REPORT ON EXAMINATION

OF

AXA ART INSURANCE CORPORATION

AS OF

DECEMBER 31, 2017

DATE OF REPORT DECEMBER 28, 2018

EXAMINER MARIBEL C. NUNEZ, C.P.C.U

TABLE OF CONTENTS

ITEM PAGE NO.

1. Scope of examination 2

2. Description of Company 3

A. Corporate governance 3

B.

Territory and plan of operation

4

C. Reinsurance ceded 6

D.

Holding company system

7

E. Significant operating ratios 11

3. Financial statements 12

A. Balance sheet 12

B.

Statement of income

13

C. Capital and surplus account 14

4. Losses and loss adjustment expenses 15

5. Subsequent events 15

6. Compliance with prior report on examination 16

7. Summary of comments and recommendations 17

One State Street, New York, NY 10004-1511 │ (212) 480-6400│ www.dfs.ny.gov

ANDREW M. CUOMO

Governor

LINDA A. LACEWELL

Acting Superintendent

April 1, 2019

Honorable Linda A. Lacewell

Acting Superintendent

New York State Department of Financial Services

Albany, New York 12257

Madam:

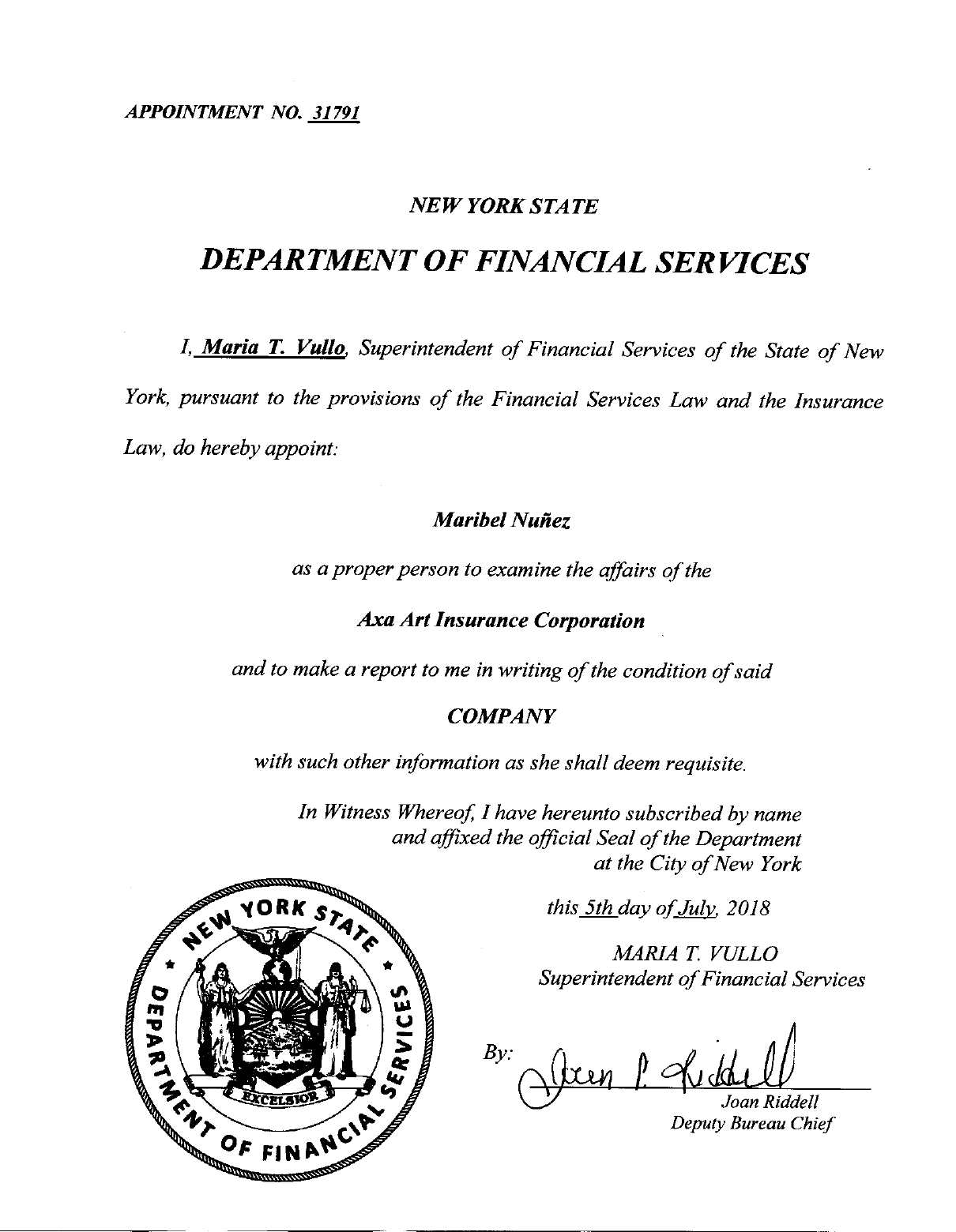

Pursuant to the requirements of the New York Insurance Law, and in compliance with the instructions

contained in Appointment Number 31791 dated July 5, 2018, attached hereto, I have made an examination

into the condition and affairs of AXA Art Insurance Corporation as of December 31, 2017, and submit the

following report thereon.

Wherever the designation “the Company” appears herein without qualification, it should be understood to

indicate AXA Art Insurance Corporation.

Wherever the term “Department” appears herein without qualification, it should be understood to mean the

New York State Department of Financial Services.

The examination was conducted at the Department.

2

1. SCOPE OF EXAMINATION

The Department has performed an examination of the Company, a multi-state insurer. The previous

examination was conducted as of December 31, 2012. This examination covered the five-year period from

January 1, 2013 through December 31, 2017. Transactions occurring subsequent to this period were

reviewed where deemed appropriate by the examiner.

This examination was conducted in accordance with the National Association of Insurance

Commissioners (“NAIC”) Financial Condition Examiners Handbook (“Handbook”), which requires that

we plan and perform the examination to evaluate the financial condition of the Company by obtaining

information about the Company including corporate governance, assessing the principles used and

significant estimates made by management, as well as evaluating the overall financial statement

presentation, management’s compliance with New York Laws, statutory accounting principles, and annual

statement instructions.

All financially significant accounts and activities of the Company were considered in accordance

with the risk-focused examination process. The Examiner relied upon audit work performed by the

Company’s independent public accountants.

