© 2023 Fannie Mae LL-2021-03 Page 1 of 7

Lender Letter (LL-2021-03)

Updated: Feb. 15, 2023

To: All Fannie Mae Single-Family Sellers

Impact of COVID-19 on Originations

The policy for sale of loans aged six months or less is now permanent policy. This will be incorporated into the Selling Guide

in a future update. Effective immediately, we are retiring the verification of employment and temporary eligibility

requirements for purchase and refinance transactions policies described below. All standard Selling Guide policies now

apply.

For a description of previous updates to this Lender Letter, refer to the Change Control Log.

Sale of loans aged six months or less

Effective: These policies became effective on May 5, 2020 and are effective until further notice.

The national response to COVID-19 and the related economic impacts have resulted in uncertainty about risks associated with

loans that have not been sold to us yet. Therefore, we are requiring that loans sold on a flow basis be no more than six months old

to be eligible for sale to us. The loan’s age will be calculated based on the following:

▪ Whole loans: from the first payment date to the date the loan data is submitted to Loan Delivery

o Example: If loan data is submitted May 2020, the first payment date can be no earlier than Nov. 1, 2019

▪ MBS loans: from the first payment date to the pool issue date

o Example: If the pool issue date is May 1, 2020 the first payment date can be no earlier than Nov. 1, 2019

NOTE : HomeStyle Renovation loans can be delivered up to 15 months after the note date provided the renovation is

completed before loan delivery and the loan is delivered with Special Feature Code 279.

Verification of self-employment

Effective: These policies became effective for loans with application dates on or after Apr. 14, 2020 and were retired on Feb. 15,

2023.

When a borrower is using self-employment income to qualify, the lender must verify the existence of the borrower’s business

within 120 calendar days prior to the note date. Due to latency in system updates or recertifications using annual licenses,

certifications, or government systems of record, lenders must take additional steps to confirm that the borrower’s business is

open and operating. The lender must confirm this within 20 business days of the note date (or after closing but prior to delivery).

Below are examples of methods the lender may use to confirm the borrower’s business is currently operating:

▪ evidence of current work (executed contracts or signed invoices that indicate the business is operating on the day the

lender verifies self-employment);

▪ evidence of current business receipts within 20 days of the note date (payment for services performed);

▪ lender certification the business is open and operating (lender confirmed through a phone call or other means); or

© 2023 Fannie Mae LL-2021-03 Page 2 of 7

▪ business website demonstrating activity supporting current business operations (timely appointments for estimates or

service can be scheduled).

See B3-3.1-07, Verbal Verification of Employment for our existing requirements.

Temporary eligibility requirements for purchase and refinance transactions

Effective: These policies became effective for loans with application dates on or after Jun. 2, 2020 and were retired on Feb. 15,

2023.

Lenders must continue to review the borrower’s credit report to determine the status of all mortgage loans. In addition to

reviewing the credit report, the lender must also apply due diligence for each mortgage loan on which the borrower is obligated,

including co-signed mortgage loans and mortgage loans not related to the subject transaction, to determine whether the

payments are current as of the note date of the new transaction. For the purposes of these requirements, “current” means the

borrower has made all mortgage payments due in the month prior to the note date of the new loan transaction by no later than

the last business day of that month. Examples of acceptable additional due diligence methods to document the loan file include:

▪ a loan payment history from the servicer or third-party verification service,

▪ a payoff statement (for mortgages being refinanced),

▪ the latest mortgage account statement from the borrower, and

▪ a verification of mortgage.

A borrower who is not current and has missed payments on any mortgage loan is eligible for a new mortgage loan if those missed

payments were resolved in accordance with the requirements in the table below.

