1

U

SING

BMP

I

NSURANCE TO

I

MPROVE

F

ARM

M

ANAGEMENT

Leah M. Harris and Scott M. Swinton

Michigan State University, December 17, 2012

I. Introduction

In the United States, more than 330 million acres of farmland supply an abundance of

high quality marketable products (EPA, 2012). Although farmers are praised for efficient

production of food, fuel, and fiber, agriculture is criticized for negative environmental impacts.

The 2004 National Water Quality Report cites agriculture as the leading contributor of nonpoint

source (NPS) pollution impairing rivers and streams (EPA, 2004). A 2012 EPA report estimates

that agriculture is responsible for 6.3 percent of total U.S. greenhouse gas emissions (EPA,

2012). Best management practices (BMP) have been developed to reduce environmental

degradation while maintaining productivity. However, for a variety of reasons, some farmers

have not adopted BMPs. Studies suggest that farmers may be hesitant to incorporate BMPs –

even profit enhancing BMPs – because of perceived down-side yield risk (Mitchell, 2004).

Agricultural BMPs are economically sound “voluntary practices that are capable of

minimizing nutrient contamination of surface and ground water” (Randall et al., 2003). Guided

by research and university recommendations, BMPs are developed by agricultural agencies and

presented to farmers as practical, cost-effective actions that can improve environmental quality.

Examples of BMPs include using comprehensive nutrient management plans (CNMP), precision

agriculture, integrated pest management (IPM), improving the timing of input applications,

incorporating cover crops, and installing riparian buffers (Mitchell and Hennessy, 2003). Many

BMPs generate savings by reducing. Agricultural research and technological advancements have

led to the development of Pareto-dominant BMPs that generate environmental benefits without

adversely affecting farm profitability – a CNMP is one example (Baerenklau, 2005).

Adoption of BMPs in the U.S. is a voluntary decision made by individual farmers.

Farmers are often hesitant to adopt suggested practices – even Pareto-dominant BMPs – because

of perceived risk and/or beliefs that BMPs will lower average productivity. Government

programs have traditionally used cost-share or payment programs to encourage adoption.

2

Programs such as the Environmental Quality Incentives Program (EQIP) use cost-shares to

promote BMP usage. While financial incentives may be necessary to achieve adoption of costly

BMPs, payments may not be the appropriate mechanism to promote Pareto-dominant BMPs that

can preserve or improve profitability. Instead of aiming to offset perceived costs of

implementation, incentive mechanisms for these BMPs must address factors such as exaggerated

risk perceptions and uncertainty that directly impact adoption decisions (Feather and Amacher,

1994; Mitchell and Hennessy, 2003).

Farmers decide to adopt BMPs they think will improve farm functionality without

adverse effects on profitability. Perceptions about BMPs are formed from prior experience and

advice from other farmers, input suppliers, and extension personnel (Mitchell, 2004). Regardless

of accuracy, these perceptions influence adoption decisions. Without accurate information, even

profit enhancing BMPs may not be adopted. Overcoming misperceptions about risk and

profitability of BMPs involves altering strongly held beliefs of farmers. BMP insurance, also

called “green insurance” has been identified as one tool to overcome risk perceptions and

promote BMP adoption by allowing farmers to try the management practices risk-free (Mitchell

and Hennessy, 2003). BMP insurance provides an incentive for farmers to adopt BMPs, but

unlike direct payments which must compensate farmers for anticipated losses based on

subjective probabilities, insurance contracts only pay indemnities for actual losses (Baerenklau,

2005). Insuring Pareto-dominant BMPs may be a cost-effective incentive to encourage the

widespread adoption of improved agricultural technologies and practices when farmers perceive

exaggerated down-side yield risk.

This paper provides an overview of how green insurance contracts can be used to

improve environmental outcomes in agricultural landscapes through the adoption of conservation

practices. Section II describes how BMP insurance can be incorporated into farmers’ expected

utility function to motivate the adoption of Pareto-dominant BMPs that farmers’ consider to be

risky. Adoption of an insured BMP provides the farmer with an opportunity to try the improved

practice and adjust their subjective views on the relative profitability and riskiness compared to

conventional practices. Section III describes two contract designs for BMP insurance. The first

contract involves making indemnity payments if BMP yields or profits are lower than the yields

or profits on a check strip managed with conventional practices. The second contract monitors a

3

group of participating BMP adopters and pays individual farmers if their profits fall below the

long-run group average more so than profit deviations of a group of non-participating

conventional farmers. The feasibility of BMP insurance is discussed in Section IV with particular

emphasis placed on concerns of high transactions costs, moral hazard, and adverse selection.

Section IV also considers how BMP insurance could be integrated with current multiple peril

crop insurance purchased by farmers through private providers. The final section summarizes the

findings and provides concluding remarks regarding the cost-effectiveness and feasibility of

using green insurance as an incentive for BMP adoption.