This examination report includes, but is not limited to, the following:

Company history

Management and control

Territory and plan of operation

Holding company description

Reinsurance

Financial statement presentation

Loss review and analysis

Significant subsequent events

Summary of recommendations

This report on examination is confined to financial statements and comments on those matters that

involve departures from laws, regulations or rules, or that are deemed to require explanation or description.

3

2. DESCRIPTION OF COMPANY

AXA Art Insurance Corporation was incorporated under the laws of the State of New York on

September 17, 1986, as Nordstern Insurance Company of America. It became licensed on February 9, 1987

and commenced business the same date. The Department approved the present name on April 2, 2001.

On January 1, 2014, the Company effectively ceased the writing of insurance business and sold the

right to renew all its U.S. policies to AXA Art Americas Corporation, a related party, for $12.7 million.

A. Corporate Governance

Pursuant to the Company’s charter and by-laws, management of the Company is vested in a board

of directors consisting of not less than thirteen nor more than twenty-one members. The board meets four

times during each calendar year. At December 31, 2017, the board of directors was comprised of the

following thirteen members:

Name and Residence

Principal Business Affiliation

Roland Augustine

New York, New York

President,

Luhring Augustine Gallery

Christiane Fischer

New York, New York

President and Chief Executive Officer,

AXA Art Insurance Corporation and

AXA Art Americas Corporation

Janine Wolf Hill

New York, New York

Director,

Fellowship Affairs and Studies Strategic

Planning of the Council on Foreign Relations

Alexander Kemper

Kansas City, Missouri

Chairman,

The Collectors Fund and

the Board of Pollenware

Kai Kuklinski

Cologne, Germany

Chief Executive Officer,

AXA Art Versicherung AG

Ana Carmen Longobardi

Sao Paulo, Brazil

Creative Vice President and Partner,

Talent Communication

Aaron Milrad

Toronto, Canada

Counsel,

Dentons Canada, LLP

4

Name and Residence

Principal Business Affiliation

Ernest Riefenhauser

New York, New York

Chief Financial Officer and Treasurer,

AXA Art Americas Corporation and

AXA Art Insurance Corporation

Alan Schwartz

Toronto, Canada

Managing Director,

Terraplan Landscape Architects and

Owner of Lonsdale Holdings

Dorit Straus

New York, New York

Independent Consultant and advocate for artists

and the arts

Marc Mitchell Tract

New York, New York

Partner,

Katten Muchin Rosenman, LLP

Dr. Alexander Wiebe

Cologne, Germany

Chief Financial Officer and Board Member,

AXA Art Versicherung AG

Anthony Williams

New York, New York

Partner,

Dentons US LLP

As of December 31, 2017, the principal officers of the Company were as follows:

