1

40

North East Scotland

Pension Fund

Unaudited Annual Report & Accounts

For the period 1 April 2023 to 31 March 2024

2

Contents

Management Commentary ......................................................................................... 3

1. Foreword ................................................................................................................ 3

2. About the North East Scotland Pension Fund ........................................................ 5

3. Administration 2023/24 ........................................................................................... 6

4. Pensions Committee & Pension Board .................................................................. 7

5. Administration and Performance .......................................................................... 14

6. Financial Performance ......................................................................................... 20

7. Economic and Market Background....................................................................... 25

8. NESPF Investment Strategy ................................................................................ 31

9. Risk ...................................................................................................................... 34

10. Funding Strategy Statement ............................................................................... 35

11. Statement of Investment Principles .................................................................... 36

12. Environmental, Social and Governance Issues .................................................. 37

13. Acknowledgement .............................................................................................. 43

Statement of Responsibilities ................................................................................... 44

Annual Governance Statement ................................................................................ 46

Governance Compliance Statement......................................................................... 51

North East Scotland Pension Fund Accounts ........................................................... 53

Notes to the North East Scotland Pension Fund Accounts ...................................... 55

Appendix 1 – Statement by the Consulting Actuary ................................................. 97

Appendix 2 – Schedule of Employers..................................................................... 102

Appendix 3 – Declared Interests ............................................................................ 104

3

Management Commentary

1. Foreword

As Convener of the Pensions Committee, I am pleased to introduce the 2023/24

Annual Report and Accounts which reflects a significant year of both challenges and

achievements.

The continued war in Ukraine, the attacks between Hamas and Israel and the

continued Cost of Living Crisis all dominated the headlines this year and contributed

towards the Fund operating within a fast changing environment.

Despite these challenges, the Fund’s Net Asset Value increased from £5,804m to

£6,237m.This increase is not as a result of any of my own decisions, but rather the

result of good decisions made by our fund managers and by staff at the NESPF.

The Fund’s investment strategy has not only positively impacted the asset value but

funding levels too. The 2023 actuarial valuation saw funding levels increase to 126%,

which further demonstrated the strength and long term security of the Fund.

While financial performance and efficiency is a primary focus, the Fund remains

committed to being a socially responsible investor. In 2023/24, the Fund engaged with

the fund managers to expand their reporting on Environmental, Social and

Governance (ESG) metrics. In the coming year, the NESPF will produce their first Task

Force on Climate Related Financial Disclosures (TCFD) report, which aims to develop

consistent climate related financial risk disclosures.

The NESPF was the first Local Government Pension Scheme (LGPS) in the UK to go

live with the new online member portal, rebranded as My Pension+. With improved

design, usability and enhanced security, the site also brings additional functionality

including personalised Annual Benefit Statement (ABS) videos for active members

produced utilising Artificial Intelligence (AI). The Fund will continue to make best use

of technological advances to improve member experience and services.

From a regulatory and compliance point of view, the long awaited McCloud remedy

came into force in October 2023, which expanded the underpin protection for certain

members. Also, The Pensions Regulator’s (TPR) new General Code of Practice took

effect in March 2024. To ensure we met both these new requirements, the Fund

updated processes, tested system developments and implemented new guidance.

In recognition of all that was achieved, I am delighted that the Fund was shortlisted for

several awards including the LGPS Fund of the Year at the LAPF awards and Defined

Benefit Scheme of the Year at the Pension Age awards. These national awards look

at best practice, performance and innovation and the nominations highlight the Fund’s

accomplishments.

Looking ahead to 2024/25, in addition to the delivery of essential services, the Fund

will proceed with several projects. These include a procurement for a Global

4

Custodian; further improvements to administrative processes; and the introduction of

the Pensions Dashboard (a government initiative that allows the public to see all their

pension savings online and in one single place).

Finally, my sincere thanks to my colleagues on the Pensions Committee and Pension

Board, our advisors and, above all, our staff for their hard work and efforts during the

year.

Councillor John Cooke

Pensions Committee Convener

5

2. About the North East Scotland

Pension Fund

The North East Scotland Pension Fund (NESPF) administers the Local Government

Pension Scheme (LGPS) for employers located throughout the North and North East

of Scotland.

The LGPS is a defined benefit public sector Pension Scheme that was established

under the Superannuation Fund Act 1972. It is one of the main public sector Pension

Schemes in Scotland and provides members with a range of valuable benefits

including an annual pension, lump sum payments and a range of pension provisions

for family and loved ones. The LGPS is administered locally by 11 government

authorities, with Aberdeen City Council acting as the Administering Authority for the

North East.

NESPF has an asset value of £6.2 billion and 77,865 members. It is the third largest

LGPS fund in Scotland.

The Fund has one primary objective; to ensure the payment of pension benefits to our

members both now and in the future. It is this single purpose that drives the Fund’s

long term policies and strategies. To achieve this objective, funds are built up from

contributions from both employees and employing bodies, together with interest,

dividends and rent from our investments.

There are strict rules and legislation which set out how the LGPS, and by extension

the Fund, operate. These include the LGPS (Scotland) Regulations which are Scottish

Statutory Instruments (SSIs) as well as separate regulations that set out Scheme

benefits, investment and governance requirements. These provide assurance for all

members, employers, taxpayers and stakeholders that the Fund operates efficiently

and manages itself to ensure our key objective, paying out pensions, is met.

6

3. Administration 2023/24

Administering Authority Aberdeen City Council

Committees Pensions Committee, Pension Board

Chief Officer – Finance Jonathan Belford

Actuary Mercer

Global Custodian HSBC

Performance Measurement HSBC

Banks Virgin Money* & HSBC

AVC Providers Prudential, Standard Life Assurance

Bulk Annuity Provider Rothesay Life Plc

External Auditor Audit Scotland

Internal Auditor Aberdeenshire Council

Investment Consultant Isio

Legal Adviser Aberdeen City Council

Employers For full details see Appendix 2

*Clydesdale Bank trading as Virgin Money

7

4. Pensions Committee & Pension

Board

Pensions Committee

While day to day administration of the Pension Fund is the duty of Pension Fund staff,

decision making and overall responsibility has been delegated to the Pensions

Committee by Aberdeen City Council.

The Pensions Committee carries out a role similar to that of trustees of a Pension

Scheme. It is the key decision maker for all matters under LGPS Regulations including

benefit administration and investment management.

As a public sector pension provider, both the Council and the Pensions Committee

recognise that they have fiduciary duties and responsibilities not only towards Pension

Scheme members and participating employers but to local taxpayers.

The Committee meets on a quarterly basis to address a range of matters such as risk

management, administration, funding, investment strategy and performance.

The Committee consists of nine elected members of Aberdeen City Council each with

equal voting rights. Following a full Council meeting in February 2024, the number of

Committee members was reduced from 13 to 9. As at 31 March 2024, the Committee

had two vacancies.

8

Membership 2023/24

Name

Member as

at

31 March

2023

Joined

Left

Member

as at

31 March

2024

Cllr John Cooke

Yes

Yes

Cllr Neil MacGregor

Yes

Yes

Cllr Dell Henrickson

Yes

Yes

Cllr Alison Alphonse

Yes

Yes

Cllr Sarah Cross

Yes

21/02/2024

Cllr Derek Davidson

Yes

Yes

Cllr Duncan Massey

Yes

Yes

Cllr Ciaran McRae

Yes

13/02/2024

Cllr Christian Allard

Yes

13/02/2024

Cllr Jennifer Bonsell

Yes

27/04/2023

Cllr Kairin van Sweeden*

07/06/2023

Yes

Cllr Alex McLellan

07/06/2023

13/02/2024

Total

10

2

(5)

7

Notes:

*Councillor van Sweeden resigned from the Pensions Committee on 12 October 2023

and was re elected on 14 December 2023.

