Page 1 of 17

MAY 2016 PROFESSIONAL EXAMINATION

ADVANCED AUDIT & ASSURANCE (3.2)

EXAMINER’S REPORT, QUESTIONS AND MARKING SCHEME

EXAMINER’S REPORT

STANDARD OF THE PAPER

The questions were featured from all the nine sections of the syllabus. The marks

allocation was also done strictly in accordance with the syllabus weighting as reflected

in the chart below.

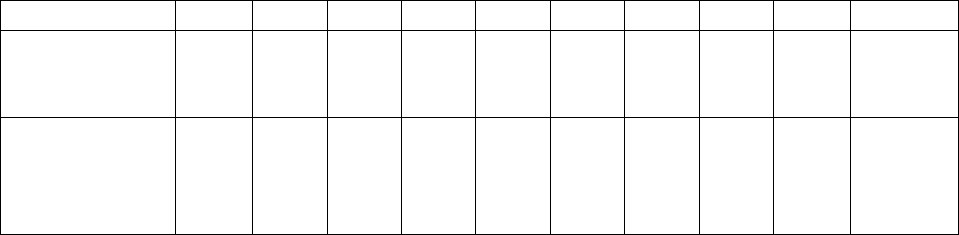

SECTIONS OF SYLLABUS COVERAGE AND WEIGHTING

SECTIONS

A

B

C

D

E

F

G

H

I

TOTAL

SYLLABUS

WEIGHTING

(%)

10

10

10

20

10

10

10

10

10

100

MARKS

ALLOTED

TO

QUESTIONS

10

10

10

20

10

10

10

10

10

100

The solutions were very detailed and responded adequately to the requirements of the

questions. The marking scheme was structured fairly to the advantage of candidates.

PERFORMANCE OF CANDIDATES

Performance in the paper fell far below expectation. Candidates demonstrated that they

did not prepare adequately and therefore lacked required knowledge to answer the

questions correctly. Answers provided did not respond to the requirements of the

questions. While many candidates wrote ‘auditing’, they did not answer the questions.

However, the approach to the questions, the style of writing and use of language

indicated that candidates did individual work and there was no sign of copy work

among candidates.

WEAKNESSES OF CANDIDATES

Many candidates resorted to defining terms as preamble to their answers when no

definition was called for. Such efforts resulted in no reward to the candidates. Some

candidates also did not know the difference between the memorandum and letter forms

for presenting reports.

Page 2 of 17

ADVANCED AUDIT & ASSURANCE QUESTIONS

QUESTION ONE

a) Everclean Water Limited processes and packages portable water for local

consumption. The factory is situated in a valley in a first-class residential area of

the city. A major road used by most residents runs in front of the factory. Often

this road is flooded with spill-over of water from the factory thus hindering

vehicular and pedestrian movement. Management of the company on such

occasions uses the services of a contractor to pump out the water from the road.

This situation contravenes the provisions of the Factories, Offices and Shops Act

1970, Act 328.Everclean Water Limited has engaged Nadab and Associates as the

auditors. In their preliminary tour of the factory the senior partners became

aware of the flooding situation in the area. Back in the office the senior partners

consulted ISA 250 “Consideration of laws and regulations in an audit of

financial statements” for guidance on the auditor’s responsibility to consider

laws and regulations in an audit of financial statements before carrying out the

audit assignment.

Required:

i) State examples of the possible type of information that might have come to the

auditors’ attention that might indicate non-compliance with the Factories, Offices

and Shops Act. (5 marks)

ii) Evaluate the possible effect on the financial statements for non-compliance

with the law according to ISA 250. (5 marks)

a) Dibidibi & Co., an audit and assurance firm, has been engaged as auditors for the

BCG Bank Ltd, a public limited liability company for some time now. BCG Bank

has sixty branches throughout the country and branches in Togo, Burkina Faso

and Cote d’Ivoire. The Bank is one of the Banks in the country which can boast

of large landed properties. Dibidibi & Co. receives about 20% of its income from

this particular client. Before last year’s audit, the bank engaged the audit firm to

value its Land and Buildings in all its branches and headquarters. This work was

executed by the audit firm and a report has been issued to management. The

report has been incorporated in this year’s financial statements to be audited

soon. Dibidibi & Co. sees BCG Bank Ltd. as a very important client whose works

are always executed with dispatch.