Name

Title

Christiane Fischer

President & Chief Executive Officer

Ernest Riefenhauser Chief Financial Officer & Treasurer

Gary Albert Kerr

Corporate Secretary

Colin Quinn Vice President, Director of Claims Management

Note: All directors and officers, except for Ernest Riefenhauser, resigned as of July 13, 2018 as result of

the acquisition of control.

B. Territory and Plan of Operation

As of December 31, 2017, the Company was licensed to write business in all fifty states and the

District of Columbia.

As of the examination date, the Company was authorized to transact the kinds of insurance as

defined in the following numbered paragraphs of Section 1113(a) of the New York Insurance Law:

5

Paragraph Line of Business

4

Fire

5 Miscellaneous property

6

Water damage

7 Burglary and theft

8

Glass

9 Boiler and machinery

10

Elevator

12 Collision

14

Property damage liability

15 Workers' compensation and employers' liability

16

Fidelity and surety

19 Motor vehicle and aircraft physical damage

20

Marine and inland marine

21 Marine protection and indemnity

Based upon the lines of business for which the Company is licensed and the Company’s current

capital structure, and pursuant to the requirements of Articles 13 and 41 of the New York Insurance Law,

the Company is required to maintain a minimum surplus to policyholders in the amount of $3,200,000.

The following schedule shows the direct and assumed premiums written by the Company for the

period under examination:

Calendar

Year

Direct

Premiums

Assumed

Premiums

Total Gross

Premiums

2013 $45,058,072 $3,277,147 $48,335,219

2014 2,575,909 2,287,597 4,863,506

2015 2,501,487 (257,373) 2,244,114

2016 2,596,091 (3,007) 2,593,084

2017 614,228 0 614,228

The Company specialized in writing inland marine and related lines of business, with an emphasis

on personal and commercial fine art coverage and other insurance floaters. The majority of the Company’s

business was generated through brokers.

6

C. Reinsurance Ceded

At December 31, 2017, the Company had the following ceded reinsurance program in effect:

Type of Contract

Treaties with AXA Art Versicherung AG

100% Unauthorized

Cession

Terrorism Excess of Loss

2 layers

$385,500,000 excess of $14,500,000 ultimate net loss,

each loss occurrence.

Reporter Excess of Loss

$385,500,000 excess of $14,500,000 each risk and

$348,000,000 excess of $14,500,000 for warehouse

and storage risks.

1

st

Lower Excess of Loss Layer

Lower CAT Excess of Loss Layer

$12,000,000 excess of $2,500,000 each risk, each loss

occurrence.

$7,250,000 excess of $14,500,000 each loss

occurrence. The Lower CAT-XL only operates if two

or more risks are involved in one loss occurrence,

regardless of the number or type of policies.

Per Occurrence Excess of Loss

4 layers

$113,250,000 excess of $21,750,000 ultimate net loss,

each occurrence. 2

nd

layer excludes Flood UK; 3

rd

layer excludes European windstorm and Flood UK; 4

th

layer covers natural Catastrophe, but excludes bush

fires, California Earthquake, European windstorm,

and UK Flood.

Non-Art Excess of Loss

3 layers

$27,550,000 excess of $1,450,000 ultimate net loss,

each risk.

Jewelry Excess of Loss $14,000,000 excess of $500,000 ultimate net loss,

each risk.

Warehouse Excess of Loss

$125,000,000 excess of $362,500,000 all risks and

$125,000,000 excess of $400,000,000 for terrorism

ultimate net loss, each risk, each loss occurrence.

Quota-Share

100% Authorized

60% quota share of all business written.