Meeting Attendance in 2023/24

Name 23/06/23 15/09/23 15/12/23 22/03/24

Overall

Attendance

Cllr John Cooke

100%

Cllr Neil MacGregor

100%

Cllr Dell Henrickson

100%

Cllr Alison Alphonse

X

X

50%

Cllr Sarah Cross

N/A

100%

Cllr Derek Davidson

100%

Cllr Duncan Massey

X

75%

Cllr Ciaran McRae

N/A

100%

Cllr Christian Allard

N/A*

N/A

100%

Cllr Jennifer Bonsell

N/A

N/A

N/A

N/A

100%

Cllr Kairin van

Sweeden

100%

Cllr Alex McLellan

**

N/A

100%

9

Notes:

* Councillor Allard did not attend the meeting on the 23 June as he was missed from

the original invitation in error.

**Councillor McLellan sent Councillor Delaney as a substitute.

Pension Board

In line with Scheme regulations, the Fund established a Pension Board in 2015/16.

The Board’s primary function is to ensure that the Fund complies with regulations and

meets the requirements of The Pensions Regulator. In doing so, the Board ensures

the Fund operates in accordance with the law, securing the effective and efficient

governance and administration of the Scheme.

Board membership comprises of eight members, four trade union representatives and

four employer representatives appointed from Councils and Scheduled or Admitted

Bodies. The Pension Board membership is shown below;

Membership 2023/24

Membership

Name

Member

as at

31

March

2023

Joined

Left

Member

as at

31

March

2024

Unison

Morag

Lawrence

(Chair)*

Yes

Yes

Aberdeenshire

Council

Cllr Stephen

Smith (Vice

Chair)

Yes

Yes

Aberdeen City

Council

Cllr Jessica

Mennie

Yes

Yes

The Moray

Council

Cllr Graham

Leadbitter

Yes

15/12/2023

No

The Moray

Council

Cllr David

Gordon

19/12/2023

Yes

First Bus

Ian Hodgson

Yes

22/09/2023

No

Robert Gordon

University

Jeremy

Lindley

15/02/2024

Yes

GMB

Neil Stirling

Yes

Yes

UCATT

Gordon

Walters

Yes

Yes

Unite

Alan Walker**

Yes

Yes

Total

8

2

(2)

8

10

Notes:

* Morag Lawrence was reappointed to the Pension Board on 13 February 2024.

** Alan Walker was reappointed to the Pension Board on 24 January 2024.

Meeting Attendance in 2023/24

Name 23/06/23 15/09/23

25/09/23*

15/12/23 22/03/24

Overall

Attendance

Morag

Lawrence

**

100%

Cllr Stephen

Smith

100%

Cllr Jessica

Mennie

***

100%

Cllr Graham

Leadbitter

N/A

100%

Cllr David

Gordon

N/A

N/A

N/A

****

100%

Ian

Hodgson

X

N/A

N/A

N/A

50%

Jeremy

Lindley

N/A

N/A

N/A

N/A

X

0%

Neil Stirling

100%

Gordon

Walters

X

80%

Alan Walker

100%

Notes:

* Pension Board additional meeting.

** Morag Lawrence sent Kenny Luke as a substitute.

*** Councillor Mennie sent Councillor Neil Copland as a substitute.

**** Councillor David Gordon attended the meeting on 15 December 2023 in an

observing role.

Apart from the Pension Board’s Annual Meeting, the Board sits at the same time as

the Pensions Committee. To further enhance transparency and openness, both the

Board and Committee receive the same reports for each meeting. These reports

include information on all areas of the Pension Fund; Investment, Accounting,

Governance, Employer Relationship, Administration and Systems.

11

In assisting with compliance, the Board can report the Fund to The Pensions Regulator

for non compliance with guidance or regulations. In 2023/24 no issues were reported

by the Board to The Pensions Regulator.

The Annual Report of the Pension Board, which reviews its activity for the year, is

available on our website: www.nespf.org.uk.

Conflicts of Interest

The Fund maintains a ‘Conflicts Register’ to record and monitor all potential or actual

conflicts noted prior to or during Pension Committee and Board meetings.

A 'Declaration of Interest' form is completed every 12 months and individuals confirm

that the information submitted is complete, accurate and is to the best of their

knowledge.

In terms of management, where an actual conflict of interest arises the following

option(s) exist:

• a member can withdraw from the discussion and decision making process;

• the Pension Board can establish a sub board to review the issue (where the

terms of reference give the power to do so); or

• if the conflict is so fundamental that it cannot be managed in any other way,

the member can resign.

Pensions Committee members are governed by the national Councillors’ Code of

Conduct. Training on the Code of Conduct was delivered by Aberdeen City Council in

May 2022. Full list of each member’s interests can be found on the Aberdeen City

Council website: https://committees.aberdeencity.gov.uk/mgMemberIndex.

Committee and Board Training 2023/24

Pensions Committee members are not legally obliged to undertake training. The Fund

feels strongly that Committee members should receive training to ensure that they

have the necessary level of knowledge and understanding to exercise their functions.

Whereas for the Board, the Public Service Pensions Act 2013 requires that members

have an appropriate level of knowledge and understanding in order to carry out their

role. The agreed Training Plan for both Committee and Board members has an

expectation that members maintain their level of knowledge and training throughout

the year. Recording and monitoring of attendance at meetings or training events

ensures the requirements of the Training Plan are met.

At the June 2019 meeting the Pensions Committee and Pension Board agreed to

undertake the online Public Service Toolkit produced by The Pensions Regulator.

The Training Report and Training Policy was approved at the June 2022 Pensions

Committee. It was recommended that Committee and Board members work through

12

and complete the Hymans LGPS Online Learning Academy (LOLA), and on an

ongoing basis thereafter as new versions were delivered.

Pensions Committee - Mandatory Training Record as at 31 March 2024

Name

Hymans

Robertson

LOLA

Version 1.0*

Hymans

Robertson

LOLA

Version 2.0*

TPR

Toolkit

Attended

Cllr John Cooke

3/3

Cllr Neil MacGregor

2/3

Cllr Dell Henrickson

3/3

Cllr Alison Alphonse

0/3

Cllr Derek Davidson

0/3

Cllr Duncan Massey

2/3

Cllr Jennifer Bonsell

1/3

Cllr Kairin van

Sweeden**

0/2

Cllr Sarah Cross**

1/3

Cllr Alex McLellan**

0/2

Cllr Ciaran McRae**

0/2

Cllr Christian Allard**

0/2

Pension Board - Mandatory Training Record as at 31 March 2024

Name

Hymans

Robertson

LOLA

Version 1.0*

Hymans

Robertson

LOLA

Version 2.0*

TPR

Toolkit

Attended

Morag Lawrence

2/3

Cllr Stephen Smith

1/3

Cllr Jessica Mennie

0/3

Cllr Graham

Leadbitter

0/3

Cllr David Gordon**

1/2

Ian Hodgson

0/3

Jeremy Lindley**

0/2

Neil Stirling

3/3

Gordon Walters

1/3

Alan Walker

3/3

Notes for Committee and Board tables above:

* Hymans Robertson LOLA Version 1.0 24 June 2022 to 23 April 2023

Version 2.0 24 April 2023 to 31 March 2024

** Leavers/joiners during the year

13

In addition to the mandatory training, the Pensions Committee and Board were offered

25 additional training opportunities including:

• Introduction training delivered by Laura Colliss, Pensions Manager, for all

new Committee and Board members;

• A variety of webinars covering topics from industry experts such as:

- Pension Dashboards;

- Cyber Risk;

- Investment Markets;

• Actuarial training delivered by Mercer;

• The NESPF Finance Forum.

Members had the option to complete further additional training courses outwith those

advertised, if they so wished.

14

5. Administration and Performance

Digital Developments

A primary focus for the NESPF throughout the course of 2023/24 was the development

of our new member self service portal.

Following an internal administration review in 2022, the NESPF placed focus on

making advancements to its systems and processes. This coincided with the

introduction of software developer, Heywood Pension Technologies’ (HPT) new

member portal and upon seeing the potential opportunities this could bring, NESPF

volunteered to be an early adopter.

Working closely alongside Heywood, the Fund commenced its journey, that included

extensive testing, to implement a new intuitive platform, My Pension+, which went live

in June 2023. The NESPF was the first LGPS in the UK to go live with the platform.

