U.S. Health Insurance Industry | 2022 Mid-Year Results

1 | Page

© 2022 National Association of Insurance Commissioners

Inside the Report Page No.

Industry Overview ................................... 1

Net Earnings ............................................ 2

Underwriting Results.......................... 2 - 3

Enrollment.......................................... 4 - 5

Premium Revenues ............................ 5 - 7

Liquidity ................................................... 8

Capital and Surplus ................................. 8

U.S. Health Insurance Industry Analysis Report

HEALTH INDUSTRY OVERVIEW

Table 1 below provides a 5-year quarterly snapshot of the U.S. Health

insurance industry’s aggregate financial results for health entities who file

with the NAIC on the health quarterly statement blank. The health

insurance industry reported a 13% increase in an underwriting gain to over

$18 billion from over $16 billion for the same period in the prior year. Net

income remained mostly unchanged at just under $17 billion for the first six

months of 2022 compared to the same period in the prior year. The

industry’s profit margin decreased modestly to 3.4% from 3.7%, while the

combined ratio remained mostly unchanged at 96%.

Notable items as compared to second quarter 2021 include the following:

• Net earned premium increased 11% ($48 billion)

• Hospital & medical expenses increased 11% ($40 billion)

• Administrative expenses increased 13% ($6 billion)

• Enrollment increased 2%

• Cash flow from operations was $25 billion

• Capital and surplus increased 3% to over $196 billion from $191 billion at December 31, 2021

(In Millions)

Chg. 2Q 2022 2Q 2021

2Q 2020

2Q 2019

2Q 2018

Direct Written Premium

11.1% $498,306 $448,705 $410,736 $379,925 $358,749

Net Earned Premium

10.8% $491,870 $444,109 $406,706 $374,079 $354,626

Net Investment Income Earned

6.8% $2,923 $2,735 $2,712 $3,145 $2,571

Underwriting Gain/Loss

12.5% $18,294 $16,268 $23,717 $15,237 $10,476

Net Income/Loss

0.5% $16,889 $16,805 $21,543 $16,876 $11,411

Total Hospital & Medical Exp.

10.5% $420,387 $380,438 $326,101 $318,456 $295,931

Loss Ratio

(0.3) pts 85.0% 85.3% 80.2% 84.7% 83.1%

Administrative Expenses

13.2% $55,888 $49,391 $57,558 $42,431 $49,877

Administrative Expense Ratio

0.2 pts 11.3% 11.1% 14.1% 11.3% 14.0%

Combined Ratio

(0.1) pts 96.3% 96.4% 94.2% 95.9% 97.1%

Profit Margin

(0.3) pts 3.4% 3.7% 5.3% 4.5% 3.2%

Enrollment

1.5% 255 251 238 233 225

Premium PMPM

9.1% $323 $296 $283 $273 $262

Claims PMPM

8.7% $276 $254 $229 $233 $218

Cash Flow from Operations

107.4% $25,256 $12,175 $38,343 $18,808 $33,404

# of Companies Filed

(1) 1,130 1,131 1,096 1,048 999

6-mo. Chg.

2Q 2022 2021 2020 2019 2018

Capital & Surplus

2.8% $196,607 $191,312 $176,334 $155,944 $151,793

Table 1

Financial Summary: June 30, 2022 - 2018

*All figures only include health entities that file financial statements with the NAIC.

Note: Adjustments to exclude affiliated amounts were made where appropriate.

