1

`

Annual Report

2021 – 2022

2

Forty-Seventh Annual Report

2021 – 2022

TO HER HONOUR

The Lieutenant Governor

of the Province of Ontario

MAY IT PLEASE YOUR HONOUR

The undersigned begs respectfully to present to Your Honour the

Annual Report of the Algonquin Forestry Authority for the year

beginning April 1, 2021 and ending March 31, 2022.

The Honourable Graydon Smith

Minister

Honourable Sir:

THE HONOURABLE GRAYDON SMITH

Minister of Natural Resources and Forestry

I have the honour to submit to you the Annual Report of the

Algonquin Forestry Authority for the year beginning April 1, 2021

and ending March 31, 2022.

David Lemkay

Chair

3

TABLE OF CONTENTS

ROLE AND MANDATE ................................................................................................................................................. 4

CHAIR’S MESSAGE ...................................................................................................................................................... 5

DESCRIPTION OF ACTIVITIES ...................................................................................................................................... 6

Harvesting ................................................................................................................................................................... 6

Quarterly Sales Volume .......................................................................................................................................... 7

Contractor (Productive) Capacity ........................................................................................................................... 8

Product Sales ........................................................................................................................................................... 8

Forest Management ................................................................................................................................................... 9

Silvicultural Effectiveness Monitoring ................................................................................................................... 10

Site Preparation, Tree Planting and Scarification ................................................................................................. 10

Tree Marking ............................................................................................................................................................ 11

Tending and Stand Improvement ........................................................................................................................... 11

FINANCIAL RESULTS .................................................................................................................................................. 12

Harvesting and the Statement of Operations .......................................................................................................... 12

Forest Renewal Fund ................................................................................................................................................. 13

Financial Position- Balance Sheet ............................................................................................................................. 13

Audited Financial Statements ................................................................................................................................... 13

ACHIEVEMENT OF STRATEGIC OBJECTIVES ............................................................................................................. 14

Operational Excellence .......................................................................................................................................... 14

Advancing Innovative Practice ............................................................................................................................. 14

Developing and Supporting Our People .............................................................................................................. 15

Indigenous Partnership ......................................................................................................................................... 16

Supporting Local Industry ..................................................................................................................................... 16

PUBLIC APPOINTMENTS – BOARD of DIRECTORS ................................................................................................... 17

ORGANIZATION CHART (Full-Time, Regular Staff as of April 1, 2021) ...................................................................... 18

4

ROLE AND MANDATE

The Algonquin Forestry Authority (the Authority, AFA) operates under the Algonquin Forestry Authority

Act, R.S.O. 1990. The Authority is a self-financing operational enterprise Ontario Crown agency. The

Minister of Natural Resources and Forestry (Minister, Ministry) is responsible for the administration of

the Algonquin Forestry Authority Act. This legislation sets out the management, objectives, and powers

of the AFA within Algonquin Provincial Park.

• Ensuring the sustainable management of Algonquin’s forests

• Planning of all forestry operations; harvest, access, renewal and tending

• Harvesting and distribution of wood products to mills

• Monitoring and reporting on forestry operations

All forestry activities are carried out under the direction of a Ministry approved Forest Management Plan

(FMP), subject to the Crown Forests Sustainability Act, 1994. These activities are subject to an

Independent Forest Audit (IFA) every ten years and the audit results are tabled in the Ontario

Legislature and made available to the public. The most recent IFA audit was conducted in 2017.

The Algonquin Park Forest is certified to Canada’s national forest certification standard Canadian

Standards Association (CSA) Z-809 2016. This certification demonstrates the Authority’s commitment

to sustainable forest management and provides the public access to results from annual independent

audits to defined standards.

A key component of the CSA Z-809 standard is the AFA’s environmental and sustainable forest

management system (ESFMS). Key objectives of the ESFMS are prevention of pollution, sustainable

forestry, continual improvement and compliance with applicable laws and guidelines. AFA receives

management direction from several different plans and legislation, but its Sustainable Forest

Management (SFM) Policy guides its day-to-day activities. AFA’s commitment to SFM can be found in its

Vision Statement:

To achieve the highest standards of sustainable forest management practices,

in order to maintain Park values for future generations.

The Authority applies the principles of SFM to balance the public’s concern for protecting Park values.

Protection of Indigenous, recreation, fisheries, wildlife habitat and natural and cultural heritage values

is of utmost importance while creating economic opportunities and maintaining a supply of forest

products to mills dependent on Park timber.

Harvesting is carefully regulated to minimize impacts on other forest values while being a significant

economic generator for the region. The Authority contracts out both harvesting and forest

management work to companies from communities in the region. The timber harvested regularly

supports 12 mills in communities such as Huntsville, Whitney, Madawaska, Pembroke, Killaloe and

Eganville. Another ten to fifteen mills in the region receive periodic supplies.

5

CHAIR’S MESSAGE

By David Lemkay

We are pleased to present this Annual Report outlining Algonquin Forestry Authority (AFA) operations

for the fiscal year 2021-2022. In its 47

th

year of operation the AFA has continued its mandate of

sustainable forest management in Algonquin Provincial Park. The Authority is committed to this

mandate on behalf of Ontarians with the economic, social and environmental benefits that the

Algonquin Park Forest provides.

The Board of Directors is most pleased to be operating within the newly completed ten-year Forest

Management Plan and lauds management and staff, particularly General Manager Jeff Leavey and Chief

Forester Gord Cumming for their exemplary work to bring this to fruition.

