Engility Corporation - Full-time

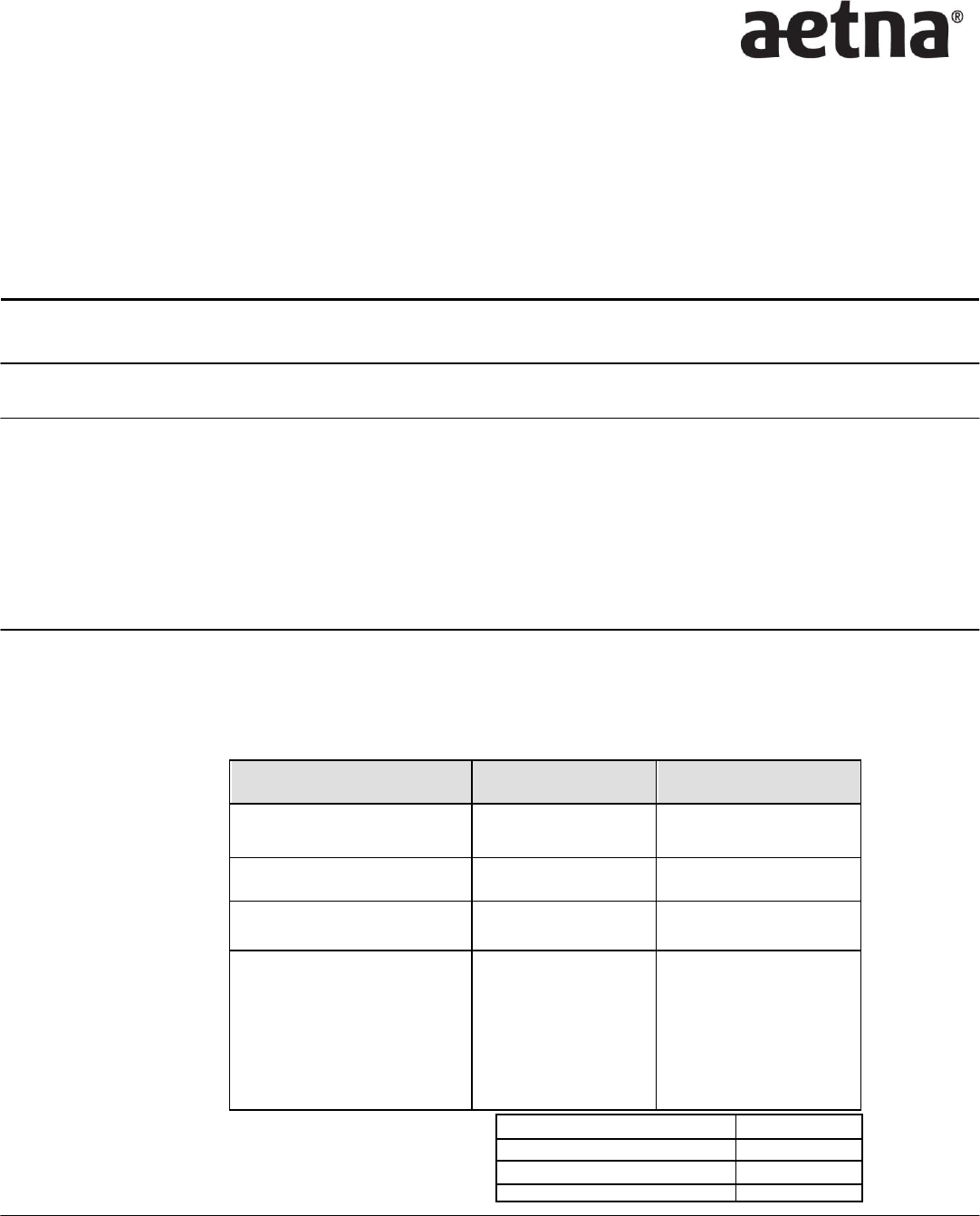

Summary of Long-Term Disability (LTD) Benefits

Your Group Long-Term Disability Benefits

Steady income for longer-lasting disabilities

Coverage Effective Date: 01/01/2019

Coverage Basics

Am I eligible for

coverage?

When does coverage

become effective?

Do I have to provide proof

of good health known as

Evidence of Insurability

(EOI) to enroll?

When will coverage that

requires proof of good

health (EOI) begin?*

How much Voluntary

Long-Term Disability can

I buy through my

employer?

