Medicare Financial Management Manual

Chapter 5 - Financial Reporting

Table of Contents

(Rev. 315, 05-17-19)

Transmittals for Chapter 5

10 - Checks Paid Method - General

20 - Summary of Procedures

30 - Establishment of Special Bank Accounts

30.1 - Execution of Bank Agreement

30.2 - Collateral Requirement

30.3 - Changes in Collateral Pledged as Security for Federal Health Insurance

Accounts

30.4 - Check Format Specifications

40 - Signature of Bank Individuals Authorized to Draw on The Letter-of-Credit

40.1 - Revision of Signature Cards

40.2 - Request for Additional Cards

40.3 - Signatures of Contractor Personnel Authorized for Federal Health

Insurance Time Account

50 - Withdrawal of Federal Funds

60 - Use of Payment Vouchers

70 - Form CMS-1521, Payment Voucher on Letter-of-Credit Transmittal

70.1 - Instructions for Completion of Form CMS-1521

80 - Form CMS-1522, Monthly Contractor Financial Report

80.1 - Instructions for Completion of Form CMS-1522

80.2 - Medicare Contractor Monthly Cash Collections Worksheet

90 - Intermediary Benefit Payment Report (Form CMS-456)

90.1 - Purpose and Scope

90.2 - Due Dates and Transmittal

90.3 - Verification of Data

90.4 - Accuracy of Data Contained on Report and Reconciliation of Data

Reflected on Monthly Intermediary Financial Report (Form CMS-1522)

90.5 - General Reporting Instructions

90.6 - Instructions for Completion of the IBPR

90.7 - Form CMS-456 - Schedule R

100 - Issuance of Letter-of-Credit

100.1 - Monthly Limitation

100.2 - Amending Letter-of-Credit

100.3 - Establishment of Accounting Records

110 - Initial Federal Health Insurance Time Account Deposit

110.1 - Subsequent Time Account Deposits and Adjustments

110.2 - Bank Account Analysis

120 - Reviewing Bank Agreements

120.1 - Terminating Bank Agreements

120.2 - Terminating Federal Health Insurance Accounts

120.3 - Phase-out Period for Federal Health Insurance Bank Accounts

130 - Invitation for Bid (IFB) to Provide Banking Services Under The Checks Paid

Method of Letter-of-Credit Financing

140 - Bonding

150 - Letter-of-Credit Check List

160 - Electronic Funds Transfer (EFT)

170 - Electronic Remittance Advice (ERA)

180 - Exhibits

190 - General Information About Termination Costs

200 - General

210 - Instructions for Completing The Form CMS-750A/B, Contractor Financial Reports

220 - Due Date

230 - Certification

240 - Instructions for Completing Form CMS-751 A/B, Status of Accounts Receivable

250 - Due Date

260 - Certification

270 - Line Item Instructions Form CMS-751A/B

270.1 - Line 1, Beginning FY Balance (Principal & Interest)

270.2 - Line 2a, New Receivables (Principal)

270.3 - Line 2b, Accrued Receivables (Principal)

270.4 - Line 3, Interest Earned (Interest)

270.5 - Line 4a, Cash/Check Collections on Receivables (Principal & Interest)

270.6 - Line 4b, Offset Collections on Receivables (Principal & Interest)

270.7 - Line 4c, Collections Deposited at Another Location (Principal & Interest)

270.8 - Line 5, Adjusted/Transferred/Waived Amounts (Principal & Interest)

270.9 - Line 6, Amounts Written-off Closed (Bad Debts)/Transferred CNC

(Principal & Interest)

270.10 - Line 7, Ending Balance (Principal & Interest)

270.11 - Line 7a, Current Receivables (Principal)

270.12 - Line 7b, Non-current Receivables (Principal)

270.13 - Line 8, Allowance for Uncollectible Accounts (Principal & Interest)

270.14 - Line 9, Total Receivables Net of Allowance

270.15 - Line 10, Cash/Offsets Received for Receivables at Another Location

(Principal & Interest).

270.16 - Line 1, Total Not Delinquent (Principal & Interest)

270.17 - Line 2, Total Delinquencies (Principal & Interest)

270.18 - Line 3, Status of Delinquent Receivables, less than or equal to 180 Days

(Principal & Interest)

270.19 - Line 4, Status of Delinquent Receivables, greater than 180 Days

(Principal & Interest)

270.20 - Line 4c, Collections Deposited at Another Location (Principal &

Interest)

270.21 - Line 10, Cash/Offsets Received for Receivables at Another Location

(Principal & Interest)

270.22 - Collections on Delinquent Debt (Principal & Interest)

270.23 - Line 5c, Transfers Out to other Medicare Contractors (Principal &

Interest)

270.24 - Line 5e, Transfers Out to other CMS Locations, POR/PSOR (Principal &

Interest)

270.25 - Line 5g, Transfers Out to other CMS Locations, Not POR (Principal &

Interest)

280 - Instructions for Completing the CMS-C751A/B, Status of Debt - Currently Not

Collectible (CNC), and CMS-MC751A/B, Status of MSP Debt - Currently Not

Collectible (CNC)

290 - Due Date

300 - Certification

310 - Line Item Instructions CMS-C751A/B - Non-MSP and CMS-MC751A/B - MSP

310.1 - Line 1, Beginning FY Balance (Principal & Interest)

310.2 - Line 2, New CNC Debt (Principal & Interest)

310.3 - Line 3, Interest Earned Since CNC Approval (Interest)

310.4 - Line 4(a) through (e), Reclassified CNC Debt (Principal & Interest)

310.5 - Lines 5(a) through (f), Amounts Transferred (Principal & Interest)

310.6 - Line 6, Ending Balance (Principal & Interest)

310.7 - Line 1, Total Aged CNC Debt (Principal & Interest)

310.8 - Collections on CNC Debt (Principal & Interest)

310.9 - Status of CNC Debt over 181 Days (Principal & Interest)

400 - Exhibits

400.1 - Exhibit 1 - Statement of Financial Position and Statement of Operations -

HI/SMI

400.2 - Exhibit 2 - Statement of Financial Position and Statement of Operations -

SMI

400.3 - Exhibit 3 - Status of Accounts Receivable - HI

400.4 - Exhibit 4 - Status of Accounts Receivable - SMI

400.5 - Exhibit 5 - Status of Non-MSP Debt - CNC - HI

400.6 - Exhibit 6 - Status of Non-MSP Debt - CNC - SMI

400.7 - Exhibit 7 - Status of MSP Accounts Receivable - HI

400.8 - Exhibit 8 - Status of MSP Accounts Receivable - SMI

400.9 - Exhibit 9 - Status of MSP Debt - CNC - HI

400.10 - Exhibit 10 - Status of MSP Debt - CNC - SMI

400.11 - Exhibit 11 - Medicare Contractor Account Definitions - Data Element

Definitions

400.12 - Exhibit 12 - Accounts Payable - Protocol for Estimating Claims - Form

CMS-750A/B, Statement of Financial Position

400.13 - Exhibit 13 - Periodic Interim Payments (PIP) Protocol for Estimating

Payables/Receivables for the Form CMS-750A/B, Statement of Financial Position

(Intermediaries Only)

400.14 - Exhibit 14 - Protocol for Estimating Allowance for Uncollectible

Accounts Form CMS H/M -751A/B, Status of Accounts Receivable

400.15 - Exhibit 15 - Protocol for Prorating Intermediary Time Account Balances

Between Form CMS 750A (HI) and Form CMS 750B (SMI)

400.16 - Exhibit 16 - Electronic Certification

400.17 - Exhibit 17 - Instructions for the Transfer of Debt Between Reporting

Entities

400.18 - Exhibit 18 - Collection Reconciliation/Acknowledgement Form

400.20 - Exhibit 20 - Procedures for Reporting Currently Not Collectible (CNC)