Meeting activity at the board level and with the Governance Committee, Finance Committee and Human

Resources Committee on strategic initiatives has been managed in virtual and hybrid format with a

return now to in-person sessions. The Board is pleased to report successful culmination of audits and

reporting for this year.

Tenure on the Board has ended for two highly esteemed members, Carl Corbett and Rodney Smith. The

addition of two new members in the persons of Robert Craftchick representing the Algonquins of

Ontario and forest entrepreneur Leo Hall ensures the appropriate Board complement, experience, and

skill sets.

Through ongoing liaison with the Ministry of Natural Resources and Forestry the Board is pursuing

certain updating of Board and staff compensation programs. We foresee certain significant changes in

management personnel on the horizon. Over the term of this year of operations, there were three

retirements from staff: Keith Fletcher, Area Manager, Martin Laflamme, Woodlands Supervisor and Jeff

Driscoll, Operations Supervisor. On behalf of the Algonquin Forestry Authority, I wish them well in their

retirement and thank them for their combined 101 years of dedicated service.

As Chair for the past three-year term, completing my overall tenure of ten years, I will be retiring from

the Board of Directors as of October 2022. Arrangements will be undertaken to fill the vacancy that my

departure will create, and we anticipate a seamless transition at that level, working with Crown.

It has been an honour to serve The Province of Ontario on the Algonquin Forestry Authority Board of

Directors and now in my final term I am pleased to offer these comments within the 47

th

Annual Report.

6

DESCRIPTION OF ACTIVITIES

The next two sections; harvesting and forest management, describe forestry activities, operational

performance, and target achievement for 2021-2022. Targets discussed herein were set out in the

Authority’s 2021 to 2024 Business Plan.

Typically, most of the harvesting and transportation of timber to market is conducted between

September and March, while forest management activities begin in April and are generally concluded by

December. This requires significant expenditures to occur early in the year that are eventually funded

later in the year by revenue generated from the sale of timber.

Performance measures are established during the business planning process three to four months

before the results of the previous year’s operations are known, therefore actual results are subject to

in-year adjustments.

Factors that can negatively affect achievement of objectives are typically

fluctuating market demand for forest products, extreme weather conditions, recreational and

biological timing limitations on operating within Algonquin Provincial Park and the availability of

human and physical resources.

The AFA plans all operations on a cost-recovery basis and as such sets volume and value targets to fund

operations within the sustainability limits for forest operations in the approved FMP. Achievement of

business targets is tracked and compared to the annual budget and quarterly performance from the

previous year on an on-going basis.

The approved FMP and AFA’s sustainable forest management plan sets targets to which performance is

also measured but reported in separate reporting documents as required by the Crown Forest

Sustainability Act, 1994 (CFSA) and Canadian Standards Association (CSA) Z-809 2016 standard

requirements, respectively.

Harvesting

The Authority operated into the 2021-22 operating year under the approved 2010-2020 Forest

Management Plan for the Algonquin Park Forest (plan extension and short-term contingency plan) for

2021-2022 operations until the new 2021-2031 forest management plan was approved in August for

implementation in September. The approved forest management plan states that a sustainable annual

harvest of 783,075 cubic metres (m3) is available from the forest. The Authority’s operations have

produced an average of 413,000 m3 over the previous five years. The 2021-2024 AFA Agency Business

Plan set out a target of 500,000 m3 for 2021-2022 based on evidence of an improving economy and the

desire to grow the business to better achieve objectives. Meeting the financial portion of the budget

requires achieving over 85% of this volume target or securing better sales rates for our products.

The 2021-2022 harvest from the forest was 348,205 tonnes, or 364,852 m3 (source: AFA Sales System),

which is well within the sustainable level that the Algonquin forest can provide but is less than the

previous year’s harvest of 395,969 tonnes.

Harvest levels are tracked in-year by the sales unit of measure, mostly green metric tonnes (tonnes),

which is the unit of measure most used by clients for payments. This year, sales were also made in

board-foot-measure (fbm), Ontario log rule and net cubic metres. Mathematical conversions from

tonnes and fbm to net cubic metres (m3) are made at year-end (March 31) for consistent reporting.

This will often differ from the volume harvested and reported in MNRF’s TREES wood measurement

7

system that reports net cubic metres by the year in which it is cut.

Operational Performance

Quarterly Sales Volume

The 2021-2022 fiscal year began in April with sales deliveries of wood harvested in the previous month.

Contractor start-ups were delayed until June by uncertain markets and rising costs of labour, insurance,

fuel and equipment. Procurement and budgeting became more complicated as some logging contractors

indicated they were leaving the business and others were cautious to commit until rising costs could be

assessed. First quarter (Q1) deliveries were still good at 102% of planned. Q1 performance this year

compares to 128% in the previous year, and similarly, was a result of the previous year’s inventories from

log yards that made it to market in Q1 (April, May, June).

Two area sawmills completed major renovations to improve lumber recovery from available supply, which

increased the demand for sawlog-quality white and red pine, but unfortunately AFA’s ability to produce could not

keep up to their needs. Efforts were made to balance the available supply amongst AFA clients. Replacing the

unplanned loss of productive capacity requires the Authority to focus on growing and supporting existing

contractors and recruiting new contractors. Affordability of operations has always been challenging, but

demographics, supply chain insecurities, fuel and labour costs have added to the complexity of issues.

Two sawmills, one in Huntsville, and the other in South River, were recently purchased by, and added to the

holdings of a sawmill in the Haliburton area. The purchase has been combined with investment in these mills and

renewed interest in timber allocations in the western portion of Algonquin Provincial Park. The increased

utilization of AFA wood supply on the west-side of the park in 2022 helped to offset some of the Authority’s lost

production.

