1

ADVANTAGE AND DISADVANTAGE OF THE NEW FRAMEWORK FOR

DOING BANKING BUSINESS IN AN INFORMATION ECONOMY

Elena Parnardzieva Stanoevska,

Faculty of Economics and Administrative Sciences, International Balkan University,

elena.parnardziev[email protected]

ABSTRACT

Modern technology related to products and services based on knowledge reduce the distance

between clients and banks which results with focusing on offering of new electronic (online) banking

products and services. Today, more and more the question is raised: At what stage each of the electronic or

physical market model is more appropriate for banking operation as a function derived from the

characteristics of the transaction? The Internet, the quick communication, the coordination and the

collaboration help banks to cut transaction costs through virtual integration with their clients. Contemporary

information and communication technology (ICT) leads towards reduction of transaction chains and

separation of some of the operational activities of the banks, i.e. towards more efficient ways models of

banking operation.

The paper deals with the challenges that the banking sector is faced as a consequence of the latest

developments of ICT. The possibility of making numerous transactions with just one click, the facilitated

access of the clients to the internet, the reckless pace and the new way of living, especially due to the Covid-

19 pandemic, further accelerated the development and the implementation of electronic banking (e-

banking). In this regard, the goal of the paper is to explore the new business model that banks need to apply

in the contemporary banking operations as well as to point out the advantages and disadvantages of

increased e-products and e-service development in the banking operation in an information economy.

KEYWORDS

E-BANKING, INFORMATION AND COMMUNICATIONS TECHNOLOGY

JEL CLASSIFICATION CODES

G210, G32, O33

1. GOALS OF THE WORK, MATERIALS AND METHODS

Primary goal of the paper is to demonstrate the new business model that traditional commercial

banks need to apply in the contemporary banking operations, as well as positive and negative aspects of

fintech products implementation. Namely, as a results of the new ICT, the new fintech products and

especially due to the Covid-19 pandemic, commercial banks will prefer electronic versus physical offers of

financial products and services and shall try to separate their basic business activities, i.e. utilize services

from external operators. For the preparation of this paper, secondary data for analytic and field research

have been used whereas surveying, inductive and deductive methods as well as analysis and synthesis

methods have been applied. Internet was used as a major tool to approach data and literature. Figures and

graphical methods have been employed for visual presentations during the research.

2

2. NEW BUSINESS MODEL IN THE BANKING SECTOR

ICT, as information-intensive, transforms the market by changing the models for commercial

banks, forming links between market actors and contributing to changes in the market structure. It changes

the market structure by expanding transactions and suppliers in the market, thus opening the possibility for

new models of organizing services and running the business. In the presence of the activities of ATM

machines, e-banking, m-banking, as a result of the change in the way the value is generated and the profit

gained and with the significant modification of the service and supply chains, a new type of business

banking model emerges. In the new model, the profit is not gained as before from the difference between

the marginal costs of the services, i.e. the differences between the active and passive interest rates, but is

gained by integrating service and supply chains. In the presence of e-banking, instead of loans, revenues

are increasingly generated from indirect sources such as generating new types of financial products and

their good presentation on the market. In addition to the direct economic benefits of e-banking, such as

reduced costs of taking over transactions in the electronic marketplace, other indirect benefits may also

arise, such as better information processing and changes in organizational form. The Internet is changing

the organization, and thus the process of risk management in banking: new channels will be opened for the

distribution of knowledge and human interactivity.

