase of almost 30% in

the number of complaints being made to the Financial Services and Pensions

Ombudsman in just one year, should be a cause for reection amongst providers.

Where appropriate, the FSPO will do what we can to assist providers in their

work to reduce complaints. We meet with providers and their representatives

and discuss trends in complaints received. We have published over 2,300 legally

binding decisions in relation to complaints against nancial service providers.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

8

Our annual Overview of Complaints and our Digests of Decisions, which provide

analyses and examples of complaints and decisions are also useful resources for

both providers and consumers.

In addition to encouraging providers of nancial services and pension products

to work to reduce the number of complaints arising, I also encourage them to

adopt an approach of seeking, where possible, to resolve complaints quickly with

their customers. It is clear that many of the consumers making complaints to this

Ofce could have had their complaints addressed by their provider, at an earlier

point in time.

Even after a complaint has been made to the FSPO, there continue to be

opportunities for providers and consumers to resolve their complaints informally.

Mediation has been central to our efforts to resolve complaints at the earliest

stage and since the introduction of mediation as the default complaint resolution

process used by the FSPO, we have achieved very considerable success in

facilitating the resolution of complaints by agreement, directly between

providers and their customers. Typically, more than 70% of complaints referred to

mediation are successfully resolved through the mediation process.

Outcomes

The outcomes for those who bring complaints to this Ofce can be signicant.

During 2023, 5,184 complaints were closed, and the outcomes of these

complaints included the following:

1,275 complainants achieved a mediation settlement through our Dispute

Resolution Service, with the value of those settlements totalling €2,943,493.

A further €1,271,754 was paid to complainants by providers to settle

complaints during the FSPO’s formal investigation process.

The combined value of compensation directed in legally binding decisions

following the formal investigation process was €321,330.

An additional €175,543 in redress from providers was noted by the FSPO as

available for acceptance by complainants, leading to legally binding decisions

where those complaints were not upheld because the offer in question was

reasonable and adequate to redress the conduct giving rise to the complaint,

and no formal direction by the Ombudsman was required.

These outcomes do not include the very signicant but unquantiable benets

of redress by rectication, secured by complainants, through a legally binding

direction of the FSPO. Examples of such rectication outcomes are detailed on

page 62.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

9

Timelines

Although the number of complaints received increased considerably in 2023,

many of these complaints were resolved early on in our processes. I would

encourage both consumers and providers to take advantage of the swift

resolutions that can be achieved through our informal dispute resolution

process. Mediation has proven to be an effective and timely method of resolving

complaints to the satisfaction of all involved.

In 2023:

85% of complaints that closed in 2023, were closed within 12 months

of the complaint being made. This was mainly through resolution in our

Dispute Resolution Services (mediation) and early-stage assessments and

interventions in our Customer Operations and Information Management

department. This includes when a complaint was resolved directly between

the parties, or if a complaint fell outside the jurisdiction of the FSPO.

For all complaints that closed in 2023, including tracker mortgage complaints,

the average time from receipt of complaint to closure, was 8.6 months.

For non-tracker mortgage complaints that closed in 2023, the average time

from receipt to closure, was 7 months.

Certain more complex complaints, including those requiring a formal adjudication

process or formal jurisdictional assessment, or both, take longer to resolve.

This reects the fact that adjudications by the Ombudsman are legally binding

and accordingly, it is important that every decision arrived at, has followed due

process and allowed both parties to make submissions and offer observations on

the evidence and on the other party’s submissions, as appropriate.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

10

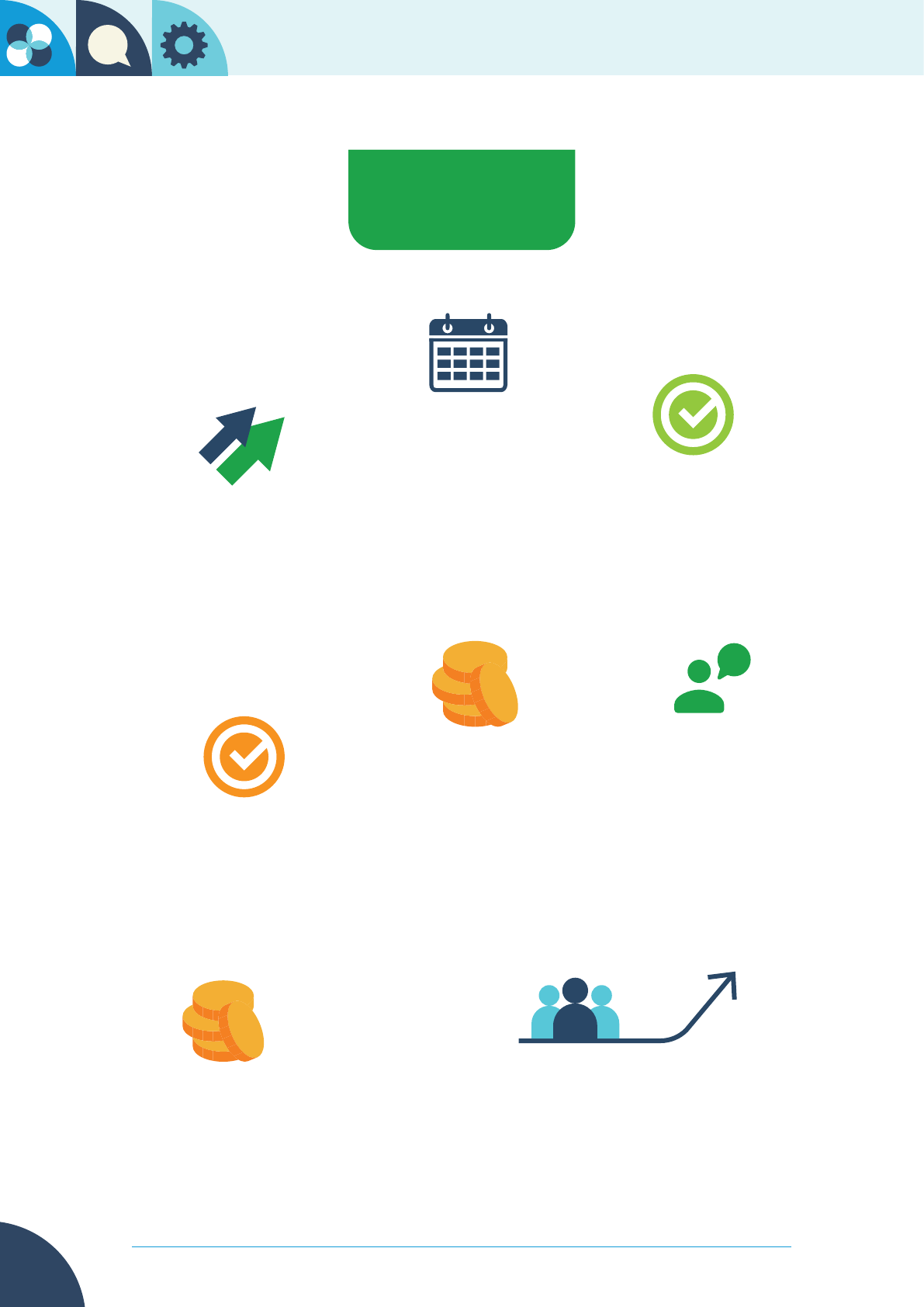

Complaints that

closed

complaints received

Non-tracker

mortgage

complaints closed

of banking

complaints

involved disputed

transactions.

Total

compensation

directed in legally

binding decisions

Workforce plan approved. Staff

to increase from 90.2 to 128

Value to the

complainant of our

Dispute Resolution

Services

24%

6,182

2023

29%

Average time

to closure

Average time

to closure

7 months

of complaints that

closed, were closed

within 12 months

42%

increase

€2,943,493

€321,330

85%

?

8.6 months

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

11

Referrals to the authorities

I had cause to formally refer 9 legally binding decisions to the Central Bank of

Ireland (CBI) during 2023. Referrals take place for a variety of reasons including

in circumstances where a complaint raises the possibility of a potentially systemic

issue, which may warrant consideration by the regulatory authorities.

For example, I referred two decisions where I was concerned that there appeared

to be a shortfall in the guidance available to regulated nancial service providers

under the Central Credit Register framework, in situations of bankruptcy, or

insolvency arrangements (decision 2023-0082 and decision 2023-0083).

In another decision, I noted the provider’s incorrect approach to its Central Credit

Register reporting obligations, in relation to accounts where the card had been

revoked, and I was concerned that this may well have impacted other customers

(decision 2023-0256).

In addition to these 9 decisions formally referred, I shared copies of 107 tracker

mortgage decisions, and 26 decisions issued in complaints concerning declined

insurance claims for business interruption losses, with the CBI in 2023.

Sharing information and our perspective, with the regulatory authorities is a vital

part of our stakeholder engagement and ensures that potentially systemic issues

are raised for consideration with the appropriate regulatory body, for such action

as may be appropriate.

Customer Service

Customer service remains the primary source of complaints made by consumers

to this Ofce in 2023, representing 24% of all such complaints. Complaints

relating to customer service issues can include a provider’s failure to provide

information, and accessibility and communication issues. It is also common

for complainants to reference failures during the provider’s internal complaint

handling process. I believe that a more responsive service from providers to their

customers, could avoid many of these complaints arising.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

12

Complainants referencing fraud

The upward trend continues in the number of complainants referencing fraud.

Financial fraud is becoming more sophisticated, and as technology moves ahead in

leaps and bounds, it can often result in even the savviest of consumers falling prey

to seemingly legitimate, but fraudulent, schemes and scams.

It is important to note that the FSPO cannot investigate instances of fraud, as that

is a matter for An Garda Síochána. However, the FSPO can investigate a complaint

which relates to suggested service failings of the nancial service provider in

dealing with a customer who suspects fraud on their account, and any complaint

about disputed transactions.

This Overview highlights some of these complaints, through the use of

anonymised case studies, where the customer came to the FSPO because they felt

their bank had not dealt with their issue appropriately.

One case study highlights the case of Diana who complained to her bank after

she had transferred €2,720 to an online trading platform, which she said was then

transferred to a fraudulent investment company. Diana hoped her bank could

recover her money through the chargeback process. Although the bank still held

Diana liable for the transactions, it noted some service issues with the handling

of her complaint. The bank noted that Diana had been credited €1721.23 by the

online trading company and offered to refund Diana an additional €1,720 as a

gesture of goodwill.

In another case study, Marie was the victim of a scam, which was carried out by

fraudsters claiming to be from the Department of Social Protection and An Garda

Síochána. Marie was informed by the fraudsters that someone had stolen her

identity, and that this person was suspected of money laundering. She transferred

€17,000 to a foreign bank account before she realised it was a scam. Although the

bank emphasised it was not responsible for Marie’s loss, it did acknowledge that

its customer service fell short of its standards. It offered Marie €4,000 in full and

nal settlement of her complaint, which she accepted.

Eileen was an elderly lady who sent a total of €82,000 to a care worker abroad,

as a result of an ad she had seen online. She nally realised that she had been the

victim of a scam when there was no sign of the care worker coming to Ireland.

Eileen’s bank said that Eileen had authorised all of the payments herself, so it was

not responsible for the loss. However, Eileen said that the bank staff member

never queried why an 80-year-old woman was sending so much money, so often,

to a very distant country. The parties resolved the dispute in mediation and on

that basis, the bank agreed to refund Eileen’s money.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

13

Market Exits

It is important to note one area of success in efforts to limit the number of

complaints arising. The departure of two major nancial service providers from

the Irish market, posed the potential for a high volume of complaints to be made

to this Ofce, given the number of impacted customers. During 2023, this Ofce

received 236 complaints identied as relating to market exit, though not all of

these complaints were in relation to the conduct of those providers leaving the

market. A total of 162 complaints relating to market exit were closed during the

year, mainly through our Registration and Assessment or Dispute Resolution

Services.

It is very positive that, to date, for the vast majority of impacted consumers,

the departure of two major banks has not given rise to issues leading to a

complaint being made to this Ofce. This outcome was achieved through the

work of many stakeholders, including providers and their representatives. The

FSPO contributed by collaboratively engaging and sharing information with

stakeholders within the Irish banking sector, including with the providers leaving

the market.

In 2022, we began tracking complaints relating to market exit in order to identify

market exit complaints from the time they were received. We engaged with

those providers leaving the market, regarding their processes and plans for

resources to address both current and future complaints. We identied trends

and patterns and shared insights with relevant internal and external stakeholders.