Debt

400.21 - Exhibit 21 - CMS Policy for Recognizing Accounts Receivable

400.22 - Exhibit 22 - Accounts Receivable Trending Analysis Procedures

400.23 – Exhibit 23 – Instructions for the Benefits Payable Survey

400.24 – Exhibit 24 – Benefits Payable Trending Analysis Procedures

410 – Unsolicited Voluntary Refunds

410.1 – General Information

410.2 – Office of the Inspector General (OIG) Initiatives

410.3 – Unsolicited/Voluntary Refund Accounts

410.4 - Receiving and Processing Unsolicited/Voluntary Refund Checks When

Identify Information is Provided

410.5 – Handling Checks or Associated Correspondence with Conditional

Endorsements

410.6 - Receiving and Processing Unsolicited/Voluntary Refund Checks when

Identifying Information is not Provided

410.7 – CMS Reporting Requirements With the Exception of MSP

410.8 – Exhibit 1 Overpayment Refund

410.9 - Exhibit 2 Unsolicited/Voluntary Refund Checks – Summary Report

410.10 - Education

411 – Exhibits

411.1 – Overpayment Refund Form

411.2 – Exhibit 2 - Unsolicited/Voluntary Refund Checks – Summary Report

411.3 – OIG Law Enforcement Demand Letter

420 – Procedures for Re-issuance and Stale Dating of Medicare Checks

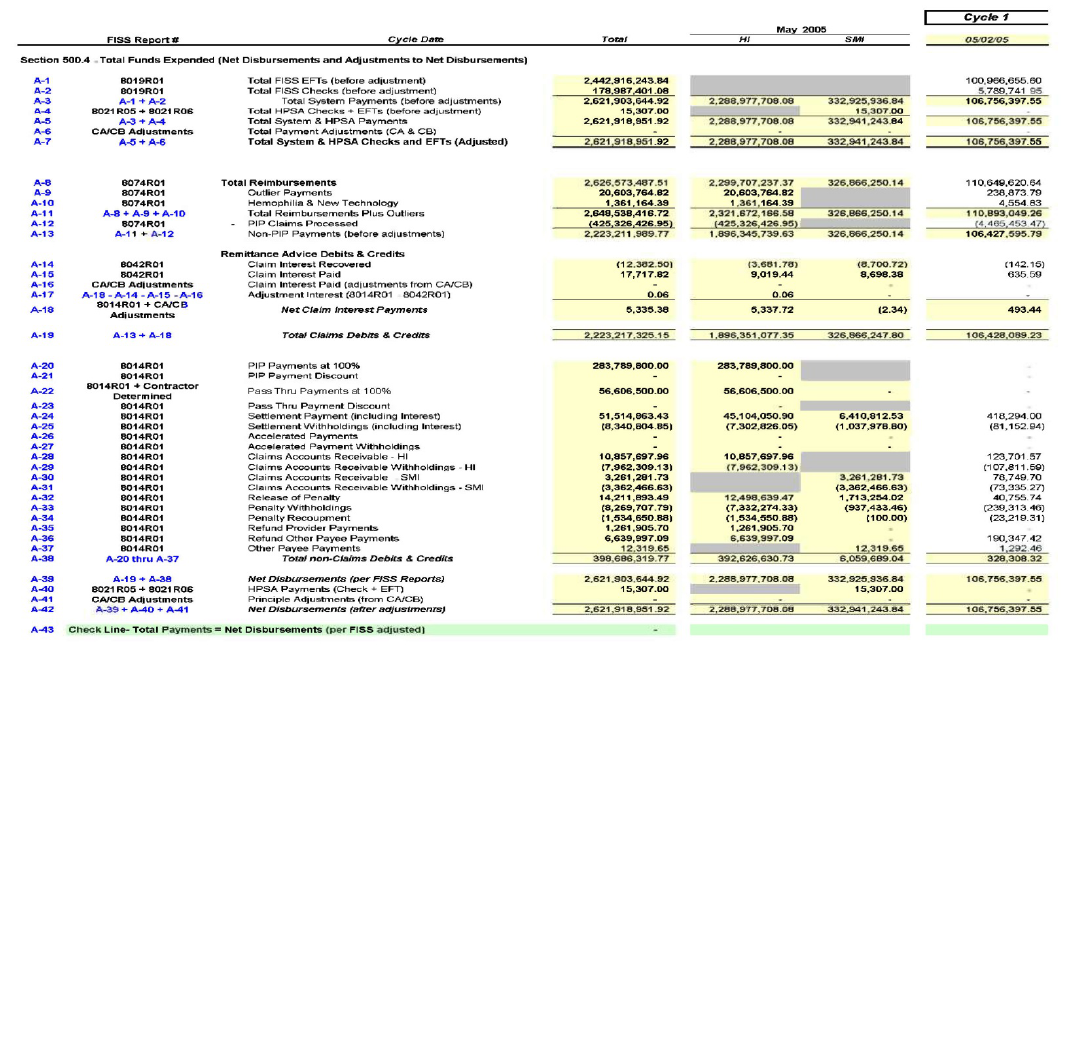

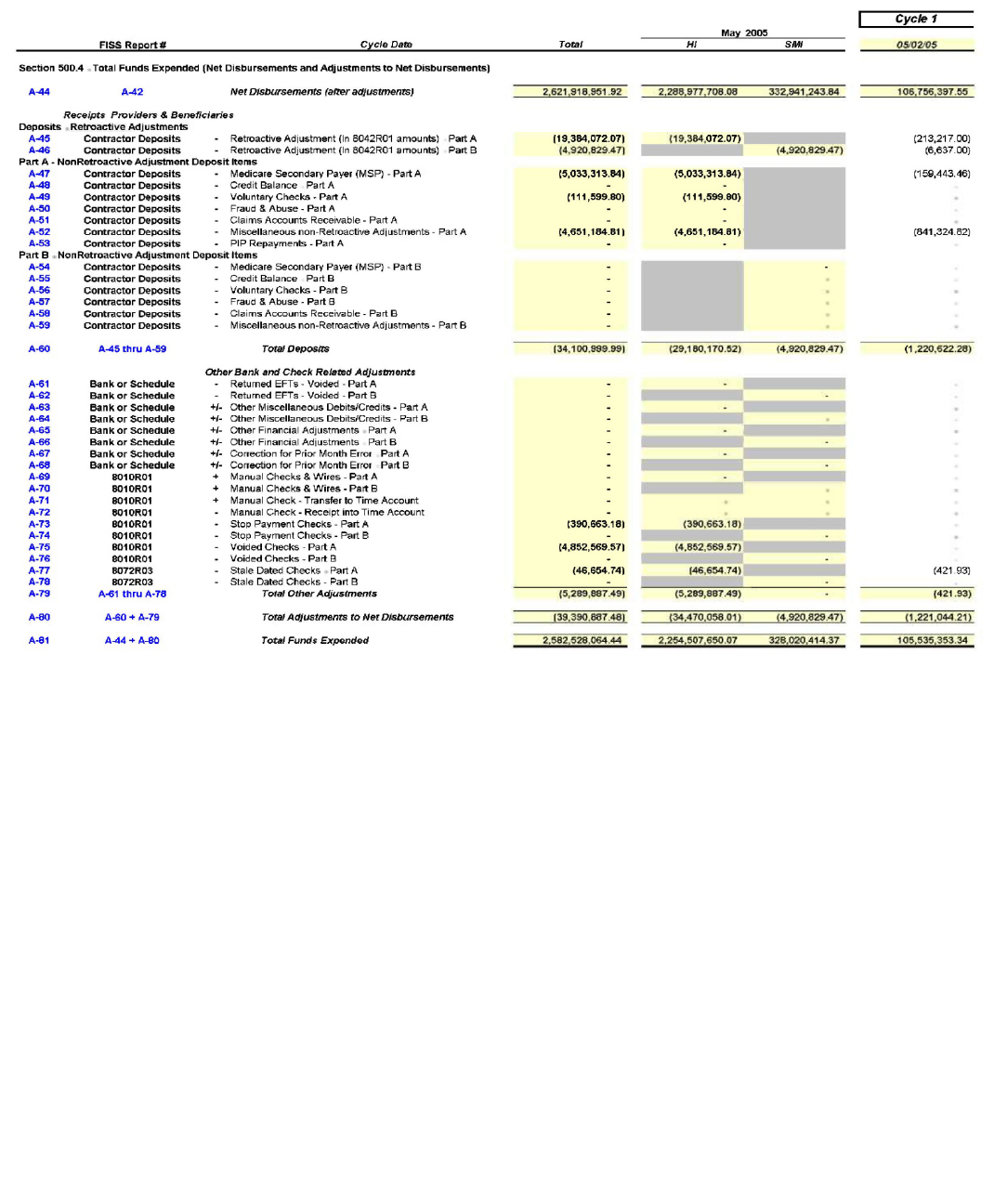

500 – Procedures for the Reconciliation of Total Funds Expended for Fiscal Intermediary

Shared System (FISS) Medicare Contractors Used in the Preparation of Form CMS-1522,

Monthly Contractor Financial Report

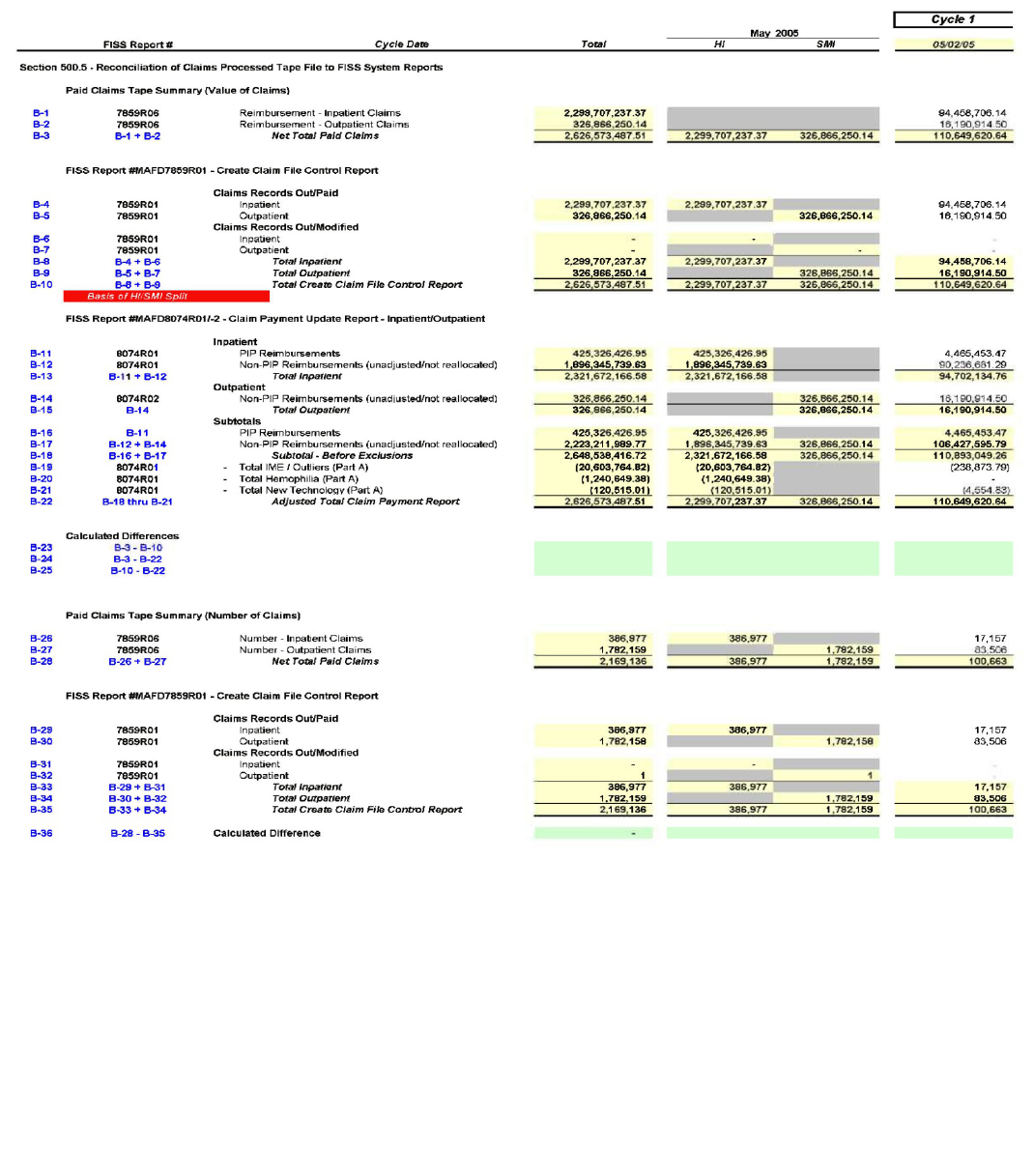

500.1 – Identification and Summarization of Detailed Claims Data Records for

Use in the Financial Reconciliation of Total Funds Expended to Fiscal

Intermediary Shared System Reports

500.2 – Using the Electronic Spreadsheet to Complete the Reconciliation of the

Detailed Claims Data File to Fiscal Intermediary Shared System Reports

500.3 – Electronic Spreadsheet Input Schedule

500.4 – Total Funds Expended (Net Disbursements and Adjustments to Net

Disbursements)

