Bank ABC in Jordan

Annual Report 2021

Ambition.

Adaptability.

Acceleration.

His Majesty King Abdullah II Bin Al-Hussein

His Royal Highness Crown Prince Hussein Bin Abdullah II

Strategic Intent

To be MENA’s

leading

international

bank.

A team

committed to

your success.

Our Promise

We are committed to

knowing our customers

and developing long-

term relationships.

Client Centric

We are trusted to deliver

every time in the right way,

demonstrating integrity to all

our stakeholders.

Consistent

We work together as one

team across our international

network, providing a superior

client experience.

Collaborative

Core Values

Bank ABC in Jordan Snapshot

13 About Bank ABC Group

15 About Bank ABC In Jordan

16 Bank ABC in Jordan Organisational Chart

17 ABC Investments (ABCI) Organisational Chart

18 Financial Highlights

18 Analysis of the Bank’s Financial Ratios and

Business Results during the Fiscal Year

20 Owners of 1% or more of Bank ABC in Jordan

shares

Strategic Report

24 Directors’ Report

28 Board of Directors

31 Executive Management

33 ABCI’s Executive Management

Table of Contents

Review of Operations

36 2021 Business Results

44 Future Developments Plan for 2022

46 Shareholdings of the Chairman and Members

of the Board

47 Representation of the Board of Directors

Financial Results

50 Independent Auditors’ Report

56 Consolidated Statement of Financial Position

57 Consolidated Statement of Prot or Loss

58 Consolidated Statement of Comprehensive

Income

59 Consolidated Statement of Changes in

Owners’ Equity

60 Consolidated Statement of Cash Flows

61 Notes to the Consolidated Financial

Statements

snapshot

Bank ABC in Jordan

10

snapshot

13 About Bank ABC Group

15 About Bank ABC In Jordan

16 Bank ABC in Jordan Organisational Chart

17 ABC Investments (ABCI) Organisational Chart

18 Financial Highlights

20 Owners of 1% or more of Bank ABC in Jordan

shares

11

BANK ABC IN JORDAN ANNUAL REPORT 2021

12

Bank ABC (incorporated as Arab Banking Corporation

B.S.C) is an international bank headquartered in Manama,

Kingdom of Bahrain. Our network spreads across ve

continents, covering countries in the Middle East, North

Africa, Europe, the Americas and Asia.

Bank ABC Group

About

13

BANK ABC IN JORDAN ANNUAL REPORT 2021

14

Bank ABC in Jordan (Arab Banking Corporation - Jordan) was

incorporated in 1990 as a Jordanian public shareholding company. It is

a member of the Bank ABC Group, MENA’s leading international bank,

Bank ABC in Jordan performs all banking operations at its Head Oce

in Amman and its 24 branches, and 52 automatic teller machines (ATMs)

located across the Kingdom of Jordan.

The bank oers a comprehensive range of nancial services that

include retail banking, corporate banking and treasury, as well as

corresponding bank services and international banking operations.

It also oers investment and brokerage services (locally, regionally,

and internationally) on behalf of its clients as well as nancial

consultancy through its aliate company, ABC Investments. The

bank also focuses on developing its innovative capabilities to oer

its clients the latest digital banking services that meet their needs

and ambitions.

Bank ABC In Jordan

About

15

BANK ABC IN JORDAN ANNUAL REPORT 2021

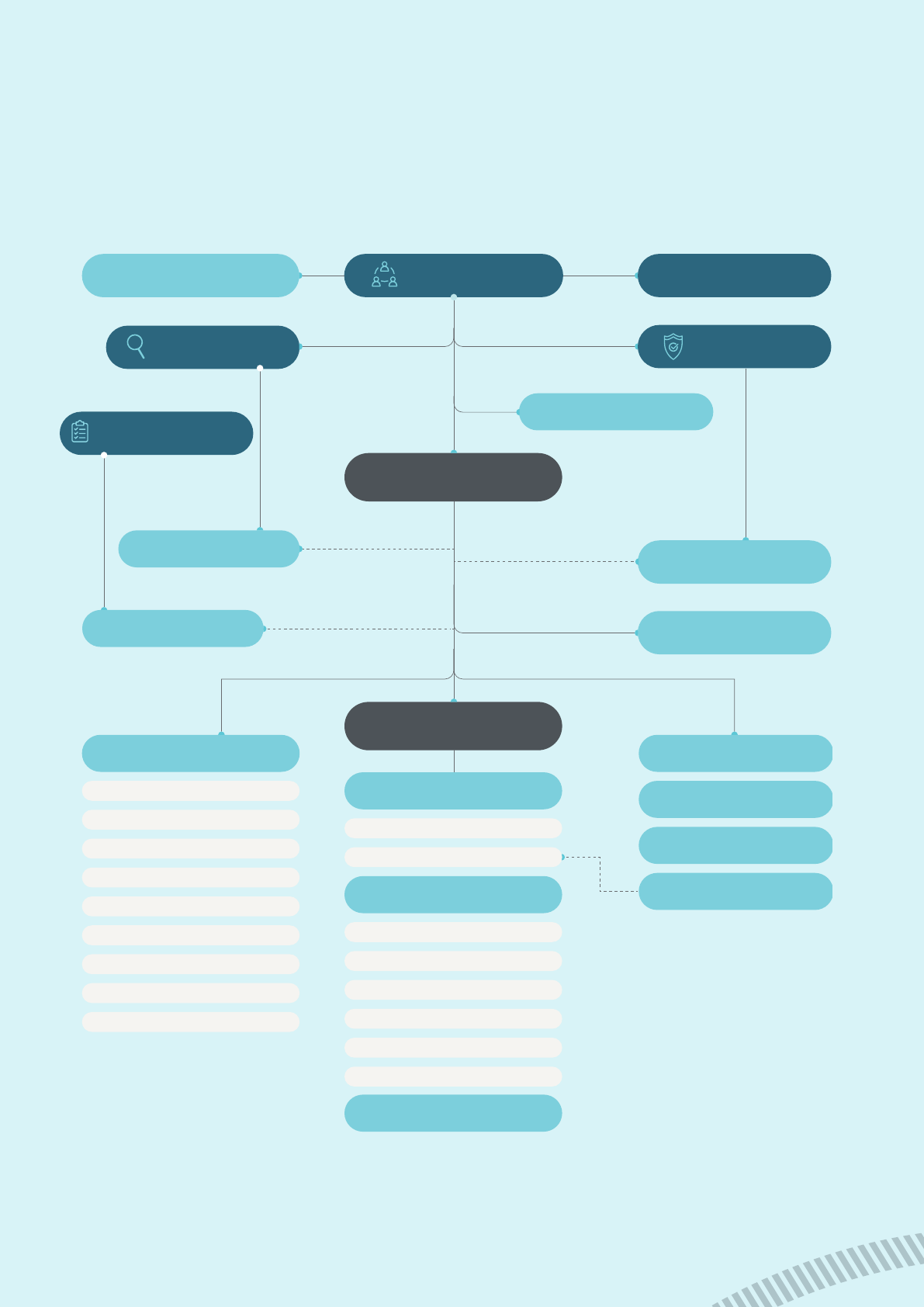

$

Board of Directors Board Committees

Audit Committee

Compliance Committee

Board Secretary

Risk Management

Department

Management

Committees

Corporate Services Department

Support Group

Procurement Supplies Department

Corporate Communications Department

Credit

Department

Human Resources

Department

Legal Affairs

Department

Financial Control

Department

Projects Management and Organization Unit

Information Technology

Operations Management

Operational Control

Information Security

Business Continuity Plan

Wholesale

Banking Group

Treasury

Retail

Banking Group

Corporates Coverage

Consumers Banking

Consumers Credit Banking

Transaction Banking

Financial Institutions Coverage

Small and Medium Enterprises

Middle Office

Business Development

General Manager

Deputy General Manager

Board Risk

Committee (BRC)