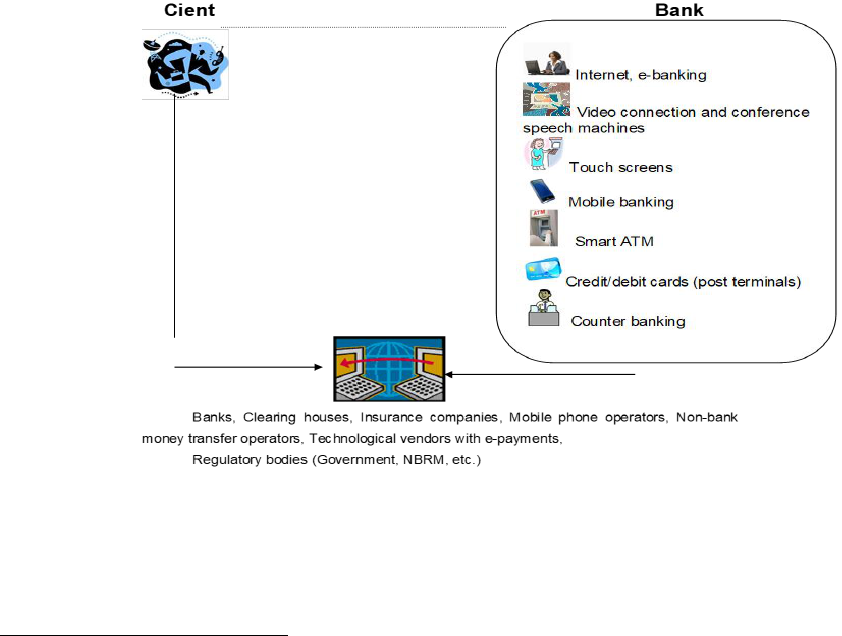

The assumptions of the new framework for doing business in banks presented below are: each bank

has Internet access, the subject of the transaction are electronically delivered products and services, the

connection will be sufficient to ensure the implementation of interactive multimedia transaction, there will

be no favoritism market access and cheap and fast computerization will be available

1

. Based on these

assumptions, the new banking framework will be as shown:

Figure 1. New framework for doing business in banks

Source: Summarized by the author

The new framework consists of horizontal transactions and a network of partners or vertical

transactions. Horizontal transactions describe the various business processes in the global transaction chain,

while vertical transactions denote the number of independent participants – a network of partners. In

1

Material goods (statements, contracts) can also be sold online, but their delivery to the consumer requires certain transport costs.

3

contrast to the functional components of the traditional banking model known in the literature as brick and

mortar, in the new model the client can access financial products and services with just one click, i.e. the

new model will be: click-click (click- click). From the point of view of the supply chain, the new ICT

transmits power from the client bank, where the next sale is just a mouse click and freely distributing a

huge amont of information about prices, products and services. As can be seen from the figure 1 above,

ICT changes the cost structure of the bank in terms of costs required for communication/customer support

and execution of financial transactions. As a result, distance is reduced, contributing to a reduction in

communication costs in two of three possible ways: by reducing the cost of remote communication

methods, by reducing communication delays, but also by reducing the volume of regular face-to-face

meetings in person. Reducing costs in each of the horizontal transaction processes in the model will provide

visible benefits not only in terms of improving financial services but will also contribute to maximum

benefits within the bank itself. Namely, the new model of full automation at all levels and processes will

enable the growth of efficiency, enhancing profitability and providing services that did not previously exist.

The vertical definition of the new business model, in addition to banks, insurers and other actors in

the network economy, includes regulatory and governmental bodies that will have to make strategic choices

and create an appropriate environment for the development of the information society. The only thing that

can increase the complexity of the new model is the number of independent participants involved in the

execution of the transaction and additionally, the technological heterogeneity and technological knowledge

of each of them. It is obvious that before starting to exchange information, network partners need to know

the way each of them runs the business. Therefore, as Simon (1991) has emphasized, The claim that markets

allow every firm to run its business with little knowledge of its partner's business is more of a fiction than

a statement. The organization must redefine its scope of influence through the active cooperation of all

participants in the overall transaction chain. In order to analyze the network of partners, which is actually

outside the scope of this study, it is necessary to focus on management, on optimizing the connection

between them, as well as on the external organizational environment.

As a result of e-banking, e-payment and their potential to reduce the costs of imperfect information,

there is a significant shortening of the supply and delivery chains of financial services, which changes the

organizational structure of banks and reduces the need for traditional branches. Traditionally, easy access

to information is provided through intermediaries. Therefore, in the new framework, any financial product

that can take digital form can easily disrupt the traditional distribution channels for such a product. Thus,

in addition to banks and payment card issuers as the main agents of e-banking and e-payment, new players

are emerging in the new framework. Namely, recently there emerged many non-bank money transfer

operators, mobile phone operators, sellers of new e-payment technology who are trying to take over some

of the value-added operations of the main agents or at least to enter into cooperative agreements with

them.Lately, instead of referring customers to bank branches, they get easy and fast access to banking

services through ATM’s cash deposit, cash withdrawals and other types of transactions. As Wiegand and