7

The majority of the Company’s premiums written was ceded to an authorized reinsurer AXA

Insurance Company, an affiliated entity, via a 60% quota share agreement effective January 1, 2008. The

Company has received approval to do so, pursuant to the provisions of Section 1308(e)(1) of the New York

Insurance law.

Reinsurance agreements with affiliates were reviewed for compliance with Article 15 of the New

York Insurance Law. It was noted that all affiliated reinsurance agreements were filed with the Department

pursuant to the provisions of Section 1505(d)(2) of the New York Insurance Law.

All ceded reinsurance agreements in effect as of the examination date were reviewed and found to

contain the required clauses, including an insolvency clause meeting the requirements of Section 1308 of

the New York Insurance Law.

Examination review found that the Schedule F data reported by the Company in its filed annual

statement accurately reflected its reinsurance transactions. Examination review indicated that the Company

was not a party to any finite reinsurance agreements. All ceded reinsurance agreements were accounted for

utilizing reinsurance accounting as set forth in SSAP No. 62R.

During the period under examination, the Company did not commute any reinsurance agreements.

D. Holding Company System

The Company is a member of the AXA Art Versicherung AG Group. The Company is a wholly-

owned subsidiary of AXA Art Holdings, Inc., a New York corporation, which is ultimately controlled by

AXA SA, a publicly-traded company based in France.

A review of the Holding Company Registration Statements filed with this Department indicated that

such filings were complete and were filed in a timely manner pursuant to Article 15 of the New York

Insurance Law and Department Regulation 52.

8

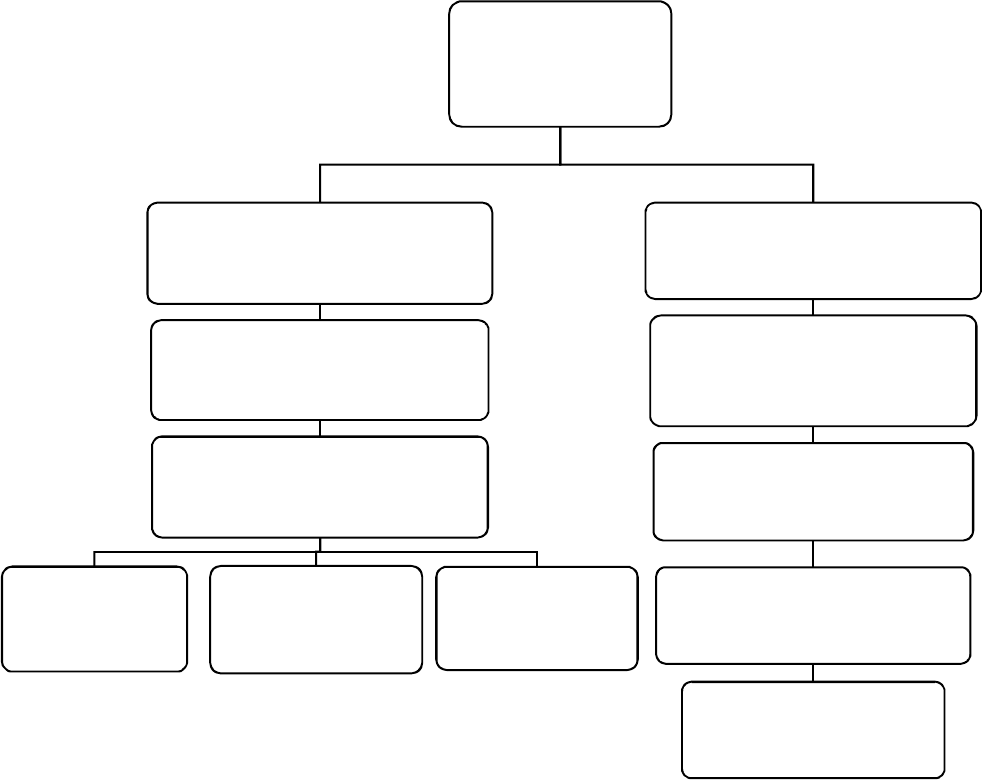

The following is an abridged chart of the holding company system at December 31, 2017:

AXA SA

(France)

100%

AXA Konzern AG

(Germany)

100%

AXA Art Versicherung, AG

(Germany)

100%

AXA Art Holdings, Inc.

