AFFORDABLE MORTGAGE

LENDING GUIDE

A Resource for Community Bankers

Part I: Federal Agencies and Government Sponsored Enterprises

Revised July 2018; Freddie Mac revised November 2018

PUBLISHED BY:

Federal Deposit Insurance Corporation

550 17th Street, NW, Washington, DC 20429

877-ASK FDIC (877-275-3342)

The Federal Deposit Insurance Corporation (FDIC) does not endorse the programs described in this publication or

any particular approach to their use. The overviews and program information included in this Guide are designed

to illustrate the broad range of options available to nancial institutions. The FDIC has taken measures to ensure

that the information and data presented in this publication is accurate and current. However, the FDIC makes no

express or implied warranty regarding such information or data, and hereby expressly disclaims all legal liability and

responsibility to persons or entities who use or access this publication and its content, based on their reliance on

any information or data that is available through this website. Each institution is responsible for assessing whether

the resources presented here are appropriate for the bank to pursue given factors such as the institution’s existing

mortgage, Community Reinvestment Act, or community development strategies, as well as business focus, nancial

condition, and market.

When citing this publication, please use the following:

Affordable Mortgage Lending Guide, Part I: Federal Agencies and Government Sponsored Enterprises

(Washington, DC: Federal Deposit Insurance Corporation, 2016; revised 2018), https://www.fdic.gov/mortgagelending.

AFFORDABLE MORTGAGE

LENDING GUIDE

A Resource for Community Bankers

Part I: Federal Agencies and Government Sponsored Enterprises

Revised July 2018; Freddie Mac revised November 2018

TABLE OF CONTENTS

About This Publication.................................................................................................................1

Program Matrix.............................................................................................................................4

U.S. Department of Housing and Urban Development (HUD) and

Federal Housing Administration (FHA).....................................................................................5

Overview of the Federal Housing Administration .............................................................. 5

Doing Business with FHA ....................................................................................................... 7

Using FHA’s Section 203(b) Mortgage Insurance Program:

A community banker conversation .....................................................................................11

Title I Programs

Property Improvement Loan Insurance ..............................................................................13

Manufactured Home Loan Insurance .................................................................................17

Title II Programs

203(b) Mortgage Insurance Program .................................................................................21

Streamline Refinance ............................................................................................................27

203(k) Rehabilitation Mortgage Insurance ........................................................................31

Other HUD Programs

184 Indian Home Loan Guarantee Program......................................................................35

Good Neighbor Next Door..................................................................................................41

U.S Department of Agriculture (USDA)...................................................................................45

Overview ................................................................................................................................45

Doing Business with USDA ..................................................................................................46

Using USDA’s Single Family Housing Guaranteed Loan Program:

A community banker conversation .....................................................................................49

Single Family Housing Guaranteed Loan Program...........................................................51

Single Family Housing Direct Loans ...................................................................................55

Single Family Housing Repair Loans and Grants ..............................................................59

U.S. Department of Veterans Affairs (VA) ...............................................................................65

Overview ................................................................................................................................65

Doing Business with VA .......................................................................................................66

Using VA’s Home Purchase Loan Program:

A community banker conversation .....................................................................................69

Home Purchase Loan Program ............................................................................................71

Interest Rate Reduction Refinance Loan.............................................................................75

U.S. Department of the Treasury Community Development

Financial Institutions Fund (CDFI Fund) .............................................................................79

Overview ................................................................................................................................79

Bank Enterprise Awards .......................................................................................................83

CDFI Program ........................................................................................................................85

Capital Magnet Fund ............................................................................................................89

Fannie Mae..................................................................................................................................93

Overview ................................................................................................................................93

Doing Business with Fannie Mae ........................................................................................94

Duty to Serve..........................................................................................................................96

Using Fannie Mae’s HomeReady™ Mortgage Product:

A community banker conversation .................................................................................. 101

HomeReady™ Mortgage .................................................................................................. 103

Standard 97 Percent Loan-to-Value Mortgage............................................................... 107

HomeStyle® Renovation Mortgage ................................................................................. 111

Standard Manufactured Housing Mortgage .................................................................. 117

MH Advantage™................................................................................................................ 123

Refi Plus™/Home Affordable Refinance Program (HARP)............................................ 127

Freddie Mac ............................................................................................................................. 131

Overview ............................................................................................................................. 131

Doing Business with Freddie Mac.................................................................................... 132

Duty to Serve....................................................................................................................... 133

Using Freddie Mac’s Home Possible® Product:

A community banker conversation .................................................................................. 137

HomeOne

SM

......................................................................................................................... 139

Home Possible®.................................................................................................................. 143

Construction Conversion and Renovation Mortgage.................................................... 147

Manufactured Home Mortgage ....................................................................................... 151

Relief Refinance

SM

/Home Affordable Refinance Program (HARP)............................... 155

FDIC’s Community Affairs Program ...................................................................................... 159

Glossary & Terms ..................................................................................................................... 161

ABOUT THIS PUBLICATION

Economic Inclusion and Opportunity

Mortgage lending is an important element of many

community banks’ business strategies. Community

banks offer mortgage products and services designed

to meet the particular needs of their communities,

including rural areas and low- and moderate-income

(LMI) borrowers. Offering affordable mortgage loans

to a wide range of customers deepens bank-customer

relationships and provides an important pathway for

borrowers to own their own homes and build wealth.

At the Federal Deposit Insurance Corporation (FDIC),

we recognize that mortgage lending is also an impor-

tant way for insured institutions to promote access and

participation in the mainstream banking system. Broad

participation in the products and services offered by

insured institutions promotes stability and condence

in the nancial system, which is the core mission of

the FDIC.

Many banks, including community banks, take advan-

tage of the opportunities to serve the particular

mortgage credit needs of their communities. The

Affordable Mortgage Lending Guide (Guide) provides

information to help make community bankers aware

of the wide range of current affordable mortgage

products. These programs can be important resources

for community banks when properly managed. Bank

management should understand the terms of these

programs, the risks they pose, and the impact on

banks’ nancial condition to ensure that they are serv-

ing their communities with prudently underwritten

and affordable mortgage products.

Outreach and Communication

To determine how the FDIC could contribute to efforts

by banks to offer prudently underwritten, affordable,

and responsible mortgage credit for LMI households,

FDIC staff met with community banks individually

and in small roundtables. Bankers provided valuable

insights into the need for affordable mortgage credit

in the communities they serve. They also discussed the

opportunities and obstacles to using federal lend-

ing programs, as well as the pros and cons of holding

loans in portfolio versus selling loans on the second-

ary market.

Some bankers described how they have harnessed

federal programs, sometimes in combination with

other nancial mechanisms like Federal Home Loan

Bank and State Housing Finance Agency products, to

expand their capabilities and serve a broader customer

base. Many banks had relationships with neighbor-

hood housing counseling organizations, which helped

provide nancial education to potential customers.

Some bankers discussed that very small banks do

not have specialized stafng or departments to offer

complex mortgage products. They decided that the

risk and cost of origination were not worth assuming

without more resources or additional risk mitigation.

Some bankers said that while they want to be involved

in mortgage lending, it was difcult to nd the time to

research potential programs, and that it was challeng-

ing to nd and retain trained mortgage staff, especially

in rural areas.

From these meetings, we concluded that community

banks might benet from a practical reference tool

to compare federal programs so they could make an

informed decision about which programs might be

the right t for their business plans and strategies to

improve lending options available for their communi-

ties. In addition, the experience of other lenders that

have found ways to use limited resources to harness

federal and other resources could provide practical

examples that may be instructive to institutions consid-

ering these opportunities.

1 | FDIC | Affordable Mortgage Lending Guide

Scope and Coverage

To assist community banks, the FDIC developed

the Affordable Mortgage Lending Guide (Guide),

which describes programs from the U.S. Department

of Housing and Urban Development (HUD) and

its Federal Housing Administration (FHA), the

U.S. Department of Agriculture (USDA), the U.S.