II. Conceptual Framework

BMP insurance offers single peril coverage that protects the farmer against losses caused

by BMP failure. Insurance is suggested as a policy tool to incentivize environmentally sound

farm management based on the assumption that farmers are risk averse and have misperceptions

regarding the effect of BMPs on farm profitability (Feather and Amacher, 1994). For example,

farmers may over-apply nutrients or pesticides to protect against potential yield losses before

facing a real threat. Excessive input applications do not improve yield, but instead the chemicals

contribute to nonpoint source pollution via runoff. In a way, farmers treat the additional inputs as

their own insurance policy against uncertainty. Studies in the Midwest find that chemical inputs

and crop insurance are treated as substitutes for corn and wheat producers (Babcock and

Hennessy, 1996; Smith and Goodwin, 1996). Following a CNMP for input applications and

employing precision agriculture are examples of Pareto-dominant practices that can maintain

high yield while producing less pollution.

Farmers are regularly faced with a variety of risks related to production, finances,

marketing, and liability (Miranowski and Carlson, 1993). Farmers lacking first-hand experience

using a particular BMP face uncertainty about the associated risks, particularly risks related to

yield and profitability (Mitchell, 2004). Farmers develop risk perceptions based on past

experiences, feedback from neighbors, information from extension services or input suppliers,

and exposure to media resources. Based on available information, farmers then form beliefs

about the BMP. Mitchell (2004) describes the decision-making process as a time when farmers

use subjective probabilities based on their knowledge and beliefs to estimate the profitability of

4

the BMP and decide to adopt the practice or stick to the status quo. If a farmer adopts a BMP, the

subjective probabilities should converge with the objective probabilities over time, but the initial

decision is based on perceptions.

Technology adoption decisions involving income risk can be modeled using expected

utility theory and incorporating risk preferences in the farmer’s utility function. If the new

practice offers a higher expected utility compared to current production methods then the farmer

is expected to adopt the technology. Building upon Mitchell’s framework, let

be a risk-

averse farmers’ utility function where

,

, and

is random per acre

profit using production technology q. Although numerous variations and combinations of

production methods are used in agriculture, this stylized framework uses two technology

classifications: the current practice () and the best management practice ().

Expected utility of profits is depicted in equation (1). Per acre market prices and production

functions for N commodities are respectively represented by

and

, where is a

vector of variable inputs, K is a vector of fixed inputs, and E is a random vector of environmental

indicators. Input quantities and prices for M variable inputs are represented by

and

,

respectively.

=

(1)

Let

be the certainty equivalent defined by

=

. The benefit, B, of BMP

adoption can then be calculated as,

. Farmers are expected to adopt BMP

technologies if

(thus,). Farmers would be indifferent between the

technologies when the certainty equivalents are equal.

When subjective probability distributions for yield and profits using BMPs do not align

with objective distributions, BMP adoption rates are suppressed by the misperception of down-

side risk (DeVuyst and Ipe, 1999; Mitchell, 2004). Following Mitchell’s (2004) framework,

,

, and

respectively represent the expected utility, certainty equivalent, and adoption

5

benefit when subjective probability distributions are used. Thus, the subjective evaluation of

expected benefits is expressed as

.

Incentives aim to increase the expected benefits using BMP technologies by increasing

the expected utility of profits. Direct payments, for example, are structured to offset the

perceived cost increase from using BMPs. Cost-shares and other payments may be necessary to

incentivize profit-decreasing BMPs or technologies with associated overhead costs, but these

incentives may not be necessary or appropriate when trying to promote profit-enhancing BMPs.

BMP insurance, also known as “green insurance” aims to shift the subjective probability

distribution so that farmers will try BMPs that they previously considered too risky. Equation 2

defines

– the EU using the BMP with a direct payment, D. Equation 3 defines

the EU using the BMP with BMP insurance, where

is the insurance indemnity

and

is the insurance premium.

=

(2)

=

(3)

Encouraging BMP adoption using a cost-share or payment requires the payment, , to be

at least as great as the expected decrease in revenue and/or increase in costs. Likewise, for BMP

insurance to induce adoption, the expected indemnity would have to offset revenue and cost

changes in addition to offsetting the cost of the insurance premium. Assume that subsidized

insurance covers all profit loss and is offered to the farmer at no cost (

. Equating

and

requires that

, where

is the expected

indemnity based on the farmer’s subjective probability distribution of profitability.

Assume the farmer has the option to participate in one of two different incentive

programs. The first program, BMP-D, offers the farmer a direct payment and, in exchange, the

farmer adopts a BMP. The second program, BMP-I, offers the farmer fully subsidized (i.e. free)

BMP insurance if the farmer adopts the BMP. Farmers participating in BMP-D will require a

6

positive payment () to adopt BMPs that are perceived to be risk increasing or profit

decreasing. Farmers participating in BMP-I know that an indemnity will be paid in the case of a

profit loss from BMP adoption.

