Cambridge Centre for Risk Studies

Scenario Best Practices

DEVELOPING

SCENARIOS FOR

THE INSURANCE

INDUSTRY

Acknowledgements

Cambridge Centre for Risk Studies gratefully acknowledges

Lighthill Risk Network for supporting the research eorts

summarised in this report. The Centre is grateful for the

expertise provided by our research team, collaborators, and

subject matter specialists. Any misinterpretation in use of the

advice provided is entirely the responsibility of the Cambridge

Centre for Risk Studies.

Report Citation

Cambridge Centre for Risk Studies, in collaboration with

Lighthill Risk Network, 2020. Developing Scenarios for the

Insurance Industry. Cambridge Centre for Risk Studies at the

University of Cambridge Judge Business School.

or

Strong, K., Carpenter, O., Ralph, D. 2020. Developing

Scenarios for the Insurance Industry. Cambridge Centre for

Risk Studies at the University of Cambridge Judge Business

School and Lighthill Risk Network.

Cambridge Centre for Risk Studies

University of Cambridge Judge Business School

Trumpington Street

Cambridge

CB2 1AG

United Kingdom

Website and Research Platform

www.jbs.cam.ac.uk/risk

Research Team

Dr Andrew Coburn, Chief Scientist

Professor Daniel Ralph, Academic Director

Simon Rue, Director of Research & Innovation

Dr Michelle Tuveson, Chairman & Executive Director

James Bourdeau, Geopolitical Risk Research

Oliver Carpenter, Lead Environmental Risk Research

Jennifer Copic, Lead Governance Risk Research

Dr Jennifer Daron, Lead Technology Risk Research

Ken Deng, Lead Financial Risk Research

Timothy Douglas, Risk Modelling

Tamara Evan, Lead Geopolitical Risk Research

Taryn Hubbard, Risk Research

Oliver Pearson, Risk Markets Research

Dr Andy Skelton, Lead Risk Modelling

Kayla Strong, Lead Scenario Analytics

Dr Timothy Summers, Senior Data Scientist

Jayne Tooke, Communications and Events

William Turner, Data Science

Lighthill Risk Network

LM01.01.02

The Leather Market

11-13 Weston Street

London, SE1 3ER

United Kingdom

Website

https://lighthillrisknetwork.org/

Members

Matthew Eagle, Managing Director,

Head of GC Analytics (Guy Carpenter)

Premal Gohil,

Head of Innovation Partnerships (Liberty Mutual)

Paul Kaye, Head of Actuarial Practice (Aon)

Shree Khare,

Group Head of Catastrophe Research (Hiscox)

Trevor Maynard,

Head of Innovation (Lloyd’s of London)

Andrew Mitchell,

Head of Catastrophe Modelling (MSAmlin)

Delimoma Oramas-Dorta,

Catastrophe Risk Analyst (Guy Carpenter)

Cameron Rye, Research Manager (MSAmlin)

David Singh, Head of Exposure

and Portfolio Management (MSAmlin)

Keith Smith,

Research and Development Manager (Lloyd’s of London)

Dickie Whitaker,

Chief Executive Ocer (Lighthill Risk Network)

The views contained in this report are entirely those of the research team of the Cambridge Centre for Risk Studies, and do not imply

any endorsement of these views by the organisations supporting the research, or our consultants and collaborators. The results of the

Cambridge Centre for Risk Studies research presented in this report are for information purposes only. This report is not intended

to provide a sucient basis on which to make an investment decision. The Centre is not liable for any loss or damage arising from its

use. Any commercial use will require a license agreement with the Cambridge Centre for Risk Studies.

Copyright © 2020 by Cambridge Centre for Risk Studies.

Cambridge Centre for Risk Studies

Scenario Best Practices

DEVELOPING

SCENARIOS FOR

THE INSURANCE

INDUSTRY

Contents

1

Introduction 5

1.1 The Insurance Industry 5

1.2 Why Use Scenarios? 5

1.3 Report Rationale and Intended Audience 6

1.4 A Framework for Scenario Development 7

2

Understanding Scenarios 8

2.1 What is a Scenario? 8

2.2 Types of Scenarios 9

3

Using Scenarios in the Insurance Industry 15

3.1 General Scenario Uses 15

3.2 Insurance Use Cases of Scenarios 17

3.3 Allocating Risk Capital 20

4

Shock Risk Scenario Development: Insurance Stress Testing 22

4.1 A Checklist for Scenarios 22

4.2 Scenario Development: a Stress Test Perspective 23

4.3 Considerations and Constraints 30

5

Scenario Development Case Study: Business Blackout 33

6

Future Perspectives on Scenarios 37

7

Glossary 38

8

References 40

Cambridge Centre for Risk Studies

4

Scenario Best Practices: Developing Scenarios for the Insurance Industry

1. Introduction

1.1 The Insurance Industry

The insurance industry comprises companies that

provide risk management by underwriting the risks of

individual entities and pooling them to spread the risk.

An insurance contract guarantees that, on the occurrence

of a specied uncertain future event, the insurer provides

a payment to the insured, and thereby assumes the risk.

In return, the insured (or policyholder) pays a premium,

or a regular fee, to the insurer for providing the coverage.

Insurance is critical in providing nancial security to

people and organisations performing their daily activities

and operations; or undertaking new and risky ventures.

There are several classes of insurance available to

accommodate a diverse range of customers with an array

of risks, which are often categorised by their asset type or

the entity being insured. Examples include property and

casualty, accident and health, or auto insurance.

1

In addition to oering traditional coverages for known

risks, supported by comprehensive industry experience

and understanding of their occurrence, insurers must

also continually adapt to emerging and uncertain risks.

Today, such risks are manifesting at an unprecedented

rate as the world is challenged by growing complexity

and interconnectedness between systems. To full the

consequent demand for insurance coverage against

emerging risks, insurers must rst evaluate such

uncertainty and ensure they can withstand potential

losses and operate sustainably. The insurance industry

shares key nancial and operational risk exposures with

the wider nancial sector, but is also uniquely exposed

to insurance risk, so internal assessments of risk must

account for the complexity of interactions between

both an insurer’s assets (premiums invested to cover

liabilities) and liabilities. One means of planning for

the future is using scenario analysis (or ‘stress testing’),

a longstanding practice within the industry, but which

continues to grow in importance as the market becomes

more aware of its benets and regulatory requirements

call for robust internal risk management.

1.2 Why Use Scenarios?

Scenarios are stories about how the future might

develop, aimed to stimulate exploration, understanding,

and discussion. Based on a coherent set of assumptions

about key deterministic relationships and driving forces,

scenarios describe plausible futures that are intended

to be scrutinised and debated. In the context of risk,

scenarios provide a tool to cope with uncertainty,

especially in the case of risks that are not well understood

or cannot be quantied or even identied. They provide

a systematic method for exploring how a complex and

diverse array of risks may impact an organisation, sector,

or economy; or in other words, how resilient these

systems are to potential disruptions. Scenarios question

whether organisations or communities can adapt to,

and even capitalise on, future changes, and stress their

existing capabilities to respond. This understanding

can be applied to support and rationalise decision

making about the future, and facilitate reporting,

management, and mitigation of risks. Scenarios are

valued for supporting creative thinking about plausible

futures, rather than attempting to accurately predict

individual outcomes.

In the insurance industry, these tools continue to

evolve in response to advancing consideration and

regulation of enterprise risk management, both within

the industry and for the insureds that the industry

indemnies. Scenarios are increasingly being used by

underwriters, analysts, risk managers, actuaries, and

other stakeholders in the (re)insurance community to

better understand the characteristics and consequences

of unknown, uncertain, or unexpected future events.

A critical distinction is made between scenarios that

examine emerging trends, which are of concern for

long-term strategic planning; and those that consider

catastrophic shocks, which trigger severe loss across a

potential range of insurance classes, and so represent

acute operational risks. This report is primarily written

to address the latter, and on the design and uses of shock

risk scenarios, which are increasingly in demand to

overcome the challenges posed in today’s and the future

risk landscape.

1. For a complete listing of the types of insurance, please refer to Multi line Data Denition

initiative (Cambridge Centre for Risk Studies, in collaboration with Risk Management

Solutions, Inc. 2018

5

Cambridge Centre for Risk Studies

1.3 Report Rationale and Intended Audience

This report intends to outline best practices for scenario

analysis within the insurance community, and to provide

a practical framework to assist practitioners engaging

with shock scenario development.

Within the report, we explore key features of, and

commonalities and dierences between, insurance

specic scenarios, and suggest how and for whom they

can be used eectively. Due to the varied applications

of scenarios and their associated development

methodologies, we focus the methodology discussion

on shock risk scenarios, and draw commonalities

from various shock scenario development techniques.

As a variety of scenario use cases have unique

requirements and maturity in the practice, development

methodologies do vary. However, we propose that

there is a general process which can be adapted and

modied for these various uses. By providing key

criteria and considerations for scenarios in the form of a

scenario development framework, we hope to equip the

reader with the necessary tools and context to develop

coherent, comprehensive, and intelligible scenarios,

which therefore eectively full their intended purpose.