This enabled earlier intervention to better manage issues, as appropriate,

thereby preventing new complaints arising and facilitating earlier resolution of

complaints. Complaints in relation to market exit were assessed and progressed,

as appropriate, in the same way as other ongoing complaints.

Tracker Mortgage related complaints

During 2023, the FSPO received 74 complaints relating to tracker mortgage

interest rates. This represents a signicant decline from the 139 such complaints

received in 2022 and is signicantly lower than in 2020, when the number of

tracker mortgage interest rate complaints received peaked, at 492 in the year.

These complaints continue to comprise a considerable portion of the work of

the FSPO, as they progress through both the informal dispute resolution process

and the formal investigation process. In 2023, this Ofce closed 224 tracker

mortgage related complaints, with 892 tracker mortgage complaints on hand at

the end of the year.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

14

I directed €38,000 in total compensation in 4 legally binding decisions concerning

tracker mortgages, which were either substantially upheld or partially upheld in

2023. A total of 103 tracker mortgage complaints were not upheld.

This Overview contains links to some of the decisions issued on tracker mortgage

interest rate complaints which may be of benet to consumers who may be

considering making a complaint, to their representatives and to providers.

My rst full year as Financial Services and Pensions Ombudsman has been

rewarding, and I look forward to another year ahead, working to deliver on our

mission of providing an impartial, accessible, and responsive complaint resolution

service that delivers fair, transparent and timely outcomes for all our customers,

and enhances the nancial services and pension environment.

Financial Services and Pensions Ombudsman (Amendment)

Bill 2023

I welcome the publication of the Financial Services and Pensions Ombudsman Bill

2023. The Bill aims to copperfasten the protection of consumers in their access

to the Financial Services and Pensions Ombudsman (FSPO) to make complaints

about the conduct of nancial service providers which have left the Irish market.

The Bill also introduces legislative amendments to ensure the Financial Services

and Pensions Ombudsman continues to discharge its statutory functions in

line with the Constitution, following a Supreme Court Decision regarding the

Workplace Relations Commission. In the context of the Bill, discussions have

also included the jurisdiction of this Ofce with regard to complaints about the

conduct of credit servicing rms and loan owners, prior to 2019. This Ofce will

continue to engage with the Minister and the Department in relation to these

matters as the Bill continues its passage through the Oireachtas.

Acknowledgements

I am grateful to all who contributed to the work of the Financial Services and

Pensions Ombudsman over the course of 2023.

I have already referenced the hard work and commitment of all of my colleagues

in the FSPO. Their continued dedication to our values of fairness, independence,

effectiveness, accessibility and integrity is greatly appreciated. I wish to thank

my colleagues on the Senior Management Team, MaryRose McGovern, Deputy

Financial Services and Pensions Ombudsman, Diarmuid Byrne, Director of

Dispute Resolution, Tara McDermott, Director of Customer Operations and

Information Management, Úna Gately, Director of Investigation Services and Áine

Carroll, Director of Corporate and Communication Services for their hard work

and dedication.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

15

I would also like to thank the Chairperson, Maeve Dineen, and members of the

Financial Services and Pensions Ombudsman Council for their support, guidance

and assistance during 2023.

Finally, I wish to express my appreciation to the Minister for Finance, Michael

McGrath TD, and his ofcials for their ongoing support and cooperation.

Liam Sloyan

Financial Services and Pensions Ombudsman

March 2024

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

16

3

FSPO’s referral of complaints

to the regulatory authories

during 2023

Section 18 of the Financial Services and Pensions Ombudsman Act 2017 (the Act),

as amended, requires the Ombudsman to cooperate with the Central Bank of

Ireland, the Competition and Consumer Protection Commission, and the Pensions

Authority (the “regulatory authorities”) in a way that contributes to promoting

the best interests of consumers and actual or potential beneciaries of nancial

or pension services, and to the efcient and effective handling of complaints.

The Act facilitates the sharing of information by the Ombudsman with the

regulatory authorities, for the purpose of the performance of the functions of the

Ombudsman, under the Act.

During 2023, the FSPO shared a copy of every legally binding decision issued,

concerning a complaint about a tracker mortgage rate of interest, with the Central

Bank of Ireland (CBI). Copies of 107 tracker mortgage decisions were sent by the

FSPO to the CBI.

The same approach was adopted for 26 legally binding decisions issued in

complaints concerning declined insurance claims for business interruption losses.

In addition to those decisions, the FSPO also refers other legally binding decisions

to the regulatory authorities, with a view to promoting the best interests of the

consumer protection framework. Referrals take place for a variety of reasons

including in circumstances where a complaint raises the possibility of a potentially

systemic issue, which may warrant consideration by the regulatory authorities.

The table below sets out the complaints which, during 2023, were referred by the

FSPO to the Central Bank of Ireland for those reasons.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

17

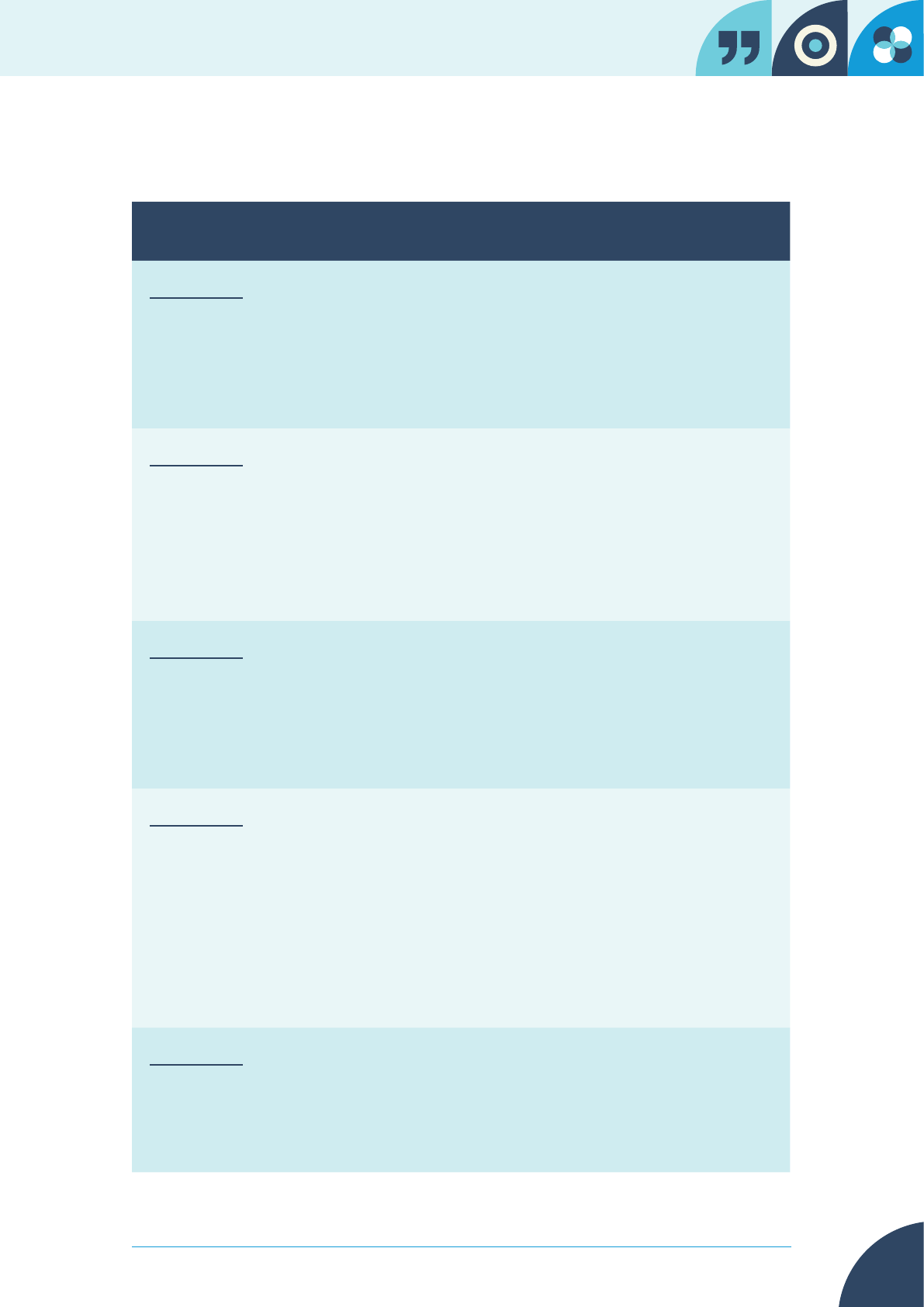

Fig. 3.1 - Complaint issues referred to the Central Bank of Ireland during 2023

Decision reference Issue raised by the complaint

2023-0160 The Ombudsman was concerned at the provider’s

reliance on a policy exclusion in its claim decision

which was no longer applicable, and which

the provider had acknowledged was an error.

This raised a potentially systemic issue in the

provider’s claim decisions.

2023-0082 The Ombudsman was concerned about an

apparent shortfall in the guidance available to

regulated nancial service providers under the

Central Credit Register framework, in situations

of bankruptcy, which can include complex sets of

circumstances, such as in the background to this

complaint.

2023-0083 The Ombudsman was concerned about an

apparent a shortfall in the guidance available to

regulated nancial service providers under the

Central Credit Register framework, in situations

of bankruptcy, or insolvency arrangements, such

as in the background to this complaint.

2023-0091 The Ombudsman was concerned that the terms

of an insurance policy in the section outlining

the cover and in the section outlining exclusions,

taken together made the policy confusing and

made it difcult for a consumer to understand

the nature and the limits of such cover, because

of the interplay between the policy wording. This

created a potentially systemic issue arising from

the likely confusion caused.

2023-0032 The Ombudsman was concerned at the poor

record keeping practices of the provider

demonstrated in its response to this complaint

and the potential impact of this on other

customers.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

18

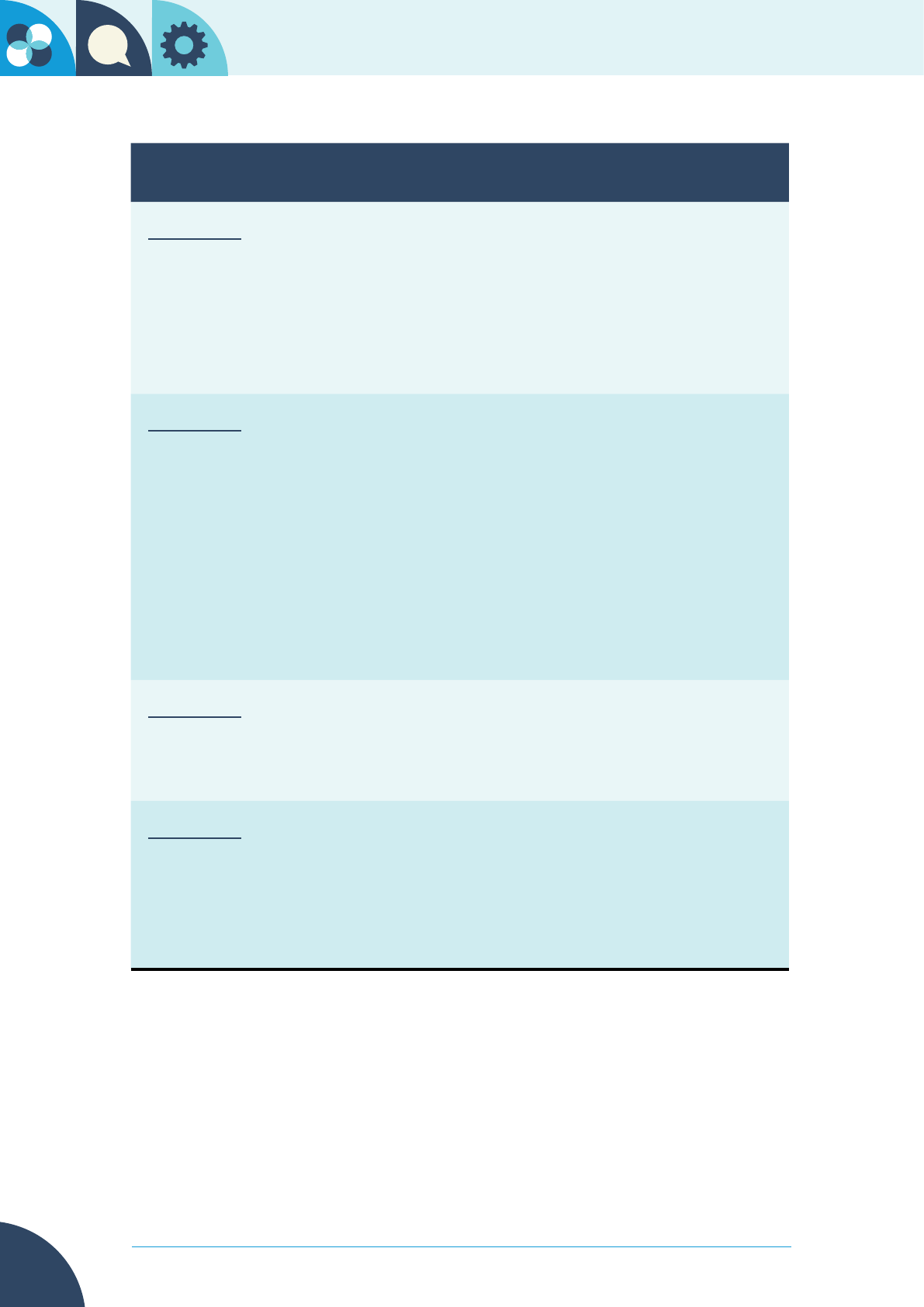

Decision reference Issue raised by the complaint

2023-0024 The Ombudsman was concerned that the

interplay between two separate policy provisions

failed to meet the provider’s obligation under

Provision 2.6 of the Consumer Protection Code,

to make relevant material information available to

its policyholder, in a way that seeks to inform, and

that this issue could be systemic in nature.