ABCI

Internal Audit

Compliance

Bank ABC in Jordan

Organisational Chart

16

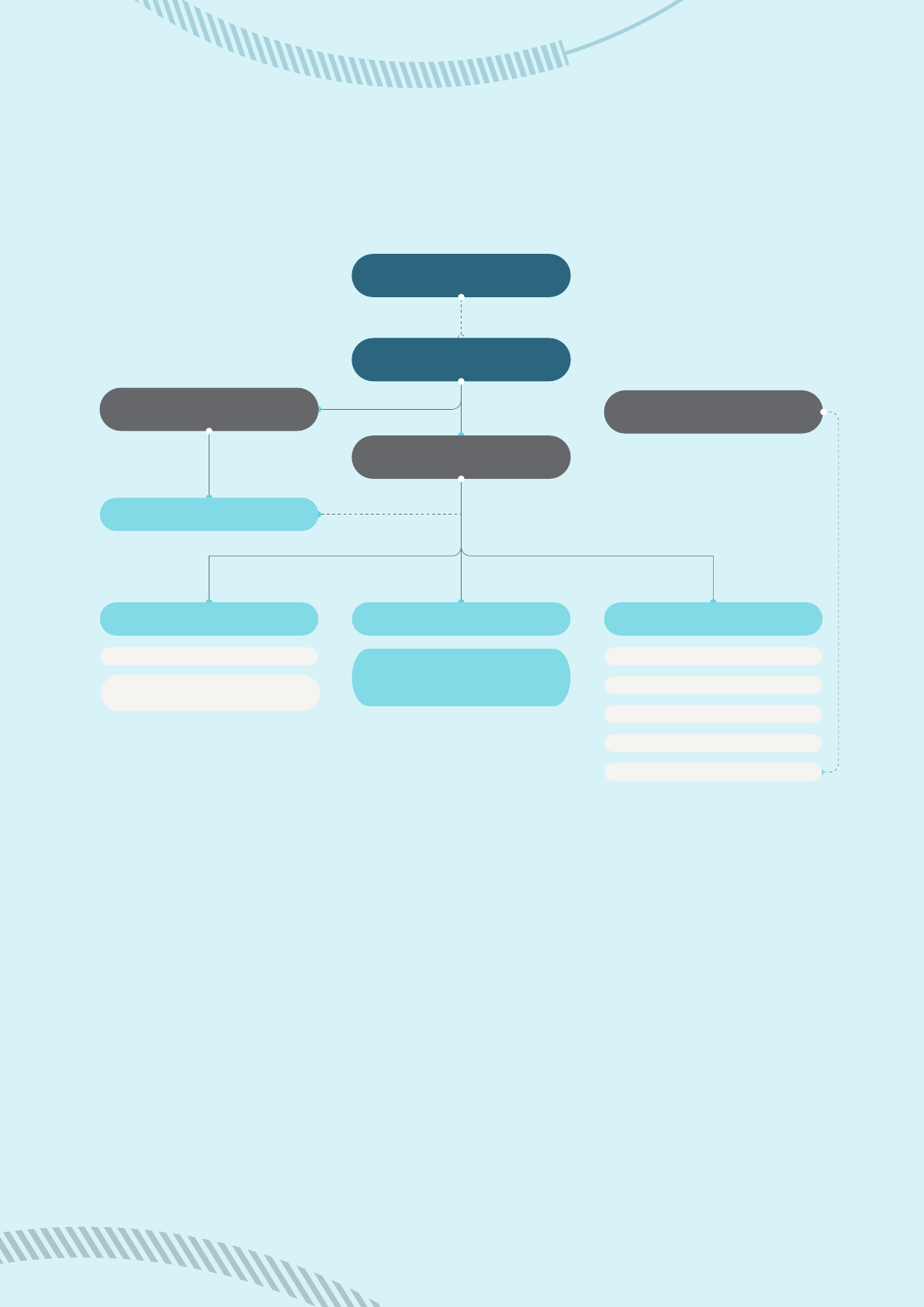

$

Board of Directors Board Committees

Audit Committee

Compliance Committee

Board Secretary

Risk Management

Department

Management

Committees

Corporate Services Department

Support Group

Procurement Supplies Department

Corporate Communications Department

Credit

Department

Human Resources

Department

Legal Affairs

Department

Financial Control

Department

Projects Management and Organization Unit

Information Technology

Operations Management

Operational Control

Information Security

Business Continuity Plan

Wholesale

Banking Group

Treasury

Retail

Banking Group

Corporates Coverage

Consumers Banking

Consumers Credit Banking

Transaction Banking

Financial Institutions Coverage

Small and Medium Enterprises

Middle Office

Business Development

General Manager

Deputy General Manager

Board Risk

Committee (BRC)

ABCI

Internal Audit

Compliance

ABCJ Board

ABCI Board of Directors

Chief Executive Officer

ABCJ Legal Affairs Department

ABCJ Compliance Department

Compliance

Brokerage Management

Local Brokerage Department

Credit Department Suport Management

Financial Control Department

Operations Department

Operations Control Department

Customer Service Department

Legal Affairs Department

Human Resorces and

Administrative Affairs

Department

Regional and International

Brokerage Department

ABC Investments (ABCI)