Are all types of illnesses

and injuries covered?

You qualify if you are an active full-time hourly or salaried employee working at least 30

hours per week.

Your Long-Term Disability coverage will begin on 01/01/2019, if you are actively at work.

New Hire/Newly Eligible: EOI is not required to enroll during your 31 - day period of initial

eligibility. If you choose not to enroll, you will be considered a "late applicant."

Annual Enrollment: EOI is required to enroll if you are a late applicant (did not enroll during

your initial eligibility period.) You will be required to submit an EOI Form (medical questionnaire)

and be approved by Aetna.

Coverage will begin after Aetna approves your EOI.

*You must be actively-at-work for coverage to begin.

You have a choice of plans that pay a monthly benefit based on a percentage of your

Pre-Disability Earnings* for a covered disability. You must submit a claim and be approved by

Aetna to receive benefits:

*Generally, Pre-Disability Earnings include your total income before taxes and any deductions for pre-tax contributions. Please

consult your Policy Documents available through your employer for additional information, including def inition of Pre-Disability

Earnings.

*

Long-Term Disability (LTD) covers injuries and illnesses that are both work-related and

non-work-related.

Disability insurance plans/policies are offered and/or underwritten by Aetna Life Insurance Company (Aetna). We are located at 151 Farmington

Avenue, Hartford, CT 06156.

26.06.305.1_(8/2016)

Page 1 of 4

©2016 Aetna Inc.

Voluntary Long-Term Disability

Option 1

Option 2

Percentage of monthly income

replacement:

50%

66

⅔

%

Maximum monthly benefit:

$10,000

$20,000

Benefits begin after a covered

Injury or Illness:

180 days

180 days

Benefits end at recovery

or:

whichever comes

first*

For disabilities starting

before age 62,

benefits

continue to age 65

.

For disabilities starting

after age

62,

benefits will

follow

a pre-deter mi ne d

sche dul e. *

For disabilities starting

before age 62,

benefits

continue to age 65

.