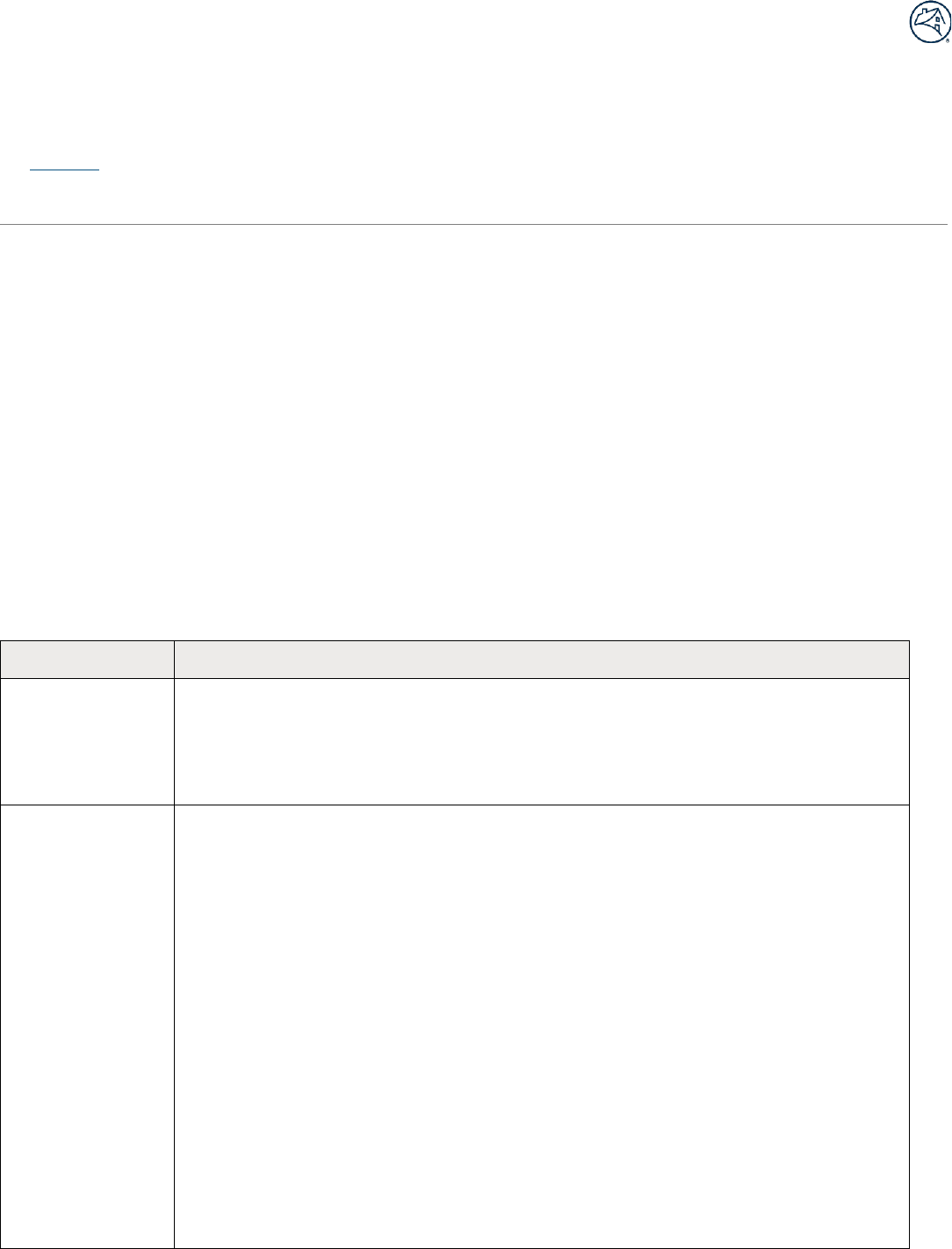

Resolution Method

Eligibility

Reinstatement

If the borrower resolved missed payments through a reinstatement, they are eligible for a new

mortgage loan. The lender must document the source of funds in accordance with eligible

sources of funds in the Selling Guide if the reinstatement was completed after the application

date of the new transaction. Proceeds from a refinance may not be used to reinstate any

mortgage loan.

