UNIVERSITY OF CALIFORNIA

GASB STATEMENT NO. 48

SALES AND PLEDGES OF RECEIVABLES AND FUTURE REVENUES AND

INTRA-ENTITY TRANSFERS OF ASSETS AND FUTURE REVENUES

Table of Contents

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Table of Contents, Page 1 of 2

1. INTRODUCTION 1

2. OVERVIEW OF THE ASSESSMENT PROCESS RELATED TO A TRANSACTION

INVOLVING EXISTING RECEIVABLES 3

How should a transaction involving an exchange of the University’s interest in the

future cash flows associated with a specific receivable be assessed in order to

determine whether the University has continuing involvement? 4

Accounting for transactions that meet the criteria to be reported as sales

(see Exhibit 3). 4

Accounting for transactions that do not qualify as sales (see Exhibit 4). 4

3. OVERVIEW OF THE ASSESSMENT PROCESS RELATED TO A TRANSACTION

INVOLVING THE SALE OF FUTURE REVENUES 6

How should a transaction involving the University’s receipt of proceeds in

exchange for cash flows from specific future revenues be assessed in order to

determine whether the University has continuing involvement? 7

Accounting for transactions that meet the criteria to be reported as sales

(see Exhibit 5).

7

Amortization of deferred revenue and transaction charges. 8

Accounting for transactions that do not qualify as sales (see Exhibit 6).

8

4. RECOGNIZING OTHER ASSETS OR LIABILITIES ARISING FROM A SALE OF

SPECIFIC RECEIVABLES OR SPECIFIC FUTURE REVENUES 9

Residual interests 9

Recourse and other obligations

9

5. PLEDGING OF FUTURE REVENUES WHEN RESOURCES ARE NOT RECEIVED BY

THE

UNIVERSITY 10

6. I

NTRA-ENTITY TRANSFERS OF ASSETS AND FUTURE REVENUES 11

UNIVERSITY OF CALIFORNIA

GASB STATEMENT NO. 48

SALES AND PLEDGES OF RECEIVABLES AND FUTURE REVENUES AND

INTRA-ENTITY TRANSFERS OF ASSETS AND FUTURE REVENUES

Table of Contents

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Table of Contents, Page 2 of 2

7. DISCLOSURES RELATED TO FUTURE REVENUES THAT ARE PLEDGED OR SOLD 12

8. ACCOUNTING AND REPORTING 13

9. IMPLEMENTATION/TRANSITION REQUIREMENT 15

10. NEXT STEPS/REQUIRED ACTIONS 16

11. EXHIBITS

Exhibit 1 Evaluation Questionnaire for Assessing the University’s Continuing

Involvement in the Sale of Existing Receivables

Exhibit 2 Evaluation Questionnaire for Assessing the University’s Continuing

Involvement in Future Revenues

Exhibit 3 Accounting for a Sale of Existing Receivables as a True Sale

Exhibit 4 Accounting for a Sale of Existing Receivables as a Collateralized

Borrowing

Exhibit 5 Accounting for a Sale of Future Revenues as a True Sale

Exhibit 6 Accounting for a Sale of Future Revenues as a Collateralized

Borrowing

Exhibit 7 Summary of Existing Transactions Requiring Review Under the

Provisions of GASB Statement No. 48

Exhibit 8 New Accounting Codes to be Established

Exhibit 9 CFR Footnote Disclosure Report

Exhibit 10 Example of an Assessment of a Transaction to Sell Certain Specific

Receivables

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 1 of 16

1. INTRODUCTION

GASB Statement No. 48, Sales and Pledges of Receivables and Future Revenues and Intra-

Entity Transfers of Assets and Future Revenues, issued in September 2006, addresses the

accounting and financial reporting requirements in transactions where the University exchanges

an interest in its expected cash flows from collecting 1) specific existing receivables or 2)

specific future revenues for immediate cash payments—generally a single lump sum, although

not always in the case of residual interests supported by a subordinate note or other form of

residual certificate. The financial reporting question addressed by this Statement is whether these

transactions should be:

Regarded as a sale, and therefore revenue, or

Regarded as a collateralized borrowing resulting in a liability.

This Statement establishes criteria that the University must use to ascertain whether the proceeds

received should be reported as revenue or as a liability. The criteria must be used to determine

the extent to which the University either retains or relinquishes control over the receivables or

future revenues through its continuing involvement with those receivables or future revenues. A

transaction must be reported as a collateralized borrowing, unless the criteria indicating that a

sale has taken place are met.

In addition, this Statement provides guidance for:

Sales of existing receivables or future revenues within the same financial reporting entity

(for example, between campuses; between a campus and a campus foundation; or

between the University and the UCRS);

Recognizing other assets and liabilities arising from the sale of specific existing

receivables or future revenues, including residual interests and recourse provisions; and

Disclosures pertaining to future revenues that have been pledged or sold.

Under GASB Statement No. 48, the University is required to:

Identify, evaluate and properly report existing and future transactions where future cash

flows associated with specific existing receivables have been exchanged to determine

whether the transaction should be reported as a true sale, or a collateralized borrowing;

Identify, evaluate and properly report existing and future transactions where future cash

flows associated with specific future revenues have been exchanged to determine whether

the transaction should be reported as a true sale, or a collateralized borrowing;

Identify and evaluate existing and future transactions where sales of existing receivables

or future revenues have occurred, or are being considered, among entities within the

University’s financial reporting entity; and

Ensure appropriate disclosure of future revenues that have been pledged or sold,

including information as to which revenues will be unavailable for other purposes and for

how long they will continue to be unavailable.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 2 of 16

GASB Statement No. 48:

Generally prescribes new reporting requirements, rather than amending previous

guidance;

Is effective for FY 2007–2008. Depending on the University’s review of previous

transactions, if the evaluation does not result in any change to previously reported results,

the University may adopt early and apply the provisions of Statement 48 for FY 2006–

2007. Otherwise, restatement of the University’s financial statements for prior periods

will be required. In that case, the University will adopt the provisions for the FY 2007–

2008 and restate FY 2006–2007 results, as outlined in paragraph 23;

Applies to all entities where these transactions have occurred or may occur including:

▫ the separately audited UCRP and PERS-VERIP financial statements;

▫ the separately audited UC Retirement Savings Plans, including the DCP, 403(b), and

457(b);

▫ the separately audited OPEB financial statements (once the OPEB Trust is established

on July 1, 2007);

▫ the campus foundations;

▫ the separately audited Medical Center, UC Press and CEB financial statements; and

▫ the separately audited Health and Welfare Plan financial statements.

This document is prepared in order to outline the University’s approach to the application of

GASB Statement No. 48 to the University’s financial statements assuming the University is in

the position of obtaining proceeds from the sale of existing receivables or future revenues, not

from the position of buying receivables or future revenues from another organization. An

evaluation questionnaire for assessing the University’s continuing involvement in the sale of

existing receivables is provided in Exhibit 1 and an evaluation questionnaire for assessing

continuing involvement in the sale of future revenues is provided in Exhibit 2. If a transaction to

buy receivables or future revenues from another organization is contemplated, please contact

UCOP Financial Management for assistance in determining the appropriate accounting and

reporting.

This document is also prepared on the basis that any sale of existing receivables or future

revenues are with organizations that are not related to the University and are not a part of the

University’s financial reporting entity. If a transaction is contemplated to buy or sell receivables

or future revenues from another organization within the University’s financial reporting entity, or

from another organization that is related to the University, please contact UCOP Financial

Management for assistance in determining the appropriate accounting and reporting.

In general, the transactions discussed in Statement 48 are not normal, ongoing operating

transactions, at least the initial transaction is not routine. The Controller and Controller’s staff

should review non-routine transactions or circumstances at year end to determine that any

situation involving an exchange of the University’s interest in the future cash flows associated

with specific existing receivables or future revenues are identified, evaluated and properly

reported.