My Pension+ offers an entirely fresh look, with enhanced technologies that vastly

improve functionality across the site. Some of the primary developments include:

• Simpler login, without the requirement of usernames and security questions;

Members can use their email address and password to access;

• Enhanced security with two factor authentication;

• Simplified navigation and design built with users in mind which incorporates

best User Experience (UX) practices;

• Retirement forecasting tools;

• Personalised explanatory videos for complex topics, e.g. Annual Benefits

Statements.

Although the new portal is now live, it remains a hybrid system. Not all features of the

previous member portal have been developed for My Pension+, with the site linking

back to the old portal for specific functionality. As such NESPF and HPT will continue

to work closely as the remaining functionality is built, with feature parity the primary

focus in 2024/25. In addition to the development of outstanding functionality, further

innovative developments on the horizon include:

• Electronic Identification verification which will allow members to verify their

identity when registering, removing the need for Fund intervention and

reducing registration lead time;

• SMS multi factor authentication;

• Fully digital, online retirement and refund processes.

15

Digital Engagement

The delivery of My Pension+ to the Fund’s membership was coordinated to coincide

with the publication of our Annual Benefit Statements. This resulted in the migration of

thousands of members to the new site and six months after the launch, over 12,500

members had registered, with a staggering 15% increase in site usage compared to

the prior year.

Registration and migration statistics as at 31 March 2024 are displayed below:

Registered

for My

Pension+

%

Members

Registered

Migrated to

My Pension+

%

Members

Migrated

Active

15,717

63.0%

7,632

48.6%

Deferred

9,948

59.1%

3,748

37.7%

Pensioners & Dependants

8,675

35.5%

2,540

29.3%

Annual Benefit Statements

Annual Benefit Statements (ABS) in 2023 were delivered online as per previous years,

however the medium of Active and Deferred statements differed. Deferred members

were able to view an ABS document that had been generated onto their record which

they could then download.

However for active members, with the implementation of My Pension+, we were able

to provide ABS via a newly designed, regulatory compliant ABS webpage which

delivers information in a easy to understand and visually engaging way. As part of the

revised ABS area, each active member can access a personalised video, outlining key

figures and information in a conversational and user friendly manner. Deferred

members will have a similar ABS page available to them ahead of their 2024

Statements.

A key advantage of using digital statements is that it allows us greater performance

monitoring. Through website analytics, ABS email testing and establishing key

performance indicators such as open and click through rates of email campaigns, the

Fund can gain a better understanding of its membership and their behaviours and thus

modify its approach to maximise engagement with them.

The overall percentage achieved for providing Annual Benefit Statements to more than

45,000 active and deferred members prior to the 31 August deadline was 99.78%

(98.31% 2022/23).

16

Pension Administration Strategy (PAS)

In December 2022 a revised PAS was approved by the Pension Committee following

a full consultation. The aim of the PAS is to aid the delivery of high quality pension

administration for the members of the Fund on behalf of its participating employers.

The underlying objectives are:

• To provide high quality pension service delivery;

• Paying pensions and calculating benefits due accurately and on time;

• Good working relationships between the NESPF and its participating

employers;

• Delivery of the LGPS requirements in line with the Scheme regulations;

• Compliance around the Codes of Practice put in place around service delivery

and service standards.

Processing Performance

Key performance

measurement

Target

Work

Volume

Target

Achieved

2023/24

2022/23

Letter notifying death in

service to dependant

5 days

45

39

87%

82%

Letter notifying retirement

estimate

10 days

496

478

96%

95%

Letter notifying actual

retirement benefit

10 days

1,738

1,596

92%

90%

Letter notifying deferred

benefit

10 days

1,980

1,875

95%

96%

Letter notifying amount of

refund

10 days

1,178

1,157

98%

98%

Letter detailing transfer in

quotes

10 days

176

122

69%

68%

Letter detailing transfer out

quotes

10 days

544

303

56%

63%

Total

6,157

5,570

91%

91%

This year saw similar performance to 2022/23 with the overall percentage achieved

above 90% for the second consecutive year.

Actual retirement benefit percentage continues to increase and the number of

retirement estimate requests continues to fall as members choose to self serve online

through My Pension+. Bulk automated processing of deferred benefits for members

with Care only service increased to almost 1,000 and continues to deliver efficiency

savings.

Transfer processing proved difficult with cases having to be stockpiled from

announcement of SCAPE rate change on 29 March 2023 until new factors delivered

17

in July 2023 and for cases impacted by McCloud from the date regulations came into

force on 1 October 2023 until new guidance was received in March 2024.

McCloud Remedy

In December 2018, the Court of Appeal ruled in McCloud v Ministry of Justice that

transitional protection offered to some members as part of pension reform amounted

to unlawful discrimination. In July 2019 following employment tribunal Government

stated difference in treatment would be remedied across all public sector Schemes.

This became known as the McCloud remedy with the LGPS (Remediable Service)

(Scotland) Regulations 2023 coming into force on 1 October 2023.

Communications were issued in December 2023 to eligible members advising that

there was no requirement to do anything whilst the Fund recalculates their benefits. In

February 2024 recalculations for 15,227 members identified a total cost of £6,900 for

pension and death benefits paid out during the remedy period from 1 April 2015 to 31

March 2022, work is underway to rectify the underpayments.

Delivering the remedy has been challenging, initially the Fund worked closely with

employers to identify any missing or incorrect data during the remedy period and this

resulted in 3,781 updates to the pensions administration system. The 18 month delay

between draft and final regulations caused issues with software already delivered

which had to be amended and re delivered in additional releases. Despite all this the

majority of work required to comply with the regulations has been completed.

Employer Data Provision

Throughout the year, good quality, timely data for all active members was provided by

the participating employers of the NESPF through the secure online portal, i-Connect.

The information uploaded monthly directly updates our member database with

starters, leavers, contributions and pay information and ensures that each members

personal details are kept up to date.

More than 1 million data events have been uploaded to the pension administration

system in 2023/24.

The use of i-Connect for data collection has provided substantial benefits to the fund

over the last few years ensuring that the Fund is in the best position to meet the

administrative and regulatory requirements of the Scheme.

The benefits include:

• Reduced administrative burden for day to day processing, contribution

reconciliation and preparations needed in advance of issuing annual benefit

statements;

• Improved data quality allowing the Fund and the participating employers to

have confidence in the triennial valuation results;

18

• Members have access to up to date information on their individual records

through My Pension+;

• Significant advantages in respect of the future challenges faced by the Fund

around being dashboard ready, applying the McCloud remedy and other

regulatory requirements.

The Fund continues to engage with participating employers, the system provider and

other pension funds around the development of i-Connect to ensure it continues to

deliver data requirements of the ever changing LGPS.

Data Quality

The Fund holds a vast amount of data on our pension administration system. This

database holds individual records for each contract of employment for all members

including active, pensioner and deferred members. The quality of the data held in

relation to these member records directly impacts on all aspects of Fund administration

including the calculation of benefits, payment of members pensions and the triennial

valuation results.

Due to the method of data collection and the level of checking and reconciliation that

is carried out the information held is consistently of a high quality. This provides

comfort for the Fund, the participating employers and the members around the

accuracy of the benefits held and the funding calculations.

The data quality scores that are provided by the Fund as part of the Pension Regulator

annual Scheme return are determined by our data analysis tool, Insights. Dashboards

and reports allows us to assess the data held against a number of parameters allowing

for direct comparison against previous years and other LGPS funds.

The annual Scheme return scores are as follows:

2022

2023

Target

Common Data

97.9%

98.7%

100%

Scheme Specific Data

99.2%

99.2%

100%

The Fund’s data quality improvement plan is revised annually in an effort to maintain

the high quality of data held and explore options for further improvement. This is

especially relevant with onboarding to the Pension Dashboards ecosystem scheduled

for 2025.

19

Complaints

NESPF aims to demonstrate the highest level of customer service at all times,

however disputes and issues sometimes arise. The Fund takes all complaints

seriously and will attempt to resolve issues in an effective and timely manner.

