© 2019 International Monetary Fund

IMF Country Report No. 19/52

AUSTRALIA

FINANCIAL SECTOR ASSESSMENT PROGRAM

TECHNICAL NOTE—SUPERVISION, OVERSIGHT, AND

RESOLUTION PLANNING OF FINANCIAL MARKET

INFRASTRUCTURES

This Technical Note on Supervision, Oversight, and Resolution Planning of Financial

Market Infrastructures for Australia was prepared by a staff team of the International

Monetary Fund as background documentation for the periodic consultation with the

member country. It is based on the information available at the time it was completed on

September 14, 2018.

Copies of this report are available to the public from

International Monetary Fund • Publication Services

PO Box 92780 • Washington, D.C. 20090

Telephone: (202) 623-7430 • Fax: (202) 623-7201

E-mail: publications@imf.org Web: http://www.imf.org

Price: $18.00 per printed copy

International Monetary Fund

Washington, D.C.

February 2019

AUSTRALIA

FINANCIAL SECTOR ASSESSMENT PROGRAM

TECHNICAL NOTE

SUPERVISION, OVERSIGHT, AND RESOLUTION PLANNING

OF FINANCIAL MARKET INFRASTRUCTURES

Prepared By

Monetary and Capital Markets

Department

This Technical Note was prepared by IMF staff in the

context of the Financial Sector Assessment Program

in Australia. It contains technical analysis and

detailed information underpinning the FSAP’s

findings and recommendations. Further information

on the FSAP can be found at

http://www.imf.org/external/np/fsap/fssa.aspx

January 22, 2019

AUSTRALIA

2 INTERNATIONAL MONETARY FUND

CONTENTS

Glossary __________________________________________________________________________________________ 3

EXECUTIVE SUMMARY __________________________________________________________________________ 5

INTRODUCTION _________________________________________________________________________________ 8

DESCRIPTION OF FINANCIAL MARKET INFRASTRUCTURES IN AUSTRALIA _________________ 9

A. Overview of Financial Market Infrastructures___________________________________________________ 9

B. Overview of the Supervisory, Oversight, and Resolution Framework __________________________ 12

C. Recent Developments _________________________________________________________________________ 14

ANALYSIS OF SELECTED ISSUES _______________________________________________________________ 15

A. Supervision and Oversight of FMIs ____________________________________________________________ 15

B. Resolution Planning and Central Bank Liquidity Support ______________________________________ 22

C. Selected Issues on ASX Clear__________________________________________________________________ 24

BOX

1. Supervision and Oversight of Cyber Risks and New Technologies ____________________________ 21

FIGURE

1. FMI Landscape in Australia ____________________________________________________________________ 11

TABLES

1. Recommendations for FMI Supervision, Oversight, and Resolution ____________________________ 7

2. Financial Resources of CCPs, 2017 Average ___________________________________________________ 11

ANNEXES

I. FSAP 2006 Recommendations and Follow-Up _______________________________________________ 28

II. CPMI-IOSCO Implementation Monitoring Assessment Results for Australia _________________ 30

III. FMI Statistics _________________________________________________________________________________ 31

IV. Governance of FMIs within the RBA _________________________________________________________ 33

V. Main Acts and Regulations for FMIs in Australia _____________________________________________ 34

AUSTRALIA

INTERNATIONAL MONETARY FUND 3

Glossary

ACCC

Australian Competition and Consumer Commission

AFMA

Australian Financial Markets Association

APRA

Australian Prudential Regulation Authority

ASX

ASX Limited

ASIC

Australian Securities and Investments Commission

AUD

Australian Dollar

CCP

Central Counterparty

CFR

Council of Financial Regulators

CFR FMI CMWG

CFR FMI Crisis Management Working Group

CHESS

Clearing House Electronic Sub-register System

Chi-X

Chi-X Australia Pty Ltd

CLS

CLS Bank

CME

Chicago Mercantile Exchange

CMG

Crisis Management Group

CPMI

Committee on Payments and Market Infrastructures

CPSS

Committee on Payment and Settlement Systems

CS facility

Clearing and Settlement facility (CCP or SSS)

CSD

Central Securities Depository

CSP

Critical Service Provider

DA

Digital Asset

DLT

Distributed Ledger Technology

D-SIB

Domestic Systemically Important Bank

ERM

Enterprise Risk Management

ESA

Exchange Settlement Account

EU

European Union

FMA

New Zealand Financial Markets Authority

FMI

Financial Market Infrastructure

FMIRC

FMI Review Committee

FRBNY

Federal Reserve Bank of New York

FSAP

Financial Sector Assessment Program

FSB

Financial Stability Board

FSS

Financial Stability Standards

IMF

International Monetary Fund

IOSCO

International Organization of Securities Commissions

IRD

Interest Rate Derivatives

LCH Ltd

LCH Limited

MPOR

Margin Period of Risk

MOU

Memorandum of Understanding

NCWO

No Creditor Worse Off

NIST

National Institute of Standards and Technology

NPP

New Payments Platform

AUSTRALIA

4 INTERNATIONAL MONETARY FUND

NZD

New Zealand Dollar

OTA

Offsetting Transaction Arrangement

OTC

Over the Counter

PFMI

CPSS

1

-IOSCO Principles for Financial Market Infrastructures

PSB

Payments System Board

PSNA

Payment Systems and Netting Act 1998

PSRA

Payment Systems (Regulation) Act 1998

RBA

Reserve Bank of Australia

RBNZ

Reserve Bank of New Zealand

RITS

Reserve Bank Information and Transfer System

RTGS

Real Time Gross Settlement

RTO

Recovery Time Objective

SSS

Securities Settlement System

SWIFT

Society for Worldwide Interbank Financial Telecommunications

1

Effective September 1, 2014, the Committee on Payment and Settlement Systems (CPSS) was renamed the

Committee on Payments and Market Infrastructures (CPMI). As the name change was after the publication of the

PFMI the reference is to CPSS.

AUSTRALIA

INTERNATIONAL MONETARY FUND 5

EXECUTIVE SUMMARY

Financial Market Infrastructures (FMIs) in Australia generally operate reliably, and the

competitive landscape has seen new entrants and competitors emerge. The Reserve Bank

Information and Transfer System (RITS), operated by the Reserve Bank of Australia (RBA), is the only

domestic systemically important interbank payment system. In addition, the domestically

incorporated ASX Limited (ASX) group operates an integrated infrastructure including trading

platforms, two central counterparties (CCPs), and two securities settlement systems (SSSs). Since

2011, the ASX has faced competition from foreign infrastructures in some markets, including Chi-X

Australia Pty Ltd (Chi-X) for cash equities trading and the LCH Limited (LCH Ltd) and the Chicago

Mercantile Exchange (CME) for some over the counter (OTC) derivatives clearing.

Supervision and oversight of FMIs is well-established with supervisory expectations

importantly strengthened over the past few years. The Australian authorities responsible for the

regulation, supervision, and oversight of FMIs are the RBA and the Australian Securities and

Investments Commission (ASIC). The RBA has sole responsibility for payment systems, while ASIC

and the RBA have complementary regulatory responsibilities for CCPs and SSSs. The FSAP

assessment is that Clearing and Settlement (CS) facility

2

supervision and oversight are strong and

that the FMI legal and regulatory framework generally is clear and transparent. The adoption of the

CPSS-IOSCO Principles for Financial Market Infrastructures (PFMI) and subsequent guidance has

strengthened the authorities’ approach with more comprehensive requirements and assessments, as

well as increased diligence in following up on findings. Cooperation among the authorities is close,

both domestically as well as with foreign authorities, although cooperation frameworks need to be

further developed to manage FMI crisis events. The mission recommends the RBA consider updating

its approach to payment systems oversight, in particular to increase the transparency around

expectations for potential (privately operated) systemically important payment systems.

Enforcement powers for the supervision of CCPs and SSSs should, however, be strengthened

in accordance with the PFMI. Currently, the RBA has no independent enforcement powers to

underpin its oversight. The RBA may request that ASIC issue a direction to comply with the FSS or to

reduce systemic risk; however, ASIC is not required to do so. Furthermore, the Minister may overrule

ASIC’s decision regarding whether to make or to revoke a direction. Although there is no evidence

of such intervention by the Minister (and, in fact the Minister has delegated certain responsibilities

to ASIC), the current legal basis for enforcing corrective actions should be strengthened with

independent powers for the RBA. It also is recommended that legislation should grant ASIC and the

ACCC the powers to promote fair and effective competition between FMIs, as such powers are

lacking. Supervisory powers could be broadened, for example, by granting rule writing powers in

addition to directions powers.

The Australian authorities have made some progress in formulating a special resolution

regime for FMIs. In 2015, the Australian government issued a high-level consultation paper to

2

CCPs and SSSs jointly are called Clearing and Settlement (CS) facilities under the Australian Corporations Act 2001.

AUSTRALIA

6 INTERNATIONAL MONETARY FUND

establish a special resolution regime for CS facilities (and trade repositories) consistent with

international standards. It requested feedback on the scope of the resolution authority, resolution

and directions powers, safeguards and funding arrangements, and international cooperation. The

CFR authorities are developing drafting instructions for legislation that would establish a resolution

regime for FMIs.

The government should prioritize finalization of its special resolution regime for domestic

FMIs, since it currently lacks the necessary framework and tools to resolve an FMI. The

authorities will need to address issues specific to Australia’s financial market structure, such as CS

facilities that are part of a vertically-integrated exchange group, the dominance of a few domestic

financial institutions and a few global banks in the Australian financial market, and issues regarding

the diversity and capacity of private-sector liquidity providers. This specific structure will have an

important bearing on the decisions that the Australian government will have to make regarding the

breadth of the authorities’ powers. Important considerations include the treatment of affiliated

entities within groups, including the implications for the point-of-entry strategy, and the breadth of

ex-ante resolvability assessments and FMI resolution plans.

New supervisory challenges, in particular related to cyber risks and new technologies, are

appropriately addressed by ASIC and the RBA; nevertheless, cyber resilience of FMIs would

further benefit from industry-wide cyber tests. RITS and ASX’s CS facilities are subject to regular

cyber resilience assessments by the authorities against CPMI-IOSCO guidance, international

standards, and good practices. Authorities could supplement these with industry-wide cyber

resilience tests to gain insights into the impact of a cyber incident on the industry as a whole. With

regard to distributed ledger technology (DLT) and other new technologies, ASIC’s and RBA’s

approach includes monitoring developments and specifying expectations. Supervision of the

replacement of ASX’s CS systems, which uses DLT technology, can be fully addressed within the

existing regulatory framework. It involves a permissioned model, where only ASX, clearing members,

and issuers would be authorized to participate. Private contractual information would be available

only to the transaction parties, and ASX would be the only permissioned writer to the ledger.