Organisational Chart

17

BANK ABC IN JORDAN ANNUAL REPORT 2021

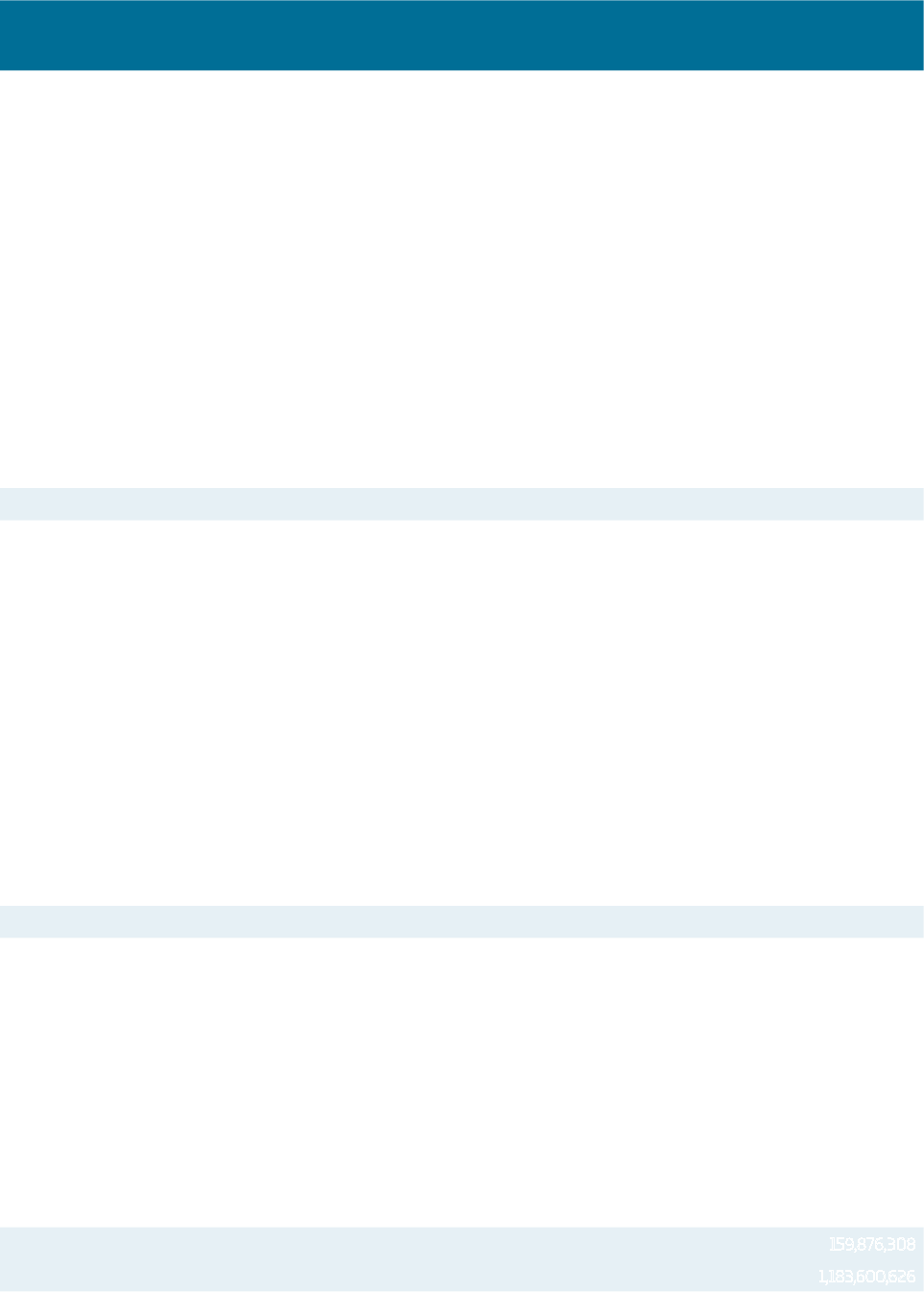

Financial Highlights

The Bank’s Main Financial Indicators between 2017 -2021

Statement / year 2021 2020 2019 2018 2017

Pretax Prots or (loss) / JD 15,127 4,207 3,455 14,211 19,433

Distributed Prots* / JD 6,600 - - 8,250 5,500

Dividends Per Share 6% 0% 0% 7. 5% 5%

Total Shareholders’ Equity / JD 168,355 159,876 156,892 160,179 160,242

Share Price / JD 0.88 0.69 0.83 0.94 1.17

* 2021 proposed dividends

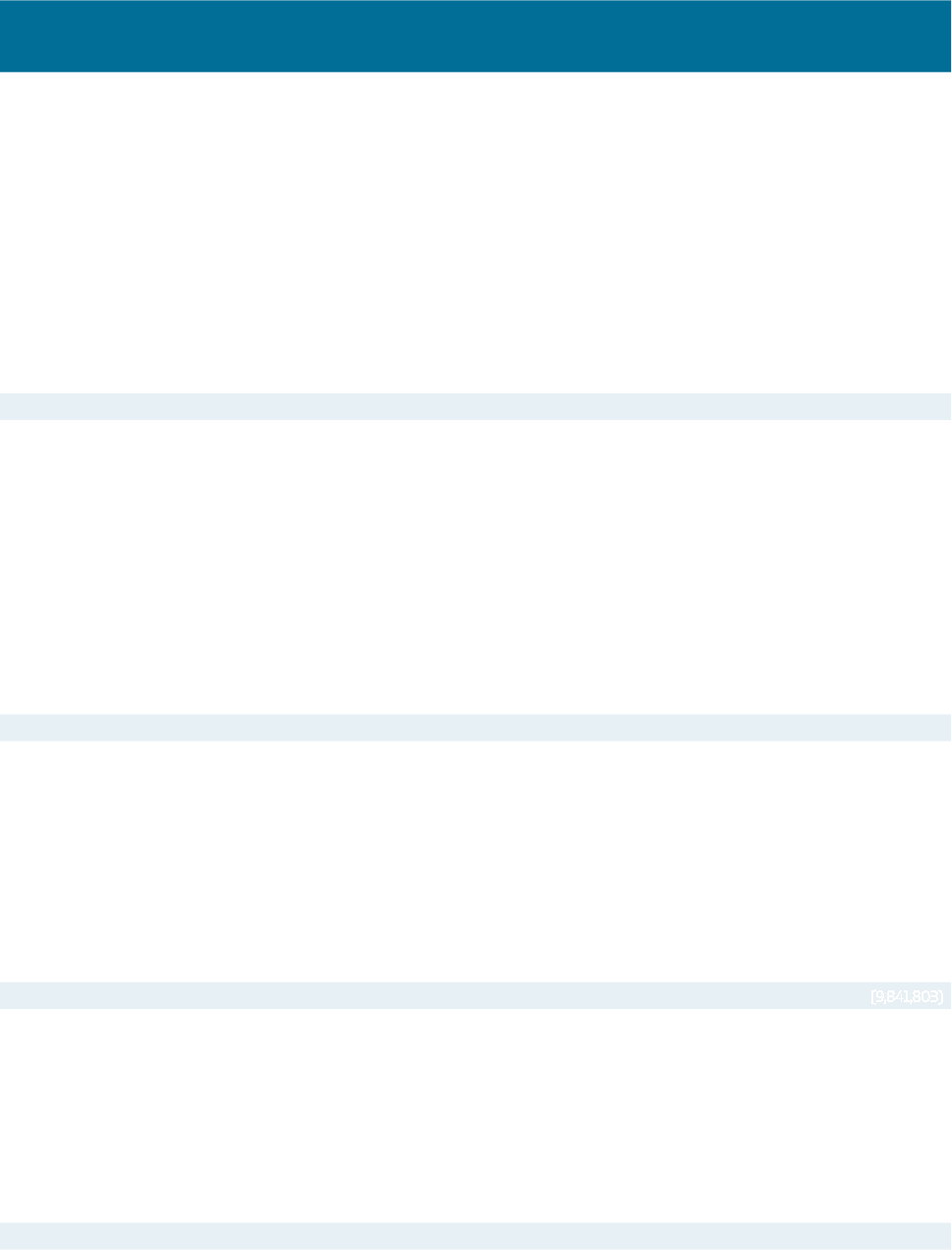

Analysis of the Bank’s Financial Ratios and Business Results during the Fiscal Year

Analysis of the Bank’s Financial Ratios and Business Results during the Fiscal Year

Main Financial Ratios 2021 (%) 2020 (%)

Return on average equity (RoE) 6 0.8

Return on average assets (RoA) 0.8 0.1

Operating expenses/ total income 55 56.7

Direct credit facilities/ customers’ deposits and margin accounts 89.4 88.4

Capital adequacy* 19.50 20.14

Non-performing facilities/ total direct facilities 8.6 8.7

Employee protability (JD,000) 17.8 2.3

* Calculation of capital adequacy is in accordance with Basel III.

18

4,207

15,127

19,433

14,211

3,455

5,500

8,250

0,000

0,000

6,600

5 %

7.5 %

0,000

0,000

6 %

160,242

160,179

156,892

159,876

168,355

1.17

0.94

0.83

0.69

0.88

15,127

6,600

%6

168,355

0.88

20202021 2019 20172018

20202021 2019 20172018

20202021 2019 20172018

20202021 2019 20172018

20202021 2019 20172018

T

h

o

u

s

a

n

d

J

D

P

r

e

t

a

x

P

r

o

fi

t

s

o

r

(

l

o

s

s

)

T

h

o

u

s

a

n

d

J

D

D

i

s

t

r

i

b

u

t

e

d

P

r

o

fi

t

s

T

h

o

u

s

a

n

d

J

D

T

o

t

a

l

S

h

a

r

e

h

o

l

d

e

r

s

’

E

q

u

i

t

y

%

D

i

v

i

d

e

n

d

s

P

e

r

S

h

a

r

e

%

S

h

a

r

e

P

r

i

c

e

19

BANK ABC IN JORDAN ANNUAL REPORT 2021

Owners of 1% or more of Bank ABC in

Jordan shares

Name Nationality

Number of

shares

%

Blocked

shares

Mortgaged

shares

% of the

mortgaged

shares from

the total

contribution

Mortgaging

party

Beneciary

Arab

Banking

Corporation

(B.S.C.),

Bahrain

Bahraini 95,676,826 86.979 1,500* - - -

Central Bank of Libya

59.37% – Libya -

Government

Kuwait Investment

Authority 29.69% –

Kuwait - Government

Social

Security

Corporation

Jordanian 2,256,124 2.051 - - - -

Social Security

Corporation

Kuwait

International

Investment

Company

Kuwaiti 1,460,244 1.328 - - - -

Kuwait Investment

Authority 31.911% -

Kuwait - Government

HH Sheikh Saad

Abdullah Al Salem Al

Sabah 9.933% - Kuwait

Kuwait Real Estate

Company KPSC

(AQARAT) 5.747 % –

Kuwait

Shareholder owning

5% and more shares:

• Kuwait International

Investment Company,

owns (18.20% ) –

Kuwait.

• Al-Raghd & Al-Manar

Real Estate Co. owns

(11.90%) – Kuwait.

• Group of Med

Al-Bahar Holding Co.

(AlDahiya Investment

Co., Kuwait Holding Co.,

Al-Rana Gen., Trad. &

Cont. Co., AlShamiya

Investment Co.,

Masader Al-Ofoq Gen.

Trad. and Cont. Co.,

Mawared Al-Ofoq Gen.

Trad. and Cont. Co.,

Al-Deera Holding. Co)

(11.79%) – Kuwait.

* Membership shares

20

21

BANK ABC IN JORDAN ANNUAL REPORT 2021

strategic

report

2021

22

24 Directors’ Report

28 Board of Directors

31 Executive Management

33 ABCI’s Executive Management

23

BANK ABC IN JORDAN ANNUAL REPORT 2021

Directors’ Report

Dear distinguished shareholders,

On behalf of my fellow members of the Board of Directors

of Bank ABC in Jordan (Arab Banking Corporation-

Jordan), it is my pleasure to present the 2021 Annual

Report, which highlights the Bank’s achievements and

consolidated nancial performance for the year ending

December 31, 2021.

Despite the unprecedented challenges and repercussions

of the COVID-19 pandemic, which is still looming over

economies worldwide, including the Jordanian economy,

Bank ABC in Jordan continued its success journey and

managed to maintain its solid nancial position, positive

results and sustainable operations, by continuing to

provide exceptional banking services and products

through multiple digital and conventional channels. This

continued success reects the tangible eorts exerted

by all members of the Bank’s executive management,

guided by the Board’s vision and directives for expanding

the Bank’s operations, enhancing risk management

frameworks and protecting the Bank’s capital and

shareholders’ interests.

The Jordanian economy showed signs of recovery

during the rst nine months of 2021 with a 2.1% increase

in GDP, compared to a -1.5% decrease during the same

period in 2020, as the reopening and resumption of

normal operation in various economic sectors stimulated

movement in the economy. On the other hand, the

ination rate in 2021 increased by 1.2%, compared to 0.3%

during the same period in 2020.

The nancial results for

2021 show that Bank ABC

in Jordan has achieved

good nancial results; as

net prot aer tax reached

JD9.6 million.

Sael Fayez Al Waary

Chairman of the Board of Directors

Directors’

Report

24

Financial Results

Bank ABC in Jordan preserved its solid capital base; as

the capital adequacy ratio reached 19.50% and nancial

leverage ratio reached 10.73%, which signicantly exceed

the ratios required by the Central Bank of Jordan.

Moreover, for the year 2021, Bank ABC in Jordan achieved

robust nancial results; as net prot aer tax reached

JD9.6 million, compared to JD1.22 million in the previous

year. The total income for 2021 grew by 8.5% to JD45

million, compared to JD41.4 million in 2020. This is due to

the increase in interest margin caused primarily by the

decrease in the rate of interest on sources of funds and

increase in other commissions and prots as a result

of the growth in the facilities portfolio, as interest and

banking commissions reached JD40.5 million, compared

to JD37.1 million in 2020; with a 9% increase.

In relation to its nancial position, the Bank’s assets grew

to JD1.23 billion in 2021, with a 4% increase; shareholders’

equity grew by 5% to JD168 million, compared to JD160

million in 2020; and return on equity reached 6%, while

the return on the Bank’s assets reached 0.8%.

Despite all challenges, the Bank’s keenness and prudent

policy for managing its credit portfolios enabled it

to perform well in 2021, as the Bank’s management

continued its eorts to increase the volume of credit

facilities, while maintaining low risk levels by ensuring

all elements of a sound credit decision. As a result, the

credit facilities portfolio in 2021 grew by 6.7% to JD693

million, compared to JD650 million in the previous

year. The qualitative development and improvement

that accompanied this increase conrms the Bank’s

success in maintaining the quality of its credit portfolio

and enhances its ability to manage its assets and

optimize available funds utilisation opportunities, while

maintaining the balance between liquidity, protability

and risk. Furthermore, the Bank was able to increase its

credit facilities portfolio by entering new risk-managed

nancing transactions to improve the quality of its credit

portfolio. This increase was the result of the expansion in

the retail and corporate sectors. The Bank also continued

its eorts to improve the quality of the portfolio by

closely monitoring all facilities accounts.

By the end of 2021, customer deposits grew by 5.6% to

JD723 million, compared to JD684 million in the previous

year; with current and savings accounts making up 15.7%

of the Bank’s total customer deposits; which reects our

customers’ trust in and strong relationship with the Bank.

This growth helped maintain a healthy liquidity ratio of

111.9% by the end of 2021.

These results demonstrate the Bank’s strong nancial

position and its ability to continue to grow and achieve

further protability, despite the challenges presented

by the COVID-19 pandemic. They also reect the

tremendous eorts of the Bank’s Board of Directors,

executive management and employees to implement the

Bank’s strategic plans, in order to maintain this growth

and implement the Bank’s policy of prudent management

of risks and banking liabilities, as part of its strategic

agenda aimed at oering the best-in-class banking

products and meeting customers’ needs in the best

possible way in line with the technological advances in

this sector.

