1

Managing

the Business

Risk of Fraud:

A Practical Guide

SPONSORED BY:

The Institute of Internal Auditors

The American Institute of

Certified Public Accountants

Association of

Certified Fraud Examiners

1

The views expressed in this document are for guidance purposes only and are not binding on organizations.

Organizations should design and implement policies and procedures that best suit them. The IIA, AICPA, and ACFE

shall not be responsible for organizations failing to establish policies and procedures that best suit their needs.

This guide is intended to be applicable globally but heavily references practices in the United States and, where

available, provides references to information from other countries, as well. We anticipate further references will be

included in future updates.

FROM THE SPONSORING ORGANIZATIONS:

The Institute of Internal Auditors

David A. Richards, CIA, CPA

President and Project Manager

The American Institute of Certified Public Accountants

Barry C. Melancon, CPA

President and CEO

Association of Certified Fraud Examiners

James D. Ratley, CFE

President

2

Toby J.F. Bishop, CPA, CFE, FCA

Director, Deloitte Forensic Center

Deloitte Financial Advisory Services LLP

Corey Anne Bloom, CA, CA•IFA, CFE

Senior Associate, Dispute Resolution and Financial

Investigation Services

RSM Richter Inc.

Joseph V. Carcello, Ph.D., CIA, CPA, CMA

Director of Research, Corporate Governance Center

Ernst & Young Professor

University of Tennessee

David L. Cotton, CPA, CFE, CGFM

Chairman

Cotton & Company LLP

Holly Daniels, CIA, CISA

Technical Director, Standards and Guidance

The Institute of Internal Auditors

Ronald L. Durkin, CPA, CFE, CIRA

National Partner in Charge, Fraud & Misconduct

Investigations

KPMG LLP

David J. Elzinga, CA•IFA, CFE

Partner, Forensic Accounting & Investigation Services

Grant Thornton LLP

Robert E. Farrell, CFE

Principal, White Collar Investigations

Bruce J. Gavioli, CPA, MBA

Partner

Deloitte Financial Advisory Services LLP

John D. Gill, JD, CFE

Research Director

Association of Certified Fraud Examiners

Sandra K. Johnigan, CPA, CFE

Johnigan, P.C.

Thomas M. Miller, CPA\ABV, CFE, PI

Technical Manager, Forensic and Valuation Services

AICPA

Lynn Morley, CIA, CGA

Morley Consulting & Training Services Inc.

Thomas Sanglier

Partner

Ernst & Young LLP

Jeffrey Steinhoff

Managing Director, Financial Management and

Assurance (Retired)

U.S. Government Accountability Office

William E. Stewart

Partner, Fraud Investigation & Dispute Services

Ernst & Young LLP

Bill Warren

Director, Fraud Risks and Controls

PricewaterhouseCoopers LLP

Mark F. Zimbelman, Ph.D.

Associate Professor and Selvoy J. Boyer Fellow

Brigham Young University

TEAM MEMBERS:

PROJECT ADVISORS:

Eleanor Bloxham

Chief Executive Officer

The Value Alliance and Corporate Governance Alliance

Larry Harrington

Vice President, Internal Audit

Raytheon Company

3

ENDORSERS:

The above organizations endorse the nonbinding guidance of this guide as being of use to management and

organizations interested in making fraud risk management programs work. The views and conclusions expressed in

this guide are those of the authors and have not been adopted, approved, disapproved, or otherwise acted upon by

a committee, governing body, or the membership of the endorser.

®

4

Managing the Business Risk of fRaud: a PRactical guide

TABLE OF CONTENTS PAGE

INTRODUCTION 5

SECTION 1: FRAUD RISK GOVERNANCE 10

SECTION 2: FRAUD RISK ASSESSMENT 19

SECTION 3: FRAUD PREVENTION 30

SECTION 4: FRAUD DETECTION 34

SECTION 5: FRAUD INVESTIGATION AND CORRECTIVE ACTION 39

CONCLUDING COMMENTS 44

APPENDICES:

APPENDIX A: REFERENCE MATERIAL 45

APPENDIX B: SAMPLE FRAMEWORK FOR A FRAUD CONTROL POLICY 48

APPENDIX C: SAMPLE FRAUD POLICY 50

APPENDIX D: FRAUD RISK ASSESSMENT FRAMEWORK EXAMPLE 55

APPENDIX E: FRAUD RISK EXPOSURES 57

APPENDIX F: FRAUD PREVENTION SCORECARD 61

APPENDIX G: FRAUD DETECTION SCORECARD 65

APPENDIX H: OCEG FOUNDATION PRINCIPLES THAT RELATE TO FRAUD 69

APPENDIX I: COSO INTERNAL CONTROL INTEGRATED FRAMEWORK 79

........................................................................................................................................................

...................................................................................................................

......................................................................................................................

..............................................................................................................................

................................................................................................................................

...............................................................................

.......................................................................................................................................

........................................................................................................................

.....................................................................

......................................................................................................................

...........................................................................

.....................................................................................................................

.......................................................................................................

.........................................................................................................

..................................................................

......................................................................

5

Managing the Business Risk of fRaud: a PRactical guide

Fraud is any intentional act or omission designed to deceive others, resulting in the victim suffering a

loss and/or the perpetrator achieving a gain

1

.

INTRODUCTION

All organizations are subject to fraud risks. Large frauds have led to the downfall of entire organizations, massive

investment losses, significant legal costs, incarceration of key individuals, and erosion of confidence in capital

markets. Publicized fraudulent behavior by key executives has negatively impacted the reputations, brands, and

images of many organizations around the globe.

Regulations such as the U.S. Foreign Corrupt Practices Act of 1977 (FCPA), the 1997 Organisation for Economic

Co-operation and Development Anti-Bribery Convention, the U.S. Sarbanes-Oxley Act of 2002, the U.S. Federal

Sentencing Guidelines of 2005, and similar legislation throughout the world have increased management’s

responsibility for fraud risk management.

Reactions to recent corporate scandals have led the public and stakeholders to expect organizations to take a

“no fraud tolerance” attitude. Good governance principles demand that an organization’s board of directors, or

equivalent oversight body, ensure overall high ethical behavior in the organization, regardless of its status as public,

private, government, or not-for-profit; its relative size; or its industry. The board’s role is critically important because

historically most major frauds are perpetrated by senior management in collusion with other employees

2

. Vigilant

handling of fraud cases within an organization sends clear signals to the public, stakeholders, and regulators about

the board and management’s attitude toward fraud risks and about the organization’s fraud risk tolerance.

In addition to the board, personnel at all levels of the organization — including every level of management, staff,

and internal auditors, as well as the organization’s external auditors — have responsibility for dealing with fraud

risk. Particularly, they are expected to explain how the organization is responding to heightened regulations, as well

as public and stakeholder scrutiny; what form of fraud risk management program the organization has in place; how

it identifies fraud risks; what it is doing to better prevent fraud, or at least detect it sooner; and what process is in

place to investigate fraud and take corrective action

3

. This guide is designed to help address these tough issues.

This guide recommends ways in which boards

4

, senior management, and internal auditors can fight fraud in

their organization. Specifically, it provides credible guidance from leading professional organizations that defines

principles and theories for fraud risk management and describes how organizations of various sizes and types can

1

This definition of

fraud

was developed uniquely for this guide, and the authors recognize that many other definitions of fraud exist, including

those developed by the sponsoring organizations and endorsers of this guide.

2

Refer to The Committee of Sponsoring Organizations of the Treadway Commission’s (COSO’s) 1999 analysis of cases of fraudulent financial

statements investigated by the U.S. Securities and Exchange Commission (SEC).

3

Refer to June 2007 SEC

Commission Guidance Regarding Management’s Report on Internal Control Over Financial Reporting Under

Section 13(a) or 15(d) of the Securities Exchange Act of 1934

and U.S. Public Company Accounting Oversight Board (PCAOB) Auditing

Standard No. 5 (AS5), An Audit of Internal Control Over Financial Reporting That Is Integrated With an Audit of Financial Statements, for

comments on fraud responsibilities.

4

Throughout this paper the terms

board

and

board of directors

refer to the governing body of the organization. The terms

chief executive

officer

(CEO) and

chief financial officer

(CFO) refer to the senior level management individuals responsible for overall organization

performance and financial reporting.