Required:

i) Identify and evaluate the significance of any threats to the Code of Ethics

for Professional Accountants raised in the case. (4 marks)

ii) Recommend safeguards to eliminate the threats (mentioned in (i) above)

or reduce them to an acceptable level. (6 marks)

(Total: 20 marks)

Page 3 of 17

QUESTION TWO

a) Papa Nii and Papa Nana who just qualified as Professional Accountants have

decided to enter into professional practice under a firm name Nana Nii &

Associates. These two have been trainee accountants of an Audit and Assurance

firm for three years before qualifying.

For their first engagement, the CEO of Mberdane Ltd. has nominated Nana Nii &

Associates for appointment as auditors of his company though Mberdane Ltd was a

former client of their former firm, Papa Nii and Papa Nana were never on the

engagement team of Mberdane Ltd.

As beginners Papa Nii and Papa Nana have intended to follow best practice as

required by ISQC 1 “Quality control for firms that perform audits and reviews of

financial statements, and other assurance related services”. However they are not

clear of the matters that they have to consider in their acceptance decision according

to the standard. They have approached you, a senior partner of their former firm

for advice.

Required:

Advise Papa Nii and Papa Nana on the matters that they may have to consider in

relation to the acceptance decision on their nomination. (10 marks)

b) Adepa Ltd, a fruit processing company has been in operation for many years. It has

managed to grow the business over the years and now has eight branches, four in

rural areas and four in urban towns in addition to the head office. The management

and those charged with governance are looking forward to the company adopting

the latest technology in production – Advanced Technology Manufacturing (ATM)

and marketing and sales though the internet.

During the last audit of the financial statements of the company, the Managing

Director suggested to the Senior Partner an assessment of the need for an internal

audit department in the company. You were the audit manager which led the

engagement team to do the audit. The Senior Partner has therefore asked you to

carry out the assignment to assess the need for an internal audit in Adepa Ltd.

Required:

Draft a report to the Senior Partner on the assessment of the need for an internal

audit department for Adepa Ltd., highlighting the factors to be considered in such

assessment. (10 marks)

(Total: 20 marks)

Page 4 of 17

QUESTION THREE

a) Your audit and assurance firm has just accepted a financial statement audit

engagement from Lunch Special Ltd. a restaurant that prepares lunch for the general

public and on special orders. The company operates at a number of sales points in

the city.

The company uses a computerised system that has networked all the Sales Points to

its Head Office. Your firm is planning the new audit and has received the draft

financial statements for the year. As the audit senior to lead the engagement team,

you are examining the financial statements, an extract of which is shown below:

Statement of Profit or Loss (Extract) Draft Audited

2015 2014

(GH¢ ‘000) (GH¢ ‘000)

Turnover 16,346 11,300

Cost of Sales 12,912 8,596

Gross Profit 3,434 2,704

Net Profit 1,962 1,130

Statement of Financial Position (Extract)

Non-current Assets 5,598 5,232

Other Current Assets 3,492 2,254

Account Receivables 3,964 2,872

Inventories 1,291 860

Account Payables 1,028 920

Required:

i) Using analytical procedures at the planning stage, state your observations

drawn from the extracts from the draft financial statements and how they

may impact on your audit of the Accounts Receivables. (10 marks)

ii) Demonstrate how you will review the opening balances in the draft

financial statements. (10 marks)

(Total: 20 marks)

QUESTION FOUR

a) Dr. Kofi Mensah has been appointed the Municipal Chief Executive (MCE) of

Kyekyewere Municipal Assembly. He has assumed duty early last month and

has carried out familiarisation tour of all the departments of the Assembly.

You are the Internal Auditor of the Assembly and has worked there for the past

two years. During your turn of briefing the MCE, you mentioned to him that the

Internal Audit Agency (IAA) exists as an apex oversight body of internal audit

units working within MDAs and MMDAs. It was established by the Internal

Page 5 of 17

Audit Agency Act (2003) with the object to co-ordinate, facilitate and provide

quality assurance for internal audit activities within the MDAs and MMDAs.