Complaints are handled in accordance with Aberdeen City Council’s Complaints

Handling Procedure. All complaints the Fund receives are monitored and recorded by

the Governance team in the Complaints Register.

If no resolution is possible at the informal stage, the complaint proceeds to the Fund’s

Internal Dispute Resolution Procedure (IDRP). The IDRP consists of two formal

stages. Stage 1 is dealt with by an independent appointed person. If the complainant

is not satisfied with the appointed person’s decision, the matter proceeds to Stage 2

of the process which is dealt with by the Scottish Ministers.

The table below is an analysis of those complaints received during 2023/24. There

were 11 complaints made during the year. Of the 7 complaints that were within the

Fund's scope to help remedy, all were resolved at the informal stage.

Complaint Analysis

Number of

Complaints

Waiting Time – Correspondence

3

Processing Delay

3

Staff Knowledge

1

No NESPF Power to Remedy

4

Total Complaints

11

Complaints may not always relate to a NESPF decision or process, for example it may

relate to an employer decision, e.g. ill health retirement. In these instances the

complainant may take their complaint directly to the Pensions Ombudsman.

Not included in the above is one prior year complaint, which was submitted to the

Pension Ombudsman Stage during 2023/24. The case is ongoing.

The full complaints procedure and IDRP process is on our website:

https://www.nespf.org.uk/about/complaints.

20

6. Financial Performance

2023/24 at a Glance

£179m

Additions

£231m

Withdrawals

£26m

Management

Expenses

£533m

Net Return on

Investments

£6,237m

Net Assets of the Fund

at the End of the Year

21

Key Statistics

41

Total Number of

Employers

77,865

Total

Membership

1,554

Votes at AGMS

52%

Members

Registered for

My Pension+

42.5

Staff Employed

(FTE)

1,832

Members to Staff

Ratio

22

North East Scotland Pension Fund Financial Summary

From the year 2022/23, the following tables are the merged figures for the NESPF

and ACCTF.

2019/20

£’000

2020/21

£’000

2021/22

£’000

2022/23

£’000

2023/24

£’000

Contributions

Less Benefits and

Expenses paid

Net Additions/

(Withdrawals)

(30,977)

(51,481)

(33,048)

(34,257)

(78,570)

Net Investment

Income

Change in Market

Value

Net Return on

Investment

(71,648)

1,462,128

181,752

(342,832)

532,616

Transfer In of

ACCTF at

Market Value

0

0

0

290,035

0

Revaluation of

Insurance Buy

In Contract

0

0

0

(35,062)

(20,924)

Net Increase/

(Decrease) in

Fund

(102,625)

1,410,647

148,704

(122,116)

433,122

Fund Balance as

at 31 March

(Market Value)

4,366,542

5,777,189

5,925,893

5,803,777

6,236,899

The monies belonging to the North East Scotland Pension Fund are managed entirely

by appointed fund managers and are held separately from any of the employing bodies

which participate in the Fund. The only exception to this is a small investment in

Aberdeen City Council’s Loan Fund, which varies year on year and represents surplus

cash from contributions not yet transferred to the fund managers.

After meeting the cost of current benefits, all surplus cash is invested and the value of

investments is then available to meet future liabilities.

23

Budget

Note

Actual

Spend

2023/24

£’000

Budget or

Forecast

2023/24

£’000

Over or

(Under)

Spend

2023/24

£’000

Administration Expenses

1

3,113

3,032

81

Oversight and Governance

Expenses

2

872

1,119

(247)

Investment Management

Expenses

3

22,039

19,886

2,153

Management Expenses Total

26,024

24,037

1,987

Where the variance is +/- 5%, an explanation is given below:

1. Over spend – Pay award and one off IT costs.

2. Under spend – Although there were increases in the Actuarial Fees and General

Expenses those increases were less than anticipated.

3. Over spend – Upturn in markets and transaction activity.

Membership Statistics

NESPF

2019/20

2020/21

2021/22

2022/23

2023/24

Active

26,275

26,315

26,961

27,751

27,708

Pensioners

22,156

22,692

23,854

26,146

27,171

Deferred

17,965

17,704

18,150

19,379

19,246

Frozen Leavers

3,021

2,664

3,111

3,602

3,740

Total

69,417

69,375

72,076

76,878

77,865

Active membership appears to have remained stable from 2022/23 to 2023/24 and

may reflect the continuing budgetary pressure faced by the Local Authorities as, in

previous years, there has consistently been an increase to the active membership

totals. The number of deferred members has remained consistent indicating that

members accessing their pensions and transferring their benefits have been in line

with the number of leavers. Pensioner numbers have increased in line with previous

years despite the early retirement exercises currently being undertaken by Local

Authorities. Frozen leavers represent the members who have left the Scheme and

have yet to claim their entitlement to a contributions refund or a transfer of their

entitlement.

24

Management Expenses

2019/20

£’000

2020/21

£’000

2021/22

£’000

2022/23

£’000

2023/24

£’000

Administration

1,822

2,236

2,388

2,958

3,113

Oversight and

Governance

422

713

615

743

872

Investment

Management

17,953

23,820

23,901

17,767

22,039

Total

Management

Expenses

20,197

26,769

26,904

21,468

26,024

Unit Cost Per Member

2019/20

£

2020/21

£

2021/22

£

2022/23

£

2023/24

£

Administrative Unit Cost

per Member

26.25

32.23

33.13

38.48

39.98

Oversight and

Governance Unit Cost

per Member

6.08

10.28

8.53

9.66

11.20

Investment Management

Unit Cost per Member

258.62

343.35

331.61

231.11

283.03

Total Cost

per Member

290.95

385.86

373.27

279.25

334.21

Remuneration Report

There is no need to produce a remuneration report as the Fund does not directly

employ any staff. All staff are employed by Aberdeen City Council and their costs

reimbursed by the Pension Fund. The councillors who are members of the Pensions

Committee and the Pension Board are also remunerated by the Council.

Note 22 to the Accounts details the Key Management Personnel. Councillor and senior

employee remuneration is detailed within the Remuneration Report of Aberdeen City

Council’s Financial Statements.

25

7. Economic and Market Background

Global Market

The past financial year was marked by volatility driven by high inflation and rapid

interest rate hikes. The stock market oscillated between fears of recession and hopes

of interest rate cuts as inflation moderated. The market overall rallied with the Morgan

Stanley Capital International All Country World Index (MSCI ACWI) GBP returning

+20.6% as technology stocks, especially those related to Artificial Intelligence (AI),

dominated while the rest of the market took time to catch up. Policymakers were

focused on balancing the risk of recession with persistent inflation. While the Federal

Reserve held rates steady, it signalled the intention to cut rates in 2024. The European

Central Bank (ECB) and Bank of England (BoE) also maintained a cautious stance.

Despite the potential delay in rate cuts, the financial markets continued to post positive

returns, driven by the anticipation of returns from AI in the technology sector and the

performance of value stocks towards the latter part of the period.

US Equities

During the year ending 31 March 2024, the US equity markets experienced a strong

and sustained rally. The S&P 500 index gained 29.88% during the 1 year period, with

high growth stocks leading the way. Last March, exuberance around AI helped the

market shake off the turbulence of the regional banking crisis. The market rally was

driven by positive economic conditions, including the Federal Reserve's expected rate

cut timeline, strong earnings, low unemployment, and high consumer spending. In

terms of index performance, the Russell 1000 Growth index outperformed the Russell

1000 Value index over the 1 year period, on the backs of the “Magnificent Seven” tech

giants (Microsoft, Apple, Nvidia, Amazon, Meta, Tesla, and Alphabet), which

accounted for a significant portion of the growth index returns. While sentiment in the

market shifted positive over the last year with many market participants growing

increasingly bullish in their outlooks, questions remain on the continued growth of

productivity, outlook for inflation and long term effects of higher interest rates.