For disabilities starting

after age

62,

benefits will

follow

a pre-deter mi ne d

sche dul e. *

Age 62,but less than age 65

36 months

Age 65,but less than age 67

24 months

Age 67,but less than age 69

18 months

Age 69 and over

12 months

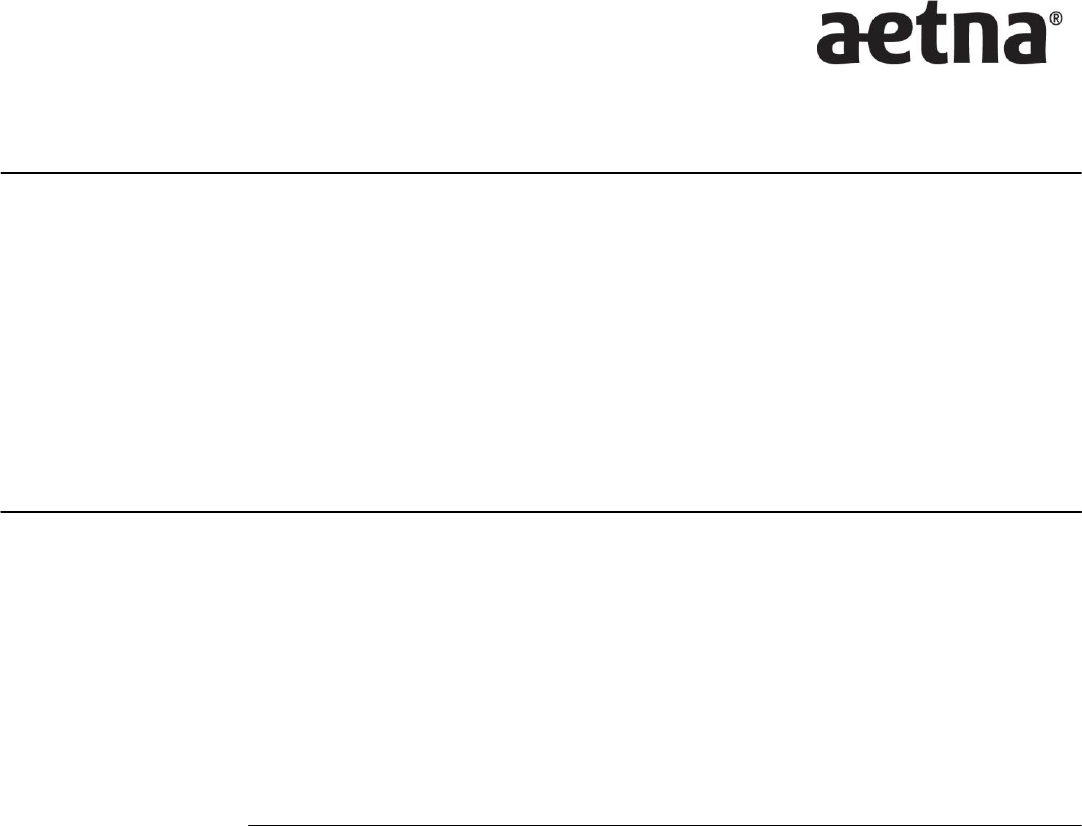

Engility Corporation - Full-time

Your Summary of Long-Term Disability (LTD) Benefits

Page 2 of 4

When am I considered to

be Disabled?

You will be considered disabled for 24 months from the date you last worked if:

After a significant mental or physical change resulting from an illness or injury, you can't

perform the material duties of your own occupation.

Your earnings are 80%, or less, of your adjusted Pre-Disability earnings.

After the first 24 months of your disability that monthly benefits are payable, you will be considered

disabled on any day that you can't perform the materials duties of any reasonable occupation*

due to illness and injury, and your earnings are 60%, or less, of your adjusted Pre-Disability

Earnings.

If your occupation requires a professional license or certification, you will not be considered

disabled solely because you lose your license or certification.

*Any "reasonable occupation" means a job you could be expected to perform satisfactorily in light of your age, education,

training, experience, station in life and physical and mental capacity.

Are there any offsets that

may reduce Long-Term

Disability?

Offsets

Your benefits may be reduced if you are receiving income from other sources. See your plan

documents for a complete listing. Examples include:

Employer sources: Government sources:

Any disability or retirement benefit

received under a retirement plan

Disability benefits received from any

statutory disability plan

Payments received from accumulated

sick time or salary continuation program

related to your current employer

Temporary disability benefits received under any

state or federal workers' compensation law

Benefits from Social Security or similar plan or

act

Income from a Governmental retirement system

earned as a result of working for your current

employer

Are there any exclusions

that apply to Long-Term

Disability?

Exclusions

You will not receive benefits under certain circumstances. Examples include:

Your disability results from an intentional self-inflicted injury; or you became injured while

committing a criminal act or driving under the influence of alcohol/drugs.

You are not under the regular care of a doctor when requesting disability benefits.

You are receiving payment under a salary continuance or retirement plan sponsored by your

employer.

Pre-existing Conditions

Pre-existing Conditions may affect the benefits paid by your Long-Term Disability policy:

A pre-existing condition is an illness, injury or pregnancy-related condition for which you were

diagnosed, received medical treatment, or prescribed medications during the 3 month period

before your coverage effective date.

No benefit will be paid for a disability that occurs during the first 12 months after your

coverage effective date that is caused by, or related to, a pre-existing condition.

Benefits will be paid for covered disabilities not related to a pre-existing condition.

Please refer to your policy documents for a complete list of income sources that will reduce your

benefits, as well as a complete list of exclusions and limitations.