Department of Veterans Affairs (VA), the U.S. Treasury

Department’s Community Development Financial

Institutions Fund (CDFI Fund), and Fannie Mae and

Freddie Mac, known as Government Sponsored

Enterprises (GSEs). The Guide focuses on guarantee,

loan purchase, and subsidy programs that can facilitate

mortgage lending by insured depository institutions.

It includes federal programs that support home pur-

chase, renance, manufactured housing, and some

home improvement lending by banks. It covers pro-

grams that are targeted to a variety of communities

and individuals including rural, Native American, LMI,

and veterans.

We discuss the requirements of each program, as well

as how to access these programs. Whether you choose

to become an agent, a correspondent selling to an

aggregator, use a broker, or become an approved

seller-servicer, the Guide explains how each of these

options work within the particular program. We also

discuss underwriting tools available and provide tech-

nical information about borrower and loan criteria. This

Guide can help you design a process to identify, assist,

and support your customers by successfully leveraging

these programs.

Suggestions for How to Use This Guide

Organized by each federal agency and GSE, the

overviews and individual program descriptions

include information about doing business with the

agency, its program requirements, and tips on get-

ting started with the program. Institutions can use this

Guide as a one-stop resource to gain an overview of

a wide variety of program resources, compare differ-

ent programs, and to help identify the next steps for

program participation.

Each program description includes insights into the

program’s purpose, technical assistance on how to

participate, and identies potential benets and chal-

lenges for community banks.

TIPS ON USING THE AFFORDABLE

MORTGAGE LENDING GUIDE

• Review the “Contents” page for a list of

all programs.

• Read the overview for the federal agency

or GSE of interest to determine loan

delivery options and other criteria.

• Read the selected program description

for specific borrower and loan standards.

• Review “Similar Programs” at the end

of each description to compare program

requirements with other products.

• Review “Resources” to make sure you

have the most up-to-date information on

program criteria.

• Select a program that best suits your

needs and use the agency/GSE contact

information to get started.

A quick review of borrower and loan criteria will help

you identify whether the program is suitable for a

particular client or a population that you are trying to

serve, such as low- and moderate-income borrowers

or other hard-to-reach populations. The descriptions

identify particular criteria that focus on target seg-

ments, underwriting exibilities, and other standards.

Each program description includes contact informa-

tion and web links for easy access to program staff

who can provide additional information about the

program, guide you through getting started, and

address other specic requirements for starting the

program at your bank.

In order to compare a range of programs to identify

what best meets your needs and the needs of your

customers, each program description concludes with

a list of similar programs for your reference.

Resources are also included in each program

description where you can nd web links to more

FDIC | Affordable Mortgage Lending Guide | 2

detailed information about the programs provided

by the GSE or agency. Where secondary programs

(e.g., Community Seconds®) are mentioned within the

main program description, a link to that program is

also included in the Resource section. Finally, links for

additional information that are referenced in the

program descriptions — such as area/county loan

limits, building codes, and lists of high-cost cities and

states — are also included in Resources.

Because borrower and loan criteria, such as income

limits, minimum credit scores, loan-to-value limits, and

debt-to-income ratios, are all subject to change (and

in many cases revised annually), the Guide provides

the most recent information available. Realizing the

need for accurate and timely information, each pro-

gram description includes a list of web links where

updates can be found.

What Bankers are Saying

In addition to the individual meetings with com-

munity banks and small roundtable discussions, the

FDIC also talked with community bankers about their

participation in specic programs. In each federal

agency and GSE “Overview,” you will nd comments

by community bankers who are incorporating federal

and GSE programs into their overall mortgage lend-

ing strategies. Bankers discuss how they have used

these programs to support their business objectives.

They also discuss using a variety of delivery options

including serving as an approved third-party origina-

tor and working with other lenders and investors to

underwrite, package and sell loans; acting as a corre-

spondent lender; and becoming an approved seller/

servicer of mortgage loans.

Supporting strong Community Reinvestment Act

(CRA) performance

Affordable mortgage lending, including to low-and

moderate-income borrowers; to low-and moder-

ate-income census tracts; and to serve people in

underserved rural communities, on tribal lands, and

in disaster areas can be responsive ways for nancial

institutions to meet the credit needs of their commu-

nities. The mortgage programs featured in this Guide,

whether they result in Home Mortgage Disclosure Act

(HMDA) reportable loans or originations reported by

another lender, can help lenders reach their business

objectives in their communities, as well as contribute

to its CRA performance.

Conclusion

The programs outlined in the Affordable Mortgage

Lending Guide can provide community bankers with

additional pathways to provide homeownership

opportunities for creditworthy borrowers in their

communities, particularly those with affordability

challenges. These programs may also represent busi-

ness opportunities for community banks looking for

prudent, sustainable nancial products to incorporate

into their mortgage business line.

While home ownership continues to be a goal for

most Americans, many people struggle to gain access

to affordable homeownership opportunities that will

enable them to build a stable future for their families.

Community banks can and do play a valuable role in

meeting the demand for affordable mortgage credit,

and we hope this Guide provides useful information

to assist bankers in considering all the options to

serve their communities with prudently underwritten

and affordable mortgage products.

