®

TOPICS OF

INTEREST

3Q 20

MARIANNE FEELEY,

CFA

Managing Director|

Public Markets

AEIOU > PPPPP

August 2020

Summary

Manager research and selection have long been described in the language of Ps – people,

process, etc. Verus believes the familiar Ps approach, while useful, leaves out important

aspects of manager assessment and their products because of its focus on inputs. The Verus

approach is grounded in key principles that focus on outputs and enables us to differentiate

between products rather than merely describe them. We outline a vowel-based approach

that concentrates research on factors that are more likely to drive investment outcomes.

Introduction

In this paper, Public Markets Managing Director Marianne Feeley, CFA, outlines

the Vowels framework, a principles-based way to ensure manager research is

based on the qualities we look for, and not only the features that are also

important. In this piece we will review the conventionally adopted approach to

manager research where topics of due diligence are defined in terms of the

“Ps” approach. We will describe the Ps and how they are useful as research

inputs but not as helpful as criteria for differentiating investment products in

terms of conviction they will meet their investment objectives. We will then

introduce the Verus Key Principles (the Vowels framework) as a more useful

way to focus research on factors that are material to outputs achieved by

investment products. In conclusion, we will illustrate how Verus integrates the

Vowels into its standard manager research process.

Conventional Manager Research and Ps

Corner any investment professional who analyzes investment managers and

their products, and it won’t be long until they start to describe their research

approach using the familiar language of “the Ps”. The Ps are a concept

developed by marketing professor Jerome McCarthy

1

in 1960 to describe the

set of tools a business uses to sell products or services to its target customers:

product, price, promotion and place. The investment industry has since

1

2

TOPICS OF INTEREST 3Q20

borrowed the concept and redefined these terms, initially developed to describe the

selling of a product, to the research process used to vet an investment product’s ability

to meet investment objectives.

There isn’t precise agreement on which or how many Ps are ideal for this purpose. A

random internet search turned up the following: people, process, price, performance,

partnership, products, portfolios and parent. Philosophy also is mentioned, although

technically a P only alphabetically and not phonetically. Most research frameworks agree

on people and process; performance is often included but just as often excluded,

perhaps on principle.

The Ps are useful as part of a research framework. They are intuitive and familiar, owing

to their origins in marketing. They also serve as a good reminder of critical inputs for

management of investment portfolios. It’s dicult to describe an investment product

without outlining the people responsible for decision making or the process for selecting

investments and constructing a portfolio. However, their usefulness is also at the root of

their limitations as criteria for a conviction-driven assessment of investment products.

The Ps are ideal for when the aim is to describe – they fall short when the aim is to

differentiate.

The key drawbacks of Ps as a research framework is due to their function as descriptors

-- they are more coverage oriented than research oriented. They also tend to encourage

a checklist mentality where all of the coverage elements are considered equally. An

analyst addresses each of the Ps individually rather than focus on the integration of

elements that work together in a successful investment product. Overall, the Ps focus

more on the “what” of an investment product rather than the “why”. Yet, it’s the “why”

that better captures the reasons one “disciplined, risk-controlled, fundamental process

managed by a deep and experienced team” is more successful than another.

Verus Key Principles (the Vowels)

The Verus manager research framework is structured around a set of key principles that

reflect Verus’ research beliefs. The focus on research beliefs allows us to concentrate on

the factors which are most likely to drive investment outcomes. To emphasize this shift

in focus, we have deliberately defined them based on the five vowels (AEIOU) rather than

a single consonant.

While we look AT Ps, we look FOR Vowels.

When evaluating investment products, Verus focuses on how the various inputs to an

investment product work in combination to produce the aspects of that product that are

consistent with a sustained ability to meet investment objectives in a consistent manner.

The emphasis is on the outputs rather than the inputs.

3

TOPICS OF INTEREST 3Q20

Naturally, the inputs are relevant but evaluated in context rather than isolation. For

instance, over the years we’ve seen the same process applied with minor variations

across multiple investment firms. We don’t evaluate the process alone, but consider the

combination of skills, professional backgrounds, risk controls, incentives, organizational

features, systems and other aspects that interact with that process for an optimal

outcome.