Key Achievements & Main Activities

The Wholesale Banking Group contributed to the national

programmes launched by the Central Bank of Jordan to

support the Jordanian economic sectors aected by the

COVID-19 outbreak. This entailed granting loans to these

sectors, under the National Programme to Contain the

Repercussions of the COVID-19 Pandemic, in addition to

adhering to the directives of the Central Bank of Jordan

regarding the postponement of instalments payable by

businesses adversely impacted by this pandemic.

In collaboration with our Parent Bank in Bahrain, the

Bank is launching a new digital platform for its corporate

customers in line with the rapid advancements in the

elds of digital payments, international trade solutions

The Bank’s total income for

2021 grew by 8.5% to JD45

million, compared to JD41.4

million in 2020.

25

BANK ABC IN JORDAN ANNUAL REPORT 2021

and cash and liquidity management. As part of the Bank’s

Wholesale Banking Digitisation Programme, in-house

solutions will be launched to automate trade and cash

management products, including initiating and approving

requests besides enquiring about foreign trade services,

in addition to cash and liquidity management solutions,

which include several solutions related to payment,

collection, liquidity management and account reporting

services.

Therefore, the provision of digital services and products

will be a qualitative shi in the nature of the services

oered to corporate customers, which will strengthen the

Bank’s status in the local market and positively impact its

market share and prots.

The Wholesale Banking Group will also be launching a

seamless digital onboarding service which will enable

corporate and institutional clients to open an account

with the Bank and complete the “Know Your Customer

(KYC)” journey in under several hours. Through this

user-friendly self-service solution, our corporate banking

clients can track their application status in real-time and

swily access the Bank’s various products and services.

Furthermore, the Bank continued to develop its business

on multiple fronts. Retail Banking Group continued to

develop the Bank’s digital banking services; enhancing the

accessibility and eciency of ABC Digital, our core digital

banking platform, while encouraging customers to use

this service. Through Digital Banking, Bank ABC in Jordan

also launched instant money transfer and receipt services

using “CliQ” system, which features the most advanced

and state-of-the-art instant payment system in Jordan;

allowing customers to send and receive funds between

accounts with all participating banks, besides to and from

electronic wallets in Jordan, instantly and free of charge.

To keep pace with the rapid technological and customer

service advancements, Bank ABC is on track to launch “ila

application”, the digital mobile-only application, in Jordan

in 2022. With the support of Bank ABC in Jordan, this

customer-centric mobile-only oering, aided by cutting-

edge Articial Intelligence and sophisticated Data Analytics,

is expected to appeal to all consumer generations, from

millennials to older age groups, and segments of society.

In the same context, the Bank’s Treasury Department

continued to oer a variety of new services as part of

its strategy of providing outstanding services that meet

our diverse customers’ needs. The Treasury Department

also managed the Bank’s liquidity eectively by providing

the Bank’s nancing needs, while continuing to full its

responsibility in terms of managing interest rate and

foreign exchange risks, keeping them within Group’s

adopted risk appetite.

Social Responsibility

Social responsibility is an essential focus of Bank ABC in

Jordan. It reects the Bank’s corporate identity and is

driven by our belief in the importance of supporting the

local community to achieve social solidarity. Therefore, the

Bank continued to support local community, focusing on

sustainable development activities by, passionately and

with the spirit of giving, adopting several initiatives aimed

at supporting the local community in line with the Bank’s

values and objectives.

Future Outlook & Objectives

At the beginning of 2022, the Bank moved into the new

Head Oce and Main Branch, which meets our current and

future needs and reects Bank ABC in Jordan’s identity

and commitment to putting customers rst. Our new

oces will enable us to maintain our steady performance

as a team; thus, enhancing our success and further

cementing our mark as one of the biggest banking groups

in the region.

Bank ABC in Jordan was

able to maintain its solid

capital base; as the capital

adequacy ratio reached

19.50% and nancial

leverage ratio reached

10.73%, which signicantly

exceed the ratios required

by the Central Bank of

Jordan.

26

The new building has all the necessary elements of

a comfortable and motivating work environment and

provides adequate spaces for various departments to

bolster work performance and communication eciency.

In addition, it boasts state-of-the-art service facilities that

enhance communication and cooperation to the benet

of the Bank’s employees and customers alike.

The new Head Oce was designed in accordance with

the best energy-ecient practices that help reduce the

Bank’s power bill, particularly as the Bank established

a solar power station to power all its buildings and

branches. The building is also equipped with an

environment-friendly lighting system, which further

reduces the Bank’s power bill and meets the Bank’s

sustainability objectives.

In line with its future vision and strategy, the Bank

is striving to strengthen its capital base, enhance

its nancial position and increase its market

competitiveness. It also seeks to maximize its

shareholders’ equity, continue to develop its risk

management practices, and expand its activities

and services in line with technological and digital

advancements. This will see the Bank further embrace

disruptive technologies to improve its oering and invest

in the broad international network of Bank ABC Group.

Finally

Considering the nancial results achieved in 2021, the

Bank’s Board of Directors submitted a recommendation

to the general assembly to distribute dividends to

shareholders at the rate of 6% of the subscribed capital.

On this occasion, I would like to express my heartfelt

gratitude to our shareholders and customers for their

support and trust, which we deeply value and take pride

in. I would also like to extend my appreciation to my

fellow Board members for their sincere commitment and

cooperation, and the Bank’s management and employees

for their dedication in oering our customers the best-

in-class services and tireless eorts, which enabled the

Bank to grow and prosper. I pray to Allah the Almighty to

make 2022 another year of growth and progress for our

beloved organisation and precious country.

May the peace and mercy of Allah be upon you.

Sael Fayez Al Waary

Chairman of the Board of Directors

27

BANK ABC IN JORDAN ANNUAL REPORT 2021

Board of Directors

B.Sc. (Hons) degree

in Computer Sciences,

University of Reading,

United Kingdom.

Mr. Al Waary is the Deputy

Group Chief Executive

Ocer of Bank ABC Group,

with over 30 years of

banking, leadership and

management experience

garnered from the many

senior positions he has

held in both London and

Bahrain.

In addition to his

Chairmanship, Mr. Al

Waary represents the

Bank as Chairman of the

Arab Financial Services

Company, Chairman of ila

Bank Advisory Board and

Chairman of Bank ABC’s

newly acquired subsidiary

in Egypt, BLOM Bank Egypt.

He has previously served

on the Boards of Bank

ABC Egypt and Banco ABC

Brasil.

Mr. Sael Al Waary

Chairman

RC GC TC ‡ ð

MBA in Financial

Management University of

Hull, England.

Bachelor’s degree in

Accounting, Garyounis

University, Benghazi,

Libya.

Mr. Matok is currently

General Manager Long

Term Portfolio since 2012.

Mr. Matok previously held

the position of Deputy

General Manager (Capital

Market) Long Term

Portfolio from 2004 to

2012. During the period

from 1998 to 2004, he was

the senior vice president

(Head of Portfolio

Department) Pak Libya

Holding Co. before that he

was a Financial Analyst

in the Libyan Foreign

Investment Co. Mr. Matok

is the Chairman of ABCI

and also Member of the

board of directors of Bank

ABC Bsc and Pak Libya

Holding Co. Previously he

was the Deputy Chairman

of ABCI and Member of

the board of directors

of Libyan Foreign Bank,

Libyan Foreign Investment

Co., Iskan Co. for Touristic &

Hotel and Asian stock fund.

Mr. Bashir Matok

Deputy Chairman

AC GC NC ‡ ð

Master’s degree in

Economics and Statistics,

University of Jordan.

Bachelor’s degree in

Economics and Statistics,

University of Jordan.

Mr. Al- Halaseh is

currently on the Board of

Directors of Arab Banking

Corporation (Jordan) and

he is the Head of the Audit

Committee. He is also a

Board Member of ABCI.

He had previously held

several senior positions

in the banking sector,

beginning his career at

the Arab Bank – Jordan

and progressing within

the Bank until becoming

branch manager. During

the years from 2001 to

2005, he worked as Chief

Credit Ocer of Credit

Management at Bank ABC

in Jordan, from which he

moved to assume the role

of Head of Credit and Risk

at Bank ABC in Tunisia.

In 2008, Mr. Al- Halaseh

moved to National Bank

of Abu Dhabi as the Head

of Credit and later as the

Head of Banking Business

Risk and Stressed Assets.

In 2013, he became the

Head of Commercial Risk

for the Gulf Region at

the National Bank of Abu

Dhabi.

Mr. Ra’fat Al Halaseh

Director

AC GC RC NC TC ‡ §

Bachelor’s degree in

Finance, Boston College,

Chestnut Hill, MA.

Mr. Zawaideh started his

career as a Credit Ocer

in Banque Francaise De

L’Orient, London- United

Kingdom during the period

from 1995 to 1996, where

his last position was in

International Marketing.

During the period from

1997 to 2012, he worked

at United Iron & Steel

Mfg. Co. plc. as the Chief

Financial Ocer. In 2014,

Mr. Zawaideh joined Steel

Mesh Industry Co., where

he is currently holding

the position of General

Manager. Mr. Zawaideh is

a Board Member of ABCI

and previously was a

Board Member of United

Iron & Steel Mfg. Co. plc.,

Investment House for

Financial Services Co. plc

and First Finance Co. plc.

Mr. Hakam Zawaideh

Director

AC GC NC ‡ §

28

Bachelor’s degree in

Mechanical Engineering,

University of Bridgeport,

Connecticut USA.

H.E. Eng. Amer Hadidi’s

experience extends

across the public, private

and business sectors in

Jordan. H.E. Eng. Hadidi

took on the role of Chief

Executive Ocer at Royal

Jordanian (2012-2014). He

also served as Economic

Advisor to His Majesty

King Abdullah II (2011-

2012), preceded by service

as Minister of Industry and

Trade in three consecutive

cabinets (2007-2011). H.E.