At the end of your briefing the MCE requested for more information on the IAA

especially its functions. You were pleased with the MCE and formerly welcomed

him to the Assembly.

Required:

Communicate to the MCE in the appropriate form detailing out the functions of

the Internal Audit Agency according to the Internal Audit Agency Act (2003).

(10 marks)

b) Dabiasem Insurance Company Ltd. prepares its annual financial statements to

31st December each year. Due to the magnitude of the transactions, interim

financial statements for each half year are prepared at the end of June every year.

This is done to facilitate the early completion and audit of the annual financial

statements. Nhwehwem & Associates are the independent financial statement

auditors of Dabiasem Insurance Co. Ltd. This year’s interim financial

information have been prepared and are ready for review.

You are the audit senior of the auditing firm and the head of the audit team to

carry out the review of the interim financial information.

Required:

Suggest the procedures you would use to carry out the review of the interim

financial information. (10 marks)

(Total: 20marks)

QUESTION FIVE

a) Broni & Co. have audited the annual financial statements of Bibini Co. Ltd., a

public limited liability company, for the year ended 31

st

December, 2014. The

accounting system of the company is partially computerised.

During the audit it was detected that just two members of staff out of one

hundred and fifty workers, were entirely and equally responsible for the

maintenance of personnel records and preparation of the payroll. The chief

accountant only confirms that the amount of the wages and salaries cheque

agrees with the total of the net wages column in the payroll, then he signs

without any reasonableness check of the amount of the total wages cheque. This

situation is a serious deficiency in the control system which can have serious

implications. As audit senior you are considering communicating this situation

to the management showing the deficiency, implications and recommendations.

Page 6 of 17

Required:

Prepare an appropriate report to management on the deficiency noted in the

internal control system for payroll. (10 marks)

b) Audit Quality has been a topical issue for discussion in the accountancy

profession in recent times. The International Auditing and Assurance Standards

Board (IAASB) has recently issued a publication on the Framework for Audit

Quality. The objectives of this publication are to raise awareness of the key

elements of audit quality; to encourage key stakeholders to explore ways to

improve audit quality; and to facilitate greater dialogue between key

stakeholders on the topic. Although audit quality is principally the responsibility

of auditors, there are many factors that contribute to it. The IAASB describes

these other factors as contextual, inputs, outputs and key interactions.

Required:

Discuss with examples what factors affect Audit Quality according to the recent

publication of the IAASB on Audit Quality. (10 marks)

(Total: 20 marks)

Page 7 of 17

ADVANCED AUDIT & ASSURANCE SCHEME

QUESTION ONE

(a) (i) Examples of the possible type of information that might have come to the

auditors’ attention that might indicate non-compliance with the Factories Act include:

Physical observation of the flooding by the Senior Partners on their visit to the

factory.

Tip-off from residents of the area, likely.

Investigation by a regulatory organisation or government department such as the

Environmental Protection Agency (EPA).

Payment of fines or penalties, if any.

Adverse media comments, likely. (5 Marks)

(ii) The auditors should consider the following, when evaluating the possible effect on

the financial statements for non-compliance with the law:

Going Concern applicability

The potential financial consequences, such as fines, damages, penalties, litigation,

threat of expropriation of assets and enforced discontinuation of operations.

Whether the potential financial consequences require disclosure like enforced

discontinuation of operations.

Whether the potential financial consequences are so serious as to call into

question the fair presentation given by the financial statements, or otherwise

make the financial statements misleading.

Provisions to be made in the accounts and contingencies. (5 Marks)

(b) (i) As the audit firm receives about 20% of its income from just one audit client, there

is a self-interest or intimidation threat. This is because the firm will be concerned about

losing the client.

The self-interest and intimidation threats are significant considering the nature and

duration of the breach – that is the high percentage of income from a single client

received for some time now; and the knowledge of the audit firm of such interest.