2023-0023 The Ombudsman was concerned about the

provider’s failure to comply with all of its

obligations pursuant to Chapter 2 of Consumer

Protection Code, which the Ombudsman was

satised constituted conduct contrary to law

within the meaning of Section 60(2)(a) of the

Financial Services and Pensions Ombudsman

Act 2017, relating to errors in dealing with the

claim, in circumstances where the policy offered

no cover or policy benets for the policyholder’s

situation.

2023-0256 The Ombudsman was concerned that the

provider’s incorrect approach to reporting

accounts where the card had been revoked, may

have impacted other customers.

2023-0254 The Ombudsman was concerned about the

likely confusion caused by policy provisions

which included a denition of “gross prot” that

deviated from its well-established and generally

understood meaning, without that signicant

difference being adequately highlighted.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

19

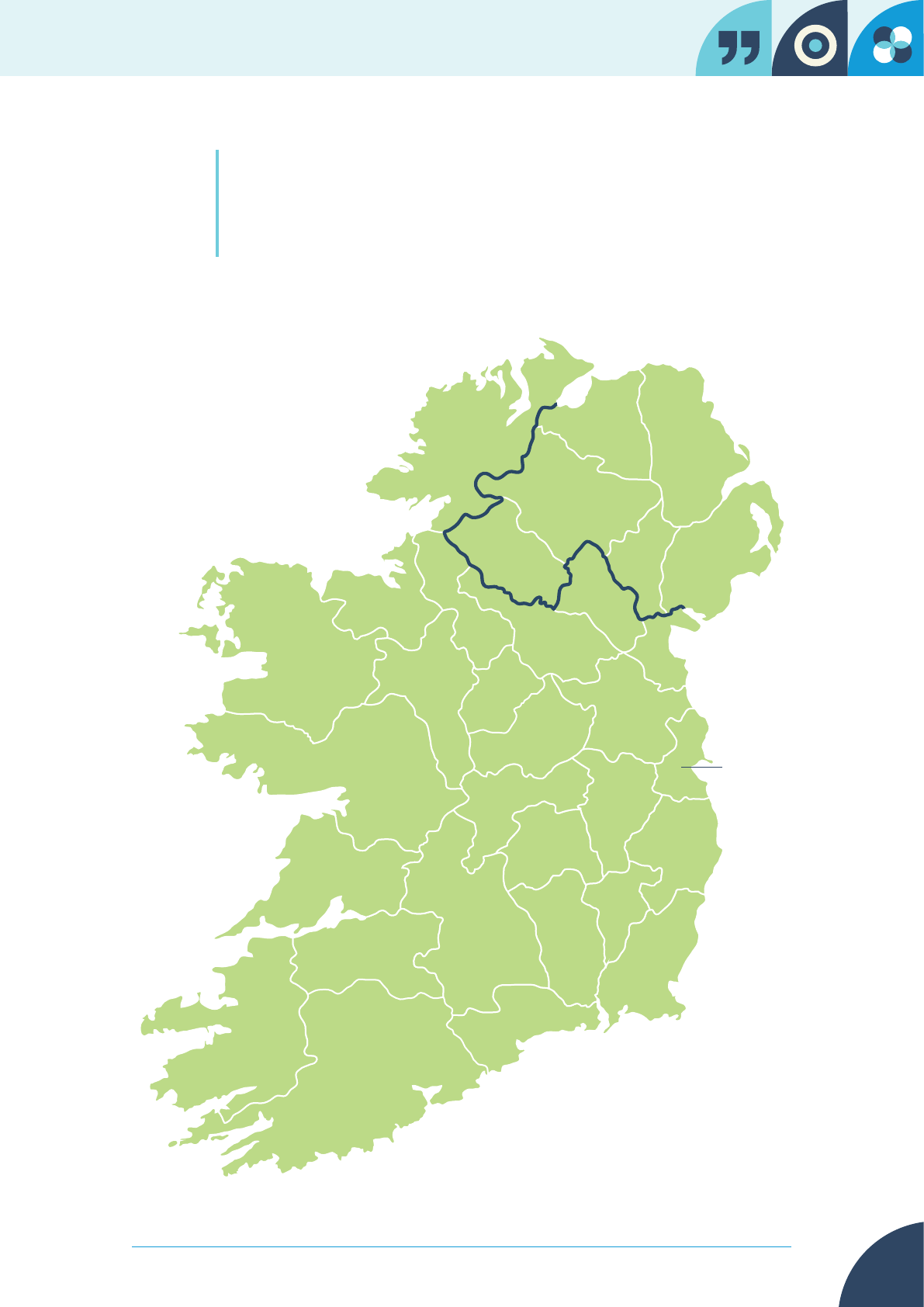

4

Complaints received by locaon

Louth

133

Dublin

1,746

Leitrim

24

Kilkenny

84

Sligo

59

Donegal

135

ROI Total

4,969

NI Total

30

Fermanagh

5

Tyrone

0

Derry

7

Antrim

10

Down

7

Armagh

1

Roscommon

55

Mayo

102

Cavan

73

Longford

38

Monaghan

56

Westmeath

74

Meath

265

Carlow

59

Kildare

283

Laois

72

Offaly

69

Limerick

158

Clare

101

Kerry

115

Cork

506

Waterford

108

Wexford

134

Wicklow

181

Galway

203

Tipperary

136

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

20

1

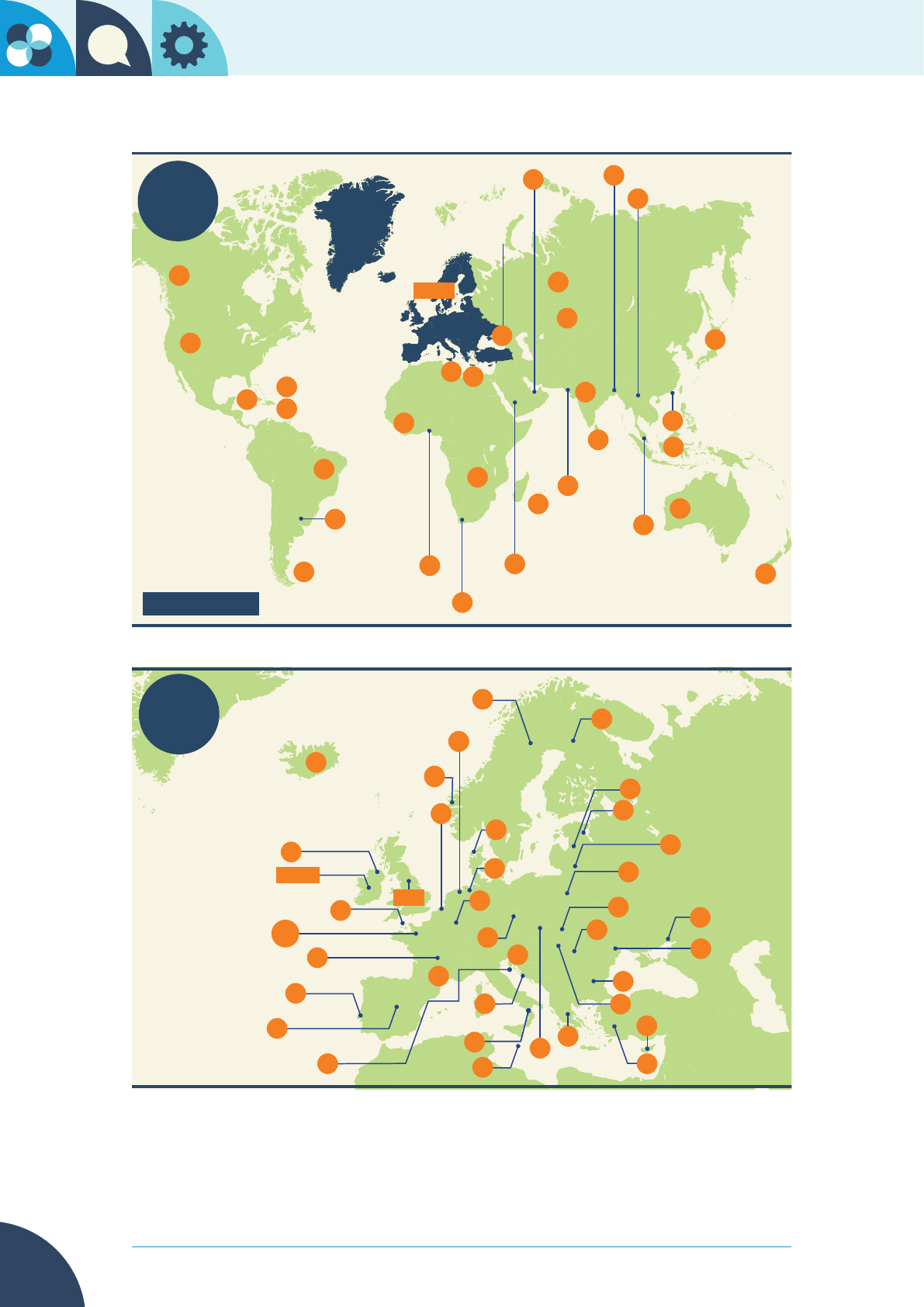

Belize

1

Guadeloupe

1

Martinique

4

Brazil

1

Thailand

2

1

India

3

Bangladesh

4

Sri Lanka

2

Singapore

Hong Kong

2

Philippines

1

Japan

5

Pakistan

1

Zambia

5

South Africa

2

Israel

1

Georgia

265 Unassigned

1

Argentina

2

Madagascar

1

Mauritius

3

Nigeria

19

USA

6

18

Australia

2

Russian

Federation

1

Kazakhstan

3

2

Saudi Arabia

9

UAE

6

New Zealand

2

Egypt

3

Ghana

Canada

Europe 5,805

Global

Total

6,182

Czechia

Netherlands

Belgium

Norway

Finland

Ireland

Estonia

Romania

Slovakia

Luxembourg

Lithuania

Malta

Bulgaria

Turkey

Italy

Poland

Denmark

Portugal

Spain

France

Guernsey

Switzerland

Germany

Austria

Bosnia and

Herzegovina

Croatia

Hungary

Cyprus

Sweden

GB

Greece

7

4

5

Latvia

4

5

Moldova

2

75

2

15

Ukraine

9

9

11

5

3

7

16

4

50

4

22

Slovenia

6

Andorra

1

128

2

Iceland

1

10

23

61

N. Ireland

30

10

83

2

3

21

5

22

169

4,969

21

5

22

Europe

5,805

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

21

5

Sectoral Analysis

This section sets out details of the complaints received in 2023 in the banking,

insurance and investment categories, as well as complaints related to pension

schemes.

A total of 6,182 complaints were received by the FSPO in 2023, a 29% increase in

comparison to 2022, where 4,781 complaints were received.

Banking complaints were the highest category of complaints received, with

3,850 complaints, or 62% of all complaints received falling into this category. This

represents a signicant increase in banking complaints to the FSPO in 2023. In

2022, 2,640 complaints received were in the banking sector.

The FSPO received 1,446 (23%) complaints relating to the insurance sector, which

accounted for the second largest category of complaints received. This compared

to 1,129 complaints received in this category in 2022.

The number of complaints received in both investment and pension categories

also rose in 2023. 461 investment complaints were received, and 336 pension

complaints were received. This compared with 366 and 233 complaints received

in these categories respectively, in 2022.