U.S. Health Insurance Industry | 2022 Mid-Year Results

2 | Page

© 2022 National Association of Insurance Commissioners

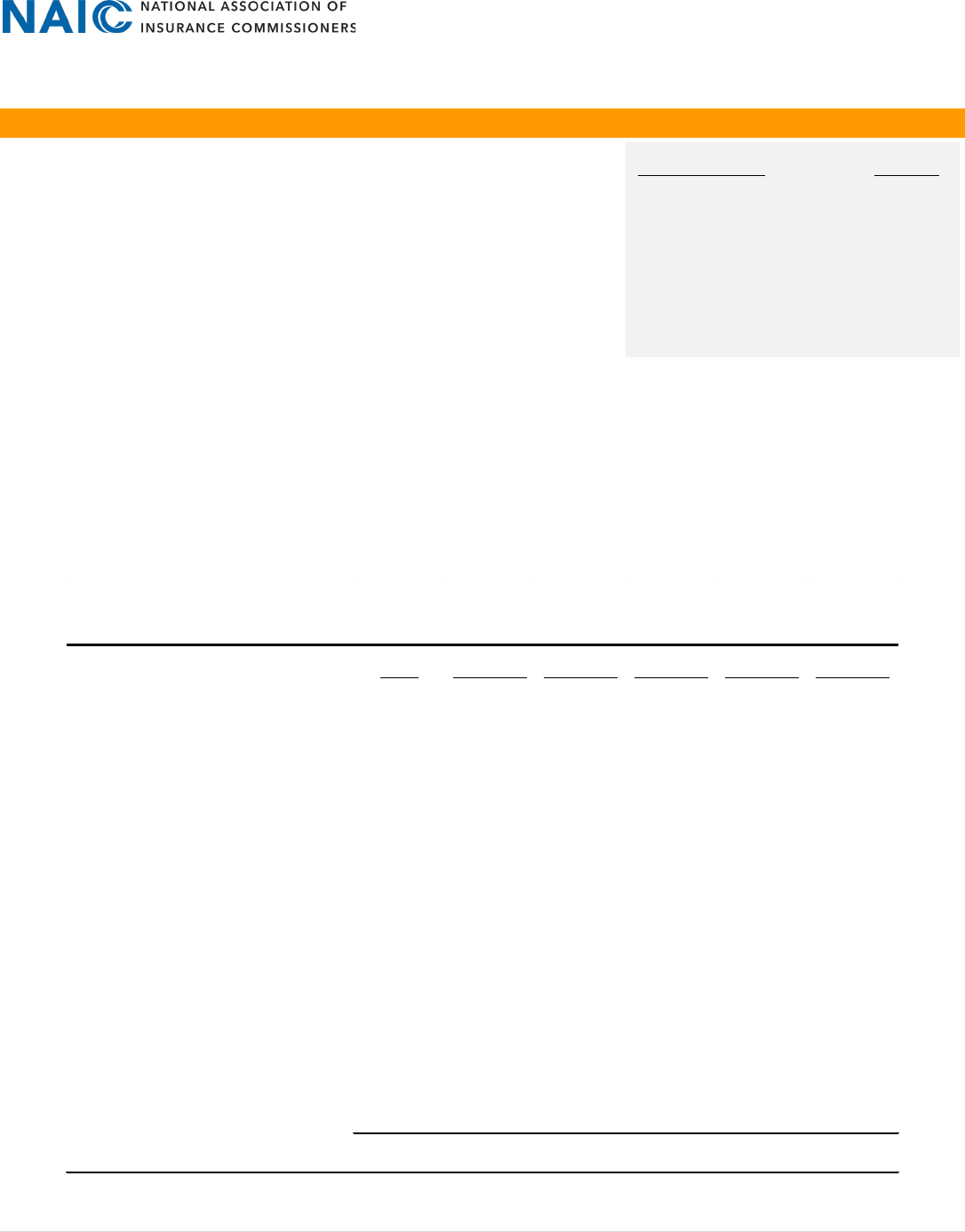

NET EARNINGS

Net income remained consistent at just under $17 billion

for the first six months of 2022 compared to the same

period in the prior year. However, the Industry reported a

13% ($2 billion) increase in underwriting gains partially

offset by a 6% ($198 million) increase in federal income

taxes incurred.

Figure 1 illustrates the trend in profitability and reflects a

profit margin of 3.4% through the second quarter of 2022

compared to a profit margin of 3.7% for the first six

months of 2021.

UNDERWRITING RESULTS

As indicated on Table 1, the increase in the industry’s

underwriting results can be attributed primarily to an 11%

($48 billion) increase in net earned premium to $491

billion from $444 billion through the first six months of

2021.

The industry partially offset these items with:

• 11% ($40 billion) increase in total hospital and

medical expenses to $420 billion from $380 billion;

and,

• 13% ($6 billion) increase in claims adjustment and

administrative expenses to $56 billion from $49

billion in the prior year period, resulting in no

change in the expense ratio of 11%.

Figure 2 illustrates the significant increase in total hospital

and medical benefits for the first six months of 2022 as

compared to the prior year period. Historically, the

Industry’s loss ratio had fluctuated modestly while

reporting consistent increases in hospital and medical

benefits. However, with the onset of the COVID Pandemic

during 2020 and lingering throughout 2021, the

aggregated loss ratio dropped to 80% in 2020 before

returning to pre-COVID levels at 85%.

Figure 3 illustrates the comparison in claims adjustment

and administrative expenses through the second quarter

of 2022 and the four prior years.

The modest decrease in the loss ratio and the slight

decrease in the administrative expense ratio culminated

in relatively no change in the combined ratio.

$295.9

$318.5

$326.1

$380.4

$420.4

83.1%

84.7%

80.2%

85.3%

85.0%

60%

70%

80%

90%

100%

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

6/30/18 6/30/19 6/30/20 6/30/21 6/30/22

$ In Billions

Hospital & Medical Benefits Medical Loss Ratio

Figure 2

Total Hospital & Medical + Loss Ratio

$11

$17

$22

$17

$18

3.2%

4.5%

5.3%

3.7%

3.4%

0%

1%

2%

3%

4%

5%

6%

$0

$5

$10

$15

$20

$25

6/30/18 6/30/19 6/30/20

6/30/21

6/30/22

$ In Billions

Figure 1

Net Income & Profit Margin (ROR)

Net Income Profit Margin

$49.9

$42.4

$57.6

$49.4

$55.9

14.0%

11.3%

14.1%

11.1%

11.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$0

$10

$20

$30

$40

$50

$60

6/30/18 6/30/19 6/30/20 6/30/21 6/30/22

$ In Billions

General Admin. Expenses Admin Expense Ratio

Figure 3

Admin Expenses & Admin Expense Ratio

U.S. Health Insurance Industry | 2022 Mid-Year Results

3 | Page

© 2022 National Association of Insurance Commissioners

Table 2 provides data from the Exhibit of Premiums, Enrollment, and Utilization by Line of Business. The table includes

comparison of direct and earned premium, claims, loss ratio, net premium and claims per member per month, and

enrollment through the second quarter of 2022 and the four prior years.

Individual Comprehensive

Hospital & Medical

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

Group Comprehensive

Hospital & Medical

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

(In Millions, Except PMPM) (In Millions, Except PMPM)

Direct Written Premium $46,308 $41,421 $38,978 $39,535 $39,262 D

irect Written Premium $83,832 $83,042 $83,226 $83,686 $82,854

Net Earned Premium $45,641 $39,816 $37,170 $38,084 $39,089 Net Earned Premium $82,803 $82,851 $82,587 $83,971 $82,544

Total Hospital & Medical Exp $35,450 $31,356 $26,734 $27,331 $26,517 T

otal Hospital & Medical Exp $69,976 $70,197 $65,097 $67,869 $67,556

Loss Ratio 77.7% 78.8% 71.9% 71.8% 67.8% Loss Ratio 84.5% 84.7% 78.8% 80.8% 81.8%

Net Premium PMPM $533 $508 $498 $521 $502 N

et Premium PMPM $518 $492 $470 $467 $445

Claims PMPM $414 $400 $358 $374 $340 C

laims PMPM $438 $417 $370 $377 $364

Margin $119 $108 $140 $147 $161 Margin $80 $75 $99 $90 $81

Enrollment

14 14 13 12 13

E

nrollment

27 28 29 30 31

Medicare Supplement

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

V

ision

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

(In Millions, Except PMPM) (In Millions, Except PMPM)