(New York)

100%

AXA Art

Insurance

Corporation

(New York)

Fine Art Services

International (US),

Inc.

(Delaware)

AXA Art Americas

Corporation

AXA Equitable Holdings, Inc.

(New York)

100%

AXA America Corporate

Solutions, Inc.

(New York)

100%

Coliseum Reinsurance Company

(New York)

100%

AXA Delaware LLC.

(New York)

100%

AXA Insurance Company

(New York)

9

At December 31, 2017, the Company was party to the following agreements with other members of

its holding company system:

Service and Expense Allocation Agreement

Effective September 1, 2005, the Company entered into a Service and Expense Allocation

Agreement with Fine Art Services International (US), Inc. (“Fine Art”). Pursuant to the agreement, the

Company has agreed to provide Fine Art with facilities, equipment, office and other space as it may require

for the conduct of its business and operations. Fine Art has agreed to provide to the Company, personnel to

provide services including, but not limited to, claims handling, consulting, clerical, administrative and

management information systems. The agreement and amendment were filed with the Department pursuant

to Section 1505(d) of the New York Insurance Law.

Effective July 1, 2009, this agreement was amended to reflect a new location of its leased premises

to the Company’s current address. This amendment was non-objected to by the Department on May 5, 2009.

Cost Allocation Agreement

Effective December 1, 2003, the Company entered into a cost allocation agreement with its parent,

AXA Art Holding, Inc. (“AAH”), whereby AAH provides services to the Company including equipment,

furniture and fixtures necessary for the operations of the Company. This agreement was filed with the

Department pursuant to Section 1505(d) of the New York Insurance Law and was non-objected to on

January 5, 2004.

Service Agreement

Effective December 1, 2003, the Company entered into a service agreement with AXA Art

Versicherung AG (“AAV”), whereby AAV provides personnel and services to the Company with respect

to the following matters: investment management, knowledge management, information technology,

corporate control and audit, legal, tax, corporate finance, marketing and communication, reinsurance,

accumulation control and underwriting guidelines. This agreement was filed with the Department pursuant

to Section 1505(d) of the New York Insurance Law and was non-objected to on January 5, 2004.

10

Tax Allocation Agreement

Effective October 1, 1994, the Company filed a consolidated federal income tax return with AXA

Art Holdings, Inc., and Fine Art Services International (U.S.), Inc. This agreement was filed with the

Department pursuant to Section 1505 of the New York Insurance Law and was non-objected to on April

13, 1995.

Administrative Service Agreement

Effective January 1, 2013, the Company and AXA Art Americas entered into an administrative

service agreement, whereby AXA Art Americas would provide the following services: claims handling,

premium collection, underwriting, policyholder services, producer management, investments, accounting

and financial, information and technology, and legal and government relations services. This agreement

was filed with the Department pursuant to Section 1505(d) of the New York Insurance Law and was non-

objected to on January 2, 2013.

Sale and Purchase of Rights to Renew Agreement

Effective January 1, 2014, the company and AXA Art Americas Corporation entered into a sale and

purchase of rights to renew agreement, whereby the Company sold the rights to renew its books of business

to AXA Art Americas for a consideration of $12.7 million. This agreement was filed with the Department

pursuant to Section 1505(d) of the New York Insurance Law and was approved on April 8, 2013.

Assumption Reinsurance Agreement

On April 2, 2017, the Company transferred via an assumption reinsurance and business transfer

agreement the entirety of its Canadian book of business to its affiliate, AXA Insurance Company (“AIC”),

thereby ceasing to actively write insurance business.

Effective December 31, 2017, the Company entered into an assumption reinsurance agreement with

its affiliate AIC, whereby, the Company ceded to AIC 100% of its business written in the State of New

York. As consideration, the Company transferred an amount equal to all gross outstanding loss reserves,

loss adjustment expense reserves, unearned premium reserves, and IBNR reserves relating to the policies

as of the effective date of the agreement.

11

E. Significant Ratios

The Company’s operating ratios, computed as of December 31, 2017, fall within the benchmark

ranges set forth in the Insurance Regulatory Information System of the National Association of Insurance

Commissioners, except for the two-year overall operating ratio, which is outside the benchmark range as a

result of the Company’s ceasing to write insurance business and transferring 100% of its losses to AIC.