3 | FDIC | Affordable Mortgage Lending Guide

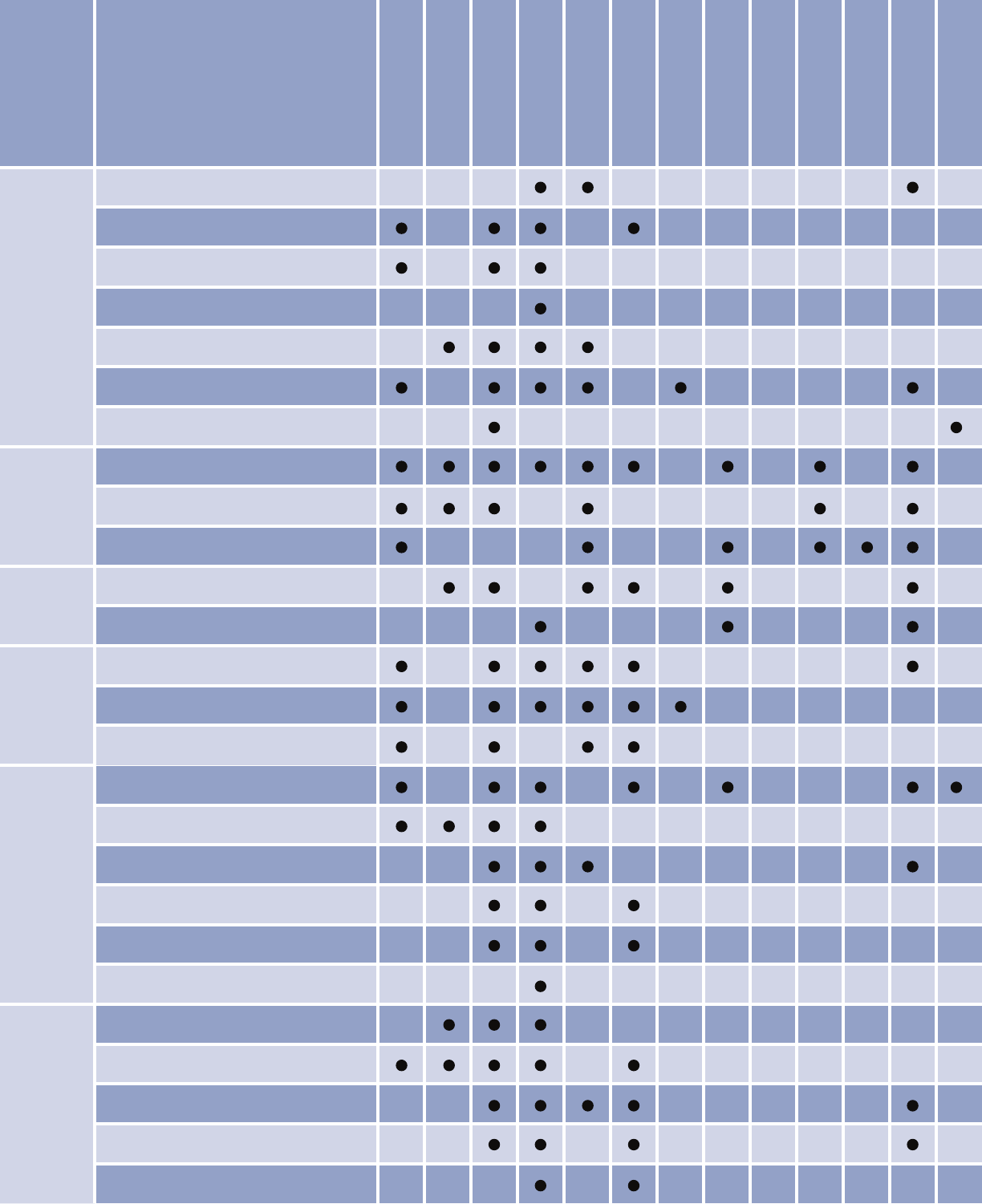

AGENCY PROGRAM NAME

LOW- AND

MODERATE-INCOME

FIRST-TIME

HOMEBUYER

PURCHASE

REFINANCE

REHABILITATION/

REPAIRS

MANUFACTURED

HOMES

NATIVE AMERICANS

VETERANS

VICTIMS OF A

DISASTER

RURAL

SENIORS

PERSONS WITH

DISABILITIES

PUBLIC SERVANTS

HUD/

FHA

FHA Title I: Property Improvement

Loan Insurance

FHA Title I: Manufactured Home

Loan Insurance

FHA Title II: 203(b) Mortgage

Insurance Program

247 &

248

203(h)

FHA Title II: Streamline Renance

FHA Title II: 203(k) Rehabilitation Mortgage

Insurance

HUD 184 Indian Home Loan Guarantee

HUD Good Neighbor Next Door

USDA

Single Family Housing Guaranteed

Loan Program

Single Family Direct Loans

variation variation

Single Family Housing Repair Loans

and Grants

VA

Home Purchase Loan Program

Tribal

land

Interest Rate Reduction Renance Loan

CDFI

FUND

Bank Enterprise Awards

CDFI Program

Capital Magnet Fund

FANNIE

MAE

HomeReady

TM

Mortgage

Standard 97 Percent Loan-To-Value

Mortgage

HomeStyle® Renovation Mortgage

Standard Manufactured Housing Mortgage

MH Advantage

TM

Re Plus

TM

/ Home Affordable Renance

Program (HARP)

FREDDIE

MAC

HomeOne

SM

Home Possible®

Construction Conversion and

Renovation Mortgage

Manufactured Home Mortgage

Relief Renance

SM

/Home Affordable

Renance Program (HARP)

If a program provides special consideration to a group or provides a certain type of housing, this is indicated in the matrix. It does not mean, for example,

that a veteran could not use Fannie Mae’s Home Possible® program, but rather, the veteran does not receive a special benet under the program.

OVERVIEW

U.S. Department of Housing and Urban Development

and Federal Housing Administration

We have included the most recent information available at the date of publication. At the end of each section,

we include a list of resources with web links where you can nd updates, as well as information about additional

programs and other helpful information related to the subject.

President Lyndon B. Johnson established the

Department of Housing and Urban Development

(HUD) in 1965 to confront the nation’s housing and

urban challenges. While there were a number of fed-

eral housing programs before HUD’s establishment,

HUD consolidated its oversight into a cabinet-level

agency. The mission of HUD is “to create strong,

sustainable, inclusive communities and quality afford-

able homes for all.” HUD funds and oversees a wide

range of community development and housing-

related activities aimed at preventing homelessness,

providing rental housing, ghting housing dis-

crimination, enhancing community and economic

development activities, and increasing homeowner-

ship opportunities.

The Federal Housing Administration (FHA), the larg-

est mortgage insurer in the world, is part of HUD. FHA

increases homeownership opportunities in the United

States by expanding mortgage nancing opportunities

and has historically provided stability to the housing

market during times of economic crisis.

OVERVIEW OF THE FEDERAL HOUSING

ADMINISTRATION

The FHA provides mortgage insurance that protects

lenders in case of borrower default. It predates the

secondary mortgage market, having been created

in 1934 as a way to stimulate the housing industry

during the Great Depression. Because FHA lending

parameters allow for higher loan-to-value ratios and

somewhat lower borrower credit scores than are typi-

cal for prime conventional loans, FHA has been an

important source of mortgage credit for households

that might otherwise nd it difcult to obtain this credit,

such as low- and moderate-income households and

rst-time homebuyers. FHA’s volume generally varies

based on the credit standards of other sources of mort-

gage nancing and on the fees it charges. Lenders are

protected by FHA’s Mutual Mortgage Insurance Fund,

which is sustained by borrower premiums.

FHA business is primarily conducted by four regional

Homeownership Centers, or HOCs, in Atlanta,

Philadelphia, Denver, and Santa Ana. Although lend-

ers should send their questions to the FHA Resource

Center (not the HOC) for immediate acknowledgement

and tracking, certain case-specic issues are subse-

quently referred to the appropriate HOC.

GINNIE MAE

Ginnie Mae is short for Government National

Mortgage Association. Ginnie Mae does not origi-

nate or purchase mortgage loans and does not

issue mortgage-backed securities (MBS). Instead,

Ginnie Mae guarantees investors the timely pay-

ment of principal and interest on MBS issued

by private lenders and others that are backed

by pools of mortgage loans insured or guaran-

teed by the Federal Housing Administration, the

U.S. Department of Veterans Affairs, the U.S.

Department of Agriculture’s Rural Development,

and the U.S. Department of Housing and Urban

Development Office of Public and Indian Housing.

Ginnie Mae securities are the only MBS to carry

the full faith and credit guaranty of the United

States government.

5 | FDIC | Affordable Mortgage Lending Guide

-

-

This section describes the paths by which a bank may become an FHA

lender, provides information on resources for banks that participate or

are considering participation, and describes the secondary market for

FHA loans before turning to descriptions of FHA and HUD programs.

While most single-family homeownership programs are covered under

Title II of the National Housing Act of 1934; certain types of specialized

mortgage lending, like small-scale renovations and manufactured hous-

ing, are covered under Title I of the Act.

Title I programs covered in this section:

Property Improvement Loan Insurance: Affordable loan insurance for

light or moderate renovations to a variety of residential and nonresi-

dential properties.

Manufactured Home Loan Insurance: Insures mortgages for manu-

factured homes that are classied as personal property or chattel

(meaning moveable property). The mortgages may also nance a lot

on which to place a manufactured home.

Title II programs covered in this section:

203(b) Mortgage Insurance Program: The core FHA single-family

mortgage insurance program, which allows low down payments for

the purchase of a primary residence or its renance. In addition to a

discussion of the basic program, special features for certain popula-

tions and geographies that experience higher barriers to credit access

are covered.

Streamline Renance: Allows homeowners to renance an exist-

ing FHA-insured loan to a lower interest rate or to a different type of

mortgage with reduced documentation and underwriting standards,

saving on transaction costs.

203(k) Rehabilitation Mortgage Insurance: Mortgage insurance for

loans that nance both the purchase of a home (or renance of an

existing mortgage) and renovation costs in a single mortgage.

Other HUD programs covered in this section:

Section 184 Indian Home Loan Guarantee Program: This HUD pro-

gram operates separately from FHA and provides access to credit for

American Indian and Alaska Native families, Alaska Villages, Tribes, or

Tribally Designated Housing Entities.