500.5 – Reconciliation of Detailed Claims Data File to FISS System Reports

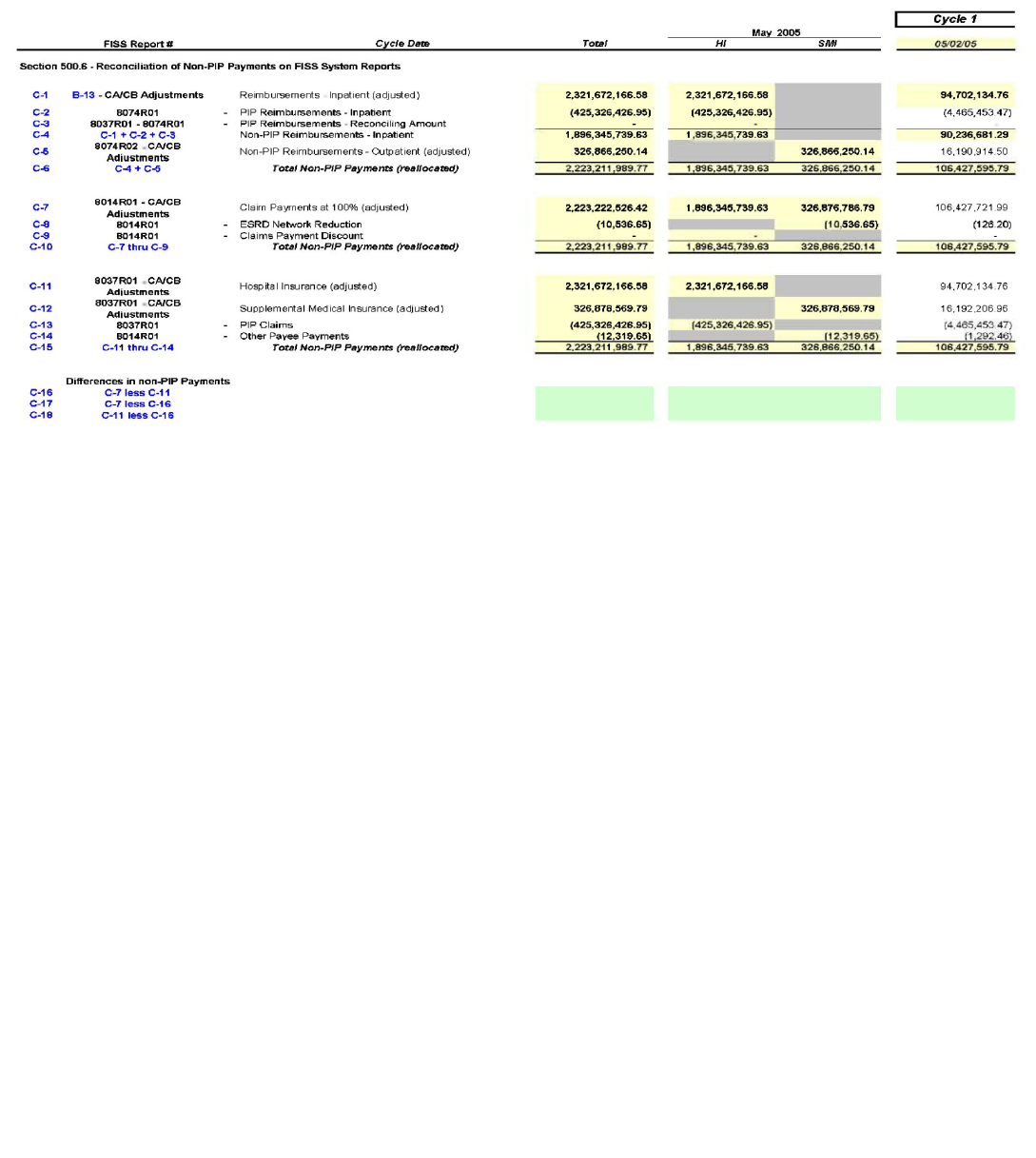

500.6 – Reconciliation of Non-PIP Payments on FISS System Reports

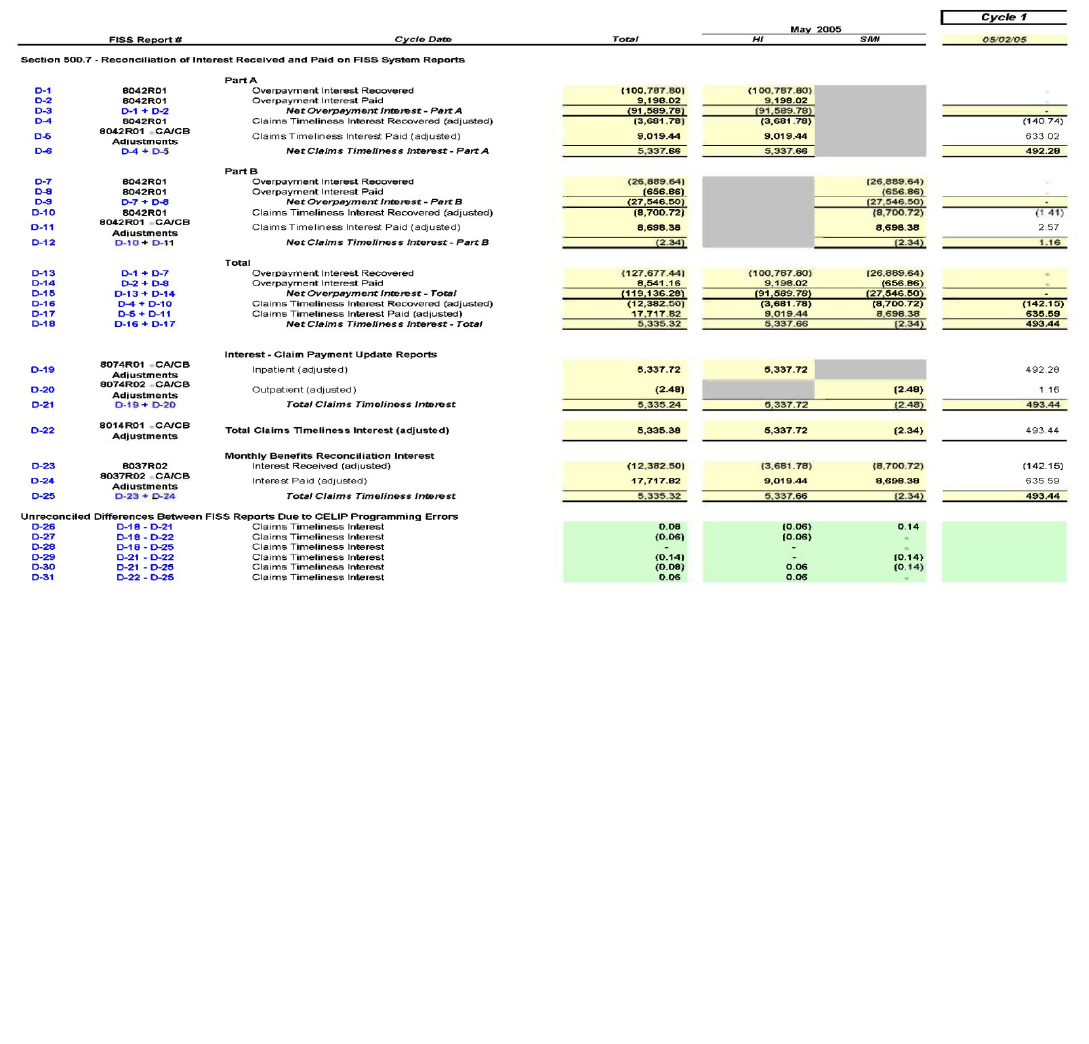

500.7 – Reconciliation of Interest Received and Paid on FISS System Reports

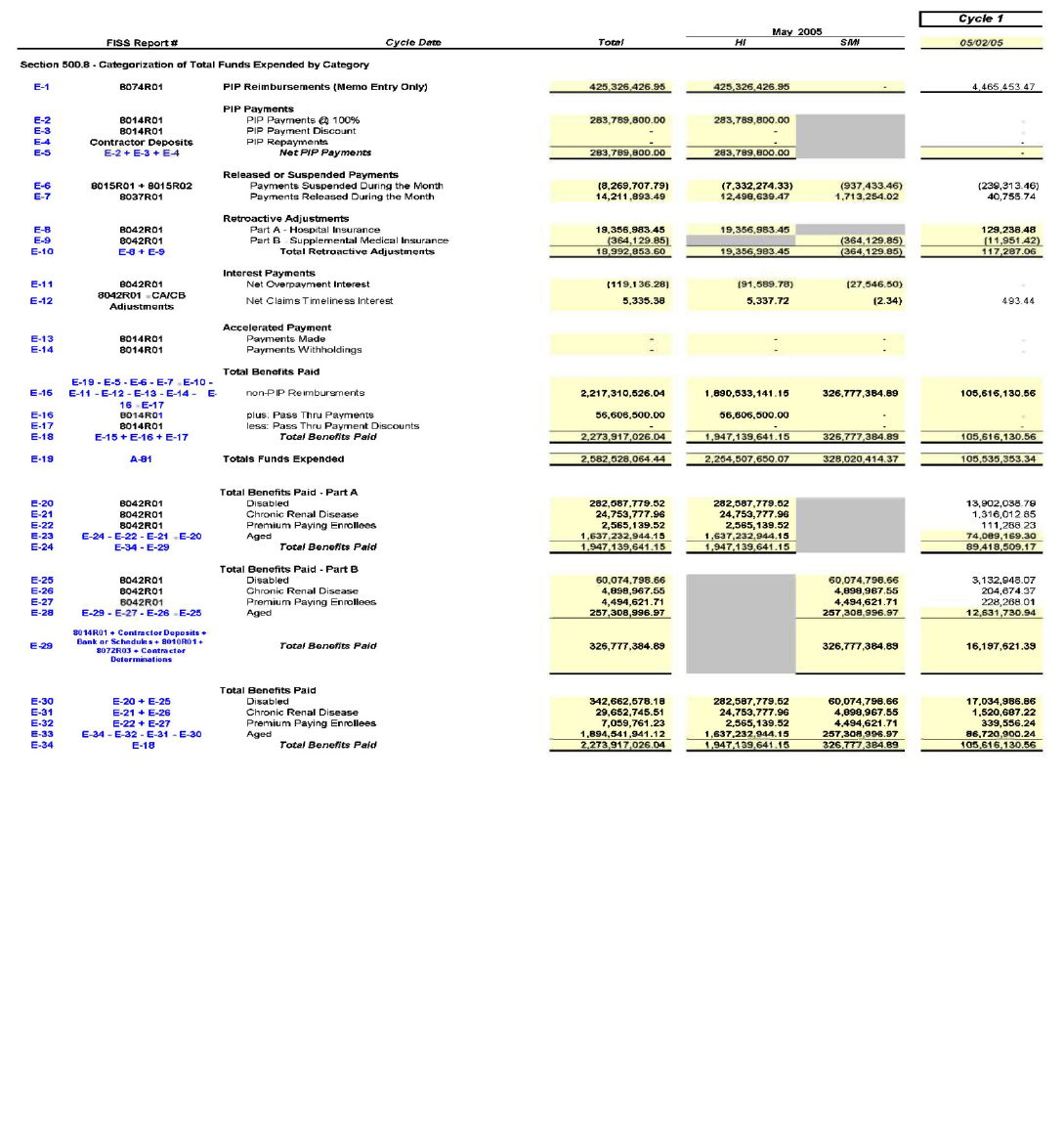

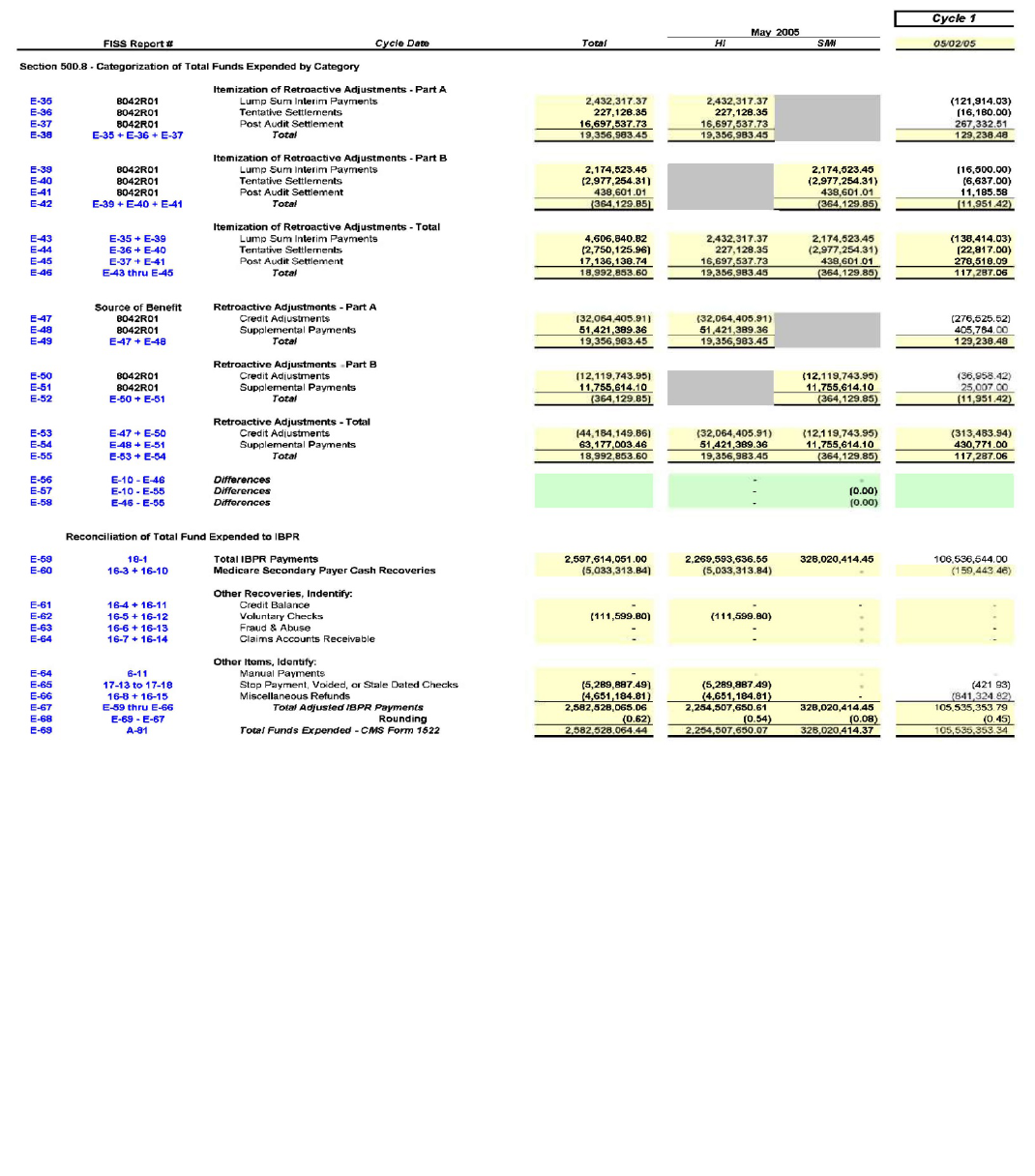

500.8 – Categorization of Total Funds Expended by Category

510-Procedures for the Reconciliation of Total Funds Expended for Multi-Carrier System