This year, the FSPO also began collecting gures for non-regulated entities and 74

complaints made about the conduct of such entities, were received.

13 complaints were labelled ‘not applicable’. This occurs where there is not

enough detail given by the complainant to assign a sector before closing the

complaint, or where the complaint was not for the nancial sector. At year end,

two complaints received had not yet been assigned to a sector. This happens

when we are waiting for further information from the complainant to enable us to

correctly determine the sector.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

22

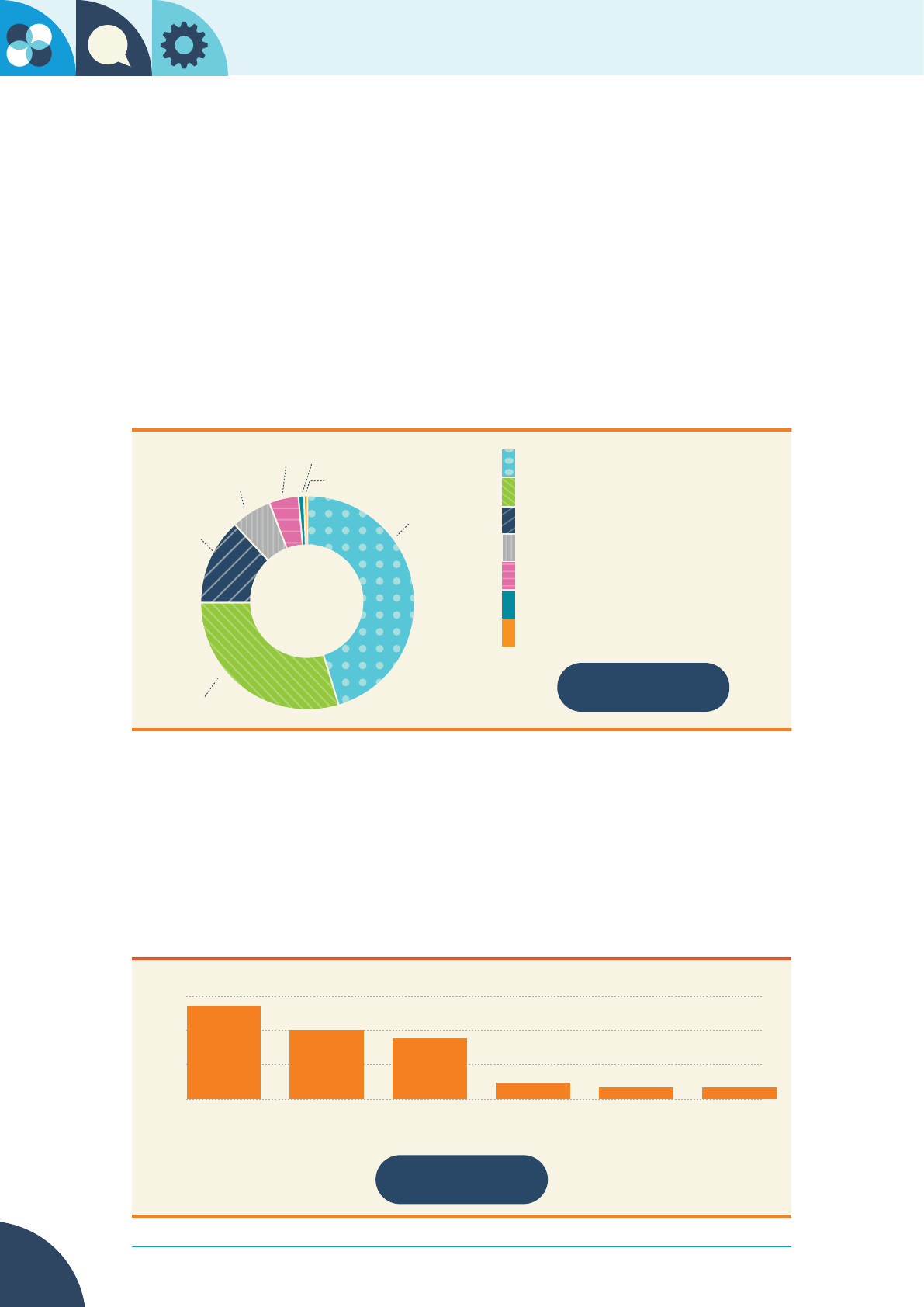

Fig. 5.1 Complaints received by sector 2023

Banking

3,850

62%

Insurance

1,446

23%

Pension Schemes

336

5%

Investment

461

7%

Not applicable

13

<1%

Non-regulated

74

1%

Unassigned at year end

2

<1%

Complaints received by sector

€

Total complaints received 6,182

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

23

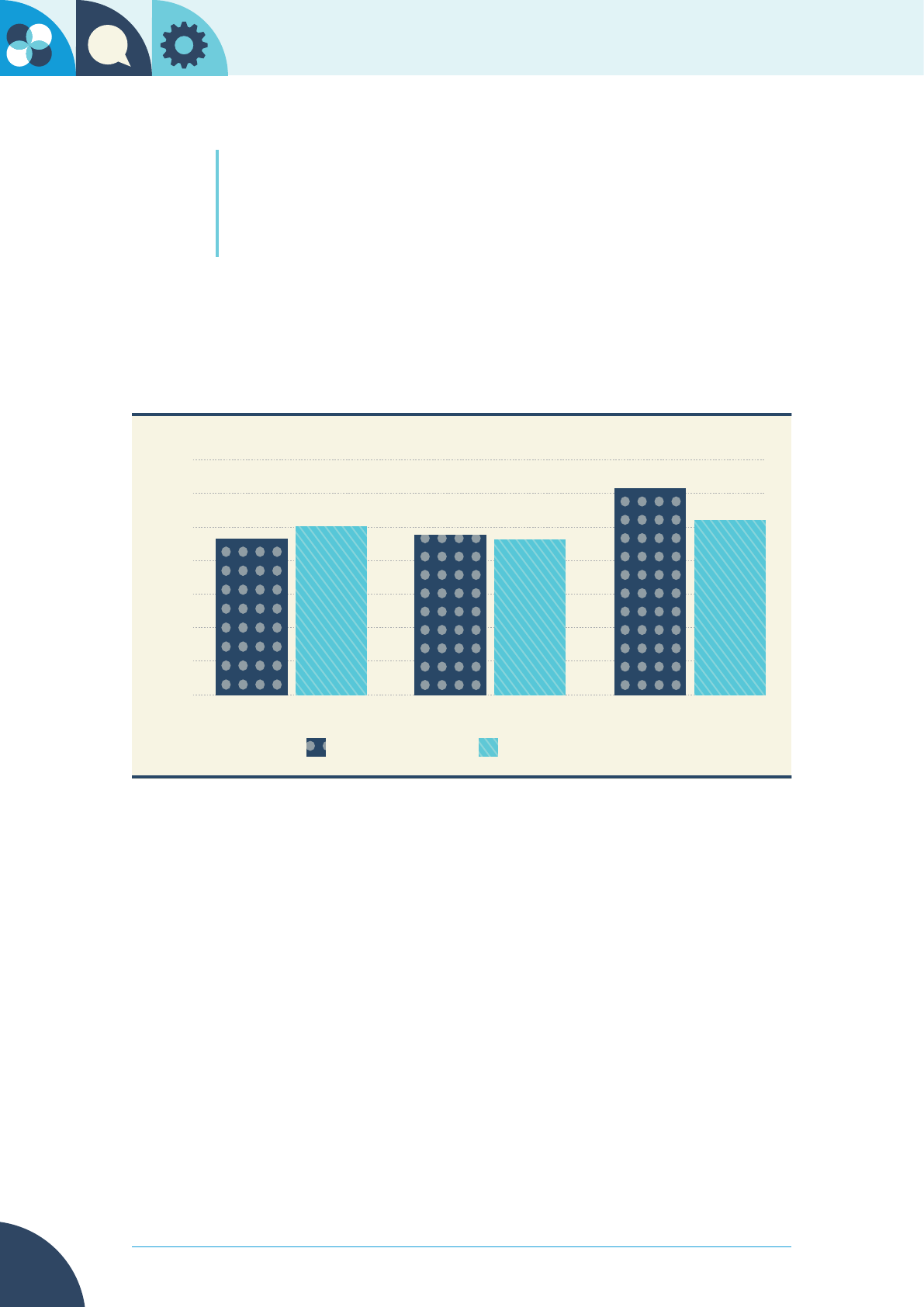

As in 2022, customer service was the conduct most complained of in 2023, with

24% of complaints relating to this conduct. Customer service complaints relate

to complaints which include issues such as communications, complaint handling,

account access issues and the failure to provide information.

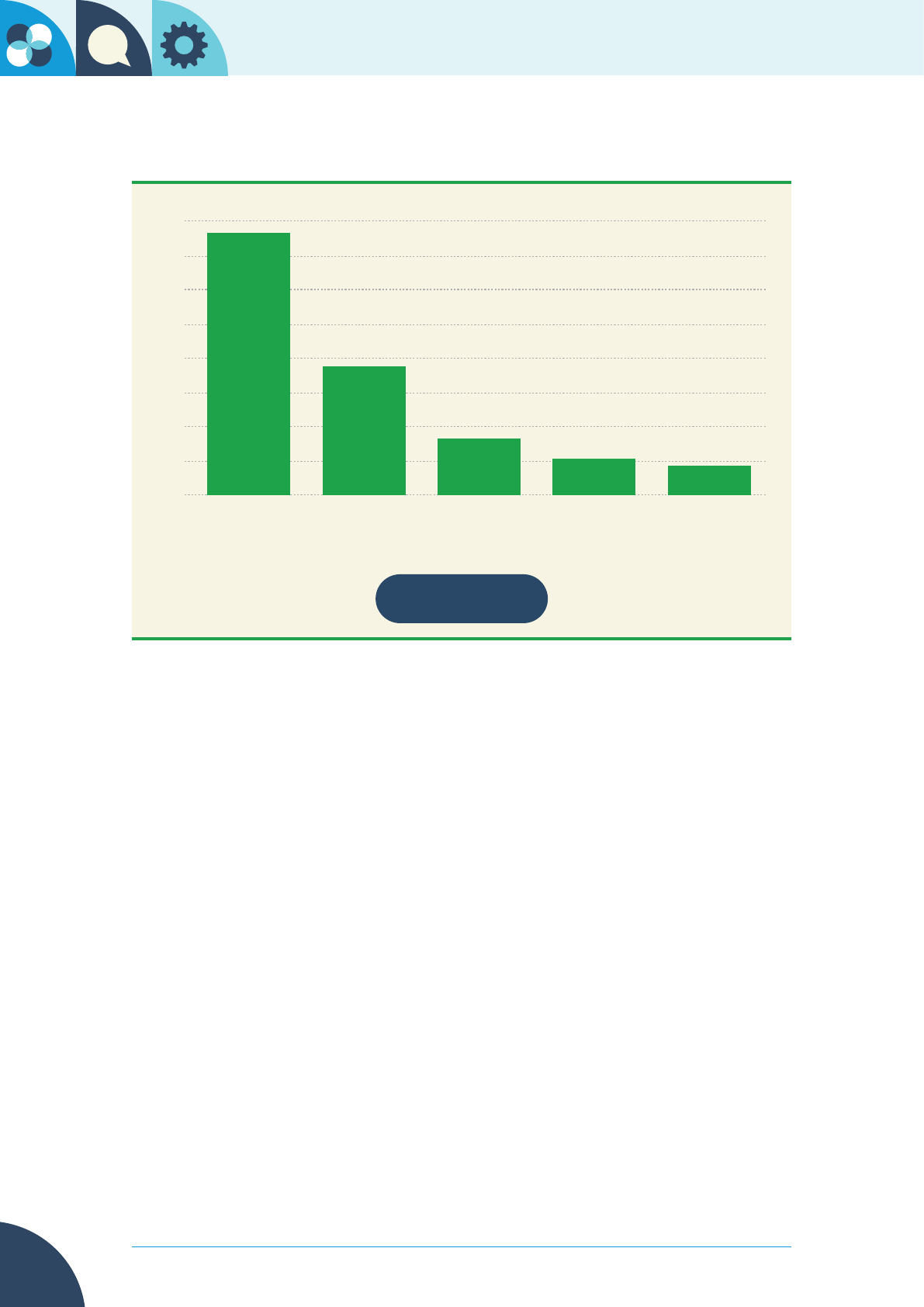

Fig. 5.2 – Top 10 conducts complained of:

0 450 900 1350 1800

1,506, (24%)

1,238, (20%)

905, (15%)

452, (7%)

292, (5%)

267, (4%)

232, (4%)

230, (4%)

216, (3%)

176, (3%)

Disputed fees and charges

Arrears handling

Maladministraon

Mis-selling

Refusal to give product/service

Advice Incorrect/Unsuitable (post-sale)

Disputed Transacons

Rejecon of Claim

Claim Handling

Customer Service

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

24

Banking Complaints 2023

The FSPO received 3,850 banking complaints in 2023, a 46% increase from the

2,640 classied as banking complaints in 2022. Banking complaints accounted for

62% of all complaints received, an increase of seven percentage points from 2022

when banking complaints accounted for 55% of all complaints received.