GASB Statement No. 48 may be ordered from the GASB’s website at www.gasb.org

. There is

no Implementation Guide at this time from the GASB for this Statement.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 3 of 16

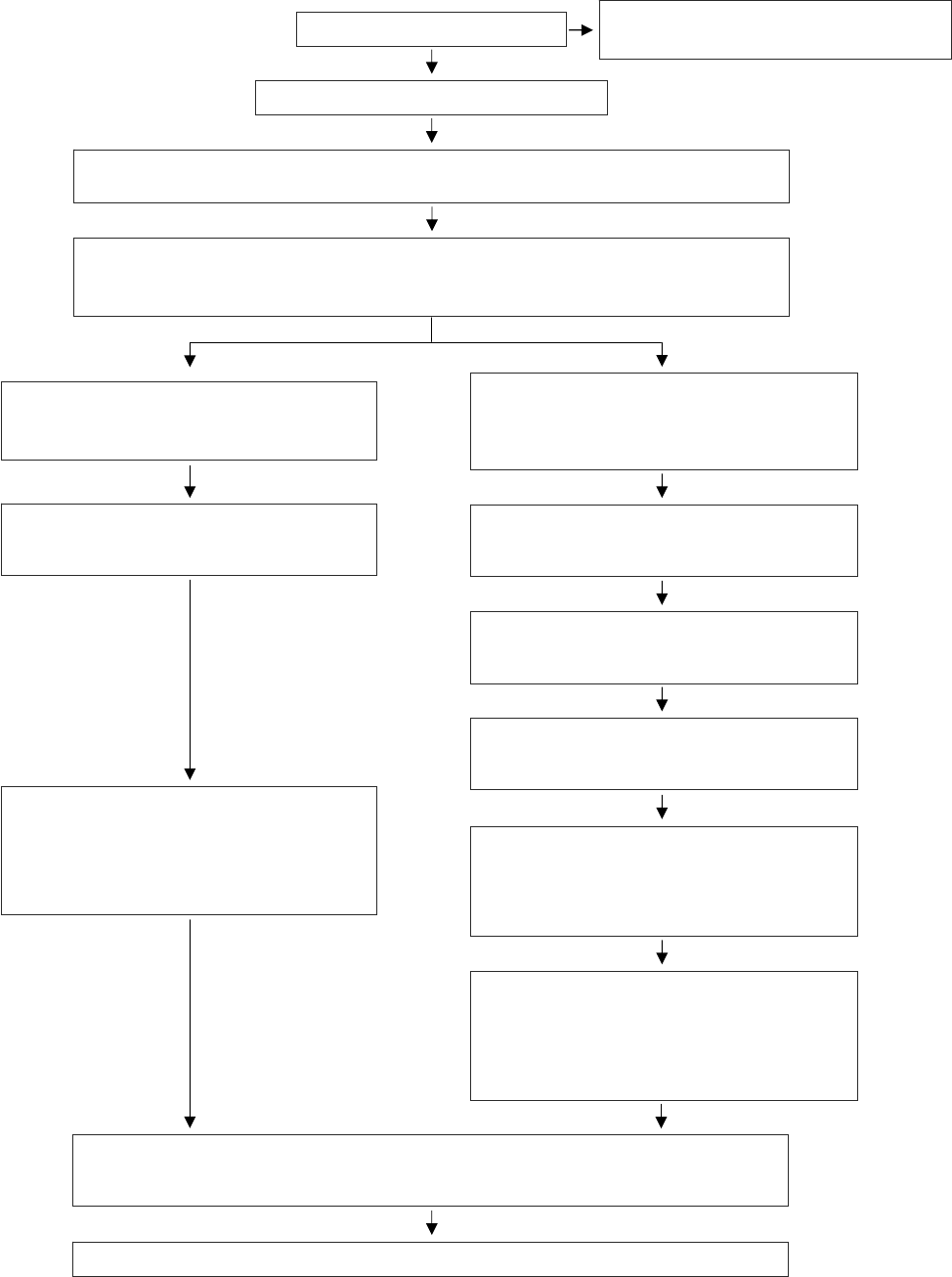

2. OVERVIEW OF THE ASSESSMENT PROCESS RELATED TO A

TRANSACTION INVOLVING EXISTING RECEIVABLES

Yes

No

Future University revenues?

See Section 3.

The University should recognize estimated liabilities arising from the purchase and sale agreement (recourse obligations

or repurchase commitments) if information prior to the issuance of the financial statements indicates an obligation under

FAS 5. ¶18

The transaction should be reported as a collateralized

borrowing and the receivables should be considered to be

pledged, not sold. ¶11

Refer to the Journal Entries in Exhibit 4.

The transaction should be reported as a sale and the

receivables sold no longer recognized as assets. ¶6

Refer to the Journal Entries in Exhibit 3.

Determine whether the proceeds received include as an

asset a residual interest resulting from a subordinate or

junior note, or a residual certificate. ¶17

Determine whether the proceeds received include as an asset

a residual interest resulting from a subordinate or junior note,

or a residual certificate. ¶17

Remove the receivables from the statement of net assets at

their carrying value, recognize the difference between

proceeds received and the carrying value as a gain or loss in

the period of the sale (gain or loss on sale of investments if

MOP loans are sold; otherwise, other operating revenue or

other operating expenses). ¶13

Report the proceeds as an asset and collateral liability in the

statement of net assets and a noncapital financing activity in

the statement of cash flows. ¶11

Retain the receivables in the statement of net assets and

report collections as a cash receipt and a reduction of the

receivable. ¶11, 12

Collections of pledged receivables that are subsequently paid

to the transferee are reported as a reduction of the

collateralized borrowing obligation in the statement of net

assets and a noncapital financing activity in the statement of

cash flows. ¶12

Collections of pledged receivables that are subsequently paid

to the transferee after the collateralized borrowing obligation

has been liquidated are reported as an operating expense in

the statement of revenues, expenses and changes in net

assets and an other operating payment in the statement of

cash flows. ¶12

The University must make the appropriate footnote disclosures as outlined in ¶21.

Does the transaction relate to:

The University’s existing receivables?

If receivables are bought and sold between the University and one of its blended or discretely presented component

units (campus foundations), contact UCOP Financial Management to assess the financial reporting ramifications.

Does the assessment of the transaction result in a determination that the University’s continuing involvement with these

receivables is effectively terminated? ¶6–9

Refer to the assessment questionnaire in Exhibit 1.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 4 of 16

How should a transaction involving an exchange of the University’s interest in the future cash

flows associated with a specific existing receivable be assessed in order to determine whether

the University has continuing involvement?

An exchange of the University’s interest in the future cash flows associated with a specific

existing receivable should be recognized for financial reporting purposes as a collateralized

borrowing rather than a sale unless the appropriate criteria are met.

The most significant factor distinguishing sales from borrowings is the continuing involvement

of the University. Certain criteria must be met that demonstrate that the University is no longer

actively involved with the specific existing receivables it has transferred to another party. A

sample of the criteria, although not an exhaustive list, includes:

Neither the University nor the buyer can cancel the sale;

The University cannot limit in any significant way the buyer’s ability to

subsequently sell or pledge the receivables;

The University no longer has access to the receivables, or the cash collected from

them in any substantive manner; and/or

The University cannot unilaterally substitute for or reacquire specific receivables

without the buyer’s consent.

A complete questionnaire to be used for assessing the University’s continuing involvement in

each transaction is shown in Exhibit 1. Completion of the questionnaire, including pertinent

references to the underlying purchase and sale contract, will serve to document the University’s

conclusion as to whether the transaction should be recorded as a true sale of receivables, or a

collateralized borrowing.

Accounting for transactions that meet the criteria to be reported as sales (see Exhibit 3).

If the criteria for sale reporting are met, the University should no longer recognize as assets the

receivables sold, removing the individual accounts at their carrying values. The difference

between the proceeds (exclusive of amounts that may be refundable) and the carrying value of

the receivables sold should be recognized as a gain or loss in the period sold.

If Mortgage Origination Program (MOP) loans are sold, the resulting gain or loss is recorded as a

gain or loss on investments since the MOP loans are included in the University’s investment

portfolio (GASB 9, ¶27). If existing receivables that are not classified as investments are sold,

the resulting gain is recorded as other operating revenue and a loss is recorded as other operating

expense (GASB 9, ¶17).

Accounting for transactions that do not qualify as sales (see Exhibit 4).

If the criteria for sale reporting are not met, the transaction should be reported as a collateralized

borrowing. The receivables should be considered for financial statements purposes as being

pledged rather than sold. Proceeds received by the University should be reported as a liability,

collateralized borrowing obligation, separated between the current and noncurrent portions, in

the statement of net assets and as other noncapital financing activity in the statement of cash

flows (GASB 9, ¶21a).