Benjamin have pointed out, over time, the e-market place will evolve from a single source of electronic

sales channels through biased markets

2

to personalized markets where the consumer (customer) can use

help in making a choice. Thus in the network economy, opportunities are opened for the creation of a third

party, the so-called "info-intermediaries"

3

or "new market founders". The effect of market founders is a new

phenomenon that is very good for consumers (customers), while suppliers (banks) lose part of their profit

margin, and market founders get the rest of the profit. If the founders of the market are owners or have a

significant interest in a supplier, they can turn the market in their favor and as a result, put consumers and

other suppliers at a disadvantage. Given that the effects of market founders can be a threat to markets,

competitive market founders are needed to prevent market distortions.

Today, the largest online payment provider, PayPal, which belongs to e-Bay, has a growing role in

the online auction market. Customers have PayPal accounts with which they make e-payments. They

2

Prejudice markets are markets where the founders of a market that is one of the suppliers, use the mechanisms of market transaction to their

advantage.

3

Info Intermediaries is an interactive agent who would research products that are in demand by the consumer and would take care of individuals

around their privacy and secure payment.

4

replenish their accounts directly by transfer from bank accounts or by means of credit cards and checks. In

just two years, PayPal accounts have doubled, with 143 million accounts in 190 countries (35 million of

which are in Europe) (UNCTAD 2007-2008). While in 2011, more than 232 million accounts were

registered, of which over 100 million were active, in 2021 PayPal operates in 202 markets and has 377

million active, registered accounts. It allows customers to send, receive, and hold funds in 25 currencies

worldwide whereas from 2021 it will allow customers to use cryptocurrencies to shop at 26 million

merchants on the network.

4

PayPal offers services not only to individuals (B2C markets) but also to legal

entities (B2B markets). New potential players in the market are Google and especially Microsoft, with the

introduction of an online micro-payment service. Additionally, large companies for telecommunications,

energy, etc. are increasingly introducing their own systems for electronic payment of monthly bills for

electricity, telephony, internet, television, etc. With the opening of this type of online payment portals by

larger corporations, the need for over-the-counter operations and the commissions that the bank charges for

this type of service are increasingly reduced. According to a research conducted at Macedonian banks, the

cost for one banking transaction implemented via Internet payment (classic payment via PP30 order

implemented through KIBS) varies from 5 to maximum 20 MKD whereas at least 20 up to maximum 45

MKD are needed for the same transaction implemented via the counter.

The research, coordination and monitoring costs that banks and other institutions have with the exchange

of financial documents, services or ideas are increasingly reduced with the online transactions. Through

cutting of transactions and processing cost, the number of branch offices required for serving the same

number of clients is reduced. It is assessed that the implementation of one transaction is several times higher

in a traditional branch office than the cost for the implementation of the same transaction by using the

Internet.

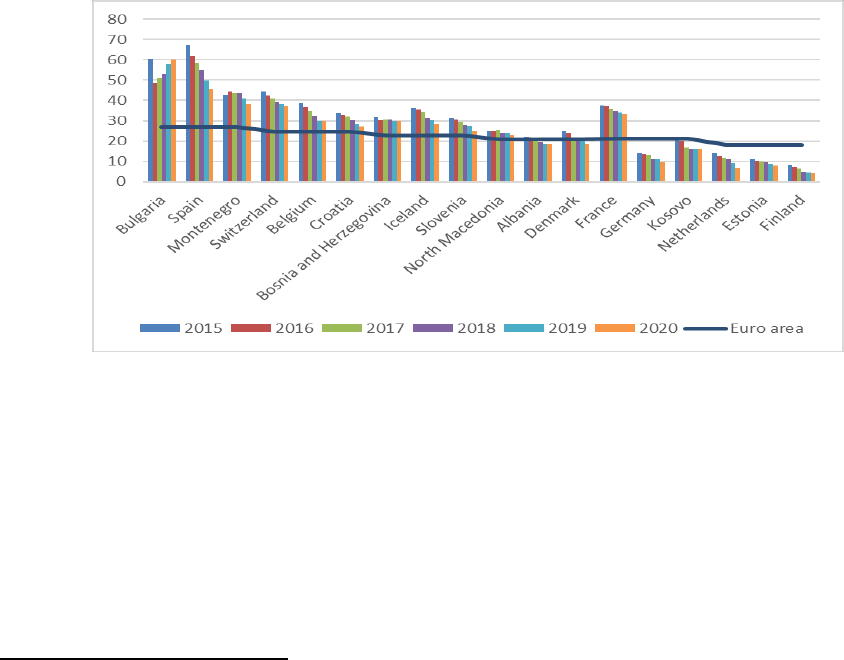

Chart 1: Number of commercial bank branches (per 100,000 adults)