This report provides insurance-specic

recommendations for scenario development, and

has been published in parallel with another report

2

which similarly outlines best practices for scenario

development in the disaster risk reduction community.

The insurance industry has a rich expertise in risk

assessment tools to price risk, employing scenarios

that tend to be expert-driven, scientically supported,

and product oriented. In contrast, within the diverse

community of disaster risk managers, scenarios

often serve to explore and incorporate the culture

and experience of various stakeholders in a more

participatory approach, for which emphasis may

be placed as much on what is learnt in the scenario

process as the end result. Developing the two reports in

parallel has provided valuable insight into the merits of

contrasting scenario approaches and has informed the

best practices advocated in both.

Report Aims

This report aims to address scenario best practices

through the following considerations:

1

The role scenarios play within the

insurance community;

2

The common and contrasting characteristics and

typologies of scenarios;

3

How scenarios are currently employed and might be

further or better used in methodologies to address

emerging risks;

4

Current scenario limitations and critiques specic to

the insurance community;

5

Stress test scenario guidance for catastrophe

risk analysis;

6

How scenario development and applications might

adapt in the future.

2. Report titled “Scenario Best Practices: Developing Scenarios for Disaster Risk Reduction”

(Cambridge Centre for Risk Studies, in collaboration with Lighthill Risk Network 2020)

6

Scenario Best Practices: Developing Scenarios for the Insurance Industry

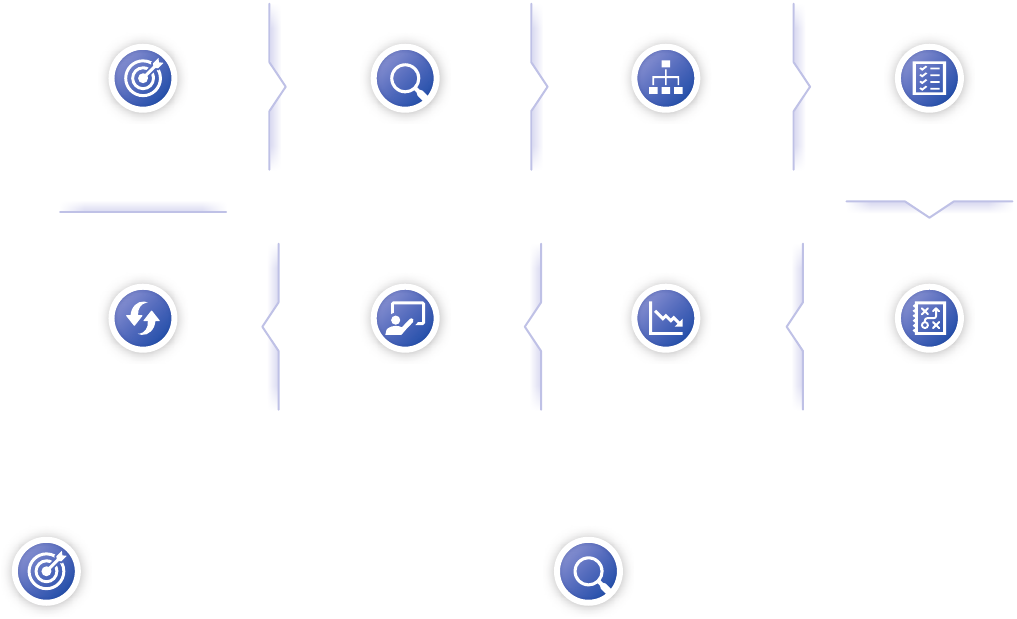

1.4 A Framework for Scenario Development

Within this report, we propose a framework for scenario

development that denes eight core steps, outlined in

Figure 1 and discussed in further detail in Section 4.

This framework is intended as a point of reference to

assist and ensure ecacy in the scenario process, rather

than as a prescriptive method that must be followed

absolutely. Further, while it outlines a linear step-by-step

structure for clarity, we encourage the scenario process

to be an iterative one, in which stakeholder engagement

provides opportunities for review and revision to ensure

it succeeds in fullling its aims.

Step 1 Scope the Risk

Identify the risk to be addressed, or, if the risk is uncertain

or unknown, dene the issues or vulnerabilities that the

scenario exercise aims to expose. In the latter case, the risk

may be identied later in the process. This contextualises

the objectives and resultant decisions of the analysis.

Step 2 Conduct Background Research

Research the topic dened in Step 1 by consulting

relevant sources of (scientic) knowledge and all

associated stakeholders within and beyond the insurance

industry. If possible, consider each dimension of risk:

hazard, exposure, and vulnerability, to recognise how and

where impacts occur.

Step 3 Frame the Scenario(s)

Consider and dene the key aims, benets, and

characteristics of a scenario and its process.

Figure 2 outlines some of the key questions the

developer should ask when framing their scenario.

Sections 2 and 3 provide the context to inform

these considerations.

Step 4 Develop Candidate Scenarios

Compose a series of candidate scenarios that capture

a range of plausible futures. Summarise scenarios with

brief outlines and key variables, and explore contrasting

characteristics. Select scenarios to progress that will

challenge and achieve the desired objectives.

Step 5 Develop a Narrative

Expand the selected scenarios with descriptions

that are interesting, challenging, and plausible for

all stakeholders. Account for all dimensions of a

future event, including context, triggers, timelines,

geography, responses, and implications.

Step 6 Assess Impacts and Materiality

Assess the impacts within the insurance industry and

in wider macro systems. Consider complexities and

interconnectivities that may cause cascading impacts

beyond the expected. Dene what constitutes a material

impact in order to focus the analysis on materially aected

assets and areas of business.

Step 7 Communicate and Act

Communicate the key ndings to stakeholders via

meaningful qualitative and quantitative outputs. The

content and complexity should be tailored to the

audience. Include a clear indication of the extent to

which the results can be relied on to inform decisions and

actions to address the risk.

Step 8 Evaluate and Update

Evaluate whether the objectives of the exercise have been

achieved and iterate the process with stakeholder input to

ensure or enhance ecacy. Be aware that the possibility and

character of a scenario will change as controlling factors

evolve, as will its impact as the industry advances, and so it

should be updated to maintain relevance and utility.

Figure 1: Scenario development framework for the insurance industry

7

Cambridge Centre for Risk Studies

2. Understanding Scenarios

2.1 What is a Scenario?

Scenarios are descriptions of potentially plausible events

that may occur in the future, leading to a particular

set of outcomes. They are based on assumptions about

key driving forces, interconnections, and relationships,

and have the ability to capture the uncertainties and

complexities of a system in a coherent manner. Scenarios

are not intended to comprehensively describe the

future, but rather to highlight focal elements of dierent

plausible futures and to highlight the key factors that

will drive future developments. Sometimes the terms

scenario, projection, and prediction (as well as others

such as forecast and outlook) are used interchangeably,

but while all are tools to investigate the future, each is

nuanced in its meaning. A prediction can be dened as

a subjective (probabilistic) statement that something

will happen in the future, while a forecast is the most

likely expected development.

3

In contrast, a projection is

a (probabilistic) statement that something will happen

under certain conditions, allowing for signicant changes

in the boundary conditions that might inuence a

prediction. A scenario-based projection is a hypothetical

construct of what could possibly happen conditional

upon fundamental assumptions.

4

These assumptions

allow some of the uncertainties that complicate more

exact statements on the future to be set aside for the

benet of a scenario exercise. The dimensions of what

constitutes a plausible event changes as external forces

shift. As a result, the scenario process is inherently an

evolving one, and scenarios which have been developed

and are relied upon should be maintained and updated

regularly to reect current conditions.

Sometimes scenario development and scenario analysis

(also called scenario ‘thinking’ or ‘planning’) are

dierentiated. Development means speculating about

the uncertainty surrounding the future and envisaging

dierent plausible future outcomes, or, in other words,

to create ’memories of the future’.

5

Scenario development

is the necessary foundation for scenario analysis, and

the two are closely linked. Scenario analysis can be

understood as the integration of scenarios into decision

making. Here, we explore both scenario development

and analysis together as the scenario process and use the

terms collectively.

The Probable, Possible and Plausible

When considering the future, we often add

‘probability’, ‘possibility’, or ‘plausibility’

qualications to emphasise relevance or importance.

These notions are implicitly dened, but often

not clearly dierentiated and so are confused. Is a

plausible future also probable? Can one future be

more plausible than another? Should any conceivably

possible future be considered? Care should be taken

in using these terms in the description of scenarios.

Key elements of the three qualiers are summarised

here to establish a distinction between them, but this

concern cannot be resolved by reducing each to a

denition. Scenario users should note that these terms

do not have any universal value, and so should ensure

the distinction between them is made suciently clear

to be useful.

6

Probability refers to the concept of chance and

likelihood, leading to an ordinal ranking of more or less

likely futures. Any future is possible, but the selection

of a probable or improbable scenario depends on

the application.