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 5 of 16

The pledged receivables should continue to be recognized as assets in the University’s statement

of net assets. Collections of these receivables that are subsequently paid to the transferee are

reported as an other noncapital financing use of cash in the statement of cash flows and reduce

the collateralized borrowing obligation in the University’s statement of net assets. Any pledged

receivables collected and paid to the transferee after the collateralized borrowing obligation has

been liquidated should be reported as an operating expense in the statement of revenues,

expenses and changes in net assets.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 6 of 16

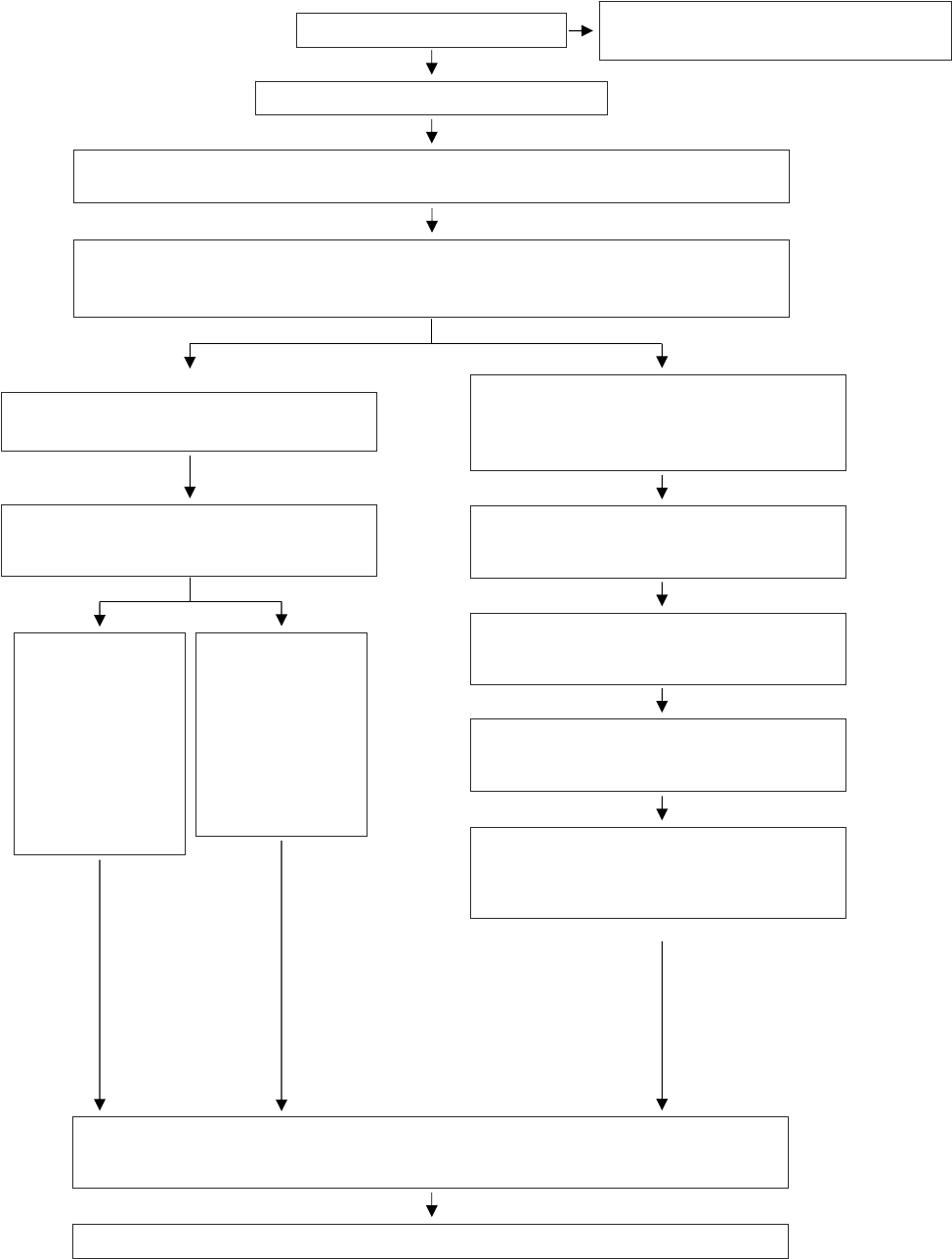

3. OVERVIEW OF THE ASSESSMENT PROCESS RELATED TO A

TRANSACTION INVOLVING THE SALE OF FUTURE REVENUES

Does the transaction relate to:

Future University revenues?

Yes

No

If future revenues are bought and sold between the University and one of its blended or discretely presented component

units (campus foundations), contact UCOP Financial Management to assess the financial reporting ramifications. ¶15

Does the assessment of the transaction result in a determination that the University’s continuing involvement with the

specific revenues is effectively terminated? ¶8–11

Refer to the assessment questionnaire in Exhibit 2.

The transaction should be reported as a collateralized

borrowing and the future revenue should be considered to

be pledged, not sold. ¶11

Refer to the Journal Entries in Exhibit 6.

The University should recognize estimated liabilities arising from the purchase and sale agreement (recourse obligations

or repurchase commitments) if information prior to the issuance of the financial statements indicates an obligation under

FAS 5. ¶18

Determine whether the proceeds received include as an

asset a residual interest resulting from a subordinate or

junior note, or a residual certificate. ¶17

Report the proceeds as an asset and collateral liability in the

statement of net assets and a noncapital financing activity in

the statement of cash flows. ¶11

Record pledged revenues as revenue in accordance with

recognition and measurement criteria appropriate to the

specific type of revenue pledged. ¶12

Collections of pledged revenues that are subsequently paid

to the transferee are reported as a reduction of the collateral

liability in the statement of net assets and a noncapital

financing activity in the statement of cash flows. ¶12

The University must make the appropriate footnote disclosures as outlined in ¶21.

The transaction should be reported as a sale. ¶14

Refer to the Journal Entries in Exhibit 5.

Determine whether the proceeds received include as an

asset a residual interest resulting from a subordinate or

junior note, or a residual certificate. ¶17

Defer revenue and

recognize the revenue

over the duration of the

sale agreement if the

future revenue sold was

not recognized

previously because the

event that would have

resulted in revenue

recognition had not yet

occurred.

1

¶14

Recognize the entire

revenue at the time of

the sale only if the

revenue sold was not

recognized previously

because of uncertainty

of realization or the

inability to reliably

measure the revenue

¶14

Defer revenue

recognition

Recognize revenue

immediately

(1) Consummation of the future revenue sale transaction is not a substitute for a revenue recognition event. They are two different determinations.

Existing University receivables?

See Section 2.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 7 of 16

How should a transaction involving the University’s receipt of proceeds in exchange for cash

flows from specific future revenues be assessed in order to determine whether the University

has continuing involvement?

The University’s receipt of proceeds in exchange for cash flows from specific future revenues

should be recognized for financial reporting purposes as a collateralized borrowing rather than a

sale, and the future revenue should be considered to be pledged, unless the appropriate criteria

are met.

The most significant factor distinguishing sales from borrowings is the continuing involvement

of the University. Certain criteria must be met that demonstrate that the University is no longer

actively involved with the future revenues it has transferred to another party. A sample of the

criteria, although not an exhaustive list, includes:

Neither the University nor the buyer can cancel the sale;

The University cannot limit in any significant way the buyer’s ability to

subsequently sell or pledge the future revenues;

The University no longer has access to the future revenues, or the cash collected

from them in any substantive manner;

The University is no longer actively involved in the future generation of the

revenues. The revenues cannot be a product of goods or services provided by the

University, or a fee or charge that the University must impose. If the revenues are

derived from grants or contributions, they cannot depend on the University

subsequently submitting applications or meeting performance provisions to

maintain eligibility to receive the revenues.

A complete questionnaire to be used for assessing the University’s continuing involvement in

each transaction is shown in Exhibit 2. Completion of the questionnaire, including pertinent

references to the underlying purchase and sale contract, will serve to document the University’s

conclusion as to whether the transaction should be recorded as a true sale of future revenues, or a

collateralized borrowing.

Accounting for transactions that meet the criteria to be reported as sales (see Exhibit 5).

If the criteria for sale reporting are met, the University should report the proceeds as either

deferred revenue or revenue. Generally, revenue should be deferred and recognized over the

duration of the sale agreement; however, there may be instances where recognition in the period

of sale is appropriate. For transactions outside the financial reporting entity, deferral is required

if the future revenue sold was not recognized previously because the event that would have

resulted in revenue recognition had not yet occurred. Consummation of the future revenue sale is

not a substitute for a revenue recognition event and, consequently, revenue from the sale should

be deferred. Revenue should be recognized at the time of the sale only if the revenue sold was

not recognized previously because of uncertainty of realization or the inability to reliably

measure the revenue.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 8 of 16

Amortization of deferred revenue and transaction charges.

Deferred revenues and transaction charges arising from the sale of future revenues should be

amortized over the life of the sale agreement using a systematic and rational method.

Accounting for transactions that do not qualify as sales (see Exhibit 6).