The majority of banking complaints concerned bank accounts (1,747), followed by

mortgages (1,150) and then other consumer credit (498). These three products

were also the three products most complained of in 2022.

Fig 5.3 Banking complaints by product 2023

Accounts 1,747

Mortgage 1,150

Consumer Credit 498

Payment Service 232

Commercial 179

Mulple Product/Service 33

Foreign Exchange 11

1,747, (45%)

1,150, (30%)

498, (13%)

33, (<1%)

179, (5%)

11, (<1%)

232, (6%)

Total 3,850

Customer service was the conduct which featured most in complaints about

banking services in 2023, as was the case in 2022. Customer service covers a

range of issues, including issues such as communications, complaint handling,

account access issues and the failure to provide information. Complaints

concerning disputed transactions and maladministration were the second and

third most common conducts respectively, featuring in complaints in the banking

sector.

Fig 5.4 – Top 6 primary Banking conducts complained of 2023

0

450

900

1350

Maladministraon Arrears

handling

Applicaon of

interest rate

Disputed fees

and charges

Disputed

transacons

1,218, (32%)

905, (24%)

796, (21%)

216, (6%)

152, (4%)

152, (4%)

Customer

Service

Total 3,850

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

25

Insurance Complaints 2023

The FSPO received 1,446 complaints related to insurance products in 2023. This

represents a 28% increase from the 1,129 complaints classied as insurance

complaints in 2022. Insurance complaints account for 23% of all complaints

received, an decrease of 1 percentage point from 2022, when insurance

complaints accounted for 24% of all complaints received. The largest number

of insurance complaints received related to motor insurance (498 complaints),

followed by private health insurance (215 complaints).

Fig 5.5 Insurance complaints by product 2023

Motor 498

Private Health Insurance 215

Home and/or Property 183

Tra ve l 171

Life 126

Accident, Illness and Other 83

Protecon 60

Miscellaneous 48

Commercial 41

Mulple Product/Service 21

215, (15%)

183, (13%)

60, (4%)

171, (12%)

498, (34%)

21, (1%)

41, (3%)

48, (3%)

83, (6%)

126, (9%)

Total 1,446

Most insurance complaints received in 2023 concerned claim handling (451

complaints) followed by complaints concerning the rejection of a claim (292

complaints). Notably, complaints concerning the conduct of ‘refusal to give

product/service’, appear fth in the top 5 conducts in 2023, having increased from

62 complaints in 2022 to 126 complaints in 2023.

Fig 5.6 – Top 5 Insurance conducts complained of 2023

Maladministraon Customer Service

Refusal to give

product/service

Claim Handling

451, (31%)

292, (20%)

155, (11%)

150, (10%)

126, (9%)

Rejecon of

Claim

Total 1,446

0

50

100

150

200

250

300

350

400

450

500

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

26

Investment Complaints 2023

The FSPO received 461 investment related complaints in 2023, a 26% increase

from the 366 classied as investment complaints in 2022. Investment complaints

accounted for 7% of all complaints received in 2023, a decrease of one percentage

point from 2022 when investment complaints accounted for 8% of all complaints

received.

The investment category includes not only investments, but also pension-related

investment products, a category for multiple products, and endowments. Some

products involve investments which are put in place to make provision for a

person’s retirement such as AVCs (Additional Voluntary Contributions), but a

product of that nature is not a “pension scheme” within the meaning of the FSPO’s

governing legislation. As a result, these products fall within the investment

products category.

Fig. 5.7 Investment complaints by product 2023

Investment 322

Pension related investment 129

Mulple Product/Service 7

Endowment 3

322, (70%)

129, (28%)

3, (<1%)

7, (2%)

Total 461

The conducts most complained of in investment complaints were

maladministration (133 complaints) and customer service (121 complaints).

Investment complaints relating to Mis-selling increased by 77% since 2022 (83

complaints in 2023).

Fig. 5.8 Top 5 Investment conducts complained of 2023

Mis-selling Advice

Incorrect/Unsuitable

(post-sale)

Management of

Fund

Maladministraon

Customer

Service

Total 461

0

100

50

150

121, (26%)

133, (29%)

46, (10%)

42, (9%)

83, (18%)

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

27

Pension Scheme Complaints 2023

The FSPO received 336 pension scheme complaints in 2023 in comparison

with 233 complaints in 2022, an increase of 44%. The majority of complaints

relating to pensions in 2023, related to occupational pension schemes (71%; 238

complaints).

Occupational pension schemes are schemes set up by an employer to provide

retirement and/or other benets for employees. This includes both public sector

and private sector occupational pension schemes.

PRSAs (Personal Retirement Savings Accounts) are pension savings accounts,

normally paid for by personal contributions, although employers can pay

contributions to these plans too. They accounted for 20% (67 complaints) of

complaints in 2023.

Trust RACs (Retirement Annuity Contracts) are schemes established under

trust and approved by the Revenue Commissioners. They are for the benet of

individuals engaged in, or connected with, a particular occupation and which

provide retirement annuities for them, or benets for their dependents.

Fig. 5.9 Pension scheme complaints by product 2023

Occupaonal Pension Scheme 238

PRSA 67

Other 29

Trust RAC 2

238, (71%)

67, (20%)

2, (<1%)

29, (9%)

Total 336

The conducts most complained of in relation to pensions were maladministration

(46%; 153 complaints) and calculation of pension benet (22%; 75 complaints).

Although the Ombudsman can direct rectication in pension complaints, the

legislation governing the FSPO sets out that the value of such rectication shall

not exceed any actual loss of benet under the pension scheme concerned. For

that reason, the Ombudsman cannot direct a pension provider to separately

compensate for acts of maladministration.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

28

Fig. 5.10 Top 5 Pension scheme conducts complained of 2023

Failure to provide

informaon/correct

informaon

Customer

Service

Refusal to give

product/service

Maladministraon

Calculaon of

Pension Benefit

Total 336

0

20

40

60

80

100

120

140

160

33, (10%)

21, (6%)

75, (22%)

153, (46%)

17, (5%)

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

29

Market Exit Complaints 2023

The departure of two major nancial service providers from the Irish market

in 2022 posed the potential for a high volume of complaints to be made to this

Ofce, given the number of impacted customers. On 1 June 2022, the FSPO

began tracking complaints relating to market exit, and sharing data and insight

with our stakeholders.

The FSPO contributed to the low volume of complaints by collaboratively

engaging and sharing information with stakeholders within the Irish banking

landscape, including with the providers leaving the market, ensuring that our

stakeholders were aware, on an ongoing basis, of the experience of the impacted

customers, as communicated to this Ofce.

In 2023, the FSPO received 236 complaints which were tagged with the keywords

‘market exit’, though not all of these complaints were in relation to the conduct of

those providers leaving the market. A total of 162 complaints relating to market

exit were closed in 2023. 55 complaints were closed at an early stage within our

Customer Operations and Information Management (COIM) department, where

either the complainant was re-directed to the nancial service provider, where

information had not been provided by the complainant in order to progress the

complaint, where a resolution had been reached, or the complaint had been

withdrawn.

A further 106 complaints were concluded within our Dispute Resolution

Service (DRS) for a variety of reasons, including where a settlement was agreed

between the parties, where a clarication was issued, where a resolution had

been reached outside of DRS, where the matter was noted to be best dealt with

by an alternative forum and where information had not been provided by the

complainant in order to progress the complaint.

One complaint was closed in Legal Services (LS) as it was outside the jurisdiction

of the FSPO. A complaint can go to Legal Services at any point in our processes,

but ideally in the early stages, should there be a jurisdictional query.

It is very positive that, to date, for the vast majority of impacted consumers,

the departure of two major banks has not given rise to issues leading to a

complaint being made to this Ofce. The FSPO contributed to this outcome by

collaboratively engaging and sharing complaint categorisation information with

relevant stakeholders within the Irish banking landscape, including with the

providers leaving the market.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