Possibility is a claim of reality; whether a future

is potentially realisable or not. It is a binary

distinction but may be challenged by absolute

(violation of established laws) or contingent (lack of

realism) reasons.

Plausibility addresses the structure of an argument

and places value on the credibility of a future, which can

hold true even though the future itself may be factually

fallacious. This is therefore a cognitive notion. Scenarios

are challenged by the dierence in interpretation of

plausibility between developers and stakeholders.

3. (MacCracken 2001) 4. (MacCracken 2001; Van Vuuren et al. 2012)

5. (Mietzner and Reger 2005; Schwartz 1997) 6. (Van der Helm 2006)

8

Scenario Best Practices: Developing Scenarios for the Insurance Industry

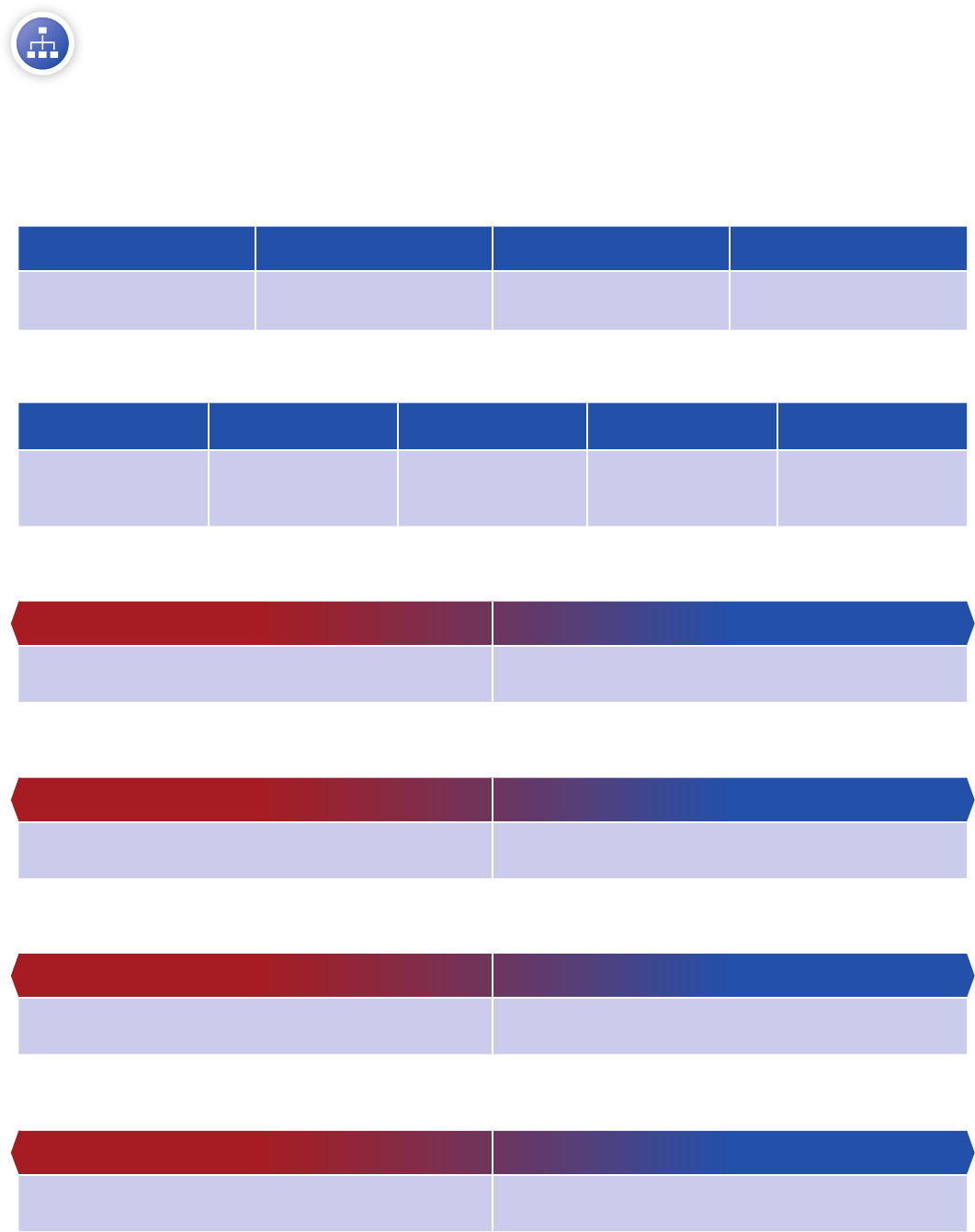

2.2 Types of Scenarios

Scenario design and development processes can be

commonly distinguished and classied, based on

the development process, their purpose, or certain

characteristics.

7

In practice, these typologies are rarely

binary or independent, and instead can be imagined

as a multi-dimensional matrix with unique outcomes.

This section proposes a series of distinctions which

are commonly used to dene scenarios. We encourage

practitioners to consider them as they construct

scenarios in the context of their scenario aims, within

the process of ‘Framing the Scenario(s)’ (Step 3 in the

Scenario Development Framework). These typologies

are illustrated in Figure 2, and discussed in detail within

this section.

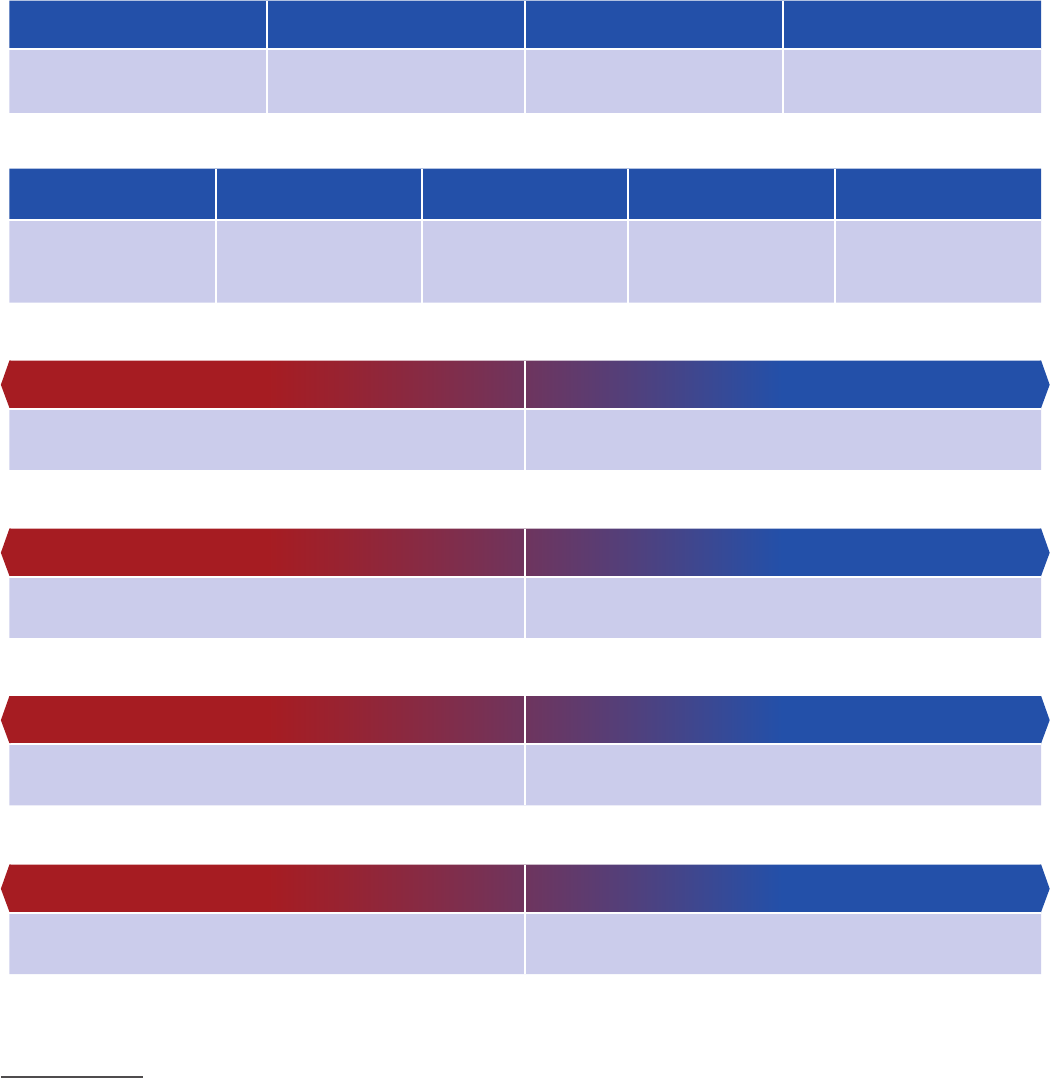

Aid Communication Demonstrate Due Diligence Identify Bias Sensitivity Analysis Addressing Uncertainty

To contextualise complex

risks and promote

stakeholder understanding

To assess risk exposures

and understand their

nancial implications

To explore partialities

that stakeholders may hold

towards certain decisions

To investigate the power

and variance of controlling

variables on a risk

To expand understanding

of the range of

plausible outcomes

Trend Risk Scenario Shock Risk Scenario

Slow-onset, trend phenomena

that emerge gradually over time

Sudden-onset, shock events

that occur quickly or unexpectedly

Exploratory - To ask ‘what if?’ Normative - To ask ‘what for?’