The Verus key principles and the reasons we believe they are important are described

below.

Alignment –

The strategy is supported by a stable organizational and team structure. Evaluation

includes examination of the alignment of the investment management firm with its

clients; alignment of investment management firm with its investment staff; alignment

of investment staff with its clients. These relationships are examined by assessing the

fund manager’s business structure, fee structure and remuneration structure for

investment staff. Alignment is an important concept that does not merely describe the

people and organization but delves into incentive structures, business model and fee

structures as tools to align interests of management, investment team and client.

Edge –

The manager has articulated an ineciency or market-based belief that informs its

investment process. This edge is typically expressed as an advantage over the

benchmark but may also be evident as an advantage over peers. Evaluation includes

examination of the market ineciency the manager seeks to exploit; in other words, we

are looking for the fund manager to express a market-based belief and to be willing to

take risk based on that belief. We are also looking for evidence that belief is reflected in

alignment, implementation, risk management and performance. Edge is an important

concept that extends beyond an investment philosophy to elucidate how the other four

Verus principles contribute to how the product is differentiated from its benchmark and

peers.

Implementation –

There is evidence that the manager’s investment approach is sensible and repeatable.

Evaluation includes examination of the tools and processes whereby the manager turns

its market-based belief into a portfolio of individual investments; we expect the

manager’s resources to be aligned with their market belief and their specific area of skill;

we expect an investment process to be logical and repeatable and to make the best use

of the manager’s resources. Implementation is an important concept that encompasses

philosophy, resource, people and process working in concert to produce a repeatable

result.

4

TOPICS OF INTEREST 3Q20

Optimal use of risk –

The manager has an effective framework to assess and manage risk inherent in its

process. Evaluation includes examination of the tools and processes whereby the

manager evaluates sources of risk in the portfolio, assesses whether they are intended

risks or unintended risks, and appropriately scales the former and mitigates the latter. It

also involves an examination of the sources of risk inherent in the process and the

verification that intended risks are aligned with the manager’s investment beliefs and

areas of skill and resource. Optimal use of risk is an important concept that addresses

both sides of the risk construct; it extends to the manager’s ability to deliberately use

risk where it has skill and to be aware of and control risk where it doesn’t.

Understandable performance–

There is evidence that historical performance appears consistent with the manager’s

expressed process. Evaluation includes examination of the manager’s means to

implement and manage risk through the lens of different market environments; the

performance results are consistent with the manager’s identified area of skill, and

conditions when the product may outperform or underperform are well understood.

Understandable performance is an important concept that is not limited to quantitative

examination of return but also the understanding of how those returns reflect our

expectations of the interaction of a manager’s skill and resource with the investment

environment. It is tempting to describe performance as “good” or “bad” and use it to

apply judgement in a rear-view mirror fashion. Ensuring performance is understood

ex-ante is one of the elements we believe to be essential to determining whether

underperformance (or outperformance) is a concern.

The principles above embody subjective information used to evaluate manager skill.

Embedded in these subjective evaluations is review of objective information including

but not limited to: performance record, risk systems, portfolio holdings, vehicle

availability and fees.

Illustrations and Examples

Although we would like to make the claim, Verus has not discovered evaluation criteria

that have never been considered before. However, we would point out that the Vowels

framework is not merely a different version of the Ps. The following table illustrates how

these concepts incorporate the broad set of inputs involved in an investment product.