30

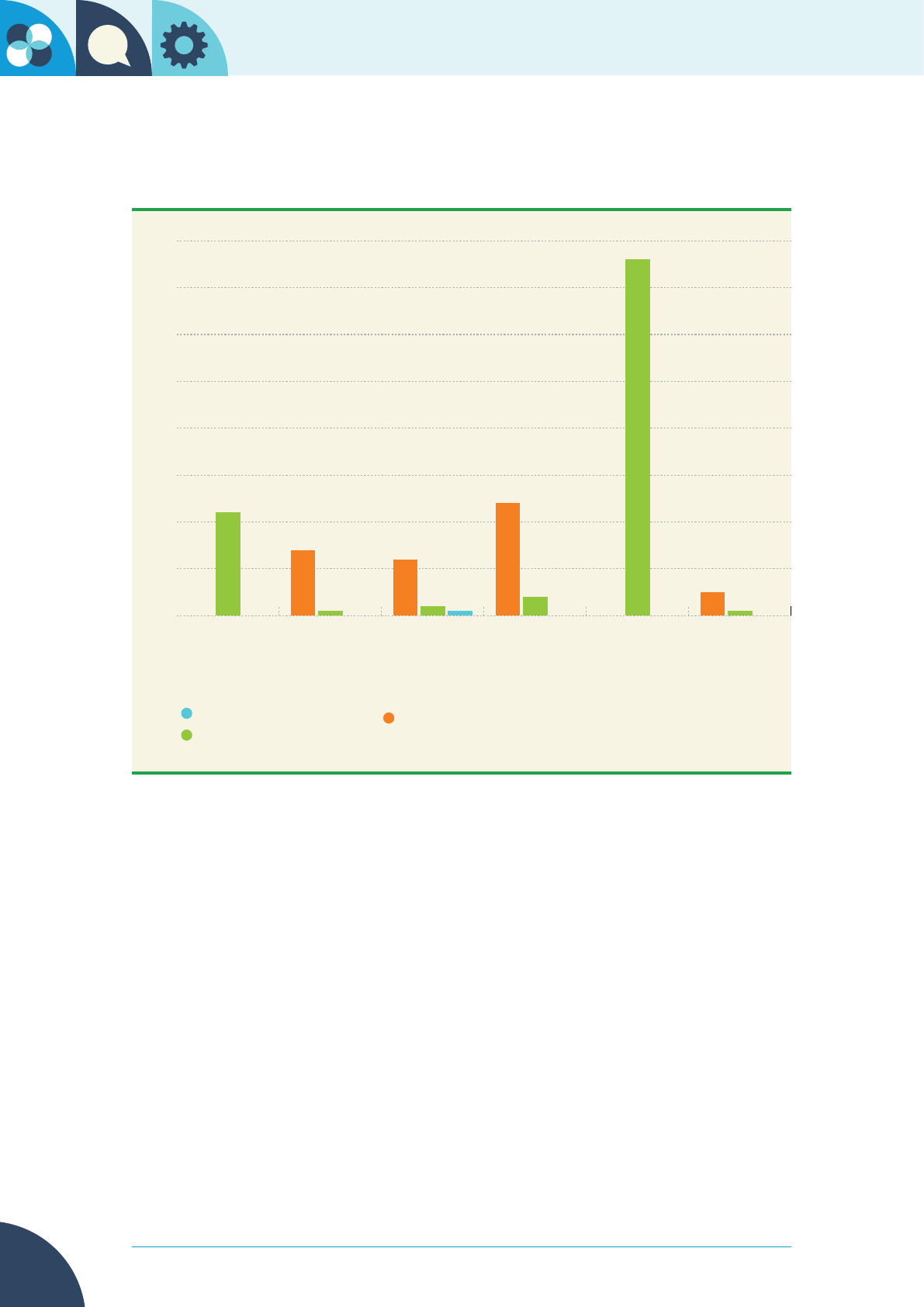

Fig. 5.11 Market Exit related complaints concluded by FSPO directorate during

2023

Clarificaon

Legal Services

Dispute Resoluon Services

Customer Operaons and

Informaon Management

Compliance

Incomplete

Outside

Jurisdicon

Resolved between

the pares

outside DRS

Mediaon

Selement

Withdrawn

0

10

20

30

40

50

60

70

80

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

31

Disputed Transactions

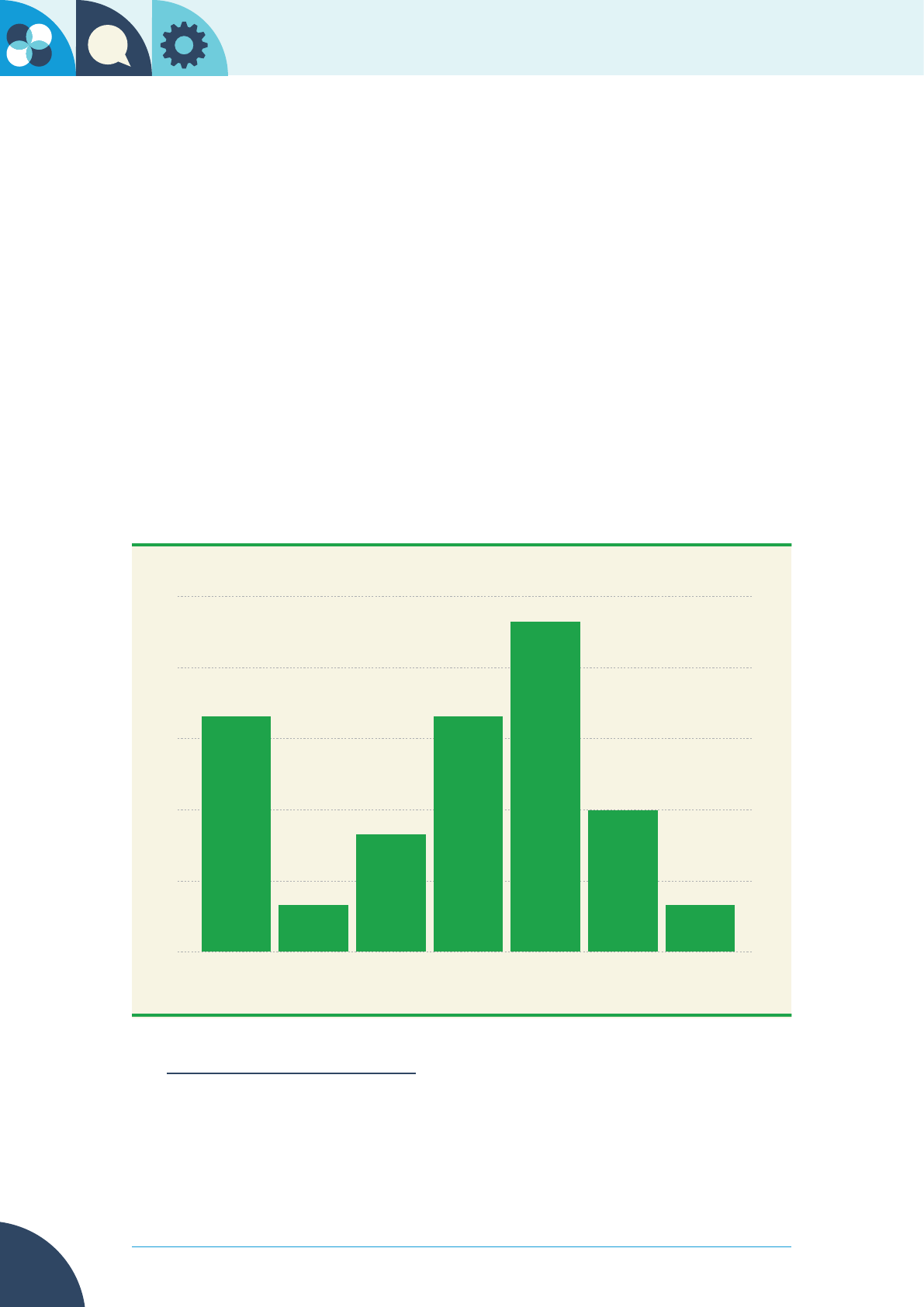

There has been a steady increase in the number of complaints received by the

FSPO in relation to disputed transactions, since 2018. Disputed transactions

include fraudulent transactions, unauthorised withdrawals, a failure to provide

security on an account and non-receipt of money.

It is important to note that the FSPO cannot investigate instances of fraud, as that

is a matter for An Garda Síochána. However, the FSPO can investigate a complaint

which relates to service failings of the provider in dealing with a customer who

suspects fraud on their account, and any complaint about disputed transactions.

In 2023, nearly a quarter of all banking complaints included the conducts grouped

under the heading of Disputed Transactions. Conducts complained of within the

grouping include disputed transactions, fraudulent transactions, failure to provide

accurate account information or balances, failure to provide security measures,

non-receipt of money, and unauthorised withdrawals.

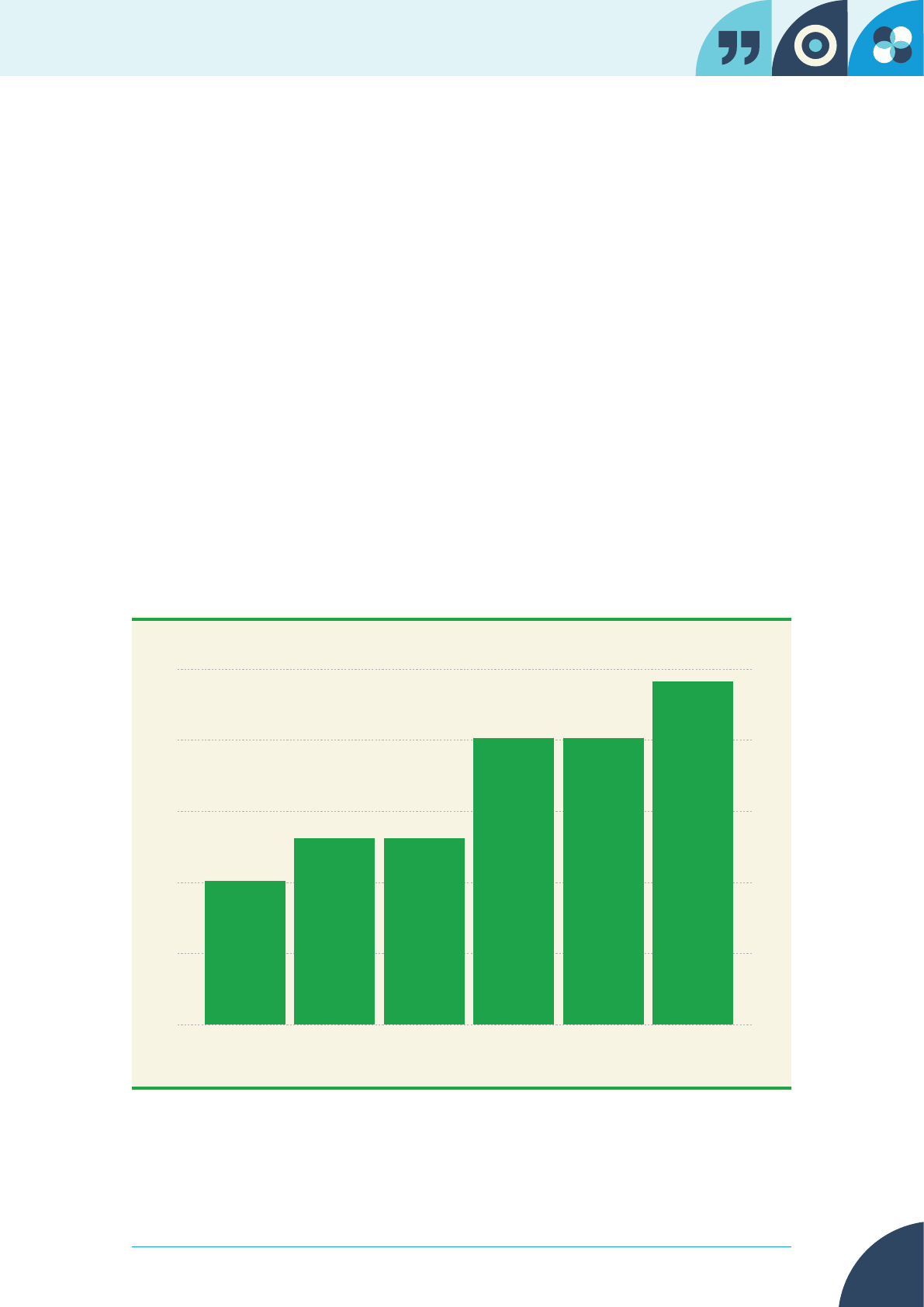

Fig 5.12 Disputed transactions as a percentage of all banking complaints

received 2018-2023

0

5

10

15

20

25

20232019 2020 2021 20222018

10%

13% 13%

20% 20%

24%

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

32

The increase in disputed transactions within the banking sector complaints

reects a distressing increase in fraud, particularly impacting vulnerable

customers. As digital transactions become more commonplace, those who may be

less familiar with online security measures are often targeted by fraudsters, but

anyone can fall for the clever tricks that criminals use.

Phishing attempts are where fraudsters, masquerading as trusted contacts, dupe

the customer into revealing their account security details. This results in disputed

transactions and may lead to a complaint to the FSPO if the customer believes

their bank hasn’t dealt with the issue appropriately.

There are a number of case studies within this Overview which demonstrate the

kind of scams that customers fall victim to. For example, Diana complained to

her bank after she had transferred money to an online trading platform, which

she said was then transferred to a fraudulent investment company. Diana felt the

bank should have started the chargeback process to recover her money.

In another complaint, Marie was the victim of a scam, which was carried out by

fraudsters claiming to be from the Department of Social Protection and An Garda

Síochána. Marie was informed by the fraudsters that someone had stolen her

identity and that this person was suspected of money laundering. She transferred

€17,000 to a foreign bank account, hoping to “protect” her money, before she

realised it was a scam.

Eugene lost €5,000 when his phone was hacked whilst on holiday on a cruise ship.

Eugene complained to his bank as he felt they could have done more to prevent

the transactions being completed.

Olive was another customer who believed she was signing up to a regulated

online trading platform to buy shares in a well-known company, when in fact, she

had signed up to an unregulated online trading platform where her investment

was sent to an unregulated fraudulent company. Olive said she lost a total of

€41,000 that she had placed with the platform. Olive said that the bank failed to