6

establish their own fraud risk management program. The guide includes examples of key program components and

resources that organizations can use as a starting place to develop a fraud risk management program effectively

and efficiently. Each organization needs to assess the degree of emphasis to place on fraud risk management based

on its size and circumstances.

EXECUTIVE SUMMARY

As noted, fraud is any intentional act or omission designed to deceive others, resulting in the victim suffering a loss

and/or the perpetrator achieving a gain. Regardless of culture, ethnicity, religion, or other factors, certain individuals

will be motivated to commit fraud. A 2007 Oversight Systems study

5

discovered that the primary reasons why fraud

occurs are “pressures to do ‘whatever it takes’ to meet goals” (81 percent of respondents) and “to seek personal

gain” (72 percent). Additionally, many respondents indicated that “they do not consider their actions fraudulent”

(40 percent) as a reason for wrongful behavior.

Only through diligent and ongoing effort can an organization protect itself against significant acts of fraud. Key

principles for proactively establishing an environment to effectively manage an organization’s fraud risk include:

Principle 1: As part of an organization’s governance structure, a fraud risk management program

6

should be in place, including a written policy (or policies) to convey the expectations of the

board of directors and senior management regarding managing fraud risk.

Principle 2: Fraud risk exposure should be assessed periodically by the organization to identify specific

potential schemes and events that the organization needs to mitigate.

Principle 3: Prevention techniques to avoid potential key fraud risk events should be established, where

feasible, to mitigate possible impacts on the organization.

Principle 4: Detection techniques should be established to uncover fraud events when preventive

measures fail or unmitigated risks are realized.

Principle 5: A reporting process should be in place to solicit input on potential fraud, and a coordinated

approach to investigation and corrective action should be used to help ensure potential

fraud is addressed appropriately and timely.

The following is a summary of this guide, which provides practical evidence for organizations committed to

preserving stakeholder value. This guide can be used to assess an organization’s fraud risk management program,

as a resource for improvement, or to develop a program where none exists.

Fraud Risk Governance

Organization stakeholders have clearly raised expectations for ethical organizational behavior. Meanwhile,

regulators worldwide have increased criminal penalties that can be levied against organizations and individuals

5

The 2007 Oversight Systems Report on Corporate Fraud, www.oversightsystems.com.

6

Fraud risk management programs, also known as anti-fraud programs, can take many forms, as noted in Section 1 (Fraud Risk Governance)

under the Fraud Risk Management Program heading.

7

who participate in committing fraud. Organizations should respond to such expectations. Effective governance

processes are the foundation of fraud risk management. Lack of effective corporate governance seriously

undermines any fraud risk management program. The organization’s overall tone at the top sets the standard

regarding its tolerance of fraud.

The board of directors should ensure that its own governance practices set the tone for fraud risk management

and that management implements policies that encourage ethical behavior, including processes for employees,

customers, vendors, and other third parties to report instances where those standards are not met. The board

should also monitor the organization’s fraud risk management effectiveness, which should be a regular item on its

agenda. To this end, the board should appoint one executive-level member of management to be responsible for

coordinating fraud risk management and reporting to the board on the topic.

Most organizations have some form of written policies and procedures to manage fraud risks. However, few have

developed a concise summary of these activities and documents to help them communicate and evaluate their

processes. We refer to the aggregate of these as the fraud risk management program, even if the organization has

not formally designated it as such.

While each organization needs to consider its size and complexity when determining what type of

formal documentation is most appropriate, the following elements should be found within a fraud risk

management program:

• Rolesandresponsibilities.

• Commitment.

• Fraudawareness.

• Afrmationprocess.

• Conictdisclosure.

• Fraudriskassessment.

• Reportingproceduresandwhistleblowerprotection.

• Investigationprocess.

• Correctiveaction.

• Qualityassurance.

• Continuousmonitoring.

Fraud Risk Assessment

To protect itself and its stakeholders effectively and efficiently from fraud, an organization should understand

fraud risk and the specific risks that directly or indirectly apply to the organization. A structured fraud risk

assessment, tailored to the organization’s size, complexity, industry, and goals, should be performed and updated

periodically. The assessment may be integrated with an overall organizational risk assessment or performed

as a stand-alone exercise, but should, at a minimum, include risk identification, risk likelihood and significance

assessment, and risk response.

8

Fraud risk identification may include gathering external information from regulatory bodies (e.g., securities

commissions), industry sources (e.g., law societies), key guidance setting groups (e.g., Cadbury, King Report

7

, and The

Committee of Sponsoring Organizations of the Treadway Commission (COSO)), and professional organizations (e.g.,

The Institute of Internal Auditors (IIA), the American Institute of Certified Public Accountants (AICPA), the Association

of Certified Fraud Examiners (ACFE), the Canadian Institute of Chartered Accountants (CICA), The CICA Alliance for

Excellence in Investigative and Forensic Accounting, The Association of Certified Chartered Accountants (ACCA),

and the International Federation of Accountants (IFAC), plus others noted in Appendix A of this document). Internal

sources for identifying fraud risks should include interviews and brainstorming with personnel representing a broad

spectrum of activities within the organization, review of whistleblower complaints, and analytical procedures.

An effective fraud risk identification process includes an assessment of the incentives, pressures, and opportunities

to commit fraud. Employee incentive programs and the metrics on which they are based can provide a map to where

fraud is most likely to occur. Fraud risk assessment should consider the potential override of controls by management

as well as areas where controls are weak or there is a lack of segregation of duties.

The speed, functionality, and accessibility that created the enormous benefits of the information age have also

increased an organization’s exposure to fraud. Therefore, any fraud risk assessment should consider access and

override of system controls as well as internal and external threats to data integrity, system security, and theft of

financial and sensitive business information.

Assessing the likelihood and significance of each potential fraud risk is a subjective process that should consider not

only monetary significance, but also significance to an organization’s financial reporting, operations, and reputation,

as well as legal and regulatory compliance requirements. An initial assessment of fraud risk should consider the

inherent risk

8

of a particular fraud in the absence of any known controls that may address the risk.

Individual organizations will have different risk tolerances. Fraud risks can be addressed by establishing practices

and controls to mitigate the risk, accepting the risk — but monitoring actual exposure — or designing ongoing or

specific fraud evaluation procedures to deal with individual fraud risks. An organization should strive for a structured

approach versus a haphazard approach. The benefit an implemented fraud risk management program provides

should exceed its cost. Management and board members should ensure the organization has the appropriate control

mix in place, recognizing their oversight duties and responsibilities in terms of the organization’s sustainability

and their role as fiduciaries to stakeholders, depending on organizational form. Management is responsible for

developing and executing mitigating controls to address fraud risks while ensuring controls are executed efficiently

by competent and objective individuals.

Fraud Prevention and Detection

Fraud prevention and detection are related, but are not the same concepts. Prevention encompasses policies,

procedures, training, and communication that stop fraud from occurring, whereas, detection focuses on activities

and techniques that promptly recognize timely whether fraud has occurred or is occurring.

7

The Cadbury Report refers to

The Report of the Committee on the Financial Aspects of Corporate Governance,

issued by the United

Kingdom on Dec. 10, 1992 and the King Report refers to the

King Report on Corporate Governance for South Africa,

issued in 1994.

8

Inherent risk is the risk before considering any internal controls in place to mitigate such risk.

9

While prevention techniques do not ensure fraud will not be committed, they are the first line of defense in

minimizing fraud risk. One key to prevention is promoting from the board down throughout the organization an

awareness of the fraud risk management program, including the types of fraud that may occur.

Meanwhile, one of the strongest fraud deterrents is the awareness that effective detective controls are in place.

Combined with preventive controls, detective controls enhance the effectiveness of a fraud risk management

program by demonstrating that preventive controls are working as intended and by identifying fraud if it does

occur. Although detective controls may provide evidence that fraud has occurred or is occurring, they are not

intended to prevent fraud.

Every organization is susceptible to fraud, but not all fraud can be prevented, nor is it cost-effective to try. An

organization may determine it is more cost-effective to design its controls to detect, rather than prevent, certain

fraud schemes. It is important that organizations consider both fraud prevention and fraud detection.