Good Neighbor Next Door: This HUD program operates separately

from FHA and provides a discount on the purchase price for public

servants (teachers, police, reghters, military) to purchase HUD-

owned homes in certain distressed communities.

TITLE I PROGRAMS IN THIS SECTION:

Property Improvement Loan Insurance:

Affordable loan insurance for light or moder

ate renovations to a variety of properties.

Manufactured Home Loan Insurance: Insures

mortgages for manufactured homes that are

classified as personal property or chattel

(meaning moveable property). The mortgages

may also finance a lot on which to place a

manufactured home.

TITLE II PROGRAMS IN THIS SECTION:

203(b) Mortgage Insurance Program: Allows

low down payments for the purchase of a

primary residence or its refinance. In addition

to a discussion of the basic program, special

features for certain populations and geogra

phies are covered.

Streamline Refinance: Allows homeowners

to refinance an existing FHA-insured loan to

a lower interest rate or to a different type of

mortgage with reduced documentation and

underwriting

standards.

203(k) Rehabilitation Mortgage Insurance:

Mortgage insurance for loans that finance

both the purchase of a home (or refinance of

an existing mortgage) and renovation costs in

a single mortgage.

OTHER PROGRAMS IN THIS SECTION:

Section 184 Indian Home Loan Guarantee

Program:

HUD program operates separately

from FHA and provides access to credit for

American Indian and Alaska Native families,

Alaska Villages, Tribes, or Tribally Designated

Housing Entities.

Good Neighbor Next Door: Provides a discount

on the purchase price for public servants

(teachers, police, firefighters, military) to

purchase HUD-owned homes in certain

distressed

communities

FDIC | Affordable Mortgage Lending Guide | 6

DOING BUSINESS WITH THE FHA

Benets

FHA’s low down payment 203(b) agship program has

helped millions of borrowers purchase their rst homes

and is one of the most recognized mortgage loan

products available today. Developing the expertise

needed to understand FHA’s expectations for lender

operations and loan delivery can be complicated;

however, there are resources to help community banks.

The FHA also insures loans for manufactured hous-

ing, rehabilitation, and for improvements on existing

homes, so doing business with the FHA may offer a

signicant set of new opportunities to serve a wide

range of borrower needs.

Delivery Options

Community banks can participate in two ways in FHA

single-family programs. First, a bank may become

an approved supervised lender with direct endorse-

ment (DE) authority. Banks granted full FHA approval

authority can originate, underwrite, fund, and ser-

vice FHA-insured single-family loans. Or, a bank can

become an FHA third-party originator (TPO), which

allows origination only.

Smaller lenders often turn to investors or aggregators

to help them carry out underwriting, funding, and/

or secondary market sales functions. Correspondent

lenders typically fund loans in their own names and

then sell them to investors, who in turn sell the loans

into the secondary market. In some cases, the corre-

spondent lenders handle the underwriting in-house.

In others, the investor acts as the underwriter. Smaller

lenders that are interested in originating loans but do

not have the internal capacity to either underwrite or

fund the loans can also work with investors to carry out

the origination function while looking to the investor to

underwrite and fund the loans in the name of the inves-

tor. Many state and local housing nance agencies, as

well as certain Federal Home Loan Banks, also work

directly to provide mortgage-lending options.

1

Originating FHA loans as a third-party originator

sponsored by an approved lender

Non-FHA approved banks can originate FHA loans

without going through the formal FHA approval

process by working with an FHA-approved lender to

sponsor them. Becoming a TPO can be useful to banks

that are interested in offering FHA loans to their cus-

tomers, but may not meet minimum standards or have

the internal capacity needed for FHA lending, or that

wish to avoid the additional costs associated with FHA

approval and annual recertication.

TPOs originate FHA loans that are underwritten and

funded in the name of a sponsoring FHA-approved

lender. However, as a TPO, the bank is subject to both

FHA loan standards and those of the sponsoring

lender, sometimes referred to as overlays. In addition,

TPO banks are reliant on their sponsoring lenders for

underwriting approval and funding timelines. For these

reasons and others, banks may choose to become an

approved FHA supervised lender with direct endorse-

ment authority.

Originating FHA loans as an approved supervised

lender with direct endorsement authority

To originate, underwrite, and fund FHA loans, a lending

institution must be approved by HUD as an FHA lender.

Approval process: Banks must follow a two-step

approval process in order to gain this status.

1. Conditional authority (basic lender approval).

Conditional authority is the authority of a bank that

has applied for and received basic FHA mortgagee

approval. A bank applying for this status must meet

minimum nancial and operational standards pertain-

ing to net worth, liquidity, stafng, and quality control

that are laid out for FHA supervised lenders. Banks

applying for underwriting authority must have an

underwriter on permanent staff. In addition, the bank

must have ve years of experience in the origination

of single-family mortgages, or a principal ofcer with

a minimum of ve years managerial experience in the

origination of single-family mortgages. Banks that are

considered large entities as dened by the U.S. Small

Business Administration (SBA), (net worth greater than

$500 million) are required to submit audited nancial

1

Detailed information regarding State Housing Finance Agencies can be

found

in the

Affordable Mortgage Lending Guide, Part II: State Housing Finance

Agencies, https://www.fdic.gov/mortgagelending. Detailed information regard-ing

Federal Home Loan Banks can be found in Affordable Mortgage Lending Guide,

Part III: Federal Home Loan Banks, https://www.fdic.gov/mortgagelending.

7 | FDIC | Affordable Mortgage Lending Guide

statements, both at the time of application and as part

of an annual recertication process. Banks with a net

worth of less than $500 million are required to submit a

copy of their call reports each year.

A bank interested in becoming an FHA-approved

lender can submit an online application using the HUD

FHA application portal. The bank must receive separate

approval for making Title I loans and Title II loans but

can apply for both at the time of its initial application.

Should a bank apply initially only for Title I or Title II

approval status, it can apply for the other status later.

Although a bank can originate FHA loans once it has

been approved as an FHA supervised lender, it is not

eligible to underwrite FHA loans until it receives FHA

direct endorsement (DE) authority

2. Direct endorsement authority. Once a bank has

received conditional authority, it must obtain uncondi-

tional DE authority to underwrite, fund, and submit FHA

loans directly for endorsement.

In general, to receive unconditional DE authority, a

bank must submit a written application to the jurisdic-

tional HOC for the state where the bank’s home ofce

is located. If approved, the bank will receive a test case

phase approval letter, reference materials, and a list

of specic requirements that the bank must meet. The

bank will also be required to participate in an entrance

conference with the HOC before the bank is allowed to

submit test cases.

During the test case phase, the bank will submit its

FHA loan les for approval to the appropriate HOC.

The HOC will issue a rm commitment (approval) or

a rm reject (denial) for each case submitted. Cases

that receive a rm commitment are approved to close

and be submitted for insurance endorsement. Upon

receipt of 15 rm commitments within a period of 12

consecutive months following the date of the entrance

conference and a determination that the bank has

demonstrated an acceptable understanding of FHA

underwriting and other requirements, the bank is

granted full and unconditional DE approval.

One or more designated underwriters employed

by the bank serves as the bank’s FHA subject matter

expert(s) as designated DE underwriters. The

underwriter’s role and responsibilities are critical ele-

ments of the DE Program and include ensuring loans

comply with FHA policies and procedures from the

underwriting and verication process through loan

closing and certication. Generally, DE underwriters

must have a minimum of three years of recent full-time

underwriting experience.

DE lenders must complete an endorsement process

for each FHA loan after closing. Most DE lend-

ers submit the insurance application electronically

through the FHA Connection electronic system and

prepare an FHA case binder for review by the HOC,

which will determine whether the les meet the neces-

sary requirements.