Loss Mitigation

Solution

If outstanding payments will be or have been resolved through a loss mitigation solution, the

borrower is eligible for a new mortgage loan if they have made at least three timely payments as

of the note date of the new transaction as follows:

▪ For a repayment plan, the borrower must have made either three payments under the

repayment plan or completed the repayment plan, whichever occurs first. Note that

there is no requirement that the repayment plan be completed.

▪ For a payment deferral, the borrower must have made three consecutive payments

following the effective date of the payment deferral agreement.

▪ For a modification, the borrower must have completed the three-month trial payment

period.

▪ For any other loss mitigation solution not listed above, the borrower must have

successfully completed the program, or made three consecutive full payments in

accordance with the program.

Verification that the borrower has made the required three timely payments may include:

▪ a loan payment history from the servicer or third-party verification service,

▪ the latest mortgage account statement from the borrower, and

© 2023 Fannie Mae LL-2021-03 Page 3 of 7

▪ a verification of mortgage.

If these requirements are met on an existing mortgage loan being refinanced, the new loan

amount can include the full amount required to satisfy the existing mortgage.

We are not considering payments missed during the time of a COVID-19-related forbearance that have been resolved to be

historical delinquencies for purposes of our excessive mortgage delinquency policy as outlined in B3-5.3-03, Previous Mortgage

Payment History. This flexibility does not apply to high LTV refinance loans, which must continue to meet the payment history

requirements in B5-7-02, High LTV Refinance Underwriting, Documentation, and Collateral Requirements for the New Loan.

Additional resources

We offer information and resources for servicers to help borrowers deal with the challenges associated with COVID-19:

▪ Summary of COVID-19 Selling Policies

▪ Ask Poli Servicing

Lenders may also contact their Fannie Mae Account Team if they have questions about this Lender Letter.

Have guide questions? Get answers to all your policy questions, straight from the source. Ask Poli.

© 2023 Fannie Mae LL-2021-03 Page 4 of 7

Attachment

Requirements for borrowers using self-employment income to qualify

Effective: These policies remain effective for loans where the most recent tax return being used to document and support

qualifying income is older than 2020.

Income Analysis

Self-employment income is variable in nature and generally subject to changing market and economic conditions. Whether a

business is impacted by an adverse event, such as COVID-19, and the extent to which business earnings are impacted can depend

on the nature of the business or the demand for products or services offered by the business. Income from a business that has

been negatively impacted by changing conditions is not necessarily ineligible for use in qualifying the borrower. However, the

lender is required to determine if the borrower’s income is stable and has a reasonable expectation of continuance.

When 2020 federal tax returns are not available lenders are required to obtain the following additional documentation to support

the decision that the self-employment income meets our requirements:

▪ an audited year-to-date profit and loss statement reporting business revenue, expenses, and net income up to and

including the most recent month preceding the loan application date; or

▪ an unaudited year-to-date profit and loss statement signed by the borrower reporting business revenue, expenses, and

net income up to and including the most recent month preceding the loan application date, and three business

depository account(s) statements no older than the latest three months represented on the year-to-date profit and loss

statement.

o For example, the business depository account statements can be no older than Aug, Sep, Oct. for a year-to-date

profit and loss statement dated through Oct. 31.

o The lender must review the three most recent depository account statements to support the level of business

revenue reported in the current year-to-date profit and loss statement. Otherwise, the lender must obtain additional

statements or other documentation to support the on-going nature of business revenue reported in the current year-

to-date profit and loss statement.

NOTE : The year-to-date profit and loss statement must be no older than 60 days old as of the note date.

Lenders must review the profit and loss statement, and business depository accounts if required, and other relevant factors to

determine the extent to which a business is still being impacted by COVID-19. The lender can use the following guidance when

performing the assessment of business operations and stability and must complete the business income assessment based on

the minimum additional documentation above. In some instances, the lender may find it necessary to obtain supplemental

documentation listed in the examples below.