Demand for sawlogs of all species from Ontario mills improved and combined with reduced harvest and

production levels, there was much less need to market summer-cut pine into Quebec to keep contractors

engaged. Summer weather was uneventful and amenable to steady harvest levels and sales. TKL in

Temiscaming, Quebec was the only mill receiving pulpwood produced from the forest and their

commitment was the only one that could be counted on for most of the year. Where possible clients

agreed to purchase timber in tree length form to help utilize pulpwood and access sawlogs. This had a

negative effect on producing hardwood veneer because sawlog recovery for sawmills was the primary

objective of most clients.

Q2 sales of 80%, compares to last year’s 74% of planned. By this quarter, the Authority was engaging

fewer contractors (see next page) but sales to local mills increased. Transportation cycle times to local

mills improved with the shorter haul distances and typically facilitates small increases to harvest levels.

Relatively good weather conditions prevailed into the Fall, but no additional harvest capacity could be

added. The cost of fuel rose dramatically during Q3, and the Authority took action to protect contractors from

the volatility and risk. This had an impact on revenues until a fuel compensation program could be arranged

with receiving mills in Q4. Sales in Q3 were similar to last year and the Authority achieved 65% of planned sales

compared to 61% in the previous year.

Snowfall accumulation was near normal and few freezing rain events occurred which allowed steady

production and deliveries (sales) throughout the winter. Q4 performance of 61% of the planned harvest

sales volume compares to 87% in the previous year and represents the reduction of capacity to produce

wood for sale in the final quarter of the year. This is the time of year that most of the higher value pine

8

sawlog volume is harvested and sold.

Overall sales volume performance for the 2021-22 year was 70% of the 500,000 m3 planned sales volume

and 89% of the budgeted sales volume target (410,000 m3) required to achieve financial targets.

Approximately 23,000 tonnes of timber were inventoried to be sold at market as soon as road conditions

would allow in April and May of the next fiscal year. Most of this volume is attributed to west-side

hardwood operations that were unable to clear landings before Spring break-up.

Contractor (Productive) Capacity

AFA’s objective to grow the business to better achieve its mandate requires implementation of key

operational strategies to increase contractor capacity to produce volumes for sale. Strategies include

lengthening the operating season (early-starts, building inventories for inclement weather and the spring

break-up period), advanced planning, advanced road building, tree marking, merchandizing yards, and

developing new/additional road building and logging contractors. These strategies represent significant

investment of human and financial capital and are at various stages of development in any given year.

Demographics and the pandemic-caused supply chain disruptions have countered efforts to attract

growth in this sector.

The Authority’s contractor workforce represents significant employment and economic value to the

area. Combined with workers in area mills, the workforce totals just under 285 jobs over the course of a

year (Feb 2021 AFA Employment Survey). This year’s roster of logging contractors changed dramatically

with the loss of one large and two smaller contracting companies. The Authority was able to engage only

six contractors in the first half of the year, increasing by one in each of Q3 and Q4 for a total of eight

compared to nine last year and to twelve the year before.

The Authority retains a professional and responsible work force to achieve its objectives and as such

actively promotes safe and effective work practices. W. F. Dombroski and Sons Logging Contractors Ltd

of Barry’s Bay, ON was awarded the annual Safety Award for the 2021/22 season amassing an impressive

57,730 person hours with no lost time accidents and no medical aids. They also managed to produce 1.5%

more volume than last year which was their highest production year so far.

In addition to the safety award, AFA and the contractors administer an “Environmental and Safety Award

System” that recognizes positive work practices. Based on a monthly score card for logging contractor

operations, including road building and hauling sectors, the top performing contractors and their workers

are formally recognized. All operations show a trend of continual improvement.

Product Sales

Sales volume in 2021-2022 was much less than planned (70%), and less than achieved in the previous year

(83%). Sales revenue during the year was projected to be sufficient to sustain forecasted program costs,

however in- year adjustments to compensate for rising costs, especially fuel, had to be made.

Pine sawlogs and poles generate more operating margin because they command a better price at

market and approximately 80% of the tree generates sawlog and better material. A hardwood tree

typically contains fewer sawlogs (20-30%) and generates narrower margins because of the higher

proportion of lower value wood (pulpwood, firewood) in the tree. A shift of markets and species mix,

and product proportions can have a significant impact on achieving financial targets.

9

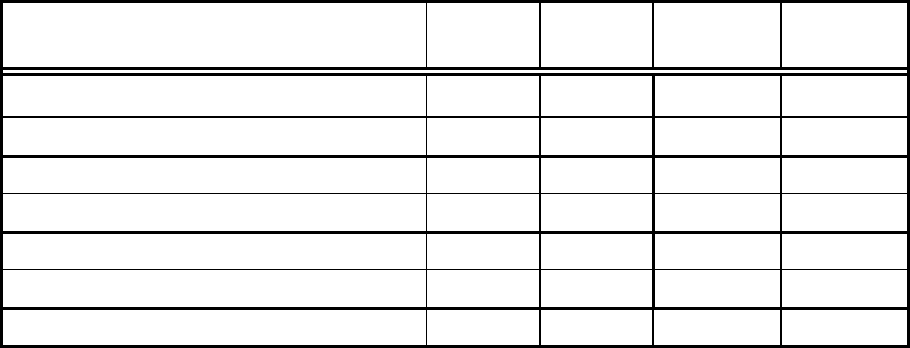

Species and product mixes are compared in the chart below to the previous year that concluded with a

positive financial position on March 31, 2021. This year’s species/product mix shifted to proportionally more

hardwood and much less veneer. The lower overall total and fewer higher value products is reflected in

the year end deficit financial position. This is discussed in the Financial Results section beginning on page

12.