UK Equities

2023 was another year where markets remained focused on interest rate policy and

inflation, as central banks deliberated on how to respond to a mixed picture from the

inflation data. Central bankers had been quick through the year to reaffirm their

commitment to curbing inflation, highlighting the need for rates to remain elevated

against the backdrop of falling goods inflation, but services inflation remained sticky,

driven by tight labour markets. Further volatility was sparked through the year, first as

the collapse of Silicon Valley Bank and Signature Bank led to concerns of a banking

26

crisis in the US. This was shortly followed by a disruption in the financial sector in

Europe as Credit Suisse was taken over by UBS in a deal brokered by the Swiss

National Bank. Then followed the rise of AI, with divergence driven by the perceived

beneficiaries versus the victims, and finally the outbreak of war in the Middle East. At

the end of 2023 interest rate expectations fell sharply and risk assets rallied. Global

equity markets rallied at the start of 2024 on strong earnings from technology names,

despite mixed macroeconomic data. The Financial Times Stock Exchange (FTSE) All

Share rose 8.4%, however lagged global equity markets on concerns around growth

in China, notably in the commercial real estate market.

European Equities

European equities delivered very strong returns over the last year, despite a backdrop

of cautious sentiment given concerns over a potential recession, weaker China macro

data and geopolitical risks. The asset class remains under owned by investors and we

observe a generally defensive positioning. European markets particularly started to

rally from November 2023 on into the end of the period as market expectations began

to look past the potential for recession which had clouded sentiment for more than 18

months. This move was supported by a dramatic fall in energy prices in the region,

which had risen because of the Russian invasion of Ukraine, feeding through, amongst

other factors, into lower inflation and an increasing likelihood of cuts to interest rates.

During the most recent earnings season, we noted more companies speaking of

stabilisation and/or potential for improvement, with very clear trajectory for increasing

orders in certain end markets.

Emerging Markets Equities

MSCI Emerging Markets ended the period up 8.5%, materially underperforming

Developed Markets, which gained +25.7%. Emerging Markets started 2023 on a

strong note as sentiment surrounding China equities meaningfully reversed amid

growing excitement around China’s much awaited reopening from the Covid-19

pandemic, and the market was hopeful for a peaking US dollar. However, China’s

reopening ultimately disappointed and the US proved remarkably resilient despite

aggressive monetary tightening. Elsewhere the trend of generative AI propelled the

technology sector to substantial gains and Taiwan reached all time highs towards the

tail end of Q1 2024 as the cases for AI grew.

Regionally, Latin America emerged as the top performer over the period with a 23.4%

increase. Peru stood out as one of the strongest performers, largely due to the

sustained high demand for its primary export, copper, in the wake of the AI boom. The

Central and Eastern Europe, Middle East, and Africa (CEEMEA) region saw a 10.6%

rise. Asia, excluding Japan, lagged (+4.3%), primarily due to China’s weakness.

27

Japanese Equities

Japan equity markets gained during this period, driven by heightened expectations of

corporate reforms by Tokyo Stock Exchange, Semiconductor and other related growth

stocks positioned to benefit from the adoption of AI, and greater inbound demand by

foreign tourists.

In April, the market experienced a rally triggered by statements by American Investor

Warren Buffet accompanied by expectations for structural reforms in domestic

companies, such as improvement in Price to Book Ratio, reopening of the economy

causing greater inbound demand, and continuation of accommodative monetary

policy. Furthermore, the market experienced a rally in growth stocks, fuelled by

heightened expectations for AI related companies. Following such rout, the market

experienced profit taking along with higher US long term interest rates which impacted

US and Japan markets. However, as the market factored in rate cuts, lower treasury

yields helped US and Japan equities to soar. Coming into 2024, data further confirmed

that Japan is finally breaking out of the deflationary cycle and entering a virtuous cycle

of price increases and wage hikes. Although Bank of Japan (BoJ) has ended its

negative interest rate policy, such reversal, confirmed Japan’s return to normal policy

and above mentioned cycle of prices increases and wage hikes.

Bonds

Q2 2023 saw negative bond market sentiment, as economic data points in developed

markets pointed to an environment in which central banks would need to continue

increasing interest rates to slow down the economy. In the US, the March Year on

Year (YoY) Consumer Price Index (CPI) inflation rate accelerated by 5.0% YoY. This

was slightly below the consensus expectation of 5.1%, and a notable decline from the

February CPI number of 6.0%. By the end of the quarter, the Federal Reserve had

paused their interest rate increases. Uncertainty surrounding the ongoing US debt

ceiling negotiations contributed to the negative sentiment. In May, a debt ceiling deal

was agreed which included a suspension of the debt ceiling until January 2025. Euro

area inflation also printed in line with expectations, with March headline and core

inflation rising to 6.9% and 5.7% YoY respectively. Meanwhile, in what was a second

consecutive upside surprise in the UK, prices accelerated by 10.1% having been

expected to accelerate by only 9.8% YoY in March. The ECB and the BoE increased

interest rates over the quarter. UK Inflation once again surprised to the upside with

core at 7.1% YoY vs expected 6.8%. The UK became the only country in the G7 with

rising inflation.

Q3 2023 saw mixed bond market performance, driven by the release of generally soft

economic data, and views on longer term inflation and interest rates. As widely

expected, after pausing its aggressive rate hiking trajectory in June, the Federal

Reserve raised key interest rates during the month. The US CPI inflation rate for the

28

month of June accelerated by 3.0% YoY. The ECB also raised rates during the month.

In the Euro Area, Gross Domestic Product (GDP) figures increased by 0.3% quarter

on quarter as expected. Once again in the UK, the main story for the month was

inflation, with core inflation remaining high while Services CPI rose, and headline

inflation met expectations. The BoE raised rates to 5.25%. Global bond market

sentiment ended the quarter negative as developed market government bond yields

generally rose over the month, driven mostly by hawkish projections by the Federal

Open Market Committee (FOMC), which left its policy rate unchanged at 5.25% to

5.50%. In Europe, the ECB raised its key interest rates, while the BoE maintained the

Bank Rate at 5.25% following the drop in inflation. However, they cut their forecasts

for economic growth for the second quarter while warning rates may need to remain

at these high levels.

Global bond market sentiment was generally negative at the start of Q4 2023, driven

predominantly by a continued ‘higher for longer’ narrative and solid economic data in

the US. In the US, the CPI inflation data for September showed increases in the Month

over Month (MoM) core and headline rates. Euro area headline inflation fell from 2.9%

YoY in October, below consensus. CPI inflation data was published during the month

in the UK. On a YoY basis prices increased marginally ahead of expectations in

September, with headline inflation printing at 6.7% against the 6.6% expected. By the

middle of the quarter, many believed that developed market central banks had finally

reached the end of their tightening cycles. In the US, headline CPI inflation was flat on

the month, holding the YoY inflation rate. In the Euro Area, headline CPI inflation

surprised to the downside and MoM CPI decelerated, as did UK inflation. Global bond

markets finished the year on a highly positive note, with bond yields falling notably in

developed markets in December. In the US and the Euro area, November CPI inflation

printed in line with expectations. In the UK, YoY November CPI was lower than

expected.

With the start of Q1 2024, global bond markets experienced a slight downturn, with

economic data and central bank communications not swaying expectations for rate

cuts in 2024, despite a challenging start to the year for risk assets. The Federal

Reserve maintained its policy rate, and the ECB noted a declining inflation trend, while

BoJ continued its ultra loose policy. Europe’s GDP growth was stagnant, but jobs

growth showed a slight increase, and the ECB maintained its rates. The BoE held the

bank rate steady with a dovish tone, and the unemployment rate was lower than

expected. The quarter ended on a high in March, where global bond market sentiment

was positive, with tightening spreads and slightly reduced yields. The US ended the

quarter with a slight decrease in core CPI both MoM (0.35%) and YoY (3.8%), while

Europe confirmed its annual inflation rates to be in line with estimates, and the UK

experienced a drop in CPI inflation YoY (3.4%). Japan’s CPI figures were in line with

expectations. Government bond yields in developed markets fell modestly, with US

treasury yields, German bund yields, and UK gilt yields all declining. Most G10

29

currencies weakened against the US dollar, except for the Canadian and Australian

dollars which appreciated slightly.