Eng. Hadidi’s previous

experience included

roles at the Ministry of

Transport, the Ministry of

Industry and Trade and

the banking sector.

H.E. Eng. Amer Hadidi

Director

AC GC NC CC ‡ §

Master of Public

Administration, Economic

Policy Management,

Columbia University,

School of International &

Public Aairs - 2016 / USA.

Master of Science,

Banking & International

Finance, City University,

Cass Business School -

2011 / United Kingdom.

Bachelor of Science,

International Business

Studies with Professional

Development, Brunel

University, Brunel

Business School - 2009/

United Kingdom.

Mr. Breish is currently

the Deputy Director

of Financial Markets

Department at Central

Bank of Libya. He was the

Head of External Portfolios

Unit at Central Bank of

Libya and had previously

held the position of

Investment Analyst. Prior

to joining Central Bank

of Libya, Mr. Breish was

Research Intern at Ubs Ag

- Investment Bank in 2008.

Mr. Breish began his career

in 2005 at Libyan Foreign

Bank as Analyst – Intern

and in 2007; he had held

the same position at Aibel

Limited. Mr. Breish has

recently joined the Board

of Directors of Moamalat

Financial Services in Libya

(owned by CBL).

Mr. Abdulrahim Breish

Director

RC CC ‡ ð

MBA in Finance, Fordham

University – 1999, New

York, NY.

BSc. in Mechanical

Engineering, NYU

Polytechnic University –

1991, New York, NY.

Mr. Ammar Khalil has over

20 years of experience in

banking across institutions

in the US and GCC.

Currently he is the Senior

Executive Ocer for Bank

ABC, leading their business

strategy for the UAE.

Prior to this, he served

as the Managing Director

and Head of Coverage for

MENA at Natixis Dubai

leading their Corporate,

Public Sector, Financial

Sponsors, Islamic Banking,

and Financial Institutions

teams. Before Natixis, he

was Head of Institutional

Banking for the MENA

region at HSBC Middle

East Bank. At HSBC, he

was tasked with building

the coverage of Banks,

NBFIs, and Public-Sector

clients. In Kuwait, he held

the position of Group

Head of Institutional

Banking at National Bank

of Kuwait. In the US, he

held various roles at The

Bank of New York, Arab

Banking Corporation NY

Branch, and Arab American

bank looking aer the

correspondent banking

business between the

MENA and US regions.

Mr. Ammar Khalil

Director

RC AC ‡ ð

Higher Diploma in Public

Law, University of Jordan –

1986, Jordan.

Bachelor of Arts in Public

Law, University of Jordan –

1983, Jordan.

Mrs. Nabulsi has long

experience in senior

managerial positions and

consultancies in the banking

industry, she also embodies

strong ties to community

and non-prot organisations

focusing on Educational and

Youth Development Programs.

Currently, she continues her

pursuit of this passion by

serving as a member of the

board of the YMWA where

she is actively engaged in

the management of the

Princess Sarvath Community

College and the Bunnayat

Centre for Special Education.

Formerly, she was CEO of

Jordan Education Initiative

(JEI) between 2013-2017.

She was also the Founder

& Managing Director of

Horizon Banking Consultants

between 2008-2013. Over

her long experience, Mrs.

Nabulsi has held senior

managerial positions at

several banks including

Capital Bank of Jordan as

a Chief Operating Ocer

(AGM-Ops & IT) through

2002-2007, Cairo Amman

Bank from 1990-2001 where

she served as Executive

Manager in Internal Audit &

Credit Risk, Documentation

& Credit Control as well as

Legal, having previously held

many other senior positions

including the position of Credit

Ocer at Bank of Jordan.

Mrs. Nabulsi started her

career with the Ministry of

Transportation Queen Alia Int.

Airport Project as the Head of

Legal Department in 1986 and

with the Ministry of Finance –

Income Tax Dept before that

in 1983. Mrs. Nabulsi is also

a non-practicing Lawyer by

original degree and training.

Mrs. Nermeen Nabulsi

Director

AC GC NC CC ‡ §

29

BANK ABC IN JORDAN ANNUAL REPORT 2021

AC Member of the Audit Committee

GC Member of the Corporate Governance Committee

RC Member of the Risk Committee

NC Member of the Nominations & Compensation Committee

TC Member of the IT Governance Committee

CC Member of the Compliance Committee

‡ Non-Executive

æ Executive

§ Independent

ð Non-Independent

Master’s degree in

Management - Economic,

Sciences and Management

University - Tunisia.

Bachelor’s degree in science

and Mathematics - 1989 /

Tunisia

Mr. Mokhtar is currently the

Group Chief Operating Ocer at

Bank ABC Bahrain, appointed in

May 2019 from Regional Chief

Operating Ocer for MENA to a

new role, Group Chief Operating

Ocer to support the delivery

of the key support areas across

the Group and oversees the

functional and Country COOs

across the Group.

Ismail Mokhtar has had several

senior positions in the banking

sectors and senior roles with

Bank ABC for over two decades.

He served Bank ABC in Tunisia

as the Deputy General Manager

and Chief Operating Ocer

before moving to the Head

Oce in Bahrain as Business

Catalyst and Project coordinator

at Group level in 2015.

Mr. Mokhtar has held past key

positions in ABC in Tunisia,

including being Commercial

Banking Head from 2009 till

2011, General Management

Coordinator and Board of

Directors Secretary from

2006 till 2015. Mr. Mokhtar was

appointed Chief Operating

Ocer and Deputy General

Manager of ABC in Tunisia from

2012 to 2015.

Before joining Bank ABC, Mr.

Mokhtar was the Head of the

Government Bond Desk at the

Treasury Department of Banque

Nationale Agricole (Tunisia) from

which he moved on to Bank ABC

in Tunisia in 2001.

Mr. Mokhtar joined the Board of

Directors of ABCJ in May 2015

and board member of ABCI from

01/03/2016 to 30/4/2018.

Mr. Ismail Mokhtar

Director

AC NC TC RC ‡ ð

Master’s degree

in Commercial and

Administrative Sciences,

Université Saint-Esprit de

Kaslik – 1986, Lebanon.

BA in Elementary

Mathematics, College de la

Sagesse – 1980, Lebanon.

Mr. Touma is currently

the First Vice President

/ Group Retail & Digital

Banking Head at Bank ABC

Bahrain. He had previously

held the positions of FVP

/ Group Retail & Digital

Banking Coordinator and

FVP/ Group Retail Banking

Planning & Development.

Before joining Bank ABC,

he started his banking

career in 1982 with

Banque Libanaise Pour Le

Commerce SAL- Lebanon

where he assumed several

positions from which

he moved to Omnilife

Insurance Company–

Cyprus (UK registered)

as the Head of Business

Development in 1991. He

moved to Banque Libanaise

Pour Le Commerce SAL-

Lebanon (BLCBANK) in 1994

as Head of Retail Products

Division. Mr. Touma served

on the Board of Directors

for Bank ABC in Tunisia

from 2009 until 2014

and Bank ABC in Jordan

from 2015 until 2017. Mr.

Touma joined the Board of

Directors of ABCJ in May

2019.

Mr. Elie Touma

Director

RC ‡ ð

MBA, Ecole Supérieure

des Aaires (ESA) - 1999,

Lebanon.

Bachelor’s degree in

economics, Université

Saint Joseph (USJ) - 1992,

Lebanon.

Mr. Sacre started his

career in 1992 with BNP

PARIBAS “BNP”- Beirut

where he graduated in

positions until he held the

position of Deputy Head

of Corporate Banking. Mr.

Sacre joined Bank ABC in

Tunisia in 2005 as Senior

Credit & Risk Ocer, and

then in 2007 he moved to

Bank ABC Bahrain where

his position was Senior

Remedial Loan Ocer. In

2013, he moved to Bank

ABC in Algeria to assume

the role of Deputy CEO. Mr.

Sacre joined Bank ABC in

Jordan’s Board of Directors

in May 2019. He served

on the Board of Directors

of Bank ABC in Tunisia

(2009-2019) and was the

Chairman of the Audit

Committee - Bank ABC in

Tunisia (2011-2016).

Mr. Jawad Sacre

Director

RC ‡ ð

30

Executive

Management

Mr. George Soa

General Manager

B. Sc. in Business

Administration,

Management, London, U.K.

Mr. George Soa began his

career in banking at HSBC

Jordan in 1990, holding

various positions in Retail and

Corporate Banking until 2001,

when he moved to Societe

Generale de Banque – Jordanie,

where he assumed several

roles in Retail banking, ending

with Retail Banking Manager.

In 2005, Mr. George Soa joined

Capital Bank as Assistant

General Manager / Head of

Personal Banking where he

stayed until joining Bank ABC

in Jordan in August 2009 as

Executive Vice President /

Head of the Retail Banking

Group. Mr. George Soa’s

career progressed at Bank

ABC in Jordan and starting

2015, he began deputizing the

General Manager until being

appointed as Deputy General

Manager in August 2019. Mr.

George Soa assumed the role

of Acting General Manager

starting November 2019

until January 2020, when Mr.

George Soa was appointed as

the General Manager of Bank

ABC in Jordan.

In addition to his roles, Mr.

George Soa has been a Board

Director at ABC Investments

since August 2018, later

becoming Deputy Chairman of

the Board in November 2019,

and was also a Board Member

of Visa Jordan Services

Company from May 2010 until

July 2011.

Mr. Adnan Al Shoubky

EVP/ Head of Support Group

BA in Public Administration

(Major) Computer

Science (Minor), Yarmouk

University; Certied

Internal Auditor (CIA).

Mr. Al Shoubky worked in

Amman Bank for Investment

from 1994- 1996 as an Internal

Auditor. During 1996 – 2006 Mr.