Investigation and Corrective Action

No system of internal control can provide absolute assurance against fraud. As a result, the board should ensure

the organization develops a system for prompt, competent, and confidential review, investigation, and resolution of

instances of noncompliance and allegations involving potential fraud. The board should also define its own role in

the investigation process. An organization can improve its chances of loss recovery, while minimizing exposure to

litigation and damage to reputation, by establishing and preplanning investigation and corrective action processes.

The board and the organization should establish a process to evaluate allegations. Individuals assigned to

investigations should have the necessary authority and skills to evaluate the allegation and determine the

appropriate course of action. The process should include a tracking or case management system where all

allegations of fraud are logged. Clearly, the board should be actively involved with respect to allegations

involving senior management.

If further investigation is deemed appropriate as the next course of action, the board should ensure that the

organization has an appropriate and effective process to investigate cases and maintain confidentiality. A consistent

process for conducting investigations can help the organization mitigate losses and manage risk associated with the

investigation. In accordance with policies approved by the board, the investigation team should report its findings to

the appropriate party, such as senior management, directors, legal counsel, and oversight bodies. Public disclosure

may also need to be made to law enforcement, regulatory bodies, investors, shareholders, the media, or others.

If certain actions are required before the investigation is complete to preserve evidence, maintain confidence,

or mitigate losses, those responsible for such decisions should ensure there is sufficient basis for those actions.

When access to computerized information is required, specialists trained in computer file preservation should be

used. Actions taken should be appropriate under the circumstances, applied consistently to all levels of employees

(including senior management), and taken only after consultation with human resources (HR) and individuals

responsible for such decisions. Consulting legal counsel is also strongly recommended before undertaking an

investigation and is critical before taking disciplinary, civil, or criminal action. As a matter of good governance,

management and the board should ensure that the foregoing measures are in place.

10

Thus, to properly address fraud risk within the organization, principles described in the following sections of this

paper are needed to make sure:

• Suitablefraudriskmanagementoversightandexpectationsexist(governance)—Principle1.

• Fraudexposuresareidentiedandevaluated(riskassessment)—Principle2.

• Appropriateprocessesandproceduresareinplacetomanagetheseexposures(preventionanddetection)

— Principles 3 & 4.

• Fraudallegationsareaddressed,andappropriatecorrectiveactionistakeninatimelymanner(investigation

and corrective action) — Principle 5.

9

section 1: fRaud Risk goVeRnance

Principle 1: As part of an organization’s governance structure, a fraud risk management program should

be in place, including a written policy (or policies) to convey the expectations of the board of directors

and senior management regarding managing fraud risk.

Corporate governance

has been defined in many ways, including “The system by which companies are directed

and controlled,”

10

and “The process by which corporations are made responsive to the rights and wishes of

stakeholders.”

11

Corporate governance is also the manner in which management and those charged with oversight

accountability meet their obligations and fiduciary responsibilities to stakeholders.

Business stakeholders (e.g., shareholders, employees, customers, vendors, governmental entities, community

organizations, and media) have raised the awareness and expectation of corporate behavior and corporate

governance practices. Some organizations have developed corporate cultures that encompass strong board

governance practices, including:

• Boardownershipofagendasandinformationow.

• Accesstomultiplelayersofmanagementandeffectivecontrolofawhistleblowerhotline.

• Independentnominationprocesses.

• Effectiveseniormanagementteam(includingchiefexecutiveofcer(CEO),chiefnancialofcer,andchief

operating officer) evaluations, performance management, compensation, and succession planning.

• Acodeofconductspecicforseniormanagement,inadditiontotheorganization’scodeofconduct.

• Strongemphasisontheboard’sownindependenteffectivenessandprocessthroughboardevaluations,

executive sessions, and active participation in oversight of strategic and risk mitigation efforts.

These corporate cultures also include board assurance of business ethics considerations in hiring, evaluation,

promotion, and remuneration policies for employees as well as ethics considerations in all aspects of their

relationships with customers, vendors, and other business stakeholders. Effective boards and organizations will also

9

The Open Compliance and Ethics Group (OCEG) Foundation principles displayed in Appendix F of this document also provide guidance on

underlying principles of good governance relative to fraud risk management.

10

Sir Adrian Cadbury, The Committee on the Financial Aspects of Corporate Governance.

11

Ada Demb and F. Friedrich Neubauer,

The Corporate Board: Confronting the Paradoxes.

11

address issues of ethics and the impact of ethical behavior on business strategy, operations, and long-term survival.

The level of board and corporate commitment to these areas varies widely and directly affects the fraud risk profile

of an organization.

Effective business ethics programs can serve as the foundation for preventing, detecting, and deterring fraudulent

and criminal acts. An organization’s ethical treatment of employees, customers, vendors, and other partners will

inuencethosereceivingsuchtreatment.Theseethicsprogramscreateanenvironmentwheremakingtheright

decision is implicit.

The laws of most countries prohibit theft, corruption, and financial statement fraud. Government regulations

worldwide have increased criminal penalties that can be levied against companies and individuals who participate

in fraud schemes at the corporate level, and civil settlements brought by shareholders of public companies or

lenders have rocketed to record amounts

12

. Market capitalizations of public companies drop dramatically at any

hint of financial scandal, and likewise, customers punish those firms whose reputations are sullied by indications of

harmful behavior. Therefore, it should be clear that organizations need to respond to such expectations, and that the

board and senior management will be held accountable for fraud. In many organizations this is managed as part of

corporate governance through entity-level controls, including a fraud risk management program

13

.

ROLES AND RESPONSIBILITIES

To help ensure an organization’s fraud risk management program effective, it is important to understand the roles

and responsibilities that personnel at all levels of the organization have with respect to fraud risk management.

Policies, job descriptions, charters, and/or delegations of authority should define roles and responsibilities related

to fraud risk management. In particular, the documentation should articulate who is responsible for the governance

oversight of fraud control (i.e., the role and responsibility of the board of directors and/or designated committee of

theboard).Documentationshouldalsoreectmanagement’sresponsibilityforthedesignandimplementationof

the fraud risk strategy, and how different segments of the organization support fraud risk management. Fraud risk

management will often be supported by risk management, compliance, general counsel, the ethics office, security,

information technology (IT), and internal auditing, or their equivalents. The board of directors, audit committee,

management, staff, and internal auditing all have key roles in an organization’s fraud risk management program.

Board of Directors

To set the appropriate tone at the top, the board of directors first should ensure that the board itself is governed

properly. This encompasses all aspects of board governance, including independent-minded board members

who exercise control over board information, agenda, and access to management and outside advisers, and

who independently carry out the responsibilities of the nominating/governance, compensation, audit, and other

committees.

12

In the United States and Europe, regulators assessed fines and penalties in excess of US $1 billion for fraudulent and/or criminal behavior

during 2007. See www.sec.gov.

13

ALARM (The National Forum for Risk Management in the Public Sector (UK)) lists a fraud risk management program as one of five

essential governance strategies to manage fraud risk. Other strategies include a zero-tolerance culture, a sound counter-fraud and corruption

framework, strong systems of internal control, and close working relationships with partners regarding fraud risk management activities.

12

The board also has the responsibility to ensure that management designs effective fraud risk management

documentation to encourage ethical behavior and to empower employees, customers, and vendors to insist those

standards are met every day. The board should:

• Understandfraudrisks.

• Maintainoversightofthefraudriskassessmentbyensuringthatfraudriskhasbeenconsideredaspart

of the organization’s risk assessment and strategic plans. This responsibility should be addressed under a

periodic agenda item at board meetings when general risks to the organization are considered.

• Monitormanagement’sreportsonfraudrisks,policies,andcontrolactivities,whichincludeobtaining

assurance that the controls are effective. The board also should establish mechanisms to ensure it is

receiving accurate and timely information from management, employees, internal and external auditors,

and other stakeholders regarding potential fraud occurrences.

• Overseetheinternalcontrolsestablishedbymanagement.

• SettheappropriatetoneatthetopthroughtheCEOjobdescription,hiring,evaluation,andsuccession-

planning processes.

• Havetheabilitytoretainandpayoutsideexpertswhereneeded.

• Provideexternalauditorswithevidenceregardingtheboard’sactiveinvolvementandconcernaboutfraud

risk management.

The board may choose to delegate oversight of some or all of such responsibilities to a committee of the board.