(MCS) Medicare Contractors Used in the Preparation of Form CMS-1522, Monthly

Contractor Financial Report

510.1 - Reconciliation of Detailed Claims Data File to Multi-Carrier System

(MCS) Report

510.2 - List of Primary MCS Reports Used in the Reconciliation of Total Funds

Expended

510.3 - Standard MCS 1522 Reconciliation Lead Schedule

510.4 - Reconciliation of Claim Payments from the Detailed Claims Data

File/Report to the Month-to-Date Analysis of Payment (MCS Report #2002 or

HBDR2002)

510.5 - Proof of Net Disbursements and Total Issues per Detailed Claims Data

File/Report

510.6 - Proof of Net Disbursements and Total Issues Per MCS Report #2002

510.7 - Reconciliation of Net Disbursements and System Issues from the Detailed

Claims Data File/Report to the Month-to-Date Analysis of Payment (HBDR2002)

510.8 - Proof of Net Disbursement per MCS Register Summary Report

(HBDR6000) to the Month-to-Date Analysis of Payments (HBDR2002 Report,

Line G

510.9 - Input Sheet for Cash Activity Items

520 – Instructions for Completion of the Contractor’s Monthly Bank Reconciliation

Worksheet

NOTE: Throughout this chapter, reference to provider includes institutional providers,

physicians, and suppliers, i.e., all delivers of health care services that are reimbursed by

either the intermediary or the carrier.

NOTE: Revision 1, the initial release of this chapter, includes a cross reference to the

source sections in current manuals. The manual is identified by A1, A2, A3, or A4 for

Intermediary Manual Parts 1 through 4; or by B1, B2, B3 or B4 for Carriers Manual Parts

1 through 4. This indicator is followed by a dash and the related section number.

10 - Checks Paid Method - General - (Rev. 5, 08-30-02)

A1-1400, B1-4400

Certified Letter-of-Credit Defined:

A certified letter-of-credit is a legal reservation of funds on deposit in the Federal

Reserve Bank that covers payments for which the contractor has contracted to pay by

issuing checks and authorizing electronic funds transfer.

The objective of the letter-of-credit checks paid method of financing is to reduce the level

of the Federal debt and the interest costs of short-term borrowing. This method provides

cash availability to meet Medicare program requirements, while at the same time,

controls the timing of cash withdrawals so that the impact of these withdrawals on the

public debt level and related financing costs is minimized. Cash flow is controlled by:

• Postponing withdrawal of funds from the U.S. Treasury until Medicare checks are

presented to the contractor's Medicare servicing bank for payment;

• Limiting the amount withdrawn at any time; and

• Reducing the amount of Federal funds required to offset bank service charges.

The Treasury Department requires all Government agencies that make advance payments

to utilize the letter-of-credit checks paid method of financing. (See Circular No. 1075,

revised February 27, 1973, and Chapter 1000 of the Treasury Fiscal Requirements

Manual.)

20 - Summary of Procedures - (Rev. 5, 08-30-02)

A1-1401, B1-4401

A contractor shall use the following steps to implement the letter-of-credit checks paid

method of financing:

• It shall notify the RO 165 days prior to the expiration of the current three-party

bank agreement when a new bank will be secured under the checks paid method;

• It shall request the latest copy of the Invitation for Bid (IFB) from the Regional

Office (RO);

• It shall use the IFB package as a guide to prepare its IFB. The language contained

in the package cannot be materially altered except for "BID FORMS AND

CONTRACTOR'S REQUIRED MEDICARE BANKING SERVICES." (See

Attachment A, Section G, of the package.) The contractor shall obtain from its

RO the implementation package that contains examples of material required for

the bid process as follows:

o Letter to Commerce Business Daily requesting IFB advertisement; and

o Sample write-ups of contractor's specifications for bank services,

computer requirements, check specifications, and electronic funds transfer

capability;

• It shall send the completed IFB to its RO for approval prior to its release for bid.

It shall send an additional copy to:

Centers for Medicare & Medicaid Services

Office of Financial Management

7500 Security Boulevard

Baltimore MD 21244-1850

• Obtain bids from two or more banks;

• Follow the Federal Acquisition Regulations (FAR), Part 14, when securing

competitive bids;

• Evaluate the bank bids and, with the concurrence of the servicing RO, select the

commercial bank that meets all of the mandatory requirements and submits the

lowest required time account balance;

• Select a commercial bank and establish special bank accounts;

• Secure Signature Cards. Use Form SF-1194 to obtain the signatures of those

individuals authorized by the bank to draw payment vouchers against the letter-

of-credit and the signature of the bank official who has the authority to designate

the authorized individuals;

NOTE: CMS executes the three-party bank agreement between the contractor, the bank,

and the Government (the servicing RO). CMS also issues a letter-of-credit that sets forth

the monthly limitation.

• Post (Bank) collateral with the Federal Reserve Bank;

• Establish (Bank) both the Benefits Account and the Time Account;

• Submit monthly letter-of-credit transmittals (form CMS-1521) via Contractor

Administrative Financial Management (CAFM) to the Funds Control Branch,

Central Office. Distribute Medicare funds withdrawn by bank via FNS-5401

payment voucher according to type of benefits; and

• Submit the monthly form CMS-1522, TAA-1b and TAA-1C, to CMS via the

CAFM system.

30 - Establishment of Special Bank Accounts - (Rev. 5, 08-30-02)

A1-1403, B1-4403

Keep all Federal funds withdrawn under the letter-of-credit separate from all other funds.

Designate the Medicare account for deposit in a special bank account established by you

in a member bank of the Federal Reserve System. Designate the special demand deposit

checking account as follows:

(Name of Contractor)

Federal Health Insurance Benefits Account

Designate the special non-interest bearing time account as follows:

(Name of Contractor)

Federal Health Insurance Time Account

Restrict withdrawals to transfer of funds to the Federal Health Insurance Benefits

account.(FHIBA)

30.1 - Execution of Bank Agreement - (Rev. 5, 08-30-02)

A1-1403.1, B1-4403.1

The contractor shall execute the three-party bank agreement with the selected commercial

bank. The bank agreement requires that the Federal Government retain a lien on all funds

held in the special bank account. The bank abides by written instructions of the

Government with regard to the deposit and withdrawal of funds. The Government also

has the right to inspect or audit the bank's books and records that pertain to the special

accounts. (Refer to Attachment C of the IFB package.)

The contractor shall use the following guidelines when it executes a bank agreement;

• It must strictly adhere to the wording and format of the bank agreement.

• It may alter only Covenant 7. The provisions of Covenant 7 may, by agreement of

all parties, be written to require either a one or two-year period of performance

following the initial two year period;

• The RO forwards an original and three copies of the completed three-party

agreement to the bank via the contractor for execution. Each copy of the bank

agreement must contain original signatures. Facsimile signatures are not

acceptable; and

• After it is countersigned by CMS, individual copies of the agreement are

distributed to:

o The contractor;

o The bank;

o The servicing RO; and

o Centers for Medicare & Medicaid Services

Office of Financial Management

7500 Security Boulevard

Baltimore MD 21244-1850

30.2 - Collateral Requirement - (Rev. 5, 08-30-02)

A1-1403.2, B1-4403.2

Posted collateral is based on the balance to be maintained in the time account less FDIC

coverage, if applicable. The RO advises the contractor, upon notification by the Federal

Reserve Bank, when collateral is posted. (Collateral must be acceptable under the

guidelines provided to the Federal Reserve by the Department of the Treasury).

The contractor shall place the collateral with the Federal Reserve Bank or Branch of the

district where its servicing financial institution is located or with a custodian designated

by the Federal Reserve Bank or Branch. It shall include a letter with the collateral that

states that the collateral is pledged as security for public money by CMS, agency account

number 5555-4454-5 under the terms of 31 CFR, Part 202 (Treasury Circular 176).

30.3 - Changes in Collateral Pledged as Security for Federal Health

Insurance Accounts - (Rev. 5, 08-30-02)

A1-1403.3, B1-4403.3

The CMS, Division of Contractor Financial Management (DCFM), monitors collateral

requirements. DCFM continuously reviews the most recent balances maintained in the

Federal Health Insurance Bank Accounts.

If an increase in pledged collateral appears necessary, DCFM requests the bank to post

additional collateral with its Federal Reserve Bank.

If a decrease in pledged collateral appears warranted, DCFM advises the Federal Reserve

Bank of the amount of excess collateral pledged.

The contractor shall direct any request for release of excess bank collateral to the local

Federal Reserve Bank.

30.4 - Check Format Specifications - (Rev. 5, 08-30-02)

A1-1403.4, B1-4403.4, B2-5215

The following phrase must appear on all checks or drafts written for purposes of paying

benefits and related administrative costs authorized under the Medicare program:

MEDICARE PAYMENT

For Health Insurance - Social Security Act

The contractor shall use the following check format specifications:

Check Front

The contractor shall center the words "Medicare Payment" at the top of the check or draft

and print these words in at lease 1/4-inch type. Contractor name and address should

appear on the face of the check. The check may also include the contractor's emblem or a

picture of a building it occupies. The contractor may not include advertising on the face

of the check. (Advertising should not appear on the envelope in which the check is

mailed.) It is expected that the type sizes of the items placed on the check will not detract

from the required "Medicare Payment" phrase.

Check Back

The contractor shall print on the back of all Medicare checks the following statement:

"This payment is made with Federal funds. Fraud in procuring, forging a signature or

endorsement, or materially altering this check is punishable under the U. S. Criminal

Code."

For carriers, assigned claims must also include the following statement:

"As provided by the terms of the law under which this check is issued, the undersigned

payee, in accepting assignment, agreed that the charge determination by the Medicare

carrier shall be the full charge for any service which the check is payable. The patient is

responsible only for the applicable deductible and coinsurance, and for non-covered

services."

It is not necessary to show the account name on the check. If one is shown, it should read

"Federal Health Insurance Benefits Account." If both Part A and Part B are shown, it

should read, "Federal Health Insurance Benefits Account - Part A" and "Federal Health

Insurance Benefits Account - Part B."

The time limitation for cashing the check (if specified on the check) cannot be less than 6

months.

The contractor shall clear formats of checks with the servicing RO prior to printing or

contracting for printing.