Al Shoubky worked with Arab

Banking Corporation (Jordan)

where his last position was

a Manager in Internal Audit

Department. Then he joined

the Arab Cooperation for

Financial Investments Co.

(ABCI) as the Deputy CEO for

Operations. In February 2009,

Mr. Al Shoubky joined again

Arab Banking Corporation

(Jordan) as Head of Internal

Audit. Since 2014, Mr. Al

Shoubky became Head of

Support Group. He was a

Board Member of ABCI for the

period 1/2014 till 8/2018, Mr.

Al shoubky reappointed as

Board Member of ABCI from

3/11/2019 till now.

Mr. Fadi Haddad

SVP/ Head of Wholesale

Banking Group

MSc. in Financial

Management, Arab

Academy for Financial and

Banking Studies.

Diploma in Financial

Analysis, Institute of

Banking Studies.

BA in General

Management, Mu’tah

University.

Mr. Haddad commenced his

career in the banking sector

in 2000 starting with the

International Islamic Arab Bank

until 2003, where he moved

across several departments

there. In 2004, Mr. Haddad

joined the Arab Banking

Corporation (Jordan) as a

manager in the Corporate

Department, where he stayed

until late 2007, aer which he

moved to the UAE, joining Arab

Bank as a Team Leader within

Corporate Banking division. In

2010, Mr. Haddad joined the

Arab Banking Corporation

(Jordan) once again as a First

Vice President in Corporate

Banking until 2018, when he

assumed his current position

as Senior Vice President/ Head

of Wholesale Banking Group.

Mr. Taj Khomosh

SVP/ Head of Retail Banking

Group

B.Sc. in Business

Administration & Political

science, University of

Jordan

Certied Innovation

Strategy (Global

Innovation Institute)

Executive leadership from

PMI.

Mr. Khomosh started his

career with ANZ Grindlay

Bank in 1999 as a Marketing

Ocer then moved to

Standard Chartered Bank

covering several posts. In

2003 he joined Mashreq Bank

Qatar as Head of Cards &

Marketing Manager, followed

by a tenure at Jordan Ahli

Bank as Head of the Direct

Sales Centers till 2007 when

he joined Arab Bank –Syria

as Head of Branches. Mr.

Khomosh later became

District Manager at Arab

Bank Jordan and Head of

Consumer Banking for Arab

Bank – Syria in 2010. From

2012 to 2016 Mr. Khomosh

was the Deputy CEO - Chief

of Retail Banking at Jordan

Dubai Islamic Bank and in

2016 moved to Mashreq Bank

UAE until 2019 as VP Regional

Manger Dubai. Thereaer, Mr.

Khomosh joined the Housing

Bank of Jordan until April

2020 when he moved to the

Arab Banking Corporation

(Jordan) as Head of the Retail

Banking Group. During his

career, Mr. Khomosh held

board memberships in the

Specialized Leasing Company

from August 2019 to March

2020, and previously in Misk

Brokerage Company from

April 2016 to July 2019

Mr. Khaldoun Ziadat

SVP/ Head of Internal Audit

MBA in Banking and

Finance, University of

Wales / UK.

Mr. Ziadat had worked in

Arab Bank as a Credit Ocer,

Credit Facilities Division/

International Branches from

2000 till 2003. Then he Joined

Cairo Amman Bank to work

in the Audit Department

till 2006. Aer that, Mr.

Ziadat joined Arab Banking

Corporation (Jordan) as Senior

Internal Auditor, where during

the said period he mingled

across many positions until

holding the current position as

SVP/ Head of Internal Audit.

Mr. Khaled Nassraween

SVP / Head of Compliance

Secretary of the Board’s

Compliance Committee

B.Sc. in Accounting,

U n i v e r s i t y o f J o r d a n .

Certied Compliance

Ocer/ Fellow of the

American Academy of

Financial Management

(FAAFM).

Certied Anti-Money

Laundering Specialist.

Fellow of ACAMS.

Mr. Nassraween had worked

across many positions in

External Audit companies

during the period 1985 till

1991, following which he

Joined Cairo Amman Bank

and worked in the Audit

Department until 1998.

Thereaer, Mr. Nassraween

joined Bank of Jordan as

Head of following up Audit’s

Report Unit until 2004 when

he joined the Arab Banking

Corporation (Jordan) as the

Head of Compliance, the role

which he continues to assume

to this date.

31

BANK ABC IN JORDAN ANNUAL REPORT 2021

Mrs. Yara Baddar

SVP / Head of Human

Resources

Secretary of the Board’s

Nominations and

Compensation Committee

Secretary of the Board’s

Corporate Governance

Committee

Master’s in Business

Administration (MBA),

University of Manchester.

M.Sc. HR & Industrial

Relations, University of

Manchester.

Mrs. Baddar began her

career in HR in 2007 when

she joined KADDB as a

Training and Development

Specialist. She later moved

to eSense Soware as a

Training Lead, and later joined

ABC Investments as HR

Manager and Acting Head of

Administration in 2010. Mrs.

Baddar subsequently moved

to Bank ABC in Jordan as Head

of Training & Organisational

Development in 2012, with

her career progressing until

assuming the role of Head of

HR in September 2019.

Mr. Husam Liswi

SVP/ Head of Operations

Management

B.Sc. in Accounting &

Business Administration,

University of Jordan.

Mr. Liswi started his career

in the banking sector in 1989

when he joined Arab Bank. Mr.

Liswi built his career in several

departments, culminating

in becoming VP / Head of

Centralized Trade Finance

Services in 2006, then Head

of Operations Department in

Arab Bank – Algeria in 2010. In

2015, Mr. Liswi joined the Arab

Banking Corporation (Jordan)

as FVP/ Banking Operations,

and he was appointed as SVP

/ Head of Operations in 2016.

Mrs. Aida Saeed

SVP / Head of Consumers

Credit

MBA in Management,

University of Jordan.

Mrs. Saeed joined Bank ABC

in Jordan in 1995 where her

career progressed across

several departments,

the majority being in

the Consumers Credit

Department. In 2009, Mrs.

Saeed became the Retail

& Credit Risk Department

Manager. In October 2015,

she became the Acting

Head of Consumers

Credit Department and

was appointed as FVP

/ Consumers Credit

Department in 2016.

Mrs. Saeed took over as

SVP / Consumers Credit

Department in 2018.

Mr. Fahed Ibrahim

SVP / Head of Treasury

B.Sc. in Economic, Al-

Yarmouk University,

Chartered Financial

Analyst (CFA).

Mr. Fahed joined Bank ABC

in Jordan in 1998 where his

career progressed across

several positions in The

Treasury department. In

October 2018, Mr. Fahed

assumed the role Acting Head

of Treasury until January

2020 he was appointed as

Head of Treasury.

Mrs. Eman Abu Hait

SVP/ Head of Risk

Management

B.Sc. in Banking and

Financial Science, Yarmouk

University.

Ms. Eman Abu-Hait built

an extensive career in

Risk Management at Cairo

Amman Bank, where her

tenure spanned over 20

years. Ms. Abu-Hait’s career

grew in Cairo Amman Bank

where it culminated by

being appointed as Credit

and Market Risk Manager in

2007. In 2013, Ms. Abu-Hait

moved to the Arab Banking

Corporation (Jordan) as Risk

Department Manager, until

2017 when she was appointed

as the Bank’s Head of Risk

Management.

Mr. Faisal Abu Znemah

FVP/ Head of Legal Aairs

The Secretary of the Board

of Directors

Secretary of the Board’s

Audit Committee

B.Sc. in Law, Babel

University – Iraq.

Mr. Abu Znemah started

his career as a legal trainee

during the years 1997 – 1999,

followed by employment

as a freelancer lawyer until

2001, when he worked for the

Housing Bank for Trade and

Finance as a lawyer and legal

advisor until 2006. Thereaer,

Mr. Abu Znemah joined the

Arab Banking Corporation

(Jordan) as lawyer and legal

advisor until June 2017 when

he was appointed as the

acting Head of the Legal

Aairs Department and was

appointed as the Head of the

Legal Aairs Department in

2018. In September 2019, he

became the Secretary of the

Board of Directors of the Arab

Banking Corporation (Jordan)

in addition to his current role.

Mr. Ali Etawi

FVP / Acting Head of

Information Technology

MA in Mathematics,

University of Mou’ta.

Mr. Etawi started his career

as a team leader in R&D

department with Batelco

during the years 1999 – 2002,

then he moved to ABC

Investments covering several

posts in 2002. In 2009 he

joined Bank ABC in Jordan

as Systems & Applications

Development Manager, In

May 2021, Mr. Etawi assumed

the role Acting Head of

Information Technology.

Mrs. Nisreen Hamati

SVP/ Chief Financial Ocer

B.Sc. in Accounting,

Philadelphia University.

Certied Public

Accountant.

Project Management

Professional.

Prior to joining the Arab

Banking Corporation (Jordan)

in April 2016 as CFO, Ms.

Hamati occupied the position

of CFO for Jordan and Iraq

during a 3-year tenure at

Citibank. Ms. Hamati’s career

began in 2000 at Deloitte as

an auditor, from which she

moved on to the banking

sector, occupying the role

of AVP - Country Product

Controller & Deputy MENA

Product Controller at Citibank

Dubai from 2003 until 2007,

at which point she was

appointed as Deputy CFO-VP

in addition to her previous

role. In 2008, Ms. Hamati

joined the Jordan Investment

Trust P.L.V as EVP-Finance &

Administration, later followed

by 3 years as a Program

Support Component Leader

at USAID Jordan Tourism

Development Project. From

2012 till 2013, Ms. Hamati

served as Head of Managerial

Accounting at Bank Al Etihad.

She has been sitting on

the board of JAMA (Jordan

Association for Management

Accounting) an aliate of IMA

since 2018 to date and was

recently appointed as the

board Treasurer.