Direct Written Premium

$6,574 $6,318 $6,122 $5,782 $5,451 Direct Written Premium $

1,470 $1,408 $1,365 $1,279 $1,311

Net Earned Premium $6,483 $6,227 $6,023 $5,757 $5,404 N

et Earned Premium $1,465 $1,408 $1,357 $1,353 $1,309

Total Hospital & Medical Exp $5,211 $4,850 $4,391 $4,743 $4,375 Total Hospital & Medical Exp $1,530 $1,477 $1,085 $1,383 $1,494

Loss Ratio 80.4% 77.9% 72.9% 82.4% 81.0% L

oss Ratio 104.5% 104.9% 80.0% 102.2% 114.1%

Net Premium PMPM $214 $210 $212 $211 $209 N

et Premium PMPM $6 $6 $6 $6 $6

Claims PMPM $172 $164 $155 $174 $169 C

laims PMPM $4 $4 $5 $7 $7

Margin $42 $47 $57 $37 $40 M

argin $2 $3 $1 ($1) ($1)

Enrollment

5 5 5 5 4

E

nrollment

39 38 37 36 34

Dental

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

F

EHBP

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

(In Millions, Except PMPM) (In Millions, Except PMPM)

Direct Written Premium $7,664 $7,392 $6,719 $7,008 $6,955 D

irect Written Premium $22,482 $21,491 $20,059 $19,872 $19,617

Net Earned Premium $7,185 $7,005 $5,878 $6,405 $6,425 Net Earned Premium $22,156 $21,848 $20,276 $20,342 $19,396

Total Hospital & Medical Exp $6,269 $6,002 $4,144 $5,454 $5,371 Total Hospital & Medical Exp $20,628 $20,167 $18,222 $18,920 $17,646

Loss Ratio 87.3% 85.7% 70.5% 85.2% 83.6% L

oss Ratio 93.1% 92.3% 89.9% 93.0% 91.0%

Net Premium PMPM $27 $26 $24 $26 $26 Net Premium PMPM $406 $401 $378 $388 $418

Claims PMPM $23 $23 $17 $22 $22 C

laims PMPM $378 $370 $339 $361 $380

Margin $3 $4 $7 $4 ($1) Margin $28 $31 $38 $27 $38

Enrollment

45 45 42 42 42

E

nrollment

9 9 9 9 8

Medicare

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

M

edicaid

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

(In Millions, Except PMPM) (In Millions, Except PMPM)

Direct Written Premium

$168,676 $141,713 $126,752 $110,031 $96,558 Direct Written Premium $151,873 $134,720 $118,435 $102,326 $95,724

Net Earned Premium $168,363 $141,285 $125,079 $109,768 $95,907 N

et Earned Premium $151,331 $132,903 $113,488 $100,181 $94,897

Total Hospital & Medical Exp $140,270 $121,156 $97,530 $90,945 $81,114 Total Hospital & Medical Exp $125,481 $113,412 $96,841 $90,872 $83,615

Loss Ratio 83.3% 85.8% 78.0% 82.9% 84.6% Loss Ratio 82.9% 85.3% 85.3% 90.7% 88.1%

Net Premium PMPM $1,197 $1,123 $1,100 $1,052 $968 N

et Premium PMPM $447 $425 $423 $392 $372

Claims PMPM $997 $963 $858 $871 $819 Claims PMPM $371 $363 $361 $356 $328

Margin $200 $160 $242 $180 $149 Margin $76 $62 $62 $36 $44

Enrollment

24 21 19 18 16

E

nrollment

57 54 48 44 44

Other Health

2Q 2022 2Q 2021 2Q 2020 2Q 2019 2Q 2018

(In Millions, Except PMPM)

Direct Written Premium $11,060 $10,549 $10,861 $10,283 $9,516

Net Earned Premium $11,057 $10,640 $11,157 $10,625 $9,829

Total Hospital & Medical Exp $11,030 $10,606 $11,092 $9,630 $8,863

Loss Ratio 99.8% 99.7% 99.4% 90.6% 90.2%

Net Premium PMPM $53 $47 $50 $52 $51

Claims PMPM $53 $46 $50 $47 $46

Margin $0 $0 $0 $5 $5

Enrollment

35 38 38 38 34

Exhibit of Premiums, Enrollment & Utilization by Lines of Business

Table 2

U.S. Health Insurance Industry | 2022 Mid-Year Results

4 | Page

© 2022 National Association of Insurance Commissioners

The CDC has reported nearly 97 million COVID-19 cases nationwide and over one million deaths since January 21, 2020.

The health insurance industry reported a 25% (over $94 billion) increase in health benefit claims incurred between June

30, 2020, and June 30, 2022. However, in 2020 offsetting factors resulting from the pandemic appear to have reduced

the overall financial impact to insurers such as reduced healthcare claims and decreased medical costs related to

cancelled or delayed utilization of healthcare benefits. These offsetting factors are also evident in the decreases in the

loss ratios for several line of business in 2020 as included in Table 2 above.

This significant increase in hospital and medical benefits in 2021 and 2022 now places the Health insurance industry

underwriting results more in line with financial results as reported pre-COVID19 pandemic in prior-year period 2019 in

relation to underwriting gains, net income, loss and administrative expense ratios and profit margin.