40 - Signature of Bank Individuals Authorized to Draw on The Letter-

Of-Credit - (Rev. 5, 08-30-02)

A1-1405, B1-4405

Signatures of bank representatives authorized to sign payment vouchers must be on file

along with the letter-of-credit at the servicing Federal Reserve Bank or branch in order to

honor payment vouchers (FMS-5401). The contractor shall submit a signature card, Form

SF-1194, for the person(s) authorized by the bank to sign payment vouchers.

NOTE: Executed signature card(s) must be received in DCFM no later than 20 calendar

days prior to the effective date of a new letter-of-credit.

40.1 - Revision of Signature Cards - (Rev. 5, 08-30-02)

A1-1405.1, B1-4405.1

The contractor shall prepare new card(s) if more than two signatures are no longer valid.

It shall prepare two original cards for every four individuals. If more than one card is

needed, i.e., more than 4 individuals are authorized, it shall number the cards 1 of 2, 2 of

2 to ensure that all cards are received.

New signature cards must contain the signatures of all individuals who will sign payment

vouchers and be certified by an official of the bank. The contractor need not resubmit a

new signature card if change in position or title of an individual authorized to sign

payment vouchers is involved.

The contractor shall mark new signature cards "Replaces and Supersedes all Previously

Submitted Cards" on the top edge of the card.

40.2 - Request for Additional Cards - (Rev. 5, 08-30-02)

A1-1405.2, B1-4405.2

The contractor shall send requests for additional signature cards to:

Centers for Medicare & Medicaid Services

Office of Financial Management

7500 Security Boulevard

Baltimore, MD 21244-1850

40.3 - Signatures of Contractor Personnel Authorized for Federal

Health Insurance Time Account - (Rev. 5, 08-30-02)

A1-1405.3, B1-4405.3

Signatures of two or more individuals designated by the contractor to sign withdrawal

requests to transfer funds from the Federal Health Insurance Time Account to the Federal

Health Insurance Benefits Account must be on file with the designated commercial bank.

50 - Withdrawal of Federal Funds - (Rev. 5, 08-30-02)

A1-1406, B1-4406

The Federal Government assures that funds are always in the Federal Reserve Bank to

honor properly drawn payment vouchers within the limits of the letter-of-credit. This

arrangement is consistent with State banking laws since it eliminates any possibility of

intent to defraud.

60 - Use of Payment Vouchers - (Rev. 5, 08-30-02)

A1-1408, B1-4408

To obtain Federal funds, the bank prepares a daily payment voucher, Treasury Form

FMS-5401, and forwards it to the servicing Federal Reserve Bank or Branch holding the

letter-of-credit.

When the bank receives the initial letter-of-credit, the bank sequentially numbers

payment vouchers drawn beginning with the number one (1). Amendments to the letter-

of-credit do not interrupt the sequential numbering of payment vouchers.

Payment vouchers are prepared only in an amount equal to the contractor's total checks,

bank debit memos, and electronic funds transferred. These vouchers are presented for

payment each day less any balance in the benefits account representing collected other

deposits or transfers from the Federal Health Insurance Time Account.

If the bank is not located in a Federal Reserve Bank (FRB) city, CMS requests the

Treasury Department to implement a telephonic method of receiving funds for the bank.

The bank calls its FRB and requests a specific funding amount. The FRB prepares the

payment voucher and a copy is sent to the bank.

The letter-of-credit provides a ceiling on the amount that may be drawn during the month

and is purposely set high to meet peak cash needs. In no instance is a payment voucher to

be drawn for less than $5,000 or more than $5,000,000 (unless the letter-of-credit has

been annotated "Authorized to draw payment vouchers in excess of $5,000,000"). Only

one payment voucher should be drawn per day. Regardless of the factors considered in

determining when and in what amount to draw payment vouchers, banks are expected to

abide by the intent of the letter-of-credit Checks Paid Method of financing system by

assuring that the total of the daily voucher processed is the minimum required to finance

current disbursements.

NOTE: The "Name and Address of Drawer" block on the Treasury Form FMS-5401

must include the name of the bank as it appears on the letter-of-credit sent by CMS and

the annotation "agent for" (name of contractor). Due to space limitations, the contractor

does not have to show the address in this block. A supply of payment vouchers is

provided to each commercial bank. Additional supplies of payment vouchers may be

ordered from:

Centers for Medicare & Medicaid Services

Office of Budget and Administration

Distribution Liason Officer

7500 Security Boulevard

Baltimore, MD 21244-1850.

70 - Form CMS-1521, Payment Voucher on Letter-Of-Credit

Transmittal - (Rev. 5, 08-30-02)

A1-1410, B1-4410

The purpose of form CMS-1521, Payment Voucher on Letter-of-Credit Transmittal, is to

record daily voucher data that the contractor's bank submits to the Federal Reserve Bank

for payment of Hospital Insurance (HI) and Supplemental Medical Insurance (SMI)

benefit payments. Administrative costs paid through the Smartlink System are also

reported on the form. Administrative costs are allocated to current or prior fiscal years

and to special projects.

Transmit form CMS-1521 to CMS by the 15th of each month via the CAFM System.

(See operating instructions for completion that are contained in the CAFM Users Guide.)

70.1 - Instructions for Completion of Form CMS-1521 - (Rev. 5, 08-30-

02)

A1-1410.1, B1-4410.1

Data comes from Treasury Form FMS-5401 Payment Voucher.

Date drawn - Contractor enters the date funds were drawn. It shall use 2 digits.

Voucher Number - Contractor enters the payment voucher number in 3 digits beginning

with voucher number 001 to 999. It shall inform the bank to start over when number 999

is reached.

Serial Number - Contractor enters the serial number of the payment voucher.

Hospital Insurance Benefits - Contractor enters the total amount drawn for HI and SMI.

The total of HI and SMI benefits should equal the total funds drawn.

NOTE: Part B contractors enter amounts for SMI only.

PMS Smartlink Communication System for Administrative Costs –

On pages 1 and 2, the contractor shall continue to report administrative costs drawn via

the PMS Smartlink Telecommunications System in the same designated "Administrative

Cost" column 4. However, it shall show these amounts after it reports all benefit payment

amounts.

Contractor shall indicate in the "date drawn" column the date the money was deposited

into its commercial bank account and not the date it requested the money. This entry

(entries) may occur on either page 1 or 2 depending on the number of entries.

Contractor shall not make entries in the columns for Voucher Number, Serial Number,

and Voucher Totals.

Contractor shall reflect the current or prior year administrative costs drawn via Smartlink.

It shall report on page 3 any special project(s) amount(s) drawn via Smartlink.

Public reporting burden for collecting this information is estimated to average 1 hour per

response. This includes time for reviewing instructions, searching existing data sources,

gathering and maintaining data needed, and completing and reviewing the collection of

information. Contractor shall send comments regarding this estimated burden or any

other suggestions for reducing the burden to:

Office of Management and Budget

Paperwork Reduction Project (0938-0361)

Washington, D.C. 20503;

and to:

Centers for Medicare & Medicaid Services

Office of Financial Operations

7500 Security Boulevard

Baltimore, Maryland 21244-1850.

80 - Form CMS-1522, Monthly Contractor Financial Report – (Rev. 5,

08-30-02)

A1-1412, B1-4412

Form CMS-1522 is designed to provide a reconciliation of Medicare benefit dollars

between CMS, the contractor, and the bank. The contractor shall transmit this report to

CMS by the 15th of each month via the CAFM System.

80.1 - Instructions for Completion of Form CMS-1522 - (Rev. 5, 08-30-

02) - (Rev. 5, 08-30-02)

A1-1412.1, B1-4412.1

• Screen 1 - Section A - Purpose for Which Funds are Drawn:

o Contractor shall reflect the current or prior year administrative costs drawn

via Smartlink. It shall report on page 3 any special project(s) amount(s)

drawn via Smartlink.

o Funds Drawn this Month - Contractor enters the total amount of Federal

funds drawn via payment vouchers during the calendar month for use as

HI benefits, line 1-B, or SMI benefits, line 2-B. Each entry must equal the

sum of the amounts shown in this category on the Form CMS-1521 dated

during the calendar month.

o Total Funds Expended This Month - Contractor enters total funds

expended for HI benefits, line 1-D, and SMI benefits, line 2-D during the

calendar month. Totals should equal the sum of all checks drawn and

electronic funds transfer payments against the special bank account during

the calendar month. (It shall include all checks issued and electronic funds

transferred, i.e. dated during the calendar month.) Any refunds received

from beneficiaries or their assignees during the calendar month because of

prior overpayments deposited in the special bank account should serve to

reduce total funds expended.

o Funds Drawn for Fiscal Year - This is a calculated field.

o Funds on Hand End of Month - This is a calculated field.

o Line 3, Drugs and Line 4, Regular Administrative Costs - Contractor shall

not use at this time.

o Bills Paid - Lines 7 and 8 - Completed by Part A intermediaries. Part B

carriers complete only line 8.

o Retro-Adjustment - Part A contractors enter credit adjustments on

appropriate lines. Part B contractors do not use lines 9 or 10.

• Benefits Bank Account

o From Bank Statement - The contractor shall take information for lines 15

through 19 from the statement of the special bank account issued by the

bank at the end of the calendar month.

o Line 15 - Balance Beginning of Month Per Bank - Contractor enters the

balance in the special bank account as of the beginning of the calendar

month as shown on the bank statement.

o Line 16a - Payment Vouchers Drawn During Month - Contractor enters

the total amount of funds drawn on payment vouchers (FMS-5401) during

the calendar month and credited to the benefits account as shown on the

bank statement. Since all checks drawn for deposit in the Time Account

are cleared through the benefits account, a payment voucher is drawn for

this transaction and is included in line 16a. The amount shown on this line

must agree with the totals from the Form CMS-1521 corresponding to the

calendar month and also with Section A, Line 5, column (b). The only

exception is for vouchers in transit (line 20).

o Line 16b - Other Deposits - Contractor enters all other deposits credited

during the month to the special bank account as shown on the bank

statement. It shall reduce the next payment voucher by the amount of the

deposited refunds in the account in order to minimize idle funds in the

account. It shall Include any credits or adjustments made to the bank

account during the calendar month in this line.

o Line 16c - Contractor shall include funds withdrawn from the Time

Account and deposited in the Benefits Account.

o Line 16d - Miscellaneous Credit Memo - Contractor enters any

miscellaneous adjustments to the benefits bank account during the

calendar month.

o Line 17 - This is a calculated field.

o Line 18A - Contractor shall subtract: Checks and EFT Payments Honored

by Bank During Month - It enters from the bank statement the total funds

charged to the special bank account as a result of checks honored and

electronic funds transferred by the bank during the month. This total must

include all checks that were drawn for deposit in the time account and

honored by the bank during the month.

o Lines 18B and C - Miscellaneous Bank Charges - Contractor enters any

miscellaneous charges made to the special bank account that are part of

the bank statement.

o Line 19 - This is a calculated field.

o Line 20 - Add: Deposits in Transit. - Enter payment vouchers drawn and

other deposits made during the calendar month that the bank has not yet

credited to the special bank account according to the statement.

o Line 21. - This is a calculated field.

o Line 22 - Subtract: Outstanding Checks. - Enter the total of all checks

issued during the current month or any previous month that the bank has

not yet paid as of the end of the calendar month. If during the calendar

month payment is stopped on any check previously issued, or any

previously issued check is otherwise voided, subtract the amount of funds

represented by that check from this total before making an entry on this

line.

o Line 23 - This is a calculated field.

o Line 24 - Highest Balance During Month Per Bank. Contractor enters the

highest balance in the special bank account during the calendar month as

reflected on the bank statement.