If the criteria for sale reporting are not met, the transaction should be reported as a collateralized

borrowing. The future revenues should be considered for financial statements purposes as being

pledged rather than sold. Proceeds received by the University should be reported as a

collateralized borrowing obligation, separated between the current and noncurrent portions, in

the statement of net assets and as other noncapital financing activity in the statement of cash

flows.

The pledged revenues should continue to be recorded as revenue by the University in accordance

with recognition and measurement criteria appropriate to the specific type of revenue pledged.

Collections of the pledged revenues that are subsequently paid to the transferee are reported as

an other noncapital financing use of cash in the statement of cash flows and reduce the

collateralized borrowing obligation in the University’s statement of net assets.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 9 of 16

4. RECOGNIZING OTHER ASSETS OR LIABILITIES ARISING FROM A SALE

OF

SPECIFIC RECEIVABLES OR SPECIFIC FUTURE REVENUES

Residual interests

If the University acquires a subordinate or junior note, or a residual certificate, representing the

right to collections that exceed a stipulated level, the University must recognize the note or

certificate as an asset representing a residual interest in:

Excess receivable collections, giving consideration to the likelihood of collection.

Residual interests recognized in the period in which the sale occurred should be

treated as an adjustment to the gain or loss. Residual interests recognized in

subsequent periods, for example, as a result of subsequent realization and

collection, should be reported as revenues once the appropriate revenue recognition

requirements have been met.

Excess future revenues, when the asset recognition criteria appropriate to the

specific type of revenue that underlies the note or certificate have been met.

Revenue recognition of the residual interest would also occur at that time.

The timing of the recognition of residual interests is difficult to generalize and should be

discussed on a transaction by transaction basis, if the situation arises.

Recourse and other obligations

The University should recognize estimated liabilities arising from the purchase and sale

agreement – for example, recourse obligations or repurchase commitments – when information

available prior to the issuance of the financial statements indicates that it is probable that a

liability has been incurred at the date of the financial statements and the amount of the liability

can be estimated. Further guidance on the recognition of these types of potential liabilities can be

found in Financial Accounting Standards Board Statement No. 5.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 10 of 16

5. PLEDGING OF FUTURE REVENUES WHEN RESOURCES ARE NOT

RECEIVED BY THE UNIVERSITY

These transactions would appear to be highly unusual for the University and do not warrant

extensive discussion in this document. These situations should be discussed with UCOP

Financial Management if they arise.

While not the case in the University at present, if the University pledges future cash flows of

specific revenues but do not receive resources in exchange for that pledge, it requires certain

disclosures and ultimately the reporting of payments made under the pledge. For example, the

University could pledge its revenues in support of debt issued by a component unit.

If this situation arises, at the time the pledge is made, the University should not recognize a

liability, and the component unit should not recognize a receivable for the futures revenues

pledged in support of its debt. The University would continue to recognize revenue from the

pledged amounts and would recognize a liability to the debt-issuing component unit and an

expense simultaneously with the recognition of the revenues that are pledged. The debt-issuing

component unit should recognize revenue when the University is obligated to make the

payments.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 11 of 16

6. INTRA-ENTITY TRANSFERS OF ASSETS AND FUTURE REVENUES

These transactions would also appear to be highly unusual for the University and do not warrant

extensive discussion in this document. They should be discussed with UCOP Financial

Management if they arise.

If a transaction is being considered that involves the transfer of capital and financial assets and/or

future revenues within the same financial reporting entity – for example, between a campus and

its foundation or a foundation and its campus – the financial reporting treatment is not the same

as if the same transaction occurred with an external entity.

In these situations, the transferee should recognize the assets or future revenues received at the

carrying value of the transferor. For example, if a campus foundation sold receivables to a

campus, the campus should recognize the receivables acquired at the carrying value of the

campus foundation. If there is a difference between the amount paid by the campus (exclusive of

amounts that may be refundable) and the carrying value of the receivables transferred, that

difference should be reported as a gain or loss by the campus foundation in their separately

audited financial statements and as an operating revenue or expense in the campus statements,

however these amounts must be reclassified in the consolidated University statements as a

nonoperating subsidy.

In an intra-entity transfer sale of future revenues, the transferor has reported no carrying value

for the rights sold because the asset recognition criteria have not been met. Therefore the

transferee should not recognize an asset and related revenue until recognition criteria appropriate

to that type of revenue are met. Instead, the transferee should report the amount paid as a

deferred charge to be amortized over the duration of the transfer agreement. The transferor

should defer the recognition of revenue from the sale and recognize it over the duration of the

sale agreement.

Any deferred revenues and charges associated with these types of transactions must be properly

disclosed in the University’s consolidated financial statements.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 12 of 16

7. DISCLOSURES RELATED TO FUTURE REVENUES THAT ARE PLEDGED

OR

SOLD

Pledged revenues are those specific revenues that have been formally committed to directly

collateralize or secure debt of the University, or directly or indirectly collateralize

2

or secure debt

of a component unit.

For each year in which the secured debt remains outstanding at the end of the year, the

University should disclose in the notes to the financial statements information about specific

revenues pledged, including:

Identification of the specific revenue pledged and the approximate amount of the pledge.

Generally, the approximate amount of the pledge would be equal to the remaining

principal and interest payments of the secured debt.

Identification of, and general purpose for, the debt secured by the pledged revenue.

The term of the commitment—that is, the period during which the revenue will not be

available for other purposes.

The relationship of the pledged amount to the total for that specific revenue, if

estimable—that is, the proportion of the specific revenue stream that has been pledged.

A comparison of the pledged revenues recognized during the period to the principal and

interest requirements for the debt directly or indirectly collateralized by those revenues.

In the year of the sale, if the University sells future revenue streams, it must disclose in the notes

to the financial statements information about the specific revenues sold, including:

Identification of the specific revenue sold, including the approximate amount and the

significant assumptions used in determining the approximate amount.

The period to which the sale applies.

The relationship of the sold amount to the total for that specific revenue, if estimable.

A comparison of the proceeds of the sale and the present value of the future revenues

sold, including the significant assumptions used in determining the present value.

2

In an indirect collateralization, the pledged revenue agreement is not directly between the University and the

bondholders. The University’s resources do not secure the debt; rather, the debt is secured by the University’s payment

to the component unit that is financed by that revenue. In this case, the University would make an annual grant to the

component unit, which, in turn, pledges that revenue as security for its debt.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 13 of 16

8. ACCOUNTING AND REPORTING

New accounting codes need to be established in the Corporate Financial System to enable

mapping to our financial statements. At this time, codes in the Current Funds group and the Loan

Funds group are being established. If a review of transactions indicates that codes are needed in

another fund group, contact UCOP Financial Management. The new codes will roll up into the

financial statements as follows:

S

TATEMENT OF NET ASSETS

CURRENT LOAN

Roll up into Current Portion of Notes and Mortgages Receivable:

CA-Note receivable – sale of receivable – sale AGC160614 AGC140614

CA-Note receivable – sale of receivable – collateralized borrowing AGC160615 AGC140615

CA-Note receivable – sale of future revenues – sale AGC160616 AGC140616

CA-Note receivable – sale of future revenues – collateralized borrowing AGC160617 AGC140617

CA-Note receivable – sale of receivable – investment AGC160618 N/A

Roll up into Notes Receivable:

NA-Note receivable – sale of receivable – sale AGC161330 AGC141330

NA-Note receivable – sale of receivable – collateralized borrowing AGC161340 AGC141340

NA-Note receivable – sale of future revenues – sale AGC161350 AGC141350

NA-Note receivable – sale of future revenues – collateralized borrowing AGC161360 AGC141360

NA-Note receivable – sale of receivable – investment AGC161370 N/A

Roll up into Deferred Revenue:

CL-Deferred revenue – sale of future revenues AGC164350 AGC144350

CL-Deferred revenue – sale of future revenues – earned AGC164360 AGC144360

Roll up into Other Current Liabilities:

CL-Collateralized borrowing obligations – sale of receivables AGC164761 AGC144761

CL-Collateralized borrowing obligations – sale of receivables – payt. AGC164762 AGC144762

CL-Collateralized borrowing obligations – sale of future revenue AGC164763 AGC144763

CL-Collateralized borrowing obligations – sale of future revenue – payt. AGC164764 AGC144764

Roll up into Other Noncurrent Liabilities:

NL-Collateralized borrowing obligations – sale of receivables AGC165571 AGC145571

NL-Collateralized borrowing obligations – sale of future revenue AGC165573 AGC145573

NL-Deferred revenue-sale of future revenues AGC165580 AGC145580

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 14 of 16

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETS

CURRENT LOAN

Roll up into Other Operating Revenue:

Gain on sale of receivables AGC208300 TC8026

Roll up into Other Operating Expense:

Loss on sale of receivables OC7630 TC8123

Payment of pledged receivables

3

OC7640 TC8124

3

Object code to be used to reflect any collections of pledged receivables subsequently paid to the transferee after the

collateralized borrowing obligation has been liquidated.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 15 of 16

9. IMPLEMENTATION/TRANSITION REQUIREMENT

For the initial year of implementation, in order to determine the effect of the restatement, if any,

of the prior period financial statements, UCOP and the campuses will need to determine whether

they have previously sold any receivables or future revenues and, if so, whether they are true

sales or a collateralized borrowing.