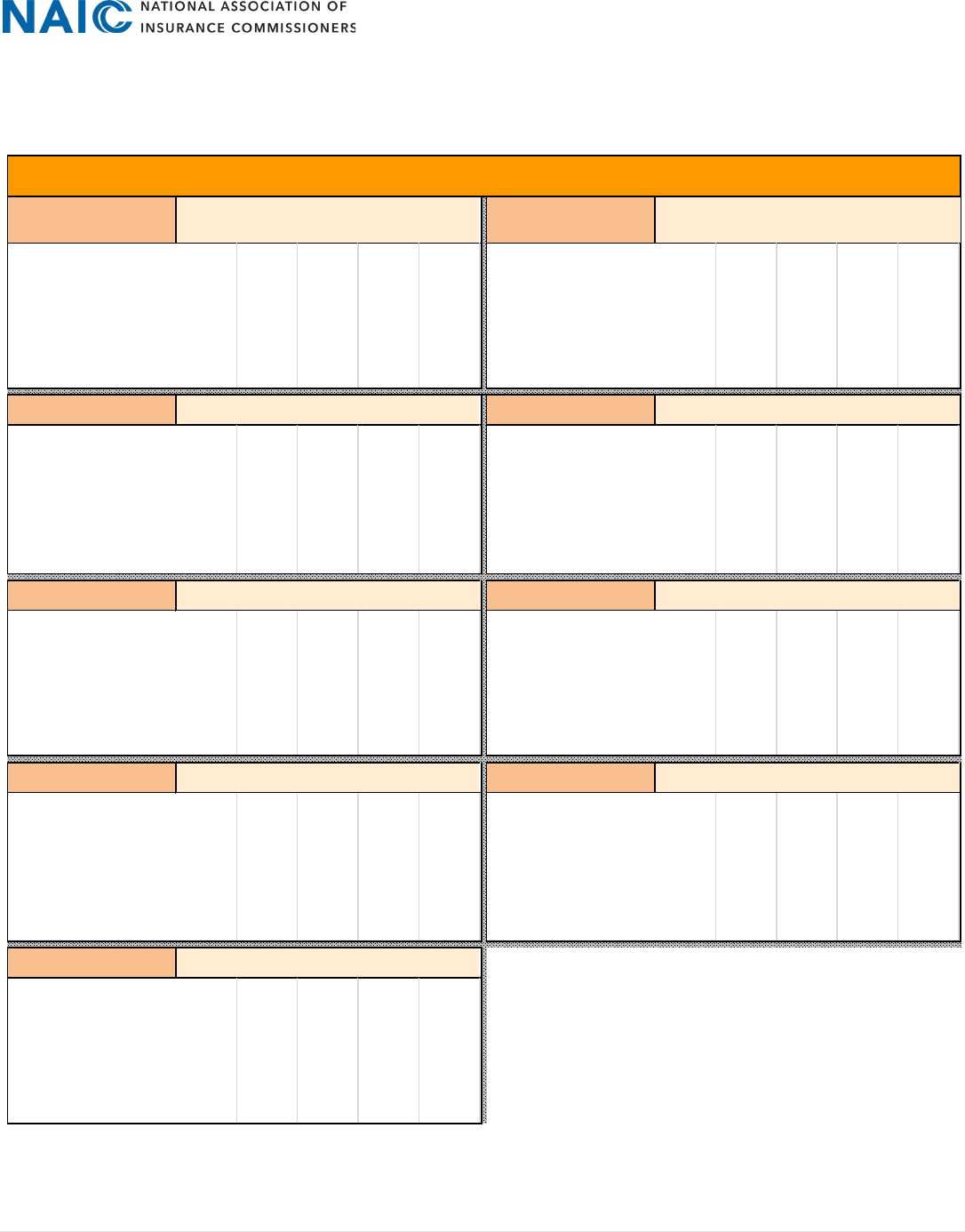

ENROLLMENT

As shown in Figure 4, the industry has experienced an

incremental increase in total enrollment of 13% (30

million) to 255 million from 225 million through the

second quarter of 2018.

The increase from 2018 is due primarily to:

• 31% (14 million) increase in Medicaid;

• 44% (7 million) increase in Medicare;

• 14% (5 million) increase in vision coverage;

• 9% (4 million) increase in dental coverage;

• 17% (1 million) increase in Federal Employee

Health Benefit Plans; and,

• 3% (1 million) increase in policies that provide

Medicare Pat D Drug coverage.

However, these lines were partially offset by:

• 13% (4 million) decrease in the group comprehensive line of business; and

• a 12% (2 million) decrease in the individual comprehensive line of business from the first six months of 2018.

As indicated above, the industry still experienced considerable growth in both Medicaid and Medicare. As a result of

increased unemployment rates caused by the pandemic, health care coverage has also been disrupted for millions of

people as most working-age adults receive health insurance coverage for themselves and their families through their

employer beginning in 2020. Many of those who lost health insurance coverage through their employer qualified for

Medicaid or had the opportunity to purchase individual health coverage through the exchange or other managed care

health providers. The shift in business concentration can also be attributed to an increase in the number of insureds

becoming eligible for either Medicare or Medicaid as evidenced by increases in enrollment in these lines. A certain

amount of the Medicaid enrollment increase is due to the continued expansion of Medicaid programs in certain states.

The U.S. has been operating under a Public Health Emergency (PHE) declared by the federal government since the start

of the COVID-19 pandemic. This declaration resulted in significantly expanded Medicaid enrollment, as well as special

coverage rules for COVID-19 vaccines, tests, and treatments. Just recently, the Department of Health and Human

Services (HHS) announced that the PHE would be extended to January 11, 2023, and that it would give at least 60 days-

notice before lifting the emergency declaration. However, once the emergency is lifted, there is the potential for

disruption in the health insurance market when the individuals potentially no longer qualify for Medicaid and what

financial impact that could have on insurers. Some estimates suggest that 15 million or more people might no longer

qualify for Medicaid.