• Time Account

o Line 15 - Balance Beginning of Month - Contractor enters the balance in

the time account as of the beginning of the calendar month as shown on

the bank statement.

o Line 16a - Other Deposits - Contractor enters the amount of funds drawn

from the benefits account for deposit in the time account.

o Line 17 - Total. - This is a calculated field.

o Line 18a - Contractor enters only amount of funds withdrawn from the

time account and deposited in the benefits account during the month.

o Line 18b - Contractor enters any miscellaneous items.

o Line 19 - Balance EOM Per Bank - This is a calculated field.

• Screen 4 - Completed by Part A Contractors Only

o Periodic Interim Payments - Contractor enters amounts paid during the

month by category.

o Accelerated Payments - Contractor enters the amount of accelerated

payments paid out and received during the month.

o Suspended Payments - Contractor enters the amount of payments

suspended and released during the month.

• Screen 5 - Bills Paid - Contractor enters the amount of money actually paid during

the calendar month as follows:

o Amount paid for disabled or disability (identified by Codes 1 and 3 as

contained in S trailer of query reply).

o Amount paid for chronic renal disease (identified by Code 2 as contained

in S trailer of query reply).

o Amount paid for premium paying enrollees (identified by Codes 8 and 9

as contained in S trailer of query reply).

o Amount paid for aged. Contractor shall complete entries for disabled,

chronic renal disease, and premium paying enrollees prior to completing

the entry. It shall then subtract the sum of these entries from the calculated

Total and enter that amount.

o Total - (Bills paid for the month). This is a calculated field.

NOTE: For those Part A intermediaries that transmit bills to CMS from more than one

point, each processing point should submit to the home office at the end of the calendar

month all of the data requested in screen 1. (It shall consolidate data related to amounts

paid in screen 1.)

• Only Part A Intermediaries complete retroactive adjustments.

• Only Part A Intermediaries complete adjustments between trust funds.

• Interest:

o Interest Received From Providers On Overpayments - Separate Check for

Interest Collected - When a check is received for interest on an

overpayment, the contractor shall deposit the check immediately in the

Medicare bank account. It shall report this check as an "Other Deposit"

(line 16b). Also, it shall report the check as "Interest Received" on screen

5 and use as a reduction to expenditures on screen 1, funds expended

column.

o Check Includes Both Interest Collected and Overpayment Recoupment -

Contractor shall deposit the check immediately into the Medicare bank

account. It shall report the entire amount of the check as an "Other

Deposit" (line 16b) on screen 2. It shall report the interest portion as

"Interest Recovered" on screen 5. Both the interest recovered and the

overpayment recoupment are used as a reduction to expenditures on screen

1, funds expended column.

o Interest Paid to Providers on Underpayments - Separate Check for Interest

Paid - When a check is issued for interest due to a provider on an

underpayment, the contractor shall report it as a "Check Honored" (line

18a) on screen 2. Also, it shall report this amount as "Interest Paid" on

screen 5 and as an increase to expenditures on screen 1, funds expended

column.

• Screen 6 - No entries are required at this time.

Public reporting burden for this collection of information is estimated to average 16 hours

per response. This includes time for reviewing instructions, searching existing data

sources, gathering and maintaining data needed, and completing and reviewing the

collection of information. Contractors may send comments regarding this estimated

burden or any other suggestions for reducing the burden to:

Centers for Medicare & Medicaid Service

Office of Financial Management

Baltimore, Maryland, 21244-1850;

and to:

Office of Management and Budget

Paperwork Reduction Project (0938-0361)

Washington, D.C. 20503.

80.2 - Medicare Contractor Monthly Cash Collections Worksheet

(Rev. 80, Issued: 10-21-05, Effective: 07-01-05, Implementation: 11-21-05)

The Medicare Contractor Monthly Cash Collections Worksheet is to identify cash

collections deposited in the Medicare Trust Funds related to Provider Overpayments.

The Medicare contractors are to follow the line by line instructions for completing the

collections worksheet. The instructions are to provide uniformity throughout all

contractors for the calculations of the data used to populate each line item. Medicare

contractors are required to maintain supporting documentation for the amounts reported

on the Medicare Contractor Monthly Cash Collections Worksheet.

Medicare contractors are required to submit the worksheet via email to

[email protected] on the 15

th

day of the following month end. For year-end,

Medicare contractors may be required to submit the Monthly Cash Collections

Worksheet in an accelerated time frame.

A. Total Monthly Principal Deposit (Using Forms CMS-1522, Forms CMS-751)

Line 1 - Enter the total ‘Other Deposits’ (Line 16b, Form CMS-1522) for the

reporting period (e.g., June 30, etc.).

Line 2 - Enter ‘Deposits-In-Transit’ (Line 20, Form CMS-1522) for the month

prior to the reporting period (e.g., May 31, etc.).

Line 3 - Enter ‘Deposits-In-Transit’ (Line 20, Form CMS-1522) for the reporting

period (e.g., June 30, etc.).

Line 4 – Enter the sum of Line 1 minus (-) Line 2 plus (+) Line 3 equal (=) ‘Total

Monthly Deposits.

Monthly Interest (Cash) Collections

Line 5 – Enter the total ‘Received-Provider Overpayment’ (Line 1, page 4, Form

CMS-1522) for reporting period (e.g., June 30, etc.).

Line 6 – Enter the total ‘Interest Offset’ for the reporting period. Total ‘Interest

Offset’ must equal the amount of the offset collections included in the

amount reported on Line 1, page 4/4, Form CMS-1522 and included in

the amount of the offset reported on Line 4b, Form CMS 751 for the

quarter ending June 30, 2005.

Line 7 – The sum of Line 5 minus (-) Line 6 equal (=) Monthly Interest Cash

Collections.

Line 8 – Monthly Interest Cash Collections = Line 7.

Line 9 – The sum of Line 4 (Total Monthly Deposits) minus (-) Line 8 Monthly

Interest Cash Collections) = Total Monthly Principal Cash Deposits.

B. Calculate HI/SMI Percentage Split (FI Only) – 12 month rolling average

Line 10 – Enter the sum of Line 4a (principal), Form CMS-751A (quarter ending

June 30, 2005). For example, Line 4a (principal) for the period ending

June 2005 plus (+) [Line 4a (principal), Form CMS-751A (period

ending September 2004) minus (-) Line 4a (principal), Form CMS-

751A (period ending June 2004)]. The sum of Line 4a (period ending

September 2004) minus Line 4a (period ending June 2004) must equal

Cash Collections for the period July 2004 – September 2004.

(NOTE: 12 months of most recent HI principal Cash Collections (e.g., July

2004 - June 2005))

Line 11 - Enter the sum of Line 4a (principal), Form CMS-751BA (quarter ending

June 30, 2005). For example, Line 4a (principal) for the period ending

June 2005 plus (+) [Line 4a (principal), Form CMS-751BA (period

ending September 2004) minus (-) Line 4a (principal), Form CMS-

751BA (period ending June 2004)]. The sum of Line 4a (period ending

September 2004) minus Line 4a (period ending June 2004) must equal

Cash Collections for the period July 2004 – September 2004.

(NOTE: 12 months of most recent SMI principal Cash Collections (e.g., July

2004 - June 2005))

Line 12 – Enter the sum of Line 10 plus (+) Line 11 = Total HI/SMI collections.

Line 13 – Enter the HI percentage split. The result of Line 10 divided by Line 12.

Line 14 – Enter the SMI percentage split. 1.00 minus the HI percentage split

(Line 13).

(NOTE: Line 14 must equal Line 11 divided by Line 12)

C. HI Monthly Cash Deposit = HI percentage split (Line 13) multiplied by Total

Monthly Principal Cash Deposit (Line 9).

D. SMI Monthly Cash Deposit = HI percentage split (Line 13) multiplied by Total

Monthly Principal Cash Deposit (Line 9).

E. The Chief Financial Officer (CFO) is required to certify/sign the Medicare

contractor Cash Collection Worksheet Attachment I (electronic signature is

acceptable if the email is sent by the CFO), as an indication of the

correctness/completeness of the data in accordance with applicable instructions.

(NOTE: The sum of C and D must equal Total Monthly Principal Cash Deposits

(Line 9))

90 - Intermediary Benefit Payment Report (Form CMS-456) – (Rev. 5,

08-30-02)

A1-1414

90.1 - Purpose and Scope - (Rev. 5, 08-30-02)

A1-1414.1

The Intermediary Benefit Payment Report (IBPR) is a report of current monthly

information that covers the categories of benefits the contractor paid and selected

statistical data that relates to those payments. CMS uses this data to:

Track benefit payments by type of provider to detect significant shifts in program

expenditures;

Monitor implementation of new programs, e.g., hospice benefits, and comprehensive

outpatient rehabilitation benefits; and

Identify operation problem areas for resolution by the contractor or CMS.

90.2 - Due Dates and Transmittal - (Rev. 5, 08-30-02)

A1-1414.2

Contractor shall input the reports accompanying the reconciliation between IBPR and the

Monthly Intermediary Financial Report (Form CMS-1522) into the CAFM system 20

work days following the report month.

90.3 - Verification of Data - (Rev. 5, 08-30-02)

A1-1414.3

The various subsidiary records that include the individual provider files must support the

data entered on the report.

The contractor must have the capability to trace all data entered on the report to the

individual provider files.

Where applicable, the Provider Statistical and Reimbursement Report and other provider

reports containing benefits paid data must support the data on the report.

90.4 - Accuracy of Data Contained on Report and Reconciliation of

Data Reflected on Monthly Intermediary Financial Report (Form CMS-

1522) - (Rev. 5, 08-30-02)

A1-1414.4

The contractor must ensure that all data reflected on the report is accurate.

Line 36, column (g) of the report, should equal the amount shown on the CMS-1522,

column (d), lines 1 and 2 in the aggregate. In the event that the amounts do not agree, the

contractor shall complete a reconciliation report.

90.5 - General Reporting Instructions - (Rev. 5, 08-30-02)

A1-1414.5

Where money is withheld from payments due the provider (as an offset) for monies due

the contractor, the contractor shall show the gross amount (less any deductibles,

coinsurance, interest, or sequestration) as the payment on the appropriate line and

column. It shall show the offset as a negative amount in its appropriate line and column.

For example, when the contractor reduces a PPS Periodic Interim Payment (PIP) for a

settlement amount due from the provider, it shall record the gross PIP amount (less any

deductibles, coinsurance, interest, or sequestration) on line lA in column 1 (a) or 1(b), as

appropriate. It shall record the offset on line 6B in column 1(a) or 1(b), as appropriate.

However, it shall record a claim adjustment (e.g., a PRO disallowance or subsequent

reversal) as a reduction of claims payments on line 2A for a non-PIP/PPS hospital.

Where the contractor makes an accelerated payment and the provider repays a portion of

the accelerated payment during the same reporting period, the contractor shall show the

net amount on the appropriate line and column.

For example, when an accelerated payment of $100,000 is made to a provider during the

period, and the provider repays $30,000 during the same period, the contractor shows

$70,000 as the net accelerated payment.

In situations where an accelerated payment is made during the period, and the contractor

recovers a portion of the accelerated payment through reduction of interim payments, it

shall show the gross amount (less any deductibles, coinsurance, interest, or sequestration)

of interim payments as payment on the appropriate line and column. It shall show the

offset amount as a negative amount on the appropriate line and column.

For example, when an accelerated payment is made for $100,000 and later in the month

$30,000 of the accelerated payment is recouped by offset against PPS/PIP amounts of

$150,000 paid to the provider, the contractor shows the $150,000 gross PPS/ PIP amount

on line 1A in column 1(a) or 1(b), as appropriate. It shows a net accelerated payment of

$70,000 ($100,000-$30,000) on line 7 in column 1(a) or 1(b), as appropriate.