BMPs that are falsely perceived to reduce profits can be adopted using both programs. If,

on average, these BMPs do not decrease profits, the average indemnity payment will be zero

which is strictly less than the average direct payment that would have to be offered in the BMP-

D program.

= 0 = average indemnity for Pareto-dominant BMPs (4)

Assuming no transactions costs

1

, using BMP insurance would be a cheaper incentive

relative to direct payments to achieve the same level of BMP adoption. Direct payment amounts

would be based on subjective probabilities, whereas, indemnity payments would be based on

objective probabilities. If farmers exaggerate the risk and losses expected from Pareto-dominant

BMPs, then they will demand higher payments upfront than the average indemnity that would be

paid in an insurance scheme. Hence, green insurance offers a more cost-effective incentive

mechanism to promote adoption of Pareto-dominant BMPs.

III. Designing BMP Insurance Contracts

Based on past research and experience with BMP guarantee programs, two contract

designs have been proposed for BMP insurance. Both designs protect farmers from potential

productivity differences (yield or profit) based solely on BMP adoption and do not cover losses

due to unrelated events such as weather conditions

2

. The more common approach involves

maintaining a check strip using status quo inputs and paying adjustments based on yield or

profitability differences between the check strip and fields managed with BMPs. Maintaining

1

As we move from theoretical framework to real world applications, the assumption of zero transactions costs is no

longer valid. This assumption will be relaxed in Section IV when the feasibility of BMP insurance is evaluated.

2

Multiple peril crop insurance (MPCI) is available to insure farmers for loss that may occur due to factors outside of

BMP adoption. MPCI insurance will be discussed further in Section IV.

7

and evaluating check strips is time consuming for both the farmer and program administrators.

Furthermore, this approach can fail if participants attempt to cheat the system by mismanaging

the check strip to receive higher indemnities – a problem known as moral hazard

3

. The second

approach, known as a group insurance contract, pays indemnities to farmers based on the annual

deviation from long run production averages among a cohort of nearby farmers. This approach

aims to lower transactions costs by using county wide information to inform claims. The

following sections will examine both insurance contracts in greater detail and will discuss