Source: World Development Indicators -http: //data.worldbank.org/indicators

The number of branches of commercial banks in Europe has been declining significantly in recent

years. A slight increase was observed only in Bulgaria. Namely, according to the data of the European

Central Bank in 2011, banks in Europe have closed 7,200 branches, i.e. their number has decreased by

about 20,000 compared to the number before the financial crisis in 2008.(Utrinski Vesnik, 2013). This

decreasing trend continue from 2015 to 2020. In an effort to reduce operating expenses and increase profits,

banks are increasingly closing their branches. Easy replacement of their functions with the application of

electronic, in particular Internet banking only further facilitates and encourages that process. Reduced

transaction costs will lead to reduced branch visits, reduced volume of high-frequency routine transactions,

i.e. the need to redesign their role or close them. The advantage of the cyber branch office over physical

4

http://en.wikipedia.org/wiki/PayPal

5

branch office is the fact that it is open for 24 hours, it covers the global market and its variable costs

continuously fall (UNCTAD 2007-2008). In Switzerland, UBS Bank, one of the largest global banks, in its

branches, with ATMs, has installed the so-called Multimat machines with screens that allow customers to

use them for transactions similar to those offered by internet banking. As a result, the employees of the

branches of this bank are becoming more and more financial advisors who help the clients in making

decisions about the source of the various financial instruments offered by the bank. Taking into account

this and many other similar examples in practice, branches will modify their appearance and role in the

future, i.e. they will look more like shops, salons, service centers that will present their new financial

products and offer financial advice. Additionally, with the development of technology and its increasing

application by customers, these functions of the branches will be easily replaced by new so-called video

terminals.

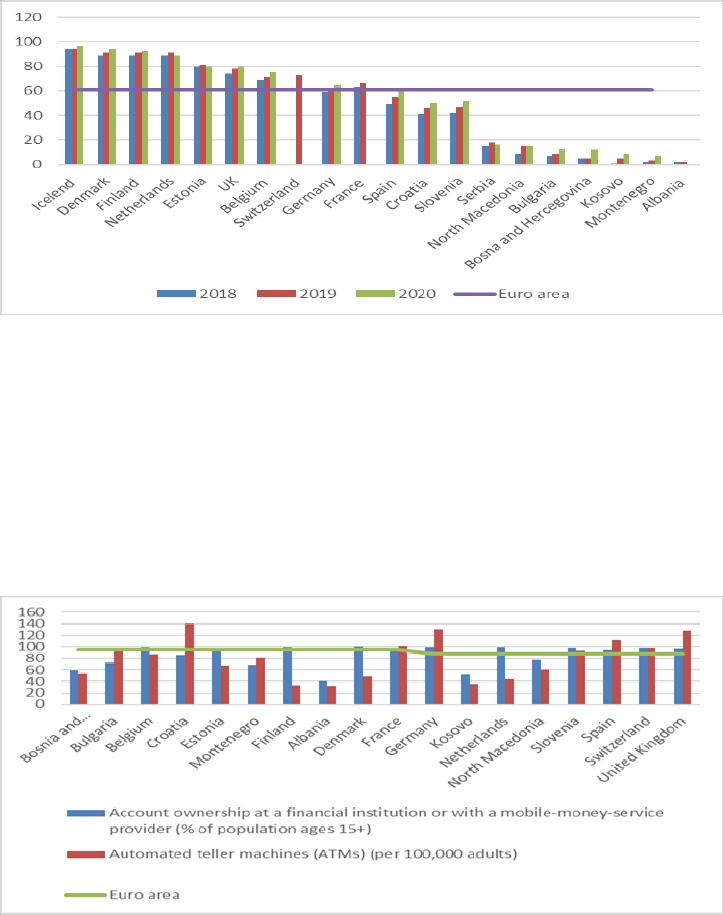

Chart 2: Individuals using Internet for internet banking (% of individuals)