90.6 - Instructions for Completion of the IBPR - (Rev. 5, 08-30-02)

A1-1414.6

A. Heading

The contractor enters its name and assigned number. Multi-regional intermediaries use

the number assigned to the home office for administrative budget and cost reporting

purposes. The contractor shall furnish a consolidated report for all locations.

The contractor enters the calendar month and year as a four-digit entry, e.g., 1000, 1100,

1200, 0101.

B. Column Definitions - Page 1

Column (a) - Single Facility - refers to payments to PPS hospitals that do not have

distinct part facilities, such as SNFs, HHAs, psychiatric units, or rehabilitation units.

• Column (b) - Facility With Distinct Parts - refers to payments to PPS hospitals

that include distinct parts, such as SNFs, HHAs, psychiatric units, or

rehabilitation units.

NOTE: The contractor enters non-PPS payments to the distinct part on the appropriate

line and column of page 2.

• Column (c) - Non-PPS Payment - refers to payments to the following:

o Hospitals excluded from PPS (e.g., psychiatric, children's, rehabilitation

and long term);

o Hospitals receiving payments via an alternative payment program (waiver

States);

o Hospitals yet to be phased into PPS; and

o PPS hospitals for bills or underpayments applicable to pre-PPS fiscal

years.

• Column (d) - Total - refers to the total of columns (a), (b), and (c).

C. Line Item Definitions - Page 1:

1. Hospital Inpatient (PIP) - refers to hospitals paid by the PIP method. The

contractor shall show these figures less any deductibles, coinsurance, and interest

for all items on the PIP bills and any sequestration applicable to this line with any

offsets shown on line 6A or 6B.

A. Inpatient Operating Payments - refers to the amount of the PIP that covers

items that would otherwise be paid on a per claim basis plus those items

paid on a per claim basis in addition to PIP payment. (Such as payments

for outliers and hemophilia blood clotting factor add-on.)

The contractor enters the PIP amounts paid as follows:

PPS Provider Payments - Payments related to services furnished after

conversion to PPS in columns 1(a) or 1(b), as applicable. This includes outlier

payments, hemophilia blood clotting factor add-on payments, disproportionate

share amounts, indirect medical education, ESRD payments, and phased-in

capital-related costs during the transition period. Non-PPS Provider Payments

- column (c) - Payments related to services furnished prior to conversion to

PPS. Payments to all providers listed in the definitions for column (c).

B. Pass Through Costs - Contractor enters the PIP payments, including any

withholdings, but less any sequestration amounts for items paid on a

reasonable cost basis as follows:

• Capital;

• Direct medical education which includes nursing and paramedical

health professional (allied health) programs and graduate medical

education;

• Kidney and other organ acquisitions;

• Bad debts; and

• Nonphysician anesthetists.

NOTE: This includes that part of capital-related costs not included in line

1A.

C. Indirect Medical Education - Contractor enters the PIP payments for the

indirect medical education adjustment, whether on a PIP or a claim-by-

claim basis for PIP providers, less any sequestration (already included in

line 1A).

NOTE: Contractor shall make entries on this line for memorandum purposes

only to identify the amount of indirect medical education for PIP hospitals.

2. Hospital Inpatient (Non-PIP), refers to hospitals paid based upon bills reviewed

and approved. Contractor shall show total payments less any reductions on line

6A or line 6B.

A. DRG Bills Paid/Non-DRG Bills Paid - Contractor enters the calculated

payment less any deductibles, coinsurance, and interest for all items on the

bill and any sequestration applicable to this line. It shall include payments

for outliers, disproportionate share, indirect medical education, high

percentage of end-stage renal disease beneficiary discharges, and

hemophilia blood clotting factor add-on payments on a claim-by-claim

basis. Also, it shall include phased-in capital-related costs during the

transition period.

For DRG bills, it shall use columns (a) and (b). For non-DRG bills paid, it

shall use column (c).

It shall report all retroactive adjustments pertaining to hospitals on line 6A or

6B.

B. Pass Through Costs - The contractor enters the interim payments, less any

sequestration, for items paid on a reasonable cost basis as follows:

• Capital;

• Direct medical education which includes nursing and paramedical

health professional (allied health) programs and graduate medical

education;

• Kidney and other organ acquisitions;

• Bad debts; and

• Nonphysician anesthetists. NOTE: This includes that part of the

capital-related costs that are not included in line 2A.

C. Indirect Medical Education - Contractor enters the interim payments for

the indirect medical education adjustment (already included in line 2A).

NOTE: Contractor shall make entries on this line for memorandum purposes only to

identify the amount of indirect medical education for non-PIP hospitals. It shall not

adjust these amounts for MSP or sequestration.

3. Outlier Payments - Contractor enters additional amounts paid for outlier cases.

NOTE: Contractor shall make entries on this line for memorandum purposes only to

identify the total outlier payments that are found in the UB82 billing form in Locator 46-

49 in Value Code 17. These amounts are already included in the amounts recorded on

lines lA and 2A.

A. Days - The contractor enters additional payments made as a result of the

length of stay exceeding the day outlier threshold criteria. It shall make

entries on this line for memorandum purposes only. These are non-add

items.

NOTE: After FY 1997, outlier days no longer exist.

B. Cost - The contractor enters additional payments made for claims where

extraordinary costs were approved. It shall make entries on this line for

memorandum purposes only. These are non-add items.

4. Subtotal - Contractor enters the total of the amounts on lines 1A, 1B, 2A, and 2B.

NOTE: The amounts included in lines 1C, 2C, 3A and 3B are memo entries only and

have been included in lines 1A, 1B, 2A and 2B.

5. Outpatient Payments - Contractor enters the payment, less deductibles,

coinsurance and sequestration for outpatient and Part B inpatient services. It shall

report any offset against these amounts on line 6A or 6B. See line 19 for reporting

SNF outpatient payments.

6. Retroactive Adjustments:

• PPS Provider Payments - Contractor enters on lines 6A and 6B (as

applicable), columns (a) or (b), the net amount of retroactive adjustments

paid and received as a result of interim rate adjustments, pass through cost

adjustments, and cost report settlements applicable to current or prior

provider fiscal years.

Contractor shall show interest on cost report overpayments and late-filed cost

reports on these lines. An example of a proper recording of a retroactive

adjustment would be an entry of $500,000 of cash received from the provider

as the first installment of the final settlement of $1,000,000 due the program

from the prior year's cost report.

Another example would be an entry of $500,000 offset against current PIP

payments due of $1,000,000. (The $1,000,000 would be shown on line 1A.)

• Non-PPS Provider Payments - Contractor enters on line 6A or 6B (as

applicable) in column (c) the net amount of retroactive adjustments paid

and received as a result of interim rate adjustments and cost report

settlements applicable to current or prior provider fiscal years.

It shall show interest on cost report overpayments and late-filed cost reports

on these lines.

7. Accelerated Payments - Contractor enters the net amount of accelerated payments

made to and collected from hospitals and distinct part units. (See §160.5 for an

explanation of the appropriate recording of offsets.)

8. Total - The contractor enters the total of lines 4 through 7.

D. Statistical Data-Hospitals-Page 1:

9. PIP:

A. Contractor enters the total number of bills processed for hospitals paid by

the PIP method.

B. Contractor enters the dollar amount that would have been paid if the bills

processed were not subject to PIP in accordance with the definition of line

2A.

10. Non-PIP - Contractor enters the total number of bills for hospitals paid on a

submitted-bill basis.

11. Number of Hospitals - Contractor enters the total number of hospitals

participating in the Medicare program.

12. Number of Admissions - Contractor enters the total number of admissions the

Common Working File (CWF) has approved for payment.

13. Number of Discharges - Contractor enters the number of discharge bills processed

during the reporting month.

14. Number of Readmissions - Contractor enters the total number of readmissions to a

hospital within 7 calendar days of discharge from an acute care facility.

15. Number of Transfers - Contractor enters in column (a) and column (b) the total

number of transfers to a PPS hospital. It enters in column (c) the total number of

transfers to a non-PPS hospital.

16. Outlier Bills:

A. Days - Contractor enters the total number of day outlier bills paid that

relate to the dollar amounts shown in line 3A.

NOTE: Outlier days have been obsolete since the end of FY 1997.

B. Costs - Contractor enters the total number of cost outlier bills paid that

relate to the dollar amounts shown in line 3B.

17. Outpatient - Contractor enters the total number of outpatient bills and Part B

inpatient bills paid that relate to the dollar amounts shown in line 5.

E. Column Definitions - Page 2

• Column (e) - Single Facility - Refers to all providers that are not part of a hospital

complex.

• Column (f) - Part of Hospital Complex - Refers to providers that are an integral

part of a hospital and are operated with other departments of the hospital under

common licensure and governance.

• Column (g) - Total - Refers to total of columns (e) and (f).

F. Line Item Definitions - Page 2

Skilled Nursing Facilities - Including swing bed payments for SNF care.

18. PIP - Contractor enters all PIP payments made to SNFs. It enters total payments

(less any deductibles, coinsurance, interest or sequestration) with any withholding

reductions being shown on line 20.

19. Bills Paid - Contractor enters total payments less any deductibles, coinsurance,

interest, or sequestration with any withholdings shown on line 20. It enters the

calculated payment, less any deductibles, coinsurance and interest for all items,

and any sequestration applicable to SNFs on a submitted-bill basis. It shall

include Part A and Part B services.

20. Retroactive Adjustments - Contractor enters the net amount of retroactive

adjustments paid and received as a result of cost report settlements and lump sum

interim rate adjustments made in prior or current provider fiscal years.

21. It shall show interest on cost report overpayments and late-filed cost reports on

this line. An example of a proper recording of a retroactive adjustment would be

an entry of $500,000 cash received from the provider as the first installment of the

final settlement of $1,000,000 due the program from the prior year's cost report.

22. Accelerated Payments - Contractor enters the net amount of accelerated payments

made to and collected from SNFs. (See §160.5) for an explanation for reporting

accelerated payments.)

23. Total SNF Payments - Contractor enters the total of lines 18 through 21.

Home Health Agencies:

23. PIP - Contractor enters all PIP payments made to HHAs including SNF-based.

24. It shall show total payments less any deductibles, coinsurance, interest, or

sequestration with any withholding reductions shown on line 25.

25. Bills Paid - Contractor shall show total payments (less any deductibles,

coinsurance, interest, or sequestration) with any withholdings shown on line 25. It

enters the calculated payment, less any deductibles, coinsurance, and interest, for

all items, and any sequestration applicable to HHAs on a submitted-bill basis. It

shall include Part A and Part B services and SNF-based HHAs payments.

26. Retroactive Adjustments - Contractor enters the net amount of retroactive

adjustments paid and received as a result of cost report settlements and lump sum

interim rate adjustments made in prior current provider fiscal years.

27. It shall show interest on cost report overpayments and late-filed cost reports on

this line. An example of a proper recording of a retroactive adjustment would be

an entry of $500,000 cash received from the provider as the first installment of the

final settlement of $1,000,000 due the program from the prior year's cost report.

28. Accelerated Payments - Contractor enters the net amount of accelerated payments

made to and collected from HHAs. (See §160.5) for an explanation for reporting

accelerated payments.)

29. Total HHA Payments - Contractor enters the total of lines 23 through 26.

Additional Providers:

28. ESRD - Contractor shall include in these columns payments to ESRD networks,

as applicable:

Column (e) - It enters net payments to independent facilities. Column (f) - It enters

net payments to hospital-based facilities.

29. Hospice - Contractor enters net payments made to hospices.

30. RHC - Contractor enters net payments made to rural health clinics (RHCs).

31. OPA/HL - Contractor enters net payments made to organ procurement agencies

and histocompatibility laboratories.