The FSAP’s assessment of elements of ASX Clear’s governance and risk management

framework identified several areas where further attention is warranted. ASX Ltd and the

authorities are encouraged to consider the impact of the current governance structure on

compliance with CS risk management requirements, including whether a simpler structure would

help meet requirements related to competition issues in the equity market more easily. The planned

FMI resolution regime will also have to address the integrated functions and any resulting obstacles

to the FMI’s resolvability. ASX Clear’s recovery plan should address its reliance on parent funding

and on other group services. Further improvements to its risk management systems should be

considered, such as the operational capacity to implement intraday margin calls, separate house and

client accounts, implementation of concentration limits on collateral, and availability of sufficient

pre-funded liquid resources before applying mechanical liquidity allocation mechanisms.

Operational risks need to be further addressed in line with authorities’ requirements.

AUSTRALIA

INTERNATIONAL MONETARY FUND 7

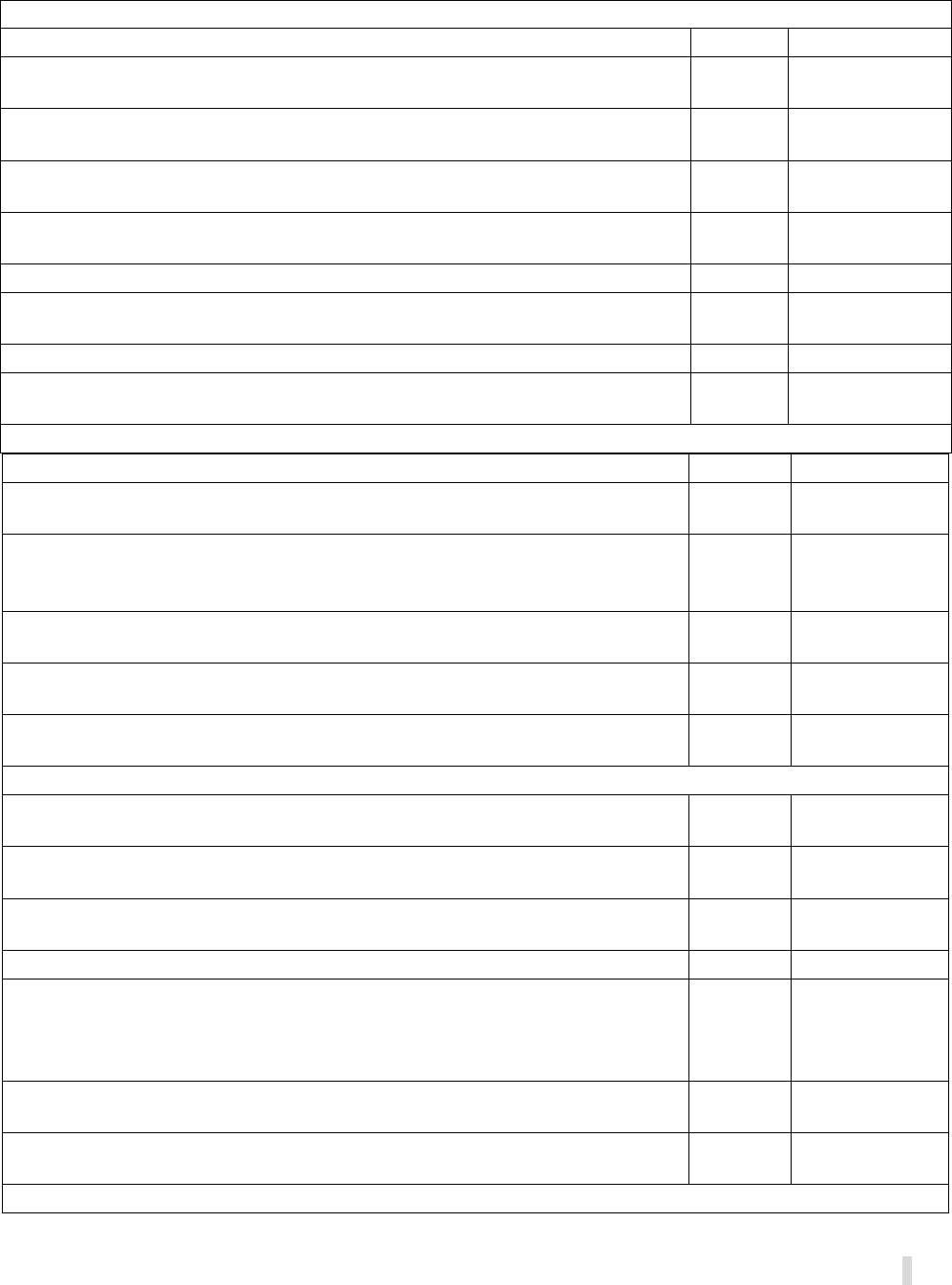

Table 1. Australia: Recommendations for FMI Supervision, Oversight, and Resolution

Recommendations for the Supervision and Oversight of FMIs

Timing

1

Responsibility

Increase transparency of regulatory expectations for potential (privately

operated) systemically important payment systems.

ST

RBA

Strengthen legal basis of direction powers for supervision of CS facilities, with

independence from the Minister and own powers for the RBA.

I

ASIC, RBA,

Treasury

Broaden the suite of enforcement tools for CS facilities.

ST

ASIC, RBA,

Treasury

Strengthen the legal and regulatory frameworks in the area of fair and effective

competition among CS facilities.

I

ASIC, RBA,

Treasury, ACCC

Complement cyber resilience assessments with industry-wide tests.

ST

CFR

Enhance the crisis communication framework for authorities for/supervisors of

CS facilities.

ST

ASIC, RBA

Update MOUs with ACCC on CS facilities matters.

ST

RBA, ASIC, ACCC

Streamline cooperation agreements with New Zealand authorities for ASX Clear

(Futures).

ST

RBA, ASIC,

RBNZ, FMA

Recommendations for the FMI Resolution Framework

Finalize the proposed special resolution regime for FMIs.

I

CFR

Address challenges related to current and potential FMI structure(s), and FMI-

specific, FMI group, FMI linkages, and inter-dependency factors.

I

CFR

Include broad directions powers in the Australian resolution regime to conduct

resolvability assessments and improve FMI resolvability ex ante. Ensure a

streamlined and timely process for issuance of directions.

I

CFR

Include broad powers in the Australian resolution regime to appoint a

statutory manager to resolve a distressed, failing, or failed FMI.

I

CFR

Include broad powers in the Australian resolution regime to transfer critical

FMI functions to a solvent third party or bridge FMI.

I

CFR

Ensure appropriate staffing with necessary knowledge and expertise regarding

resolution of systemically-important FMIs.

I

RBA, ASIC, and

Treasury

Recommendations to strengthen ASX Clear’s observance of the PFMI

Clarify the point at which settlement is final in the operating rules.

I

ASX Clear and

ASX Settlement

Address procyclicality through the annual validation process for margin

models.

ST

ASX Clear

Consider ring-fencing CS facilities within the ASX group structure through a

dedicated ERM, risk committee, staff, and risk management systems.

ST

ASX

Address group interdependencies fully in ASX Clear’s recovery plan.

I

ASX Clear

Replace the aging CHESS system with modern technology to increase

operational reliability and support compliance with financial risk management

requirements (e.g., operational capacity to conduct intraday margin calls and

segregated house and client accounts).

ST-MT

ASX Clear

Increase and diversify qualifying liquid resources to move the use of OTAs to a

later stage in the waterfall.

I

ASX Clear

Apply concentration limits on collateral and broaden the range of eligible

collateral to include government and semi-government bonds.

I

ASX Clear

1

I–Immediate (within 1 year); ST–Short-term (within 1 to 2 years); MT–Medium-Term (within 3 to 5 years).

AUSTRALIA

8 INTERNATIONAL MONETARY FUND

INTRODUCTION

3

1. FMIs are systemically important due to the central role that they play in interbank,

money, and capital markets.

4

FMIs provide the central infrastructure to clear and settle payments,

securities, and derivatives transactions and therefore lie at the core of the functioning of a sound

financial system. If FMIs are not properly managed, they could be sources of financial shocks and

risk transmission and potentially could have a negative impact on economic and financial stability.

For example, the failure of one of the payment systems or SSSs could result not only in losses

spreading through the system, but also in an ineffective implementation of monetary policy and a

loss of confidence in the financial system.

2. CCPs concentrate credit risk, and potentially could exacerbate or cause systemic

disruptions if they fail to absorb losses. A CCP does not eliminate counterparty credit risk but

manages it on behalf of its clearing participants. The concentration of credit risks in a CCP comes

with systemic externalities, in particular the possibility that a CCP could amplify adverse aggregate

shocks, for example, if it fails to manage the default of one or more participants. The potentially

pro-cyclical nature of a CCP’s margin calls and haircutting practices during a stress event could act

as macrofinancial feedback mechanisms that could increase market disruptions. The internationally

accepted presumption therefore is that, in principle, CCPs are systemically important, at least in the

jurisdiction where they are located, because of their critical roles in the markets they serve.

5

3. Important tools to manage systemic risks of CCPs include oversight, supervision, and,

more recently, crisis management planning, particularly resolution planning. In Australia,

authorities have adopted these tools to promote the stability of the financial system. ASIC and the

RBA are the authorities responsible for oversight and supervision of CCPs that provide services to

the Australian market. The Council of Financial Regulators (CFR)—made up of the RBA, ASIC, the

Australian Prudential Regulation Authority (APRA), and the Treasury—has started working on a

resolution framework for FMIs, with a focus on CCPs. The CFR is closely engaged in the development

of drafting instructions for legislation that is intended to be ready for introduction to Parliament in

2019.

4. The main objective of this note is to analyze systemic risks related to FMIs in Australia,

in particular CCPs. The note contains an analysis of:

3

The Technical Note was prepared by Froukelien Wendt, Senior Financial Sector Expert from the IMF Monetary and

Capital Markets Department and Heidilynne Schultheiss from the United States Federal Deposit Insurance

Corporation (on detail as an IMF external expert), for the 2018 Australia FSAP. Their analysis was based on

information provided by the authorities, publicly available information, including self-assessments of Australian FMIs,

and discussions with the RBA, ASIC, ACCC, APRA, Treasury, ASX, banks, and other financial institutions.