To stimulate imaginative thinking about the future

and widen understanding of available options

To better understand the path to desirable futures

and evaluate the impact of decisions

Figure 2: Framing a scenario – scenario typologies and applications

What is the scenario for?

How can the scenario benet stakeholders?

On what timescale does the risk materialise?

Which is the more important scenario outcome?

Who owns and contributes to the scenario process?

Understanding Tail Risks Understanding Emerging Risks Strategic Planning Accumulation Management

To identify and understand extreme,

low probability risks

To imagine and comprehend

new or evolving risks

To dene a resilient strategy

for the future that alleviates risks

To explore possible extreme or maximal

correlated losses to insurance portfolios

Participatory - Bottom-up, co-production of knowledge Expert-Driven - Top-down, analytical

To incorporate stakeholder culture, knowledge,

and experience in the process and end product

To deliver rigorous scientic descriptions

of plausible futures to decision makers

Probabilistic Deterministic

To estimate the likelihood of occurrence

based on the variance of quantied causal parameters

To speculatively explore phenomena

that involve a high degree of uncertainty

Is the scenario required to dene the likelihood of an outcome?

7. E.g. (Mietzner and Reger 2005; Henrichs et al. 2010; Van Vuuren et al. 2012)

9

Cambridge Centre for Risk Studies

Trend Risk Versus Shock Risk Scenarios

Scenarios can be developed to consider either sudden-

onset, shock events that emerge quickly or unexpectedly,

or slow-onset, trend phenomena that emerge gradually

over time. The type of risk dictates how the scenario is

developed and how it may be used.

Trend risks require users to consider temporality and

identify both short-term signals and long-term impacts.

The latter are likely to be less noticeable than short-

term events and are dicult to align with organisational

decision making, which tends to focus on much shorter

future outlooks; as a result, it can be more dicult to

incentivise mitigation measures for long-term threats.

If eective action is taken, there is the benet of having

enough time to determine the best method to mitigate or

alleviate the risk. Trend risks are typically not insurable

yet are a topic of increasing interest within the insurance

sector, for example, as seen in the corporate uptake of an

Environmental, Social, and Governance (ESG) agenda,

and in response to growing awareness of the increasingly

pronounced impacts of climate change. Insurers are

increasingly needing to make decisions on how to

address trend risks, whether it be through an adaptive

process to keep losses within an insurable window, or

the discontinuation of certain insurance policies. To best

support these decisions, trend risk scenarios remain an

important component of scenario analysis, regardless of

whether the risk is currently insured.

In contrast to trend risks, shock risks are sudden events

which may not have been anticipated and trigger impacts

that materialise rapidly. The focus of these scenarios is

The Origin of Trend Scenarios

Trend risk scenarios have historically been used

within operational or strategic planning and have

roots in policy and operational settings. The Cold

War futurist, Herman Kahn, and others at RAND

Corporation, are regarded as among the founders of

the construction and use of scenarios in the 1950s

and 1960s, primarily in the security arena (e.g., how

a country would function after a nuclear conict),

and encouraged the philosophy of how to ‘think the

unthinkable’.

8

He described a scenario as:

“a set of hypothetical events set in the future

constructed to clarify a possible chain of causal

events as well as their decision points”.

9

Other notable research was being

undertaken at the time by the

Stanford Research Institute,

who oered long-range planning

facilities to support their military

and business consulting. They were

among the rst to formalise and

utilise scenario planning techniques

for decision making by businesses

and governments.

Kahn’s scenario methodology

used mathematical models and

forecasting techniques and set a

precedent for the future of scenario planning.

10

In

the 1970s, this methodology was adapted by Pierre

Wack’s newly formed Planning Scenario team at

the Royal Dutch Shell Group for use in a corporate

setting, primarily to anticipate developments in the

volatile oil and gas markets. ‘Shell’ scenarios were

notable for their trend risk analysis and strategic

planning purposes, and followed seven broad steps

11

:

1

Decide drivers for change/assumptions

2

Bring drivers together into a viable framework

3

Produce seven to nine initial mini scenarios

4

Narrow down two to three scenarios

5

Draft the scenarios

6

Identify the issues arising

The value of Shell’s futuristic

approach was rst realised in the

1973 Arab–Israeli (Yom Kippur)

War, when the rst oil embargo

caught most companies by surprise.

Shell had considered and strategized

for the implications of an oil price

shock, and thus overcame the worst

shocks, and emerged from the crisis

as the sector leader.

Image 1: Herman Kahn of RAND Corporation

(National Archives, 1963)

8. (Kahn 1961) 9. (Amer, Daim, and Jetter 2013)

10. (Durance and Godet 2010) 11. (Jeerson 2012)

10

Scenario Best Practices: Developing Scenarios for the Insurance Industry

to identify events which might “shock” the system and

have a valuable role in tactical planning. The impact of

such scenarios is likely to be acute, rather than accruing

slowly as in the case of trend risks, and they are more

commonly hedged by conventional insurance products.

The impacts associated with a shock event will demand

an immediate response from the insurance community.

The focus of this report is on shock risk scenarios, which

have a wider variety of typologies and methodologies

specic to the insurance industry. The dialogue within

the report is written from a stress test perspective yet is

often applicable in trend risk discourses.

Although stress test scenarios in the form of shocks have

been used by the insurance industry for decades, their

use via modelled catastrophe theory was precipitated

in the insurance industry following Hurricane Andrew

in 1992. At the time, Hurricane Andrew was the most

expensive insured event recorded, and triggered over $16

billion in losses.

12

The nancial impacts caused eleven

insurers to go out of business in the state of Florida and

caused heavy strain on the global insurance community.

13

In the following years, the insurance focused credit

agency, A.M. Best, required American insurers to report

their modelled losses. Lloyd’s of London similarly

introduced their realistic disaster scenarios (RDS)

in 1995 (see Section 5 for an example RDS, Business

Blackout, used as a model case study for scenario

development). The intention of these scenarios was to

provide a communal exercise for insurance organisations

to stress their portfolios and identify any potential

weaknesses which do not meet regulatory thresholds.

The application of stress tests quickly evolved beyond

regulatory purposes and has become a valuable tool in

risk exploration and response planning.

Exploratory Versus Normative

An important distinction concerns the purpose of

scenario development. Scenarios range on a continuum

between exploratory, with the purpose of educating and

expanding awareness of plausible futures, to normative,

with a primary aim to facilitate decision making. Often,

the goal is to concurrently balance exploratory and

decision-based functions.

Exploratory eorts ask, ‘what if?’, as a helpful way to

create a ‘future memory’.

14

This approach explores a wide

and contrasting range of potentially plausible futures

as a function of diverging assumptions (in other words

questioning ‘what would happen if this happens?’), with

the aim of widening the scope of options considered by

users and stimulating imagination and creative thinking

about the future. The focus here is on learning about the

process under analysis, raising awareness, developing

a descriptive assessment of plausible futures, and

taking a specied issue or environment as the subject of

analysis.

15

Exploratory scenarios often apply a forecasting

approach, dening scenarios on the basis of a set of

imposed rules dened from the base year onwards.

16

In contrast, normative scenarios primarily ask, ‘what

for?’. To utilise such a scenario for decision making,

a more narrowly dened set of criteria and objectives

must be explicitly dened.

17

A normative approach

typically uses scenarios that are formulated in technical,

quantitative terms (and thus have less emphasis on

narrative) so that the paths to desirable, or undesirable,

futures can be analysed. The intention is to evaluate

the impact of a set of variants concerning specic

interventions (behaviours and decisions) relative to a

baseline, based on some form of valuation.

18

Such eorts

tend to focus on delivering a product, in the form of a

specic alternative to address a problem, or an advising

tool for evaluating alternatives.

19

A normative approach

can be more easily combined with a backcasting

approach (as opposed to forecasting), dening scenario

pathways only after rst describing the end-points and

reasons back from these end-points, and exploring short-

term decisions to make these changes happen.

20

12. (Grant 2015) 13. (Grant 2015) 14. (Tourki, Keisler, and Linkov 2013)

15. (Riddell et al. 2018; Tourki, Keisler, and Linkov 2013) 16. (Van Vuuren et al. 2012)

17. (Birkmann et al. 2015) 18. (Henrichs et al. 2010; Tourki, Keisler, and Linkov 2013)

19. (Tourki, Keisler, and Linkov 2013) 20. (Robinson 1990; Dreborg 1996)

11

Cambridge Centre for Risk Studies

Participatory Versus Expert-Driven

Another divergence in scenario design concerns who

‘owns’ the process, with a key distinction made between

top-down, expert-driven (or ‘analytical’) approaches

and bottom-up, participatory approaches. Both have

advantages and disadvantages, and each may serve

dierent purposes, although they are not necessarily

discrete, with eective scenarios often including

elements of both. We emphasise the importance

of participation in the scenario process, since this

dimension is often undervalued or excluded in insurance

applications of scenarios.