Lender Insurance Program

The Lender Insurance (LI) Program enables high-

performing FHA-approved lenders to endorse FHA

mortgage loans without a pre-endorsement review. To

become an LI lender, lenders must have and maintain

at all times, unconditional DE authority and must have

a claim/default rate for the state(s) in which the uncon-

ditional DE lender has underwritten loans that is at,

or below, 150 percent for at least two years before its

application for participation in the LI Program.

Selling FHA Loans

Lenders do not typically keep FHA loans in their port-

folios. Instead, they are generally pooled and used as

collateral for mortgage-backed securities (MBS). FHA

does not purchase and securitize loans. Instead, FHA

loans are delivered to the secondary market through

Ginnie Mae’s guaranteed mortgage-backed securities.

Securities are issued by private nancial institutions

and the timely payment of principal and interest to

investors in these securities is guaranteed by Ginnie

Mae, a government ofce within HUD. FHA-approved

lenders can deliver FHA-endorsed loans as MBS by

becoming a Ginnie Mae approved issuer or by selling

FHA loans to third-party Ginnie Mae approved industry

conduits or aggregators. See Resources at the end of

this section for a list of Ginnie Mae approved issuers.

FDIC | Affordable Mortgage Lending Guide | 8

System Requirements and Quality Control

FHA loans can be manually or electronically under-

written. All FHA loans are required to go through the

FHA TOTAL (Technology Open to Approved Lenders)

Mortgage Scorecard system except Streamline

Renances and assumptions. The TOTAL Mortgage

Scorecard is based on credit and application variables

and, when combined with an approved automated

underwriting system’s functionalities, is used to provide

an underwriting recommendation that either deems

the borrower’s credit is acceptable or requires the loan

to be underwritten manually by an FHA DE underwriter.

All FHA-approved mortgagees must also implement

and continuously have in place a written quality control

plan for the origination and/or servicing of FHA-

insured mortgages to assure compliance with FHA’s

origination and servicing requirements and to protect

against unacceptable risk and fraud. The quality control

function must be independent of the origination and

servicing functions and can be fullled by using in-

house staff or an outside rm.

Neighborhood Watch Early Warning System

Neighborhood Watch is an electronic database and

monitoring system intended to help HUD/FHA staff,

FHA lenders, and the public analyze the Title II loan

performance of FHA lenders. Neighborhood Watch

data can be used to compare a specic lender’s FHA

loan performance against other lenders in a geo-

graphic area in order to help identify and address

potential problems related to early delinquency

patterns. Specically FHA uses a “compare ratio” to

compare a lender’s early default rate (typically the

percentage of loans that are 90 days or more delin-

quent within the rst two years of origination) against

those operating within the same region. Lenders with

a compare ratio at twice the average or higher are

subject to disciplinary action. More information about

Neighborhood Watch can be found at

https://entp.hud.gov/sfnw/public/.

9 | FDIC | Affordable Mortgage Lending Guide

RESOURCES

Direct access to the following web links can be found on FDIC’s Affordable Mortgage Lending Center

at https://www.fdic.gov/mortgagelending.

FHA Handbook: Single Family Housing Policy Handbook 4000.1

https://www.hud.gov/program_ofces/housing/sfh/handbook_4000-1

FHA lender approval application

https://www5.hud.gov/FHALender/

FHA lender approval application instructions

http://portal.hud.gov/hudportal/documents/huddoc?id=SFH_LEND_REQAPPROVAL-LEAP.PDF

Homeownership Centers and areas served

https://www.hud.gov/program_ofces/housing/sfh/sfhhocs

Neighborhood Watch

https://entp.hud.gov/sfnw/public/

Doing Business with Ginnie Mae

https://www.ginniemae.gov/doing_business_with_ginniemae/Pages/default.aspx

Ginnie Mae approved issuers

http://www.ginniemae.gov/issuers/third_party_providers/Pages/document_custodian.aspx

FHA Connection Electronic System

https://entp.hud.gov/clas/index.cfm

FHA Lender Insurance Program

http://portal.hud.gov/hudportal/HUD?src=/program_ofces/housing/sfh/lender/lendins

FHA TOTAL Mortgage Scorecard

http://portal.hud.gov/hudportal/HUD?src=/program_ofces/housing/sfh/total

FDIC | Affordable Mortgage Lending Guide | 10

A COMMUNITY BANKER CONVERSATION

Using FHA’s Section 203(b) Mortgage Insurance Program

The FDIC talked with community bankers about their participation in the Federal Housing Administration’s

Section 203(b) Mortgage Insurance Program. The following are excerpts from these discussions.

The Section 203(b) Mortgage Insurance Program is the

core FHA single-family mortgage insurance program,

which allows low down payments for the purchase of a

primary residence or for renancing a mortgage.

Working with the FHA

One small community bank recently decided to add

home mortgage loans to its line of products. The

bank representative explained that as the bank did its

product evaluation, management concluded that the

Federal Housing Administration’s (FHA) Section 203(b)

Mortgage Insurance Program would be of interest in

the local market.

The lender added that the bank wanted to offer a loan

that would help rst-time homebuyers who needed

a lower down payment option. Aligning that market

need with the bank’s policy of selling 100 percent

of the mortgage loans it originates into the second-

ary market led them to the Section 203(b) Mortgage

Insurance Program.

Becoming an FHA Lender

The banker said that one challenge to its plan to origi-

nate FHA loans was that the bank would be unable

to gain approval as an FHA direct endorsement (DE)

lender because it fell short of the requirements for

audited nancials and minimum asset levels set by

the FHA. The bank, therefore, chose to pursue table

funding. Under this arrangement, the bank acts as an

FHA-sponsored third-party originator (TPO) to origi-

nate the loan and then works with an FHA-approved

direct endorsement (DE) sponsoring lender or mort-

gagee to underwrite and fund the loan.

As a TPO, the bank meets with the borrowers and

originates and processes the initial loan application,

including collecting FHA-required documentation. The

bank then sends the loan le to the FHA DE mort-

gagee that underwrites the loan and communicates

any outstanding closing conditions that need to be

satised by the borrower back to the bank. Once fully

approved, the mortgagee initiates the closing and the

loan is funded and closed in the mortgagee’s name.

The representative said, “The rst table-funding FHA-

approved mortgagee that the bank worked with took

too long to get the approval in place due to a cum-

bersome process. However, once we identied more

effective DE partners, established clear and open

lines of communication, and initiated the process to

become approved to originate FHA loans as a TPO,

we were able to get up and running within a couple

of months.” She went on to say that “the quality of the

DE sponsoring lender can make a huge difference in

the efciency of the loan approval process. When you

have an outstanding issue on a loan during the under-

writing process, you want to know that you and your

sponsoring lender will be working as a team to resolve

the issue as effectively and efciently as possible.”

Challenges of Offering FHA Loans

When asked what the biggest challenge is with using

the FHA 203(b) product, one of the representatives

stated that it is forming an effective partnership with a

strong FHA approved DE underwriter. As the origina-

tor of the loan, the bank is responsible for meeting

with borrowers, taking loan applications, and col-

lecting FHA-required documentation. Even after

completing an origination package and sending it off

to the underwriter, back-and-forth communications

and competing business priorities of the underwriter

(including transactions with other TPOs) occasionally

extend wait times.

11 | FDIC | Affordable Mortgage Lending Guide

Another banker, who is also a TPO, pointed out that “the biggest challenge

my bank has is that since we are not the lender, we do not have as much

control over the approval as we do with loans that we underwrite our-

selves; however, in our experience, the FHA product is really not difcult [to

originate] once you gain some experience.” The representative went on to

say that his bank only does a few mortgages a year, but has been making

Section 203(b) loans for the past eight years so customers can benet from

the 15-year and 30-year terms. “If you are already originating mortgage

loans, the learning curve is fairly easy.”