This information must be reported to Amal Smith ([email protected]

or 510/ 987.0940) in

UCOP Financial Management by April 1, 2007 using the format shown in Exhibits 1 and 2.

02/27/07 DRAFT Preliminary Conclusions—Subject to Continuing Discussions with PwC Page 16 of 16

10. NEXT STEPS — REQUIRED ACTIONS

Responsibility

(C, OP)

Required

Completion

Date

Action Item/Task

C, OP March 2007

Evaluate existing transactions – Determine whether any previous

sale of existing receivables or future revenues is a collateralized

borrowing (Exhibits 1 and 2).

OP March 2007

Assign new accounting codes—Assign new accounting codes to

record the sale of receivables or future revenues (Exhibit 8).

C 1-Apr-07

Submit evaluation of existing transactions—Submit to UCOP the

evaluation performed in March 200 to determine whether any

previous sale of existing receivables or future revenues is a

collateralized borrowing (Exhibits 1 and 2).

OP April 2007

Decide whether to implement early – Based upon the evaluation

of existing transactions, determine whether the University will

implement Statement No. 48 for FYE June 30, 2007.

OP April 2007

Add accounting codes to CFR driver tables—Add new sale of

receivable or future revenue accounting codes to CFR driver tables.

OP April 2007 Develop footnote reports—Develop CFR footnote reports to

accumulate sale of receivable or future revenue information (see

Exhibit 9).

C May 2007 Establish new accounting codes in campus ledger—Establish

new sale of receivable or future revenue accounting codes in

campus ledger.

C May 2007 Restate FYE June 30, 2006, as necessary, if implemented early.

C, OP June 2007 Fiscal Closing Calendar—Add a step to the fiscal closing calendar

to review any sales of existing receivables or future revenues for

proper financial reporting treatment.

02/27/07 Exhibit 1, Page 1 of 3

EXHIBIT 1: EVALUATION QUESTIONNAIRE FOR ASSESSING THE

UNIVERSITY’S CONTINUING INVOLVEMENT IN THE SALE OF

EXISTING RECEIVABLES

A significant aspect of the assessment is the degree to which the University retains or relinquishes to the

transferee control over the existing receivables. A transaction in which the University receives or is

entitled to proceeds in exchange for the future cash flows from existing receivables should be reported as

a sale if the University’s continuing involvement with these receivables is effectively terminated

(¶6).

The determination of whether the University’s continuing involvement is effectively terminated is

dependent upon an evaluation of the following criteria. A “yes” answer to any one of the questions

indicates the University’s continuing involvement is not

effectively terminated and, therefore, the

transaction should not

be reported as a sale.

Transaction Assessed:

Conclusion:

Yes/No

Source Document/

Specific Reference

Questions 1–3 outline the criteria to determine whether the

substance of the transaction is indicative of whether the sale has

been substantively consummated.

1. Is the transferee’s ability to subsequently sell or pledge the

receivables significantly limited by the constraints imposed

by the University, either in the transfer agreement or through

other means?

(¶6a)

2. Does the University have the option or ability to unilaterally

substitute for or reacquire specific accounts from among the

receivables transferred? Note: The ability or obligation to

substitute for defective accounts, at the option of the

transferee, would not violate this criterion. For example,

accounts that do not possess the characteristics stipulated in

a transfer agreement may be replaced by ones that do

possess those traits. In addition, insignificant “clean-up”

calls by which the University may reacquire remaining

uncollected accounts when the outstanding secured debt

reaches a specified minimum balance would likewise not

violate this criterion.

(¶6b)

3. Is the sale agreement cancellable by either party, including

cancellation through payment of a lump sum or transfer of

other assets or rights?

(¶6c)

Questions 4–6 outline the criteria to determine whether the

transferee has a separate legal standing from the University.

4. Is the separate organization’s legal entity the same as the

University’s legal entity?

(¶7a)

5. Do the corporate powers of the transferee organization fail to

distinguish it as being legally separate from the University?

(¶7a)

02/27/07 Exhibit 1, Page 2 of 3

Yes/No

Source Document/

Specific Reference

6. Do the corporate powers of the transferee organization

preclude it from being sued in its own name without

recourse to the University, or preclude it from the right to

buy or sell, lease or mortgage property without the

University’s approval?

(¶7a)

Question 7 outlines the criteria to determine whether the

receivables are isolated from the University should it become the

subject of a bankruptcy proceeding.

7. Do provisions in the transfer agreement (or provided

elsewhere in statutes, charters or other governing documents

or agreements) fail to protect the transferee from the claims

of the University’s creditors?

(¶7c)

If “yes” to any one

of Questions 1–7, the University has

continuing involvement and the transaction must be recorded as

a collateralized borrowing, not a true sale of the receivables.

If “no” to all

of Questions 1–7, continue to assess whether the

receivables are isolated from the University.

Generally, banking arrangements should eliminate access by the

University or its component units to the cash generated by

collecting the receivables. Access is eliminated when payments

on individual accounts are made directly to a custodial account

maintained for the benefit of the transferee.

8. Are payments on individual accounts made through the

University (and, presumably, then remitted to the transferee),

as opposed to payments on individual accounts made

directly to a custodial account maintained for the benefit of

the transferee?

(¶7b)

If the answer to all

of Questions 1–7 and Question 8 is “no,” then

the transaction must be reported as a true sale of receivables and

not a collateralized borrowing.

If the answer to Question 8 is “yes” it tentatively leads to a

presumption of a collateralized borrowing that may be mitigated

by “no” answers to the following questions. It may be that the

University continues to service the accounts, or obligors may

misdirect their payments to the University rather than the

transferee. In this circumstance, access to the cash generated by

collecting the receivables is deemed to be eliminated if all

of the

answers to the following questions are “no.”

9. Does the University have an obligation to advance amounts to

the transferee before it collects equivalent amounts from the

underlying individual accounts? Note: The payments to the

transferee should be made only from the resources generated by

the specific receivables rather than from the University’s own

resources.

(¶7b(1))

02/27/07 Exhibit 1, Page 3 of 3

Yes/No

Source Document/

Specific Reference

10. Is the cash collected by the University on behalf of the

transferee remitted to the transferee after significant delay?

(¶7b(2))

11. Are earnings on invested collections held by the University

instead of passed on to the transferee?

(¶7b(2))

12. Do the University’s general ledger and accounts receivable sub-

ledger fail to consider sale proceeds from the transferee as

satisfaction of individual accounts?

(¶7b(3))

13. Does the University fail to indicate in its records which

accounts have been transferred and which collections pertain to

those accounts?

(¶7b(3))

If the answers to Questions 1–7 and 9–13 are “no,”

notwithstanding the fact that the answer to Question 8 is “yes,”

then the transaction must be recorded as a true sale, not as a

collateralized borrowing.

Prepared by: Date:

Reviewed by: Date:

02/27/07 Exhibit 2, Page 1 of 3

EXHIBIT 2: EVALUATION QUESTIONNAIRE FOR ASSESSING THE

UNIVERSITY’S CONTINUING INVOLVEMENT IN FUTURE REVENUES

A significant aspect of the assessment is the degree to which the University retains or relinquishes to the

transferee control over the future revenues. A transaction in which the University currently receives or is

entitled to proceeds in exchange for future cash flows from future

revenues should be reported as a sale if

the University’s continuing involvement with these future revenues is effectively terminated

(¶8). Note,

however, that recognition of the revenue may need to be deferred.

The determination of whether the University’s continuing involvement is effectively terminated is

dependent on an evaluation of the following criteria. A “yes” answer to any one of the questions indicates

the University’s involvement is not

terminated and, therefore, the transaction should not be reported as a

sale.

Transaction Assessed:

Conclusion:

Yes/No

Source Document/

Specific Reference

Questions 1–4 outline the criteria to determine whether the

University maintains active involvement in the future generation of

revenues exchanged for current proceeds. Active involvement

generally requires a substantive action or performance by the

University. The University must determine whether the primary,

fundamental activity or process that generates a specific revenue

requires a continuing active involvement

(¶9).