Expert-driven approaches have the objective of providing

rigorous descriptions of plausible futures, including

details that are well supported by available science.

21

Such approaches are oriented towards decision makers,

and as a result tend to neglect other stakeholders. They

are analytical in approach and allow for exploration

of large-scale phenomena, for example global climate

change, which may pose logistical diculties to

participatory approaches.

In a participatory approach, scenario developers

work together with stakeholders, namely the people

potentially aected by scenario outcomes, rather than

delivering scenarios as a top-down means of education.

Participation targets and integrates stakeholder needs

and values, and while scientic and technical knowledge

remains important, such approaches makes use of

cultural perspectives, knowledge, and experience beyond

the involved experts to dissect complex issues. No group

knows everything, and each will learn from others

through the scenarios, providing everyone is represented

in the discussion. Eective communication of scenario

information is much easier than accurate communication

of technical information (such as probabilistic risk). Such

diverse engagement is eective in developing community

understanding and investment in decision making,

builds trust, and encourages broader acceptance of the

ultimate scenario outcomes.

22

Participatory approaches

enable scenario developers to understand, examine, and

discuss the links between phenomena at dierent scales

– for example how global or sub-national trends relate to

the vulnerability in specic regions or municipalities.

23

Scientic and technological developments have driven an

increasing role of technology and expertise in scenario

approaches but demands for improved participation and

accountability; and criticism of technical expertise, have

also grown. Within the insurance industry scenarios

are generally expert-driven, although there has been a

recent eort to better involve stakeholders. Examples

include community partnerships and local risk planning

initiatives, or the rise of social impact bonds.

24

Further distinctions can be made, aligning with

exploratory or normative, and participatory or expert-

driven approaches, as follows:

Intuitive versus formal processes

Process design refers to how scenarios are developed,

or their methodological aspects, ranging from

intuitive to formal approaches. Intuitive processes

focus on qualitative knowledge and are participatory,

incorporating many perspectives from a wide range of

backgrounds and knowledge bases.

25

In contrast, formal

processes regard scenario development as an analytical

and systematic exercise, and so depend on quantitative

inputs to build conceptual or computational models.

They are exclusive in the way they only incorporate views

from specic stakeholders or areas of expertise.

26

Process versus product orientation

The scenario development process can be at least as

important for the user as the product, for example if

a scenario is intended to support a specic decision.

A process-oriented scenario includes the user in

development, so that they may learn from the experience

and feedback to enhance scenario ecacy. However,

in many contexts, scenarios are instead communicated

in a linear process, with an end product deliverable

such as a report and or a quantication of loss. In this

case the product is typically more important than the

process, with the potential advantage of reaching a target

audience beyond those participating in the process. If

this is the case, quality, transparency, and legitimacy

need to be emphasised in order to ensure scenarios are

relevant to the user community and can be readily used

for planning and decision making.

27

Qualitative versus quantitative

The distinction between qualitative and quantitative

information is clear in scenario development, but the

contrasting methods may be, and perhaps should

be, combined. Qualitative information, specically

narratives, provide logic to scenario assumptions and

help to dene plausible future developments in situations

where formal modelling is not possible. They provide

an eective way to derive information at dierent scales

or for dierent topics (for example regional scenarios

nested within global narratives). Quantication, via

modelling, adds scientic rigour to scenarios, expanding

on numerical estimates of futures developments (often

based on simulation tools) where relevant and reliable

information is available. Quantitative outputs can

strengthen communication through clear denitions

and rules.

28

21. (Star et al. 2016) 22. (Star et al. 2016) 23. (Birkmann et al. 2015)

24. For more information on social impact bonds see (Social Finance Inc. 2012)

25. (Van Notten et al. 2003; Tourki, Keisler, and Linkov 2013)

26. (Tourki, Keisler, and Linkov 2013) 27. (Van Vuuren et al. 2012) 28. (Henrichs et al. 2010)

12

Scenario Best Practices: Developing Scenarios for the Insurance Industry

Deterministic Versus Probabilistic

Scenarios are also characterised as either deterministic

or probabilistic. A deterministic scenario is created by

selecting a specic set of parameters and conditions,

while a probabilistic scenario considers a multiplicity of

outcomes, each with its own probability of occurrence,

depending on the probability distribution of the input

parameters and conditions.

29

A deterministic scenario

treats the probability of occurrence as nite, whereas

probabilistic modelling is intended to address the

uncertainty with a ‘complete’ probability distribution of

synthesised events.

Deterministic scenarios are recognisable by their focus

on the causal chain of circumstances that will give rise

to unusual or extreme outcomes. They are an eective

means of exploring phenomena speculatively or

hypothetically when they are not very well understood

or there is a high degree of uncertainty. They can also be

very valuable for exploring emerging risks, specically

where market or policy responses are uncertain.

In comparison, production of a probabilistic scenario is

possible when the underlying process is well understood,

and the causal parameters can be characterised with

estimates of their occurrence rates and distribution.

Each step in the causal chain has a dened distribution

of outcome likelihoods, and the model stochastically

samples from this distribution in many simulations. The

probability of an outcome and its uncertainty structure

is very sensitive to the assumptions made for the input

parameters.

30

By incorporating random variations into

the model, stochastic outcomes show a range of scenario

outcomes, and the likelihood of these permutations.

Techniques for probabilistic modelling are well

understood and documented, and are used in analysis,

such as natural catastrophe modelling, where the

subject phenomena have been comprehensively studied

and for which it is possible to estimate the uncertainty

distributions of the underlying variables.

There is overlap in deterministic and probabilistic

scenarios. For example, probabilistic modelling

can be used to generate a deterministic scenario,

typically such as the worst, best, or most likely case

events. Caution should be taken when comparing

the two types, as probabilistic scenarios still contain

deterministic attributes. Specically, probabilistic

scenarios require all potential outcomes to be dened,

yet in practice the universe is not a closed system.

There are outcomes of future probabilistic scenarios

which cannot be recognised at present; thus, it is not

possible to achieve a perfect probability estimation. Both

deterministic and probabilistic scenarios are used by the

insurance community.

Probability theory is critical in the industry, where

the likelihood of future events is required to develop

a policy or price a premium. This is true even where

signicant uncertainty exists, and it is in this case where

deterministic scenarios can be particularly important

to address uncertainty, providing reference points on

a journey towards probability. It is also important to

note that probabilistic scenarios are only useful when

understood, and where decision makers are not familiar

with the theory, it may be unhelpful or even misleading.

For example, return periods, or recurrence intervals,

are standard calculations for describing the magnitude

of potential events – such as a 1-in-100-year ood – but

are prone to misconceptions and misuses that are well

acknowledged but still widespread.

31

In cases where

communicating scenarios to non-experts is required, it

may be that probability should not be depended on, and

a deterministic approach could have greater value.

29. (Renard, Alcolea, and Ginsbourger 2013) 30. (Lorenz 1963) 31. (Serinaldi 2015)

13

Cambridge Centre for Risk Studies

14

Scenario Best Practices: Developing Scenarios for the Insurance Industry

3. Using Scenarios in the Insurance Industry

This section documents the various roles that scenarios play within the insurance industry and

explores who is using, or could better use, scenarios. The application of scenarios can be broadly

categorised into universal uses of scenarios, and those specic to the insurance industry.

3.1 General Scenario Uses

The action of developing a scenario carries a series of benets, some of which are simply a consequence of

the scenario building process. We highlight a series of outcomes that were often cited by insurance industry

representatives whose comments informed the development of this report, and were notably consistent,

regardless of a scenario’s intended use or application. These are individually discussed below.

Supporting Decision Making

Scenarios can be highly eective tools in support of

decision making, oering a creative and structured

mechanism to test and validate decisions in a scenario

planning process. When managers make decisions about

the future, concerning either near-term operations or long-

term strategy, they cannot only expect positive outlooks,

and must also be proactive in preparing for negative

events. This proactive outlook is a key characteristic of

enterprise risk management, contrasting with the typically

reactive approach of traditional risk management.

Scenarios facilitate discussion on how risks can be planned

for and be managed or mitigated eectively with robust

decisions and strategies. Further, decision makers must

factor in the associated risks on the belief of a certain set of

assumptions, the validity of which scenarios test.

Aiding Communication

Scenarios routinely function as a communication tool in

the industry, facilitating the sharing of ideas, risks, or

responses. Communication may occur formally during

the distribution process, or more informally during

the development and research phase. Scenarios are

especially valuable when discussing abstract ideas, or

complex risks, as they provide examples and context

to the issue, ensuring a consistent interpretation and

understanding. Furthermore, by providing a well-crafted

scenario which is mutually accessible to multiple parties,

consumers of the scenario have an equal platform

for communication across dierent sectors or areas

of expertise.