Benets of Offering FHA Loans

One bank representative said that her bank combines the FHLBank

of Cincinnati’s Welcome Home program with its FHA loans. Welcome

Home provides up to $5,000 for down payments and closing costs to

eligible homebuyers with a minimum subsidy match of $500 provided by

the borrower.

Another banker added that his bank combines the FHA 203(b) product with

grants from the Federal Home Loan Bank of Topeka. He said that overall,

FHA loans are not a signicant portion of the bank’s mortgage lending busi-

ness, but having it available is very important because it gives customers

more options.

One banker estimated that 95 percent of her bank’s FHA loans are for

rst-time homebuyers, including many younger borrowers who have not

had the time or the nancial experience to build a high credit score. She

noted that FHA’s credit score thresholds can be lower than government-

sponsored enterprise (GSE) low down payment programs. Another helpful

feature for young borrowers is the ability to use gift funds from relatives

to cover a portion of the down payment and closing costs. Older, more

established family members helping younger relatives buy their rst home

is a common and long-standing tradition in many communities, which FHA

guidelines generally support. The representative also points out that many

renters can actually save money by becoming homeowners. “Rents are high

and it’s often cheaper to buy a home than to rent.”

FDIC | Affordable Mortgage Lending Guide | 12

FHA | TITLE I PROGRAMS

Property Improvement Loan Insurance

Insuring loans for borrowers to improve their property

BACKGROUND AND PURPOSE

The Title I Property Improvement Loan Insurance

program insures loans that lenders make to borrowers

to nance alterations and repairs of single-family,

multifamily, and nonresidential properties. Loans may

also nance site improvements, as well as construction

of nonresidential properties, as long as the nonresi-

dential uses are consistent with the property’s zoning.

The program is designed to help low- and moderate-

income (LMI) borrowers improve their homes and

is an alternative for homeowners with limited home

equity, who cannot use their home’s equity to nance

signicant home repairs. The improvements can be

conducted by the property owners themselves or

through a contractor. The improvements must

substantially protect or improve the basic livability

or utility of the property. In general, improvements

must be permanent, hardwired, or hard-plumbed to

the property. FHA insures lenders against the risk of

default for up to 90 percent of the loan.

This program differs from FHA’s Section 203(k)

Rehabilitation loan program in that a Title I Property

Improvement Loan only covers the amount of the

proposed repairs, not the purchase of the property.

The two programs can be used together on the same

home. Title I Property Improvement Loans are typically

second or subordinate liens but may also be unsecured

if the loan amount is less than $7,500. Only lenders

approved by HUD specically for this program can

make loans covered by Title I insurance.

BORROWER CRITERIA

Income limits: This program has no income limits.

Credit: There is no minimum credit score require-

ment for the program, but HUD expects that lenders

will undertake a thorough review of the borrower’s

credit history by pulling a credit report, verifying

PROGRAM NAME

Property Improvement Loan Insurance

AGENCY

Federal Housing Administration

EXPIRATION DATE

Not Applicable

APPLICATIONS

To participate, lenders must be FHA approved for the Title I loan program. Lenders may access

FHA’s Lender Requirements and the online lender application at:

https://www.hud.gov/program_ofces/housing/sfh/lender/lendappr

WEB LINK

https://www.hud.gov/program_ofces/housing/sfh/title/title-i

CONTACT

INFORMATION

Telephone: (800) CALL-FHA (225-5342) Email: [email protected]. Lenders that want to apply for

FHA approval should include the words “New Applicant” in the email subject line and include a

contact person and phone number in the email body so that a Lender Approval representative

may contact you.

APPLICATION PERIOD

Continuous

GEOGRAPHIC SCOPE

National

13 | FDIC | Affordable Mortgage Lending Guide

-

-

-

-

employment, and checking that the borrower is not delinquent or in

default on a federally guaranteed loan obligation.

First-time homebuyers: First-time homebuyers can take advantage of

the program as long as they have or take title of the property at closing.

When improvements are for a residential property, the home must have

been occupied for at least 90 days.

Occupancy and ownership of other properties: Title I loans may be used

to nance permanent property improvements that protect or improve

the basic livability or utility of the property, including manufactured

homes, single-family and multifamily homes, nonresidential structures,

and the preservation of historic homes. The loans can also be used for

re safety equipment. Funds can be used to nance the construction of

a nonresidential structure on the property, as long as the nonresiden-

tial uses are subordinate to the residential uses and consistent with the

property’s zoning. To be eligible for a Title I loan, borrowers must be:

1. the owner of the property being improved;

2. the person leasing the property (if the lease extends at least six

months after the loan is scheduled to be fully repaid); or

3. someone purchasing the property under a land installment contract.

Special populations: There is no targeted population, but the program

is a tool for both homeowners and persons leasing the property to

make improvements.

Special assistance for persons with disabilities: Title I loans can be used

for improvements that make the home more accessible to a disabled

person. Improvements can include remodeling kitchens and baths for

wheelchair access, lowering kitchen cabinets, or installing wider doors

and exterior ramps.

Verication of property improvements: Loan proceeds must be used

only for purposes established in the loan application. If the borrower

uses a dealer to execute the improvement work, the lender must

receive a copy of the proposal or contract describing in detail the work

to be performed and cost estimates. If the borrower is completing the

improvements, they must provide the lender with a detailed written

description of the work, materials, and cost.

List of acceptable property improvements:

• Improvements for accessibility to a disabled person such as remod-

eling kitchens and baths for wheelchair access, lowering kitchen

cabinets, installing wider doors and exterior ramps, and the like.

• Improvements must protect or improve the livability or utility of

the property.

• Loans cannot be used to nance luxury-type items such as swimming

pools or outdoor replaces, or to pay for work completed before the

loan application.

POTENTIAL BENEFITS

HUD-approved Title I lenders

can offer improvement loans for

various property types including

manufactured home proper

ties. The manufactured home is

not required to be real property.

However, in order to use the loan

to finance site improvements, the

borrower must comply with the

criteria for owning, or otherwise

being authorized to execute liens

against the underlying land.

Title I property improvement

loans can be originated con

currently with the purchase or

refinance of an existing property.

The loans may also be originated

at any point after the prop

erty purchase.

POTENTIAL CHALLENGES

The lender must be approved by

HUD as a Title I lender.

Lenders that want to offer dealer

loans, where a contractor helps

the borrower with financing,

instead of directly lending to the

borrower, must approve the deal

ers through a separate process.

The lender must verify that the

property improvement dealer

has a net worth of $32,000 and

meets HUD guidelines. A jointly

signed HUD-approved form

documents the approval and

lenders must annually recertify

the dealers to whom they extend

dealer loans.

FDIC | Affordable Mortgage Lending Guide | 14

• Loan proceeds may be used for alterations and/or

repairs of single-family, multifamily, and nonresi-

dential property types and for site improvements.

LOAN CRITERIA

Loan limits: Title I approved lenders can offer eligible

borrowers improvement loans for up to 20 years on

either single-family or multifamily properties. The

maximum loan amount is $25,000 for a single-family

house, $25,090 for a manufactured house on a perma-

nent foundation, and $7,500 for a manufactured house

not on a permanent foundation (classied as personal

property). To improve a two- to four-unit structure, the

maximum loan amount is $60,000 or an average of

$12,000 per dwelling unit, whichever is less.

Loan-to-value limits: The program does not require

an appraisal, and borrowers are not required to have

equity in the property. A loan amount greater than

$7,500 must be secured by a recorded lien on the

improved property. The lien does not have to be a

rst lien on the property, but it must not be placed

in less than second position. A Title I loan may be

secured in third place by exception when the rst and

second loans were originated to nance the prop-

erty’s purchase.

Adjustable-rate mortgages: Lenders must offer xed-

rate loans (no adjustable-rate terms are permitted) and

charge market-rate interest.