1. Does the University produce or provide the goods or services

that are exchanged for the revenues.

(¶9a)

2. Does the University levy or assess taxes, fees, or charges and

can the University directly influence the revenue base or the

rate(s) applied to that base to generate the revenues?

(¶9b)

3. Is the University required to submit applications for grants or

contributions from other governments, organizations or

individuals to obtain the revenues?

(¶9c)

Note: This application criterion refers to ongoing

requirements that qualify the University to continue to

receive grants or contributions in future years, rather than an

initial application or qualification process that remains

effective without further effort by the University.

4. Is the University required to meet grant or contribution

performance provisions to qualify for those revenues?

(¶9d)

Questions 5–7 outline the criteria to determine whether the

substance of the transaction is indicative of whether the sale has

been substantively consummated

.

02/27/07 Exhibit 2, Page 2 of 3

Yes/No

Source Document/

Specific Reference

5. Is the transferee’s ability (or the ability of the ultimate

holder/owner of the future cash flows) to subsequently sell

or pledge the future cash flows significantly limited by

constraints imposed by the University, either in the transfer

agreement or through other means?

(¶8b)

6. Does the contract, agreement, or other arrangement between

the original resource provider (a grantor organization, for

example) and the University prohibit the transfer or

assignment of those resources?

(¶8d)

7. Is the sale agreement cancellable by either party, including

cancellation through payment of a lump sum or transfer of

other assets or rights?

(¶8e)

If “yes” to any one of Questions 1–7, the University has

continuing active involvement and the transaction must be

recorded as a collateralized borrowing, not a true sale of the

future revenues.

If “no” to all of Questions 1–7, continue to assess whether the

future revenues are isolated from the University.

Generally, banking arrangements should eliminate access by the

University or its component units to the cash generated by

collecting the future revenues. Access is eliminated when cash

collection of future revenues are made directly to a custodial

account maintained for the benefit of the transferee.

8. Are cash collections of future revenues made through the

University (and, presumably, then remitted to the transferee),

as opposed to cash collections of future revenues made

directly to a custodial account maintained for the benefit of

the transferee?

(¶8c)

If the answer to all

of Questions 1–7 and Question 8 is “no,” then

the transaction must be reported as a true sale of future revenues

and not a collateralized borrowing.

If the answer to Question 8 is “yes” it tentatively leads to a

presumption of a collateralized borrowing that may be mitigated by

“no” answers to the following questions. It may be that the

University continues to collect the future revenues, or obligors may

misdirect their payments to the University rather than the transferee.

In this circumstance, access to the cash generated by collecting the

future revenues is deemed to be eliminated if all

of the answers to

the following questions are “no.”

9. Does the University have an obligation to advance amounts

to the transferee before it collects equivalent amounts from

the future revenues? Note: The payments to the transferee

should be made only from the resources generated by the

specific future revenues rather than from the University’s

own resources.

(¶7b(1))

02/27/07 Exhibit 2, Page 3 of 3

Yes/No

Source Document/

Specific Reference

10. Is the cash collected by the University on behalf of the

transferee remitted to the transferee after significant delay?

(¶7b(2))

If the answers to Questions 1–7 and 9–10 are “no,”

notwithstanding the fact that the answer to Question 8 is “yes,”

then the transaction must be recorded as a true sale, not as a

collateralized borrowing.

The University may remain associated with specific revenues in

ways that do not

constitute the primary or fundamental activity

that generates the revenues and thus would not be considered to

be actively involved in the generation of those revenues.

Perform an assessment of the following, although a “yes” answer

is informational and not indicative of active involvement.

11. Does the University hold title to revenue-producing assets

(for leases, rents or royalty income, for example)?

(¶10a)

12. Does the University own a contractual right to a stream of

future revenues?

(¶10b)

13. Does the University maintain an association with the future

revenues by retaining the required characteristics of the

future revenues in order for the cash to flow?

(GASB

Statement No. 33 ¶20a)

14. Does the University maintain an association with the future

revenues by meeting time requirements specified by

enabling legislation or the provider?

(GASB Statement No. 33

¶20b)

15. Does the University maintain an association with the future

revenues by incurring allowable costs under the applicable

programs where the provider offers resources on a

reimbursement (“expenditure-driven”) basis?

(GASB

Statement No. 33 ¶20c)

16. Does the University maintain an association with the future

revenues by meeting a specified action required by the

provider of the resources? The provider’s offer of resources

is contingent upon a specified action of the recipient and that

action has occurred. (For example, the University is required

to raise a specific amount of resources from third parties or

to dedicate its own resources for a specified purpose and has

complied with those requirements.)

(GASB Statement No. 33

¶20d)

17. Has the University agreed to refrain from specified acts or

transactions (e.g., agreeing to non-competition restrictions)?

(¶10d)

Prepared by: Date:

Reviewed by: Date:

02/27/07 Exhibit 3, Page 1 of 1

EXHIBIT 3: ACCOUNTING FOR A SALE OF EXISTING RECEIVABLES AS A TRUE SALE

Debit (Credit) Increase (Decrease)

Transaction Reference Statement of Net Assets SRECNA Statement of Cash Flows

Reconciliation of Net Operating Income

(Loss) to Net Cash Provided (Used) by

Operating Activities

1. Receive $990 in cash and a

$20 note receivable upon sale

of $1,000 of existing

University MOP loans that are

classified as Investments.

Cash $990

Note receivable-sale of

receivables-investments

1

$20

AGC 160618 (Current)

AGC 161370 (Noncurrent)

Investments (MOP loan) ($1,000)

AGC 161140

A/R STIP Invest. Sales $1,000

AGC 160562

A/R STIP Invst. Sales-Settlements

AGC 160563 ($1,000)

Proceeds from sale of

investments (investing

activity) $990

N/A—Not an operating transaction.

This is an investing transaction.

(Gain) loss on sale of

investments ($10)

AGC 208281

OR

Receive $990 in cash and a

$20 note receivable upon sale

of $1,000 of existing

University receivables that are

not

classified as investments.

Cash $990

Note receivable-sale of

Receivables-sale

2

$20

AGC 160614 (Current)

AGC 161330 (Noncurrent)

Notes receivable-collection ($1,000)

AGC 160612 (Current)

AGC 161320 (Noncurrent)

Collections of loans from student

and employees (operating

activity) $990

Accounts receivable ($20)

Accounts receivable $1,000

Other operating revenues

3

Gain on sale of receivable ($10)

AGC 208300

Operating income (loss) $10

Note: Example is for sale of current funds notes receivable; new codes for sales of loan funds receivables can be found in Exhibit 8.

(1) New notes receivable-sale of receivables-investments will be recorded in noncurrent assets (AGC 161370) and the current portion will be reclassified to current assets (AGC 160618) at year end.

(2) New notes receivable-sale of receivables-sale will be recorded in noncurrent assets (AGC 161330) and the current portion will be reclassified to current assets (AGC 160614) at year end.

(3) Other operating expenses if a loss on sale (OC7630).

02/27/07 Exhibit 4, Page 1 of 1

EXHIBIT 4: ACCOUNTING FOR A SALE OF EXISTING RECEIVABLES AS A COLLATERALIZED BORROWING

Debit (Credit) Increase (Decrease)

Transaction Reference Statement of Net Assets SRECNA Statement of Cash Flows

Reconciliation of Net Operating Income

(Loss) to Net Cash Provided (Used) by

Operating Activities

1. Receive $990 in cash and a

$20 note receivable upon sale

of $1,000 of existing

University MOP loans that are

classified as Investments, or

other receivables that are not

classified as investments, and

record collateralized

borrowing obligation.

Cash $990

Note receivable-sale of

receivable-collateralized

borrowing

1

$20

AGC 160615 (Current)

AGC 161340 (Noncurrent)

Collateralized borrowing

obligations-sales of receivables

2

($1,010)

AGC 164761 (Current)

AGC 165571 (Noncurrent)

Proceeds from collateralized

borrowing obligations (other

noncapital financing) $1,010

Collections of loans from student

and employees (operating

activity) ($20)

N/A—Not an operating transaction.

This is a noncapital financing

transaction.

Accounts receivable ($20)

2. Collect $50 of pledged

receivables (non-investment

receivables in this example),

including $5 interest income.

Cash $50

Notes receivable-collection ($45)

AGC 160612 (Current)

AGC 161320 (Noncurrent)

Collections of loans from student

and employees (operating

activity) $45

Accounts receivable $45

Other operating revenue ($5)

Other receipts/payments

(operating activity) $5

Operating income (loss) $5

3. Remit $50 payment to

transferee.