4

See Introduction to the CPSS-IOSCO Principles for Financial Market Infrastructures, April 2012. FMIs cover payment

systems, securities settlement systems (SSSs), central securities depositories (CSDs), central counterparties (CCPs),

and trade repositories.

5

See introduction of the PFMI report paragraph 1.20.

AUSTRALIA

INTERNATIONAL MONETARY FUND 9

a. The regulation, supervision, and oversight of FMIs in Australia, with the objective of

analyzing how well the supervisory and oversight structure is able to identify and manage

vulnerabilities related to FMIs. The team assessed the regulatory framework, supervisory

practices, available resources, transparency, adoption of international standards, and

coordination and cooperation mechanisms between and among authorities, both

domestically and cross-border. The analysis includes supervisory practices regarding cyber

risks and DLT.

b. Crisis management arrangements for FMIs, in particular the proposed resolution framework

for FMIs.

c. Some key elements of the governance and risk management rules, procedures, and practices

of ASX Clear, the CCP for cash equities and equity derivatives.

6

5. Recommendations in this note are based on the internationally-agreed standards for

FMIs, i.e., the PFMI. The analysis of the regulation, supervision, and oversight of FMIs is based on

the PFMI’s five responsibilities for authorities, whereas the assessment of ASX Clear is based on the

PFMI principles and related guidance. The analysis of the resolution framework for FMIs takes into

account the FSB Key Attributes of Effective Resolution Regimes for Financial Institutions and related

guidance on CCP resolution and resolution planning issued by the FSB.

6. The analysis builds on findings of earlier assessments. Earlier assessments are comprised

of the recommendations made during the 2006 Australia FSAP (Annex I), as well as the findings of

the CPMI-IOSCO implementation monitoring assessments (Annex II).

DESCRIPTION OF FINANCIAL MARKET

INFRASTRUCTURES IN AUSTRALIA

A. Overview of Financial Market Infrastructures

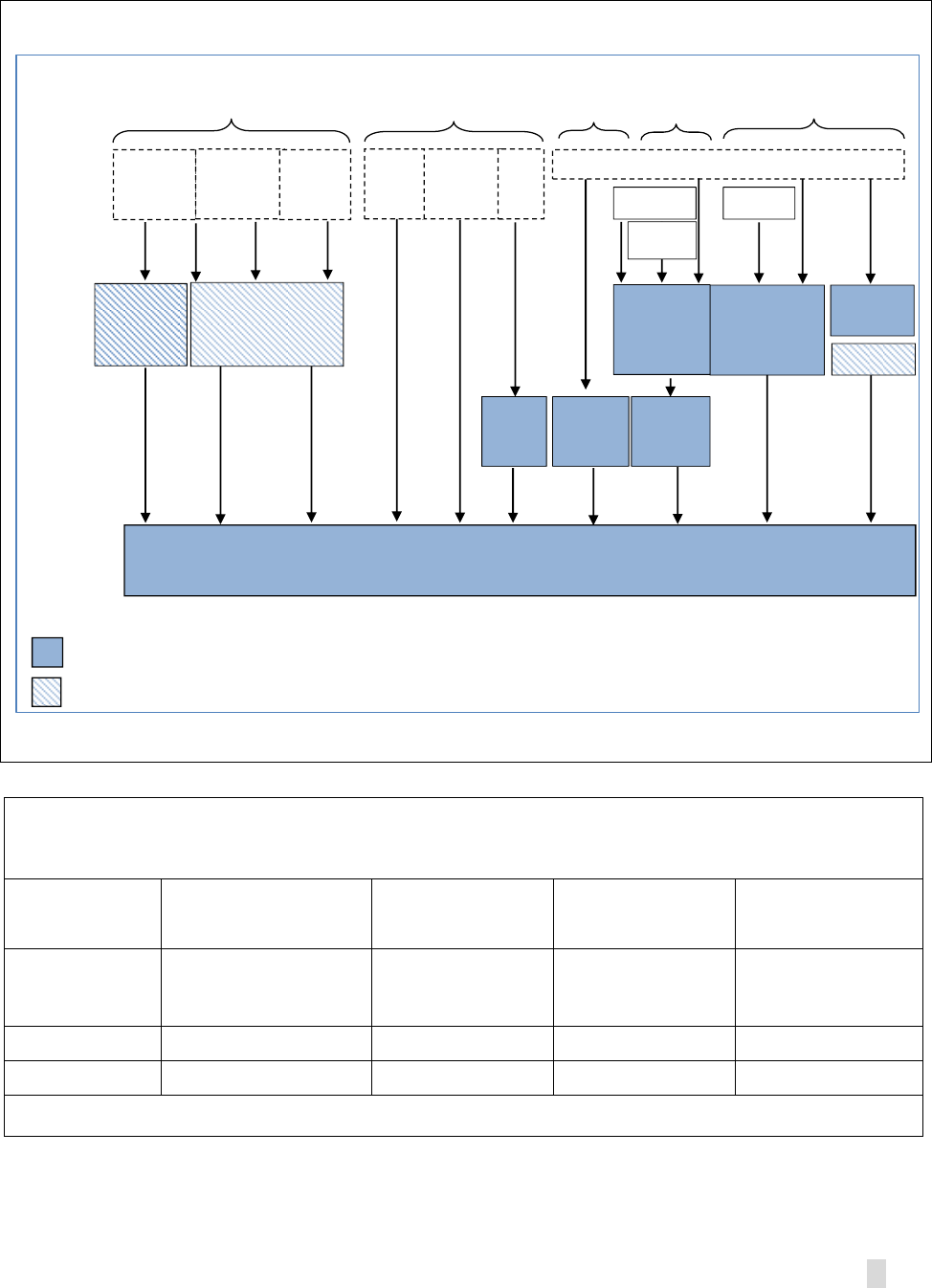

7. The following FMIs offer payment, clearing, and settlement services in Australia (see

also Figure 1):

Payment systems

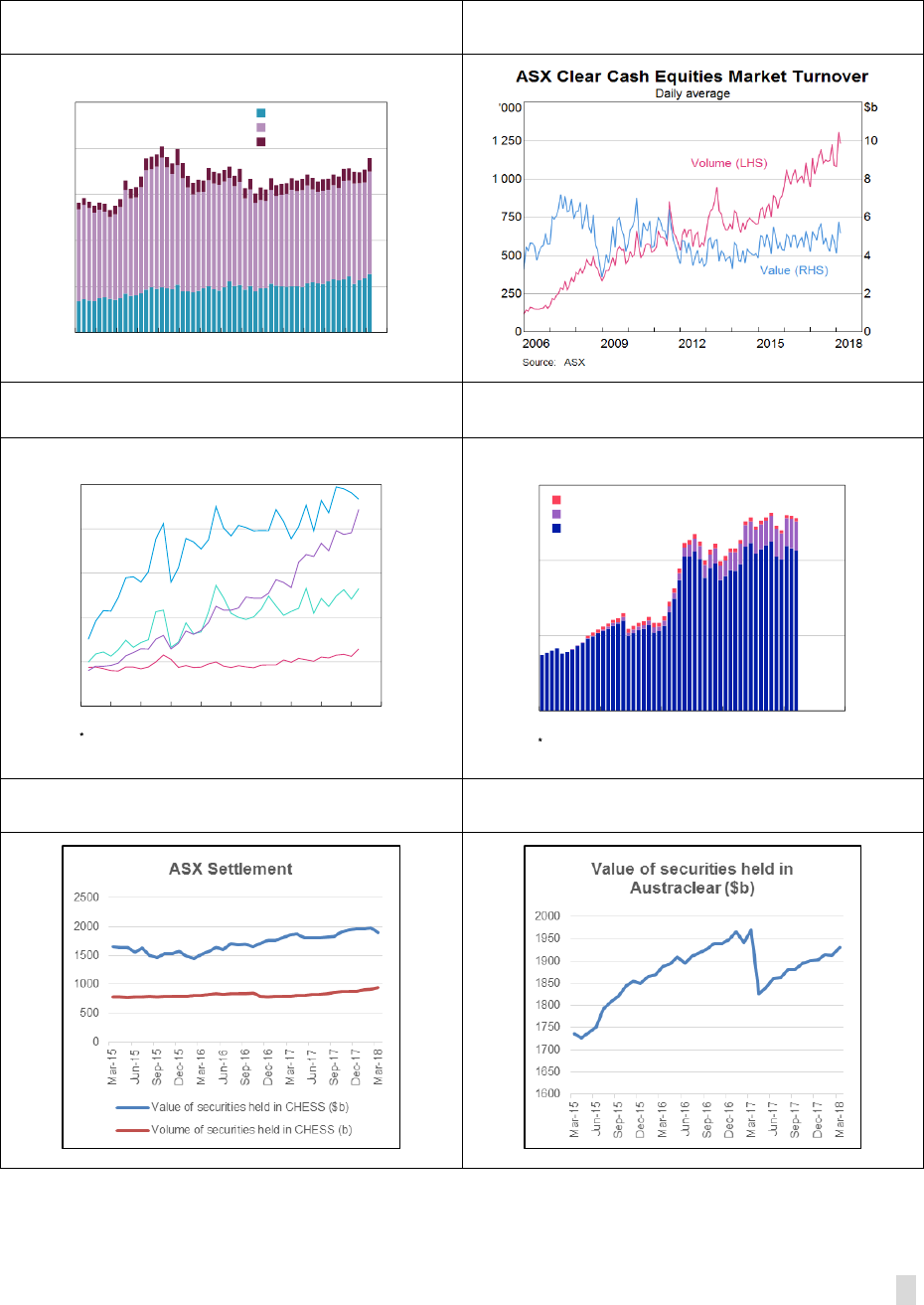

a. RITS is the principal domestic payment system in terms of the aggregate value of payments. It

handles time-critical, high value payments, and is used to settle payments from other

systemically important FMIs. Between April 2017 and March 2018, it settled an average of over

47,000 real-time gross settlement (RTGS) transactions each day, with an aggregate daily value

of around AUD 180 billion (11 percent of annual GDP).

b. CLS Bank (CLS) is an international payment system for settling foreign exchange trades in

18 currencies, including the Australian dollar.

6

The team selected some key elements related to governance and risk management of ASX Clear, but did not

analyze the complete risk management framework, nor did the team assess details of the margin, collateral, stress

testing, or liquidity risk policies. The analysis cannot be considered a full assessment against the PFMI.