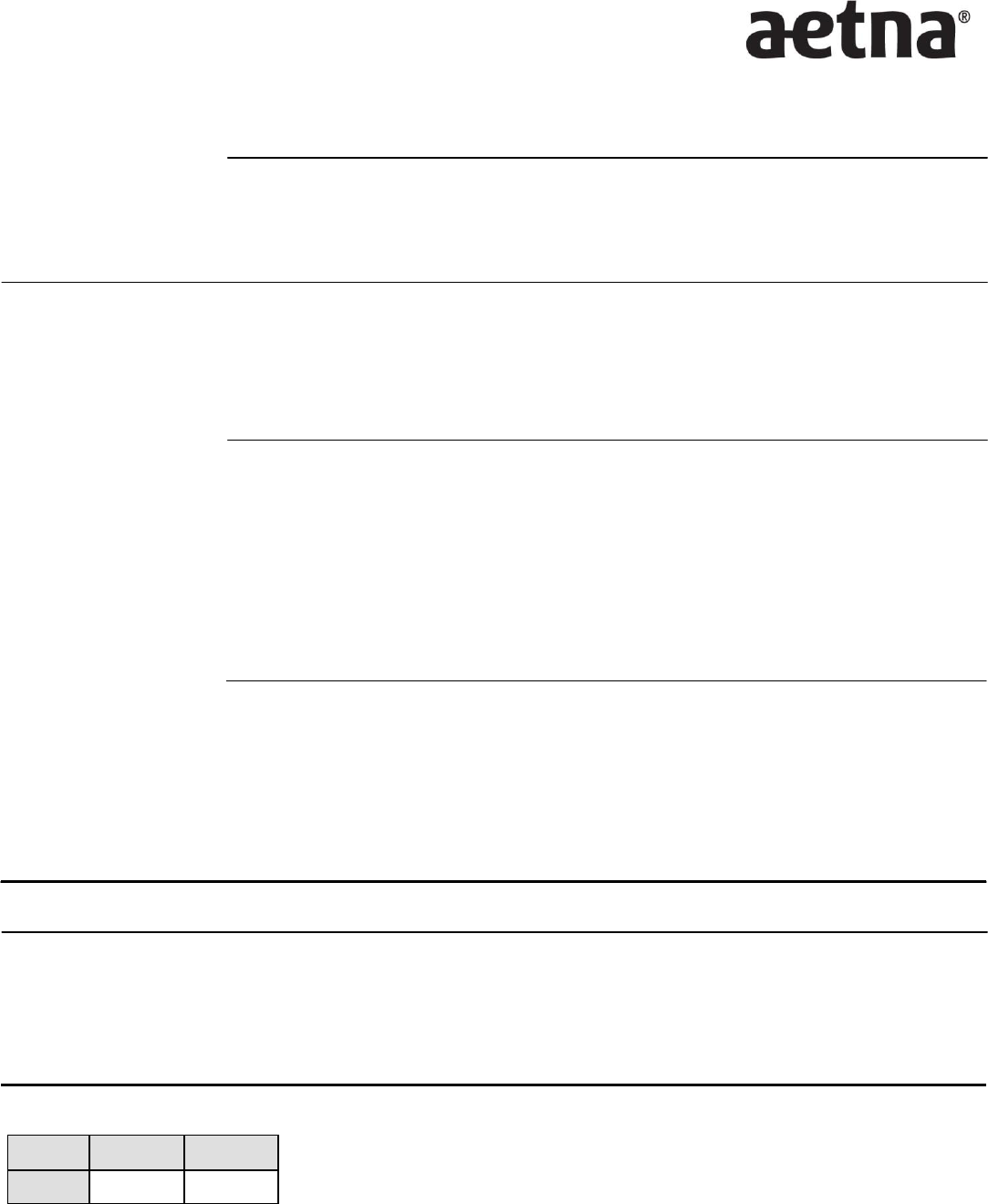

Engility Corporation - Full-time

Your Summary of Long-Term Disability (LTD) Benefits

Page 3 of 4

Are there any limitations

that apply to Long-Term

Disability?

Limitations

You can receive benefit payments for Long-Term Disabilities resulting from mental illness,

alcoholism and substance abuse for a total of 24 months per occurrence. This time period may be

extended if you are confined to a hospital.

Is there anything else I

should know about my

plan?

Recurring disabilities

If you return to work and become disabled again from the same illness or injury, it may be

considered the same disability. If it is, you will only have to satisfy one elimination period and may

be eligible to begin receiving benefits immediately if:

The disability recurs during the elimination period and within 30 consecutive days of work or the

disability recurs after the elimination period and within 6 consecutive months of work.

Partial disabilities

Partial disability benefits allow you to work, earn income and continue receiving benefits so you

can receive up to 100% of your income during the first 12 months of your disability. You are

considered partially disabled if, due to an injury or illness:

You are performing some of the material duties of your own occupation

And you are earning 80% or less than your Pre-Disability Earnings

After the first 12 months, partial disability benefits can continue based on a formula that you will

find in your policy documents.

Vocational Rehabilitation and Return to Work

Our goal is to help you return to gainful employment. Consultants will review each claim to

determine if rehabilitation services would be appropriate and effective. We will work with your

employer to provide reasonable accommodations to help you return to work. You may even

qualify for an increase in your benefits by participating in a rehabilitation program.

What additional features should I know about?

Survivor Benefit If you die during a period when you qualify for disability benefits we will pay your eligible survivor a

lump sum equal to 6 months of your gross disability benefit.