$359

$380

$411

$449

$498

225

233

238

251

255

210

215

220

225

230

235

240

245

250

255

260

$0

$60

$120

$180

$240

$300

$360

$420

$480

$540

6/30/18 6/30/19 6/30/20 6/30/21 6/30/22

In Millions

$ In Billions

Figure 4

Enrollment & Direct Written Premium

Direct Written Premium Enrollment

U.S. Health Insurance Industry | 2022 Mid-Year Results

5 | Page

© 2022 National Association of Insurance Commissioners

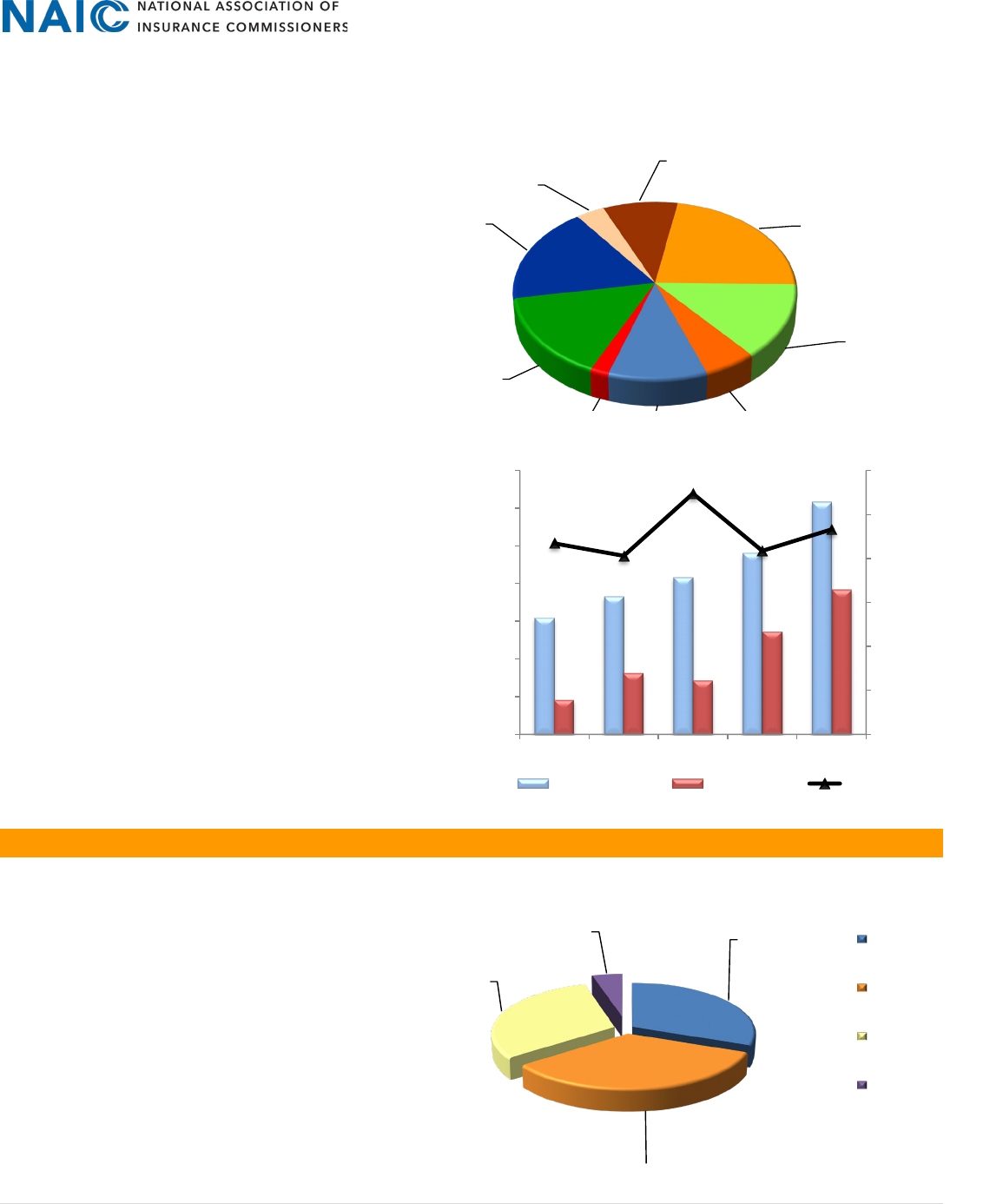

The industry recorded over 255 million members

enrolled in various types of health insurance

products. As shown on Figure 5, Medicaid

represents 22% of total enrollment; Dental 18%;

Vision 15%; Medicare Pt D 14%; Group

Comprehensive 10%; Medicare at 9%; and

Individual Comprehensive 6%. A shift in business

concentration can be attributed to an increase in

the number of insureds becoming eligible for

either Medicare or Medicaid as evidenced by

increases in enrollment in these lines. A certain

amount of Medicaid enrollment increases is likely

due to the continued expansion of Medicaid

programs in certain states.