Operating Ratios Result

Net premiums written to surplus as regards policyholders

0%

Liabilities to liquid assets (cash and invested assets less investments in affiliates) 15%

Two-year overall operating 999%

Underwriting Ratios

The underwriting ratios presented below are on an earned/incurred basis and encompass the five-

year period covered by this examination:

Amounts

Ratio

Losses and loss adjustment expenses incurred $ 6,105,831 27.79%

Other underwriting expenses incurred 14,277,924 64.99

Net underwriting

gain

1,586,930

7.22

Premiums earned

$

21,970,685

100.00%

The Company’s reported risk based capital score (RBC) was 15,205.80% at 12/31/2017. The RBC

is a measure of the minimum amount of capital appropriate for a reporting entity to support its overall

business operations in consideration of its size and risk profile. An RBC of 200 or below can result in

regulatory action.

There were no financial adjustments in this report that impacted the company’s RBC score.

12

3. FINANCIAL STATEMENTS

A. Balance Sheet

The following shows the assets, liabilities and surplus as regards policyholders as of December 31,

2017 as reported by the Company:

Assets

Assets

Assets Not

Admitted

Net Admitted

Assets

Bonds $ 9,103,355 $ 0 $ 9,103,355

Cash, cash equivalents and short

-

term investments

280,216

280,216

Receivables for securities 3,000,000 3,000,000

Investment income due and accrued

48,050

48,050

Current federal and foreign income tax recoverable

and

interest thereon

198,114 198,114

Receivables from parent, subsidiaries and affiliates 104,503 0

104,503

Total

a

ssets

$

12,734,238

$

0

$

12,734,238

Liabilities, surplus and other funds

Liabilities

Other expenses (excluding taxes, licenses and fees) $ 31,673

Net deferred tax liability

1,882,296

Total

liabilities

$

1,913,969

Surplus and Other Funds

Common capital stock

$

3,000,001

Gross paid in and contributed surplus 4,931,809

Unassigned funds (surplus)

$

2,888,459

Surplus as regards policyholders

10,820,269

Total

liabilities, surplus and other funds

$

12,734,238

13

B. Statement of Income

The net income for the examination period as reported by the Company was $15,706,980 as detailed

below:

Underwriting Income

Premiums earned

$21,970,685

Deductions:

Losses and loss adjustment expenses incurred $ 6,105,831

Other underwriting expenses incurred

14,277,924

Total underwriting deductions

20,383,755

Net underwriting gain or (loss)

$

1,586,930

Investment Income

Net investment income earned

$

1,593,579

Net realized capital gain 14,591,578

Net investment gain or (loss)

$

16,185,157

Other Income

Net gain or (loss) from agents' or premium balances charged off

$

301,571

Realized foreign exchange gain/loss (1,261,804)

Gain on sale of reinsurance recoverable

126,145

Total other income

(834,088)

Net income before federal

and foreign income taxes

$

16,937,999

Federal and foreign income taxes incurred

1,231,019

Net

i

ncome

$

15,706,980

14

C. Capital and Surplus

Surplus as regards policyholders decreased $19,061,961 during the five-year examination period

January 1, 2013 through December 31, 2017 as reported by the Company, detailed as follows:

Surplus as regards policyholders

as

report

ed

by the Company as of December 31, 2012

$29,882,230

Gains in

Losses in

Surplus Surplus

Net income

$15,706,980

Net unrealized capital gains or (losses)

2,021,986

Change in net unrealized foreign exchange capital

gain (loss)

111,754

Change in net deferred income tax

1,224,987

Change in non-admitted assets 2,245,218

Cumulative effect of changes in accounting

principles

1,225,878

Surplus adjustments paid in

4,002,990

Dividends to stockholders

27,408,703

Change in status of funded pension

991,097

Correction of errors

551,209

Correction of deferred tax item

3,810,113

Duplication of deferred tax non

-

admitted change

__________

1,200,028

Total gains and losses $20,719,491 $39,781,452

Net increase (decrease) in surplus

$

(19,061,961)

Surplus as regards policyholders

as

report

ed by

the Company as of December 31, 2017

$ 10,820,269

No adjustments were made to surplus as a result of this examination

At December 31, 2017, capital paid in was $3,000,001 consisting of 2,332 Shares of $1,286.45 par

value per share common stock. Gross paid in and contributed surplus decreased by $4,002,990 during the

examination period, as follows:

15

Year Description

Amount

2012 Beginning gross paid in and contributed surplus

$8,934,800

2016 Stock redemption * $(4,002,990)

Net decrease to paid in and contributed surplus (4,002,990)

2017 Ending gross paid in and contributed surplus $4,931,810

* In 2016, the Company entered into a stock redemption plan with its parent, AXA Art Holdings, Inc.,

pursuant to which, the Company reduced the number of its outstanding shares from 3,000 to 2,332 and

increased the par value per share from $1,000 to $1,286.45. The consideration paid by the Company was

$4,002,990.