Conversion If your employment ends, you may be eligible to convert to a disability conversion contract as a

temporary policy until you become insured under another group plan. This conversion plan can

provide $4,000 of LTD coverage.

How much does Voluntary Long-Term Disability cost?

Monthly Rates per $100 of Covered Monthly Payroll:

Option 1

Option 2

Rate

$0.277

$0.498

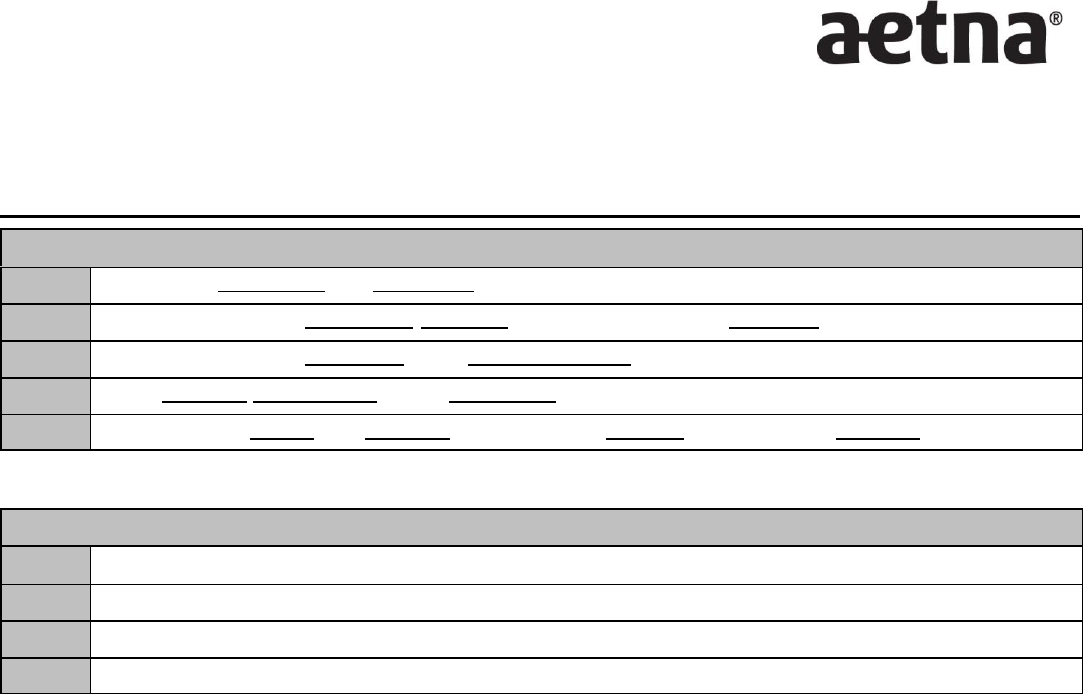

Engility Corporation - Full-time

Your Summary of Long-Term Disability (LTD) Benefits

Premium calculation

Calculation:

Step 1:

Annual Salary / 12 = Covered Monthly Payroll

Step 2:

Covered Monthly Payroll x % Percentage of Benefit = Monthly Benefit*

Step 3:

Covered Monthly Payroll / 100 = # Units

Step 4:

# Units x Rate = $ Premium Per Month

Step 5:

Monthly Premium x 12 = Annual Premium / # Pay Periods = $ Payroll Deduction

*Please note: Step 2 calculates monthly benefit and is not necessary for premium calculation. Subject to $10,000.000

maximum monthly benefit.

Example: Option 1, $45,000 annual salary

Step 1:

$45,000 / 12 = $3,750.000 Covered Monthly Payroll

Step 2:

$3,750.000 x .50 = $1,875.000 Monthly Benefit

Step 3:

$3,750.000 / 100 = 37.500 # Units

Step 4:

37.500 x 0.277 (Rate) = $10.39 Premium Per Month

This material is for information only. Insurance plans contain exclusions and limitations. See plan documents for a complete description of benefits, exclusions, limitations and

conditions of coverage. Policies may not be available in all states, and rates and benefits may vary by location. Policies are subject to United States economic and trade

sanctions. Not all services are available in all states. Policy form numbers issued in Idaho and Oklahoma include: GR-9/GR-9N and/or GR-29/GR-29N.

26.06.305.1_(8/2016)

Page 4 of 4

©2016 Aetna Inc.