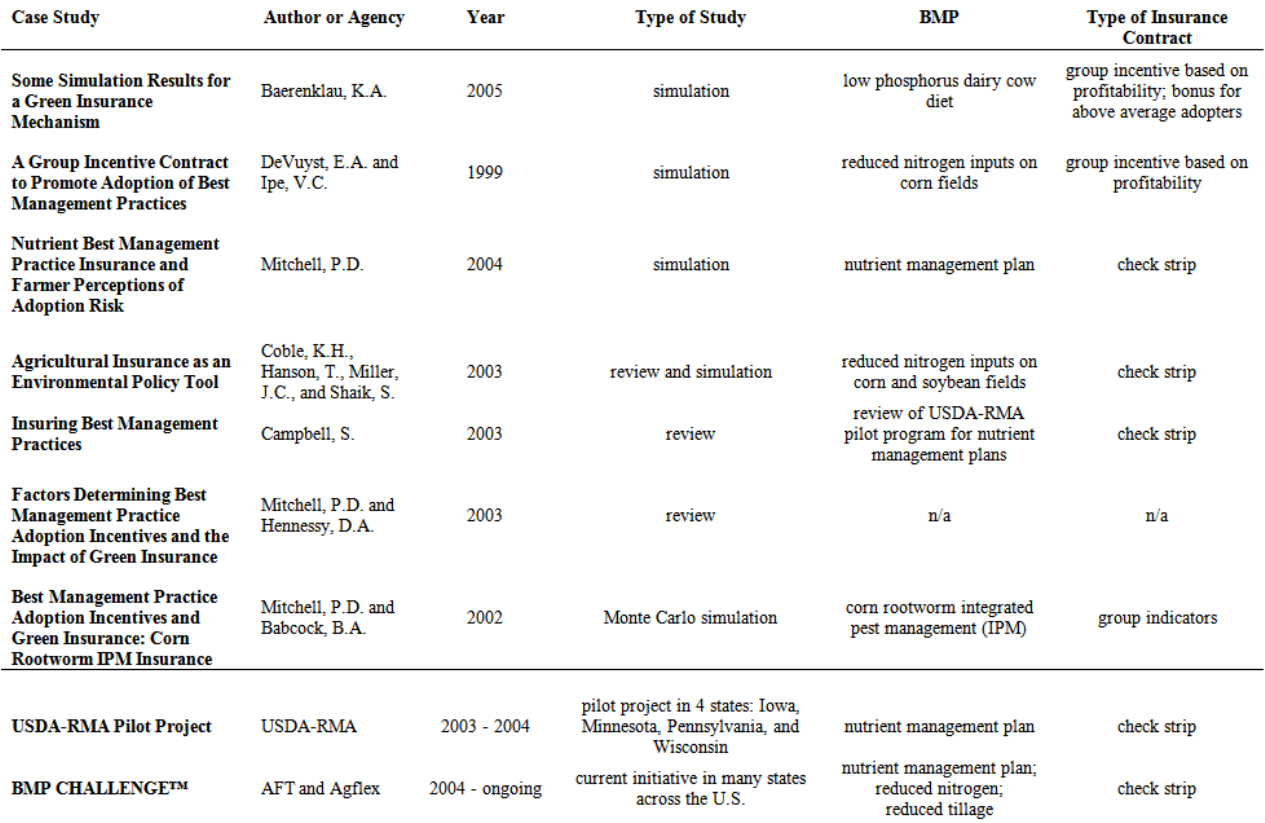

applications of each design. Table A, in the Appendix, presents an overview of BMP insurance

case studies and lists the contract design used in each example.

Contracts employing check strip and field comparisons

The check strip approach was proposed for the U.S. Department of Agriculture’s Risk

Management Agency (USDA-RMA) pilot project in 2003 and is currently employed by the BMP

CHALLENGE™ run by American Farmland Trust (AFT) and Agflex (AFT, 2012; Mitchell,

2004). The RMA insurance product was designed to insure farmers who adopt a comprehensive

nutrient management plan (CNMP). The BMP CHALLENGE™ is available to farmers who

adopt CNMPs or use reduced tillage practices

4

. Although the programs focus on two particular

types of BMPs, the concept can be applied to other technologies.

Farmers participating in this type of program enroll part of their property in the insurance

contract and agree to employ the BMP on enrolled acres. After enrollment, a crop consultant

visits the farm and, in cooperation with the farmer, designs a CNMP for nitrogen and phosphorus

inputs (and can provide advice about tillage practices). During the visit the consultant marks a

comparison strip (approx. 40 by 60 feet) that the farmer would manage using current, status quo

production methods. Both sides of the check strip are bordered by similarly sized strips of land

on which the farmer follows the BMP guidelines prescribed by the consultant. The crop

consultant returns at the time of harvest to inspect the check strip and insured acreage. Insurance

3

Problems with moral hazard and adverse selection are mentioned later in this section and addressed more fully in

section IV.

4

Information about the BMP CHALLENGE™ was acquired through personal communication with Brian Brandt,

Director, Agricultural Conservation Innovations Center, American Farmland Trust.

8

payments are made if productivity of the BMP strips fell below that of the check strip.

Productivity can be measured by comparing yields or profitability. The RMA pilot program

insured against yield differences, whereas the BMP CHALLENGE™ pays the farmer if

profitability of BMP fields is lower. By basing payments on differences in profitability, the

BMP CHALLENGE™ accounts for changes in input costs – for example, although yield from

BMP fields may have been slightly lower than the status quo check strip, the farmer could have

increased profits because of savings from reduced inputs.

Although both programs used the check strip contract design, the contracts differ in

implementation. The RMA pilot insurance was offered in four states (Iowa, Minnesota,

Pennsylvania, and Wisconsin) and participants were charged a premium of $5.65 or $9.39 per

acre, depending on location (Campbell, 2003; Mitchell, 2004). To provide additional incentive,

the program offered a credit of $2 per acre paid toward the insurance premium if the farmer did

not request an adjustment after harvest. After experiencing low enrollment, the pilot program

ended in 2004 and has not been replaced by a similar program.

The BMP CHALLENGE™ is an externally funded program to promote BMP adoption

and is not technically an insurance product. Farmers can enroll limited acreage free of charge and

are reimbursed for profit loss. If BMP adoption increases profit, farmers contribute one-third of

their profit (up to $6 per acre) back into the program. The BMP CHALLENGE™ is intended to

be a short term program to allow farmers to test Pareto-dominant BMPs with hopes that farmers

will update their risk perceptions through experience and continue using the practice in the

future. Since the project was initiated in 2004, more than 7000 acres across the Midwest have

been enrolled in the Nutrient BMP CHALLENGE™ and Reduced Tillage BMP

CHALLENGE™.

Group incentive contracts

Group incentive contracts have been developed to overcome the moral hazard issues

associated with paying farmers for productivity losses based on individual, on-farm yield

measurements. Moral hazard occurs if farmers change their production behavior in a way that

manipulates the insurance contract and results in greater indemnity payments. In BMP insurance,

9

moral hazard arises because it is difficult to distinguish loss due to BMP adoption from loss due

to other management factors. Contracts based on group indicators of productivity that cannot be

manipulated by a single farmer are less likely to encounter moral hazard (Baerenklau, 2005;

DeVuyst and Ipe, 1999). If appropriately designed, these contracts can also incentivize change in

aggregate behavior by motivating farmers to improve production practices relative to neighbors.

Additionally, group contracts lower monitoring costs by eliminating the need to inspect

individual fields.