5

TOPICS OF INTEREST 3Q20

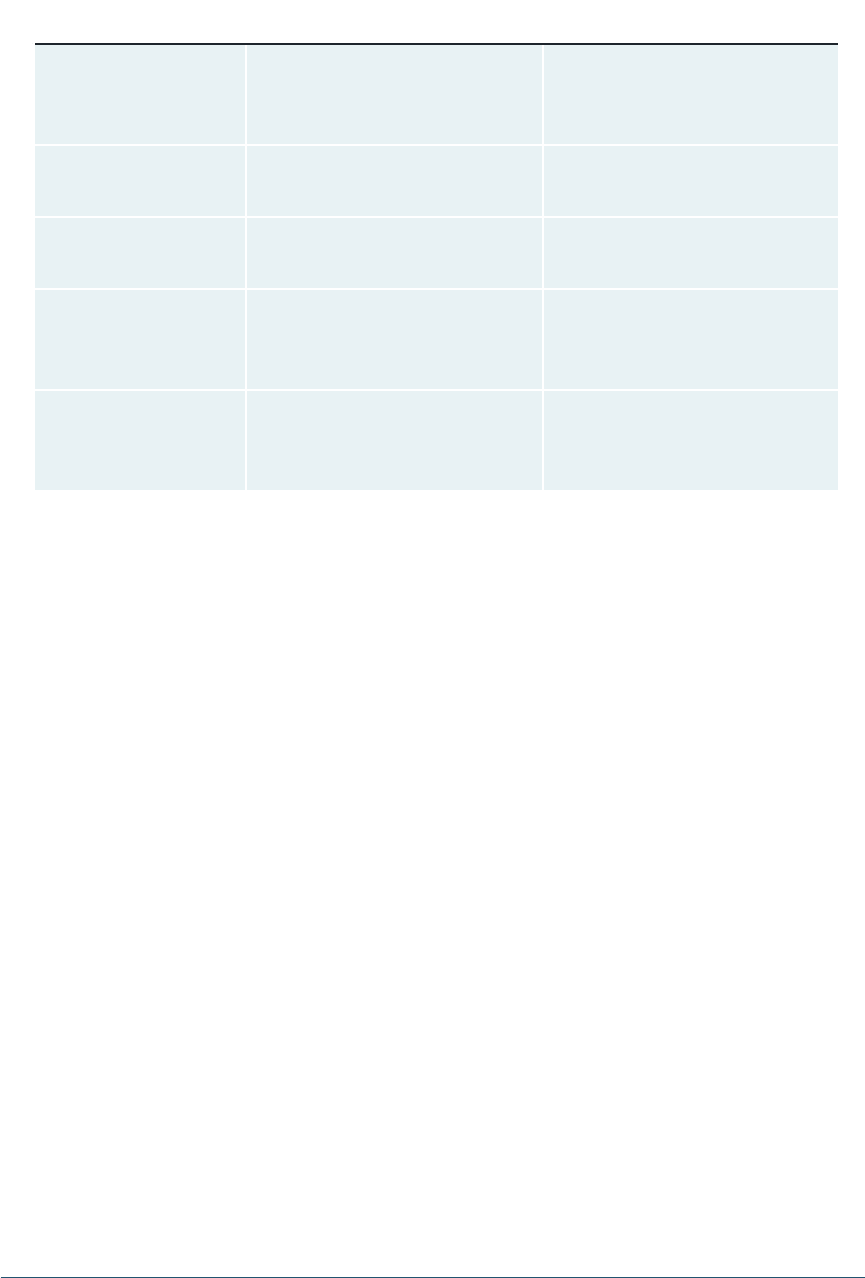

Principle Ps Incorporated Other Concepts

Alignment People, Partners, Parent,

Product, Price

Incentives, Succession,

Capacity,

Attraction/Retention

Edge Philosophy, Process,

People, Portfolio, Parent

Culture, Resources, Tools

Implementation Process, Portfolio, People Research, Consistency,

Logic, Adaptation, Tools

Optimal use of risk Process, Portfolio, People,

Performance

Skill, Holdings,

Measurement, Tools,

Adaptation, Liquidity

Understandable

performance

Performance, Process,

Portfolio

Learning, Environment,

Style, Adjustment,

Attribution

A few generic examples demonstrate how the Vowels contribute to clarity around degree

of conviction in a product and changes or concerns.