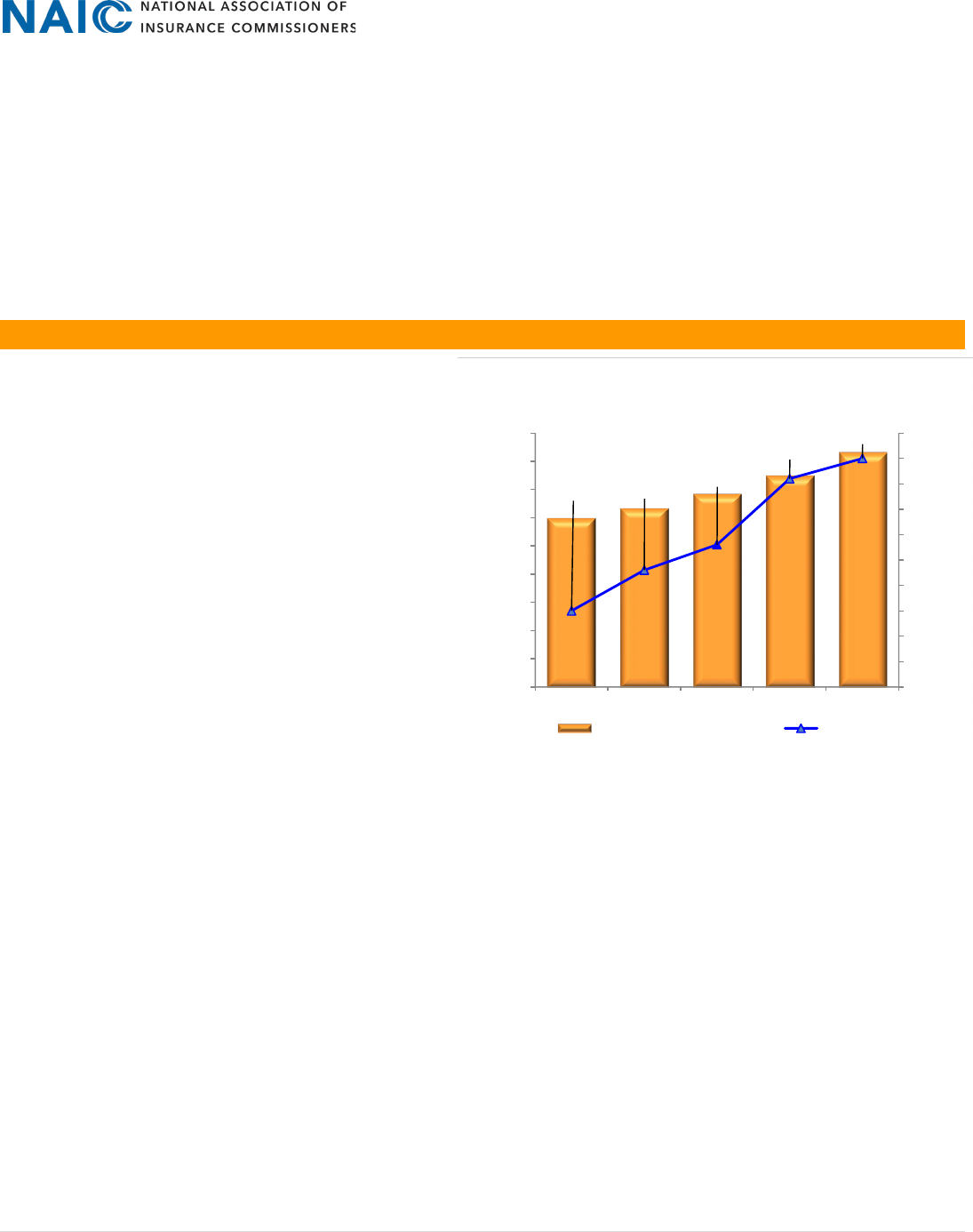

As depicted in Figure 6, health entities’ earned

premium per member per month (PMPM)

increased 23% over a five-year period to $323

from $262 for the first six months of 2018, while

claims PMPM increased 27% to $276 from $218. It

is evident premium PMPM increased

incrementally through the five years illustrated in

the adjacent graph while claims PMPM decreased in

2020 due to decreased medical costs related to

cancelled or delayed medical utilization of

healthcare benefits in 2020. As show in the graph,

the margin in 2021 and 2022 returned to a margin

more comparable to pre-pandemic periods.

PREMIUM REVENUES

Figure 4 above illustrates the growth in direct written

premium. In comparison to the first six months of 2021,

the industry reported an 11% ($50 billion) increase in

direct written premium to $498 billion from $449

billion. The increase is primarily on the Medicare, and

Medicaid lines of business.

Figure 7 illustrates the mix of direct written premium

for the first six months of 2022. As insureds have

become eligible for either Medicare and/or Medicaid as

evidenced by increases in enrollment in these lines,

there has been a gradual shift in the allocation of

premium between the lines of business over the last

five years. In comparison to the first half of 2021, direct

31%

34%

31%

4%

Figure 7

2nd Qtr 2022

Direct Health Premium Written by Line

Comprehensive

Medicare

Medicaid

FEHBP

6%

10%

2%

15%

18%

4%

9%

22%

14%

Indiv Comp Grp Comp

Med Supp

Vision Dental FEHBP

Medicare Medicaid Other - Med Pt D

Figure 5

Enrollment by Line of Business

$43

$41

$55

$42

$47

$0

$10

$20

$30

$40

$50

$60

$200

$220

$240

$260

$280

$300

$320

$340

6/30/18 6/30/19 6/30/20 6/30/21 6/30/22

$ In Dollars

Figure 6

Premium PMPM vs Claims PMPM

Premium PMPM Claims PMPM Margin

U.S. Health Insurance Industry | 2022 Mid-Year Results

6 | Page

© 2022 National Association of Insurance Commissioners

comprehensive medical decreased to below 31% from just above 33% of total written premium, while Medicare

increased to nearly 34% from 32%, Medicaid increased to 31% from just under 30%, and FEHBP remained mostly

unchanged at just below 5%.

Table 3 below provides a breakout of direct written premium by line of business. The largest dollar increases in written

premium from the first six months of 2021 was a 19% ($27 billion) increase in Medicare, and a 13% ($17 billion) increase

in Medicaid.

Table 4 on the next page includes direct written premium for the four largest revenue-generating lines of business as

reported by each state on Schedule T of the quarterly financial statement. The state of Florida reports the greatest dollar

amount of direct written premium on both the comprehensive medical and Medicare lines of business through the

second quarter of 2022. Florida recorded just under $15 billion in comprehensive medical premium after recording an

increase from the prior-year quarter while recording just under $20 billion in Medicare premium, which is a 26%

increase from the prior-year quarter. The state of Texas reported just under $19 billion in Medicaid premium including a

36% increase over the prior-year quarter. The state of Maryland reported just over $2 billion in premium revenue for the

federal employee health benefit plan line of business including a 7% increase over the prior-year quarter.

(In Millions)

Chg.

$ Chg.