Comparison of Annual Sales Volume (m3) by Broad Species Groupings and Product Categories

Species/Product

2020-2021

% of Cut

2021-2022

% of Cut

Conifer Sawlogs (pine, spruce, hemlock, cedar) 145,951 35%

117,800 32%

Hardwood Sawlogs (maple, beech, oak, poplar, birch) 67,081 16%

67,207 18%

Conifer Pulpwood 24,744 6%

16,262 4%

Hardwood Pulpwood 161,964 39%

144,952 40%

Red Pine Poles 16,188 4%

18,465 5%

Veneer 1,280 0.3%

166 0.04%

Total 417,208

364,852

Forest Management

The approved 2021-2031 Forest Management Plan (FMP) for the Algonquin Park Forest details the goals,

objectives, and strategies for the ten-year period. Operations in 2021-2022 were conducted under an

approved short term plan extension from April to June, a short-term contingency plan from July to

September and under the 2021-31 FMP after its completion and approval in September 2022. Forest

management activities in Algonquin Park must follow FMP prescriptions and within the FMP framework.

Targets set out in the FMP are further refined in the Agency Business Plan (see the following table) as

required to reflect operational realities such as actual harvest levels.

AFA’s Sustainable Forest Management Plan (CSA SFM certified) was rewritten in 2017/18, underwent a re-

registration audit in September 2018 and subsequent surveillance audits in 2019, 2020 and 2021. No non-

conformances were identified in the latest 2021 surveillance audit and certification to the CSA Z809-16

standard has been maintained.

Forest management activities such as prescription setting and tree marking occur in advance of

harvesting and need to be of sufficient area to support logging activities for the year. Forest

management activities are carefully implemented to rely on some of the previous year’s “banked” areas

and not invest too far in advance. Contractor capacity to carry out planned activities continue to be

impacted by COVID-19-related labour and supply chain challenges, particularly in tending and site

preparation operations.

Forest management also includes forest renewal (silviculture) activities conducted on areas that have

been harvested. The only exception is tree marking that is a pre-harvest treatment. Target setting and

budgeting, therefore, are based on the forests needs or post-harvest stages of development. The

following section briefly outlines forest management performance targets and achievements.

10

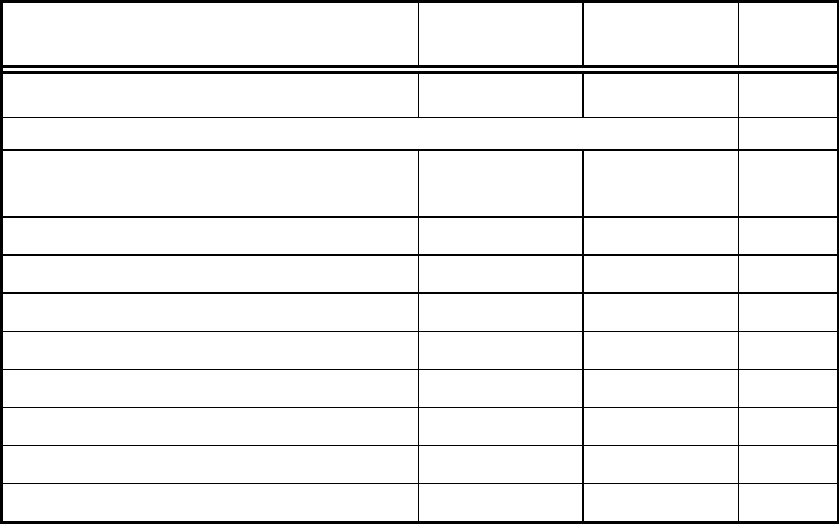

Operational Performance

AFA Harvest & Forest Management Programs – 2021-2022 Budget versus Actual

Program

2021-

2022

Budget

2021-

2022

Actual

% of

Target

Harvest (m3) 410,000

364,852 89%

Silvicultural Activities

Silvicultural Effectiveness Monitoring Surveys

(ha)

2,000

1,921

96%

Scarification (ha) 50

0

0%

Site preparation (ha) 455

406 89%

Stand Improvement (ha) 3,000

1,624 54%

Tending (ha) 1,500

881 59%

Tree marking (ha) 8,000

6585 82%

Tree planting

(# trees ‘000s) 420

689 164%

Tree planting stock (‘000s) 330

800 242%

Tree seed collection (hl) 45

0 0%

Silvicultural Effectiveness Monitoring

Regeneration assessments were conducted on nearly 2,000 hectares to ensure that regeneration

treatments are progressing as planned. Results of ‘Free to Grow’ assessments are reported in the

Management Unit Annual Report to MNRF in November each year and available to the public. All

selection management areas receive tree marking audits to ensure appropriate results to

predetermined standards but are not included in the reported monitoring figures. Regardless of the

prescribed harvest systems, the actual annual monitoring is reflective of harvest progress and

scheduling of treatments and does not include surveys completed to determine plantation survival.

Annual targets are usually a refinement of FMP targets based on additional information and a better

understanding of actual harvest depletions, stage of management and survey timing. This year’s

achievement saw 96% of planned area completed.

Site Preparation, Tree Planting and Scarification

A total of 689,437 tree seedlings were planted on 538 hectares in 2021/22 representing a target

achievement of 164%. Average density for the 2021/22 tree plant was approximately 1,280 trees per hectare

which is slightly higher than traditional. The tree planting program and stock purchases for future years

were increased in-year because of higher planned densities and more site preparation on pine shelterwood

areas to be completed in 2021/22 and 2022/23.