The first example is an overall product description laying out the degree of conviction

within the vowel framework:

Alignment –

We believe that Manager’s partnership with Parent in 2016 allowed the firm more resources

so that they can better focus on investing. Conversely, partnership with the large firm

decreased the alignment of key investment professionals at Manager with firm outcomes.

Incentive compensation motivates professionals to debate and challenge ideas.

Edge –

We believe the simplicity and structure of the team’s philosophy create an edge. The team

believes that trends that benefit growth and profitability for the companies it owns tends to

be more powerful and longer lived than widely believed. Manager is truly a research driven

firm, and the independence of professionals in conduct of research helps to retain staff.

Implementation –

The stability of the team that operates under one shared philosophy helps the team make repeatable decisions.

The team has access to resources such as people and technology that translate investment edge into a portfolio.

Optimal use of risk –

The approach is benchmark agnostic with an absolute return target over the cycle. Stock specific risk is the

primary focus, and tracking error can be high. The team has focused more on its sell discipline recently.

6

TOPICS OF INTEREST 3Q20

Understanding performance –

Long-term growth approach leads to better performance in risk-on markets;

broad portfolio may suffer in narrow or momentum-driven markets. The product

is not appropriate for short-term benchmark-oriented clients.

The second example illustrates how we use the Vowels framework to analyze change in

investment management firm and put that change in context of the principles-based

elements that support conviction in the product.

Our initial read is that Smith’s hiring is part of Manager’s long-term business continuity and succession

planning. Speed of implementation of Manager’s research agenda appears to be the primary area

that Firm management are looking to improve with Smith leading the charge. As for the departure

of Jones, we viewed her as a competent member of the team, but not necessarily integral. We view

these changes as something to monitor, but no reason for immediate action. Given the organizational

change, we will watch for any material changes to the investment team (none are expected).

The third example reflects rearmation of conviction in a product that endured

significant underperformance in 2018.

Based on this meeting, we are rearming conviction in the Manager’s strategy. On balance, we believe

the recent succession related issues, new incentive structure, and strategy line up rationalization were

thoughtfully handled and make sense as the firm tries to maintain proper alignment with outside

investors. From an investment and risk management perspective, we appreciate the continued emphasis

on identifying, profiting from and rewarding short ideas along with the ongoing effort to better position

portfolios for rapidly changing regimes across the market. Finally, we are pleased to see the fund post strong

short-term performance during the current equity volatility as it digs out from its 2018 drawdown.

Conclusion

It is important when assessing actively managed investment products, to make the distinction between

inputs and outcomes and to use each appropriately. We believe framing the inputs to an investment product

by looking at Ps (philosophy, process, etc.) is certainly useful to ensure we have considered the key features

of that product. However, if we stop there, we have engaged in more of a cataloging exercise rather than a

critical assessment of the product’s value proposition. We view the Vowels (Alignment, Edge, Implementation,

Optimal use of risk, Understandable performance) as the differentiators we are looking for rather than

merely descriptors we can look at. By implementing a Vowels-based approach to manager research, Verus

focuses attention on the aspects of an investment product that are critical to drive investment outcomes.

1

1

A"McCarthy's 4PS59.

1Anderson, L. McTier, and Ruth Lesher Taylor. "McCarthy's 4PS: Timeworn or Time-Tested?" Journal of

Marketing Theory and Practice 3, no. 3 (1995): 1-9. Accessed May 19, 2020. www.jstor.org/stable/40469759.

7

TOPICS OF INTEREST 3Q20

Disclosures

Past performance is no guarantee of future results. This report or presentation is provided for informational

purposes only and is directed to institutional clients and eligible institutional counterparties only and

should not be relied upon by retail investors. Nothing herein constitutes investment, legal, accounting or

tax advice, or a recommendation to buy, sell or hold a security or pursue a particular investment vehicle

or any trading strategy. The opinions and information expressed are current as of the date provided or

cited only and are subject to change without notice. This information is obtained from sources deemed

reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. This

report or presentation cannot be used by the recipient for advertising or sales promotion purposes.