AUSTRALIA

10 INTERNATIONAL MONETARY FUND

CCPs:

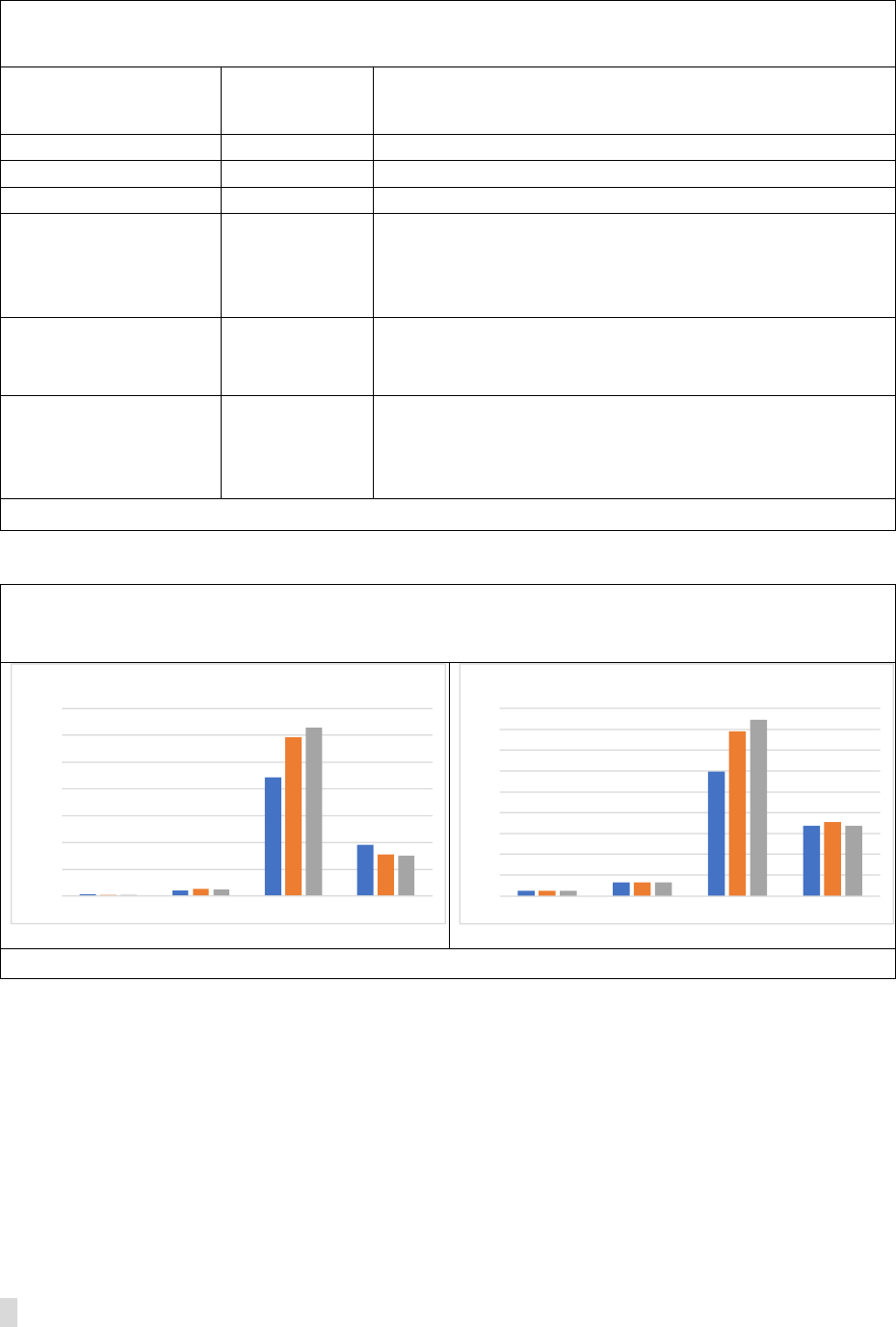

c. ASX Clear Pty Limited (ASX Clear) is the CCP for ASX-quoted cash equities, debt products and

warrants traded on the ASX and Chi-X markets, equity-related derivatives traded on the ASX

market and OTC, and Chi-X quoted warrants traded on Chi-X. The daily average value of cash

equity trades in the first half of 2018 was approximately AUD 5 billion (see FMI statistics in

Annex III).

d. ASX Clear (Futures) Pty Limited (ASX Clear (Futures)) provides CCP services for futures and

options on interest rate, equity, energy and commodity products traded on the ASX 24

market, as well as AUD- and NZD-denominated OTC interest rate derivatives (IRD).

e. LCH Ltd's SwapClear service provides CCP services for OTC IRD.

f. CME is licensed to provide CCP services for OTC IRD, and non-AUD IRD traded on the CME

market or the Chicago Board of Trade market for which CME permits portfolio margining for

OTC IRD.

SSSs and CSDs:

g. ASX Settlement Pty Limited (ASX Settlement) is a SSS for ASX-quoted cash equities, debt

products and warrants traded on the ASX and Chi-X markets. ASX Settlement also provides

SSS services for non-ASX listed securities quoted on other trading platforms in Australia.

h. Austraclear Pty Limited (Austraclear) provides SSS services for trades in debt securities,

including government bonds and repurchase agreements.

i. IMB Limited provides SSS services for trades in its own securities.

8. Australian authorities consider these FMIs to be systemically important in Australia,

with the exception of CME and IMB. As for payment systems, the RBA considers size,

interconnectedness, and substitutability in determining which systems are systemically important.

ASIC and the RBA consider domestic CS facilities (CCPs and SSSs) to be of systemic importance

given the central role that they play in financial markets. An exception is IMB Limited, given the very

narrow scope of its clearing and settlement activities. The systemic importance of foreign CS

facilities in Australia is determined based on a set of criteria, including the CS facility’s connections

to the Australian financial system and the materiality of these connections. Based on these criteria,

authorities do not consider CME to be systemically important for the Australian system at this

juncture. Table 2 contains an overview of the size of financial resources held by the four CCPs active

in Australia.

9. ASX Clear (Futures) is also systemically important for New Zealand banks. New Zealand

financial institutions depend on the operations of ASX Clear (Futures) for the clearing of NZD IRD.

Currently, New Zealand banks clear indirectly through direct clearing members of ASX Clear

(Futures).