These responsibilities should be documented in the board and applicable committee charters. The board should

ensure it has sufficient resources of its own and approve sufficient resources in the budget and long-range plans to

enable the organization to achieve its fraud risk management objectives.

Audit Committee (or similar oversight body)

14

The audit committee should be composed of independent board members and should have at least one financial

expert, preferably with an accounting background. The committee should meet frequently enough, for long

enough periods, and with sufficient preparation to adequately assess and respond to the risk of fraud, especially

management fraud, because such fraud typically involves override of the organization’s internal controls. It is key

that the audit committee receive regular reports on the status of reported or alleged fraud.

An audit committee of the board that is committed to a proactive approach to fraud risk management maintains

an active role in the oversight of the organization’s assessment of fraud risks and uses internal auditors, or

other designated personnel, to monitor fraud risks. Such a committee also provides the external auditors with

evidence that the committee is committed to fraud risk management and will discuss with the external auditor the

auditors’ planned approach to fraud detection as part of the financial statement audit.

Management Override of

Internal Controls: The Achilles’ Heel of Fraud Prevention

, an AICPA publication, provides valuable information for

audit committees that take this approach.

14

This heading discusses more detailed governance roles, using the audit committee as an illustration. Some organizations may require

this level of responsibility by the full board, or the board may delegate it to a risk management committee, strategic planning committee,

etc. Accounting standards and securities regulations in each country provide more detailed guidance as to what is a best practice or legal

requirement in their jurisdictions.

13

At each audit committee meeting, the committee should meet separately from management with appropriate

individuals, such as the chief internal audit executive and senior financial person. The audit committee should

understand how internal and external audit strategies address fraud risk. The audit committee should not only focus

on what the auditors are doing to detect fraud, but more importantly on what management is doing to prevent

fraud, where possible.

The audit committee should be aware that the organization’s external auditors have a responsibility to plan and

perform the audit of the organization’s financial statements to obtain reasonable assurance

15

about whether the

financial statements are free of material misstatement, whether caused by error or fraud. The extent and limitations

of an external audit are generally governed by the applicable audit standards in place.

16

The audit committee

should insist on openness and honesty with the external auditors. The external auditors should also have

commitment and cooperation from the audit committee. This includes open and candid dialogue between audit

committee members and the external auditors regarding the audit committee’s knowledge of any fraud or suspected

fraud affecting the organization as well as how the audit committee exercises oversight activities with respect to

the organization’s assessment of the risks of fraud and the programs and controls the organization has established

to mitigate these risks.

The audit committee should also seek the advice of legal counsel whenever dealing with issues of allegations

of fraud. Fraud allegations should be taken seriously since there may be a legal obligation to investigate

and/or report them.

In addition, since reputation risk resulting from fraudulent behavior often has a severe impact on shareholder

value, the audit committee should provide specific consideration and oversight of this exposure when reviewing

the work of management and internal auditors, and ask them to be alert for and report such exposure as they

carry out their duties.

Management

Management has overall responsibility for the design and implementation of a fraud risk management

program, including:

• Settingthetoneatthetopfortherestoftheorganization.Asmentioned,anorganization’scultureplaysan

important role in preventing, detecting, and deterring fraud. Management needs to create a culture through

words and actions where it is clear that fraud is not tolerated, that any such behavior is dealt with swiftly

and decisively, and that whistleblowers will not suffer retribution.

15

The inherent limitations of an external audit regarding matters related to fraud are described in applicable audit standards. The standards

acknowledge that owing to the inherent limitations of an external audit, there is an unavoidable risk that some material misstatements of the

financial statements — particularly those resulting from fraud — will not be detected, even though the external auditor has properly planned

and performed in accordance with generally accepted standards.

16

Internationally, refer to International Standards on Auditing (ISA) No. 240,

The Auditor’s Responsibility to Consider Fraud in an Audit of

Financial Statements

. In the United States, refer to Statement of Auditing Standards (SAS) No. 99 (AU sec 316), Consideration of Fraud in

a Financial Statement Audit; SAS No. 1 (AU sec 1), Codification of Auditing Standards and Procedures; PCAOB AS5; and Section 10A of the

Securities Exchange Act of 1934. In Canada, refer to

CICA Handbook

–

Assurance

Section 5135, The Auditor’s Responsibility to Consider

Fraud. One may also refer to the International Organisation of Supreme Audit Institutions (INTOSAI), the International Federation

of Accountants (IFAC) International Auditing and Assurance Standards Board (IAASB), and the Association of Chartered Certified

Accountants (ACCA).

14

• Implementingadequateinternalcontrols—includingdocumentingfraudriskmanagementpoliciesand

procedures and evaluating their effectiveness — aligned with the organization’s fraud risk assessment.

To conduct a reasonable evaluation, it is necessary to compile information from various areas of the

organization as part of the fraud risk management program.

• Reportingtotheboardonwhatactionshavebeentakentomanagefraudrisksandregularlyreportingon

the effectiveness of the fraud risk management program. This includes reporting any remedial steps that are

needed, as well as reporting actual frauds.

Whenever the external auditor has determined that there is evidence that fraud may exist, the external auditor’s

professional standards require that the matter should be brought to the attention of an appropriate level of

management. The external auditor should report fraud involving senior management directly to those charged with

governance (e.g. the audit committee).

In many organizations, one executive-level member of management is appointed to be responsible for fraud risk

management and to report to the board periodically. This executive, a chief ethics officer for instance, is responsible

for entity-level controls that establish the tone at the top and corporate culture. These expectations are often

documented in the organization’s values or principles, code of conduct, and related policies; demonstrated through

executive communications and behaviors; and included in training programs. The person appointed should be

familiar with the organization’s fraud risks and process-level controls, and is often responsible for the design and

implementation of the processes used to ensure compliance, reporting, and investigation of alleged violations.

Staff

Strong controls against fraud are the responsibility of everyone in the organization. The importance of internal

controls in fraud risk management is not a new concept. In 1992, after more than three years of collaboration

between corporate leaders, legislators, regulators, auditors, academics, and many others, COSO presented a common

definition of internal controls and provided a framework against which organizations could assess and improve their

internal control systems. COSO identified five components in its landmark

Internal Control–Integrated Framework

—

control environment, risk assessment, control activities, information and communication, and monitoring — that

may serve as the premise for the design of controls. The elements are deeply intertwined and overlapping in their

nature, providing a natural interactive process to promote the type of environment in which fraud simply will not be

tolerated at any level.

17

All levels of staff, including management, should:

• Haveabasicunderstandingoffraudandbeawareoftheredags.

• Understandtheirroleswithintheinternalcontrolframework.Staffmembersshouldunderstandhowtheir

job procedures are designed to manage fraud risks and when noncompliance may create an opportunity for

fraud to occur or go undetected.

• Readandunderstandpoliciesandprocedures(e.g.thefraudpolicy,codeofconduct,andwhistleblower

policy), as well as other operational policies and procedures, such as procurement manuals.

17

Appendix I suggests control activities aligned with each COSO component.

15

• Asrequired,participateintheprocessofcreatingastrongcontrolenvironmentanddesigningand

implementing fraud control activities, as well as participate in monitoring activities.

• Reportsuspicionsorincidencesoffraud.

• Cooperateininvestigations.

Internal Auditing

The IIA’s Definition of Internal Auditing states, “Internal auditing is an independent, objective assurance and

consulting activity designed to add value and improve an organization’s operations. It helps an organization

accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness

of risk management, control, and governance processes.” In relation to fraud, this means that internal auditing

provides assurance to the board and to management that the controls they have in place are appropriate given the

organization’s risk appetite.

Internal auditing should provide objective assurance to the board and management that fraud controls are

sufficient for identified fraud risks and ensure that the controls are functioning effectively. Internal auditors may

review the comprehensiveness and adequacy of the risks identified by management — especially with regard to

management override risks

18

.

Internal auditors should consider the organization’s assessment of fraud risk when developing their annual audit

plan and review management’s fraud management capabilities periodically. They should interview and communicate

regularly with those conducting the organization’s risk assessments, as well as others in key positions throughout

the organization, to help them ensure that all fraud risks have been considered appropriately. When performing

engagements, internal auditors should spend adequate time and attention to evaluating the design and operation

of internal controls related to fraud risk management. They should exercise professional skepticism when reviewing

activities and be on guard for the signs of fraud. Potential frauds uncovered during an engagement should be

treated in accordance with a well-defined response plan consistent with professional and legal standards. Internal

auditing should also take an active role in support of the organization’s ethical culture.