This type of green insurance mechanism was originally proposed by DeVuyst and Ipe

(1999) and was extended by Baerenklau (2005). The contract pays indemnities to participating

farmers if their profits fall below their long-run group average more so than profit deviations of

nonparticipating farmers. The nonparticipating farmers act like a control group as they are

subject to the same stochastic shocks as the insured participants. Indemnities are paid based on

the following equation:

. (5)

is the indemnity paid per unit in time t, is the average profit per unit with

representing

long-term average profit,

is the farmer i’s input choice in period t, and

is farmer i’s

baseline input choice.

is an indicator function that take the value 1 only if the agent’s input

choice qualifies her to participate in the program. The superscripts P and N represent the

participating farmers and nonparticipating farmers, respectively. The number of participating

farmers is denoted by

. Parameters and K are set by the regulator to provide flexibility in the

incentive mechanism. Setting adds curvature to the scaling term and can be used to reward

farmers who adopt nutrient management plans in which they apply fewer chemicals relative to

other participants. Parameter K places an upper limit on the size of the scaling term.

The “max” term functions as a signal to first determine if an indemnity is due and then

the indemnity is scaled by the “min” term to minimize free riding. The “max” term provides an

indemnity to participants if the average profit in time t of the insured BMP adopters deviates

10

below their average long run profit more than the deviation from the long run average profit

experienced by the nonparticipants in time t. The “min” term then scales the indemnity by

allowing the incentive to vary depending on the extent of adoption relative to other BMP

participants. Scaling rewards farmers who make above average reductions in input applications

and discourages farmers from only adopting the minimum requirement to qualify for the

program. The K term in the minimization operator can be set by regulators to place an upper

limit on the magnitude of the scaling coefficient, thus limiting the size of each indemnity.

This contract is similar to the “area yield” insurance that is currently offered as a multiple

peril crop insurance (MPCI) option by crop insurance providers. These insurance contracts pay

farmers if the yield in a geographic area (e.g. county) falls below a predetermined threshold. “If

no single farm is large enough to significantly affect this average yield, then each agent’s

dominant strategy is to operate his or her farm in good faith; hence there is no moral hazard

dilemma” (Baerenklau, 2005 pp. 96).

Although this type of insurance contract avoids the transactions costs associated with

establishing and monitoring check strips, it introduces other data requirements and costs of

implementation. First of all, the insurance provider would need to have accurate data about the

long-run profitability of both participating farmers and non-participating farmers. Furthermore,

providers would need to know the profit experienced by participating and non-participating

farmers each year in which BMP adopters are insured. Group contracts can provide an effective

incentive for farmers who feel that production on their farm is positively correlated with the

other group members. However, group contracts could deter participation from farmers who are

not comfortable with indemnities relying on group averages that may or may not reflect their

experience with the BMP(s) being insured.

Baerenklau (2005) analyzed the effectiveness of the group BMP insurance contract (eq.

5) on the adoption of reduced-phosphorus diets in Wisconsin. In Wisconsin, farmers were known

to feed dairy cows approximately 4.8 grams of phosphorus per kilogram of dry matter (g/kg DM)

despite research that showed that cows only need 3.3–3.8 g/kg DM to maintain the same level of

milk production. The additional phosphorus supplement increased feeding costs by $13 per cow

annually and contributed to nutrient runoff that threatened local waterways. Although reducing

the level of phosphorus in dairy feed would be Pareto-efficient, farmers were not adopting the

11

new diet recommendation. Simulation results based on a theoretical model of rational decision-

making under uncertainty indicated that the group insurance contract had a significant impact on

adoption behavior. Furthermore, by charging an insurance premium, the insurance product could

be offered at no cost to the program administrator. The study concluded that, when subjective

beliefs limit BMP adoption, environmental benefits could be achieved at a lower cost by using a

green insurance mechanism rather than relying on payment schemes.

IV. Is Agricultural BMP Insurance Feasible?

In general, insurance is purchased by risk averse individuals who are willing to pay a

premium for coverage that offers protection against the possibility of large financial losses. In an

agricultural setting, crop insurance is purchased by farmers who desire protection from crop loss

due to uncertain factors like annual climate. Agricultural BMP insurance would provide similar

protection by insuring farmers against lower yields or profits after adopting specified BMPs. The

question remains, is BMP insurance feasible in today’s agricultural setting? Will farmers demand

this type of insurance and who will supply the policies?

One might assume that rational farmers would adopt a BMP if it was coupled with a

green insurance mechanism because the policy would protect the farmer from perceived negative

welfare effects. One might also assume that insurance providers would be willing to offer

policies for Pareto-efficient BMPs at low rates (or free with government subsidies) because these

BMPs should not lower farm productivity hence indemnities would not need to be paid. In a

theoretical world these predictions may be sensible, but they are naïve without considering the

complexities of implementing BMP insurance in the real world. Insurance providers will require

compensation to issue BMP policies to cover overhead and administrative costs and maintain a

profitable business.