Demonstrating Due Diligence

The insurance industry is required to practice due

diligence to keep themselves and their insureds safe.

One component of due diligence is recognising what

risks exist, and where vulnerabilities exist within the

organisation. Scenarios assist in achieving this due

diligence, as they provide a systemic and comparable

platform for examining these risks, and a sheltered

sandbox to identify and test potential vulnerabilities.

These exercises can aid in answering questions such

as what silent exposure may exist, or if there is clash

potential on existing policies. By addressing areas

of uncertainty and taking informed risks, insurers

can demonstrate that potential consequences have

been considered and reasonable precautions have

been taken.

Identifying Bias

Scenarios provide a platform to explore hypothetical

outcomes and identify potential (dis)inclinations or

partialities that organisations have towards certain

situations and decisions. Taking a broad set of

scenarios mitigates well known behavioural eects like

conrmation and availability biases. Such an approach

also allows for alternative responses to be compared

to a baseline. By setting these processes up in advance,

insurers can be mindful of these issues and take

proactive measures to ensure that the decision-making

process remains objective. This yields a systemic benet

that is realised over time.

15

Cambridge Centre for Risk Studies

Scenarios to Support Robust Decision Making

Deep Uncertainty

Deep uncertainty exists when decision makers do

not know, or cannot agree on, a system in question

and its boundaries, the probabilities of model inputs,

or the consequences of interest and their relative

importance.

32

Such uncertainties persist for many drivers of global

change, including environmental, economic, or

technological developments. Societal perspectives

and preferences also change over time, including

stakeholders’ interests and their evaluation of

plans. As the future unfolds, plans are adapted to

developments, so decisions are part of the storyline

and an essential component of uncertainty.

33

Innovative analytical approaches

34

of ‘decision

making under deep uncertainty’ are emerging to

cope with uncertainty, and to help decision makers

evaluate robust and adaptive management strategies.

They help to build a consensus between stakeholders

with dierent values, priorities, and solutions, who

can agree on a decision for very dierent reasons.

35

The process reveals future threats, as well as

opportunities, confronting each plan. This paradigm

relies on exploratory modelling, typically involving

scenario approaches that harness speculation and

imagination to consider ‘unknown unknowns’.

36

Robust Decision Making

Robust decision making (RDM)

37

is one example of

a dened approach for analysing deep uncertainty,

which uses iterative, model-based scenario analysis.

The RDM methodology helps decision makers to

identify and improve robust strategies by testing

them against a very large exploratory scenario set

(of hundreds of possible futures) to reveal their

strengths and limitations. Statistical analyses of

model iterations identify the key conditions under

which strategies fail to satisfy their objectives. RDM

also has a participatory component, with stakeholder

deliberation used to dene (un)desirable outcomes,

and to rule out implausible scenarios.

38

Robust strategies will satisfy decision makers’

objectives in many scenarios, rather than being

optimal in any single future.

39

In other words, they

are ‘good enough’, rather than optimal options,

aiming to minimise regret rather than maximise

expected utility. RDM also helps to compare

strategies along other dimensions such as cost,

feasibility, and social acceptability.

40

RDM has been widely applied to explore where

deep uncertainty exists, including in the domains of

climate change

41

, risk and resource management

42

,

and insurance specic applications, for example the

feasibility of terrorism insurance

43

. An important

consideration of RDM is that it requires large

amounts of quantitative information and a high

degree of expert knowledge.

32.(Kwakkel, Walker, and Haasnoot 2016; Hallegatte et al. 2012) 33.(Haasnoot et al. 2013) 34.See (Haasnoot et al. 2013; Kwakkel, Walker, and

Haasnoot 2016) for discussions of various approaches to support decision making under deep uncertainty 35.(Tuck 2016) 36.(Olabisi 2017)

37.See (RAND Corporation 2019) for detailed use cases 38.(Olabisi 2017) 39.(Rozenberg et al. 2017) 40.(Rozenberg et al. 2017; Lempert et al.

2013) 41.(Lempert, Popper, and Bankes 2003; Lempert and Kalra 2011) 42.e.g. (Sayers, Galloway, and Hall 2012; Beven and Alcock 2012; Popper

et al. 2009) 43.(Lempert et al. 2013) 44.(Roxburgh 2009)

Sensitivity Analysis

Insurers are required to make assumptions and

estimates daily, considering many dierent variables and

evaluating their potential interaction with one another,

towards making a cost-benet analysis. Scenarios can

assist in this process, as they allow users a sheltered

environment to explore uncertainties and investigate

alternative futures which may arise, incorporating a

greater appreciation of the direct and indirect impacts of

their decision choices today.

Addressing Uncertainty

Scenarios expand understanding of a range of plausible

outcomes, each supported by a dening sequence of

events. Humans inherently expect that change will

occur gradually and that the future will reect the

past. By generating deeper insight into the underlying

drivers of change, scenarios may demonstrate how

and why changes could develop quickly and otherwise

unexpectedly, and which drivers do or do not have the

ability to cause consequential change.

44

16

Scenario Best Practices: Developing Scenarios for the Insurance Industry

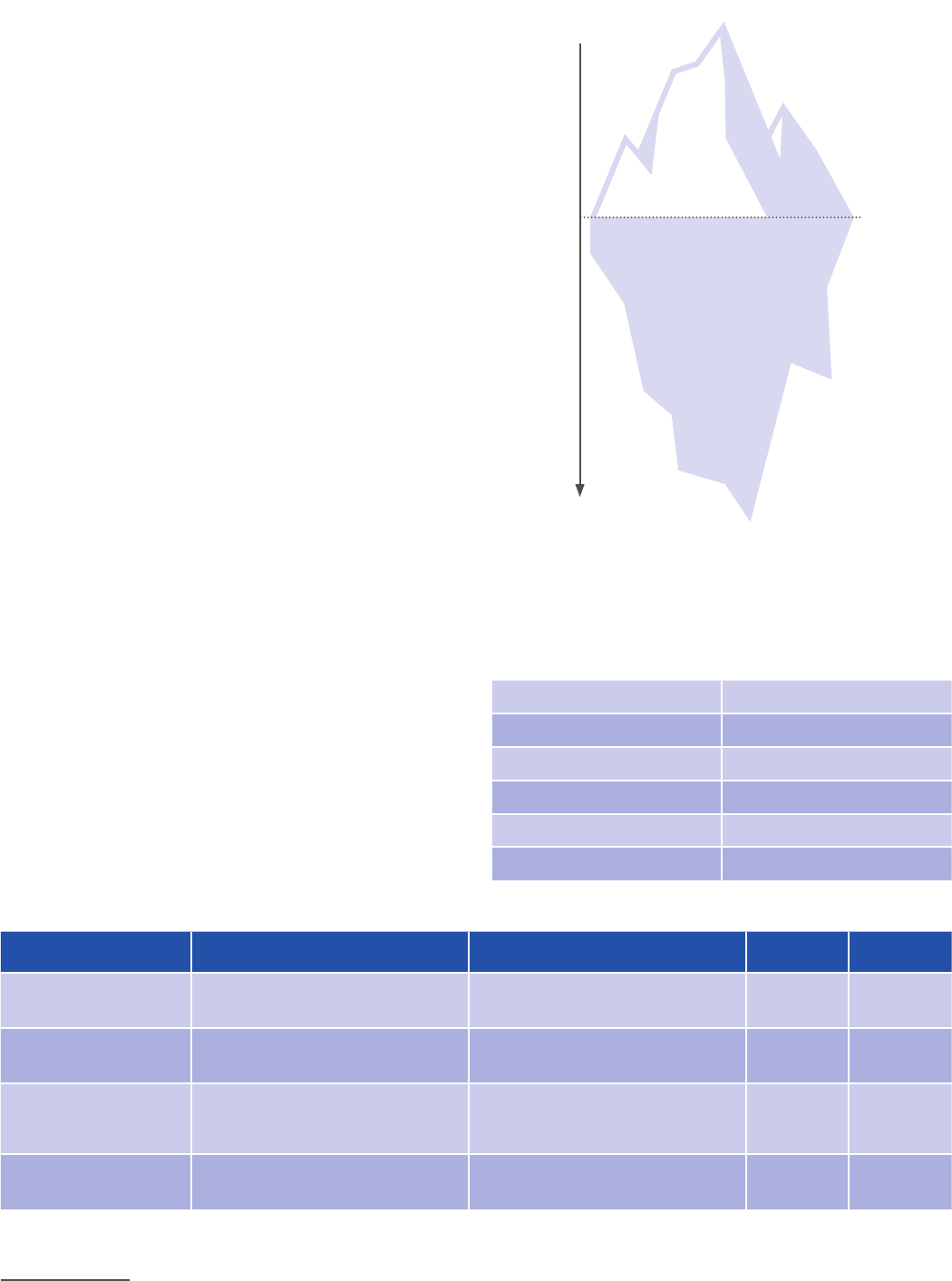

Systems Thinking

The capability to capture interconnectivities between

complex systems, or ‘system of systems’, is critical

to scenario planning. Systems thinking is a holistic

approach to address complex interconnections and causal

relationships, rather than on snapshots and independent

aspects, of a problem. Given the abundance of resources

on this topic, only a brief overview is provided here, with

an emphasis on the importance of wholly understanding

systems when using scenarios. The approach exposes

that which is not immediately obvious, providing a lens

to detect underlying controlling forces and relationships

between individual components, to understand the entirety

of a system. The iceberg analogy

45

(Figure 3) is a useful

way to illustrate systems thinking and enable practitioners

to appreciate the deeper perspective. As humans, we

typically notice events in the world around us (the ‘tip’ of

the iceberg) in a reactive and counteractive mode, only

seeing a small part of the underlying dynamics. Only when

we look below the (water) surface for patterns of behaviour

can the event be better understood with scenarios that

explore how interconnectivities may control the future.