Homeownership counseling: Housing counseling is

not required for participation in the program.

Mortgage insurance: FHA insures private lenders

against the risk of default for up to 90 percent of any

single loan. The annual premium for this insurance is

$1 per $100 of the amount advanced. The insurance

premium may be charged to the borrower separately,

but it is sometimes covered by a higher interest charge.

Debt-to-income ratio: The borrower must have a maxi-

mum DTI of 45 percent, meaning total xed expenses

(including payments on the property improvement

loan) may not exceed 45 percent of gross income. In

the event the borrower has student loan debt, regard-

less of the payment status, FHA’s policy is to include

either the actual documented payment, provided the

payment will fully amortize the loan over its term or the

greater of 1 percent of the total student loan balance

or the monthly payment reported on the borrower’s

credit report in the debt-to-income calculation.

Renance: Borrowers that meet certain requirements

may renance the loan with a Title I lender.

Potential Benets

• HUD-approved Title I lenders can offer improve-

ment loans for various property types including

manufactured home properties. The manufactured

home is not required to be real property. However,

in order to use the loan to nance site improve-

ments, the borrower must comply with the criteria

for owning, or otherwise being authorized to

execute liens against the underlying land.

• Title I property improvement loans can be origi-

nated concurrently with the purchase or renance of

an existing property. The loans may also be origi-

nated at any point after the property purchase.

• No security is needed for loan amounts

below $7,500.

• Loans originated through this program may receive

favorable consideration under the CRA, depending

on the geography or income of the participat-

ing borrowers.

Potential Challenges

• The lender must be approved by HUD as a Title

I lender.

• Lenders that want to offer dealer loans, where a con-

tractor helps the borrower with nancing, instead of

directly lending to the borrower, must approve the

dealers through a separate process. The lender must

verify that the property improvement dealer has a

net worth of $32,000 and meets HUD guidelines. A

jointly signed HUD-approved form documents the

approval and lenders must annually recertify the

dealers to whom they extend dealer loans.

• The lender must be familiar with the unique forms

and requirements of this program.

SIMILAR PROGRAMS

• FHA 203(k) Rehabilitation Mortgage Insurance

• USDA Single Family Housing Repair Loans

and Grants

15 | FDIC | Affordable Mortgage Lending Guide

RESOURCES

Direct access to the following web links can be found at https://www.fdic.gov/mortgagelending.

General information

http://portal.hud.gov/hudportal/HUD?src=/program_ofces/housing/sfh/title/title-i

HUD Handbook 1060.2 REV-6 for Title I Property Improvement and Manufactured Home Loans (issued in 1996

and includes program rules)

http://portal.hud.gov/hudportal/documents/huddoc?id=10602HSGH.pdf

HUD Handbook 4000.1

http://portal.hud.gov/hudportal/documents/huddoc?id=40001HSGH.pdf

Title I Letter TI-473, “Publication of Final Rule on November 7, 2001 Regarding: Strengthening the Title I Property

Improvement and Manufactured Home Loan Insurance Programs and Title I Lender/Title II Mortgagee Approval

Requirements” (includes insurance premium information)

http://portal.hud.gov/hudportal/HUD?src=/program_ofces/administration/hudclips/letters/title1

Direct link: https://www.hud.gov/sites/documents/ti-473.doc

Title I Lender Letter TI-470, “Clarications to the Title I Property Improvement Program” (includes debt-to-income

information)

http://portal.hud.gov/hudportal/HUD?src=/program_ofces/administration/hudclips/letters/title1

Direct link: https://www.hud.gov/sites/documents/ti-470.doc

HUD Guidelines for Dealers (see section 201.27 “Requirements for dealer loans” in HUD Handbook 1060.2 REV-6)

http://portal.hud.gov/hudportal/documents/huddoc?id=10602HSGH.pdf

Dealer/Contractor Application Form HUD-55013 (to be completed by lender)

http://portal.hud.gov/hudportal/documents/huddoc?id=55013.pdf

FDIC | Affordable Mortgage Lending Guide | 16

FHA | TITLE I PROGRAMS

Manufactured Home Loan Insurance

Providing affordable homeownership opportunities through manufactured

home loans, lot loans, and home/lot combination loans

BACKGROUND AND PURPOSE

Manufactured homes have traditionally been nanced

as personal property through higher interest, short-

term chattel loans. The Manufactured Home Loan

Insurance program increases the availability of afford-

able nancing for buyers of manufactured homes by

offering longer term and lower interest rate nancing

than with conventional loans. A manufactured home

need not be treated as real property under state law

to be eligible for this program. The U.S. Department of

Housing and Urban Development (HUD) has provided

this type of loan insurance since 1969.

The Manufactured Home Loan Insurance program

through the Federal Housing Administration (FHA)

insures mortgages made by private lenders that

nance the purchase or renance of a manufactured

home and/or the lot on which the home is located. The

program offers insurance for three types of loans:

(1) manufactured home loan, (2) manufactured home

lot loan, and (3) manufactured home land and lot

combination loan. FHA insures private lenders against

the risk of default for up to 90 percent of the loss of any

individual loan.

BORROWER CRITERIA

Income limits: This program has no income limits.

Credit: HUD has not established a minimum credit

score level for the program. The score will affect only

the amount of down payment required, not program

eligibility.

PROGRAM NAME

Manufactured Home Loan Insurance

AGENCY

Federal Housing Administration

EXPIRATION DATE

Not Applicable

APPLICATIONS

WEB LINK

https://www.hud.gov/program_ofces/housing/sfh/title/manuf14

CONTACT

INFORMATION

APPLICATION PERIOD

Continuous

GEOGRAPHIC SCOPE

National

To participate, lenders must be FHA-approved for the Title I loan program. Lenders may access

FHA’s Lender Requirements and the online lender application at

https://www.hud.gov/program_ofces/housing/sfh/lender/lendappr

Telephone: (800) CALL-FHA (225-5342) Email: [email protected]. Lenders that want to apply for

FHA approval should include the words “New Applicant” in the email subject line and include a

contact person and phone number in the email body so that a Lender Approval representative

may contact you.

17 | FDIC | Affordable Mortgage Lending Guide

-

First-time homebuyers: The program is not limited to rst-time home-

buyers and can be used to renance the property.

Occupancy and ownership of other properties: Borrowers must occupy

the property as their primary residence. The program is limited to the

purchase or renance of a manufactured home with or without the lot

on which the home is placed. HUD denes a manufactured home as

a transportable structure comprised of one or more modules, each

built on a permanent chassis. The manufactured home must be the

primary residence for a single family. The manufacturer of the home

must comply with HUD safety and livability standards and certify it as

compliant by afxing the “HUD Seal” to each home. Eligible manufac-

tured homes must also meet the Model Manufactured Home Installation

Standards and carry a one-year manufacturer’s warranty if the unit is

new. The home must be installed on a home site that meets established

local standards for site suitability and has an adequate water supply and

sewage disposal facilities available.

The purchase loan may also be used to nance accessories offered by

the dealer including the cost for skirting, garage, carport, patio, or other

comparable appendage to the home. The combination home and lot

loan product provides insurance for purchase of a parcel of real estate

that is used for placement of the approved manufactured home unit.

Required documentation: The borrower must complete a credit applica-

tion form (HUD-56001-MH).

LOAN CRITERIA

Loan limits: Title I insurance may be used for loans of up to $92,904

for a manufactured home and lot and $23,226 for a lot only. A HUD-

approved appraiser must appraise the lot.

Loan-to-value limits: Borrowers with a credit score of 500 or lower are

required to make a minimum down payment of 10 percent for a maxi-

mum LTV of 90 percent. Borrowers with a credit score above 500 are

required to make a 5 percent minimum down payment for a maximum

LTV of 95 percent.

Adjustable-rate mortgages: Adjustable-rate products are not permitted.