Secondly, the valuation services provided by the audit firm. If an audit firm performs a

valuation which will be included in financial statements audited by that firm, a self-

review threat arises. This threat is significant as the valuation of Land and Buildings of

all branches of the bank including the head office is material to the financial statement

to be audited. (4 Marks)

(ii) The possible safeguards for the self-interest or intimidation threats include:

Reducing the dependence on the client

Implementing external quality control reviews; or

Consulting a third party, such as a professional regulatory body or a professional

accountant, on key audit judgments.

Page 8 of 17

Internal quality control reviews.

As the bank is a public interest entity and the firm’s total fees has been that high for two

consecutive years, the Code of Ethics provides that the firm shall:

Disclose this to those charged with governance;

Conduct a review, either by an external professional accountant or by a

regulatory body.

Since the total fees significantly exceed 15%, a pre-issuance review shall be required.

That is a review before the audit opinion on the second year’s financial statements.

The safeguards for the self-review threat from the valuation services will include:

Second partner review

Confirming that the client understands the valuation and the assumptions used

Ensuring that the client acknowledges responsibility for the valuation

Using separate personnel for the valuation and the audit.

(6 Marks)

(Total: 20 Marks)

EXAMINER’S COMMENTS

Candidates were required in question (a) to state the types of information that will

come to the auditor’s attention that might indicate that a client has not complied with

the provisions of the factories, offices and shops Act. Many candidates repeated the

information given in the preamble without relating it to the question. Other candidates

were able to provide the right answers.

Candidates were asked in the other part to evaluate the possible effects on the financial

statements for non-compliance with law according to ISA 250. Some candidates gave

the right answers but other candidates wrote about the effect of the non-compliance on

the business, such as bad publicity and boycott of products, rather than the effects on

the financial statements, namely, provisions and contingencies and going concern

applicability etc.

Question 1 (b)

This question on ethics demanded identification and evaluation of the significance of

any threats to objectivity and safeguards to deal with them.

(i) Receipt of about 20% of practice income from one client

(ii) Valuation of land and building for an audit client. Many candidates were able to

identify the threats to together with the required safeguards. Some candidates

missed the right answers and wrote about advocacy and familiarity threats

instead of self-interest and self-review threats.

Page 9 of 17

QUESTION TWO

(a) The standard, ISQC 1 provides three main issues to be considered for acceptance of

nomination. These are the integrity of the client, the competence of the firm and ethical

requirements. The matters to consider on the integrity of a client include the following:

The identity and business reputation of the client’s principal owners, key

management, related parties and those charged with governance.

The nature of the client’s operations, including its business practices

Information concerning the attitude of the client’s principal owners, key

management, and those charged with governance towards matters such as

aggressive interpretation of accounting standards / internal control environment

Whether the client is aggressive with fixing and maintaining the firm’s fees as

low as possible

Any indication of an inappropriate limitation on the scope of work

Any indication that the client might be involved in money laundering or other

criminal activities

The reasons for the proposed appointment of the firm and non-reappointment of

the previous firm.

The matters to consider on the competence of the audit firm include:

Knowledge of the relevant industry by the firm’s personnel

Experience with relevant regulatory or reporting requirements

Personnel with the necessary capabilities and competence

Availability of experts if needed

Ability to complete the engagement within the reporting time.

The ethical issues border on the need for the firm to consider whether acceptance of the

nomination will create any conflict of interest or other ethical issues. The firm must also

ensure that the previous auditors have been properly removed in accordance with the

law.

(10 Marks)

(b). 15th September, 2015.

REPORT ON ASSESSMENT OF THE NEED FOR INTERNAL AUDIT IN ADEPA

LTD. TO THE SENIOR PARTNER.

In assessing the need for an internal audit function in Adepa Ltd., consideration should

be given to the following factors:

The cost of setting up an internal audit department versus the predicted benefits

Predicted savings in external fees where work carried out by consultants will be

carried out by the new internal audit department.

Page 10 of 17

The complexity and scale of the Adepa Ltd.’s activities and the systems

supporting those activities especially with the current growth of the company

and the desire to use the most modern technology in its activities

The ability of existing managers and employees to carry out assignments that

internal audit may be asked to carry out

Management’s perceived need for assessing risk and internal control as

demonstrated by the management of Adepa Ltd.