Delving further into understanding these dynamics at a

structural level enables exploration of the structural level

of various risks facing an organisation.

46

3.2 Insurance Use Cases of Scenarios

In addition to the generic benets that scenarios provide

during the development and decision-making process,

scenarios have specic and unique benets to the variety

of users within the insurance industry (Table 1). This

report proposes that the insurance applications can

be categorised into four use cases. These uses overlap

and share common traits and should be recognised

as interconnected components. These use categories

are summarised in Table 2, and are described on the

next page.

(Enterprise) Risk Managers Regulators

Accumulation Controllers Claims Managers

Underwriters Risk Capital Controllers

Pricing Actuaries Business Planners

Advisors Investment Manager

Transaction Intermediaries Product Designers

Table 1: Example scenario users within the insurance industry

Use Category Description Example Uses Trend Shock

Understanding Tail Risk Identify extreme, low probability risks Reinsurance purchasing,

counterfactualanalysis

✓ ✓

Understanding

EmergingRisk

Identify new and undened risks and

policies

Understanding policy wording, trialling a

concept, problem verication

✓ ✓

Strategic Planning Identify risks and opportunities for

anorganisation

Short-term and long-term planning,

particularly with regard to strategic

response to opportunities or threats

✓

Accumulation Management Identify maximal potential losses and

potential for risks to scale

Probable maximum loss (PML)

identication, clashscenarios

✓

Table 2: Uses of scenarios within the insurance industry

Figure 3: Systems thinking – the iceberg analogy

(adapted from Senge, 1990; Van der Merwe, 2008)

Events

Patterns of Behaviour

Structure of

the system

Casual relationships,

driving forces,

assumptions

Increasing ability to inuence and learn

45. (Kauman 1980) 46. (Van der Merwe 2008)

17

Cambridge Centre for Risk Studies

Understanding Tail Risk

Within the insurance industry, a tail risk refers to an

extreme and highly unlikely event which has signicant and

often immediate consequences. The term ’tail’ originates

from statistics – for example, if outcomes are distributed

according to a standard bell curve (normal distribution),

then outcomes that are more than three standard deviations

below or above the expected outcome (the mean) only occur

in 0.3% of cases – these are the tails of the distribution.

These extremes, with either positive or negative impacts,

are, by denition, highly improbable and dicult to predict.

Within the insurance industry, the focus is typically on

the severe negative impacts that result in losses, although

recognising the improbable positive outcomes also are

of interest. As the exercise is hypothetical, variables can

be adapted and controlled to explore dierent potential

outcomes and their consequences. These scenarios assist in

answering the hypothetical question “what if?” and provide

a reference point to build from. As events unfold and the

probability distribution of a risk evolves, the denition of a

tail risk may also change.

Understanding Emerging Risks

An emerging risk is a new risk, changing risk, or novel

combination of risks for which the broad impacts, costs and

optimal management strategies are not yet well understood.

Emerging risks are driving an increase in insurance

exposure. Emerging risks oer opportunities for new

products in the market but are also a potential threat to

capital adequacy. Understanding the breadth of the risk and

its potential consequences can allow insurers to embrace

emerging risks and limit unintended exposure. Scenarios

are a tool in exploring these risks, as they provide a

platform to develop hypothetical events and consequences.

As emerging risks are fundamentally uncertain, scenarios

allow exploration of hypothetical events through which

these uncertainties can be stressed. This provides a gauge

of the potential hazard severity or scale, and what limits or

precautions should be taken at the time. When a specic

outcome has not occurred in reality, scenarios can be used

to see what pay-outs may be triggered, and how dierent

policies may be interrupted should such a risk emerge.

Strategic Planning

Strategic planning is the process by which an organisation

denes its strategy for the future, with consideration of

trend risks which have the potential to threaten strategic

goals. This can range from determining resources and areas

of investment, to setting priorities and targets. Specically,

scenarios are often used as they allow users to identify and

adjust factors which may impact these goals. Scenarios can

be used to project what may occur in the short- and long-

terms if conditions remain consistent, but also estimate

how the future might vary with various internal and

external inuences. Scenarios fundamentally support the

needs of communication across dierent stakeholders and

areas of expertise and provide a communal platform for

discussion and problem solving. When considering strategic

planning, members of an organisation can contribute to

scenario building, creating a holistic planning process.

While, as previously discussed, trend risks are typically

not insured via the current range of insurance products,

insurers are increasingly being called on to address

trend risks. Therefore, strategic planning should not

only be considered as relevant to an insurer’s internal

risk management, but also as an opportunity for insurers

to address trend risks that threaten the strategies of

organisations that serve the industry with business.

18

Scenario Best Practices: Developing Scenarios for the Insurance Industry

Cyber Terrorism: AnEmerging Risk

Cyber terrorism has remained one of the most

notable emerging risks within the insurance industry

and continues to build its reputation as a potential

cyber insurance game-changer. Cyber terrorism

is dened by the Federal Bureau of Investigations

as: ‘any remediated, politically motivated attack

against information, computer systems or computer

programs, and data which results in violence against

non-combatant targets by sub-national groups or

clandestine agents’.

47

Cyber security professionals, governments, and law

enforcement are becoming increasingly concerned

with the potential for traditional terrorism groups

to exploit the cyber landscape to cause physical

destruction and human injury.

48

Insurers have

been reluctant to oer coverage for cyber terrorism

in their insurance products due to signicant

uncertainties surrounding the probability and

severity of cyber terrorism events. In a recent review

of 26 cyber armative policies, only 12% of cyber

insurance products oered terrorism coverage

in 2016.

49

The ambiguity around the process of

attribution of cyber attacks to terrorist actors has

also compounded this uncertainty.

50

Scenarios have played a key role in the developing

the market for cyber terrorism coverage by

quantifying the potential exposure (particularly silent

exposure) insurers could face when a cyber terrorist

event occurs. Research commissioned by Pool Re, the

UK’s mutual terrorism reinsurance pool with the UK

Government, highlighted realistic cyber terrorism

scenarios that could result in signicant physical

damage and thus trigger silent exposure in property

lines. In response to the identication and estimated

quantication of this cyber terrorism insurance

gap, Pool Re have expanded their terrorism product

coverage to include explicit cover for property

damage and the resulting business interruption

caused by cyber terrorism.

51

Accumulation Management

Accumulation management, also described as

aggregation risk management, considers what risks exist

within a portfolio of insurance policies for large numbers

of claims to arise from the same underlying cause or

event. Scenarios of the events that could cause large

numbers of simultaneous, correlated losses identify the

potential systemic attributes that policy holders might

share. This allows insurers to test the loss potential for

their specic portfolio to those extreme losses. They also

enable the exploration of hypotheses of how the risk

might scale or increase in magnitude if a variable were

to change. By estimating how large an event might be

and how likely it is to occur, an insurer can eectively

protect their exposure through limits and exclusions. A

use of the scenario might be to help insurers design their

terms and conditions, product design, and the limits and

deductibles they might oer to protect themselves from

taking large systemic losses.

Similarly, in identifying what the maximum loss for

insurers might be, exposure limits can be introduced to

limit what is insured, or what inclusions and exclusions

are considered. This type of scenario is referred to as the

Probable Maximum Loss (PML) and is often required

when deciding a risk appetite or tolerance of loss for a

line of insurance business and can be used to regulate

the amount of new business that is underwritten in

the future.

Scenarios play a valuable role when discussing

accumulation and maximum loss, as they provide a trial

ground to explore what types of events would cause

broad impacts, especially across multiple portfolios,

or classes of insurance. They are also helpful when

considering limits and exclusions, as insurers can trial

what amount of risk they feel comfortable accepting, in a

controlled environment.

47. (Alford 2017) 48. (Broadhurst et al. 2017)

49. (Risk Management Solutions Inc, in collaboration with Cambridge Centre for Risk Studies 2016)

50. (Evan et al. 2017) 51. (Insurance Journal 2018)

19

Cambridge Centre for Risk Studies

3.3 Allocating Risk Capital

Capital modelling is used when deciding how much

capital should be priced and reserved to cover potential

risks.