2Q 2022

2Q 2021

2Q 2020

2Q 2019

2Q 2018

Individual Comprehensi

11.8% $4,887 $46,308 $41,421 $38,978 $39,535 $39,262

Group Comprehensive

1.0% $790 $83,832 $83,042 $83,226 $83,686 $82,854

Medicare Supplement

4.0% $256 $6,574 $6,318 $6,122 $5,782 $5,451

Vision

4.4% $62 $1,470 $1,408 $1,365 $1,279 $1,311

Denta l

3.7% $272 $7,664 $7,392 $6,719 $7,008 $6,955

FEHBP

4.6% $991 $22,482 $21,491 $20,059 $19,872 $19,617

Medicare

19.0% $26,964 $168,676 $141,713 $126,752 $110,031 $96,558

Medicaid

12.7% $17,152 $151,873 $134,720 $118,435 $102,326 $95,724

Other Heal th

4.8% $511 $11,060 $10,549 $10,861 $10,283 $9,516

Table 3

Direct Written Premium by Lines of Business

U.S. Health Insurance Industry | 2022 Mid-Year Results

7 | Page

© 2022 National Association of Insurance Commissioners

($ in Millions)

State 2Q 2022 2Q 2021 % Chg. 2Q 2022 2Q 2021 % Chg. 2Q 2022 2Q 2021

%

Pt Chg.

2Q 2022 2Q 2021 % Chg.

Alabama

$3,004 $2,747 9.3% $3,916 $3,376 16.0% $19 $15 22.1% $402 $454 (11.4)%

Al as ka

$319 $278 14.9% $3 $2 33.8% $0 $0 0.0% $264 $227 16.3%

Ari zona

$1,824 $1,671 9.1% $3,592 $2,900 23.8% $138 $133 3.8% $373 $389 (4.1)%

Arkansas

$2,039 $1,942 5.0% $1,702 $1,439 18.3% $805 $671 20.0% $160 $155 3.0%

California

$1,428 $1,423 0.3% $2,389 $2,033 17.5% $0 $0 0.0% $3 $3 0.9%

Colorado

$2,794 $2,812 (0.6)% $2,952 $2,343 26.0% $657 $570 15.3% $437 $449 (2.8)%

Connecticut

$1,582 $1,639 (3.5)% $2,217 $1,870 18.6% $0 $0 0.0% $180 $174 3.5%

Delaware

$387 $349 11.1% $323 $197 64.0% $0 $0 0.0% $95 $92 4.1%

District of Columbia

$1,126 $1,068 5.4% $232 $63 268.5% $912 $767 18.9% $905 $803 12.8%

Florida

$14,498 $12,726 13.9% $19,721 $15,627 26.2% $11,517 $9,537 20.8% $1,443 $1,383 4.4%