Source: Eurostat

However, as statistics show, although e-banking, online or mobile payment lead to changes, they

will still not eliminate the role of banks and their branches. Developing countries, especially Balkan

countries are far from the average of the Euro area of 61 percent usage of the internet banking. Except for

Croatia and Slovenia that are slightly better at using this category of Internet services. According to the

United Nations International Telecommunication Union (ITU) nearly three billion people or 37 percent of

the world's population have never used the Internet even though due to the coronavirus pandemic the

number of Internet users has increased from 4.1 billion people in 2019 to 4.9 billion in 2021.

Chart 3: Using of ATMs and a mobile-money-service provider in 2017

Source: World Development Indicators -http: //data.worldbank.org/indicators

6

Given the growing penetration of mobile smartphones, it is very likely that they will become the

main channel for the transfer of online payments, especially in those countries and regions where there are

few branches and ATM networks.

3. ELECTRONIC LENDING

Electronic lending (e-lending) or also known as web lending (CreditOnWeb) is a modular system

that automates the entire lending process. It is loan or lending software that automates and manages the

loan lifecycle from origination to collection. It is a holistic view of borrower transactions on a single

platform, regardless of the type of loan, size of business, or industry regulations. Automation includes:

collecting data and information about the client, evaluating his rating, detailed definitions of credit

applications (type of loan, type of collateral), as well as monitoring the entire work process up to the

approval phase. Additionally, e-lending supports activities related to disbursement of already approved

credit lines and the daily obligations of monitoring, including loan refinancing, restructuring, activating,

writing off already approved loans, activating collateral, as well as continuous updating of data and

information. Its application is possible for all clients of the bank (population, small, medium and large

corporations), where there are special modules for economic group assessment and analysis of economic

sectors. The introduction of automated instruments to support the overall lending process enables easier

monitoring of the life cycles of the agreed processes, as well as overcoming the operational risks from the

manual activities.

Namely, the advantages of electronic lending are in the direction of:

saving time (reducing the time required to go to the bank, preparing contracts and other

documents in the lending process);

lower operating costs and increased efficiency;

eliminate a paper workflow, as well as minimizes error and effort when tracking and

reconciling loans across enterprises and stockholders (reduction of operational risks);

to control credit risk, better customer interaction, configure loan products, provide analytics,

and create dashboards and reports

standardization of business processes;

greater opportunities to support and monitor increased volume and growth of lending.

Figure 2: Schematic presentation of the main e-lending activities

7

The new e-lending system implies the possibility for banks to evaluate their customers for all their

products from a single credit application. Namely, with the help of the system, the analysis and assessment

of the credit risk at the level of each client would be performed, taking into account all the products of the

bank (credit cards, consumer loans, mortgage, etc.). Based on the initial application of the client and

analysis of the additional amount of credit that he / she can submit, an analysis of the products that would

be appropriate for the client is performed, ie the system would suggest the best instructions. The new system

would set credit limits, offer products that the client could use, and make final decisions about approving

or rejecting the loan application. With the introduction of an individual customer management system,

which means setting pre-approval limits for each product, banks have managed to increase profitability by

9% and reduce the chances of bad placements in almost all products by more than 60% (Gordon, FICO

2012). Namely, the new electronic approach to decision-making improves the risk management process,

by reducing application and processing costs and by increasing banks' profits from the influx of new

customers.

Electronic lending can be easily integrated with the legal system, i.e. it has the opportunity to apply

a wide range of stages of legal procedures in order to integrate the data and avoid unnecessary information

and functions. Namely, there is a special software tool Acalled CONTMAN, which enables the automatic

preparation of standard contracts (contracts defined by the legal service), as well as the management of

texts in a working version if negotiated with the client. Also, with a special module for creating reminder

messages, it is possible to enter and record some future obligations that the client has to fulfill.