19

The importance an organization attaches to its internal audit function is an indication of the organization’s

commitment to effective internal control. The internal audit charter, which is approved by the board or designated

committee, should include internal auditing’s roles and responsibilities related to fraud. Specific internal audit

roles in relation to fraud risk management could include initial or full investigation of suspected fraud, root cause

analysis and control improvement recommendations, monitoring of a reporting/whistleblower hotline, and providing

ethics training sessions.

20

If assigned such duties, internal auditing has a responsibility to obtain sufficient skills

and competencies, such as knowledge of fraud schemes, investigation techniques, and laws. Effective internal audit

functions are adequately funded, staffed, and trained, with appropriate specialized skills given the nature, size,

and complexity of the organization and its operating environment. Internal auditing should be independent (have

independent authority and reporting relationships), have adequate access to the audit committee, and adhere to

professional standards.

18

Refer to the AICPA’s

Management Override of Internal Controls: The Achilles’ Heel of Fraud Prevention

publication.

19

Refer to IIA Practice Advisory 2130-1: Role of the Internal Audit Activity and Internal Auditor in the Ethical Culture of an Organization.

20

For additional information, refer to IIA Practice Advisories 1210-A2-1: Auditor’s Responsibilities Relating to Fraud Risk Assessment,

Prevention, and Detection; and 1210-A2-2: Auditor’s Responsibilities Relating to Fraud Investigation, Reporting, Resolution, and

Communication; as well as the IIA–UK and Ireland Fraud Position Statement.

16

FRAUD RISK MANAGEMENT PROGRAM COMPONENTS

Most organizations have written policies and procedures to manage fraud risks, such as codes of conduct, expense

account procedures, and incident investigation standards. They usually have some activities that management

has implemented to assess risks, ensure compliance, identify and investigate violations, measure and report the

organization’s performance to appropriate stakeholders, and communicate expectations. However, few have

developed a concise summary of these documents and activities to help them communicate and evaluate their

processes. We refer to the aggregate of these as the fraud risk management program (“program”), even if the

organization has not formally designated it as such.

It is management’s prerogative, with oversight from the board, to determine the type and format of documentation

it wishes to adopt for its program. Suggested formats include:

• Asinglecomprehensiveandcompletedocumentthataddressesallaspectsoffraudriskmanagement(i.e.,a

fraud control policy

21

).

• Abriefstrategyoutlineemphasizingtheattributesoffraudcontrol,butleavingthedesignofspecic

policies and procedures to those responsible for business functions within the organization.

• Anoutline,withinacontrolframework,referencingrelevantpolicies,procedures,plans,programs,reports,

and responsible positions, developed by the organization’s head office, divisions, or subsidiaries.

22

While each organization needs to consider its size and complexity when determining what type of formal

documentation is most appropriate, the following elements should be found within a fraud risk

management program:

Commitment

The board and senior management should communicate their commitment to fraud risk management. One method

would be to embed this commitment in the organization’s values or principles and code of conduct. Another method

is issuing a short document (e.g., letter) made available to all employees, vendors, and customers. This summary

document should stress the importance of fraud risk mitigation, acknowledge the organization’s vulnerability to

fraud, and establish the responsibility for each person within the organization to support fraud risk management.

The letter should be endorsed or authored by a senior executive or board member, provided to employees as part

of their orientation process, and reissued periodically. The letter could serve as the foundation for, and may be the

executive summary of, a fraud control policy.

Fraud Awareness

An ongoing awareness program is a key enabler to convey fraud risk management expectations, as well as

an effective preventive control. Awareness of fraud and misconduct schemes is developed through periodic

21

For examples of fraud control policies, see Appendices B and C.

22

Some organizations centralize fraud risk management information under the chief ethics officer or within a framework used by internal

auditing or the chief financial officer. Others may have this information spread out across the organization — for example, investigation

standards and files in legal, hiring and training information in human resources, hotline information in internal auditing, risk assessment in the

enterprise risk management group — and will need to compile it to do an effective evaluation and to enable concise reporting to the board.

17

assessment, training, and frequent communication. An organization’s fraud risk management program will assist

the organization with fraud awareness. Documentation to support fraud awareness should define and describe

fraud and fraud risks.

23

It should also provide examples of the types of fraud that could occur and identify potential

perpetrators of fraud.

When designing fraud awareness programs, management should consider who should attend, frequency and length,

cultural sensitivities, guidance on how to solve ethical dilemmas, and delivery methods. Management should also

consider the training needs of the board or board committee members.

Affirmation Process

An organization should determine whether there are any legal issues involved with having an affirmation process,

which is the requirement for directors, employees, and contractors to acknowledge they have read, understood,

and complied with the code of conduct, a fraud control policy, and other such documentation to support the

organization’s fraud risk management program. There is a fraud risk to the organization of not having an affirmation

process. This should be acknowledged and accepted at or above a senior management level.

The affirmation process may be handled electronically or via manual signature. Organizations implementing best

practice often also require personnel to acknowledge that they are not aware of anyone who is in violation of the

policies. Management should establish consequences for refusal to sign-off and apply such action consistently.

Some organizations include terms in their contracts that require service providers to agree to abide by the

organization’s code of conduct, a global standard, or the like, which may also prevent fraud. Others require senior

management to sign a code of conduct specific to employees at higher levels of the organization and require service

providers to sign separate agreements on specific topics, such as confidentiality or use of company technologies.

Conflict Disclosure

A process should be implemented for directors, employees, and contractors to internally self-disclose potential or

actualconictsofinterest.Onceconictsareinternallydisclosed,thereareseveraldecisionpaths:

• Managementmayassertthatthereisinfact,aconictandrequiretheindividualtoterminatetheactivity

or leave the organization.

• Managementmayaccepttheinternaldisclosureanddeterminethatthereisnoconictofinterestinthe

situation described.

• Managementmaydecidethatthereisapotentialforconictofinterestandmayimposecertainconstraints

ontheindividualtomanagetheidentiedriskandtoensurethereisnoopportunityforaconicttoarise.

Thedisclosureofapotentialconictofinterestandmanagement’sdecision

24

should be documented and disclosed

to legal counsel. Any constraints placed on the situation need to be monitored. For example, a buyer who has

23

Refer to Section 2 (Fraud Risk Assessment) for a more detailed discussion of fraud risks and risk assessments.

24

ConictofinterestpolicyprovisionwaiversforexecutiveofcersofNewYorkStockExchange-listedcompaniescanonlybegrantedbythe

board of directors or a committee thereof, and such waivers have to be disclosed to shareholders promptly. Waivers for executive officers of

NASDAQ-listedcompaniescanonlybegrantedbyindependentboardmembers,andsuchwaiversneedtobedisclosed.

18

recently been hired in the purchasing department is responsible for all purchases in Division A. His brother has a

localhardwarestorethatsuppliesproducttoDivisionA.Thebuyerdisclosesthepotentialconictofinterestand

is told that transactions with the hardware store are permitted, as long as the department supervisor monitors a

monthly report of all activity with the hardware store to ensure the activity and price levels are reasonable and

competitive. When the buyer is promoted or transferred, the constraints may be removed or altered.

Other disclosure processes may also exist, such as insider trading disclosures. Those processes that mitigate

potential fraud risk should be linked to the fraud risk management program. Organizations should evaluate the

legal requirements and/or business benefits of disclosing their code of conduct, fraud control policy, or related

statements to the public.

Fraud Risk Assessment

25

The foundations of an effective fraud risk management program are rooted in a risk assessment, overseen by the

board, which identifies where fraud may occur within the organization. A fraud risk assessment should be performed

on a systematic and recurring basis, involve appropriate personnel, consider relevant fraud schemes and scenarios,

and mapping those fraud schemes and scenarios to mitigating controls. The existence of a fraud risk assessment and

the fact that management is articulating its existence may even deter would-be fraud perpetrators.

The system of internal controls in an organization is designed to address inherent business risks. The business risks

are identified in the enterprise risk assessment protocol, and the controls associated with each risk are noted.