Transactions Costs, Moral Hazard, and Adverse Selection

BMP insurance will only be effective if transactions costs, moral hazard, and adverse

selection problems are minimal. Until now, we have assumed that transactions costs in a BMP

insurance contract are zero, thus allowing farmers to obtain insurance at little or no cost. The

12

reality, however, is that an insurance program carries numerous transactions costs for both the

regulator and the participating farmers. Regulators face costs during contract development in

addition to the costs of monitoring and enforcing the policies. Farmers also incur costs of

participating in the insurance contracts – many of these costs involve the opportunity cost of time

to enroll in the program and to learn how to implement a new BMP as specified in the contact.

The magnitude of costs affects the feasibility of an insurance program. If costs – including

transactions costs – are higher than the benefits offered, farmers will not willingly obtain BMP

insurance. Likewise, companies won’t offer BMP insurance products that are expensive to

implement.

BMP insurance contracts must also be designed to address two classic insurance

problems: moral hazard and adverse selection. Moral hazard and adverse selection are both

problems that occur because of asymmetric information that exists when farmers hold

information that insurance firms lack. The farmer could choose to manage carelessly after

obtaining insurance coverage (moral hazard) or the farmer who knows her farm operation is

riskier than most could be more prone to buy insurance (adverse selection). Obtaining additional

information can mitigate both issues, but acquiring this information is expensive due to the

increased transactions costs of monitoring. Feasible contract designs must be able to effectively

limit asymmetric information while maintaining modest costs of implementation.

Moral hazard is likely the more problematic of the two concerns because insured farmers

may have perverse incentives to make riskier or less practical management decisions than they

would have without insurance. Furthermore, many of these decisions are not observable, thus

they cannot be easily monitored by program administrators. Policies include “several provisions

to mitigate this moral hazard, including documentation requirements, requiring a certified crop

consultant to develop the nutrient BMP, as well as denying claims when evidence of differential

weed or insect management is apparent” (Mitchell, 2004, pp. 671).

Potential behavioral changes of insured farmers can greatly affect the environmental

impact of incentive programs. Risk reduction from insurance has the potential to increase

production of riskier crops that require more inputs. Research has suggested that crop insurance

may promote the expansion of more input intensive and riskier crops such as corn or cotton

(Coble et al., 2003; Seo et al., 2005; Turvey, 1992; Wu, 1999). If farmers obtaining BMP

13

insurance allocate additional acreage to input intensive crops, the environmental benefits of

lowering input levels per acre could be outweighed by the impact of additional acreage of input

hungry crops which require higher fertilizer levels even when a strict CNMP is followed. Future

research should address the question of how BMP insurance may stimulate behavioral changes

and how these changes will impact the environment.

Adverse selection is a problem if insurance contracts allow farmers to select plans that

are more likely to pay indemnities. This concern can be directly addressed through appropriate

program design that limits manipulation of the contracts for personal gain. For example,

contracts using a single state-wide premium may be more prone to adverse selection. Mitchell

(2004) finds that premiums based on state average yields require farmers with lower than

average yields to pay too much and high performing farmers pay too little. Above average

producers have an incentive to buy the insurance because they will likely receive more money

from claims than they will pay for their annual premium.

Integrating BMP insurance with current crop insurance policies

BMP contracts must be carefully stipulated so they can be offered in conjunction with

current crop insurance policies. Since the 1930s, multiple peril crop insurance (MPCI) has been

available to U.S. farmers and has traditionally insured against yield losses until 1996 when the

USDA began offering revenue insurance options (Coble et al., 2003). Since 1980, the US crop

insurance program has functioned as a private-public partnership. Private companies offer

insurance contracts to farmers, evaluate claims, and offer adjustments. The U.S. government,

through the USDA Risk Management Agency (RMA), approves insurance rates and reinsures

the policies issued by private companies. Government involvement helps overcome challenges

that may prevent private firms from entering the market such as adverse selection, moral hazard,

and other transactions costs.

Private insurers are run as profit maximizing firms and as such are concerned about their

own exposure to risk and uncertainty. The lack of homogeneous and uncorrelated losses

increases risk for private insurers, thus increasing rates for farmers. “A private insurance

company seeking to maximize profits will charge a premium rate that exceeds the expected

indemnity for the individual policy,” (Coble et al., 2003, pp. 398). Government is better able to

14

absorb losses from widespread shocks such as drought or flood events. Government involvement

allows farmers to receive insurance at a subsidized rate and allows insurance companies to offer

policies to a broader base of clients. Without federal reinsurance it could be difficult for small

farmers or producers of more risky crops to obtain affordable coverage.

The public-private partnership was designed to balance private sector goals and the needs

of American farmers – this partnership would also be important when supplementing MPCI

policies with BMP insurance coverage. Government reinsurance would be instrumental to

expand the availability of green insurance by protecting private companies against uncertainty

surrounding the new product. Public benefits from environmental improvements would motivate

government involvement, but private insurers would also need to find value in selling BMP

contracts. The 2003 RMA pilot project provides evidence that it may be difficult to generate

interest in selling green insurance. Well-designed and easily implemented contracts are necessary

to receive support from the private insurance sector.