(www.exprivia.it)

4. ADVANTAGES AND DISADVANTAGES FROM THE DEVELOPMENT OF

E-PRODUCTS AND E-SERVICES IN BANKING OPERATIONS

Today, under the pressure of digitalization, increasing financial liberalization, globalization and

increasing competition, banks tend to increasingly use more sophisticated information methods and

technologies, in order to reduce risks, increase efficiency, productivity and profitability in operations. New

fintech products such as Internet e-banking, mobile phones-mobile banking, plastic money-plastic cards,

are becoming increasingly crucial in the banking industry. The Internet penetration today is stronger than

ever. According to the EU agenda, 9.2 billion Euros are expected to be invested in the key digital

technologies between 2021-2027. The goal of the new investment Digital Europe Program is to ensure that

all Europeans possess the skills and the necessary infrastructure to meet a full range of digital challenges.

(European Commission, 2020) If we consider the global growing tendency of the Internet penetration, the

application of mobile and wireless communication and uncertainties caused by Covid-19, it can be

concluded that the innovative tools in banking sector are predestined for further even greater growth and

development.

Technology is often seen as a mechanism for improving productivity and efficiency in banking. E-

news in banking reduces transactional, ie coordination costs, intensifies and modifies traditional risks, cause

changes in the organization of banking operations, as well as increase the efficiency of operations. The

gains from the increased banking efficiency are followed by the qualitative improvements of the existing

banking services and the creation of constantly new products. However, e-innovations in banking need to

be analyzed from both sides of the equation: positive changes and new opportunities on the one hand, and

challenges and dangers on the other. As a modern method of identifying customers, e-banking contributes

to the erosion of economic and geographical boundaries by allowing people to communicate and do

business anywhere and anytime. Namely, with the electronic transmission, the transactions are performed

without movements by the clients. Therefore, by removing geographical boundaries and allowing

customers to conduct transactions around time and space, e-banking significantly reduces the importance

of time and contributes to huge time and cost savings. The Internet, as a means of electronic payment,

reduces communication costs and expands the limits of banking capacity. It unites banks and customers all

over the world, generates different pricing mechanisms, ie enables comparison of financial products and

services. The Internet, leads to redistribution of resources and consequently to improved competitiveness.

8

With its use, financial products can be easily converted into a digitized information stream with zero

transport costs.The speed and low transaction costs of e-banking and e-payment are the strongest driving

force for the exponential growth of the Internet in the financial sector. Thus e-banking sè more becoming

internet banking or online banking.

The advantages of the development of e-products and e-services in the banking business can be

summarized primarily in: a) the possibility of presence everywhere; b) faster and greater access to new

types of banking transactions; c) increasing ability to consolidate operations in financial operations and

improve overall efficiency; d) drastic reduction of transaction costs; e) increased competitiveness,

flexibility and responsibility to customers. E-banking has the potential to accelerate existing trends and

introduce new ways of doing business, organizing work and networking in society. Lower transaction costs,

network effects created by increased returns and larger economies of scale, which can be achieved through

the use of e-services online.

From the point of view of the clients, the advantages from the development of ICT, especially from

the appearance of online e-banking are: a) opportunity and possibility for payment from anywhere in the

world; b) improved quality of services; c) personalized banking products and services; d) rapid response;

e) low fees and commissions; f) new banking e-products and e-services. Namely, the advantage of

electronic banking is that before the transaction is completed even in the traditional way, by posting the

necessary information in an available form online, customers are a priori in a position to know which

financial product they want and can use.

Today, e-banking and other fintech products takes a swings in economic terms and their potential

are growing. There are a number of challenges that need to be overcome in order to take full advantage. In

addition to non-proprietary standards and the open nature of electronic operations will lead towards

increased transparency and competition (positive effects) will also lead and potential invasions of privacy

(adverse effects). Limitations, shortcomings of e-news in banking can be identified as:

1. Overflow of information syndrome. Namely, the average users, individuals or companies,

especially small and medium-sized ones, may be confused and do not know how to work and research with

an obvious definite list of information services.

2. Need for certain new costs for physical installation and maintenance of the new ICT (websites,

hardware, software programs). The entry fee can be quite high, not only in terms of the capital costs required

to introduce the technology, but also in terms of understanding the technology, especially how to make full

use of it. However, despite the fact that some websites, hardware and software programs cost thousands of

millions of dollars in the markets, there are of course cheap and simpler ones that can be more easily

designed and upgraded.