AUSTRALIA

INTERNATIONAL MONETARY FUND 11

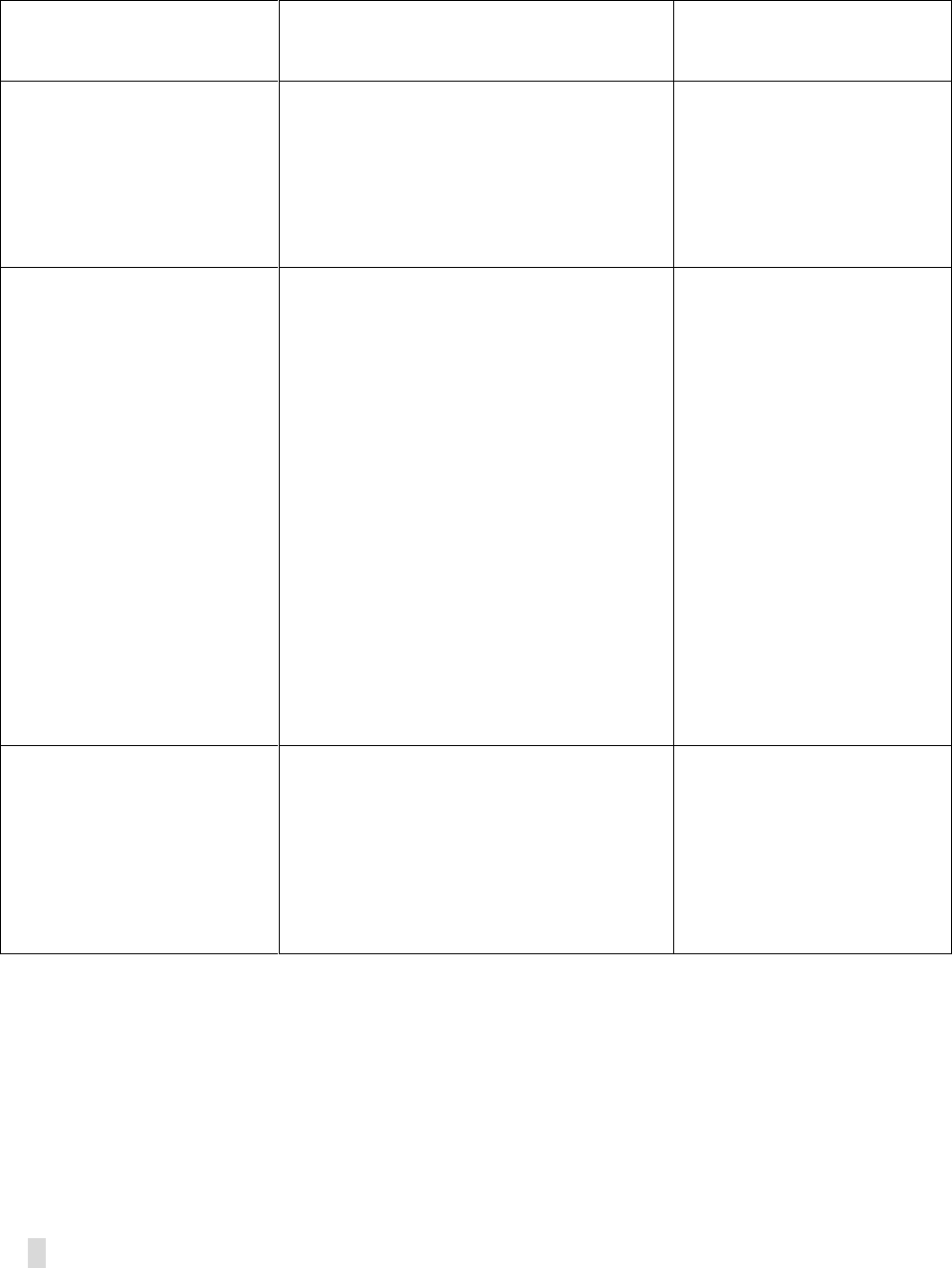

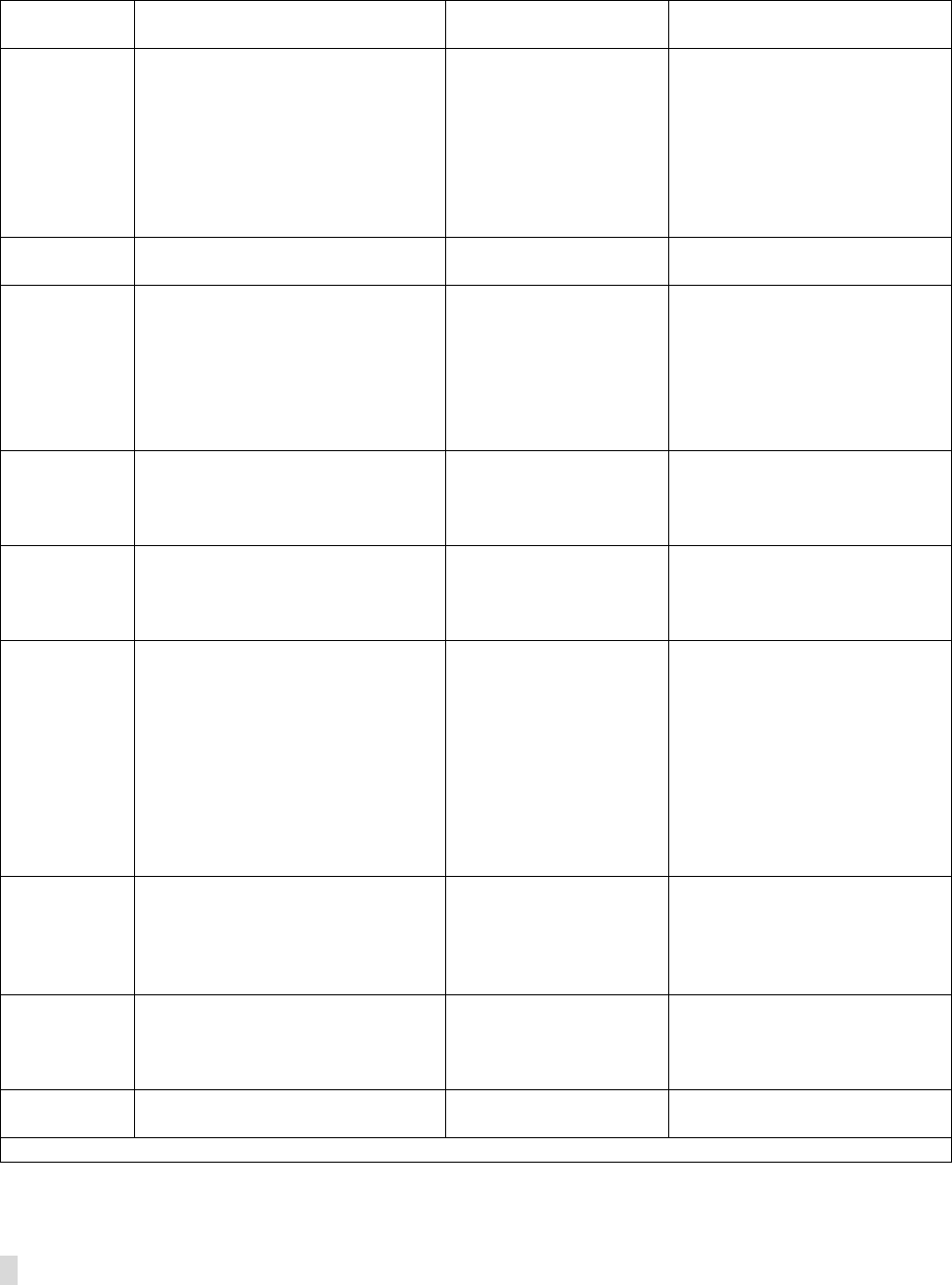

Figure 1. FMI Landscape in Australia

Source: IMF Mission.

Table 2. Australia: Financial Resources of CCPs, 2017 Average

(In millions of AUD)

ASX Clear

ASX Clear

(Futures)

LCH Ltd

SwapClear

CME IRD Service

Initial Margin

(excluding add-

ons)

1,090

(cash 150; equity

derivatives 940)

5,425

118,060

31,205

1

Default Fund

250

650

7,908

3,540

Total

1,340

6,075

125,968

34,745

1

This includes add-ons.

Source: RBA.

Source of

transfers:

Property

Inter-

bank

Clearing

system:

Securities/

FX

settlement

system:

RITS

(RTGS payment system)

Cash

settlement

system:

Large value payments

FX

Equities

OTC market

ASX Clear

Futures

Derivatives

LCH.

Ltd

Systemically important FMI in Australia

Non-Systemically important payment system or FMI in Australia

CLS

Retail payments

Cards,

ATM,

POS

Credit

and debit

transfers

AusPayNet

governed retail

systems

Checks

Austra

Clear

ASX Clear

ASX

Settle-

ment

Cards

Clearing

(Visa, MC,

ePAL

Debt

Securities

CME

ASX

Chi-X

ASX24

AUSTRALIA

12 INTERNATIONAL MONETARY FUND

10. The Direct Entry system, governed by the Australian Payments Network Limited’s

(AusPayNet’s) rules, is the largest retail payment system. AusPayNet is a self-regulatory industry

body that is responsible for rules and procedures for clearing and settling payments, including High

Value Clearing Stream payments, direct entry payments, check payments and ATM transactions in

Australia. Non-cash retail payments’ daily aggregate value between April 2017 and March 2018 was

around AUD 70 billion. Direct entry payments, comprising credit transfers and direct debits,

represented almost 90 percent of this value.

11. Card payments can be cleared domestically or through the international schemes.

There are three main debit cards operating in Australia: the domestic eftpos system (which is

managed by ePAL) and the international card schemes Mastercard and Visa. Most debit cards in

Australia are ‘dual-network’ meaning they have a functionality that enables a payment to be

processed via either eftpos or one of the two other networks. The international card schemes also

offer their respective four-party (American Express, MasterCard, and Visa) and three-party (American

Express and Diners Club) credit and charge cards in Australia.

12. The New Payments Platform (NPP) is a fast payments system launched in February

2018. The NPP enables close-to-immediate funds availability to payment recipients on a 24/7 basis,

even where the payer and payee use different financial institutions. In order to support this

functionality, the RBA has developed a Fast Settlement Service in RITS, which enables every single

payment made on the platform, regardless of its size, to be settled in real-time in central bank

funds, across each financial institution’s Exchange Settlement Account (ESA).

B. Overview of the Supervisory, Oversight, and Resolution Framework

13. The RBA is responsible for regulating and overseeing payment systems in Australia.

The RBA’s role is set out in the Reserve Bank Act, which states that the Payments System Board (PSB)

is responsible for determining the RBA’s payments system policy and ensuring that the RBA’s

powers are exercised in a way that will best contribute to: (i) controlling risk in the financial system;

(ii) promoting the efficiency of the payments system; and (iii) promoting competition in the market

for payment services, consistent with overall stability of the financial system. The PSB is comprised of

the RBA Governor as chair, one other RBA appointee, an appointee from the APRA, and up to five

other independent members. The PSB is one of the two Boards of the RBA, along with the Reserve

Bank Board. Annex IV illustrates the governance arrangements for FMIs in the RBA. In 2014, the RBA

also established the FMI Review Committee (FMIRC) to strengthen the governance arrangements for

policy decisions and approval of FMI assessments (see Responsibility D for further information).

14. The RBA’s payments system policy, functions, and powers are derived from three

dedicated Acts. These Acts are (i) the Payment Systems (Regulation) Act 1998 (PSRA), which allows

the RBA to gather information from participants in a payments system, designate a payment system

AUSTRALIA

INTERNATIONAL MONETARY FUND 13

and set Standards and Access Regimes for designated payment systems;

7

(ii) the Payment Systems

and Netting Act 1998 (PSNA), which provides additional legal certainty regarding settlement finality

in approved RTGS systems and netting arrangements;

8

and (iii) Part 7.3 of the Corporations Act

2001, which establishes conditions for the licensing and operation of CS facilities. Annex V lists these

and other relevant laws and regulations for FMIs in Australia.

15. The RBA shares responsibilities with ASIC for CS facilities. ASIC has responsibility for

market integrity and consumer protection for financial products and for facilities that trade, clear or

settle transactions involving financial products. Part 7.3 of the Corporations Act specifies how ASIC

and the RBA have separate, but complementary, responsibilities for CS facilities. The RBA has a

regulatory role in determining the Financial Stability Standards (FSS) for CS facilities. In addition, it

has supervisory powers for assessing compliance of CS facilities with the FSS. ASIC is responsible for

assessing compliance with the license requirements for CS facilities under the Corporations Act to

ensure that services are provided in a fair and effective manner. ASIC and the RBA have executed a

Memorandum of Understanding (MoU) to promote transparency, help prevent unnecessary

duplication of effort, and minimize the regulatory burden on CS facilities. In 2016, to streamline the

regulatory process, the Minister delegated her role in CS facility licensing and non-disallowance of

operating rules to ASIC officers.

16. The Treasury is responsible for providing advice to the Australian Government on the

financial sector’s regulatory framework. Treasury’s role is to support the drafting of legislation,

for example, in the area of FMI supervision and FMI resolution.

17. APRA’s role is limited to its seat on the PSB. As Australia’s prudential regulator of banks,

APRA has responsibility for the supervision of, among others, authorized deposit-taking institutions,

which are participants in the payments system and offer payment services to users such as

households and firms. APRA’s seat on the PSB primarily reflects its role as supervisor of payment

system participants.

18. These authorities coordinate FMI-related issues within the CFR. The CFR is a

non-statutory coordinating body for Australia’s main financial regulators, chaired by the RBA, and

comprised of the agency heads and one other senior representative from each of the RBA, APRA,

ASIC, and the Treasury. The CFR allows for sharing of information and, if needed, coordinating

responses to potential threats to financial stability. Recent FMI-related activities of the CFR include

developing (i) a special resolution regime for FMIs); and (ii) regulatory expectations and related legal

reforms to support fair and effective competition for trade and post-trade infrastructures (with the

involvement of the Australian Competition and Consumer Commission (ACCC)). These activities,

coordinated by an FMI Steering Committee, are performed by dedicated CFR working groups.

7

To date, the RBA has designated nine payment systems, all of which are retail payment systems, although not all

retail payment systems are designated.

8

Market netting declarations or approvals under the PSNA, which are the responsibility of Treasury or the Minister,

support the enforceability of FMI rules.