Contract design would be critical when integrating MPCI and BMP insurance contracts to

avoid doubling coverage and limiting exposure to moral hazard or adverse selection, as discussed

earlier. Losses from compounding factors affecting production, such as rainfall and temperature,

are covered by multiple peril insurance and should not be double-counted when evaluating

claims. Designing a contract that clearly delineates between BMP failure and losses due to

factors such as climate would be crucial to avoid payment of undue indemnities.

Linking supply and demand

The existence of agricultural insurance markets depends on the presence of demand and

the ability of suppliers to offer effective BMP insurance policies (Coble et al., 2003). Since crop

insurance policies already exist, one could argue that, under certain circumstances, demand for

BMP insurance could be met by the same companies. It is unclear, however, where the demand

would originate. Furthermore, careful consideration must be given to the conditions under which

insurance providers will be able to offer BMP insurance.

Demand could come from farmers or from other stakeholders with an agenda to promote

BMPs to improve environmental quality. The nature of the demand would influence the type of

15

policies offered by insurance providers. Farmer demand could be spurred by numerous factors,

including regulation, environmental concern, or because BMP adoption provides the farmer with

additional recognition in a certification or verification program. Regulation of agriculture, or the

threat thereof, may spur farmers to seek additional support and protection when changing

agricultural practices (Coble et al., 2003). For example, if the EPA imposed strict rules regarding

nonpoint source pollution originating from agriculture and outlined approved BMPs that farmers

could adopt, farmer demand for BMP insurance could grow significantly. Without regulation

some farmers may seek BMP insurance when trying new production practices to improve

environmental stewardship. Demand driven by regulation may target long term insurance

options, whereas more short term policies to support BMP trials may be adequate in other

circumstances.

Adequate supply of BMP insurance at a national level would likely involve a public-

private partnership as discussed in the previous section. Federal support and participation from

crop insurance companies would lead to the creation of BMP policies that could meet new

demand. Federal involvement would protect private insurance firms from uncertainty and risk

surrounding the new policies while allowing heterogeneous groups of farmers to obtain

coverage. The feasibility of continued BMP insurance provision would depend on the providers’

ability to offer coverage while maintaining low transactions costs and avoiding problems of

asymmetric information. Increasing demand and the development of effective policies could set

the stage for strong growth of the BMP insurance market that promotes enhanced environmental

stewardship.

V. Conclusion

Agricultural BMPs are designed to improve the environment while sustaining

profitability, yet farmers are sometimes hesitant to adopt the practices due to perceived risk of

lower and more variable yields. Instead, many farmers tend to overuse fertilizers and other inputs

to protect against the uncertainty of annual growing conditions. In this sense, the premature or

excessive use of agricultural inputs often serves as self-provided insurance against yield losses.

But the resulting chemical runoff can have detrimental effects on the ecosystem. Furthermore,

research has shown that many BMPs developed through university and federal research result in

16

the same average yield as that obtained by over applying chemicals. These BMPs are considered

Pareto-dominant as they limit nonpoint source pollution while maintaining profitability.

Motivating adoption of Pareto-dominant BMPs requires addressing the risk perceptions of

farmers and creating an incentive for farmers to test BMPs on their own fields.

Agricultural BMP insurance protects farmers from the perceived risk of BMP adoption

by paying indemnities for losses due to BMP failure. BMP insurance can be designed in different

ways to address the common insurance issues of moral hazard and adverse selection. Two

contracts have been suggested for BMP insurance. One involves planting check strips and

comparing yields between BMPs and status quo production methods. The other contract design

pays BMP adopters if their annual yield deviates from long-run production averages more

drastically than the yield of non-adopters in the same year. Each contract aims to differentiate

loss from BMP failure from loss from other correlated risks such as weather.

The transactions costs of measuring and monitoring conventional crop performance and

paying indemnities are important impediments to cost effective provision of BMP insurance.

Contracts that require insurance adjusters to visit individual farms are costly and still cannot

always identify moral hazards that would require the company to make high indemnity

payments. Group contracts aim to lower transactions costs by comparing yield deviations

between groups of participating and non-participating farmers. Although the costs to monitor

farm-level yields are lower, they still represent significant transaction costs. Also, while this

approach lowers the occurrence of moral hazard, it is still subject to adverse selection.

For BMP insurance to be successful, it must be integrated into the current crop insurance

market. However, past programs have found it difficult to generate support for green insurance in

the private sector due to high transactions costs and uncertainty surrounding the new policy

(Campbell, 2003). Furthermore, farmers have been reluctant to purchase the unfamiliar and often

complex policy. Overcoming impediments surrounding the use of BMP insurance requires

generation of both supply and demand. Offering additional incentives (e.g. subsidies) to

insurance providers may expedite the process of incorporating BMP policies in existing crop

insurance contracts. Government regulators can also spur farmer demand by providing incentives

to purchase green insurance. But supporting the BMP insurance market is a costly endeavor. For

17

the investment to be worthwhile, the environmental benefits of providing BMP insurance must

outweigh the costs.