Forest management reporting conventions differentiate between site preparation for artificial

regeneration (planting) and scarification for natural regeneration. Both treatments employ the same

equipment to expose mineral soil for seeding or to create plantable spots. Site prepared areas may be

deferred from planting if they demonstrate high potential to regenerate naturally during good seed

years. Approximately four hundred and six hectares were site prepared for planting in future years,

representing 89% of planned levels, with zero hectares of scarification completed. Area scheduled for

11

site preparation is guided by post-cut needs and stock ordered for the upcoming season to ensure site

prepared areas are planted expeditiously post treatment.

Private nurseries are growing approximately 800,000 seedlings under contract with AFA for planting in

upcoming years. Trees planted in Algonquin Park are grown from seed sources appropriate for planting

within the park. No seed was collected during 2021-22 as there were few opportunities due to an

unusually poor cone year. A review of stored seed inventories reveals sufficient volume of seed for our

near-term growing stock needs.

Tree Marking

To implement forest management systems in Algonquin Park it is first necessary to designate which

trees are to be harvested and which ones are to be retained, while protecting other resource values. This

is completed by trained and certified tree markers who follow the prescriptions prepared by Registered

Professional Foresters in the Forest Management Plan. Tree marking is directly related to annual

harvest levels and with reduced contractor and labour capacity during the 2021-22 year the result was

lower than anticipated area tree marked. Tree marking was carried out on approximately 6585 hectares

in 2021-22 representing 82% of business planned levels and was sufficient to provide for the actual area

harvested and getting a head start on marking for the next operating year.

Tending and Stand Improvement

Manual tending was performed on 311 hectares to release established white pine and red pine

regeneration from competing vegetation. A further 570 hectares of even-aged understory improvement

work was completed to improve light conditions for regeneration establishment. This represents 59% of

the annual planned tending area. Stand tending is directly related to yearly harvest levels and during 2021-

22 there was less than anticipated area that received tending primarily because of reduced harvest

coupled with labour shortages to perform some of the manual tending work that is performed post-

harvest.

Stand improvement was completed on 1,624 hectares to assist growth of residual trees and natural

regeneration in areas managed under the selection system. This represents 54% of business planned

levels. Area available for stand improvement fluctuates with hardwood selection harvest areas,

influenced by 2021/22 market preference towards softwood and subsequent lower than anticipated

hardwood area harvested. Stand improvement may be carried out concurrently with harvest operations,

without the need for renewal account funding, such as when firewood and pulpwood markets are strong.

Only funded stand improvement is budgeted and reported.

The Authority is satisfied with its operational and forest management performance relative to 2021/22

harvest levels when considering the various complications through the past two years, ultimately

resulting in lost contractor capacity and reduced harvest levels. Development and revision of targets to

ensure achievement of FMP targets are completed annually within the business planning, work planning

and budgetary processes.

12

FINANCIAL RESULTS

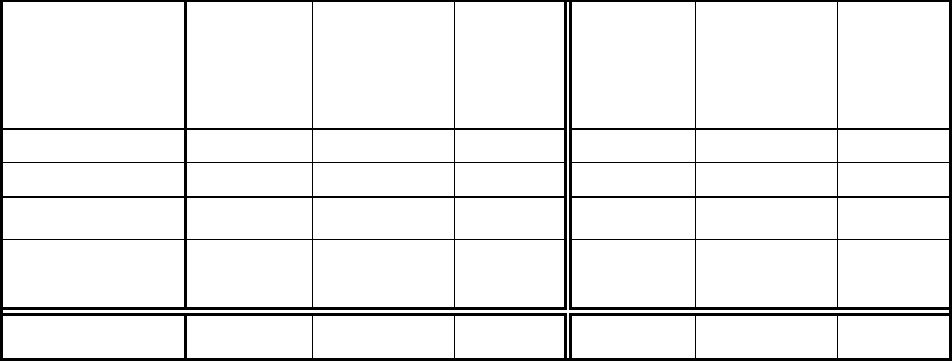

AFA Financial Performance – 2021-2022 Budget versus Actual

2021/22

Budget

General Fund

$ (000s)

2021/22

Budget

Renewal Fund

$ (000s)

2021/22

Budget

Total

$ (000s)

2021/22

Actual

General Fund

$ (000s)

2021/22

Actual

Renewal Fund

$ (000s)

2021/22

Actual

Total

$ (000s)

Revenue

25,550

2,550

28,100

23,304

1,979

25,283

Expense 23,200 1,950 25,150 21,598 1,660 23,258

Operating Income 2,350 600 2,950 1,706 319 2,025

Administrative &

Other

2,280 510 2,790 1,863 255 2,118

Net Income <Loss> 70 90 160

(157)

64 (93)

Harvesting and the Statement of Operations

The following commentary references financial information in the Audited Financial Statements and are

summarized in the table above to compare with budgeted targets. The budget is based on achieving

85% of the business plans’ target volume and with estimates based on values from the previous year’s

margins, species and product mixes. The year over year vagaries of markets and weather weigh on

expectations of results achievable on March 31. The Authority manages year over year profit/losses

while achieving the objective of financial self-sufficiency over the longer term. This year’s loss of

$93,448 combines with previous year’s profits/losses resulting in a positive balance of $262,330 over the

past five years (AFA Annual Reports 2017-18 to 2021-2022).