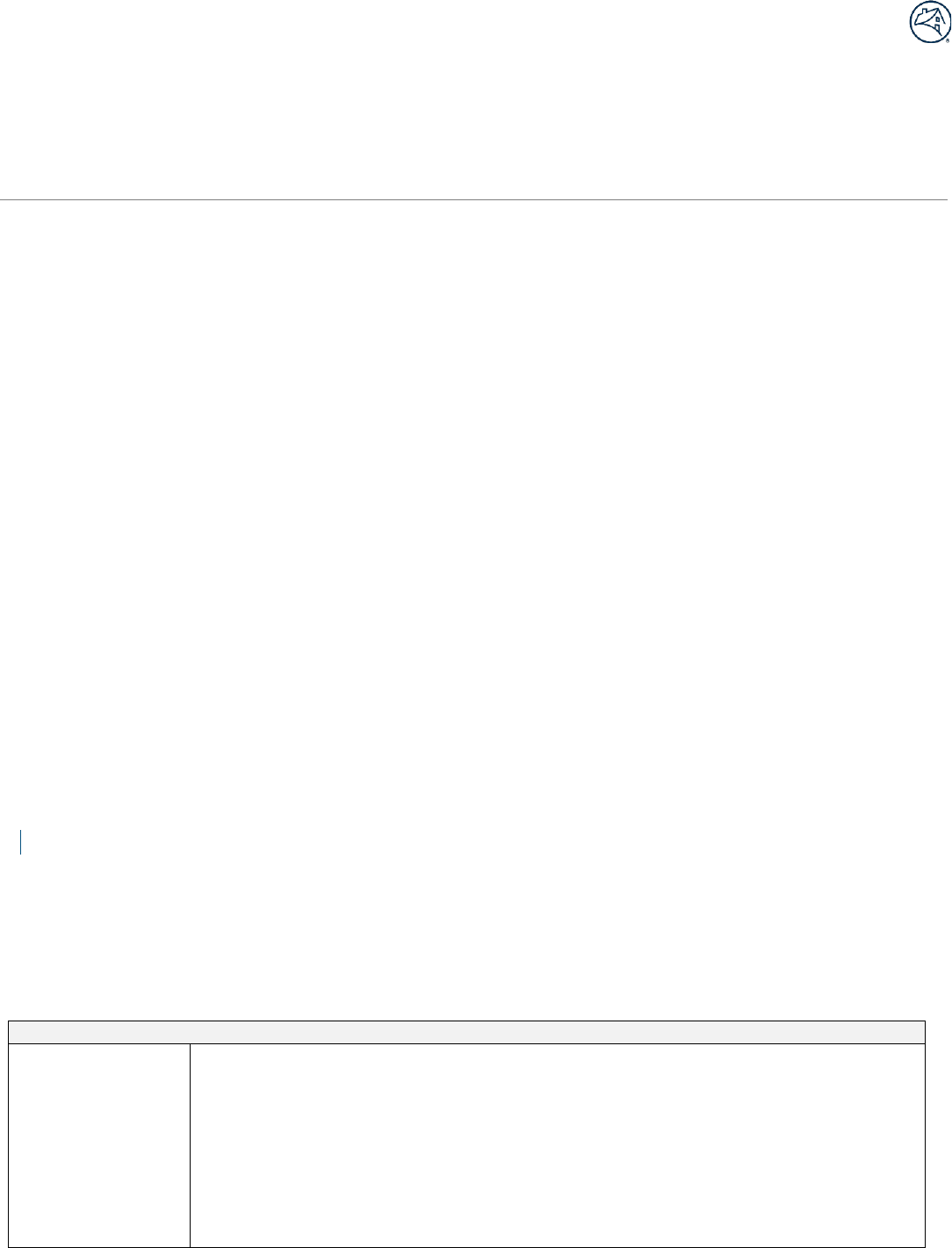

Assessing the Impact of COVID-19

Business operations

▪ Have business operations been maintained or modified to support continued business

income?

For example, review an updated business plan.

▪ Is the business continuing to operate in the current location or an alternate location suitable

for business operations?

For example, perform an Internet search or verify through a third-party source.

▪ Is there a demand for the product or service currently offered by the business?

For example, obtain current business receipts or purchase contracts.