anticipate, prevent or notify her of the fraudulent nature of the online trading

platform.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

33

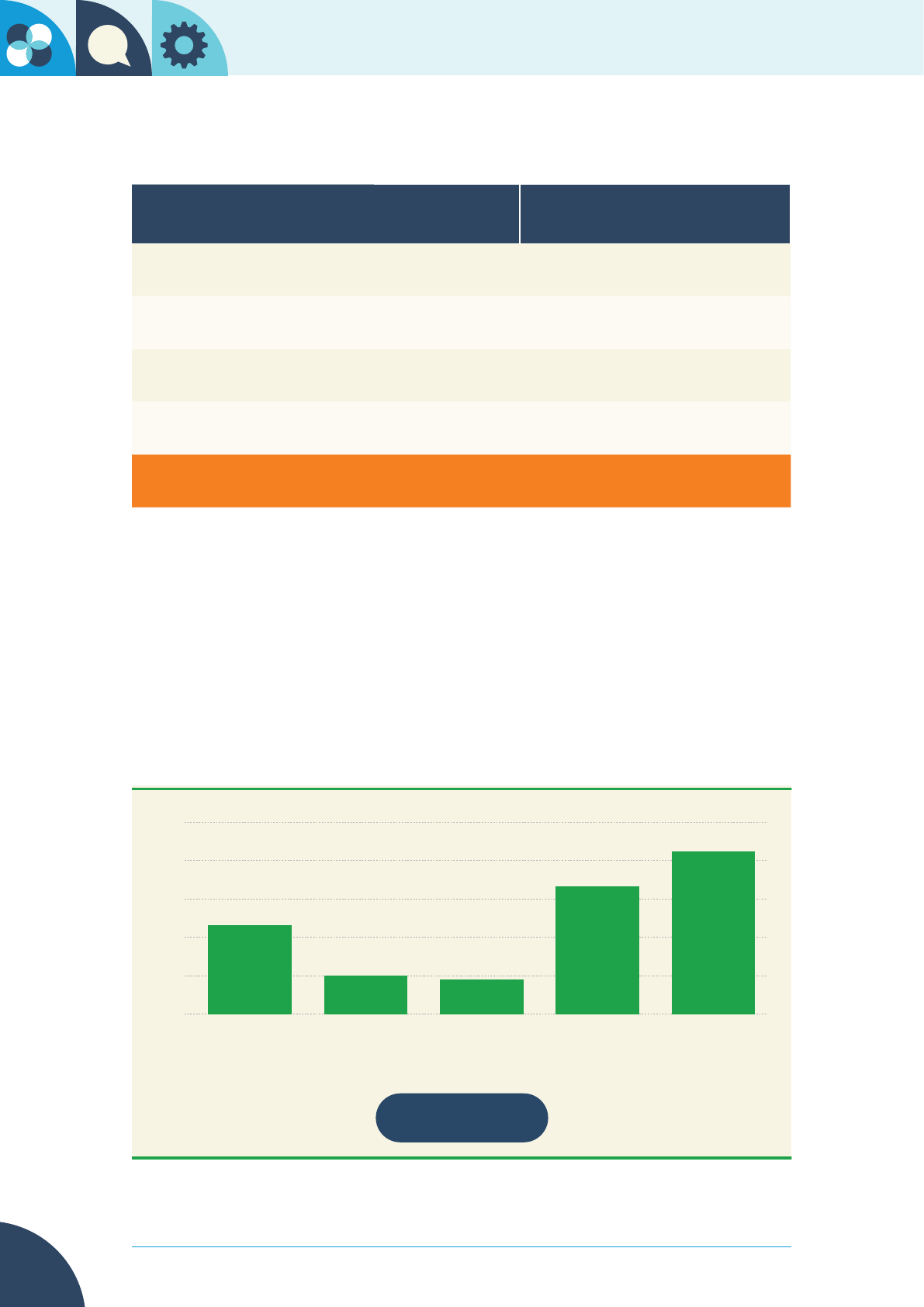

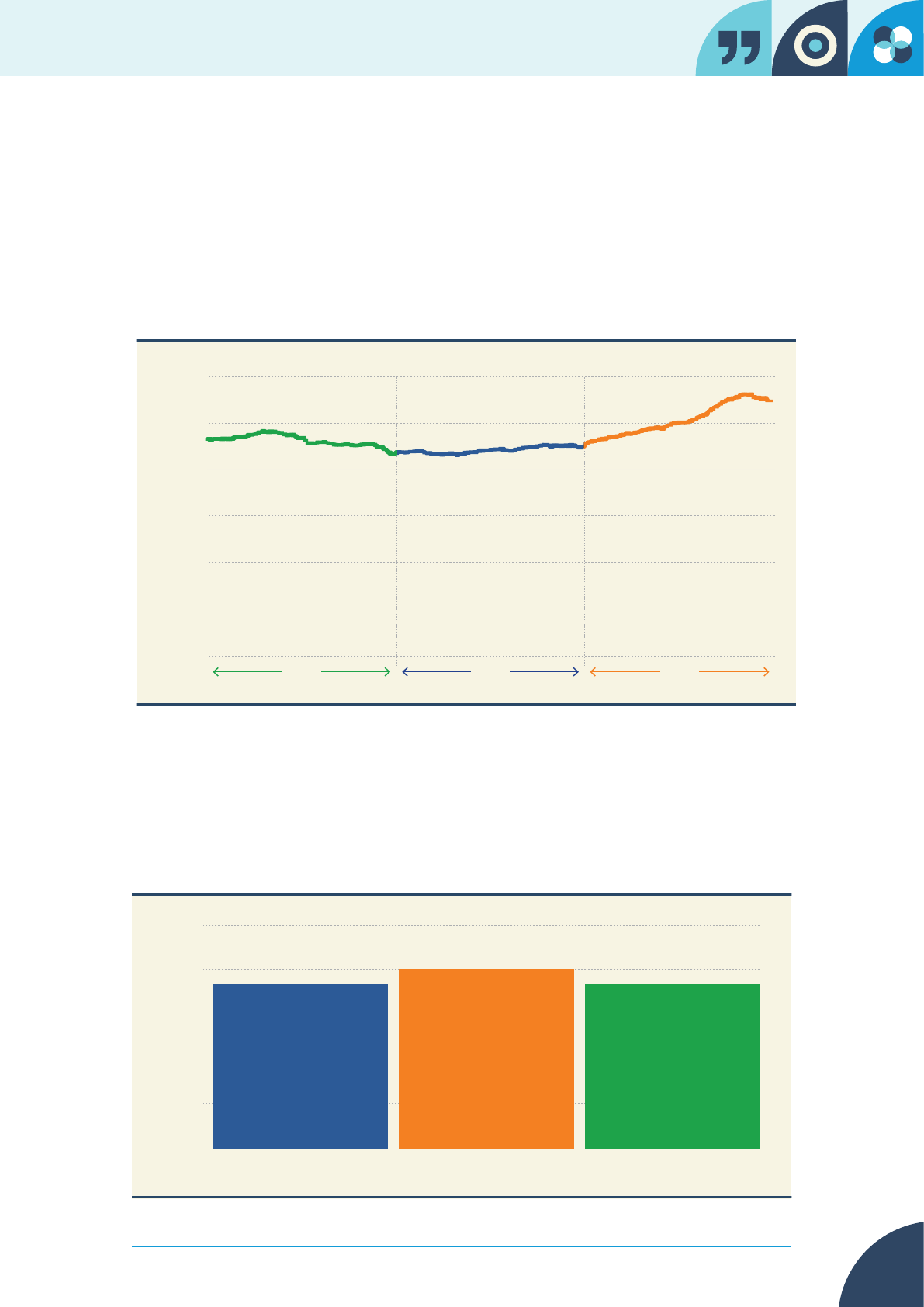

Tracker Mortgage Complaints 2023

The FSPO received 74 tracker mortgage related complaints in 2023. As can be

seen from gure 5.13, the number of tracker mortgage complaints received each

year continues to decline.

At the end of 2023 we had closed 224 tracker mortgage complaints and had 892

on hand.

Fig. 5.13 – Tracker mortgage interest rate related complaints 2021-2023

Complaints received Complaints closed Complaints on hand at year end

0

200

400

600

800

1000

1200

202320222021

74

224

892

250

370

1,115

139

247

1,030

The Ombudsman issued 107 tracker mortgage interest rate related legally

binding decisions in 2023. Three of these decisions were partially upheld, with a

total value of €28,000 directed to be paid to the complainants. One complaint was

substantially upheld, and the Ombudsman directed an amount of €10,000 to be

paid in compensation in this instance.

The remaining 103 complaints where a legally binding decision was issued, were

not upheld.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

34

Fig 5.14 – Tracker mortgage interest rate decisions issued in 2023

Decision outcome

Number of

decisions

Overall value of directions

issued in tracker decisions

Upheld 0 €0

Partially Upheld 3 €28,000

Substantially Upheld 1 €10,000

Not Upheld 103 €0

Total 107 €38,000

An additional 117 tracker mortgage complaints were closed for a variety of

reasons, without a legally binding decision being issued. In 23 complaints a

clarication was issued, allowing the complaint to close. 10 complaints closed

where information had not been provided by the complainant in order to progress

the complaint. In 9 complaints, the FSPO determined the complaints were outside

its jurisdiction. 33 complaints closed on the basis of a settlement agreement

between the complainant and the provider, and 42 complaints were withdrawn.

Fig 5.15 Tracker mortgage complaints closed without a legally binding decision

in 2023

Outside Jurisdicon Withdrawn

Selement

Clarificaon

Compliance

Incomplete

Total 117

0

10

20

30

40

50

9

33

10

23

42

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

35

It is evident from the outcomes of the tracker mortgage decisions issued, that

we continue to receive a considerable number of complaints from people whose

complaint about a tracker mortgage rate is not upheld, following an investigation

of the complaint. Many people remain of the belief that they are entitled to a

tracker mortgage interest rate, either from the time when they took out the

mortgage loan or from a date during the life of the mortgage loan, even though

they have no contractual or other entitlement to such a rate.

The following case studies of certain decisions issued by the FSPO in 2023, offer

an insight into some of the arguments raised in tracker mortgage complaints made

to the FSPO. The details below include links to the individual decisions which are

published on the FSPO website. Each decision addresses the individual complaint

made in its individual circumstances, as a result of which the complaints below

were not upheld:

Case Study 1

Eloise and Jean drew down a mortgage loan with the bank in 2004 and took

out a separate top-up loan with the bank in 2008. The bank offered them a

variable interest rate in respect of both loans, and they were advised by the

bank that a variable interest rate was the best option at the time.

As time passed, Eloise and Jean realised that the bank never discussed

tracker interest rates with them when they applied for their mortgage

loan nance. They believed they were entitled to a tracker interest rate

in respect of both mortgage loans, because they felt that they were not

properly advised by the bank in relation to their interest rate options, and

they believed that they were misled by the bank into accepting the variable

interest rate that was offered to them. (Decision 2023-0236)

Case Study 2

Fabio and Mia took out a mortgage loan with the bank in 2005 which

operated on a tracker interest rate of ECB + 1.1%. They approached the

bank for additional borrowings in 2008 as they decided to sell their existing

home and purchase a new home. Fabio and Mia had to fully redeem their

existing mortgage loan when selling their existing mortgaged property and

the bank offered them a new mortgage loan commencing on a one-year

discount loan-to-value variable interest rate.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

36

Case Study 2

One of the special conditions in the mortgage loan agreement for Fabio and

Mia’s new mortgage loan provided that at the end of the discount interest

rate period, was that they could choose an interest rate which was then

being offered by the bank and in the absence of any selection by them, a

variable interest rate would apply “which may be a tracker variable rate”.

When the discount variable interest rate expired, the bank only offered

them a range of xed interest rates and an LTV (loan-to-value) variable

interest rate. Fabio and Mia selected the LTV variable interest rate at the

time.

They believed they had an entitlement to a tracker interest because the

reference to a tracker interest rate in the special conditions of the mortgage

loan agreement guaranteed that they had a contractual entitlement to a

tracker interest rate on the expiry of the discounted variable interest rate

period. (Decision 2023-0135)

Case Study 3

Evelyn and Finn drew down a mortgage loan with the bank in 2006 when

they bought their home. This mortgage loan operated on a tracker interest

rate. In 2013, their property was in negative equity, and they decided to sell

the house and purchase a new property. In doing so, they had to redeem

their original mortgage loan, which was subject to a tracker interest rate,

and they then drew down a new mortgage loan on a variable interest rate.

At this time, in 2013, the bank did not allow them to transfer the tracker

interest rate on the original mortgage loan, to their new mortgage loan.

After drawing down the new mortgage loan in 2013, Evelyn and Finn

learned that the bank intended to launch a new tracker portability product

in the rst quarter of 2014. This tracker portability product allowed

customers to move home and keep the existing tracker interest rate that

applied to their primary mortgage, plus an additional 1%.

Evelyn and Finn felt they were entitled to a tracker interest rate, because

if the bank had notied them that it intended to introduce a tracker

portability product, they would have waited to sell their home and they

could have retained the tracker interest rate that applied to their original

mortgage loan. (Decision 2023-0188)

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

37

Case Study 4

Maedhbh’s mortgage loan account was considered by the bank as part of

the Central Bank of Ireland directed Tracker Mortgage Examination (the

“Examination”). The bank identied that a failure had occurred on her account

because, on the basis of the terms and conditions of her mortgage loan

agreement, she may have had an expectation that she would be given the

option to avail of the bank’s then prevailing tracker interest rate, when the

xed interest rate period on her mortgage loan account expired. Maedhbh’s

mortgage loan account was deemed to be impacted under that Examination.

The bank offered Maedhbh compensation, but she was not happy with the

amount offered because she considered it inadequate, so she appealed this to

the bank’s Independent Appeals Panel, but her appeal was unsuccessful.

Because Maedhbh was not satised with the decision of the Independent

Appeals Panel and she felt that a tracker interest rate should have been

applied to her mortgage loan account, she decided to make a complaint to the

FSPO. Maedhbh’s complaint was subsequently placed on hold for a number

of months. This was because of an investigation by the FSPO in respect of

another complaint against the same bank, which dealt with similar issues

to those arising in Maedhbh’s complaint. When the legally binding decision

issued in relation to that other complaint (see decision 2020-0103), the

bank indicated that it accepted that legally binding decision in full and that it

intended to apply the FSPO’s approach and compensatory direction to other

mortgage loan account holders who were also affected by that particular

conduct of the bank. Maedhbh was one of these mortgage account holders.

As a result, the bank offered Maedhbh further redress and compensation to

include applying a 12% reduction to her mortgage balance and an interest

refund based on the interest charged on the 12% balance reduction, from the

date her xed rate period ended.