Mr. Nabeel Qazzaz

SVP / Chief Credit Ocer

MA in Accounting &

Finance, Arab Academy

for Banking and Financial

Sciences.

BA in Banking and

Financial Sciences,

Yarmouk University.

Mr. Qazzaz started his

career in banking with Arab

Bank in 1995 where his

career progressed across

several departments, the

majority being at the Credit

Department. In 2010, he

moved to Capital Bank of

Jordan as the Corporate

Banking Department Manager

aer which he joined Bank

ABC in Jordan in 2012 as the

Credit Review Department

Manager. In March.2019, Mr.

Qazzaz became Acting Chief

Credit Ocer until December

2019 when he was appointed

as the Bank’s Chief Credit

Ocer.

32

Mr. Moataz Maraqa

CEO

BA in Business

Administration,

University of Jordan;

MA in Banking &

Finance, Arab Academy

for Banking Studies.

Mr. Maraqa has more than

29 years’ of experience in

investments and private

banking at Banks and

Financial Institutes. He

is holding the position of

CEO, ABCI.

Board of Directors

• Mr. Bashir Matok – Chairman.

• Mr. George Soa - Deputy Chairman.

• Mr. Hakam Zawaideh.

• Mr. Ra’fat Al Halaseh.

• Mr. Adnan Al Shoubky.

Brief on ABC Investments (ABCI)

ABC Investments was incorporated as a limited liability company

(LLC) in Amman on 25 January 1990. It owns the trademark (ABC

Investments). It is one of the premier nancial institutions of Bank

ABC Group based in Bahrain, and it is fully owned by Bank ABC

in Jordan. Its capital amounts to een million and six hundred

thousand Jordanian Dinars JD15,600,000 divided into 15,600,000

shares, each valued at one Jordanian Dinar. ABC Investments

is a member of the capital market institutions that performs

its activities through qualied and accredited technical and

administrative personnel of very high eciency.

ABC Investments was one of the rst nancial service companies

licensed by the Jordan Securities Commission (JSC) to work as:

- Financial broker in local, regional and international markets.

- Margin nancing.

- Financial advisory.

- Issuance Management/ best eorts.

- Dealer.

- Investment Management.

ABC Investments (ABCI) Executive

Management

33

BANK ABC IN JORDAN ANNUAL REPORT 2021

operations

Review of

34

operations

36 2021 Business Results

44 Future Developments Plan for 2022

46 Shareholdings of the Chairman and Members

of the Board

47 Representation of the Board of Directors

35

BANK ABC IN JORDAN ANNUAL REPORT 2021

Review of Operations

Despite all challenges,

the Bank’s keenness

and prudent policy for

managing its credit

portfolios enabled it to

perform well in 2021.

Bank’s Achievements in the Fiscal Year

Directors’ Report on the Bank’s Business Results in

2021

The Board of Directors of Bank ABC in Jordan is pleased

to extend its thanks and appreciation to the Bank’s

shareholders and present to you its report on the

nancial statement for 2021, Bank’s achievements and

the activities, services and products oered during the

previous year. The Bank continued to implement its

strategy of oering its customer the best services in

accordance with the international best practices and

technologies by developing its electronic services and

making them more user-friendly and ecient through

ABC Digital.

Despite the ongoing economic and political challenges

imposed by the COVID-19 pandemic on the Jordanian and

global economy, Bank ABC in Jordan has demonstrated

a high level of resilience in dealing with the pandemic;

as it was able to sustain its operations in an ecient

and eective manner that ensures the safety of its

employees and provision of the best services to its

customers, while complying with the instructions of the

Central Bank Of Jordan, including continuing to postpone

the installments payable by the sectors aected by

the COVID-19 pandemic. The Bank also implemented a

number of measures to maintain the quality of its credit

36

facilities portfolio and ensure comfortable liquidity ratios,

in addition to increasing its investment in digital banking

solutions and electronic banking services oered to

individuals and corporates alike.

These results conrm the Bank’s solid position and its

ability to continue to grow and achieve further prots,

despite the fact that the Bank’s performance has been

aected by the prevailing economic climate in the

Kingdom and the region in general due to the COVID-19

pandemic. These results reect the great eorts exerted

by the Bank’s Board of Directors, executive management

and employees to achieve the Bank’s strategic plan, in

order to continue this growth and implement the Bank’s

policy of prudent management of risks and banking

liabilities, as part of its future strategies and plans

aimed at oering more banking products and meeting

customers’ needs using the best methods in line with the

technological advances in this area.

At the beginning of 2022, the Bank moved to the new

Head Oce and main branch which meets its current and

future needs and reects Bank ABC in Jordan’s identity

and well-established values that put customers rst,

while continuing its steady performance as a team; thus

enhancing our success and distinction as one of the

biggest banking groups in the region. The new building

has all the necessary elements of a comfortable and

motivating work environment and provides adequate

spaces for various departments to increase working and

communication eciency, in addition to customer and

employee service facilities that enhance communication

and cooperation to the benet of the Bank and its

customers alike. The new Head Oce was designed in

accordance with the best energy-ecient practices that

help reduce the Bank’s power bill, particularly as the

Bank established a solar power station to provide power

to all Bank’s building and branches, in addition to the

environment-friendly lighting system in the new building

and Main Branch to further reduce the electricity bill and

enhance the sustainability of the Bank’s objectives.

Financial Results

Bank ABC in Jordan continued to maintain its solid and

healthy nancial position; as the capital adequacy ratio

reached 19.50% and nancial leverage ratio reached

10.73%, which signicantly exceed the ratios required by

the Central Bank of Jordan. Moreover, the nancial results

for 2021 show that Bank ABC in Jordan has achieved

good nancial results; as net prot aer tax reached

JD9.6 million, compared to JD1.22 million in the previous

year and the total income for 2021 grew by 8.5% to

JD45 million, compared to JD41.4 million in 2020; due to

the increase in interest margin caused primarily by the

decrease in the rate of interest on sources of funds and

increase in other commissions and prots as a result

of the growth in the facilities portfolio, as interest and

banking commissions reached JD40.5 million, compared

to JD37.1 million in 2020; with a 9% increase.

In terms of the nancial position, The Bank’s assets grow

to JD1.23 billion in 2021, with a 4% increase, shareholders’

equity grow by 5% to JD168 million, compared to JD160

million in 2020, and return on equity reached 6%, while

the return on Bank’s assets reached 0.8%.

By the end of 2021, customer deposits grew by 5.6% to

JD723 million, compared to JD684 million in the previous

year; with current and savings accounts making up 15.7%

of the Bank’s total customer deposits; which reects

customers’ trust in and strong relationship with the Bank.

This growth helped maintain a healthy liquidity ratio of

111.9% by the end of 2021.

37

BANK ABC IN JORDAN ANNUAL REPORT 2021

Credit Facilities Portfolio

Despite all challenges, the Bank’s keenness and prudent

policy for managing its credit portfolios enabled it

to perform well in 2021, as the Bank’s management

continued its eorts to increase the volume of credit

facilities; while maintain low risk levels by ensuring all

elements of a sound credit decision. Therefore, the

credit facilities portfolio in 2021 grew by 6.7% to JD693

million, compared to JD650 million in the previous year, in

addition to the qualitative development and improvement

that accompanied this increase, which conrms the

Bank’s success in maintaining the quality of its credit

portfolio and enhances its ability to manage its assets

and optimize available funds utilisation opportunities,

while maintaining balance between liquidity, protability

and risk. Furthermore, the Bank was able to increase

its credit facilities portfolio by interring into new risk-

managed nancing transactions to improve the quality

of its credit portfolio. This increase was the result of the

expansion in the retail and corporate sectors. The Bank

also continued its eorts to improve the quality of the

portfolio by closely monitoring all facilities accounts and

taking the necessary action to address accounts with

indicators of possible default.

Retail Banking

Despite the challenges that had been imposed

by COVID-19 pandemic in 2021, the Bank remained

committed, through its Retail Banking Group (RBG), to

implementing its strategic plans, aiming at developing

its products and services to meet the various needs of

its customers from, both, the public and private sectors,

which eventually served the Jordanian society.

RBG continued developing its electronic banking services

and encouraged its customers to use them, such as ABC

Digital, which enables customers to remotely carry out

their banking transactions in a user-friendly and safe

manner. Moreover, customers were motivated to use

contactless payment tools by not only providing them

with advanced banking cards that oer latest security

features and that can be used wirelessly, but also by

educating them on how to use them.

Having mentioned the above, it should be emphasized

that in 2021, RBG also oered its customers highly

ecient Automated Teller Machines (ATMs) with

advanced features that align with the Bank’s digitization

strategy and launched the CliQ service that has become

the most advanced and state-of-the-art payment service

in Jordan, that allows funds transfer either between

accounts held with all participating banks, or between

electronic wallets in Jordan instantly and free of charge.

To keep pace with the rapid technological and digital

development and for a better customer service, plans

were set, and necessary measurement were put in place

to launch “ila” application, which is a digital user-friendly

application that is based on articial intelligence and

data analysis technologies, which will be available in 2022

using smart phones only. This revolution is expected to

allow the bank to attract and serve a wider customer

base, starting with millennials, and ending with other

segments of the Jordanian society.

It is worth mentioning that RBG includes the Credit

Department, the Collection Department, Branches’

management and Business Development Department,

the Product Development and Marketing Department,

Sales Department, and Digitization Department, through

which the Group has been able to oer a variety of

distinctive services to individuals from all groups of the

Jordanian society that meet their banking needs.

The mentioned retail divisions have also enabled the

Group to acquire new customers and strengthen the

loyalty of existing ones, which helped in the achievement

of a signicant growth in sales and in an improvement

in customer satisfaction while maintaining risk at low

level, which was translated into an increase in the bank’s

prots despite the dicult situation imposed on various

economic sectors by the COVID-19 pandemic.