AUSTRALIA

14 INTERNATIONAL MONETARY FUND

19. The ACCC is involved in competition issues related to FMIs and payments systems. The

ACCC is responsible for ensuring that FMI and payment system operators and participants comply

with the general provisions of the Competition and Consumer Act 2010 (which govern competition

law in Australia generally). One aspect of this has been that it has conducted an investigation into

the regulations and procedures for the five clearing systems operated by AusPayNet in an

authorization context (where the ACCC may authorize conduct that otherwise would breach

competition law), as well as for the NPP. To promote a coordinated policy approach on competition

and access in the payments system, the ACCC and the RBA have signed a MoU that outlines how

they will work together. Under the relevant legislation the ACCC retains responsibility for

competition and access in a payments system unless the RBA imposes an access regime or sets

standards for that system. More recently, the ACCC has provided advice to ASIC and the RBA on

competition for trade and post-trade infrastructures and also was involved in developing the CFR’s

policy statements related to competition in the cash equity market.

C. Recent Developments

20. Recent developments include the development of a resolution regime for CCPs and

the adoption of DLT for the ASX securities clearing and settlement system:

a. In February 2015, the Australian government issued a high-level consultation paper,

“Resolution Regime for Financial Market Infrastructures,” that sought stakeholder views on

legislative proposals to establish a special resolution regime for domestic CS facilities and

systemically-important trade repositories, consistent with international standards. The paper

solicited feedback on topics including the scope of the resolution regime, the resolution

authorities, resolution powers, directions powers, safeguards and funding arrangements, and

international cooperation and support. In October 2015, the Government issued its response

to the 2014 Financial System Inquiry, in which it agreed that regulators should be provided

with clear powers in the event that a prudentially-regulated financial entity or FMI fails, in

order to help ensure a smooth functioning, resilient financial system. The Government

subsequently strengthened the resolution regime for prudentially-regulated entities, and

now is developing a resolution regime for FMIs, building on the CFR’s November 2015 paper

“Resolution Regime for Financial Market Infrastructures: Response to Consultation,” lessons

learned in developing the banking and insurance resolution regime, and recent advances in

international guidance and practice.

b. The ASX commenced a process for evaluating replacement options for the Clearing House

Electronic Sub-register System (CHESS) in 2015 and announced in December 2017 its plans

to replace CHESS with a new system that will include a permissioned, private DLT system.

The DLT part of the system consists of a shared, replicated ledger and a distributed database

synchronizing mechanism, where initially only ASX and clearing and settlement members

would be authorized to participate and the ASX is the only permissioned writer to the

ledger. The system is expected to provide market efficiencies through the elimination of

messaging and manual processes to ensure the integrity of databases and industry

AUSTRALIA

INTERNATIONAL MONETARY FUND 15

standardization across databases. The ASX is working with vendor Digital Asset (DA), in

which it owns a minority stake, to develop the replacement system.

ANALYSIS OF SELECTED ISSUES

A. Supervision and Oversight of FMIs

21. This section analyzes the extent to which the regulation, supervision, and oversight for

FMIs are in line with the five responsibilities of the PFMI. The objective is to benchmark

Australia’s regulatory, supervisory, and oversight framework against international standards and

analyze whether there are any gaps or issues of concern that could enable the buildup of systemic

risk.

Regulation, supervision and oversight of FMIs (Responsibility A)

22. The RBA’s role as overseer of the RITS payment system is clearly described in the joint

statement issued by ASIC and the RBA on implementing the PFMI in 2013. The statement

outlines that oversight of RITS is a key element of the PSB's responsibility for the safety and stability

of payment systems in Australia under the RBA Act. Furthermore, the statement contains criteria to

identify payment systems that are subject to RBA supervision: the payment system (i) is the sole

payment system in the country or the principal system in terms of the aggregate value of payments;

(ii) mainly handles time-critical, high-value payments; and (iii) is used to effect settlement in other

systemically important FMIs. The RBA plans to monitor developments in other payment systems and

periodically reviews whether other systems should be subject to PFMI assessments. This approach is

not yet formalized.

23. The PSRA gives the RBA a legal basis for regulating and overseeing payment systems,

which in practice is applied only to certain retail payment systems. The PSRA provides the RBA

with a legal basis to oversee payments systems through designation and standard setting for

payment systems. The RBA may use these powers only if it considers that it would be in the public

interest to do so. The PSRA additionally empowers the RBA to require a participant in a payment

system (whether designated or not) to give the RBA information relating to the payment system and

its participants. To date, only certain retail payment systems have been designated under the PSRA,

whereas other systems, for example the NPP, have not been designated.

24. The RBA considers CLS to be systemically important for the Australian financial system

and conducts oversight through the CLS oversight committee chaired by the Federal Reserve

Bank of New York (FRBNY). The RBA relies on the FRBNY for the oversight of CLS and participates

as a member of the CLS Oversight Committee. The joint statement and PSRA do not currently cover

oversight of foreign-based payment systems.

25. It is recommended that the RBA considers reviewing its approach to payment systems

oversight, in particular by providing greater clarity as regards requirements for systemically

and less systemically important payment systems. In line with approaches in other countries, the

AUSTRALIA

16 INTERNATIONAL MONETARY FUND

RBA could explicitly link the systemic importance of a payment system or service to (a selection of)

requirements in the PFMI (as far as not done yet), review consistency of existing requirements with

key concepts of the PFMI, and ensure that the oversight approach sufficiently allows addressing risks

related to new developments in the payments industry.

9

This would improve transparency, add

clarity to potential (privately operated) systemically important payment system providers, and could

support the RBA in conducting its oversight responsibilities effectively. More specifically the RBA

could consider:

a. Outlining the criteria for determining whether a payment system will be deemed to be

systemically important and required to meet the requirements of the PFMI.

b. Creating a category of prominent, but less systemically important, payment systems which

might be expected to meet some subset of the PFMI.

c. Developing a formal approach for conducting a ‘horizon scanning process’ to avoid a

situation in which a payment system that meets the criteria is not overseen.

26. The Corporations Act clearly outlines the criteria for CS facilities to be subject to

supervision in Australia. It defines a CS facility, requires that a CS facility can only operate under a

license provided by the Minister, and permits the imposition of conditions on a license. The Minister

can grant an exemption to a CS facility from the licensing requirement. In granting an exemption,

the Minister takes into account factors, which are set out in ASIC’s Regulatory Guide 211, and

include the nature and scale of the facility’s activities, the profile of its participants, and the financial

products for which it provides services. The division of responsibilities between ASIC and the RBA

regarding CS facilities is clearly outlined in the Corporations Act. The MOU provides for

arrangements to handle overlap in responsibilities, which in practice are managed through

cooperation and coordination (see Responsibility E).

27. The RBA also considers critical service providers (CSPs) in its supervisory approach.

Under the FSS, CS facilities are expected to scrutinize critical service providers against the oversight

expectations for CSPs (PFMI Annex F). The key CSP for RITS is the Society for Worldwide Interbank

Financial Telecommunications (SWIFT), an international interbank messaging system, as the failure

of SWIFT would severely impair the ability of members to effect third-party payments, as well as the

management of Austraclear settlements via the RITS Automated Information Facility (that uses

SWIFT messages). The RBA is represented in the SWIFT Oversight Forum, and through it receives

information on the oversight activities of the National Bank of Belgium and the SWIFT Oversight

Group.

9

For example, align an access regime imposed under the PSRA with the key considerations of principle 18 on access

and participation requirements, such as the requirement that an FMI should allow for fair and open access to its

services based on reasonable risk-related requirements.

AUSTRALIA

INTERNATIONAL MONETARY FUND 17

Powers and resources (Responsibility B)

28. The RBA uses its internal governance structure for oversight and operations of RITS to

induce change within RITS operations or enforce corrective action. Oversight activities are

located in the Payments Policy Department, whereas RITS operations are conducted within the

Payments Settlements Department. Both departments report to different managers within the RBA’s

organizational hierarchy with reporting lines converging at the level of the Deputy Governor.

Assessment findings are discussed within the PSB, which is chaired by the Governor and largely

comprised of independent board members. This process helps induce changes in RITS’s

arrangements consistent with the recommendations. The publication of assessment reports may

further induce changes. The two departments have established information-sharing arrangements,

which include information on material developments. The Payments Policy Department also has

access to a wide range of RITS data, such as on RITS activity, liquidity usage and availability, and

incidents.

29. RBA powers for other payment systems, which are designated under the PSRA, are

available as specified in the PSRA. The PSRA allows the RBA to obtain information from payments

system participants, to designate a payment system, and to set access regimes and standards for

designated payment systems. The PSRA also specifies the fines that apply if certain rules are

breached.

30. Information powers for CS facilities are clearly outlined in the Corporations Act. A

licensed CS facility is obliged under section 821C of the Corporations Act to give such assistance to

ASIC or the RBA as reasonably is requested in relation to the performance of the regulators’

respective functions. This assistance may include access to books and records or provision of other

relevant information. In addition, the ASIC Act gives ASIC inspection and investigation powers,

including the power to inspect books, require the production of documents, and summon

individuals to appear before ASIC and answer inquiries.

31. Enforcement powers for CS facilities rest with the Minister and ASIC. ASIC has powers

to undertake an assessment of a CS facility’s compliance with its obligations under the Corporations

Act, whereas the RBA has the power to assess compliance with the FSS. The Minister has powers to

require a special report, as well an audit report on the special report. If the Minister considers that a

CS facility licensee is not complying with its obligations as a CS facility licensee, the Minister may

give the licensee a written direction. ASIC also is empowered to give the licensee a direction in

writing, either at its own instigation or at the request of the RBA. A direction issued by the Minister

or ASIC is enforceable by court order. As a final resort, the Minister has the power to suspend or

cancel a license where the CS facility licensee has breached one or more of its obligations under the

Corporations Act. In 2016, the Minister delegated her role to ASIC for more timely consideration of

decisions.

32. It is recommended that the legal basis for ASIC’s and RBA’s supervisory enforcement

powers for CS facilities be strengthened and independence from the Minister be increased.

Under the current provisions, RBA has no independent enforcement powers. The RBA may request

AUSTRALIA

18 INTERNATIONAL MONETARY FUND

that ASIC issue a direction; however, ASIC is not required to do so. Furthermore, the Minister may

overrule ASIC’s decision to make or to revoke a direction and the Minister can still exercise the

powers that they have delegated should they deem it necessary. Although there is no evidence of

such intervention by the Minister, the power of the Minister weakens ASIC’s enforcement powers

and could constrain both ASIC and the RBA in carrying out their supervisory responsibilities. It is

therefore recommended to strengthen the legal basis for directions powers and ensure sufficient

independence from the Minister in day to day supervision. The mission recommends that RBA is

granted enforcement powers independently from ASIC.