Operating revenues for the year were $25,282,988 which represents a decrease of $2,338,822 or

8.5 % compared to 2020/21 and about over $2.8 million less than budgeted.

Demand and our ability to supply contractor produced forest products decreased by about 14.7% during

the year and slightly higher stumpage and selling prices were achieved resulting in a 9.62% decrease in

product sales dollars. Standing timber sales volumes increased significantly in 2021/22 (60.85%) as

required mill volumes (Almaguin, Huntsville and Haliburton mills) were obtained by the parties from

inside our forest management unit.

"Other revenue" of $2,228,807 as compared to $2,391,317 in 2020/21 has been itemized in Note 8. The

majority of the decrease relates to the reduction in interest charged on overdue accounts receivable.

The timelier payment of amounts due to the Authority has had a positive impact on cash balances.

Costs for contracted production, direct labour and stumpage were higher than the previous year due to

higher stumpage rates and contractor costs. Combined with slightly lower spending on public access

road maintenance and increased cost of operations planning, the results show a decrease in operating

income to $2,025,053 as compared to $2,513,666 in the previous year. Operations planning costs

associated with our Environmental Management System, certification and the FMP process were

$307,911 as compared to $225,795 in the previous year.

Administration costs for the year were $2,118,501 which represents a decrease of $323,959 or 13.3%

13

compared to 2020/21. The decrease is primarily related to the retirement of some long-term employees

and the reduced cost of new employees at the lower end of the approved pay grids.

Forest Renewal Fund

The method of accounting for Crown Stumpage reflects the requirements of the Crown Forest

Sustainability Act. The forest renewal portion of the Crown Stumpage Matrix is retained by the

Authority, in trust for the Crown, and is to be used to fund eligible forest renewal work on a cost

recovery basis. The forest renewal revenue of $1,566,771 ($1,793,270 in 2020/21) from stumpage

represents amounts charged by the Ministry to customers during the year for renewal fund purposes.

Lower sales volumes of about 10.8% did result in lower renewal revenue and because of changes in the

species mix, in particular pine volumes that were down over the previous year, the overall renewal

revenues were down by 12.64%. There were no changes made to the species unit renewal rates in the

year.

Actual allowable forest renewal expenditures incurred during the year amounted to $1,915,323 as

compared to $2,112,635 in 2021. This decrease was related to the decreased direct program costs.

Total revenue in the renewal fund of $1,566,771($1,793,270 in 2020/21) has been sufficient to cover the

costs of renewal operations and administration in this period. A surplus of $63,687 is lower than the

surplus of $69,130 in 2021

Financial Position- Balance Sheet

The Statement of Financial Position disclosure reflects disclosure requirements affecting government

not-for-profit organizations, such as the Authority, recommended by the Canadian Public Sector

Accounting Standards including the 4200 standards for government not-for-profit organizations. Funds

received in advance of the planned expenditure are disclosed as "Deferred Contributions" and amounts

once referred to, in a single disclosure component, as "Retained Income" have been disclosed as

threeseparate components of ‘Net Assets'. This disclosure clarifies the restricted/unrestricted nature of

our net asset position.

At March 31, 2022, our cash was $3,119,511 higher and our accounts receivable balance was $3,016,243

lower than the previous year balances. This change resulted from greatly improved customer payment

patterns and a slightly earlier end of year operating season that resulted in higher cash and lower

accounts receivable.

March 31 payables and accruals were higher by $269,755 compared to 2020/21 most of which relates to

amounts due one contractor who delivered all their inventory just prior to the year end and these

monies were owed and included in the accounts payable.

The Renewal Account balance of $3,614,982 ($3,551,295 in 2021) remains well above the minimum

required balance of $1,500,000.

Audited Financial Statements

The Auditor General of Ontario is the auditor of record for the Authority. The auditor’s report and

accompanying financial statements for the 2021-22 fiscal year can be found at

Annual Reports |

Algonquin Forestry Authority

14

ACHIEVEMENT OF STRATEGIC OBJECTIVES

This Annual Report is the second report summarizing achievement of strategic objectives from the

Authority’s 2020-2030 Strategic Plan and follows through on the commitment to report progress

toward achieving the Strategic Plan’s five key measures.

Operational Excellence

• Forest Management Results – achieve FMP/business plan targets with rationale.

o Achieved only 70% of the business-planned harvest level. Productive capacity and lack of

pulpwood markets are the core limiting factors. Seeking harvest capacity additions and

creating opportunities for growth is on-going. In-year adjustments to programs were made

to match forest management and other business levels to reduced harvest levels.

o Similarly, silviculture target achievement was reasonable considering harvest levels. A

shortage of skilled contractors continues to affect delivery of projects. Progress is being

made to increase silvicultural contractor capacity with plans to finish carry-over projects

during the 2022/23 season. The tree plant program was increased to catch up on

previously harvested (mostly pine) areas with correspondingly reduced tending and

stand improvement (hardwood) programs.

• Positive Financial Results – demonstrate Agency financial self-sufficiency

o Achieved 89% of financial budget with a negative bottom line that is still manageable given the

Authority’s overall financial position.

o Improved receivables account and cash on hand.

o Balanced annual renewal revenues and expenditures.

• Environmental and Sustainable Forest Management System - performance including results

of audits.

o The summer Internal audit was completed and findings entered for action. This helped

prepare the AFA for the annual surveillance audit (S3) later in the fall. The S3 audit completed

by a new Registrar (KPMG) had zero (0) findings of non-conformance with only two (2)

Opportunities for Improvement and four (4) good practices identified.

o At year-end there were no unresolved forest compliance issues. Operational issues and

remedies were fewer.