The Retail Banking

Group continued its

development of its digital

banking services; making

them more accessible and

ecient, by developing

its online banking service

(ABC Digital).

38

The Bank also continued oering its traditional banking

services and products to individuals through its twenty-

four branches that are located across the Kingdom, such

as deposits, remittances, loans, in addition to products

that are tailor-made for specic segments, such as the

clinic nancing loan for doctors, Ultimate account, Innite

and Signature cards that target the elite segment,

through which customers receive worldwide privileges,

such as free access to VIP lounges at airports, concierge

services and travel insurance, and more and more

privileges that met their aspirations.

On the other hand, in 2021 the Bank through its

RBG focused on social media (SM) platforms due to

their signicance in communication and engagement

creation by launching several promotional campaigns

on the Bank’s ocial Facebook and Instagram brand

pages, such as “Fawazir Ramadan”, “Eid Al Adha” and

“Answer and Win” campaigns, which called the public

to subscribe to the Bank’s SM pages and to participate

in those campaigns in order to win many prizes. This

contributed unprecedently to a noticeable increase in the

number of the bank’s fans on SM and to the elevation of

engagement level with the public.

Finally, in 2021 the Bank was as active in supporting

local community as it was in supporting its customers.

This was evident through RBG’s sponsorship to several

social and developmental events and activities in Amman

and other governorates including, but not limited to

its sponsorship to IFEX, the celebration of the rst

centenary of the Jordanian state “Centennial Backpack

Initiative” and the COVID-19 Media Observatory of the

National Forum for Awareness and Development.

Wholesale Banking

The Wholesale Banking Group includes the Large

Enterprises Department and SMEs Department, in

addition to the Financial Institutions Department and

Transaction Banking Unit.

The Group oers a distinctive set of comprehensive

banking solutions and services that cater to the needs

and activities of the Bank’s customers operating in

various economic sectors, as well as all small, medium

and large enterprises in Jordan and abroad, through a

network of local branches and Bank ABC Group’s external

branches across the world, in addition to a network of

correspondent banks in various countries.

In line with the Bank’s approach, the Wholesale Banking

Group’s strategy seeks to expand its customer base

by attracting new customers from promising economic

sectors, with a focus on companies that operate in

devensive sectors as well as blue-chip companies and

government and quasi-government corporations, while

maintaining the quality of the portfolio. The Wholesale

Banking Group also aims to increase its share of

operating accounts and focus on trade nance and

ancillary business that generate commissions and prots

from indirect facilities. The Group aspires to develop

digital banking channels with a key focus on increasing

the number of customers interacting through these

channels; in order to save them time, and enable them to

carry out a wide array of nancial transactions anytime

and anywhere in a secure and innovative manner.

The Group will continue to upgrade existing services

and launch new services to keep pace with the rapidly

changing business environment.

Considering the ongoing impact of the COVID-19

pandemic on the various economic sectors in the

Kingdom, the Bank continued to oer loans as part of

the National Program to Contain the Repercussions of

COVID-19 launched by the Central Bank of Jordan. Further,

and in line with CBJ’s instructions and circulars regarding

the postponement of installments payable by aected

companies, the Bank has complied with said instructions.

Treasury

The Treasury Department oers a range of services to

retail and corporate customers to meet their various

nancial requirements, including foreign exchange,

money market, capital market and safe custody of their

securities, in addition to providing various investment

solutions to hedge for market risks of uctuations in

exchange and interest rates.

In light of the challenges imposed on the local and

global market in 2021 as a result of COVID-19 pandemic,

which aected many economic sectors, the Treasury

Department was able to eectively manage the Bank’s

liquidity by providing the Bank’s nancing needs, while

continuing to full its responsibility in terms of managing

interest rate and foreign exchange risks in order to

keep them within the Group’s adopted risk appetite. The

Treasury Department continuously strives to oer a

variety of new services as part of its strategy of oering

outstanding services that meet the various needs of

Bank’s customers.

39

BANK ABC IN JORDAN ANNUAL REPORT 2021

Risk Management and Internal Systems’ Control

Bank ABC in Jordan has solid and eective control

systems, in addition to its prudent policies in terms

of credit granting, nonperforming debt management,

provisions policy, expected credit loss volume and

liquidity and risk management, as well as policies relating

to the business continuity management plan to ensure

the continuity of the Bank’s businesses during times of

crisis.

The Bank’s Board of Directors has emphasized the

importance of the control role by setting up several

committees of the Board of Directors, including the

Risk Management Committee, Corporate Governance

Committee, Nomination and Remuneration Committee

and Audit Committee, all of which have clear control

functions that assist the Bank in periodically and

eectively assessing the control role.

In 2021, the Risk Management Department continued to

implement the risk strategy developed and approved by

the Bank’s Board of Directors for the years 2021-2023,

which addresses methods of measuring and managing

all nancial and non-nancial risks, including credit risk,

market risk, liquidity risk, interest rate risk, concentration

risk, operational risk and IT risk, in addition to ensuring

that the business results relating to these risks remain

within the Bank’s acceptable risk appetite and in line with

relevant regulations.

In addition, the Bank was able to maintain a solid capital

base by maintaining regulatory capital adequacy and

liquidity ratios that exceed the minimum ratios required

by the Central Bank of Jordan and Basel Committee, as

well as stress testing (sensitivity analysis) and scenario

testing in accordance with relevant instructions of the

Central Bank of Jordan.

In 2021, the Bank continued to apply IFRS9 requirements

by implementing the policies and methodologies

developed by the parent organisation in Bahrain to

comply with the requirements of this standard, as

well as the Board of Directors’ approval of the policies,

methodologies and bases related to the calculation of

expected credit loss (provisions) in accordance with IFRS9

requirements and in line with the relevant instructions of

the Central Bank of Jordan.

Technological Developments

Based on Bank ABC’s comprehensive strategy and future

vision of the need to provide its services to its customers

anywhere and at any time and keep pace with the

latest technological developments in all sectors in line

with the customers’ desires and conduct, as well as the

importance of adapting to the digital and technological

trends in place, the Bank’s IT Department has developed

and improved the bank’s infrastructure in accordance

with international best practices, and provided

technological and technical support through the serious

work of the IT team in various departments and sections,

in addition to ensuring the continuity and sustainability

of the bank’s outstanding services in a exible manner to

enable the Bank to carry out its business to serve as a

model by delivering strong performance levels across all

its channels and branches. Bank ABC’s IT Department is

moving quickly to lead the digitisation of Jordan’s banking

sector as part of consistent and comprehensive scientic

methodologies to ensure the provision of better and

timely services to the Bank’s customers in Jordan.

Human Capital Management and Focus On Talent

Driven by its belief in the importance of human resources

as the key pillar of business success, and to keep pace

with the realities and conditions of the market and the

challenges of recruiting talents and in order to retain

its competent employees, Bank ABC in Jordan updated

a number of its policies relating to human resources, in

order to encourage the retention of competent sta.

The Bank also amended and updated the subsidiary

organisational structures of a number of departments

and amended the relevant job description cards in line

with work requirements, which achieved a more uid

ow of work and better advancement opportunities

for employees, while also ensuring compliance with the

requirements of regulatory and control bodies.

The Human Resources Department also ensured the

continuity of self-development and enhancement and

development of knowledge and competencies in light

of the limited face-to-face training opportunities, while

observing social distancing requirements under the

current circumstances created by the COVID-19 pandemic.

40

This was done by increasing distance interactive training

activities for employees, including training programmes

that cover new developments in the banking industry and

relevant regulations, which resulted in optimal utilisation

of all the abilities of the Bank’s human resources as was

reected in their performance.

In light of business continuity requirements and public

interest, the Human Resources Department has

constantly kept employees up to speed on the defense

orders related to the COVID-19 pandemic, and provided

them with the necessary explanations and clarications

to ensure full compliance and implementation of these

orders, in addition to providing health and safety

guidelines and explaining the correct procedures to be

followed, as well as the extensive education on infection

prevention measures through regular circulars.

To keep its ongoing approach of fully and thoroughly

implementing the instructions of control bodies,

particularly the instructions of the Central Bank

of Jordan, the Bank has continued to implement

its executive action plan in order to implement the

instructions of the Corporate Governance Code, by

updating and implementing all the required policies

in accordance with this Code, in addition to taking

the necessary steps to full the requirements of the

Governance and Management of Information and Related

Technologies Instructions.

Business Continuity Management

Bank ABC in Jordan continuously strives to be a leading

bank that oers its customers with uninterrupted

banking services by adopting a crisis management

and business continuity strategy that includes a set of

objectives based on the Bank’s strategic vision that will

be completed this year.

Furthermore, the Bank periodically updates its business

continuity plan, which is based on a set of operational

principles and rules that ensure immediate response to

emergencies in the event of any crisis or disaster, in order

to continue the provision of reliable banking services to

customers with high eciency that ensures customer

satisfaction. This is achieved by communicating with

the relevant employees in various departments of the

Bank to update the business continuity plans and review

the results of the business impact analysis of Bank’s

regulations and procedures.

Since the rst outbreak of COVID-19, Bank ABC in Jordan

has been managing the pandemic through the Crisis

Management Team of the executive management, which

has been managing and operating the Bank in line with

the directions and guidelines issued by the Central Bank

of Jordan during this pandemic. The team also addressed

the COVID-19 pandemic and implemented a number of

decisions and actions to ensure the continuity of Bank’s

activities and operations under the following main

themes:

· Operational Resilience: The Bank has activated

the COVID-19 emergency plan which includes

implementing the best health practices and relevant

precautions in all Bank’s buildings and branches. In

accordance with CBJ’s instructions regarding the

maximum permissible operating capacity during the

pandemic, the Bank divided its employees into three