33. Furthermore, it is recommended that authorities are granted additional powers to

support fair and effective competition between/among infrastructures. Competition between

trading platforms, e.g., between ASX and Chi-X, necessitates a legal and regulatory framework that

supports and ensures a level playing field. The CFR’s regulatory expectations for ASX’s conduct in

providing access to its monopoly cash equity CS services require transparent and non-discriminatory

treatment and terms and conditions, including pricing, that are fair and reasonable.

10

Treasury, in

cooperation with ASIC, the ACCC, and the RBA, is well-advanced in pursuing legislative changes to

make the regulatory expectations legally enforceable. ASIC would be provided with rule-making

powers, whereas the ACCC would be granted an arbitration power that would provide for binding

resolution of material disputes between ASX and a user seeking access to ASX CS services (including

ASX Clear and ASX Settlement). In case of potential competition between post-trade infrastructures,

the RBA would be involved from a financial stability perspective.

34. ASIC has sufficient staff resources to fulfill the responsibilities under its supervision

mandate. ASIC’s Market Infrastructure team is responsible for supervising and assessing the

operations of licensed CS facilities, financial markets, trade repositories, credit rating agencies, and

benchmark administrators, as well as considering new license applications. The team sits within the

broader Market Integrity Group, which also includes Market Supervision and Market Enforcement.

The Market Infrastructure team currently is comprised of 32 people directly involved in markets

infrastructure, of which the CS facilities team has at least five members, including a senior manager

and at least one technical senior specialist with appropriate experience, skills, and knowledge.

35. The RBA also has sufficient staff to fulfill the responsibilities under its supervision and

oversight mandate. A team of 21 people in the Payments Policy Department is responsible for FMI

oversight and policy development, with 17 staff members involved in regulation and oversight of CS

facilities. The RBA has also established arrangements to seek advice on specific issues from technical

experts (e.g., legal, IT) in other areas of the RBA. The team has appropriate experience, skills, and

knowledge to perform its duties. The department also has developed its own FMI training program,

with sessions on a range of relevant topics.

10

Regulatory Expectations for Conduct in Operating Cash Equity Clearing and Settlement Services in Australia, CFR,

updated in September 2017.

AUSTRALIA

INTERNATIONAL MONETARY FUND 19

Transparency (Responsibility C)

36. The RBA is transparent regarding its oversight requirements, and publicly discloses its

policies and regulations related to payment systems. RBA’s high-level objectives with regard to

payment systems are outlined in the RBA Act. This Act, the joint statement, the PSRA, the RBA’s

policies, PSB reports, assessment reports (including ratings), explanatory texts, and a range of other

information are disclosed to the public through the RBA’s website.

37. ASIC and the RBA are transparent in their supervisory requirements, and publicly

disclose their policies and regulations regarding the CS facilities. The Corporations Act, ASIC’s

Regulatory Guide 211, CS facility licensees, the FSS, the joint statement on implementing the PFMI in

Australia, as well as assessment reports (including ratings), media releases, explanatory texts, and a

range of other information are disclosed to the public through the RBA website and the ASIC

website.

Implementation of the PFMI (Responsibility D)

38. ASIC and the RBA have publicly adopted the PFMI. The joint statement outlines that ASIC

and the RBA are committed to apply the PFMI in their supervision and oversight of all FMI types.

Authorities also have adopted additional guidance regarding the PFMI, such as the guidance on

cyber resilience for financial market infrastructures issued in June 2016, recovery of financial market

infrastructures—revised report issued in July 2017, and resilience of central counterparties, issued in

July 2017.

39. The authorities apply the PFMI through detailed assessments and day-to-day

supervision and oversight activities. The PFMI are reflected in the FSS, with the FSS being more

specific on certain requirements, for example, on recovery and orderly wind-down, financial

resources, and the requirement that CCP services should be provided by a legal entity that is

separate from those providing services that could expose the CCP to unrelated risks. Authorities

have conducted one full assessment against the PFMI in 2014, and plan to repeat this on a five-year

basis. On an annual basis the RBA conducts an assessment against the FSS, reflecting the majority of

PFMI requirements. ASIC uses the PFMI in its thematic assessments, for example, on cyber resilience

of CS facilities. Furthermore, the authorities use the five responsibilities to conduct self-assessments

of their regulation, supervision, and oversight of FMIs in Australia.

40. RBA’s oversight of RITS has been effective in enhancing RITS’s observance of the

PFMI. The Payments Policy Department and the Payments Settlements Department organize

monthly meetings attended by the two departments’ senior management, and quarterly working-

level meetings. These formal review points, combined with ad hoc engagement, provide

opportunities to discuss material developments and identify oversight priorities. The mission found

that the oversight activities of the Payment Policy Department are comprehensive and that the

governance structure within the RBA supports independent oversight and is effective in inducing

change. In case of disagreement between the two departments, the issues are escalated, in some

cases to the level of the Governor. In crisis events the Assistant Governor responsible for the

Payment Policy Department is part of the crisis management team.

AUSTRALIA

20 INTERNATIONAL MONETARY FUND

41. Supervision of CS facilities is also effective with supervisory expectations having

increased importantly in recent years. Authorities meet quarterly on a technical level, every six

months at a strategic level, and every year with the ASX Board. The adoption of the PFMI and

follow-up CPMI-IOSCO guidance increased the level of supervisory requirements and engagement

with CS facilities. The annual FSS assessments are comprehensive with authorities following up on

detailed findings. The annual deep dive themes are thorough and allow for a good understanding of

the risks and gaps in compliance with the PFMI/FSS. The annual assessments started with deep dives

into financial risks and more recently into operational risks, whereas for the coming year legal risks

will be subject to a deep dive analysis. The mission found that, for example, ASX has strengthened

its financial risk management following RBA assessments and is in the process of following up on

requirements from both ASIC and the RBA regarding operational risk. Box 1 illustrates authorities’

supervision and oversight on two topical issues, cyber resilience and new technologies.

42. Consistent application of the PFMI across FMIs is promoted through the FMIRC within

the RBA. Following its self-assessment against the five responsibilities, the RBA created the FMIRC

as a senior-level internal review committee to review day-to-day oversight activities. The FMIRC

reports to both the Executive Committee and the PSB. Its main responsibilities concern review, and

for CS facilities, approval of the staff’s routine oversight and supervisory decisions, including the

interpretation of the PFMI, review of an FMI’s progress in meeting the RBA’s recommendations,

review of the FMI assessments, and for CS facilities, approval of the assessments. For RITS, the

approval of the assessments is the responsibility of the PSB. Consistency is further supported by the

publication of detailed assessment reports, including assessments of each relevant FMI’s observance

of the Principles.

Cooperation among authorities (Responsibility E)

43. Cooperation among domestic authorities is strong. ASIC and the RBA cooperate

effectively with respect to their responsibilities under the Corporations Act based on their prescribed

responsibilities, and more generally under the RBA-ASIC MOU. Although there is overlap,

inconsistencies and gaps are avoided through frequent and constructive communication and

coordination. The two authorities consult each other as part of their assessments, and typically

organize joint meetings with CS facilities, or otherwise brief each other on the outcomes of the

meetings. More broadly, the mission found that the CFR typically facilitates constructive

coordination among authorities.

44. MOUs covering the relationships between the ACCC and RBA and ASIC need to be

updated to better support information sharing among authorities. The RBA works with the

ACCC under an MOU that sets out aspects of how the two agencies will work together in relation to

payments systems. The relevant legislation sets out that the ACCC has general responsibility for

competition, while the RBA has specific responsibilities in relation to payments systems, including

the ability to impose an access regime or set standards for designated systems.

AUSTRALIA

INTERNATIONAL MONETARY FUND 21

Box 1. Supervision and Oversight of Cyber Risks and New Technologies

Cyber resilience is a key supervisory priority for the RBA and ASIC, with important progress being

made. The RBA conducted an initial assessment of RITS, and the RBA and ASIC jointly conducted an initial

assessment of ASX CS facilities, based on the 2016 CPMI-IOSCO cyber resilience guidance. External reviews

also were conducted against industry standards. On the two-hour recovery time objective (RTO)

requirement, it was agreed that the FMIs will implement enhancements to systems that would provide a

material net benefit to the FMI’s capability to meet the two-hour RTO. In addition, ASIC assessed cyber

resilience of other regulated entities operating in Australia’s financial markets using standards-based

surveillance tools and self-assessments adapted from the United States National Institute of Standards and

Technology (NIST) Framework. ASIC recently commenced a second round of these assessments.

Authorities could supplement the assessments with industry-wide cyber resilience tests to gain

insights into the impact of a cyber incident on the industry as a whole to support further

strengthening of resilience. Industry-wide cyber resilience tests conducted in other countries involved

supervisors, FMIs, banks, and other market participants with technical and high-level representatives.

Scenarios reflect cyber events, and the crisis is managed through active role playing with involvement of IT

and back offices, and simulated news streams.

A main supervisory challenge for the coming years will be the ASX’s replacement of the CHESS

system. Given the early stage of this project, no regulatory approvals have been granted by ASIC or the

RBA; however, authorities have engaged closely with ASX on the design and business requirements,

including functional, non-functional, and technical specifications for the replacement system. Now that ASX

has released the replacement system’s functional scope and the implementation roadmap, the regulators

plan to discuss with ASX the regulatory approvals and milestones for the system to go live. Given the scope

and systemic importance of the replacement system, authorities have allocated specific staffing resources

to oversee this work. Authorities are encouraged to continue their diligent approach of engaging with ASX

at all levels to ensure that operational risks are identified, managed, and mitigated.

More generally with regard to DLT and other new technologies, ASIC’s and RBA’s approach includes

monitoring developments and specifying expectations. At this stage, ASIC’s and the RBA’s view is that

the existing regulatory framework accommodates the emerging application of DLT to FMIs. Specifically, for

ASX’s CHESS replacement, a preliminary self-assessment of ASX against the FSS concluded that there is

nothing intrinsic to the envisaged DA DLT technology that would prevent ASX Clear and ASX Settlement

from complying with their regulatory obligations on an ongoing basis. More generally, ASIC developed an

information sheet to help ASIC and interested parties evaluate whether the use of DLT would allow an

entity to meet its regulatory obligations. All CS facilities are expected to demonstrate the appropriateness

of its technology (and human resources) for the services that it offers.

45. Designation of a payment system under the PSRA by the RBA does not, by itself,

remove that system from the ACCC’s jurisdiction. The MOU discusses how the two agencies will

share information and coordinate policy in relation to payments systems. ASIC also has an MOU

with the ACCC detailing cooperation arrangements. Both MOUs should be updated to reflect more

recent cooperation on competition for CS facilities (ASIC and the RBA) and trading platforms (ASIC),

in particular to facilitate the sharing of information among authorities.