3. Restraint in the application of web-based strategies due to the observed "uncertainty" about the

use of the Internet as a business environment and as a basis for contact. The basic business needs and goals

in banking are for transactions to be private, secured, guaranteed and timely. Not all of them can be filled

with online e-banking. Fintech product are sensitive to external attacks. Without adequate collateral

technology in banking, incalculable financial damage (high operating risks) as well damage to its reputation

(high reputation risk). Namely, a confidential document may be made public or pass into the hands of

competitors. Additionally, misuse of credit cards or banking information may compromise the client, or in

addition to simple theft, financial documents may be altered and illegal transactions may be conducted -

high operational risks. Risk of using e-news in banking is created by providers, while insecurity claims are

created by end users. Therefore, while the new ICT may drastically reduce some transactional, distribution

costs, new costs associated with building trust and reducing risks will arise.

4. Internet e-banking reduces the volume of face-to-face meetings. Given that preferences for an

alternative variant of the product are often explained more easily by the use of gestures and intonations than

by grammatical sentences, we can really argue that e-banking has its limitations. When transactions are

performed online, customers are faced with asymmetric information. With inability to physically verify the

information being exchanged. By making the information in a richer electronic (digital) form, an attempt is

made to overcome the problem with the asymmetry of the information. However, Internet information very

often has a commercial motivation and value, thus the accuracy of such information is often questioned.

9

Given that at the current stage of development there is a lack of statistics that can measure the level,

growth and composition of e-products and e-services in banking, it is still unclear whether fintecks is the

key that will help banks simplify and improve business processes in their operations. Through capital

increase, technological change leads to changes in capital and labor, to an increase in capital productivity,

which in turn leads to growth and development. In the long run, the combination of new banking products,

expanded market research, income gains and reduced fees and commissions as a result of increased

productivity will lead to increased net profits. Namely, in the long run, every bank probably will have more

advantages than disadvantages of increased volume and facilitated access to information, products and

services. Banks that will be the first to be able in their strategies to implement e-innovations in banking,

will also be leaders and first beneficiaries of finteck gains.

5. CONCLUSION

At the current level of development, although there are more and more network (electronic) bank

branches, neobanks, it is still too early to talk about massive switching of all clients to full use of online

electronic financial services, especially considering the conservative behavior and their habits to link to

existing services. Although in the last decade there is increasing number of neobank as Chriss Britt (CEO

of CHIME biobank) has said that they’re “more like a consumer software company than a bank,” i.e. they

mostly make money when customers swipe their debit and credit cards in contrast to the big banks who

make most of their money on fees, penalties, and loans. (Volenik, 2021) Large European banks are actively

joining each other in technology groups in order to further develop security in payment systems. They have

prepared plans to develop an integrated approach to the inclusion of electronic services in all their branches

and affiliates. Today, banks in Europe and the United States are increasingly embracing the click and mortar

model or the brick and click approach. They combine the benefits of traditional banking (face-to-face

interactions) with the speed, 24/7 availability and lower costs of e-banking. However, the innovation of the

click approach, ie the innovations in ICT continue to continuously transform the business banking model.

Whether the traditional commercial banks will fully apply the new ICT features depends on the flexibility

of the employees and the existing efforts of the bank to innovate. The first step that every bank should think

of in terms of application of e-products and e-services is to contemplate and determine its position with

regards to:

• The position that it has on the banking and financial market,

• Current and planned developments of the other players on the market,

• The nature of the services that it delivers compared with the services of its major competitors,

• The type and the size of risks it will be faced with and can manage during each operation,

• The type of clients it attracts and supports (especially whether or not they have an opportunity to

be connected with the Internet).

Generally, as the fintech products develops and due to the increase of transactional costs for the

organization of the physical market banks fail to take the advantages offered by the e-market and in doing

so to make best use of the production factors. Thus, it is more efficient to perform the transaction on the

physical market up to the level where the losses and the costs are equal with the marketing costs spent if

the transaction is performed via the electronic market. The lower adaptation costs (easier organizational

implementation) as well as the high value changes are significant factors for early acceptance of the new

architecture. (Bresnahan 2001).