Continual improvement continues to be demonstrated. The

Authoritys’ ESFMS will be maintained and used to support shifting SFM certification

from the CSA standard to the Sustainable Forestry Initiative (SFI) forest management

standard.

Advancing Innovative Practice

• Savings or gains through investment – research and innovation.

o Supported field program (admin, procurement, logistics) to collect data to support LiDAR

acquisition on French-Severn and Algonquin Park Forests. Supports use of new

technology for forest inventories.

o Continued utilization of VPN and other support for people working from home. Meetings

held virtually. Savings of travel and accommodation costs.

o Continued use of 3D workstations acquired in 2019 for FMP allocation exercises and

operational planning – reduced expensive field time.

15

o Utilized GPS trackers for graders. Realized gain in productivity.

• Partnerships developed to support research and innovation.

o Contributed to CRIBE/NextFor wood utilization projects

o Participated with MNRF and OFIA to support eFRI program and acquisition of LiDAR ground

data.

o Contributed to FMPM Revision project and FMP Advisory Group, Scaling Manual Advisory

Group and the Provincial Forest Inventory Advisory Committee.

• Research and innovation projects initiated.

o 2021 Employment Survey completed.

o Support for KTTD projects (tech development and transfer projects) provided to

accelerate the delivery of a LiDAR enhanced Algonquin Park FRI and build forest

structure models from ground sourced and LiDAR data.

o Use of UAV for low level aerial reconnaissance is being investigated.

o Manual tending operations to promote regeneration of other species in beech bark disease infested

areas has been initiated with support funding from Forestry Futures Trust and help from the Ontario

Forest Research Institute.

Developing and Supporting Our People

• Worker engagement.

o New ways to communicate with staff and contractors were developed during the pandemic:

newsletters, bi-weekly teleconferences, video conferencing, outdoor-distanced meetings.

o Incentive awards for contractors were maintained during the pandemic. The 2021-22

results were shared by email letter. The newsletter also provided AFA program updates,

compliance awareness and notice of upcoming training.

• Worker attraction and retention.

o Contract staff positions were maintained, communicated upcoming recruitment initiatives.

o Supported staff working from home – work/life balance, accommodation.

o Active succession planning and management in progress. Several leadership development strategies

have been implemented to prepare for potential near-term vacancies.

• Job security and competitive compensation.

o Competitive salary project reviewed by AFA Board, and analyses is planned for 2022. Grid is current to

June 2022.

o Longer term contract and seasonal contract positions are maintained for career

development, fluctuating workloads, and protection of the core organizational structure.

• Participation in training and recognition.

o Tree marking certification training is back on track after the pandemic caused hiatus – several AFA

attended Level 2 and refresher courses..

o New “Safe Driving on Forest Roads” training rolled out to staff and written into AFA

policy.

o Staff engagement survey conducted and used to develop Wellness Day programme.

o Wellness Day 2021 held with all staff. Included respectful workplace training, program

updates, H&S training and open discussion.

16

o Electronic ESFMS training matrix and records reviewed, updated and system revised to

improve utility. Plans to expand the system to other aspects of AFA staff training have

been initiated.

Indigenous Partnership

• Indigenous Community Engagement.

o AWS, FMP and FMP Planning Team engagement have been conducted and/or underway.

Pandemic related community engagement has required more virtual meetings.

• Indigenous people attending training facilitated by AFA.

o AFA representative attended 2021 Hunt Monitor session to review AFA forest activities and hunt

signage. Seven monitors and five ANR attended.

• Staff and Board members receiving Indigenous cultural awareness training,

o Three staff completed training online. Board of Directors have initiated a different approach.

o Cultural awareness is recognized as part of interaction between AFA and Indigenous communities.

• Projects involving Indigenous communities in the local forestry sector.

o Preliminary business development discussions have occurred with the Algonquins of

Pikwakanagan First Nation resulting in an application for federal funding to conduct a

forestry business opportunity project that AFA would help design and implement.

o Supported start-up of two Indigenous tending contractors. Both indicate they will return for

another season.

o Currently developing one logging contractor new to AFA in 2018.

o Birch bark collection facilitated by AFA tree markers resulted in cultural benefit and

training opportunities.

Supporting Local Industry

• Wood using mills, logging operators, silviculture and other contractors engaged.

o Demand from Ontario mills and under-production has limited use of the full roster of

wood using mills developed over the last two years.

o Fewer logging operators engaged than last year, but three have grown to produce more

volume. New entries and expansion opportunities are being examined.

• Annual utilization of prescribed sustainable annual harvest level (739,067 m3).

o Year over year improvement is the goal.

o 364,852 m3 is less than last year’s 417,207 m3. The pandemic, pulpwood markets and

productive capacity were factors.

• New jobs in wood mills and logging operations as a result of business with AFA.

o Clients report challenges with finding reliable workers for available positions. Two mills indicate

wanting to add another shift but need more wood supply to support.

o A jobs survey was completed in February 2021. According to the survey, there are 285 people

employed in Algonquin wood’s activities and over 4,000 people employed in the mills receiving wood

from the Algonquin Park Forest and tree nurseries that provide seedlings for renewal.

o This represents a loss of jobs in the woods of about 15, likely a result of mechanization.

o The increase in people at mills and nurseries of about 700 jobs is the effect of adding more

facilities to our sales program.