UK Property

The past year has been a dynamic period for the UK real estate market, characterised

by a mix of challenges and opportunities. At the end of 2023, we reflected on what

was a very challenging year for the UK real estate markets, as investors grappled with

the implications of higher costs of debt and falling valuations. In the prior 18 months,

we have seen inflation remain persistently high and, as a result, have witnessed

continual rises in the base rate, totalling 500 basis points in that time. The ramifications

of such a large change in the macro environment have been felt throughout all financial

markets. This has affected all assets and led to repricing in line with this fundamental

rebasing as the period of great moderation comes to an end.

In the UK, debt costs continued to remain above yields, even for prime properties,

which caused a widening of the bid ask spread as buyer and seller expectations moved

further apart. The lack of price discovery from subdued transaction activity made it

difficult to monitor pricing and led to a steep decline in liquidity across all sectors.

Capital market activity ended the year on a weak note. In 2023, UK All Property

transaction volumes totalled £32 billion, which is 42% below the five year average. As

yields decompress in 2024, we expect buyer and seller expectations to become more

aligned, supporting a pickup in transaction volumes.

We began to observe a degree of stabilisation by the end of Q4 2023. Valuations

remained steady for several months following a 22% decline in the UK real estate

market from peak pricing in June 2022. This reflected a level of transparency

compared to much of the rest of the world and indicated that the significant correction

appears to be behind us.

It seems that an inflection point is imminent in 2024, with inflation seemingly on a

downward trajectory and interest rates at the peak of the hiking cycle as the BoE held

rates steady at 5.25%, and forward guidance is becoming slightly more dovish. The

renewal in the relative attractiveness of the UK real estate market will be driven by the

first rate cut forecasted to happen later in 2024, coupled with the growing optimism

surrounding the UK’s macroeconomic climate, now in expansionary territory,

translating to a more positive outlook for the real estate market going into 2024.

30

Market Returns

1 Year

(% p.a.)

3 Year

(% p.a.)

5 Year

(% p.a.)

Equities

FTSE All Share Index

2.9

13.8

5.0

FTSE All World Index

-6.9

15.9

7.4

FTSE All World ex UK Index

-7.2

15.9

7.6

FTSE North American Index

-3.1

18.0

13.1

FTSE European (ex UK) Index

2.1

14.9

4.9

FTSE Japan Index

2.0

7.8

3.9

FTSE Developed Asia (ex Japan) Index

-9.5

14.0

2.5

FTSE Emerging Markets Index

-4.3

29.4

13.9

Bonds

FTSE Actuaries UK Conventional Gilts

All Stocks Index

-16.3

-9.1

-3.1

ICE BofA Sterling Non Gilts Index

-10.3

-3.1

-0.8

FTSE Actuaries UK Index Linked Gilts

All Stocks Index

-26.7

-7.6

-3.2

Source: Bloomberg

31

8. NESPF Investment Strategy

The Fund’s Investment Strategy is one of diversified investment. This means that

investments are spread across different investment asset types and different

countries, sectors and companies in order to reduce the overall risk.

There are a range of Fund Managers employed to again spread risk, with different

style biases, each with clear and documented agreements in place detailing their

investment mandates. In addition, the Fund employ an independent Global Custodian.

The objective of the Investment Strategy is to deliver long term returns which are

greater than the growth in expenditure to be paid out in pensions. The investment

strategy is monitored on an ongoing basis by the Pensions Committee and Pension

Board, focusing on long term investment with consideration given to short term tactical

considerations if appropriate.

The suitability of particular investments and types of investments are detailed in the

Statement of Investment Principles. The Fund takes proper advice at reasonable

intervals regarding their investments through their appointed advisors.

Asset Structure 2023/24

Asset Class

Distribution as at

31 March 2023

Distribution as at

31 March 2024

Fund

Actual

%

Fund

Benchmark

%

Fund

Actual

%

Fund

Benchmark

%

Equities (including

alternative assets)

63.3

55.0

63.5

55.0

Bonds/Credit

17.7

22.5

17.9

22.5

Property/Infrastructure

15.9

20.0

16.4

20.0

Cash/Other

3.1

2.5

2.2

2.5

Total

100.0

100.0

100.0

100.0

During the first part of 2023 and given the volatility in markets, NESPF slowed its

rebalancing efforts, making selective and tactical changes in line with its investment

strategy where appropriate. Given the rise in equity markets towards the back end of

2023 and into 2024, this has positively increased the overweight to equities and

therefore allocations have been made to infrastructure and direct lending, with more

rebalancing to follow.

32

The current Investment Strategy for the North East Scotland Pension Fund is set out

in the Statement of Investment Principles as follows:

Equities 50.0% (range +/- 5%)

Alternative Assets (including private equity) 5.0% (range +/- 5%)

Bonds/Credit 22.5% (range +/- 5%)

Property/Infrastructure 20.0% (range +/- 5%)

Cash/Other 2.5% (range +/- 5%)

North East Scotland Pension Fund Performance

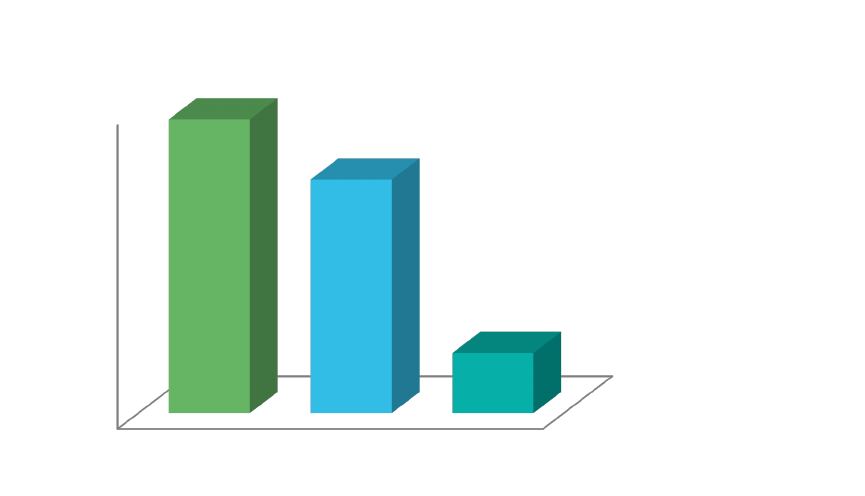

Investment returns over the last year have been strongly positive delivering 9.5%,

given a difficult market backdrop with constant changes regarding sentiment towards

interest rates and inflation affecting different asset classes. In the shorter term some

of the active Equity holdings are behind benchmark, but performance is beginning to

turn around and the NESPF has conviction in these positions as a long term investor.

A number of benchmarks are also arbitrarily higher this year on Sterling Overnight

Index Average (SONIA) targets, which is not necessarily reflective of the asset class

it is measuring against.

It is notable that the NESPF continues to outperform the benchmark returns over

longer periods and similarly comparators such as CPI and Average Earnings over the

longer term. This provides assurance that the Fund’s Investment Strategy works and

will continue to deliver the required returns over the longer term.

33

The graph below shows the NESPFs performance over the short, medium and long

term against the Fund’s customised benchmark.

Whilst employee contribution rates and benefits payable are set by statute, the long

term liabilities of the NESPF are linked either to wage inflation or to price inflation. It is

the NESPFs performance against these benchmarks that affect the long term

employer contribution rate, which is variable. Over the longer term, the performance

of the NESPF remains ahead of both Average Earnings and CPI.

Year Ending

2021/22

%

2022/23

%

2023/24

%

Since

Inception

Annualised

%

CPI*

7.0

10.1

3.2

2.9

Average Earning*

7.0

5.8

5.7

3.3

NESPF Return

2.4

-4.1

9.5

8.1

*Source: Office of National Statistics

Investment Management Structure

Details of the Investment Management Structure is in the “Investments Analysed by

Fund Manager” Note to the Accounts.