Down payment sources: Borrowers are responsible for paying the down

payment. No part of the costs payable by the borrower may be loaned,

advanced, or paid to or for the benet of the borrower by the dealer, the

manufacturer, or any other party to the loan transaction. If the borrower

obtains all or any part of such costs through a gift or a loan from some

other source, the borrower must disclose the source of such gift or loan

on the credit application.

Homeownership counseling: Housing counseling is not required

for participation in the program, but it is recommended for all rst-

time homebuyers.

POTENTIAL BENEFITS

The insurance provided by FHA

under this program helps protect

Title I approved lenders from

credit risk, though the coverage

provided is 90 percent of the loss

as opposed to 100 percent for

other FHA Title II programs.

In many states, manufactured

homes are considered personal

property rather than real estate.

Title I insurance, backed by the

FHA, helps families finance

homes classified as personal

property and where conventional

financing may be limited.

The Manufactured Home Loan

Insurance program may allow

community banks to expand

their customer base in low- and

moderate-income communities.

POTENTIAL CHALLENGES

HUD must approve lenders to

participate in the Title I pro

gram before they can offer the

loan product.

A HUD-approved appraiser must

appraise the lot. In some areas

of the country, it can take 30-60

days to complete the appraisal.

The FHA-approved lender is

also responsible for approving

manufactured home dealers to

participate in the program.

FDIC | Affordable Mortgage Lending Guide | 18

Mortgage insurance: The program has different stan-

dards than other FHA-insured single-family programs.

The upfront mortgage insurance premium (UFMIP) is

the obligation of the lender, but may be passed on to

the borrower and must not exceed 2.25 percent. The

annually adjusted mortgage insurance premium (MIP)

is paid monthly and must not exceed 1.0 percent of the

remaining insured principal.

Debt-to-income ratio: Similar to other FHA-insured

single-family programs, HUD requires lenders to

calculate two ratios to determine if a borrower can

reasonably meet the expected expenses. First, the

Mortgage Payment Expense to Effective Income ratio

(or front-end DTI) should not exceed 31 percent.

Second, the Total Fixed Payment to Effective Income

ratio (or back-end DTI) should not exceed 43 percent.

Ratios that exceed 31 percent or 43 percent may be

acceptable if the lender documents qualied “signi-

cant compensating factors.” The ratios increase to 33

percent and 45 percent when the home being nanced

can be documented as Energy Star compliant. In the

event the borrower has student loan debt, regardless

of the payment status, FHA’s policy is to include either

the actual documented payment, provided the pay-

ment will fully amortize the loan over its term or the

greater of 1 percent of the total student loan balance

or the monthly payment reported on the borrower’s

credit report in the DTI calculation.

Renance: Allowed.

Loan Parameters

Financing fees: The interest rate is set by the lender.

Loan parameters: Loan limits and terms were updated

in 2008 because of the FHA Manufactured Housing

Loan Modernization Act of 2008. (See below.)

Dealers: Dealers are the persons or rms that make

manufactured home retail sales, and it is common for

dealers to establish a formal business relationship

with a lender to facilitate nancing for the purchaser.

Lenders must verify the dealer’s nancial statements

and submit a Dealer/Contractor Application form

(HUD-55013) to HUD before working with dealers to

provide Title I nancing to borrowers.

Trade equity from existing Manufactured Housing:

Many manufactured home dealers offer equity-like

contributions for home purchasers who trade in an

old model of home to buy a new one, similar to an

automobile trade-in program. The maximum equity

contribution from the traded manufactured home is the

lesser of the appraised value or sales price. Any costs

resulting from the removal of the manufactured home

or any outstanding indebtedness secured by liens

on the manufactured home must be deducted from

the maximum equity contribution. Trade-ins for cash

funds are considered a seller inducement and are not

permitted. Land equity is not addressed as a potential

equity contribution.

LOAN TYPE

PURPOSE LOAN LIMIT MAXIMUM LOAN TERM

Manufactured home loan

To purchase or renance a

manufactured home unit

$69,678 20 years

Lot loan

To purchase and develop a lot on

which to place a manufactured home

$23,226 15 years

Combination loan for lot

and home

To purchase or renance a

manufactured home and lot on which

to place the home

$92,904

20 years (25 years for

multi-unit homes)

19 | FDIC | Affordable Mortgage Lending Guide

Potential Benets

• The insurance provided by FHA under this program

helps protect Title I approved lenders from credit

risk, though the coverage provided is up to 90 per-

cent of the loss of any individual loan as opposed

to 100 percent for other FHA Title II programs.

• In many states, manufactured homes are consid-

ered personal property rather than real estate.

Title I insurance, backed by the FHA, helps families

nance homes classied as personal property and

where conventional nancing may be limited.

• The Manufactured Home Loan Insurance

program may allow community banks to expand

their customer base in low- and moderate-

income communities.

• The Manufactured Home Loan Insurance program

may help community banks access the secondary

market, providing greater liquidity to enhance their

lending volume.

• The Manufactured Home Loan Insurance program

offers competitive pricing and terms.

• Loans originated through the Manufactured Home

Loan Insurance program may receive favorable

consideration during the bank’s CRA evaluation,

depending on the geography and income of the

participating borrowers.

Potential Challenges

• HUD must approve lenders to participate in

the Title I program before they can offer the

loan product.

• A HUD-approved appraiser must appraise the lot.

In some areas of the country, it can take 30-60 days

to complete the appraisal.

• The FHA-approved lender is also responsible for

approving manufactured home dealers to partici-

pate in the program.

SIMILAR PROGRAMS

• Fannie Mae Standard Manufactured

Housing Mortgage

• Freddie Mac Manufactured Home Mortgage

RESOURCES

Direct access to the following web links can be found

at https://www.fdic.gov/mortgagelending.

General information

http://portal.hud.gov/hudportal/HUD?src=/

program_ofces/housing/sfh/title/manuf14

Applications

http://portal.hud.gov/hudportal/HUD?src=/

program_ofces/housing/sfh/lender/lendappr

HUD Handbook 4000.1

https://www.hud.gov/sites/documents/

40001HSGH.PDF

Title I Letter TI-481, “Changes to the Title I

Manufactured Home Loan Program” (details

major changes to the program made by The FHA

Manufactured Housing Loan Modernization Act of

2008 and includes updates to loan limits, LTV rates,

insurance premiums, and underwriting criteria)

https://www.hud.gov/sites/documents/ti-481.pdf

Borrower Credit Application Form HUD-56001-MH (to

be completed by borrower)

https://www.hud.gov/sites/documents/

56001MH.PDF

Dealer/Contractor Application Form HUD-55013 (to

be completed by lender)

https://www.hud.gov/sites/documents/55013.PDF

FDIC | Affordable Mortgage Lending Guide | 20

FHA | TITLE II PROGRAMS

203(b) Mortgage Insurance Program

Affordable low down payment lending traditionally for rst-time

homebuyers and underserved communities

BACKGROUND AND PURPOSE

The 203(b) mortgage insurance program, or the Basic

Home Mortgage Loan, is the centerpiece of all FHA

mortgage insurance programs for one- to four-unit

residential properties, including individual condo-

minium units or manufactured homes on real estate.

The purpose of the Section 203(b) program is to

provide approved lenders with mortgage insurance

to protect them against the risk of default on mort-

gages that are made to qualied buyers who may not

otherwise qualify for conventional loans or who live in

underserved areas. Insured mortgages can be used to

nance the purchase of new or existing one- to four-

unit structures and can be used to renance both FHA

and non-FHA mortgages.

Down payments may be lower than conventional mort-

gages because the federally backed insurance allows

lenders to nance up to 96.5 percent of the value of

the home. This results in down payments as low as 3.5

percent. Out-of-pocket costs to borrowers in some

cases can be lowered through a variety of sources