COSO’s

Enterprise Risk Management–Integrated Framework

describes the essential ERM components, principles, and

concepts for all organizations, regardless of size.

Reporting Procedures and Whistleblower Protection

Documentation should not only articulate the organization’s zero tolerance

26

for fraud, it should also establish the

expectation that suspected fraud must be reported immediately and provide the means to do so. The channels to

report suspected fraud issues should be clearly defined and communicated. These may be the same or different from

channels for reporting other code of conduct violations.

Considering that people commit fraud and that people are an organization’s best asset in preventing, detecting, and

deterring fraud, an organization should consider promoting available fraud reporting resources that individuals may

access, such as a fraud or ethics page on the organization’s Web site, an ombudsman, or a whistleblower hotline.

To encourage timely reporting of suspected issues, the organization should communicate the protections afforded

to the individual reporting the issue — often referred to as whistleblower protection. In some countries, securities

regulations require organizations to have whistleblower protection.

25

For more information on fraud risk assessments, refer to Section 2: Fraud Risk Assessment.

26

ALARM (The National Forum for Risk Management in the Public Sector (UK)) lists a culture of zero tolerance as one of five essential

governance strategies to manage fraud risk. Other strategies include an embedded strategic approach to risk management, a sound counter-

fraud and corruption framework, strong systems of internal control, and close working relationships with partners regarding fraud risk

management activities.

19

Investigation Process

27

Organizations should require that an investigation process be in place. Once an issue is suspected and reported, an

investigation process will follow. The board and management should have a documented protocol for this process,

including consideration of who should conduct the investigation — whether it be internal personnel or hiring

experts in this field — rules of evidence, chains of custody, reporting mechanisms to those charged with governance,

regulatory requirements, and legal actions. Organizations should also consider whether to require all employees, as a

condition of employment, to cooperate fully with an investigation into any alleged or suspected fraud.

Corrective Action

Asadeterrent,policiesshouldreecttheconsequencesandprocessesforthosewhocommitorcondonefraudulent

activity. These consequences may include termination of employment or of a contract and reporting to legal and

regulatory authorities. The organization should articulate that it has the right to institute civil or criminal action

against anyone who commits fraud.

Whenfrauddoesoccurwithintheorganization,policiesshouldreecttheneedtoconductapostmortemtoidentify

the control weakness that contributed to the fraudulent act. The postmortem should lead to a remediation of any

identified control deficiencies. Internal auditors are important resources for this activity.

Process Evaluation and Improvement (Quality Assurance)

Documentation should describe whether, and/or how, management will periodically evaluate the effectiveness of the

fraud risk management program and monitor changes. It may include the need for measurements and analysis of

statistics, benchmarks, resources, and survey results. The results of this evaluation should be reported to appropriate

oversight groups and be used by management to improve the fraud risk management program.

Continuous Monitoring

The fraud risk management program, including related documents, should be revised and reviewed based on the

changing needs of the organization, recognizing that documentation is static, while organizations are dynamic.

Fraudriskmanagementprogramdocumentationshouldbeupdatedonanongoingbasistoreectcurrentconditions

andtoreecttheorganization’scontinuingcommitmenttothefraudriskmanagementprogram.

section 2: fRaud Risk assessMent

Principle 2: Fraud risk exposure should be assessed periodically by the organization to identify specific

potential schemes and events that the organization needs to mitigate.

Regulators, professional standard-setters, and law enforcement authorities have emphasized the crucial role

risk assessment plays in developing and maintaining effective fraud risk management programs and controls.

28

27

Refer to Section 5 (Investigation and Corrective Action) for more details on the investigation process and corrective action.

28

Refer to June 2007 SEC Guidance to Management; PCAOB AS5; IIA Practice Advisory 1210-A2-1: Auditor’s Responsibilities Relating to

Fraud Risk Assessment, Prevention, and Detection;

COSO for Small Business:

Principle 10–Fraud Risk; SAS No. 99, Consideration of Fraud in A

Financial Statement Audit; and ISA No. 240.

20

Organizations can identify and assess fraud risks in conjunction with an overall enterprise risk assessment or

on a stand-alone basis.

Guidance for conducting a fraud risk assessment is provided in this section of the guide. Organizations can tailor this

approach to meet their individual needs, complexities, and goals.

The foundation of an effective fraud risk management program should be seen as a component of a larger

enterprise risk management (ERM) effort and is rooted in a risk assessment that identifies where fraud may occur

and who the perpetrators might be. To this end, control activities should always consider both the fraud scheme and

the individuals within and outside the organization who could be the perpetrators of each scheme. If the scheme

is collusive

29

, preventive controls should be augmented by detective controls, as collusion negates the control

effectiveness of segregation of duties.

Fraud, by definition, entails intentional misconduct, designed to evade detection. As such, the fraud risk assessment

team should engage in strategic reasoning to anticipate the behavior of a potential fraud perpetrator.

30

Strategic

reasoning, which is also important in designing fraud detection procedures that a perpetrator may not expect,

requires a skeptical mindset and involves asking questions such as:

• Howmightafraudperpetratorexploitweaknessesinthesystemofcontrols?

• Howcouldaperpetratoroverrideorcircumventcontrols?

• Whatcouldaperpetratordotoconcealthefraud?

With this in mind, a fraud risk assessment generally includes three key elements:

•

Identify inherent fraud risk

31

— Gather information to obtain the population of fraud risks that could

apply to the organization. Included in this process is the explicit consideration of all types of fraud schemes

and scenarios; incentives, pressures, and opportunities to commit fraud; and IT fraud risks

specific to the organization.

•

Assess likelihood and significance of inherent fraud risk

— Assess the relative likelihood and potential

significance of identified fraud risks based on historical information, known fraud schemes, and interviews

with staff, including business process owners.

•

Respond to reasonably likely and significant inherent and residual fraud risks

— Decide what the response

should be to address the identified risks and perform a cost-benefit analysis of fraud risks over which the

organization wants to implement controls or specific fraud detection procedures.

29

A collusive scheme is one performed by two or more individuals working together.

30

T. Jeffrey Wilks and M.F. Zimbelman, “Using Game Theory and Strategic Reasoning Concepts to Prevent and Detect Fraud,”

Accounting

Horizons

, Volume 18, No. 3 (September 2004).

31

The initial assessment of fraud risk should consider the inherent risk of particular frauds occurring in the absence of internal controls. After

all relevant fraud risks have been identified, internal controls are mapped to the identified risks. Fraud risks that remain unaddressed by

appropriate controls comprise the population of residual fraud risks.