9.5%

1.9%

6.8%

8.1%

13.2%

6.0%

6.6%

7.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1 Year 3 Year 5 Year Since inception

NESPF

Benchmark

34

9. Risk

A key element to risk management is the structured delegation of powers from the

Council to the Pensions Committee and then to Senior Officers. To complement the

delegation to Senior Managers, there is extensive and detailed accountability back to

Committee on how these delegations have been exercised. Full details of the structure

of delegated powers are contained in the Pension Fund’s Governance Statement.

Investment Risk is recognised as falling into two distinct areas: Manager Skill (alpha)

and Market Risk (beta). The structure of the Investment Strategy reflects this and is

designed with the support of external expert advice. Details are contained in the

Statement of Investment Principles and the Funding Strategy Statement.

The operational management of investment risk forms the basis of quarterly reporting

to the Pensions Committee and Pension Board.

The Fund’s approach to risk is dynamic and can be revised in response to short term

market events.

Benefit Risk is also recognised as falling into two distinct areas: Operational Risk

(regulation compliance and staffing) and Information Technology (IT) risks. The risks

associated with the operational payment of benefits and recording of pensioner

records produces a complex set of risks. These are mitigated with the use of a

dedicated pension administration system that is thoroughly and regularly tested,

combined with the hierarchical checking of output by pension staff. IT risk is mitigated

by using an externally hosted benefit administration system subject to regular update

and review.

It is recognised that all services are very dependent upon third party contracts ranging

from IT through to investment managers. All are subject to regular review and

monitoring.

Risk Management

Risk management is an ongoing process with quarterly reporting provided to the

Pensions Committee and can be found within the Committee packs. These reports

detail the progress achieved in the implementation of the action plan, the ongoing

review of the Risk Register and reporting of new risks that have been identified. It is

also key that the Fund has its own dedicated Risk Management Policy which forms

part of the Risk Management Framework along with the Risk Register.

35

10. Funding Strategy Statement

The long term objective of the Fund is to achieve and maintain sufficient assets to pay

all pension benefits as they fall due. The Funding Strategy Statement (FSS) addresses

the issue of managing the need to fund those benefits over the long term, whilst at the

same time facilitating scrutiny and accountability through improved transparency and

disclosure.

The purpose of the FSS is therefore:

• To establish a clear and transparent Fund specific strategy which will identify

how employers’ pension liabilities are best met going forward by taking a

prudent longer term view of funding those liabilities.

• To establish contributions at a level to “secure the solvency” of the Pension

Fund and the “long term cost efficiency.”

• To have regards to the desirability of maintaining, as much as possible, a

constant primary contribution rate.

The FSS is required as part of Regulation 56 of the Local Government Pension

Scheme (Scotland) Regulations 2018. As part of the 2023 actuarial valuation, the FSS

for the North East Scotland Pension Fund was reviewed, with employers consulted on

the revised version.

The full statement is available at www.nespf.org.uk.

36

11. Statement of Investment Principles

This statement sets out the principles governing decisions about investments for the

North East Scotland Pension Fund. All investment decisions are governed by the Local

Government Pension Scheme (Management and Investment of Funds) (Scotland)

Regulations 2016. The Fund objective is to meet benefit liabilities as they fall due at a

reasonable cost to participating employers, given that employee contributions are

fixed. “Reasonable” in this context refers to both the absolute level of contribution –

normally expressed as a percentage of pensionable payroll – and its predictability. The

employer contribution rates are impacted by both the assessed level of funding (ratio

of the value of assets to liabilities) and the assumptions underlying the actuarial

valuation.

The NESPF target is to maintain a 100% funding level. ‘Growth’ assets, such as

equities, are expected to give a higher long term return than ‘liability matching’ assets,

such as bonds. The benefit of higher investment returns is that, over the long term, a

higher level of funding should achieve lower employer contribution rates. However, the

additional investment returns from growth assets come with a price: greater volatility

relative to the liabilities, thus introducing risk. The risk is evidenced by the potential

volatility of both the funding level and the employer contribution rate. There is therefore

a trade off between the additional investment return from greater exposure to growth

assets and its benefits – higher funding level, lower employer contribution level – and

the benefits of greater predictability – of both funding level and employer contribution

rate – from having greater exposure to liability matching assets.

The trade off and its consequences on both funding level and employer contribution

level, were examined by the Pensions Committee and led to the strategic

benchmarks.

The full statement is available at www.nespf.org.uk.

37

12. Environmental, Social and

Governance Issues

Responsible Investment & Engagement

As a long term investor the Fund has a duty to engage with the companies we invest

in on Environmental, Social and Governance (ESG) issues, and to work with others to

effect change.

What does this look like in practice?

There are several things that we as an investor can do to make changes for the better.

Collaboration

There are limits to what we can achieve as a single investor and believe greater

progress can be made through collaboration with other investors. Our main

collaboration is with the Local Authority Pension Fund Forum (LAPFF). We also

engage with our Fund Managers on a regular basis.

LAPFF brings together a diverse range of Local Authority Pension Funds (87 funds

and 6 pools) with combined assets of over £350 billion. The Forum provides a unique

opportunity for Britain's local authority pension funds to discuss shareholder

engagement and investment issues.

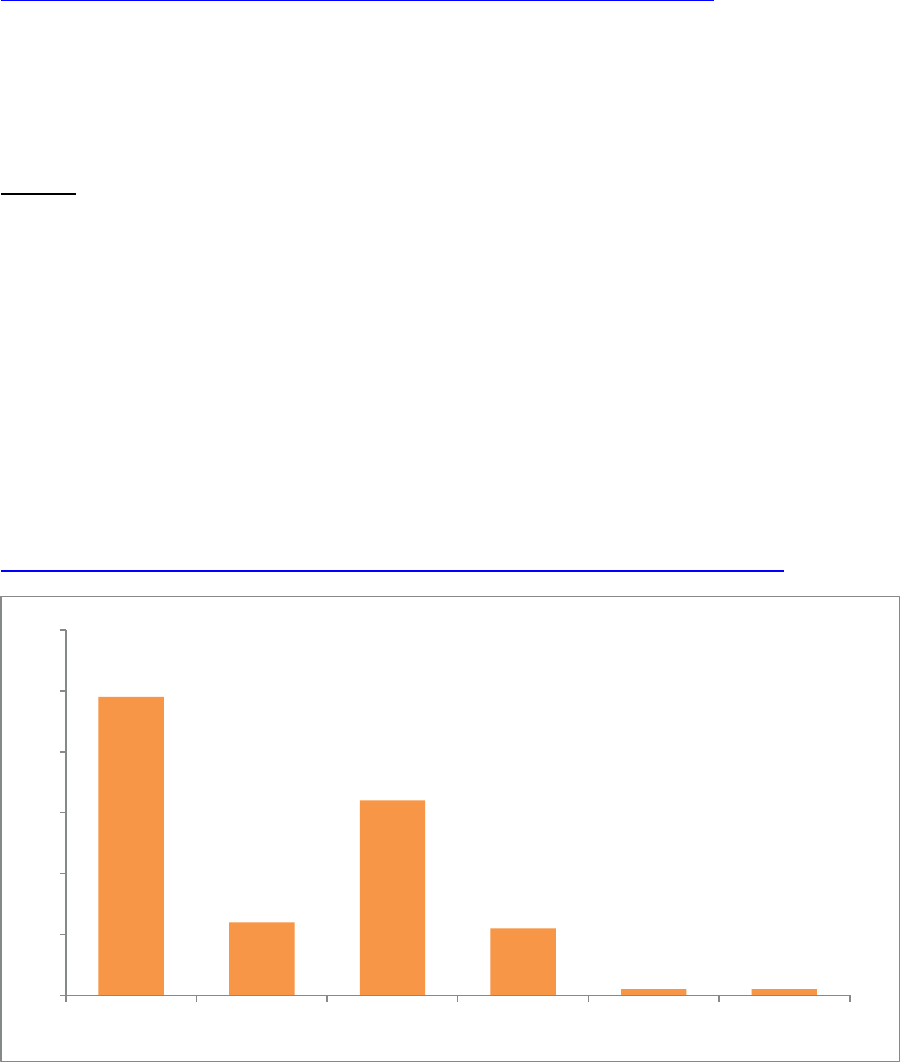

The graph below breaks down the engagements LAPFF has carried out in relation to

the Sustainable Development Goals (SDG). The 17 SDGs are integrated. LAPFF

recognise that action in one area will affect outcomes in others, and that development

must balance social, economic, and environmental sustainability.