Whether it will be more cost effective or desirable to outsource the work

The pressure from external stakeholders to establish an internal audit

department.

If the volume of internal audit work required is such that the price differential between

employing an internal audit team and outsourcing the work is small, the company will

need to consider that there are longer term benefits such as:

Establishing an internal audit department will help maintain a group of highly

skilled people which may help the business develop faster that it would

otherwise have been

Working in internal audit can be a route providing training for future senior

executives because internal auditors are likely to obtain knowledge of many

aspects of the business and liaise with personnel at all levels.

If management considers these factors, it will be in a position to take a decision on the

establishment of an internal audit department.

Signed

Audit Manager. (10 Marks)

(Total: 20 Marks)

EXAMINER’S COMMENTS

Question 2 (a)

Candidates were asked to advise a newly established firm on matters the partners may

consider in relation to the acceptance of a new client in accordance with the

requirements of ISQC1. Many candidates gave the right answers, namely matters

bothering on the integrity of the client, the competence of the firm and ethical

requirements.

Question 2 (b)

This question demanded highlighting factors to be considered in assessing the need for

internal audit in a client’s business. Instead of highlighting the relevant factors, many

candidates outlined the functions of internal audit, while others wrote about the

advantages of internal audit.

Page 11 of 17

QUESTION THREE

(a). The following are the observations made from the draft financial statements and the

impact on the audit of the Account Receivable:

(i) Turnover has gone up by 45% from last year while Account Receivable has increased

by 38%. The impact of this observation on the audit of Account Receivable would be on

the confirmation of the end of year balances through the circularisation of customers

and reconciliation of customer statements. Also management policy on discount should

be checked and ensure proper record of discounts taken by customers.

(ii) Account Receivable payment period has reduced from 93 days last year to 89 days

this year. Information on payment terms with customers must be obtained to establish

payment expectations. Customers’ payments must be reconciled with cash and bank

balances to ensure that there is no risk of unrecorded receipts.

(iii) Account Receivables have increased by 38%, not consistent with the reduction in

the customer payment period from 93 days to 89 days. There is the risk of not properly

accounting for cash received from customers. Watch out for teeming and lading, check

for possible bad debts and ensure appropriate authorisation for them.

(iv) The Gross Profit Margin has reduced from 24% last year to 21% this year. This calls

for the checking of completeness and accuracy of the Turnover and Account Receivable

figures. Ensure that all invoices have been properly accounted for in both Sales Account

and Account Receivable Accounts. (10 Marks)

b) The following procedures could be applied to review the opening balances in the

draft financial statement:

i. Determine whether the closing balances of 2014 have been correctly brought

forward to 2015.

ii. Determine whether the opening balances reflect the application of appropriate

accounting policies.

iii. Review the predecessor auditor’s working papers to obtain evidence regarding the

opening balances.

iv. For the non-current assets obtain audit evidence by examining the accounting

records and other information underlying the opening balances.

v. For the current assets and liabilities obtain some audit evidence from the current

period audit procedures. For example, the collection of account receivable and

payment of account payable during the current period will provide some audit

evidence of their existence, rights and obligations, completeness and valuation at the

beginning of the period.

vi. For the inventories, obtain some audit evidence from the current periods audit

procedures on the closing inventory balance as well as additional audit procedures

such as:

Observing a current physical inventory count and reconciling it back to the

opening inventory quantities.

Performing audit procedures on the valuation of the opening inventory item

Page 12 of 17

Performing audit procedures on gross profit and cut-off.

vii. Obtain sufficient appropriate audit evidence about:

Whether the accounting policies reflected in the opening balances have been

applied consistently in the current period’s financial statements; and

Whether changes in the accounting policies have been accounted for properly

and adequately presented and disclosed in accordance with the applicable

financial reporting framework.

viii. Read the most recent financial statement and the predecessor auditor’s report for

information relevant to the opening balances.