With the growing reduction of the corporate structure of the banks, expansion of the subcontractors

and the new founders of the markets will contribute to increasing the number of participants in both

domestic and international payment operations. New players of the financial markets (non banking

operators for money transfers, techno sellers with e-payment, neobank, operators with mobile phones) will

increase competition and reduce the profitability of the traditional commercial banks. The success and

profitability of the banks will be largely determined by their ability and skills to allocate every saved capital

in sufficiently flexible multiple instruments which will be repeatedly applied and will reduce the risk level

10

in the decision-making process. Economy of Scale will be prerequisite for the long-term profitability and

sustainability of the banks. Some banks will be able to independently access the organic growth by

exploring the available cost-effective solutions; others are likely to decide to be merged with or taken over

by other banks.

Internet e-banking and other fintech products increases the number of new users entering

exponentially, i.e. it creates a cycle of self-empowerment, as customers reduce their costs and increase their

efficiency by doing business online, so they are increasingly convincing their business partners to do the

same. Therefore, it is very likely that there is an asymmetry in the ability of banks to control the entry into

the electronic market. Cyber attacks remains highest threats in the informational economy. Proposing new

and secure online payment systems solutions will still be one of the challenges for banks and regulators in

the 21st century.

REFERENCES:

Adrian Volenik, 10 Biggest Digital Banks in July 16, 2021, https://topmobilebanks.com/blog/biggest-

digital-banks-2021/

Anderson Richard and Associates (2010) “Risk Appetite-reality vs. aspirations ”, Independent Governance

Risk and Assurance, Working Paper no. 2, pp.1-8

Basel committee on banking supervision - BCBS (2018) '' Sound Practices on the implications of fintech

developments for banks and bank supervisors ", Bank for international settlements, pp. 1-49

Chavan, Jayshree (2013) “Internet Banking-Benefits and Challenges in an Emerging Economy”,

International Journal of Research in Business Management (IJRBM), Vol.1, Issue 1, June 2013, 19-

26

Bank for International Settlement (2004) “Survey of developments in electronic money and internet and

mobile payments”, Committee on payment and settlement systems, pp.1-230

Daniela Yu and Jon Hughes (2016), Struggle for Banks: Migrating Customers to Digital, Business Journal

Detsche Bank Research (2011) “Update on online and mobile banking” www.dbresearch.com

Ernst and Young (2010)“Three ways banks are rethinking risk strategies”, Annual Bank Risk Survey Report

European Commission (2020), Digital Economy and Society Index (DESI) 2020 Use of internet services

pp.124

International Trade Center (2017) “International e-payment” pp.23-28

Marous, Jim (2013) “Will the Power of Mobile Make Bank Branches Disappear?”, Paper,

www.limmarous.blogspot.com, pp.1-10

NBRNM (2018) “Decision on the Methodology for security of the bank's information system” published

in the Official Gazette of the Republic of North Macedonia no. 78/18

NBRNM (2020) “Bank performance survey on business activities and risks in 2020”, pp.1-30

NBRNM (2020) “Financial stability risk assessment survey in the Republic of North Macedonia”, pp.1-20

OECD (2018) “Digitalization and Finance”, Financial Markets, Insurance and Pensions, www.oecd.org

pp.1-110

Pablo Hernández de Cos (2019) “The future path of the Basel Committee: some guiding principles”,

Institute for International Finance (IIF) Annual Membership Meeting, Washington DC

Sangani Priyanka (2011) “Internet: The reason behind increase in productivity at companies”, ET Bureau,

http: //articles.economictimes.indiatimes.com, pp.1-8

Sokolov, Dmitri (2007) “E-banking: Risk Management practices of the Estonian Banks”, Published in

Working Papers in Economics, Tallinn University of Technology Discussion Paper, pp.21-37

Transforming Consumer Banking Through Internet Technology (2013)

http://www.dynamicnet.net/news/white_papers/internetbanking.htm

United Nations Conference on Trade and Development (2008) “E-Banking and E-Payments: Implications

for Developing and Transition Economies”, Information Economy Report, Geneva, Chapter 5

United Nations (2018) “Financing for Development: Progress and Prospects 2018”, Report of the Inter-

agency Task Force on Financing for Development, Chapter 3, pp159-174

11

World Development Indicators, 2021 https://databank.worldbank.org/

Wigand, Rolf T. and Robert I. Benjamin “Electronic Commerce: Effects on Electronic Markets”,

www.ascusc.org/jcmc/vol1/issue3/wigand.html

https://www.radiomof.mk/