Georgi a

$4,701 $4,515 4.1% $6,024 $4,078 47.7% $2,852 $2,319 23.0% $850 $853 (0.3)%

Hawaii

$1,768 $1,730 2.2% $1,005 $678 48.2% $1,127 $1,043 8.1% $240 $229 5.0%

Idaho

$1,090 $1,063 2.5% $906 $658 37.8% $317 $261 21.8% $113 $120 (6.5)%

Illinois

$8,859 $8,523 3.9% $5,840 $4,745 0.0% $8,159 $7,332 11.3% $706 $640 10.4%

Indiana

$1,964 $1,836 7.0% $3,659 $2,497 46.5% $4,188 $3,932 6.5% $381 $373 2.3%

Iowa

$1,917 $1,823 5.2% $1,277 $1,032 23.8% $2,983 $2,823 5.7% $151 $145 3.7%

Kansas

$700 $667 4.8% $1,029 $803 28.2% $2,047 $1,908 7.3% $69 $74 (6.5)%

Kentucky

$1,832 $1,832 (0.0)% $3,091 $2,629 17.6% $4,934 $5,382 (8.3)% $267 $256 4.3%

Louisiana

$2,106 $2,039 3.3% $3,154 $2,648 19.1% $5,568 $5,101 9.2% $255 $241 5.9%

Maine

$919 $860 6.9% $942 $785 20.0% $0 $0 0.0% $124 $116 6.9%

Maryland

$2,525 $2,393 5.5% $1,344 $1,042 29.0% $1,786 $1,646 8.5% $2,041 $1,916 6.6%

Massachusetts

$6,845 $6,854 (0.1)% $1,983 $1,678 18.2% $2,981 $2,622 13.7% $485 $426 14.0%

Michigan

$7,009 $6,635 5.6% $6,690 $6,068 10.3% $4,193 $3,881 8.0% $399 $424 (6.1)%

Minnesota

$3,376 $3,274 3.1% $3,247 $2,849 14.0% $4,841 $4,023 20.3% $364 $325 11.9%

Mississippi

$1,105 $1,032 7.1% $1,407 $1,006 39.9% $976 $1,204 (18.9)% $183 $192 (4.4)%

Missouri

$2,296 $2,185 5.1% $4,203 $3,456 21.6% $1,665 $1,290 29.1% $409 $394 3.8%

Montana

$559 $497 12.6% $348 $292 19.2% $0 $0 0.0% $118 $118 0.1%

Nebras ka

$1,166 $1,090 7.0% $685 $512 33.9% $1,146 $975 17.5% $137 $131 4.2%

Nevada

$1,460 $1,343 8.6% $1,956 $1,684 16.1% $1,212 $1,175 3.1% $124 $130 (4.9)%

New Hampshi re

$858 $846 1.4% $448 $352 27.4% $629 $590 6.6% $170 $157 8.5%

New Jers ey

$4,758 $4,760 (0.0)% $3,326 $2,786 19.4% $6,881 $6,219 10.6% $522 $527 (1.0)%

New Mexi co

$539 $481 11.9% $1,139 $868 31.2% $3,266 $2,839 15.0% $150 $190 (21.3)%

New York

$11,903 $11,430 4.1% $10,389 $9,354 11.1% $5,191 $4,867 6.7% $940 $895 5.1%

North Carolina

$4,642 $4,188 10.9% $6,375 $5,189 22.9% $3,741 $0 0.0% $622 $621 0.2%

North Dakota

$848 $833 1.8% $133 $100 33.1% $199 $180 10.9% $66 $67 (1.5)%

Ohio

$4,636 $4,389 5.6% $7,733 $6,609 17.0% $11,194 $10,246 9.3% $709 $666 6.6%

Okl ahoma

$1,988 $1,932 2.9% $1,753 $1,409 24.4% $0 $0 0.0% $388 $386 0.6%

Oregon

$3,080 $3,059 0.7% $3,049 $3,098 (1.6)% $3,625 $2,169 67.2% $279 $270 3.3%

Pennsylvania

$5,933 $6,889 (13.9)% $9,164 $8,131 0.0% $15,304 $13,966 9.6% $743 $725 2.4%

Rhode Island

$625 $627 (0.4)% $725 $593 22.3% $1,134 $1,061 6.9% $62 $63 (1.6)%

South Carolina

$2,242 $2,215 1.2% $2,967 $1,577 88.1% $1,893 $1,735 9.1% $344 $317 8.4%

South Dakota

$730 $689 5.9% $211 $172 22.3% $0 $0 0.0% $112 $94 19.4%

Tennes s ee

$2,351 $2,226 5.6% $4,734 $4,203 12.6% $3,423 $3,279 4.4% $428 $409 4.5%

Texas

$13,274 $12,485 6.3% $16,615 $12,841 29.4% $18,813 $13,828 36.0% $1,805 $1,682 7.3%

Utah

$1,800 $1,633 10.2% $1,213 $1,052 15.3% $640 $511 25.3% $342 $333 2.5%

Vermont

$379 $364 4.0% $211 $116 82.3% $0 $0 0.0% $49 $52 (5.4)%

Virginia

$3,799 $3,640 4.4% $3,378 $2,716 24.4% $6,797 $6,126 10.9% $1,434 $1,409 1.8%

Washington

$4,628 $4,444 4.1% $3,840 $2,909 32.0% $4,375 $4,018 8.9% $564 $536 5.3%

West Virginia

$566 $522 8.4% $1,321 $1,140 15.9% $1,209 $1,108 9.1% $223 $223 0.3%

Wisconsin

$4,005 $3,915 2.3% $3,543 $3,278 8.1% $1,450 $1,307 10.9% $367 $321 14.3%

Wyomi ng

$323 $280 15.6% $39 $8 386.1% $0 $0 0.0% $60 $47 27.7%

Ameri ca n Samoa

$0 $0 0.0% $0 $0 0.0% $0 $0 0.0% $0 $0 0.0%

Guam

$44 $15 189.5% $0 $0 0.0% $0 $0 0.0% $12 $13 (4.4)%

Puerto Ri co

$642 $627 2.4% $4,015 $4,088 0.0% $1,642 $1,291 27.2% $110 $100 0.0%

U.S. Virgin Islands

$3 $7 (50.4)% $21 $18 0.0% $0 $0 0.0% $1 $1 (40.2)%

Northern Mariana Islands

$1 $1 31.9% $0 $0 0.0% $0 $0 0.0% $0 $0 0.0%

Aggrega te Other Al i en

$638 $532 20.0% $0 $0 0.0% $0 $0 0.0% $0 $0 0.0%

Table 4 - Direct Written Premium by Line of Business by State

As reported on Schedule T

Comprehensive Medical

Medicare

Medicaid

FEHBP

U.S. Health Insurance Industry | 2022 Mid-Year Results

8 | Page

© 2022 National Association of Insurance Commissioners

CASH FLOW AND LIQUIDITY

The health insurance industry reported a significant increase in operating cash flow to $25 billion in the first half of 2022

as compared to operating cash flow of $12 billion in the first half of 2021. The considerable increase in positive cash flow

is due primarily to an 11% ($47 billion) increase in premiums collected partially offset by 10% ($36 billion) increase in

benefits and loss-related payments.

As illustrated in Figure 8, liquid assets and

receivables increased 5% ($20 billion) to

$384 billion in the first six months of 2022

as compared to the prior year period while

current liabilities increased 10% ($20

billion) to $225 billion. This resulted in a

decrease in the ratio of liquid assets and

receivables to current liabilities to 171%

from 178% for the period ended June 30,

2021.

CAPITAL AND SURPLUS

Health entities reported a 3% ($5 billion)

increase in capital and surplus to over

$196 billion from over $191 billion at Dec.

31, 2021, as illustrated in Figure 9. The

increase is due primarily to net income of

$17 billion and additional paid-in surplus

of $2 billion. However, these items were

partially offset by a $6 billion increase in

unrealized capital losses, dividends of $4

billion paid to stockholders, and a $2

billion increase in non-admitted assets.

Figure 9

Capital & Surplus Account

$138

$152

$156

$176

$192

$191

$197

$0

$40

$80

$120

$160

$200

$240

$0

$5

$10

$15

$20

$25

$30

$35

2017 2018 2019

2020 2Q 2021 2021 2Q 2022

$ In Billions

Net Income Dividends to Stockholders Capital & Surplus

160%

165%

170%

175%

180%

185%

190%

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

6/30/18 6/30/19 6/30/20

6/30/21

6/30/22

$ In Billions

Figure 8

Ratio of Liquid Assets & Receivables to Current Liabilities

Liquid Assets & Receivables

Current Liabilities

Ratio of Liquid Assets & Receivables to Current Liabilities

U.S. Health Insurance Industry | 2022 Mid-Year Results

9 | Page

© 2022 National Association of Insurance Commissioners

Health Industry Disclosure: In some states the health industry is regulated by a Department/Office of Insurance other

than the Departm

ent of Insurance. Therefore, not all health insurers may be required to file financial statements with

the NAIC.

Financial Regulatory Services Division

Financial Analysis and Examinations Department

Contacts:

Bill Rivers, Health Financial Analysis Program Manager

816.783-8142

Bruce Jenson, Assistant Director Solvency Monitoring

BJenso[email protected]g

816.783.8348

Jane Koenigsman, Sr. Financial Analysis Manager II

816.783.8145

Disclaimer: The NAIC 2022 Mid-Year Health Insurance Industry Analysis Report is a limited scope analysis based on the

aggregated information filed to the NAIC’s Financial Data Repository as of June 30, 2022, and

written by the Financial

Regulatory Services Department staff. This report does

not constitute the official opinion or views of the NAIC

membership or any particular state insurance department.