(10 Marks)

(Total: 20 Marks)

EXAMINER’S COMMENTS

Question 3a (i)

Candidates were asked to draw observations from preliminary analytical review and

the effect of their observations on the audit of receivables (Statement of profit and loss

extract was provided). Some candidates were able to compute and interpret the

relevant analytical measures, namely increase or decrease in turnover gross profit,

receivables and the receivables collection period. The necessary audit tests were also

given. Many candidates did not know which analytical measures were needed to

answer the question and ended up computing ratios for all the elements of the financial

information extract given. They could also not interpret the results correctly resulting

in wrong auditing procedures being used.

Question 3a (ii)

This question required demonstration of how to review opening balances in draft

financial statements. Some candidates were able to follow the applicable procedures for

review of opening balances. Other candidates did not know that opening balances

involve mainly statement of financial position figures and went the extra mile of

including statement of profit or loss figures in the review

QUESTION FOUR

(a) The appropriate form of communicating to a superior in an organisation is through a

Memorandum. The answer should therefore be set out in a Memorandum form.

MEMORANDUM

To: Municipal Chief Executive

From: Internal Auditor

Subject: Functions of the Internal Audit Agency

Date: 15th September, 2015

___________________________________________________________________________

As requested during our interaction on your familiarisation tour of the Internal Audit

Department, the functions of the Internal Audit Agency (IAA) are detailed below.

Page 13 of 17

The IAA is required to ensure that:

1) The financial activities and operating information reported internally and

externally is accurate, reliable and timely.

2) The financial activities of MDAs and MMDAs are in compliance with laws,

policies, plans, standards and procedures.

3) National resources are adequately safeguarded.

4) National resources are used economically, effectively and efficiently.

5) Plans, goals and objectives of MDAs and MMDAs are achieved.

6) Risks are adequately managed in the MDAs and MMDAs.

In addition to these, the IAA must:

7) Promote economy, efficiency and effectiveness in the administration of

government programmes and operations.

8) Prepare plans to be approved by the Board for the development and

maintenance of an efficient internal audit for the MDAs and MMDAs.

9) Facilitate the prevention and detection of fraud.

10) Provide a means for keeping the MDAs and MMDAs fully and currently

informed about problems and deficiencies related to the administration of their

programmes and operations and the necessity for appropriate corrective action.

Finally, the IAA is required to monitor, undertake inspections and evaluate the internal

auditing of the MDAs and MMDAs. I shall be available for any further discussion when

necessary.

Thank you.

Signed.

Internal Auditor

(10 Marks)

(b) The procedures that could be used to review the interim financial information

include:

i. Reading last year’s audit and previous review files.

ii. Considering any significant risks that were identified in the prior year audit.

iii. Reading the most recent and comparable interim financial information.

iv. Considering materiality.

v. Considering the nature of any corrected or uncorrected misstatement in last

year's financial statements.

vi. Considering significant financial accounting and reporting matters of ongoing

importance.

vii. Considering the results of any interim audit work for this year’s audit.

viii. Considering the work of internal audit.

ix. Asking management what their assessment is of the risk that the interim

financial statements might be affected by fraud.

Page 14 of 17

x. Asking management whether there have been any significant changes in

business activity, and if so, what effect they have had.

xi. Asking management about any significant changes in internal controls and the

potential effect on preparing the interim financial information.

xii. Asking how the interim financial information has been prepared and the

reliability of the underlying accounting records.

(10 Marks)

(Total: 20 Marks)

EXAMINER’S COMMENTS

Question 4 (a)

Candidates were asked to communicate to an MCE in an appropriate form, detailing

the functions of the Internal Audit Agency according to the Internal Audit Agency Act

(2003). Since candidates were presumed to be internal auditors of the assembly, the

appropriate form of communication was a memorandum. While some candidates

provided the right answers in the appropriate form of communication-memo-others

just wrote out the functions while some candidates rather gave the functions of internal

audit.

Question 4 (b)

Candidates were required to suggest procedures to use to carry out review of interim

financial information. As usual some candidates were able to give the right answers but

others used general auditing tests as answers, while others treated it as review of the

historical financial statement during the annual statutory audit.

QUESTION FIVE

(a) REPORT TO MANGEMENT

The Directors

Bibini Co. Ltd

10 Wansema Lane, Somewhere City

15th September, 2015.

Dear Sirs,

Following our recent audit of your company, we are writing to advise you of various

matters which came to our attention.