Cash ($50)

Collateralized borrowing

obligations-sale of receivables-

payment

2

$50

AGC 164762 (Current)

Payments under collateralized

borrowing obligations (other

noncapital financing) ($50)

N/A—Not an operating transaction.

This is a noncapital financing

transaction.

4. Remit $25 final payment to

transferee that exceeds the

collateral borrowing

obligation.

Cash ($25)

Other operating expense $25

OC 7640

Other receipts/payments

(operating activity) ($25)

Operating income (loss) ($25)

Note: Example is for sale of current funds notes receivable; new codes for sales of loan funds receivables can be found in Exhibit 8.

(1) New notes receivable-sale of receivables-collateralized borrowing will be recorded in noncurrent assets (AGC 161340) and the current portion will be reclassified to current assets (AGC 160615)

at year end.

(2) New collateralized borrowing obligations-sale of receivables will be recorded in noncurrent liabilities (AGC 165571) and the current portion will be reclassified to current liabilities (AGC

164761) at year end. Payments during each fiscal year will be debited to AGC 164762 to correctly reflect the transaction in the financial statements and footnotes. After fiscal year end, the

balance in AGC 164762 must be closed into AGC 164761 so that AGC 164762 reflects only current fiscal payments for collateralized borrowing obligations.

02/27/07 Exhibit 5, Page 1 of 1

EXHIBIT 5: ACCOUNTING FOR A SALE OF FUTURE REVENUES AS A TRUE SALE

Debit (Credit) Increase (Decrease)

Transaction Reference Statement of Net Assets SRECNA Statement of Cash Flows

Reconciliation of Net Operating Income

(Loss) to Net Cash Provided (Used) by

Operating Activities

1. Receive $990 in cash and a

$20 note receivable upon sale

of future University revenues.

Defer revenue recognition.

Cash $990

Note receivable-sale of future

revenues-sale

1

$20

AGC 160616 (Current)

AGC 161350 (Noncurrent)

Deferred revenue-sale of future

revenue

2

($1,010)

AGC 164350 (Current)

AGC 165580 (Noncurrent)

Collections from sale of future

revenues (other operating

receipts) $990

Accounts Receivable ($20)

Deferred revenue $1,010

2. Recognize deferred

revenue using a systematic

and rational method over the

duration of the sale agreement.

Deferred revenue-sale of future

revenue-earned

2

$60

AGC 164360 (Current)

Revenue (dependent on the

proper classification of

revenue sold) ($60)

AGC various

Source based upon proper

classification of revenue sold

(operating activity) $60

Other (other operating payments)

($60)

Deferred revenue ($60)

Operating income (loss) $60

OR

Receive $990 in cash and a

$20 note receivable upon sale

of future University revenues.

Recognize all revenue at time

of sale.

Cash $990

Note receivable-sale of future

revenues-sale

1

$20

AGC 160616 (Current)

AGC 161350 (Noncurrent)

Revenue (dependent on the

proper classification of

revenue sold) ($1,010)

AGC various

Source based upon proper

classification of revenue sold

(operating activity) $1,010

Other (other operating payments)

($20)

Accounts Receivable ($20)

Operating income (loss) $1,010

Note: Example is for sale of current funds future revenues; new codes for sales of loan funds future revenues can be found in Exhibit 8.

(1) New notes receivable-sale of future revenues will be recorded in noncurrent assets (AGC 161350) and the current portion will be reclassified to current assets (AGC 160616) at year end.

(2) New deferred revenue-sale of future revenues will be recorded in noncurrent assets (AGC 165580) and the current portion will be reclassified to current assets (AGC 164350) at year end. The

reclassification of revenue earned during each fiscal year will be debited to AGC 164360 to correctly reflect the transaction in the financial statements and footnotes. After fiscal year end, the

balance in AGC 164360 must be closed into AGC 164350 so that AGC 164360 reflects only current fiscal year reclassification of revenue earned.

02/27/07 Exhibit 6, Page 1 of 1

EXHIBIT 6: ACCOUNTING FOR A SALE OF FUTURE REVENUES AS A COLLATERALIZED BORROWING

Debit (Credit) Increase (Decrease)

Transaction Reference Statement of Net Assets SRECNA Statement of Cash Flows

Reconciliation of Net Operating Income

(Loss) to Net Cash Provided (Used) by

Operating Activities

1. Receive $990 in cash and a

$20 note receivable upon sale

of future University revenues

and record a collateralized

borrowing obligation.

Cash $990

Note receivable-sale of future

revenues-collateralized borrowing

1

$20

AGC 160617 (Current)

AGC 161360 (Noncurrent)

Collateralized borrowing

obligation-sale of future revenues

2

($1,010)

AGC 164763 (Current)

AGC 165573 (Noncurrent)

Proceeds from collateralized

borrowing obligations (other

noncapital financing) $990

N/A—Not an operating transaction.

This is a noncapital financing

transaction.

Accounts receivable ($20)

2. Record $50 pledged

revenue as revenue in

accordance with the

recognition and measurement

criteria appropriate to the

specific type of revenue

pledged.

Cash $50

Revenue (dependent on the

proper classification of

revenue sold) ($50)

AGC various

Revenue (classification dependent

on type) (operating activity) $50

Operating income (loss) $50

3. Remit $50 payment to

transferee.

Cash ($50)

Collateralized borrowing

obligation-sale of future revenue-

payment

2

$50

AGC 164764 (Current)

Payments under collateralized

borrowing obligations (other

noncapital financing) ($50)

N/A—Not an operating transaction.

This is a noncapital financing

transaction.

Note: Example is for sale of current funds future revenues; new codes for sales of loan funds future revenues can be found in Exhibit 8.

(1) New notes receivable-sale of future revenues-collateralized borrowing will be recorded in noncurrent assets (AGC 161360) and the current portion will be reclassified to current assets (AGC

160617) at year end.

(2) New collateralized borrowing obligation-sale of future revenues will be recorded in noncurrent liabilities (AGC 165573) and the current portion will be reclassified to current liabilities (AGC

164763) at year end. Payments during each fiscal year will be debited to AGC 164764 to correctly reflect the transaction in the financial statements and footnotes. After fiscal year end, the

balance in AGC 164764 must be closed into AGC 164763 so that AGC 164764 reflects only current fiscal payments for collateralized borrowing obligations.

Exhibit 7: Summary of Existing Transactions Requiring Review Under the Provisions of GASB Statement No. 48

Campus Foundation Campus Medical Center Foundation Campus Medical Center Foundation Campus Medical Center Foundation

1. Sale of accounts receivable: Has your

location entered into a transaction where you

have exchanged your interest in the collection

of existing accounts receivable for an

immediate cash payment...sale of receivables?

(1) No No (2) No No No No No (3) No No

2. Purchase of accounts receivable: Has

your location entered into a transaction where

you have purchased from an unrelated third-

party their interest in the collection of their

existing accounts receivable for an immediate

cash payment?

No No No No No No No No No (4) No No

3. Sale of future revenues: Has your location

entered into a transaction where you have

exchanged your interest in the generation and

collection of future revenues for an immediate

cash payment?

No No No (2) No No No No No (5) No No

4. Purchase of future revenues: Has your

location entered into a transaction where you

purchased from an unrelated third-party their

interest in their generation and collection of

future revenues for an immediate cash

payment?

No No No No No No No No No (6) No No

5. Sale or donation of any assets: Has your

location entered into any transaction with

another campus or campus foundation where

you have been on either end of a sale or

donation of any assets at a value other than

carrying value?

No No No No No No No No No No No No

6. Sale or donation of any future revenues:

Has your location entered into any transaction

with another campus or campus foundation

where you have been on either end of a sale o

r

donation of any future revenues at a value

other than carrying value?

No No No No No No No No No No No No

7. Pledge of future revenues: Other than for

external debt, are you aware of any situations

on your campus where revenues are pledged

as security for repayment thereby making a

portion of the revenues legally and

contractually unavailable for other purposes?

No No No No No No No No No (7) No No

(1) At UCOP we have completed several transactions over the past several years where UC has sold its interest in groups of MOP and SHLP loans to seven financial institutions for a cash payment under purchase, sale and servicing

agreements. UC continues to service the loans by collecting monthly loan payments via payroll deduction and receipt of cash and remitting payments to the buyers monthly.

(2) San Francisco - Possible future sale of patent revenue/receivable to an outside agency. Also School as Lender transactions - 2 loans processed to "qualify" for the program, but campus does not think it will participate.

(3) Los Angeles. The sale of Law School Stafford Loans to Wachovia Bank approximately one week after we own and disburse them. The School As Lender program was initiated in FY06, however, I believe we did not sell any loa

until FY07 as the initial loans made in April 2006 were from internal resources and we made to maintain our eligibility for the program. We have since contracted with a third party to make and sell the loans on our behalf. We are

trying to obtain a full set of the contractual documents so we can review this program more carefully.