32. CORF - Contractor enters net payments made to comprehensive outpatient

rehabilitation facilities (CORFs).

33. Distinct Part Units - Contractor enters net payments made to exempt distinct part

rehabilitation and psychiatric units.

34. All Others - Contractor enters net payments made to other providers not listed in

lines 28 -33.

NOTE: Contractor shall make adjustments, pertaining to providers, identified on lines

28 through 34 directly to the specific line. This includes checks received and offsets or

withholdings.

35. Total - Contractor enters the total of lines 28 through 34.

36. Grand Total - Contractor enters the total of lines 8(d), 22(g), 27(g) and 35(g).

G. Statistical Data - Page 2:

37. SNF:

• Number of SNFs - Contractor enters the total number of participating

SNFs.

• Number of Admissions - Contractor enters the total number of SNF

admissions.

38. HHA:

• Number of HHAs - Contractor enters the total number of participating

HHAs.

• Number of Bills - Contractor enters the total number of bills processed.

(Audit intermediaries should not complete this line.)

39. Number of Transfers to Distinct Part Units - Contractor enters the total number of

transfers to distinct part units for which payments are shown in line 33.

It shall use edit checks to ensure completeness, arithmetical accuracy, and to discover

inconsistencies. It shall have an authorized official sign and date the report.

90.7 - Form CMS-456 - Schedule R - (Rev. 5, 08-30-02)

A1-1414.7

(Page 3 of 3 of the Monthly Intermediary Benefit Payment Report) Reconciliation

Between IBPR and CMS-1522.

A. Purpose and Scope

The contractor shall use the Schedule R to account for any variances between line 36(g),

Total on the IBPR, and the HI and SMI Benefits reported on lines 1(d) and 2(d) of the

CMS-1522 Report.

Schedule R is an integral part of the IBPR and must be completed each month whether or

not a variance exists between the IBPR and the CMS-1522 Report. If there is no variance,

the contractor shall complete line 36(g) of the IBPR and HI and SMI Benefits for lines

1(d) and 2(d) of the Form CMS-1522. If there is a variance, it shall reconcile the two

reports by completing the appropriate lines.

It must have the capability to substantiate all amounts reflected on Schedule R.

Schedule R includes line items that will facilitate the contractor's reconciliation process.

It shall input the Schedule R, along with pages 1 and 2 of the IBPR, into the Contractor

Administrative Budget and Financial Management System (CAFM) for each report

month.

B. Instructions for Completion of Schedule R:

Heading - The contractor enters the report month and year. (See §160.6A) for

intermediary name and number.) Also, it enters its current letter-of-credit number.

Line Item Definitions - Schedule R:

CMS-456 (IBPR) Column:

Line 36(g) Total - Contractor enters the amount obtained from page 2 of 3 on line 36(g)

of the IBPR.

Medicare Secondary Payer (Non-Providers Cash Recoveries) - Contractor enters the cash

receipts and offsets applied to claims payments or other refunds that are received from

attorneys, beneficiaries, insurance companies or other non-providers. These amounts

should be negative numbers since they represent cash receipts.

Other Recoveries Identify - Contractor enters recovered or offset amounts not included in

any other line item (lines 1 through 36 or lines 1 and 3 of Schedule R). These amounts

should be negative numbers since they represent cash receipts.

Other Items Identify (Lines 3A through 3E) - Contractor enters any other benefit

payments or refunds not included elsewhere on the CMS-456 or on lines 1 and 2. The

items shown here may be unique to its operation and should be identified accordingly. It

shall itemize each major category on lines 3A. through 3E. These amounts could be

positive or negative numbers.

Total - Contractor enters the sum of all line items in this column. It must take care to

subtract negative amount(s) included on the above lines. The total amount must equal the

amount in the total adjacent CMS-1522 column.

1. Remarks - Contractor enters an explanation to clarify any item or amount.

• Line Item Definitions - Schedule R:

CMS-1522

1. HI Benefits, Line 1 (d) - Contractor enters the HI benefits amount from form

CMS-1522 in line 1(d).

2. SMI Benefits, Line 2(d) - Contractor enters the SMI benefits amount from form

CMS-1522 in line 2(d).

3. Subtotal - Contractor enters the total HI and SMI benefit amounts.

4. Other Items Identify - Contractor enters any other benefit payments or refunds

that may be unique to your operation that are not included on lines 1(d) or 2(d) of

form CMS-1522. It shall itemize each major category and identify on line 1

through 6. These amounts could be positive or negative numbers.

5. Total - Contractor enters the sum of all line items in this column. It must take care

to subtract negative amounts included in items 1 through 6. The total amount must

equal the amount in the total adjacent CMS-456 column.

Public reporting burden for this collection of information is estimated to average 30 hours

per response. This includes time for reviewing instructions, searching existing data

sources, gathering and maintaining data needed, and completing and reviewing the

collection of information. Send comments regarding this estimated burden or any other

aspect of this collection of information, including suggestions for reducing the burden, to:

Centers for Medicare & Medicaid Services

Office of Financial Management

7500 Security Boulevard

Baltimore MD 21244-1850

and to:

Office of Management and Budget

Paperwork Reduction Project (0938-0361)

Washington DC 20503

100 - Issuance of Letter-Of-Credit - (Rev. 5, 08-30-02)

A1-1416, B1-4414

The Letter-of-Credit, Standard Form-1193, authorizes a Federal Reserve Bank or Branch

to advance funds to a designated commercial bank on behalf of CMS. Under the Checks

Paid Method of financing, a letter-of-credit is issued to authorize the designated

commercial bank to withdraw funds for deposit only to the contractor's Benefits Account

when a bank presents a payment voucher (FMS-5401).

Upon receipt of the properly executed signature cards and notification from the Federal

Reserve Bank that the required collateral has been posted, CMS prepares and certifies a

letter-of-credit in favor of the designated commercial bank. The certified letter-of-credit,

together with the executed signature cards, are sent to the Treasury Department for

forwarding to the servicing Federal Reserve Bank or Branch. A copy of the certified

letter-of-credit and signature cards are also sent to the contractor, the RO, and the

designated commercial bank.

100.1 - Monthly Limitation - (Rev. 5, 08-30-02)

A1-1416.1, B1-4414.1

The letter-of-credit specifies a maximum amount of funds that the bank may draw during

each month. The ceiling amount on the letter-of-credit is established at a sufficiently high

level to provide for fluctuations in monthly disbursement patterns and is based upon

benefit payments estimated by CMS and the contractor. The unused portion of the letter-

of-credit is revoked at the end of each month, and the full monthly ceiling amount is

automatically renewed at the beginning of each month. There is no carryover of any

unused ceiling amount. Each month stands by itself.

100.2 - Amending Letter-of-Credit

(Rev. 236, Issued: 06-13-14, Effective: 06-02-14, Implementation: 07-15-14)

All requests for new or amended Letters Of Credit, whether considered routine or

emergency, must be submitted no later than 6 business days prior to the calendar date of

the actual need. All requests must be sent via email to DFSE@cms.hhs.gov; the

appropriate Regional Office (RO) contacts should also be copied on the request.

Conditions requiring new LOCs include but are not limited to:

• A new MAC joins the Medicare program;

• A MAC assumes a new workload from another MAC;

• A complete or partial change in MAC’s name;

• A change in the name of the MAC’s servicing bank; or

• A change in the Federal Reserve Bank or Branch servicing the MAC’s

commercial bank.

Conditions requiring amended LOCs include but are not limited to:

• A permanent increase or decrease in the LOC funding limitation due to significant

change in Medicare workload or expenditure that is expected to affect the MAC’s

financial needs;

• A temporary increase in the LOC funding limitation to cover all Medicare checks

and Electronic Funds Transfer (EFT) payments presented to the bank for payment

within a given month.

100.3 - Establishment of Accounting Records - (Rev. 5, 08-30-02)

A1-1416.3, B1-4414.3

The contractor shall establish adequate accounting records to ensure that:

• The total monetary amount on the payment vouchers issued during the month

does not exceed the monthly limitation established by the letter-of-credit;

• Funds drawn are properly allocated between HI and SMI benefits. The contractor

shall establish memorandum accounts to separate the respective benefit payments;

• Refunds received from providers or beneficiaries resulting from prior

overpayments or retroactive adjustments are immediately deposited into the

FHIBA. The contractor shall credit all such deposits on the day following the date

of receipt in its mail room or initial point of entry. (It shall credit within 2 days if

the bank is not located in the same city as the contractor.); and

• Bank charges for services furnished are in accordance with the contractual

agreement and that the volume by types of service (e.g., checks paid and deposits)

are in agreement with the contractor's records.

110 - Initial Federal Health Insurance Time Account Deposit - (Rev. 5,

08-30-02)

A1-1418, B1-4416

To preclude excessive use of Federal funds, the contractor shall delay the initial deposit

in the Time Account until it has actually started processing checks that are cleared against

the FHIBA. It shall effect the initial deposit of Federal funds into the Federal Health

Insurance Time Account by drawing a check on the new FHIBA payable to the Time

Account.

It shall establish the amount of the initial time deposit check by re-computing the Award

Schedule (AS) (Page 2 of 2) that the selected bank submits to reflect the effective prime

rate (i.e., prime minus one percent) in effect on the date the new accounts are

implementation.

It shall make the check payable to the designated bank with the following directive

clearly printed on the reverse:

For Deposit Only In (Name of Contractor)

Federal Health Insurance Time Account

The contractor shall delay use of the Federal Health Insurance Accounts until the Federal

Reserve Bank has received authorization from the Treasury Department for the

designated commercial bank to process payment vouchers under the letter-of-credit

procedure.

110.1 - Subsequent Time Account Deposits and Adjustments – (Rev. 5,

08-30-02)

A1-1418.1, B1-4416.1

The quarterly review of bank activity in the Benefits Account may disclose the need for

an adjustment in the Time Account balance. When an adjustment is indicated, the

contractor shall make the adjustment within 15 calendar days after the close of the

quarter.

It shall follow the procedures outlined for the initial Time Account deposit as described

in §110 to increase the Time Account balance.

To decrease the Time Account balance, it shall prepare a Time Account withdrawal slip

that instructs the bank to transfer the amount of the required reduction from the Time

Account to the FHIBA.

NOTE: The contractor shall report all initial deposits and subsequent adjustments in the

Time Account balance on form CMS-1522

110.2 - Bank Account Analysis

(Rev. 158, Issued: 09-25-09, Effective: 10-26-09, Implementation: 10-26-09)

To ensure a continuing evaluation of all bank services and associated charges, the

contractor shall adhere to the following procedures:

• Arrange to receive from the bank its account analysis on a regular monthly basis

no later than the 10th of the following month. Bank analysis must include:

o Bank Processing Charges (Schedule of Itemized Bank Services Provided

Report); and

o A list of daily closing bank balances (Recap of Daily Available Balances).

• The contractor shall verify the accuracy of the data presented for the average daily

bank balance, units of service, and all other computations on the bank's account

analysis.

• The contractor shall complete and forward, within 15 calendar days after the end

of each month to CMS electronically (Excel; [email protected];), the

following schedules:

o Monthly account activity of bank processing charges (Schedule of

Itemized Bank Services Provided Report); and

o Recap of Daily Available Balances (Recap of Daily Available Balances).

120 - Reviewing Bank Agreements - (Rev. 5, 08-30-02)

A1-1420, B1-4418

The contractor shall determine if it wants to continue, renegotiate, or terminate the bank

agreement by reviewing the bank's performance and processing charges for the present

term. It shall review 165 days prior to the expiration of the three-party bank agreement.

If the bank's performance is acceptable, and the bank does not request a rate increase, the