21

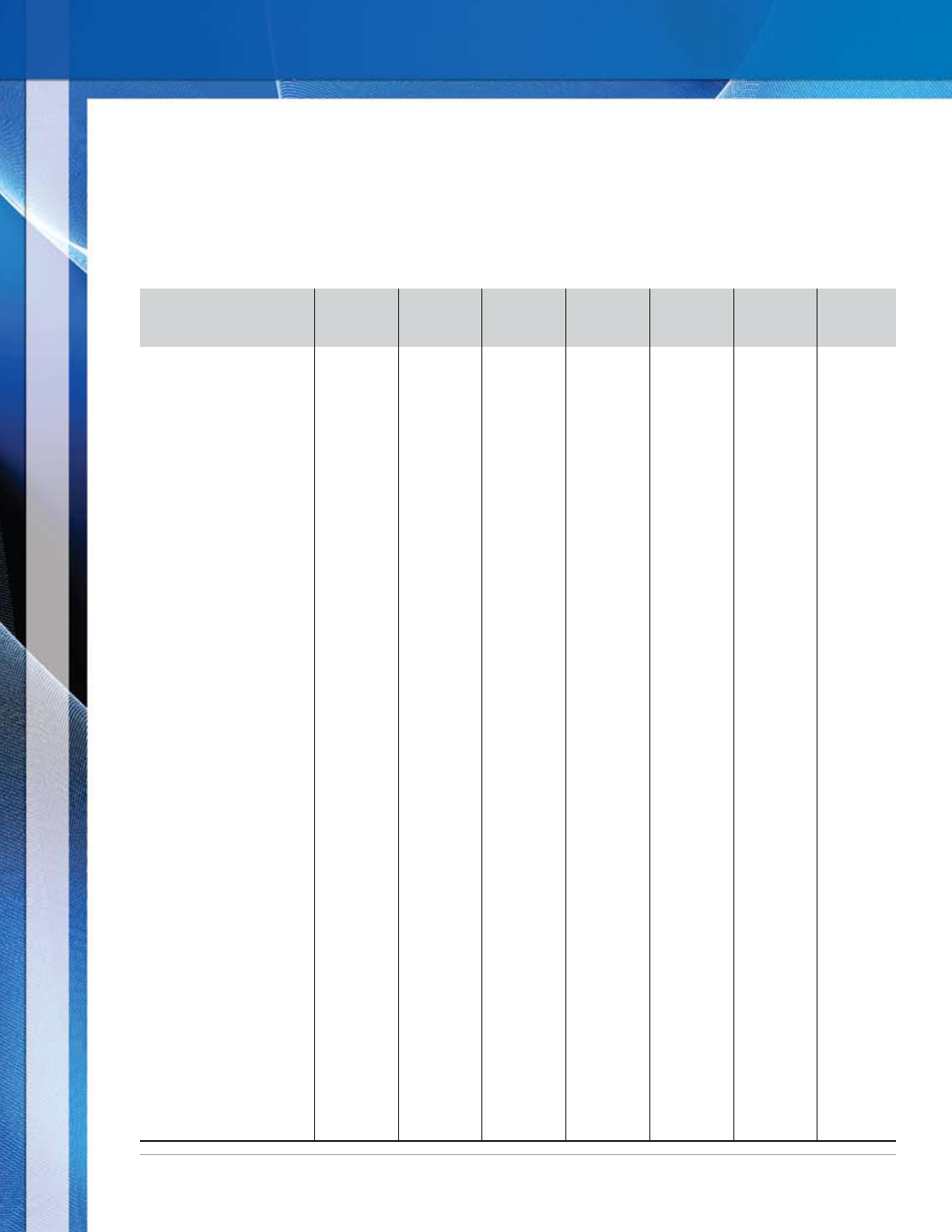

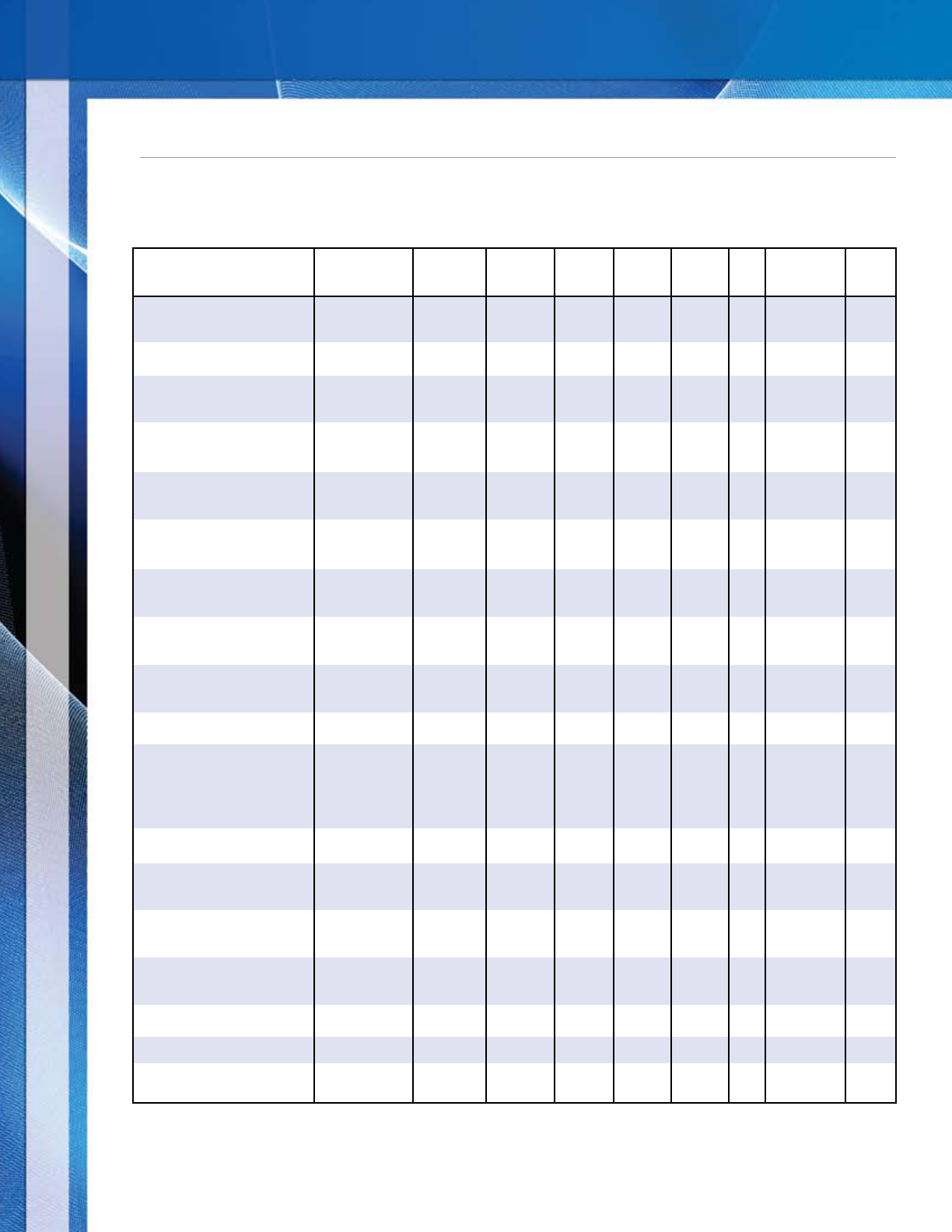

Organizations should apply a framework to document their fraud risk assessment. The framework below illustrates

how the elements of fraud risk identification, assessment, and response are applied in a rational, structured

approach. This example begins with a list of identified fraud risks and schemes, which are then assessed for relative

likelihood and significance of occurrence. Next, the risks and schemes are mapped to the people and/or departments

that may be impacted and to relevant controls, which are evaluated for design effectiveness and tested to validate

operating effectiveness. Lastly, residual risks are identified, and a fraud risk response is developed.

32

Identified

Fraud Risks and Schemes

Financial reporting

Revenue recognition

- Backdating agreements

- Channel stuffing

- Inducing distributors to

accept more product than

necessary

- Holding books open

- Via recording detail

transactions in a sub-ledger

- Via recording top-side

journal entries

- Additional revenue risks

Management estimates

- Self insurance

- Altering underlying detail

claims and estimate data

- Fraudulently changing

underlying assumptions in

estimation of liability

- Allowance for bad debts

- Altering underlying A/R

aging to manipulate

computation

- Fraudulent input from

sales persons or credit

department on credit quality

- Additional estimates

Disclosures

- Footnotes

- Additional disclosures

Misappropriation of assets

Cash/check

- Point of sale

- Accounts receivable application

process

- Master vendor file controls

override

- Additional risks

- Inventory

- Theft by customers

- Theft by employees

- Other assets at risk

Corruption

- Bribery

- Aiding and abetting

Other Risks

Likelihood Significance

People and/or

Department

Existing

Anti-fraud

Controls

Controls

Effectiveness

Assessment

Residual

Risks

Fraud Risk

Response

32

Refer to Appendix D of this document for an example of the use of this framework.

22

THE RISK ASSESSMENT TEAM

A good risk assessment requires input from various sources. Before conducting a risk assessment, management

should identify a risk assessment team. This team should include individuals from throughout the organization

with different knowledge, skills, and perspectives and should include a combination of internal and external

resources such as:

• Accounting/nancepersonnel,whoarefamiliarwiththenancialreportingprocessandinternalcontrols.

• Nonnancialbusinessunitandoperationspersonnel,toleveragetheirknowledgeofday-to-dayoperations,

customer and vendor interactions, and general awareness of issues within the industry.

• Riskmanagementpersonnel,toensurethatthefraudriskassessmentprocessintegrateswiththe

organization’s ERM program.

• Legalandcompliancepersonnel,asthefraudriskassessmentwillidentifyrisksthatgiverisetopotential

criminal, civil, and regulatory liability if the fraud or misconduct were to occur.