38

LAPFF engagement work examples are noted below:

Mining and Human Rights

Context – LAPFF has been engaging with major mining companies on human rights

for the last five years. This engagement stemmed from tailings dam collapses in Brazil

linked to mining companies BHP, Vale and from Rio Tinto's destruction of cultural

heritage at Juukan Gorge in Australia.

Activities –LAPFF has undertaken an engagement with Grupo Mexico in relation to a

tailings pond leak at one of its operations in Sonora, Mexico. Certain health problems

and environmental damage – in particular, water contamination – are linked to this

leak. LAPFF has met once with the company and once with affected community

members at this stage and will look to progress the engagement in the coming year.

Human rights engagements with Rio Tinto and Anglo American are continuing too.

LAPFF also attended the 2024 African Mining Indaba in Cape Town, South Africa in

first quarter of 2024.

Outcomes – Positive outcomes for LAPFF members after visiting Brazil is that LAPFF

published a report of its findings after thorough engagement with both the affected

communities and the companies involved. Translation of the report into Portuguese

was also completed.

LAPFF is continuing to work with Rio Tinto to ensure that their relationship with

communities affected by their operations globally are improving.

0

100

200

300

400

500

600

700

Number of Engagements

Engagement Work

SDG Engagements 2023

39

Engagement with Anglo American is taking place primarily through LAPFF’s

participation in the new Principles for Responsible Investment (PRI) Advance human

rights initiative.

LAPFF submitted a response to the United Nations (UN) Working Groups consultation

on investors and ESG, which included the submission of its reports and work with

affected community members. This focus appears to be of interest at the international

level, and LAPFF will continue to work with the UN Working Group and other

stakeholders to inform best practice on mining and human rights, while linking the work

to financial materiality for investors.

Climate

Context – Drax owns the UK’s largest power generation site in Yorkshire. It consists

of a coal burning plant converted to burning wood pellets, mainly imported from North

America. It meets approximately 7-8% of the UK’s electricity demand. Despite the

switch from coal, Drax is the UK’s largest carbon emitter as stated in research by

climate think tank Ember and is government subsidised.

Drax uses the concept of ‘dynamic carbon sinks’ to justify its claims to carbon

neutrality, i.e., forests are harvested and the wood that is burned regrows.

Activities – LAPFF engaged with Drax in first quarter of 2024 as there are questions

about the time scale over which new growth of trees will compensate for the >10 Million

Tonnes (MT) of CO

2

Drax emits each year. The Forum sought to understand the

company’s business model, associated risks and sustainability of the supply chain for

wood pellets for combustion at Drax Power Station, which are mainly imported.

LAPFF responded to the consultation from the Department of Energy Security and Net

Zero on prolonging the subsidy to Drax. LAPFF’s response to the consultation covered

the evidence that Drax’s supplies of wood are not carbon neutral, nor sustainable as

a supply source (being dependent on US imports). BBC Panorama had its second

exposé of Drax’s activities that showed that not only has Drax been cutting and using

whole trees, but that the trees cut were from rare forest wood, rather than managed

plantations.

LAPFF attended the 2023 AGM and there was significant unease at Drax’s activities,

with no shareholders speaking positively. There were also representations from

people in the southern US states concerned about cutting down primary forest and

health affecting emissions from pellet plants.

Outcomes – Achievements have been wholly negative as LAPFF has seen no

evidence that the forest stock in the US is growing to offset Drax’s emissions. From

Drax commissions “catchment area” reports it is apparent that rather than a

quantitative test to prove contemporaneous offset, the test in the reports is that forest

stock is not shrinking. There is significant concern that Drax is contributing to net

increases in atmospheric carbon, in addition to wood being an inefficient source of

40

energy which, per unit of energy obtained, creates more carbon emissions than even

coal.

Drax’s answer is that things will be clearer once the company is able to capture carbon

from its burning by using carbon capture technology. However, that is not proven at

scale and is heavily subsidy dependent, on top of an already exceptionally large

subsidy required for pellet burning. Drax’s activities continue to attract cross party

criticism.

The above are just a couple of examples of engagement carried out by LAPFF, more

in depth information can be found at http://www.lapfforum.org.

Fund Managers

Through our fund managers we can engage with companies more directly by raising

concerns and meeting with Senior Management and Executives.

Fund managers report their engagements on a quarterly basis so we can monitor

engagement activity.

The below is one example of such activity being undertaken through one of our Fund

Managers.

Biodiversity on offshore wind farm

Through one of our Infrastructure portfolios the Fund invests in an offshore wind farm

in the Dutch part of the North Sea, on the border with Belgium. The biodiversity of the

construction site was assessed as the project commenced. The action taken was the

release of 2,400 flat oyster tables. The oyster tables were placed on the base of some

of the wind turbines in October 2020.

A team of researchers reviewed the oyster tables in 2023. The outcome being they

discovered in addition to the survival, presence and growth in oyster larvae they also

increase biodiversity. For this they used Environmental DNA traces in the water and

an underwater camera, The underwater water videos showed a lot of life around the

foundations with a total of the 65 species found. The researchers will return with the

hope of seeing the oysters have settled in the shell layer and rock surrounding the

wind turbine.

Other ways the Pension Funds collaborate are by being members/signatories of the

following ESG initiatives:

• 2022 Global Investor Statement;

• 2022 Non Disclosure Campaign (NDC);

• Bangladesh Accord on Fire and Building Safety (the Accord);

• Climate Action 100;

• Carbon Disclosure Project;

• Principles for Responsible Investment.

41

Further information on these initiatives can be found on our website:

https://www.nespf.org.uk/about/investment/responsible-investment/.

By working together, we and other investors can use our collective size to influence

decision making and promote the highest standards of corporate governance and

corporate responsibility.

Voting

As an institutional shareholder we have a responsibility to make full use of our voting

rights which enables the Fund to promote good governance practices in the

companies in which we invest.

The Fund vote in house on all our active managers holdings and over the last year

have voted at 106 Annual General Meetings/Special meetings on 1,554 resolutions.

The Fund’s voting advice is provided by Pensions & Investments Research

Consultants Ltd (PIRC). Additional advice is also received from the Local Authority

Pension Fund Forum.

Further information on the Fund’s Voting record can be found on our website:

https://www.nespf.org.uk/about/investment/responsible-investment/voting/.

49

12

32

11

1 1

0

10

20

30

40

50

60

UK Europe USA/Canada Asia Japan South America

Votes

Region

Voting By Region 23/24

42

During the year to 31 March 2024, the main reasons for casting a vote against a

resolution are listed below:

Directors

● Insufficient independent representation on the board.

● Global Diversity and Inclusion efforts of the company.

● Executives who are employees should not be additionally rewarded with bonuses or

Long Term Incentive Plans (LTIPs) for duties that are considered part of the job.

● The Chair cannot effectively represent two corporate cultures.

● Company has not disclosed quantified targets for the performance criteria of its

variable remuneration policy.

Share Issues/Repurchase

● No clear case as to how this would benefit long term shareholders.

Annual Reports

● Concerns over sustainability policies and practice.

908

491

140

16

12

21

2

For Against Abstain Non Voting

Items

Withheld

Items

US Frequency

Vote on Pay

Withdrawn

0

100

200

300

400

500

600

700

800

900

1000

Resolution

Votes

Voting By Resolutions 23/24

43

13. Acknowledgement

The production of the Unaudited Annual Report and Accounts is very much a team

effort involving many staff as well as information supplied by our advisors. We would

like to take this opportunity to acknowledge the considerable efforts of staff in the

production of the 2023/24 Unaudited Annual Report and Accounts.

Angela Scott Jonathan Belford, CPFA Councillor John Cooke