17

PUBLIC APPOINTMENTS – BOARD of DIRECTORS

DATE OF FIRST APPOINTMENT

CURRENT TERM’S

EXPIRATION

CHAIR: David Lemkay

Douglas, ON

September 12, 2012 October 16, 2022

Sarah Bros

North Bay, ON

February 1, 2013 February 3, 2024

Gordon Clark – Vice Chair

Coldwater, ON

June 30, 2016 July 8, 2023

Carl Corbett

Huntsville, ON

June 22, 2016 June 5, 2022

Robert Howe October 25, 2019 October 24, 2022

Barry’s Bay, ON

Damion Ketchum

Toronto, ON

August 4, 2016 September 25, 2022

Charles Lauer

Peterborough, ON

January 5, 2015 February 4, 2024

Rodney Smith

Arnprior, ON

August 4, 2016 August 15, 2022

The total remuneration paid to Directors for this fiscal period is $17,844.

OFFICERS: Jeffrey W. Leavey Timothy K. Doyle, CPA, CA

General Manager Secretary-Treasurer

2021-2022 GENERAL MEETINGS:

May 7, 2021

Video Conference

June 25, 2021

Video Conference

September 10,

2021

Video Conference

October 29 & 30, 2021

Huntsville, ON

Decemberer 10, 2021

Video Conference

January 25, 2022

Video Conference

February 4, 2022

Video Conference

18

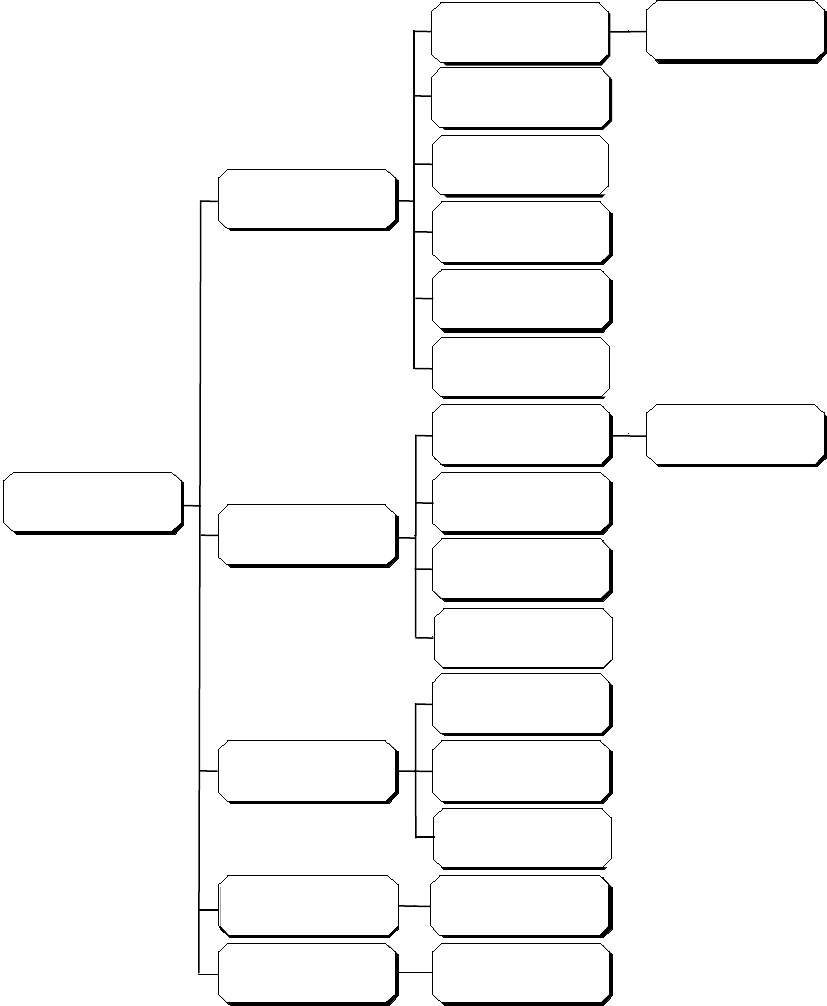

ORGANIZATION CHART (Full-Time, Regular Staff as of April 1, 2021)

Gord Cumming, RPF

Chief Forester

Vacant

Wood Measurement Clerk

Jessica Condon

Financial Officer

Jim Turney

Operations Supervisor

Dane Brown

Operations Supervisor

Tracey Bradley, RPF

Area Forester

Amy Vanderwal

Administrative Assistant

Jeff Driscoll

Operations Supervisor

Ryan Lake

Operations Supervisor

Tom Dolan, RPF

Area Forester

Jack Massey

Forest Technician

Evan Dombroskie

Woodland

s Supervisor

Stephen Bursey, RPF

Manager of Operations/

Pembroke

Shanagh Hore

Operation

s Supervisor

Vacant

Forest Technician

Jeff Leavey

General Manager

Keith Fletcher, RPF

Area Manager

Marty Laflamme

Woodlands Supervisor

Tim Doyle, CA

Treasurer

Cindi Sandiland

Administrative Assistant

Rob McPhee

Supervisor

of Information

and Communication

David Webster

GIS Officer

Shaun Dombroskie, RPF

Monitoring & Measurement

Supervisor

19

Algonquin Forestry Authority

8 Crescent Road, Unit B3-1 84 Isabella Street, #7

Huntsville, ON P1H 0B3 Pembroke, ON K8A 5S5

Tel: 705-789-9647

Fax: 705-789-3353 Tel: 613-735-0173

Fax: 613-735-4192

Huntsville.office@algonquinforestry.on.ca pembroke.office@algonquinforestry.on.ca

This publication is available in French upon request.

Sur demande, vous pouvez obtenir la version française de ce rapport annuel.