After engaging the services of a third-party representative, Maedhbh

informed the FSPO that she was no longer seeking a tracker interest rate

to be applied to her mortgage loan account and was satised that a 12%

reduction had been applied to the mortgage balance. However, Maedhbh was

not satised with the interest refund offered by the bank. In this regard, she

was of the view that she was entitled to an increased interest refund, because

the bank incorrectly calculated the interest refund on a simple interest basis,

instead of on a compound interest basis. (Decision 2023-0268)

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

38

Case Study 5

Senan was employed by the bank and was therefore able to avail of a

staff preferential interest rate in respect of a certain portion of his overall

borrowings. To facilitate this, Senan drew down two mortgage loans with

the bank in 2008. He availed of a staff preferential interest rate in respect

of the rst mortgage loan, and he opted for a tracker interest rate in respect

of the second mortgage loan. The staff preferential interest rate was more

benecial to Senan at the time, because it was lower than the available

tracker interest rate.

In 2009, the bank moved Senan’s rst mortgage loan to its standard

variable interest rate when the staff preferential interest rate became less

advantageous. The bank gave Senan the option to opt out of this “switch” by

choosing to remain on the staff preferential interest rate, or by choosing to

switch to one of the xed interest rates on offer from the bank at the time.

Senan was not offered a tracker interest rate at this time. He did not opt out

of the “switch” and therefore his mortgage loan was moved to the standard

variable interest rate.

The terms and conditions of Senan’s mortgage loan agreement that related

to xed interest rate loans, stated that he would be given the option to avail

of the bank’s then prevailing tracker interest rate when his mortgage loan

account came off a xed interest rate period. Senan was of the view that

the bank should have offered him a tracker interest rate when the staff

preferential interest rate was removed from his mortgage loan account

because he understood that the staff preferential interest rate was a xed

interest rate, rather than a variable interest rate. (Decision 2023-0111)

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

39

Case Study 6

Lenka previously had a mortgage loan with the bank which she held jointly

with her former spouse, secured on their home. This mortgage loan account

was on a tracker interest rate. After their relationship broke down, Lenka

took over the monthly mortgage loan repayments. She requested the bank

to transfer the mortgage loan into her sole name, but the bank refused to

do this. Instead, Lenka had to fully pay off the jointly held mortgage loan and

make a new application for a loan in her sole name. The bank informed her

at the time that it had to carry out an assessment of her affordability, before

offering her a loan facility in her own name. At the time when Lenka applied

for the new mortgage loan, tracker interest rates had been withdrawn

from the market, and were no longer available as part of the bank’s product

offering. As a result, Lenka was offered a mortgage loan commencing on a

three-year xed interest rate which she accepted.

Lenka felt she should have been allowed to keep the tracker interest rate

when she applied to have the joint mortgage loan put into her sole name,

because she did not want to change any other details of the mortgage loan

or apply for any further borrowings. Lenka simply wanted to remove the

name of the other borrower from the mortgage loan. (Decision 2023-0070)

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

40

6

How we managed complaints in

2023

In 2023, the FSPO received 6,182 complaints, a signicant increase of 29% in

comparison to the number of complaints received in 2022. We also closed more

complaints during this period (5,184 complaints), 12% more than in 2022 (4,647

complaints).

Fig 6.1 – Complaints received and closed 2021-2023

Complaints received Complaints closed

0

1000

2000

3000

4000

5000

6000

7000

4,658

5,010

4,781

4,647

6,182

5,184

202320222021

Despite closing more complaints than in each of the preceding two years, we

ended the year with more complaints on hand than in the same period in 2022,

due to the signicant increase in the volume of complaints received over the

course of 2023.

Complaints on hand are the number of active complaints on any given day. Closed

complaints may be reopened due to new information being received at any point

in the year, so the number of complaints on hand shows the volume of complaints

over the time period.

Following the approval of the FSPO’s Workforce Plan in December 2023, the

sanctioned staff complement in the FSPO was increased from 90.2 to 128.

Arising from this approval of the Workforce Plan there are 35 further roles to be

recruited in 2024. This recruitment process has commenced, and we estimate

these roles will be lled by September 2024.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

41

These additional resources will assist us in addressing the rising number of

complaints received, as well as supporting our strategic ambition to evolve and

innovate our services and the organisation, with a strong focus on our customers

and external stakeholders and audiences.

Fig 6.2 – Complaints on hand by date 2021-2023

6,000

5,000

4,000

3,000

2,000

1,000

0

2022 20232021

The proportion of complaints received through the FSPO’s online complaint form

in 2023, fell from 80% received in 2022 to 74%. This was due to a signicant

number of complaints coming through as email queries, which our staff then set

up directly on our complaint system.

Fig 6.3 – Percentage of complaints received online 2021-2023

2023

2021

74%80%74%

100%

80%

60%

40%

20%

0%

2022

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

42

Fig 6.4 – How we managed complaints in 2023

Total number of complaints closed

5,184

Customer Operations and

Information Management

2,441

Dispute Resolution Services

2,049

Investigation Services

512

Legal Services

182

See page 43

See page 49

See page 60

See page 76

Withdrawn complaints

247 complaints were withdrawn at various points in our processes in 2023.

The reason for withdrawal of a complaint can vary depending on the stage at

which the complaint is withdrawn. A common theme, regardless of the stage

at which a complaint is withdrawn, is where the complaint has been resolved

to the complainant’s satisfaction by the provider. While the FSPO encourages

settlements at the earliest stage, a settlement at any stage is always encouraged

and welcome. Complainants may also withdraw their complaint due to a change

in life circumstances. The FSPO is always willing to take such matters into

consideration and may offer to put the complaint on hold for a time instead, if

appropriate.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

43

Customer Operations and

Information Management

complaints

closed

2,441

When a complaint is received, the Registry and Assessment team reviews and

assesses it. This initial assessment provides an opportunity for the FSPO to

determine if the complainant has provided all the necessary information to

progress the complaint and to ensure the provider has been given the opportunity

to resolve the complaint rst. In many cases, this preliminary work allows the

complaint to close, if the complainant is subsequently satised with the provider’s

resolution of the complaint.

The complaint is assessed to conrm that it is eligible for the statutory jurisdiction

of the FSPO. Not all complaints are eligible for investigation by the FSPO and so

the assessment of the complaint’s eligibility takes place at the earliest possible

stage. This may include determining whether the conduct complained of falls

within the statutory time limits, checking that consent has been provided by all

of the account or policy owners, or we may need to check if a nancial service

provider is regulated.

This early assessment service has enabled the FSPO to use its resources in the

most efcient manner. More importantly, this service has enabled the FSPO to

provide a greatly improved customer experience, ensuring the complainant is

informed early on in the process if their complaint falls outside the FSPO’s remit.

In some circumstances, the Customer Operations and Information Management

(COIM) team may need to refer a complaint to our Legal Services team for a

detailed legal review. Once the COIM team has completed its assessment the

complaint is either referred to Dispute Resolution Services for mediation or,

where the complaint cannot progress any further, it will be closed.

In an effort to get the most meaningful data from our complaints, a set of new

closure codes for our complaint management system was introduced at the end

of 2023. The purpose of these new closure codes is to better describe the reasons

for closing a complaint, as well as to provide a more integrated set of codes which

can be used by the organisation as a whole. This will enhance our reporting on

complaint outcomes going forwards.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

44

Fig. 6.5 – COIM complaint closure reasons 2023

Closure reason Number of complaints closed

Outside jurisdiction 844

Compliance incomplete 766

Resolved 628

Withdrawn 177

Other 26

Total 2,441

COIM closed 844 complaints during 2023 as they were outside the jurisdiction of

this Ofce. Examples of this would be where the provider is not regulated within

the European Economic Area, where the provider was not providing a nancial

service, or the complaint was outside the time limits allowed for investigation of

the complaint. The FSPO received an increased number of complaints relating

to disputed transactions in 2023, (380 more complaints were received in 2023

under this conduct heading than in 2022), which includes the category of fraud.

Where fraud was the only conduct complained of, this complaint was closed and

labelled as ‘outside jurisdiction’, because the FSPO cannot investigate matters of

fraud, as this is a matter for An Garda Síochána.

In 766 instances where the complaint was closed, the complaint was closed as

‘compliance incomplete’. In these complaints, the complaint could not proceed to

an investigation as there was information outstanding from the complainant, or in

some cases the complainant could not be contacted.

In many cases, complainants make a complaint to the FSPO without having rst

made a complaint to their provider. It is important to ensure the provider has

been given the opportunity to resolve the complaint rst, as it is only when a

complainant has been unable to resolve their complaint or dispute with a nancial

service provider or a pension provider, that they can refer their complaint to

the FSPO. During 2023, 628 such complaints were made to the FSPO, where

subsequent notication to the provider of the existence of a complaint, allowed

the complaint to be resolved to the customer’s satisfaction.

In addition, 177 complaints were withdrawn by the complainant at this early

stage.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

45

Customer Operations and Information

Management Case Studies

Customer Operations and Information Management: Case Study 1

Customer falls victim to scam text

Following receipt of a scam text message, Sophia had €1,000 taken from her

bank account, as a result of fraud. When Sophia contacted her bank, it said

it would investigate the matter. Following its investigation, the bank said it

could not do anything, as she had authorised the transaction herself. Sophia

then submitted a complaint to the FSPO.

As part of the registration and assessment of the complaint, the

Registration Team contacted the bank and asked for further information.

The bank carried out a further review of the complaint and made the

decision to refund the full amount to Sophia.

Sophia said:

I have just been refunded the full amount from the fraud scam I fell

victim to. I would like to sincerely thank you for your help with this

matter, it is appreciated enormously.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

46

Customer Operations and Information Management: Case Study 2

Credit Union apologises for poor customer

service

Rita took out a loan with her credit union. Rita said she had been unable to

get a statement on her loan, despite asking for it three times. Rita also said

that despite always paying her loan, she was contacted excessively by her

credit union, and funds from her savings, which she had received following

the death of her father, had been used by the credit union to pay off her

loan, without her approval.

As a result, Rita submitted a complaint to the FSPO. On receipt of Rita’s

complaint, the Registration and Assessment Team contacted Rita’s credit

union to request information. On receipt of the request, the credit union

began a further investigation into Rita’s complaint. The credit union said it

had not previously received a complaint from Rita and it arranged to meet

her. This resulted in the resolution of the complaint.

Rita contacted the FSPO, explaining that the credit union had refunded the

money her father had left her, xed her credit rating and apologised.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

47

Customer Operations and Information Management: Case Study 3

Bank continued to incorrectly report customer

to Central Credit Register

Sergey went through the bankruptcy process and was discharged from

bankruptcy in 2017. Despite being discharged, his bank continued to report

Sergey’s credit rating to the Central Credit Register (CCR). Sergey believed

this to be incorrect and it resulted in him being unable to obtain credit from

any nancial institution. Sergey said this also impacted his wellbeing. Sergey

said he had contacted his bank but was told that nothing could be done.

Sergey submitted a complaint to the FSPO. The complaint was referred to

the Registration & Assessment team, who contacted the bank to request a

nal response letter from it. In its nal response, the bank agreed to request

the deletion of the records from the CCR.

Sergey was happy with that outcome and said: “It [the complaint] was closed

as the FSPO communicated with the lender on my behalf and got the result

we wanted in a short space of time, so the case was closed.

Thank you to the FSPO, I couldn’t have done it without you guys so

many thanks.

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

48

Customer Operations and Information Management: Case Study 4

Customer complains regarding lack of

contact from her bank

Pamela used her credit card to book a holiday. The travel company Pamela

booked with ceased trading at short notice, so Pamela requested a refund

but was unsuccessful. Pamela engaged with her bank, seeking a chargeback,

but this was declined.

Pamela submitted a complaint to her bank but had difculty in getting a

response to her complaint. She then submitted a complaint to the FSPO.

Following a review of the complaint, the Registration and Assessment team

wrote to Pamela’s bank and asked it to review the complaint and issue its

nal response within 10 working days. The bank reviewed the complaint

and then offered Pamela a refund in addition to a gesture of goodwill for the

lapse in service.

Pamela wrote to us to say:

I am so grateful to you for getting such a comprehensive,

satisfactory and prompt reply from [my bank] for me.

They have acknowledged the difculties and exasperation I

experienced hence I will accept their offer of goodwill…

Overview of Complaints 2023 | Financial Services and Pensions Ombudsman

49

Dispute Resolution Services

complaints

closed

2,049

Our Dispute Resolution Service is a voluntary and condential service that aims

to resolve complaints against nancial service providers or pension providers as

quickly as possible through mediation.