46. Cooperation in times of crisis needs to be enhanced through a dedicated

communication framework for CS facilities that is regularly tested. ASIC has developed a

market wide industry crisis communication framework. The RBA has a crisis communication

AUSTRALIA

22 INTERNATIONAL MONETARY FUND

framework for payment systems. In addition, authorities need to enhance their crisis communication

framework that includes communication in case of incidents that affect CS facilities. The CFR could

be used to facilitate effective communication and coordination if an FMI was in financial or

operational distress. The CFR could, for instance, provide a forum to discuss the implications for a

distressed FMI’s participants, financial markets, and the public at large. Such a framework could

leverage lessons learned in developing CFR communications arrangements to manage crises in

prudentially-regulated entities. The framework needs to be regularly tested to identify and solve

potential barriers to communicate and coordinate effectively during a crisis.

47. International cooperation typically is facilitated by an MOU and allows for information

sharing and crisis management with foreign authorities. RBA’s participation in the CLS and

SWIFT oversight committees provides the RBA with information about the observance of these

systems with the PFMI. In addition, through these fora the RBA could identify issues that could be

relevant for FX settlement involving the AUD and messaging services for RITS, CLS, other FMIs, and

participants. The RBA and ASIC also cooperate with the Bank of England, the European Securities

and Markets Authority, and the U.S. Commodity Futures Trading Commission in relation to the

supervision of LCH Ltd, the ASX CCPs, and CME. For resolution and crisis management, Australian

authorities participate in the Crisis Management Group (CMG) for LCH Ltd.

48. A cooperation arrangement with New Zealand authorities is in place for ASX Clear

(Futures), which could be consolidated through a multilateral MOU that includes all relevant

agencies. Cooperation arrangements exist between the RBA and Reserve Bank of New Zealand

(RBNZ), and between ASIC and the New Zealand Financial Markets Authority (FMA). For clarity

reasons it is recommended to consolidate the relationship agreements between the Australian and

New Zealand authorities, for example, by including the FMA and ASIC in the RBNZ/RBA MOU for

CCPs located in Australia. This will ensure that all authorities are able to receive the same

information at the same time.

B. Resolution Planning and Central Bank Liquidity Support

49. The Australian authorities have made some progress in formulating a special

resolution regime for FMIs but need to finalize it expeditiously. In terms of a resolution

framework for FMIs, as noted above, authorities have issued a public consultation and currently are

working to refine the design of the FMI resolution regime and prepare drafting instructions for FMI

resolution legislation, with a view to having legislation ready for introduction into Parliament in

2019. Authorities are encouraged to proceed thoughtfully but with priority since Australia currently

lacks the necessary framework and tools to resolve an FMI that is in distress, failing, or that has

failed.

50. The authorities need to address issues specific to Australia’s financial market structure,

such as CS facilities that are part of a vertically-integrated exchange group, the dominance of

major domestic banks and a few global banks in the Australian financial market, and issues

regarding the diversity and capacity of private-sector liquidity providers. This specific structure

will drive the decisions that the Australian government will have to make regarding the breadth of

AUSTRALIA

INTERNATIONAL MONETARY FUND 23

authorities’ powers, particularly with respect to affiliated entities within groups. The point-of-entry

strategy is another important factor, where a balance will need to be struck between predictability

for FMIs and clearing and market participants and flexibility for resolution authorities to manage a

multitude of stress situations. Authorities are encouraged, in line with other jurisdictions, to use

pre-positioning powers to enhance the timeliness and efficacy of resolution actions in times of

stress. This includes the preparation of ex-ante resolvability assessments and FMI resolution plans

and the imposition of requirements on FMIs to remove any barriers to implementation of resolution.

Resolution plans should address the specific nature of FMIs. For example, resolution plans for CCPs

should take into account issues such as risk management, margining, collateral, and investment

interdependencies within the ASX group, the preservation of netting sets within and across ASX

entities, ensuring that positions and collateral are kept together, and any necessary license transfers.

The authorities should ensure that they currently and will have appropriate staffing with necessary

knowledge and expertise regarding systemically-important FMIs to support the formulation,

implementation, and operationalization phases of resolution.

51. The authorities should review, and could benefit from, the experiences of and lessons

learned in the formulation and codification of Australia’s bank and insurer resolution regime.

The legal framework for bank resolution was strengthened by the Crisis Resolution Powers Bill

passed in February 2018. Experiences regarding recovery planning, directions powers, stay

arrangements, and safeguards are well developed for banks and could provide lessons and guidance

for FMI resolution planning. Other aspects that are less developed, such as no creditor worse off

(NCWO) principles, and resolution planning are addressed in parallel FSAP recommendations for

bank resolution, and also should be considered in designing the FMI resolution regime.

11

The

interactions between the bank resolution regime and FMI resolution regime also are relevant since

banks are FMI participants. Bank resolution plans should be used to help better understand banks’

exposures to FMIs, and more broadly, the interconnections between FMIs and banks that are their

participants, liquidity providers, investment counterparties, custodians, investment managers, and

settlement mechanisms.

52. The authorities need to address some potentially controversial issues that are common

across CS structures and jurisdictions, such as the time limitations on stays, payment

moratoria, suspension of shareholder rights and writing down of equity, application of the

NCWO principle and its counterfactual, payment of claims, temporary last-resort public

funding, and allocation of and recoupment of any losses, each of which potentially could

present obstacles. Authorities could benefit from the experiences of and lessons learned by other

jurisdictions through their regular and more specialized coordination and communication efforts

with other supervisors and resolution authorities.

53. CCPs that are licensed in Australia have access to ESAs and liquidity facilities of the

RBA. CCPs that are systemically important in Australia are required to settle their AUD obligations

using an ESA in their name or a related body that is acceptable to the RBA. Currently, CCPs can hold

funds as overnight deposits at the RBA, but large daily variations in balances without notice to the

11

See FSAP 2018 Technical Note ‘Bank Resolution and Crisis Management.’

AUSTRALIA

24 INTERNATIONAL MONETARY FUND

RBA are discouraged as they could complicate the implementation of monetary policy. Access to the

overnight deposit facility reduces the CCPs’ exposures to the risk that one (or more) of their

commercial counterparties failed overnight. CCPs can also obtain central bank liquidity support

against eligible collateral.

C. Selected Issues on ASX Clear

54. This section analyzes some key elements of the governance and risk management

framework of ASX Clear that are relevant from a financial stability perspective. ASX Clear’s

rules, procedures and practices are benchmarked against the PFMI and international practices. The

team did not analyze the complete risk management framework, nor did the team assess details of

the margin, collateral, stress testing, or liquidity risk policies.

Systemic risk

55. ASX Clear’s systemic risk related to its central role in the equity market is generally

well managed through governance and risk management frameworks, but improvements on

certain aspects are warranted. As sole CCP for equity markets in Australia, ASX Clear is critical for

the functioning of domestic equity markets. Although credit exposures are short term (settlement is

on T+2) compared to derivatives clearing, its interconnectedness with the broader financial system

(35 participants, including the 4 domestic systemically important banks (D-SIBs), large foreign banks,

2 trading platforms, 1 SSS) and its efficiencies through multilateral netting, would create liquidity

and credit stresses among its participants in case of its failure. It is therefore of systemic importance

that ASX Clear manages its credit, liquidity, operational, and other risks in a prudent manner. The

mission found that ASX Clear operations generally are reliable, however, additional steps are

warranted to increase compliance with the PFMI. This is discussed in the remainder of this section.

56. The potential procyclicality of ASX Clear’s margins and collateral haircuts is limited

through conservative haircut setting. In setting haircuts, ASX Clear uses a 20-year historic period,

which included the high volatility observed during the 2008 global financial crisis, and a 99.9 percent

confidence level. The calibration of haircuts is intended to ensure that they remain relatively stable

during stress circumstances, and as such prevent the exacerbation of volatility, liquidity strains, and

general financial distress. Procyclicality could be addressed more comprehensively through the

annual validation process for margin models.

Legal risk (Principles 1, 8)

57. ASX Clear has a sound legal basis for its clearing activities. The Corporations Act, PSNA,

and the ASX Clear rules govern novation, netting, and collateral arrangements, as well as default

procedures, and the enforceability of related rights and obligations. ASX Clear currently has no

overseas clearing members and does not accept non-domestic collateral. If ASX Clear allows access

to non-local clearing members or accepts non-domestic collateral it should identify and mitigate

potential conflicts of law through legal opinions, in line with good international practices.

AUSTRALIA

INTERNATIONAL MONETARY FUND 25

58. Although the PSNA provides a firm statutory foundation for finality of settlement, the

rules of ASX Settlement should more clearly define the point at which settlement is final. The

operating rules of ASX Settlement are the relevant rules for settlement of transactions cleared by

ASX Clear. The rules currently describe the payment and security delivery rights and obligations of

participants at the time of settlement in CHESS at T+2 (i.e., 11.30 a.m.), as well as the last

opportunity for settlement participants to revoke a transaction. The rules do not, however, explicitly

describe the point at which settlement is final. Including the exact point that settlement is final is

required by the PFMI to quickly ascertain positions of the clearing participants in a resolution

scenario.

Governance and overall risk management approach (Principles 2, 3)

59. ASX is implementing and fine-tuning its group-wide enterprise risk management

(ERM) model but should consider addressing CCP-specific risks more directly. The ERM is

implemented at the group level, and although counterparty credit risks are included as a risk type

reviewed by the ASX Board, along with, for example, strategic risk, CCP-specific risks could be

marginalized in the overall scheme. Although the two ASX CCPs have individual boards that review

risk information and external Risk Consultative Committees, the CCPs do not have CCP-specific

internal risk committees. Rather, risks are discussed in the Audit and Risk Committee at the ASX Ltd

Board level. Also, as a result of the group-wide risk management approach and the sharing of

services and staff provided by ASX Operations Pty Limited to the CCPs, each CCP does not have its

own dedicated staffing, including risk management staffing. ASX should consider establishing CCP-

specific internal risk committees, dedicated CCP-specific risk management and staffing, risk

management systems, and resolution-friendly shared services agreements that account for intra-

group inter-dependencies. An option could include a separate risk committee for each of the CCPs

with a dedicated ERM for each of the CCPs, and inclusion of critical staff and systems within each of

the CCP legal entities. Such a separation would also make it simpler when considering safe and

effective competition issues in the equity market.

60. ASX Clear’s recovery plan should more comprehensively address intragroup

interdependencies. The recovery plan currently identifies a few interdependencies with other