• Internalauditpersonnel,whowillbefamiliarwiththeorganization’sinternalcontrolsandmonitoring

functions. In addition, internal auditors will be integral in developing and executing responses to significant

risks that cannot be mitigated practically by preventive and detective controls.

• Ifexpertiseisnotavailableinternally,externalconsultantswithexpertiseinapplicablestandards,keyrisk

indicators, anti-fraud methodology, control activities, and detection procedures.

Management, including senior management, business unit leaders, and significant process owners (e.g., accounting,

sales, procurement, and operations) should participate in the assessment, as they are ultimately accountable for the

effectiveness of the organization’s fraud risk management efforts.

FRAUD RISK IDENTIFICATION

Once assembled, the risk assessment team should go through a brainstorming activity to identify the organization’s

fraud risks. Effective brainstorming involves preparation in advance of the meeting, a leader to set the agenda

and facilitate the session, and openness to ideas regarding potential risks and controls

33

. Brainstorming enables

discussions of the incentives, pressures, and opportunities to commit fraud; risks of management override of

controls; and the population of fraud risks relevant to the organization.

34

Other risks, such as regulatory and legal

misconduct and reputation risk, as well as the impact of IT on fraud risks also should be considered in the fraud risk

identification process.

The organization’s fraud risk identification information should be shared with the board or audit committee and

comments should be solicited. The board also should assess the implications of its own processes with respect to its

contribution to fraud risk, including incentive pressures.

33

Sources of information about good brainstorming practices include (a) Mark S. Beasley and Gregory Jenkins, “A Primer for Brainstorming

Fraud Risks,” Journal of Accountancy, December 2003, and (b) Michael J. Ramos, “Brainstorming Prior to the Audit,” in

Fraud Detection in a

GAAS Audit: Revised Edition

, Chapter 2: “Considering Fraud in a Financial Statement Audit.”

34

Refer to Appendix E: Fraud Risk Exposures of this document for a list of potential fraud risk which could be used in brainstorming.

23

Incentives, Pressures, and Opportunities

Motives for committing fraud are numerous and diverse. One executive may believe that the organization’s business

strategy will ultimately be successful, but interim negative results need to be concealed to give the strategy time.

Another needs just a few more pennies per share of income to qualify for a bonus or to meet analysts’ estimates.

The third executive purposefully understates income to save for a rainy day.

The fraud risk identification process should include an assessment of the incentives, pressures, and opportunities to

commit fraud. Incentive programs should be evaluated — by the board for senior management and by management

for others — as to how they may affect employees’ behavior when conducting business or applying professional

judgment (e.g., estimating bad debt allowances or revenue recognition). Financial incentives and the metrics on

which they are based can provide a map to where fraud is most likely to occur. There may also be nonfinancial

incentives, such as when an employee records a fictitious transaction so he or she does not have to explain an

otherwise unplanned variance. Even maintaining the status quo is sometimes a powerful enough incentive for

personnel to commit fraud.

Also important, and often harder to quantify, are the pressures on individuals to achieve performance or other

targets. Some organizations are transparent, setting specific targets and metrics on which personnel will be

measured.Otherorganizationsaremoreindirectandsubtle,relyingoncorporateculturetoinuencebehavior.

Individuals may not have any incremental monetary incentive to fraudulently adjust a transaction, but there may be

ample pressure — real or perceived — on an employee to act fraudulently.

Meanwhile, opportunities to commit fraud exist throughout organizations and may be reason enough to commit

fraud. These opportunities are greatest in areas with weak internal controls and a lack of segregation of duties.

However, some frauds, especially those committed by management, may be difficult to detect because management

can often override the controls. Such opportunities are why appropriate monitoring of senior management by a

strong board and audit committee, supported by internal auditing, is critical to fraud risk management.

Risk of Management’s Override of Controls

As part of the risk identification process, it is important to consider the potential for management override of

controls established to prevent or detect fraud. Personnel within the organization generally know the controls and

standard operating procedures that are in place to prevent fraud. It is reasonable to assume that individuals who

are intent on committing fraud will use their knowledge of the organization’s controls to do it in a manner that

will conceal their actions. For example, a manager who has the authority to approve new vendors may create and

approve a fictitious vendor and then submit invoices for payment, rather than just submit false invoices for payment.

Hence, it is also important to keep the risk of management’s override of controls in mind when evaluating the

effectiveness of controls; an anti-fraud control is not effective if it can be overridden easily.

Population of Fraud Risks

The fraud risk identification process requires an understanding of the universe of fraud risks and the subset of risks

specific to the organization. This may involve obtaining information from external sources such as industry news;

criminal, civil, and regulatory complaints and settlements; and organizations such as The IIA, AICPA, ACFE, and CICA.

24

This also involves understanding the organization’s business processes and gathering information about potential

fraud from internal sources by interviewing personnel and brainstorming with them, reviewing complaints from the

whistleblower hotline, and performing analytical procedures.

Various taxonomies are available to organize fraud risks. Appendix H displays the Foundation Principles issued by

the Open Compliance and Ethics Group (OCEG) that relate to fraud risk identification. The ACFE, on the other hand,

classifies occupational fraud risks into three general categories: fraudulent statements, misappropriation of assets,

and corruption

35

. Using the ACFE’s categories as a starting point, a more detailed breakout can be developed to

produce an organization-specific fraud risk assessment. For example, potential fraud risks to consider in the ACFE’s

three general categories include:

1) Intentional manipulation of financial statements, which can lead to:

a) Inappropriately reported revenues.

b) Inappropriately reported expenses.

c) Inappropriatelyreectedbalancesheetamounts,includingreserves.

d) Inappropriately improved and/or masked disclosures.

e) Concealing misappropriation of assets.

f) Concealing unauthorized receipts and expenditures.

g) Concealing unauthorized acquisition, disposition, and use of assets.

2) Misappropriation of:

a) Tangible assets by:

i) Employees.

ii) Customers.

iii) Vendors.

iv) Former employees and others outside the organization.

b) Intangible assets.

c) Proprietary business opportunities.

3) Corruption including:

a) Bribery and gratuities to:

i) Companies.

ii) Private individuals.

iii) Public officials.

b) Receipt of bribes, kickbacks, and gratuities.

c) Aiding and abetting fraud by other parties (e.g., customers, vendors).

Fraudulent Financial Reporting

Each of the three categories outlined by the ACFE includes at least one scheme of how the fraud could occur.

For instance, acceleration of revenue recognition can be achieved via numerous schemes, including backdating

agreements, recognizing revenue on product not shipped by period end, or channel stuffing. Some fraudulent

35

The ACFE’s Report to the Nation on Occupational Fraud and Abuse.

25

financial reporting schemes are common across all organizations (e.g., setting aside unsupported reserves for

use in future periods and fraudulent top-side entries); other schemes are more industry-specific (e.g., backdating

agreements at software companies or channel stuffing for organizations that sell via distributors). Each scheme that

could be relevant to the organization should be considered in the assessment.

Organizations can use the framework in Appendix D to identify specific areas of greatest risk and as a foundation

for customizing the assessment process for their specific needs. For example, starting with the revenue recognition

component of fraudulent financial reporting, the assessment should consider the following questions:

• Whatarethemaindriversofrevenueattheorganization?

• Arerevenuesprimarilyfromvolumesalesofrelativelyhomogeneousproducts,oraretheydrivenbya

relativelyfewindividualtransactions?

• Whataretheincentivesandpressurespresentintheorganization?

• Arerevenuesrecordedsystematicallyormanually?

• Arethereanyrevenuerecognitionfraudrisksspecictotheorganization’sindustry?

For significant marketplace disclosures (e.g., loan delinquency percentages) consider the following questions:

• Whatcontrolsareinplacetomonitorinternalgatheringandreportingofthesedisclosures?

• Isthereoversightfromsomeonewhosecompensationisnotdirectlyaffectedbyhisorherperformance?

• Doessomeonemonitortheorganization’sdisclosuresinrelationtootherorganizationsandaskhard

questionsaboutwhethertheorganization’sdisclosuresareadequateorcouldbeimproved?

The types of fraudulent financial reporting outlined by the ACFE typically focus on improving the organization’s

financial picture by overstating income, understating losses, or using misleading disclosures. Conversely, some

organizations understate income to smooth earnings. Any intentional misstatement of accounting information

represents fraudulent financial reporting.