4. LOSSES AND LOSS ADJUSTMENT EXPENSES

The examination liability for the captioned items of $0 is the same as reported by the Company as

of December 31, 2017.

On December 31, 2017, the Company transferred via 100% assumption reinsurance agreement all

gross outstanding loss reserves, loss adjustment expense reserves, unearned premium reserves, and IBNR

reserves relating to the policies as of the effective date of the agreement.

5. SUBSEQUENT EVENTS

On July 13, 2018, the Department approved the acquisition of control of the Company by Munich

Re Digital Partners US Holding Corporation (“MRDP”), a Delaware domiciled company whereby, MRDP

acquired 100% of the issued and outstanding common stock of the Company for a consideration of an

amount equal to the sum of:

a) The statutory capital and surplus of the domestic insurer; plus

b) An amount equal to the product of $150,000 multiplied by the number of states or jurisdictions in

which the Company holds an active license; plus

c) An amount equal to the product of $125,000 multiplied by the number of states or jurisdictions in

which the Company holds a restricted license.

The purchase price of $21 million was paid in cash and was funded via a capital contribution to

MRDP from its parent company.

16

As result of the acquisition of control, on July 31, 2018, the Company amended the Restated

Assumption Reinsurance Agreement whereby the Company transferred 100% of its business written in New

York to AXA Insurance Company; at the same time, it entered into and Administrative Services Agreement,

whereby AIC provides the Company administrative services and claim processing of policies.

6. COMPLIANCE WITH PRIOR REPORT ON EXAMINATION

The prior report on examination contained nine recommendations as follows (page numbers refer

to the prior report):

ITEM

PAGE NO.

A. Reinsurance

i. It was recommended that the Company execute a written agreement

before entering into any reinsurance arrangement.

7

ii. It was recommended that the Company comply with Section 1505(b) of

the New York Insurance Law.

7

iii. It was recommended that going forward, the Company adhere to the

provisions of Section 1505(d)(2) of the New York Insurance Law and

notify the Superintendent in writing before entering into any agreements

with affiliates.

9

B. Accounts and Records

i. It was recommended that the Company exercise greater care in the

preparation of its annual statement and file such in compliance with the

NAIC Annual Statement Instructions.

14

ii. It was recommended that the Company’s applications for insurance

contain the language required by Section 403(d) of the New York

Insurance Law.

14

iii. It was recommended that the Company keep records of the methods used

in allocating intercompany expenses and make these records available to

the examination team in accordance with the Department Regulation 30

Part 107.4(e).

14

17

iv. It was recommended that the Company report its salaries and payroll

taxes independently as prescribed in Department Regulation 30, Part

105.9.

15

v. It was recommended that the Company maintains its records as required

by Department Regulation 152(b)(7).

16

C.

Risk Management and Internal Control

i.

It was recommended that the Company put certain control procedures in

place and fully document each risk mitigation strategy in order for

examiners to evaluate the existence of controls in place at the Company

and to determine whether the control procedures are operating as

expected, applied throughout the entire period of reliance, and performed

on a timely basis.

16

Note: The prior report comments are no longer applicable due to the sale of the Company.

7. SUMMARY OF COMMENTS AND RECOMMENDATIONS

This report contains no comments or recommendations.

Respectfully submitted,

/S/

Maribel C. Nuñez, CPCU

Associate Insurance Examiner

STATE OF NEW YORK )

)ss:

COUNTY OF NEW YORK )

Maribel C. Nuñez, being duly sworn, deposes and says that the foregoing report, subscribed by her, is true

to the best of her knowledge and belief.

/S/

Maribel C. Nuñez, CPCU

Subscribed and sworn to before me

this day of , 2019.