52

The role of capital allocation modelling in the

insurance industry is typically focused on ensuring

capital requirements for regulatory purposes are met,

without signicantly impacting daily underwriting

decisions.

53

This is a method known as ‘Regulatory Risk

Based Capital’. Under Solvency II pillar one, insurers are

obligated to meet the Minimum Capital Requirement and

Solvency Capital Requirement.

54

To meet these requirements, insurers can either use

a ‘one size ts all’ prescriptive model provided by the

regulator, which uses a standard formula, or else develop

an internal capital model (ICM).

55

The use of partial or

fully internal capital models goes beyond the scope of

regulatory compliance by providing greater insight into

a company’s risk prole and is essential for navigating

towards ecient capital allocation.

56

To validate a modelling process of capital allocation,

insurers often develop scenarios to assess the resilience

of these capital reserves to shock and trend risks.

Scenario modelling is used to validate insurers decisions

on the allocation of capital across lines of insurance by

estimating their exposure to a disaster scenario.

Using clash aggregation modelling techniques, insurers

can test their capital allocation reserves based on

a disaster scenario that impacts multiple lines of

insurance. Clash modelling allows insurers to better

understand their potential losses across multiple

lines of business and develops a narrative for capital

requirements necessary to cover these losses.

Solvency II

In 2009, the European Union Insurance and

Occupational Pensions Authority (EIOPA),

57

a

nancial regulator body of the European Union,

introduced the EU Solvency II Directive. The

directive aims to homogenise EU insurance

regulation and focuses on an enterprise risk

management approach towards required capital

standards.

58

Solvency II is primarily concerned with

the level of capital reserves insurance companies

should hold to reduce the risks of insolvency.

59

This

legalisation was driven by the events of 2008, when

the Financial Crisis and subsequent Great recession

highlighted the necessity for insurance companies to

manage their capital allocation to remain solvent. To

ensure the solvency of EU insurance companies, the

Solvency II program has three main areas, known

as ‘pillars’:

Pillar 1: Financial Requirements

Pillar 2: Governance and supervision

Pillar 3: Reporting and Disclosure

Pillar 1, known as the ‘quantitative pillar’, puts

demands on the required economic capital that

insurance companies must hold.

60

The pillar

stipulates two thresholds that insurance companies

must adhere too: Solvency Capital Requirement

(SCR) and Minimum Capital Requirement (MCR).

The SCR requires insurers to estimate the level of

capital needed to meet quantiable risks on their

existing portfolios, including one year’s expected

new business.

61

MCR is the lower bound of the SCR

and is the level of capital in which regulators would

consider the insurer to be in signicant danger of

insolvency. The MCR is calibrated in the Solvency II

regulations as 85% value-at-risk over one year from

valuation date.

62

Pillar 2 is known as the ‘qualitative pillar’ which

sets out clear requirements regarding how the

quantitative objectives of pillar 1 should be achieved.

The pillar requires companies to design eective

systems of governance which are proportionate to

the nature, complexity and scale of operations.

63

An

insurer must have written internal policies in relation

to risk management systems and internal controls of

the organisation. Under the Own Risk and Solvency

Assessment (ORSA) area Solvency II, insurers must

action a signicant self-assessment of the risk they

are exposed to in the short and medium run.

64

ORSA

aims to go beyond the modelling requirements in

pillar 1 and for the insurer to think about additional

risks the insurer may be exposed to.

Pillar 3 outlines the reporting requirements of

company’s risk with respect to which information

should be disclosed such as risk exposure and

concentration, and the frequency with which this

information should be reported.

65

52.(Cummins 2000) 53.(GIRO Working Party 2016) 54.(Vandenabeele 2014) 55.(Krvavych 2018) 56.(Boonen 2017)

57.Formerly known as the Committee of European Insurance and Occupational Pensions Supervisors 58.( Vandenabeele 2014)

59.(House of Commons Treasury Committee 2018) 60.(Boonen 2017) 61.(Lloyd’s of London n.d.) 62.(Vandenabeele 2014)

63.(Financial Services Commission 2009) 64.(House of Commons Treasury Committee 2018) 65.(Vandenabeele 2014)

20

Scenario Best Practices: Developing Scenarios for the Insurance Industry

21

Cambridge Centre for Risk Studies

4. Shock Risk Scenario Development:

InsuranceStress Testing

There are many types of scenarios which have been developed by the insurance industry, for particular

applications and with diering development methods. During the literature review and consultation

process for this report, a wide variety of techniques and development processes were identied

in surveys of insurers and stakeholders. There is no standardised approach, consensus, or single

proto-typical method in use. Instead, there are common features across multiple methodologies.

In this section we focus on the underlying similarities and propose a series of checkpoints to ensure

developed scenarios can be applied widely and meet the needs of the broader insurance community.

4.1 A Checklist for Scenarios

The rst checkpoint in the scenario development

process is identifying who the scenario users are,

and how they hope the scenario will be used in the

future. Within the insurance community there are an

abundance of potential users with individual needs

and criteria for a scenario. The best way to gauge these

needs is by talking with the intended audience or users

and taking the time to understand what they hope a

scenario to achieve. Supporting the direct feedback from

future users, scenario developers should also reect on

the following:

Background Knowledge refers to the existing

familiarity that users have with the subject. This is

an indicator for the type of narrative and level of

description that should be provided. If the scenario

is proposing an event that is novel to the user, the

scenario and its associated documentation should

provide additional resources regarding the current

risk landscape and use additional description when

suggesting cascading impacts. Comparatively, if the

user is very familiar with the proposed risk event, the

scenario can address a dierent level of detail and

specication. The terminology and language used

to describe the risk should also be adapted based

on the familiarity of the end user with the subject

matter. As a standard practice, the scenario should

include enough research and reference material so

that it remains widely accessible, regardless of the key

audience’s familiarity.

User Resource is the amount of time and human capital

that the user can be expected to dedicate to read and

interpret the scenario. The resource allowance should dictate

the length and detail of a scenario. Should the scenario be

intended for a user interested in new and emerging risks

over a long-term period, more resources may be allocated to

reviewing an extensive report and background material. If,

for example, the user is focused on the clash risk of a specic

area, there may be a greater urgency to understand potential

outcomes and losses, and so fewer resources would be

available to review an extensive report.

Existing Guidelines refer to the rules and regulations

that may have been put in place by the user regarding the

scenario’s development and presentation. This is most

commonly seen in the case of regulators and authorising

bodies, who are required to review and compare large

numbers of scenarios in a short period of time. Prior to

the development of the scenario, one should check to

ensure that available guidelines required by the user are

reected. These guidelines might include the types of

scenarios required, the number of variants included, and

the loss estimation process.

Audience refers to how the user intends to share the

material, and whether it will remain as an internal

resource, or be published externally for public use. Public

scenarios will require signicantly more documentation

and reference material than those for internal use, to

mitigate potential ambiguity.

22

Scenario Best Practices: Developing Scenarios for the Insurance Industry

4.2 Scenario Development: a Stress Test Perspective

The next several checkpoints in scenario development

relate to its construction. The intention of the report is to

provide an accessible resource and guide for developing

scenarios, but the process is varied and often attuned

to the specic needs and interests of stakeholders.

Accordingly, the steps discussed below are recommended

checkpoints to consider as a practitioner works through

the scenario process. Users should adapt the methodology

to create scenarios which work best for them, given their

audience, resources, and desired use. Further, while it

outlines a linear step-by-step structure for clarity, we

encourage the scenario process to be an iterative one, in

which stakeholder engagement provides opportunities

for review and revision to ensure it succeeds in fullling

its aims.

A case study of a worked example of scenario development

using this framework is provided in Section 5, based on

the 2015 Lloyd’s Business Blackout Report

66

, originally

developed to address emerging cyber risk within the

insurance industry.

There are various types of scenarios which can be used

within the insurance industry (Section 2.2). This section

focuses specically on stress test scenarios, which are

among the most widely used scenario types and carry the

greatest potential for external agency development. Many

of the recommendations made for stress test scenarios are

broadly applicable to other forms of scenario development.

A stress test is an exercise conducted within the insurance

and nance community to explore an organisation’s limits

and dene the magnitude of event that would ‘stress’ the

institution. This is often measured in terms of nancial

capital, with stress tests imagining extremely expensive

events leading to an inux of insurance claims or nancial

losses. Stress tests often focus on rare and extreme events

(tail risks) which result in a dramatic impact.

Within the insurance industry, stress tests are a common

requirement for external regulation and internal planning

and are a recognised means of evaluating the robustness

of an institution, both currently and in the future. The

process of developing a stress test involves both creating

a hypothetical event and identifying the consequences

that event would have upon the organisation/insurance

sector. This report suggests that the scenario development

process is best considered an iterative progression rather

than a linear trajectory. This is due to ongoing adaptations

and adjustments which are made as a researcher learns

more during the scenario’s development. The process is

summarised in Figure 4. The process can essentially start

at any phase within the process, though most will nd it