(4) Los Angeles. In the same transaction noted above (3), we borrow the funds from Wachovia Bank using a line of credit, loan those funds to students, then sell them back to Wachovia Bank within one week's time.

Berkeley San Francisco Los AngelesDavis

UCOP

(5) Los Angeles. The future revenues would be the interest and principle of the funds loaned to students for Stafford Loans. We sell the loans to Wachovia prior to much interest accrual or any collection requirements.

(6) Los Angeles. We purchase from Wachovia their interest in the generation and collection of future revenues related to Stafford Loan fund. Later we sell them back.

(7) Los Angeles. I'm not certain whether the contract states that we pledge our receivables as part of the loan from Wachovia Bank or not. I would need to see the contract.

02/27/07 Exhibit 7, Page 1 of 2

Exhibit 7: Summary of Existing Transactions Requiring Review Under the Provisions of GASB Statement No. 48

1. Sale of accounts receivable: Has your

location entered into a transaction where you

have exchanged your interest in the collection

of existing accounts receivable for an

immediate cash payment...sale of receivables?

2. Purchase of accounts receivable: Has

your location entered into a transaction where

you have purchased from an unrelated third-

party their interest in the collection of their

existing accounts receivable for an immediate

cash payment?

3. Sale of future revenues: Has your location

entered into a transaction where you have

exchanged your interest in the generation and

collection of future revenues for an immediate

cash payment?

4. Purchase of future revenues: Has your

location entered into a transaction where you

purchased from an unrelated third-party their

interest in their generation and collection of

future revenues for an immediate cash

payment?

5. Sale or donation of any assets: Has your

location entered into any transaction with

another campus or campus foundation where

you have been on either end of a sale or

donation of any assets at a value other than

carrying value?

6. Sale or donation of any future revenues:

Has your location entered into any transaction

with another campus or campus foundation

where you have been on either end of a sale o

r

donation of any future revenues at a value

other than carrying value?

7. Pledge of future revenues: Other than for

external debt, are you aware of any situations

on your campus where revenues are pledged

as security for repayment thereby making a

portion of the revenues legally and

contractually unavailable for other purposes?

Campus Foundation Campus Medical Center Foundation Campus Foundation Campus Foundation Campus Medical Center Foundation Campus Foundation

No No No No No No No No No No No No No No

No No No No No No No No No No No No No No

No No No No No No No No No No No No No No

No No No No No No No No No No No No No No

No No No No No No No No No No No No No No

No No No No No No No No No No No No No No

No No No No No No No No No No No No No No

(6) Los Angeles. We purchase from Wachovia their interest in the generation and collection of future revenues related to Stafford Loan fund. Later we sell them back.

(7) Los Angeles. I'm not certain whether the contract states that we pledge our receivables as part of the loan from Wachovia Bank or not. I would need to see the contract.

Irvine MercedRiverside San Diego Santa Cruz Santa Barbara

(5) Los Angeles. The future revenues would be the interest and principle of the funds loaned to students for Stafford Loans. We sell the loans to Wachovia prior to much interest accrual or any collection requirements.

(1) At UCOP we have completed several transactions over the past several years where UC has sold its interest in groups of MOP and SHLP loans to seven financial institutions for a cash payment under purchase, sale and servicing

agreements. UC continues to service the loans by collecting monthly loan payments via payroll deduction and receipt of cash and remitting payments to the buyers monthly.

(2) San Francisco - Possible future sale of patent revenue/receivable to an outside agency. Also School as Lender transactions - 2 loans processed to "qualify" for the program, but campus does not think it will participate.

(3) Los Angeles. The sale of Law School Stafford Loans to Wachovia Bank approximately one week after we own and disburse them. The School As Lender program was initiated in FY06, however, I believe we did not sell any loans until

FY07 as the initial loans made in April 2006 were from internal resources and we made to maintain our eligibility for the program. We have since contracted with a third party to make and sell the loans on our behalf. We are trying to obtain

a full set of the contractual documents so we can review this program more carefully.

(4) Los Angeles. In the same transaction noted above (3), we borrow the funds from Wachovia Bank using a line of credit, loan those funds to students, then sell them back to Wachovia Bank within one week's time.

02/27/07 Exhibit 7, Page 1 of 2

02/27/07 Exhibit 8, Page 1 of 1

EXHIBIT 8: NEW ACCOUNTING CODES TO BE ESTABLISHED

CURRENT LOAN

CA-Note receivable – sale of receivable – sale AGC160614 AGC140614

CA-Note receivable – sale of receivable – collateralized borrowing AGC160615 AGC140615

CA-Note receivable – sale of future revenues – sale AGC160616 AGC140616

CA-Note receivable – sale of future revenues – collateralized borrowing AGC160617 AGC140617

CA-Note receivable – sale of receivable – investment AGC160618 N/A

NA-Note receivable – sale of receivable – sale AGC161330 AGC141330

NA-Note receivable – sale of receivable – collateralized borrowing AGC161340 AGC141340

NA-Note receivable – sale of future revenues – sale AGC161350 AGC141350

NA-Note receivable – sale of future revenues – collateralized borrowing AGC161360 AGC141360

NA-Note receivable – sale of receivable – investment AGC161370 N/A

CL-Deferred revenue – sale of future revenues AGC164350 AGC144350

CL-Deferred revenue – sale of future revenues – earned AGC164360 AGC144360

CL-Collateralized borrowing obligations – sale of receivables AGC164761 AGC144761

CL-Collateralized borrowing obligations – sale of receivables – payt. AGC164762 AGC144762

CL-Collateralized borrowing obligations – sale of future revenue AGC164763 AGC144763

CL-Collateralized borrowing obligations – sale of future revenue – payt. AGC164764 AGC144764

NL-Collateralized borrowing obligations – sale of receivables AGC165571 AGC145571

NL-Collateralized borrowing obligations – sale of future revenue AGC165573 AGC145573

NL-Deferred revenue – sale of future revenues AGC165580 AGC145580

Operating Revenue – Gain on sale of receivables AGC208300 TC8026

Operating Expense – Loss on sale of receivables OC7630 TC8123

Operating Expense – Payment of pledged receivables

1

OC7640 TC8124

1

Object code to be used to reflect any collections of pledged receivables and revenue subsequently paid to the transferee

after the collateralized borrowing obligation has been liquidated.

GASB Statement No. 48

Exhibit 9 - Footnote Disclosure Report: Collateralized Borrowing Activity

Debit (Credit)

A

BCDE

Reclassification

Beginning New from Long-Term Payments Ending

Balance Obligations (Calculated Number) To Buyer Balance

Collateralized Borrowing Activity-Sale of Receivables

Current Portion

CL- Collateralized Borrowing Obligations-Sale of Receivables (1)

Payments to Buyer 164762 + 144762

Reclassification From Long Term (5)

CL- Collateralized Borrowing Obligations-Sale of Receivables (1)

Current Activity Sum Sum Sum Sum

Noncurrent Portion

NL- Collateralized Borrowing Obligations-Sale of Receivables 165571 + 145571

New Collateralized Mortgage Obligations (3)

Reclassification To Current (6)

NL- Collateralized Borrowing Obligations-Sale of Receivables 165571 + 145571

Noncurrent Activity Sum Sum Sum Sum Sum

Total Collateralized Borrowing Activity-Sale of Receivables Sum Sum Sum Sum Sum

Collateralized Borrowing Activity-Sale of Future Revenue

Current Portion

CL- Collateralized Borrowing Obligations-Sale of Future Revenue (2)

Payments to Buyer 164764 + 144764

Reclassification From Long Term (7)

CL- Collateralized Borrowing Obligations-Sale of Future Revenue (2)

Current Activity Sum Sum Sum Sum

Noncurrent Portion

NL- Collateralized Borrowing Obligations-Sale of Future Revenue 165573 + 145573

New Collateralized Mortgage Obligations (4)

Reclassification To Current (8)

NL- Collateralized Borrowing Obligations-Sale of Future Revenue 165573 + 145573

Noncurrent Activity Sum Sum Sum Sum

Total Collateralized Borrowing Activity-Sale of Future Revenue Sum Sum Sum Sum

(1) 164761 + 164762 + 144761 + 144762

(2) 164763 + 164764 + 144763 + 144764

(3) Calculated: E(165571 + 145571) - D(164762 + 144762) - A(165571 + 145571)

(4) Calculated: E(165573 + 145573) - D(164764 + 144764) - A(165573 + 145573)