More empirical research is needed to explore the effect of BMP insurance on farmers’

decisions to adoption conservation practices. If BMP insurance can induce farmers to require

disproportionately lower financial incentives to adopt environmentally beneficial BMPs, then it

may be part of a cost-effective solution to improve agro-environmental management. However,

if BMP insurance does not reduce other subsidy costs enough to cover its direct and transaction

costs, then BMP insurance may not be justifiable as a cost-effective public policy.

In conclusion, if designed appropriately, BMP insurance has the potential to be a cost-

effective way to meet public environmental goals while protecting farmers against perceived

risks to their livelihoods. However, recent attempts to offer BMP insurance have failed due to the

high transactions costs imposed on private insurance companies and low demand from farmers.

In light of these costs, future research should explore the justifiable level of subsidy for BMP

insurance. Specifically, there is a need to determine 1) how much BMP insurance influences

farmers’ willingness to adopt BMPs and 2) what is the value of the environmental benefits

associated with BMP adoption.

18

References

AFT. 2012. "AFT's Environmental Solutions." American Farmland Trust, Accessed 06/01/2012.

http://www.farmland.org/programs/environment/solutions/bmp-challenge.asp.

Babcock, B.A., and D.A. Hennessy. 1996. "Input demand under yield and revenue insurance."

American Journal of Agricultural Economics 78(2):416.

Baerenklau, K.A. 2005. "Some Simulation Results for a Green Insurance Mechanism." Journal

of Agricultural and Resource Economics 30(1):94-108.

Brandt, B. Personal Communication. American Farmland Trust.

Campbell, S. 2003. "Insuring Best Management Practices." Journal of Soil and Water

Conservation 58(6):116A-116A,117A.

Coble, K.H., T. Hanson, J.C. Miller, and S. Shaik. 2003. "Agricultural insurance as an

environmental policy tool." Journal of Agricultural and Applied Economics 35(2):391-

405.

DeVuyst, E.A., and V.C. Ipe. 1999. "A Group Incentive Contract to Promote Adoption of Best

Management Practices." Journal of Agricultural and Resource Economics 24(2):367-382.

EPA, 2004. National Water Quality Inventory: Report to Congress, U.S. Environmental

Protection Agency. Office of Water, Washington, DC.

EPA, 2012. Inventory of U.S. Greenhouse Gas Emissions and Sinks: 1990-2010, U.S.

Environmental Protection Agency, Washington, D.C.

Feather, P.M., and G.S. Amacher. 1994. "Role of information in the adoption of best

management practices for water quality improvement." Agricultural Economics 11(2-

3):159-170.

Miranowski, J.A., and G.A. Carlson. 1993. Agricultural Resource Economics: An Overview, ed.

G.A. Carlson,D. Zilberman, and J.A. Miranowski. New York Oxford University Press,

pp. 3-27.

Mitchell, P.D. 2004. "Nutrient Best Management Practice Insurance and Farmer Perceptions of

Adoption Risk." Journal of Agricultural and Applied Economics 36(3):657-673.

Mitchell, P.D., and D.A. Hennessy. 2003. Factors Determining Best Management Practice

Adoption Incentives and the Impact of Green Insurance, ed. B.A. Babcock,R.W. Fraser,

and J.N. Lekakis. Boston, Kluwer Academic Publishers.

Randall, G., G. Rehm, and J. Lamb. 2003. Best Management Practices for Nitrogen Use in

Southeastern Minnesota, ed. U.o.M. Extension. St. Paul. Regents of the University of

Minnesota. Accessed 06/03/2012. http://www.extension.umn.edu/distribution/crop

systems/DC8557.pdf,

19

Seo, S., P.D. Mitchell, and D. Leatham. 2005. "Effects of Federal Risk Management Programs

on Optimal Acreage Allocation and Nitrogen Use in a Texas Cotton-Sorghum System."

Journal of Agricultural and Applied Economics 37:685-699.

Smith, V.H., and B.K. Goodwin. 1996. "Crop insurance, moral hazard, and agricultural chemical

use." American Journal of Agricultural Economics 78(2):428.

Turvey, C.G. 1992. "An Economic Analysis of Alternative Farm Revenue Insurance Policies."

Canadian Journal of Agricultural Economics/Revue canadienne d'agroeconomie

40(3):403-426.

Wu, J. 1999. "Crop Insurance, Acreage Decisions, and Nonpoint-Source Pollution." American

Journal of Agricultural Economics 81(2):305.

20

V1. Appendix

Table A: Summary of BMP insurance papers and programs