We have set below the areas of significant deficiency which we noted, together with our

recommendations. These recommendations have already been discussed with the

Managing Director and his comments have been included.

As the purpose of the audit is to form an opinion on the company’s financial statements,

you will appreciate that our examination cannot necessarily be expected to disclose all

shortcomings of the system and for this reason, the matters raised may not be the only

ones which exist.

Page 15 of 17

Deficiencies

Preparation of payroll and maintenance of personnel records.

Under your present system, just two members of staff are entirely and equally

responsible for the maintenance of personnel records and preparation of the payroll.

Furthermore, the only independent check of any nature on the payroll is that the chief

accountant confirms that the amount of the wages cheque presented to him for

signature agrees with the total of the net wages column in the payroll. This latter check

does not involve any consideration of the reasonableness of the amount of the total net

wages cheque or the monies being shown as due to individual employees.

Implications

It is a serious deficiency of your present system, that so much responsibility is vested in

the hands of just two people. This situation is made worse by the fact that there is no

clearly defined division of duties between the two of them. In our opinion, it would be

far too easy for fraud to take place in this area (for example, by inserting the names of

ghost employees into the personnel records and hence on to the payroll) and/or for

clerical errors to go undetected.

Recommendations

i. A person other than the two clerks should be made responsible for

maintaining the personnel records and for periodically (but on surprise basis)

checking them against the details on the payroll.

ii. The two wages clerks should be allocated specific duties in relation to the

preparation of the payroll, with each clerk independently reviewing the work

of the other.

iii. When the payroll is presented in support of the cheque for signature to the

chief accountant, he should be responsible for assessing the reasonableness of

the overall charge for wages that week.

We should appreciate your comments as to how you propose to deal with the matters

raised in this letter. If you require any further information or advice, please contact us.

We have prepared this letter for your use only. It should not be disclosed to a third

party and we can assume no responsibility to any third party to whom it is disclosed

without our written consent.

We would like to take this opportunity to thank you and your staff for your help and

co-operation during the course of our audit.

Yours faithfully,

Broni and Co.

(10 Marks)

Page 16 of 17

(b) The recent publication by the IAASB on audit quality, describes the factors that

contribute to audit quality as contextual factors, input factors, output factors and key

interaction factors.

Contextual factors determining audit quality include:

Business practices and commercial law

Laws and regulation relating to financial reporting

The applicable financial reporting framework

Information systems

Corporate governance

Financial reporting timetable

Broader cultural factors

Audit regulation

Litigation environment

Attracting talent

Inputs into audit quality are factors which may contribute to a high quality audit and

would include the following:

Values, ethics and attitudes of auditors and the audit firm

Knowledge, experience and time allocated to perform the audit.

Outputs from audit quality may flow from:

The auditor

The audit firm

The entity

Audit regulators

Key interactions with regard to audit quality include:

Auditors and management, those charged with governance, users and regulators

Management and those charged with governance, users and regulators

Those charged with governance and regulators and users

Regulators and users.

(10 Marks)

(Total: 20 Marks)

Page 17 of 17

EXAMINER’S COMMENTS

Question 5 (a)

Preparation of an appropriate report to management on deficiencies noted in maternal

control system for payroll was demanded of candidates. Strangely enough many

candidates could not handle the question very well. They did not use the letter form for

the presentation. Some candidates could not identify and describe clearly the

weaknesses in the control system. Few candidates however did the right thing by using

the letter format, spelling out the deficiencies, the implications and recommendations.

Question 5 (b)

This question involved discussing with examples, factors that affect Audit Quality

according to the recent publication of the IAASB on Audit Quality. Many candidates

discussed general factors affecting Audit Quality but could not go beyond the IAASB

classification of the factors under ‘contextual’, ‘inputs’, ‘outputs’ and ‘interactions’.

CONCLUSION

The standard of the paper reflected attempts to raise the paper to the required level and

this trend must be followed. The full coverage of the syllabus in featuring questions

and the adherence to the syllabus weighting in the allocation of marks to questions

must be maintained. Candidates should be advised to prepare adequately before

requesting to write the examination.