© 2023 Fannie Mae LL-2021-03 Page 5 of 7

Assessing the Impact of COVID-19

▪ Is the business operation and/or revenue temporarily restricted due to state shelter in place,

stay at home or other similar state or local orders?

▪ Is the impact to the business operations negligible due to the nature of the business?

For example, obtain a written explanation from the business owner or confirmation that income

is seasonal apart from the event timeline.

Business Income

The lender must complete a business income assessment by comparing the year-to-date net

business income from the year-to-date profit and loss statement to historical business income

calculated using the Cash Flow Analysis (Form 1084)* for a similar timeframe (such as monthly).

▪ Lenders can make standard adjustments to business cash flow (net income on the profit and

loss statement) in accordance with B3-3.4-04, Analyzing Profit and Loss Statements when

making this determination.

▪ When the lender determines net business income is impacted, but profit and loss details are

not sufficient to determine the income is stable at the reduced level, the lender can obtain

additional documentation to supplement the profit and loss statement (such as a month-to-

month income trending analysis) to make this determination. If stability cannot be

confirmed, the income is not eligible for qualifying purposes. See B3-3.1-01, General Income

Information for details.

Example

Historical monthly self-employment income calculated using Form 1084 = $2,000

Current level of stable monthly self-employment income as determined by the lender using

details from the year-to-date profit and loss statement and other supplemental

documentation = $1,000

The impact of the COVID 19 pandemic on current business income results in a 50% decline

from historical levels. See Business Income Calculation Adjustment below for next steps.

*Form 1084 or any other type of cash flow analysis form that applies the same principles.

Business Stability

▪ Does the profit and loss identify a significant imbalance between expenses and revenue that

may impact financial stability? Or have modifications to current business operations been

made to correct this imbalance? (Consider documenting with an updated business plan)

▪ Do prior year business tax returns demonstrate ample financial liquidity due to a history of

retained earnings?

▪ Do current business account balances (excluding Paycheck Protection Program (PPP) or other

similar COVID-19 related loans or grants) support the financial ability of the business to

operate given current market and economic conditions?

A current balance sheet may be used to support the lender’s determination of business stability,

in conjunction with the profit loss statement.

Business Income Calculation Adjustment

When the lender determines current year net business income is still being impacted by the COVID-19 pandemic and is

▪ less than the historical monthly income calculated using Form 1084, but is stable at its current level, the lender must

reduce the amount of qualifying income calculated using Form 1084 to no more than the current level of stable income

as determined by the lender (see Business Income above).

© 2023 Fannie Mae LL-2021-03 Page 6 of 7

▪ more than the historical income calculated using Form 1084, the lender must use no more than the currently stable level

of income calculated using Form 1084 to qualify the borrower.

In all cases, qualifying income must be supported by documentation, including any supplemental documentation obtained by the

lender.

© 2023 Fannie Mae LL-2021-03 Page 7 of 7

Change Control Log

The following table provides a description of the updates that were previously made to this Lender Letter in 2022.

Date of Update

Description of Update

July 06, 2022

▪ Removed the suspension of bulk acquisitions. We will consider bulk transactions on a limited

basis, with a focus on providing a channel for liquidity for smaller lenders.

▪ Updated the allowable delivery timeframe for HomeStyle

®

Renovation loans to align with the

15-month time period permitted in the Selling Guide for completion of the renovation.

Feb. 02, 2022

▪ Effective immediately we retired the COVID-19 temporary requirements for borrowers with

qualifying income derived from self-employment provided the most recent federal income tax

returns are not older than 2020. Lenders may follow standard Selling Guide policies with respect

to self-employment income.

▪ If the most recent federal income tax returns are dated before 2020, lenders must continue to

apply the prior requirements, which are now described (unchanged) in the Attachment to this

Lender Letter.

▪ Note that the temporary requirements for Verification of Self-employment continue to apply to

all loans using self-employment income to qualify.

▪ Removed guidance for furloughed borrowers; refer to temporary leave income in B3-3.1-09,

Other Sources of Income for additional information.